INDIAN BANKING INDUSTRY Banking in India originated in the last decades of the 18th century. The oldest bank in existence in India is the State Bank of India, a government-owned bank that traces its origins back to June 1806 and that is the largest commercial bank in the country. Central banking is the responsibility of the Reserve Bank of India, which in 1935 formally took over these responsibilities from the then Imperial Bank of India, relegating it to commercial banking functions. After India's independence in 1947, the Reserve Bank was nationalized and given broader powers. In 1969 the government nationalized the 14 largest commercial banks; the government nationalized the six next largest in 1980. Currently, India has 96 scheduled commercial banks (SCBs) - 27 public sector banks (that is with the G overnment of India holding a stake), 31 private banks (these do not have g overnment stake; they may be publicly listed and traded on stock exchanges) and 38 foreign banks. They have a combined network of over 53,000 branches and 17,000 ATMs. According to a report by IC RA Limited, a rating agency, the public sector banks hold over 75 percent of total ass ets of the banking industry, with the private and foreign banks holding 18.2% and 6.5% respectively

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 1/53

INDIAN BANKING INDUSTRY

Banking in India originated in the last decades of the 18th century. The oldest bank in existence

in India is the State Bank of India, a government-owned bank that traces its origins back to June

1806 and that is the largest commercial bank in the country. Central banking is the

responsibility of the Reserve Bank of India, which in 1935 formally took over these

responsibilities from the then Imperial Bank of India, relegating it to commercial banking

functions. After India's independence in 1947, the Reserve Bank was nationalized and given

broader powers. In 1969 the government nationalized the 14 largest commercial banks; the

government nationalized the six next largest in 1980. Currently, India has 96 scheduled

commercial banks (SCBs) - 27 public sector banks (that is with the Government of India holding

a stake), 31 private banks (these do not have government stake; they may be publicly listed and

traded on stock exchanges) and 38 foreign banks. They have a combined network of over

53,000 branches and 17,000 ATMs. According to a report by ICRA Limited, a rating agency, the

public sector banks hold over 75 percent of total assets of the banking industry, with the

private and foreign banks holding 18.2% and 6.5% respectively

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 2/53

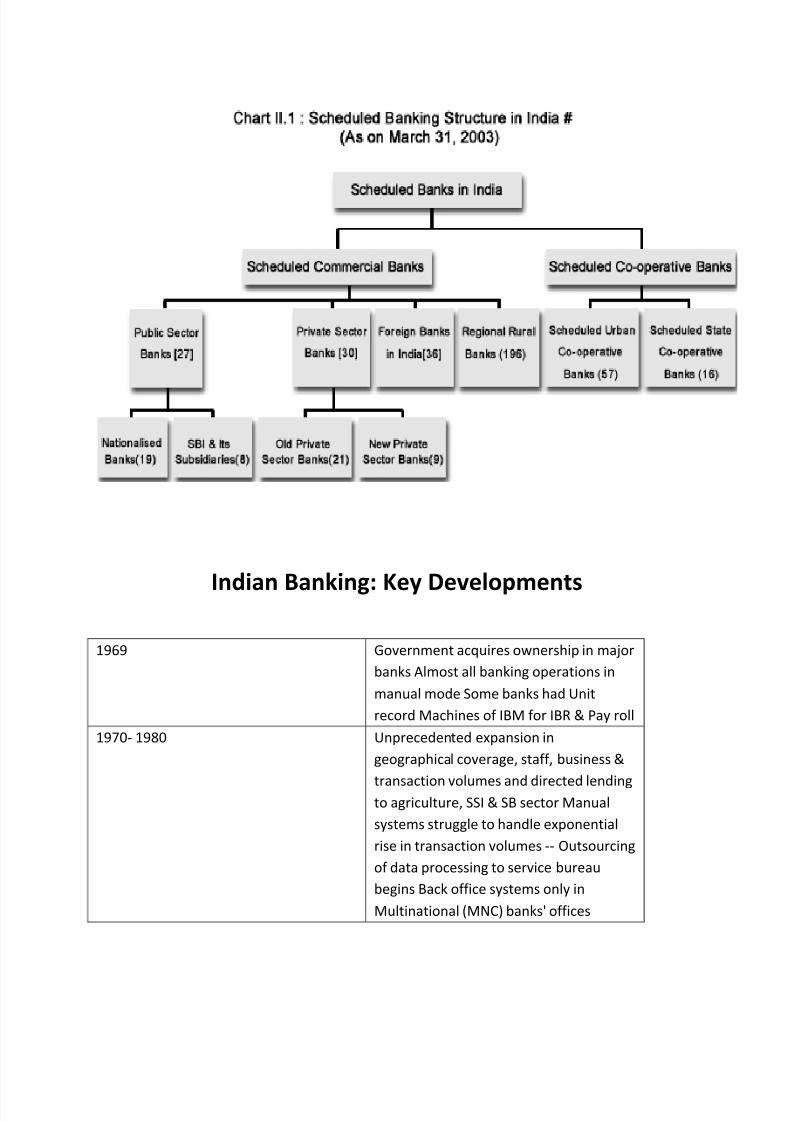

Indian Banking: Key Developments

1969 Government acquires ownership in major

banks Almost all banking operations in

manual mode Some banks had Unit

record Machines of IBM for IBR & Pay roll

1970- 1980 Unprecedented expansion in

geographical coverage, staff, business &

transaction volumes and directed lendingto agriculture, SSI & SB sector Manual

systems struggle to handle exponential

rise in transaction volumes -- Outsourcing

of data processing to service bureau

begins Back office systems only in

Multinational (MNC) banks' offices

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 3/53

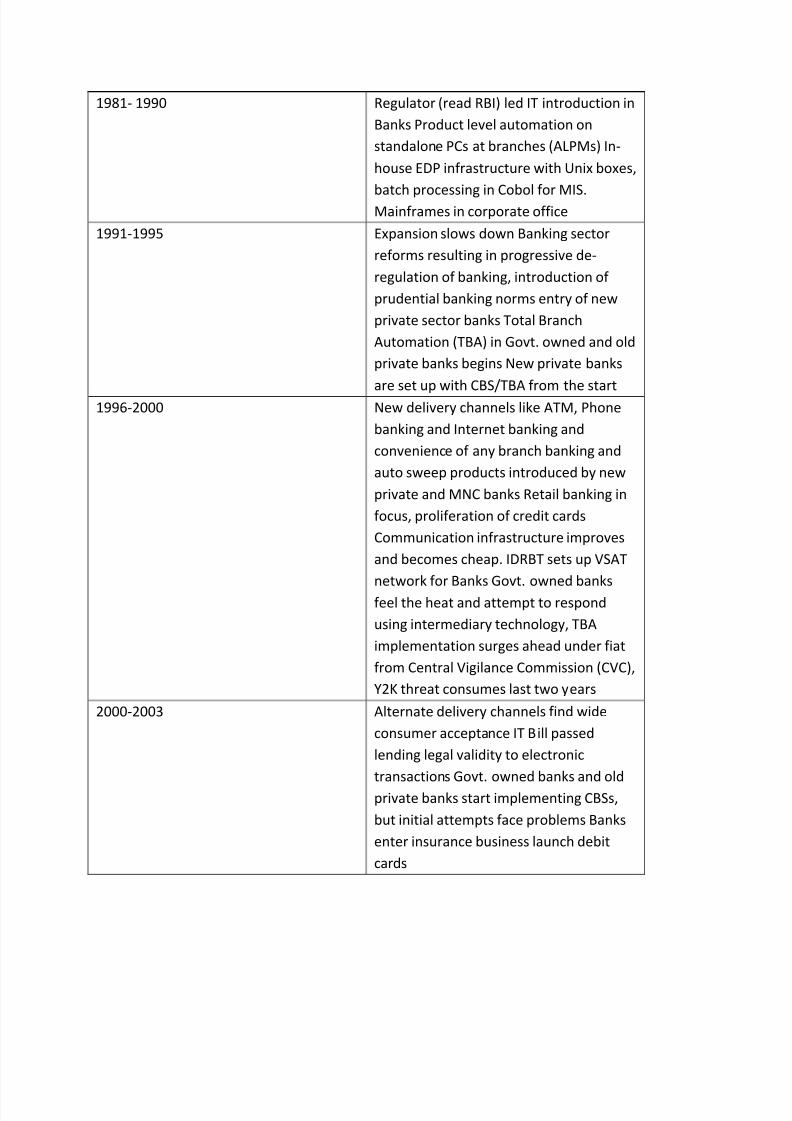

1981- 1990 Regulator (read RBI) led IT introduction in

Banks Product level automation on

standalone PCs at branches (ALPMs) In-

house EDP infrastructure with Unix boxes,

batch processing in Cobol for MIS.Mainframes in corporate office

1991-1995 Expansion slows down Banking sector

reforms resulting in progressive de-

regulation of banking, introduction of

prudential banking norms entry of new

private sector banks Total Branch

Automation (TBA) in Govt. owned and old

private banks begins New private banks

are set up with CBS/TBA from the start1996-2000 New delivery channels like ATM, Phone

banking and Internet banking and

convenience of any branch banking and

auto sweep products introduced by new

private and MNC banks Retail banking in

focus, proliferation of credit cards

Communication infrastructure improves

and becomes cheap. IDRBT sets up VSAT

network for Banks Govt. owned banks

feel the heat and attempt to respond

using intermediary technology, TBA

implementation surges ahead under fiat

from Central Vigilance Commission (CVC),

Y2K threat consumes last two years

2000-2003 Alternate delivery channels find wide

consumer acceptance IT Bill passed

lending legal validity to electronic

transactions Govt. owned banks and old

private banks start implementing CBSs,

but initial attempts face problems Banks

enter insurance business launch debit

cards

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 4/53

Major Developments

The State Bank of India (SBI) has posted a net profit of US$ 1.56 billion for the nine

months ended December 2009, up 14.43 per cent from US$ 175.4 million posted in the

nine months ended December 2008. The SBI is adding 23 new branches abroad bringing

its foreign-branch network number to 160 by March 2010. This will cement its leading

position as the bank with the largest global presence among local peers. Amongst the

private banks, Axis Bank's net profit surged by 32 per cent to US$ 115.4 million on 21.2

per cent rise in total income to US$ 852.16 million in the second quarter of 2009-10,

over the corresponding period last year. HDFC Bank has posted a 32 per cent rise in its

net profit at US$ 175.4 million for the quarter ended December 31, 2009 over the figure

of US$ 128.05 million for the same quarter in the previous year.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 5/53

INTRODUCTION TO NPA

MEANING OF NPA

Non Performing Asset means an asset or account of borrower, which has been classified

by a bank or financial institution as sub-standard, doubtful or loss asset, in accordance

with the directions or guidelines relating to asset classification issued by RBI. An amountdue under any credit facility is treated as "past due" when it has not been paid within 30

days from the due date. Due to the improvement in the payment and settlement

systems, recovery climate, up gradation of technology in the banking system, etc., it was

decided to dispense with 'past due' concept, with effect from March 31, 2001.

