All required disclosure and analyst certification appear on the last two pages of this report. Additional information is available upon request. Redistribution or reproduction is prohibited without written permission (Member of Alliance Bank group) PP7766/03/2013 (032116) 24 September 2012 Get in for the long term We initiate coverage on SapuraKencana Petroleum with a BUY call and a TP of RM2.71. Long term growth prospects of SAKP are solid with a 24% 4-year CAGR going into 2016 given their RM14.6bn orderbook and new assets to be delivered starting as early as 2QFY14. We expect strong contract flow going forward from Malaysian developments and also globally, of at least RM4bn per annum. The O&G all-rounder SapuraKencana Petroleum (SAKP), the result of a recent merger between SapuraCrest and Kencana Petroleum, is the only Malaysian integrated offshore oil & gas service provider with full-fledged EPCIC (engineering, procurement, construction, installation and commissioning) capabilities. The company has a strong presence in Malaysia and various regions including Asia, Australasia, Middle East, Europe, and the Americas. The group focuses on 5 areas i.e. (1) development and production, (2) EPCIC, (3) drilling, (4) marine services, and (5) operations and maintenance. RM14.6bn orderbook, new assets on the way, active tendering of >RM10bn YTD, SAKP has secured RM3.2bn of contracts, bringing their latest outstanding orderbook to RM14.6bn. We expect more to come and see that a minimum target of RM4bn in contracts per annum is achievable. Aggressive capex spend in Malaysia as well as growing traction overseas will underpin orderbook growth going forward. New strategic assets like the 2 derrick pipe lay vessels and 2 new rigs are key earnings drivers going forward. Charters rates for pipe lay vessels can rise up to RM1.2m/day while self-erecting tender rigs are fetching RM0.45m/day. Margins are high for these vessels at up to 30% at gross level and higher for drilling rigs at 45% at gross level. SAKP is tendering for more than RM10bn in contracts and we have identified up to 16 new projects largely in Malaysia that are prospects for the group. Notable projects include fabrication and/or installation for the North Malay Basin, a Pan Malaysian diving support umbrella contract, a second marginal field, participation in EOR projects (Angsi, Bokor, St Joseph), and other potentials in Australia (Browse LNG), Taiwan (Block F) and also Vietnam. Besides these, a second Petrobras tender for pipe lay support vessels continues to hang in the balance (no firm bids submitted yet) and the group’s recent installation in the Gulf of Mexico could signal a whole new region of growth for SAKP. SAKP’s key thrust going forward would be to secure turnkey projects, where the group can realise their EPCIC potential. Strong earnings growth starting FY14 Going forward into FY16, we expect SAKP’s earnings to record a 4-year CAGR of 24%. 1.8% y-o-y growth in FY13 core earnings is expected as only 8.5 months of Kencana’s earnings will be consolidated into the newly merged entity. For FY14, we expect strong growth of 46.6%, driven by the full-year consolidation of Kencana’s earnings, coupled with new asset deliveries and growth in EPCC. FY15 will see another 35.1% of growth given new asset deliveries and in FY16, we project for 15.4% growth as the Petrobras contract would have kicked off. Valuation and recommendation We initiate coverage with a BUY call and a TP of RM2.71. Our TP is derived from pegging SAKP’s FY14 EPS of 13.6sen to an industry peak cycle P/E multiple of 20x which is justified given its strong earnings growth. Key risks to our assumptions include:- (1) decline in crude oil prices leading to lower offshore capex, thus resulting in decelerating contract flow and idle assets, (2) late delivery of new assets, (3) unforeseen late delivery on contracts which may result in cost overruns and/or penalties, (4) stiff competition, and (5) delay in contract awards. SapuraKencana Petroleum Buy Oil & Gas Bloomberg Ticker: SAKP MK | Bursa Code: 5218 Initiating Coverage Analyst Team Coverage [email protected] +603 2722 1565 12-month upside potential Target price 2.71 Current price (as at 21 Sept) 2.36 Capital upside (%) 14.9 Net dividends (%) 1.1 Total return (%) 15.0 Key stock information Syariah-compliant? Yes Market cap (RM m) 11,810 Issued shares (m) 5,004 Free float (%) 46 52-week high / low (RM) 2.53 / 1.94 3-mth avg volume (‘000) 9,803 3-mth avg turnover (RM m) 3 Share price performance 1M 3M 6M Absolute (%) -3.3 6.3 N/A Relative (%) -1.6 4.4 N/A Share price chart Major shareholders % Dato’ Seri Shahril Shamsuddin 20.2 Dato’ Mohkzani Mahatir 15.9 EPF 12.3

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

All required disclosure and analyst certification appear on the last two pages of this report. Additional information is available upon request. Redistribution or reproduction is prohibited without written permission

(Member of Alliance Bank group) PP7766/03/2013 (032116)

24 September 2012

Get in for the long term We initiate coverage on SapuraKencana Petroleum with a BUY call and a TP of RM2.71. Long term growth prospects of SAKP are solid with a 24% 4-year CAGR going into 2016 given their RM14.6bn orderbook and new assets to be delivered starting as early as 2QFY14. We expect strong contract flow going forward from Malaysian developments and also globally, of at least RM4bn per annum. The O&G all-rounder SapuraKencana Petroleum (SAKP), the result of a recent merger between SapuraCrest

and Kencana Petroleum, is the only Malaysian integrated offshore oil & gas service provider with full-fledged EPCIC (engineering, procurement, construction, installation and commissioning) capabilities. The company has a strong presence in Malaysia and various regions including Asia, Australasia, Middle East, Europe, and the Americas. The group focuses on 5 areas i.e. (1) development and production, (2) EPCIC, (3) drilling, (4) marine services, and (5) operations and maintenance.

RM14.6bn orderbook, new assets on the way, active tendering of >RM10bn YTD, SAKP has secured RM3.2bn of contracts, bringing their latest outstanding

orderbook to RM14.6bn. We expect more to come and see that a minimum target of RM4bn in contracts per annum is achievable. Aggressive capex spend in Malaysia as well as growing traction overseas will underpin orderbook growth going forward.

New strategic assets like the 2 derrick pipe lay vessels and 2 new rigs are key earnings drivers going forward. Charters rates for pipe lay vessels can rise up to RM1.2m/day while self-erecting tender rigs are fetching RM0.45m/day. Margins are high for these vessels at up to 30% at gross level and higher for drilling rigs at 45% at gross level.

SAKP is tendering for more than RM10bn in contracts and we have identified up to 16 new projects largely in Malaysia that are prospects for the group. Notable projects include fabrication and/or installation for the North Malay Basin, a Pan Malaysian diving support umbrella contract, a second marginal field, participation in EOR projects (Angsi, Bokor, St Joseph), and other potentials in Australia (Browse LNG), Taiwan (Block F) and also Vietnam. Besides these, a second Petrobras tender for pipe lay support vessels continues to hang in the balance (no firm bids submitted yet) and the group’s recent installation in the Gulf of Mexico could signal a whole new region of growth for SAKP.

SAKP’s key thrust going forward would be to secure turnkey projects, where the group can realise their EPCIC potential.

Strong earnings growth starting FY14 Going forward into FY16, we expect SAKP’s earnings to record a 4-year CAGR of 24%. 1.8% y-o-y growth in FY13 core earnings is expected as only 8.5 months of Kencana’s

earnings will be consolidated into the newly merged entity. For FY14, we expect strong growth of 46.6%, driven by the full-year consolidation of Kencana’s earnings, coupled with new asset deliveries and growth in EPCC. FY15 will see another 35.1% of growth given new asset deliveries and in FY16, we project for 15.4% growth as the Petrobras contract would have kicked off.

Valuation and recommendation We initiate coverage with a BUY call and a TP of RM2.71. Our TP is derived from pegging

SAKP’s FY14 EPS of 13.6sen to an industry peak cycle P/E multiple of 20x which is justified given its strong earnings growth.

Key risks to our assumptions include:- (1) decline in crude oil prices leading to lower offshore capex, thus resulting in decelerating contract flow and idle assets, (2) late delivery of new assets, (3) unforeseen late delivery on contracts which may result in cost overruns and/or penalties, (4) stiff competition, and (5) delay in contract awards.

