KDN PP 7705/05/2012 (029799) 2014 progress through sharing IN TOUCH IN TOUCH An exclusive publication for Members of The Institute of Internal Auditors Malaysia www.iiam.com.my 2012/2013 Graduation & Corporate Awards Ceremony KPMG Malaysia’s Fraud, Bribery and Corruption Survey 2013 JAN – MAR 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

KDN PP 7705/05/2012 (029799)

2014 progress through sharingIN TOUCHIN TOUCH

An exclusive publication for Members of The Institute of Internal Auditors Malaysiawww.iiam.com.my

2012/2013 Graduation & Corporate Awards Ceremony

KPMG Malaysia’s Fraud, Bribery and Corruption Survey 2013

JAN – MAR 2014

editorsays

contents

1 I Keeping In Touch

President Ranjit SinghMBA (UK), CRMA, CMIIA, CA (M), CPA (M)

Vice Presidents Philip Satish RaoCMIIA, CPA (AUST), CPA (M), CA (M)

Shabaruddin Ibrahim MIA, MICPA, FCA, CFIIA

Hon. Secretary Lucy Wong Kam YangMBA (AUST), CIA, CMIIA, CRMA, FCMA, CGMA, CA(M)

Hon. Treasurer Mohamed Farook NasarMBA(USM), CIA, CRMA, CMIIA, ICSA (UK)

Governors Christine Ong May Ee, B.ACC (HONS) (SG), CIA, CRMA, CMIIA, FCA (AUST), CA (M) Nickson Choo Wei SinB.ACC (HONS), CMIIA, CISA, CFE, CA (M)

Devanesan EvansonLLB (HONS) (UK), CFIIA, CA (M), FCCA (UK)

Mohd Khaidzir ShahariBACC (HONS), CIA, CMIIA, CA (M)

Dr Nurmazilah Dato’ MahzanPHD (UK), CIA, CRMA, CMIIA, CA (M), CPA (M)

Zahran TaslimanB.ACC (HONS), CIA, CCSA, CMIIA

Alan Chang Kong ChongB.ECONOMICS (AUST), CIA, CFSA, CPA (AUST), CCP (IBBM)

Nik Hasnan Nik Abd KadirBSC (HONS), CIA, CMIIA

CHAIRMAN Sarawak District Society Woo Yoke Meng CFIIA Auditor Baker Tilly Monteiro HengSolicitor KC Lim & Co STAFFExecutive Director / Nur Hayati BaharuddinTechnical Director MBA, CIA, CCSA, CFSA, CGAP, CRMA, CMIIA,

FCPA, CA(M)

Senior Certification Manager Zaimah Ismail BBA(Hons), AIIA

Senior Technical Manager Sivamalar ThuraisingamBA(Hons)(UK), CIA, CCSA,CMIIA

Senior Finance Manager Lee Fook Sun MAcc(Aust), CMIIA, CA(M), CRMA

Technical Manager Tengku Idreena Tuan Ismail BA(Hons)

Assistant Manager Jess Liu Shiak Peng B.Com(Aust) – Corporate Services Assistant Manager Siti Rohani Umar BA(Hons) – Membership Assistant Manager Irwan Noor Hadi Dahili B.Comm(Hons) – Professional Development Assistant Manager – Technical Vinitha Tanialnathan MBA (Finance)

Senior Certification Executive Siti Arafah Abdul Aziz BSc(Hons)

Accounts Executive Jessie Liew Siau Yan BA(Hons)

Accounts Executive Sally Goh Syed LeeTraining Executive Josie R. OmildaTraining Executive Mohammad Faiz Fauzi BBA (Finance)

Training Executive Mohammad Akmal Hakim Akram BBA (Finance)

Membership Executive Nor Shazwani Mohamad Shafiee BMgt(Hons)

Membership Executive Noor Adiha Abu Bakar BBA(Hons)

Administrative Executive Raja Nur Aina Raja Mohammad Noordin B.Econ(Hons)

Admin Officer Nur Zuhairah Zamberi BSc(Hons)

Admin Officer Yusliza Md YusofAdmin Officer Syazana Dzulkefli BBA(Hons)

Training Officer Ahmad Farouk RosmanDespatch Cum Office Assistant Hamdani Mohd Sahit Mashud

EDITORIAL BOARDPSC Chairman Lucy Wong Kam Yang MBA (AUST), CIA, CRMA, CMIIA, FCMA, CGMA, CA(M)

Deputy Chairman Zahran Tasliman B.Acc (Hons), CIA, CCSA, CMIIA

Chief Editor Dr Suresh Kannan PHD, MBA, BA (Hons) Acc, CMIIA

Committee Members P. Shanthi Palaniappan CIA, CMIIA

Sky Chan Kin Kwan B.ACC (Hons), CIA, CMIIA

Abdul Azim Abd Jalil BSc (Hons), AIIA

Production & Circulation Zaimah Ismail BBA (Hons), AIIA

Siti Rohani Umar BA (Hons)

Nor Shazwani Mohamad Shafiee BMgt (Hons)

Noor Adiha Abu Bakar BBA (Hons)

THE INSTITUTE OF INTERNAL AUDITORS MALAYSIA160-3-3 Kompleks Maluri, Jalan Jejaka,Taman Maluri, 55100 Kuala Lumpur, Malaysia.Tel: (603) 9282 1148 Fax: (603) 9282 1241E-mail: [email protected] Website: www.iiam.com.my

Printed by: PENCETAK WENG FATT SDN BHD (19847-W)

Lot 6, Lorong Kilang A, Off Jalan Kilang, 46050 Petaling Jaya, Selangor Darul Ehsan.

BOARD OF GOVERNORS AND STAFF2013/2014

On 21 March 2014, the Institute held its Graduation and Corporate Award Ceremony 2012/2013. Amongst the recipients for the Corporate Awards are RHB Bank Berhad, Sime Darby Berhad, UMW Corporation Sdn Bhd, Tenaga Nasional Berhad, Lembaga Hasil Dalam Negeri Malaysia, Ernst & Young, KPMG, Crowe Horwath Governance Sdn Bhd, Columbus Advisory Sdn Bhd, QSR Brands (M) Holdings Sdn Bhd, Nestle Products Sdn Bhd and Prokhas Sdn Bhd.

On the same day, 41 CIA, 1 CCSA, 1 CFSA and 2 CRMA graduates who attended the Graduation received their scrolls from Paul Sobel, Chairman of the Board of Directors, IIA Global. The Past President Award went to Neoh Mii Tze. Congratulations to all the graduates on their achievement.

Also featured in the membership column of this newsletter is a brief on the two networking sessions, one held in Kuala Lumpur and the other in Johor Baru. Also in the same column is the reminder to members who may have overlook on their annual subscription to the institute. The Institute has four easy methods of payment.

The training schedule for the April, May and June 2014 is published in this newsletter. Check out the trainings that you wish to attend.

Happy reading

Dr Suresh KannanChief Editor

VISIONTo be the national voice of the internal audit profession: Advocating its value, promoting best practices, and providing exceptional service to its members.

MISSIONTo provide dynamic leadership for the global profession of internal auditing. Activities in support of this mission will include: • Advocating and promoting the value that internal audit professionals add to their

organisations; • Providing comprehensive professional educational and development opportunities;

standards and other professional practice guidance; and certification programmes; • Researching, disseminating, and promoting to practitioners and stakeholders

knowledge concerning internal auditing and its appropriate role in control, risk management, and governance;

• Educating practitioners and other relevant audiences on best practices in internal auditing; and

• Bringing together internal auditors to share information and experiences.

OBJECTIVES1. To be the recognised voice for the internal audit profession;2. To develop and sustain the internal audit profession in Malaysia through appropriate

infrastructure, coordination, support and communication; and3. To provide exceptional service to IIA Malaysia’s members.

MOTTO : “PROGRESS THROUGH SHARING”The Institute maintains its motto “Progress Through Sharing” and share with our members information on new trends, latest internal audit techniques, regulatory and statutory requirements and the emerging issues affecting the profession.

