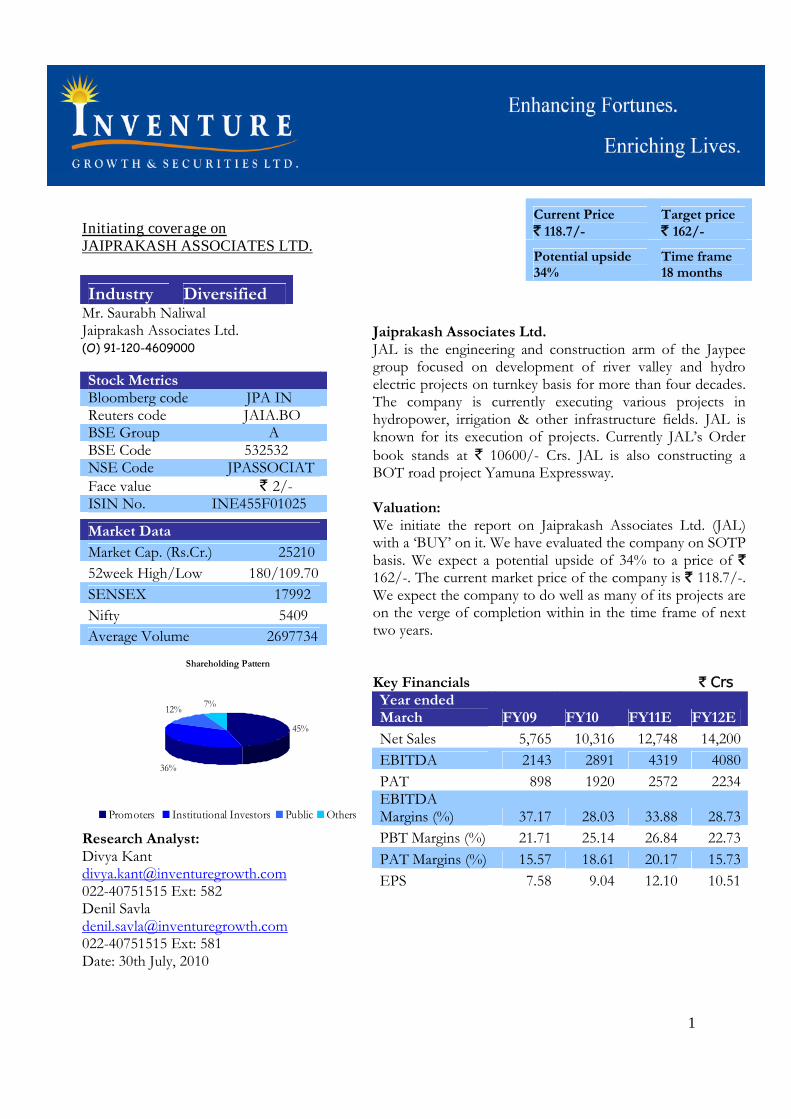

1 Initiating coverage on JAIPRAKASH ASSOCIATES LTD. Industry Diversified Mr. Saurabh Naliwal Jaiprakash Associates Ltd. (O) 91-120-4609000 Stock Metrics Bloomberg code JPA IN Reuters code JAIA.BO BSE Group A BSE Code 532532 NSE Code JPASSOCIAT Face value ` 2/- ISIN No. INE455F01025 Market Data Market Cap. (Rs.Cr.) 25210 52week High/Low 180/109.70 SENSEX 17992 Nifty 5409 Average Volume 2697734 Shareholding Pattern 45% 36% 12% 7% Promoters Institutional Investors Public Others Research Analyst: Divya Kant [email protected] 022-40751515 Ext: 582 Denil Savla [email protected] 022-40751515 Ext: 581 Date: 30th July, 2010 Jaiprakash Associates Ltd. JAL is the engineering and construction arm of the Jaypee group focused on development of river valley and hydro electric projects on turnkey basis for more than four decades. The company is currently executing various projects in hydropower, irrigation & other infrastructure fields. JAL is known for its execution of projects. Currently JAL’s Order book stands at ` 10600/- Crs. JAL is also constructing a BOT road project Yamuna Expressway. Valuation: We initiate the report on Jaiprakash Associates Ltd. (JAL) with a ‘BUY’ on it. We have evaluated the company on SOTP basis. We expect a potential upside of 34% to a price of ` 162/-. The current market price of the company is ` 118.7/-. We expect the company to do well as many of its projects are on the verge of completion within in the time frame of next two years. Key Financials ` Crs Year ended March FY09 FY10 FY11E FY12E Net Sales 5,765 10,316 12,748 14,200 EBITDA 2143 2891 4319 4080 PAT 898 1920 2572 2234 EBITDA Margins (%) 37.17 28.03 33.88 28.73 PBT Margins (%) 21.71 25.14 26.84 22.73 PAT Margins (%) 15.57 18.61 20.17 15.73 EPS 7.58 9.04 12.10 10.51 Current Price ` 118.7/- Target price ` 162/- Potential upside 34% Time frame 18 months

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Initiating coverage onJAIPRAKASH ASSOCIATES LTD.

Industry DiversifiedMr. Saurabh NaliwalJaiprakash Associates Ltd.(O) 91-120-4609000

Stock MetricsBloomberg code JPA INReuters code JAIA.BOBSE Group ABSE Code 532532NSE Code JPASSOCIATFace value ` 2/-ISIN No. INE455F01025

Market Data

Market Cap. (Rs.Cr.) 25210

52week High/Low 180/109.70

SENSEX 17992

Nifty 5409

Average Volume 2697734

Shareholding Pattern

45%

36%

12%7%

Promoters Institutional Investors Public Others

Research Analyst:Divya [email protected] Ext: 582Denil [email protected] Ext: 581Date: 30th July, 2010

Jaiprakash Associates Ltd.JAL is the engineering and construction arm of the Jaypeegroup focused on development of river valley and hydroelectric projects on turnkey basis for more than four decades.The company is currently executing various projects inhydropower, irrigation & other infrastructure fields. JAL isknown for its execution of projects. Currently JAL’s Orderbook stands at ` 10600/- Crs. JAL is also constructing aBOT road project Yamuna Expressway.

