ReportNo. 16506-IN India 1997 EconomicUpdate: Sustaining RapidGrowth May 30, 1997 Country Operations, Industry & Finance Division Country Department II South Asia Region U Document Of the wormd Bank Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Report No. 16506-IN

India1997 Economic Update:Sustaining Rapid GrowthMay 30, 1997

Country Operations, Industry & Finance DivisionCountry Department IISouth Asia Region

U

Document Of the wormd Bank

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

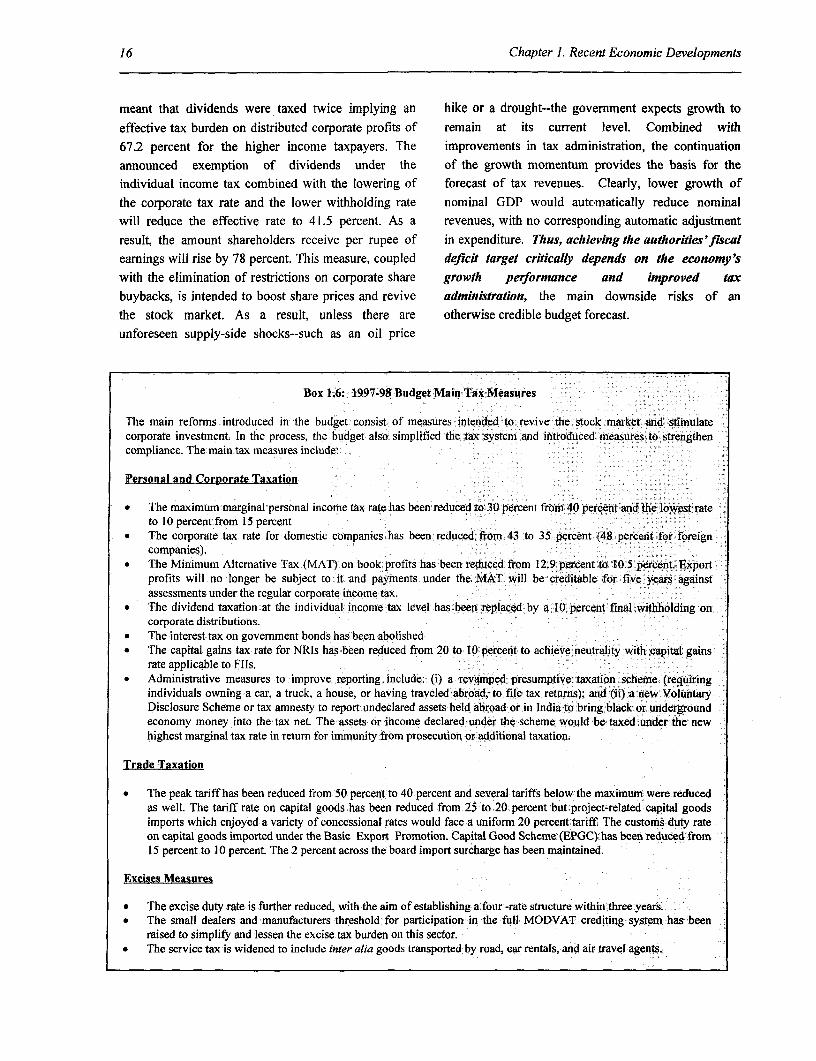

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

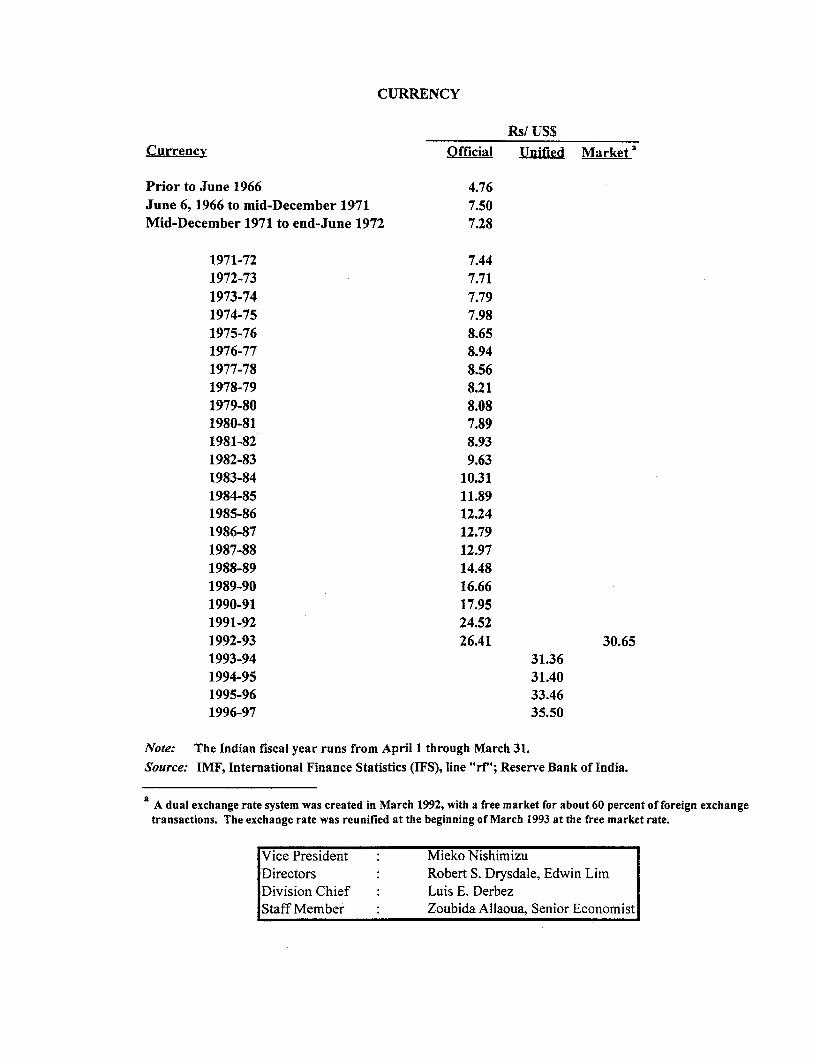

CURRENCY

Rs/ US$Currency Official Unified Market a

Prior to June 1966 4.76June 6, 1966 to mid-December 1971 7.50Mid-December 1971 to end-June 1972 7.28

1971-72 7.441972-73 7.711973-74 7.791974-75 7.981975-76 8.651976-77 8.941977-78 8.561978-79 8.211979-80 8.081980-81 7.891981-82 8.931982-83 9.631983-84 10.311984-85 11.891985-86 12.241986-87 12.791987-88 12.971988-89 14.481989-90 16.661990-91 17.951991-92 24.521992-93 26.41 30.651993-94 31.361994-95 31.401995-96 33.461996-97 35.50

Note: The Indian fiscal year runs from April 1 through March 31.Source: IMF, International Finance Statistics (IFS), line "rf"; Reserve Bank of India.

A dual exchange rate system was created in March 1992, with a free market for about 60 percent of foreign exchangetransactions. The exchange rate was reunified at the beginning of March 1993 at the free market rate.

Vice President Mieko NishimizuDirectors Robert S. Drysdale, Edwin LimDivision Chief Luis E. DerbezStaff Member Zoubida Allaoua, Senior Economist

ABBREVIATIONS AND ACRONYMS

BE Budget Estimates MPBF Maximum Permissible Bank FinanceBOLT Build-Operate-Lease-Transfer MTM Mark to MarketBOP Balance of Payments MTO Multimodal Transport servicesBOO Build-Won-Operate MUV Manufactures Unit ValueBOT Build-Operate-Transfer MW MegawattBSE Bombay Stock Exchange NBFCs Non Bank Financial CompaniesCEA Central Electricity Authority NCAER National Council of Applied EconomicCEM Country Economic Memorandum ResearchCERC Central Electricity Regulatory Commission NFA Net Financial AssetsCFS Container Freight Station NHAI National Highways Authority of IndiaCGE Computable General Equilibrium NPV Net Present ValueCMNAP Common Minimum National Action Plan NRER(A) Non-Resident External Rupee AccountCMP Common Minimum Program NSE National Stock ExchangeCONCOR Container Corporation of India NTB Non-Tariff BarriersCRR Cash Reserve Requirement NTPC National Thermal Power CorporationCSO Central Statistical Organization O&M Overhaul and MaintenanceDOT Department of Telecommunications OCC Oil Coordination CommitteeDRS Debt Reporting System OECD Organization for Economic CooperationEAS Employment Assurance Scheme and DevelopmentECB Euro-Convertible Bond OTCEI Over-the-Counter ExchangeEU European Union (formerly the EC) ONGC Oil and Natural Gas CorporationFCI Food Corporation of India PD Primary DealersFCNRA Foreign Currency (Non-Resident) Accounts PDS Public Distribution SystemFDI Foreign Direct Investment PE Public Enterprise/Fll Foreign Institutional Investor PLF Plant Load FactorFIPB Foreign Investment Promotion Board PLR Prime Lending RateGATT General Agreement on Tariffs and Trade POL Petroleum, Oil and LubricantsGDP Gross Domestic Product PPP Purchasing Power ParityGDR Global Depository Receipts PRI Panchayati Raj InstitutionsGNFS Goods and Non-factor Services PWD Public Works DepartmentGNP Gross National Product R&D Research and DevelopmentGOI Government of India RBI Reserve Bank of IndiaHSEB Haryana State Electricity Board RE Revised EstimatesHUDCO Housing and Urban Development REB Regional Electricity Board

Corporation RER Real Exchange RateHYV High Yielding Varieties REER Real Effective Exchange RateICD Inland Container Depot RLDC Regional Load Dispatch CenterICDS Integrated Child Development Scheme RRB Rural Regional BankICICI Industrial Credit and Investment SAIL Steel Authority of India Ltd.

Corporation of India SBI State Bank of IndiaIDBI Industrial Development Bank of India SC Scheduled CastesIDF Indian Development Forum SCICI Shipping Credit and InvestmentIDFC Infrastructure Development Finance Corporation of India

Company SDP State Domestic ProductIFCl Industrial Financial Corporation of India SDR Special Drawing RightsIGIDR Indira Gandhi Institute for Development SEB State Electricity Board

Research SEBI Security and Exchange Board of IndialIP Index of Industrial Production SERC State Electricity Regulatory CommissionIMF International Monetary Fund SICA Sick Industrial Companies ActIOC Indian Oil Corporation SIL Special Import LicenseIPP Independent Power Producers SITC Standard Industrial Trade ClassificationIRDP Integrated Rural Development Program SLR Statutory Liquidity RequirementsISO International Standards Organization SSA Sub-Saharan AfricaJRY Jawahar Rozgar Yojana SSI Small Scale IndustryKwh Kilowatt-hour ST Scheduled TribesLAC Latin America and the Caribbean STCI Securities Trading Corporation of IndiaMAT Minimum Alternative Tax TFC Tenth Finance CommissionMFA Multifiber Agreement TOT Terms of TradeMFIL Mahindra Ford India Limited TRAI Telecom Regulatory Authority of IndiaMMMF Money Market Mutual Fund TRIPS Traded Intellectual Property RightsMODVAT Modified Value Added Tax UP Uttar PradeshMOF Ministry of Finance UT Union TerritoryMOP Ministry of Power VAT Value Added TaxMOST Ministry of Surface Transport WPI Wholesale Price IndexMOU Memorandum of Understanding WTO World Trade Organization

CONTENTS

CurrencyAbbreviations and AcronymsAcknowledgmentsEconomic Development DateExecutive Summary

Chapter 1 Recent Economic Developments ........................................................................ I

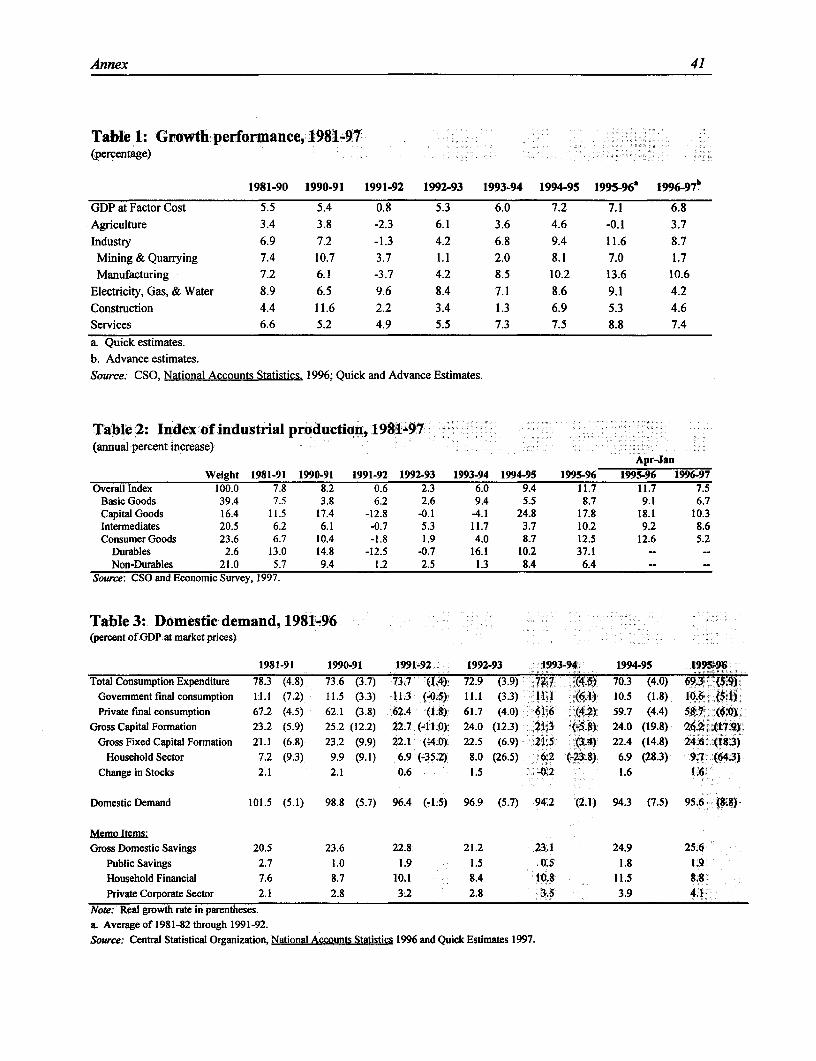

A. Recent Economic Developments ...................................................................... 1IA strong supply response ...................................................................... 1IStrong saving and investment performance .................................................................... 2Fiscal developments remain a serious concern ............................................................... 2Monetary policy eased but inflation remains moderate ...................... ............................3Exports and imports growth slowed down; the external accounts remain strong ...........5