SapuraKencana Petroleum Buy Oil & Gas Bloomberg Ticker: SAKP MK | Bursa Code: 5218

Initiating Coverage

Analyst Team Coverage [email protected] +603 2722 1565 12-month upside potential Target price 2.71 Current price (as at 21 Sept) 2.36 Capital upside (%) 14.9 Net dividends (%) 1.1 Total return (%) 15.0 Key stock information Syariah-compliant? Yes Market cap (RM m) 11,810 Issued shares (m) 5,004 Free float (%) 46 52-week high / low (RM) 2.53 / 1.94 3-mth avg volume (‘000) 9,803 3-mth avg turnover (RM m) 3 Share price performance 1M 3M 6M Absolute (%) -3.3 6.3 N/A Relative (%) -1.6 4.4 N/A Share price chart

Major shareholders % Dato’ Seri Shahril Shamsuddin 20.2 Dato’ Mohkzani Mahatir 15.9 EPF 12.3

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

2

SNAPSHOT OF FINANCIAL AND VALUATION METRICS

Figure 1 : Key financial data

FYE 31 Jan FY12PF FY13F FY14F FY15F FY16F Revenue (RM m) 4,672.6 4,333.6 5,453.2 6,361.5 6,884.4 EBITDA (RM m) 711.3 957.9 1,296.8 1,573.8 1,709.0 EBIT (RM m) 646.6 768.3 1,007.2 1,234.2 1,319.4 Pretax profit (RM m) 688.1 726.0 978.9 1,264.2 1,428.6 Reported net profit (RM m) 454.5 462.9 678.7 916.9 1,057.9 Core net profit (RM m) 454.5 462.9 678.7 916.9 1,057.9 EPS (sen) 9.1 9.2 13.6 18.3 21.1 Core EPS (sen) 9.1 9.2 13.6 18.3 21.1 Alliance / Consensus (%) - 87.3 90.1 101.2 94.6 Core EPS growth (%) 47.5 1.8 46.6 35.1 15.4 P/E (x) 26.0 25.5 17.4 12.9 11.2 EV/EBITDA (x) 20.4 15.2 12.3 10.2 9.5 ROE (%) 8.9 7.7 10.3 11.2 11.6 Net gearing (%) 0.5 0.4 0.5 0.5 0.4 Net DPS (sen) - 1.8 2.7 3.7 4.2 Net dividend yield (%) - 0.8 1.1 1.6 1.8 BV/share (RM) 1.02 1.20 1.31 1.46 1.63 P/B (x) 2.3 2.0 1.8 1.6 1.4 Source: Alliance Research, Bloomberg

Figure 2 : SapuraCrest forward P/E trend Figure 3 : Kencana Petroleum forward P/E trend

Source: Alliance Research, Bloomberg Source: Alliance Research, Bloomberg

Figure 4 : Peer comparison

Company Call

Target price (RM)

Share price (RM)

Mkt Cap (RM m)

EPS Growth (%) P/E (x) P/BV (x) ROE (%) Net Dividend

Yield (%) CY12 CY13 CY12 CY13 CY12 CY13 CY12 CY13 CY12 CY13

SapuraKencana Buy 2.71 2.36 11,810.3 4.5 43.0 25.6 17.9 2.0 1.8 7.8 10.1 0.7 1.1 Bumi Armada Buy 4.90 3.71 10,866.7 39.3 42.9 21.7 15.2 2.8 2.3 12.8 15.5 0.7 0.7 Deleum Neutral 1.93 1.76 264.0 6.7 7.0 8.5 8.0 1.0 1.0 12.1 12.1 5.6 6.0 Petronas Chemicals N/R N/R 6.54 52,320.0 20.0 9.0 13.6 12.5 2.4 2.2 18.1 18.0 3.8 4.1 Petronas Dagangan N/R N/R 21.82 21,677.2 N/A 10.2 22.3 20.2 3.9 3.7 17.6 18.1 4.0 4.0 MMHE N/R N/R 4.81 7,696.0 55.8 19.9 23.9 20.0 2.9 2.7 12.0 13.5 1.7 2.0 Dialog N/R N/R 2.34 5,631.7 -0.1 25.3 29.6 23.6 4.5 4.0 19.4 19.3 1.5 1.7 Average 50.5 15.8 17.4 15.1 2.8 2.6 16.0 16.6 2.9 3.2 Source: Alliance Research, Bloomberg Share price date: 21 September 2012

0

5

10

15

20

25

30

2007

2008

2009

2010

2011

2012

P/E (x) P/E Average P/E +1/-1 SD +2/-2 SD

0

5

10

15

20

25

30

35

40

2006

2007

2008

2009

2010

2011

P/E (x) P/E Average P/E +1/-1 SD +2/-2 SD

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

3

COMPANY OVERVIEW Integrated O&G service provider SAKP, the result of a recent merger between SapuraCrest and Kencana Petroleum, is the only Malaysian integrated offshore oil & gas service provider with full-fledged EPCIC (engineering, procurement, construction, installation and commissioning) capabilities. The company has presence in Malaysia and various regions including Asia, Australasia, Middle East, Europe, and the Americas. Services that the group provides are focused on 5 areas which are:- (1) development and production, (2) EPCIC, (3) drilling, (4) marine services, and (5) operations and maintenance. Figure 5 below gives us a visual of all the services provided by SAKP as well as the type of assets used in carrying out these activities. Figure 6 provides a brief on the group’s 5 divisions.

Figure 5 : Snapshot of SAKP’s activities across the O&G offshore value chain

Source: Company

A one of its kind home grown O&G offering

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

4

Figure 6 : 5 key segments of SAKP

Source: Company Large asset base to support their services SAKP has the largest asset base amongst Asian peers, especially for the IPF (installation of pipes and facilities) and drilling services. SAKP also has several assets currently under construction and these include an array of self-erecting tender rigs, derrick pipelay vessels, pipelay support vessels and also workboats. To note, participation in the Berantai marginal oil field project would not have been feasible for SAKP had they not had the right facilities to carry out field development works. Figure 7 below maps out the group’s assets according to business division.

Figure 7 : Strategic assets of the group

Source: Company

SAKP has 5 core business segments…

…and a full range of assets to support their services

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

5

Big on partnerships with international players Both SapuraCrest and Kencana Petroleum have in the past been inclined to forming joint ventures and partnerships with international players. The move to grow via partnerships has allowed knowledge transfer to the group and also opened the doors to international markets. It is via these partnerships and JV’s, we believe, that SAKP has managed to break into markets like Australia, India and Brazil. Currently, key partnerships and JV’s that SAKP has include:- Seadrill – A longtime partner of SapuraCrest and now a shareholder of SAKP. Seadrill

continues to be committed to the group despite having recently pared down their stake. It co-owns 5 self-erecting tender assisted drilling rigs (SETR) together with SAKP. Besides this, Seadrill is also a JV partner for delivery of 3 vessels for charter to Petrobras.

Petrofac – a 50:50 JV with Petrofac was formed some 1.5 years ago to execute a risk service contract on the Berantai marginal field for Petronas. Prior to this partnership, Kencana Petroleum in its own capacity was a key fabricator for Petrofac’s Malaysian projects and continues to be so.

Subsea7 – SapuraCrest in 2007 formed a partnership with Subsea7 to build the state-of-the-art Sapura3000 vessel which is now a key earnings contributor for the group. This partnership, we believe, has equipped SAKP with much knowledge on deepwater installation works and launched the group into this market segment.

Bechtel – Collaboration to fabricate and assemble an LNG processing facility at the Wheatstone natural gas development off Australia. This partnership has resulted in a EPCC contract worth RM1bn which is currently ongoing.

Larsen & Toubro – Together with SAKP co-owns a pipelay barge called to LT3000. The partnership has allowed SAKP into the Indian offshore installation market.

Leighton – SAKP has a joint venture with Leighton Engineering to build a water pipeline in Labuan.

Saipem – Despite technically being a competitor, Kencana Petroleum had collaborated with Saipem on the fabrication of superstructures for the Chevron Gorgon LNG project in Australia. The project value was roughly RM1bn and awarded in 2010.

GE oil & gas – SAKP has a long term service agreement for the provision of maintenance services for gas turbines under license for GE. This forms part of the group’s O&M (operations and maintenance) business.

Major shareholders of SAKP SAKP’s major shareholders include:- Dato’ Seri Shahril bin Shamsuddin and Shahriman bin Shamsuddin who collectively own

20% Dato’ Mokhzani bin Mahathir with 15.9% Seadrill post-merger had 11.8% but the company has since pared down their stake to

4%. We do not view Seadrill’s move to pare down their stake in SAKP to be negative as both companies continue to work closely together in drilling activities and for the Petrobras contract. In a press statement, Seadrill highlighted that the paring down of their stake in SAKP was to raise funds for rig building. Seadrill said that they were fully committed to continue to working with SAKP to develop new JV businesses. Only recently, Seadrill formed a new joint venture with SAKP to fund the 3 vessels to be chartered to Petrobras come 2016. On top of this JV, Seadrill has existing joint ventures with SAKP on 5 SETRs. Management Dato’ Seri Shahril Shamsuddin takes the helm of SAKP as the President & Group CEO. Dato’ Mohkzani also continues to play an integral role in the company as the Executive Vice Chairman and handles the corporate and finance activities of the group. Other than that, each business division is helmed by its own respective head of operations as set out in Appendix 1.

