Incomplete Markets, Heterogeneity and Macroeconomic Dynamics Bruce Preston and Mauro Roca Presented by Yuki Ikeda February 2009 Preston and Roca (presenter: Yuki Ikeda) 02/03 1 / 20

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Incomplete Markets, Heterogeneity and MacroeconomicDynamics

Bruce Preston and Mauro Roca

Presented by Yuki Ikeda

February 2009

Preston and Roca (presenter: Yuki Ikeda) 02/03 1 / 20

Introduction

Stochastic general equilibrium models with incomplete markets and acontinuum of heterogeneous agents

The problem: the state vector includes the whole cross-sectionaldistribution of wealth (in�nite-dimensional object) in the presence ofaggregate uncertainty

The pioneered method to solve this type of models: Krusell andSmith (1998)

Summarize the in�nite-dimensional cross-sectional distribution of assetby a �nite set of momentsThe behaviour of future aggregate capital can be almost perfectlydescribed using only the mean of the wealth distribution(Higher moments matter very little)

Preston and Roca (presenter: Yuki Ikeda) 02/03 2 / 20

Introduction

Stochastic general equilibrium models with incomplete markets and acontinuum of heterogeneous agents

The problem: the state vector includes the whole cross-sectionaldistribution of wealth (in�nite-dimensional object) in the presence ofaggregate uncertainty

The pioneered method to solve this type of models: Krusell andSmith (1998)

Summarize the in�nite-dimensional cross-sectional distribution of assetby a �nite set of momentsThe behaviour of future aggregate capital can be almost perfectlydescribed using only the mean of the wealth distribution(Higher moments matter very little)

Preston and Roca (presenter: Yuki Ikeda) 02/03 2 / 20

Introduction

Stochastic general equilibrium models with incomplete markets and acontinuum of heterogeneous agents

The problem: the state vector includes the whole cross-sectionaldistribution of wealth (in�nite-dimensional object) in the presence ofaggregate uncertainty

The pioneered method to solve this type of models: Krusell andSmith (1998)

Summarize the in�nite-dimensional cross-sectional distribution of assetby a �nite set of momentsThe behaviour of future aggregate capital can be almost perfectlydescribed using only the mean of the wealth distribution(Higher moments matter very little)

Preston and Roca (presenter: Yuki Ikeda) 02/03 2 / 20

Introduction

Stochastic general equilibrium models with incomplete markets and acontinuum of heterogeneous agents

The problem: the state vector includes the whole cross-sectionaldistribution of wealth (in�nite-dimensional object) in the presence ofaggregate uncertainty

The pioneered method to solve this type of models: Krusell andSmith (1998)

Summarize the in�nite-dimensional cross-sectional distribution of assetby a �nite set of moments

The behaviour of future aggregate capital can be almost perfectlydescribed using only the mean of the wealth distribution(Higher moments matter very little)

Preston and Roca (presenter: Yuki Ikeda) 02/03 2 / 20

Introduction

Stochastic general equilibrium models with incomplete markets and acontinuum of heterogeneous agents

The problem: the state vector includes the whole cross-sectionaldistribution of wealth (in�nite-dimensional object) in the presence ofaggregate uncertainty

The pioneered method to solve this type of models: Krusell andSmith (1998)

Summarize the in�nite-dimensional cross-sectional distribution of assetby a �nite set of momentsThe behaviour of future aggregate capital can be almost perfectlydescribed using only the mean of the wealth distribution(Higher moments matter very little)

Preston and Roca (presenter: Yuki Ikeda) 02/03 2 / 20

Introduction

Contributions of the paper

A new approach to solving this class of models based on perturbationmethods

An analytic characterization of the evolution of the wealth distribution(up to the order of the approximation)Continuously distrubuted random variables / not constrained by thenumber of state variablesUnderstanding of the role of heterogeneity in aggregate dynamics

Preston and Roca (presenter: Yuki Ikeda) 02/03 3 / 20

Introduction

Contributions of the paper

A new approach to solving this class of models based on perturbationmethods

An analytic characterization of the evolution of the wealth distribution(up to the order of the approximation)

Continuously distrubuted random variables / not constrained by thenumber of state variablesUnderstanding of the role of heterogeneity in aggregate dynamics

Preston and Roca (presenter: Yuki Ikeda) 02/03 3 / 20

Introduction

Contributions of the paper

A new approach to solving this class of models based on perturbationmethods

An analytic characterization of the evolution of the wealth distribution(up to the order of the approximation)Continuously distrubuted random variables / not constrained by thenumber of state variables

Understanding of the role of heterogeneity in aggregate dynamics

Preston and Roca (presenter: Yuki Ikeda) 02/03 3 / 20

Introduction

Contributions of the paper

A new approach to solving this class of models based on perturbationmethods

An analytic characterization of the evolution of the wealth distribution(up to the order of the approximation)Continuously distrubuted random variables / not constrained by thenumber of state variablesUnderstanding of the role of heterogeneity in aggregate dynamics

Preston and Roca (presenter: Yuki Ikeda) 02/03 3 / 20

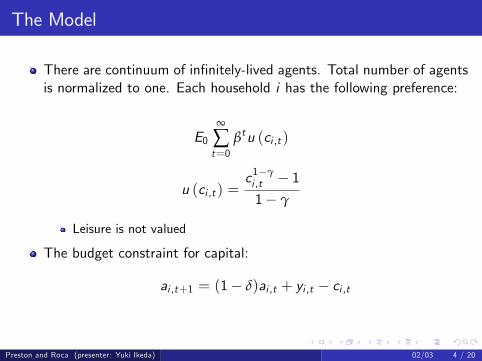

The Model

There are continuum of in�nitely-lived agents. Total number of agentsis normalized to one. Each household i has the following preference:

