April 14, 2022 1 Rating: ACCUMULATE | CMP: Rs1,749 | TP: Rs1,899 Margin pressure overpowering revenue growth Quick Pointers: Positive surprise in revenue guidance (13-15% YoY CC) and strong headcount addition (~22K, 7.5% QoQ, 21%YoY) indicate strength in demand EBIT margin guidance reduced to 21-23% for FY23 (vs 22-24% for FY22) We cut Infy’s rating to Accumulate from Buy and DCF based target price to Rs. 1899 (earlier: Rs.2204) as we cut EPS estimates by 10.6%/8.2% for FY23/24E led by ~100-130bps cut in EBIT margins, lower than expected exit revenue growth rate, and increase in risk free rate to 7.2% (earlier: 6.8%). EBIT margin guidance of 21-23% for FY23 vs cons expectations of 22-24% came as negative surprise as it is below pre-covid levels (23%+ over FY17-19). Strong revenue guidance of 13-15% YoY CC for FY23 (vs cons expectations of 12-14%) despite low TTM TCV of $9.5 bn (vs $14.1 bn last year) led by largest ever large deal pipeline, strong client metrics and net new wins (40% in FY22) indicate Infy’s ability to capitalize strong demand environment. We have already baked in 13.8% YoY USD growth for FY23, however negative surprise in margins can be a drag on FY23 EPS. Infy has already reported weak exit EBIT margins of 21.6% in Q4 (-200bps QoQ). Lower than expected EBIT margin guidance of 21-23% for FY23 factors in headwinds from supply side cost pressures, return of travel and facility costs, investments in building deeper digital capabilities and potential drop in utilization levels. We assign DCF based TP of INR 1899 (earlier: 2204) with implied target multiple of 28x on FY24 EPS (earlier: 30x). Infy is currently trading at 30x/26x on earnings of INR 57.8/68.4 for FY23/24E respectively with revenue CAGR of 12.6% and EPS CAGR of 14.1% over FY22-24E. Big miss in Q4 revenue: Infy reported revenue of $4,280 mn, 1.2% QoQ CC (Ple: 3%, Cons: 3%), 0.2% QoQ USD (Ple: 2.6%, Cons: 2.6%). Weakness in growth was due to lower calendar working days, Covid leaves in Jan, contractual provision taken for one client (likely to reverse in future) and sharp sequential decline in Life Sciences vertical (-11.4% QoQ USD) due to several one-time deals in this vertical in Q3FY22. Full year FY22 revenue growth of 19.7% YoY CC was within guidance range of 19.5-20% YoY CC Healthy deal momentum and strong pipeline led to strong revenue guidance: Infy reported healthy deal TCV of $2.3 Bn, 7% YoY, -11% QoQ. Management gave strong revenue guidance of 13-15% YoY CC for FY23 (vs cons expectations of 12-14%) despite lower TTM TCV of $9.5 bn compared to $14.1 bn last year led by – 1) strong net new TCV of 48% in FY22, 2) largest pipeline in terms of large deals, 3) potential client mining opportunities (6 clients added in $100 mn bucket and 5 in $50 mn range in FY22) and 4) robust deal conversion and market share gains. Infosys (INFO IN) April 14, 2022 Q4FY22 Result Update ☑ Change in Estimates | ☑ Target | ☑ Reco Change in Estimates Current Previous FY23E FY24E FY23E FY24E Rating ACCU MUL ATE BUY Target Price 1,899 2,204 Sales (Rs. m) 14,10, 446 15,92, 987 14,30, 767 16,14,398 % Chng. (1.4 ) (1.3 ) EBITDA (Rs. m) 3,47,1 73 3,96,3 40 3,63,0 34 4,09,535 % Chng. (4.4 ) (3.2 ) EPS (Rs.) 57.8 68.4 64.7 74.5 % Chng. (10. 6) (8.2 ) Key Financials - Consolidated Y/e Mar FY21 FY22 FY23E FY24E Sales (Rs. bn) 1,005 1,216 1,410 1,593 EBITDA (Rs. bn) 279 315 347 396 Margin (%) 27.8 25.9 24.6 24.9 PAT (Rs. bn) 195 221 243 287 EPS (Rs.) 45.9 52.5 57.8 68.4 Gr. (%) 17.3 14.6 10.1 18.3 DPS (Rs.) 32.4 37.1 24.0 24.0 Yield (%) 1.9 2.1 1.4 1.4 RoE (%) 27.3 29.0 31.4 30.6 RoCE (%) 34.5 36.7 40.2 38.4 EV/Sales (x) 7.1 5.9 5.0 4.3 EV/EBITDA (x) 25.6 22.6 20.4 17.1 PE (x) 38.1 33.3 30.2 25.6 P/BV (x) 9.7 9.7 9.3 6.8 Key Data INFY.BO | INFO IN 52-W High / Low Rs.1,954 / Rs.1,311 Sensex / Nifty 58,339 / 17,476 Market Cap Rs.7,356bn/ $ 96,552m Shares Outstanding 4,207m 3M Av g. Daily Value Rs.13240.41m Shareholding Pattern (%) Promoter’s 13.46 Foreign 34.17 Domestic Institution 15.31 Public & Others 37.06 Promoter Pledge (Rs bn) - Stock Performance (%) 1M 6M 12M Absolute (4.0) 2.3 25.2 Relativ e (8.6) 6.5 4.1 Aditi Patil [email protected] | 91-22-66322381

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

April 14, 2022 1

Rating: ACCUMULATE | CMP: Rs1,749 | TP: Rs1,899

Margin pressure overpowering revenue growth

Quick Pointers:

Positive surprise in revenue guidance (13-15% YoY CC) and strong headcount

addition (~22K, 7.5% QoQ, 21%YoY) indicate strength in demand

EBIT margin guidance reduced to 21-23% for FY23 (vs 22-24% for FY22)

We cut Infy’s rating to Accumulate from Buy and DCF based target price to

Rs. 1899 (earlier: Rs.2204) as we cut EPS estimates by 10.6%/8.2% for

FY23/24E led by ~100-130bps cut in EBIT margins, lower than expected exit

revenue growth rate, and increase in risk free rate to 7.2% (earlier: 6.8%). EBIT

margin guidance of 21-23% for FY23 vs cons expectations of 22-24% came as

negative surprise as it is below pre-covid levels (23%+ over FY17-19).

Strong revenue guidance of 13-15% YoY CC for FY23 (vs cons expectations

of 12-14%) despite low TTM TCV of $9.5 bn (vs $14.1 bn last year) led by

largest ever large deal pipeline, strong client metrics and net new wins (40%

in FY22) indicate Infy’s ability to capitalize strong demand environment. We

have already baked in 13.8% YoY USD growth for FY23, however negative

surprise in margins can be a drag on FY23 EPS. Infy has already reported

weak exit EBIT margins of 21.6% in Q4 (-200bps QoQ). Lower than expected

EBIT margin guidance of 21-23% for FY23 factors in headwinds from supply

side cost pressures, return of travel and facility costs, investments in building

deeper digital capabilities and potential drop in utilization levels.