Valuation:We initiate the report on Jaiprakash Associates Ltd. (JAL)with a ‘BUY’ on it. We have evaluated the company on SOTPbasis. We expect a potential upside of 34% to a price of `162/-. The current market price of the company is ` 118.7/-.We expect the company to do well as many of its projects areon the verge of completion within in the time frame of nexttwo years.

Key Financials ` CrsYear endedMarch FY09 FY10 FY11E FY12E

Net Sales 5,765 10,316 12,748 14,200

EBITDA 2143 2891 4319 4080

PAT 898 1920 2572 2234EBITDAMargins (%) 37.17 28.03 33.88 28.73

PBT Margins (%) 21.71 25.14 26.84 22.73

PAT Margins (%) 15.57 18.61 20.17 15.73

EPS 7.58 9.04 12.10 10.51

Current Price` 118.7/-

Target price` 162/-

Potential upside34%

Time frame18 months

2

Table of Contents Page No.

Investment Rationales …… 3-5

Power Business...... 6

Hospitality sector…... 7

Risk and Concerns 9

Valuation: Cement 10

Valuation :Construction 11

Valuation: Power ……. 12

Valuation: Real estate & YEP 14

Valuation: Hotel & Other business 15

Price Derivation 16

Profit & Loss statement …… 18

Balance sheet statement …… 19

Cash flow statement …… 20

Ratio analysis…… 20

Quarterly statement…. 21

Peer set analysis…. 22

3

Cement sales to rise on the back ofstrong demand…..

JAL to buy Duncan’s Kanpur fertilizerplant with 50% stake in JV with ISGTraders a part of Duncan group…..

Construction sector boosts themargins…..

Investment Rationales

Cement sector to boost growthRevenues from cement sector are expected to gain fromstrong demand in the northern and central markets.However, its ability to manage operational costs, especially inthe construction division, would lead increase in margins. Forthe quarter ended in June, 2010 the shipment have reported65% rise to 1.33MT. As company is eager to complete itsambitious BOT road project of Yamuna Expressway, theinternal demand is expected to increase.

JAL to venture into fertilizers bizJaypee group is looking to expand in fertilizer business injoint venture with Duncan industries. The fertilizer factorysits on a 250-acre plot on outskirts of Kanpur. The revivaland rehabilitation of the said unit will be done through a jointventure (JV) company of Jaypee Fertilizers & Industries andISG Traders, a part of Duncan Industries Ltd. The unit has acapacity to generate `1700 crore - `1800 crore in annualrevenue, and deliver profit before tax of around ` 175 crore.The deal, however, needs the approval of the Board forIndustrial and Financial Reconstruction.

Managing operational cost to increase marginsYear ended March 2010; sales and other operating incomejumped ~74% to ` 10,316 crore while net profit surged by ~90 per cent to ` 1,920 crore. The company has benefitedfrom its strong market position in UP and Madhya Pradesh.Construction business accounted for ~52% of total revenuein the FY10 this is a clear sign of execution in projects suchas the Yamuna Expressway. However there has been pressureon operational cost. Increase in higher input cost canpressurize the margins going further. But on comparing toindustry margins/growth JP Associates still remains to beattractive.

4

JAL is aggressively aiming atcompletion of its projects ….

Jaypee Infratech IPO:Yamuna Expressway

Map of ExpresswaySource: YEA

Aggressive ExpansionThe company is in expansion mode. Company is aiming atthe capacity of 33 MTPA by FY13. Recently company hassetup plant in Gujarat and a plant is under construction inAssam. The implementation of on going group projects isprogressing satisfactorily and on completion Jaypee groupwill be the 3rd largest cement producing group. Companyplans to invest around ` 10,000 crore in the next three years.Apart from this company is also venturing into thermalpower projects and its first thermal plant BINA-I, is on theverge of completion. Company is also expecting its Hydropower plant Karcham Wangtoo to be completed in FY12E.JAL is also keen on completion of its BOT road projectYamuna expressway.

Jaypee Infratech IPOJaypee group came with an IPO of Jaypee Infratech.Company and shifted its most ambitious project to this i.e.Yamuna Expressway a 165Km six lane expresswayconnecting Noida to Agra along river Yamuna. On this BOTproject company will have a right to earn toll revenue fromtraffic for 36 years.

Further, company will develop 5 townships in 6175 acres ofland that will be acquired by YEA (Yamuna ExpresswayAuthority) and this land will be leased for a period of 90years. The development plan is for residential (50%),commercial (33%), and Institutional (17%) purposes.

The development of expressway along with development ofreal estate projects will benefit each other. Earnings from realestate will subsidize the development of expressway and giveadditional traffic during and after full development. Betterinfrastructure including connectivity will increase themarketability and price for realty projects along theexpressway.

5

The project is one of its kinds. JAL willdevelop expressway along with realestate.

JAL has rights for 90 years to lease outland in 5 new townships to bedeveloped along side YamunaExpressway

Jaypee greens to set up luxurioustownship in Noida

The cost for the project is estimated to be ~` 9739.2 Croreand as on 28th Feb.2010 company has already deployed`.6250 Crore.

The funding of the project has been done in the followingpattern:

Funding Pattern Rs. Cr

IPO 1500

DEBT 6000

Contributions from Promoters 1250Contribution from Real EstateDevelopments 989.29Total 9739.29

The five townships will be of 1235 acre each. JIL had takenpossession of approximately 3,897 acres end March 2010 andremaining is being done through YEA. The land has beenacquired at a low cost from YEA as compared to its realestate competitors making the profit margins look good inthis segment going forward. The five locations are:

One in Noida

Two in Gautam Budh Nagar

One in Aligarh

One in Agra

Three locations are profitably planned in the high yield NCRregion. 5 townships will mean ~400 million sq ft. And pricefor the same to be ~` 2500 Sq. Ft.