The company has valuable partnerships which have helped

them grow through the years

The largest shareholder is Dato’ Shahril followed by Dato’ Mohkzani

Since the listing, Seadrill has pared down their stake, due to their own

fund raising needs

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

6

SEGMENT OVERVIEW The EPCIC segment (which consists of the IPF and EPCC businesses) is SAKP’s largest revenue and earnings contributor and is the mainstay of the group’s business. Annually, we expect the segment to contribute up to 60% to group earnings. The next largest earnings contributor is the drilling segment. With an existing 6 rigs and 2 new ones currently being built, the drilling business will maintain its 25-30% annual contribution going into FY16. Other income streams for the group are from the marine segment and also from operations and maintenance. FY14 will signal the start of earnings contribution from the group’s production and development segment. Production and development - Berantai In January 2011, a consortium led by Petrofac Energy Development (50% interest), SapuraCrest (25%) and Kencana (25%) was awarded the first domestic Risk Service Contract (RSC) by PETRONAS to carry out the development and production of petroleum from Berantai, a marginal oil field off Terengganu, for 8 years. The project is divided into 2 phases. Berantai Phase 1 involves the supply of a well head platform to support drilling of 18 wells, with pipelines linking the adjacent platform in Angsi. For Phase 2, another well head platform is also going to be installed and both platforms will be connected to an FPSO (floating production storage and offloading vessel). SAKP has recently made an investment in the FPSO together with Petrofac, taking a 49% stake in the vessel. The total investment in the vessel amounts to RM1.04bn and is expected to be ready by next year in time for the field to go into production.

Figure 8 : Berantai full development plan

Source: Petrofac With a combined stake of 50%, the RSC award enabled SAKP to move up the value chain by participating in oil field development, production and operation. Total investment that SAKP will make to bring oil to the surface is RM2.7bn (includes the fabrication, installation and FPSO). The investment sum will then be recouped when the field goes into production. The RM2.7bn will be paid back to the company over a 6-year period on a straight line basis with a mark-up on the capex. On top of this, the consortium is expected to earn a remuneration fee calculated on a per barrel basis, to an agreed but yet undisclosed ceiling. Notably, the remuneration will be based on the group’s operational efficiency (in producing oil) and not based on the level of crude oil prices. Payback from this project is expected to commence in 2QCY13 onwards. We initially expect the project to turn in a half year contribution of RM30m in profits for FY14 and RM60m per annum thereafter. This assumption includes the return of capex spent to SAKP as well as estimated profit from hydrocarbon production. We believe that successful execution of the Berantai project will set the group up for more marginal fields in the coming years. PETRONAS has earmarked some 25 fields prime for an RSC and has so far only awarded 3 of these. We expect SAKP to be vying for another marginal field project and is likely to partner with Petrofac for the venture again. Several fields are pending tender at this juncture and these include Tembikai and Cenang.

The Berantai project is SAKP’s maiden foray into production and

development

Total capex amounts to RM2.7bn…

…which will be recovered, along with a remuneration fee, starting

FY14

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

7

EPCIC – EPCC and installation Prior to the merger, SapuraCrest’s core business was focused on installation of pipelines and facilities (IPF) while Kencana’s core business was focused on engineering, procurement, construction and commissioning (EPCC). Thus the combination of both businesses results in the core earnings driver of the group which is the EPCIC (engineering, procurement, construction, installation and commissioning) segment. EPCC SAKP has a wealth of experience in the EPCC segment and has a good delivery track record so far using their in-house resources. The group focuses on EPCC of major offshore O&G facilities like rigs, vessels, jackets, topsides, individual modules and subsea structures. To note, subsea structures is a relatively new area for the group and was acquired along with the Clough business prior to the merger. The group is also experienced with conversion of old offshore assets into floating production vessels and also mobile offshore production units. EPCC activities take place at the Lumut Fabrication Yard which is some 3 km from the open seas of the Straits of Malacca and also at the Labuan Shipyard which is located in the port of Victoria Harbour in Labuan island. Lumut Fabrication Yard (100% owned) 2nd largest fabricator in Malaysia after MMHE with 270 acres of yard space with an

estimated capacity of up to 90,000mtpa. Covered fabrication workshops within their yard spanning 85,600sq m allow them 24

hour activities in all weather conditions. 633 meter water front with water depth of 9-12 metres. Total load-out capacity of

30,000mt. Crawler, rough terrain, mobile and gantry cranes ranging from 20 tonnes to 600 tonnes.

Figure 9 : Lumut Fabrication Yard

Source: Company

Labuan Shipyard (50% owned) 74 acres with up to 36,000mtpa capacity. The shipyard’s load-out facilities comprise a 7,000-tonne capacity Syncrolift shiplift

system, a 12,000-tonne capacity skidway and quay and a 3,000-tonne capacity loadout skidway and quay. The yard also possesses approximately 900 metres of deep water wharfage for ships.

EPCIC is the bread and butter business of the group

SAKP has an illustrious fabrication track record

All of their fabrication is done at the Lumut Yard

Eventually, the group hopes to be able to utilize the Labuan shipyard

as well

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

8

Installation Installation is an activity that is complementary to EPCC. Installation can be divided into 3 types of activities which are: - (1) installation of pipelines and facilities (IPF), (2) installation of subsea umbilicals, risers and flowlines (SURF), and (3) hook up and commissioning (HUC). Typically, a field operator will tender out EPCC and IPF and/or SURF and HUC contracts separately as most EPCC companies do not have vessels of their own to carry out installation. Either that or the EPCC companies would lease a vessel from an IPF provider and carry out the work with a low margin. As such, having the installation business combined with EPCC is SAKP’s true strength. The group will eventually be able to join hands in bidding for turnkey EPCIC projects which are larger in size and would extend over a longer period, thus providing good earnings visibility. SAKP has 5 IPF vessels which are the Sapura3000, LTS3000, QP2000, Clough Challenge and Java Constructor. The QP2000 was previously only 26% owned but post the merger the group decided to fully acquire the vessel from their partner. Besides these 5 vessels, SAKP has been leasing a pipe lay barge called the Enterprise 3 from Perisai Petroleum Teknologi (Non-Rated) as they do not have sufficient capacity for their umbrella contract in Malaysia. For SURF activities, SAKP has the Normand Clough, which is a subsea installation vessel. The Normand Clough is currently working at Berantai and is slated to go to Russian waters for the Shakalin project later this year.

Figure 10 : IPF and SURF vessels

Source: Company The EPCC and installation business can be easily integrated in the future for SAKP to become a turnkey contractor, we believe. From the Figures 11 and 12 below, we note that both businesses already have common customers which would help with bidding activity. Turnkey projects are a key thrust for SAKP going forward as it would allow them to maximise cost efficiencies and secure larger projects with lengthy timelines which would improve earnings visibility.

Installation activities are complementary to the EPCC

business

SAKP has 5 strategic assets in this segment

This fleet gives the group a near monopoly of the Malaysian

installation market segment

The EPCC and Installation business can be integrated given a similar

customer base

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

9

Figure 11 : EPCC customer base Figure 12 : Installation customer base

Source: Company Source: Company

Drilling SAKP owns 6 self-erecting tender assisted rigs (SETR) that are used for development drilling which involves drilling production wells from existing platforms. These SETR rigs are designed as a cost efficient and flexible drilling systems for development scenarios involving multiple well slot fixed offshore platforms whereby the rig moves from platform to platform using its own derrick equipment set which is lifted by its own crane. Only the KM-1 rig is wholly-owned by the group while the rest are jointly owned with Seadrill. All of SAKP’s rigs are currently tendered out on long term contracts with the earliest contract expiry in Jan 2013 for the T-10 rig. With these 6 rigs, SAKP is the largest Asian rig owners and one of the largest SETR owners globally. According to Rigzone, there are only 29 units of SETRs globally with a current utilisation rate of 86.2% (one year ago global utilisation was 82.1%). SETR’s are often used in Malaysian/Southeast Asian waters as they are suitable for shallower developments with calm weather environment. As shown in Figure 13 below, day rates for the group’s rigs typically range from RM350k/day to RM450k/day. The range in day rates depend largely on the rig’s drilling depth capabilities and also whether the charter is a bareboat charter or coupled with services. Overall, the drilling segment provides SAKP with the strongest margin. We estimate a 45% margin at gross level going forward for the drilling operations.