Accordingly, as from that date, a Non performing asset (NPA) shell be an advance where

1] Interest and /or installment of principal remain overdue for a period of more than

180 days in respect of a Term Loan,

2] The account remains 'out of order' for a period of more than 180 days, in respect of

an overdraft/ cash Credit(OD/CC),

3] The bill remains overdue for a period of more than 180 days in the case of bills

purchased and discounted,

4] Interest and/ or installment of principal remains overdue for two harvest seasons but

for a period not exceeding two half years in the case of an advance granted for

agricultural purpose, and

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 6/53

5] Any amount to be received remains overdue for a period of more than 180 days in

respect of other accounts. The bill remains overdue for a period of more than 90 days in

the case of bills purchased and discounted,

6] Interest and/ or installment of principal remains overdue for two harvest seasons but

for a period not exceeding two half years in the case of an advance granted for

agricultural purpose.

7] Any amount to be received remains overdue for a period of more than 90 days in

respect of other accounts.

ASSET CLASSIFICATION

Assets are classified into following four catagaries

A] Standard Asset

B] Sub-Standard Asset

C] Doubtful Asset

D] Loss Asset

Standard Asset:-

Standard assets are the ones in which the bank is receiving interest as well as the

principal amount of the loan regularly from the customer. Here it is also very important

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 7/53

that in this case the arrears of interest and the principal amount of loan do not exceed

90 days at the end of financial year. If asset fails to be in category of standard asset that

is amount due more than 90 days then it is NPA and NPAs are further need to classify in

sub categories.

From the year ending 31.03.2000, the banks should make a general provision of a

minimum of 0.40 percent on standard assets on global loan portfolio basis.

The provisions on standard assets should not be reckoned for arriving at net NPAs.

The provisions towards Standard Assets need not be netted from gross advances but

shown separately as 'Contingent Provisions against Standard Assets' under 'Other

Liabilities and Provisions - Others' in Schedule 5 of the balance sheet.

Banks are required to classify non-performing assets further into the following three

categories based on the period for which the asset has remained non-performing and

the reasonability of the dues:

1] Sub-standard Assets

2] Doubtful Asset

3] Loss Asset

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 8/53

Sub-standard Asset:-

With effect from 31 March 2005, a substandard asset would be one, which has

remained NPA for a period less than or equal to 12 month. The following features are

exhibited by substandard assets: the current net worth of the borrowers / guarantor or

the current market value of the security charged is not enough to ensure recovery of the

dues to the banks in full; and the asset has well-defined credit weaknesses that

jeopardize the liquidation of the debt and are characterized by the distinct possibility

that the banks will sustain some loss, if deficiencies are not corrected.

Provisioning norms:

A general provision of 10 percent on total outstanding should be made without making

any allowance for DICGC/ECGC guarantee cover and securities available.

Doubtful Assets:

A loan classified as doubtful has all the weaknesses inherent in assets that were classified as

sub-standard, with the added characteristic that the weaknesses make collection or liquidation

in full, on the basis of currently known facts, conditions and values highly questionable and

improbable. With effect from March 31, 2005, an asset would be classified as doubtful if it

remained in the sub-standard category for 12 months.

Provisioning Norms::

100 percent of the extent to which the advance is not covered by the realisable value of

the security to which the bank has a valid recourse and the realisable value is estimated

on a realistic basis.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 9/53

In regard to the secured portion, provision may be made on the following basis, at the

rates ranging from 20 percent to 50 percent of the secured portion depending upon the

period for which the asset has remained doubtful:

Period for which the

advance has been

considered as doubtful

Provision requirement (%)

Up to one year 20

One to three years 30

More than three years:

(1) Outstanding stock of

NPAs as on March 31, 2004.

(2) Advances classified as

doubtful more than three

years on or after April 1,

2004.

60% with effect from March

31, 2005. 75% effect from

March 31, 2006. 100% with

effect from March 31, 2007.

Additional provisioning consequent upon the change in the definition of doubtful assets

effective from March 31, 2003 has to be made in phases as under:

i. As on31.03.2003, 50 percent of the additional provisioning requirement on the assets which

became doubtful on account of new norm of 18 months for transition from sub-standard asset

to doubtful category.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 10/53

ii. As on 31.03.2002, balance of the provisions not made during the previous year, in addition to

the provisions needed, as on 31.03.2002.

Banks are permitted to phase the additional provisioning consequent upon the reduction in the

transition period from substandard to doubtful asset from 18 to 12 months over a four year

period commencing from the year ending March 31, 2005, with a minimum of 20 % each year.

Loss Assets:

A loss asset is one which considered uncollectible and of such little value that its continuance as

a bankable asset is not warranted- although there may be some salvage or recovery value. Also,

these assets would have been identified as loss assets by the bank or internal or external

auditors or the RBI inspection but the amount would not have been written-off wholly.

Provisioning Norms

The entire asset should be written off. If the assets are permitted to remain in the books for anyreason, 100 percent of the outstanding should be provided for.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 11/53

0

5000

10000

15000

20000

25000

30000

35000

Standard Asset Sub-standard Asset Loss Asset Doubtful Asset

Public Sector Bank

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

Standard Asset Sub-standard Asset Loss Asset Doubtful Asset

Private Sector banks

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 12/53

TYPES OF NPA:

1. Gross NPA

2. Net NPA

Gross NPA:

Gross NPAs are the sum total of all loan assets that are classified as NPAs as per RBI guidelines

as on Balance Sheet date. Gross NPA reflects the quality of the loans made by banks. It

consists of all the nonstandard assets like as sub-standard, doubtful, and loss assets. It can be

calculated with the help of following ratio:

Gross NPAs Ratio =

Gross NPAs

------------------------

Gross Advances

Net NPA:

Net NPAs are those type of NPAs in which the bank has deducted the provision regarding NPAs.

Net NPA shows the actual burdenof banks. Since in India, bank balance sheets contain a huge

amount of NPAs and the process of recovery and write off of loans is very time consuming, the

provisions the banks have to make against the NPAs according to the central bank guidelines,

are quite significant. That is why the difference between gross and net NPA is quite high. It can

be calculated by following:

Net NPAs =

Gross NPAs Provisions

-------------------------------------

Gross Advances Provision

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 13/53

Impact of NPAs upon Banks

They erode current profits through provisioning requirements.

They result in reduced interest income.

They require higher provisioning requirements affecting profits and accretion to capital.

They limit recycling of funds, set in assets-liability mismatches, etc.

Adverse impact on Capital Adequacy Ratio.

ROE and ROA goes down because NPAs do not earn.

Banks rating gets affected.

Banks cost of raising funds goes up.

RBIs approval required for declaration of dividend if Net NPA ratio is above 3%.

Bad effect on Goodwill & equity value.

Drain on Profitability

Impact on capital adequacy

Adverse effect on credit growth as the bankers prime focus becomes zero percent risk

and as a result turn lukewarm to fresh credit.

Excessive focus on Credit Risk Management

High cost of funds due to NPAs.

Early Symptoms

Financial.

Operational and Physical.

Attitudinal Changes.

Others ( death of person , competition in the market etc.)

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 14/53

Factors contributing to N.P.A.

Poor Credit discipline

Inadequate Credit & Risk Management

Diversion of funds by promoters

Funding of non-viable projects

In the early 1990s PSBs started suffering from acute capital inadequacy and

lower/ negative profitability. The parameters set for their functioning did not

project the paramount need for these corporate goals.

The banks had little freedom to price products, cater products to chosen

segments or invest funds in their best interest

Since 1970s, the SCBs functioned as units cut off from international banking and

unable to participate in the structural transformations and new types of lending

products.

Audit and control functions were not independent and thus unable to correct

the effect of serious flaws in policies and directions

Banks were not sufficiently developed in terms of skills and expertise to regulate

the humongous growth in credit and manage the diverse risks that emerged in

the process

Inadequate mechanism to gather and disseminate credit information amongst

commercial banks

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 15/53

Effective recovery from defaulting and overdue borrowers was hampered on

account of sizeable overhang component arising from infirmities in the existing

process of debt recovery, inadequate legal provisions on foreclosure and

bankruptcy and difficulties in the execution of court decrees.

Underlying Reasons for NPAs in India

Internal Factors

Inefficiency in management

Slackness in credit management and monitoring

Lack of co-ordination among lenders.

Problem of bad credit appraisal.

Inappropriate Technology/technical problems

Funds borrowed for a particular purpose but not use for the said purpose.

Project not completed in time.

Poor recovery of receivables.

Excess capacities created on non-economic costs.

In-ability of the corporate to raise capital through the issue of equity or other debt

instrument from capital markets.

Business failures.

Diversion of funds for expansion\modernization\setting up new projects\ helping orpromoting sister concerns.