E0∞

∑t=0

βtu (ci ,t )

u (ci ,t ) =c1�γi ,t � 11� γ

Leisure is not valued

The budget constraint for capital:

ai ,t+1 = (1� δ)ai ,t + yi ,t � ci ,t

Preston and Roca (presenter: Yuki Ikeda) 02/03 4 / 20

The Model

There are continuum of in�nitely-lived agents. Total number of agentsis normalized to one. Each household i has the following preference:

E0∞

∑t=0

βtu (ci ,t )

u (ci ,t ) =c1�γi ,t � 11� γ

Leisure is not valued

The budget constraint for capital:

ai ,t+1 = (1� δ)ai ,t + yi ,t � ci ,t

Preston and Roca (presenter: Yuki Ikeda) 02/03 4 / 20

The Model

There are continuum of in�nitely-lived agents. Total number of agentsis normalized to one. Each household i has the following preference:

E0∞

∑t=0

βtu (ci ,t )

u (ci ,t ) =c1�γi ,t � 11� γ

Leisure is not valued

The budget constraint for capital:

ai ,t+1 = (1� δ)ai ,t + yi ,t � ci ,t

Preston and Roca (presenter: Yuki Ikeda) 02/03 4 / 20

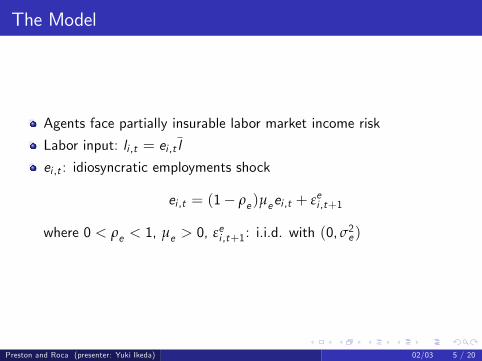

The Model

Agents face partially insurable labor market income risk

Labor input: li ,t = ei ,t l

ei ,t : idiosyncratic employments shock

ei ,t = (1� ρe )µeei ,t + εei ,t+1

where 0 < ρe < 1, µe > 0, εei ,t+1: i.i.d. with (0, σ2e )

Preston and Roca (presenter: Yuki Ikeda) 02/03 5 / 20

The Model

Agents face partially insurable labor market income risk

Labor input: li ,t = ei ,t l

ei ,t : idiosyncratic employments shock

ei ,t = (1� ρe )µeei ,t + εei ,t+1

where 0 < ρe < 1, µe > 0, εei ,t+1: i.i.d. with (0, σ2e )

Preston and Roca (presenter: Yuki Ikeda) 02/03 5 / 20

The Model

Agents face partially insurable labor market income risk

Labor input: li ,t = ei ,t l

ei ,t : idiosyncratic employments shock

ei ,t = (1� ρe )µeei ,t + εei ,t+1

where 0 < ρe < 1, µe > 0, εei ,t+1: i.i.d. with (0, σ2e )

Preston and Roca (presenter: Yuki Ikeda) 02/03 5 / 20

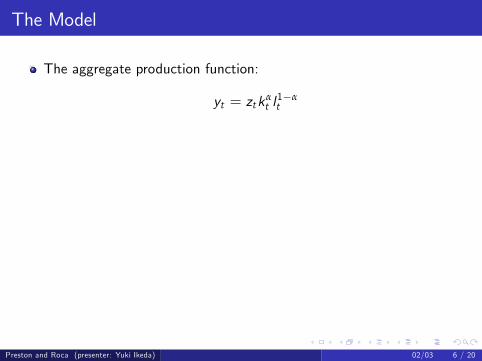

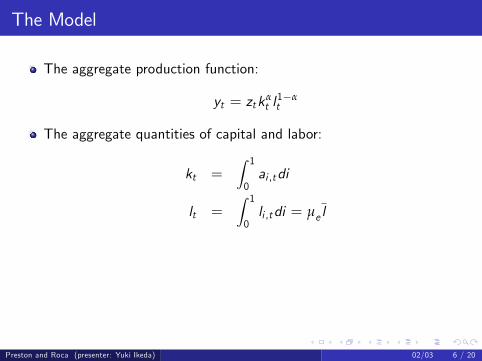

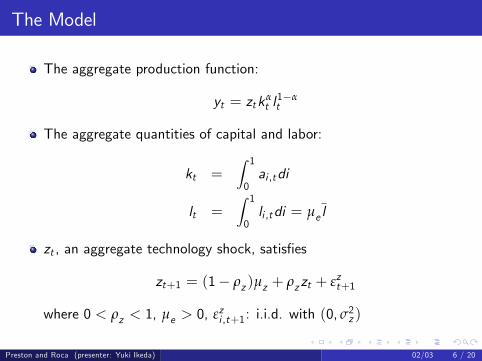

The Model

The aggregate production function:

yt = ztkαt l1�αt

The aggregate quantities of capital and labor:

kt =Z 1

0ai ,tdi

lt =Z 1

0li ,tdi = µe l

zt , an aggregate technology shock, satis�es

zt+1 = (1� ρz )µz + ρzzt + εzt+1

where 0 < ρz < 1, µe > 0, εzi ,t+1: i.i.d. with (0, σ2z )

Preston and Roca (presenter: Yuki Ikeda) 02/03 6 / 20

The Model

The aggregate production function:

yt = ztkαt l1�αt

The aggregate quantities of capital and labor:

kt =Z 1

0ai ,tdi

lt =Z 1

0li ,tdi = µe l

zt , an aggregate technology shock, satis�es

zt+1 = (1� ρz )µz + ρzzt + εzt+1

where 0 < ρz < 1, µe > 0, εzi ,t+1: i.i.d. with (0, σ2z )