Figure 13 : Drilling rig and current contracts

Rig Specifications Contract period Customer Ownership Day rate

(RM/day)

KM-1 11.88 - 243.84 metres depth. Built in 2010.

Sept 2010 - Aug 2015, option to extend for up to another 5 years

Petronas Carigali 100% 453,151

T-3 10 - 122 metres depth. Built 1980 and modified in 2001.

Feb 2005 - June 2013 Sedrill 51% 350,000

T-6 10 - 122 metres depth. Built 1982 and modified in 2000.

Dec 2010 - Apr 2013, option for 2 extensions of 3 months each

CHOCSV and Carigali PTTEP

51% 350,000

T-9 9 - 2,000 metres with prelaid mooring. Built in 2003.

Apr 2012 - March 2013, option to extend for 12 months

Petronas Carigali 51% 443,836

T-10 9 - 2,000 metres with prelaid mooring. Built in 2007.

Jan 2011 - Jan 2013. Seadrill 51% 450,000

Teknik Berkat

10 - 152 metres. Built in 1990 and modified in 2005.

Pending new contract details Petronas Carigali 51% 450,000

Source: Company, Alliance Research

The group has 6 self-erecting tender assisted rigs and are the

largest rig owner in Southeast Asia

Rig charter is a lucrative business, with daily rates of up to

RM450k/day and gross margins of 45%

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

10

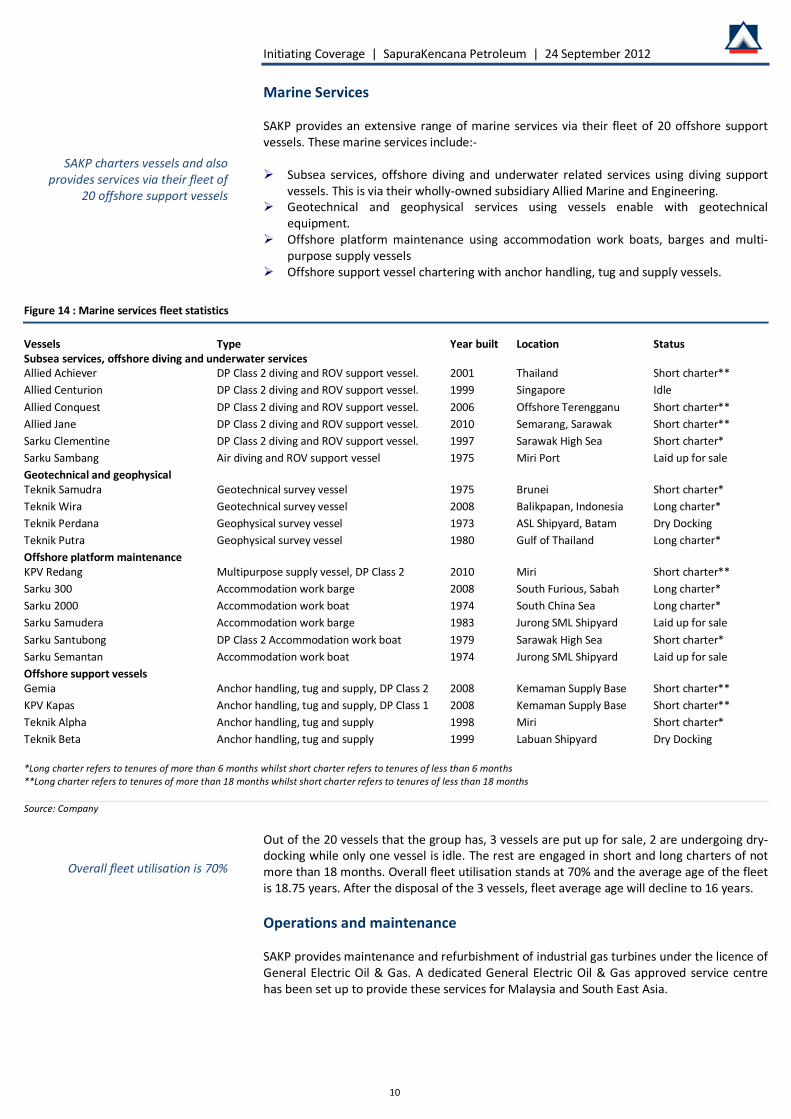

Marine Services SAKP provides an extensive range of marine services via their fleet of 20 offshore support vessels. These marine services include:- Subsea services, offshore diving and underwater related services using diving support

vessels. This is via their wholly-owned subsidiary Allied Marine and Engineering. Geotechnical and geophysical services using vessels enable with geotechnical

equipment. Offshore platform maintenance using accommodation work boats, barges and multi-

purpose supply vessels Offshore support vessel chartering with anchor handling, tug and supply vessels.

Figure 14 : Marine services fleet statistics Vessels Type Year built Location Status Subsea services, offshore diving and underwater services Allied Achiever DP Class 2 diving and ROV support vessel. 2001 Thailand Short charter** Allied Centurion DP Class 2 diving and ROV support vessel. 1999 Singapore Idle Allied Conquest DP Class 2 diving and ROV support vessel. 2006 Offshore Terengganu Short charter** Allied Jane DP Class 2 diving and ROV support vessel. 2010 Semarang, Sarawak Short charter** Sarku Clementine DP Class 2 diving and ROV support vessel. 1997 Sarawak High Sea Short charter* Sarku Sambang Air diving and ROV support vessel 1975 Miri Port Laid up for sale Geotechnical and geophysical Teknik Samudra Geotechnical survey vessel 1975 Brunei Short charter* Teknik Wira Geotechnical survey vessel 2008 Balikpapan, Indonesia Long charter* Teknik Perdana Geophysical survey vessel 1973 ASL Shipyard, Batam Dry Docking Teknik Putra Geophysical survey vessel 1980 Gulf of Thailand Long charter* Offshore platform maintenance KPV Redang Multipurpose supply vessel, DP Class 2 2010 Miri Short charter** Sarku 300 Accommodation work barge 2008 South Furious, Sabah Long charter* Sarku 2000 Accommodation work boat 1974 South China Sea Long charter* Sarku Samudera Accommodation work barge 1983 Jurong SML Shipyard Laid up for sale Sarku Santubong DP Class 2 Accommodation work boat 1979 Sarawak High Sea Short charter* Sarku Semantan Accommodation work boat 1974 Jurong SML Shipyard Laid up for sale Offshore support vessels Gemia Anchor handling, tug and supply, DP Class 2 2008 Kemaman Supply Base Short charter** KPV Kapas Anchor handling, tug and supply, DP Class 1 2008 Kemaman Supply Base Short charter** Teknik Alpha Anchor handling, tug and supply 1998 Miri Short charter* Teknik Beta Anchor handling, tug and supply 1999 Labuan Shipyard Dry Docking *Long charter refers to tenures of more than 6 months whilst short charter refers to tenures of less than 6 months **Long charter refers to tenures of more than 18 months whilst short charter refers to tenures of less than 18 months Source: Company

Out of the 20 vessels that the group has, 3 vessels are put up for sale, 2 are undergoing dry-docking while only one vessel is idle. The rest are engaged in short and long charters of not more than 18 months. Overall fleet utilisation stands at 70% and the average age of the fleet is 18.75 years. After the disposal of the 3 vessels, fleet average age will decline to 16 years. Operations and maintenance SAKP provides maintenance and refurbishment of industrial gas turbines under the licence of General Electric Oil & Gas. A dedicated General Electric Oil & Gas approved service centre has been set up to provide these services for Malaysia and South East Asia.

SAKP charters vessels and also provides services via their fleet of

20 offshore support vessels

Overall fleet utilisation is 70%

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

11

Besides that, SAKP also repairs and refurbishes SBM (single buoy moorings) and valves. The group is currently the Malaysian market leader for SBM repairs. On valves, the group has a workshop in Kemaman which carries out maintenance and overhaul of o-valves for storage facilities, refineries and petrochemical plants.