Willful defaults, siphoning of funds, fraud, disputes, management disputes, Mis-

appropriation etc.,

Deficiencies on the part of the banks viz. in credit appraisal, monitoring and follow-ups,

delay in settlement of payments\ subsidiaries by government bodies etc.,

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 16/53

External Factors

Recession.

Input / power shortage

Price escalation.

Exchange rate fluctuation

Accidents and natural calamities,

Liberalization of Economy/ removal of restrictions/reduction of tariffs.

Sluggish legal system.

Long legal tangles.

Changes that had taken place in labour laws

Lack of sincere effort & Industrial recession.

Scarcity of raw material, labour and other resources.

Shortage of raw material, raw material\input price escalation, power shortage,

industrial recession, excess capacity, natural calamities like floods, accidents.

Failures, nonpayment\ over dues in other countries, recession in other countries,

externalization problems, adverse exchange rates etc.

Government policies like excise duty changes, Import duty changes etc.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 17/53

Current Situation in Banking Industry

A] Public Bank:-

Asset quality in public sector banks have been going from bad to worse for last several years,

and it is not a new phenomenon. Unfortunately or fortunately management of all banks have

been manipulating the figures year after year in close nexus with team of auditors and officialsof Reserve Bank of India and that of Banking Division in Ministry of Finance to conceal bad

assets. They have put pressure on field official in branches and taught not to improve the

quality and take strong initiative to recover the money from bad borrowers but taught only

various tactics to conceal bad assets to reduce provisioning towards bad assets as per RBI

guidelines.

At corporate level top officials of banks including CMD and ED have used various false and fake

pleas such as global recession, interest rate hikes, bad monsoons, natural calamities etc to give

various reliefs to bad borrowers instead of tightening the screws to trap bad officials and badborrowers. Top management of bank management have never diagnosed the real causes of

bad assets whenever it is found to increase due to some reason or the other. Clever bank

management do not want to take action against erring official, corrupt sanctioning official

because they themselves are part of dirty game of bad lending. This is why bank management

have wrongly but willfully and invariably pleaded that if action is taking against credit officers

and top executives , credit growth will immensely suffer and they will not be in a position to

achieve the target set by Finance Minister.

After complete introduction of Core Banking Solution (CBS) in banks, Reserve bank of India

advised banks to calculate bad assets called as Non Performing assets (NPA) on common

terminology using advanced technology and not manually . Banks are slowing getting pressure

to assess their quality of assets through automated system taking advantage of CBS technology.

Since management of banks find now difficult to conceal bad assets under CBS oriented NPA

assessment system, total of bad assets is now being exposed in Balance sheet and it has

reached a level of 3% of total advances.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 18/53

It is to be noted here that NPA percentage is still more than what it has been revealed during

last few quarters. Still banks have not declared their entire NPA and after taking RBI hidden

consent. Of course they are gradually exposing their bad assets and this is why quantum of bad

assets has not jumped to highest position in one time but it is rising quarter after quarter.Officials of RBI, top management of each PSB and official of Ministry of Finance all know very

well that actual quantum of bad assets in government banks is far more than 5% of total

advances. In more than 25% of three year old branches gross NPA is more than 25% of total

advances. There are many such branches where gross NPA is even more than 50% of total

advances.

Clever bank management are trying their best to show minimum percentage of gross NPA by

either manipulating the system secretly or by resorting to fresh lending by opening new

branches and resorting to fresh bulk lending to big corporate, to real estate sector and to

mutual funds so that total advances in banks increases which in turn reduces percentage of

Gross NPA compared to Total Advances. But this story will not help for longer period until there

is adequate improvement in quality and moral integrity of credit sanctioning authority , honesty

in promotion processes in banks ,improvement in legal machineries which may help in recovery

from willful defaulters , tightening of screws on Chartered Accountants , Valuers and official of

rating agencies and change in attitude of politicians. Bank management has to increase number

of staff in branches, reduce staff at administrative offices and award honest officers by stopping

and punishing corrupt officers who were rising in their career through unfair ways and means.

Till now bank management has not tried to cure the real disease and at the same time

government of India have also not improved the quality of legal system and not tried to

inculcate good culture in politicians who are using bank loan to enhance their personal wealth

and to increase their vote banks.

It is very sad that all the time when proportion of bad assets increases in banks , management

of banks accuse global recession, interest rate hike, bad monsoon, natural calamities etc but

not punish the real culprit. It is remarkable here that when most of top official have occupied

the top post and come through bad routes and when they have themselves created and

accumulated bad assets in their banks they are not in a position to punish the real culprit and

hence they are searching always some weak scapegoat , some lame excuses and pleading some

irrelevant reasons before MOF for deteriorating quality of bad assets in banks.

Million dollar questions is Who will bell the cat when even officials in RBI and MOF are equally

weak and guilty. System is not corrupt but corruption has become the system in banks. Not

only banks but all other government departments including judiciary are also victim of same

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 19/53

disease. It is therefore not surprising that public demand led by Anna for strong Lokpal Bill is

gaining momentum month after month, day after day and none can stop this.Government can

torture Anna, Ramdeo and their followers but cannot stop public revolt without punishing

corrupt officials and corrupt politicians.

t is true that net interest margin has gone up slightly because Public sector banks in general

have stopped giving preferential higher rate of interest to bulk depositors. But this is one time

phenomenon. Cost of deposit will slowly go up because banks have during last year increased

deposit interest rate many times for retail depositors and because of probable increase in

savings rate. But banks in general will not like to raise interest on their advances to compete in

the market and to abide by government directive or under pressure of Ministry of Finance or to

extend preferred rate to preferred borrowers who extend golden gifts to officials of bank. As a

result yield on advances will come down and hence NIM will also see considerable erosion.

Provisioning will go up as bad assets grow and profit will come down and government will have

to infuse capital time and again to fulfill Basel norms of Capital adequacy Ratio.

Obviously when credit growth coming down, NIM s under pressure ,ratio of NPA is going up

quarter after quarter , provisioning need is increasing and other income is shrinking, future of

not only SBI but of all public sector bank appears to be bleak. Other banks have too published

their balance sheet for the September quarter registering growth in bad assets, increase in

provisioning and fall in profit. Still RBI officials and MOF say that health of Indian bank is good.

It is worthwhile to mention here that total of bad assets in PS banks as on 30th September 2011

has crossed one trillion rupees. Even Moody had downgraded rating of SBI and in last few days

Moody lowered its outlook on banking system, showing slowing credit growth and concernedabout asset quality..

B] Private Banks:-

The gross Non Performing Assets (NPA) of the new private sector banks was much higher than

that of the public sector banks in the country. ''The percentage of NPAs to gross advances for

public sector banks was 2.27 per cent, while the same for new private sector banks was 3.22

per cent as on March this year.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 20/53

International NPA status

China

A] Causes

1. Moral Hazard: The SOEs believe that there the government will bail them out in case

of trouble and so they continue to take high risks.

2. Bankruptcy laws favour borrowers and law courts are not reliable enforcement

vehicles.

3. Political and social implications of restructuring big SOEs force the government to

keep them afloat.

4. Banks are reluctant to lend to the private enterprises due to

a. Non-standard accounting practises

b. While an NPA of an SOE is financially undesirable, an NPA of a private

enterprise is both financially and politically undesirable.

Measures

1. Reducing risk by strengthening banks, raising disclosure standards and spearheading

reforms of the SOEs by reducing their level of debt 8

2. Laws were passed allowing the creation of asset management companies, foreign

equity participation in securitisation and asset backed securitisation.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 21/53

Thailand

A] Causes

1. Liberalised capital and current account and external borrowings with inaccurate

assessment of exchange rate risk and risk of capital flight in a crisis.

2. A legal system that made credit recovery time consuming and difficult.

3. Real estate speculators look massive loans projecting high growth in demand and

prices of properties. When this did not materialise all the loans went bad.

B] Measures

1. Amendments were made to the Bankruptcy Act.

2. Corporate Debt Restructuring Advisory Commission was set up for the takeover

and restructuring of banks.

Korea

A] Causes

1. Directed credit: Protracted periods of interest rate control and selective credit

allocations gave rise to an inefficient distribution of funds.

2. The compressed growth policy via aggressive, leveraged expansion worked well

as long as the economy was growing and the ROI exceeded the cost of capital.

3. Lack of Monitoring Banks relied on collaterals and guarantees in the allocation of

credit, and little attention was paid to earnings performance and cash flows.

B] Measures

1. Speed of Action - The speedy containment of systemic risk and the domestic credit

crunch problem with the injection of large public funds for bank recapitalization were

critical steps towards normalizing the financial system.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 22/53

2. Corporate Restructuring Vehicles (CRVs) and Debt/Equity Swaps were used to

facilitate the resolution of bad loans.

Japan

A] Causes

1. Investments were made real estate at high prices during the boom. The recession

caused prices to crash and turned a lot of these loans bad.

2. Legal mechanisms to dispose bad loans were time consuming and expensive and

NPAs remained on the balance sheet.

3. Expansionary fiscal policy measures administered to stimulate the economy

supported industrial sectors like construction and real estate, which may have further

exacerbated the problem.

B] Measures

1. Amendment of foreign exchange control law (l997) and the threat of suspension of banking

business in case of failure to satisfy the capital adequacy ratio prescribed.Legislation to improve

information flow has been passed.

2. Accounting standards Major business groups established a private standardsettingvehicle

for Japanese accounting standards (2001) in line with internationalstandards.

3. Government Support - The governments committed public funds to deal with banking

sector weakness.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 23/53

State Bank of India

State Bank of India is the biggest and the leader bank in our country. SBI is treated as largest

bank because of its highest business profile and highest number of branches and it is called as

leader bank among public sector banks because other banks follow what normally SBI do. It

may be interest rate policy or loan policy or branch expansion policy, SBI normally shows the

route to other bank. In the last week RBI deregulated saving interest rate and a few privatebanks raised interest rate on saving s deposit. But since SBI did not increase savings interest

rate other banks are also silent on this issue.