Preston and Roca (presenter: Yuki Ikeda) 02/03 6 / 20

The Model

The aggregate production function:

yt = ztkαt l1�αt

The aggregate quantities of capital and labor:

kt =Z 1

0ai ,tdi

lt =Z 1

0li ,tdi = µe l

zt , an aggregate technology shock, satis�es

zt+1 = (1� ρz )µz + ρzzt + εzt+1

where 0 < ρz < 1, µe > 0, εzi ,t+1: i.i.d. with (0, σ2z )

Preston and Roca (presenter: Yuki Ikeda) 02/03 6 / 20

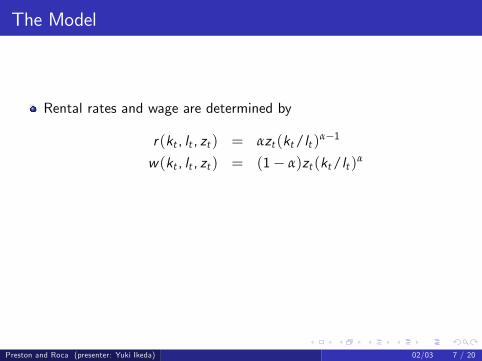

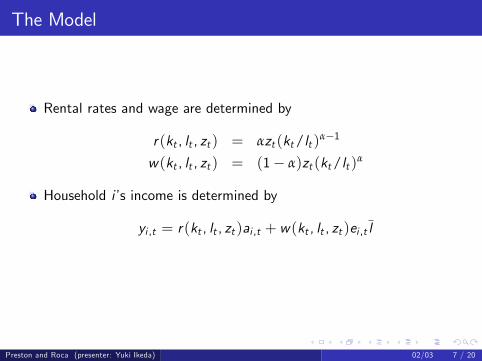

The Model

Rental rates and wage are determined by

r(kt , lt , zt ) = αzt (kt/lt )α�1

w(kt , lt , zt ) = (1� α)zt (kt/lt )α

Household i�s income is determined by

yi ,t = r(kt , lt , zt )ai ,t + w(kt , lt , zt )ei ,t l

Preston and Roca (presenter: Yuki Ikeda) 02/03 7 / 20

The Model

Rental rates and wage are determined by

r(kt , lt , zt ) = αzt (kt/lt )α�1

w(kt , lt , zt ) = (1� α)zt (kt/lt )α

Household i�s income is determined by

yi ,t = r(kt , lt , zt )ai ,t + w(kt , lt , zt )ei ,t l

Preston and Roca (presenter: Yuki Ikeda) 02/03 7 / 20

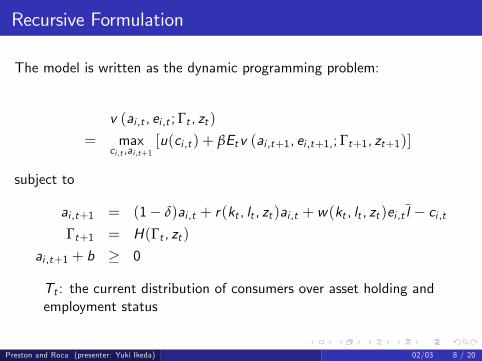

Recursive Formulation

The model is written as the dynamic programming problem:

v (ai ,t , ei ,t ; Γt , zt )= max

ci ,t ,ai ,t+1[u(ci ,t ) + βEtv (ai ,t+1, ei ,t+1,; Γt+1, zt+1)]

subject to

ai ,t+1 = (1� δ)ai ,t + r(kt , lt , zt )ai ,t + w(kt , lt , zt )ei ,t l � ci ,tΓt+1 = H(Γt , zt )

ai ,t+1 + b � 0

Tt : the current distribution of consumers over asset holding andemployment status

Preston and Roca (presenter: Yuki Ikeda) 02/03 8 / 20

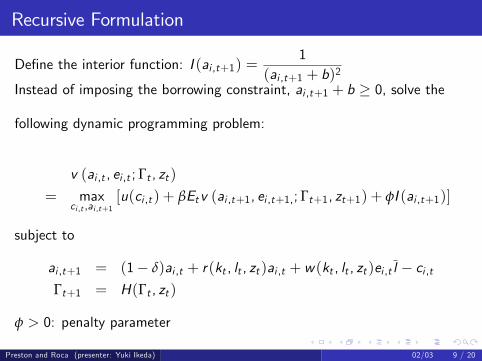

Recursive Formulation

De�ne the interior function: I (ai ,t+1) =1

(ai ,t+1 + b)2Instead of imposing the borrowing constraint, ai ,t+1 + b � 0, solve the

following dynamic programming problem:

v (ai ,t , ei ,t ; Γt , zt )= max

ci ,t ,ai ,t+1[u(ci ,t ) + βEtv (ai ,t+1, ei ,t+1,; Γt+1, zt+1) + φI (ai ,t+1)]

subject to

ai ,t+1 = (1� δ)ai ,t + r(kt , lt , zt )ai ,t + w(kt , lt , zt )ei ,t l � ci ,tΓt+1 = H(Γt , zt )

φ > 0: penalty parameter

Preston and Roca (presenter: Yuki Ikeda) 02/03 9 / 20

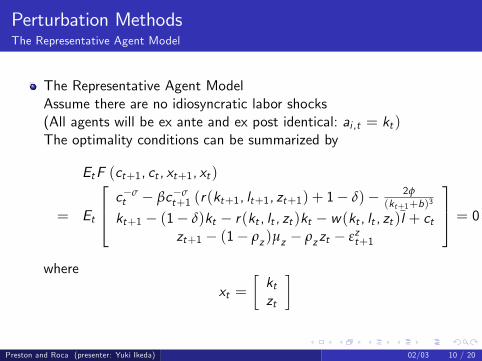

Perturbation MethodsThe Representative Agent Model

The Representative Agent ModelAssume there are no idiosyncratic labor shocks(All agents will be ex ante and ex post identical: ai ,t = kt )The optimality conditions can be summarized by

