Ndiamé Diop Lead Economist, Indonesia October 22, 2015 Indonesia Economic Quarterly October 2015 In times of global volatility

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Ndiamé Diop

Lead Economist, Indonesia

October 22, 2015

Indonesia Economic

Quarterly

October 2015

In times of global volatility

Introduction

These are times of heightened global

volatility…

…making policy making in emerging

economies challenging.

In this difficult environment, Indonesia

is forecast to grow at 4.7 percent in

2015 and 5.3 percent in 2016

But there are important downside

risks …

… triggering a policy response to

support businesses and people in the

short run…and to facilitate investment

and long-term growth.

3

Uncertain global conditions

Recent developments and outlook for Indonesia

Uncertainty and risks

Recent government policy response

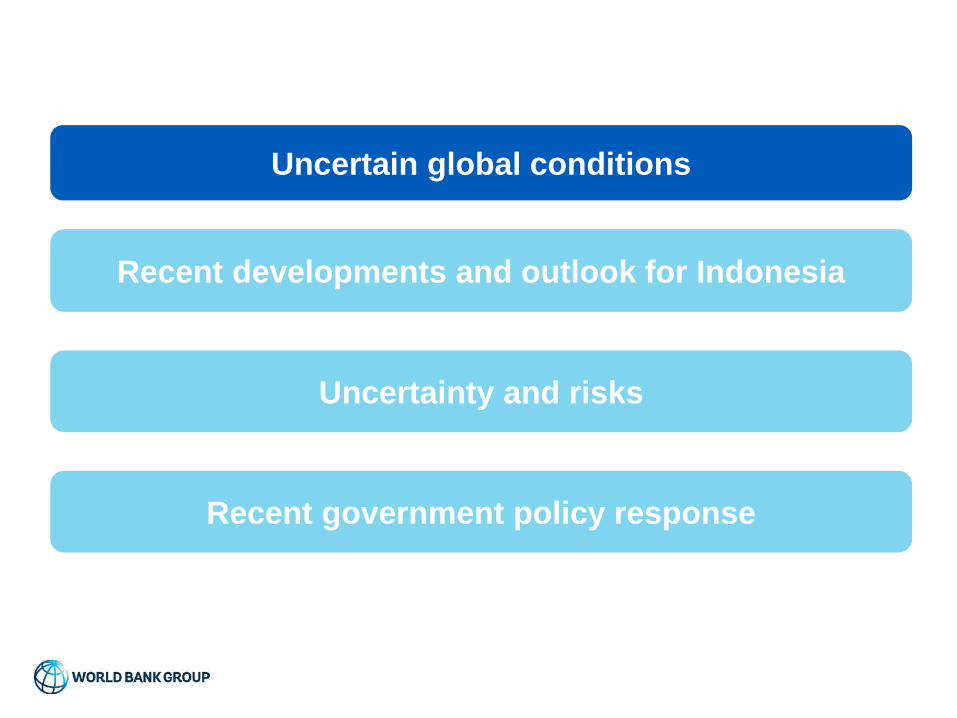

Global growth is still subdued

World Bank projections for global growth in 2015, 2016 and 2017, percent

Source: World Bank East Asia Pacific Economic Update, October 2015: Staying the Course