We assign DCF based TP of INR 1899 (earlier: 2204) with implied target

multiple of 28x on FY24 EPS (earlier: 30x). Infy is currently trading at 30x/26x

on earnings of INR 57.8/68.4 for FY23/24E respectively with revenue CAGR of

12.6% and EPS CAGR of 14.1% over FY22-24E.

Big miss in Q4 revenue: Infy reported revenue of $4,280 mn, 1.2% QoQ CC

(Ple: 3%, Cons: 3%), 0.2% QoQ USD (Ple: 2.6%, Cons: 2.6%). Weakness in

growth was due to lower calendar working days, Covid leaves in Jan,

contractual provision taken for one client (likely to reverse in future) and sharp

sequential decline in Life Sciences vertical (-11.4% QoQ USD) due to several

one-time deals in this vertical in Q3FY22. Full year FY22 revenue growth of

19.7% YoY CC was within guidance range of 19.5-20% YoY CC

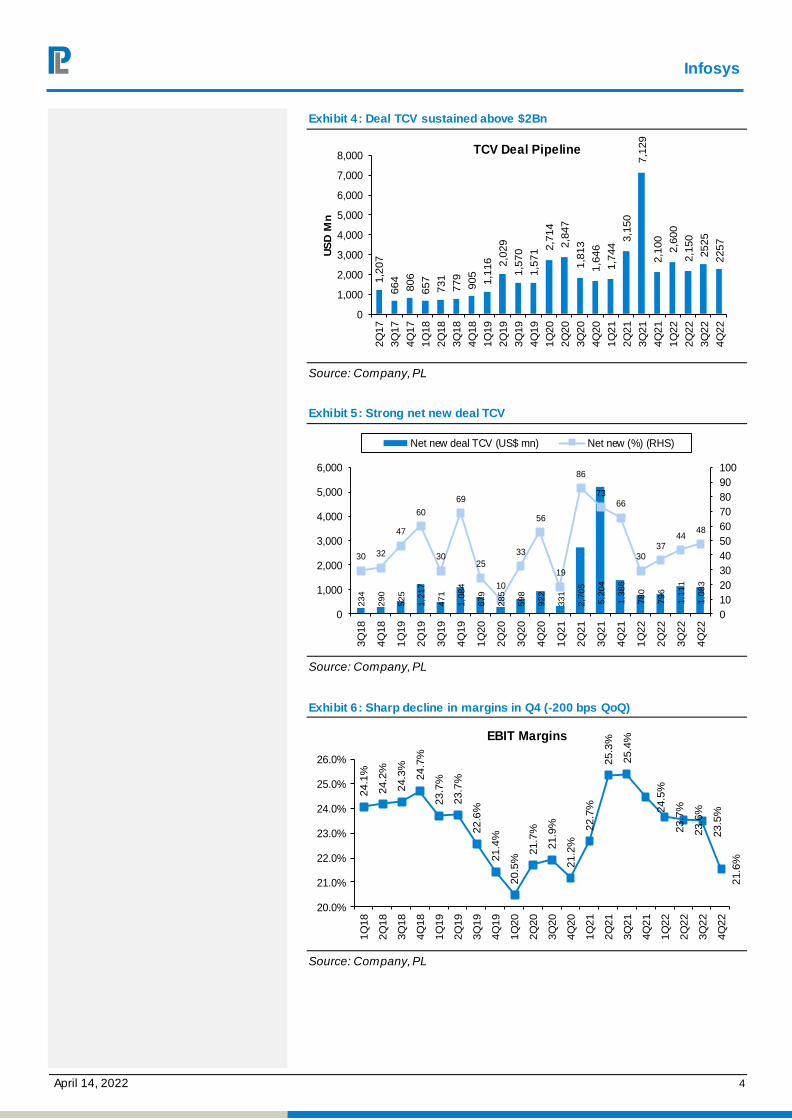

Healthy deal momentum and strong pipeline led to strong revenue

guidance: Infy reported healthy deal TCV of $2.3 Bn, 7% YoY, -11% QoQ.

Management gave strong revenue guidance of 13-15% YoY CC for FY23 (vs

cons expectations of 12-14%) despite lower TTM TCV of $9.5 bn compared to

$14.1 bn last year led by – 1) strong net new TCV of 48% in FY22, 2) largest

pipeline in terms of large deals, 3) potential client mining opportunities (6 clients

added in $100 mn bucket and 5 in $50 mn range in FY22) and 4) robust deal

conversion and market share gains.

Infosys (INFO IN)

April 14, 2022

Q4FY22 Result Update

☑ Change in Estimates | ☑ Target | ☑ Reco

Change in Estimates

Current Previous

FY23E FY24E FY23E FY24E

Rating ACCU MUL ATE BUY

Target Price 1,899 2,204

Sales (Rs. m) 14,10,446 15,92,987 14,30,767 16,14,398

% Chng. (1.4 ) (1.3 )

EBITDA (Rs. m) 3,47,173 3,96,340 3,63,034 4,09,535

% Chng. (4.4 ) (3.2 )

EPS (Rs.) 57.8 68.4 64.7 74.5

% Chng. (10.6) (8.2 )

Key Financials - Consolidated

Y/e Mar FY21 FY22 FY23E FY24E

Sales (Rs. bn) 1,005 1,216 1,410 1,593

EBITDA (Rs. bn) 279 315 347 396

Margin (%) 27.8 25.9 24.6 24.9

PAT (Rs. bn) 195 221 243 287

EPS (Rs.) 45.9 52.5 57.8 68.4

Gr. (%) 17.3 14.6 10.1 18.3

DPS (Rs.) 32.4 37.1 24.0 24.0

Yield (%) 1.9 2.1 1.4 1.4

RoE (%) 27.3 29.0 31.4 30.6

RoCE (%) 34.5 36.7 40.2 38.4

EV/Sales (x) 7.1 5.9 5.0 4.3

EV/EBITDA (x) 25.6 22.6 20.4 17.1

PE (x) 38.1 33.3 30.2 25.6

P/BV (x) 9.7 9.7 9.3 6.8

Key Data INFY.BO | INFO IN

52-W High / Low Rs.1,954 / Rs.1,311

Sensex / Nifty 58,339 / 17,476

Market Cap Rs.7,356bn/ $ 96,552m

Shares Outstanding 4,207m

3M Av g. Daily Value Rs.13240.41m

Shareholding Pattern (%)

Promoter’s 13.46

Foreign 34.17

Domestic Institution 15.31

Public & Others 37.06

Promoter Pledge (Rs bn) -

Stock Performance (%)

1M 6M 12M

Absolute (4.0) 2.3 25.2

Relativ e (8.6) 6.5 4.1

Aditi Patil

[email protected] | 91-22-66322381

Infosys

April 14, 2022 2

Big miss in Q4 margins: EBIT margin of 21.6%, declined by 200bps QoQ

(PLe: 22.9%, Cons: 23.2%) led by headwinds of - 1) 1.6% impact of lower

calendar working days and contractual provision, 2) 0.7% due to drop in

utilization (87%, -150bps QoQ), 3) 1% due to visa costs, third party costs and

absence of one-off benefits present in Q3 partially offset by salary related

benefit (1.1%) because of lower working days, leave costs etc. FY23 margins

stood at 23% (vs guidance range of 22-24%)

Negative surprise in margin guidance: Margin guidance downgraded 21-

23% for FY23 vs cons expectations of 22-24% factoring in headwinds from -1)

supply side pressures due to elevated attrition levels, 2) return of travel and

facility costs, 3) investments in building deeper digital capabilities, highly skilled

tech talent and sales and marketing to continue gaining market share, 4) further

drop in utilization levels (comfortable levels of 85% vs current 87%). These

headwinds will be partially offset by pyramid optimization, value led pricing

gains and operating efficiencies.

