© 2016 CRISIL Ltd. All rights reserved. India’s future prospects in apparel exports Ajay Srinivasan Director Research August 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

India’s future prospects in apparel exports

Ajay Srinivasan

Director

Research

August 2016

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

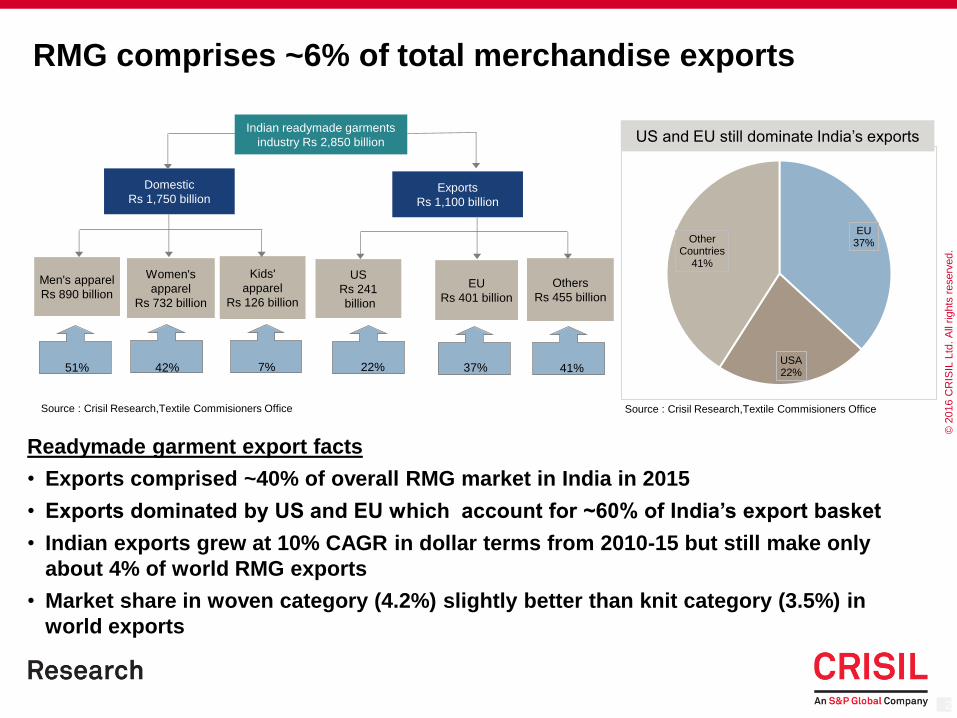

RMG comprises ~6% of total merchandise exports

Readymade garment export facts

• Exports comprised ~40% of overall RMG market in India in 2015

• Exports dominated by US and EU which account for ~60% of India’s export basket

• Indian exports grew at 10% CAGR in dollar terms from 2010-15 but still make only

about 4% of world RMG exports

• Market share in woven category (4.2%) slightly better than knit category (3.5%) in

world exports

2

51% 42% 7% 22% 37% 41%

Indian readymade garments

industry Rs 2,850 billion

Domestic

Rs 1,750 billion Exports

Rs 1,100 billion

Men's apparel

Rs 890 billion

Women's

apparel

Rs 732 billion

Kids'