Further SBI claims to be one of top ranked global banks and our government feels proud for it. I

however feel that SBI may in near future become one of the most critically sick and sinking

bank like Lehman Brother. Moreover when assets of bank like SBI starts ringing alarm signal,

one can very well imagine the worst scenario prevailing in other Public sector banks. Credit

growth and deposit growth, both have come down in SBI whereas NPA has gone up from

3.38%last year to 4.19% this September. Position of other banks is also bad but their exposurewill take place only when fully adopt CBS system and applies honestly prudential norms of

income recognition and asset classification as per system only.

State Bank of India, the country's top lender, beat estimates with a 12.40 per cent rise in

quarterly net profit but a rise in non-performing assets disappointed investors and its stock was

down 5 per cent after the results.

Worries about worsening asset quality in Asia's third-largest economy prompted Moody's

Investors Service earlier on Wednesday to cut its outlook on the Indian banking sector to

"negative" from "stable."

Net non-performing assets at SBI increased to 2.04 percent of total assets at the end of

September from 1.70 percent a year earlier, spooking investors.

"It is the increase in NPAs (non-performing assets) that hit the stocks today. It is a concern for

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 24/53

the entire sector," said Arun Khurana, fund manager at UTI Banking Fund.

However, going forward we expect pain from legacy NPAs to subside," he added.

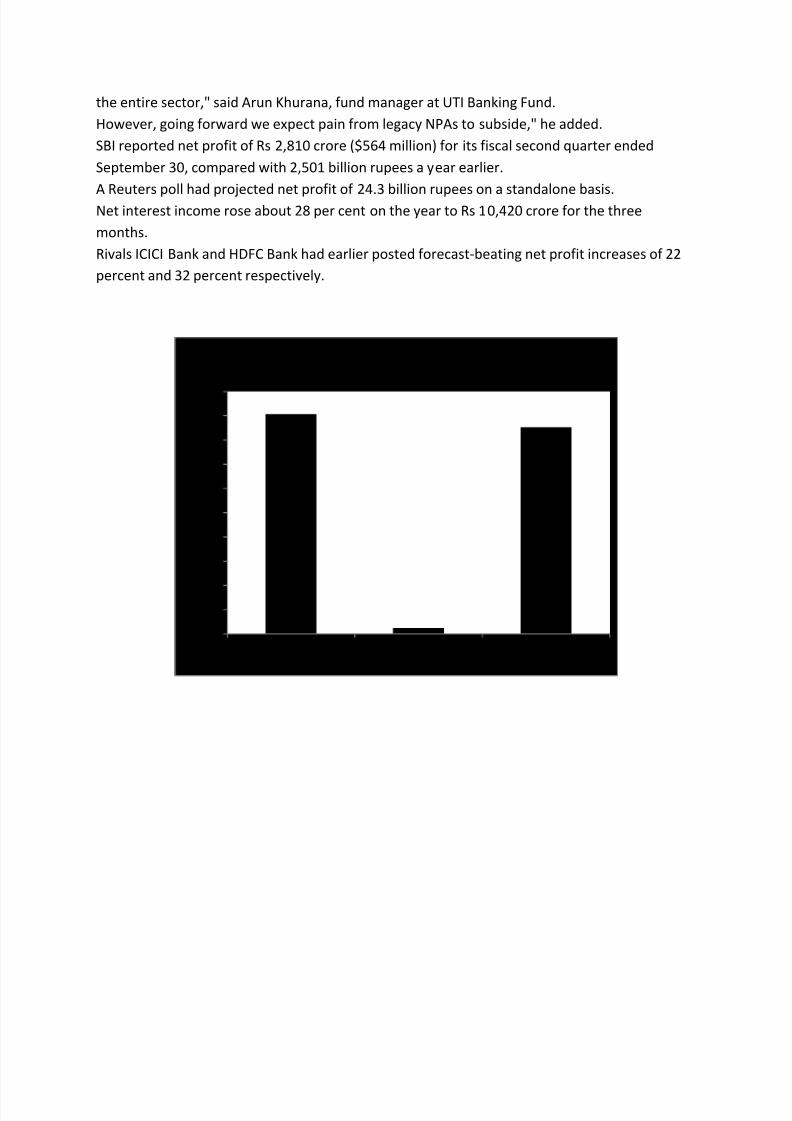

SBI reported net profit of Rs 2,810 crore ($564 million) for its fiscal second quarter ended

September 30, compared with 2,501 billion rupees a year earlier.

A Reuters poll had projected net profit of 24.3 billion rupees on a standalone basis.Net interest income rose about 28 per cent on the year to Rs 10,420 crore for the three

months.

Rivals ICICI Bank and HDFC Bank had earlier posted forecast-beating net profit increases of 22

percent and 32 percent respectively.

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

Priority sector Public sector non-priority sector

SBI

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 25/53

Bank of Maharashtra

Asset quality

Gross NPA stood at 3.46% and the Net NPA at 2.02%

Total Cash Recoveries in Non Performing Assets is Rs.96.14 crore of which the recovery in

written off accounts was at Rs.11.30 crore.

NPA Provision Coverage Ratio improved from 52.38% to 54.70% on Y-o-Y basis.

Bank of Maharashtra net dips on higher NPA provisioning

Bank of Maharashtra posted a Q3 FY 11 net profit of Rs 90.25 crore, a 20 per cent dip over the

corresponding quarter of the previous fiscal (Rs 112 crore) largely on account of higher

provisioning for NPAs.

Depreciation of Rs 28.24 crore on investments (-13.1 crore in the same period last year) and a

drop in its treasury income to Rs 12.8 crore from Rs 30.99 crore also impacted the bottom line.

The bank provided Rs 117.81 crore for NPA provision coverage during the quarter ended

December 31, 2010, against Rs 46.66 crore in Q3 FY 10.

The coverage now stands at 60.02 per cent and will be 70 per cent by September 2011.

Mr A. S. Bhattacharya, Chairman and Managing Director, said the bank will focus on recoveries

and on developing the mid-corporate business segment.

A separate cell has been established in the Central Office for the purpose of loans from Rs 5-50

crore. Five micro asset recovery cells have been set up in Aurangabad, Latur, Nashik, Satara and

Solapur to follow up on small accounts of Rs 10 lakh and below.

Our current NPAs stand at Rs 1,377 crore, and 64 per cent of these are loans below Rs 10 lakh.These five cells recovered Rs 10 crore in one week, Mr Bhattacharya said, adding that the

target was to recover Rs 110 crore by March 2011.

Five more such cells will be set up as the bank hopes to bring the NPAs down to Rs 1,000 crore

by September-end, he said.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 26/53

During the quarter under review, BoM's total business crossed the one-lakh crore mark and

stood at Rs 1,06,514.98 crore on December 31, 2010.

One of the priorities for the new Chairman and Managing Director of Bank of Maharashtra, Mr

A.S. Bhattacharya, would be to bring down the bank's high non-performing asset (NPA) level in

the next six months.

our gross NPAs at 3.58 per cent may be one of the highest in the industry, and we want to

reduce it to less than 3 per cent by March, he told Business Line. He hoped to reduce net NPAs

to less than 2 per cent, from the current 2.18 per cent.

NPAs were high on account of Rs 120 crore of agriculture debt waiver added during the quarter.

And now all NPAs are system driven, and an alarm is generated by the system when any

account shows signs of sickness, he pointed out. For loans of Rs 1 lakh and below, any signs of

sickness would be addressed by the branch office, while the regional office would addresssickness in loans of Rs 1 lakh to Rs 10 lakh and the head office will handle loans above Rs 10

lakh.

According to him, 64 per cent of the bank's NPAs was from small and marginal borrowers, and

to arrest gross NPAs and net NPAs, we plan to set up five micro-asset recovery units in

Maharashtra for the recovery of small loans, he said. The exclusive teams will only work on

recovery of these loans.

Since the bank has over 900 of its 1,500 branches in Maharashtra, these units would be set up

there, and if the experiment is successful, we will set up such units in Bangalore, Hyderabadand Uttar Pradesh.As of now, the bank is not looking at Chennai, but if small loan recovery

does not happen in Chennai, we will set up a unit there, said Mr Bhattacharya.

On the dip in profits in the second quarter of this fiscal, he pointed out that provisioning was

doubled during the quarter to strengthen the bank's balance sheet.

The bank was also hopeful of growing its net interest margin to 2.7 per cent by the fiscal-end

from current levels of 2.54 per cent. With the bank's cost of deposits at 5.24 per cent now, Mr

Bhattacharya felt that it will increase as a result of the recent monetary policy.By March, he

expected it to be between 5.3 per cent and 5.35 per cent.