Quarterly attrition dropped by 500bps QoQ: LTM IT services attrition

increased to 27.7%, +220bps QoQ, +1680 bps YoY. However, quarterly

attrition is down 500bps QoQ. Quarterly attrition may not inch further down in

near term due to wage hike cycle in Q1FY23. We expect supply side cost

pressures to start easing in H2FY23.

Highest ever headcount addition: Infy continued its aggressive hiring with

highest ever net headcount addition of 21,948, 7.5% QoQ, 21%YoY. (vs avg

net addition 10,816 in last 3 quarters). Infy added 85K freshers (27% of FY22

total headcount) in FY22 and have initial target to add 50K in FY23 which can

be ramped up depending on demand momentum.

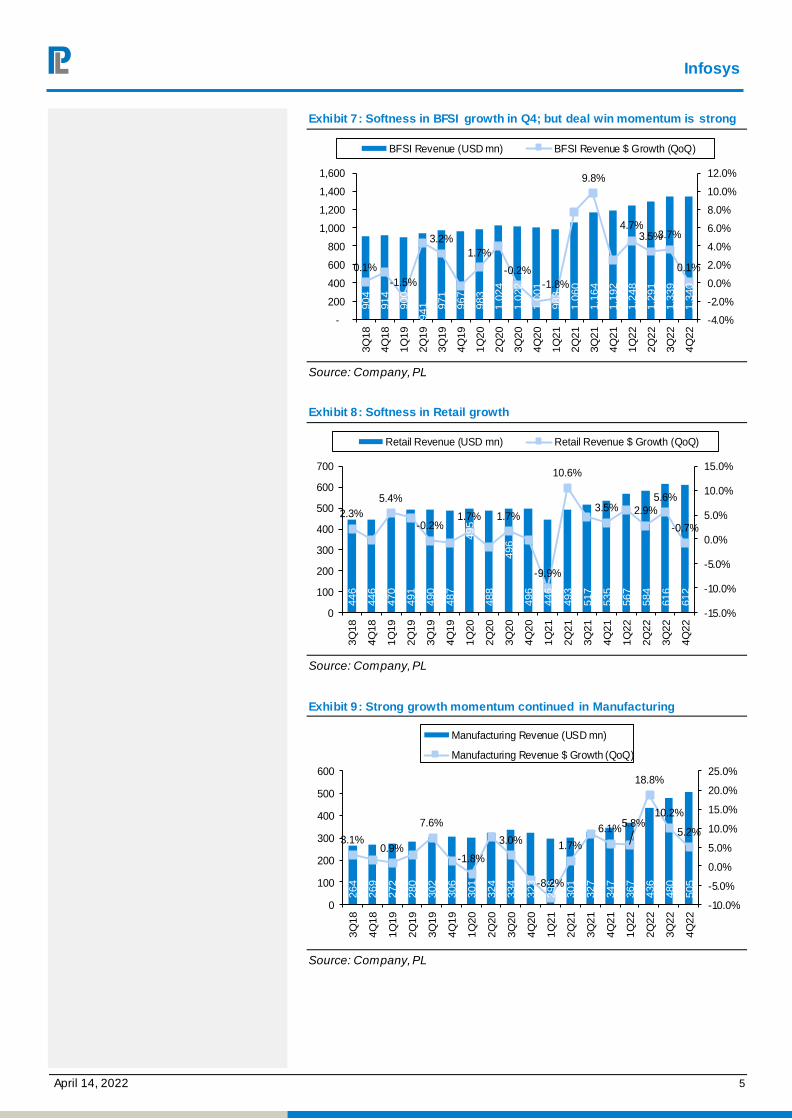

Strong demand across all verticals:

BFSI was flat QoQ, but Infy won 8 large deals in this segment in Q4 and

27 in FY22. Large deal pipeline is healthy in BFSI across all markets.

In Retail (-0.7% QoQ) demand is coming from integrated outsourcing

deals, e-commerce, supply chain, revenue growth initiatives. Infy won 16

large deals in Retail in FY22.

In E&U there is strong demand for digital transformation, CX, operational

efficiency improvement initiatives with 4 large deals in Q4 and 18 in FY22.

Infy won 6 large deals in Q4 and 13 in FY22 in Manufacturing with strong

demand from engineering, IoT, ERP, cloud, digital transformation.

In Communication demand is strong in areas of CX, network

simplification, time to market, integrated data etc. In HiTech clients are

spending on edge computing, commerce, cybersecurity etc.

In Life Sciences there is strong traction in digital transformation, clinical

trials reducing time, digital drug engagement etc.

Digital revenues grew by 2% QoQ

and 36.2% YoY (in USD terms) and

now account to 59.2% of total

revenue (vs 58.5% in Q3FY22)

Return to office will bring back travel and facility expenses. Infy has a three

phased plan to start working from

office in a phased manner. Currently

95% people working from home

Infosys

April 14, 2022 3

Transitioning from Russia: Infy does not have active business relationships

with Russian domiciled companies. Through their Russian delivery centres

they service global clients based in Russia. Infy is transitioning this business

from Russia to other global locations . Infy employs less than 100 people in

Russia, miniscule compared to total employee strength of ~3.14 lakhs.

Robust cash conversion: DSO days decreased to 67 (vs 71 days in Q3FY22

and 71 days in 4QFY21). FCF/NI for the quarter was 101% and for full year

FY22 at 103%.