JAL has been developing luxurious township in Noida andGreater Noida spread over 450 acres. Jaypee Greens is a realestate arm of JAL integrating homes with a golf course,landscaped emerald spaces, resort living and commercialdevelopments. So far JAL has sold ~3.18 million sq ft. at anaverage realization of around ` 5412 per Sq Ft. Totalamounting to ` 1721 Crore for which company has collected~` 1192 Crore. The sales volume is expected to increase to1.5 million Sq Ft. in FY12 from ~0.5 in FY 10.

6

The power sectorJAL has been an established player in thissegment. It is the only integrated solutionprovider for hydropower projects in thecountry with the track record of strongproject implementation in differentcapacities and participation in project thathave added over 8840 MW ofhydroelectricity to the national gridbetween 2002- 2009.

Company’s ambitious; a 1000MW hydropower project at KARCHAMWANGTOO (HP) is scheduled to becompleted in of FY12E. Company claimsthat after completion of this project itwould be able to alter the scale of

operations and cash flows of JPVL (Jaiprakash power ventureLtd.) substantially.

Company claims that it will be able to sell almost 20% of itspower generated on a merchant basis.

Bina Thermal Plant (5x250) is expected to be completed intwo phases of which (2x250) to be commercialized towardsthe end of FY11 and second phase to be completed inQ4FY14.

A 1,320MW thermal project, located at Nigire (MP), is alsohoused in the company. Few projects require financial closureor various licenses, whereas, few are underway but companyhopes to accomplish the projects on time.

Project wise breakup

Project Fuel Location Capacity(MW) Status

BASPA-II Hydro HP 300 Operational

Vishnuprayag Hydro UK 400 Operational

Karcham Wangtoo Hydro HP 1000 FY11E

Bina Phase I Thermal MP 500 FY11E

Nigrie Thermal MP 1320 FY13E

Bara Phase I( Unit 1) Thermal UP 660 FY13E

Kannur Thermal Kerla 240 FY13EBara Phase I (Unit

2&F66) Theramal UP 1320 FY14E

Karchana Phase I Thermal UP 1320 FY14E

Bina Phase II Thermal MP 750 FY14E

7

We expect strong pickup in hotelbusiness mainly because of CommonWealth Games.

JAL is into IT sector with JILIT

Hospitality SectorJAL owns four five star deluxe hotels in North India. Thehotel business suffered post 26/11; along with that thepercentage of tourists declined due to slowdown in economy.This division’s profitability was adversely impacted due tolower average room rates (ARR’s).

The condition is expected to improve in FY11 mainlybecause of economic revival and Common wealth gamesbeing held in New Delhi.

The four Hotels are:

Hotel Siddharth ( Delhi)

Hotel Vasant Continental ( Delhi)

Hotel Jaypee Palace ( Agra)

Jaypee Residency Manor (Mussoorie)

Company faces competition in this segment from other majorplayers like ITC, Hotel Leela Ventures and others. The othermajor competition is from the unorganized market in thissector. Company is also planning a Spa- hotel in Noida.

Other business venturesJAL has ventured into IT sector with JILIT (JIL InformationTechnology Ltd.). It specializes into various businesssegments such as:

Software Development and Consultancy Networking and Communication Content Development Learning Solutions Multimedia Services

It operates the private network of VSAT’s in Northern Indiathat connects the Group’s various project sites, cementlocations and Hydropower stations. This facilitates seamlessconnectivity for video conferencing of remote locations anddata connectivity for the ERP solutions of the E&C, Cementand Hydropower divisions and Educational institutions.

8

JAL is developing racing circuit with itsJPSK Sports Pvt. Ltd…

Segment Revenue

JLIT aims at providing education solutions to schools inIndia and abroad. They intend to provide education withimproved content.

JAL is coming up with F1 racing Circuit

JAL ventured into sports with JPSK Sports Pvt. Ltd. to set upF1 racing circuit which has been designed by well knownGerman architect Herman Tike, who has earlier designedworld-class racing circuits in Malaysia, Bahrain, China,Turkey, Indonesia, the UAE, South Africa, South Korea andthe US. This racing circuit is being developed in outskirts ofDelhi.

Company also intends to establish Cricket stadium along withhockey arena and a sports training academy.

``

` CrC

Particular FY08 FY09 FY10 FY11E FY12EConstruction 1,795 2,943 5,300 6,020 7,100Cement/Cement Products 2,070 2,450 3,351 4,943 5,487Hotel/Hospitality 31 155 159 170 190Wind Power 18 28 30 33 36Real Estate 256 441 586 853 917Other revenue 188 268 1472 1385 1290Total revenue 4,358 6,285 10,897 13,404 15,020Less Inter segment Transfer 84.5 140.2 206 256 310Less other Income 289 380 375 400 510Net Revenue 3,984 5,765 10,316 12,748 14,200

9

JAL may face problems arising due tocertain risk and concerns especially onthe funding part of the projects

Risk & Concerns

JAL has high debt to equity ratio which is still a causeof concern. JAL has many projects underway fundingthe projects is still to be seen.

Although economy has picked up after recession butany unexpected change in economic environmentcould adversely affect the business.

Increased competition in engineering andconstruction may put pressure on business activities.JAL is heavily dependent on the EPC projects. Anydelay arising from external factors could affect thedivision’s growth trajectory, going forward.

Fluctuation in commodity prices could adverselyimpact the business.

JAL is aggressive in capacity addition and hasprojects lined up which not only need huge fundsbut also faster execution skills. The ability tocomplete the projects on time and with the availableresources is to be seen.