apparel

Rs 126 billion

US

Rs 241

billion

EU

Rs 401 billion

Others

Rs 455 billion

Source : Crisil Research,Textile Commisioners Office

EU 37%

USA 22%

Other Countries

41%

US and EU still dominate India’s exports

Source : Crisil Research,Textile Commisioners Office

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

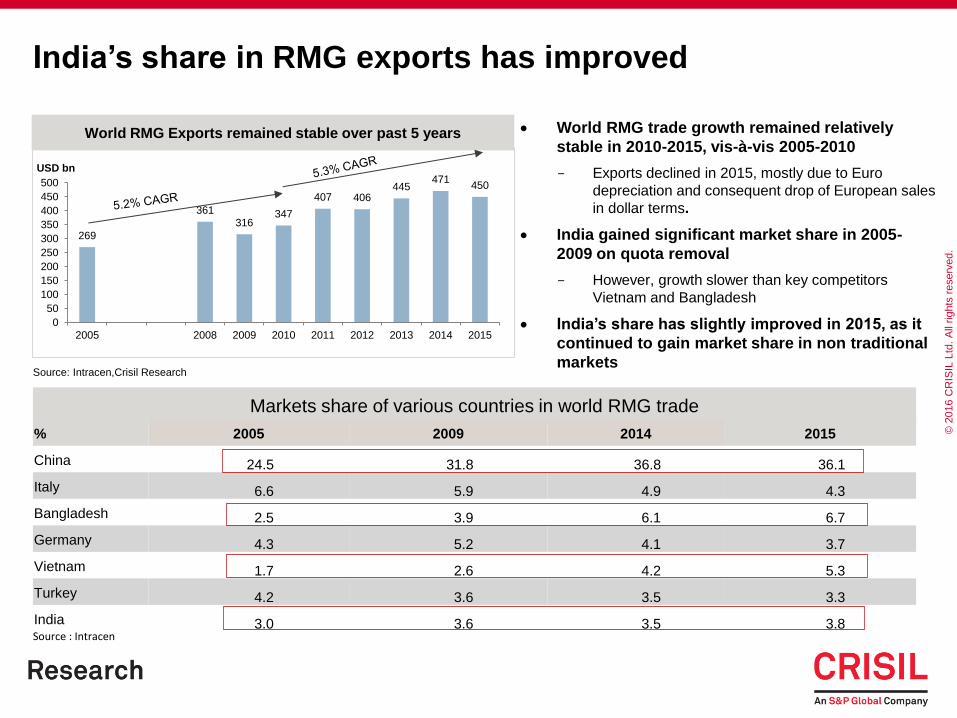

India’s share in RMG exports has improved

3

Source: Intracen,Crisil Research

World RMG Exports remained stable over past 5 years World RMG trade growth remained relatively

stable in 2010-2015, vis-à-vis 2005-2010

- Exports declined in 2015, mostly due to Euro

depreciation and consequent drop of European sales

in dollar terms.

India gained significant market share in 2005-

2009 on quota removal

- However, growth slower than key competitors

Vietnam and Bangladesh

India’s share has slightly improved in 2015, as it

continued to gain market share in non traditional

markets

Markets share of various countries in world RMG trade

% 2005 2009 2014 2015

China 24.5 31.8 36.8 36.1

Italy 6.6 5.9 4.9 4.3

Bangladesh 2.5 3.9 6.1 6.7

Germany 4.3 5.2 4.1 3.7

Vietnam 1.7 2.6 4.2 5.3

Turkey 4.2 3.6 3.5 3.3

India 3.0 3.6 3.5 3.8 Source : Intracen

269

361 316

347

407 406 445

471 450

0

50

100

150

200

250

300

350

400

450

500

2005 2008 2009 2010 2011 2012 2013 2014 2015

USD bn

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

India's knit exports accounted 3.5% of world exports in 2015

4

Indian knit exports dominated by T-shirts, Women suits and men shirts

Indian knit exports cater less to the Jerseys &Pullovers and Women Innerwear which account

for 29% of world knit export

India’s market share in Jerseys and Pullovers, which is the largest knit category, is ~0.5%

Source: Intracen ,CRISIL Research

Product

Share in World

Exports

Share in India's

exports

Tshirts 19% 37%

Women Suits 17% 9%

Jerseys and Pullovers 23% 4%

Women Innerwear 6% 1%

Men's Suits and Jackets 6% 5%

Women Bathrobes and Pyjamas 6% 7%

Mens Shirt 4% 10%

Babies Garment 3% 9%

Mens underpant 3% 6%

Garments 3% 8%

Total value (USD billion) in 2015 224 7.7

(Market Share in world)

2010 2015

5% 8%

2.2% 2.6%

0.5% 0.5%

3% 5%

4% 4%

6% 3%

7% 9%

6% 9%

5% 8%

3% 10%

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

United Arab Emirates

United Kingdom

France

Saudi Arabia

Canada

Poland

Afghanistan

Nigeria

-30

-20

-10

0

10

20

30

-15 -5 5 15 25 35

An

nu

al g

row

th o

f p

art

ne

r co

un

trie

s im

po

rts fro

m th

e

wo

rld

be

twe

en

20

11

-20

15

,%

Annual growth of India's exports to the partner countries between 2011-2015, %

Declining Markets

Growth Markets

Growth of world market for the selected product : 3%

India’s export

growth to

partner >

Partner

Import

growth from

the world

India’s export

growth to

partner <

Partner

Import

growth from

the world

Bubble size is

proportional to

share in the

world imports

of partner

countries

Description Criteria Countries

Slow markets where India performing well Growth in India exports > Partners Imports Germany, Spain , South Africa, France, Ireland

and United Kingdom

Growth markets where India performing

well

Growth in India exports > Partners Imports for the

category

UAE, Poland, Afghanistan, Mexico, Australia,

US

Growth markets where India not

performing well (share in the world imports

> 2%)