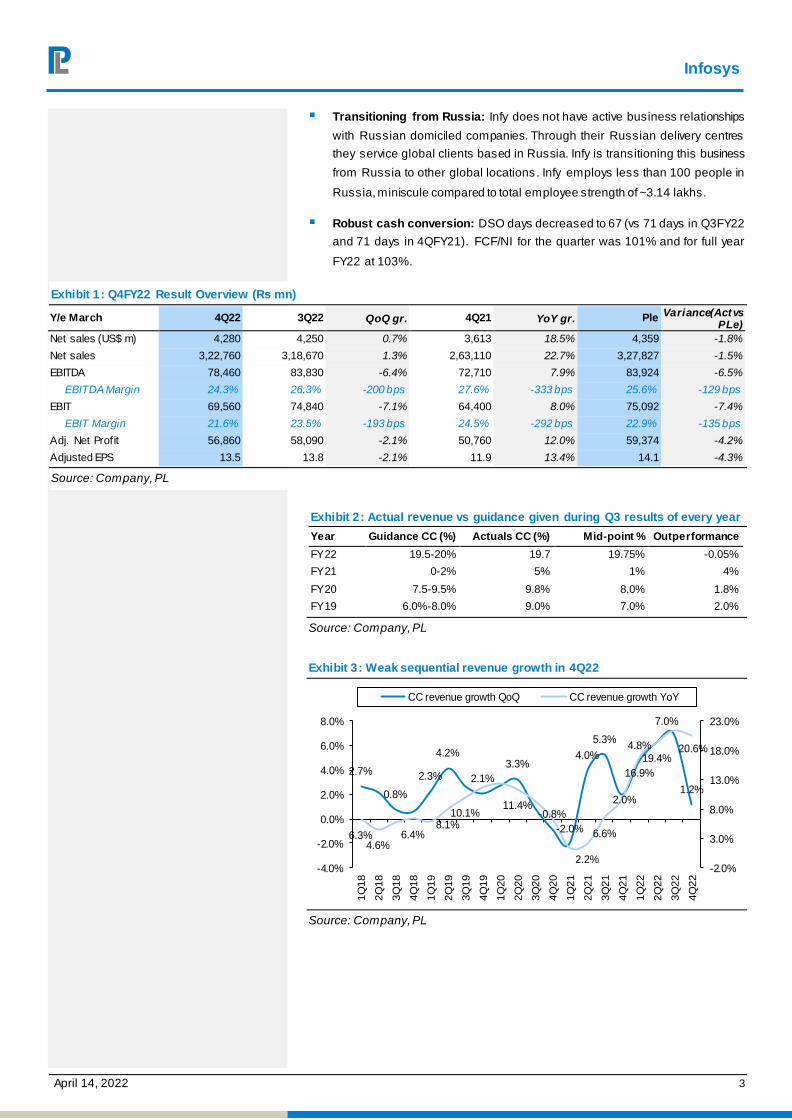

Exhibit 1: Q4FY22 Result Overview (Rs mn)

Y/e March 4Q22 3Q22 QoQ gr. 4Q21 YoY gr. Ple Variance(Act vs PLe)

Net sales (US$ m) 4,280 4,250 0.7% 3,613 18.5% 4,359 -1.8%

Net sales 3,22,760 3,18,670 1.3% 2,63,110 22.7% 3,27,827 -1.5%

EBITDA 78,460 83,830 -6.4% 72,710 7.9% 83,924 -6.5%

EBITDA Margin 24.3% 26.3% -200 bps 27.6% -333 bps 25.6% -129 bps

EBIT 69,560 74,840 -7.1% 64,400 8.0% 75,092 -7.4%

EBIT Margin 21.6% 23.5% -193 bps 24.5% -292 bps 22.9% -135 bps

Adj. Net Profit 56,860 58,090 -2.1% 50,760 12.0% 59,374 -4.2%

Adjusted EPS 13.5 13.8 -2.1% 11.9 13.4% 14.1 -4.3%

Source: Company, PL

Exhibit 2: Actual revenue vs guidance given during Q3 results of every year

Year Guidance CC (%) Actuals CC (%) Mid-point % Outperformance

FY22 19.5-20% 19.7 19.75% -0.05%

FY21 0-2% 5% 1% 4%

FY20 7.5-9.5% 9.8% 8.0% 1.8%

FY19 6.0%-8.0% 9.0% 7.0% 2.0%

Source: Company, PL

Exhibit 3: Weak sequential revenue growth in 4Q22

2.7%

0.8%

2.3%

4.2%

2.1%

3.3%

-0.8%

-2.0%

4.0%

5.3%

2.0%

4.8%

7.0%

1.2%

6.3%4.6%

6.4%8.1%

10.1%11.4%

2.2%

6.6%

16.9%

19.4%20.6%

-2.0%

3.0%

8.0%

13.0%

18.0%

23.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

2Q

21

3Q

21

4Q

21

1Q

22

2Q

22

3Q

22

4Q

22

CC revenue growth QoQ CC revenue growth YoY

Source: Company, PL

Infosys

April 14, 2022 4

Exhibit 4: Deal TCV sustained above $2Bn

1,2

07

664

806

657

731

779

905

1,1

16 2,0

29

1,5

70

1,5

71 2

,714

2,8

47

1,8

13

1,6

46

1,7

44 3

,150

7,1

29

2,1

00

2,6

00

2,1

50

2525

2257

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

2Q

21

3Q

21

4Q

21

1Q

22

2Q

22

3Q

22

4Q

22

US

D M

n

TCV Deal Pipeline

Source: Company, PL

Exhibit 5: Strong net new deal TCV

23

4

29

0

52

5

1,2

17

47

1

1,0

84

67

9

28

5

59

8

92

2

33

1

2,7

05

5,2

04

1,3

86

78

0

79

6

1,1

11

1,0

83

30 32

47

60

30

69

25

10

33

56

19

86

7366

3037

4448

0

10

20

30

40

50

60

70

80

90

100

0

1,000

2,000

3,000

4,000

5,000

6,000

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

2Q

21

3Q

21

4Q

21

1Q

22

2Q

22

3Q

22

4Q

22

Net new deal TCV (US$ mn) Net new (%) (RHS)

Source: Company, PL

Exhibit 6: Sharp decline in margins in Q4 (-200 bps QoQ)

24.1

%

24.2

%

24.3

%

24.7

%

23.7

%

23.7

%

22.6

%

21.4

%

20.5

%

21.7

%

21.9

%

21.2

%

22.7

%

25.3

%

25.4

%

24.5

%

23.7

%

23.6

%

23.5

%

21.6

%

20.0%

21.0%

22.0%

23.0%

24.0%

25.0%

26.0%

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

2Q

21

3Q

21

4Q

21

1Q

22

2Q

22

3Q

22

4Q

22

EBIT Margins

Source: Company, PL

Infosys

April 14, 2022 5

Exhibit 7: Softness in BFSI growth in Q4; but deal win momentum is strong

904

914

900

941

971

967

983

1,0

24

1,0

22

1,0

01

983

1,0

60

1,1

64

1,1

92

1,2

48

1,2

91

1,3

39

1,3

40

0.1%

-1.5%

3.2%

1.7%

-0.2%

-1.8%

9.8%

4.7%3.5%3.7%

0.1%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

-

200

400

600

800

1,000

1,200

1,400

1,600

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

2Q

21

3Q

21

4Q

21

1Q

22

2Q

22

3Q

22

4Q

22

BFSI Revenue (USD mn) BFSI Revenue $ Growth (QoQ)

Source: Company, PL

Exhibit 8: Softness in Retail growth

446

446

470

491

490

487

495

488

496

496

446

493

517

535

567

584

616

612

2.3%

5.4%

-0.2%1.7% 1.7%

-9.9%

10.6%

3.5% 2.9%

5.6%

-0.7%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

0

100

200

300

400

500

600

700

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

2Q

21

3Q

21

4Q

21

1Q

22

2Q

22

3Q

22

4Q

22

Retail Revenue (USD mn) Retail Revenue $ Growth (QoQ)