EARNINGS CATALYSTS RM14.6bn outstanding orderbook Inclusive of new contracts awarded YTD amounting to RM3.2bn, SAKP’s total outstanding orderbook is estimated at RM14.6bn. 88% of the group’s orderbook lies in the EPCIC segment. Within the EPCIC segment, RM2.5bn consists of fabrication jobs (EPC) while the remaining RM10.3bn is for IPF/HUC/SURF jobs. The Petrobras contract itself amounts to RM4.2bn but only commences in FY16 onwards. In terms of geographical distribution, more than 50% of the group’s orderbook is from international contracts (Brazil and Australia particularly) and the remainder from Malaysia. Positive to note also is that SAKP recently broke into the Gulf of Mexico market with an installation job to be carried out by the Sapura3000. Besides size, SAKP’s existing orderbook also offers some recurring income, especially from the drilling segment. Despite that the outstanding orderbook from the drilling segment is small (RM0.8bn) in comparison to the group’s total orderbook, it contributes 20-30% of group profits per annum. On forward earnings, we view that up to 60% of FY14 earnings are secured from existing orderbook. The remainder of earnings is expected to come from contract replenishment and from newly delivered assets. We discuss new assets in another segment below.

Figure 15 : Latest orderbook breakdown

Source: Company

Figure 16 : Contracts awarded YTD Date Customer Completion

(FY) Value

(RM m) Project/Location Contract Type

Jan-12 Petrovietnam n/a 300 Vietnam Installation Feb-12 Murphy Sarawak 2Q13 101 Patricia & Serendah Fabrication Feb-12 ExxonMobil 2Q14 74 Tapis Fabrication Mar-12 Petronas Carigali FY15 162 Peninsula M’sia drilling Drilling Apr-12 Petronas Gas FY14 35 Onshore gas processing Fabrication May-12 Murphy Sarawak 2Q14 460 Serendah Fabrication May-12 Petrofac 4Q13 49 MOPU Conversion Fabrication May-12 Petronas Carigali 4Q14 1,300 Pan Malaysia Installation Installation May-12 Origin 3Q14 157 Origin Otway Australia Installation Jul-12 Murphy Sarawak 3Q13 250 Patricia & Serendah Fabrication Aug-12 PTTEP Australasia (Ashmore Cartier) Pty Ltd 4Q14 50 Montara HUC Aug-12 KPOC 2Q15 106 Kebabangan HUC Sep-12 Construcciones Maritimas Mexicanas S.A. de C.V. 4Q13 135 Gulf of Mexico Installation TOTAL RM3.2bn Source: Company

Healthy orderbook that extends well into 2016

We view that up to 60% of FY14 earnings are already secured via

existing orderbook

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

12

Healthy times for the offshore O&G industry The current climate of the O&G industry is conducive for service providers. Crude oil prices appear to be sustained at high levels and production companies are actively spending to increase and/or sustain hydrocarbon output. In Malaysia itself, offshore spending is rife with PETRONAS’s RM300bn capex plan, ExxonMobil (RM37bn) and Shell’s (RM3.5bn) investments into enhanced oil recovery (EOR) and also new developments like the North Malay Basin (RM15bn). Based on our quarterly compilation, contract awards have been flowing in consistently this year and is expected to peak in 4Q12. We expect similar patterns going into 2013 and possibly 2014 given the development plans put forth by production companies in Malaysia. Furthermore, Malaysian companies like SAKP are making good headway into the global arena as well, thus creating stronger contract flow numbers that have been seen since 4Q11.

Figure 17 : Contracts awarded to Malaysian O&G service providers

Source: Bursa Malaysia RM10bn tenderbook and growing, aiming for turnkey projects At the moment, SAKP notes that they are bidding for more than RM10bn worth of contracts globally. To sustain earnings going forward, SAKP hopes to add up to RM4bn of new orders per annum starting FY14 but we believe that the group can do more given their growing traction overseas and also increase in asset base. In the more immediate term of FY13, we expect the group to add another RM0.5-1bn in jobs before the financial year is out. Oncoming jobs in the near term include a new diving support contract and also ad-hoc installation jobs. We believe that SAKP will truly come into its own when they win a turnkey EPCIC contract. Since the merger, the fabrication and IPF divisions have not yet joint hands for bidding activities and continue to bid for contracts separately. With a larger balance sheet and diversified asset base, turnkey contracts would enable the group to go after projects with larger value and increased complexity. At the same time, with combined procurement and project management, the group may be able to turn in stronger margins. Currently, fabrication margins at gross level range from 15 to 20% while IPF margins range from 15 to 25%. A turnkey project could up margins to 20-25% across the whole EPCIC segment, we believe. In Figure 18, we have made a list of 16 projects that SAKP can participate in, including as a turnkey contractor. We see ample opportunity for the group in Malaysia given the many redevelopment projects, new gas projects and also new marginal fields. Besides that, regional opportunities are also available for the group in Thailand, Australia and Vietnam. That said, despite the group’s regional thrust, we expect turnkey projects to come from Malaysian waters first, given SAKP’s track record here.

The industry is in the pink of health with active spending plans

SAKP hopes to add at least RM4bn of new jobs per annum to sustain

earnings

We look forward to the group securing an EPCIC contract as it

could mean stronger margins

Current tender market is healthy with ample projects for SAKP to bid

for

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

13

Figure 18 : New contract tracker

Country NOC/IOC Project Opportunities Est

contract value

Est Award timeline

Contenders /Project status

Malaysia Hess North Malay Basin

Central processing platform, wellhead platform, pipeline installation, hook up and commissioning. Turnkey potential.

RM1-2bn 2013 Hess has just started scouting for yards. Tender expected to be opened to regional players.

Malaysia Petronas Carigali

Malaysia Diving support umbrella contract RM500m-RM1bn

2H12 SapuraKencana's contract (via Allied Marine) ends in 3H12 and it is expected to be renewed.

Malaysia Petronas Carigali

Bokor re-development

25k tonne processing platform and 7 other platforms. Turnkey potential.

RM1-1.5bn 2013

Not yet open for tender. Tender expected to be opened to regional players

Malaysia Petronas Carigali

Tembikai and Cenang Marginal Fields

Development of a marginal field RM1-2bn 2H12 Petronas Carigali is pending announcement on this project. Other interested parties include Dialog.

Malaysia Hess Belud South - 1 FEED fabrication wellhead platform. RM200-

400m 2013 SapuraKencana reportedly confirmed for wellhead platform. No announcement yet.

Malaysia Shell Malikai & Kebabangan Installation of a tension leg platform RM1-

1.5bn 2014 SapuraKecana, Technip, Swiber eyeing pipeline and installation. No news of tender yet.

Malaysia Petronas Carigali Block SK 316

FEED and EPCIC. 10k mt platform for floatover installation. Turnkey potential.

RM1-1.5bn 2013

Tender may be regional. MMHE-Technip strong contenders because of FEED expertise however SAKP can perform installation, especially floatovers.

Malaysia Petronas Carigali

Angsi CEOR Topside fabrication for CEOR vessel RM200-400m

2013 MISC is in talks with KencanaHL for topside fabrication for their vessel. Other bidders include Bumi Armada.

Vietnam Petrovietnam Nam Con Son 300km pipe laying RM1-1.5bn n/a

Regional tender. Bids reportedly submitted. No news on timelines.

Indonesia Husky Madura FPSO & wellhead platform installation RM100-200m 2013 SapuraKencana, Swiber, Bakri, Supasi

reportedly bidding for installation

Indonesia Petronas Carigali Kepodang

Transportation and installation of a wellhead platform, the 110-kilometre export trunkline and associated pipelines.

RM400-700m 2013

Reportedly six bidders including SAKP's subsidiary, TL Offshore.

Thailand Carigali Hess Block A-18 Up to 40k mt of fabrication with gas processing platform and installation. Turnkey potential.

RM2-2.5bn 2013

Strong regional contenders for this contract. Indication that it may be awarded to Korean competitors. However, installation works still up for grabs.

Australia Woodside Browse LNG 4 leg steel jacket 28,000mt. 25,000mt topsides. Also 1200km umbilicals. Turnkey potential.

RM500-1bn 2013

SapuraKencana, Chiwan Sembawang, McDermott, Penglai Jutal, Offshore Oil Eng. Corp.

Thailand Petronas Carigali

Bunga Dahlia & Teratai PM 302

Fabrication and Installation of platforms RM500-2bn

2012 SapuraKencana, FPSO tender not out yet.

Malaysia Shell St Joseph Chemical EOR Supply of Chemical injection vessel. RM500-

1bn 2H12- 2013

It was announced that Shell is going to Re-tender this projects. New bidders not known

Taiwan CPC Corporation Block F

Offshore processing platform with a 12,000-tonne jacket and a 9000-tonne topside

RM775m 2013 Retendered in April 2012

Source: Company

New strategic assets to further grow earnings Other than the 3 pipelay support vessels (PLSV) to be delivered to Petrobras starting end-FY15, SAKP also has 2 derrick pipe lay vessels (DLB) and 2 new drilling rigs coming on-stream. Delivery of new assets and their subsequent charter are key thrusts for earnings growth going forward. Given that deliveries mostly commence in FY14 onwards, the bulk of our growth expectations in FY14 and FY15 is owing to the new assets. To note, we forecast for 46.6% growth in FY14 and another 35.1% of growth in FY15.

