venezueia IndustrialSector Report March 15, 1991 Brazil, Peru and Venezuela Energy and Induistry Division Country Department I Latin America and theCaribbean Region FOR OFFICIALUSEONLY o ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~~~ 3 .. o' '3 u~~~~~~~~~~~~~~~~~~~~~~ > j ) 5 < ' O \~~~~~ - - . ~ ~ ~ ~ ~ ~ ~ ~ . .3 . . 3 t ' ' ' ' ' 7 ' ' ' ' t '' ' ;" '0'3'" -V. CU'' ' ' ''* D ~ ~ ~ '3 .- - y 0 ~ ~ ~ ~ ~ ~ t ,_ ~ ~~~~~~~ O '3 '3 . U 3\ 3 _ *~~~~~~~~~~~~~~~~~~~ '3 Document ofthe YWrld Bank << .~~~~~~~~~~~- ". , _ ' , 4 o~~~~~~~~~~~~~~~~~1 ' . 3 This documnent has a restriicted distribution anci may beused by recipients . , only hn the perfomrnance oftheir official duties. Its contents 'may nototerwise be disclosed without World Bank authorization.. ^ - ' : Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

venezueiaIndustrial Sector Report

March 15, 1991

Brazil, Peru and Venezuela Energy and Induistry DivisionCountry Department ILatin America and the Caribbean Region

FOR OFFICIAL USE ONLY

o ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~~~ 3 .. o' '3

u~~~~~~~~~~~~~~~~~~~~~~ > j ) 5 < ' O

\~~~~~ - -

. ~ ~ ~ ~ ~ ~ ~ ~ . .3 . . 3

t ' ' ' ' ' 7 ' ' ' ' t '' ' ;" '0'3'" -V.

CU'' ' ' ''*

D ~ ~ ~ '3 .- - y

0 ~ ~ ~ ~ ~ ~ t

,_ ~ ~~~~~~~ O

'3 '3 . U

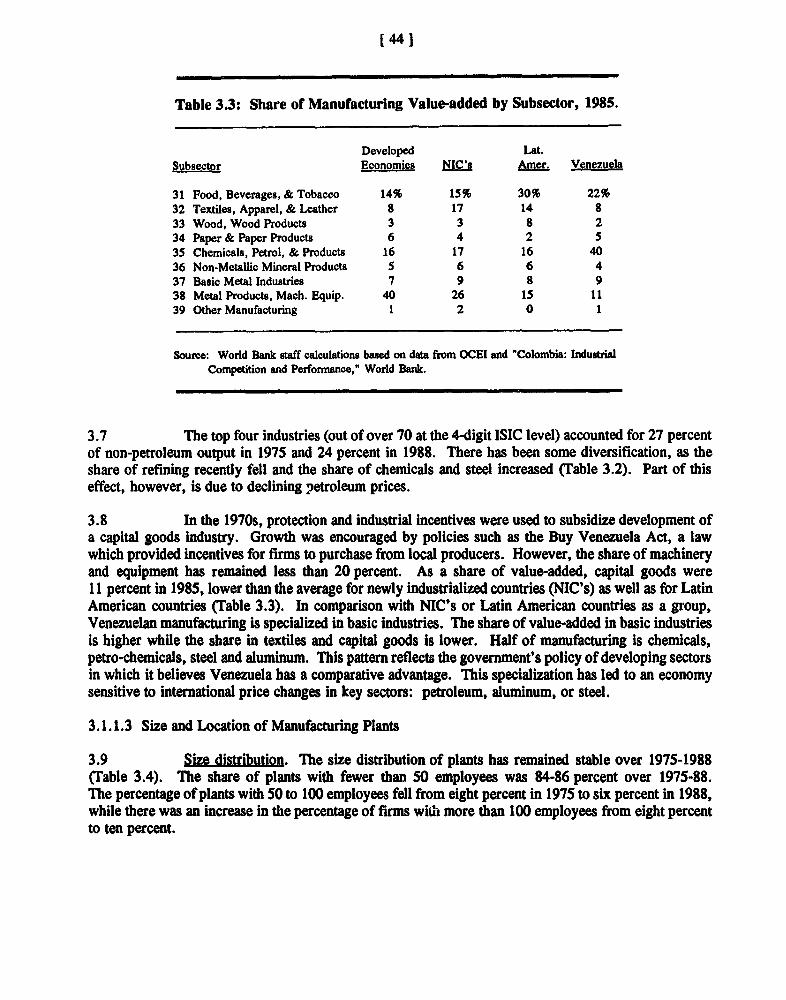

3\ 3 _

*~~~~~~~~~~~~~~~~~~~ '3

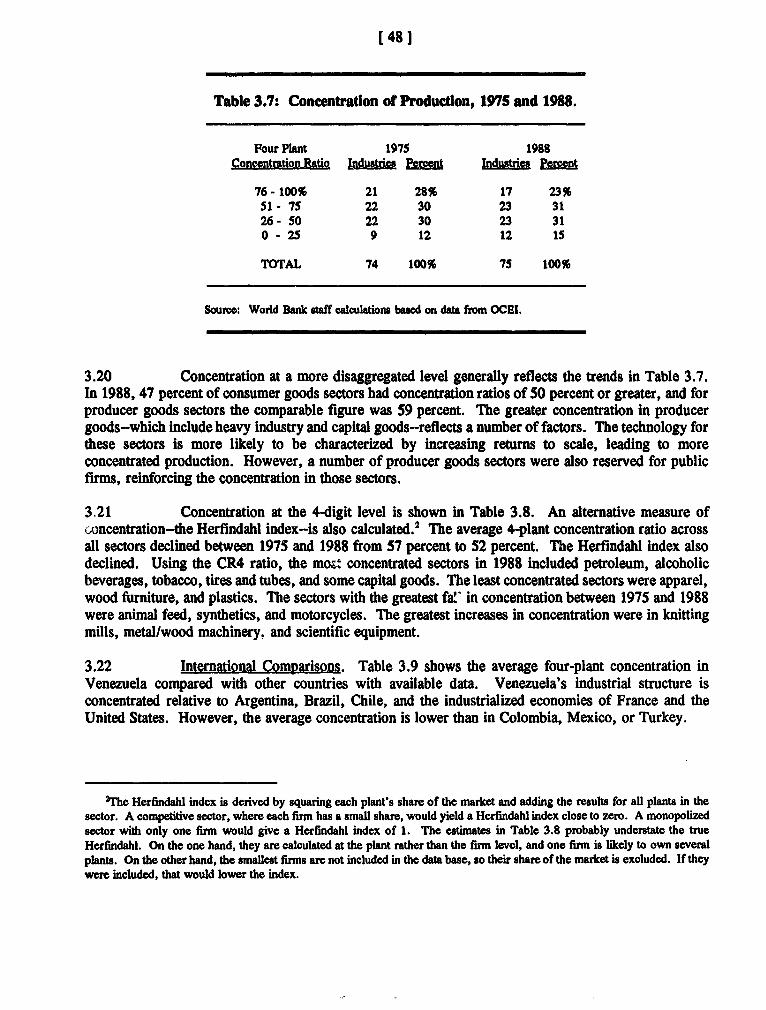

Document of the YWrld Bank <<.~~~~~~~~~~~- ". ,

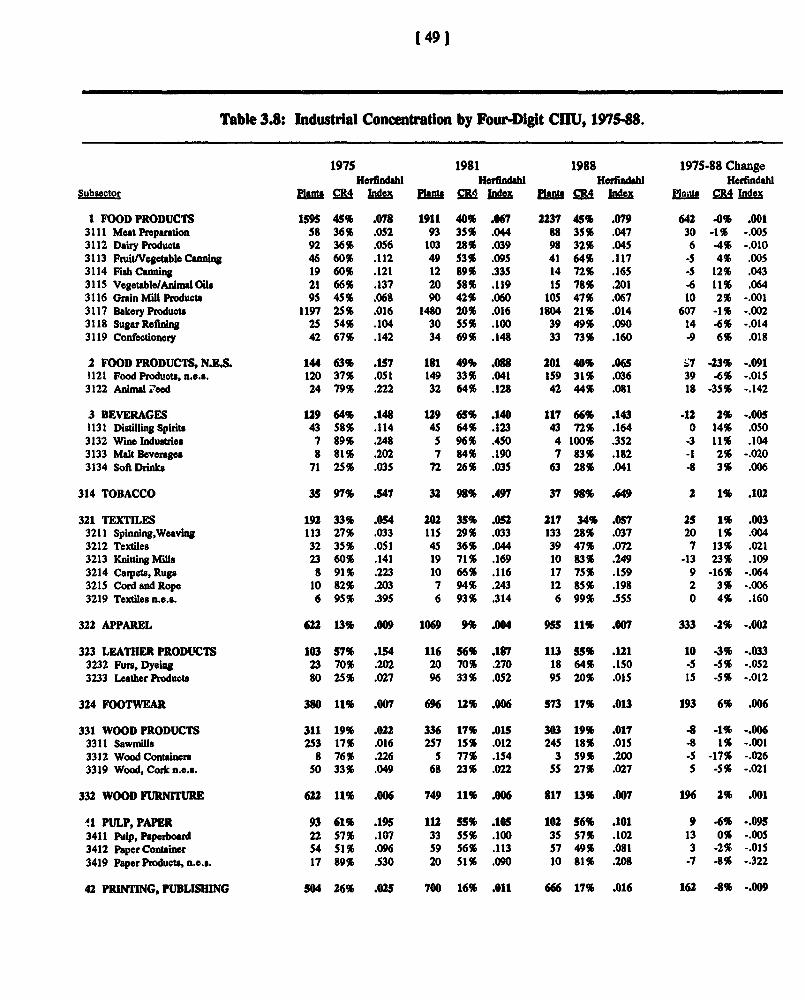

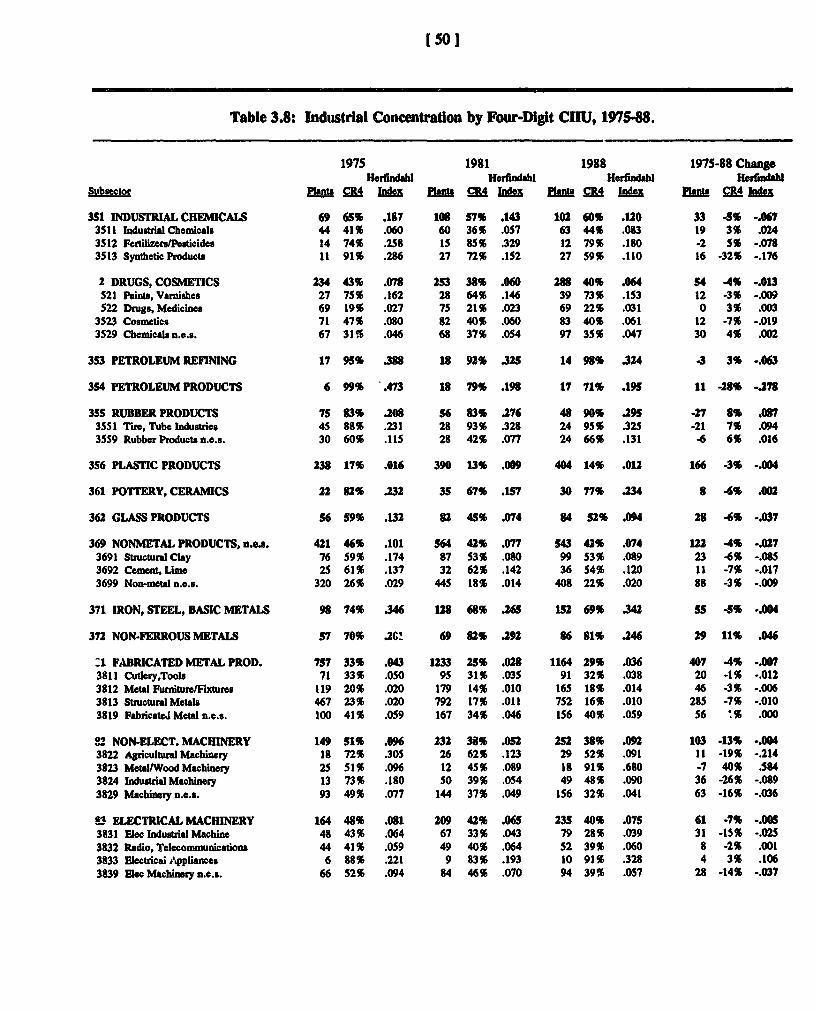

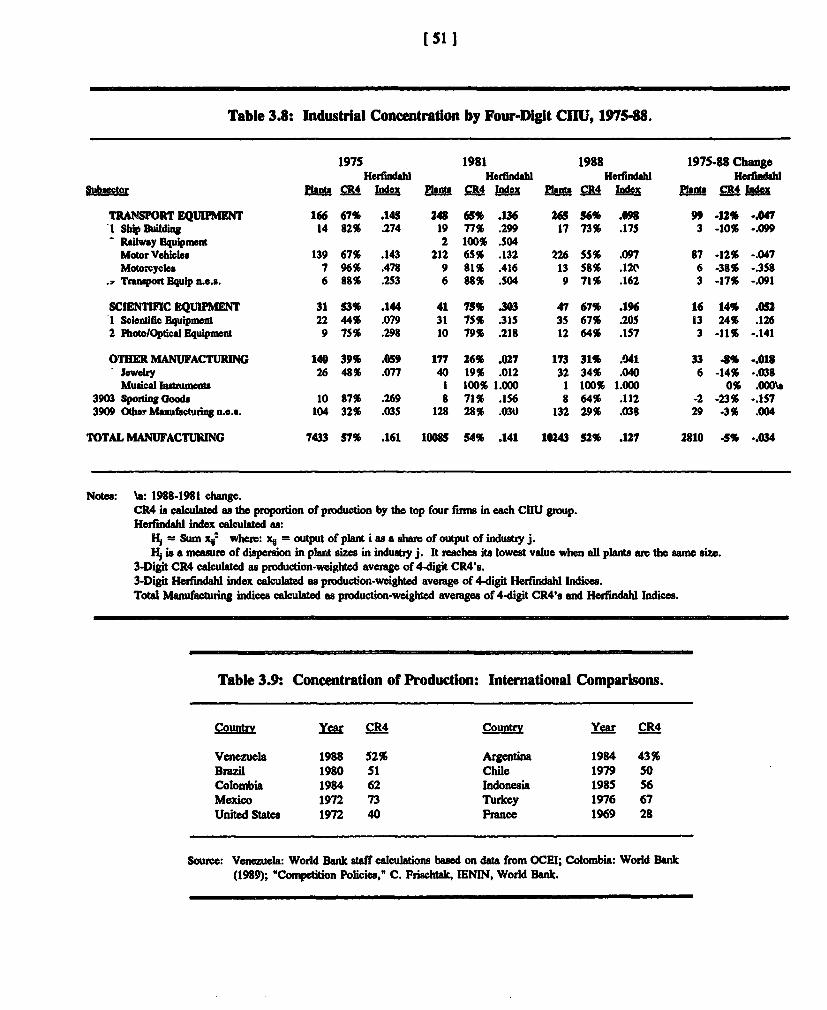

_ ' , 4 o~~~~~~~~~~~~~~~~~1 ' . 3

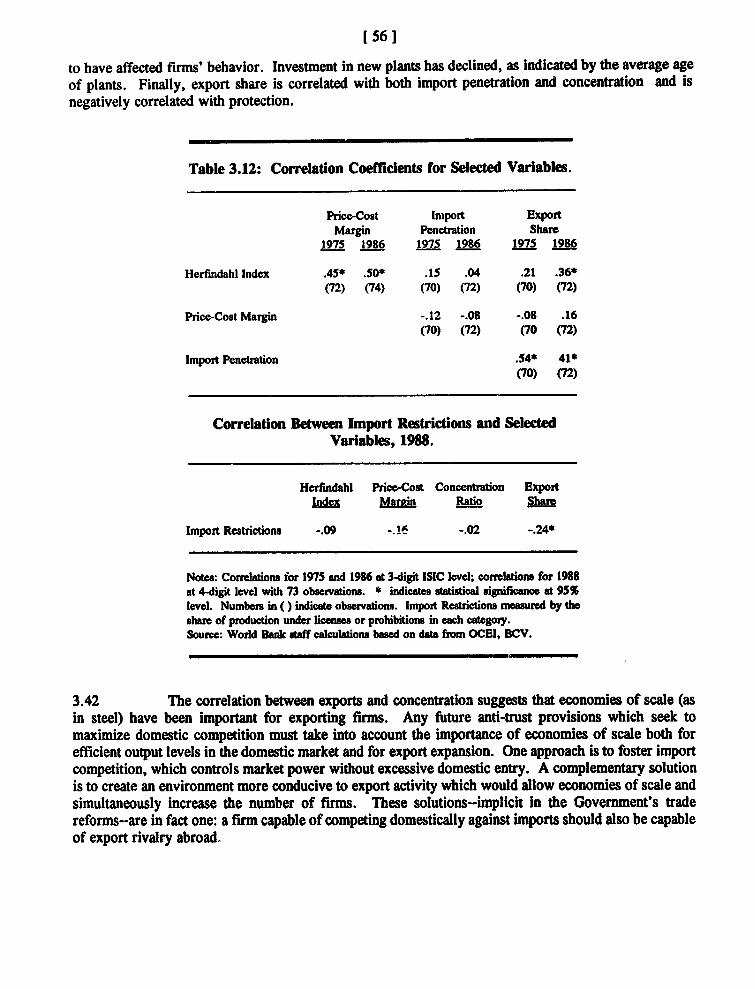

This documnent has a restriicted distribution anci may be used by recipients . ,only hn the perfomrnance of their official duties. Its contents 'may not oterwisebe disclosed without World Bank authorization.. ^ - ' :

