LIFE INSURANCE IN INDIA EMERGING PERSPECTIVE INTRODUCTION Life Insurance in India was nationalised by incorporating Life Insurance Corporation (LIC) in 1956. All private life insurance companies at that time were taken over by LIC. In 1993 the Government of Republic of India appointed RN Malhotra Committee to lay down a road map for privatisation of the life insurance sector. While the committee submitted its report in 1994, it took another six years before the enabling legislation was passed in the year 2000, legislation amending the Insurance Act of 1938 and legislating the Insurance Regulatory and Development Authority Act of 2000. The same year that the newly appointed insurance regulator - Insurance Regulatory and Development Authority IRDA -- started issuing licenses to private life insurers. LIST OF LIFE INSURERS (AS OF SEPT, 2006) Apart from Life Insurance Corporation, the public sector life insurer, there are 14 other private sector life insurers, most of them joint ventures between Indian groups and global insurance giants. LIFE INSURER IN PUBLIC SECTOR 1. Life Insurance Corporation of India LIFE INSURERS IN PRIVATE SECTOR 1. Bajaj Allianz Life PRANAV,SURAT 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LIFE INSURANCE IN INDIA EMERGING PERSPECTIVE

INTRODUCTION

Life Insurance in India was nationalised by incorporating Life Insurance Corporation (LIC) in 1956. All private life insurance companies at that time were taken over by LIC.

In 1993 the Government of Republic of India appointed RN Malhotra Committee to lay down a road map for privatisation of the life insurance sector.

While the committee submitted its report in 1994, it took another six years before the enabling legislation was passed in the year 2000, legislation amending the Insurance Act of 1938 and legislating the Insurance Regulatory and Development Authority Act of 2000. The same year that the newly appointed insurance regulator - Insurance Regulatory and Development Authority IRDA -- started issuing licenses to private life insurers.

LIST OF LIFE INSURERS (AS OF SEPT, 2006)

Apart from Life Insurance Corporation, the public sector life insurer, there are 14 other private sector life insurers, most of them joint ventures between Indian groups and global insurance giants.

LIFE INSURER IN PUBLIC SECTOR

1. Life Insurance Corporation of India

LIFE INSURERS IN PRIVATE SECTOR

1. Bajaj Allianz Life

PRANAV,SURAT 1

1. Tata AIG Life 2. ICICI Prudential Life Insurance 3. HDFC Standard Life 4. Birla Sunlife 5. SBI Life Insurance 6. Kotak Mahindra Old Mutual Life Insurance 7. Aviva Life Insurance

8. Reliance Life Insurance Company Limited - Formerly known as AMP Sanmar LIC

9. Metlife India Life Insurance 10. ING Vysya Life Insurance 11. Max Newyork Life Insurance 12. Sahara Life Insurance - Now they are not into business 13. Shriram Life Insurance 14. Bharti AXA Life Insurance Co Ltd

Indian Insurance Industry Overview

All life insurance companies in India have to comply with the strict

regulations laid out by Insurance Regulatory and Development

Authority of India (IRDA). Therefore there is no risk in going in for

private insurance players. In terms of being rated for financial strength

like international players, only ICICI Prudential is rated by Fitch India at

National Insurer Financial Strength Rating of AAA(Ind) with stable

outlook indicating the highest claims paying ability rating.

Life Insurance Corporation of India (LIC), the state owned behemoth,

remains by far the largest player in the market. Among the private

sector players, ICICI Prudential Life Insurance(JV between ICICI Bank

and Prudential PLC)is the largest followed by Bajaj Allianz Life

Insurance Company Limited (JV between Bajaj Group and Allianz). The

private companies are coming out with better products which are more

beneficial to the customer. Among such products are the ULIPs or the

Unit Linked Investment Plans which offer both life cover as well as

scope for savings or investment options as the customer

desires.Further, these type of plans are subject to a minimum lock-in

period of three years to prevent misuse of the significant tax benefits

offered to such plans under the Income Tax Act. Hence, comparison of

such products with mutual funds would be erroneous.

Legal frameworks

At the legal and regulatory levels, Booz Allen's review identified a wide

variability in the maturity of the frameworks that govern regional

insurance markets. Until recently, almost all MENA countries had

outdated insurance laws and regulations; some countries had no

insurance law at all. Over the past few years, many countries have

initiated serious efforts to upgrade their regulatory frameworks, as

evidenced by the enactment of new laws. They have strengthened the

independence and supervisory capabilities of regulatory entities in line

with the core principles of the International Association of Insurance

Supervisors (IAIS); they have also issued sector guidance notes

covering, for example, governance, market conduct, and risk

management.

That said, there still remains a wide variation in the

comprehensiveness and application of legal frameworks across the

region. Accordingly, insurance regulators in countries with under-

developed legal frameworks should seek to upgrade their legal

frameworks and ensure that they reflect international best practices,

such as the principles of the IAIS. In addition, policymakers should seek

to establish a specialized insurance judicial authority to resolve

insurance disputes in countries where such an authority does not exist.

Finally, in countries where there is a rapidly growing demand for

takaful (Sharia-compliant) insurance, the legal framework should also

promulgate adequate legislation to address this form of insurance.

Regulatory bodies and processes

The comprehensiveness and effectiveness of regulatory processes,

especially supervisory processes, varies considerably across the

region. Countries such as Bahrain and Jordan, which have well-

developed regulatory frameworks, are either applying or developing

risk-based supervision processes that comply with the standards of

international bodies such as IAIS. Other countries, such as Qatar,

Kuwait, and the United Arab Emirates, have less-developed supervisory

processes that are more administrative in orientation.

'In parallel with upgrading legal frameworks, policymakers in the

region should seek to empower their insurance regulatory bodies. The

empowerment of the regulatory body should be constituted in the legal

framework, which should address the body's legal form, ensure its

independence, vest appropriate authorities, and clarify any

overlapping responsibilities with other governmental entities,' said

Maher Hammoud, Senior Associate, Booz Allen Hamilton.

In addition, regulators should seek to enhance their capabilities,

especially in the area of supervision (including staff and IT). In

upgrading supervisory capabilities, regulators should take into account

the guidelines set out as part of the IAIS core principles.

Nature of competition

The insurance markets of the Middle East are generally competitive,

and although there is significant involvement of the private sector in

the insurance industry, this is offset to some extent by a high degree

of market fragmentation. In particular, many markets of the MENA

region are characterized by a large number of small players when

measured by capital employed.

There are a number of ramifications of the current low levels of

capitalization. At an overall industry level, this results either in

insurance being placed directly outside of the region through

international brokers or in the practice of fronting, whereby local

insurers retain a small portion of the risk and transfer the remaining

risk to their international reinsurance partners.

'As a consequence of the lack of capacity, risk-management and

actuarial capabilities in the region remain underdeveloped, resulting in

a disproportionate reliance on international reinsurers to assess the

risks and provide appropriate pricing guidelines,' Mr. Vayanos said.