New Releases 2Membership 3Academic Relations 7Professional Development 10Technical 12

editor says

newreleases

Value and Competency –�e Stakeholder PerspectiveThe Institute of Internal Auditors R e s e a r c h Foundation (IIARF) undertook this research project to

obtain stakeholder perspectives on internal audit competency levels and the value internal audit brings to organisations.

Both internal auditors and stakeholders were asked to respond to an identical survey that listed 25 measures for competencies, including attributes such as communication, confidentiality, and risk identification. The survey also asked respondents to rate internal audit value through various measures, such as role in developing management, visibility, level of respect in the organisation, ability to initiate change, and overall performance.

Responses were obtained from 993 internal auditors from IIA membership and 185 stakeholders from contacts made by IIARF committees and the research team.

The results regarding competencies were analysed from two different perspectives:1. which competencies were rated higher/

lower, and 2. which competencies showed the largest

rating gap between internal auditor and stakeholder perspectives.

The competencies with the higher ratings were:• Ethics• Confidentiality• Objectivity• Professionalism

Notably, more than 90% of all respondents rated internal audit as very good or excellent for both ethics and confidentiality.

The competencies with lower ratings were:• Conflict resolution/negotiation skills• Business process analysis• Ability to demonstrate/promote the value of

the internal audit function• Data collection and analysis tools and

techniques

The competencies where stakeholders gave internal auditors a significantly lower rating than the internal auditors gave themselves were:• Understanding the business• Business process analysis• Problem-solving skills• Problem-identification skills• Judgment• Objectivity

The responses to measures about internal audit value showed that the value of internal audit was recognised overall, but there was also room for improvement. In other words, significant percentages of both stakeholders and internal auditors chose a rating of 3 on a scale of 1 to 5 for questions about internal audit value, visibility, respect, and overall performance.

Other measures of value were ability to initiate change and use of internal audit as a management training ground. Respondents indicated that changes were implemented in response to about 5 out of 10 of the audits in which they were involved. Internal audit was not used extensively as a training ground for management in the survey respondents’ organisations.

The findings about competency and value from this report can be used by internal auditors and stakeholders to promote professional growth and achieve organisational objectives.

The latest project from The IIA R e s e a r c h Foundation shares career insights and the legacy of one of the profession’s own, Richard F. Chambers. Lessons

Learned on the Audit Trail chronicles his career in internal auditing. Chambers offers strong advice as he recounts the most defining moments in his distinguished career. His journey on the audit trail spans nearly 40 years with stops in both government and the corporate sector and, since 2009, as President and CEO of The Institute of Internal Auditors. In Lessons Learned on the Audit Trail, his first book release, Chambers shares many of the key events and insights gained during his impressive career, as well as valuable lessons he learned along the way. Richard F. Chambers, CIA, CGAP, CCSA, CRMA, candidly recounts personal experiences to illustrate critical lessons that every internal auditor will likely learn during their own journeys in the profession.

“I have learned a number of important lessons in my career — some early on, some much later,” Chambers says. “The paradox of what you pick up later in life is you have less time to apply those lessons. But if I can help just one internal auditor become better prepared for the challenges and opportunities that lie ahead in this profession, then my efforts writing this book will be well worth it.”

Chambers imparts life-based lessons on such vital topics as the importance of:• Building and sustaining relationships with

internal audit stakeholders • Demonstrating value • Deploying risk-based audit planning and

the dynamic nature of risk • Achieving and sustaining a “seat at the

table”

Chambers’ career is unique in so many ways — across government and private and not-for-profit sectors — that there are sure to be key takeaways for new and seasoned practitioners alike. “Whether it’s in internal auditing or life in general,” Chambers writes, “we all aspire to make this world a better place, even if only in small ways.”

While there are many lessons yet to be learned, Chambers’ insight will help better prepare those entering the internal audit profession for the challenges and numerous opportunities that lie ahead.

“Every internal audit professional wants to look back on their career with the satisfaction of knowing our work made a signi�cant di�erence.” – Richard Chambers

Keeping In Touch I 2

Lessons Learned on the Audit Trail

IIA Malaysia members can purchase ‘Lessons Learned on the Audit Trail’ at an introductory price of RM100 per copy. This offer is valid until 30 April 2014 or while stocks last.

Tel : 603-92821148 E-mail : [email protected]

For further inquiries, please contact Idreena (ext. 119)

INTRODUCTORY OFFER -Get your copy now !

membership

3 I Keeping In Touch

WELCOMENew Members from January - March 2014Professional MembersOoi Soh Yeep 210014Tam Kok Meng 210108Lau Min Wei 210112Mohamed Razib Mohamed Agil 210114Norhayati Maamor 210115Lalitha A/P Ponnudurai 210153Lee Chong Leng 210154Ms Chan Wan Theng 210163 Associate MembersRajesh A/L Tarasia Singh 210010Nahzatul Shareena Sharifuddin 210011Mohd Izam Mispardi 210012Azli Aliuddin 210015Tan Sook Looi 210016Tan Hui Xian 210017Caryn Goh Loo Hui 210018Ghazana Said Atan 210019Mohd Khalid Mustafa 210020Aris Fadzillah Zulkifli 210021Shah Rizal Hidayat Shariff 210022Mohd Shahril Ahmad 210023Meor Mohamed Mustaqim 210024 Mohamed Khairi Nur Shahida Abdul Jamil 210025Yuvaraj A/L Ganesan 210026Tan Lee Hua 210027Kuhan A/L Muniandy 210028Wong Poh Wei 210029Haizul Idham Rahman 210030Nurul Ain Abu Zarin 210031Ngu Yii Ee 210032Nazmirul Nanyan 210033Nor Saadah Hasan 210034Nurbazlina Mohd Nasir 210035Nik Zulkifli Nik Setapa 210036Jarolhidah Chemiran 210037Sulaiman Saiban 210038Thomas A/L M A E Abraham 210039Julian Suresh A/ L J. P Amarasena 210040Shamsul Adzmir Abdullah Halim Kamil 210041Siti Salwa Ismail 210042Lim Ker Wei 210043Low Ern Tze 210044Mohd Kamil Hafidz Sharifuddin 210045Mohd Aizuddin Mohammad Shamshuri 210046Nurul Fazidatul Akma Abd Jalil 210047Shalini A/P Thiruchelvam 210048Peter Simon Anak Lingam 210049Julie Huang Ying 210050Nicole Lee Ai Sym 210051Mohd Hidayat Mohd Hussein 210052Azmi Muhamad 210053Nurul Faizal Mohd Dan 210054Norazhar Mohd Sharif 210055Khairizal Ab Karim 210056Mohd Izzuwan Mohd Natzri 210057Mohd Irwan Mohd Hashim 210058Mohd Badli Shah Mohd Said 210059Shaharudin Mohd Sa’ad 210060Sathisveran A/L Palakrisnan 210061Norhanisah Hussin 210062John Edward Arkosi 210063Vinothini A/P Perampalam 210064Masdiah Abdul Hamid 210065Ng Munn Yinn 210066Andrea Chong Hon Ngian 210067