Source: Company, PL

Exhibit 9: Strong growth momentum continued in Manufacturing

264

269

272

280

302

306

301

324

334

323

296

301

327

347

367

436

480

505

3.1%0.9%

7.6%

-1.8%

3.0%

-8.2%

1.7%

6.1%5.8%

18.8%

10.2%

5.2%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

0

100

200

300

400

500

600

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

2Q

21

3Q

21

4Q

21

1Q

22

2Q

22

3Q

22

4Q

22

Manufacturing Revenue (USD mn)

Manufacturing Revenue $ Growth (QoQ)

Source: Company, PL

Infosys

April 14, 2022 6

Exhibit 10: Subcontracting expenses remain at elevated levels

10,6

10

10,9

00

10,4

10

11,0

70

12,9

10

15,2

30

16,1

90

16,0

10

16,4

00

16,5

10

17,2

10

17,0

40

16,2

60

16,3

40

18,3

90

19,8

50

24,5

40

30,5

40

35,1

10

35,8

80

6.2% 5.9%6.7%

7.6% 7.5% 7.5%6.9% 6.7%

7.5%7.7%

8.8%

10.3%11.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

4,000

8,000

12,000

16,000

20,000

24,000

28,000

32,000

36,000

40,000

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

2Q

21

3Q

21

4Q

21

1Q

22

2Q

22

3Q

22

4Q

22

Subcontracting Expenses As a % of sales

Source: Company, PL

Exhibit 11: Changes in Estimates

FY23E FY24E

USD revenues (US$ m)

- New 18,558 20,688

- Old 18,826 20,966

Change (%) -1.4% -1.3%

EBIT Margin

- New 22.0% 22.6%

- Old 23.4% 23.5%

Change (%) -134 bps -94 bps

Recurring EPS - Fully diluted (Rs)

- New 57.8 68.4

- Old 64.6 74.5

Change (%) -10.6% -8.2%

Source: PL

Exhibit 12: Infosys One year forward PE

30.4

33.5

31.2

10.0

15.0

20.0

25.0

30.0

35.0

Apr-

10

Oct-10

Apr-

11

Oct-11

Apr-

12

Oct-12

Apr-

13

Oct-13

Apr-

14

Oct-14

Apr-

15

Oct-15

Apr-

16

Oct-16

Apr-

17

Oct-17

Apr-

18

Oct-18

Apr-

19

Oct-19

Apr-

20

Oct-20

Apr-

21

Oct-21

Apr-

22

P/E Mean Mean + Std Dev Mean - Std Dev

Source: Company, PL

Infosys

April 14, 2022 7

Exhibit 13: TCS One Year Forward P/E chart

12.3

16.2

23.7 26.8

19.3

28.5

33.4

30.4

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Apr-

10

Oct-10

Apr-

11

Oct-11

Apr-

12

Oct-12

Apr-

13

Oct-13

Apr-

14

Oct-14

Apr-

15

Oct-15

Apr-

16

Oct-16

Apr-

17

Oct-17

Apr-

18

Oct-18

Apr-

19

Oct-19

Apr-

20

Oct-20

Apr-

21

Oct-21

Apr-

22

P/E Mean Mean + Std Dev

Mean - Std Dev Mean + 2SD

Source: Company, PL

Exhibit 14: Geography-wise revenues

(US$ m) 4Q22 3Q22 QoQ gr. 4Q21 YoY gr.

North America 2,628 2,627 0.1% 2,226 18.1%

Europe 1,079 1,058 1.9% 882 22.3%

India 137 128 7.4% 108 26.4%

Rest of World 437 438 -0.3% 397 9.8%

Total 4,280 4,250 0.7% 3,613 18.5%

as % of Total

North America 61.4% 61.8% -40 bps 61.6% -20 bps

Europe 25.2% 24.9% 30 bps 24.4% 80 bps

India 3.2% 3.0% 20 bps 3.0% 20 bps

Rest of World 10.2% 10.3% -10 bps 11.0% -80 bps

Source: Company, PL

Exhibit 15: Vertical-wise revenues

4Q22 3Q22 QoQ gr. 4Q21 YoY gr.

Financial Services 1,340 1,339 0.1% 1,192 12.4%

Manufacturing 505 480 5.2% 347 45.6%

Communication Services 548 531 3.1% 434 26.4%

Retail CPG 612 616 -0.7% 535 14.5%

Life Sc & Healthcare 282 319 -11.4% 246 15.0%

Others 993 965 2.9% 860 15.5%

Total 4,280 4,250 0.7% 3,613 18.5%

as % of Total

Financial Services 31.3% 31.5% -20 bps 33.0% -170 bps

Manufacturing 11.8% 11.3% 50 bps 9.6% 220 bps

Communication Services 12.8% 12.5% 30 bps 12.0% 80 bps

Retail CPG 14.3% 14.5% -20 bps 14.8% -50 bps

Life Sc & Healthcare 6.6% 7.5% -90 bps 6.8% -20 bps

Others 23.2% 22.7% 50 bps 23.8% -60 bps

Source: Company, PL

Infosys

April 14, 2022 8

Exhibit 16: Client Metrics

4Q22 3Q22 QoQ gr. 4Q21 YoY gr.

Number of Clients

Active 1741 1,738 0.2% 1626 7.1%

Added during the period 110 111 -0.9% 130 -15.4%

Revenue concentration (US$ m)

Top 10 clients 830 859 -3.3% 661 25.6%

Top 25 clients 1,515 1,526 -0.7% 1,236 22.6%

Top 11-25 clients 685 667 2.6% 574 19.2%

Non Top 25 2,765 2,724 1.5% 2,377 16.3%

Total 4,280 4,250 0.7% 3,613 18.5%

Revenue concentration (%)

Top 10 clients 19.4% 20.2% -80 bps 18.3% 110 bps

Top 25 clients 35.4% 35.9% -50 bps 34.2% 120 bps

Account Receivables (days) 67 71 (4) 71 (4)

Source: Company, PL

Exhibit 17: Utilization inching downwards

4Q22 3Q22 QoQ gr. 4Q21 YoY gr.

Utilization (%)

Include Trainees 80.0% 82.7% -270 bps 82.2% -220 bps

Exclude Trainees 87.0% 88.5% -150 bps 87.7% -70 bps

Source: Company, PL

Exhibit 18: Consistent growth in digital revenues (59.2% revenue share)

Revenues by offering 4Q22 3Q22 QoQ gr. 4Q21 YoY gr.