Pub

lic D

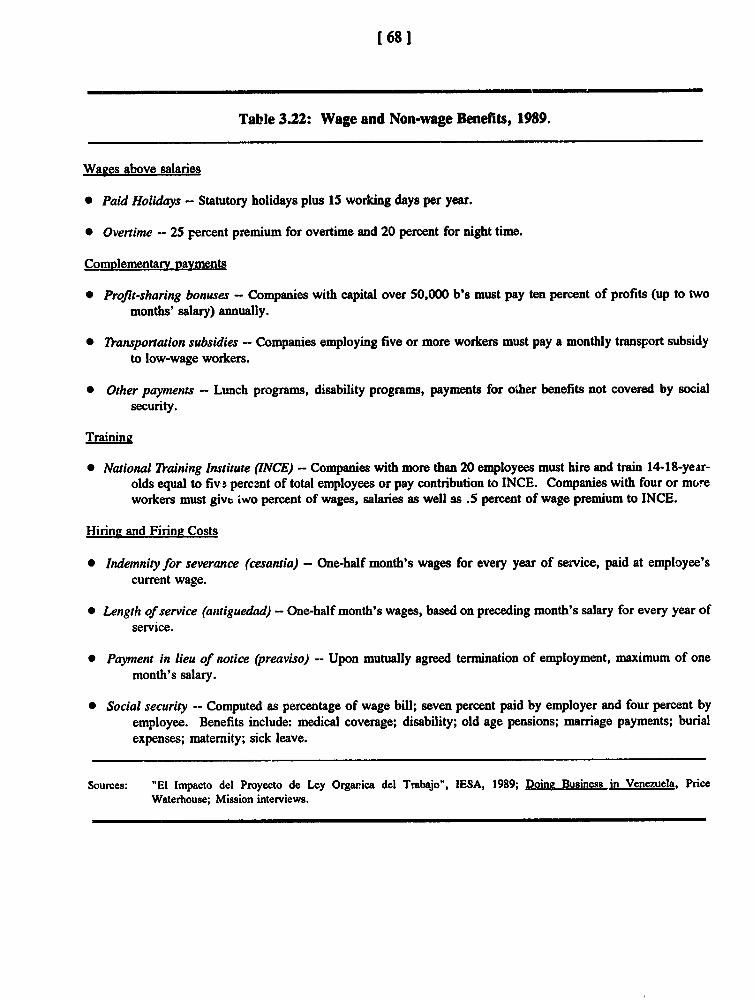

iscl

osur

e A

utho

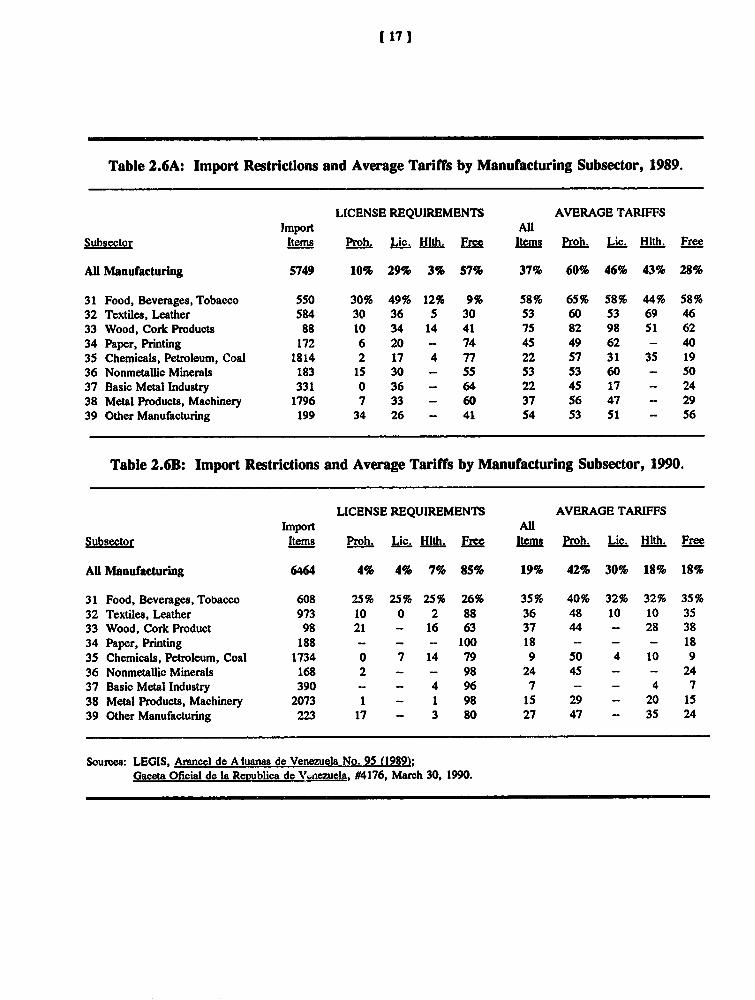

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

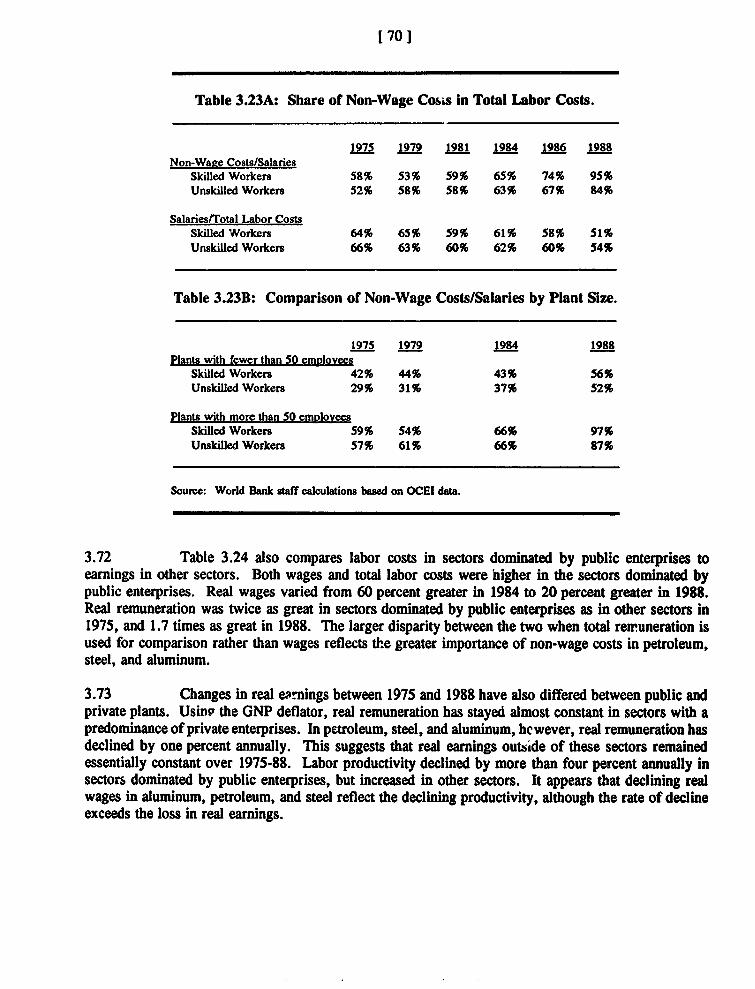

osur

e A

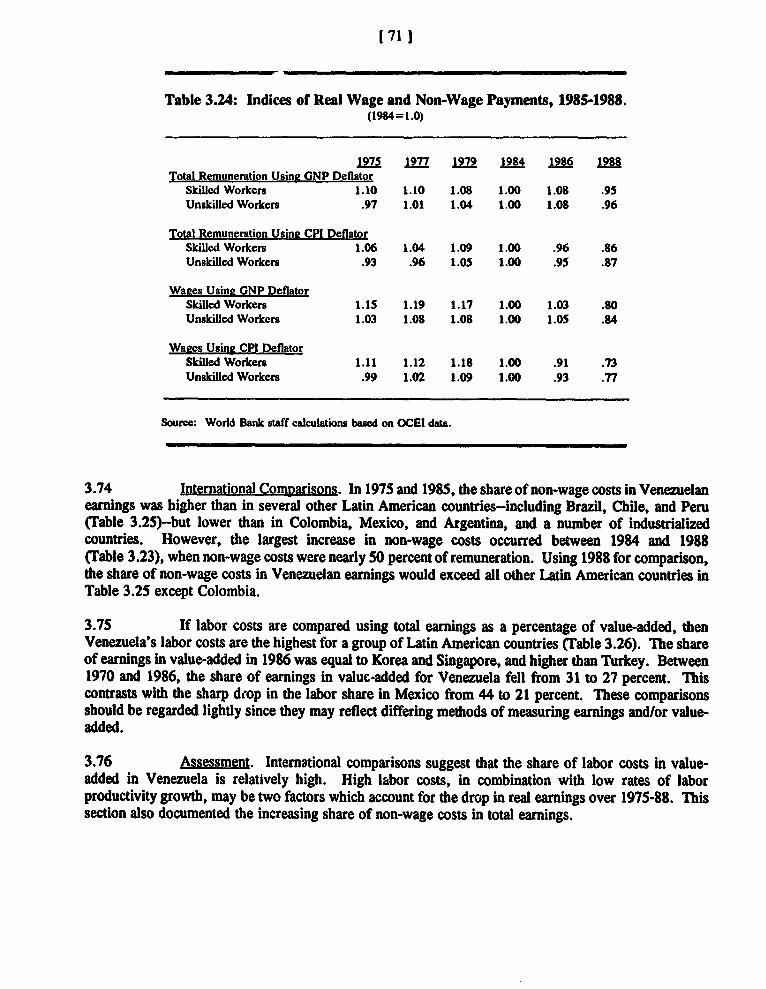

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EOUIVALENTS

Currency Unit = Bolivar (Bs)US$1 = 48.75 Bs

(As of September 26, 1990)

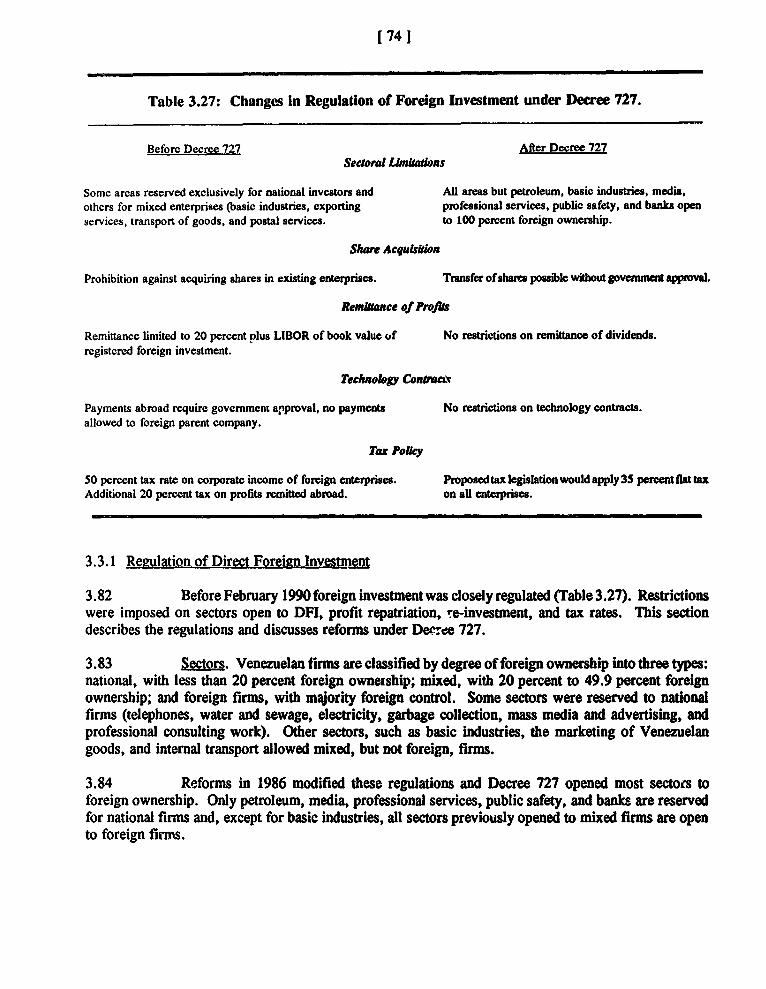

ACRONYMS

LCASA - Aluminio del Caroni, S.A. (State-owned aluminum company)HV - Banco Central de Venezuela (Central bank)ADAFE - Compaiifa An6nima de Administraci6n y Fomento El6ctrico (State-owned electric

company)NTV - Compafifa An6nima Venezolana de Tel6fonos (State-owned telephone company)AVN - CompafiMa An6nima Venezolana de Navegaci6n (State-owned shipping line)DRPOINDUSTRIA - Small and Medium Industry Development CorporationK]D - Completely-knocked-down assembly unitNC - Central North Coastal RegionR - Concentration RatioVG - Corporaci6n Venezolana de GuayanaFl - Direct Foreign InvestmentPZ - Export Processing Zone[NEXPO - Export Financing FundIV - Fondo de Inversiones de Venezuela (Venezuelan Investment Fund)DNCAFE - Fondo de Caf6 (Coffee buying and exporting board)3)NCREI - Fondo de Credito Industrial (Government industrial development fund)DNTUR - Fondo de Turismo (Government tourism development fund)DP - Gross Domestic Product4CE - Instituto Nacional de Cooperaci6n Educativa (Government training institute)iP - Instituto Nacional de Puertos (Government ports institute)[BOR - London Inter-Bank Offer RateIC - Newly Industrialized CountryTB - Non-tariff BarrierCEI - Oficina Central die Estadfstica e Informatica (Statistical agency)EQUIVEN - Petroqufmica de Venezuela (State-owned chemical producer)DVSA - Petr6leos de Venezuela, S.A. (State petroleum producer)VP - Precio de Venta al Pdblico (Maximum retail price)ECADI - Oficina del iogimen de Cambios Diferenciales (Office of the differential exchange rate)IPI - Registro de Informaci6n de Proyectos Industriales (Industrial investment registry)[DOR - Siderurgica del Orinoco (State-owned steel company)[EX - Superintendencia de Inversiones Extranjeras (Superintendent of foreign investment)[VENSA - Sidertrgica Venezolana, S.A. (Private steel company)DE's - State-Owned EnterprisesENALUM - Industrias Venezolanas de Aluminio (State-owned aluminum company)IASA - Venezolana Internacional de Aviaci6n (State-owned international airline)

FOR OMCIAL USE ONLY

TABLE OF CONTENTS

LIST OF TABLES .............................................. - iv-

LIST OF FIGURES .............................................. - vi -

EXECUTIVE SUMMARY.... vii

1. INTRODUCTION ............................................ [11

2. INDUSTRIAL POLICY: THE 1980'S AND THE REFORM ............... . 7]

2.1 Trade Policy ................... .[-.-.-.*............ 81

2.1.1 Import Restrictions ..................................... [ 81

2.1.1.1 Foreign Exchange Controls [ 812.1.1.2 Non-tariff Barriers [1412.1.1.3 Tariffs [1912.1.1.4 Import Restrictions: Combined Effects [ 2012.1.1.5 Reform of the Import Regime [ 25 ]

2.1.2 Export Incentives ..................................... [25 ]

2.2 Public Enterprises ......................................... [27]

2.2.1 Distribution of Ownership ................................ [30]2.2.2 Policy Instruments .[.................................... 3012.2.3 Domestic Market Practices ....... [....................... 32]2.2.4 Impact on the Industrial Private Sector ........................ [ 33]2.2.5 Recent Policy Changes .................................. [ 34 12.2.6 Recommendations ..................................... [ 35 1

2.3 Other Instruments of Industrial Policy ........................... [36]

2.3.1 Price Controls . 3612.3.2 Financial Incentives ................... *.l 37 12.3.3 Tax Policy .[ 38]2.3.4 Production Subsidies .[ 39]

3. POLICIES AND PERFORMANCE IN THE MANUFACTURING SECTOR ..... 41

3.1 Overview of the Manufacturing Sector: Structure. Behavior. Performance .. 41

3.1.1 Structure of the Manufacturing Sector ........................ 41

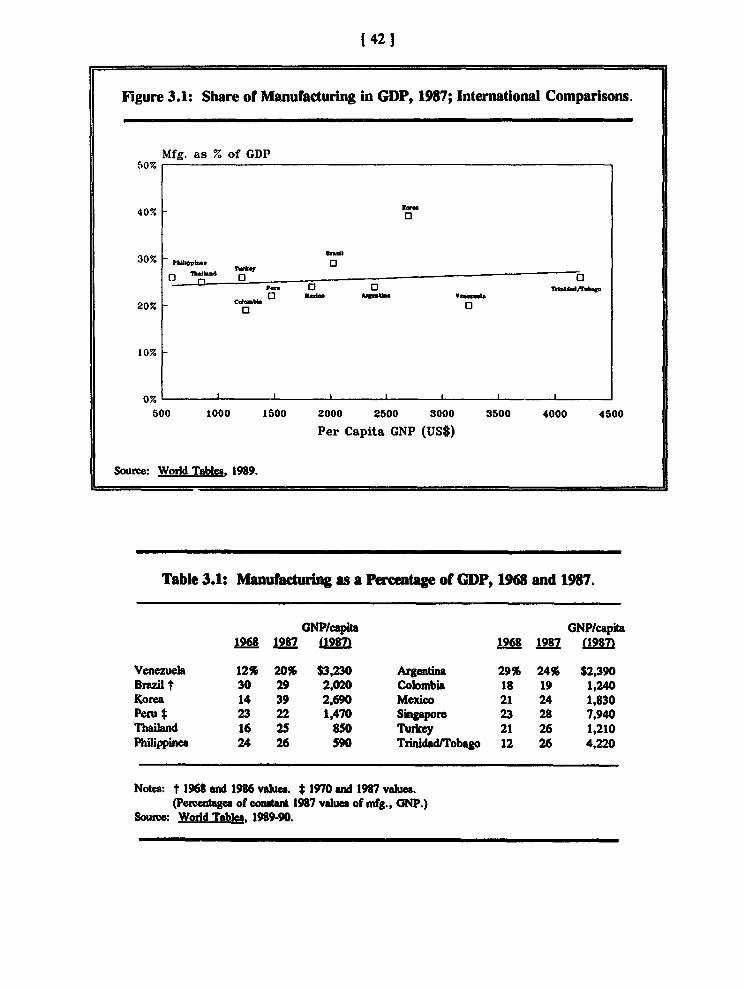

3.1.1.1 Share of Manufacturing in GDP 41

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

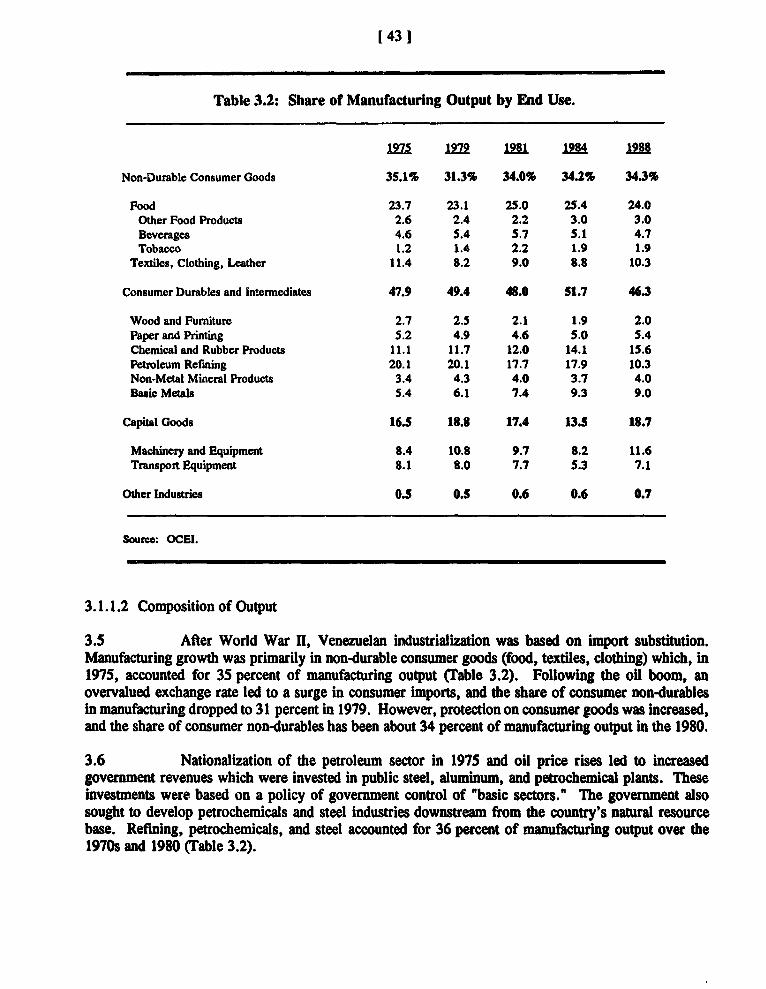

3.1.1.2 Composition of Output 1433.1.1.3 Size and Location of Manufacturing Plants [ 4413.1.1.4 Concentration of Production 1 47 1