EtF (ct+1, ct , xt+1, xt )

= Et

264 c�σt � βc�σ

t+1 (r(kt+1, lt+1, zt+1) + 1� δ)� 2φ(kt+1+b)3

kt+1 � (1� δ)kt � r(kt , lt , zt )kt � w(kt , lt , zt )l + ctzt+1 � (1� ρz )µz � ρzzt � εzt+1

375 = 0where

xt =�ktzt

�

Preston and Roca (presenter: Yuki Ikeda) 02/03 10 / 20

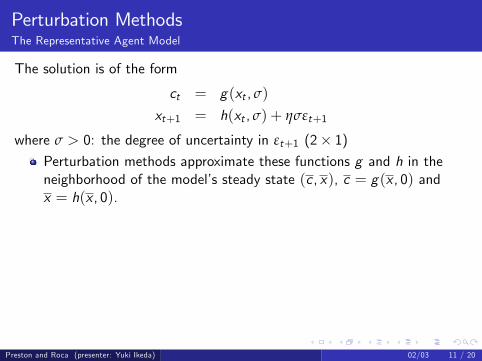

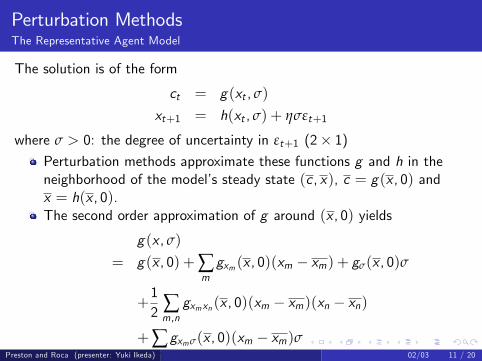

Perturbation MethodsThe Representative Agent Model

The solution is of the form

ct = g(xt , σ)

xt+1 = h(xt , σ) + ησεt+1

where σ > 0: the degree of uncertainty in εt+1 (2� 1)Perturbation methods approximate these functions g and h in theneighborhood of the model�s steady state (c , x), c = g(x , 0) andx = h(x , 0).

The second order approximation of g around (x , 0) yields

g(x , σ)

= g(x , 0) +∑mgxm (x , 0)(xm � xm) + gσ(x , 0)σ

+12 ∑m,ngxmxn (x , 0)(xm � xm)(xn � xn)

+∑mgxmσ(x , 0)(xm � xm)σ

+12 ∑m,ngσxm (x , 0)(xm � xm)σ+

12gσσ(x , 0)σ2

where m, n = 1, 2.

Preston and Roca (presenter: Yuki Ikeda) 02/03 11 / 20

Perturbation MethodsThe Representative Agent Model

The solution is of the form

ct = g(xt , σ)

xt+1 = h(xt , σ) + ησεt+1

where σ > 0: the degree of uncertainty in εt+1 (2� 1)Perturbation methods approximate these functions g and h in theneighborhood of the model�s steady state (c , x), c = g(x , 0) andx = h(x , 0).The second order approximation of g around (x , 0) yields

g(x , σ)

= g(x , 0) +∑mgxm (x , 0)(xm � xm) + gσ(x , 0)σ

+12 ∑m,ngxmxn (x , 0)(xm � xm)(xn � xn)

+∑mgxmσ(x , 0)(xm � xm)σ

+12 ∑m,ngσxm (x , 0)(xm � xm)σ+

12gσσ(x , 0)σ2

where m, n = 1, 2.

Preston and Roca (presenter: Yuki Ikeda) 02/03 11 / 20

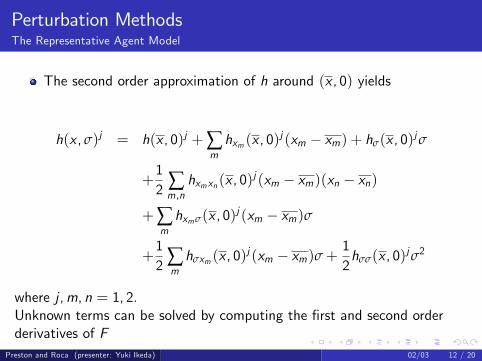

Perturbation MethodsThe Representative Agent Model

The second order approximation of h around (x , 0) yields

h(x , σ)j = h(x , 0)j +∑mhxm (x , 0)

j (xm � xm) + hσ(x , 0)jσ

+12 ∑m,nhxmxn (x , 0)

j (xm � xm)(xn � xn)

+∑mhxmσ(x , 0)j (xm � xm)σ

+12 ∑mhσxm (x , 0)

j (xm � xm)σ+12hσσ(x , 0)jσ2

where j ,m, n = 1, 2.Unknown terms can be solved by computing the �rst and second orderderivatives of F

Preston and Roca (presenter: Yuki Ikeda) 02/03 12 / 20

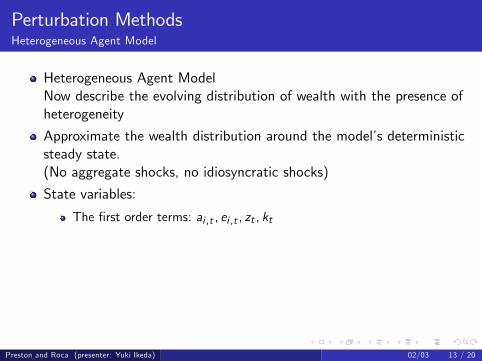

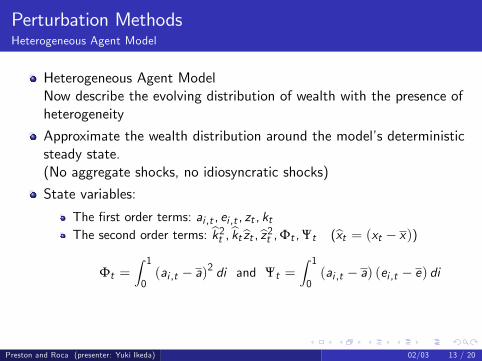

Perturbation MethodsHeterogeneous Agent Model

Heterogeneous Agent ModelNow describe the evolving distribution of wealth with the presence ofheterogeneity