Projects such as power are long gestation projectsand are dependent on several factors such requisitelicenses, approvals, permit, natural disasters, labordisputes and adverse weather conditions. Thecompany may be unable to complete the projects intime. This, in turn, will escalate the cost of theprojects.

10

JAL is aggressively increasing thecapacity but managing the cost ofoperations is to be seen

We have valued JAL on EV/Ton basis;in line with other leading players

Valuation

Cement

JAL for last two years has been aggressively increasing thecapacity and this trend is expected to be continued in future.JAL is ambitious and expects to achieve 33MTPA by the endFY13, but we expect the capacity to increase to 30MTPA.

Cement is an important commodity and is directly related toinfrastructure sector. The demand and supply mismatch seencan be worrisome for the company. JAL’s cement realizationhas been range bound for the last two years and as companyis intentionally increasing its capacity the realizations areexpected to fall. But as the demand is expected to increase innorth and central India we expect the realization to beeffected marginally.

We have valued JAL cement division’s EV/ Ton multiple at~$110 (at a discount of ~25% to the leading player) andarrive at a value of `.39/-

Valuation

Capacity in FY12E 30

EV/Tonne (USD) 110

INR 47

EV (`) 14200

Less: net Debt 6000

Equity Value 8200

Price per share 39

11

Order Book

45%

20%3%

5%

27%

Yamuna Expressway Karcham WangtooZirakpur Parwanoo Highway Bagliharothers

JAL has maintained its margins

between 13-15% and it is expected in

future….

Construction Division

JAL’s order book stands at~ ` 10600 Crore excluding GangaExpressway which itself amounts for around ` 30000 crore.~94% of the orders are in house. The execution of theprojects has to be seen in future.

JAL’s construction division is expected to post revenue atCAGR of ~20% between FY09- FY12E. Along with this theconstruction margins are continuously maintained between13-15% throughout and we expect margins to be maintained.The margins for JAL command better than other mid capplayers. But, the execution and management of resources hasto be kept under a check.

We have valued this division on EV/ EBITDA basis,assigning a multiple of ~7 (discounted in line with othermajor industrial players). But as we expect revenues to grow,we expect the division to perform. We expect the division tocontribute per share ` 44/-

Construction

EV/EBITDA 7

EV(`) 16280

Net equity value 9280

Price per Share 44

12

Power Division

JAL owns 76.2% subsidiary named JPVL (Jaiprakash Power

Ventures Ltd.) through which it is thriving hard to make it

big. Currently JAL has a portfolio of 13470 MW. Out of this,

700MW is operational and another 1500MW is expected

around FY12E. Along with this JPVL is diversifying into

other fuel mix with its first thermal plant named BINA-I;

which is expected to be completed in FY12E. Further there

are many projects like Karcham Wangtoo, Nigrie, Bara-I and

Bara-II and Karchana-I. These projects are expected to be

completed till FY15. The other projects with JPVL that are

under planning or at various stages of clearances sum up the

total power portfolio at 13470MW.

Presence of JAL in power

Source: Company, IGSL Research

13

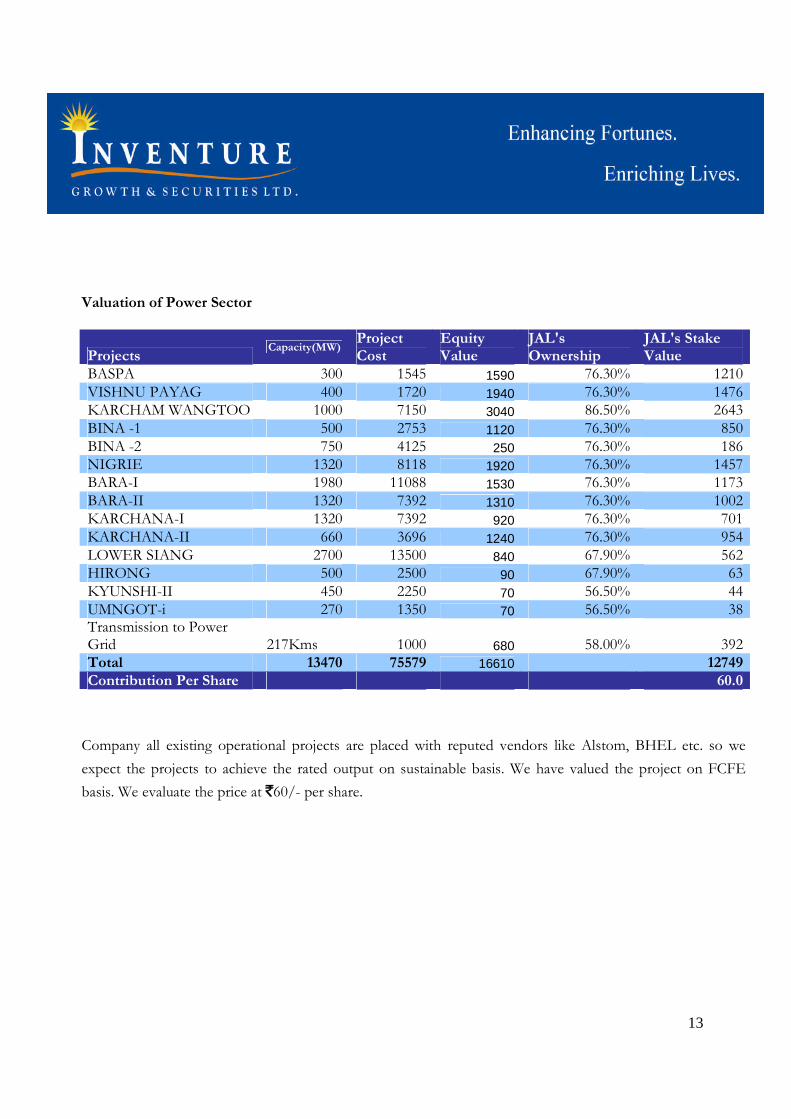

Valuation of Power Sector

ProjectsCapacity(MW)