0

1

2

3

4

5

6

2013 2014 2015* 2016* 2017*

Developing countries

High-income countries

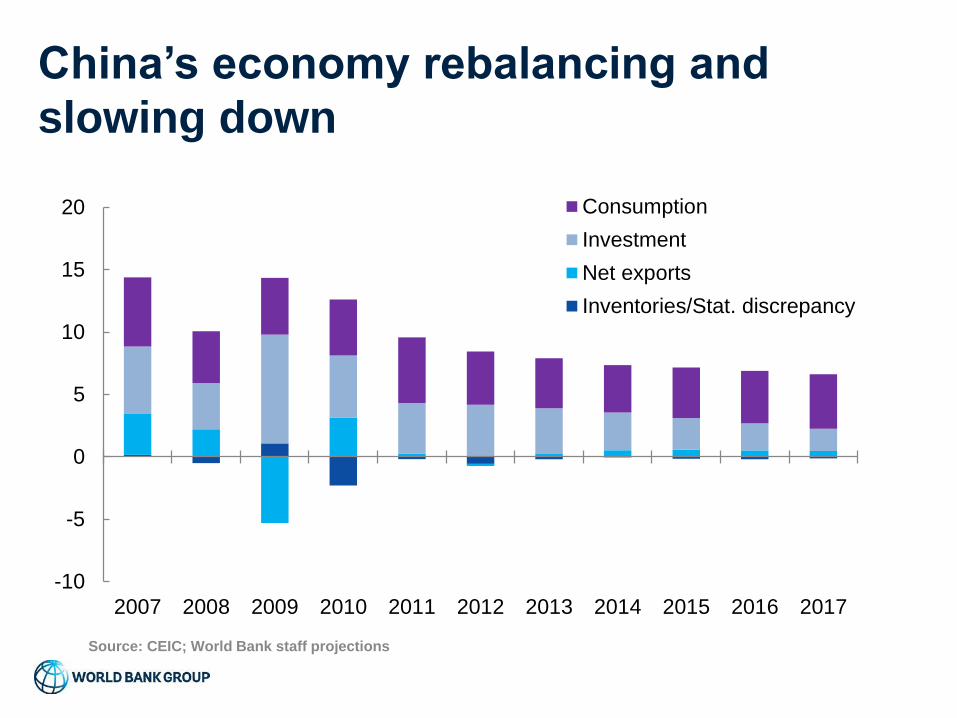

China’s economy rebalancing and

slowing down

Source: CEIC; World Bank staff projections

-10

-5

0

5

10

15

20

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Consumption

Investment

Net exports

Inventories/Stat. discrepancy

Global commodity prices are also

persistently lowIndex, 2010 = 100

Source: World Bank Commodity Outlook, October 2015

60

80

100

120

140

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Energy

Non-energy

70

75

80

85

90

95

100

105

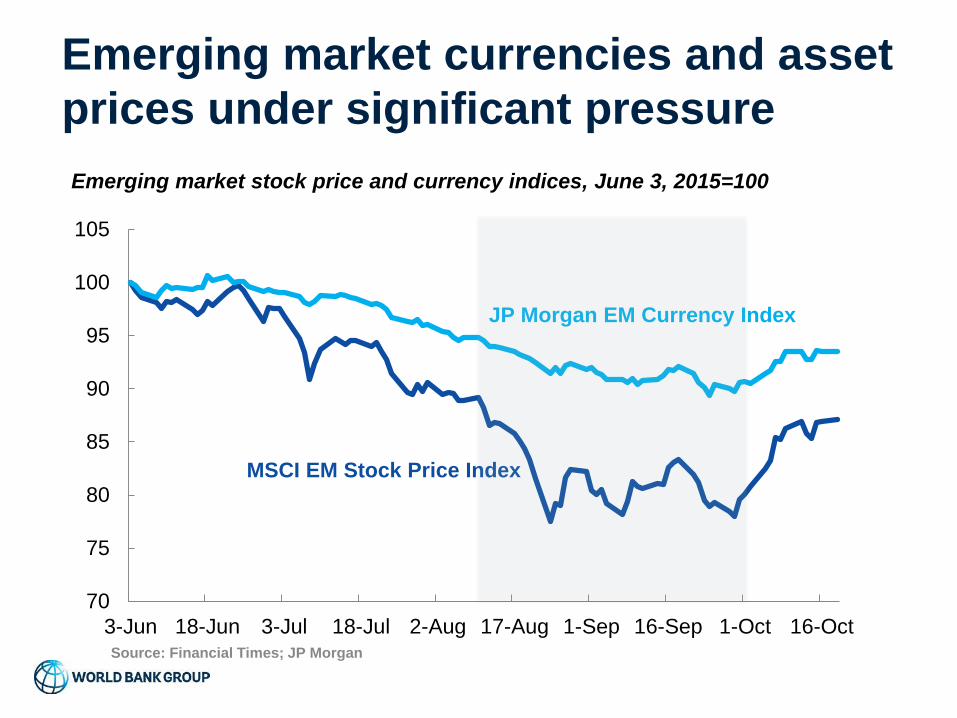

3-Jun 18-Jun 3-Jul 18-Jul 2-Aug 17-Aug 1-Sep 16-Sep 1-Oct 16-Oct

MSCI EM Stock Price Index

JP Morgan EM Currency Index

Emerging market currencies and asset

prices under significant pressure

Source: Financial Times; JP Morgan

Emerging market stock price and currency indices, June 3, 2015=100

Uncertain global and regional conditions

