COUNCIL OF MINISTERS REGULATIONS NO. [ ]/2016 REGULATIONS ISSUED PURSUANT TO THE FEDERAL INCOME TAX PROCLAMATION These Regulations are issued by the Council of Ministers pursuant to Article 5 of the Definitions of Powers and Duties of the Executive Organs of the Federal Democratic Republic of Ethiopia Proclamation No. 916/2015 and Article 99 of the Federal Income Tax Proclamation No 979/2016. PART ONE GENERAL 1. Short Title These Regulations may be cited as the “Council of Ministers Federal Income Tax Regulations --/2016”. 2. Definitions 1/ In these Regulations: a) “Proclamation” means the Federal Income Tax Proclamation No. 979/2016; and b) “Repealed Proclamation” means the Income Tax Proclamation 286/2002(as amended), Mining Income tax Proclamation 53/1993 and all amendments there to and petroleum operations Income tax no 296/1986 and all amendments thereto. 2/ A term used in these Regulations has the same meaning as in the Proclamation or the Federal Tax Administration Proclamation, as the case may be, unless the context requires otherwise. PART TWO APPLICATION OF TERMS USED IN THE PROCLAMATION 3. Interest An amount, however described, paid by r a mutual finance association as the return on deposits with, or member‟s contributions to, the association shall be treated as interest for the purposes of the Proclamation.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

COUNCIL OF MINISTERS REGULATIONS NO. [ ]/2016

REGULATIONS ISSUED PURSUANT TO

THE FEDERAL INCOME TAX PROCLAMATION

These Regulations are issued by the Council of Ministers pursuant to Article 5

of the Definitions of Powers and Duties of the Executive Organs of the Federal

Democratic Republic of Ethiopia Proclamation No. 916/2015 and Article 99 of the

Federal Income Tax Proclamation No 979/2016.

PART ONE

GENERAL

1. Short Title

These Regulations may be cited as the “Council of Ministers Federal Income

Tax Regulations --/2016”.

2. Definitions

1/ In these Regulations:

a) “Proclamation” means the Federal Income Tax Proclamation

No. 979/2016; and

b) “Repealed Proclamation” means the Income Tax Proclamation

286/2002(as amended), Mining Income tax Proclamation

53/1993 and all amendments there to and petroleum operations

Income tax no 296/1986 and all amendments thereto.

2/ A term used in these Regulations has the same meaning as in the

Proclamation or the Federal Tax Administration Proclamation, as the

case may be, unless the context requires otherwise.

PART TWO

APPLICATION OF TERMS USED IN THE PROCLAMATION

3. Interest

An amount, however described, paid by r a mutual finance association

as the return on deposits with, or member‟s contributions to, the

association shall be treated as interest for the purposes of the

Proclamation.

FITR/Bochu/8/5/2017

2

4. Permanent Establishment

1/ In determining whether a person exceeds the 183-day period specified

in Article 4(2)(c) of the Proclamation, account shall be taken of a

connected project of the person or of a related person.

2/ When a person operates a building site, or conducts a project or

activity referred to in Article 4(3) of the Proclamation, any connected

activities conducted by a related person shall be added to the period of

time during which the first-mentioned person has operated the building

site or conducted the project or activities for the purpose of

determining whether the 183-day period is exceeded.

5. Resident Individual

1/ Subject to sub-article (3), in calculating the number of days an

individual is present in Ethiopia for the purposes of Article 5(2)(c) of

the Proclamation:

a) a part of a day that an individual is present in Ethiopia

(including the day of arrival in, and the day of departure from,

Ethiopia) shall count as a whole day of such presence;

b) the following days in which an individual is wholly or partly

present in Ethiopia shall count as a whole day of such presence:

(1) a public holiday;

(2) a day of leave, including sick leave;

(3) a day in which the individual‟s activity in Ethiopia is

interrupted because of a strike, lock-out, delay in the

receipt of supplies, adverse weather conditions, or

seasonal factors;

(4) a day spent by the individual on holiday in Ethiopia

before, during, or after any activity conducted by the

individual in Ethiopia.

2/ A day or part of a day when an individual is in Ethiopia solely by

reason of being in transit between two different places outside Ethiopia

shall not count as a day present in Ethiopia.