3.1.2 Market Structure and Behavior ............................. [53 1

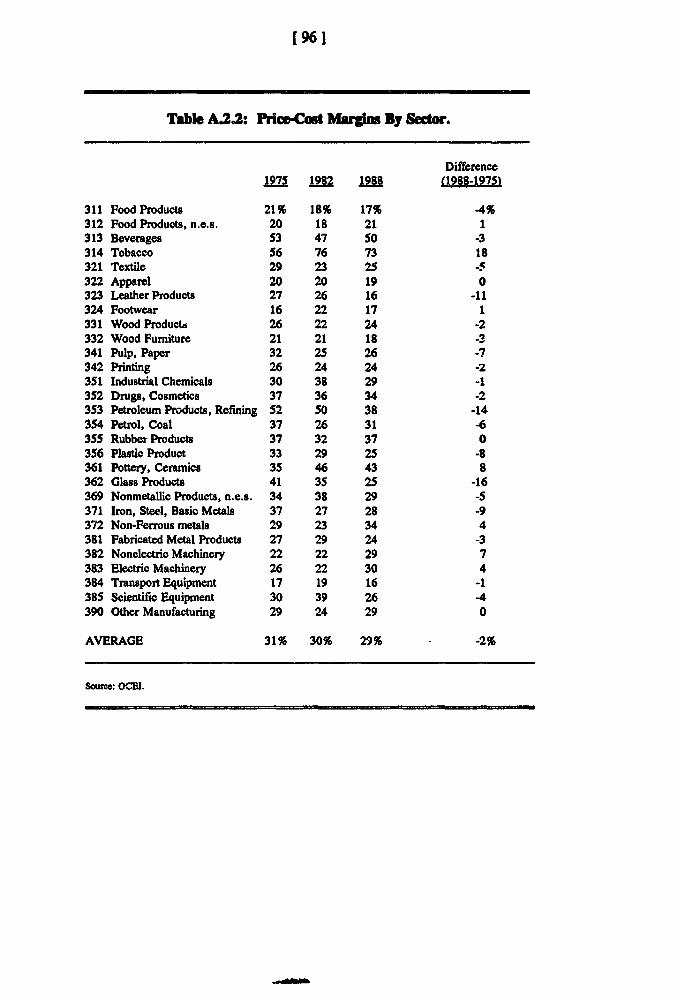

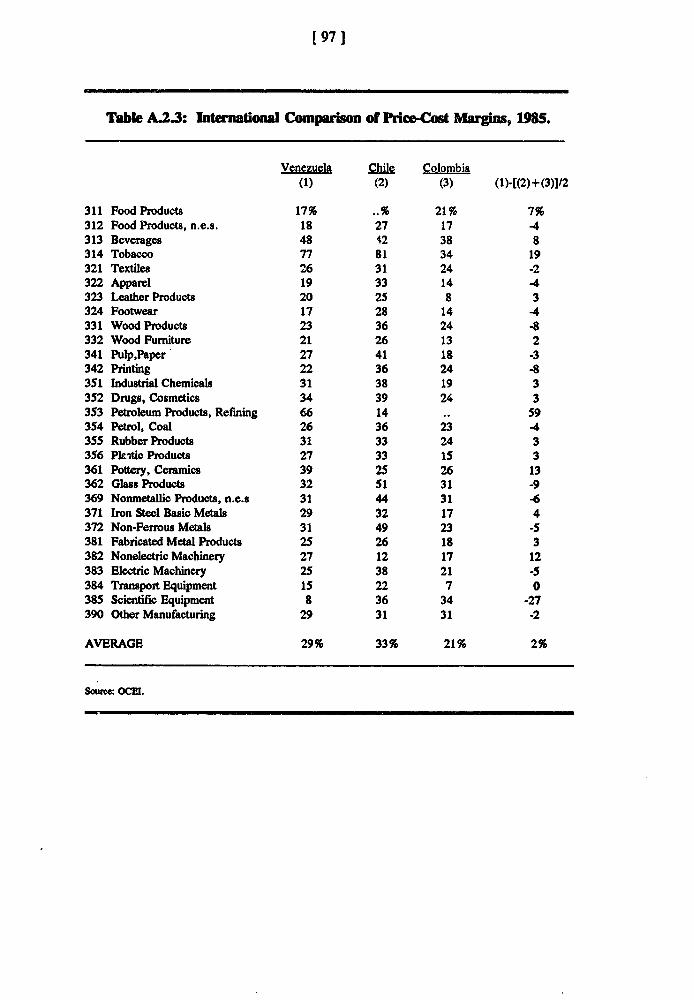

3.1.2.1 Concentration and Price-Cost Margir,s [ 54 13.1.2.2 Price-Cost Margins, Concentration, Import Competition and Export

Orientation [55 1

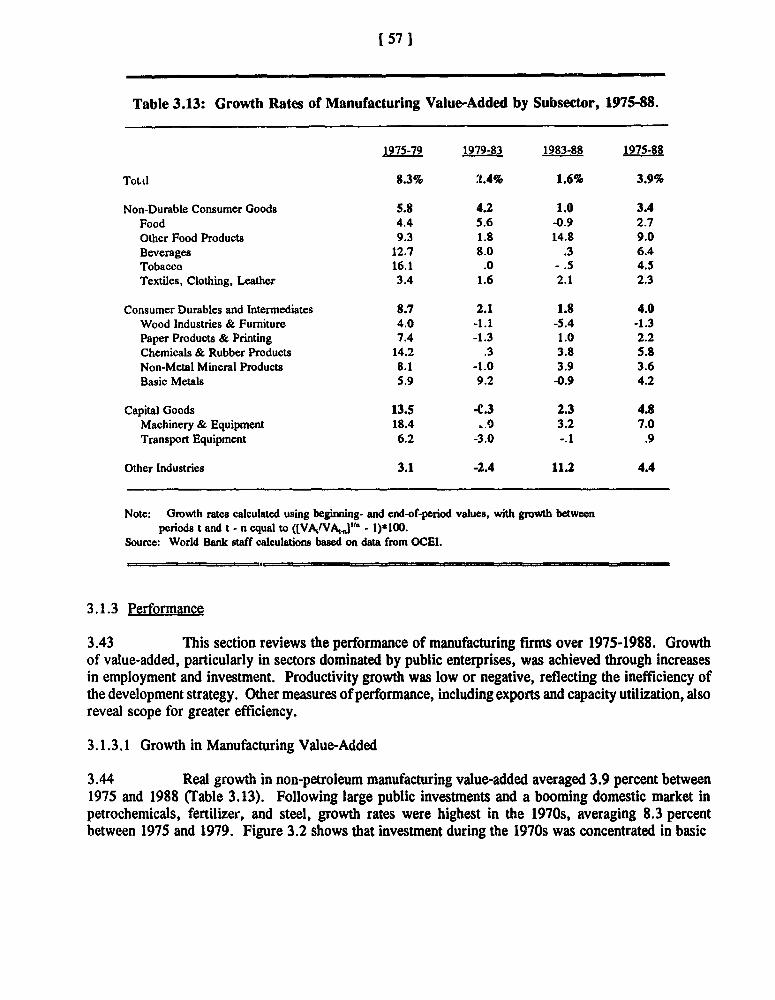

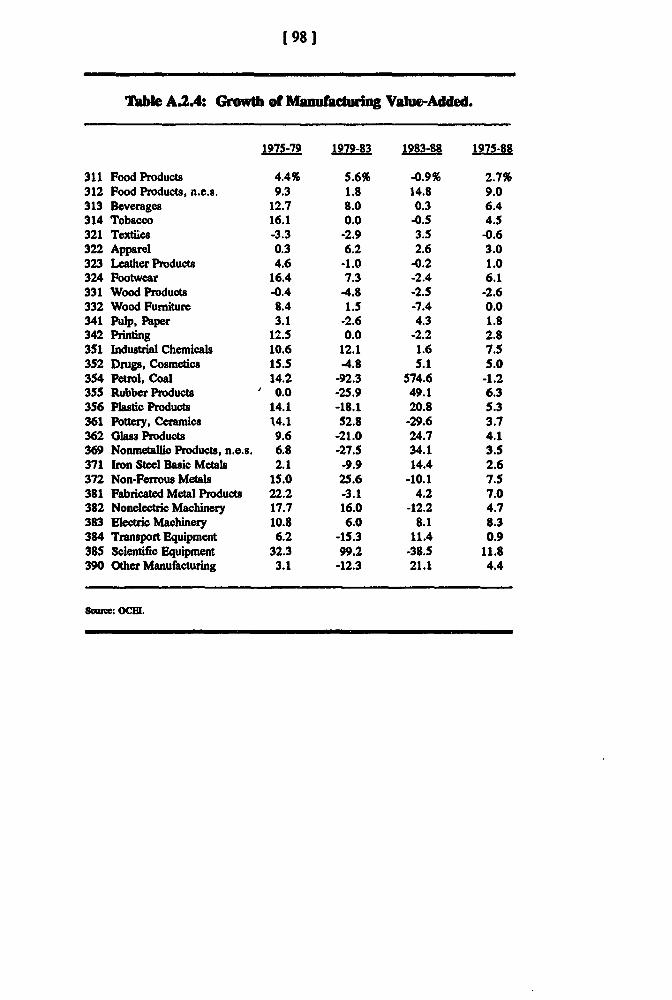

3.1.3 Performance ........................................ [57 1

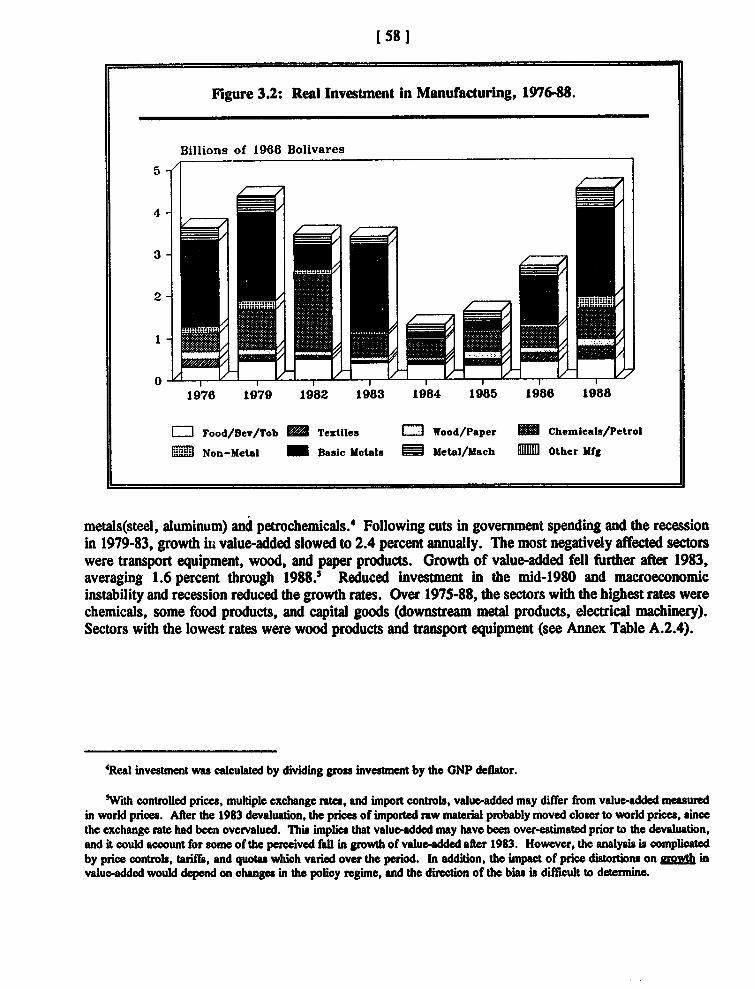

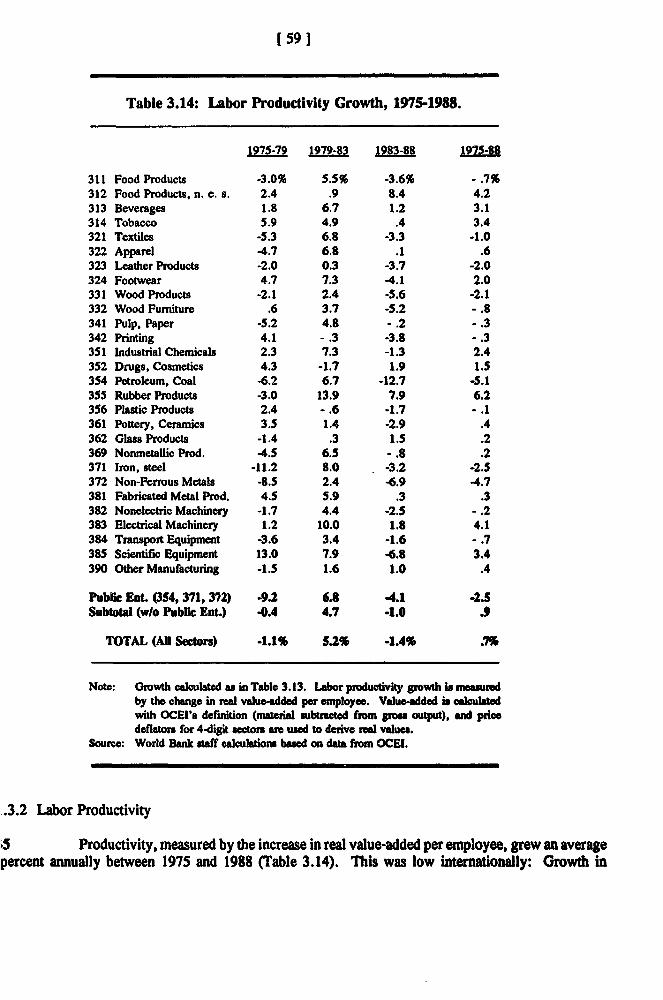

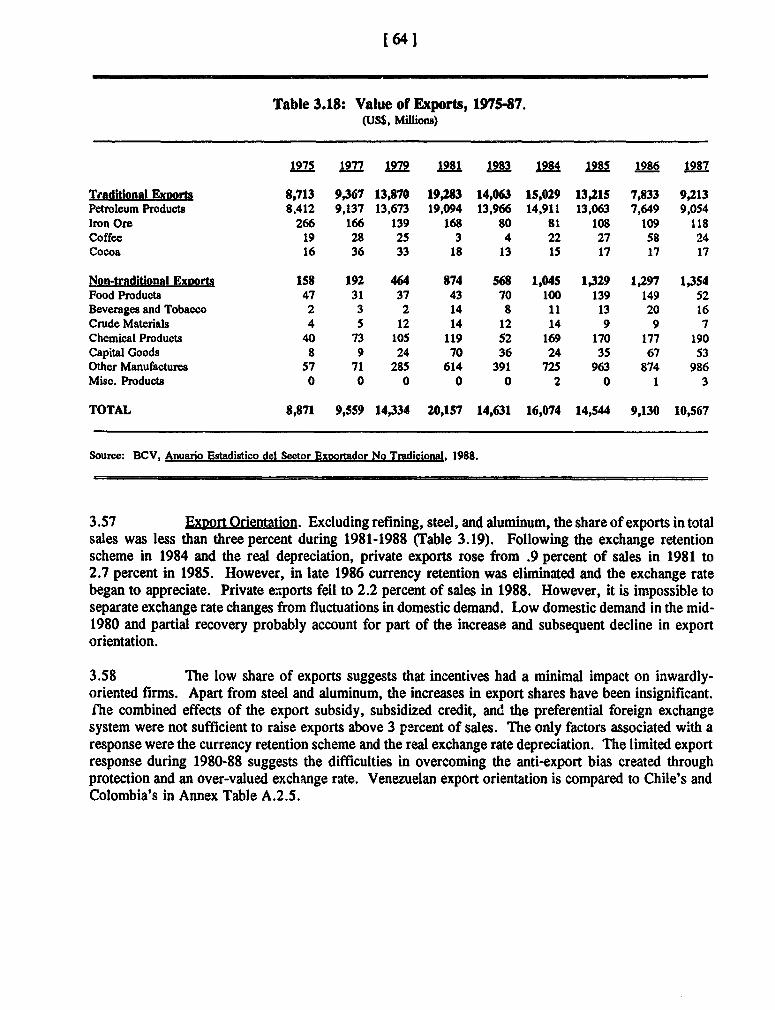

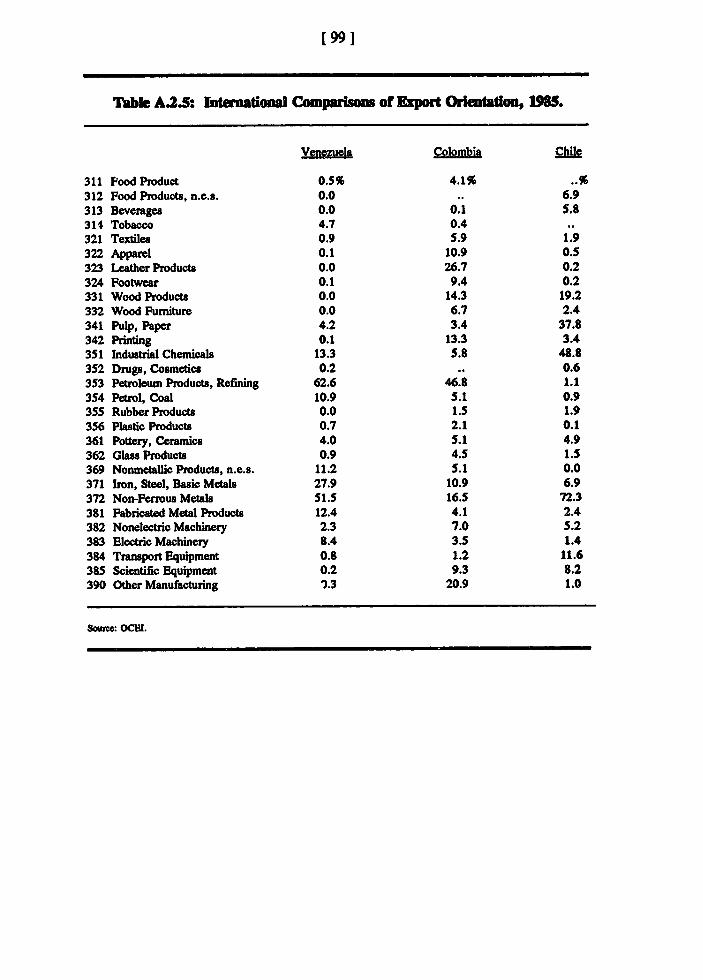

3.1.3.1 Growth in Manufacturing Value-Added [57 13.1.3.2 Labor Productivity [59 13.1.3.3 Productivity of Investment [61]3.1.3.4 Composition of Exports and Export Performance l61 ]3.1.3.5 Capacity Utilization [66 1

3.1.4 Ass,jssment ......................................... [67 1

3.2 Labor in the Manufacturing Sector: Policies and Evidence .............. [ 67 J

3.3 Foreign Investme,i .in the Manufacturing Sectr .[ 73 ]

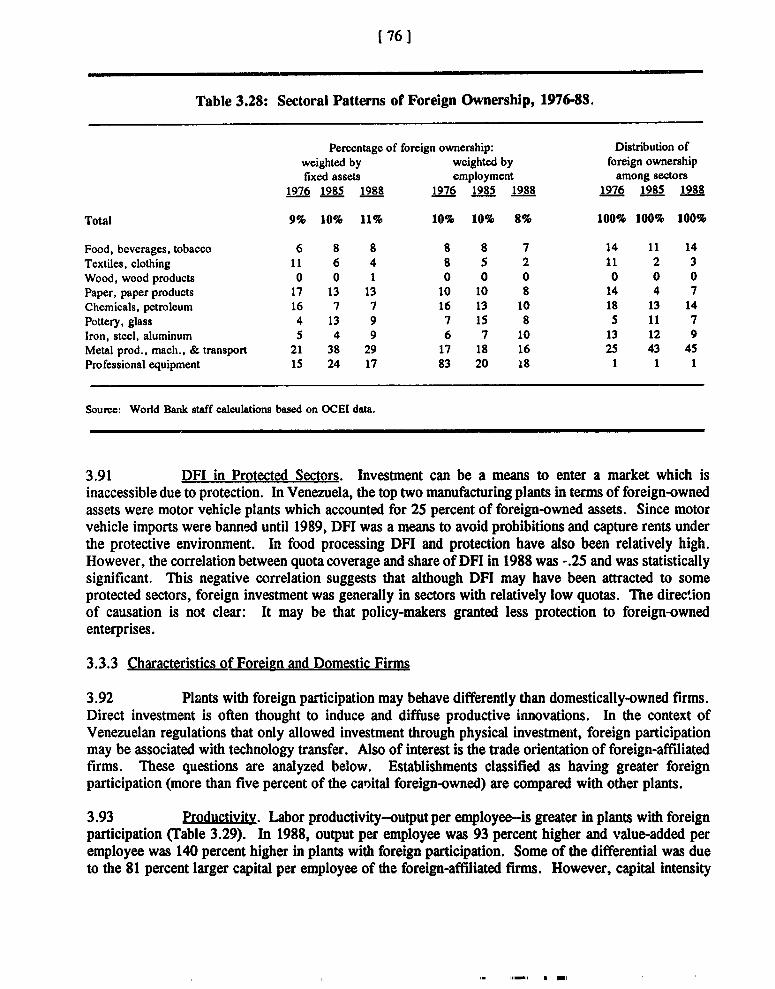

3.3.1 Regulation of Direct Foreign Investment ....................... [ 74 j3.3.2 Sectoral Pattern of Foreign Investment ........................ [ 75 J3.3.3 Characteristics of Foreign and Domestic Firms ................... [76]

4. AGENDA FOR THE 1990'S . . . 791

4.1 Trade Reform: Next Steps ............... [80]

4.1.1 Exchange R ........ [............................... [814.1.2 Uniform Treatment of Sectors ............................. 814.1.3 Licenses ........................................... [82]4.1.4 Tariffs ............................................ 82]4.1.5 Exemptions ......................................... [83 ]4.1.6 Exports and Export Subsidies .............................. 83]4.1.7 Export Processing Zones ................................. 84 14.1.8 Export Credit and Export Credit Insurance ..................... [854.1.9 Public Services ....................................... [851

4.2 Role of the Development Ministry ............ .. ................ 86 1

4.2.1 Investment Climate .................................... [86 1

4.2.1.1 Investment Promotion [87 1

- iii-

4.2.2 promotion of CompetitiQn ................................ 1891

4.2.2.1 Antitrust Legislation [901

4.2.3 InfQmatigiad Research ................................ 1941

APPENDIX 1 .. ................................................ ( 95 1

BIBLIOGRAPHY ............................................... 1011

- iv -

LIST OF TABLES

Table 1.1: Structure of Production and Domestic Absorption, 1971-88 ................... 21Table 1.2: Structure of Production--International Comparisons, 1965-87 ... .............. 3 1Table 1.3: Per Capita Manufactured Exports' 1980, 1987 .......................... [5 Table 1.4: International Comparisons of Productivity ............................. [6]