Recent developments and outlook for Indonesia

Uncertainty and risks

Recent government policy response

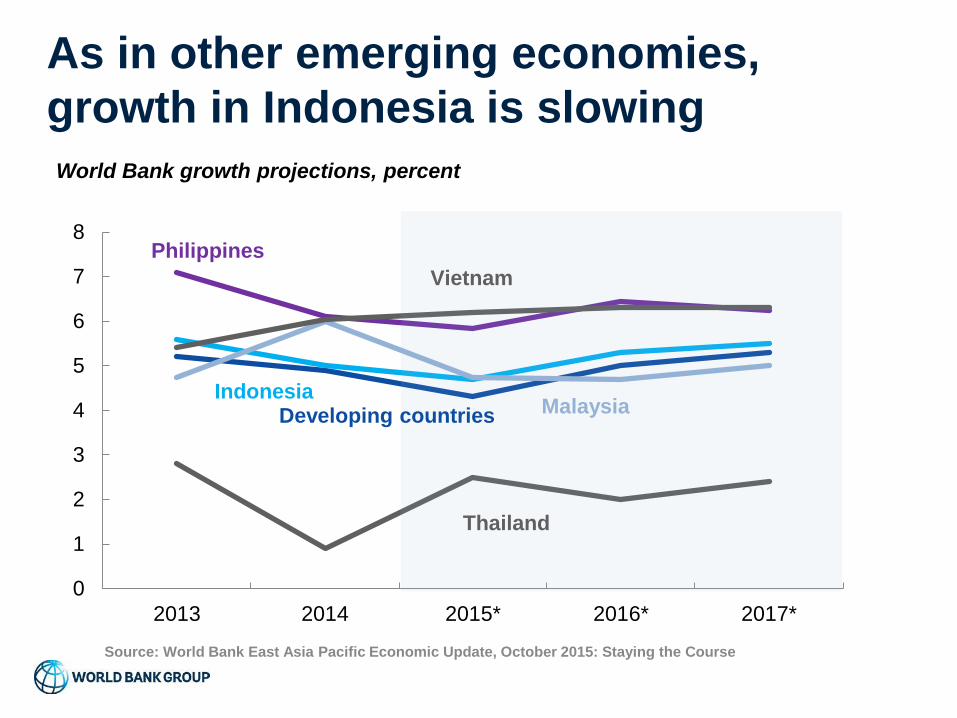

As in other emerging economies,

growth in Indonesia is slowing

Source: World Bank East Asia Pacific Economic Update, October 2015: Staying the Course

0

1

2

3

4

5

6

7

8

2013 2014 2015* 2016* 2017*

Developing countriesIndonesia

Malaysia

Philippines

Vietnam

Thailand

World Bank growth projections, percent

Public capital spending improved

significantly in recent months

Note: * Real capital expenditure is calculated using the implicit total fixed investment deflator with 2010

base from the national accounts

Source: Ministry of Finance; World Bank staff calculations

January – September cumulative realization in nominal and real terms (LHS), IDR

trillion; real capex growth (RHS), percent*

-30

-20

-10

0

10

20

30

40

-40

-20

0

20

40

60

80

100

2011 2012 2013 2014 2015

Capital expenditure (nominal, LHS) Capital expenditure (real, LHS)

Real growth (%, RHS)