6. Shares and bonds

1/ The reference to “shares and bonds” in Article 59(7)(c) of the

Proclamation includes any interest in shares or bonds, such as, in the

case of shares, a right or option to acquire shares.

FITR/Bochu/8/5/2017

3

2/ A gain arising on disposal of an interest in a share in, or a bond issued

by, a resident company shall be Ethiopian source income.

PART THREE

SCHEDULE ‘A’ INCOME

CHAPTER ONE

FRINGE BENEFITS

7. Chapter One of Part Three Definitions

1/ In this Part:

a) “Employee share scheme” means an agreement or arrangement

under which an employer company or a related company may

allot shares to an employee of the employer company;

b) “Household personnel” means a housekeeper, cook, driver,

gardener, or other domestic assistant;

c) “Market lending rate”, in relation to a month, means:

(1) for a commercial bank, the lending rate on loans and

rediscount facilities granted by the National Bank of

Ethiopia to commercial banks that prevailed in Ethiopia

during the month; or

(2) for any other person, [the lowest commercial lending

interest rate] that prevailed in Ethiopia during the

month;

d) “Medical expenditure” means expenditures for the supply of

medical, dental, or nursing services, including the cost of

supply of any medicines incidental to the supply of such

services;

e) “Related company”, in relation to a company, means another

company that is a related person in respect of the first-

mentioned company;

f) “Remote area” means a location that is [50] kilometres from an

urban centre with a population of [20,000];

g) “Services” includes the use of property and the making

available of any facility.

h) “Vehicle” means a motor vehicle designed to carry a load of less

than 1 tonne and fewer than 9 passengers;

FITR/Bochu/8/5/2017

4

2/ In this Chapter:

a) a reference to an “employer” includes a related person of the

employer and a third party acting under an arrangement with an

employer or a related person of the employer; and

b) a reference to an “employee” includes a related person of the

employee.

8. Fringe Benefits

1/ For the purposes of Article 12(1)(b) of the Proclamation and subject to

this Article, the following are fringe benefits:

a) a debt waiver fringe benefit;

b) a household personnel fringe benefit;

c) a housing fringe benefit;

d) a discounted interest loan fringe benefit;

e) a meal or refreshment fringe benefit;

f) a private expenditure fringe benefit;

g) a property or services fringe benefit;

h) an employee share scheme fringe benefit;

i) a vehicle fringe benefit;

j) a residual fringe benefit.

2/ A benefit is not a fringe benefit to the extent that, if the employee had

acquired the benefit, the expenditure incurred by the employee in

acquiring the benefit would have been incurred in deriving

employment income.

3/ In determining whether a benefit is a fringe benefit and the value of a

fringe benefit, any restriction on transfer of the benefit and the fact that

the benefit is not otherwise convertible to cash are to be disregarded.

4/ The following benefits are not treated as fringe benefits for the

purposes of the Proclamation or these Regulations:

a) a benefit that is exempt income under Schedule „E‟ of the

Proclamation;

FITR/Bochu/8/5/2017

5

b) a benefit the value of which, after taking into account the

frequency with which the employer provides similar benefits, is

so small as to make accounting for it unreasonable or

administratively impracticable in accordance with the directive

to be issued by the minister;

c) subsidy to a meal or refreshment provided in a canteen, cafeteria,

or dining room operated by, or on behalf of, an employer solely

for the benefit of employees and that is available to all non-

casual employees on equal terms;

d) the provision of accommodation or housing to a non-

managerial employee in a remote area if:

(1) the employee‟s usual place of employment is in the

remote area; and

(2) it is necessary for the employer to provide the

accommodation or housing to the employee in the

remote area because the nature of the employer‟s

business is such that the employee is likely to move

frequently from one residential location to another or

there is insufficient suitable residential accommodation

available in the remote area;

e) health insurance premiums and medical expenditures paid by

an employer on behalf of an employee;

f) the provision of a mobile phone by an employer for use by an

employee;

g) the payment by an employer of the cost of mobile phone calls

made by an employee, including with a mobile phone provided

by the employer;

h) tuition fees paid by an employer for the benefit of an employee

for attendance at a course offered by a university, college, or

other institution providing adult education courses;

i) the provision of the services of a security guard for the benefit

of an employee.

9. Debt Waiver Fringe Benefit

1/ The waiver by an employer of the obligation of an employee to pay or

repay an amount owing to the employer is a debt waiver fringe benefit.