B. Highlights of Structural Reformns ....................................................................... 6Increase in competition ....................................................................... 6Structural reforms have continued in 1996-97 ................................................................ 9Agriculture is becoming a focus of reform ................................................................... 14

C. Economic Management Issues ...................................................................... 14Possible slow down in investment and growth ............................................................. 16The 1997-98 budget: a creative but fiscally risky supply-side initiative ...................... 16Fiscal adjustment in the 1997-98 budget ...................................................................... 18Fiscal vulnerabilities ...................................................................... 18External account vulnerabilities ....................................................................... 21

Chapter 2 Changing States' Development Policies ....................................................................... 21

A. States Issues: A Summing Up ...................... ................................................. 21India's pre- 1991 development strategy and inter-government transfers have

shaped the states' development policies .................................................................. 21Some aspects of the system of transfers have discouraged states' fiscal discipline ...... 23The states face three crises--fiscal, infrastructure, human resources development ....... 24

B. State Reforms: Priorities and Progress ...................................................................... 28Reforming infrastructure policies ....................................................................... 28Restructuring states' public expenditures ..................................................................... 31Strengthening resource mobilization ...................................................................... 32Improving inter-governmental transfers ...................................................................... 32

Chapter 3 Sustaining Rapid Growth ...................................................................... 33

A. Policy Priorities ....................................................................... 33B. External Prospects and Financing ...................................................................... 36

Annex ....................................................................... 39

Statistical Appendix ...................................................................... 55

List of Tables

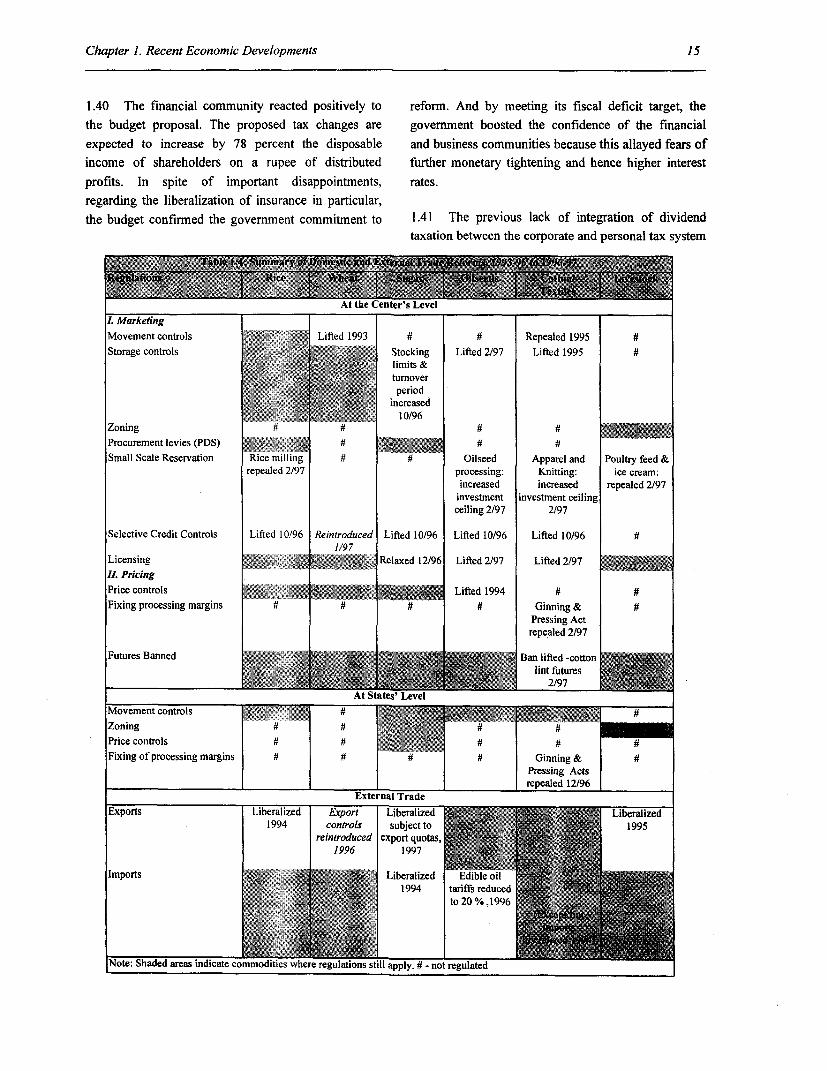

Table 1.1 Evolution of the Public Deficit, 1990-97 .................................................... 2Table 1.2 Merchandise Export and Import Slowdown, 1995-1996 ................................................ 5Table 1.3 Industrial Disputes: 1981-85 to 1995-96 ..................................................... 9Table 1.4 Summary of Domestic and External Trade Reforms, 1995-96 to IS197-98 .................. 15

Table 2.1 India - State Profiles, 1995-96 .................................................... 22Table 2.2 Central Plan Loans as a Percentage of Plan Capital Expenditure of States .................. 25

List of Boxes

Box 1.1 The High Cost of Government Subsidies ..................................................... 3Box 1.2 The Automobile Industry's Response to Liberalization ................................................ 7Box 1.3 State Bank of India (SBI) Responds to Competition ..................................................... 8Box 1.4 Improving Corporate Governance in India ..................................................... 8Box 1.5 Non-Bank Financial Companies .................................................... 13Box 1.6 1997-98 Budget Main Tax Measures .................................................... 17Box 1.7 The Targeted Public Distribution System .................................................... 19

Box 2.1 Reforms in Rajasthan .................................................... 27Box 2.2 Establishing Fiscal Sustainability in Andhra Pradesh ................................................... 28Box 2.3 State Power Reforms: A Beginning .................................................... 29Box 2.4 The December 1996 Common Minimum National Action Plan for ]?ower .................. 30Box 2.5: Haryana Sees the Benefits of Reform .................................................... 31

List of Figures

Figure 1.1 Economic Growth .................................................... IFigure 1.2 Trends in manufacturing Growth ..................................................... 2Figure 1.3 Trends in Savings ..................................................... 2Figure 1.4 Gross Domestic Investment ..................................................... 3Figure 1.5 Money Supply ..................................................... 4Figure 1.6 Inflation Rates ......... . . . . ... . . 4Figure 1.7 Year to Date Nominal export Growth, 1991-1996 .......................................... 5Figure 1.8 Export Growth, 1990-1996 .......................................... 5Figure 1.9 Exchange Rate Movements .......................................... 5Figure 1.10 Foreign Investment .......................................... 6Figure 1.11 Funds Raised by the Financial Institutions During 1995-96 ......................................... 12Figure 1.12 Non-Perforrming Advances ......................................... 14Figure 1.13 Trends in the Stock Markets ..................................... 16

Figure 2.1 Net Transfers to States as a Percent of GDP ..................................... 24Figure 2.2 Key Components of State Governments' Expenditure ..................................... 24Figure 2.3 States' Debt vrs Per-capaita Income ..................................... 32

Figure 3.1 Debt and Non-Debt Flows ..................................... 38

ACKNOWLEDGMENTS

This report was prepared by a team led by Tzanninis and Martin Muhleisen (IMF).Zoubida Allaoua. It draws on contributions Primary statistical and computationalfrom Mona Haddad, William Mccarten, V.J. assistance was received from Bhaskar NaiduRavishankar (state issues, fiscal), Miria and Rajni Khanna. The report benefitted fromPigato and Uri Dadush (external sectors), Luis Ernesto Derbez (Division Chief)Dina Umali-Deininger (agriculture), Joelle continuous support.Chassard, Kari Nyman, Djamal Mostefai(power), Harald Hansen (transport). Roberto The report benefitted from and reflectsZagha (Lead Economist) contributed to the discussions held with the Indian authorities inreport and provided guidance. Rui Coutinho May 1997. We gratefully acknowledge thewho participated in the discussions with the cooperation of government officials, the RBI,government also provided invaluable and members of the business community forassistance. The report benefited from their valuable time and assistance.comments from John Williamson (ChiefEconomist), Luis Serven (reviewer), Colin Arrangements for mission to India were madeBruce, Sanjay Kathuria, Benoit Blarel, Keith by Padma Gopalan and Sheni Rana. TheHinchliff, James Hanson, and Dimitri report was desktoped by Lin Chin.

ECONOMIC DEVELOPMENT DATA

GNP Per Capita (US$, 1995-96): 350'

Gross Domestic Product (1995-96)

Annual Growth Rate (% p.a, constant prices)% of 70-71- 75-76- 80-81- 85-86- 91-92 92-93-

US$ Bln GDP 75-76 80-81 85-86 90-91 95-96GDP at Factor Cost 294.6 89.7 3.4 4.2 5.4 5.9 0.8 6.4GDP at Market Prices 328.3 100.0 3.3 4.2 5.6 6.2 0.4 6.3GrossDomesticlnvestment 86.1 26.2 5.3 3.7 5.7 9.5 -11.0 12.8Gross National Saving 79.8 24.3 4.4 2.6 3.5 8.7 -0.3 10.7Current Account Balance -6.4 -1.9 -- - -- -- -- --

Output, Employment and Productivity (1990-91)

Value Added Labor Force b V. A. per WorkerUS$ Bln. % of Tot Mill. % of Tot. US$ % of Avg.

Agriculture 82.5 31.0 186.2 66.8 443 46.4Industry 78.0 29.3 35.5 12.7 2198 230.2Services 105.7 39.7 57.2 20.5 1848 193.7Total/ Average 266.2 100.0 278.9 100.0 954 100.0

Government Finance

General Government Central GovernmentRs. Bin. % of GDP Rs. Bln. % of GDP95-96 95-96 90-91-95-96 95-96 95-96 90-91-95-96

RevenueReceipts 2174.1 19.8 19.6 1101.3 10.0 10.1Revenue Expenditures 2539.5 23.1 23.3 1398.6 12.7 13.2Revenue Surplus/ Deficit (-) -365.3 -3.3 -3.7 -297.3 -2.7 -3.1

Capital Expenditures d 416.2 3.8 4.2 305.1 2.8 3.4

External Assistance (net) e 3.2 0.0 0.6 3.2 0.0 0.6

Money, Credit, and Prices

89-90 90-91 91-92 92-93 93-94 94-95 95-96(Rs. billion outstanding, end of period)

Money and Quasi Money 2309.5 2658.3 3170.5 3668.3 4344.1 5308.0 6018.4Bank Credit to Govermnent (net) 1171.5 1401.9 1582.6 1762.4 2039.2 2224.2 2574.1Bank Credit to Commercial Sector 1517.0 1717.7 1879.9 2201.4 2377.7 2896.6 3409.0

(percentage or index numbers)Money and Quasi Money as % of GDP 50.6 49.6 51.4 52.0 53.7 55.7 54.8Wholesale Price Index (1981-82 = 100) 165.7 182.7 207.8 228.7 247.8 274.7 294.8

Annual Percentage Changes in:Wholesale Price Index 7.4 10.3 13.7 10.1 8.4 10.9 7.3Bank Credit to Government (net) 20.3 19.7 12.9 11.4 15.7 9.1 15.7Bank Credit to Commercial Sector 14.4 13.2 9.4 17.1 8.0 21.8 17.7

a The per capita GNP estimate is at market prices, using World Bank Atlas methodology. Other conversions to dollars in thistable are at the prevailing average exchange rate for the period covered.

b. Total Labor Force from 1991 Census. Excludes data for Assam and Jammu & Kashmir.c. Transfers between Centre and States have been netted out.d. All loans and advances to third parties have been netted out.e. As recorded in the government budget.

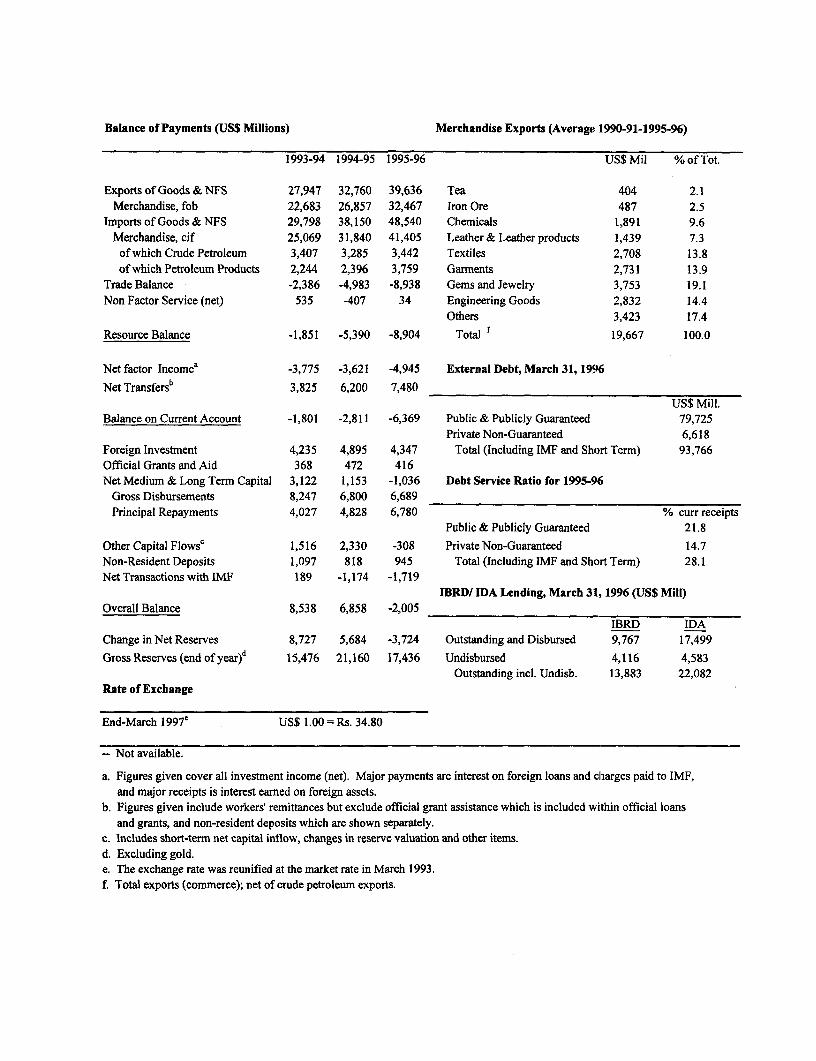

Balance of Payments (US$ Millions) Merchandise Exports (Average 1990-91-1995-96)

1993-94 1994-95 1995-96 US$ Mil % of Tot.