Digital 59.2% 58.5% 70 bps 51.5% 770 bps

Core 40.8% 41.5% -70 bps 48.5% -770 bps

Revenue by offering ( $mn)

Digital 2,534 2,239 13.2% 1762 43.8%

Core 1,746 1,759 -0.7% 1754 -0.5%

Source: Company, PL

Infosys

April 14, 2022 9

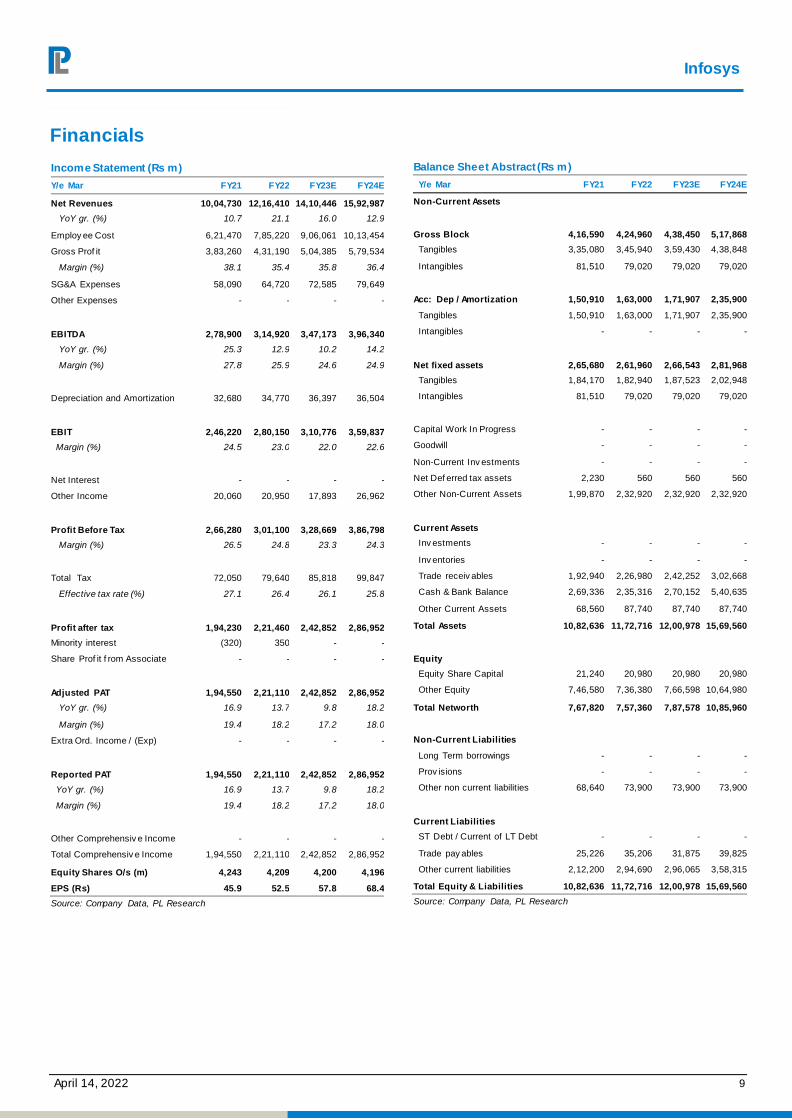

Financials Income Statement (Rs m)

Y/e Mar FY21 FY22 FY23E FY24E

Net Revenues 10,04,730 12,16,410 14,10,446 15,92,987

YoY gr. (%) 10.7 21.1 16.0 12.9

Employ ee Cost 6,21,470 7,85,220 9,06,061 10,13,454

Gross Prof it 3,83,260 4,31,190 5,04,385 5,79,534

Margin (%) 38.1 35.4 35.8 36.4

SG&A Expenses 58,090 64,720 72,585 79,649

Other Expenses - - - -

EBITDA 2,78,900 3,14,920 3,47,173 3,96,340

YoY gr. (%) 25.3 12.9 10.2 14.2

Margin (%) 27.8 25.9 24.6 24.9

Depreciation and Amortization 32,680 34,770 36,397 36,504

EBIT 2,46,220 2,80,150 3,10,776 3,59,837

Margin (%) 24.5 23.0 22.0 22.6

Net Interest - - - -

Other Income 20,060 20,950 17,893 26,962

Profit Before Tax 2,66,280 3,01,100 3,28,669 3,86,798

Margin (%) 26.5 24.8 23.3 24.3

Total Tax 72,050 79,640 85,818 99,847

Effective tax rate (%) 27.1 26.4 26.1 25.8

Profit after tax 1,94,230 2,21,460 2,42,852 2,86,952

Minority interest (320) 350 - -

Share Prof it f rom Associate - - - -

Adjusted PAT 1,94,550 2,21,110 2,42,852 2,86,952

YoY gr. (%) 16.9 13.7 9.8 18.2

Margin (%) 19.4 18.2 17.2 18.0

Extra Ord. Income / (Exp) - - - -

Reported PAT 1,94,550 2,21,110 2,42,852 2,86,952

YoY gr. (%) 16.9 13.7 9.8 18.2

Margin (%) 19.4 18.2 17.2 18.0

Other Comprehensiv e Income - - - -

Total Comprehensiv e Income 1,94,550 2,21,110 2,42,852 2,86,952

Equity Shares O/s (m) 4,243 4,209 4,200 4,196

EPS (Rs) 45.9 52.5 57.8 68.4

Source: Company Data, PL Research

Balance Sheet Abstract (Rs m)

Y/e Mar FY21 FY22 FY23E FY24E

Non-Current Assets

Gross Block 4,16,590 4,24,960 4,38,450 5,17,868

Tangibles 3,35,080 3,45,940 3,59,430 4,38,848

Intangibles 81,510 79,020 79,020 79,020

Acc: Dep / Amortization 1,50,910 1,63,000 1,71,907 2,35,900

Tangibles 1,50,910 1,63,000 1,71,907 2,35,900

Intangibles - - - -

Net fixed assets 2,65,680 2,61,960 2,66,543 2,81,968

Tangibles 1,84,170 1,82,940 1,87,523 2,02,948

Intangibles 81,510 79,020 79,020 79,020

Capital Work In Progress - - - -

Goodwill - - - -

Non-Current Inv estments - - - -

Net Def erred tax assets 2,230 560 560 560

Other Non-Current Assets 1,99,870 2,32,920 2,32,920 2,32,920

Current Assets

Inv estments - - - -

Inv entories - - - -

Trade receiv ables 1,92,940 2,26,980 2,42,252 3,02,668

Cash & Bank Balance 2,69,336 2,35,316 2,70,152 5,40,635

Other Current Assets 68,560 87,740 87,740 87,740

Total Assets 10,82,636 11,72,716 12,00,978 15,69,560

Equity

Equity Share Capital 21,240 20,980 20,980 20,980

Other Equity 7,46,580 7,36,380 7,66,598 10,64,980

Total Networth 7,67,820 7,57,360 7,87,578 10,85,960

Non-Current Liabilities

Long Term borrowings - - - -

Prov isions - - - -

Other non current liabilities 68,640 73,900 73,900 73,900

Current Liabilities

ST Debt / Current of LT Debt - - - -

Trade pay ables 25,226 35,206 31,875 39,825

Other current liabilities 2,12,200 2,94,690 2,96,065 3,58,315

Total Equity & Liabilities 10,82,636 11,72,716 12,00,978 15,69,560

Source: Company Data, PL Research

Infosys

April 14, 2022 10

Cash Flow (Rs m)