ProjectCost

EquityValue

JAL'sOwnership

JAL's StakeValue

BASPA 300 1545 1590 76.30% 1210VISHNU PAYAG 400 1720 1940 76.30% 1476KARCHAM WANGTOO 1000 7150 3040 86.50% 2643BINA -1 500 2753 1120 76.30% 850BINA -2 750 4125 250 76.30% 186NIGRIE 1320 8118 1920 76.30% 1457BARA-I 1980 11088 1530 76.30% 1173BARA-II 1320 7392 1310 76.30% 1002KARCHANA-I 1320 7392 920 76.30% 701KARCHANA-II 660 3696 1240 76.30% 954LOWER SIANG 2700 13500 840 67.90% 562HIRONG 500 2500 90 67.90% 63KYUNSHI-II 450 2250 70 56.50% 44UMNGOT-i 270 1350 70 56.50% 38Transmission to PowerGrid 217Kms 1000 680 58.00% 392Total 13470 75579 16610 12749Contribution Per Share 60.0

Company all existing operational projects are placed with reputed vendors like Alstom, BHEL etc. so we

expect the projects to achieve the rated output on sustainable basis. We have valued the project on FCFE

basis. We evaluate the price at `60/- per share.

14

JAL is coming up with luxurious

township in Greater Noida with its

eminent project Jaypee Greens

JAL has 5 land parcels of 1250 ha along

side Yamuna Expressway

Real Estate Division

Jaypee Greens- Luxurious Township

This luxurious township is expected to come up with average

realizations of ` 5400 sq/ft. and construction cost of `

2600 Sq/ft. We have modeled the realizations and cost

escalations of ~5% and we expect the project to get

accomplished by FY14.

Yamuna Expressway – Land Parcels for Real Estate

development

The project is spread over 415 million sq ft of which

company is eager to develop around 80 million sq ft, specially

located in the area of NCR and for this company has

reported order booking also. Going forward we have hiked

the realizations and cost escalations of ~5% Per annum. So

far company has been able to launch ~20 million sq ft. at an

average realization price of ~` 3500 sq ft. It is expected as the

project gets into motion the real estate arm of Yamuna

expressway will be one of the profitable business for JAL.

We expect the real estate arm to contribute ` 11 per share.

We have evaluated the sector on EV/EBITDA basis.

15

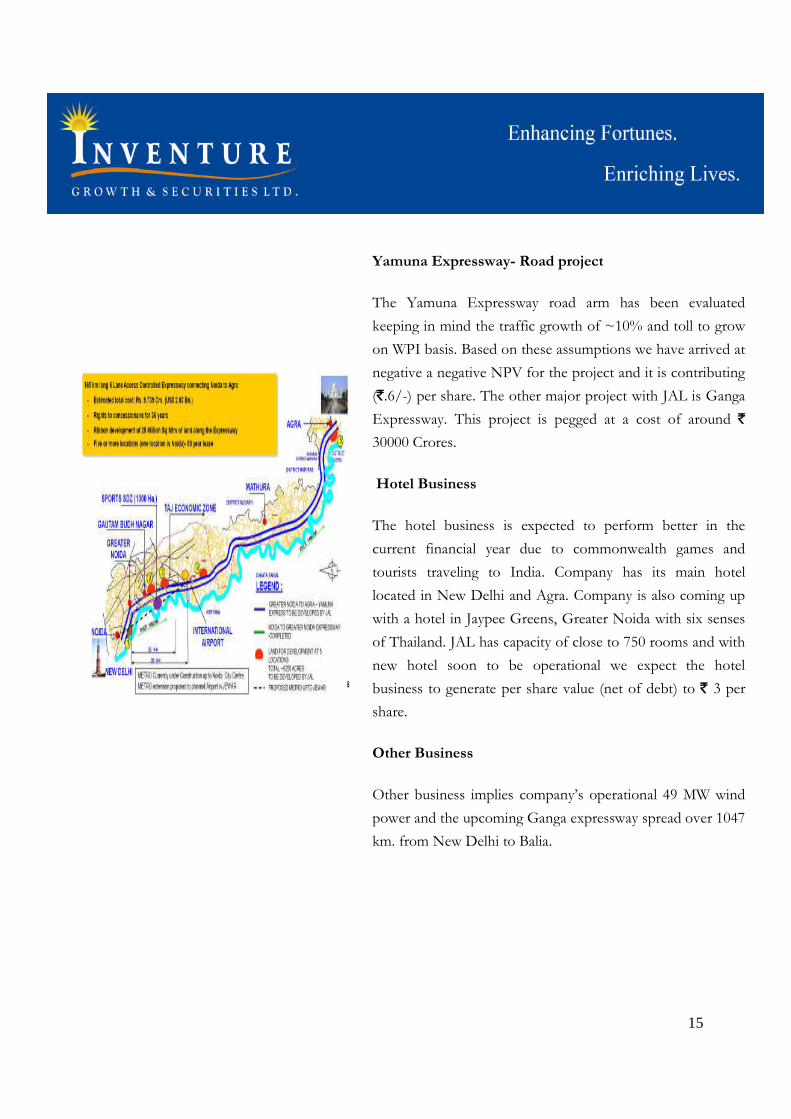

Yamuna Expressway- Road project

The Yamuna Expressway road arm has been evaluated

keeping in mind the traffic growth of ~10% and toll to grow

on WPI basis. Based on these assumptions we have arrived at

negative a negative NPV for the project and it is contributing

(`.6/-) per share. The other major project with JAL is Ganga

Expressway. This project is pegged at a cost of around `

30000 Crores.

Hotel Business

The hotel business is expected to perform better in the

current financial year due to commonwealth games and

tourists traveling to India. Company has its main hotel

located in New Delhi and Agra. Company is also coming up

with a hotel in Jaypee Greens, Greater Noida with six senses

of Thailand. JAL has capacity of close to 750 rooms and with

new hotel soon to be operational we expect the hotel

business to generate per share value (net of debt) to ` 3 per

share.