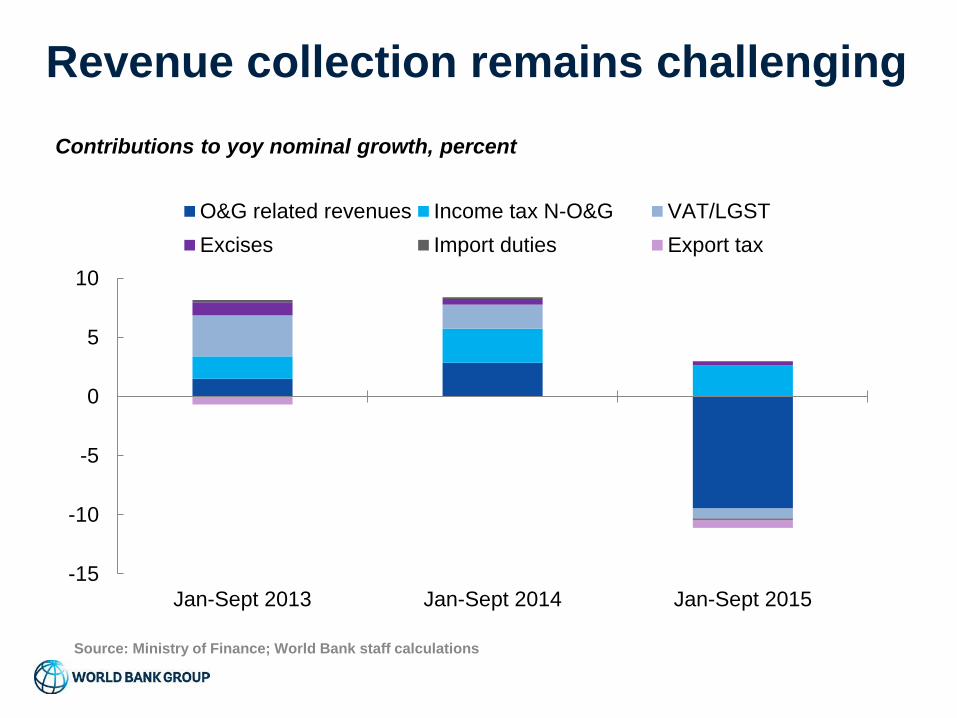

Revenue collection remains challenging

Source: Ministry of Finance; World Bank staff calculations

Contributions to yoy nominal growth, percent

-15

-10

-5

0

5

10

Jan-Sept 2013 Jan-Sept 2014 Jan-Sept 2015

O&G related revenues Income tax N-O&G VAT/LGST

Excises Import duties Export tax

Baseline GDP growth in 2015 unchanged

Note: Revisions are relative to July 2015 IEQ.

Source: BI; BPS; World Bank staff projections

October 2015 IEQ Revisions

(percentage change, unless otherwise

indicated) 2014 2015p 2016p 2015 2016

Real GDP 5.0 4.7 5.3 0.0 -0.2

Consumer prices 6.4 6.5 5.2 -0.3 -0.1

Current account balance (% of GDP) -3.1 -2.0 -2.6 0.7 0.3

Uncertain global and regional conditions

Recent developments and outlook for Indonesia

Uncertainty and risks

Recent government policy response

Near-term uncertainty and risks are

elevated

• Uncertainty about timing and short-term impact of FED lift off

• Risk of China slowing more than expected;

• Risk of severe El Niño;

• Corporate balance sheets, in particular in resource sector;

• These risks to the outlook imply that the forecast pick-up in

growth is not guaranteed.

Uncertain global and regional conditions

Recent developments and outlook for Indonesia

Uncertainty and risks

Recent government policy response

Room for strong countercyclical policy

response limited

• Monetary easing space may be expanding but

uncertainty about FED lift-off is a constraint.

• Space for a stronger fiscal boost is constrained by

the sharp decline in oil and gas fiscal revenues

and weakening VAT/LGST collection.

Short-term stimulus and structural

reforms through policy packages

Efforts to support businesses and people are justified;

Efforts to accelerate capex spending and budget absorption

are important;

Steps taken to reduce regulatory burden and obstacles to

business conduct welcome;

Certain aspects of the package are particularly encouraging:

Removal/ simplification of import licenses (11 regulations so far),

Simplification of investment licensing,

New wage setting mechanism,

Measures to expedite application process for land use permits.

Going forward

Further measures to support manufacturing and tourism

growth and export would help enhance growth and

maintain a low CAD.

Process improvements (e.g. fully paperless electronic

applications and a risk-based import approval regime),

and an institutionalized, centralized screening process for

new regulations will further help.

Strong recovery in growth that generates strong capital

inflows (FDI) could strengthen the Rupiah.

El Niño is expected to moderately raise

domestic rice prices and inflation

El Niño is projected to increase

rice prices by about 5 percent

and CPI inflation by 0.3 p.p.

Poor households spend a larger

share of their income on food

and may be impacted more by

higher prices.

More severe El Niño conditions

may double the above effects.

Implementing Indonesia's national health

insurance system

JKN aims to provide access

to healthcare to all

Indonesians, thus supporting

broader developmental

objectives.

Implementation is

proceeding, but more can be

done to expand coverage

and improve financial

sustainability.

Improving housing outcomes

Indonesia faces a large

housing deficit and an

increasing need for

affordable housing,

particularly in urban areas.

There is strong political

momentum to increase the

supply of affordable housing,

but spending in the sector

needs to be more equitable

and effective.

Related Documents