Y/e Mar FY21 FY22 FY23E FY24E Year

PBT 2,66,280 3,01,100 3,28,669 3,86,798

Add. Depreciation 32,680 34,770 36,397 36,504

Add. Interest - - - -

Less Financial Other Income 20,060 20,950 17,893 26,962

Add. Other - - - -

Op. prof it bef ore WC changes 2,98,960 3,35,870 3,65,066 4,23,302

Net Changes-WC (63,464) (28,950) 9,201 (12,474)

Direct tax (72,050) (79,640) (85,818) (99,847)

Net cash from Op. activities 1,63,446 2,27,280 2,88,449 3,10,982

Capital expenditures (30,940) (37,250) (93,350) (51,929)

Interest / Div idend Income - - - -

Others - - - -

Net Cash from Invt. activities (30,940) (37,250) (93,350) (51,929)

Issue of share cap. / premium 3,950 (1,920) - -

Debt changes - - - -

Div idend paid (1,37,487) (1,56,241) (1,00,602) (1,00,602)

Interest paid - - - -

Others 47,757 (70,949) (1,12,031) 1,12,031

Net cash from Fin. activities (85,780) (2,29,110) (2,12,633) 11,430

Net change in cash 46,726 (39,080) (17,534) 2,70,483

Free Cash Flow 1,32,506 1,90,030 1,95,100 2,59,053

Source: Company Data, PL Research

Quarterly Financials (Rs m)

Y/e Mar Q1FY22 Q2FY22 Q3FY22 Q4FY22

Net Revenue 2,78,960 2,96,020 3,18,670 3,22,760

YoY gr. (%) 17.9 20.5 22.9 22.7

Raw Material Expenses 1,76,770 1,89,470 2,05,160 2,13,820

Gross Prof it 1,02,190 1,06,550 1,13,510 1,08,940

Margin (%) 36.6 36.0 35.6 33.8

EBITDA 74,320 78,310 83,830 78,460

YoY gr. (%) 21.4 10.6 13.1 7.9

Margin (%) 26.6 26.5 26.3 24.3

Depreciation / Depletion 8,290 8,590 8,990 8,900

EBIT 66,030 69,720 74,840 69,560

Margin (%) 23.7 23.6 23.5 21.6

Net Interest - - - -

Other Income 5,730 4,760 4,590 5,870

Profit before Tax 71,760 74,480 79,430 75,430

Margin (%) 25.7 25.2 24.9 23.4

Total Tax 19,750 20,200 21,210 18,480

Effective tax rate (%) 27.5 27.1 26.7 24.5

Profit after Tax 52,010 54,280 58,220 56,950

Minority interest 60 70 130 90

Share Prof it f rom Associates - - - -

Adjusted PAT 52,070 54,350 58,350 57,040

YoY gr. (%) 23.0 12.2 11.5 12.3

Margin (%) 18.7 18.4 18.3 17.7

Extra Ord. Income / (Exp) - - - -

Reported PAT 52,070 54,350 58,350 57,040

YoY gr. (%) 23.0 12.2 11.5 12.3

Margin (%) 18.7 18.4 18.3 17.7

Other Comprehensiv e Income - - - -

Total Comprehensive Income 52,070 54,350 58,350 57,040

Av g. Shares O/s (m) 4,255 4,219 4,199 4,200

EPS (Rs) 12.2 12.9 13.9 13.6

Source: Company Data, PL Research

Key Financial Metrics

Y/e Mar FY21 FY22 FY23E FY24E

Per Share(Rs)

EPS 45.9 52.5 57.8 68.4

CEPS 53.6 60.8 66.5 77.1

BVPS 181.0 179.9 187.5 258.8

FCF 31.2 45.1 46.5 61.7

DPS 32.4 37.1 24.0 24.0

Return Ratio(%)

RoCE 34.5 36.7 40.2 38.4

ROIC 37.1 42.9 45.2 38.2

RoE 27.3 29.0 31.4 30.6

Balance Sheet

Net Debt : Equity (x) (0.4) (0.3) (0.3) (0.5)

Debtor (Day s) 70 68 63 69

Valuation(x)

PER 38.1 33.3 30.2 25.6

P/B 9.7 9.7 9.3 6.8

P/CEPS 32.6 28.8 26.3 22.7

EV/EBITDA 25.6 22.6 20.4 17.1

EV/Sales 7.1 5.9 5.0 4.3

Div idend Yield (%) 1.9 2.1 1.4 1.4

Source: Company Data, PL Research

Infosys

April 14, 2022 11

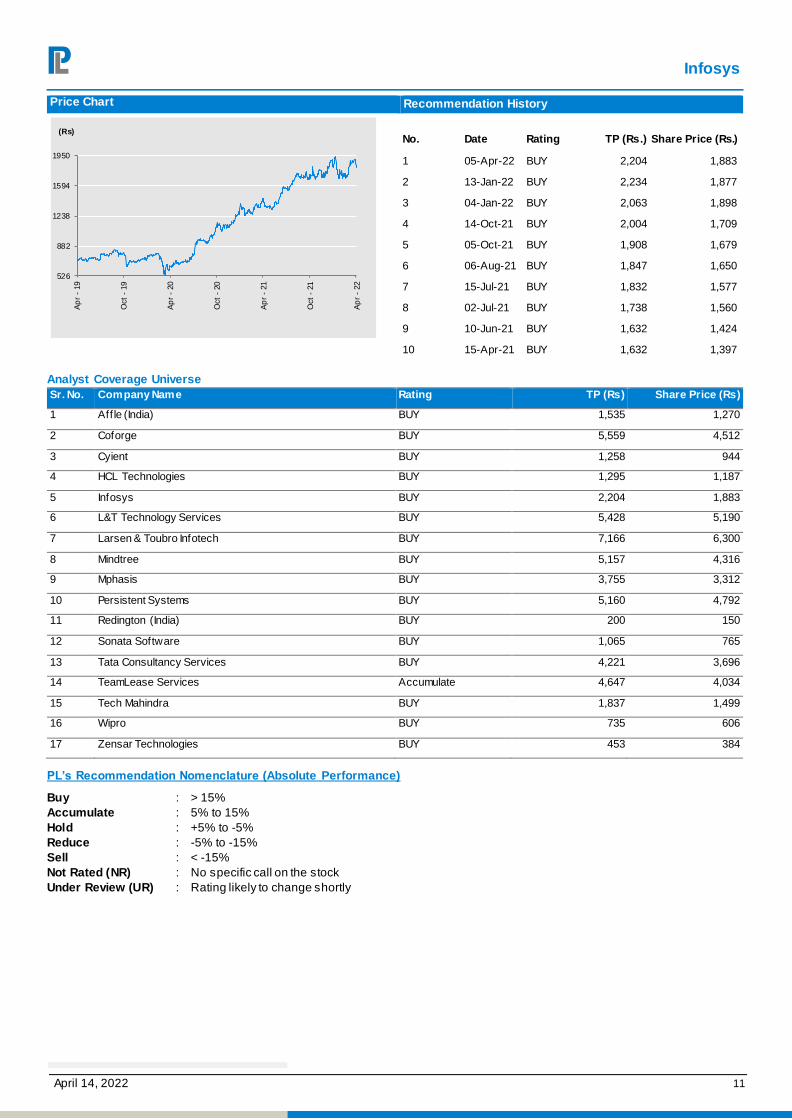

Price Chart Recommendation History

No. Date Rating TP (Rs.) Share Price (Rs.)