Exports of Goods & NFS 27,947 32,760 39,636 Tea 404 2.1Merchandise, fob 22,683 26,857 32,467 Iron Ore 487 2.5

Imports of Goods & NFS 29,798 38,150 48,540 Chemicals 1,891 9.6Merchandise, cif 25,069 31,840 41,405 Leather & Leather products 1,439 7.3

of which Crude Petroleum 3,407 3,285 3,442 Textiles 2,708 13.8of which Petroleum Products 2,244 2,396 3,759 Garments 2,731 13.9

Trade Balance -2,386 -4,983 -8,938 Gems and Jewelry 3,753 19.1Non Factor Service (net) 535 -407 34 Engineering Goods 2,832 14.4

Others 3,423 17.4

Resource Balance -1,851 -5,390 -8,904 Total 19,667 100.0

Net factor Incomea -3,775 -3,621 -4,945 External Debt, March 31, 1996

Net Transfersb 3,825 6,200 7,480US$ Mill.

Balance on Current Account -1,801 -2,811 -6,369 Public & Publicly Guaranteed 79,725Private Non-Guaranteed 6,618

Foreign Investment 4,235 4,895 4,347 Total (Including IMF and Short Term) 93,766Official Grants and Aid 368 472 416Net Medium & Long Term Capital 3,122 1,153 -1,036 Debt Service Ratio for 1995-96

Gross Disbursements 8,247 6,800 6,689Principal Repayments 4,027 4,828 6,780 % curr receipts

Public & Publicly Guaranteed 21.8

Other Capital Flowsc 1,516 2,330 -308 Private Non-Guaranteed 14.7Non-Resident Deposits 1,097 818 945 Total (Including IMF and Short Term) 28.1Net Transactions with IMF 189 -1,174 -1,719

IBRD/ IDA Lending, March 31, 1996 (US$ Mill)Overall Balance 8,538 6,858 -2,005

IBRD IDAChange in Net Reserves 8,727 5,684 -3,724 Outstanding and Disbursed 9,767 17,499

Gross Reserves (end of yeard 15,476 21,160 17,436 Undisbursed 4,116 4,583Outstanding incl. Undisb. 13,883 22,082

Rate of Exchange

End-March 1997e US$ 1.00 = Rs. 34.80

- Not available.

a. Figures given cover all investment income (net). Major payments are interest on foreign loans and charges paid to IMF,and major receipts is interest earned on foreign assets.

b. Figures given include workers' remittances but exclude official grant assistance which is included within official loansand grants, and non-resident deposits which are shown separately.

c. Includes short-term net capital inflow, changes in reserve valuation and other items.d. Excluding gold.e. The exchange rate was reunified at the market rate in March 1993.f Total exports (commerce); net of crude petroleum exports.

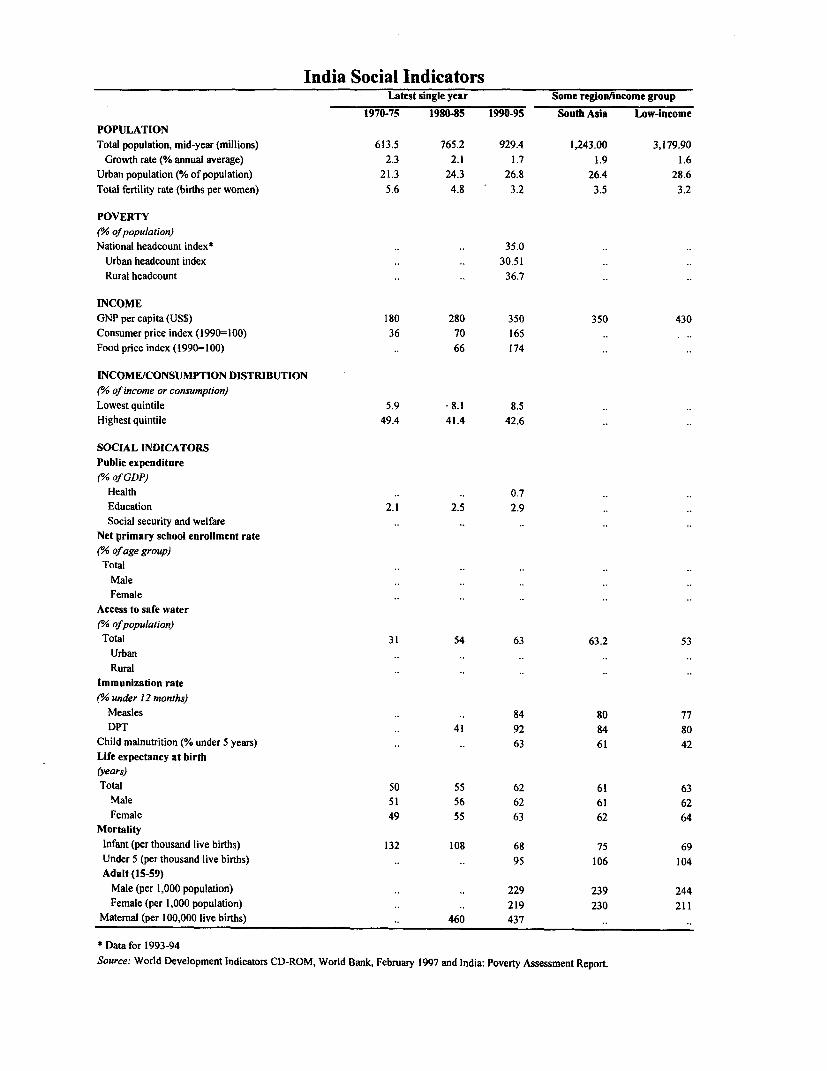

India Social IndicatorsLatest single year Some region/income group

1970-75 198045 1990-95 South Asia Low-income

POPULATIONTotal population, mid-year (millions) 613.5 765.2 929.4 1,243.00 3,179.90

Growth rate (% annual average) 2.3 2.1 1.7 1.9 1.6

Urban population (% of population) 21.3 24.3 26.8 26.4 28.6

Total fertility rate (births per women) 5.6 4.8 3.2 3.5 3.2

POVERTY('% of population)

National headcount index* .. .. 35.0

Urban headcount index .. .. 30.51

Rural headcount .. .. 36.7

INCOMEGNP per capita (US$) 180 280 350 350 430

Consumer price index (1990=100) 36 70 165

Food price index (1990=100) .. 66 174

INCOME/CONSUMPTION DISTRIBUTION

(% of income or consumption)Lowest quintile 5.9 -8.1 8.5

Highest quintile 49.4 41.4 42.6

SOCIAL INDICATORSPublic expenditure

(l% of GDP)Health .. .. 0.7

Education 2.1 2.5 2.9

Social security and welfare

Net primary school enrollment rate(3/ of age group)Total

MaleFemale

Access to safe water('/o of population)Total 31 54 63 63.2 53

UrbanRural

Immunization rate

(% under 12 months)Measles .. .. 84 80 77

DPT .. 41 92 84 80

Child malnutrition (% under 5 years) .. .. 63 61 42

Life expectancy at birth(years)

Total 50 55 62 61 63

Male 51 56 62 61 62

Female 49 55 63 62 64

MortalityInfant (per thousand live births) 132 108 68 75 69

Under 5 (per thousand live births) .. .. 95 106 104

Adult (15-59)Male (per 1,000 population) , 229 239 244

Female (per 1,000 population) .. .. 219 230 211

Maternal (per 100,000 live births) .. 460 437

* Data for 1993-94

Source: World Development Indicators CD-ROM, World Bank, February 1997 and India: Poverty Assessment Report.

EXECUTIVE SUMMARY

1. A number of reports issued in 1996-97 (the reduction of the central government fiscal deficit,Ministry of Finance's Economic Survey; the Reserve consolidated fiscal imbalances remain serious,Bank of India's (RBI) Annual Report; the RBI Report however, and excessively slow progress is being madeon Currency and Finance; the RBI Report on Trend to correct them. A May 1997 government paper showsand Progress of Banking in India; the India that implicit and explicit subsidies for "non-merit"Development Report (IGIDR); the government goods absorb an alarming 11 percent of GDP and are aappointed Expert Group Report on Infrastructure; the major factor behind India's chronically high fiscal1997-98 Budget speech; the RBI April Credit Policy; deficits. Inflation has increased moderately (fromand the May 1997 Ministry of Finance's discussion below 5 percent in May 1996 to 6 percent in Maypaper on government subsidies) document 1997, point-to-point), partly the result of a morecomprehensively India's past and recent performance, expansionary monetary stance (broad money growtharticulate the governments' development objectives, accelerated from 13.7 percent to 15.6 percent).and provide an accurate picture of the policychallenges the country faces. Because of the 3. Underlying the economy's strong economiccomprehensiveness and depth of this documentation to performance are important structural transformations.which interested readers are referred to, this report The declining role of the public sector since the start ofcomments only on salient recent economic and policy the reform program in 1991, both as producer of goodsdevelopments. and services and economic regulator, is one of India's

most fundamental structural change sinceThe Economy is Stronger and More Independence. The liberalization of the economy has

Competitive opened to the private sector areas previously the

exclusive domain of the public sector--such as heavy2. The reforms of the past six years brought manufacturing, banking, civil aviation,about an unprecedented strong economic telecommunications, power generation andperformance. For the third year in a row, GDP is distribution, ports, and roads. Equally important, theestimated to have grown by about 7 percent in the liberalization of the economy has reduced distortionsfiscal year 1996-97 ending on March 31, placing India and increased external and internal competition.among the world's best performing economies. Unlikesimilar episodes in the past, this expansion has been 4. In agriculture, the sector's terms of trade havedriven by private investment (which reached the improved. As a result, agricultural commodities havehistorically high level of 18 percent of GDP out of a been one of India's fastest growing exports, andtotal investment of 26 percent in the last two years), commercial crops are expanding rapidly. In Industy,and has not put pressure on the balance of payments. In firms are restructuring and entering into joint venturesspite of the persistent poor performance of public and alliances with foreign firms. Productivity hassavings, national savings have risen (from 23 percent increased and consumers have a wider range of betterof GDP in 1991-92 to 26 percent of GDP in 1996-97). quality goods from which to choose. ImportantThe country's external position is strong. The current legislative changes, deregulation, and foreign investorsaccount deficit was 1.1 percent of GDP in 1996-97; the are improving corporate governance of industrial andcountry's US$94 billion external debt declined to 27 financial firms. The regulatory and institutionalpercent of GDP in 1996-97 from 34 percent in 1991- framework of the ftnancial sector has been92, and the debt service to 24 percent of current strengthened considerably. In the banking system,account receipts from 29 percent. In spite of the although still vulnerable, the financial health of the

ii Executive Summary

public banks has improved and 19 out of the 27 public with some degree of success, particularly in bridges.sector banks reached the capital adequacy ratio of 8 Also, legislative changes have been announced topercent in 1995-96. The entry of new private banks and facilitate land acquisition--an irnportant impediment tothe mainstreaming of Non-Bank Finance Companies private investment in roads. In power, where the need(NBFCs) in a financial sector still dominated by public is the greatest, private sector interest to invest thebanks (which control 85 percent of the system's assets) strongest, and action by state governments essential tohave increased competition and forced the latter to transform this interest into concrete investments, areduce costs, and improve quality of service. Similar conference of state Chief Ministers reached agreementdevelopments have taken place in civil aviation. In on a Common Minimum National Action Plan for

infrastructure, while much too slowly to address Power (CMNAP) reforms, issued by the Ministry ofIndia's infrastructure crisis, private investrnent is Power in December 1996. Much of the CMNAP hastaking place in ports, power, and toll bridges. A new been inspired by the pioneering reforms Orissa startedfinancial institution (IDFC) has been established to a few years ago. The CMNAP envisages changes infacilitate the development of a long-term rupee bond legislation to enable the states to have their ownmarket for infrastructure financing. Last but not least, independent power regulatory agencies, with authorityincreased competition in product markets has led to an to grant licenses including for distribution, and fiximprovement in industrial relations with a consequent tariffs. This would remove the main impediments to

decline in labor disputes. large scale private investment in a sector that needs iturgently. Some states are giving the CMNAP's