Booz Allen suggests that regulators should seek to further raise the

competitive bar through higher capital requirements and the

introduction of governance and risk-management requirements. In

highly fragmented markets, regulators should investigate the option of

increasing capital requirements to stimulate market consolidation and

increase the level of risk-retention capacity. This in turn would result in

larger local companies with the resources to invest in capabilities, and

would also reduce the level of fronting.

On the governance side, regulators should introduce minimum

governance requirements such as the establishment of internal

functions (for example, an internal audit), the definition of fit and

proper criteria for board members and senior management, the

development of policies and procedures manuals, and the formation of

an investment policy subject to review and approval by the board.

In countries where there is a rapidly growing demand for takaful

insurance, regulators should identify, develop, and disseminate risk-

management best practices that take into account the contractual

relationships of Islamic insurance products.

Skills and training

Across the region, the insurance sector is characterized by a shortage

of skills - particularly product development, underwriting, and actuarial

skills. The absence of skills clearly affects the development of the

sector, specifically in the areas of product innovation, risk assessment,

and pricing. This situation is exacerbated by nationalization

requirements in some countries, which extend the time required to

train and equip staff for key positions, and the availability of highly

attractive positions in other areas of the financial services sector.

Cultivating the growth of a pool of skilled local insurance professionals

is paramount to the development of the insurance sector, given the

existing acute shortage of skills. As such, the study proposes that

policymakers and regulators act as catalysts in the development of

professional knowledge in three ways:

In general, it is customary to set minimum requirements for insurance

professionals that go beyond general educational attainment and

include specialized insurance qualifications. Regulators can influence

the market in raising the standards of training programs by adopting

internationally accredited programs and selectively approving local

programs that meet minimum criteria.

Training programs can be organized by the regulator, the industry

itself (such as associations of insurance companies and the companies

themselves), and by the private sector as the demand for such training

increases. In countries where the demand for takaful products is

growing rapidly, regulators need to ensure the availability of training

programs to educate the market on these relatively new products.

Regulators can require companies to take a more active role in

developing the expertise of their employees by mandating training

budgets and staff training programs.

Market-led Initiatives

Promoting the involvement of industry-wide bodies, whether at a local

or regional level, is a valuable enabler for the development of the

market by providing forums for the harmonization of standards and

activities, and for the sharing of best practices. In particular,

policymakers and regulators can play a valuable role in promoting

more active involvement from industry associations, encouraging the

adoption of market standards, fostering the availability of granular

market statistics, generating consumer awareness of insurance, and

raising the profile of the industry to attract new talent.

By way of example, Malaysia has been very successful in raising the

awareness of life insurance. In 2003, a joint initiative, InsuranceInfo,

was launched by Bank Negara (the Central Bank and insurance

regulator of Malaysia) and other industry players. InsuranceInfo covers

topics such as standard life insurance, annuities, investment-linked

insurance plans, and child education plans. InsuranceInfo disseminates

this information primarily through its website, as well as through

booklets made available in branches of selected insurance companies

and articles published in major newspapers. This program has

contributed to the development of the life insurance market, which

generated premiums of US$4.8 billion in 2005 - more than three times

those in the entire MENA region.

Insurance has always been a politically sensitive subject in India.

Within less than 10 years of independence, the Indian government

nationalized private insurance companies in 1956 to bring this

vital sector under government control to raise much needed

development funds.

Since then, state-owned insurance companies have grown into

monoliths, lumbering and often inefficient but the only alternative.

They have been criticized for their huge bureaucracies, but still have

millions of policy holders as there is no alternative.

Any attempt to even suggest letting private players into this vital

sector has met with resistance and agitation from the powerful

insurance employees unions. The Narasimha Rao government

(1991-96) which unleashed liberal changes in India's rigid economic

structure could not handle this political hot potato. Ironically, it is

the coalition government in power today which has declared its

intention of opening up insurance to the private sector. Ironical

General insurance industry grew by 15 per cent in the August led

by Anil Ambani group firm Reliance General Insurance, which recorded

the highest growth of 161 per cent in gross premium as compared to a

year ago.

The 12 non-life insurers collected Rs 2,116 crore in premium in August,

against Rs 1,839 crore during the same period in the previous year,

according to data collected by regulator the Insurance Regulatory

Development Authority (IRDA).

During the month, market leader New India Assurance's premium

collection witnessed a dip of one per cent to Rs 358 crore as compared

to Rs 363 crore a year ago.

In the private sector, the largest player, ICICI Lombard collected 22 per

cent higher premium at Rs 302 crore.

Private players increased their business to Rs 881 crore in August from

Rs 662 crore in the same month last year, the data shows.

With a premium collection of Rs 155 crore in August, against Rs 59

crore a year ago, Reliance General Insurance became the fastest

growing insurer.

In percentage terms, while the public sector could increase their

premiums by just 5 per cent, eight private sector players clocked

premium growth of 33 per cent.

Post-detariffing, the private sector seems to be gaining in market share

faster than their public sector counterpart in the industry.

Market share of private players during the period went up to 42 per

cent as against 58 per cent accounted for by those in the public sector.

Lessons from the insurance sector

Patterns in the insurance sector in India post-liberalisation have so far

contradicted the predictions of those who argued that the opening up

would deliver lower prices and better services for consumers.

DESPITE what people in general are told, there are very few things in

the discipline of economics which are undisputed. Much of what is

presented as "obvious" or "inevitable" often has poor foundations in

theory and little justification in terms of empirical experience. Recent

theoretical work indeed tends to point to the fragility of assumptions

that underlie many established axioms. Truly, economics is at best an

inexact science, highly probabilistic, and ultimately dependent upon

intuition or "hunch".

Nevertheless, there are some arguments which are almost universally

accepted (given the ceteris paribus condition, "other things remaining

equal"). Thus, one of the first things that students of economics are

taught is that when there are more producers in the market,

competition tends to drive the price down to a level which is lower than

when there are fewer producers.

The same is therefore supposed to be true of markets which were

previously closed to competition, and are opened to new entrants. The

expectation is that when monopolies or oligopolies are forced to

confront new players, they will respond by lowering their prices or

improving quality, even if the new entrants have higher costs to begin

with.

This is why supporters of the Insurance Regulatory and Development

Authority Bill, 1999 argued that opening up the sector to more

domestic and foreign competition would ensure much better conditions

for consumers. It was argued that more products (in the form of new

types of insurance policies) would be available and that premium rates

would fall as new entrants offered them, and that the existing

nationalised insurance companies would be forced to deal with the

threat and even reality of competition.

But such are the peculiarities of economics in the current context that

even this obvious expectation has been belied. In fact, so far precisely

the opposite tendency has been observed. Several new insurance

companies, almost all with some foreign backing as well, have entered

the market over the past six months in particular. Yet on July 1, a

number of nationalised general insurance companies took measures to

raise rates of premium and actually reduce the number of types of

policies on offer.