1 05-Apr-22 BUY 2,204 1,883

2 13-Jan-22 BUY 2,234 1,877

3 04-Jan-22 BUY 2,063 1,898

4 14-Oct-21 BUY 2,004 1,709

5 05-Oct-21 BUY 1,908 1,679

6 06-Aug-21 BUY 1,847 1,650

7 15-Jul-21 BUY 1,832 1,577

8 02-Jul-21 BUY 1,738 1,560

9 10-Jun-21 BUY 1,632 1,424

10 15-Apr-21 BUY 1,632 1,397

Analyst Coverage Universe

Sr. No. Company Name Rating TP (Rs) Share Price (Rs)

1 Aff le (India) BUY 1,535 1,270

2 Coforge BUY 5,559 4,512

3 Cyient BUY 1,258 944

4 HCL Technologies BUY 1,295 1,187

5 Infosys BUY 2,204 1,883

6 L&T Technology Services BUY 5,428 5,190

7 Larsen & Toubro Infotech BUY 7,166 6,300

8 Mindtree BUY 5,157 4,316

9 Mphasis BUY 3,755 3,312

10 Persistent Systems BUY 5,160 4,792

11 Redington (India) BUY 200 150

12 Sonata Software BUY 1,065 765

13 Tata Consultancy Services BUY 4,221 3,696

14 TeamLease Services Accumulate 4,647 4,034

15 Tech Mahindra BUY 1,837 1,499

16 Wipro BUY 735 606

17 Zensar Technologies BUY 453 384

PL’s Recommendation Nomenclature (Absolute Performance)

Buy : > 15%

Accumulate : 5% to 15%

Hold : +5% to -5%

Reduce : -5% to -15%

Sell : < -15%

Not Rated (NR) : No specific call on the stock

Under Review (UR) : Rating likely to change shortly

526

882

1238

1594

1950

Ap

r -

19

Oct

- 19

Ap

r -

20

Oct

- 20

Ap

r -

21

Oct

- 21

Ap

r -

22

(Rs)

Infosys

April 14, 2022 12

ANALYST CERTIFICATION

(Indian Clients)

We/I, Ms. Aditi Patil- MBA Finance Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately ref lect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or wil l be directly or indirectly related to the specific recommendation(s)

or v iew(s) in this report.

(US Clients)

The research analy sts, with respect to each issuer and its securities covered by them in this research report, certify that: All of the views expressed in this research report accurately ref lect his or her or their personal views about all of the issuers and their securities; and No part of his or her or their compensation was, is or will be directly related to the specific

recommendation or views expressed in this research report.

DISCLAIMER

Indian Clients

Prabhudas Lilladher Pvt. Ltd, Mumbai, India (hereinafter referred to as “PL”) is engaged in the business of Stock Broking, Portfolio Manager, Depository Participant and distribution for third party financial products. PL is a subsidiary of Prabhudas Lilladher Advisory Services Pvt Ltd. which has its various subsidiaries engaged in business of commodity broking,

inv estment banking, financial services (margin funding) and distribution of third party financial/other products, details in respect of which are available at www.plindia.com.

This document has been prepared by the Research Division of PL and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported

or copied or made available to others without prior permission of PL. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security.

The inf ormation contained in this report has been obtained from sources that are considered to be reliable. However, PL has not independently verified the accuracy or completeness of the same. Neither PL nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made av ailable or expressed herein or for any omission therein.

Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or

otherwise of any investments will depend upon the recipient's particular circumstances and, in case of doubt, advice should be sought from an independent expert/advisor.

Either PL or its affiliates or its directors or its employees or its representatives or its clients or their relatives may have position(s), make market, act as principal or engage in transactions

of securities of companies referred to in this report and they may have used the research material prior to publication.

PL may from time to time solicit or perform investment banking or other services for any company mentioned in this document.

PL is a registered with SEBI under the SEBI (Research Analysts) Regulation, 2014 and having registration number INH000000271.

PL submits that no material disciplinary action has been taken on us by any Regulatory Authority impacting Equity Research Analysis activities.

PL or its research analysts or its associates or his relatives do not have any financial interest in the subject company.

PL or its research analysts or its associates or his relatives do not have actual/beneficial ownership of one per cent or more securities of the s ubject company at the end of the month immediately preceding the date of publication of the research report.

PL or its research analysts or its associates or his relatives do not have any material conflict of interest at the time of publication of the research report.

PL or its associates might have received compensation from the subject company in the past twelve months.

PL or its associates might have managed or co-managed public offering of securities for the subject company in the past twelve months or mandated by the subject company for any

other assignment in the past twelve months.

PL or its associates might have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve m onths.

PL or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject

company in the past twelve months

PL or its associates might have received any compensation or other benefits from the subject company or third party in connection with the research report.

PL encourages independence in research report preparation and strives to minimize conflict in preparation of research report. PL or its analyst s did not receive any compensation or other benef its from the subject Company or third party in connection with the preparation of the research report. PL or its Research Analysts do not have any material conflict of interest

at the time of publication of this report.

It is conf irmed that Ms. Aditi Patil- MBA Finance Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding

twelv e months

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

The Research analysts for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its

or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report.

The research analysts for this report has not served as an officer, director or employee of the subject company PL or its research analysts have not engaged in market making activity

f or the subject company

Our sales people, traders, and other professionals or affiliates may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expressed

herein. In rev iewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest.

PL and its associates, their directors and employees may (a) from time to time, have a long or short position in, and buy or sell the securities of the subject company or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the subject company or act as an

adv isor or lender/borrower to the subject company or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions.

US Clients

This research report is a product of Prabhudas Lilladher Pvt. Ltd., which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker-dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or

regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

This report is intended for distribution by Prabhudas Lilladher Pvt. Ltd. only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted

onward to any U.S. person, which is not the Major Institutional Investor.

In reliance on the exemption from registration provided by Rule 15a-6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major

Institutional Investors, Prabhudas Lilladher Pvt. Ltd. has entered into an agreement with a U.S. registered broker-dealer, Marco Polo Securities Inc. ("Marco Polo").

Transactions in securities discussed in this research report should be effected through Marco Polo or another U.S. registered broker dealer.

Prabhudas Lilladher Pvt. Ltd. 3rd Floor, Sadhana House, 570, P. B. Marg, Worli, Mumbai-400 018, India | Tel: (91 22) 6632 2222 Fax: (91 22) 6632 2209

www.plindia.com

Related Documents