Muhammad Asyraf Rosli 210068Carrie Teo Ching Shi 210069Lionel Jovenes Anak Jolly 210070Lim Jiun Horng 210071Ho Pei Wah 210072Saufi Izwan Ishak 210073Saifullah Nadzarawi 210074Dr Fathyah Hashim 210075Zairulzahairy Zainol 210076Nur Hazirah Mohamad Helmi 210077Wan Nor Azmina Wan Daud 210078Priya Devi A/P Paramanathan 210079Chew Joo Khoon 210080Wajahat Umar Pirzada 210081Ng Yuen Heng 210082Siau Wui Kee 210083Datuk Lim Siong Eng 210084Kevin How Kow 210085Petrus Gimbad 210086Low Yuen Mun 210087Salina Sidek 210088Ahmad Zawawi Jamal 210089Narayanan A/L Gunasegaran 210090Lee Jun Xian 210091Norhayati Ahmad 210092Jasmine Minotty Anak Akaw 210093Nazreen Ali 210094Lau Wei Ping 210095Khoo Li Lin 210096Nik Norisra Nik Norzlan Thani 210097Siti Aisyah Abu Kasim 210098Bernard Loh Kok Leong 210099Tang Chi Ming 210100Hazwan Awang Kechik 210101Mohd Yusri Karim 210102Tan Kim Leong 210103Norhaliana Khalil 210104Benedict Kiong Chong Soon 210105Muhamad Sabri Said 210106Leong Kah Mun 210107Sabarina Mohammed Shah 210109Ahmed Tirmizi Abdul Jalil 210110Mohamad Fadli Nor Ramli 210111Valerie Sung Pei Woon 210113Mohd Sidki Hassan 210116Adnan Khalid Ali 210117Lee Bee Suet 210118Cherylyn Tan ‘G’ Min 210119Premalatha A/P Thangaraj 210120Mohd Yusof Ismail 210121Rozarina Shahri 210122Nur Hazlina Muhammad 210123Fauzi Pin 210124Muhammad Syafiq S.M. Abdul Wahid 210125Siew Bee Pei 210126Thinakaran A/L Kannan 210127Ms Wong Fung Shien 210128Sri Ganesh A/L Sivananthan 210129Koh Mei Sin 210130Renee Siew Pik Yee 210131Abd Karim Ahmad 210132Mohd Sukri Ramlee 210133Vinitha A/P Tanialnathan 210134Johariah Urib Mohd Ariffin 210135Mohamad Muzhafar Mazmi 210136Mohd Fazrin Rahman 210137Noor Farahana Roselan 210138Ngu Ling Yen 210139

Saudah Ahmad 210140Abdul Aziz Affendi 210141Mohd Izray Ibrahim 210142Nor Hamizah Abdul Hamid 210143Noor Azman Hafeez Rozly-Azni 210144Mohd Asrul Affendi Ab Jalil 210145Fiezatin Ambran 210146Ahmad Faizal Abdullah 210147Mohd Farid Nazmi Mohamed 210148Ummu Ummairah Yusuf 210149Yang Ayuni Shazwani Mohamad Habali 210150Redhalina Abdullah 210151Pu Shuan How 210152Julia Idaly Mohd Yusof 210155Lim Chee Sin 210156Salwa Faharudin 210157Nurhafizah Hamzah 210158Abang Fiqry Ruzail Basri 210159Yazkhiruni Yahya 210160Thau Yu Liang 210161Mohd Ismail Ibrahim 210162Anne Ting Ai Nee 210164

Student MemberYahya Zakaria 210013

Upgraded MembersSunil Rajamony 207943Syed Jamalludin Syed Osman 206869Lee Eng Choon 209349Lee Ee-Leng 208968Loh Seong Yew 207732Cheu Teck Hee 208539Saifol Azman Ahmad Tauffik 208686Soh Chee Wei 208889Kausalyah A/P Nookaiah 209690

Corporate MembersGenting Plantations Berhad C0403IIUM Holdings Sdn Bhd C0404Majlis Perbandaran Johor Bahru Tengah C0405Bridge Corporate Advisory Sdn Bhd C0406Majlis Pebandaran Ampang Jaya C0407

Members with writing talent, here’s the opportunity to share your thoughts with your friends in the internal audit fraternity. The Editorial Board welcomes contributions from members. We accept articles, short stories, jokes, tips, etc.

We encourage submission of fraud findings and audit stories that reflect the new age of internal auditing – those that emphasise best practices, use of technology and value-added results. If your article is published, you will be awarded a token from IIA Malaysia.

We need your contributions!

Keeping In Touch I 4

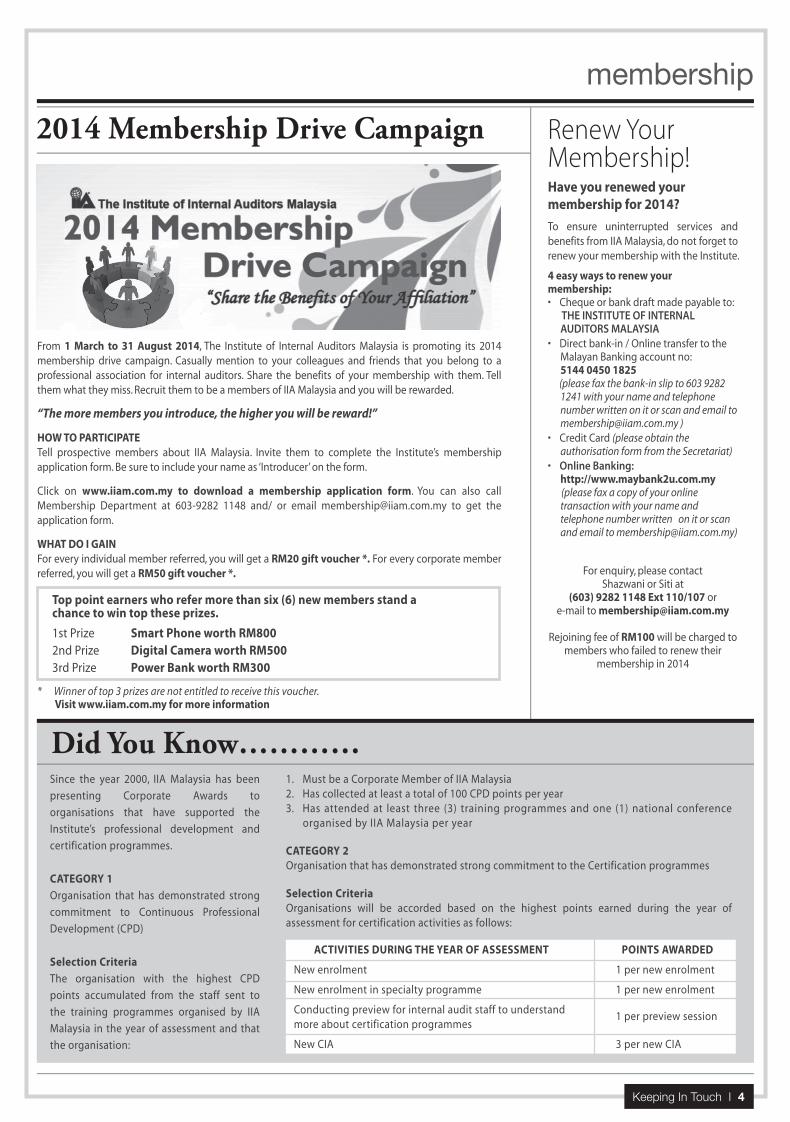

2014 Membership Drive Campaign

Did You Know…………

Have you renewed your membership for 2014?To ensure uninterrupted services and benefits from IIA Malaysia, do not forget to renew your membership with the Institute.

4 easy ways to renew your membership:• Cheque or bank draft made payable to: THE INSTITUTE OF INTERNAL

AUDITORS MALAYSIA• Direct bank-in / Online transfer to the

Malayan Banking account no: 5144 0450 1825

(please fax the bank-in slip to 603 9282 1241 with your name and telephone number written on it or scan and email to [email protected] )

• Credit Card (please obtain the authorisation form from the Secretariat)

• Online Banking: http://www.maybank2u.com.my

(please fax a copy of your online transaction with your name and telephone number written on it or scan and email to [email protected])

For enquiry, please contact Shazwani or Siti at

(603) 9282 1148 Ext 110/107 or e-mail to [email protected]

Rejoining fee of RM100 will be charged to members who failed to renew their

membership in 2014

Renew Your Membership!

* Winner of top 3 prizes are not entitled to receive this voucher.Visit www.iiam.com.my for more information

1st Prize Smart Phone worth RM8002nd Prize Digital Camera worth RM5003rd Prize Power Bank worth RM300

Top point earners who refer more than six (6) new members stand a chance to win top these prizes.