A demonstration against the opening up of the insurance sector to

private players. The overall effect of the entry of private companies

into the sector is that consumers, who were supposed to be the main

beneficiaries of the change, will in fact be worse off.

The rates offered for vehicle insurance show this very clearly. Rates of

premium on cars have gone up by around 40 per cent on average.

Meanwhile, a category like third party insurance for two-wheelers, for

which the premium rates used to be quite low, has seen an increase of

nearly three times. Some companies even plan not to provide

insurance for this category at all. When questioned about these

increases, insurance officers have pointed to the effect of the new

multinational-assisted entrants into the insurance business, and the

much higher rates they are charging!

In other words, what they are suggesting is that now competition is

going to be based not on prices, as was fondly believed earlier, but on

profits. Insurance companies, not just the private ones but even in the

public sector, are anxious to show profits on all lines of activity.

Indeed, the public sector companies are especially keen to show that

they are no less efficient than private players, and therefore end up

using very similar tactics.

What this shows most starkly is that the cross-subsidisation which was

characteristic of the insurance sector earlier, and which indeed is

typical of most public sector service provision, is disappearing. The

general insurance companies have already been instructed to calculate

profits on each line of business separately. Life insurance is likely to

follow suit.

The irony is that both the life insurance and general insurance

corporations were already highly profitable in the aggregate. Their

cross-subsidies, which were based on some notions of income and the

ability of people to pay, and the need to provide insurance services to

as many people as possible, did not prevent them from providing large

surpluses to government coffers. Now, however, because they are

concerned about showing profit rates or margins which are comparable

to those of the private sector, they are likely to turn more cautious and

more stingy about providing insurance cover to a range of consumers,

simply in order to maintain "competitive" profitability.

What does this mean for consumers? It means the complete opposite

of what was promised when the insurance sector was liberalised. Thus,

not only have premium rates gone up quite sharply, but it may become

more difficult to be eligible for a whole range of policies. So people

may actually find it more difficult or more expensive to take on policies

in areas where they really require it, that is, where they are in fact at

risk.

Also, rates of claim settlement in India were earlier the highest in the

world, at more than 90 per cent in life insurance and 70 per cent in

general insurance, compared to around 40 per cent internationally in

both categories. These rates are now likely to fall, as companies try to

ensure higher profit margins through resort to this method as well. This

means that in the event of some misfortune, which may be covered by

the policy on paper, the policy-holder would be less likely than before

to get his or her claim settled.

This whole process may appear very paradoxical. But actually it brings

out very clearly why privatisation of certain services, as well as the

opening up of this sector in particular, may be very problematic, and

why the concerns of critics at the time were not misplaced. It should

also be noted that this is quite unlike the privatisation of loss-making

concerns in the manufacturing sector, which often simply reflects the

urgent need to restructure and allow the government to move out of

dead-end economic activities.

THERE were many points with respect to insurance sector liberalisation

that the critics had raised. There was the possibility of fraud by, or

failure of, private companies, which would adversely affect those who

had sunk their life savings in such companies. The high incidence of

such cases was indeed why the companies in India had been

nationalised in the first place. There was the potential misuse of the

huge pool of savings raised by this sector, which could be utilised for

productive investment, including by the state.

In addition to these very serious worries, there was also the concern

that consumers, who were supposed to be the main beneficiaries,

would in fact be adversely affected. At the time such fears were simply

laughed at. But already, with the recent change in the price structure,

there is evidence that such a tendency of worsening conditions for

insurance consumers may not be so far-fetched.

It is especially sad because it is so unnecessary. It is bad enough that

private sector insurance companies, in their zeal to cut costs and

improve profitability indicators, ignore the basic interests of people

and effectively deny important sections of people insurance cover for

different categories. This is, after all, only to be expected in a business

driven entirely by profit. In fact, one of the reasons for curtailing

services and raising costs is the huge increase in advertising costs

which all the companies - private and public - are now engaging in,

which makes the need to generate more revenue even more

imperative.

But when public sector companies start behaving in exactly the same

way, then it is worse than pointless. The entire purpose of having

public provision of such services is to ensure that they do not simply

behave like other private players. The meeting of broader social goals

can then be achieved by cross-subsidisation, which is sustainable as

long as the entire operation remains profitable. There is no need for

such enterprises to be as profitable as possible using any possible

means, because then the basic objective of using public corporations

to provide public services would not be met.

The tragedy is that when the government itself starts imposing upon

such public companies the pressure of being profitable at all costs,

people will end up finding little to choose between the public and

private sectors. It could well be that there is an implicit agenda in this,

eventually to privatise these large and profitable public sector

companies which would anyway behave no differently from private

players.

While this may serve the purpose of those who are ideologically

committed to the destruction of public sector activity independent of

context, it can do little to serve the real interests of the citizens of this

country.

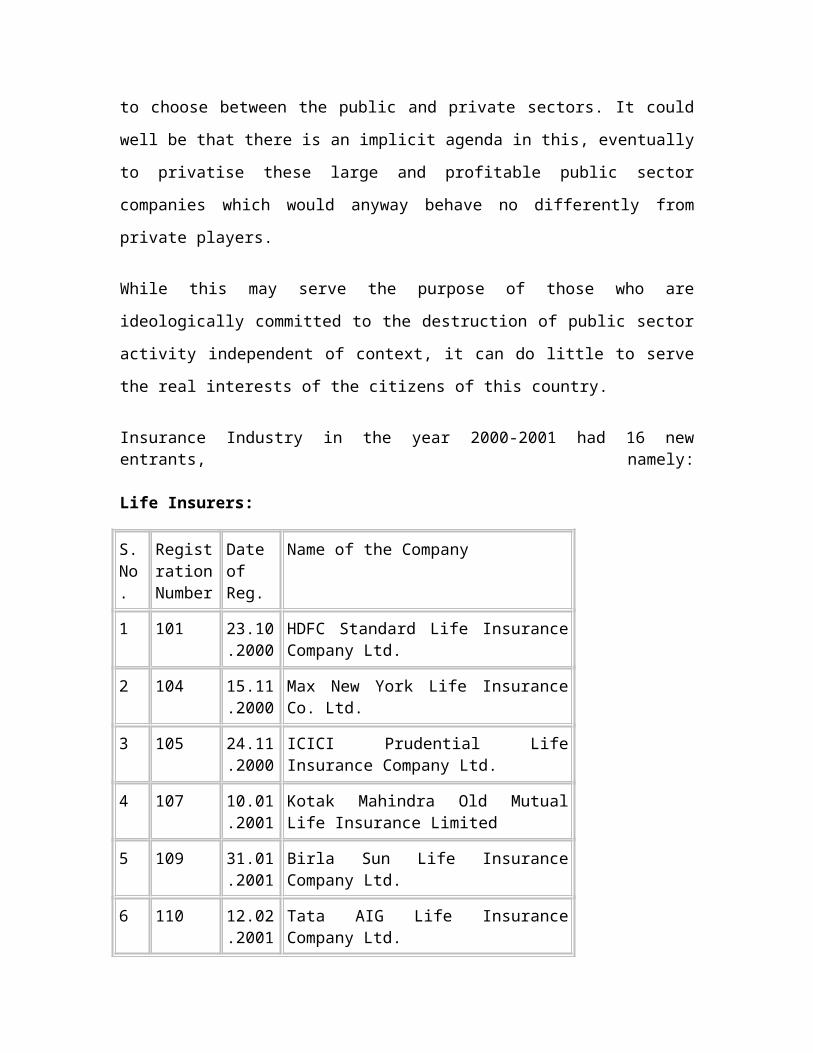

Insurance Industry in the year 2000-2001 had 16 new entrants, namely:

Life Insurers:

S.No.