Growth in India exports < Partners Imports for the

category

Canada

Growth markets where India not

performing well(share in the world imports

< 2%)

Growth in India exports < Partners Imports for the

category

Saudi Arabia and Nigeria

Source: Intracen ,CRISIL Research

Opportunities for market diversification in knit segment

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

6

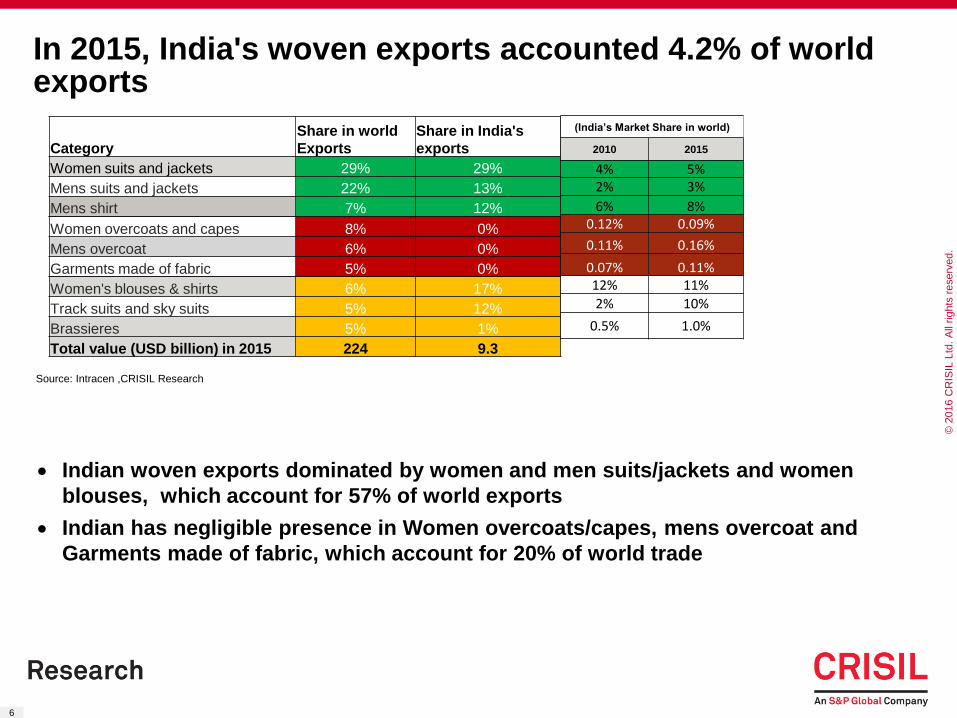

Indian woven exports dominated by women and men suits/jackets and women

blouses, which account for 57% of world exports

Indian has negligible presence in Women overcoats/capes, mens overcoat and

Garments made of fabric, which account for 20% of world trade

Source: Intracen ,CRISIL Research

In 2015, India's woven exports accounted 4.2% of world exports

Category

Share in world

Exports

Share in India's

exports

Women suits and jackets 29% 29%

Mens suits and jackets 22% 13%

Mens shirt 7% 12%

Women overcoats and capes 8% 0%

Mens overcoat 6% 0%

Garments made of fabric 5% 0%

Women's blouses & shirts 6% 17%

Track suits and sky suits 5% 12%

Brassieres 5% 1%

Total value (USD billion) in 2015 224 9.3

(India’s Market Share in world)