2/ The value of a debt waiver fringe benefit shall be the amount waived.

FITR/Bochu/8/5/2017

6

10. Household Personnel Fringe Benefit

1/ The services of household personnel provided by an employer to an

employee is a household personnel fringe benefit.

2/ The value of a household personnel fringe benefit for a month shall be

the total employment income paid to the household personnel in that

month for services rendered to the employee reduced by any payment

made by the employee for such services.

11. Housing Fringe Benefit

1/ Accommodation or housing provided by an employer to an employee

is a housing fringe benefit.

2/ The value of a housing fringe benefit provided by an employer to an

employee for a month when the employer owns the accommodation or

housing shall be the fair market rent of the accommodation or housing

for the month reduced by any payment made by the employee for the

accommodation or housing.

3/ The value of a housing fringe benefit provided by an employer to an

employee for a month when the employer leases the accommodation or

housing shall be the rent paid by the employer for the accommodation

or housing during the month reduced by any payment made by the

employee for the accommodation or housing.

12. Discounted Interest Loan Fringe Benefit

1/ A loan provided by an employer to an employee is a discounted

interest loan fringe benefit if the interest rate under the loan is less than

the market lending rate.

2/ The value of a discounted interest loan fringe benefit for a month shall

be the difference between the interest paid by the employee on the loan

for the month, if any, and the interest that would have been paid by the

employee on the loan for the month if the loan had been made at the

market lending rate for that month.

13. Meal or Refreshment Fringe Benefit

1/ A meal or refreshment provided by an employer to an employee is a

meal or refreshment fringe benefit.

2/ The value of a meal or refreshment fringe benefit shall be the total cost

to the employer of providing the meal or refreshment reduced by any

amount paid by the employee for the meal or refreshment.

14. Vehicle Fringe Benefit

FITR/Bochu/8/5/2017

7

1/ A vehicle provided by an employer to an employee wholly or partly

for the private use of the employee is a vehicle fringe benefit.

2/ Subject to sub-articles (3) and (4), the value of a vehicle fringe benefit

for a month shall be the amount calculated in accordance with the

following formula:

(A x 5%)

12

where:

A is the cost to the employer of acquiring the vehicle or, if the

vehicle is leased by the employer, the fair market value of the

vehicle at the commencement of the lease.

3/ The value of a vehicle fringe benefit calculated under sub-article (2)

shall be reduced by the following:

a) any payment made by the employee for the use of the vehicle

or for maintenance and running costs;

b) the proportion of the use of the vehicle (if any) by the

employee in the conduct of employment;

c) the proportion of the month (if any) that the vehicle was not

provided to the employee for private use.

4/ If an employer has held a vehicle for more than five years, the value of

component A in the formula in sub-article (2) shall be 50% of the

amount determined under sub-article (2).

5/ A reference in this Article to a vehicle being provided to an employee

for private use includes a vehicle that is made available to an employee

for private use even if the employee did not actually use the vehicle for

a private use on a particular day.

15. Private Expenditure Fringe Benefit

1/ Subject to sub-article (3), the payment of expenditure by an employer

is a private expenditure fringe benefit to the extent that the expenditure

gives rise to a private benefit to an employee.

2/ The value of a private expenditure fringe benefit shall be the amount of

the expenditure treated as a private expenditure fringe benefit under

sub-article (1).

3/ This Article shall not apply to expenditure paid by an employer that is

a fringe benefit under another Article in this Part other than Article 18

of these Regulations.

FITR/Bochu/8/5/2017

8

16. Property or Services Fringe Benefit

1/ The transfer of property or provision of services by an employer to an

employee is a property or services fringe benefit.

2/ Subject to sub-article (3), the value of a property or services fringe

benefit shall be:

a) if the employer supplies the property or services to customers

in the ordinary course of business, 75% of the normal selling

price of the property or services; or

b) in any other case, the cost to the employer of acquiring the

property or services.

3/ The value of a property fringe benefit determined under sub-article (2)

shall be reduced by any payment made by the employee for the

property or services.

4/ For the purposes of sub-article (2)(a), if the property or services fringe

benefit is the provision of free or subsidised air travel by an employer

that is an airline operator, the normal selling price is the standard

economy fare for the flight provided by the employer.