Other Business

Other business implies company’s operational 49 MW wind

power and the upcoming Ganga expressway spread over 1047

km. from New Delhi to Balia.

16

We recommend a ‘BUY’ for Jaiprakash Associates Ltd. at the current levels of ` 118.70/- with a 34%

potential upside target of ` 162/-. The conglomerate has ventured into businesses like construction, cement

manufacturing, hotel, real estate and power manufacturing. Considering its diversified portfolio, we have

evaluated company on SOTP basis.

Total valuation `

Cement 39

Construction 44

Hotel 3

Real Estate 11

Power 60

Yamuna Expressway -6

Others 11

Total 162

17

Despite the pressure on the operations

JAL is expected to maintain its margins

at the current levels….

Technically, JAL is constantly gettingsupport at the current levels

JAL has underperformed as compared

with the SENSEX. We expect the stock

to pick up in near future…..

Margins

0.00

10.00

20.00

30.00

40.00

FY09 FY10 FY11E FY12E%

EBITDA % PBDT % PBT % PAT %

Source: IGSL Research

3 Months Bollinger band chartSource: Yahoo, IGSL Chart

Index Comparison

Source: IGSL Research

18

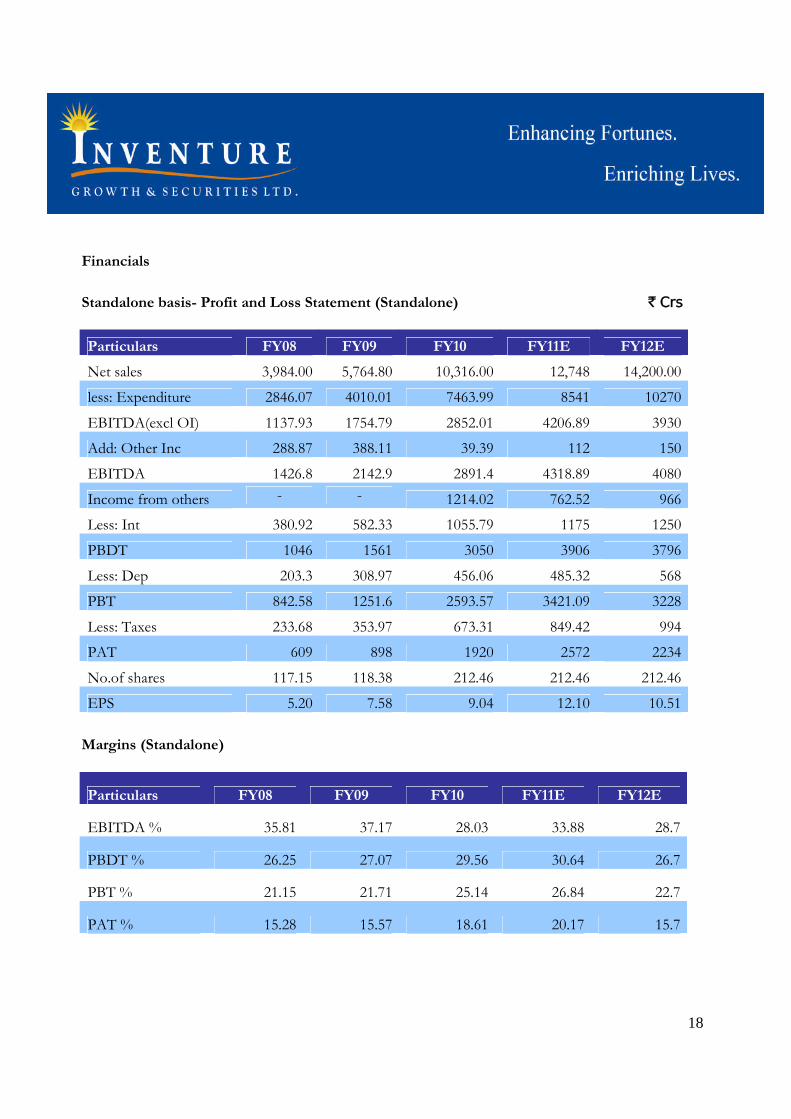

Financials

Standalone basis- Profit and Loss Statement (Standalone) ` Crs

Particulars FY08 FY09 FY10 FY11E FY12E

Net sales 3,984.00 5,764.80 10,316.00 12,748 14,200.00

less: Expenditure 2846.07 4010.01 7463.99 8541 10270

EBITDA(excl OI) 1137.93 1754.79 2852.01 4206.89 3930

Add: Other Inc 288.87 388.11 39.39 112 150

EBITDA 1426.8 2142.9 2891.4 4318.89 4080

Income from others - - 1214.02 762.52 966

Less: Int 380.92 582.33 1055.79 1175 1250

PBDT 1046 1561 3050 3906 3796

Less: Dep 203.3 308.97 456.06 485.32 568

PBT 842.58 1251.6 2593.57 3421.09 3228

Less: Taxes 233.68 353.97 673.31 849.42 994

PAT 609 898 1920 2572 2234

No.of shares 117.15 118.38 212.46 212.46 212.46

EPS 5.20 7.58 9.04 12.10 10.51

Margins (Standalone)