Approximate the wealth distribution around the model�s deterministicsteady state.(No aggregate shocks, no idiosyncratic shocks)

State variables:

The �rst order terms: ai ,t , ei ,t , zt , ktThe second order terms: bk2t , bktbzt ,bz2t ,Φt ,Ψt (bxt = (xt � x))

Φt =Z 10(ai ,t � a)2 di and Ψt =

Z 10(ai ,t � a) (ei ,t � e) di

In sum, xt = [ai ,t , ei ,t , zt , kt ,Φt ,Ψt ]0

Preston and Roca (presenter: Yuki Ikeda) 02/03 13 / 20

Perturbation MethodsHeterogeneous Agent Model

Heterogeneous Agent ModelNow describe the evolving distribution of wealth with the presence ofheterogeneity

Approximate the wealth distribution around the model�s deterministicsteady state.(No aggregate shocks, no idiosyncratic shocks)

State variables:

The �rst order terms: ai ,t , ei ,t , zt , ktThe second order terms: bk2t , bktbzt ,bz2t ,Φt ,Ψt (bxt = (xt � x))

Φt =Z 10(ai ,t � a)2 di and Ψt =

Z 10(ai ,t � a) (ei ,t � e) di

In sum, xt = [ai ,t , ei ,t , zt , kt ,Φt ,Ψt ]0

Preston and Roca (presenter: Yuki Ikeda) 02/03 13 / 20

Perturbation MethodsHeterogeneous Agent Model

Heterogeneous Agent ModelNow describe the evolving distribution of wealth with the presence ofheterogeneity

Approximate the wealth distribution around the model�s deterministicsteady state.(No aggregate shocks, no idiosyncratic shocks)

State variables:

The �rst order terms: ai ,t , ei ,t , zt , ktThe second order terms: bk2t , bktbzt ,bz2t ,Φt ,Ψt (bxt = (xt � x))

Φt =Z 10(ai ,t � a)2 di and Ψt =

Z 10(ai ,t � a) (ei ,t � e) di

In sum, xt = [ai ,t , ei ,t , zt , kt ,Φt ,Ψt ]0

Preston and Roca (presenter: Yuki Ikeda) 02/03 13 / 20

Perturbation MethodsHeterogeneous Agent Model

Heterogeneous Agent ModelNow describe the evolving distribution of wealth with the presence ofheterogeneity

Approximate the wealth distribution around the model�s deterministicsteady state.(No aggregate shocks, no idiosyncratic shocks)

State variables:

The �rst order terms: ai ,t , ei ,t , zt , kt

The second order terms: bk2t , bktbzt ,bz2t ,Φt ,Ψt (bxt = (xt � x))Φt =

Z 10(ai ,t � a)2 di and Ψt =

Z 10(ai ,t � a) (ei ,t � e) di

In sum, xt = [ai ,t , ei ,t , zt , kt ,Φt ,Ψt ]0

Preston and Roca (presenter: Yuki Ikeda) 02/03 13 / 20

Perturbation MethodsHeterogeneous Agent Model

Heterogeneous Agent ModelNow describe the evolving distribution of wealth with the presence ofheterogeneity

Approximate the wealth distribution around the model�s deterministicsteady state.(No aggregate shocks, no idiosyncratic shocks)

State variables:

The �rst order terms: ai ,t , ei ,t , zt , ktThe second order terms: bk2t , bktbzt ,bz2t ,Φt ,Ψt (bxt = (xt � x))

Φt =Z 10(ai ,t � a)2 di and Ψt =

Z 10(ai ,t � a) (ei ,t � e) di

In sum, xt = [ai ,t , ei ,t , zt , kt ,Φt ,Ψt ]0

Preston and Roca (presenter: Yuki Ikeda) 02/03 13 / 20

Perturbation MethodsHeterogeneous Agent Model

Heterogeneous Agent ModelNow describe the evolving distribution of wealth with the presence ofheterogeneity

Approximate the wealth distribution around the model�s deterministicsteady state.(No aggregate shocks, no idiosyncratic shocks)

State variables:

The �rst order terms: ai ,t , ei ,t , zt , ktThe second order terms: bk2t , bktbzt ,bz2t ,Φt ,Ψt (bxt = (xt � x))

Φt =Z 10(ai ,t � a)2 di and Ψt =

Z 10(ai ,t � a) (ei ,t � e) di

In sum, xt = [ai ,t , ei ,t , zt , kt ,Φt ,Ψt ]0

Preston and Roca (presenter: Yuki Ikeda) 02/03 13 / 20

Perturbation MethodsHeterogeneous Agent Model

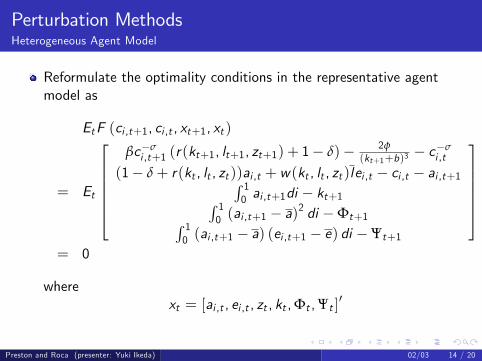

Reformulate the optimality conditions in the representative agentmodel as

EtF (ci ,t+1, ci ,t , xt+1, xt )