5. Reforms have continued during 1996-97 in recommendations serious consiideration and taken stepsspite of political uncertainty. The positive effects of towards their implementation. In coal, major reformsthe reforms have demonstrated the extent to which have freed imports from licensing restrictions, reducedIndia stands to gain from deregulation and better fiscal tariffs to 5-10 percent, pursued the liberalization ofmanagement, and have helped create some consensus private investment in the sector, lifted price controls onon the need to continue liberalizing the economy and high grade coal and will lift the remaining restrictionscorrecting fiscal imbalances. This may explain why, over the next 2-3 years. Also, a decision was taken tonotwithstanding three changes of government of very divest shares in Coal India's subsidiaries.diverse political backgrounds, reforms have continuedin 1996-97 and expanded into some new areas, albeit at 7. This progress notwithstanding, it is evident thata rate that can be seen as excessively gradual. the induction of private capital in areas which for

decades have been under publjic sector monopoly has6. The investment regime has been liberalized been slower than anticipated, and so have its results.further, with particular emphasis on foreign Unless investment in infrastructure expandsinvestment--approval procedures have been simplified significantly, India's emerging infrastructure crisis mayand restrictions on end-use relaxed. Announced a few prevent the country from sustaining the high levels ofyears ago, the independent Telecom Regulatory growth that the last few years have shown to be withinAuthority of India has started its operations. In the reach. In particular, remarkably little progress has beencase of major ports (regulated by the central made in addressing the fundamental policy andgovernment), an independent Tariff Authority was institutional changes (most of which under theestablished, guidelines have been issued for private exclusive purview of state authorities) needed toinvestment through BOT-type contracts. Several expand urban infrastructure and alleviate theprivate investments in minor ports (under the states' tremendous problems of India's fast growing cities.jurisdiction) have already taken place. In roads, while Water supply systems--rural and urban--continue to bethere is awareness in India that this is an area where the poorly managed by state-government institutions at apublic sector will retain a major role, attempts have high cost to the economy (the subsidy for irrigationbeen made nonetheless to facilitate private sector entry

Executive Summary iii

alone is close to 2 percent of GDP) and insufficient has promoted the National Securities Depositoryefforts are being made to attract private investment. Limited (NSDL) to facilitate scripless trading and the

National Clearing Corporation Limited (NCCL) to8. The liberalization of the *rade regime has guarantee all trade done on the NSE. Screen-basedcontinued. Tariff reductions announced in the 1997-98 trading has now been generalized to other exchanges.Budget presented to Parliament in February 1997 All transactions in debt securities, previously handledbrought the maximum rate down to 40 percent and the by brokers in an unregulated telephone market, areaverage import-weighted rate to 20 percent. The now done solely through the NSE which has emergedFinance Minister announced its intention to reduce it as the premier exchange for scripless trading in debt asfurther to East Asian levels. The new Exim Policy well as stock instruments. Finally, SEBI, the securitieseliminated licensing requirements for about one-sixth and exchange board of India, is strengthening itsof consumer goods (essentially, the only imports still oversight capacity and the transparency of capitalrestricted) and India has indicated its readiness to markets. It has introduced inter alia new and moreeliminate gradually the remaining licensing effective guidelines for public issues and takeovers.restrictions.

11. A key objective of the tax reform pursued by9. Several measures were taken also to the Center since 1991 has been to simplify and broadenstrengthen the banking system, increase banks' the base of the tax system by lowering rates,operational autonomy, and improve the functioning streamlining the rate structure, and improving taxof financial markets. Of particular importance, banks administration. Some of the most severe distortions ofare now required to mark to market 60 percent of their the tax system have been corrected. The 1997-98portfolios. Virtually all interest rates are now market Budget maintains the overall direction of tax reforms.determined with the exception of interest rates on In particular, it simplified India's tax system further,lending for amounts below Rs. 200,000, and on reduced import tariffs, and brought corporate anddeposits of below one year. Cash reserve requirements personal rates in line with those of East Asia. In thewere reduced from 14 percent of deposits in April process, the budget also seeks to improve the rules1996 to 10 percent in January 1997; reserve governing tax sharing between the central governmentrequirements on inter-bank liabilities have been and the states and strengthen compliance.abolished; regulations governing loan syndication andamounts of credit for working capital purposes have 12. There was also some progress in deregulatingbeen eliminated; and prudential regulations were agriculture. The strong response of agriculture totightened further. The elimination of CRR on inter- reforms created favorable conditions for thebank liabilities coupled with the RBI's rationalization government to re-introduce--after a 31-year hiatus--of its refinance rates into a single rate is expected to futures trading in cotton lint, jute and jute goods andhelp establish a reference interest rate which would partially lift restrictions on commodity trading such ashelp develop a yield curve and improve RBI's ability those on storage, credit and movement controls,to manage monetary and exchange rate policies. particularly for cotton and oUlseeds. Export quotas on

cotton and cotton yam were raised and the number of10. Regarding capital markets, the Depositories yam quota exemptions expanded. Sugar exportsAct was passed to provide the legal framework for the (subject to quotas) were decanalized in January 1997.dematerialization of securities and their secure transfer To boost rice exports, the government removed thethrough electronic book entry. The establishment of the minimum export price but declining government stocksmodem electronic securities exchange system, the led to the reimposition of the levy on rice millsNational Stock Exchange (NSE), transformed the exporting non-basmati rice. Recent liberalizationfunctioning of the stock markets in India by increasing measures notwithstanding, agriculture continues to betheir transparency through scripless trading. The NSE

iv Executive Summary

highly regulated by both central and state governments 15. The authorities responded to this situationat a high cost to the economy and the poor. through a number of measures taken at different points

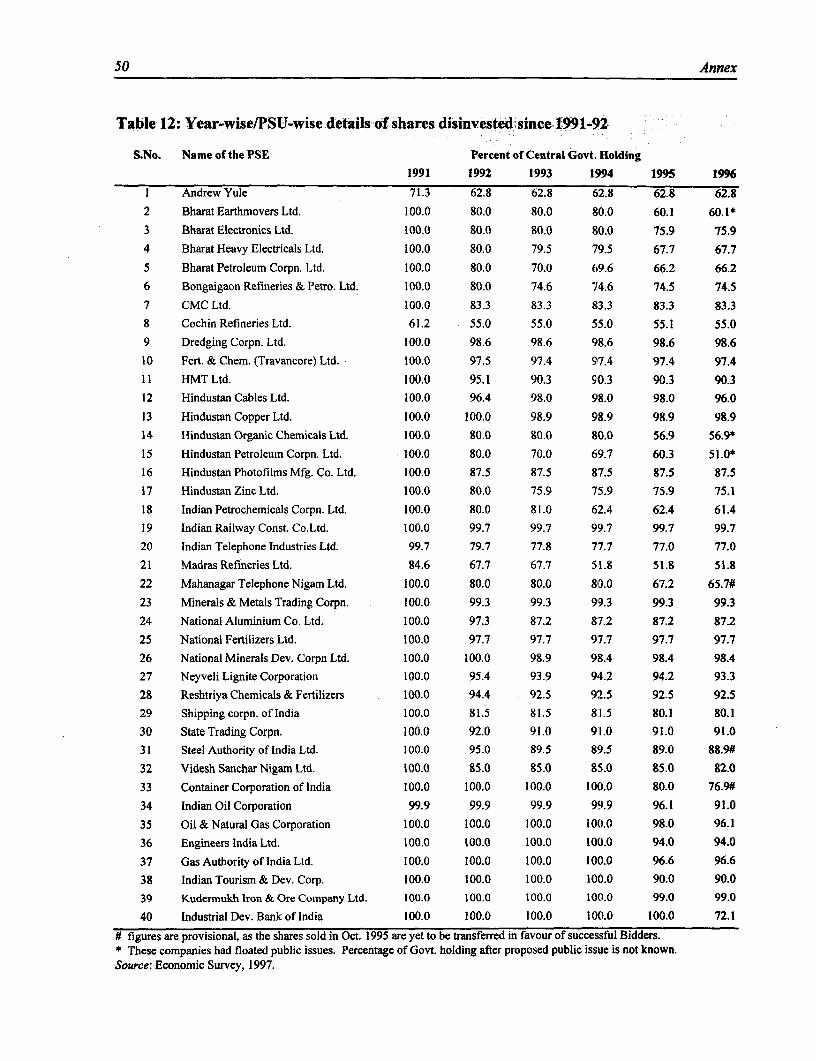

in time. First, there was a relaxation of monetary13. There was less progress in reforming public policies which led to a decline in short-term realenterprise (PEs), however. While public enterprises interest rates. Second, a number of measures wereare now more exposed to competition, their autonomy introduced to encourage private investment--remains limited and this has reduced the ability of their particularly FDI. These were the removal of entrymanagers to introduce essential restructuring. Thus, barriers (reservation policy) to a number of industries--with a few exceptions, the financial performance of mostly selected agro-industries--and relaxation of scalePEs has failed to improve. A Disinvestment limitations. Third, important regulatory changes wereCommission which was established in 1996 to examnine introduced to facilitate private investment inoptions for reducing central government equity in infrastructure. Finally, a pro-reform budget aimed atcentral public enterprises has since submitted an boosting confidence was presented to Parliament onapproach paper and two reports articulating a strategy-- February 28, 1997.which was amply debated by the public at large andexperts in the privatization field--for reforming PEs on 16. The 1997-98 budget: a creative but fiscallythe basis of which the Commission recommended the risky supply-side initiative. The main objective of thefull or partial privatization of nine public enterprises. 1997-98 Budget is to reactivate private investment.While these are positive steps, there are no signs yet Towards this objective, several measures were taken tothat its recommendations will be adopted by the revive the stock market. Corporate taxation wasgovermnent and that a rapid process of disinvestment sharply reduced (from 43 percent to 35 percent) and iswill take place. now in line with that in East Asia. Dividend taxation at

the individual income tax level was repealed andEconomic Management Issues replaced by a 10 percent final withholding on corporate

distributions. Other measures (such as allowing share14. Possible slowdown in investment and growth. buy-backs, announcing the reform of the Company'sDuring 1996-97, a number of developments raised Act, and increasing the cap on ownership by foreignapprehension on the future course of the economy and institutional investors in Indian companies from 24on its capacity to sustain the rates of growth of the last percent of paid-up capital to 30 percent) were intendedthree years. In particular, declines in the rates of to improve the business climate, increase privategrowth of imports of capital goods (which declined by investment, and sustain growth. Combined with7 percent), of corporate profits (5 percent), of lending improvements in tax administration, the reactivationcommitments by specialized long-term financial of private investment is critical to achieve the 1997-98institutions (30 percent), and of primary equity issues fiscal deficit target of 4.5 percent of GDP and(22 percent) gave rise to the perception that investment represents the main downside risks of an otherwiseand growth might have declined. The reasons were credible budget forecast. The 'budget also reduced thebelieved to be a tepid stock market which led maximum marginal personal income tax rate to 30corporations to delay security issues; high real interest percent from 40 percent and the lowest rate to 10rates; and commercial banks' heightened aversion to percent from 15 percent; further simplified the exciserisk (largely a result of tighter enforcement of tax structure; and introduced measures to strengthenprudential regulations and the Indian Bank debacle), all compliance. Also, tariff reductions for capital goodsof which made it difficult to reach financial closure on were more pronounced than for the rest.investment projects, leading many firms to postponeinvestment decisions. Political uncertainty was an 17. Fiscal adjustment in the 1996-97 and 1997-98obvious additional factor. budgets. Deferred pay adjustments associated with the

Fifth Pay Commission's recommendations (for which

Executive Summary v

0.3 percent of GDP had been budgeted) into 1997-98 amounts of central government grants to each stateand other minor expenditure adjustment offset the and, until the 1996 Tenth Finance Commission whichimpact of a shortfall in privatization (0.4 percent of discontinued this practice, on unconditional debtGDP) proceeds, allowing the government to meet its forgiveness for highly indebted states. Driven mostlyfiscal deficit target of 5 percent of GDP in 1996-97 by the objective of mobilizing finance for the(from 5.5 percent of GDP in 1995-96). The 1997-98 investment plans of the states, the Planningbudget projects a 0.5 percent fiscal correction to 4.5 Commission makes recommendations on centralpercent of GDP in 1997-98 to be achieved mainly by government loans and grants to the states, and on themaintaining tax revenue at its current share of GDP, amounts of states' borrowings from captive sources:and modestly accelerating privatization. However, this "'market borrowings" from commercial banks,fiscal deficit target may be difficult to achieve without insurance companies and pension funds, all of whichadditional measures. In particular, the budget relies must invest a share of their resources in "designatedupon improved compliance to offset the impact of the securities", such as state bonds.sharp cuts in taxation and maintain tax revenue at itscurrent share of GDP. 20. Starting in the early 1970s, both the Finance

and the Planning Commissions recommendedChanging States' Development Policies gradually but persistently increasing transfers to the

states. These developments built expectations that the18. India's pre-1991 development strategy and states needed not be overly concerned with mobilizing

inter-governmental transfers have shaped the states' resources since ever-expanding and politically moredevelopment and fiscal policies. The Indian expedient financing would be forthcoming. As a result,Constitution gives the states considerable autonomy to throughout the 1970s and 1980s, the states rapidlydefine their development policies. The states are expanded investments in physical infrastructureresponsible for the provision and regulation of key (power, irrigation, ports, roads), and provision of socialinfrastructure and social services, including primary services, without establishing mechanisms for costeducation and basic health. They defined their recovery and for maintaining these assets and programsdevelopment policies at a time when national policies in the long run. Prices charged for power, water,excluded private investment from key sectors of the irrigation and other services declined to levelseconomy. Where permitted, central licensing equivalent to a small fraction--in some cases zero--ofauthorities, not the enabling environment, determined production costs.the volume and composition of private investment.Consequently, across India, states' development 21. The states face three crises-fiscal,

policies focused on expanding public investment, often infrastructure, and human resource development Byin areas which are not the public sector's comparative the second half of the 1980s, it became evident that theadvantage. For this expansion, they relied on transfers states were experiencing considerable fiscalrecommended by the Finance and Planning difficulties. Implicit and explicit subsidies for goodsCommissions, two institutions which command and services which are not of a public nature rose toconsiderable respect in India, and whose reach about 7 percent of GDP. They also expandedrecommendations are generally accepted by the central public employment to the point that in most statesgovernment. wages and pensions absorb between 4-5 percent of the

state GDP, and 9-10 percent is not infrequent. They19. Driven mainly by the objective of equalizing contracted debt without establishing the financial basethe availability of infrastructure and social services for its servicing. As a result, fiscal stress becameacross India, Finance Commissions make evident. In particular, there was a deterioration in therecommendations: on how to share with each state quality of spending. While the states' fiscal deficittaxes collected by the central government, on the remained relatively stable at around 3 percent of GDP,