This would put pressure on net interest margins, he admitted, adding that the silver-lining was

that the bank's yield on advances, which was 9.14 per cent during the second quarter, would

increase to 9.6 per cent soon.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 27/53

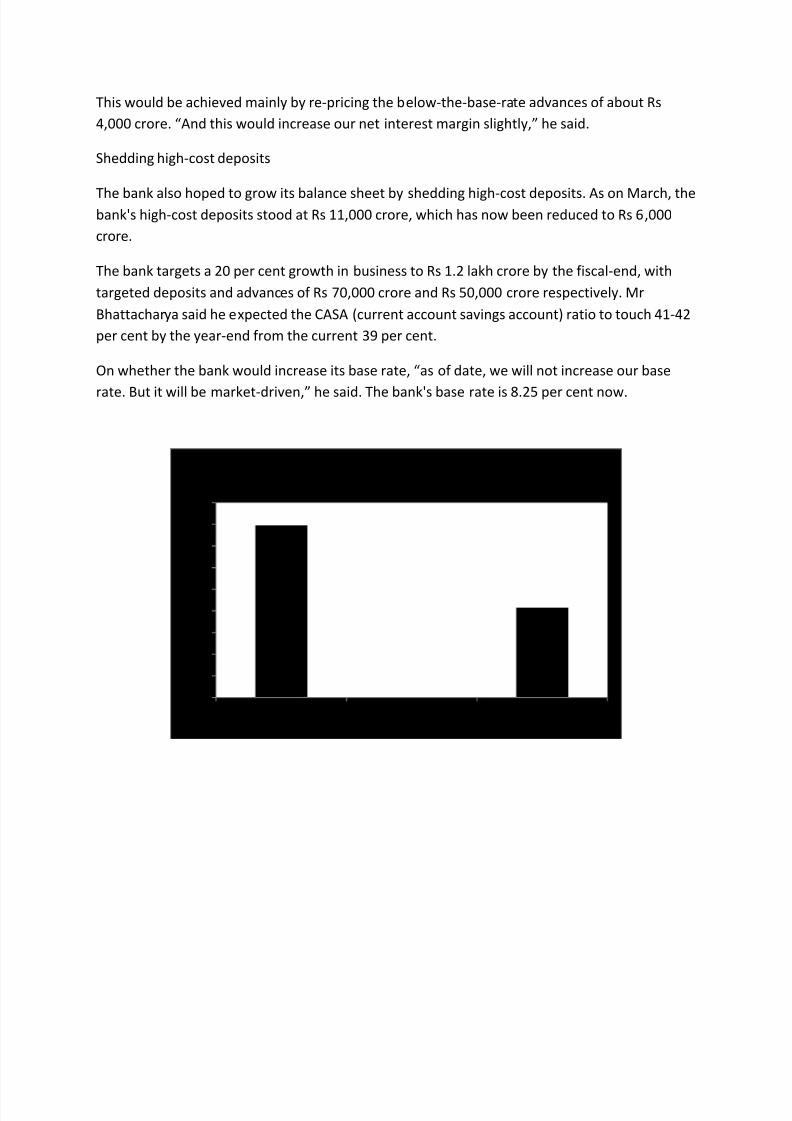

This would be achieved mainly by re-pricing the below-the-base-rate advances of about Rs

4,000 crore. And this would increase our net interest margin slightly, he said.

Shedding high-cost deposits

The bank also hoped to grow its balance sheet by shedding high-cost deposits. As on March, thebank's high-cost deposits stood at Rs 11,000 crore, which has now been reduced to Rs 6,000

crore.

The bank targets a 20 per cent growth in business to Rs 1.2 lakh crore by the fiscal-end, with

targeted deposits and advances of Rs 70,000 crore and Rs 50,000 crore respectively. Mr

Bhattacharya said he expected the CASA (current account savings account) ratio to touch 41-42

per cent by the year-end from the current 39 per cent.

On whether the bank would increase its base rate, as of date, we will not increase our base

rate. But it will be market-driven, he said. The bank's base rate is 8.25 per cent now.

0

100

200

300

400

500

600

700

800

900

Priority sector Public sector non-priority sector

BOM

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 28/53

Punjab National Bank

Punjab National Bank's gross non-performing assets may come down by Rs 300-400 crore in

January-March following the relaxation in infrastructure lending norms announced by

Reserve Bank of India in its annual monetary policy statement.

Our gross NPAs will come down to that extent. To that extent, provisioning on these

accounts will also fall but it may not have an impact on net profit in January-March," said a

senior official close to the development.

On April 29, in its annual monetary policy statement, RBI relaxed the norms on NPAs caused

by time overrun in commencement of commercial production in the case of infrastructure

projects to two years from one year earlier.

According to the new norms, banks will have to classify an infrastructure loan as a sub-

standard asset if the date of commercial production under the project extends beyond two

years after the date of completion of the project as originally envisaged.

The new norms have come into effect from March 31. According to analysts, Punjab

National Bank is likely to benefit the most from the prudential norms relaxation as it had

huge NPAs in this segment.

Most state-run banks will be benefited from relaxation of the norms, the bank official said.

High NPAs were a major cause of concern to the Delhi-based PNB. The bank's net NPAs rose

to 1.33 per cent in October-December from 0.42 per cent a year ago.

Chairman and Managing Director K C Chakrabarty had said at the time of announcing Oct-

Dec results that the bank aims to bring down net NPAs below 1 per cent by the end of

march.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 29/53

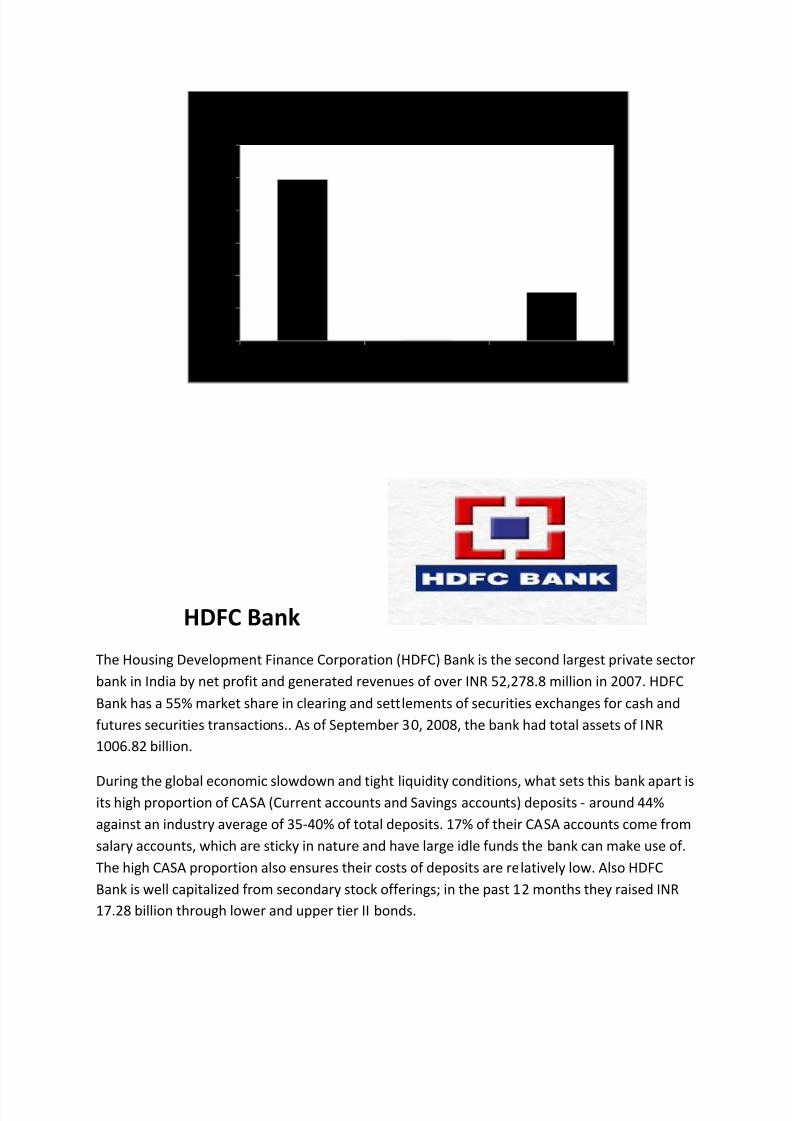

HDFC Bank

The Housing Development Finance Corporation (HDFC) Bank is the second largest private sector

bank in India by net profit and generated revenues of over INR 52,278.8 million in 2007. HDFC

Bank has a 55% market share in clearing and settlements of securities exchanges for cash and

futures securities transactions.. As of September 30, 2008, the bank had total assets of INR

1006.82 billion.

During the global economic slowdown and tight liquidity conditions, what sets this bank apart isits high proportion of CASA (Current accounts and Savings accounts) deposits - around 44%

against an industry average of 35-40% of total deposits. 17% of their CASA accounts come from

salary accounts, which are sticky in nature and have large idle funds the bank can make use of.

The high CASA proportion also ensures their costs of deposits are relatively low. Also HDFC

Bank is well capitalized from secondary stock offerings; in the past 12 months they raised INR

17.28 billion through lower and upper tier II bonds.

0

500

1000

1500

2000

2500

3000

Priority sector Public sector non-priority sector

PNB

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 30/53

On February 25, 2008 HDFC Bank agreed to buy Centurion Bank of Punjab. The combined entity

has the largest branch network in private banks in India, a strong deposit base of around INR

1220 billion and net advances of around INR 890 billion.

NPA

supported by a strong growth in its fee-based revenue and net interest incomes, private sector

lender, HDFC Bank ,has clocked a 31 per cent jump in its net profit in the third quarter.

Fee-based income grew by 12.4 per cent to Rs 723.7 crore (Rs 7.23 billion) in Q3 FY 10 as

compared to the year-ago period and emerged as a major contributor to the overall growth

along with the net interest income, Paresh Sukthankar, executive director, HDFC Bank said.

The net interest income (NII), during the quarter, went up by 12.4 per cent to Rs 2,223.9 crore,

(Rs 22.23 billion) driven by asset growth. The net interest margin of the lender improved to 4.3

per cent in Q3 as against 4.2 per cent in the year-ago period, Sukthankar said.

Sukthankar said the bank was hopeful to maintain the NIM, the spread between interest

earned and interest expended, between 4 per cent-4.3 per cent in FY10.

However, an expected hike in the RBI Cash Reserve Ratio in the near future and the apex bank's

directive to calculate savings deposit rates on a daily basis by April might put pressure on banks'

margins moving ahead, he said.

The lender also saw its non-performing assets declining slightly in the third quarter, enabling it

to lower the NPA provisioning in Q3, he said.

The bank provided Rs 437.9 crore (Rs 4.37 billion) for bad loans in Q3 as against Rs 465.4 crore

in the year-ago period. "As far as NPAs are concerned, all I can say that it does appear that the

worst is behind us. NPA formation seems to have slowed down," Sukhthankar said.

Gross non-performing assets as of December declined to 1.6 per cent of gross advances as

against 1.9 per cent a year-ago. HDFC Bank's gross advances expanded by 21 per cent in Q3

FY10 to Rs 1,21,051 crore (Rs 1210.51 billion) compared to a year-back, while growth in the

retail advances was at around 11 per cent.