ACTIVITIES DURING THE YEAR OF ASSESSMENT POINTS AWARDED

New enrolment 1 per new enrolment

New enrolment in specialty programme 1 per new enrolment

Conducting preview for internal audit staff to understand 1 per preview session

more about certification programmes

New CIA 3 per new CIA

Since the year 2000, IIA Malaysia has been

presenting Corporate Awards to

organisations that have supported the

Institute’s professional development and

certification programmes.

CATEGORY 1Organisation that has demonstrated strong

commitment to Continuous Professional

Development (CPD)

Selection Criteria The organisation with the highest CPD

points accumulated from the staff sent to

the training programmes organised by IIA

Malaysia in the year of assessment and that

the organisation:

1. Must be a Corporate Member of IIA Malaysia2. Has collected at least a total of 100 CPD points per year 3. Has attended at least three (3) training programmes and one (1) national conference

organised by IIA Malaysia per year

CATEGORY 2Organisation that has demonstrated strong commitment to the Certification programmes

Selection Criteria Organisations will be accorded based on the highest points earned during the year of assessment for certification activities as follows:

membership

From 1 March to 31 August 2014, The Institute of Internal Auditors Malaysia is promoting its 2014 membership drive campaign. Casually mention to your colleagues and friends that you belong to a professional association for internal auditors. Share the benefits of your membership with them. Tell them what they miss. Recruit them to be a members of IIA Malaysia and you will be rewarded.

“The more members you introduce, the higher you will be reward!”

HOW TO PARTICIPATETell prospective members about IIA Malaysia. Invite them to complete the Institute’s membership application form. Be sure to include your name as ‘Introducer’ on the form.

Click on www.iiam.com.my to download a membership application form. You can also call Membership Department at 603-9282 1148 and/ or email [email protected] to get the application form.

WHAT DO I GAINFor every individual member referred, you will get a RM20 gift voucher *. For every corporate member referred, you will get a RM50 gift voucher *.

membership

5 I Keeping In Touch

MEMBERS’ NETWORKING SESSION IN KUALA LUMPUR

“Contemporary Issues Relating to Internal Audit”

“Fraud”

On 12th March 2014, IIA Malaysia organised a

Beginning Auditors Networking Session for

members at IIA Malaysia Training Hall with a

turnout of 24 participants. The session was held

for members to meet and share information.

The networking was started with the

ice-breaking session conducted by Dr Suresh N

Kannan. After the ice-breaking session, Zahran

Tasliman, Governor, IIA Malaysia & Chief Audit

Executive of QSR Brands (M) Holdings Sdn Bhd

gave an informative talk on “Contemporary

Issues Relating to Internal Audit” and was

followed by a question and answer session. The

evening concluded with an opportunity for the

participants and speakers to network while

enjoying refreshments.

Zahran Tasliman presented a talk

The participants listening attentively to the speaker’s explanation

MEMBERS’ NETWORKING SESSION IN JOHOR IIA Malaysia organised a Members’

Networking Session at Tanjong Puteri Golf

Resort Berhad on 24 March 2014. The

networking session saw 28 participants

attending the session. Devanesan Evanson,

Past President & Governor of IIA Malaysia gave

a talk on “FRAUD” to the audience. After the

talk and a questions and answers session,

participants and speakers enjoyed an

opportune time to further network with one

another during the refreshment.

Devanesan Evanson presented a talkParticipants listening to the presentation with interest

DisclaimerOpinions expressed herein do not necessary represent those of IIA Malaysia. Neither IIA Malaysia or the Editorial Board is responsible for the

accuracy of any statement, opinion or advice contained herein. Readers should rely on their own due diligence in making decisions concerning any

matter herein. All materials in any form contained herein are copyrighted by IIA Malaysia. Reproduction and/or storage and/or retrieval in whole or

part in whatsoever manner is not permitted without the written consent from IIA Malaysia.

Publisher : The Institute of Internal Auditors Malaysia

Typesetting : Bluefish Design

Keeping In Touch I 6

2012/2013 Corporate Award

membership

From left to right: Wong Yih Yin, Chief Internal Auditor, RHB Bank Berhad; Nik Maziah Nik Musthapa, Head, Group Corporate Assurance, Property Division, Sime Darby Berhad; Ahmad Al Juhari Darman, Senior General Manager, Internal Audit, UMW Corporation Sdn Bhd; Rosli Mohd Rose, Acting Chief Internal Auditor, Tenaga Nasional Berhad; Abd Aziz Hashim, Deputy CEO, Lembaga Hasil Dalam Negeri Malaysia; Lee Min On, Partner, KPMG; Lucy Wong, Chairman, Professional Services Committee of IIA Malaysia; Paul Sobel, Chairman, Board of Directors, IIA Global; Ranjit Singh, President of IIA Malaysia; Amos Law, Associate Director, Crowe Horwath Governance Sdn Bhd; Derek Lee, Executive Director, Columbus Advisory Sdn Bhd; Noor Aini Ismail, Manager, Internal Audit, Prokhas Sdn Bhd; Lydia Ong, Operational Auditor, Nestle Products Sdn Bhd; Kamaruldzaman Salleh, Chief Corporate Services, QSR Brands (M) Holdings Sdn Bhd, Sandra Stephanie Theraviam, Executive Director, Ernst & Young.

Since the year 2000, IIA Malaysia has been

presenting Corporate Awards to organisations

that have supported the Institute’s professional

development and certification programmes.

At the recent 2012/2013 Graduation and

Corporate Award Ceremony held on 21 March

2014, The Institute honoured various

organisations for their support in 2012 and

2013. Ranjit Singh, President of IIA Malaysia

accompanied by Lucy Wong, Chairman of the

Professional Services Committee presented the

following awards to the recipients in the

respective organisations:

CATEGORY 1 Organisation that has demonstrated strong

commitment to Continuous Professional

Development (CPD)

2012 & 2013 Corporate Award

Tier 1 RHB Bank Berhad

Tier 2 Sime Darby Berhad

Tier 3 UMW Corporation Sdn Bhd

Tier 4 Tenaga Nasional Berhad

Public Sector Lembaga Hasil Dalam

Negeri Malaysia

CATEGORY 2Organisation that has demonstrated strong commitment to the Certification programmes