RegistrationNumber

Date of Reg.

Name of the Company

1 101 23.10.2000

HDFC Standard Life Insurance Company Ltd.

2 104 15.11.2000

Max New York Life Insurance Co. Ltd.

3 105 24.11.2000

ICICI Prudential Life Insurance Company Ltd.

4 107 10.01.2001

Kotak Mahindra Old Mutual Life Insurance Limited

5 109 31.01.2001

Birla Sun Life Insurance Company Ltd.

6 110 12.02.2001

Tata AIG Life Insurance Company Ltd.

7 111 30.03.2001

SBI Life Insurance Company Limited .

8 114 02.08.2001

ING Vysya Life Insurance Company Private Limited

9 116 03.08.2001

Bajaj Allianz Life Insurance Company Limited

10 117 06.08.2001

Metlife India Insurance Company Pvt. Ltd.

11 133 04.09.2007

Future Generali India Life Insurance Company Limited

12 135 19.12 IDBI Fortis Life Insurance Company

.2007 Ltd.

General Insurers :

S.No. Registration Number

Date of Registration

Name of the Company

1 102 23.10.2000

Royal Sundaram Alliance Insurance Company Limited

2 103 23.10.2000

Reliance General Insurance Company Limited.

3 106 04.12.2000

IFFCO Tokio General Insurance Co. Ltd

4 108 22.01.2001

TATA AIG General Insurance Company Ltd.

5 113 02.05.2001

Bajaj Allianz General Insurance Company Limited

6 115 03.08.2001

ICICI Lombard General Insurance Company Limited.

7 131 03-08-2007

Apollo DKV Insurance Company Limited

8 132 04-09-2007

Future Generali India Insurance Company Limited

9 134 16-11-2007

Universal Sompo General Insurance Company Ltd.

Yr: 2001-2002 : ( From 1st Jan 2001 to Dec. 2002)

Insurance Industry in this year, so far has 5new entrants; namely

Life Insurers:

S.No.

RegistrationNumber

Date of Reg.

Name of the Company

1 121 03.01.2002

AMP Sanmar Life Insurance Company Limited.

2 122 14.05.2002

Aviva Life Insurance Co. India Pvt. Ltd.

General Insurers :

S.No. Registration Number

Date of Registration

Name of the Company

1 123 15.07.2002

Cholamandalam General Insurance Company Ltd.

2. 124 27.08.2002

Export Credit Guarantee Corporation Ltd.

3. 125 27.08.2002

HDFC-Chubb General Insurance Co. Ltd.

Yr: 2003-2004 : ( From 1st Jan 2003 till Date)

Insurance Industry in this year, so far has 1new entrants; namely

Life Insurers:

S.No.

RegistrationNumber

Date of Reg.

Name of the Company

1 127 06.02.2004

Sahara India Insurance Company Ltd.

Yr: 2004-2005 :

Insurance Industry in this year, so far has 1new entrants; namely

Life Insurers:

S.No.

RegistrationNumber

Date of Reg.

Name of the Company

1 128 17.11.2005

Shriram Life Insurance Company Ltd.

INSURANCE BUSINEES:

Insurance business is divided into four classes :

1) Life Insurance 2) Fire Insurance 3) Marine Insurance and 4) Miscellaneous Insurance.

Life Insurers transact life insurance business; General Insurers transact the rest.

No composites are permitted as per law.

LEGISLATION (as on 1.4.2000):

Insurance is a federal subject in India. The primary legislation that deals with insurance business in India is:

Insurance Act, 1938, and Insurance Regulatory & Development Authority Act, 1999.

INSURANCE PRODUCTS (as on 1.4.2000) (for latest information get in touch with the current insurers – website information of insurers is provided at the web page for insurers ):

Life Insurance:

Popular Products: Endowment Assurance (Participating), and Money Back (Participating). More than 80% of the life insurance business is from these products.

General Insurance:

Fire and Miscellaneous insurance businesses are predominant. Motor Vehicle insurance is compulsory.

Tariff Advisory Committee (TAC) lays down tariff rates for some of the general insurance products (please visit website of GIC for details )

2001

New products have been launched by life insurers. These include linked-products. For details, please visit the websites of life insurers.

INFORMATION

About the insurance industry, the following documents may be helpful:

Malhotra Committee Report (The Report of the Committee on Reforms in the Insurance Sector);

IRDA's First Annual Report - 2001

CUSTOMER PROTECTION:

Insurance Industry has Ombudsmen in 12 cities. Each Ombudsman is empowered to redress customer grievances in respect of insurance contracts on personal lines where the insured amount is less than Rs. 20 lakhs, in accordance with the Ombudsman Scheme. Addresses can be obtained from the offices of LIC and other insurers.

Parties to contract

There is a difference between the insured and the policy owner (policy holder), although the owner and the insured are often the same person. For example, if Joe buys a policy on his own life, he is both the owner and the insured. But if Jane, his wife, buys a policy on Joe's life, she is the owner and he is the insured. The policy owner is the guarantee and he or she will be the person who will pay for the policy. The insured is a participant in the contract, but not necessarily a party to it.

The beneficiary receives policy proceeds upon the insured's death. The owner designates the beneficiary, but the beneficiary is not a party to the policy. The owner may change the beneficiary unless the policy has an irrevocable beneficiary designation. With an irrevocable beneficiary, that beneficiary must agree to any beneficiary changes, policy assignments, or cash value borrowing.

In cases where the policy owner is not the insured (also referred to as the cestui qui vit or CQV), insurance companies have sought to limit policy purchases to those with an "insurable interest" in the CQV. For life insurance policies, close family members and business partners will usually be found to have an insurable interest. The "insurable interest" requirement usually demonstrates that the purchaser will actually suffer some kind of loss if the CQV dies. Such a requirement prevents people from benefiting from the purchase of purely speculative policies on people they expect to die. With no insurable interest requirement, the risk that a purchaser would murder the CQV for insurance proceeds would be great. In at least one case, an insurance company which sold a policy to a purchaser with no insurable interest (who later murdered the CQV for the proceeds), was found liable in court for contributing to the wrongful death of the victim (Liberty National Life v. Weldon, 267 Ala.171 (1957)).