vi Executive Summary

capital, education, health and operations and on employment, and reduction of consumptionmaintenance expenditure started to decline from the subsidies) to eliminate wasiteful spending and makemid-1980s, and interest expenditure to increase. room for priority programs in public infrastructure,Resources for operations and maintenance became health and education; and (iv) tax reforms to provideinsufficient and infrastructure begun to exhibit signs of stable sources of revenue at a low efficiency cost.decay. These trends were exacerbated by the reformsstarted in 1991 when growth of central government 24. In many states, policy, pricing and institutionaltransfers declined and eventually became negative, and reforms of key sectors would bring about the neededinterest payments increased. Most states found fiscal restructuring. For example, power and irrigationthemselves unable to play their central role in India's sector reforms--particularly increases in power anddevelopment: to provide key infrastructure, health, and water tariffs--would generate large fiscal gains ineducation. virtually all of India's 25 states. In some states, such

reforms, alone, would be sufficient to restore fiscalState Reforms: Priorities and Progress sustainability. In others, putting the states' public

finances on a sustainable path would require more22. The reforms underway since 1991 have comprehensive reforms of public expenditures, such asradically changed the framework within which states' public enterprise reform, freeze on public employment,development policies are implemented. States can reduction in consumption subsidies and aattract private capital in such sectors as power, rationalization and retargeting of the states' welfareirrigation, ports, roads, and all areas of manufacturing-- programs. Finally, in highly indebted states, sectoraland it is its ability to attract private capital which now reforms and public expenditure restructuring may needdetermines a state's growth performance. Development to be complemented by debt refinancing.spending therefore needs to be more narrowly focusedon the state's areas of comparative advantage, where it 25. Several states have already started to implementcomplements rather than substitutes for the private sector reforms, particularly in power-where about fivesector. This is a radical departure from the pre-1991 states have taken the first steps towards increasingperiod, when the volume of public development tariffs, establishing an independent regulatory agency,spending was a key determinant of a state's growth and privatizing generation and distribution in a processperformance. of reform that will take several years to be brought to

its logical conclusion--ports, roads, and, to a lesser23. Attracting private capital requires states to extent, water and irrigation, although a few states haveprovide an enabling and investor-friendly environment. already begun moderately adjusting water tariffs, andThat is, good quality and abundant infrastructure, an devolving maintenance to farmers' associations. Albeiteducated labor force, a business-friendly public extremely modest, some progress has also been madeadministration, and moderate levels of taxation. in restructuring public expenditure with a view toSignificant reforms are needed to bring this about in reducing unproductive expenditure. In particular, thereIndia's states. In particular, it requires: (i) policy, is growing recognition of the need to controlpricing, institutional, and regulatory reforms to recruitment to reduce the wage bill, eliminate poorlytranslate private sector interest to invest in targeted welfare programs, and privatize publicinfrastructure into commercially viable ventures--and enterprises. On the revenuefront, reforms are neededimprovements in the states' capacity to manage to increase cost recovery (as an essential part of sectorcommercially enforceable contracts; (ii) an reform), broaden the base, improve the efficiency ofenvironment conducive to efficient public investment taxation, and ensure tax harmronization across states.in areas where the public sector will remain important Some states have already taken significant steps in thissuch as roads and urban services; (iii) public direction, but much remains to be done.expenditure restructuring (such as privatization, freeze

Executive Summary vii

Policy Priorities percent of GDP for the past few years, of which

consolidated central and state governments deficit26. India's overarching development objective amounts to 6.8 percent of GDP at present. Yet, it isduring its Ninth Plan period (1997-02) is achieving and only with a more rapid decline in fiscal imbalances thatsustaining high annual rates of growth of 7-8 percent the high real interest rates that have prevailed in theand ensuring that this growth benefits the poor. A recent past will decline. A target of 4 percent of GDPbroad consensus has emerged across India's political for the consolidated central and state governmentsspectrum for this objective and for continuing the deficit may be a realistic goal to achieve in the next 3-4liberalization of the economy. At what speed this will years. Reducing central and state governmentsbe done remains however an unresolved--yet critical-- subsidies on "non-merit goods" which absorb 11issue because it will determnine the country's growth percent of GDP at present could provide the resourcesperformance. needed to reach, and perhaps exceed, this target. A

more rapid privatization of public enterprises would27. The rapid growth of the last few years has enable the government to retire public debt and reduceshown how much India stands to gain from interest costs. The benefits of a more rapid correctionderegulation and fiscal adjustment. It has also shown of fiscal imbalances go well beyond just lower interestthat the economy is facing capacity constraints, most rates and higher investment. Lower fiscal deficits andnotably in infrastructure. High real interest rates are interest rates would provide favorable conditions for ananother indication of stress on domestic resources acceleration of banking reform, would help improvewhich has been at the origin of pressures put on the the health of the financial system, would provide moreauthorities to accelerate, perhaps prematurely, the flexibility to the RBI in the conduct of monetaryopening of the capital account--a development that in policy, would reduce pressure for opening the capitalall circumstances would need to be carefully account ahead of the structural reforms needed to makesynchronized with India's progress in structural it a success, and would make it easier to manage surgesreforms. Resources are also being strained in in capital inflows, and possible external shocks.

agriculture which has grown dependent on extremely International experience shows that a strong fiscallarge subsidies (power, water, fertilizer, to name just position has a central role in managing effectively thethe main ones). These subsidies put an unsustainably capital and current accounts of the balance oflarge burden on central and state government budgets, payments.and also are at the origin of microeconomic distortions

and misuse of resources (of which overexploitation of 29. Also, as highlighted in the May 1997groundwater resources and poor energy conservation government paper on subsidies, central and statepolicies are two important examples) which reduce government deficits are linked to significantproductivity growth. microeconomic distortions whose cost they bear. Again

in this case, the benefits of fiscal corrections go beyond28. The centrality of fiscal adjustment. As it has improve, the maeroeeon o beyond

forthepas sverl yar, rducng nda'sfisal improvements in the macroeconomic framework--for the past several years, reducing India's fiscal because they are tantamount to correcting severe priceimbalances remains of central importance for the distortions and misguided sector policies which areachievement of the country's development goals. preventing private investment and hamperingWhile gains have been made in reducing the central development. Power is one well known case where thegovernment fiscal deficit, those have been offset in the correction of price distortions would not only reducerecent past by a deterioration in the financial position state governments fiscal imbalances (by 2 percent ofof public enterprises, mostly because of the large cost GDP), but would also lead to a more efficient use of

(0.8 percent of GDP in 1996-97) of subsidizing oil resources, and provide the basis for private capital inproducts. As a result, the consolidated public sector power and the much needed capacity expansion.deficit has remained at the relatively high level of 9 Similar situations exist in other sectors.

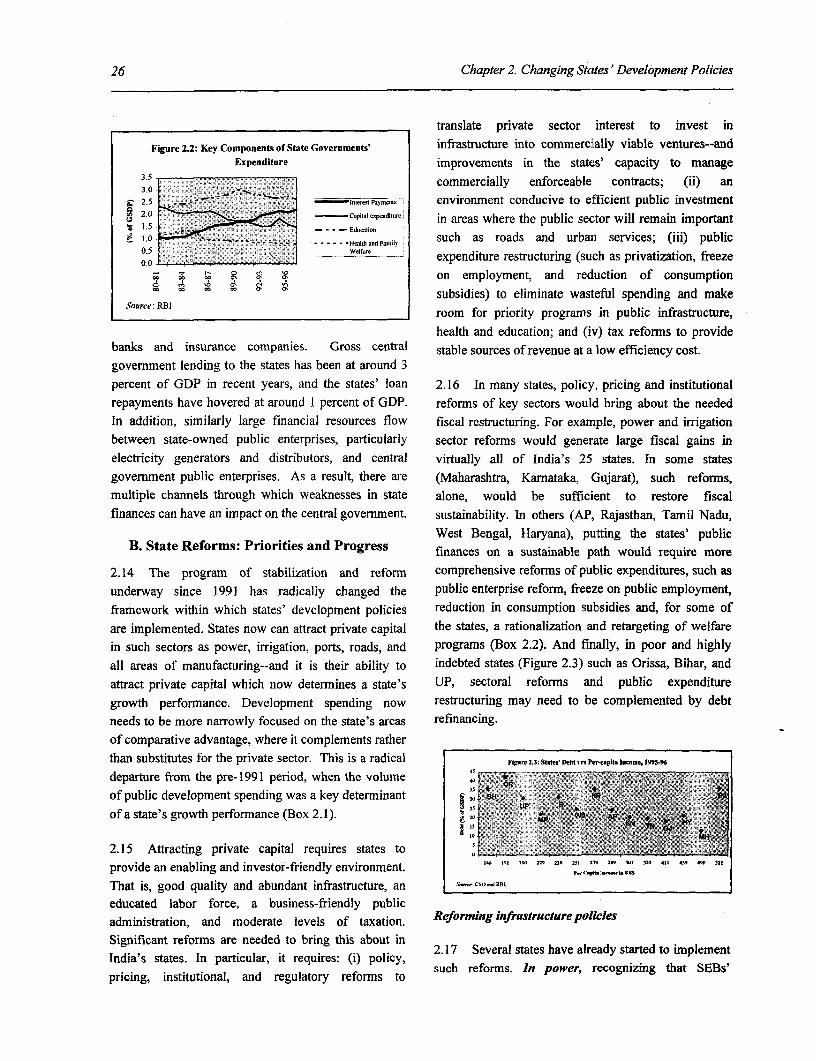

viii Executive Summary

30. In addition to the macro-and micro-economic 33. At the same time, to support agriculturaldimensions of fiscal adjustment, a third, and at least as reforms, it would be essential to bring rural creditimportant one, is that of expenditure composition, reform to its logical conclusion. A coherent strategy forparticularly at the level of the states. In most states, the increasing flows to agriculture and other ruralcost of subsidies, of an excessively large labor force, economic -activities must address issues of access toand of government activities which are not of a financial services by the rural population in general, asdevelopment nature absorb a large share of state well as the financial sustainability of the rural financialgovernments budgets. To a large extent, the institutions themselves. Further measures are neededdeterioration of India's infrastructure, and the to encourage and facilitate an orderly re-orientation ofdifficulties the country is experiencing to mobilize India's rural financial system from the supply-ledresources to accelerate the development of its human approach of concessional, targeted agriculture credit, toresources are the result of states' pricing and sectoral the systematic development of demand-oriented ruralpolicies and the associated implied subsidies--and it is financial markets.also with the states that lies their resolution. Recentdeclines in central government financial support to the 34. Deregulating agriculture. Deregulation wouldstates have provided some--but as yet insufficient-- enable agriculture to achieve potentially largeimpetus to the states to start taking corrective actions. efficiency gains and provide a basis for the removal of

subsidies. The 1997-98 Budget contains the first steps31. Addressing the challenge of infrastructure. of a promising beginning of reforms at the level of theMuch has been said and written on India's central government, which could provide impetus--infrastructure problems. The recently completed report although it has not thus far--for similar reforms at theof an Expert Group on infrastructure provides a level of the states. Intimately related to thesobering review of India's tremendous infrastructure liberalization of agriculture is the deregulation of agro-problems and makes three recommendations to address industry where important segments are still regulatedthem. Thefirst is fiscal reforms to strengthen state and by industrial licenses or scale limitations that imposelocal governments capacity to mobilize resources to large costs to an industry characterized by economiesinvest in infrastructure. This is particularly important of scale. Because the incomes of the poor are sofor infrastructure of a public nature where benefits are closely associated with the fortunes of the agriculturalbest captured through taxation. The second is sector, a liberalization of agriculture would not onlyregulatory and pricing reforms to translate India's have positive growth effects, it would also helpimmense infrastructure needs into viable commercial increase the incomes of the pooir.ventures, capable of attracting private capital. Thethird is financial sector reforms to enable the large 35. Completing the liberalization of the trade andpool of India's financial savings to flow to high returns investment regimes remains an important policyinfrastructure investments. objective. India's import-weighted tariff has been

reduced from 87 percent in 1991-92 to around 2032. Banking reforms. Further banking and financial percent at present. The 1997-98 budget indicates thatderegulation (reducing government equity in the the process will continue, until India reaches the tariffcapital of public banks and further reductions in the levels of its East Asian neighbors. There are alsoSLR) would reduce the influence of government on indications that the government intends to eliminatecommercial banks' basic business decisions (such as restrictions on consumer goods in a phased manner.on hiring, on pay scales, branch expansion or closure), Implementation of this agenda would improveand permit more vigorous competition from private considerably the competitiveness of India'sbanks. The RBI is gradually strengthening its oversight manufacturing, as would a further deregulation of thecapabilities, and this provides the basis for a further investment regime. The radical liberalization of the lastderegulation of the banking system. six years notwithstanding, extremely costly regulations

Executive Summary ix

continue to restrict investment in areas reserved for private sector shows strong interest in investing in asmall scale and agro-industries. number of infrastructure areas, particularly power and

telecommunications, an important role remains for36. A prudent management of tlhe capital account public sector investment in some key areas--such asremains appropriate until fiscal consolidation has been roads, rural infrastructure and social services--whichachieved, the instruments and markets for indirect would need to be substantially increased. Suchmonetary control are more fully developed, the investments are crucial for sustaining rapid growth andcommercial banking system is strengthened, trade ensuring that the poor participate in the growthliberalization is complete and exports sufficiently process.diversified. Consistent with this objective, the pace of

liberalization of restrictions on debt-related capital and 38. The Bank therefore recommends that theshort-term capital would need to be gradual, tailored to members of the IDF should aim for officialthe pace of fiscal consolidation, progress in development assistance that directly supports prioritystrengthening the domestic financial system, and public investments in physical infrastructure andexport performance. Priority would be given to human capital development. This investment wouldmeeting the needs of long-term infrastructure financing also help crowd-in the necessary complementaryas the government has indicated in its 1997-98 private investment particularly in physicalExternal Commercial Borrowing guidelines. infrastructure. In addition to the financial flows,Otherwise, there would be a danger of prompting official development assistance is also crucial to buildvolatile financial conditions and sharp cross-border institutional capacity particularly at the level of thesurges in short-term funds that would be difficult to state and local governments. Therefore, as had lastmanage and could put serious stress on the domestic year's CEM, this report makes a case for India'sbanking system. continued access to long-termn assistance, including a

substantial concessional component. In view of its stillExternalfinancing requirements current high debt burden, India would need to continue

to prudently manage its external debt. With an37. India will continue to need to rely on official topuelymngisexmadb.Wth n37.elopIndiaswilotinue, notoithaneedigtorel goffica expected modest current account deficit of 2 percent ofdevelopment assistance, notwithstanding the growing GPoe h etfwyasadtencsaybidrole of private inflows. Besides India's low level of per uP oferve ndia would til reqetoalygross

capia GP (U$35), ofical evelpmet asistnce up of reserves, India would still require total grosscapita GDP (US$350), official development assistance fiacnoflsetUS1ilonn1979,ndnis also critically necessary for India to meet its

average of about US$17 billion in each of theenormous needs for infrastructure and human resource foloig four yS. bilatera an multilatedevelopment. As indicated in the Poverty Assessment particint atls years IiaDelopmentFramReport, distributed to members of India Development patcanstlstyr'IdiDelomtFruReport,IF dIsibut toversy ofmn widiDevpmeaant pledged about US$6.7 billion in official assistance to

Fou ID) ndaspoet rmis iepra n India's development efforts as a recognition of India'sthe lives of many of India's more than 300 million commioment tofreforms n neto aceeatepoor are burdened by poor health, illiteracy, and social

' ' ~~~~growth and reduce poverty and a similar amount isinequalities. Prospects for improving their standards of expeted rethis yert and non-debt commeria

living depend on India's ability to promote growth andsources are expected to account for the country's

invest in human resources development. While the remaining financing needs.