2012 Corporate Award1st Place Tenaga Nasional Berhad2nd Place KPMG3rd Place Crowe Horwath Governance

Sdn Bhd QSR Brands (M) Holdings

Sdn Bhd Nestle Products Sdn Bhd Prokhas Sdn Bhd

2013 Corporate Award1st Place Ernst & Young2nd Place KPMG Columbus Advisory Sdn Bhd3rd Place Sime Darby Berhad

Congratulations

Keeping In Touch I 87 I Keeping In Touch

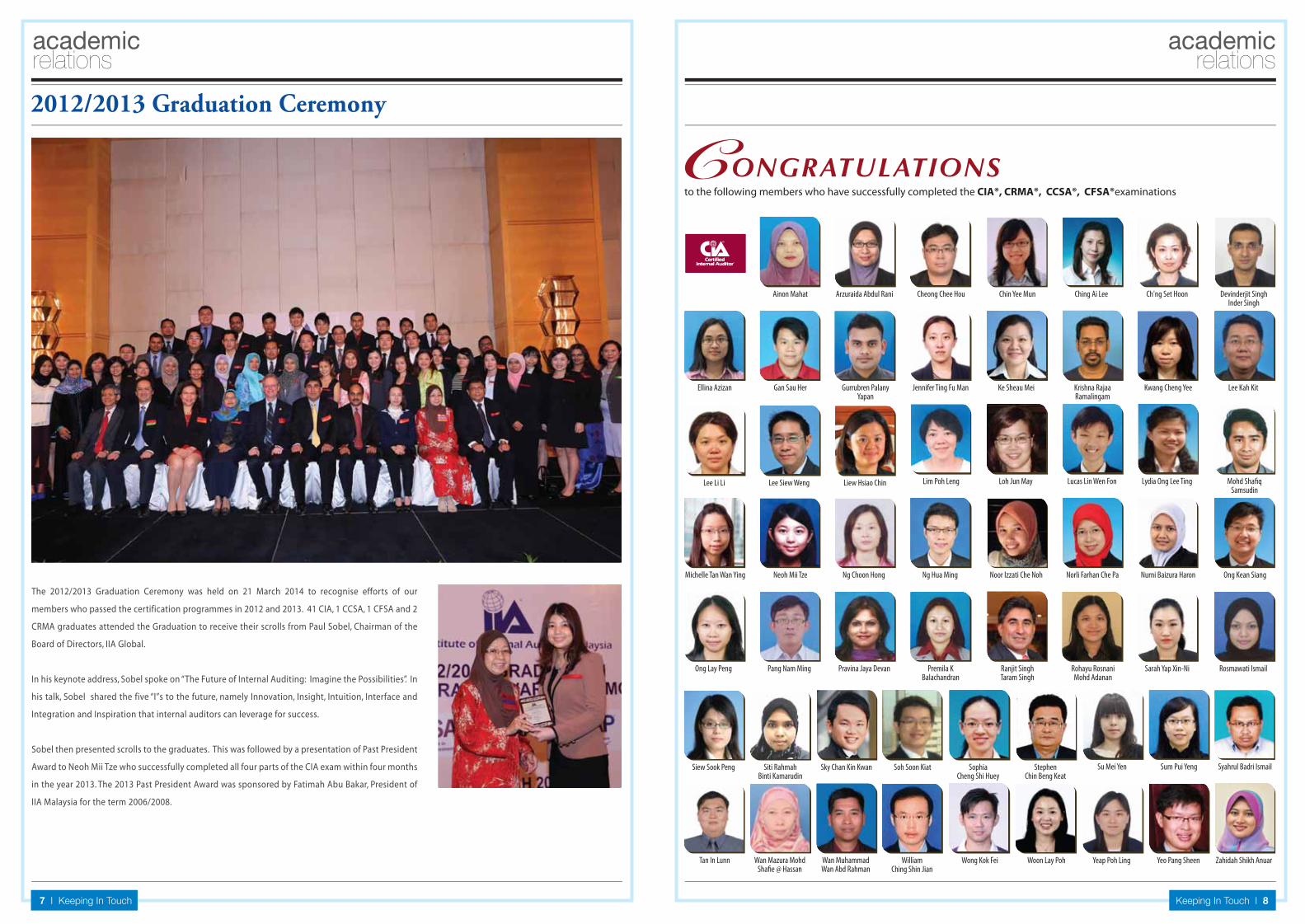

2012/2013 Graduation Ceremony

academicrelations

academicrelations

The 2012/2013 Graduation Ceremony was held on 21 March 2014 to recognise efforts of our

members who passed the certification programmes in 2012 and 2013. 41 CIA, 1 CCSA, 1 CFSA and 2

CRMA graduates attended the Graduation to receive their scrolls from Paul Sobel, Chairman of the

Board of Directors, IIA Global.

In his keynote address, Sobel spoke on “The Future of Internal Auditing: Imagine the Possibilities”. In

his talk, Sobel shared the five “I”s to the future, namely Innovation, Insight, Intuition, Interface and

Integration and Inspiration that internal auditors can leverage for success.

Sobel then presented scrolls to the graduates. This was followed by a presentation of Past President

Award to Neoh Mii Tze who successfully completed all four parts of the CIA exam within four months

in the year 2013. The 2013 Past President Award was sponsored by Fatimah Abu Bakar, President of

IIA Malaysia for the term 2006/2008.

to the following members who have successfully completed the CIA®, CRMA®, CCSA®, CFSA®examinations

ONGRATULATIONSC

Ainon Mahat Chin Yee MunArzuraida Abdul Rani Cheong Chee Hou Ching Ai Lee Ch'ng Set Hoon Devinderjit Singh Inder Singh

Gan Sau Her Gurrubren Palany Yapan

Krishna Rajaa Ramalingam

Kwang Cheng Yee Lee Kah Kit

Lee Li Li Lim Poh Leng Loh Jun May Lucas Lin Wen Fon Lydia Ong Lee Ting Mohd Sha�q Samsudin

Michelle Tan Wan Ying Neoh Mii Tze Ng Choon Hong Ng Hua Ming Noor Izzati Che Noh Norli Farhan Che Pa Nurni Baizura Haron

Ke Sheau MeiJennifer Ting Fu Man

Liew Hsiao ChinLee Siew Weng

Ellina Azizan

Ong Kean Siang

Pravina Jaya Devan Premila K Balachandran

Ranjit Singh Taram Singh

Rohayu Rosnani Mohd Adanan

Rosmawati IsmailSarah Yap Xin-NiOng Lay Peng Pang Nam Ming

Stephen Chin Beng Keat

Su Mei Yen Syahrul Badri Ismail

William Ching Shin Jian

Wong Kok Fei Woon Lay Poh Yeap Poh Ling Zahidah Shikh Anuar

Sum Pui Yeng

Yeo Pang SheenTan In Lunn Wan Mazura Mohd Sha�e @ Hassan

Wan Muhammad Wan Abd Rahman

Siew Sook Peng Sky Chan Kin KwanSiti Rahmah Binti Kamarudin

Sophia Cheng Shi Huey

Soh Soon Kiat

Call us today at +603 9282 1148 or email us at [email protected] www.iiam.com.my for more details

Enhance your professional value with IIA Certifications:• Distinguish yourself from your peers.• Communicate your depth of knowledge in internal auditing.• Demonstrate your ability to provide assurance, insight, and objectivity.

Apply for the Certified Internal Auditor® (CIA®)or one of the IIA’s four specialty certifications today.

ALL OF THE RIGHT PIECES FORYOUR CAREER DEVELOPMENT PUZZLE

9 I Keeping In Touch

academicrelations

IIA Malaysia – Aimst University Sealed A Collaboration

Cheu Teck Hee Khoo Chee Peng Razly Zakaria

Chew Swee Ai Loo Mei Ling

In our pursuit to bring internal audit education in the country to the next level, IIA Malaysia has signed a Memorandum of Understanding with AIMST University to seal collaboration on a new education programme called Bachelor of Internal Auditing and Management.

The MOU was signed by Ranjit Singh, President of IIA Malaysia and Prof Dr Premkumar Rajagopal , Chief Executive & Vice Chancellor of AIMST University. Under this collaboration, IIA

Malaysia and AIMST University shall work together to offer the bachelor’s degree programme, which is targeted to commence in mid 2015.

The bachelor’s degree programme, which will cover internal auditing, management and business subjects will be developed based on the IIA Global Model Internal Audit Curriculum.

The following photographs were not available at the time of printing:• Andrew Chew Soon Lim• Aziah Marzuki• Jon-Michael Chia Eu Jin• Kavitha Subramaniam• Lee Chern Lin• Lim Sing Yieng• Soh Chee Wei• Tay Lang Fang

“Bachelor of Internal Auditing and Management is targeted to commence in mid 2015 at AIMST University”

Keeping In Touch I 10

High Impact Operational Audit of Human Resource Management

Workshop on Forensic Investigations: Practical Workshop for Beginners

Value Added Business Controls: �e Right Way to Manage Risk Workshop

A two-day workshop on Value Added

Business Controls: The Right Way to Manage

Risk took place on 12 & 13 March 2014. The

workshop was conducted by Monnie Goh

and guided the participants on how to use

controls to detect and prevent fraud, design

cost-effective control systems, identify

“hard” and “soft” controls, and analyse

existing control systems. The workshop is

highly recommended for junior internal

auditor.

Corporate Governance Review – Roadmap to Boardroom Presence

This three-day workshop conducted by Stanley

Yap took place at Istana Hotel Kuala Lumpur on 3

- 5 March 2014. The workshop provided

guidance and assistance to internal auditors who

are required to carry out an audit of the

operations in Human Resource Department.

Among others, the workshop covered topics

such as an overview of human resource

management, awareness of the labour law in

Malaysia, how to conduct an operational audit

and etc.

The updated version of Forensic Investigations:

Practical Workshop for Beginners was

successfully held on 26 – 27 February and

attracted 29 participants. The trainer for the

workshop was Suresh D. The two-day workshop

equiped participants with real world

investigative and evidence gathering skills. Upon

completion of the workshop, the participants

should be able to carry out basic investigation

confidently, independently and professionally.