Contract terms

Special provisions may apply, such as suicide clauses wherein the policy becomes null if the insured commits suicide within a specified

time (usually two years after the purchase date; some states provide a statutory one-year suicide clause). Any misrepresentations by the insured on the application is also grounds for nullification. Most US states specify that the contestability period cannot be longer than two years; only if the insured dies within this period will the insurer have a legal right to contest the claim on the basis of misrepresentation and request additional information before deciding to pay or deny the claim.

The face amount on the policy is the initial amount that the policy will pay at the death of the insured or when the policy matures, although the actual death benefit can provide for greater or lesser than the face amount. The policy matures when the insured dies or reaches a specified age (such as 100 years old).

Costs, insurability, and underwritingThe insurer (the life insurance company) calculates the policy prices with an intent to fund claims to be paid and administrative costs, and to make a profit. The cost of insurance is determined using mortality tables calculated by actuaries. Actuaries are professionals who employ actuarial science, which is based in mathematics (primarily probability and statistics). Mortality tables are statistically-based tables showing expected annual mortality rates. It is possible to derive life expectancy estimates from these mortality assumptions. Such estimates can be important in taxation regulation.[1] [2]

The three main variables in a mortality table have been age, gender, and use of tobacco. More recently in the US, preferred class specific tables were introduced. The mortality tables provide a baseline for the cost of insurance. In practice, these mortality tables are used in conjunction with the health and family history of the individual applying for a policy in order to determine premiums and insurability. Mortality tables currently in use by life insurance companies in the United States are individually modified by each company using pooled industry experience studies as a starting point. In the 1980s and 90's the SOA 1975-80 Basic Select & Ultimate tables were the typical reference points, while the 2001 VBT and 2001 CSO tables were published more recently. The newer tables include separate mortality tables for smokers and non-smokers and the CSO tables include separate tables for preferred classes. [3]

Recent US select mortality tables predict that roughly 0.35 in 1,000 non-smoking males aged 25 will die during the first year of coverage after underwriting.[2] Mortality approximately doubles for every extra ten years of age so that the mortality rate in the first year for underwritten non-smoking men is about 2.5 in 1,000 people at age 65.

[3] Compare this with the US population male mortality rates of 1.3 per 1,000 at age 25 and 19.3 at age 65 (without regard to health or smoking status).[4]

The mortality of underwritten persons rises much more quickly than the general population. At the end of 10 years the mortality of that 25 year-old, non-smoking male is 0.66/1000/year. Consequently, in a group of one thousand 25 year old males with a $100,000 policy, all of average health, a life insurance company would have to collect approximately $50 a year from each of a large group to cover the relatively few expected claims. (0.35 to 0.66 expected deaths in each year x $100,000 payout per death = $35 per policy). Administrative and sales commissions need to be accounted for in order for this to make business sense. A 10 year policy for a 25 year old non-smoking male person with preferred medical history may get offers as low as $90 per year for a $100,000 policy in the competitive US life insurance market.

The insurance company receives the premiums from the policy owner and invests them to create a pool of money from which it can pay claims and finance the insurance company's operations. Contrary to popular belief, the majority of the money that insurance companies make comes directly from premiums paid, as money gained through investment of premiums can never, in even the most ideal market conditions, vest enough money per year to pay out claims. [citation needed]

Rates charged for life insurance increase with the insured's age because, statistically, people are more likely to die as they get older.

Given that adverse selection can have a negative impact on the insurer's financial situation, the insurer investigates each proposed insured individual unless the policy is below a company-established minimum amount, beginning with the application process. Group Insurance policies are an exception.

This investigation and resulting evaluation of the risk is termed underwriting. Health and lifestyle questions are asked. Certain responses or information received may merit further investigation. Life insurance companies in the United States support the Medical Information Bureau (MIB) [4], which is a clearinghouse of information on persons who have applied for life insurance with participating companies in the last seven years. As part of the application, the insurer receives permission to obtain information from the proposed insured's physicians.[5]

Underwriters will determine the purpose of insurance. The most common is to protect the owner's family or financial interests in the

event of the insured's demise. Other purposes include estate planning or, in the case of cash-value contracts, investment for retirement planning. Bank loans or buy-sell provisions of business agreements are another acceptable purpose.

Life insurance companies are never required by law to underwrite or to provide coverage to anyone, with the exception of Civil Rights Act compliance requirements. Insurance companies alone determine insurability, and some people, for their own health or lifestyle reasons, are deemed uninsurable. The policy can be declined (turned down) or rated.[citation needed] Rating increases the premiums to provide for additional risks relative to the particular insured.[citation needed]

Many companies use four general health categories for those evaluated for a life insurance policy. These categories are Preferred Best, Preferred, Standard, and Tobacco.[citation needed] Preferred Best is reserved only for the healthiest individuals in the general population. This means, for instance, that the proposed insured has no adverse medical history, is not under medication for any condition, and his family (immediate and extended) have no history of early cancer, diabetes, or other conditions.[citation needed] Preferred means that the proposed insured is currently under medication for a medical condition and has a family history of particular illnesses.[citation needed] Most people are in the Standard category.[citation needed] Profession, travel, and lifestyle factor into whether the proposed insured will be granted a policy, and which category the insured falls. For example, a person who would otherwise be classified as Preferred Best may be denied a policy if he or she travels to a high risk country.[citation needed] Underwriting practices can vary from insurer to insurer which provide for more competitive offers in certain circumstances.

Life insurance contracts are written on the basis of utmost good faith. That is, the proposer and the insurer both accept that the other is acting in good faith. This means that the proposer can assume the contract offers what it represents without having to fine comb the small print and the insurer assumes the proposer is being honest when providing details to underwriter.[citation needed]

[edit] Death proceeds

Upon the insured's death, the insurer requires acceptable proof of death before it pays the claim. The normal minimum proof required is a death certificate and the insurer's claim form completed, signed (and typically notarized).[citation needed] If the insured's death is suspicious and the policy amount is large, the insurer may investigate the

circumstances surrounding the death before deciding whether it has an obligation to pay the claim.

Proceeds from the policy may be paid as a lump sum or as an annuity, which is paid over time in regular recurring payments for either a specified period or for a beneficiary's lifetime.[citation needed]

[edit] Insurance vs. assurance

Outside the United States, the specific uses of the terms "insurance" and "assurance" are sometimes confused. In general, in these jurisdictions "insurance" refers to providing cover for an event that might happen, while "assurance" is the provision of cover for an event that is certain to happen. However, in the United States both forms of coverage are called "insurance".

When a person insures the contents of their home they do so because of events that might happen (fire, theft, flood, etc.) They hope their home will never be burglarized, or burn down, but they want to ensure that they are financially protected if the worst happens. This example of Insurance shows how it is a way of spending a little money to protect against the risk of having to spend a lot of money.

When a person insures their life they do so knowing that one day they will die. Therefore a policy that covers death is assured to make a payment. The policy offers assurance on death; even if the policy has a prescribed termination date the policy is still assured to pay on death and therefore is an assurance policy. Examples include Term Assurance and Whole Life Assurance. An accidental death policy is not assured to pay on death as the life insured may not die through an accident, therefore it is an insurance policy.