I

Chapter RECENT ECONOMIC DEVELOPMENTS

1.1 A number of reports issued in 1996-97 (the A. Recent Economic Developments

Ministry of Finance's Economic Survey; the Reserve

Bank of India's (RBI) Annual Report; the RBI Report A strong supply response

on Currency and Finance; the RBI Report on Trend

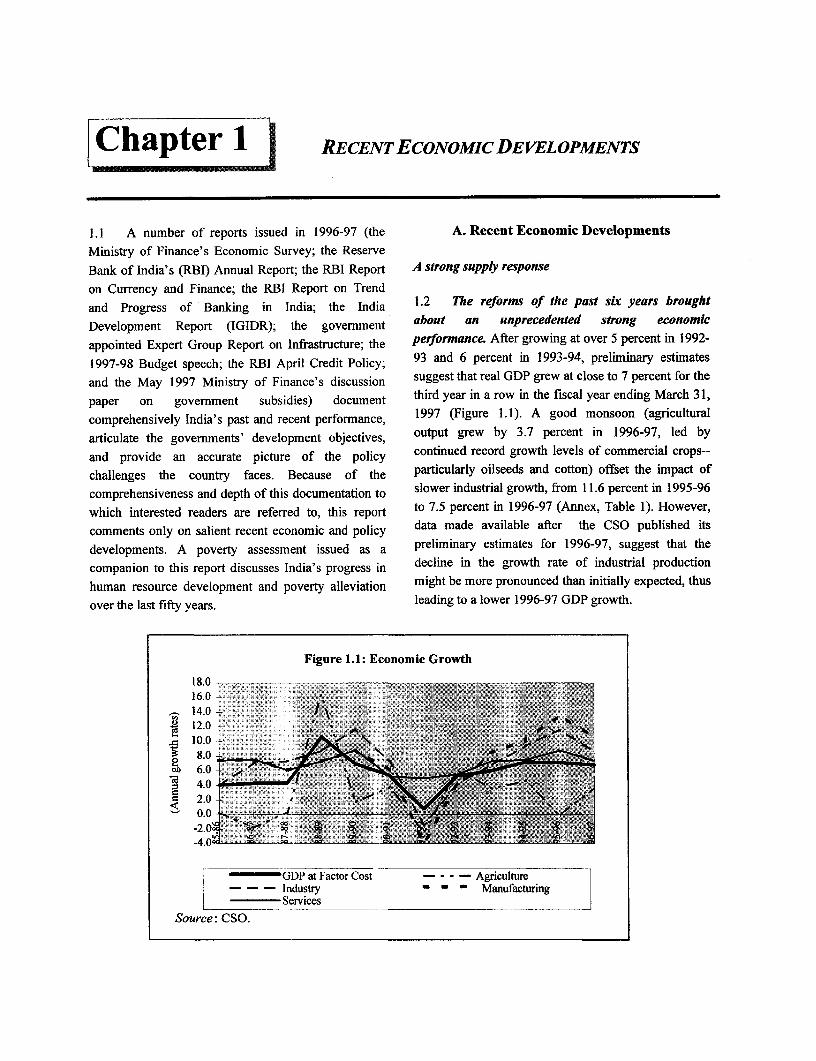

and Progress of Banking in India; the India 1.2 The reforms of the past six years brought

Development Report (IGIDR); the government about an unprecedented strong economic

appointed Expert Group Report on Infrastructure; the performance. After growing at over 5 percent in 1992-

1997-98 Budget speech; the RBI April Credit Policy; 93 and 6 percent in 1993-94, preliminary estimates

and the May 1997 Ministry of Finance's discussion suggest that real GDP grew at close to 7 percent for the

paper on government subsidies) document third year in a row in the fiscal year ending March 31,

comprehensively India's past and recent performance, 1997 (Figure 1.1). A good monsoon (agricultural

articulate the governments' development objectives, output grew by 3.7 percent in 1996-97, led by

and provide an accurate picture of the policy continued record growth levels of commercial crops--

challenges the country faces. Because of the particularly oilseeds and cotton) offset the impact of

comprehensiveness and depth of this documentation to slower industrial growth, from 11.6 percent in 1995-96

which interested readers are referred to, this report to 7.5 percent in 1996-97 (Annex, Table 1). However,

comments only on salient recent economic and policy data made available after the CSO published its

developments. A poverty assessment issued as a preliminary estimates for 1996-97, suggest that the

companion to this report discusses India's progress in decline in the growth rate of industrial production

human resource development and poverty alleviation might be more pronounced than initially expected, thus

over the last fifty years. leading to a lower 1996-97 GDP growth.

Figure 1.1: Economic Growth

16 0-;-.

1 4.012.0 -

10.0

50 8.0 i i

-4.0 - i

I ' ~~GDP at Factor Cost --- Agriculture

- - Industiy - - - ManufacturingL_______ Services

Source: CS0.

2 Chapter 1. Recent Economic Developments

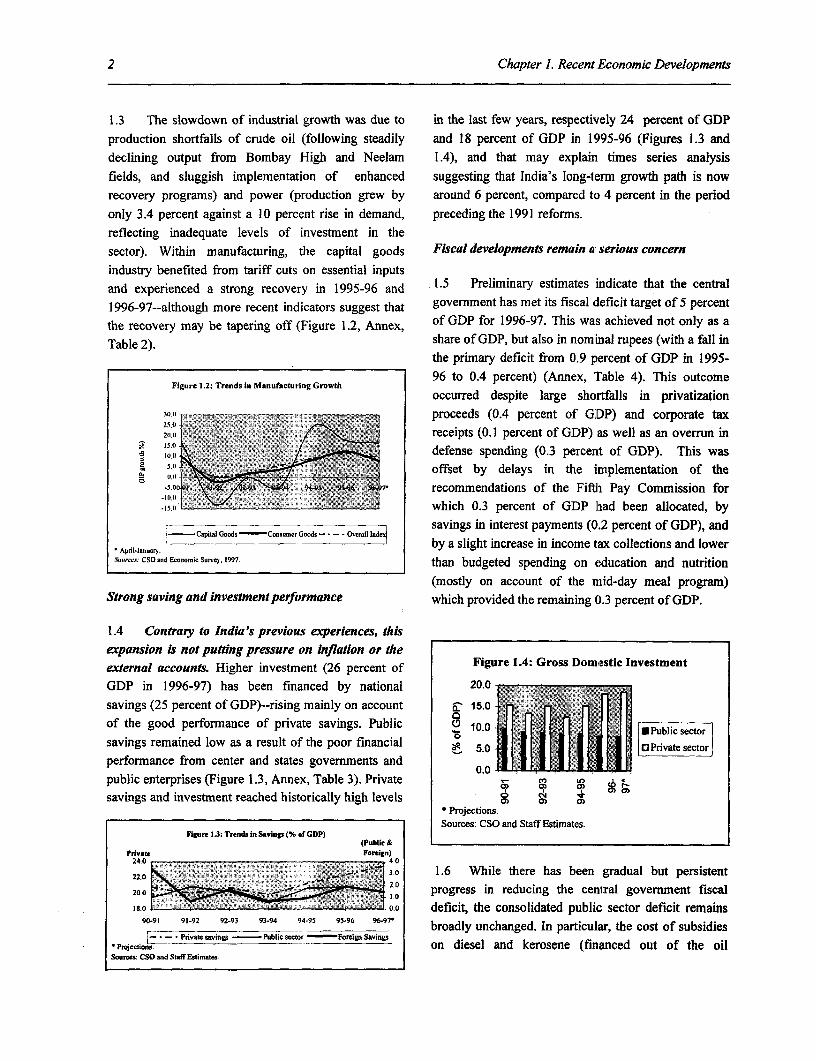

1.3 The slowdown of industrial growth was due to in the last few years, respectively 24 percent of GDPproduction shortfalls of crude oil (following steadily and 18 percent of GDP in 1995-96 (Figures 1.3 anddeclining output from Bombay High and Neelam 1.4), and that may explain times series analysisfields, and sluggish implementation of enhanced suggesting that India's long-term growth path is nowrecovery programs) and power (production grew by around 6 percent, compared to 4 percent in the periodonly 3.4 percent against a 10 percent rise in demand, preceding the 1991 reforms.reflecting inadequate levels of investment in thesector). Within manufacturing, the capital goods Fiscal developments remain a serious concernindustry benefited from tariff cuts on essential inputsand experienced a strong recovery in 1995-96 and 1.5 Preliminary estimates indicate that the central1996-97--although more recent indicators suggest that government has met its fiscal deficit target of 5 percentthe recovery may be tapering off (Figure 1.2, Annex, of GDP for 1996-97. This was achieved not only as aTable 2). share of GDP, but also in nominal rupees (with a fall in

the primary deficit from 0.9 percent of GDP in 1995-96 to 0.4 percent) (Annex, Table 4). This outcome

Figure 1.2: Trends in Manufacturing Growthoccurred despite large shortfalls in privatization

30.11 L proceeds (0.4 percent of GIDP) and corporate tax20A ~~~~~~~~~~receipts (0.1 percent of GDP) as well as an overrun in

MO ,,,,, 15defense spending (0.3 percent of GDP). This was(0 ~~~~~~~~~offset by delays in the implementation of the

;,,,, iM, X e iii ,7- recommendations of the Fifth Pay Commission for-150 =l S Swhich 0.3 percent of GDP had been allocated, by--Capital (loads Consomcr (loads - . - .savings in interest payments (0.2 percent of GDP), ande-CopitalGoods-ConnuncrOood--Ocalde

* ApdI-Ioooc by a slight increase in income tax collections and lowerC,os CSOand Econotic Sun 1997 than budgeted spending on education and nutrition

(mostly on account of the nlid-day meal program)Strong saving and investment performance which provided the remaining 0.3 percent of GDP.

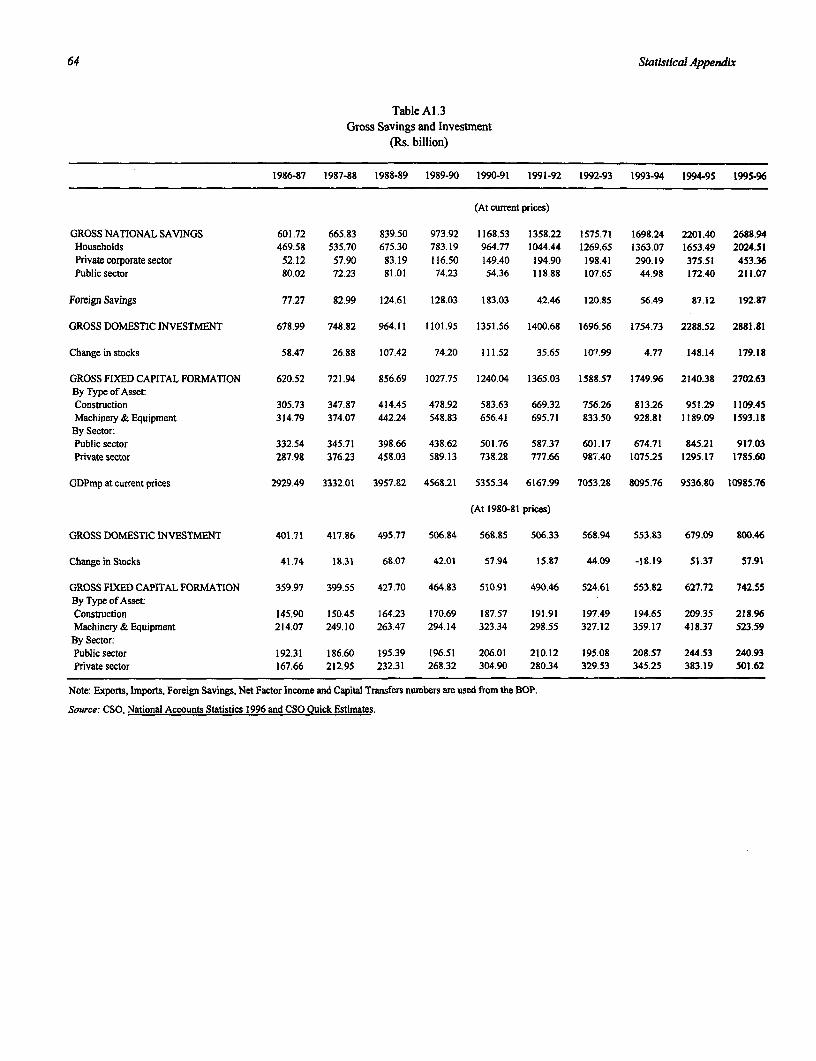

1.4 Contrary to India's previous experiences, thisexpansion is not putting pressure on inflation or theexternal accounts. Higher investment (26 percent of Figure 1.4: Gross Domiestic InvestmentGDP in 1996-97) has been financed by national 20.0savings (25 percent of GDP)--rising mainly on account a 2 o 7 7 7fl0of the good performance of private savings. Public % 10.0 l U Public sector

savings remained low as a result of the poor financial a 50 III 1I I 0 Privatesector

performance from center and states governments and o.0 :Privat e seoL0.0

public enterprises (Figure 1.3, Annex, Table 3). Private . °> savings and investment reached historically high levels C co

* Projections.Sources: CSO and Staff Estimates.