However, the bank suffered a loss of Rs 26.5 crore (Rs 265 million) in its treausry portfolio as

against a profit of Rs 232.1 crore in the same quarter last year. Going by the current indications,

HDFC Bank expects to grow its loan book 3-5 per cent above the industry in FY10, Sukthankar

said, adding, it hopes to maintain a healthy growth both in its auto and home loan portfolios.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 31/53

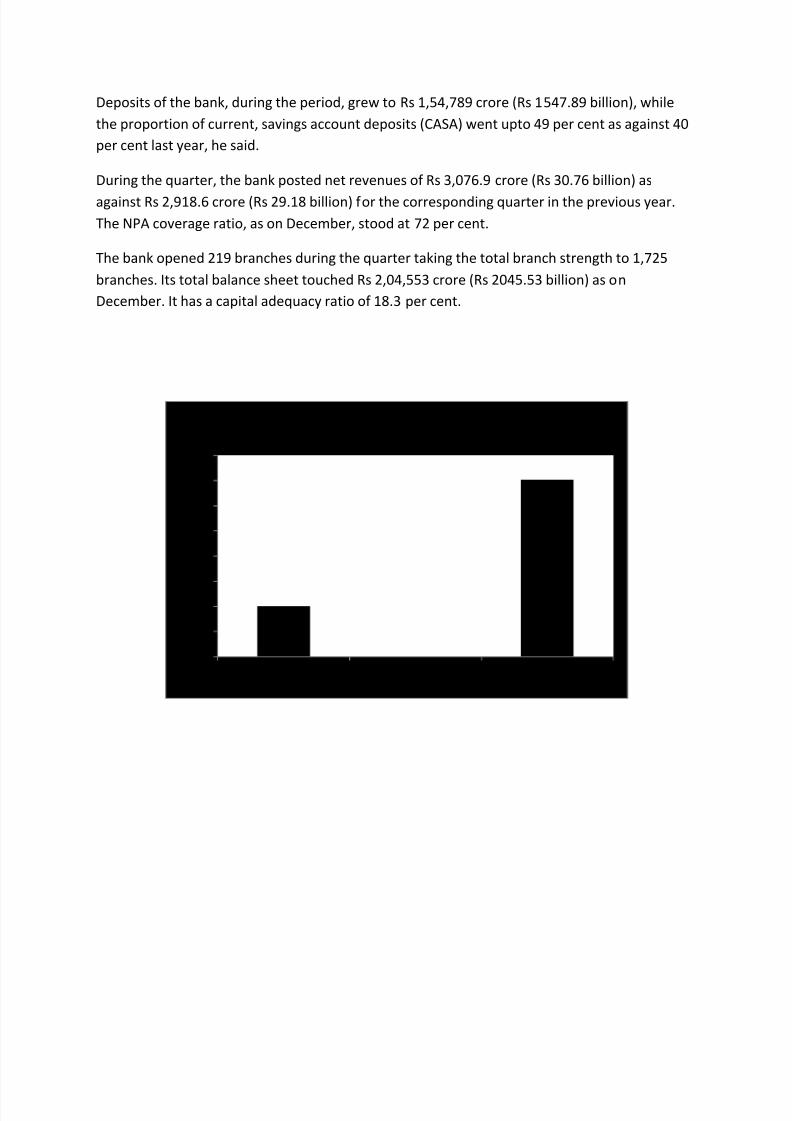

Deposits of the bank, during the period, grew to Rs 1,54,789 crore (Rs 1547.89 billion), while

the proportion of current, savings account deposits (CASA) went upto 49 per cent as against 40

per cent last year, he said.

During the quarter, the bank posted net revenues of Rs 3,076.9 crore (Rs 30.76 billion) as

against Rs 2,918.6 crore (Rs 29.18 billion) for the corresponding quarter in the previous year.

The NPA coverage ratio, as on December, stood at 72 per cent.

The bank opened 219 branches during the quarter taking the total branch strength to 1,725

branches. Its total balance sheet touched Rs 2,04,553 crore (Rs 2045.53 billion) as on

December. It has a capital adequacy ratio of 18.3 per cent.

0

200

400

600

800

1000

1200

1400

1600

Priority sector Public sector non-priority sector

HDFC

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 32/53

ICICI Bank

Even as ICICI Bank, the second largest commercial bank in the country, has cut down itsmaximum exposure to any industry from 15% to 12% of its total assets, the power sector has

replaced the chemical sector as the maximum generator of sticky assets for the bank in 2004-

05.

The non-performing assets out of the power sector in its pre-Dabhol revival phase has gone up

from over Rs 620 crore to Rs 737 crore in the reporting period. The power sector contributes

almost 21% of NPA for the bank. Next to power is the chemicals sector, which has created the

maximum amount of sticky assets. However, in absolute amount as well in percentage terms,

the share of the chemicals sector in the NPA chart has fallen during 2004-05. While in absolute

amount it has gone down to Rs 403 crore from Rs 747 crore, in percentage terms it has plunged

from 7.47% to 4.03% during the reporting period.

Textiles has continued to be the third largest sector in the NPA list. But surprisingly, one

category of exposure, 'other infra telecom', from zero level in 2003-04 has created Rs 214 crore

of sticky assets in 2004-05.

The improved situation in the iron & steel sector has pushed back the sector from the sixth (Rs

139 crore) position to 10th (Rs 67 lakh) position in 2004-05. The agriculture sector, which has

become the current focus of the bank has generated Rs 27 lakh worth of sticky assets in the

reporting period. The bank has also restructured its asset portfolio by having more exposures

for crude petroleum and refining, roads, ports, railways and telecommunication. Keeping its

retail lending and iron & steel business as the top two segments, it has reduced its exposure in

power, chemicals and engineering sector during 2004-05.

0

1000

2000

3000

4000

5000

6000

7000

8000

Priority sector Public sector non-priority sector

ICICI

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 33/53

Impact of NPA in banking sector on Indian Economy

Shares of State Bank of India (SBI) today plummeted by over 7% on the bourses, amid concerns

over a rise in the lender's non-performing assets (NPAs) and a rating downgrade of the entire

Indian banking sector by Moody's.

The country's largest PSU bank today reported its second-quarter results, wherein it disclosed a

rise in NPAs and also fell short of the market expectations for its overall financial performance.

Besides, global rating agency Moody's today downgraded its outlook on the Indian banking

system to "negative", from "stable" earlier.

Selling pressure was significant in the stocks of other financial sector companies as well.ICICIBank settled with a loss of 2.16%, HDFC Bank lost 1.50%, IDBI Bank fell by 3.19% and Union

Bank ended 2.10% lower.

The BSE banking index also dropped by 2.62%.

The shares of SBI opened on a positive note this morning, but slipped into the red after the

announcement of its quarterly results and the news of the Moody's rating action.

The stock settled 7.2% down at Rs 1,853.40 at the NSE, while it closed 6.76% lower at Rs

1,862.50 at the BSE.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 34/53

In the process, the company's market value dipped by over Rs 8,500 crore to Rs 1,18,268 crore.

Decline in the SBI stock was a major contributor in today's fall of 207.43 points in the market

benchmark Sensex.

Analysts said that the shares of SBI fell mainly on concerns of rise in NPAs, as its bad loans have

risen considerably in export-oriented units and metal industry.

"SBI reporting higher than expected NPA and Moody downgrade of Indian banking system to

negative were enough to create capitulation in the shares for the day," Inventure Growth and

Securities Head Research.

Moody's today downgraded the outlook of the Indian banking system on concerns related to

economic slowdown, which is affecting asset quality, capitalisation and profitability of the

banks.

With a 48.60% jump in net profit to Rs 3,470.43 crore for the Jul-Sep quarter, its gross NPA

increased to 4.19% of total assets at the end of September, from 3.38% a year ago.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 35/53

Management of NPA

Preventive measures

Formation of the Credit Information Bureau (India) Limited (CIBIL)

Release of Wilful Defaulters List. RBI also releases a list of borrowers with

aggregate outstanding of Rs.1 crore and above against whom banks have filed

suits for recovery of their funds

Reporting of Frauds to RBI

Norms of Lenders Liability framing of Fair Practices Code with regard to

lenders liability to be followed by banks, which indirectly prevents accounts

turning into NPAs on account of banks own failure

Risk assessment and Risk management

RBI has advised banks to examine all cases of wilful default of Rs.1 crore and

above and file suits in such cases. Board of Directors are required to review NPA

accounts of Rs.1 crore and above with special reference to fixing of staff

accountability.

Reporting quick mortality cases

Special mention accounts for early identification of bad debts. Loans and

advances overdue for less than one and two quarters would come under this

category. However, these accounts do not need provisioning

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 36/53

NPA MANAGEMENT RESOLUTION

Compromise Settlement Schemes

Restructuring / Reschedulement

Lok Adalat

Corporate Debt Restructuring Cell

Debt Recovery Tribunal (DRT)

Proceedings under the Code of Civil Procedure

Board for Industrial & Financial Reconstruction (BIFR)/ AAIFR

National Company Law Tribunal (NCLT)

Sale of NPA to other banks

Sale of NPA to ARC/ SC under Securitization and Reconstruction of Financial Assets and

Enforcement of Security Interest Act 2002 (SRFAESI)

Liquidation

Compromise Settlement Schemes

Banks are free to design and implement their own policies for recovery and write off

incorporation compromise and negotiated settlements with board approval

Specific guidelines were issued in May 1999 for one time settlement of small

enterprise sector.