Table 2.1: Foreign Exchange Sales and Exchange Rates, 1984-87 ..................... 9Table 2.2: Imports by Type ar. ' Exchange Rates, 1981-88 ......................... [10]Table 2.3: Percentage of 1986 Imports at Free Market Rate ........................ 12 ]Table 2.4: Benefits to Merchandise Importers from the Preferential Exchange Rate, 1984-

87 .[. 14]Table 2.5A: Import Restrictions and Average Tariffs by Sector and Stage of Processing,

1989 ................................................... [16]Table 2.5B: Import Restrictions and Averaga Tariffs by Sector and Stage of Processing,

1990 . .................................................. [16]Table 2.6A: Import Restrictions and Average Tariffs by Manufacturing Subsector, 1989 ... ..... 17 1Table 2.6B: Import Restrictions and Average Tariffs by Manufacturing Subsector, 1990 ........ [17 ]Table 2.7A: Production Coverage of NTB's by Manufacturing Subsector, 1989 .... ......... 18 ]Table 2.7B: Production Coverage of NTB's by Manufacturing Subsector, 1990 .... ......... [18 ]Table 2.9: Manufacturing Value Added by State and Private Firms .................... [ 311

Table 3.1: Manufacturing as a Percentage of GDP, 1968 and 1987 ..................... [ 42]Table 3.2: Share of Manufacturing Output by End Use ........................... [ 43]Table 3.3: Share of Manufacturing Value-added by Subsector, 1985 ................... [ 441Table 3.4: Distribution of Plants by Size, 1975-1988 ............................ [45]Table 3.5: Comparison of Plant Sizes, 1984 ....... ................ .......... [ 45]Table 3.6: Distribution of Manufacturing Plants by State, 1975-88 .................... - 46 lTable 3.7: Concentration of Production, 1975 and 1988 ........................... [48]Table 3.8: Industrial Concentration by Four-Digit CIIU, 1975-88 ..................... [49]Table 3.9: Concentration of Production: International Comparisons ................... t]Table 3.10: Distribution of Plants by Age, 1975-1988 ............................ [53 Table 3.11: Price-Cost Margins by Degree of Concentration ........................ 54]Table 3.12: Correlation Coefficients for Selected Variables ................ [-. 56]Table 3.13: Growth Rates of Manufacturing Value-Added by Subsector, 1975-88 .... ......... [ 57]Table 3.14: Labor Productivity Growth, 1975-1988 .............................. [ 59]Table 3.15: Gross Investment as a Percentage of Value-Added, 1976-88 ................. [ 60]Table 3.16: Composition of Manufactured Exports, 1981-88 ........................ [61]Table 3.17: Types of Manufactured Exports, 1981-1988 ........................... [ 63 ]Table 3.18: Value of Exports, 1975-87 ...................................... [ 641Table 3.19: Export Orientation by Subsector .................................. [ 65]Table 3.20: Capacity Utilization, 1984-88 ....................-.- ... [ 66]Table 3.21: Factors Affecting Capacity Utilization, 1984-88 ......................... [ 66]Table 3.22: Wage and Non-wage Benefits, 1989 ................................ [ 68]Table 3.23A: Share of Non-Wage Costs in Total Labor Costs ......................... [70]Table 3.23B: Comparison of Non-Wage Costs/Salaries by Plant Size .................... [70]Table 3.24: Indices of Real Wage and Non-Wage Payments, 1985-1988 ................. [71]Table 3.25: Non-wage Costs: International Comparisons .......................... [ 72]Table 3.26: Total Earnings as a Percentage of Value-Added: International Comparisons ... .... [ 72]

- v -

Table 3.27: Changes in Regulation of Foreign Investment under Decree 727 ............... [74 lTable 3.28: Sectoral Patterns of Foreign Ownership, 1976-88 ..... ................... 76 ]Table 3.29: Behavior of Plants with 5% or More Foreign Participation and Plants with 100%

Domestic Participation, 1976-88 .................................. [77]Table 3.30: Sectoral Comparison of Foreign and Domestic Firms in 1988 ................ [78 ]

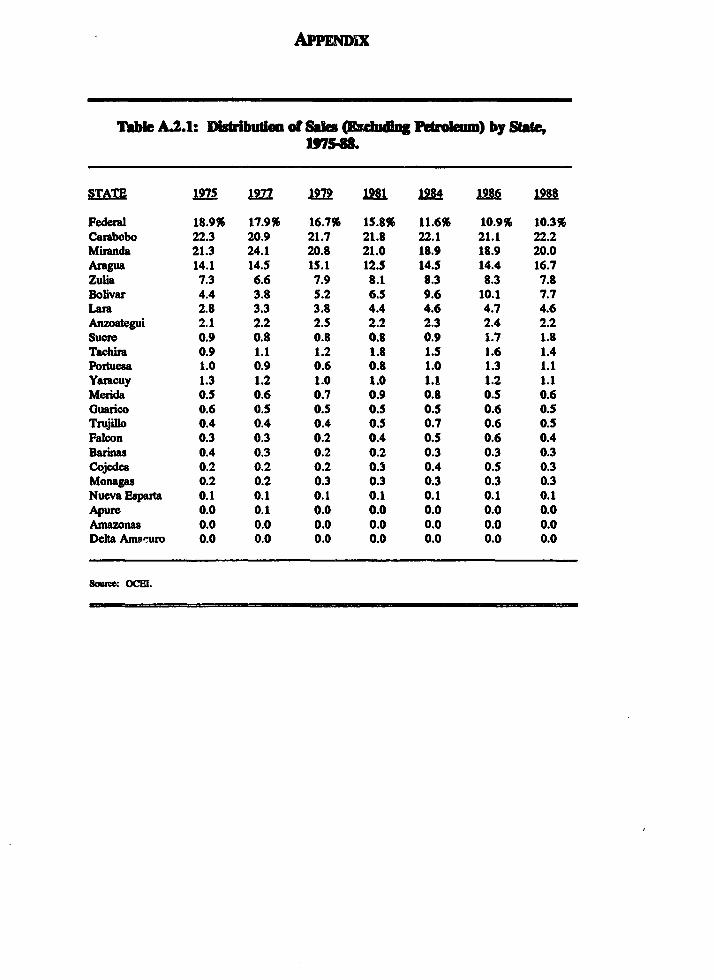

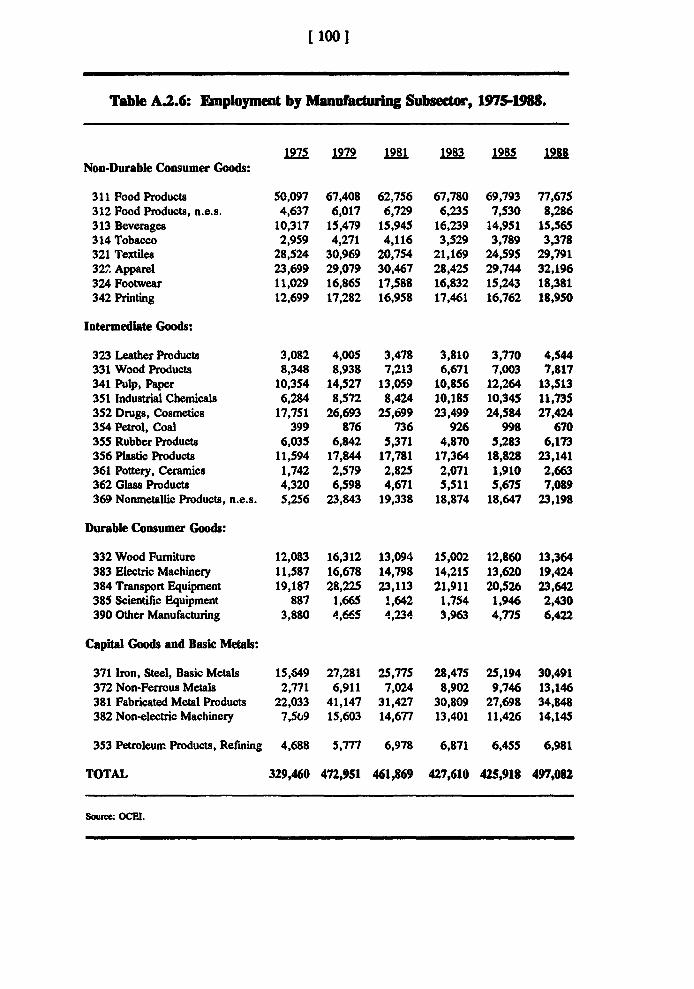

Table A.2. 1: Distribution of Sales (Excluding Petroleum) by State, 1975-88 ................ 95 ]Table A.2.2: Price-Cost Margins By Sector .................................... [ 96 ]Table A.2.3: Intemational Comparison of Price-Cost Margir.s, ' 985 .................... [ 97 ]Table A.2.4: Growth of Manufacturing Value-Added .............................. [ 98 ]Table A.2.5: International Comparisons of Export Orientation, 1985 .................... [ 99 lTable A.2.6: Employment by Manufacturing Subsector, 1975-1988 .................... [100 ]

- vi

I,s OF FIGURES

Box 1: Arbitrage Gains betwe,en Venezuelan and U. S. Financial Markets at Parallel Exchange Rates, 1984-89 ~ ................................................... [ 4]

Figure 2.1: Price and Output Under Official and Free Market Exchange Rates . ..... ........ 1 20 1Figure 2.2: Price and Output with Import Quotas. ............................... [ 22 ]Figure 2.3: Price and Output with Import Quotas On Outputs and Inputs ..... ............ [ 23 1

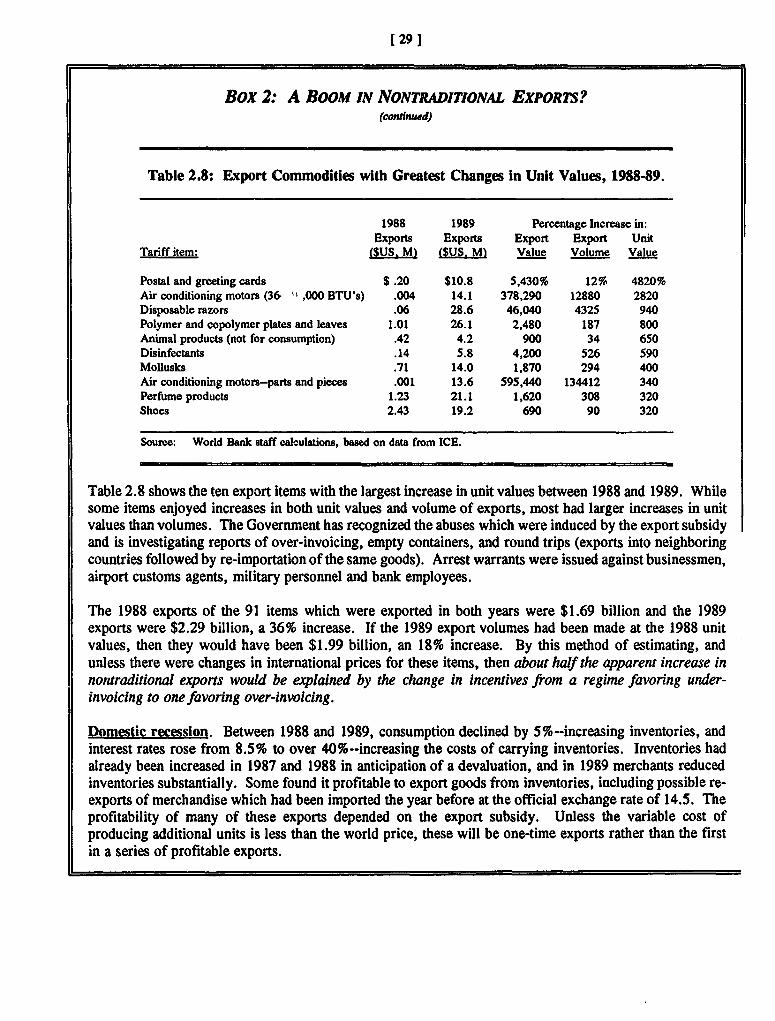

Box 2: A Boom in Nontraditional Exports? . 28 1

Figure 3.1: Share of Manufacturing in GDP, 1987; International Comparisons. [42 1Figure 3.2: Real Investment in Manufacturing, 1976-88. [ 58 lFigure 3.3: Non-Traditional Exports and the Real Effective Exchange Rate. [ 62 1

This' reprtisaed onwrk by :A-nnk: .Irisn .ol ... d.cnslat,Lntrt1et Lr~ h...(o.nsult. , ..M . .. . ..... i . . p,.ng ..n . . p .

h1gh-quality u in stein

EXECUTIVE SUMMARY

1. Introduction

1. Between 1974 and 1982 Venezuela enjoyed windfall oil revenues equal to about two years'GOP and supplemented these resources with foreign borrowing. The Government sought to diversify theindustrial base, reserving for itself the "strategic sectors" or "basic industries"--principally aluminum,steel, and energy. Private investors were encouraged to develop activities which would substitute forimports and which were' downstream from the basic industries. Import substitution was encouraged byprotection through tariffs and licenses, by directed credit, and by investment controls.

2. When oil prices dropped in the 1980s, the bolfvar became overvalued, but it could not bemaintained. In 1983 the bolfvar was devalued and a multiple exchange rate system was introduced.Exchange controls, which were changed frequently, ad.-d more discretionary incentives. Price controlswere applied throughout the economy. Many private exports were prohibited, and the anti-export biasdiscouraged most others.

3. The result was an uncoordinated, inefficient system characterized by contradiction,redundancy, and discretion. Through most of the 1980s, the government controlled every aspect of afirm's decisions: input prices and quantities, output prices, investments, employment conditions andmarket access. Venezuelans found the most profitable investment opportunities were outside the country.The petroleum windfalls had favored Venezuela, but the Government's economic policies encouragedhigher consumption and lower private investment, productivity, and GDP.

2. Ind4ustrial Policy: the 1980s and the Reform

4. Industrial policy in the 1980s concentrated power in government ministries and supplantedmarket-based tests of efficiency. Policy may have been based on benevolent intentions of maintainingwages and aiding poorer consumers, but the result was unnecessary costs and inefficiencies which werepassed on to labor in unemployment and to consumers in higher prices, lower quality, poorer service,and a reduced range of products.

2.1 Trade Policy

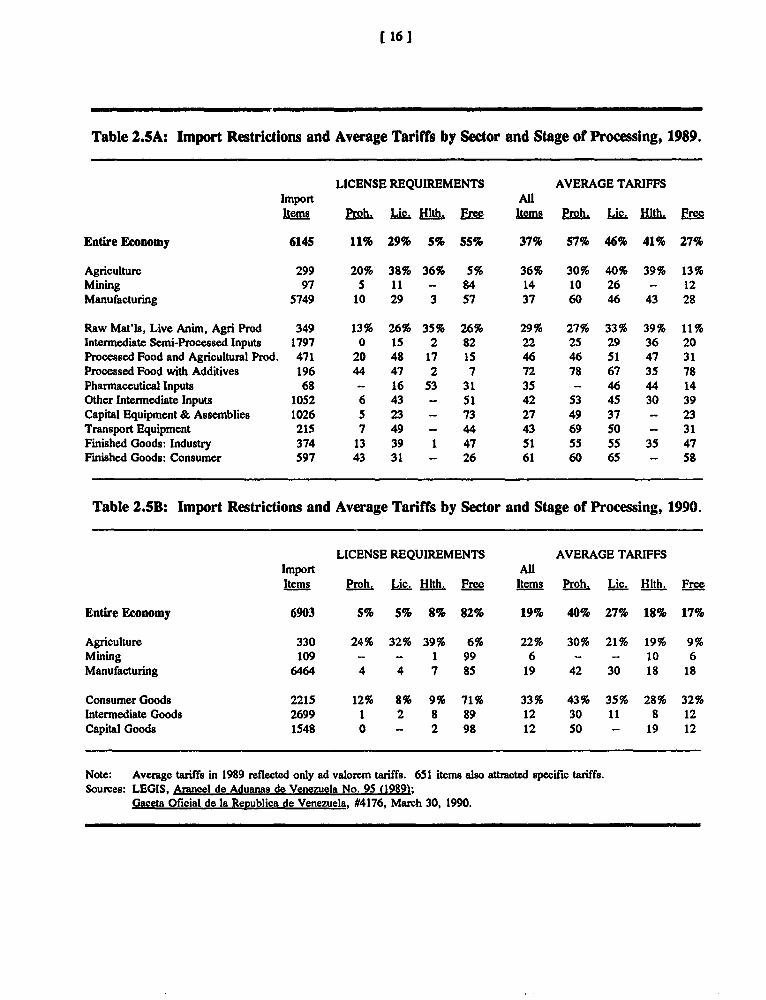

5. The most potent instruments of industrial policy during the 1980s were administered throughtrade policy: exchange allocations, import licenses and delegations, tariff exonerations, and exportincentives. Even with large export subsidies, the import controls created a regime in which the industrialsector had little incentive to compete in international markets.

6. 2.1. 1 Import Restrictions. To import most items into Venezuela, it was necessary to obtainan import permit from the Development or the Agricultural Ministry which would be granted only ifdomestic producers did not object. Licenses protected an estimated 50 percent of the manufacturingsector. Tariffs were prohibitive, but exonerations were commonly given if there was no domesticproduction. Tariff exonerations were worth about three percent of GDP annually.

7. Importers applied for foreign exchange at the official rate. Ten percent of imports enteredat the free market rate, which averaged 110 percent above the official rate. This large differential wasa heavy barrier to imports which made the right to exchange at the official rate a valuable benefit.

- viii -

Benefits .o merchandise importers--awarded with little control or accountability--were equal to betweenfive and 20 percent of GDP annually.

8. The combined impacts of these programs were large, but it is impossible to determine fromtheory how the benefits were divided among importers, workers, producers, and consumers. It has beencompletely reformed with the goal of applying licenses and prohibitions to protect no more than fivepercent of domestic p ouction, placing all tariffs in the range of ten to twenty percent by 1993, andmaintaining a unified, floating exchange rate.

9. 2.1.2 Export Incentives. Exporters were required to surrender their foreign exchange at theofficial rate but were offered three principal incentives: a currency retention scheme; an export subsidy;and preferential credit. The incentives favored low value-added exports. They were changed fre(iuentlyand without much prior notice so that exporters were reluctant to plan on them. Currency retention, atits peak in 1966, paid an estimated 2.8 percent of GDP for exJEorts which were about two percent ofGDP. The export subsidy averaged .3 percent of GDP (and 18 percent of the fob price of the exportswhich received it) and the value of export credit was probably less that .01 percent of GDP.

10. Currency retention was eliminated in 1987 and under the reform program the export subsidywas fixed at 30 percent of fob price for one year and reduced in stages to 15 percent and five percent.The high export subsidy, coupled with the free market exchange rate and the domestic recession led toan increase of nontraditional e:xports from $1.87 billion in 1988 to $2.79 billion in 1989. However, bylooking at changes in unit values of expoits, it is estimated that half the apparent increase can beac.ounted for by the change from a regime which rewarded und-r-invoicing to one which rewarded over-invo:cing: Either 1988 exports were higher than reported or 1989 exports were lower, or both.