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

14

Two new specialised assets pending delivery to highlight are:- The Sapura3500 which is slated to be delivered in 4QFY14. As the name indicates, the

Sapura3500 will be able to perform higher tonnage installation than the Sapura3000 and possibly also work at deeper depths. As it is, the Sapura3000 has charter rates ranging from RM500k/day to RM1m/day (depending on the job complexity). As such, the Sapura3500 would be able to garner even better rates of up to RM1.2m/day.

The KM3 rig which will be delivered in 1QFY15. The drilling rig will not be a tender assisted rig like the rest of the rigs that SAKP has but will be able to handle deeper depths and be similar to a jack up. Currently, SAKP’s drilling rigs fetch rates of roughly RM400k/day and yield up to 45% gross margins. A rig with deeper depth specifications will likely be able to fetch better rates at RM500k/day or more.

Figure 19 : Asset delivery timeline according to financial year end

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 Sapura3500

Sapura1200

Petrobras 1

Petrobras 2

Petrobras 3

KM2 Rig

KM3 Rig

Source: Company

FINANCIAL HIGHLIGHTS Strong earnings growth ahead Going forward into FY16 and taking into consideration the earnings drivers mentioned above, we expect SAKP’s earnings to record a 4- year CAGR of 24%. For FY13 though, we only expect flattish y-o-y growth as only 8.5 months of earnings from Kencana Petroleum will be consolidated. Assuming that full year results are consolidated, the group is expected to achieve growth of about 15% in FY13. Come FY14, we expect a year of strong growth at +46.6% (RM215.8m in profit growth) due to:- (1) full-year earnings contribution from Kencana, (2) delivery and charter of the KM2 SETR in 2H14, and (3) maiden returns from the Berantai marginal field project commencing in 2H14 onwards. To note, the Sapura3500 will also be delivered in FY14 but only in 4Q as such we have not factored in any earnings contribution from the Sapura3500 during this year. The Berantai project is expected start turning in returns from 2Q14 onwards and for the year; we expect a RM30m net profit contribution. Going into FY15, we expect another RM283.2m (35% y-o-y growth) of additional profits as there will be a full year of earnings contribution from the Sapura3500, KM2 rig and Berantai contract. Furthermore, the Sapura1200 vessel and KM3 will also be completed in 1QFY15, thus we assumed at least 6 months of earnings contribution from both assets. Further to this, the first vessel for Petrobras will be delivered in 4QFY15, however we have assumed that the contract will officially commence in FY16 only. FY16 will see growth of 15.4%.

SAKP hopes to venture into deeper waters with the new Sapura3500

vessel

They also hope to move to deeper waters for their drilling operations

We expect SAKP to record a 4- year CAGR of 24%.

FY13 will show flat earnings, but

growth will kick in from FY14 onwards

Strong growth will continue into FY15 given new assets and the

Berantai contract

And FY16 as the Petrobras charter kicks in

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

15

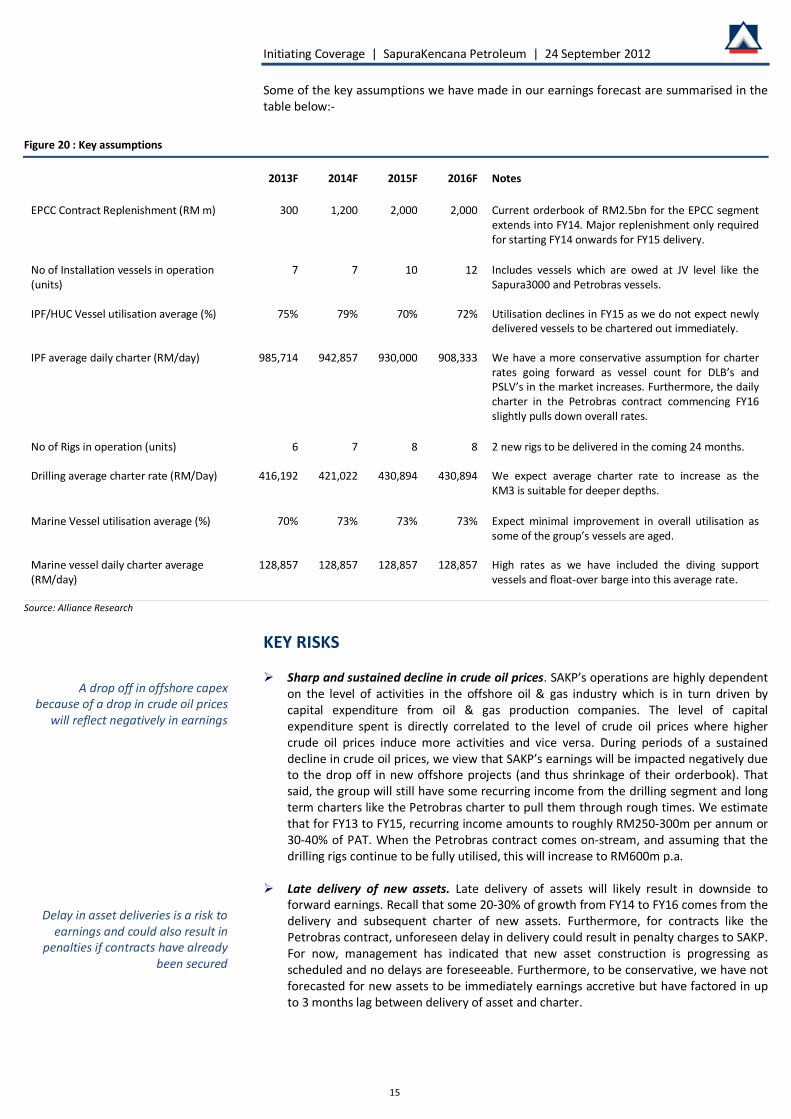

Some of the key assumptions we have made in our earnings forecast are summarised in the table below:-

Figure 20 : Key assumptions

2013F 2014F 2015F 2016F Notes EPCC Contract Replenishment (RM m) 300 1,200 2,000 2,000 Current orderbook of RM2.5bn for the EPCC segment

extends into FY14. Major replenishment only required for starting FY14 onwards for FY15 delivery.

No of Installation vessels in operation (units)

7 7 10 12 Includes vessels which are owed at JV level like the Sapura3000 and Petrobras vessels.

IPF/HUC Vessel utilisation average (%) 75% 79% 70% 72% Utilisation declines in FY15 as we do not expect newly delivered vessels to be chartered out immediately.

IPF average daily charter (RM/day) 985,714 942,857 930,000 908,333 We have a more conservative assumption for charter rates going forward as vessel count for DLB’s and PSLV’s in the market increases. Furthermore, the daily charter in the Petrobras contract commencing FY16 slightly pulls down overall rates.

No of Rigs in operation (units) 6 7 8 8 2 new rigs to be delivered in the coming 24 months.

Drilling average charter rate (RM/Day) 416,192 421,022 430,894 430,894 We expect average charter rate to increase as the

KM3 is suitable for deeper depths. Marine Vessel utilisation average (%) 70% 73% 73% 73% Expect minimal improvement in overall utilisation as

some of the group’s vessels are aged.

Marine vessel daily charter average (RM/day)

128,857 128,857 128,857 128,857 High rates as we have included the diving support vessels and float-over barge into this average rate.

Source: Alliance Research

KEY RISKS Sharp and sustained decline in crude oil prices. SAKP’s operations are highly dependent

on the level of activities in the offshore oil & gas industry which is in turn driven by capital expenditure from oil & gas production companies. The level of capital expenditure spent is directly correlated to the level of crude oil prices where higher crude oil prices induce more activities and vice versa. During periods of a sustained decline in crude oil prices, we view that SAKP’s earnings will be impacted negatively due to the drop off in new offshore projects (and thus shrinkage of their orderbook). That said, the group will still have some recurring income from the drilling segment and long term charters like the Petrobras charter to pull them through rough times. We estimate that for FY13 to FY15, recurring income amounts to roughly RM250-300m per annum or 30-40% of PAT. When the Petrobras contract comes on-stream, and assuming that the drilling rigs continue to be fully utilised, this will increase to RM600m p.a.