Guidelines were modified in July 2000 for recovery of NPAs of Rs.5 crore and less as

on 31st March 2007.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 37/53

Restructuring and Rehabilitation

y Banks are free to design and implement their own policies for restructuring/

rehabilitation of the NPA accounts

y Reschedulement of payment of interest and principal after considering the Debt

service coverage ratio, contribution of the promoter and availability of security

Lok Adalats

y Small NPAs up to Rs.20 Lacs

y Speedy Recovery

y Veil of Authority

y Soft Defaulters

y Less expensive

Corporate Debt Restructuring

y The objective of CDR is to ensure a timely and transparent mechanism for

restructuring of the debts of viable corporate entities affected by internal and

external factors, outside the purview of BIFR, DRT or other legal proceedings

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 38/53

y The legal basis for the mechanism is provided by the Inter-Creditor Agreement (ICA).

All participants in the CDR mechanism must enter the ICA with necessary

enforcement and penal clauses.

y The scheme applies to accounts having multiple banking/ syndication/ consortium

accounts with outstanding exposure of Rs.10 crores and above.

y The CDR system is applicable to standard and sub-standard accounts with potential

cases of NPAs getting a priority.

y Packages given to borrowers are modified time & again

y Drawback of CDR Reaching of consensus amongst the creditors delays the process

DRT Act

y The banks and FIs can enforce their securities by initiating recovery proceeding

under the Recovery if Debts due to Banks and FI act, 1993 (DRT Act) by filing an

application for recovery of dues before the Debt Recovery Tribunal constituted

under the Act.

y On adjudication, a recovery certificate is issued and the sale is carried out by an

auctioneer or a receiver.

y DRT has powers to grant injunctions against the disposal, transfer or creation of

third party interest by debtors in the properties charged to creditor and to pass

attachment orders in respect of charged properties

y In case of non-realization of the decreed amount by way of sale of the charged

properties, the personal properties if the guarantors can also be attached and sold.

y However, realization is usually time-consuming

y Steps have been taken to create additional benches

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 39/53

National company law tribunal

y In December 2002, the Indian Parliament passed the Companies Act of 2002 (Second

Amendment) to restructure the Companies Act, 1956 leading to a new regime of

tackling corporate rescue and insolvency and setting up of NCLT.

y NCLT will abolish SICA, have the jurisdiction and power relating to winding up of

companies presently vested in the High Court and jurisdiction and power exercised

by Company Law Board

y The second amendments seeks to improve upon the standards to be adopted to

measure the competence, performance and services of a bankruptcy court by

providing specialized qualification for the appointment of members to the NCLT.

y However, the quality and skills of judges, newly appointed or existing, will need to

be reinforced and no provision has been made for appropriate procedures to

evaluate the performance of judges based on the standards

Sale of NPA to other banks

y A NPA is eligible for sale to other banks only if it has remained a NPA for at least two

years in the books of the selling bank

y The NPA must be held by the purchasing bank at least for a period of 15 months before

it is sold to other banks but not to bank, which originally sold the NPA.

y The NPA may be classified as standard in the books of the purchasing bank for a period

of 90 days from date of purchase and thereafter it would depend on the record of

recovery with reference to cash flows estimated while purchasing

y The bank may purchase/ sell NPA only on without recourse basis

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 40/53

y If the sale is conducted below the net book value, the short fall should be debited to

P&L account and if it is higher, the excess provision will be utilized to meet the loss on

account of sale of other NPA.

Sarfesi act 2002

y SARFESI provides for enforcement of security interests in movable (tangible or

intangible assets including accounts receivable) and immovable property without the

intervention of the court

y The bank and FI may call upon the borrower by way of a written legal notice to

discharge in full his liabilities within 60 days from the date of notice, failing which the

bank would be entitled to exercise all or any of the rights set out under the Act.

y Another option available under the Act is to takeover the management of the secured

assetsy Any person aggrieved by the measures taken by the bank can proffer an appeal to DRT

within 45 days after depositing 75% of the amount claimed in the notice.

y Chapter II of SARFESI provides for setting up of reconstruction and securitization

companies for acquisition of financial assets from its owner, whether by raising funds by

such company from qualified institutional buyers by issue of security receipts

representing undivided interest in such assets or otherwise.

y The ARC can takeover the management of the business of the borrower, sale or lease of

a part or whole of the business of the borrower and rescheduling of payments,

enforcement of security interest, settlement of dues payable by the borrower or take

possession of secured assets

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 41/53

y Additionally, ARCs can act as agents for recovering dues, as manager and receiver.

y Drawback differentiation between first charge holders and the second charge holders

Legal Aspects of NPA

Securitisation

The concept of securitisation has been adopted more recently from the

American financial system and has been described as processing of acquiring

financial asset and packaging the same for investments by several investors. The

term securitisation has not been defined as such, but has been used in certain

rules, regulations and notifications. In the recently enacted the Securitisation

and Reconstruction of Financial Assets and Enforcement of Security Interest Act,

2002 (for short the Securitisation Act) the term securitisation has been defined

as acquisition of financial assets by any securitisation company or

reconstruction company from any originator, whether by raising of funds by such

securitisation company or reconstruction company from qualified institutional

buyers by issue of security receipts representing undivided interests in such

financial assets or otherwise.

The Securitisation Act, 2002

The Securitisation Act has been enacted mainly for tackling the growing menace

non-performing assets by securitisation of assets by sale to ARC, which is to issue

of security receipts to the investor and for enforcement of security interest by

banks and financial institutions. Initially, many were delighted to find that the

securitisation process as a class has come to stay in the Indian legal system, and

the problem of the non-performing assets of banks and financial institution

would stand resolved since the banks and financial institutions would be able to

enforce its security interest without intervention of the courts. The quantum of

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 42/53

non performing assets has been growing by leaps and bounds and has been

playing havoc on the Indian financial system since as at the end of the year 2001

the total amount of outstanding NPAs stood at Rs.83,500/- crores. After

enactment of the Securitisation Act, 2002 the wilful defaulters cannot now hide

behind long-winded judicial process but at the same time the bank also cannotrecover dues arising out of underwriting commitments obligations and equity

finance by way of share subscriptions, so also the shares acquired by exercise of

option for conversion of loan into equity. The Securitisation Act, 2002 does not

also ensure or guarantee full recovery of the entire outstanding over dues fully.

In the result the financial health of the banks will not improve because, in

absence of adequate assets not more than 20 percent of NPAs would be

recovered by resorting to the provisions of the Securitisation Act, 2002. The IT

Tribunal ruling in case of Vishvapriya Financial Service and Securities Ltd would

jolt development of asset securitisation in autofinance and housing finance

sector. The company was utilising funds obtained from the investors for

deployment in fixed income security and had guaranteed fixed rate of return.

The contention of the company that it was only agent for the investors and has

evolved only a pay-through structure was not accepted by the tribunal, which

held that the company was liable for the withholding taxes on the payments

made to the investors.

RBI guidelines For NPA

RBI introduced, in 1992-93, the prudential norms for income recognition, asset

classification & provisioning IRAC norms in short in respect of the loan portfolio

of the UCBs. The objective, inter-alia, was to bring out the true picture of a banks

loan portfolio. The fallout of this momentous regulatory measure for the

managementof the UCBs was to divert its focus to profitability, which till then used

to be a low priority area for it. Asset quality assumed greater importance for the

UCBs when RBI introduced the Basel norms for Capita Adequacy from year-ended

March 31, 2002 in the aftermath of serious financial problems in the sector.

Maintenance of high quality credit portfolio continues to be a major challenge for

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 43/53

the UCBs, especially with RBI gradually moving towards convergence with more

stringent global norms for impaired assets.

A] The quality of a banks loan portfolio can impact its profitability, capital and

liquidity. Asset quality problems are at the root of other financial problems forbanks, leading to reduced net interest income and higher provisioning costs. If loan

losses exceed the Bad and Doubtful Debt Reserve, capital strength is reduced.

Reduced income means less cash, which can potentially strain liquidity. Market

knowledge that the bank is having asset quality problems and associated financial

conditions may cause outflow of deposits. Thus, the performance of a bank is

inextricably linked with its asset quality. Managing the loan portfolio to minimise

bad loans is, therefore, fundamentally important for a financial institution in todays

extremely competitive and market driven business environment. This is all the more

important for the UCBs, which are at a disadvantage vis-à-vis the commercial banks

in terms of professionalised management, skill levels, technology adoption and

effective risk management systems and procedures.

B] Management of NPAs begins with the consciousness of a good portfolio, which

warrants a better understanding of risks in lending. The Board has to decide a

strategy keeping in view the regulatory norms, the business environment, its market

share, the risk profile, the available resources etc. The strategy should be reflected

in Board approved policies and procedures to monitor implementation. The

essentialcomponents of sound NPA management are i) quick identification of NPAs,

ii) theircontainment at a minimum level and iii) ensuring minimum impact of NPAs

on the financials. A two-pronged strategy of preventing slippage of standard assets

NPA category and reducing NPAs through cash recovery, up gradation, compromise,

legal means etc., is called for.

2. Preventing NPAs

At the pre-disbursement stage, appraisal techniques of bank need to be sharpened.

All technical, economic, commercial, organizational and financial aspects of the

project need to be assessed realistically. Bankers should satisfy themselves that the

project is technically feasible with reference to technical know how, scale of

production etc. The project should be commercially feasible in that all background

linkages by way of availability of raw materials at competitive rates and that all

forward linkages by way of assured market are available. It should be ensured

assumptions on which the project report is based are realistic. Some projects are

born sick because of unrealistic planning, inadequate appraisal and faulty

implementation.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 44/53

As the initiative to sanction or reject the project proposal lies with the banker, he

can exercise his judgment judiciously. The banker should at the pre-sanction stage

notonly appraise the project but also the promoter his character and his capacity.

It is said that it is more prudent to sanction a 'B' class project with an 'A' class

entrepreneur than vice-versa. He has to ensure that the borrower complies with allthe terms of sanction before disbursement.

A major cause for NPA is fixation of unrealistic repayment schedule. Repayment

schedule may be fixed taking into account gestation or moratorium period,

harvesting season, income generation, surplus available etc. If the repayment

schedule is defective both with reference to quantum of instalment and period of

recovery, assets have a tendency to become NPA.