2.2 Public Enterprises

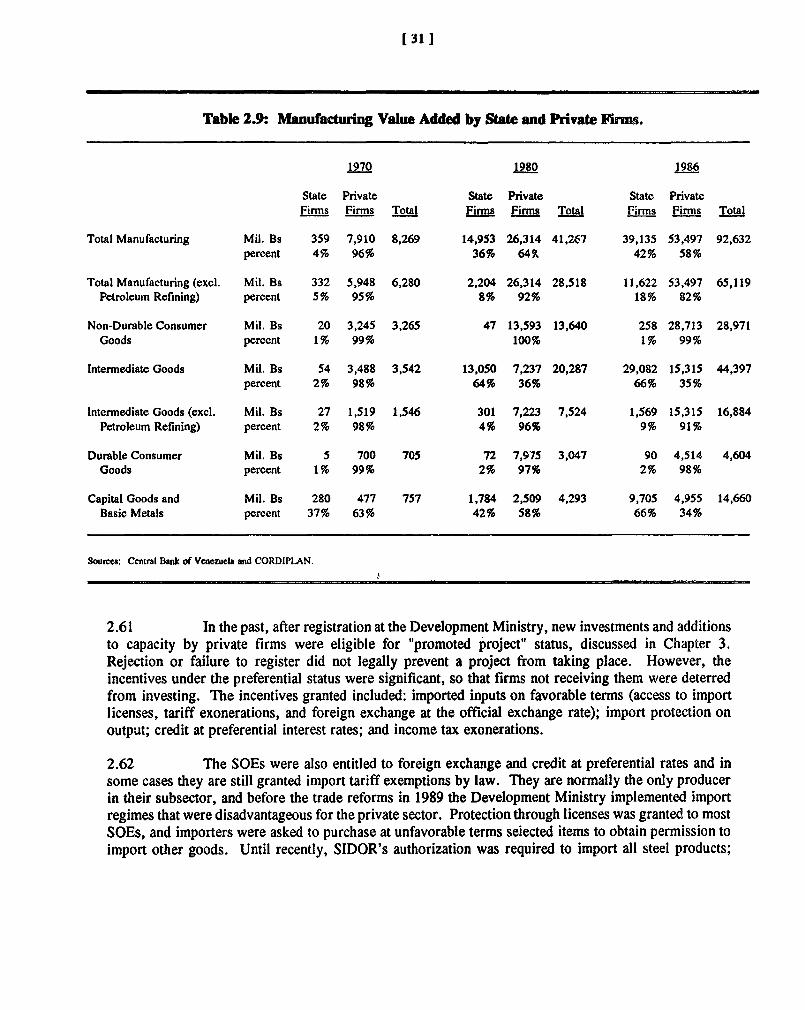

i1. State-owned enterprises (SOEs) produced 26 percen' of GDP in 1988. While petroleumaccounted for most production SOE also produced nine percent of goods and 18 percent of services. TheSOEs are concentrated in resource-based, export-oriented activities and in services. Their businesspractices vis-a-vis the private sector have reflected their monopolistic positions and resulted in transfersfrom private to public firms and in high-cost, unreliable goods and services. The Government's reformprogram--especially restructuring and privatization of major SOEs and trade and price liberalization--islikely to improve quality and services, but additional measures could be taken to increase SOEs' exposureto market forces.

2.3 Other Instruments of Industrial Policy

12. 2.3.1 Price Controls. In theory, every price was subject to Government controls, but theDevelopment Ministry regulated carefully the prices of 43 "basic necessities" and another 86 "priority"goods and services. The price controls caused occasional serious shortages and encouraged illegalexports. Under the reform program, controls were eliminated on all but 17 items.

13. 2.3.2 Financial Incentives. The Government channelled credit on favorable terms throughspecialized institutions. The total value of the subsidies to industry was relatively small, and directedcredit is being reduced under the financial sector reform program.

- ix -

14. 2.3.3 Tax Policy. Corporate tax rates are telatively high, but there are extensive exemptionswhich reduce the tax base, encourage evasion, distort resource allocation and, because they are sowidespread, lose much of their force. The tax system is being reformed in consultation with the IMF.

15. 2.3.4 Production Subsidies. Direct subsidies were used for food production and distribution:fertilizers, animal feed, powdered milk, corn meal, and coffee. The subsidies were not large as apercentage of GDP, but were large relative to the industries they affected. Subsidies have been retainedonly for fertilizer and powdered milk.

3. Policies and Performance in the Manufacturing Sector

16. Manufacturing output grew at an average rate of 3.9 percent between 1975 and 1988 due tolarge public investments, import protection, and targeted incentives. The cost of the industrial policiesof the 1970s and 1980s is reflected in reduced productivity, low capacity utilization, and the failure ofVenezuelan firms to compete effectively in international markets.

3.1 Overview of the Manufacturing Sector: Structure, Behavior, Performance

17. 3.1. I Structure of the Manufacturing Sector. The share of industry in GDP was 38 percentin 1987, while the share of manufacturing was 20 percent. Although manufacturing increased from12 percent of GDP in 1968, it is lower than in other countries at comparable stages of development.

1 8. In comparison with NIC's or Latin American countries as a group, Venezuelan manufacturingis specialized in basic industries. The share of value-added in basic industries is higher while the sharein textiles and capital goods is lower. Half of manufacturing is chemicals, petro-chemicals, steel andaluminum. This pattern reflects the government's policy of developing sectors in which it believesVenezuela has a comparative advantage.

19. Location. Industrial development centered in the central-northern-coastal (CNC) region wherethe largest markets were located. Apart from proximity to markets and access to better communicationand transportation, the CNC region benefitted from subsidized infrastructure and access to the centralgovernment which grants industrial in_entives. Location policies adopted in the .9- have not had aclear effect in moving production out of the Caracas area. Although restrictions on plant location led tosome movement out of Caracas, most plants seem to have moved to the surrounding areas. A mnoreefficient approach would be to set prices for utilities and housing services which reflect regionaldifferentials in costs and demand.

20. Plant Concentration. In 1975, 58 percent of all sectors had concentration ratios of 50 percentor greater. In 1988, 47 percent of consumer goods sectors had concentration ratios of 50 percent orgreater and, for producer goods sectors, the comparable figure was 59 percent. The greater concentrationin producer goods--which include heavy industry and capital goods--reflects a number of factors. Thetechnology for these sectors is more likely to be characterized by increasing returns to scale, leading tomore concentrated production. However, a number of producer goods sectors were also rserved forpublic firms, reinforcing the concentration in those sectors. Although the manufacturing sector has highconcentration, production levels in some sectors are below efficient scales. In the automotive industry,there are 15 assemblers in a market which fell from 163,000 units in 1982 to 26,000 units in 1989. Since

x -

production should be at least 100,000 units to exploit economies of scale, auto assemnbly cannot beefficient by international standards without exports.

21. Industrial policies have contributed to concentration. Restrict.ons on entry into key sectors,investment licenses, and exchange allocations have benefitted incumbents and reduced competition.Concentration does not necessarily reduce economic welfare, particularly where it permits the exploitationof economies of scale. Both in concentrated domestic markets and the contrasting case of fragmentedproduction, pressure from imports can either provide competition or the necessary impetus towardsconsolidation of production. Complementary domestic regulatory measures, however, may be necessary.Consolidation of production cannot occur without relatively easy exit and bankrupt%;y policies.

22. 3.1.2 Market Structure and Behavior. Concentration affected firms' pricing. There is asignificant, positive relation between one measure of concentration and price-cost margins during 1975-88. Import competition, which could be the chief element of market discipline in a small economy, doesnot seem to have affected firms' behavior. Investment in manufacturiig has declined, as indicated by theaverage age of plants. Finally, export share is positively correlated with both import penetration andconcentration and is negatively correlated with protectiou.

23. The correlation between exports and concentration suggests that economies of scale (as insteel) have been important for exporting firms. Any future anti-trust provisions which seek to maximizedomestic competition must take into account the importance of economies of scale both for efficientoutput levels in the domestic market and for export expansion. One approach is to foster importcompetition to control market power. A complementary solution is to create an environment moreconducive to export activity which would allow economies of scale and simultaneously increase thenumber of firms. These solutions--mp!icit in the Government's trade reforms-are in fact one: a firmcapable of competing domestically against imports should also be capable of export rivalry abroad.

24. 3.1.3 Performance. The period 1975-88 was characterized by inefficient growth of output.Large investments, financed by oil revenues, were directed to steel, aluminum, and petrochemicals.Manufacturing growth, which averaged eight percent during the late 197Cs, fell below two percent in themid-1980s. Inefficiency is evident in low growth of labor productivity or--in sectors dominated by publicenterprises--declines in the rates of output per worker. Other signs of inefficiency include high ratios ofinvestment to value-added in public enterprises, low rates of capacity utilization, and the manufacturingsector's inability to compete internationally.

3.2 Labor in the Manufacturing Sector: Policies and Evidence

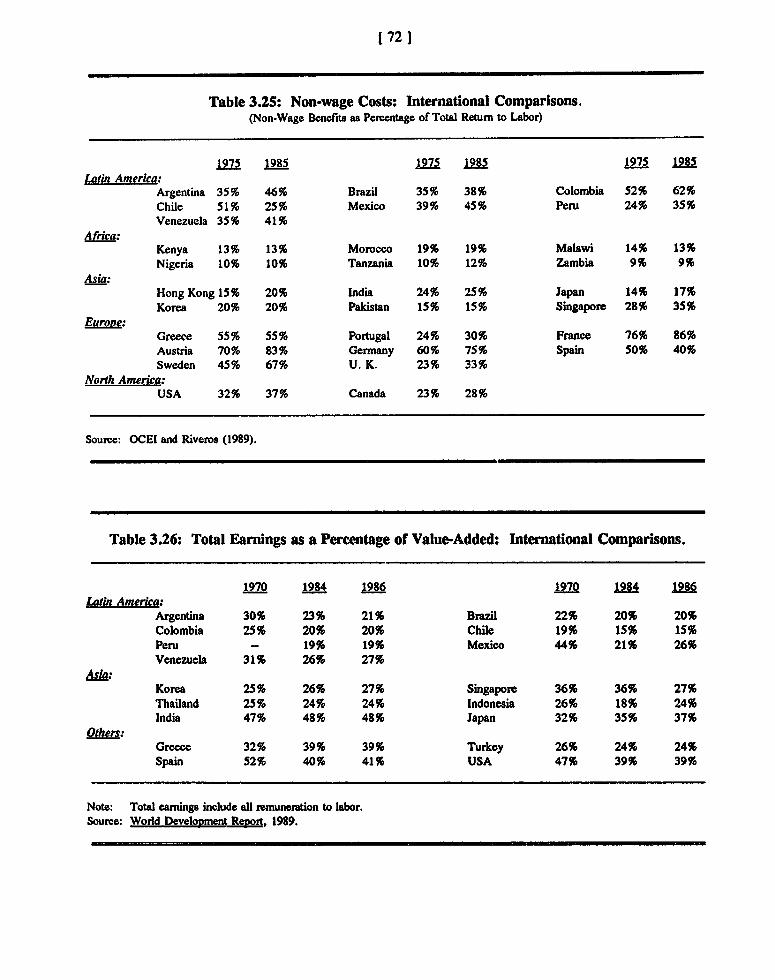

25. In the 1970s and 1980s, the government introduced measures to increase wages and non-wagebenefits. The evidence suggests that, although non-wage costs increased as a share of total labor coststo the employer, real wages fell between 1975 and 1988.

26. Changes in real earnings between 1975 and 1988 have differed between public and privateplants. Real remuneration stayed almost constant in sectors with-. a predominance of private enterprises.In petroleum, steel, and aluminum, however, real remuneration declined by one percent annually. Thissuggests that real earnings outside of these sectors remained essentially constant over 1975-88. Laborproductivity declined by more than four percent annually in sectors dominated by public enterprises, butincreased in other sectors. It appears that declining real wages in aluminum, petroleum, and steel reflectdeclining productivity, although the rate of productivity decline exceeds the loss in real earnings.

- xi -

27. International comparisons suggest that the share of labor costs in value-added in Venezuelais relatively high. High labor costs, in combination with low rates of labor productivity growth, may betwo factors which account for the drop in real earnings over 1975-88.

3.3 Foreign Investment in the Manufacturing Sector

28. Direct foreign investment (DFI) has been small in the manufacturing sector. Restrictions wereimposed on sectors open to DFI, on profit repatriation, on re-investment, and on tax rates. Theserestrictions were reformed in February 1990. Only petroleum, media, professional services, publicsafety, and banks are reserved for national firms and, except for petroleum production and iron ore, allsectors previously opened to mixed firms are open to foreign firms.

29. Very few plants have any foreign ownership. In 1988, 94 percent of plants were domesticallyowned, three percent were "mixed," and two percent were "foreign." The pattern of limited foreignparticipation held--although less strongly--among large firms: For firms with more than 100 employeesin 1988, 85 percent were 100 percent domestically owned. Foreign ownership is narrowly concentratedin a few large establishments and mixed enterprises. In 1988 three sectors (metal products andmachinery, chemicals, and food processing) accounted for almost three-quarters of foreign ownership.

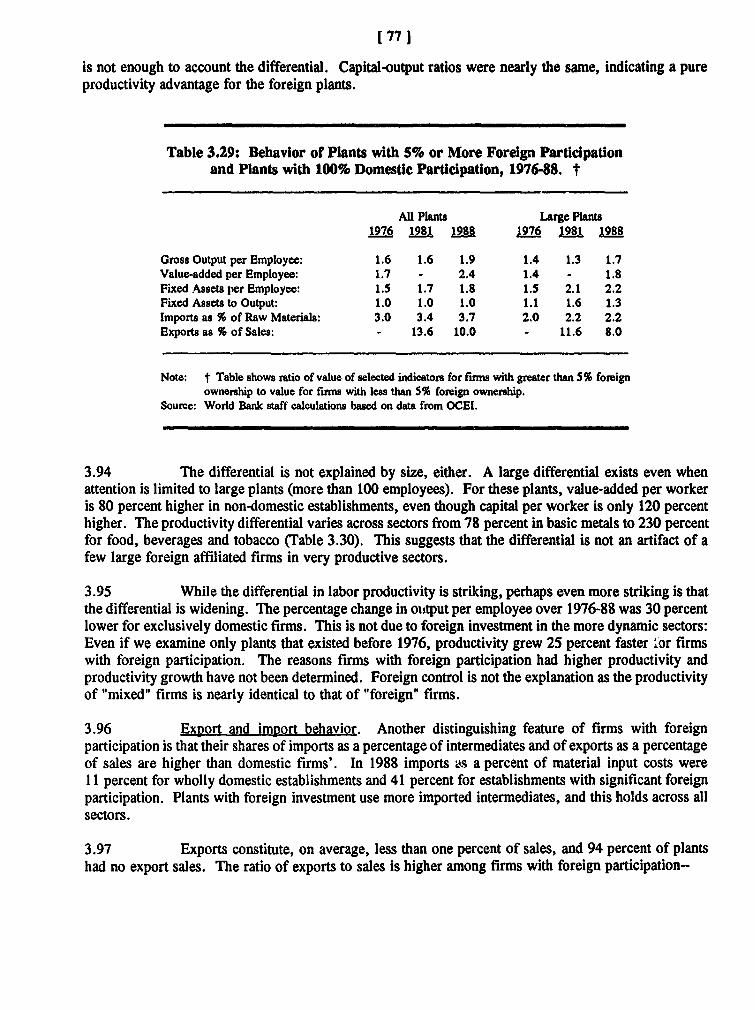

30. Labor productivity (output per employee) is greater in plants with foreign participation, andthe differential has been widening. Another distinguishing feature of firms with foreign participation isthat their shares of imports as a percentage of intermediates and of exports as a percent of sales are higherthan domestic firms'. The superior productivity and export performance of plants with foreignparticipation suggests that recent reforms, which open the economy to greater foreign participation, mayhave beneficial effects on performance.

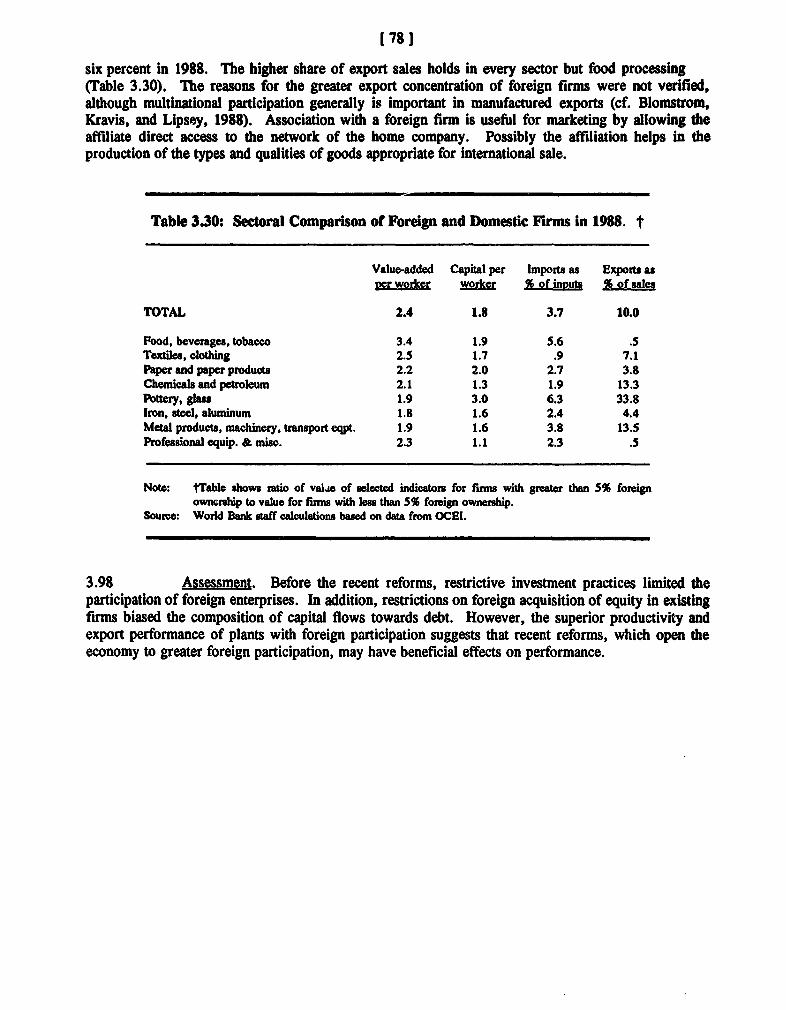

4. Agenda for the 1990s

31. The Venezuelan Government has abandoned the instruments it used to control the industrialsector in the 1980s, and is eliminating other discretionary industrial incentives. The economy is beingopened to foreign investment; taxes are being reformed; and privatization, public enterprise restructuring,and financial sector reform programs are being introduced. The thrust of these reforms is to reduce theGovernment's role in the economy and to give greater prominence to market-based incentives anddecisions. For the industrial sector, the outstanding items on the policy agenda are the continuation ofthe trade policy reforms and implementation of a domestic policy regime supportive of internalcompetition. The role of the Development Ministry in support of these reforms lies in promotingcompetition, fostering efficient investment, and providing and supporting information, research, andanalysis to advance the broad interests of the industrial sector in economic policy-making.

4.1 Trade Reform: Next Steps

32. The trade reform has replaced the system of uncontrolled, ad hoc protection and costly exportsubsidies with a system which--when it is fully implemented in 1993--will use effective exchange ratemanagement in place of directed programs aimed at import substitution or export promotion. Moderatetariffs-between ten percent and 20 percent--would offer additional protection for domestic economicactivities, and the Government's intention is to provide comparable levels of effective protection to allsectors to encourage efficient resource allocation. Licenses would provide further protection to no more

- xii -

than five percent of domestic manufacturing. This protection through licenses and tariffs would leavea residual anti-export bias which would be accepted as a cost to the economy. Export subsidies wouldbe eliminated.

33. 4.1. 1 Exchange Rate. The most important single element of the trade reform program hasbeen unifying and floating the exchange rate. Exchange rate management will encourage an efficientallocation of resources between the traded goods sector (importables and exportables) and the nontradedsector. In the future it will be necessary to manage the exchange rate to accommodate unexpectedchanges in petroleum prices. The Government is studying an oil stabilization fund to absorb revenueswhen prices are high and to utilize them when prices are low. Exchange rate management will benecessary to allow investors and producers to form reliable expectations of future exchange rates.

34. 4.1.2 Uniform Treatment of Sectors. One of the cornerstones of the adjustment program hasbeen to re-orient the economy based on transparent, broadly applicable general principles rather than theprevious array of industry-specific rules and standards. With the notable exception of agriculture (whichis currently being addressed) the Government has, to date, maintained an admirable degree of uniformityof treatment among sectors. Tnis is an important element of the program, both politically-to showimpartiality, and economically--to allow market forces, rather than bureaucratic or political judgements,to reveal the activities which are most robust.

35. 4.1.3 Licenses. As the Government approaches its medium-term goal of reducing licensesand prohibitions to protect no more than five percent of manufacturing, it will have to consider longer-term objectives. It should look at a longer-term goal of eliminating all licenses and prohibitions. Withtariffs, internal prices move with world prices, separated only by the percentage of the tariff rate. Tothe extent that the Government wishes to exempt some sectors from the forces of the adjustment program(expressed in Venezuela by the five percent target for licenses and prohibitions), it would be preferableto grant them through fixed-term (one-to-three years) tariff protection slightly (five-to-ten percent) abovethe ceiling for other sectors.

36. 4.1.4 Tariffs. The most important tariff reductions are yet to come. At each step, a greaterproportion of the domestic economy will be subject to foreign competition. Manufacturers which areunchallenged by imports with a 50 percent tariff will find greater competition at 20 percent.