A policy might also be assured for other reasons. For example an endowment policy is designed to provide a lump sum on maturity. Under certain types of policy the lump sum is guaranteed. Therefore, this may also be called an assurance policy.

The test of whether a policy is assurance or insurance is that with an assurance policy the insured event will definitely occur (at some point) whereas with an insurance policy there is a risk the insured event might occur.

With regard to Whole Life policies, the question is not whether the insured event (in this case death) will occur, but simply when. If the policy has nonforfeiture values (or cash values) then the policy is assured to pay.

During recent years, the distinction between the two terms has become largely blurred. This is principally due to many companies offering both types of policy, and rather than refer to themselves using both insurance and assurance titles, they instead use just one.

Types of life insurance

Life insurance may be divided into two basic classes – temporary and permanent or following subclasses - term, universal, whole life, variable, variable universal and endowment life insurance.

Temporary (Term)

Term life insurance (term assurance in British English) provides for life insurance coverage for a specified term of years for a specified premium. The policy does not accumulate cash value. Term is generally considered "pure" insurance, where the premium buys protection in the event of death and nothing else. (See Theory of Decreasing Responsibility and buy term and invest the difference.) Term insurance premiums are typically low because both the insurer and the policy owner agree that the death of the insured is unlikely during the term of coverage.

The three key factors to be considered in term insurance are: face amount (protection or death benefit), premium to be paid (cost to the insured), and length of coverage (term).

Various (U.S.) insurance companies sell term insurance with many different combinations of these three parameters. The face amount can remain constant or decline. The term can be for one or more years. The premium can remain level or increase. A common type of term is called annual renewable term. It is a one year policy but the insurance company guarantees it will issue a policy of equal or lesser amount without regard to the insurability of the insured and with a premium set for the insured's age at that time. Another common type of term insurance is mortgage insurance, which is usually a level premium, declining face value policy. The face amount is intended to equal the amount of the mortgage on the policy owner’s residence so the mortgage will be paid if the insured dies.

A policy holder insures his life for a specified term. If he dies before that specified term is up, his estate or named beneficiary(ies) receive(s) a payout. If he does not die before the term is up, he receives nothing. In the past these policies would almost always exclude suicide. However, after a number of court judgments against the industry, payouts do occur on death by suicide (presumably except

for in the unlikely case that it can be shown that the suicide was just to benefit from the policy). Generally, if an insured person commits suicide within the first two policy years, the insurer will return the premiums paid. However, a death benefit will usually be paid if the suicide occurs after the two year period.

[edit] Permanent

Permanent life insurance is life insurance that remains in force (in-line) until the policy matures (pays out), unless the owner fails to pay the premium when due (the policy expires). The policy cannot be canceled by the insurer for any reason except fraud in the application, and that cancellation must occur within a period of time defined by law (usually two years). Permanent insurance builds a cash value that reduces the amount at risk to the insurance company and thus the insurance expense over time. This means that a policy with a million dollars face value can be relatively inexpensive to a 70 year old because the actual amount of insurance purchased is much less than one million dollars. The owner can access the money in the cash value by withdrawing money, borrowing the cash value, or surrendering the policy and receiving the surrender value.

The three basic types of permanent insurance are whole life, universal life, and endowment.

[edit] Whole life coverage

Whole life insurance provides for a level premium, and a cash value table included in the policy guaranteed by the company. The primary advantages of whole life are guaranteed death benefits, guaranteed cash values, fixed and known annual premiums, and mortality and expense charges will not reduce the cash value shown in the policy. The primary disadvantages of whole life are premium inflexibility, and the internal rate of return in the policy may not be competitive with other savings alternatives. Riders are available that can allow one to increase the death benefit by paying additional premium. The death benefit can also be increased through the use of policy dividends. Dividends cannot be guaranteed and may be higher or lower than historical rates over time. Premiums are much higher than term insurance in the short-term, but cumulative premiums are roughly equal if policies are kept in force until average life expectancy.

Cash value can be accessed at any time through policy "loans". Since these loans decrease the death benefit if not paid back, payback is optional. Cash values are not paid to the beneficiary upon the death of the insured; the beneficiary receives the death benefit only. If the

dividend option: Paid up additions is elected, dividend cash values will purchase additional death benefit which will increase the death benefit of the policy to the named beneficiary.

[edit] Universal life coverage

Universal life insurance (UL) is a relatively new insurance product intended to provide permanent insurance coverage with greater flexibility in premium payment and the potential for a higher internal rate of return. A universal life policy includes a cash account. Premiums increase the cash account. Interest is paid within the policy (credited) on the account at a rate specified by the company. This rate has a guaranteed minimum but usually is higher than that minimum. Mortality charges and administrative costs are charged against (reduce) the cash account. The surrender value of the policy is the amount remaining in the cash account less applicable surrender charges, if any.

With all life insurance, there are basically two functions that make it work. There's a mortality function and a cash function. The mortality function would be the classical notion of pooling risk where the premiums paid by everybody else would cover the death benefit for the one or two who will die for a given period of time. The cash function inherent in all life insurance says that if a person is to reach age 95 to 100 (the age varies depending on state and company), then the policy matures and endows the face value of the policy.

Actuarially, it is reasoned that out of a group of 1000 people, if even 10 of them live to age 95, then the mortality function alone will not be able to cover the cash function. So in order to cover the cash function, a minimum rate of investment return on the premiums will be required in the event that a policy matures.

Universal life policies guarantee, to some extent, the death proceeds, but not the cash function - thus the flexible premiums and interest returns. If interest rates are high, then the dividends help reduce premiums. If interest rates are low, then the customer would have to pay additional premiums in order to keep the policy in force. When interest rates are above the minimum required, then the customer has the flexibility to pay less as investment returns cover the remainder to keep the policy in force.

The universal life policy addresses the perceived disadvantages of whole life. Premiums are flexible. The internal rate of return is usually higher because it moves with the financial markets. Mortality costs and administrative charges are known. And cash value may be considered

more easily attainable because the owner can discontinue premiums if the cash value allows it. And universal life has a more flexible death benefit because the owner can select one of two death benefit options, Option A and Option B.

Option A pays the face amount at death as it's designed to have the cash value equal the death benefit at age 95. Option B pays the face amount plus the cash value, as it's designed to increase the net death benefit as cash values accumulate. Option B does carry with it a caveat. This caveat is that in order for the policy to keep its tax favored life insurance status, it must stay within a corridor specified by state and federal laws that prevent abuses such as attaching a million dollars in cash value to a two dollar insurance policy. The interesting part about this corridor is that for those people who can make it to age 95-100, this corridor requirement goes away and your cash value can equal exactly the face amount of insurance. If this corridor is ever violated, then the universal life policy will be treated as, and in effect turn into, a Modified Endowment Contract (or more commonly referred to as a MEC).