Late delivery of new assets. Late delivery of assets will likely result in downside to

forward earnings. Recall that some 20-30% of growth from FY14 to FY16 comes from the delivery and subsequent charter of new assets. Furthermore, for contracts like the Petrobras contract, unforeseen delay in delivery could result in penalty charges to SAKP. For now, management has indicated that new asset construction is progressing as scheduled and no delays are foreseeable. Furthermore, to be conservative, we have not forecasted for new assets to be immediately earnings accretive but have factored in up to 3 months lag between delivery of asset and charter.

A drop off in offshore capex because of a drop in crude oil prices

will reflect negatively in earnings

Delay in asset deliveries is a risk to earnings and could also result in

penalties if contracts have already been secured

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

16

Late delivery on contracts. Delivery of projects is dependent on various factors which

include timely delivery of critical equipment, weather conditions, obtaining necessary and relevant regulatory approvals, performance of sub-contractors and suppliers. Delay in completion of projects may result in cost overruns or imposition of late delivery penalties.

Delays in contract awards. More often than not, projects will be called to tender and

then retendered due to disagreements on pricing and/or technicalities and this most often happens in the fabrication segment. Delayed projects could result in lumpy earnings for the group if they are waiting on large projects to replenish orderbook. That said, casting their net wide minimises this risk and having an existing large orderbook minimises dependence on contract award timelines.

Competition. Key competitive factors in the market that SAKP faces includes experience,

duration required for completion of projects, access to suitable equipment, machineries and vessels to carry out projects, track record requirements, financial strength, technical capability, price, range, capability to deliver and also economies of scale. We view that while the group has fared well against global competitors so far, snagging jobs as far as Brazil and Mexico, losing out on contracts because of the factors mentioned above is a risk nonetheless. In the global offshore O&G arena, SAKP’s key competitors include players like McDermott, Saipem, Technip, Swiber, and Emas Offshore. In Malaysia, the group has no direct competitor but does compete with MMHE for fabrication contracts and vessel players like Alam Maritim, Petra Perdana, Dayang Enterprises and also Bumi Armada for vessel related contracts (charters, installation and HUC).

Foreign exchange fluctuations. The group transacts largely in USD and AUD. While the

group has some natural hedge (as their costs are also in the said foreign currencies), there may be translation losses when converted back to ringgit for the purpose of financial reporting. However, this would only be the case in which the ringgit strengthens against foreign currencies. Looking back historically at both SapuraCrest and Kencana’s earnings though, we have noted that the drilling segment is usually the most affected by foreign currency translation losses/gains as all contracts are in USD.

VALUATION AND RECOMMENDATION Initiating coverage with a Buy We initiate coverage on SAKP with a BUY call and a target price of RM2.71. Our TP is derived from pegging SAKP’s FY14 EPS of 13.6sen to an industry peak cycle P/E multiple of 20x which is justified given the strong earnings growth ahead. The valuation methodology is inline with that used for our valuation on Bumi Armada, another oil & gas stock with strong earnings growth. We highlight that real growth for the company will only be seen from FY14 onwards. In the interim, FY13 earnings are expected to be flattish y-o-y as only 8.5 months of Kencana Petroleum’s earnings will be consolidated. FY14 will see strong growth, largely because of the low base seen in FY13 and also because of new assets being delivered, maiden contributions from the Berantai project and stronger earnings in the EPCC business. We also highlight that our FY13 and FY14 earnings are conservative, making up 87.3% and 90.1% of consensus estimates, respectively. For FY13, we believe the differential arises from lack of full adjustment in consensus earnings for the 8.5months contribution from Kencana for the financial year. We view some immediate term downgrade risk to earnings when earnings are announced on the 24 September. There is also expected to be a one-off charge of RM138m for listing expenses in the 2QFY13 results. As for FY14, the difference from consensus likely arises from different expectations on earnings accretion from new asset deliveries. We have skewed most of the earnings accretion from new assets to FY15.

Fabrication contracts are often subject to delays and this could

result in lumpy earnings

While SAKP has held its own so far, as they move to new markets they

are up against stiff competition from global leaders

The drilling segment may see fluctuations in earnings due to

foreign currency translation gains or losses

Initiating with a BUY and a TP of RM2.71

Growth will kick in from FY14 onwards

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

17

APPENDIX I Management team

Figure 21 : Management team

Source: Company

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

18

APPENDIX II Glossary

Figure 22 : Glossary

Anchor Handling Tug and Supply (AHTS) A vessel which performs the four said functions. Typically used to provide logistic support to offshore oil

rigs, platforms and other offshore installations. Able to tow rigs, barges and other mobile structures from location to location.

Break horse power The amount of power generated by motor without taking into consideration any amount of various auxiliary components which may slow the speed of the motor. Usually AHTS vessels are classified by their break horsepower.

Brownfield An oil & gas field that has previously been developed

Dynamic positioning (DP) A computer controlled system to automatically maintain a vessels position and heading by using its propellers and thrusters. The dynamic positioning level (DP2 or DP3) indicates the degree of redundancy built into the system. DP allows a vessel to work in deep waters where anchoring is not possible.

EPCIC Engineering, procurement, construction, installation and commissioning.

Greenfield An oil & gas field that has not been developed

HSE Health, Safety and Environment

Jackets Legs of an offshore oil platform which are piled into the sea bed. Consists of three to eight main legs connected to each other by bracings.

Modules Any or various modular sets of equipment designed to perform one or more functions and be installed on an offshore platform.

MOPU Mobile offshore production unit. A movable and transportable facility that is used to perform offshore production. Basic types of mobile units include bottom supported units and floating units.

Offshore platform A structure located in a marine environment that houses workers and equipment for hydrocarbon production and processing. Offshore platforms are comprised of Topsides and Jackets.

Topsides All hardware that lies above the surface of the sea i.e. the upper part of a ship's side or a platform. Topsides include oil production plants, accommodation blocks and also the drilling rig. Topside are often modular in design and can be changed when necessary.

ROV A remotely operated vehicle, which is a tethered underwater vehicle. Source: Alliance Research

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

19

SapuraKencana Petroleum Financial Summary

Balance Sheet Income StatementFY 31 Jan (RM m) 2012PF 2013F 2014F 2015F 2016F FY 31 Jan (RM m) 2012PF 2013F 2014F 2015F 2016F

PPE 2,797.1 3,538.7 5,249.1 5,909.4 6,519.8 Revenue 4,672.6 4,333.6 5,453.2 6,361.5 6,884.4Investment properties 4,911.8 4,911.8 4,911.8 4,911.8 4,911.8 EBITDA 711.3 957.9 1,296.8 1,573.8 1,709.0Property development - - - - - Depreciation & amortisatio (64.7) (189.7) (289.7) (339.7) (389.7)Inventories 88.3 47.5 119.5 139.4 169.8 EBIT 646.6 768.3 1,007.2 1,234.2 1,319.4Receivables 2,145.4 1,881.9 2,429.3 2,938.9 3,398.7 Net interest expense (61.3) (163.5) (177.0) (156.0) (145.5)Other assets 94.0 40.8 40.8 41.8 42.8 Share of associates 102.7 121.2 148.6 186.1 254.7Depos i t, bank and cash 2,124.4 3,156.1 2,371.4 2,045.3 1,801.6 Pretax profi t 688.1 726.0 978.9 1,264.2 1,428.6Total Assets 12,161.0 13,576.8 15,121.9 15,986.6 16,844.5 Taxation (90.4) (108.9) (146.8) (189.6) (214.3)

Minori ty interest (143.1) (154.2) (153.3) (157.7) (156.4)LT borrowings 3,435.4 4,435.4 4,935.4 4,635.4 4,335.4 PATMI 454.5 462.9 678.7 916.9 1,057.9ST borrowings 1,065.9 1,015.9 965.9 915.9 865.9 Adj PATMI 454.5 462.9 678.7 916.9 1,057.9Payables 2,145.8 1,549.1 1,947.9 2,271.4 2,476.5 Other l iabi l i ties 64.5 64.5 64.5 64.5 64.5 Key Statistics & RatiosLiabilities 6,711.6 7,064.9 7,913.7 7,887.2 7,742.3 FY 31 Jan 2012PF 2013F 2014F 2015F 2016F