Among the areas covered in the workshop were

fraudster mindset, investigative and interview

techniques and evidence gathering

methodology. It explained how to place

evidence together to prove a breach or abuse of

the law and internal controls and etc.

Corporate Governance workshop was conducted

in collaboration between IIA Malaysia and ACCA

Malaysia. It was conducted at Prince Hotel &

Residence Kuala Lumpur on 10 & 11 March 2014

by Wee Hock Kee. The two-day workshop

provided the participants with a set of practical

tools and techniques for conducting corporate

governance review and how to implement it

within the organisation.

professionaldevelopment

11 I Keeping In Touch

2014 Audit Committee Conference

Beginning Auditor Tools and Techniques Workshop

IIA Malaysia in collaboration with Malaysian Institute of Accountants successfully organised a

conference with theme “Stepping Up for Better Governance” on 20 March 2014. The conference

attracted more than 280 participants comprising directors, members of audit committee and

internal audit practitioners. The objective of the conference was to assist audit committee members

to address practical issues in instilling and maintaining good corporate governance. It was a full day

event packed with information and knowledge sharing sessions that are useful and beneficial to the

participants in dealing with the significant challenges faced by audit committee members today.

This four-day workshop was held at Hotel

Istana Kuala Lumpur on 20-23 January 2014.

The trainer of the workshop was Lee Chew

Foong. Through activities in the workshop such

as team exercises, group discussions, and

trainer’s presentations, participants gained

fundamental knowledge that allowed them to

prepare properly for and conduct a successful

audit, using preliminary surveys and

evidence-gathering techniques. In addition,

basic understanding of how to identify risks

and internal controls in auditing was stressed,

along with interpersonal and team-building

skills.

Workshop on Management Audit Monitoring of Construction ProjectThis workshop previously known as Audit,

Management and Monitoring of Construction

Projects was organised on 10 & 11 February

2014. The workshop was conducted by

Gusharan Singh. Through team exercises,

group discussions, and trainer’s presentations,

participants gained knowledge that would

enable them to highlight the importance of the

need to be aware of the weaknesses and

shortcomings that exist in the construction

industry. These weaknesses and shortcomings

can cause huge direct financial losses to an

organisation and at the same time damage the

company’s reputation. It can also provide

opportunities to create fraudulent situations

and mismanagement that may not be noticed

until it’s too late.

“The objective for this conference is to assist audit committee members to address practical issues in instilling and maintaining good corporate governance.”

Part of speakers for 2014 Audit Committee Conference. From left Ranjit Singh, Poel J Sobel,Datuk Mohd Nasir Ahmad, Megat Mizan Nicholas Denney and Dato’ Sri Che Khalib Mohamad Noh

professionaldevelopment

1. In the survey, it was mentioned that 89% of the respondents felt that the quantum of fraud had increased over the last three years. In your opinion, what are the challenges and opportunities that internal auditors will face by this increase in the quantum of fraud?

Naturally, everyone including internal

auditors will face challenges. This is because the perpetrator is getting smarter. Increasingly IT related fraud and cyber-crime are now a major issue and this calls for internal auditors to be well equipped in skills and tools in this area.

The first step is for internal audit (IA) to educate top management that fraud is a problem that needs to be addressed. IA may play a key role in creating awareness by encouraging training to all employees to understand what ethical and unethical behaviour are. IA has to ensure that the

company has a working, credible and anonymous whistle blowing programme. This is something we find that all multinational companies tend to have. For example, if an employee were to whistle blow in the developed markets, the company would immediately send a team to investigate it.

What I see is that internal auditors would have a greater challenge managing bribery and corrupt practices within their firm. Internal auditors must assess and make appropriate recommendations for improving the governance process. IA should review governance practices and advocate good governance at all levels of management.

2. What can internal auditors do to prepare for this rise of fraud incidents?

All practitioners need to improve

themselves, i.e. up-skilling. If they were to take on the role of fraud investigators, though not as a full scale investigator, they need to equip themselves with fraud detection and investigation tools. For example, for companies in the trading and services sector of listed companies, the numbers of trading transactions are huge and they should have data analytic tools and the skills to use these tools. The advantage of using data analytic software is the ability to analyse large amount of data by running certain routine checks to flag out any irregularity or anomaly. Then the auditor can further investigate the irregular transactions.

IA can play a key role as fraud detector rather than a full scale fraud investigator. This is because forensic investigation and internal audit have different methodologies. For example, internal audit methodology prescribes sampling whereas a forensic investigator would focus on uncovering the evidence relating to the suspicion of fraud. IA can be the main source of identifying possible incidents of frauds if they have the necessary skills. Internal auditors need to understand what the red flags are indicating possible fraud in their industry and make assessment if such red flags do exist. For example in the construction industry, the volume of procurement is huge and so is the value, hence internal auditors need to be well trained to identify business processes that could be affected by procurement fraud.

3. Fraud is said to be linked to poor corporate governance. Could you clarify this statement?

Effective fraud management needs to be a

holistic top down approach. It is important for top management to set the right tone at the top and inculcate the right culture that has zero tolerance of fraud, bribery and corruption. Top management should also ‘walk the talk’ and lead by example by avoiding any unethical or questionable behaviour, such as having a close relationship with a particular supplier or

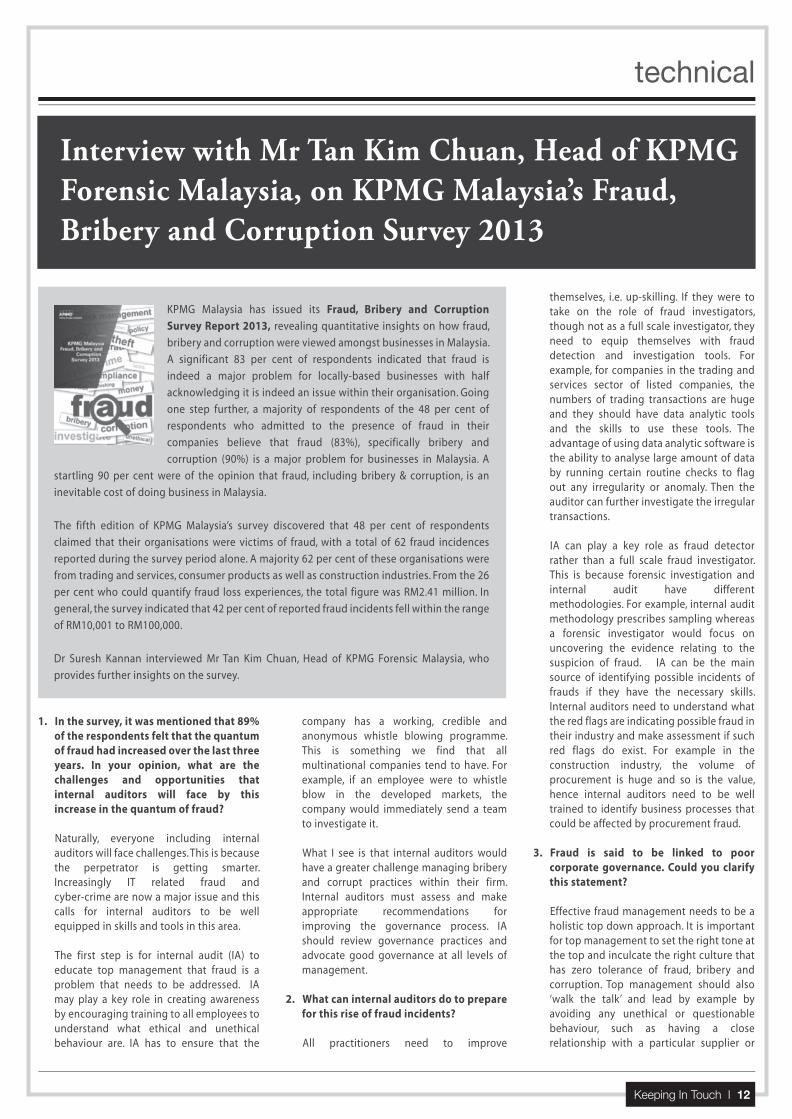

KPMG Malaysia has issued its Fraud, Bribery and Corruption

Survey Report 2013, revealing quantitative insights on how fraud,

bribery and corruption were viewed amongst businesses in Malaysia.