= Et

2666664βc�σi ,t+1 (r(kt+1, lt+1, zt+1) + 1� δ)� 2φ

(kt+1+b)3� c�σ

i ,t

(1� δ+ r(kt , lt , zt ))ai ,t + w(kt , lt , zt )lei ,t � ci ,t � ai ,t+1R 10 ai ,t+1di � kt+1R 1

0 (ai ,t+1 � a)2 di �Φt+1R 1

0 (ai ,t+1 � a) (ei ,t+1 � e) di �Ψt+1

3777775= 0

wherext = [ai ,t , ei ,t , zt , kt ,Φt ,Ψt ]

0

Preston and Roca (presenter: Yuki Ikeda) 02/03 14 / 20

Perturbation MethodsHeterogeneous Agent Model

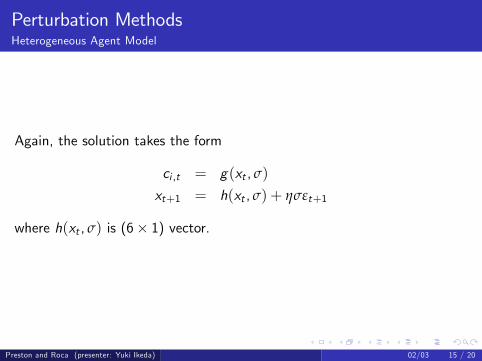

Again, the solution takes the form

ci ,t = g(xt , σ)

xt+1 = h(xt , σ) + ησεt+1

where h(xt , σ) is (6� 1) vector.

Preston and Roca (presenter: Yuki Ikeda) 02/03 15 / 20

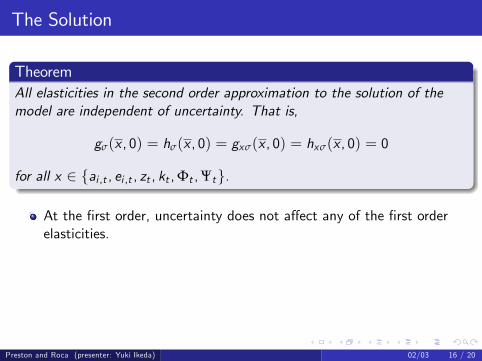

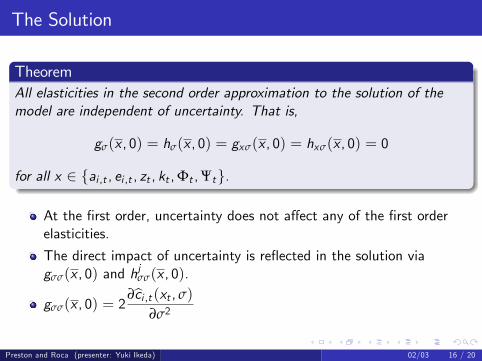

The Solution

TheoremAll elasticities in the second order approximation to the solution of themodel are independent of uncertainty. That is,

gσ(x , 0) = hσ(x , 0) = gxσ(x , 0) = hxσ(x , 0) = 0

for all x 2 fai ,t , ei ,t , zt , kt ,Φt ,Ψtg.

At the �rst order, uncertainty does not a¤ect any of the �rst orderelasticities.

The direct impact of uncertainty is re�ected in the solution viagσσ(x , 0) and h

jσσ(x , 0).

gσσ(x , 0) = 2∂bci ,t (xt , σ)

∂σ2

Preston and Roca (presenter: Yuki Ikeda) 02/03 16 / 20

The Solution

TheoremAll elasticities in the second order approximation to the solution of themodel are independent of uncertainty. That is,

gσ(x , 0) = hσ(x , 0) = gxσ(x , 0) = hxσ(x , 0) = 0

for all x 2 fai ,t , ei ,t , zt , kt ,Φt ,Ψtg.

At the �rst order, uncertainty does not a¤ect any of the �rst orderelasticities.

The direct impact of uncertainty is re�ected in the solution viagσσ(x , 0) and h

jσσ(x , 0).

gσσ(x , 0) = 2∂bci ,t (xt , σ)

∂σ2

Preston and Roca (presenter: Yuki Ikeda) 02/03 16 / 20

The Solution

TheoremAll elasticities in the second order approximation to the solution of themodel are independent of uncertainty. That is,

gσ(x , 0) = hσ(x , 0) = gxσ(x , 0) = hxσ(x , 0) = 0

for all x 2 fai ,t , ei ,t , zt , kt ,Φt ,Ψtg.

At the �rst order, uncertainty does not a¤ect any of the �rst orderelasticities.

The direct impact of uncertainty is re�ected in the solution viagσσ(x , 0) and h

jσσ(x , 0).

gσσ(x , 0) = 2∂bci ,t (xt , σ)