Share capi ta l 5,004.4 5,004.4 5,004.4 5,004.4 5,004.4 GrowthReserves 116.8 1,025.2 1,568.1 2,301.7 3,148.0 Revenue 7.5% -7.3% 25.8% 16.7% 8.2%Shareholders' equity 5,121.1 6,029.5 6,572.5 7,306.1 8,152.4 EBITDA 17.3% 34.7% 35.4% 21.4% 8.6%Minori ty interest 328.2 482.4 635.7 793.4 949.8 Pretax profi t 28.4% 5.5% 34.8% 29.2% 13.0%Total Equity 5,449.4 6,511.9 7,208.2 8,099.5 9,102.2 Net profi t 47.5% 1.8% 46.6% 35.1% 15.4%

Adj EPS 47.5% 1.8% 46.6% 35.1% 15.4%Total Equity and Liabilities 12,161.0 13,576.8 15,121.9 15,986.6 16,844.5

ProfitabilityEBITDA margin 15.2% 22.1% 23.8% 24.7% 24.8%

Cash Flow Statement Net profi t margin 9.7% 10.7% 12.4% 14.4% 15.4%FY 31 Jan (RM m) 2012PF 2013F 2014F 2015F 2016F Effective tax rate 15.4% 15.0% 15.0% 15.0% 15.0%

Return on assets 3.7% 3.4% 4.5% 5.4% 5.9%Pretax profi t 688.1 726.0 978.9 1,264.2 1,428.6 Return on equity 8.9% 7.7% 10.3% 11.2% 11.6%Depreciation & amortisatio 64.7 189.7 289.7 339.7 389.7 Change in working capi ta l 97.6 (159.2) (72.0) (20.9) (31.3) LeverageNet interest received / (pa i (61.3) (163.5) (177.0) (156.0) (145.5) Tota l debt / tota l assets 37.0% 40.1% 39.0% 34.7% 30.9%Tax pa id (90.4) (108.9) (146.8) (189.6) (214.3) Tota l debt / equity 87.9% 90.4% 89.8% 75.9% 63.8%Others (70.7) 42.3 28.3 (30.1) (109.3) Net debt / equity 46.4% 38.1% 53.7% 48.0% 41.7%Operating Cash Flow 628.0 526.3 901.0 1,207.3 1,317.9

Key DriversCapex (690.4) (2,500.0) (2,000.0) (1,000.0) (1,000.0) FY 31 Jan 2012PF 2013F 2014F 2015F 2016FOthers - - - - - - Investing Cash Flow (690.4) (2,500.0) (2,000.0) (1,000.0) (1,000.0) EPCC new orderbook - 300.0 1,200.0 2,000.0 2,500.0

IPF avg charter (RMk/day) - 985.7 942.9 930.0 908.3Issuance of shares - 2,148.0 - - - IPF avg charter (RMk/day) - 416.2 421.0 430.9 430.9 Changes in borrowings 628.3 950.0 450.0 (350.0) (350.0) Dividend pa id - (92.6) (135.7) (183.4) (211.6) ValuationOthers - - - - - FY 31 Jan 2012PF 2013F 2014F 2015F 2016FFinancing Cash Flow 628.3 3,005.4 314.3 (533.4) (561.6)

EPS (sen) 9.1 9.2 13.6 18.3 21.1

Net cash flow 565.9 1,031.8 (784.7) (326.1) (243.6) Adj EPS (Sen) 9.1 9.2 13.6 18.3 21.1Forex (36.6) - - - - P/E (x) 26.0 25.5 17.4 12.9 11.2Beginning cash 1,595.1 2,124.4 3,156.2 2,371.4 2,045.3 EV/EBITDA (x) 20.4 15.2 12.3 10.2 9.5Ending cash 2,124.4 3,156.2 2,371.4 2,045.3 1,801.7

Net DPS (sen) - 1.8 2.7 3.7 4.2Net dividend yield % 0.0 0.8 1.1 1.6 1.8

BVPS (RM) 1.02 1.20 1.31 1.46 1.63*PF - ProForma P/BV (x) 2.3 2.0 1.8 1.6 1.4

Price Date: 21 September 2012

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

20

DISCLOSURE Stock rating definitions Strong buy - High conviction buy with expected 12-month total return (including dividends) of 30% or more Buy - Expected 12-month total return of 15% or more Neutral - Expected 12-month total return between -15% and 15% Sell - Expected 12-month total return of -15% or less Trading buy - Expected 3-month total return of 15% or more arising from positive newsflow. However, upside may not be sustainable Sector rating definitions Overweight - Industry expected to outperform the market over the next 12 months Neutral - Industry expected to perform in-line with the market over the next 12 months Underweight - Industry expected to underperform the market over the next 12 months Commonly used abbreviations Adex = advertising expenditure EPS = earnings per share PBT = profit before tax bn = billion EV = enterprise value P/B = price / book ratio BV = book value FCF = free cash flow P/E = price / earnings ratio CF = cash flow FV = fair value PEG = P/E ratio to growth ratio CAGR = compounded annual growth rate FY = financial year q-o-q = quarter-on-quarter Capex = capital expenditure m = million RM = Ringgit CY = calendar year M-o-m = month-on-month ROA = return on assets Div yld = dividend yield NAV = net assets value ROE = return on equity DCF = discounted cash flow NM = not meaningful TP = target price DDM = dividend discount model NTA = net tangible assets trn = trillion DPS = dividend per share NR = not rated WACC = weighted average cost of capital EBIT = earnings before interest & tax p.a. = per annum y-o-y = year-on-year EBITDA = EBIT before depreciation and amortisation PAT = profit after tax YTD = year-to-date

Initiating Coverage | SapuraKencana Petroleum | 24 September 2012

21

DISCLAIMER This report has been prepared for information purposes only by Alliance Research Sdn Bhd (Alliance Research), a subsidiary of Alliance Investment Bank Berhad (AIBB). This report is strictly confidential and is meant for circulation to clients of Alliance Research and AIBB only or such persons as may be deemed eligible to receive such research report, information or opinion contained herein. Receipt and review of this report indicate your agreement not to distribute, reproduce or disclose in any other form or medium (whether electronic or otherwise) the contents, views, information or opinions contained herein without the prior written consent of Alliance Research. This report is based on data and information obtained from various sources believed to be reliable at the time of issuance of this report and any opinion expressed herein is subject to change without prior notice and may differ or be contrary to opinions expressed by Alliance Research’s affiliates and/or related parties. Alliance Research does not make any guarantee, representation or warranty (whether express or implied) as to the accuracy, completeness, reliability or fairness of the data and information obtained from such sources as may be contained in this report. As such, neither Alliance Research nor its affiliates and/or related parties shall be held liable or responsible in any manner whatsoever arising out of or in connection with the reliance and usage of such data and information or third party references as may be made in this report (including, but not limited to any direct, indirect or consequential losses, loss of profits and damages). The views expressed in this report reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendation(s) or view(s) in this report. Alliance Research prohibits the analyst(s) who prepared this report from receiving any compensation, incentive or bonus based on specific investment banking transactions or providing a specific recommendation for, or view of, a particular company. This research report provides general information only and is not to be construed as an offer to sell or a solicitation to buy or sell any securities or other investments or any options, futures, derivatives or other instruments related to such securities or investments. In particular, it is highlighted that this report is not intended for nor does it have regard to the specific investment objectives, financial situation and particular needs of any specific person who may receive this report. Investors are therefore advised to make their own independent evaluation of the information contained in this report, consider their own individual investment objectives, financial situations and particular needs and consult their own professional advisers (including but not limited to financial, legal and tax advisers) regarding the appropriateness of investing in any securities or investments that may be featured in this report. Alliance Research, its directors, representatives and employees or any of its affiliates or its related parties may, from time to time, have an interest in the securities mentioned in this report. Alliance Research, its affiliates and/or its related persons may do and/or seek to do business with the company(ies) covered in this report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell or buy such securities from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory or underwriting services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report. AIBB (which carries on, inter alia, corporate finance activities) and its activities are separate from Alliance Research. AIBB may have no input into company-specific coverage decisions (i.e. whether or not to initiate or terminate coverage of a particular company or securities in reports produced by Alliance Research) and Alliance Research does not take into account investment banking revenues or potential revenues when making company-specific coverage decisions. In reviewing this report, an investor should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additional information is, subject to the overriding issue of confidentiality, available upon request to enable an investor to make their own independent evaluation of the information contained herein. Published & printed by: ALLIANCE RESEARCH SDN BHD (290395-D) Level 19, Menara Multi-Purpose Capital Square 8, Jalan Munshi Abdullah 50100 Kuala Lumpur, Malaysia Tel: +60 (3) 2692 7788 Fax: +60 (3) 2717 6622 Bernard Ching Email: [email protected] Executive Director / Head of Research

Related Documents