2010 2015

4% 5% 2% 3%

6% 8% 0.12% 0.09%

0.11% 0.16%

0.07% 0.11% 12% 11%

2% 10%

0.5% 1.0%

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

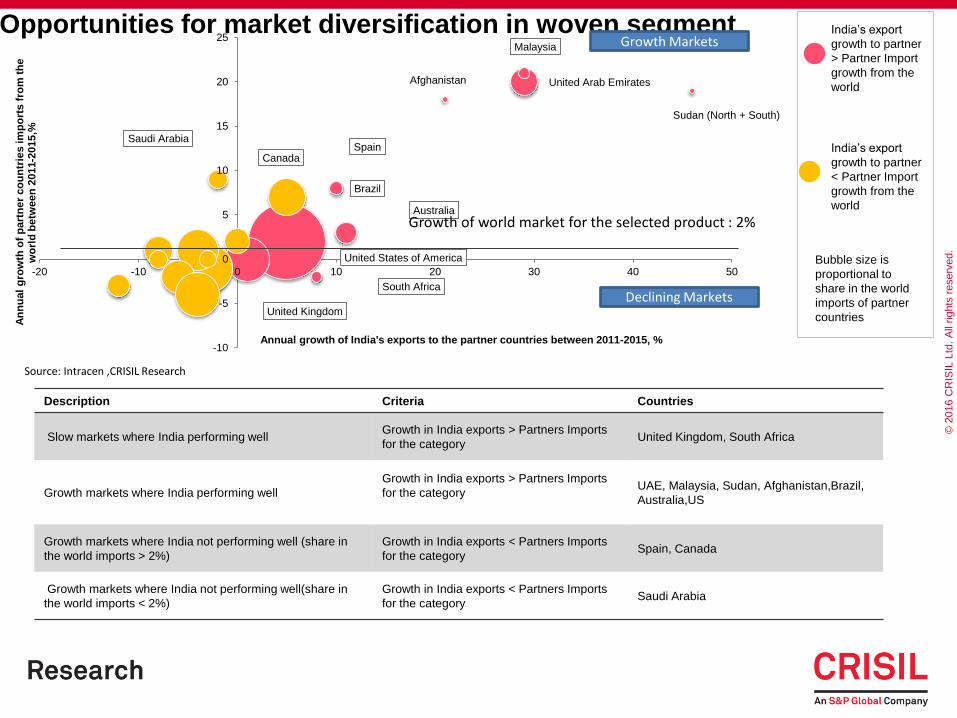

India’s export

growth to partner

> Partner Import

growth from the

world

India’s export

growth to partner

< Partner Import

growth from the

world

Bubble size is

proportional to

share in the world

imports of partner

countries

Description Criteria Countries

Slow markets where India performing well Growth in India exports > Partners Imports

for the category United Kingdom, South Africa

Growth markets where India performing well

Growth in India exports > Partners Imports

for the category

UAE, Malaysia, Sudan, Afghanistan,Brazil,

Australia,US

Growth markets where India not performing well (share in

the world imports > 2%)

Growth in India exports < Partners Imports

for the category Spain, Canada

Growth markets where India not performing well(share in

the world imports < 2%)

Growth in India exports < Partners Imports

for the category Saudi Arabia

United States of America

United Arab Emirates

United Kingdom

Spain Saudi Arabia

Canada

Brazil

Malaysia

Afghanistan

Australia

Sudan (North + South)

South Africa

-10

-5

0

5

10

15

20

25

-20 -10 0 10 20 30 40 50

An

nu

al

gro

wth

of

pa

rtn

er

co

un

trie

s im

po

rts

fro

m t

he

w

orl

d b

etw

ee

n 2

01

1-2

01

5,%

Annual growth of India's exports to the partner countries between 2011-2015, %

Opportunities for market diversification in woven segment Growth Markets

Declining Markets

Growth of world market for the selected product : 2%

Source: Intracen ,CRISIL Research

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

Textile package marginally positive for apparel exports

• Duty drawback on MMF fabric inputs to make India more cost competitive and boost MMF exports

• Flexible labour laws a significant structural change, which should help the industry scale up production based on market needs

Source : Ministry of Textiles, CRISIL Research

Textile package not a game changer but would support export growth

Special package for Textile exports

Increase in overtime caps on working hours (from 3

to 8 hrs a week)

EPF Scheme (Govt. to bear 12% of employers’ contribution for 3 yrs for employees earning

less than Rs 15,000 pm)

Additional incentives under ATUFS (Outcome based

incentives; increase in subsidy to 25% )

Enhanced duty drawback coverage (duty drawback

to enhance MMF capabilities)

Enhancing scope of 80 JJAA of Income Tax Act (provision

of 240 days relaxed to 150 days)

Introduction of fixed term employment

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

India less competitive than Bangladesh and Vietnam

India scores high on raw material availability, but loses out on machinery, market diversification

and mix by fabric. Absence of FTAs and low scale of operations also hamper India’s prospects

9

India’s moderate competitiveness in export market

Note: L: Low; M: Moderate; H: High

Source: CRISIL Research

• Bangladesh enjoys zero duty in EU; China has FTAs with many of its

markets; Vietnam has signed trade agreements with the EU and US

• China gets maximum support from its government

• India exports 59% to US & EU; China ships only 44%

• But shipments to non-US/non-EU markets growing at an impressive

pace

• Majority of RMG exports from India are cotton-based

• Smaller scale of operation and lower labour and machine productivity

hamper India’s efficiency.

• However, surplus cotton availability is a positive.