∂σ2

Preston and Roca (presenter: Yuki Ikeda) 02/03 16 / 20

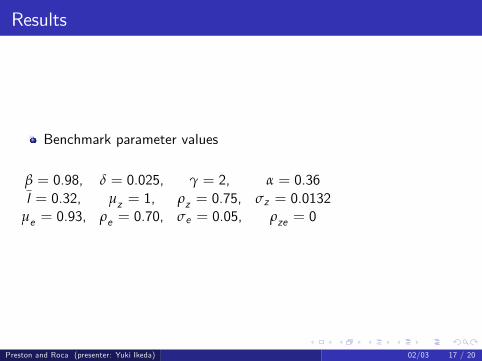

Results

Benchmark parameter values

β = 0.98, δ = 0.025, γ = 2, α = 0.36l = 0.32, µz = 1, ρz = 0.75, σz = 0.0132

µe = 0.93, ρe = 0.70, σe = 0.05, ρze = 0

Preston and Roca (presenter: Yuki Ikeda) 02/03 17 / 20

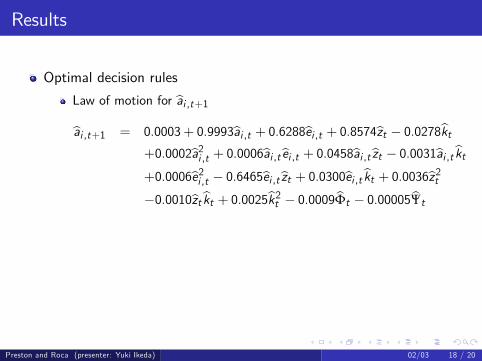

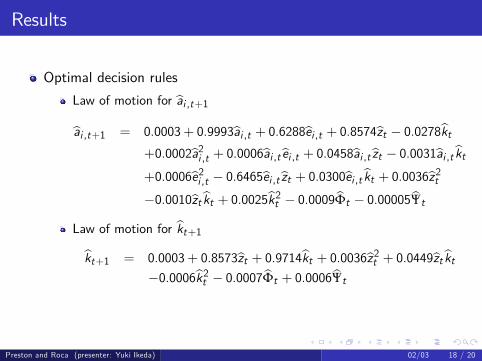

Results

Optimal decision rules

Law of motion for bai ,t+1bai ,t+1 = 0.0003+ 0.9993bai ,t + 0.6288bei ,t + 0.8574bzt � 0.0278bkt

+0.0002ba2i ,t + 0.0006bai ,tbei ,t + 0.0458bai ,tbzt � 0.0031bai ,tbkt+0.0006be2i ,t � 0.6465bei ,tbzt + 0.0300bei ,tbkt + 0.0036bz2t�0.0010bztbkt + 0.0025bk2t � 0.0009bΦt � 0.00005bΨt

Law of motion for bkt+1bkt+1 = 0.0003+ 0.8573bzt + 0.9714bkt + 0.0036bz2t + 0.0449bztbkt�0.0006bk2t � 0.0007bΦt + 0.0006bΨt

Preston and Roca (presenter: Yuki Ikeda) 02/03 18 / 20

Results

Optimal decision rules

Law of motion for bai ,t+1bai ,t+1 = 0.0003+ 0.9993bai ,t + 0.6288bei ,t + 0.8574bzt � 0.0278bkt

+0.0002ba2i ,t + 0.0006bai ,tbei ,t + 0.0458bai ,tbzt � 0.0031bai ,tbkt+0.0006be2i ,t � 0.6465bei ,tbzt + 0.0300bei ,tbkt + 0.0036bz2t�0.0010bztbkt + 0.0025bk2t � 0.0009bΦt � 0.00005bΨt

Law of motion for bkt+1bkt+1 = 0.0003+ 0.8573bzt + 0.9714bkt + 0.0036bz2t + 0.0449bztbkt�0.0006bk2t � 0.0007bΦt + 0.0006bΨt

Preston and Roca (presenter: Yuki Ikeda) 02/03 18 / 20

Results

Optimal decision rules

Law of motion for bai ,t+1bai ,t+1 = 0.0003+ 0.9993bai ,t + 0.6288bei ,t + 0.8574bzt � 0.0278bkt

+0.0002ba2i ,t + 0.0006bai ,tbei ,t + 0.0458bai ,tbzt � 0.0031bai ,tbkt+0.0006be2i ,t � 0.6465bei ,tbzt + 0.0300bei ,tbkt + 0.0036bz2t�0.0010bztbkt + 0.0025bk2t � 0.0009bΦt � 0.00005bΨt

Law of motion for bkt+1bkt+1 = 0.0003+ 0.8573bzt + 0.9714bkt + 0.0036bz2t + 0.0449bztbkt�0.0006bk2t � 0.0007bΦt + 0.0006bΨt

Preston and Roca (presenter: Yuki Ikeda) 02/03 18 / 20

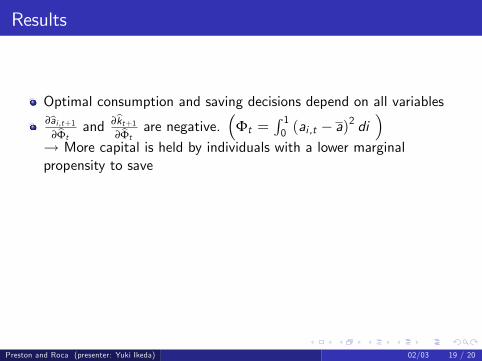

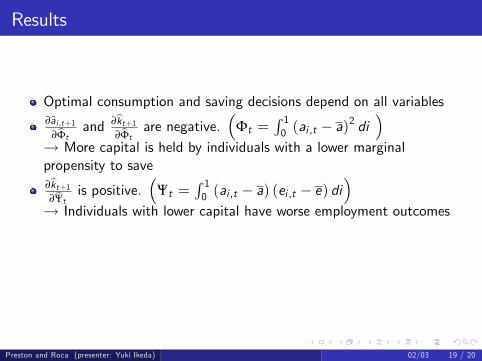

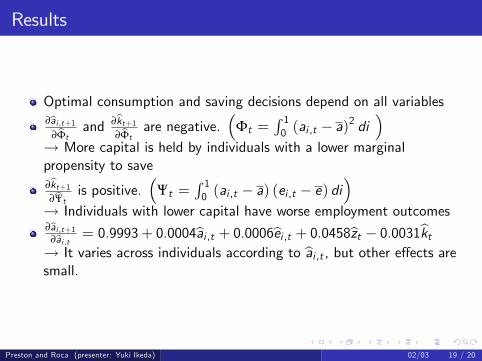

Results

Optimal consumption and saving decisions depend on all variables

∂bai ,t+1∂bΦt

and ∂bkt+1∂bΦt

are negative.�

Φt =R 10 (ai ,t � a)

2 di�

! More capital is held by individuals with a lower marginalpropensity to save∂bkt+1∂bΨt is positive.