Figure 1.3: Trends in Savings (% of GDP) lI ~~~~~~~~~~~~~~~~~~(Public &I

Prvate Foren)24.0 4.022.0 3.0 1.6 While there has been gradual but persistent

2.020.0 2 0 progress in reducing the central government fiscal18.- - . .0 deficit, the consolidated public sector deficit remains

90l91 91.92 92-93 93-94 94-95 95-96 broadly unchanged. In particular, the cost of subsidies; = *- Private savings - Public sector Foreip Savings

Projections.- on diesel and kerosene (financed out of the oilSources: CSO and StaffEstimates.

Chapter 1. Recent Economic Developments 3

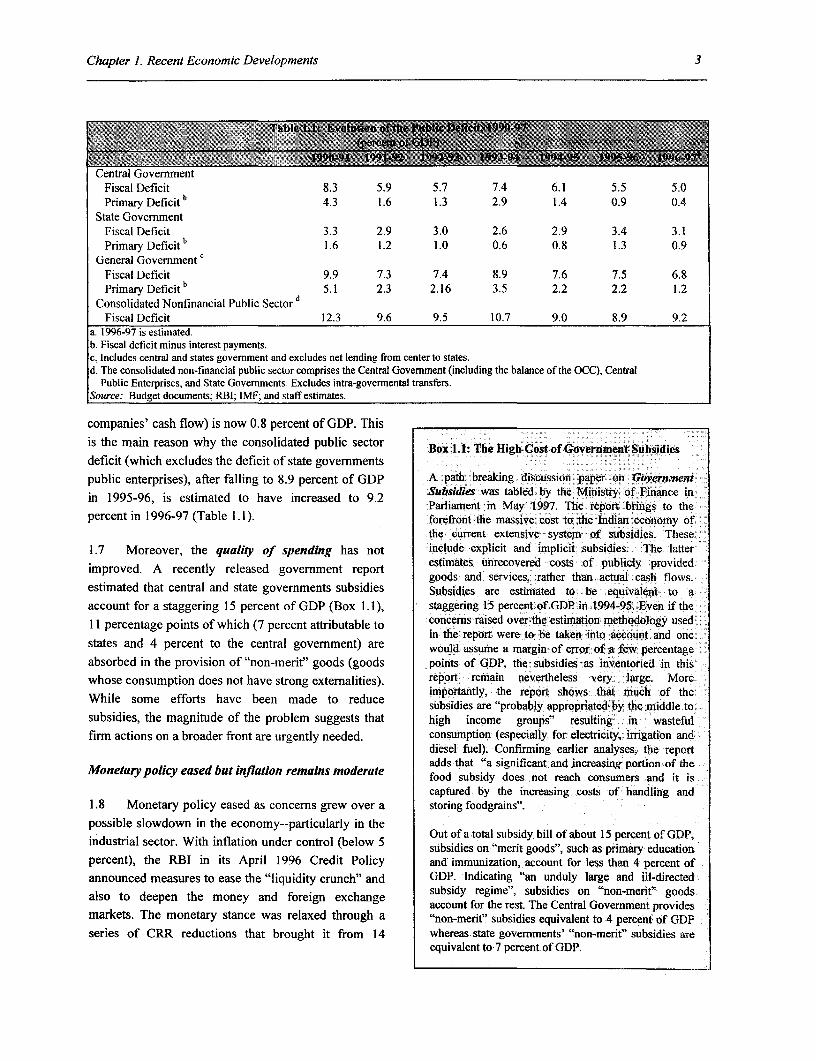

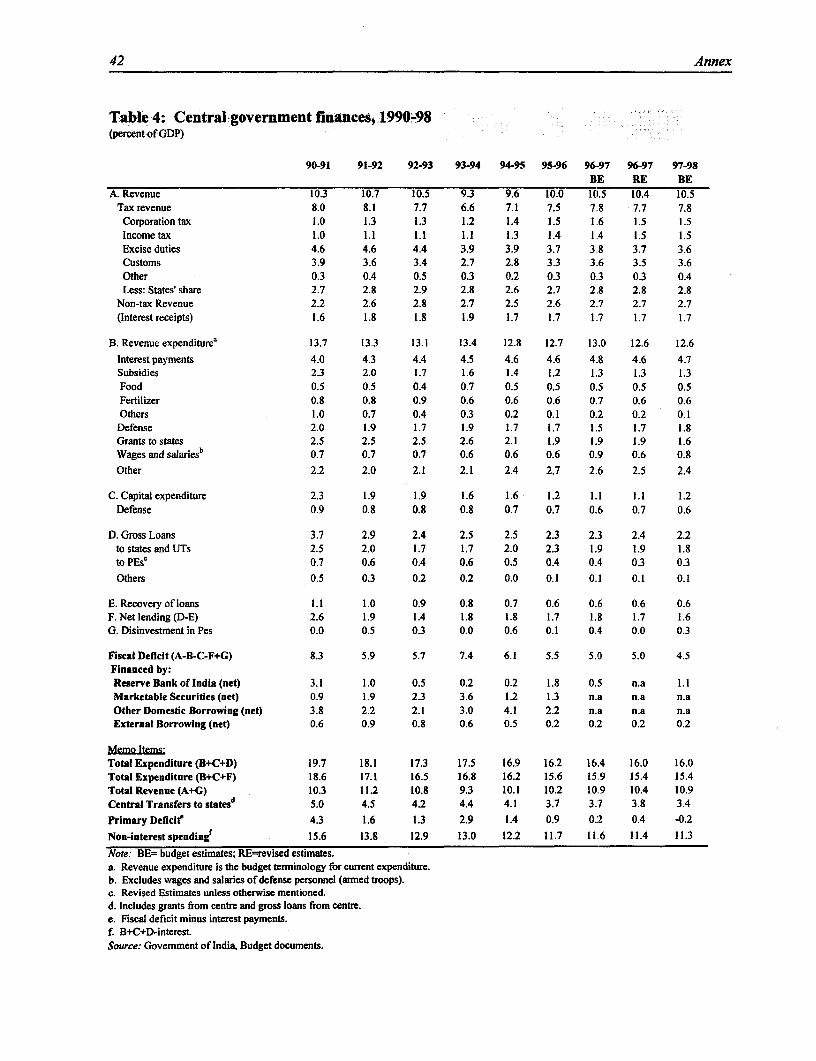

Central GovernmentFiscal Deficit 8.3 5.9 5.7 7.4 6.1 5.5 5.0Primary Deficitb 4.3 1.6 1.3 2.9 1.4 0.9 0.4

State GoveNnmentFiscal Deficit 3.3 2.9 3.0 2.6 2.9 3.4 3.1Primary Deficit b 1.6 1.2 1.0 0.6 0.8 1.3 0.9

General Government'cFiscal Deficit 9.9 7.3 7.4 8.9 7.6 7.5 6.8Primary Deficit b d . 2.3 2.16 3.5 2.2 2.2 1.2

Consolidated Nonfinancial Public SectordFiscal Deficit 12.3 9.6 9.5 10.7 9.0 8.9 9.2

a. 1996-97 is estimated.b. Fiscal deficit minus interest payments.c. Includes central and states govemment and excludes net lending from center to states.d. The consolidated non-financial public sector comprises the Central Govemment (including the balance of the OCC), Central

Public Enterprises, and State Govemments. Excludes intra-govermental transfers.Source: Budget documents; RBI; IMF; and staff estimates.

companies' cash flow) is now 0.8 percent of GDP. This

is the main reason why the consolidated public sector Box 1.1: The High Cost of Government Subsidiesdeficit (which excludes the deficit of state governmentspublic enterprises), after falling to 8.9 percent of GDP A path breaking discussion paper on Governmentin 1995-96, is estimated to have increased to 9.2 Subsities was tabled by the Ministry of Finance inParliament in May 1997. The report brings to thepercent in 1996-97 (Table 1.1). forefront the massive cost to the Indian economy of

the current extensive system of subsidies. These1.7 Moreover, the quality of spending has not include explicit and implicit subsidies. The latter

improveyreleased goverunment report estimates unrecovered costs of publicly providedgoods and services, rather than actual cash flows.

estimated that central and state governments subsidies Subsidies are estimated to be equivalent to aaccount for a staggering 15 percent of GDP (Box 1.1), staggering 15 percent of GDP in 1994-95. Even if the11 percentage points of which (7 percent attributable to concerns raised over the estimation methodology used

in the report were to be taken into account and onestates and 4 percent to the central government) are would assume a margin of error of a few percentageabsorbed in the provision of "non-merit" goods (goods points of GDP. the subsidies as inventoried in thiswhose consumption does not have strong externalities). report remain nevertheless very large. More

importantly, the report shows that much of theWhile some efforts have been made to reduce subsidies are "probably appropriated by the middle tosubsidies, the magnitude of the problem suggests that high income groups" resulting in wastefulfirm actions on a broader front are urgently needed. consumption (especially for electricity, irrigation and

diesel fuel). Confirming earlier analyses, the reportadds that "a significant and increasing portion of the

Monetary policy eased but inflation remains moderate food subsidy does not reach consumers and it iscaptured by the increasing costs of handling and

1.8 Monetary policy eased as concerns grew over a storing foodgrains".possible slowdown in the economy--particularly in the

Out of a total subsidy bill of about 15 percent of GDP,industrial sector. With inflation under control (below 5 subsidies on "merit goods", such as primary educationpercent), the RBI in its April 1996 Credit Policy and immunization, account for less than 4 percent ofannounced measures to ease the "liquidity crunch" and GDP. Indicating "an unduly large and ill-directed

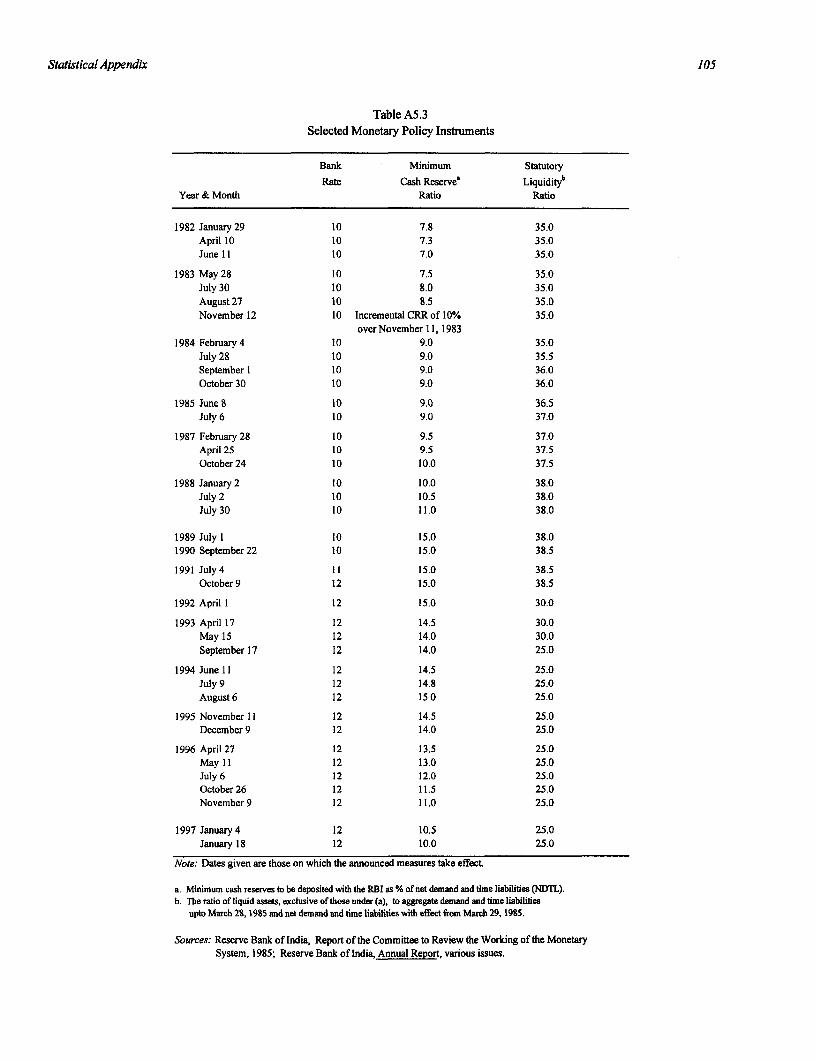

subsidy regime", subsidies on "non-merit" goodsalso to deepen the money and foreign exchange account for the rest. The Central Government providesmarkets. The monetary stance was relaxed through a "non-merif' subsidies equivalent to 4 percent of GDPseries of CRR reductions that brought it from 14 whereas state governments' "non-merit" subsidies are

equivalent to 7 percent of GDP.