Particulars FY08 FY09 FY10 FY11E FY12E

EBITDA % 35.81 37.17 28.03 33.88 28.7

PBDT % 26.25 27.07 29.56 30.64 26.7

PBT % 21.15 21.71 25.14 26.84 22.7

PAT % 15.28 15.57 18.61 20.17 15.7

19

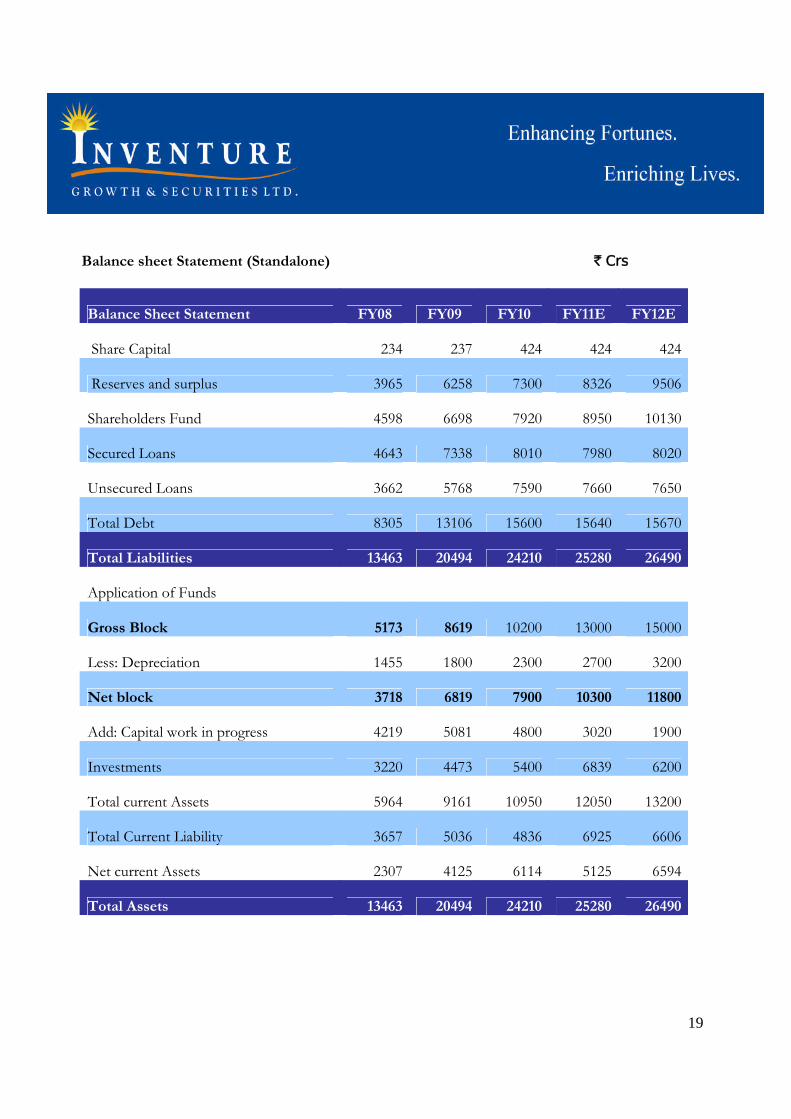

Balance sheet Statement (Standalone) ` Crs

Balance Sheet Statement FY08 FY09 FY10 FY11E FY12E

Share Capital 234 237 424 424 424

Reserves and surplus 3965 6258 7300 8326 9506

Shareholders Fund 4598 6698 7920 8950 10130

Secured Loans 4643 7338 8010 7980 8020

Unsecured Loans 3662 5768 7590 7660 7650

Total Debt 8305 13106 15600 15640 15670

Total Liabilities 13463 20494 24210 25280 26490

Application of Funds

Gross Block 5173 8619 10200 13000 15000

Less: Depreciation 1455 1800 2300 2700 3200

Net block 3718 6819 7900 10300 11800

Add: Capital work in progress 4219 5081 4800 3020 1900

Investments 3220 4473 5400 6839 6200

Total current Assets 5964 9161 10950 12050 13200

Total Current Liability 3657 5036 4836 6925 6606

Net current Assets 2307 4125 6114 5125 6594

Total Assets 13463 20494 24210 25280 26490

20

Cash Flow Statement (Standalone) ` Crs

Particular FY08 FY09 FY10E FY11E FY12E

Opening balance 1429 1815 2884 3059 3176

Net profit before taxes 843 1252 2594 3421 3228

Changes in Working Capital 18 -862 -660 -720 -710

Cash generated from operations [A] 1012 523 225 130 80

Net cash from investing activities[B] -4257 -3713 -3772 -3822 -3872

Cash generated from financing activities[C] 3631 4259 3722 3809 3839

Net Changes in Cash (A+B+C) 386 1070 175 117 47

Cash at the end of the year 1815 2884 3059 3176 3222

Ratios (Standalone)