�Ψt =

R 10 (ai ,t � a) (ei ,t � e) di

�! Individuals with lower capital have worse employment outcomes∂bai ,t+1

∂bai ,t = 0.9993+ 0.0004bai ,t + 0.0006bei ,t + 0.0458bzt � 0.0031bkt! It varies across individuals according to bai ,t , but other e¤ects aresmall.

Preston and Roca (presenter: Yuki Ikeda) 02/03 19 / 20

Results

Optimal consumption and saving decisions depend on all variables∂bai ,t+1

∂bΦtand ∂bkt+1

∂bΦtare negative.

�Φt =

R 10 (ai ,t � a)

2 di�

! More capital is held by individuals with a lower marginalpropensity to save

∂bkt+1∂bΨt is positive.

�Ψt =

R 10 (ai ,t � a) (ei ,t � e) di

�! Individuals with lower capital have worse employment outcomes∂bai ,t+1

∂bai ,t = 0.9993+ 0.0004bai ,t + 0.0006bei ,t + 0.0458bzt � 0.0031bkt! It varies across individuals according to bai ,t , but other e¤ects aresmall.

Preston and Roca (presenter: Yuki Ikeda) 02/03 19 / 20

Results

Optimal consumption and saving decisions depend on all variables∂bai ,t+1

∂bΦtand ∂bkt+1

∂bΦtare negative.

�Φt =

R 10 (ai ,t � a)

2 di�

! More capital is held by individuals with a lower marginalpropensity to save∂bkt+1∂bΨt is positive.

�Ψt =

R 10 (ai ,t � a) (ei ,t � e) di

�! Individuals with lower capital have worse employment outcomes

∂bai ,t+1∂bai ,t = 0.9993+ 0.0004bai ,t + 0.0006bei ,t + 0.0458bzt � 0.0031bkt! It varies across individuals according to bai ,t , but other e¤ects aresmall.

Preston and Roca (presenter: Yuki Ikeda) 02/03 19 / 20

Results

Optimal consumption and saving decisions depend on all variables∂bai ,t+1

∂bΦtand ∂bkt+1

∂bΦtare negative.

�Φt =

R 10 (ai ,t � a)

2 di�

! More capital is held by individuals with a lower marginalpropensity to save∂bkt+1∂bΨt is positive.

�Ψt =

R 10 (ai ,t � a) (ei ,t � e) di

�! Individuals with lower capital have worse employment outcomes∂bai ,t+1

∂bai ,t = 0.9993+ 0.0004bai ,t + 0.0006bei ,t + 0.0458bzt � 0.0031bkt! It varies across individuals according to bai ,t , but other e¤ects aresmall.

Preston and Roca (presenter: Yuki Ikeda) 02/03 19 / 20

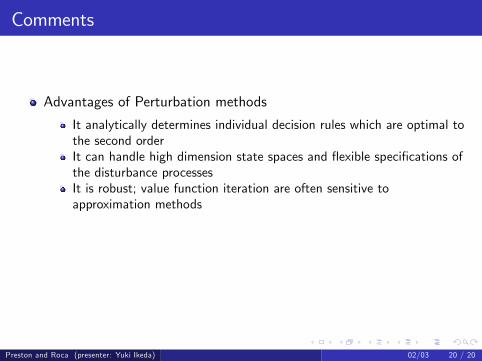

Comments

Advantages of Perturbation methods

It analytically determines individual decision rules which are optimal tothe second orderIt can handle high dimension state spaces and �exible speci�cations ofthe disturbance processesIt is robust; value function iteration are often sensitive toapproximation methods

Disadvantages of Perturbation methods

It cannot be used in the presence of occasionally binding constraints(the use of interior function)

Preston and Roca (presenter: Yuki Ikeda) 02/03 20 / 20

Comments

Advantages of Perturbation methods

It analytically determines individual decision rules which are optimal tothe second order

It can handle high dimension state spaces and �exible speci�cations ofthe disturbance processesIt is robust; value function iteration are often sensitive toapproximation methods

Disadvantages of Perturbation methods

It cannot be used in the presence of occasionally binding constraints(the use of interior function)

Preston and Roca (presenter: Yuki Ikeda) 02/03 20 / 20

Comments

Advantages of Perturbation methods

It analytically determines individual decision rules which are optimal tothe second orderIt can handle high dimension state spaces and �exible speci�cations ofthe disturbance processes

It is robust; value function iteration are often sensitive toapproximation methods

Disadvantages of Perturbation methods

It cannot be used in the presence of occasionally binding constraints(the use of interior function)

Preston and Roca (presenter: Yuki Ikeda) 02/03 20 / 20

Comments

Advantages of Perturbation methods

It analytically determines individual decision rules which are optimal tothe second orderIt can handle high dimension state spaces and �exible speci�cations ofthe disturbance processesIt is robust; value function iteration are often sensitive toapproximation methods

Disadvantages of Perturbation methods

It cannot be used in the presence of occasionally binding constraints(the use of interior function)

Preston and Roca (presenter: Yuki Ikeda) 02/03 20 / 20

Comments

Advantages of Perturbation methods

It analytically determines individual decision rules which are optimal tothe second orderIt can handle high dimension state spaces and �exible speci�cations ofthe disturbance processesIt is robust; value function iteration are often sensitive toapproximation methods

Disadvantages of Perturbation methods

It cannot be used in the presence of occasionally binding constraints(the use of interior function)

Preston and Roca (presenter: Yuki Ikeda) 02/03 20 / 20

Comments

Advantages of Perturbation methods

It analytically determines individual decision rules which are optimal tothe second orderIt can handle high dimension state spaces and �exible speci�cations ofthe disturbance processesIt is robust; value function iteration are often sensitive toapproximation methods

Disadvantages of Perturbation methods

It cannot be used in the presence of occasionally binding constraints(the use of interior function)

Preston and Roca (presenter: Yuki Ikeda) 02/03 20 / 20

Related Documents