• China has the best infrastructure in among major textile exporters

Factors Ranking

Policy parameters

FTAs and access policies L

Government policies M

Market parameters

Diversification M

Growth in key markets M

Product diversification

(mix by fabric and range of offering) M

Efficiency parameters

Scale of operations L

Labour cost M

Exports infrastructure M

Raw material availability H

Final ranking M

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

10.7

13.8 12.9

14.4

16.7 17.2

23.0

-

5

10

15

20

25

2010 2011 2012 2013 2014 2015 2016P 2020P

Long term RMG export growth to be moderate

Exports growth in 2015 moderated to 3% as compared to 15% growth in 2014 due to

- Decline in demand from Europe due to sharp (~16%) Euro depreciation

- Deceleration of growth in Non US-EU markets (from 26% export growth in 2014 to 9% in 2015)

Lower export competitiveness to slowdown export growth to 5-7 % CAGR in the next

5 years

15

Growth in exports to moderate India’s market share relatively stable

P: Projected

Source: OTEXA; Eurostat; Ministry of Commerce; CRISIL Research Note: Data for US (in USD), data for EU (in Euro)

Source: OTEXA; Eurostat; CRISIL Research

% India's market shares

US EU Other mkts

2004 3.4 5.5 2.2

2010 4.4 6.8 2.6

2011 4.3 6.8 3.0

2013 4.1 6.2 3.9

2014 4.2 6.3 4.2

2015 4.3 6.3 4.6

2020P 4.2 6.0 6.0

Growth

driven by

prices

Growth Slowdown in 2015

(2013-12%, 2014-15%, 2015-3%)

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

16

About us

CRISIL Limited

CRISIL is a global analytical company providing ratings, research, and risk and policy advisory services. We are India's leading ratings agency. We are also the foremost provider of

high-end research to the world's largest banks and leading corporations.

CRISIL is majority owned by S&P Global Inc., a leading provider of transparent and independent ratings, benchmarks, analytics and data to the capital and commodity markets

worldwide.

CRISIL Research

CRISIL Research is India's largest independent integrated research house. We provide insights, opinion and analysis on the Indian economy, industry, capital markets and companies.

We also conduct training programs to financial sector professionals on a wide array of technical issues. We are India's most credible provider of economy and industry research. Our

industry research covers 86 sectors and is known for its rich insights and perspectives. Our analysis is supported by inputs from our network of more than 5,000 primary sources,

including industry experts, industry associations and trade channels. We play a key role in India's fixed income markets. We are the largest provider of valuation of fixed income

securities to the mutual fund, insurance and banking industries in the country. We are also the sole provider of debt and hybrid indices to India's mutual fund and life insurance

industries. We pioneered independent equity research in India, and are today the country's largest independent equity research house. Our defining trait is the ability to convert

information and data into expert judgements and forecasts with complete objectivity. We leverage our deep understanding of the macro-economy and our extensive sector coverage to

provide unique insights on micro-macro and cross-sectoral linkages. Our talent pool comprises economists, sector experts, company analysts and information management specialists.

CRISIL Privacy Notice

CRISIL respects your privacy. We use your contact information, such as your name, address, and email id, to fulfil your request and service your account and to provide you with

additional information from CRISIL and other parts of S&P Global Inc. and its subsidiaries (collectively, the “Company”) you may find of interest.

For further information, or to let us know your preferences with respect to receiving marketing materials, please visit http://www.crisil.com/privacy. You can view the Company’s

Customer Privacy at https://www.spglobal.com/privacy.

Last updated: April 2016

Disclaimer

CRISIL Research, a division of CRISIL Limited (CRISIL) has taken due care and caution in preparing this Report based on the information obtained by CRISIL from sources which it

considers reliable (Data). However, CRISIL does not guarantee the accuracy, adequacy or completeness of the Data / Report and is not responsible for any errors or omissions or for

the results obtained from the use of Data / Report. This Report is not a recommendation to invest / disinvest in any company covered in the Report. CRISIL especially states that it has

no financial liability whatsoever to the subscribers/ users/ transmitters/ distributors of this Report. CRISIL Research operates independently of, and does not have access to information

obtained by CRISIL’s Ratings Division / CRISIL Risk and Infrastructure Solutions Limited (CRIS), which may, in their regular operations, obtain information of a confidential nature. The

views expressed in this Report are that of CRISIL Research and not of CRISIL’s Ratings Division / CRIS. No part of this Report may be published / reproduced in any form without

CRISIL’s prior written approval.

No content below the line No content below the line

© 2

016 C

RIS

IL L

td.

All

rig

hts

reserv

ed.

Thank you

Ajay Srinivasan

Director

Related Documents