A significant 83 per cent of respondents indicated that fraud is

indeed a major problem for locally-based businesses with half

acknowledging it is indeed an issue within their organisation. Going

one step further, a majority of respondents of the 48 per cent of

respondents who admitted to the presence of fraud in their

companies believe that fraud (83%), specifically bribery and

corruption (90%) is a major problem for businesses in Malaysia. A

startling 90 per cent were of the opinion that fraud, including bribery & corruption, is an

inevitable cost of doing business in Malaysia.

The fifth edition of KPMG Malaysia’s survey discovered that 48 per cent of respondents

claimed that their organisations were victims of fraud, with a total of 62 fraud incidences

reported during the survey period alone. A majority 62 per cent of these organisations were

from trading and services, consumer products as well as construction industries. From the 26

per cent who could quantify fraud loss experiences, the total figure was RM2.41 million. In

general, the survey indicated that 42 per cent of reported fraud incidents fell within the range

of RM10,001 to RM100,000.

Dr Suresh Kannan interviewed Mr Tan Kim Chuan, Head of KPMG Forensic Malaysia, who

provides further insights on the survey.

Keeping In Touch I 12

technical

Interview with Mr Tan Kim Chuan, Head of KPMG Forensic Malaysia, on KPMG Malaysia’s Fraud, Bribery and Corruption Survey 2013

being entertained when travelling abroad on a business trip. They should also create fraud awareness within the management and employees by explaining to them in the language that they can understand.

In assessing the effectiveness of the

company’s fraud control, it is also important to look at an organisation’s control culture in relation to the complexity of the business, the dynamism of the challenges faced by the business and also what were the management’s reaction to past control failures.

4. Please share an experience where the internal auditors detected possible fraud.

There was a case of a company that had

persistent high debtors and the internal auditors had reported this to the audit committee requesting for higher management action. We were called in to investigate this and we started to probe ‘behind’ these debtors and the transactions. We also investigated the background of these debtors and found certain ‘hidden’ transactions that had diverted funds to off-shore accounts controlled by the Managing Director. Our report led to legal recovery actions taken against the perpetrator.

5. What is the state of the internal audit function of Malaysian listed companies in battling fraud?

Internal audit functions in Malaysia are

well versed in the area of internal control but there are still gaps in the area of fraud detection and investigation. Internal auditors need to understand the industries their organisations operate in and exercise healthy scepticism when performing internal audit work.

6. Inadequate skill sets of the internal audit team were mentioned as the second highest reason which allowed for fraud to happen. In your experience, what is the skill set required for the internal audit team in battling fraud?

For example, when examining a transaction, internal auditors need to apply their industry knowledge and question the business justification if it does not make business sense.

At times, internal auditors cannot just accept a document at face value but will need to look behind it to understand the

business transaction. They should question a transaction if it does not make sense i.e. they should refuse to accept a ‘surface explanation’. From experience, often than not fraudulent transactions are concealed by complete documentation to avoid detection to untrained eyes.

Another skill as mentioned earlier is the ability to recognise red flags. When we are called in to investigate a fraud, we have noted that all the documents were previously reviewed by the internal auditors but they had missed noting the fraud red flag in the transaction.

The reality is that we are living in a world where millions of dollars are transacted through a piece a paper. The CEO would sign off millions of dollars of transaction by relying on a spreadsheet prepared by the CFO as companies empower executives and there is a heavy reliance on trust. Internal auditors must have the ability to assess whether those who are put in trust positions really understand the transactions and are not ‘blindly’ signing off. Internal auditors must have a ‘fresh pair of eyes’ when reviewing these transactions.

7. How would you rate the ‘tone at the top’ of managing fraud in corporate Malaysia?

Increasingly, more companies are getting more serious about the tone at the top, especially the GLCs. The GLCs are aware of this issue and would not hesitate to seek external help from both the internal and external auditors to manage these issues. However, there are still a large segment of companies in Malaysia be it listed or non-listed that do not take this issue seriously. There are situations where there were suspected irregularities but management is reluctant to engage external help and are also reluctant to report to the appropriate authorities, perhaps fearing of any negative impact to their reputation. Thus they tend to deal with them internally but if they are not handled properly, they might have problem taking actions against the perpetrator or it would impact their recovery actions. They may just ask the fraudster to resign and this fraudster is likely to join another company. He or she would get smarter from the previous experience and tends to commit another major fraud in the new company.

The right attitude of such companies

should be to inform the authorities such as the police or MACC if it is misappropriation or corruption related matters. Such an attitude will send a strong message to the other employees in the company that committing fraud is not tolerated.

8. The 2013 Fraud Survey had included assessment on bribery and corruption. Could you share the rationale for this inclusion?

The issue of bribery and corruption is topical and we had discussed this with MACC Chief Commissioner, YBhg Tan Sri Abu Kassim and thereafter decided to include this in the 2013 survey to find out how corporate Malaysia views and manage bribery and corruption. The issue of bribery and corruption is a subset of the types of fraud. I would say that there are three main types of fraud, the first being misappropriation of assets, the second is fraudulent financial reporting and the third is bribery and corruption.

Increasingly globally there is a growing trend to confront the problem of bribery and corruption such as the OECD convention, the US Foreign Corrupt Practices Act and the UK Bribery Act.

Under the US Foreign Corrupt Practices Act, a Malaysian company acting as an agent of the US principal may subject the US principal to regulatory actions if they are involved in any bribery with government officials here. Even for a US company who intends to acquire a Malaysian company, they will conduct due diligence on the target company’s relationship with vendors, government and customers because of successor’s liability. The government has announced its intention to incorporate ‘corporate liability’ provisions in our MACC Act which will hold companies liable for any bribery and corruption practices committed by their employees. Thus it is timely that our fraud survey had dedicated a section on bribery and corruption.

technical

13 I Keeping In Touch

Tan Kim Chuan, Head of KPMG Forensic

Malaysia

9. The survey showed that 76% of companies now have fraud and misconduct reporting channel in place compared to 62% in 2009, yet the number of fraud incidents have increased. Could you explain this phenomenon?

It is most likely that in the past, without proper channels, fraud and misconduct went unreported. It is also possible that in the past, those companies that had reporting channels were ineffective such as the employees were not aware of the existence of such channels or do not have much confidence in them, leading to unreported incidents.

10. Could you explain how a fraud and misconduct hotline managed by an external party may help in reducing incidents of fraud?

A hotline managed by an external party is likely to provide greater credibility and confidence to those who wish to whistle blow. When a call comes through, a dedicated trained staff (independent of the company) would answer the phone, and this would give a higher degree of confidentiality. The caller can remain anonymous throughout the communication and this increases their confidence to reveal more information during the call. From our experience, employees have more confidence on a whistle blowing channel that is managed by an independent external party instead of internally.

11. Based on the survey, what would be your advice to internal auditors to prevent and mitigate incidents of fraud?

As mentioned earlier, internal auditors should attend training to upgrade the skills in forensic investigation, data analytics, interviewing and techniques in conducting background checks. Internal auditors should recognise that by acquiring these skills they will be better equipped to detect, prevent and respond to incidents of fraud.

Apart from training and acquiring these skills, internal auditors will need to enhance their internal audit methodology to include continuous auditing of those areas that are prone to fraud.

12. Do you think that the size of a company and its sta� remuneration package does impact the likelihood of fraud to occur?

No, based on our experience, size of a company does not matter as fraud can hit both large and small companies. What motivates a fraudster is that they have an incentive to defraud the company, namely in the form of cash or an asset that could quickly be turned into cash. It could be that the fraudster is a compulsive gambler, enjoys an expensive lifestyle or a situation arose where he or she needs a huge sum of cash. As such, a good remuneration package may not be able to control this kind of situation.