4 Chapter 1. Recent Economic Developments

percent in April 1996 to 10 percent in January 1997, imbalances still high, the risk of an acceleration ofand through other measures that lowered the pre- inflation in the future remains significant. Despite theemption of NRI deposits. In addition, in its April 1997 monetary easing, bank lending grew at slower ratescredit policy, the RBI reduced the cost of funds to than last year and the Prime ]Lending Rate (PLR)--thebanks by lowering the interest rate ceiling on deposits "benchmark" interest rate for domestic and foreignof more than 30 days and less than one year, and by banks lending--fell by less than two percentage points,deregulating interest rates on FCNR(B) deposits. Banks remaining at 14.0-15.0 percent, with most lendingwere also given more leeway in determining their risk taking place at 16.5-19.5 and higher rates for someexposure. To improve its liquidity management, the borrowers. Because of its beneficial effects onRBI reduced banks' access to automatic refinance of corporate profitability and on bank's balance sheets,export credit from April 1996 and removed the the easing of monetary policy will, however, haverefinance facility against government securities. positive effects on banks' profitability.

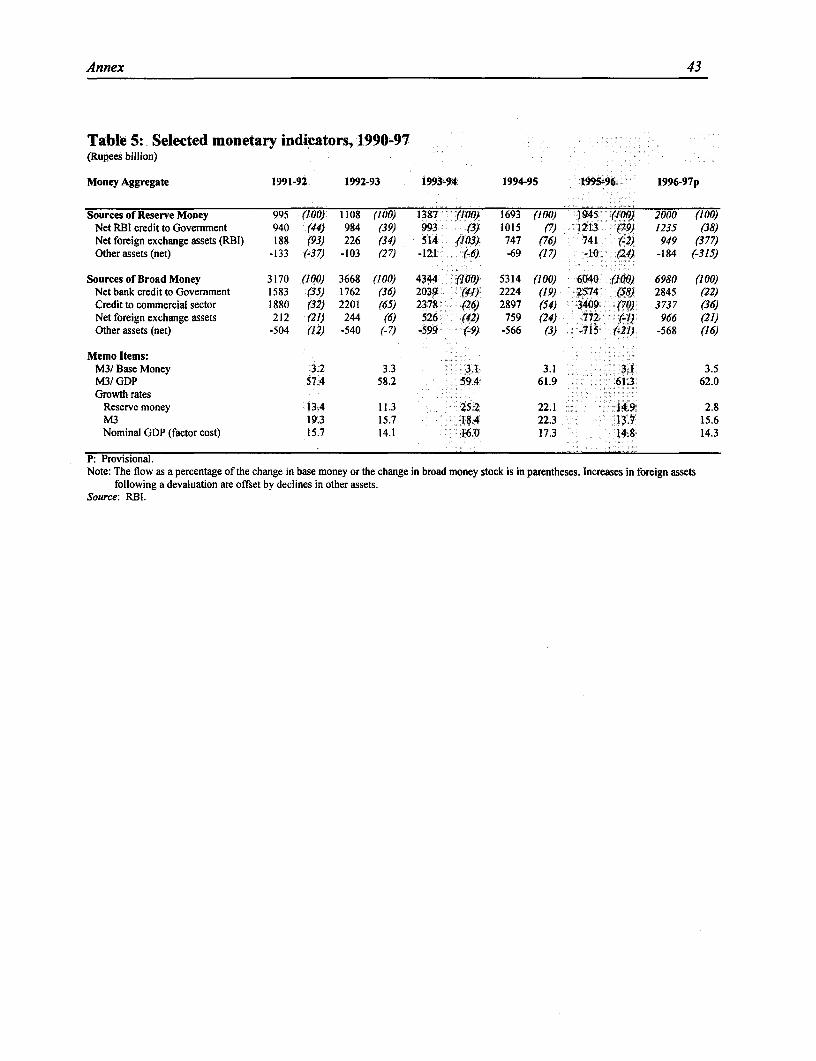

1.9 Broad money (M3) grew by 15.6 percent 1.11 Money and Foreign Exchange Markets have

(Figure 1.5) compared with 13.7 percent in 1995-96 been more stable. Increased liquidity, resumption ofbut remained within the target range of 15.5-16 percent repos by the RBI, banks' heiglhtened aversion to riskfor 1996-97 (15-15.5 percent for 1997-98). Banks' (in the wake of the Indian B3ank debacle followingimproved liquidity positions, combined with lower major losses associated with speculative lending whichgrowth of RBI credit to the government (2.3 percent wiped out the Bank's entire net worth) and a slowdowncompared with 20 percent in 1995-96), helped offset of bank credit (from 18 percent in 1995-96 to 10.5the expansionary effect on reserve money of a 28 percent in 1996-97) reduced' volatility in the callpercent increase in RBI's foreign exchange assets money and foreign exchange markets. Call money(Annex, Table 5). However, inflation rose from 5 markets were stable with the rate falling from anpercent in March 1996 to 7.2 percent in March 1997 average high of 35 percent during November 1995 toexceeding the government's 6-7 percent target for around 6 percent in November 1996. The rate fell1996-97 (Figure 1.6), before declining to around 6 further to around 2 percent during January 1997. Bankspercent in May 1997. In addition to the relaxation of returned to risk-free government securities above andmonetary policy, the rise in inflation was fueled by the beyond what is required under the SLRs. This helpedJuly 1996 adjustment in administered petroleum prices the government to reduce its reliance on the RBI creditand increases in food prices that abated in the latter line ("ad-hocs"). Consequently, net RBI credit to thepart of the fiscal year. government rose by 2.3 percent during 1996-97

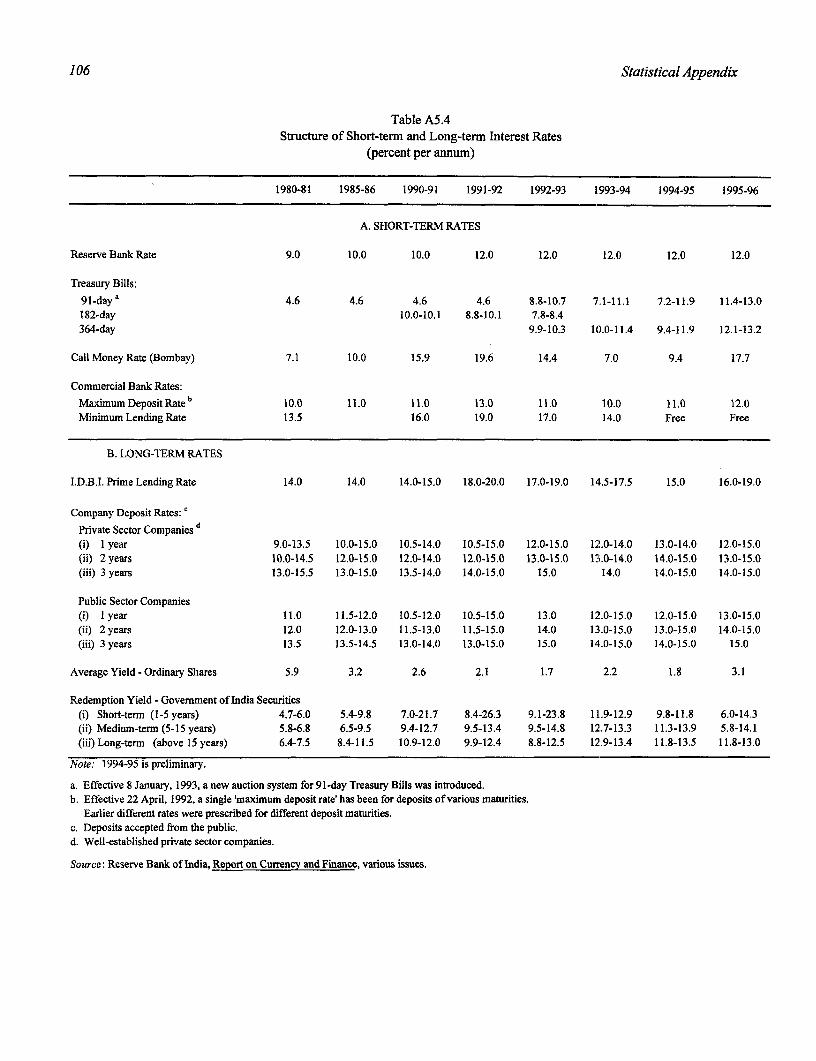

compared with the 20 percent growth in 1995-96.1.10 The relaxation of monetary policy reducedinterest rates but the yield curve stiffened. While the Exports and imports growth slowed down; theinterest rate on 91-day Treasury bills has fallen from external accounts remain strong13 percent in March 1996 to 8 percent recently (March1997), long-term rates remained almost unchanged at 1.12 In response to the sharp depreciation of the realclose to 14 percent (Annex, Table 6). This possibly exchange rate in 1991-93 and reduction of importreflects financial markets' perception that, with fiscal tariffs since 1991, and thus of the anti-export bias

Figure 1.5: Money Supply (M3) Figure 1.6: Inflation Rates (WPI)

24 ' ^22 14

14 Z)~~~~~~~~~~~~~~~~~~

@ = 5 s X g~~z O 5 a . 86 = t; >f

[ -9S 96 -96-97 1 < -95-96 -96-97.S-: RBI. &,ursc: Govemment statistics.

Chapter 1. Recent Economic Developments 5

implicit in the previous trade regime, exports grew atTable 1.2- Merchandise Export and fIporf Sowdowpvrates in excess of 20 percent during 1993-96. As i9954996

growth and corporate restructuring gained momentum, Exports on_-oi-l ;;ail mportsimports grew by slightly over 20 percent in 1995-96, importsdriven by capital goods imports. Growth(value)

1995 20.9 28.2 27.01996 4.1 -1.0 34.4

1.13 However, during 1996-97, there was a Change in Growthsignificant slowing down of growth of external trade Rates -16.8 -29.2 7.4

flows (Figure 1.7). India's exports in nominal US$ of which:'grew by only 4.1 percent in 1996-97 compared with 21 Volume -9.4 -14.7 -7.9percent in 1995-96. Assuming that India's export of which in percent:

External demand -3.3Figure 1.7: Year to Date Nominal Export Growth, 1991-1996 Domestic factors -6.1

Pereet (seasonally adjusted, year-on-year. based on USS) 1. The decomposition between volume and price effects is based30 . . I on data for the first nine months of the year.25 1 Source: Staff Estimates, IECAP

20 - {* ; - i -- 1992 to specify the exact contribution of each. Supported by

1 5 -:- .' ~ - 1993 a small current account deficit combined with large

- 1995 capital inflows (the RBI has been accumulatings ,t-% . >,- ; lreserves), the nominal exchange rate has remained

c _ - ;, stable at around Rs. 35-36/US$ since May 1996,.5 ..: ....... ... .: .. : l leading to some real appreciation.

-L; tio n ' 'F 0 z aS5airte Itmatenoinoal Financial Statistics. IMF.____Fin____ i___ 1___St___i _____i-___IMF.____ 1.14 Two noteworthy sector specific developments

were the decline in exports of gems and jewelry and ingrowth is 40 percent higher than growth in world trade exports of leather products. The fall in the value of cut(the trend of the last few years), Table 1.2 summarizes and polished diamond exports are explained by weakerthe estimated contribution of different factors to the demand in key markets such as Japan, and priceexport slowdown. It shows that price effects, namely declines due the failure of Argyle Diamond--one ofthe appreciation of the US dollar, accounted for a large India's largest suppliers--to renew its distributionshare of the decline in nominal exports (in SDR terms, contract with De Beer's Central Selling Organization inthe decline in export growth is much more modest: mid 1996. Following a Supreme Court decision thatfrom 17.2 percent in 1995-96 to 9.3 percent in 1996- tightened regulations on environmental protection, the97) (Figure 1.8). The table also suggests that domestic leather industry suffered a major fall in production andfactors played an important role in the slowdown of exports as a result of the closure of small scaleexports. Infrastructure constraints, the cost of credit, tanneries due to their inability to set up effluent-some appreciation of the real exchange rate (Figure 1.9 treatment plants.and Annex, Table 7), and sector specific developmentsare all believed to have played a role but it is difficult

Figure 1.8: Export Growth, 1990-96 Figure 1.9: Exchange Rate Movements(seaon.ally adjusted, year-onyear grwoth in percent based on US$)

150.0 37.036.0

140.0 35.0

130.0 ~~~~~~~~~~~~~34.033.Oa

25.U >t __vEw-,,wa1 < S-1300- < -6- < ---- i -32.04% ~~~~~~~~~~~~s31.0~

ffi 1>0 ts, M \ ,s, 5 f s4\ >*t, e } _ ] l0 0 >30.0_s.o \.5 * ' :\ . t -- RER - - -REER EXR |29.0

100.0 28.0

Note: * Cosr iros of Cl Hons KooH . onoKn sig . Kart. M-. IsM . Pth,i`pFI es Z A ZS.ir".nw onsd Ttoai. Sotarce: IMF.So-rece IMF. teteiatiosil Fbraciial Sato. s1s.

6 Chapter 1. Recent Economic Developments

1.15 The growth of the dollar value of imports and services and economic regulator, is one of India'sduring 1995-1996 reflected the fluctuations of the US most fundamental structural changes sincedollar. After growing by 30 percent in 1995-96, Independence. The liberalization of the economy hasimports rose by only 7.4 percent in dollar terms over opened to the private sector areas previously theApril to December 1996-97, in spite of a 34 percent exclusive domain of the public sector--such as heavyincrease in oil imports. Non-oil imports actually manufacturing, banking., civil aviation,declined by I percent due to a fall in capital goods telecommunications, power generation andimports. distribution, ports, and roads. Equally important, the

liberalization of the economy has reduced distortions1.16 In 1996-97, increased private transfers helped and increased external and internal competition.offset a rise in the trade deficit (by US$500 million) Agriculture's terms of trade have improved. Led byand kept the current account deficit at 1.1 percent of commercial crops, agricultural commodities are one ofGDP in 1996-97, from 1.8 percent in 1995-96--well India's fastest growing exports. In manufacturing,below what the government considers sustainable (2 Indian firms have restructured and upgraded theirpercent). industrial basis, often throug;h alliances with foreign

firms. There is growing presence of multi-nationals.1.17 The capital account remains strong. As in Indicative of improved product quality, the number of