37. As the Government approaches its medium-term target of a ten-to-twenty percent tariff range,it should consider its longer-term goals. It may wish to examine a longer-term goal of a unified tariffat a rate between five and ten percent or lower. The ten-to-twenty percent range could leave higheffective protection for activities of low value-added. Further, it would mean that Venezuelan consumerswould be paying prices 20 percent above world levels for many items, and it would continue to encourageinvestment in low value-added, inwardly-oriented industries. If Venezuelan industries are to becompetitive in world markets, they must also be competitive at home, and the surest way ofaccomplishing that would be to eliminate tariff protection so that investment would be directed to thoseactivities where Venezuela would be most competitive.

38. 4.1.5 Exemptions. Discretionary tariff exonerations have been eliminated except for someassembly operations. There also are exemptions, established in law, for some entities such as state-ownedenterprises, universities, and the central government. The remaining discretionary exemptions should beeliminated, and legislation should be introduced to abolish statutory exemptions.

- xiii -

39. 4.1.6 Expors and Exort Subsidies. Over the years, the role of export subsidies has beenforgotten and the Government had to fend off many spurious claims for exporters' right to the subsidy.The subsidy initially compensated exporters who, under the multiple exchange rate regime, were requiredto surrender their foreign exchange to the Central Bank at the official rate. With the unification andfloating of the exchange rate, the subsidy no longer served that purpose, and the Government was correctin reducing it and in its plans to eliminate it as soon as an effective duty and indirect tax rebate schemeis available to exporters.

40. 4.1.7 Export Processing Zones. There is interest within Venezuela in establishing exportprocessing zones (EPZ's). These zones are economic enclaves within which manufacturing for exportoccurs under virtual free trade conditions by exempting exporters from some administrative procedures,customs duties, and perhaps other taxes and/or labor laws. These are not an effecdive solution to long-term problems of efficient resource allocation, and will be less attractive in Venezuela as the trade reformlowers tariffs and other obstacles to international trade. While the Government should not discourageprivate development of EPZ's, it should avoid any programs which would subsidize them.

41. 4.1.8 Export Credit and EWport Credit Insurance. FINEXPO has offered credit at subsidizedrates to a limited number of exporters. There is no justification for these subsidies and they encouragemany distortions in the industrial incentives. Exporters should pay market rates for credit. TheGovernment should encourage the development of private markets which could provide suitableinstruments for export credit and insurance.

42. Exporters have sought subsidies for an export credit insurance scheme which would allowthem to export to risky clients in countries with poor credit records without bearing the political and/orcommercial risk of default. The Government should not subsidize such programs without a carefulanalysis to establish that the benefits would exceed the costs and risks. The records of most officialexport credit insurance agencies in other countries are poor. As long as there are no laws which preventprivate insurers from offering export credit insurance in Venezuela, the fact that it is not offered or is"too costly" most likely indicates that the exports involved would be too risky and should not beundertaken.

43. 4.1.9 Public Services. It is widely argued that the private sector has adjusted to the tradereforms and that the public sector has not. Entrepreneurs point to a long list of state-owned enterprisesand government services which are costly and inefficient: products of the basic industries,communications, electricity, water, shipping, ports, and customs administration. The Government hasbegun a program of restructuring and privatization which will address these concerns, but the programis a year-and-a-half behind the trade reforms. The correct policy response is not, as some haveadvocated, to offset these cost penalties with subsidies but, as the Government's restructuring andprivatization is designed to do, to eliminate them at the source. It is incumbent on the Government toplace its industrial sector in a more competitive position by eliminating government-imposed obstacles.The appropriate governmental role in promoting industrial competitiveness and exports lies in placingproducers in the most advantageous competitive positions through efficient services and infrastructure.

4.2 Role of the Development Ministry

44. The Development Ministry has been restructured to adopt a role compatible with an outward-oriented economy. The Ministry has four institutional objectives: (a) Increased productivity, productquality, and service; (b) Increased foreign investment and access to technology; (c) Increased capacity

- xiv -

to monitor industrial performance; and (d) Stronger analytical bases to formulate policy and to identifypublic sector obstacles to competitiveness. The responsibilities the Ministry must undertake can begrouped into three categories: those which make the country internationally competitive and maintaina favorable investment climate; those which maintain and promote competition within the domesticmarket; and those which collect, analyze, and disseminate information in support of the other two.

45. 4.2.1 Investnent Climate. The general economic health and political stability in a country,along with resources and markets, are the primary determinants of industrial investment. In this regard,the Government's reform program has eliminated many of the impediments to industrial investment, bothdomestic and foreign. There are areas where further policy changes would enhance Venezuela'sinternational competitiveness:

* Tax Reform. Tax rates on corporate profits are higher in Venezuela (50 percent) than they are in othercountries which compete for investment. Legislation to reform the entire tax system is pending but,until it is passed, investors will defer decisions in cases where this would make a difference.

* Labor Legislation. Labor laws intrude heavily into employee and managerial freedom to negotiateterms and conditions of employment. They impose requirements which make Venezuelan labor lesscompetitive with other nations.

* Training and Education. The quality of the labor force is as important to investors as the price. TheNational Training Institute (INCE) and the public education system need to implement programs whichwill more efficiently prepare Venezuelan labor for employment in modern industrial occupations.

* Technology. Technology transfers have been inhibited by policies which discouraged foreigninvestment and by import restrictions on capital goods. These policies have been reformed, and theDevelopment Ministry should ensure that no other government policies--such as outdated patent laws-will inhibit introduction of state-of-the-art technology in Venezuela.

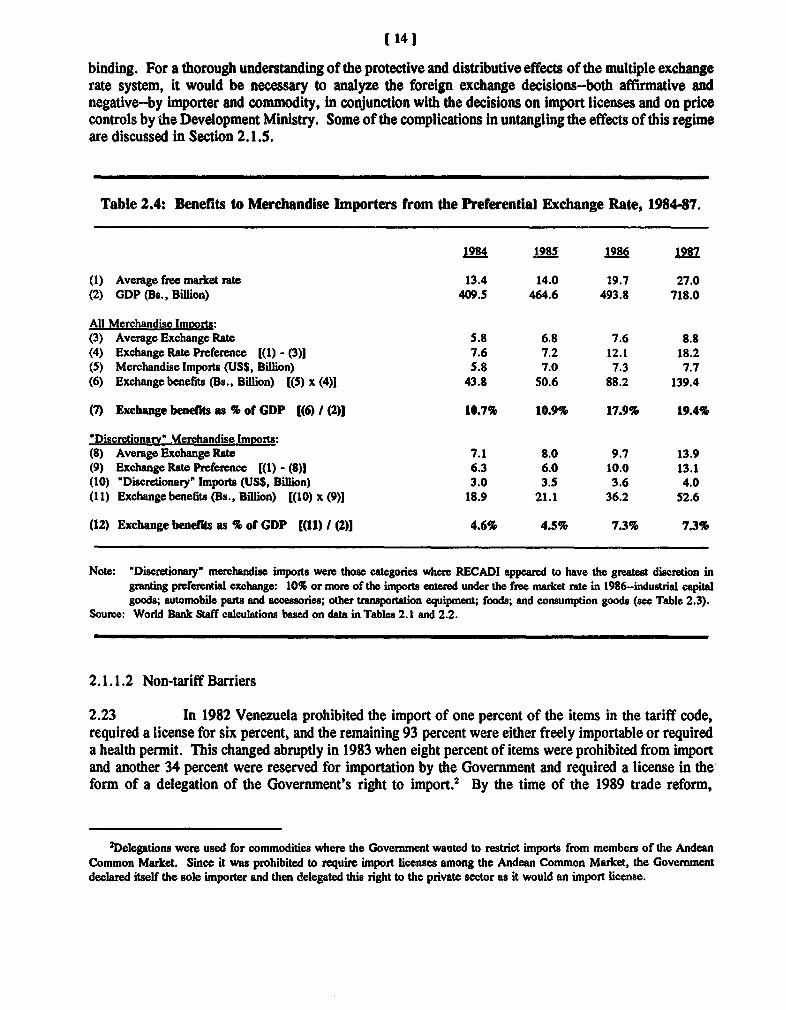

* Investment Promotion. Venezuela has much to offer, and this is becoming more widely recognizedinternationally. Effective investment promotion, in conjunction with the private sector, may acceleratesome decisions.

46. 4.2.2 Promotion of Competition. In a small economy like Venezuela's, the principal sourceof competition is the world market, and the Development Ministry is responsible for continuing the tariffreform. It is also important to maintain a competitive environment in nontraded goods. Reforms of somelaws and regulations can contribute to a more competitive economy:

* Patents and Copyrights. Venezuela's laws of intellectual property rights have been criticized fordiscouraging research and innovation and deterring foreign investors from introducing advancedtechnology. Legislation has been drafted to increase protection of intellectual property rights inVenezuela, and the Development Ministry should take an active role in advocating appropriate changes;

* Product Standards. Weights and Measures. The Development Ministry, in setting standards, shouldlook abroad toward international norms which would maximize domestic competition. This would beof the greatest benefit to consumers, who would have wider selection, and to domestic producers who,by adapting to international norms, would be able to compete in larger markets.

- xv -

* Maximum Retail Price. The consumer protection law requires-among other things--that manufacturersset a maximum retail price (precio de venta al pablico, PVP). It is not clear under what conditionsthe PVP protects consumers, and the requirement should be replaced with a provision which makesthe PVP optional.

* Financial Sector Reform. An efficient financial sector facilitates resource mobilization and allocation.The financial sector reform should encourage internal competition, however, the Development Ministryshould study with other affected Ministries the feasibility of greater foreign ownership of commercialbanks.

* Bankruptcy. An important element of vigorous competition is exit by firms which are unable tocompete. This frees resources to move to more dynamic, expanding activities and leads to a stronger,more competitive economy. The Development Ministry should ensure that bankruptcy regulations andprocedures are consistent with best international practice.

* Antitrust Legislation. The strongest form of consumer protection would come from vigorous,competitive markets. As tariffs are reduced, international competition will reduce the prices of tradedgoods and drive producers' prices toward international levels. For domestic distribution and for othernontraded goods, it may be desirable to rely on antitrust legislation to enforce competitive norms andbehavior.

47. 4.2.3 Information and Research. The Development Ministry should undertake a systematicinventory of the economic information and systems available in Venezuela and in other countries andshould develop recommendations to improve the quality and availability of reliable data, and ensure thatthey are gathered and disseminated in a cost-effective fashion. Without such data it is impossible tomeasure the effects of any policy, much less to approximate the effects of alternative policies. In thisregard, the Development Ministry should continue to give priority to computerizing its own records andmaking these available to researchers who would be interested in measuring the effects of the policies andeconomic decisions made during the 1980s. The Ministry itself does not have sufficient resources toanalyze these data, but they would be of interest to an international body of scholars seeking tounderstand and measure the effects of Venezuelan industrial policy during the 1980s.

March 13. 19919:11 am

1. INTRODUCIION

1.1 Between 1958 and 1972 Venezuela's non-oil GDP grew an average of 6.8 percent per year.Manufacturing (excluding oil refining) was the fastest growing sector, at a rate of 7.8 percent. Thisresulted from foreign investment and import substitution which reduced the share of imports in privateconsumption from 30 percent at the end of the 1950s to three percent in 1970. In the 1970s and early1980s, the Government was awash in oil revenues. Bourginon (1989) estimates the windfall during 1974-78 averaged a 20 percent increase annually above what GDP would have been without the boom, and,during 1979-82, 27 percent of GDP. Over the nine years, the windfall totalled approximately two years'GDP. These resources were supplemented by foreign borrowing, and Venezuela's external debt wentfrom $1.5 billion in 1975 to $38.2 billion in 1983. The $36.7 billion increase in debt is equal to aboutone-half of the 1988 GDP.

1.2 The Government sought to diversify the industrial base, reserving for itself investment in "strategicsectors" or "basic industries"-principally aluminum, steel, and energy. Large public investments weremade through the Venezuelan Investment Fund (Fondo de Inversiones de Venezuela, FIV) and theVenezuelan Corporation of Guayana (Corporacion Venezolana de Guayana, CVG). Direct foreigninvestment was discouraged or prohibited, and private investors were encouraged to invest--generally--indomestic activities which would substitute for imports and-specifically-in activities downstream fromthe basic industries. This import substitution was encouraged by protection through tariffs and licenses,by directed credit at below-market rates, and by controls on investments.

1.3 When oil prices dropped in the 1980s, the bolfvar became overvalued, but it could not bemaintained. In 1983, following a series of currency crises and losses of foreign exchange reserves, thebolfvar was devalued and a multiple exchange rate system was introduced. Exchange controls, whichwere changed frequently, introduced a new layer o. discretionary incentives. Price guidelines andcontrols were applied throughout the economy. Some exports were prohibited, and the industrialincentives discouraged most others. It was widely felt that the role of industry was to satisfy the localmarket and that only if there was a "surplus," could it be exported.

1.4 The layers upon layers of intervention produced an uncoordinated, inefficient system characterizedby contradiction, redundancy, and discretion. Through most of the 1980s, the industrial sector operatedin an environment in which government controlled every aspect of a firm's decisions: input prices andquantities, output prices, investments, and market access. Bourginon (1989, p. 322) has characterizedthis period as "... a dramatic failure of economic policy under complex yet seemingly exceptionallyfavorable conditions. Nothing appears to have been gained from the windfalls in terms of non-oil GDP*during 1973-82. Consumption has been the only winner."

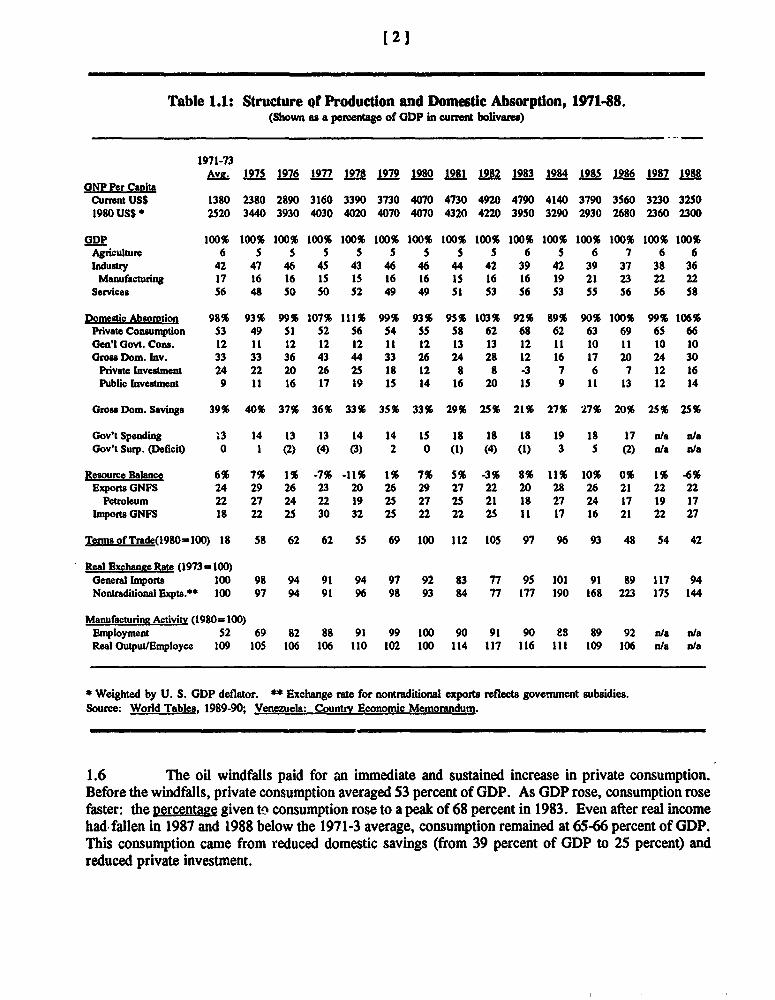

1.5 Table 1. 1 shows the structure of production and domestic absorption during this period. RealGNP per capita (exDressed in 1980 US$), which was relatively stable during 1976-83, rose and fell withthe terms of trade. In 1988 it was only 53 percent of its 1981 peak, and about 10 percent below the1971-73 average. Expressed in constant US$, all sectors declined, but measured in 1980 bolivares, onlythe non-manufacturing industrial sector declined: agriculture grew at an annual rate of 4.3 percent,manufacturing at 3.8 percent, and services at 1.8 percent between 1981 and 1988 (cf. World Tables.1989-90).

[2)

Table 1.1: Structure Qf Production and Domestic Absorption, 1971488.(Shown as a percertage of GDP in curnt bolivares)

1971-73Ave. 1975 1976 1977 1978 1979 1980 1981 1 1983 1984 1985 1986 1987 198R

ONP Per CapitaCumnt USS 1380 2380 2890 3160 3390 3730 4070 4730 4920 4790 4140 3790 3560 3230 32S01980 USS * 2520 3440 3930 4030 4020 4070 4070 4320 4220 3950 3290 2930 2680 2360 2300

GDP 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%Agrculture 6 5 S 5 5 5 5 5 S 6 5 6 7 6 6Indusry 42 47 46 45 43 46 46 44 42 39 42 39 37 38 36

Manufacturing 17 16 16 IS IS 16 16 15 16 16 19 21 23 22 22Services 56 48 50 50 52 49 49 51 53 56 53 55 56 56 58

Domesic Absorption 98% 93% 99% 107% 111% 99% 93% 9S% 103% 92% 89% 90% 100% 99% 106%Private Consumption 53 49 S1 52 S6 S4 SS 58 62 68 62 63 69 6S 66Gen'lGovt.Cons. 12 11 12 12 12 11 12 13 13 12 11 10 11 10 10Gross Dom. Inv. 33 33 36 43 44 33 26 24 28 12 16 17 20 24 30

Private Investment 24 22 20 26 25 18 12 8 8 -3 7 6 7 12 16Public Investment 9 11 16 17 19 IS 14 16 20 15 9 11 13 12 14

Gross Dom. Savings 39% 40% 37% 36% 33% 3S% 33% 29% 25% 21% 27% 27% 20% 2S% 25%

Gov't Spending .3 14 13 13 14 14 IS 18 18 18 19 18 17 n/a rJaGov't Surp. (Deficit) 0 1 (2) (4) (3) 2 0 (1) (4) (1) 3 5 (2) n/a n/a

Resource Balance 6% 7% 1% -7% -11% 1% 7% 5% -3% 8% 11% 10% 0% 1% -6%Exports GNFS 24 29 26 23 20 26 29 27 22 20 28 26 21 22 22

Petroleum 22 27 24 22 19 25 27 25 21 18 27 24 17 19 17ImportsGNFS 18 22 25 30 32 25 22 22 25 11 17 16 21 22 27

TermsofTrade(1980=100) 18 58 62 62 S5 69 100 112 105 97 96 93 48 54 42

Real Exchanee Rate (1973 = 100)General lmpotts 100 98 94 91 94 97 92 83 77 95 101 91 89 117 94Nontraditional Expts.** 100 97 94 91 96 98 93 84 77 177 190 168 223 17S 144

Manufacturing Activity (1980= 100)Employment 52 69 82 88 91 99 100 90 91 90 88 89 92 n/a n/aReal Output/Employee 109 10S 106 106 110 102 100 114 117 116 111 109 106 n/a n/a

* Weighted by U. S. GDP deflator. *# Exchange rate for nontraditional exports reflects government subsidies.Source: World Tables, 1989-90; Venezuela: Country Economic Memorandum.

1.6 The oil windfalls paid for an immediate and sustained increase in private consumption.Before the windfalls, private consumption averaged 53 percent of GDP. As GDP rose, consumption rosefaster: the percentage given to consumption rose to a peak of 68 percent in 1983. Even after real incomehad fallen in 1987 and 1988 below the 1971-3 average, consumption remained at 65-66 percent of GDP.This consumption came from reduced domestic savings (from 39 percent of GDP to 25 percent) andreduced private investment.