At the post-disbursement stage, bankers should ensure that the advance does not

become and NPA by proper follow-up and supervision to ensure both assets creation

and asset utilisation. Bankers can do either off-site surveillance or on site inspection

to detect whether the unit / project is likely to become NPA. Instead of waiting for

the mandatory period before classifying an asset as NPA, the banker should look for

early warning signals of NPA.

The following are the sources from which the banker can detect signals, which

need quick remedial action:

a) Scrutiny of accounts and ledger cards During a scrutiny of these, banker can

be on alert if there is persistent regularity in the account, or if there is any

default in payment of interest and instalment or when there is a downward

trend in credit summations and frequent return of cheques or bills,

b) Scrutiny of statements If the scrutiny of the statements submitted by the

borrower reveal a sharp decline in production and sales, rising level of

inventories, diversion of funds, the banker should realise that all is not well

with the unit.

c) External sources The banker may know the state of the unit through external

sources. Recession in the industry, unsatisfactory market reports, unfavourable

changes in government policy and complaints from suppliers of raw material,

may indicate that the unit is not working as per schedule.

d) Computerisation of loan monitoring In computerised branches, it is possible

to computerise the loan monitoring system so that accounts, which show signs

of sickness or weakness can be monitored more closely than other accounts.

Personal visit and face-to-face discussion By inspecting the unit the banker is

able to see for himself where the problem lies - either production bottlenecks or

income leakage or whether it is a case of willful default. During discussion with the

borrower, the banker may come to know details relating to breakdown in plant and

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 45/53

machinery, labour strike, change in management, death of a key person,

reconstitution of the firm, dispute among the partners etc. All these factors have a

bearing on the functioning of the unit and on its financial status.

Special Mention category of accounts Based on warning signals obtained

through both off-site and on-site monitoring, banks may classify accounts withirregularities persisting for more than 30 days under Special Mention or Potential

NPA category. This will help the bank to initiate proactive remedial measures for

early regularisation. The measures include timely release of additional funds to

borrowers with temporary liquidity problems and restructuring of accounts of

sincere and honest borrowers after considering cases on merit.

On going classification Although classification of assets is a yearly .

banks would do well to have a system of on going classification of assets and

quarterly provisioning. This helps in assessing provisioning requirements well inadvance. All doubts regarding classification should be settled internally and a system

of fixing accountability for failure to comply with the regulatory guidelines should be

introduced.Strategy for reducing provision The extent of provision for doubtful

asset is with

reference to secured and unsecured portion. Cent percent provision needs to be

made for the unsecured portion. If banks can ensure that the loan outstanding is

fully secured by realisable security, the quantum of provision to be made would be

less.

It takes one year for a sub standard asset to slip into doubtful category. Therefore,as soon as an account is classified as substandard, the banker must keep strict vigil

over the security during the next one year because in the event of the account being

classified as doubtful, the lack of security would be too costly for the bank.

3. Reducing NPAs

Cash recovery Banks, instead of organising a recovery drive based on overdues,

must short list those accounts, the recovery of which would provide impetus to the

system in reducing the pressure on profitability by reduced provisioning burden.

Vigorous efforts need to be made for recovery of critical amount (overdue interest

and

instalment) that can save an account from NPA classification:

a) In case of a term loan, the banker gets 90 days after the date of default to take

appropriate action and to persuade the borrower to pay interest or instalment

whichever is due.

b) In case of a cash credit account, the banker gets 90 days for ensuring that the

irregularity in the account is rectified.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 46/53

c) In case of direct agricultural loans, the account is classified NPA only after

two crop seasons (from sowing to harvesting) from the due date in case of

short duration loans and one crop season from the due date in case of long

duration loans.

Up gradation of assets Once accounts become NPA, then bankers should takesteps to up grade them by recovering the entire overdues. Close follow-up will

generally ensure success.

Compromise settlements Wherever feasible, in case of chronic NPAs, banks can

consider entering into compromise settlements with the borrowers.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 47/53

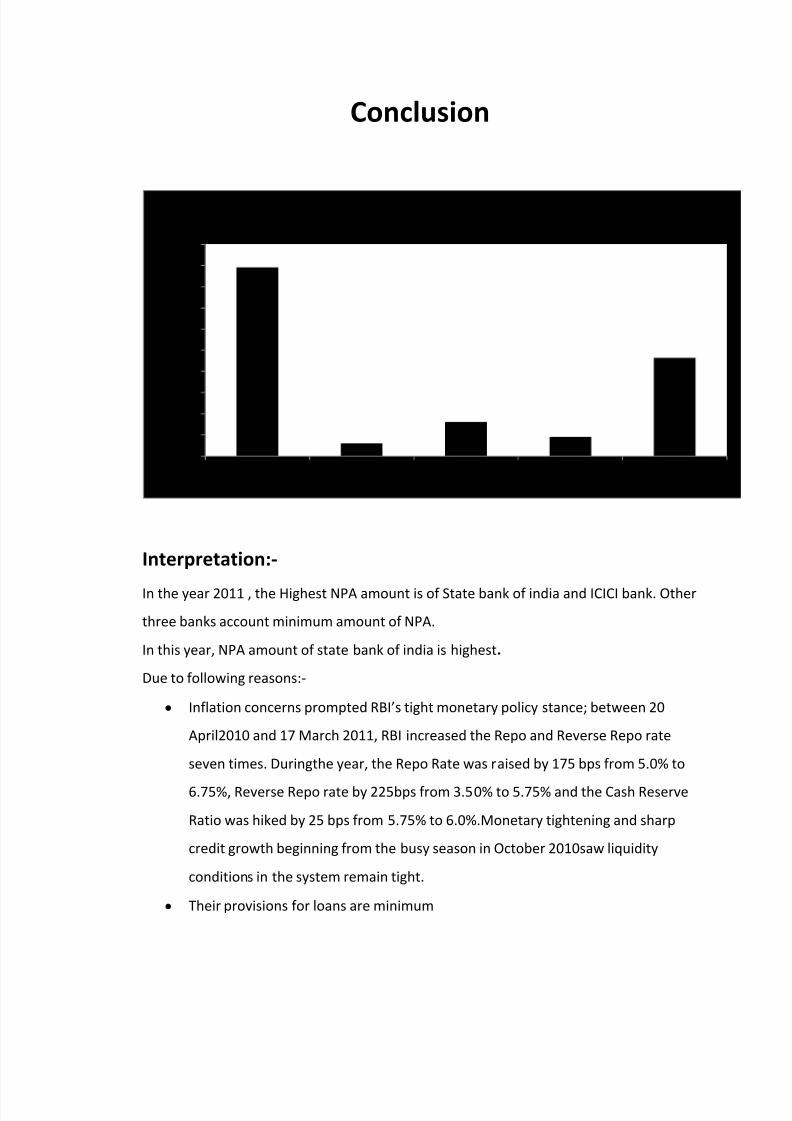

Conclusion

Interpretation:-

In the year 2011 , the Highest NPA amount is of State bank of india and ICICI bank. Other

three banks account minimum amount of NPA.

In this year, NPA amount of state bank of india is highest.

Due to following reasons:-

y Inflation concerns prompted RBIs tight monetary policy stance; between 20

April2010 and 17 March 2011, RBI increased the Repo and Reverse Repo rate

seven times. Duringthe year, the Repo Rate was raised by 175 bps from 5.0% to

6.75%, Reverse Repo rate by 225bps from 3.50% to 5.75% and the Cash Reserve

Ratio was hiked by 25 bps from 5.75% to 6.0%.Monetary tightening and sharp

credit growth beginning from the busy season in October 2010saw liquidity

conditions in the system remain tight.

y Their provisions for loans are minimum

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

SBI BOM PNB HDFC ICICI

NPA-2011

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 48/53

y They do not make sufficient research & scrutiny.

y They do not take back up security in form of cash, commodity, property.

y Inappropriate working system

y They dont have enough power recovery

y Improper management to recover the NPA through IPO, or issue of debt

instrument in capitalmarket

y Deficiencies on the part of the banks viz. in credit appraisal, monitoring and

follow-ups, delay in settlement of payments\ subsidiaries by government bodies

Measures taken by SBI

y Risk Scoring Model has been introduced in the Personal Segment portfolio

forstandardized and objective credit assessment.

y A strong collection mechanism in place is the vital link towards asset quality.

AccountTracking Centres have also been set up at all Local Head Offices for centralised

follow upof borrowers in the NPA category. New Code has been set up at the account

level foridentifying borrowers right from the 7th day of default.

y Campaign Operation Sampark has been launched as a part of a special drive for

updatingcontact details of all borrowers. Delinquent accounts have also been mapped

to individualstaff for focused monitoring, and NPA Dashboard has been launched as a

data tool for realtime monitoring of NPAs.

y Restructuring of impaired Standard Assets as well as viable non-performingassets, both

under CDR mechanism as well as under the Banks own scheme, has beengiven top

priority for arresting new additions and for reducing the existing level ofNPAs.

y Proactive steps have also been taken for prevention of NPAs.

8/3/2019 Indepth Report

http://slidepdf.com/reader/full/indepth-report 49/53

y The Bank referred 10 cases with aggregate exposure of Rs. 1,378.93 crores to

CDRmechanism during 2010-11, out of a total of 49 cases referred to CDR by the Whole

Bankingsystem including SBI. Out of these 49 cases, the Bank has exposure on 25 cases

aggregatingRs 2,250.24 crores.

The NPA is one of the biggest problems that the Indian Banks are facing today. If the proper

management of the NPAs is not undertaken it would hamper the business of the banks. If the

concept of NPAs is taken very lightly it would be dangerous for the Indian banking sector.

The NPAs would destroy the current profit, interest income due to large provisions of the

NPAs, and would affect the smooth functioning of the recycling of the funds Banks also

redistribute losses to other borrowers by charging higher interest rates. Lower deposit rates

and higher lending rates repress savings and financial markets, which hampers economic

growth.

Public sector banks are more efficient than private sector with regard to the management