Secondly the fraudster will rationalise his action such as the ‘boss makes more money than me while I do more work than him’ or ‘my colleague is doing it, why not me’. Apart from these other factors, weak internal

controls do contribute to the likelihood of fraud to be committed.

13. In your opinion, do you think community values will assist in fraud deterrence?

There is no evidence to show that community values have an impact on fraud. Fraud does happen in all types of communities and has happened not only in for-profit organisations but also charitable organisations. Likewise, it is incorrect to profile that citizens from certain countries are likely to commit fraud, as this is an incorrect generalisation of a statement when a certain country has a higher incidence of fraud.

14. Your survey indicated that certain business sectors have higher occurrence of fraud. Does this mean that either these companies in these sectors have inadequate fraud risk management systems or are more prone to fraud occurrence?

Based on our recent survey, corporate Malaysia has responded that fraud is becoming more industry aligned due to the nature of the industry.

15. You mentioned that larger companies and multinationals have a dedicated team to detect and investigate fraud. In your opinion, should smaller companies co-source with external services providers activities relating to fraud detection, due to resource constraints?

Yes, we strongly support the idea that smaller companies to consider co-sourcing their internal audit and investigation functions, to optimise their resources. The first step is for the business to recognise that fraud does not only happen in big companies but can happen to companies of all sizes, as indicated in our survey. It is a business imperative which should be taken seriously. Instead of only reacting when they are hit by fraud, companies can benefit by assessing their control measures and develop the appropriate strategies for prevention, detection and response to the risk of fraud, as part of the fraud risk management framework.

Keeping In Touch I 14

technical

Dr Suresh Kannan interviewing Tan Kim Chuan

For the full survey report, please refer to: http://www.kpmg.com/MY/en/IssuesAndInsights/ArticlesPublications/Documents/2013/fraud-survey-report.pdf

Approaching the report differently this year, KPMG Malaysia included a section on bribery and corruption for the first time in the survey. A substantial 71 per cent of respondents believed that bribery and corruption is an inevitable cost of doing business in Malaysia, whilst 64 per cent believed that business in Malaysia is not able to proceed without paying bribes.

Other notable findings in this category include:• 80 per cent of respondents believe that

bribery and corruption has increased over the last three years,

• 90 per cent of respondents see it as a major problem for business in the country,

• 65 per cent admitted that it is a major concern for their businesses, and

• 46 per cent acknowledged that complaints of bribery and corruption have been received.

Whilst the KPMG Report indicated relatively low incidents of bribery and corruption, the level of complacency around this risk is of most concern. An alarming 61 per cent of respondents indicated that their companies lack adequate monitoring procedures, with 62 per cent reporting the lack of procedures to facilitate robust due diligence on business partners.

The threat of bribery and corruption, including the damage it can do and the apparent lack of engagement by senior management in addressing this issue, is another major cause for concern.

Bribery and Corruption

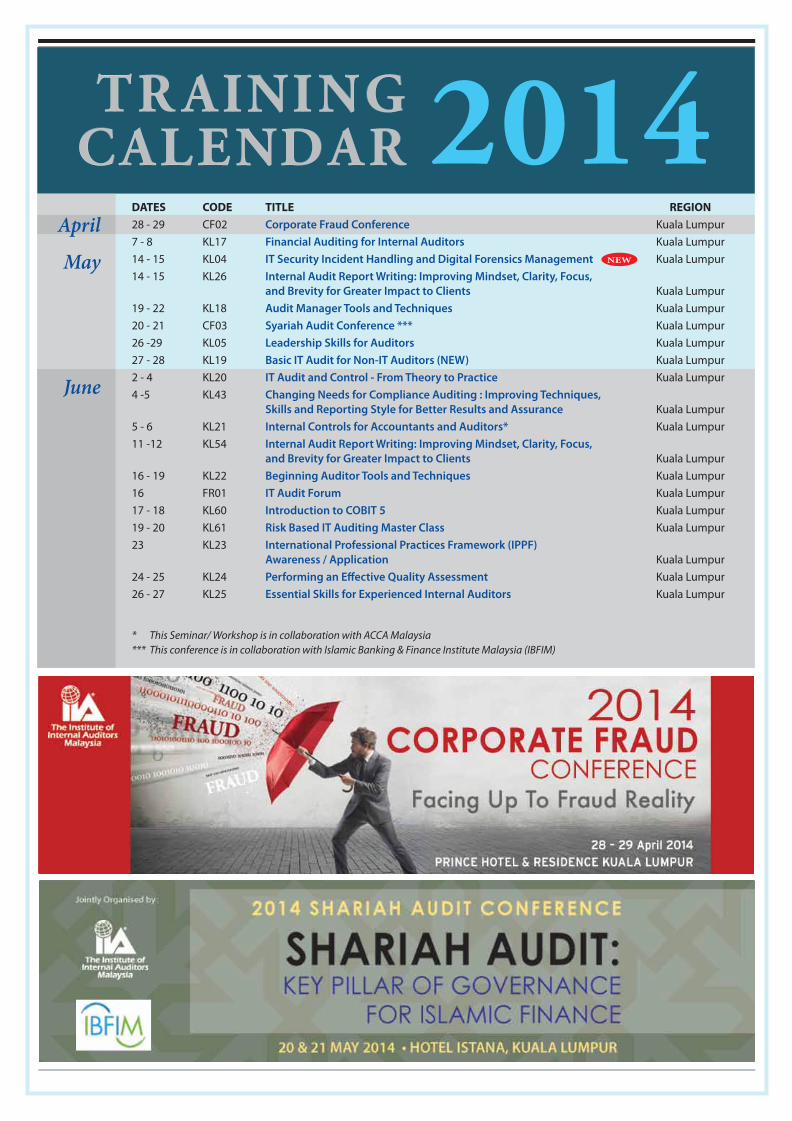

2014TR AININGCALENDAR

*** This conference is in collaboration with Islamic Banking & Finance Institute Malaysia (IBFIM)* This Seminar/ Workshop is in collaboration with ACCA Malaysia

April

June

May NEW

DATES CODE TITLE REGION28 - 29 CF02 Corporate Fraud Conference Kuala Lumpur7 - 8 KL17 Financial Auditing for Internal Auditors Kuala Lumpur14 - 15 KL04 IT Security Incident Handling and Digital Forensics Management Kuala Lumpur14 - 15 KL26 Internal Audit Report Writing: Improving Mindset, Clarity, Focus, and Brevity for Greater Impact to Clients Kuala Lumpur19 - 22 KL18 Audit Manager Tools and Techniques Kuala Lumpur20 - 21 CF03 Syariah Audit Conference *** Kuala Lumpur26 -29 KL05 Leadership Skills for Auditors Kuala Lumpur27 - 28 KL19 Basic IT Audit for Non-IT Auditors (NEW) Kuala Lumpur2 - 4 KL20 IT Audit and Control - From Theory to Practice Kuala Lumpur4 -5 KL43 Changing Needs for Compliance Auditing : Improving Techniques, Skills and Reporting Style for Better Results and Assurance Kuala Lumpur5 - 6 KL21 Internal Controls for Accountants and Auditors* Kuala Lumpur11 -12 KL54 Internal Audit Report Writing: Improving Mindset, Clarity, Focus, and Brevity for Greater Impact to Clients Kuala Lumpur16 - 19 KL22 Beginning Auditor Tools and Techniques Kuala Lumpur16 FR01 IT Audit Forum Kuala Lumpur17 - 18 KL60 Introduction to COBIT 5 Kuala Lumpur19 - 20 KL61 Risk Based IT Auditing Master Class Kuala Lumpur23 KL23 International Professional Practices Framework (IPPF) Awareness / Application Kuala Lumpur24 - 25 KL24 Performing an E�ective Quality Assessment Kuala Lumpur26 - 27 KL25 Essential Skills for Experienced Internal Auditors Kuala Lumpur

Related Documents