(3J

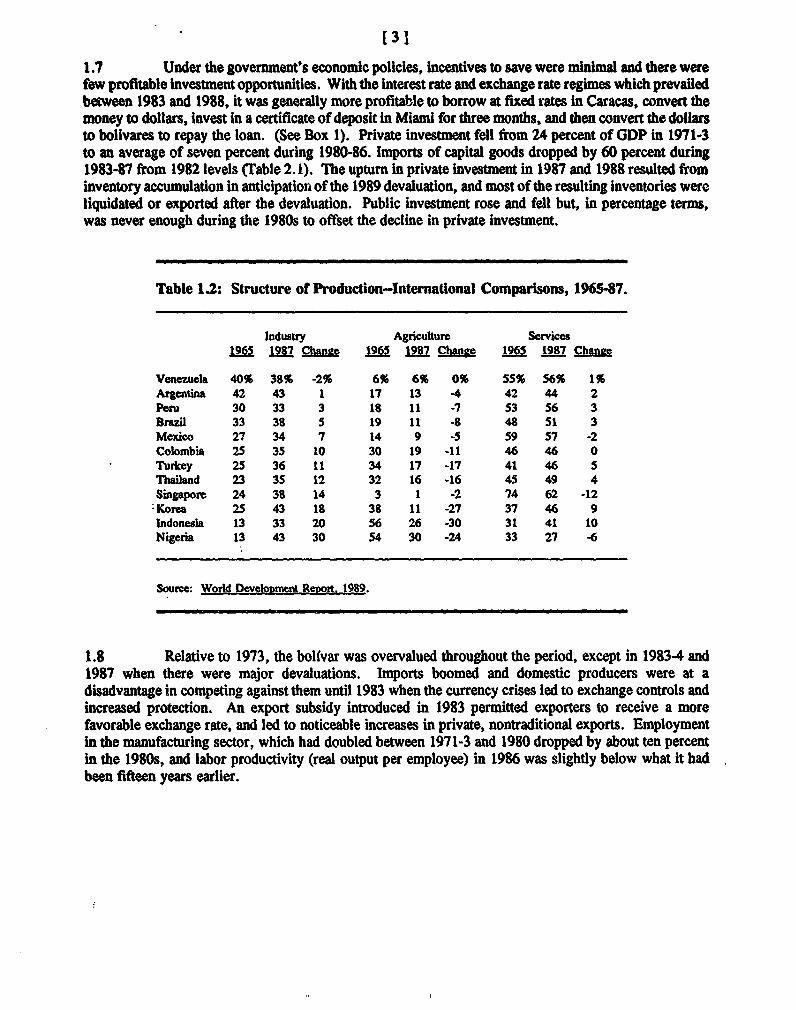

1.7 Under the government's economic policies, incentives to save were minimal and there werefew profitable investment opportunities. With the interest rate and exchange rate regimes which prevailedbetween 1983 and 1988, it was generally more profitable to borrow at fixed rates in Caracas, convert themoney to dollars, invest in a certificate of deposit in Miami for three months, and then convert the dollarsto bolivares to repay the loan. (See Box 1). Private investment fell from 24 percent of GDP in 1971-3to an average of seven percent during 1980-86. Imports of capital goods dropped by 60 percent during1983-87 from 1982 levels (Table 2.1). The upturn in private investment in 1987 and 1988 resulted frominventory accumulation in anticipation of the 1989 devaluation, and most of the resulting inventories wereliquidated or exported after the devaluation. Public investment rose and fell but, in percentage terms,was never enough during the 1980s to offset the decline in private investment.

Table 1.2: Structure of Production-International Compasons, 1965-87.

Industry Agriculture Services1965 1987 Chanc 1965 1987 Changee 1 1987 Chanc

Venezuela 40% 38% -2% 6% 6% 0% 55% 56% 1%Argentina 42 43 1 17 13 -4 42 44 2Peru 30 33 3 18 11 -7 53 56 3Brazil 33 38 5 19 11 -8 48 51 3Mexico 27 34 7 14 9 -5 59 57 -2Colombia 25 35 10 30 19 -11 46 46 0Turkey 25 36 11 34 17 -17 41 46 5Thailand 23 35 12 32 16 -16 45 49 4Singapore 24 38 14 3 1 -2 74 62 -12Korea 25 43 18 38 11 -27 37 46 9Indonesia 13 33 20 56 26 -30 31 41 10Nigeria 13 43 30 54 30 -24 33 27 -6

Soure: World Development Reron. 1989.

1.8 Relative to 1973, the bolfvar was overvalued throughout the period, except in 19834 and1987 when there were major devaluations. Imports boomed and domestic producers were at adisadvantage in competing against them until 1983 when the currency crises led to exchange controls andincreased protection. An export subsidy introduced in 1983 permitted exporters to receive a morefavorable exchange rate, and led to noticeable increases in private, nontraditional exports. Employmentin the manufacturing sector, which had doubled between 1971-3 and 1980 dropped by about ten percentin the 1980s, and labor productivity (real output per employee) in 1986 was slightly below what it hadbeen fifteen years earlier.

[31

1.7 Under the government's economic policies, incentives to save were minimal and there werefew profitable investment opportunities. With the interest rate and exchange rate regimes which prevailedbetween 1983 and 1988, it was generally more profitable to borrow at fixed rates in Caracas, convert themoney to dollars, invest in a certificate of deposit in Miami for three months, and then convert the dollarsto bolivares to repay the loan. (See Box 1). Private investment fell from 24 percent of GDP in 1971-3to an average of seven percent during 1980-86. Imports of capital goods dropped by 60 percent dur.ng1983-87 from 1982 levels (Table 2.1). The upturn in private investment in 1987 and 1988 resulted frominventory accumulation in anticipation of the 1989 devaluation, and most of the resulting inventories wereliquidated or exported after the devaluation. Public investment rose and fell but, in percentage terms,was never enough during the 1980s to offset the decline in private investment.

Table 12: Structure of Production-International Comparisons, 1965487.

Industry Agriculturm Services196S 1987 Chanze 1965 1987 Chane 1965 1987 Change

Venezuela 40% 38% -2% 6% 6% 0% 55% 56% 1%Argentina 42 43 1 17 13 -4 42 44 2Peru 30 33 3 18 11 -7 53 56 3Brazil 33 38 5 19 11 -8 48 51 3Mexico 27 34 7 14 9 -5 59 57 -2Colombia 25 35 10 30 19 -11 46 46 0Turkey 25 36 11 34 17 -17 41 46 5Thailand 23 35 12 32 16 -16 45 49 4Singapore 24 38 14 3 1 -2 74 62 -12

'Korea 25 43 18 38 11 -27 37 46 9Indonesia 13 33 20 56 26 -30 31 41 10Nigeria 13 43 30 54 30 -24 33 27 -6

Souce: World Development Report. 1989.

1.8 Relative to 1973, the bolfvar was overvalued throughout the period, except in 19834 and1987 when there were major devaluations. Imports boomed and domestic producers were at adisadvantage in competing against them until 1983 when the currency crises led to exchange controls andincreased protection. An export subsidy introduced in 1983 permitted exporters to receive a morefavorable exchange rate, and led to noticeable increases in private, nontraditional exports. Employmentin the manufacturing sector, which had doubled between 1971-3 and 1980 dropped by about ten percentin the 1980s, and labor productivity (real output per employee) in 1986 was slightly below what it hadbeen fifteen years earlier.

l 5 ]

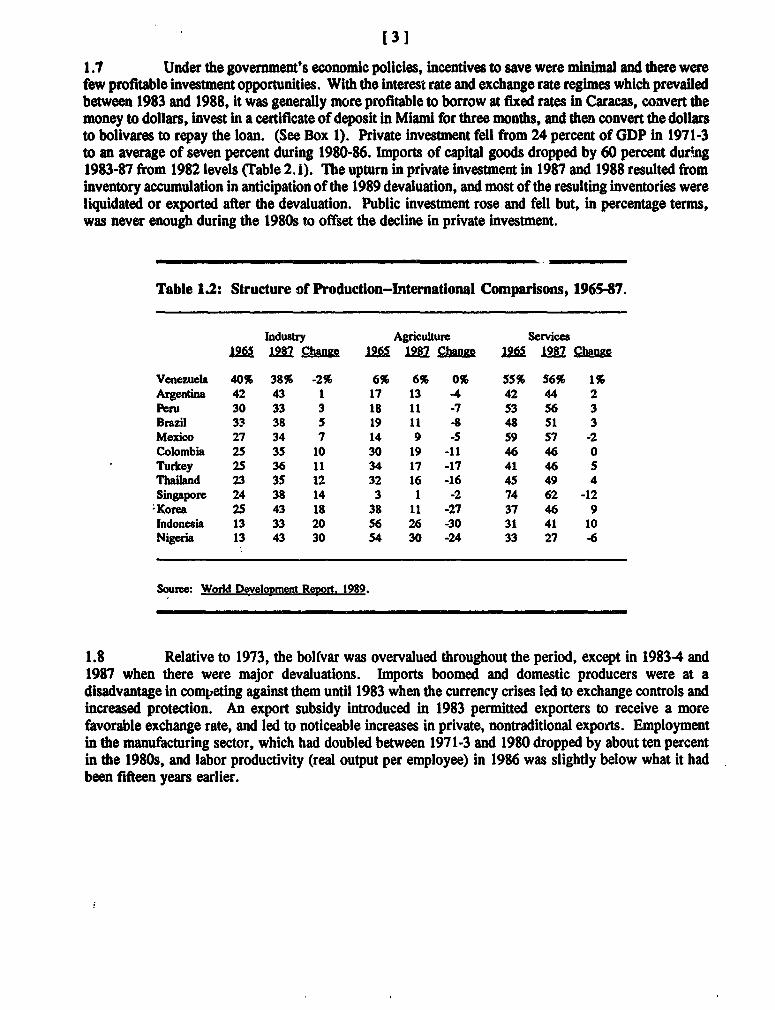

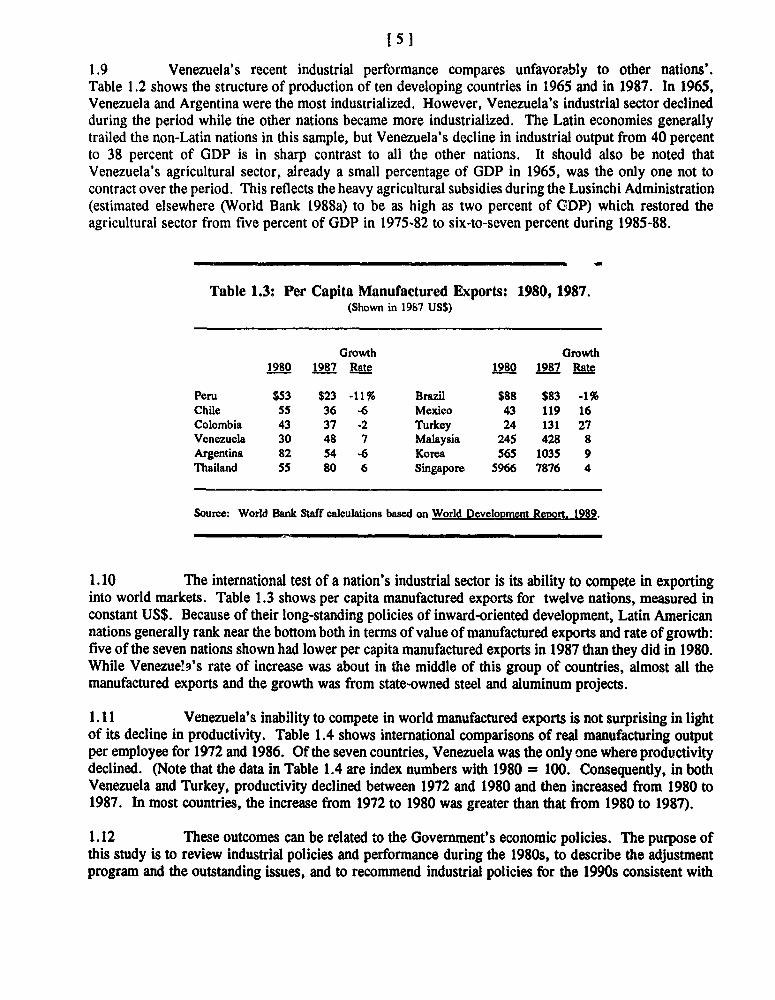

1.9 Venezuela's recent industrial performance compares unfavorably to other nations'.Table 1.2 shows the structure of production of ten developing countries in 1965 and in 1987. In 1965,Venezuela and Argentina were the most industrialized. However, Venezuela's industrial sector declinedduring the period while tne other nations became more industrialized. The Latin economies generallytrailed the non-Latin nations in this sample, but Venezuela's decline in industrial output from 40 percentto 38 percent of GDP is in sharp contrast to all the other nations. It should also be noted thatVenezuela's agricultural sector, already a small percentage of GDP in 1965, was the only one not tocontract over the period. This reflects the heavy agricultural subsidies during the Lusinchi Administration(estimated elsewhere (World Bank 1988a) to be as high as two percent of CDP) which restored theagricultural sector from five percent of GDP in 1975-82 to six-to-seven percent during 1985-88.

Table 1.3: Per Capita Manufactured Exports: 1980, 1987.(Shown in 1987 USS)

Growth Growth1980 1987 Rate 1980 1987 Rate

Peru $53 $23 -11% Brazil $88 $83 -1%Chile 55 36 -6 Mexico 43 119 16Colombia 43 37 -2 Turkey 24 131 27Venezuela 30 48 7 Malaysia 245 428 8Argentina 82 54 -6 Korea 565 1035 9Thailand 55 80 6 Singapore 5966 7876 4

Source: World Bank Staff calculations based on World Develooment ReMort. 1989.

1.10 The international test of a nation's industrial sector is its ability to compete in exportinginto world markets. Table 1.3 shows per capita manufactured exports for twelve nations, measured inconstant US$. Because of their long-standing policies of inward-oriented development, Latin Americannations generally rank near the bottom both in terms of value of manufactured exports and rate of growth:five of the seven nations shown had lower per capita manufactured exports in 1987 than they did in 1980.While Venezue!a.'s rate of increase was about in the middle of this group of countries, almost all themanufactured exports and the growth was from state-owned steel and aluminum projects.

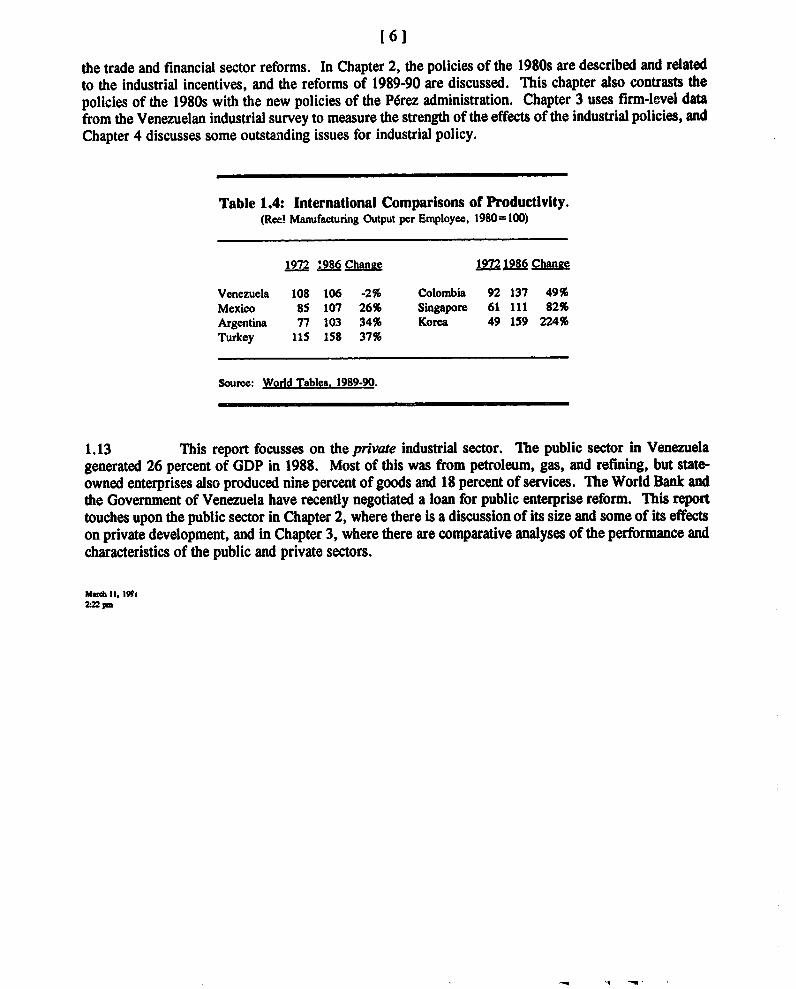

1.11 Venezuela's inability to compete in world manufactured exports is not surprising in lightof its decline in productivity. Table 1.4 shows international comparisons of real manufacturing outputper employee for 1972 and 1986. Of the seven countries, Venezuela was the only one where productivitydeclined. (Note that the data in Table 1.4 are index numbers with 1980 = 100. Consequently, in bothVenezuela and Turkey, productivity declined between 1972 and 1980 and then increased from 1980 to1987. In most countries, the increase from 1972 to 1980 was greater than that from 1980 to 1987).

1.12 These outcomes can be related to the Government's economic policies. The purpose ofthis study is to review industrial policies and performance during the 1980s, to describe the adjustmentprogram and the outstanding issues, and to recommend industrial policies for the 1990s consistent with

[61

the trade and financial sector reforms. In Chapter 2, the policies of the 1980s are described and relatedto the industrial incentives, and the reforms of 1989-90 are discussed. This chapter also contrasts thepolicies of the 1980s with the new policies of the PNrez administration. Chapter 3 uses firm-level datafrom the Venezuelan industrial survey to measure the strength of the effects of the industrial policies, andChapter 4 discusses some outstanlding issues for industrial policy.

Table 1.4: International Comparisons of Productivity.(Rcea! Manufacturing Output per Employee, 1980= 100)

1972 :986 Chanec 1972 1986 Chance

Venezuela 108 106 -2% Colombia 92 137 49%Mexico 85 107 26% Singapore 61 111 82%Argentina 77 103 34% Korea 49 159 224%Turkey 115 158 37%

Source: World Tables. 1989-90.

1.13 This report focusses on the private industrial sector. T'he public sector in Venezuelagenerated 26 percent of GDP in 1988. Most of this was from petroleum, gas, and refining, but state-owned enterprises also produced nine percent of goods and 18 percent of services. The World Bank andthe Govermment of Venezuela have recently negotiated a loan for public enterprise reform. This reporttouches upon the public sector in Chapter 2, where there is a discussion of its size and some of its effectson private development, and in Chapter 3, where there are comparative analyses of the performance andcharacteristics of the public and private sectors.

Matc 11. 199&PMl

2. INDUSTRIAL POLICY: THE 1980S AND THE REFORm

2.1 During the 1980s-particularly after the introduction of the multiple exchange rate systemin February 1983--the Venezuelan Government managed industrial policy through a comprehensive,uncoordinated series of ad hoc instruments which were orimarily intended to achieve objectives other thanefficient industrial development. Entrepreneurial discretion was sharply restricted and firms' successdepended more on bureaucratic whim than on a market test of efficiency of production or distribution.Government limited managerial prerogatives in significant ways:

* The prices and quantities of imported inputs were contz^?'ed by licenses, tariffs (which could bereduced upon application), government import monopolies, and foreign exchange allocations.Government allowed domestic producers to prevent importation of competing merchandise.Domestically produced inputs were subject to price controls. Labor costs and terms of employmentwere controlled by distorting labor laws.

* Output prices were regulated and foreign competition was restrained bv import prohibitions, licenses,and foreign exchange allocations.

* Investments to expand production or to enter new markets were regulated. Government permits gaveinvestors concessional credit, imported inputs, and preferential foreign exchange. Investments incertain geographic regions were discouraged.

e Exports were discouraged and permits were necessary. Exporters received the official--rather thanthe free market-exchange rate, but were eligible for an offsetting subsidy plus preferential credit.The incentive regime and rates were frequently changed and exporters were unable to predictaccurately their export receipts more than a few weeks in advance.

2.2 There was a benevolent intention and an internal logic-albeit, misguided-to the policies.The multiple exchange rate system was meant to protect consumers, permitting preferential rates for"essential" items such as food, clothing, medicines, or inputs into their production. The import controlsand tariff exonerations were meant to protect employment and production, ensuring that there weresufficient imported inputs and an absence of foreign competition to keep industry employed. With noforeign competition, price controls were intended to protect consumers against monopolistic pricing.Further, the price controls were thought to be necessary to ensure that the benefits of the preferentialforeign exchange would be passed on to consumers. However, where items were being subsidized, itwas necessary to prohibit their exportation so that only Venezuelan residents would benefit. Finally, withinvestors entitled to concessional credit and other subsidies to capital, investment controls would ensurethat there would not be too much investment.

2.3 These policies, though well-intended, built distortions upon distortions and increasinglysubstituted governmental discretion and judgement for market-based transactions. For the policies to havebeen efficiently administered, they would have demanded information and analytical resources which arebeyond the reach of any government. There is no example of a government which has efficientlyadministered such policies, and many examples of governments which have failed.