But universal life has its own disadvantages which stem primarily from this flexibility. The policy lacks the fundamental guarantee that the policy will be in force unless sufficient premiums have been paid and cash values are not guaranteed.

Universal life policies are sometimes erroneously referred to as self-sustaining policies. In the 1980s, when interest rates were high, the cash value accumulated at a more accelerated rate, and universal life coverage was often sold by agents as a policy that could be self-paying. Many policies did sustain themselves for a prolonged period, but the combination of lower interest rates and an increasing cost of insurance as the insured ages meant that for many policies, the cash option was diminished or depleted.

Variable universal life Insurance (VUL) is not the same as universal life, even though they both have cash values attached to them. These differences are in how the cash accounts are managed; thus having a great effect on how they are treated for taxation. The cash account within a VUL is held in the insurer's "separate account" (generally in mutual funds, managed by a fund manager).

Limited-pay

Another type of permanent insurance is Limited-pay life insurance, in which all the premiums are paid over a specified period after which no

additional premiums are due to keep the policy in force. Common limited pay periods include 10-year, 20-year, and paid-up at age 65.

Endowments

Endowments are policies in which the cash value built up inside the policy, equals the death benefit (face amount) at a certain age. The age this commences is known as the endowment age. Endowments are considerably more expensive (in terms of annual premiums) than either whole life or universal life because the premium paying period is shortened and the endowment date is earlier.

In the United States, the Technical Corrections Act of 1988 tightened the rules on tax shelters (creating modified endowments). These follow tax rules as annuities and IRAs do.

Endowment Insurance is paid out whether the insured lives or dies, after a specific period (e.g. 15 years) or a specific age (e.g. 65).

Accidental death

Accidental death is a limited life insurance that is designed to cover the insured when they pass away due to an accident. Accidents include anything from an injury, but do not typically cover any deaths resulting from health problems or suicide. Because they only cover accidents, these policies are much less expensive than other life insurances.

It is also very commonly offered as "accidental death and dismemberment insurance", also known as an AD&D policy. In an AD&D policy, benefits are available not only for accidental death, but also for loss of limbs or bodily functions such as sight and hearing, etc.

Accidental death and AD&D policies very rarely pay a benefit; either the cause of death is not covered, or the coverage is not maintained after the accident until death occurs. To be aware of what coverage they have, an insured should always review their policy for what it covers and what it excludes. Often, it does not cover an insured who puts themselves at risk in activities such as: parachuting, flying an airplane, professional sports, or involvement in a war (military or not). Also, some insurers will exclude death and injury caused by proximate causes due to (but not limited to) racing on wheels and mountaineering.

Accidental death benefits can also be added to a standard life insurance policy as a rider. If this rider is purchased, the policy will generally pay double the face amount if the insured dies due to an

accident. This used to be commonly referred to as a double indemnity coverage. In some cases, some companies may even offer a triple indemnity cover.

Related life insurance products

Riders are modifications to the insurance policy added at the same time the policy is issued. These riders change the basic policy to provide some feature desired by the policy owner. A common rider is accidental death, which used to be commonly referred to as "double indemnity", which pays twice the amount of the policy face value if death results from accidental causes, as if both a full coverage policy and an accidental death policy were in effect on the insured. Another common rider is premium waiver, which waives future premiums if the insured becomes disabled.

Joint life insurance is either a term or permanent policy insuring two or more lives with the proceeds payable on the first death.

Survivorship life or second-to-die life is a whole life policy insuring two lives with the proceeds payable on the second (later) death.

Single premium whole life is a policy with only one premium which is payable at the time the policy is issued.

Modified whole life is a whole life policy that charges smaller premiums for a specified period of time after which the premiums increase for the remainder of the policy.

Group life insurance is term insurance covering a group of people, usually employees of a company or members of a union or association. Individual proof of insurability is not normally a consideration in the underwriting. Rather, the underwriter considers the size and turnover of the group, and the financial strength of the group. Contract provisions will attempt to exclude the possibility of adverse selection. Group life insurance often has a provision that a member exiting the group has the right to buy individual insurance coverage.

Senior and preneed products

Insurance companies have in recent years developed products to offer to niche markets, most notably targeting the senior market to address needs of an aging population. Many companies offer policies tailored to the needs of senior applicants. These are often low to moderate face value whole life insurance policies, to allow a senior citizen purchasing insurance at an older issue age an opportunity to buy affordable

insurance. This may also be marketed as final expense insurance, and an agent or company may suggest (but not require) that the policy proceeds could be used for end-of-life expenses.

Preneed (or prepaid) insurance policies are whole life policies that, although available at any age, are usually offered to older applicants as well. This type of insurance is designed specifically to cover funeral expenses when the insured person dies. In many cases, the applicant signs a prefunded funeral arrangement with a funeral home at the time the policy is applied for. The death proceeds are then guaranteed to be directed first to the funeral services provider for payment of services rendered. Most contracts dictate that any excess proceeds will go either to the insured's estate or a designated beneficiary.

These products are sometimes assigned into a trust at the time of issue, or shortly after issue. The policies are irrevocably assigned to the trust, and the trust becomes the owner. Since a whole life policy has a cash value component, and a loan provision, it may be considered an asset; assigning the policy to a trust means that it can no longer be considered an asset for that individual. This can impact an individual's ability to qualify for Medicare or Medicaid.

Investment policies

With-profits policies

Some policies allow the policyholder to participate in the profits of the insurance company these are with-profits policies. Other policies have no rights to participate in the profits of the company, these are non-profit policies.

With-profits policies are used as a form of collective investment to achieve capital growth. Other policies offer a guaranteed return not dependent on the company's underlying investment performance; these are often referred to as without-profit policies which may be construed as a misnomer.

Insurance/Investment Bonds

Pensions

Pensions are a form of life assurance. However, whilst basic life assurance, permanent health insurance and non-pensions annuity business includes an amount of mortality or morbidity risk for the insurer, for pensions there is a longevity risk.

A pension fund will be built up throughout a person's working life. When the person retires, the pension will become in payment, and at some stage the pensioner will buy an annuity contract, which will guarantee a certain pay-out each month until death.

Annuities

An annuity is a contract with an insurance company whereby the purchaser pays an initial premium or premiums into a tax-deferred account, which pays out a sum at pre-determined intervals. There are two periods: the accumulation (when payments are paid into the account) and the annuitization (when the insurance company pays out). For example, a policy holder may pay £10,000, and in return receive £150 each month until he dies; or £1,000 for each of 14 years or death benefits if he dies before the full term of the annuity has elapsed. Tax penalties and insurance company surrender charges may apply to premature withdrawals (if indeed these are allowed; in most markets outside the U.S. the policy owner has no right to end the contract prematurely).

Tax and life insurance

Taxation of life insurance in the United States

Premiums paid by the policy owner are normally not deductible for federal and state income tax purposes.

Proceeds paid by the insurer upon death of the insured are not includible in taxable income for federal and state income tax purposes; however, if the proceeds are included in the "estate" of the deceased, it is likely they will be subject to federal and state estate and inheritance tax.