Ratios FY09 FY10 FY11E FY12E

Earnings Per Share (Rs) 7.6 9.0 12.1 10.5

Book Value (Rs) 31.5 37.3 42.1 47.7

PE Ratio 15.65 13.13 9.81 11.29

EBITDA (%) 37.17 28.03 33.88 28.73

PBTM (%) 21.71 25.14 26.84 22.73

PATM (%) 15.57 18.61 20.17 15.73

Total Debt/Equity 2.13 2.06 1.82 1.62

21

Quarterly Results Y-o-Y (Standalone) ` Crs

Particulars Jun-10 Jun-09 Var% Mar-10 Mar-09 Var%

Gross Sales 3,174 2,067 54 3,345 2,085 60

Net Sales 3,174 2,067 54 3,345 2,085 60

Other operating income 40 50 -19 1 67 -98

EBITDA 3,214 2,117 52 3,347 2,152 56

Total Expenditure 2,532 1,525 66 2,491 1,380 81

Other Income 3 0 0 12 43 -72

Operating Profit 686 591 16 867 815 6

Interest 328 222 48 299 168 78

Exceptional Items 512 273 88 -2 0 0

PBDT 870 643 35 566 647 -12

Depreciation 150 102 48 133 102 30

PBT 720 541 33 433 544 -20

Tax 204 50 309 189 159 19

Profit After Tax 516 491 5 244 385 -37

Margins Y-o-Y

Particulars Jun-10 Jun-09 Var% Mar-10 Mar-09 Var%

EBIDTAM% 21.33 27.94 -23.7 25.91 37.88 -31.6

PBDTM% 27.07 30.36 -10.8 16.92 30.06 -43.7

PBTM% 22.4 25.56 -12.4 12.94 25.3 -48.9

PATM% 16.05 23.2 -30.8 7.29 17.91 -59.3

22

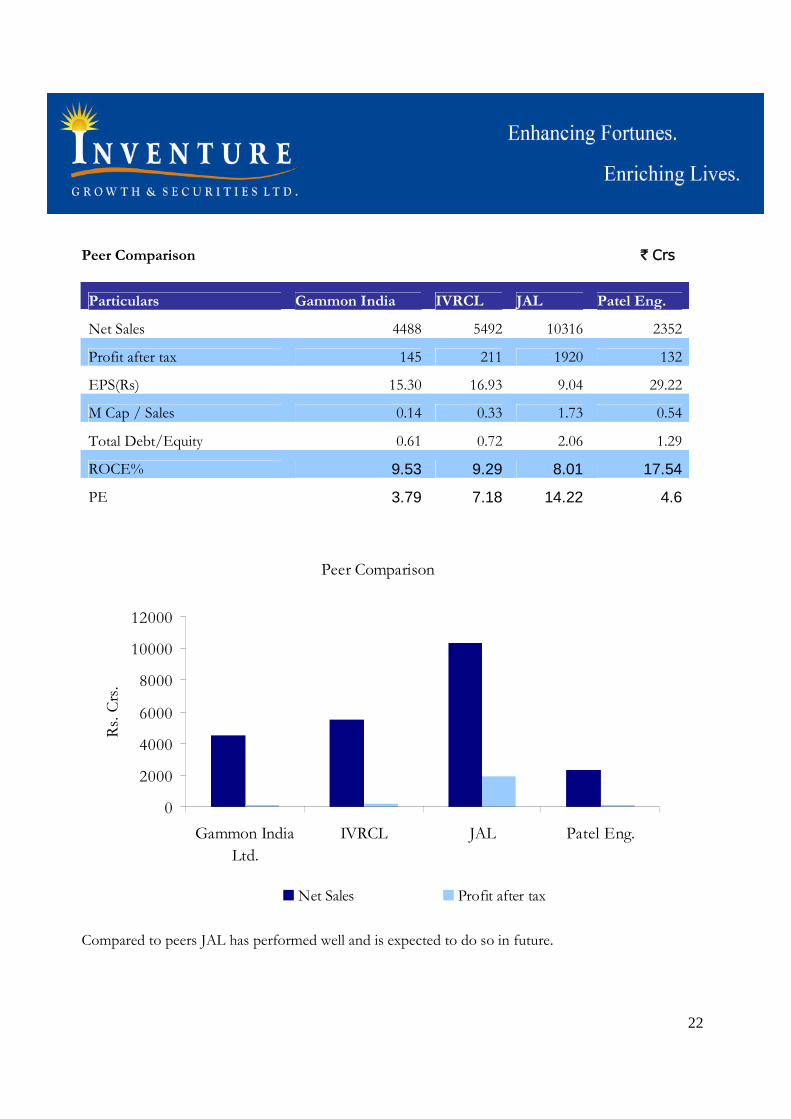

Peer Comparison ` Crs

Particulars Gammon India IVRCL JAL Patel Eng.

Net Sales 4488 5492 10316 2352

Profit after tax 145 211 1920 132

EPS(Rs) 15.30 16.93 9.04 29.22

M Cap / Sales 0.14 0.33 1.73 0.54

Total Debt/Equity 0.61 0.72 2.06 1.29

ROCE% 9.53 9.29 8.01 17.54

PE 3.79 7.18 14.22 4.6

Peer Comparison

0

2000

4000

6000

8000

10000

12000

Gammon India

Ltd.

IVRCL JAL Patel Eng.

Rs.

Crs

.

Net Sales Profit after tax

Compared to peers JAL has performed well and is expected to do so in future.

23

For any queries please feel free to contact our Institutional Research Team

Disclaimer

This Document has been prepared by Inventure Growth & Securities Ltd. The information, analysis and estimates contained herein are based onInventure’s assessment and have been obtained from sources believed to be reliable. Neither Inventure Growth & Securities Ltd nor any of itsemployees or associates accepts any liability whatsoever direct or indirect that may arise from the use of information herein and shall not beresponsible for its completeness and accuracy. It is not an offer to sell or a solicitation to buy securities. This document is for circulation only

Visit us at www.inventuregrowth.com

Please send your Feed Back to [email protected]

Inventure Growth & Securities LtdCorporate Office: - Viraj Tower, 2nd Floor, Near Landmark,

Western Express Highway, Andheri East, Mumbai - 400 069.Tel.:- +91-22-40751515, Fax: - +91-22-40751535

Names Designation E-Mail Id.ContactNumber

SALES

Ravinder Kasliwal Head Institutional Sales [email protected] 40751565/66

Dealing

Shiv Damani Institutional Dealer [email protected] 22723797

Vinit Rita Institutional Dealer [email protected] 40751565/66

Rashda Ainapore Institutional Dealer [email protected] 40751565/66

Research

Denil Savla Research Analyst [email protected] 40751515 * 581

Divya Kant Research Analyst [email protected] 40751515 * 582

Anshuman Jain Research Analyst [email protected] 40751515 * 579

Sanjeev Haria Research Analyst [email protected] 40751515

Sibayan Banerjee Technical Analyst [email protected] 22723797

Ashok Patel Technical Analyst [email protected] 22723797

Madhu Patel Technical Analyst [email protected] 22723797

Related Documents