2.4 The concentration of power in governmental ministries left wide discretion and in some casesfostered corruption. Businessmen found the most profitable use of their time to be seeking privileges (or

[ 8 ]

preventing their competitors from receiving concessions), and visitors to economic ministries commonlyfound queues of well-dressed executives waiting outside offices for hearings on applications for someprivilege which officials were empowered to grant. While these policies were meant to serve theVenezuelan consumer, they imposed additional business costs on the industrial sector which were passedon to labor, in the form of unemployment, and to consumers in higher prices, lower product quality,poorer service, and a reduced range of goods and services.

2.1 Trgde Policy

2.5 The principal and most pot-nt instruments of industrial policy during the 1980s wereadministered through international trade policy--exchange allocations, import licenses and delegations,tariff exonerations, and export incentives. Despite large export subsidies, the import controls created ananti-export bias and the industrial sector had little incentive to compete in international markets.

2.1.1 Import Restrictions

2.6 For someone to import most items into Venezuela, he had first to obtain an import permit(a license or a delegation) from the Development or the Agricultural Ministry. This would be grantedonly if domestic producers did not object. Since tariffs were prohibitive, he had to apply for anexoneration which would reduce the tariff to a reasonable level. Then, he had to apply to an agency ofthe Finance Miristry for foreign exchange at one of the preferential rates.

2.1.1.1 Foreign Exchange Controls

2.7 From 1973 to February 1983, Venezuela maintained a fixed exchange rate of 4.3 bolivaresto the US$. The bolfvar became incroasingly overvalued (see the real exchange rate indices inTable 1.1), and in early 1983 there were a series of currency crises which were resolved by introducingthe multiple exchange rate system which was maintained through early 1989. Initially, the rate of 4.3Bs./US$ was retained for the petroleum sector, "essential" imports, Pid foreign debt service. An"official" rate of 6.0 applied to most commercial transactions, and a free market rate (which variedbetween 7.5 and 17.0 during the first year) applied to nontraditional exports, tourism, and capital. Theofficial rate was raised to 7.5 in March, 1984, and subsequently to 14.5 in December, 1986, and therewere numerous movements of items among categories. At one point, there was the 4.3 rate for foreigndebt, a 6.0 preferential rate, the 7.5 official rate, and the free market rate. Over 1984-88 the free rateranged from 60 percent to 200 percent above the official rate, averaging 110 percent (see Box 1). InFebruary, 1989, the multiple exchange rates were unified and the exchange rate was floated.

2.8 Table 2.1 shows the foreign exchange sales by the Central Bank at the various rates during1984-87. It also shows the average exchange rates for sales and for purchases. Collins (1988) pointsout that the multiple exchange rate system altered relative prices, effectively taxing some transactions andsubsidizing others. In 1986, for example, the average purchase rate was 8.5 and the average sales ratewas. 8.7 so that sales of dollars were subsidized by purchases (predominately petroleum exports).However, not all sales were subsidized. The 7 percent of sales which received the preferential rate of4.3 (debt repayment) were subsidized by about 50 percent, those sales at the official rate of 7.5 weresubsidized by 12 percent, and sales at the free rate (averaging 19.7) were taxed at 130 percent. Over thefour years, the Central Bank's sales of foreign exchange exceeded purchases and there was a net reductionof $2.1 billion of international reserves.

191

Table 2.1: Foreign Exchange Sales and Exchange Rates, 1984-87.(Billions of USS)

Rate(Bs./US$) 1984 1985 1986 1987

4.3 $5.0 (31%) $1.6 (11%) $1.0 ( 7%) $ .8 ( 5%)6.0 2.4 (15%) 1.4 ( 9%)7.5 7.1 (45%) 10.0 (70%) 11.7 (81%) 6.8 (41%)8.7 1.0 ( 6%)

14.5 7.1 (43%)Free Mkt 1.5 ( 9%) 1. (10%) 1.7 (12%) .7 (4%)TOTAL $16.0 $14.3 $14.4 $16.3

Averaze RatesFree Market Sales 13.4 14.0 19.7 27.0All Sales 6.8 7.7 8.7 11.2All Purchases 6.1 6.5 8.5 11.9

Source: BCV.

2.9 Merchandise imports accounted for about half of the C>ntral Bank's foreign exchange salesbetween 1984 and 1987. Table 2.2 shows the average exchange rate which applied to each category ofmerchandise imports each year during 1983-88, together with imports in US$. For each category, anexchange rate index was calculated by dividing its average exchange rate by the average for all importsin the year. An index above 100 indicates that the average exchange rate effectively taxed importers ofthat class of goods in order to subsidize importers of goods with indices below 100. This tax/subsidyis in addition to any subsidy provided generally for sales of dollars by taxing the purchase of dollars.The last three columns show for 1983-88: average import levels; average import levels as a percentageof 1981-82 imports; and the (unweighted) average of the six ai'nual exchange indices. Table 2.2 revealsmuch about the distortions which the exchange regime imposed on the industrial sector during the 1980s.

2.10 Merchandise imports peaked in 1981-82. Imports declined by 50 percent in 1983, thenincreased gradually through 1987. There was a relatively large increase in 1988, made up mostly of rawmaterials (up 40 percent), capital goods (up 24 percent), transportation equipment (up 41 percent), andconsumer durables (up 100 percent) in anticipation of the devaluation of 1989. Over 1983-88, importsaveraged 68 percent of the 1981-82 level.

2.11 The structure of imports in Table 2.2 reflects the intensification of the import substitutionunder the industrial policies of the 1980s. While imports during 1983-88 were only 68 percent of 191-82 levels, raw materials actually increased (103 percent), capital goods were relativelyunaffected(68 percent) while final goods were below 68 percent: food (38 percent), alcoholic beverages(53 percent), and consumption goods (55 percent). The category of transportation equipment illustratesmost clearly the import substitution bias, with assembled units cut sharply while materials for the

I to I

Tuble 2.2: Imports by Type and Exchange Rates, 1981-88.(Imports in Billions of USS)

1981-2 1983 1984 1985 1986 1987 1988 1983-88:A.&. kw,rt. A.g.

AVg F.Adwng Fxdw.p: Etxedbu: Exduo: Exdu: USS S of F.ci.In48 bnpu Rateh c Indhiex hm- Rate h Ridncx Ima FtR e Index blots Rat 1ex IIYCXI Rawc tndcx 1 142 W¢dx

ilOTrAl. $11.7 $5.8 5.8 100 S7.0 6.8 100 57.3 7.6 100 57.7 - 100 $8.7 13.2 100 $11.5 18.6 100 $8.0 680k 100

Ran MhideriaIs $3.0 $2.1 5.1 87 S3.0 6.1 90 $2.7 7.0 92 $2.6 7.9 90 53.4 12.1 91 $4.8 15.8 85 53.1 103% 89inidtilir 2.7 1.8 4.9 85 2.5 6.1 90 2.3 7.1 94 2.1 8.0 91 2.9 12.4 94 4.3 16.0 86 2.7 99% 90Agriculturc .2 .2 4.3 74 .2 5.0 74 .2 6.2 82 .3 7.5 85 .4 9.4 71 .3 12.4 67 .3 118% 76EK.tri,it) Nianing .1 .2 7.5 129 .2 7.4 109 2 6.5 86 .2 7.4 84 .2 12.9 98 .2 15.3 82 .2 2124 98

C:naital (oods $3.1 $1.3 6.6 113 $1.5 7.3 108 $3.9 8.0 lOS $2.3 9.1 104 $2.5 14.1 107 $3.1 20.2 109 52.1 68% 108Induibtry 2.5 1.1 6.6 113 1.3 7.3 108 1.7 8.0 106 2.0 9.3 105 2.2 14.1 107 2.6 20.5 110 1.8 72% 108Agriculture .2 .0 5.0 86 .0 7.0 103 101 .1 7.8 s 105 .1 20.0 108 .1 40%ElcctriJiq/Mining .3 .1 7.0 119 .1 7.4 109 . i.Y/ 104 .2 8.5 9# .L 14.3 108 .3 17.8 96 .2 59% 106

Tr.msnwort IlnDt. $1.9 S.9 7.1 122 5.9 7.3 108 $1.0 7.6 99 $1.4 8.1 91 $1.2 14.4 109 $1.7 20.9 113 53.2 63% 107Automilotive 3.5 .7 7.1 122 .8 7.3 108 .8 7.6 99 1.1 7.9 90 1.0 14.4 109 1.2 20.7 III .9 64% 107

Assnb1ed Autos I .0 5.5 94 .0 7.0 103 .0 7.7 101 .0 7.9 *30 .0 13.7 104 .0 20.5 110 .0 19% 100Asscmb1cd Cargo4 .1 6.2 107 .0 6.8 100 .1 7.5 99 .2 7.6 86 .1 1.'.4 102 .2 19.2 103 .1 27% 99CKD's--Autos .6 .4 7.4 127 .5 7.4 108 .4 7.5 99 .6 7.6 86 .5 14.2 108 .5 20.4 110 .5 75% 106CKD's--Cargo .0 .1 7.6 129 .1 7.4 108 .1 7.5 98 .1 7.6 86 .1 14.5 109 .1 20.5 110 .1 213% 107Parts/Access. .3 .1 7.1 123 .2 7.4 109 .2 7.8 102 .2 9.1 103 .3 15.1 114 .4 21.5 116 .2 89% III

Other 4 .2 7.0 119 .2 7.3 108 .2 7.5 99 .2 8.8 99 .2 14.6 III .5 2!.5 116 .2 60% 109

Cowstruction.Mi 5.2 6.1 10S 5.2 7.3 108 5.2 7.5 99 5.2 8.2 93 5.3 13.7 103 S.3 19.4 104 5.2 24% 102

Food Prod':cts 5.5 4.7 80 5.6 S.0 73 S.5 5.7 74 5.2 9.0 102 5.3 9.9 75 5.1 18.7 101 5.4 38% 84Basic .4 4.5 78 .4 4.6 68 .3 5.2 68 .1 8.8 100 .2 9.3 71 .1 17.6 95 .2 39% 80Non-basic .3 .1 5.2 89 .1 6.0 89 .2 6.4 83 .1 9.1 103 .1 10.6 81 .0 21.8 117 .1 38% 94

Alcohol/Bvgc. 5.1 5.1 8.3 142 5.1 12.4 183 5.1 13.2 174 5.1 19.9 225 $.1 17.1 129 5.1 21.9 138 5.1 53% 162

Comistalilotioal $3.8 5.7 5.8 99 5.8 8.2 120 $1.0 9.2 121 51.0 10.9 124 53.0 13.9 105 $1.4 21.4 115 $3.0 55% 114Luxury .7 .2 6.1 104 .2 9.3 137 .3 9.7 128 .3 12.1 137 .3 14.2 107 .3 20.7 112 .3 37% 121

Durable .3 .1 5.6 95 .1 8.1 119 .2 8.9 117 .1 9.9 113 .2 13.0 99 .2 19.7 106 .1 45% 108Non-Durable .4 .1 6.6 113 .1 10.4 153 .1 11.0 144 .1 15.0 170 .1 135.8 119 .1 22.3 120 .1 30% 137

Non-Luxury 1.1 .S 5.7 97 .6 7.8 114 .7 9.0 119 .7 10.6 120 .7 13.8 104 1.0 21.6 116 .7 67% 312Durable .5 .2 5.6 96 .2 7.4 109 .3 8.2 108 .3 9.5 107 .3 14.5 110 .7 21.9 118 .3 65% 108Non-Durable .6 .3 5.7 98 .4 7.9 117 .5 9.5 123 .4 11.4 129 .4 13.3 100 .4 20.9 113 .4 68% 114

Note: Exchange indices were calculated by dividing each category's average exchange rate by the average rate for all transactions in the year. An indcxgreater than 100 indicates that importers of that item imponted relatively more at the free market rate and an index lcss than 100 indicates thatrelatively more imports were at the official rate.

Source: OCEI, Anuario del Comercio Exterior de Venezuela, various years.

[11l

assembly industry rose absolutely or, at least, relative to the decline in imports: assembled autos were19 percent of 1981-82 levels and assembled cargo vehicles were 27 percent, while automobile CKD kitswere 75 percent and cargo vehicle CKD's were 213 percent. Motor vehicle sales were 163,000 units in1982, and fell 25 percent to an average of 122,000 units over 1983-88.'

2.12 Over 1983-88, the relatively most heavily subsidized commodities through the exchange ratewere foods and raw materials. By contrast, the most heavily taxed were consumer goods--particularly"luxuries"--and alcoholic beveiages. Capital goods and transportation equipment were taxed aboutequally. This pattern of taxing consumption goods and subsidizing inputs could increase the protectionfor domestic production. The Foreign Trade Institute estimated that the average domestic value addedin Venezuela was 65 percent. For a good with 65 percent domestic content, an 11 percent subsidy toinputs together with a 14 percent tax on outputs would, by itself, lead to effective protection of27 percent. However, the foreign exchange system effectively imposed a tax on importers ofconsumption goods which averaged between 8 percent (durables) and 37 percent (non-durable luxurygoods) so that effective protection rates would be in the range of 18 percent to 64 percent. Effectiveprotection would also vary with the level of domestic value added. In the case of goods where the valueadded is 35 percent, effective protection on consumer goods would be higher: in the range of 23 percentto 106 percent. Consequently, the exchange system distorted prices, conferring the greatest benefits onproducers of low value-added, non-durable luxuries such as cosmetics and toiletries. Alcoholic beveragesenjoyed particularly large nominal protection-as high as 125 percent in 1986-through the exchange rate.

2.13 In the case of agriculture, it would appear that protection through the exchange regime waslower than that provided to industry. Agricultural inputs were more favored through the exchange rate.However, since food imports also entered at favorable rates, effective protection was lower and, in cases,could even have been nega.ive. For example, in 1984 (1985), agricultural inputs entered at an averageexchange rate of 5.0 Bs./US$ (6.2), while "basic" foods entered at 4.6 (5.2).

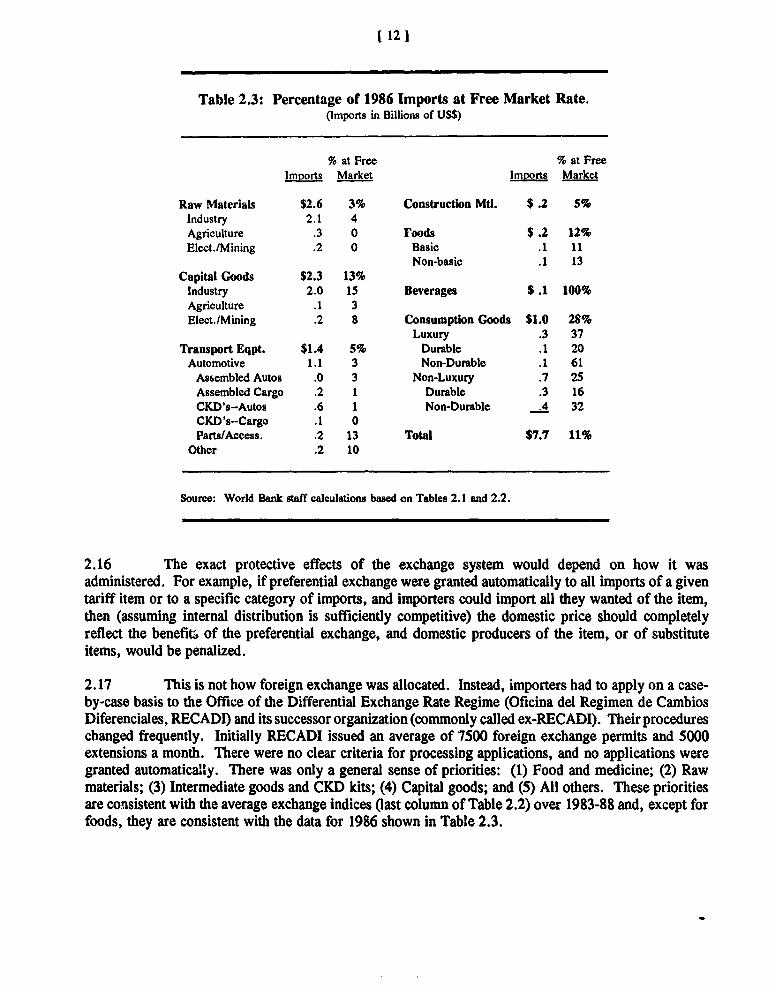

2.14 In 1986 all merchandise imports entered either at the official rate of 7.5 Bs./US$ or at thefree market rate which varied between 14.9 and 27.1 Bs./US$, with an average for the year for alltransactions of 19.7. Assuming that all import categories paid about the same average free rate, it ispossible to infer from Table 2.2 the percentage of each type of merchandise which was imported at thefree market rate in 1986. These percentages are shown in Table 2.3. (In other years imports enteredat multiple official rates and we cannot reproduce these calculations with existing data.)

2.15 For most categories of merchandise, sufficient foreign exchange was available at the officialrate so that importers resorted to the free market only occasionally. However, alcoholic beveragesentered exclusively at the free rate and nearly 30 percent of consumer goods imports had to use the freemarket. Capital goods for industry, parts and accessories for transportation equipment, and non-basicfoods also had above-average use of the free market rate. The system promoted the consumption (anddiscouraged the production) of the subsidized goods while discouraging the consumption (promoting theproduction) of the taxed goods. Since the purpose of the preferential exchange rates was to assist thepoor, the system's incentives were perverse: they encouraged the consumption and discouraged theproduction of "essential" commodities-food and pharmaceuticals.

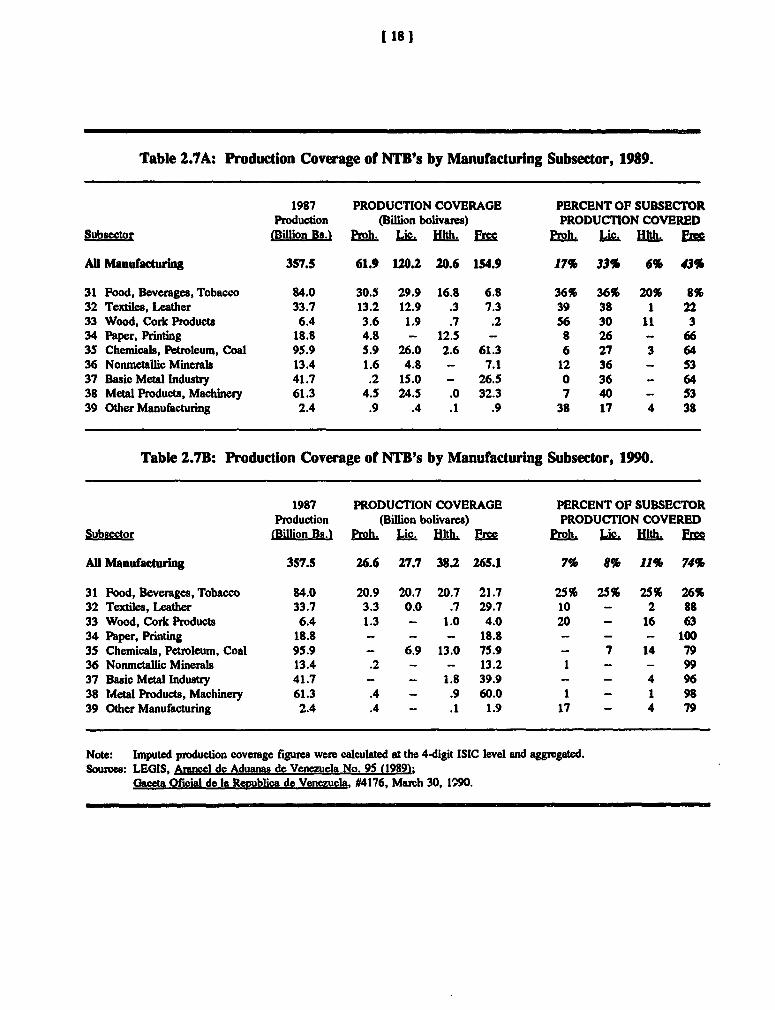

'Under the adjuatment program, CKCD kits were removed from the official exchange mte (14.5 Bs./USS) and paid the freemarket rate (35-40 Bs./US$). Sales fell to 26,000 units in 1989.

[ 121

Table 2.3: Percentage of 1986 Imports at Free Market Rate.(Imports in Billions of USS)

% at Free % at FreeImports Market Imnorts Market

Raw Materials $2.6 3% Construction Mtl. $ .2 5%Industry 2.1 4Agriculture .3 0 Foods $ .2 12%Elect./Mining .2 0 Basic .1 11