Cash value increases within the policy are not subject to income taxes unless certain events occur. For this reason, insurance policies can be a legal and legitimate tax shelter wherein savings can increase without taxation until the owner withdraws the money from the policy. On flexible-premium policies, large deposits of premium could cause the contract to be considered a "Modified Endowment Contract" by the IRS, which negates many of the tax advantages associated with life insurance. The insurance company, in most cases, will inform the policy owner of this danger before applying their premium.

Tax deferred benefit from a life insurance policy may be offset by its low return or high cost in some cases. This depends upon the insuring company, type of policy and other variables (mortality, market return,

etc.). Also, other income tax saving vehicles (i.e. IRA, 401K or Roth IRA) appear to be better alternatives for value accumulation, at least for more sophisticated investors who can keep track of multiple financial vehicles. The combination of low-cost term life insurance and higher return tax-efficient retirement accounts can achieve better performance, assuming that the insurance itself is only needed for a limited amount of time.

The tax ramifications of life insurance are complex. The policy owner would be well advised to carefully consider them. As always, Congress or the state legislatures can change the tax laws at any time.

Taxation of life assurance in the United Kingdom

Premiums are not usually allowable against income tax or corporation tax, however qualifying policies issued prior to 14 March 1984 do still attract LAPR (Life Assurance Premium Relief) at 15% (with the net premium being collected from the policyholder).

Non-investment life policies do not normally attract either income tax or capital gains tax on claim. If the policy has as investment element such as an endowment policy, whole of life policy or an investment bond then the tax treatment is determined by the qualifying status of the policy.

Qualifying status is determined at the outset of the policy if the contract meets certain criteria. Essentially, long term contracts (10 years plus) tend to be qualifying policies and the proceeds are free from income tax and capital gains tax. Single premium contracts and those run for a short term are subject to income tax depending upon your marginal rate in the year you make a gain. All (UK) insurers pay a special rate of corporation tax on the profits from their life book; this is deemed as meeting the lower rate (20% in 2005-06) liability for policyholders. Therefore if you are a higher rate taxpayer (40% in 2005-06), or become one through the transaction, you must pay tax on the gain at the difference between the higher and the lower rate. This gain may be reduced by applying a complicated calculation called top-slicing based on the number of years you have held the policy.

Although this is complicated, the taxation of life assurance based investment contracts may be beneficial compared to alternative equity based collective investment schemes (unit trusts, investment trusts and OEICs). One feature which especially favors investment bonds is the ability to draw 5% of the original investment amount each policy year without being subject to any taxation on the amount withdrawn. The withdrawal is deemed by HMRC (Her Majesty's Revenue and

Customs) to be a payment of capital and therefore the tax calculation is deferred until further encashment above the 5% limit. This is an especially useful tax planning tool for higher rate taxpayers who expect to become basic rate taxpayers at some predictable point in the future (e.g. retirement).

The proceeds of a life policy will be included in the estate for inheritance tax (IHT) purposes. Policies written in trust may fall outside the estate for IHT purposes but it's not always that simple. If in doubt you should seek profession advice from an IFA (Independent Financial Adviser) who is registered with the government regulator: the Financial Services Authority.

Pension Term Assurance

Although available before April 2006, from this date pension term assurance became widely available in the UK. Most UK product providers adopted the name "life insurance with tax relief" for the product. Pension term assurance is effectively normal term life assurance with tax relief on the premiums. All premiums are paid net of basic rate tax at 22%, and higher rate tax payers can gain an extra 18% tax relief via their tax return. Although not suitable for all, PTA briefly became one of the most common forms of life assurance sold in the UK until the Chancellor, Gordon Brown, announced the withdrawal of the scheme in his pre-budget announcement on 6 December 2006. The tax relief ceased to be available to new policies transacted after 6 December 2006, however, existing policies have been allowed to continue to enjoy tax relief so far.

History

Insurance began as a way of reducing the risk of traders, as early as 5000 BC in China and 4500 BC in Babylon. Life insurance dates only to ancient Rome; "burial clubs" covered the cost of members' funeral expenses and helped survivors monetarily. Modern life insurance started in late 17th century England, originally as insurance for traders: merchants, ship owners and underwriters met to discuss deals at Lloyd's Coffee House, predecessor to the famous Lloyd's of London.

The first insurance company in the United States was formed in Charleston, South Carolina in 1732, but it provided only fire insurance. The sale of life insurance in the U.S. began in the late 1760s. The Presbyterian Synods in Philadelphia and New York created the Corporation for Relief of Poor and Distressed Widows and Children of Presbyterian Ministers in 1759; Episcopalian priests organized a similar fund in 1769. Between 1787 and 1837 more than two dozen life

insurance companies were started, but fewer than half a dozen survived.

Prior to the American Civil War, many insurance companies in the United States insured the lives of slaves for their owners. In response to bills passed in California in 2001 and in Illinois in 2003, the companies have been required to search their records for such policies. New York Life for example reported that Nautilus sold 485 slaveholder life insurance policies during a two-year period in the 1840s; they added that their trustees voted to end the sale of such policies 15 years before the Emancipation Proclamation.

Market trends

Life insurance premiums written in 2005

According to a study by Swiss Re, EU was the largest market for life insurance premiums written in 2005 followed by the USA and Japan.

] Criticism

Although some aspects of the application process (such as underwriting and insurable interest provisions) make it difficult, life insurance policies have been used in cases of exploitation and fraud. In the case of life insurance, there is a motivation to purchase a life insurance policy, particularly if the face value is substantial, and then kill the insured.

The television series Forensic Files has included episodes that feature this scenario. There was also a documented case in 2006, where two elderly women are accused of taking in homeless men and assisting them. As part of their assistance, they took out life insurance on the men. After the contestability period ended on the policies (most life contracts have a standard contestability period of two years), the women are alleged to have had the men killed via hit-and-run car crashes.[6]

Recently, viatical settlements have thrown the life insurance industry into turmoil. A viatical settlement involves the purchase of a life insurance policy from an elderly or terminally ill policy holder. The policy holder sells the policy (including the right to name the beneficiary) to a purchaser for a price discounted from the policy value. The seller has cash in hand, and the purchaser will realize a profit when the seller dies and the proceeds are delivered to the purchaser. In the meantime, the purchaser continues to pay the

premiums. Although both parties have reached an agreeable settlement, insurers are troubled by this trend. Insurers calculate their rates with the assumption that a certain portion of policy holders will seek to redeem the cash value of their insurance policies before death. They also expect that a certain portion will stop paying premiums and forfeit their policies. However, viatical settlements ensure that such policies will with absolute certainty be paid out. Some purchasers, in order to take advantage of the potentially large profits, have even actively sought to collude with uninsured elderly and terminally ill patients, and created policies that would have not otherwise been purchased. Likewise, these policies are guaranteed losses from the insurers' perspective.

Related Documents