17. Employee Share Scheme Benefit

1/ The value of a right or option to acquire shares granted to an employee

under an employee share scheme shall not be treated as a fringe benefit

or otherwise included in employment income and:

a) if the employee exercises the right or option, this Article

applies; or

b) if the employee disposes of the right or option, Article 59 of the

Proclamation shall apply to the disposal on the basis that the

right or option is a class „B‟ taxable asset.

2/ The allotment of shares to an employee under an employee share

scheme, including shares allotted as a result of the exercise of an

option or right to acquire the shares, is an employee share scheme

fringe benefit.

3/ Subject sub-article (4), the value of an employee share scheme fringe

benefit shall be the fair market value of the shares at the date of

allotment reduced by the employee‟s contribution for the shares.

4/ If shares allotted to an employee under an employee share scheme are

subject to a restriction on the transfer of the shares, the employee is

FITR/Bochu/8/5/2017

9

treated as having derived the employee share scheme benefit on the

earlier of:

a) the time the employee is able to freely transfer the shares; or

b) the time the employee disposes of the shares.

5/ When sub-article (4) applies, the fair market value of the shares is

determined at the time the employee share scheme benefit is derived as

determined under sub-article (4).

6/ In this Article, “employee‟s contribution”, in relation to shares allotted

to an employee under an employee share scheme, means the sum of the

consideration, if any, given by the employee:

a) for the shares; and

b) for the grant of any right or option to acquire the shares.

18. Residual Fringe Benefit

1/ A benefit provided by an employer to an employee not covered by

another Article in this Part is a residual fringe benefit.

2/ The value of a residual fringe benefit is the fair market value of the

benefit determined at the time it is provided, as reduced by any

payment made by the employee for the benefit.

19. Limitation of Tax Liability on Fringe Benefits

Notwithstanding the provisions of this chapter, the aggregate tax liability on

fringe benefits shall under any circumstance not exceed 10% of the salary

income of the employee.

CHAPTER TWO

FOREIGN EMPLOYMENT INCOME

20. Foreign Employment Income

1/ Article 93(1) of the Proclamation shall apply to a resident employee

employed by a non-resident employer otherwise than as an employee

of an Ethiopian permanent establishment of the non-resident.

2/ If a resident employee has derived foreign employment income for a

calendar month on which the employee has paid foreign income tax,

the employee shall be allowed a tax credit of an amount equal to the

lesser of:

a) the foreign income tax paid; or

FITR/Bochu/8/5/2017

10

b) the employment income tax payable in respect of the foreign

employment income calculated by applying the average rate of

employment income tax applicable to the resident employee to

the foreign employment income of the employee for the month.

3/ Article 45(3), (4), and (5) of the Proclamation shall apply for the

purposes of the tax credit allowed under this Article on the basis that

the reference to “business income tax” is a reference to “employment

income tax” and the reference to “tax year” is a reference to the

“calendar month”.

4/ In this Article:

a) “Average rate of employment income tax”, in relation to a

resident employee for a calendar month, means the percentage

that the employment income tax payable by the employee for

the month, before the allowance of any tax credit, is of the total

employment income of the employee for the month;

b) “Foreign employment income” means foreign income that is

taxable under Schedule „A‟ of the Proclamation;

c) “Foreign income tax” means income tax, including withholding

tax, imposed by the government of a foreign country or a

political subdivision of a government of a foreign country, but

does not include a penalty, additional tax, or interest payable in

respect of such tax;

d) “Resident employee” means an employee who is a resident of

Ethiopia.

PART FOUR

SCHEDULE ‘B’ INCOME

21. Rental Payment Covering More Than One Year

If a lessor or sub-lessor to whom Article 15(5) of the Proclamation applies

receives an amount of rental income for a period in excess of one year, the

total amount of rental income received shall be treated as having been derived

in the tax year in which it was received but the tax payable on the amount

shall be calculated by prorating the rental income over the number of tax years

to which the payment relates.

22. Lease of Business Assets

Income derived from the lease of a business, including goods, equipment, and

buildings that are part of the normal operation of a business, shall be taxable

under Schedule „C‟ of the Proclamation.

FITR/Bochu/8/5/2017

11

23. Depreciation of a Rental Building, Furniture, and Equipment

For the purposes of Article 15(7)(c) of the Proclamation, the deduction

allowed for a tax year for depreciation of a rental building, furniture, and

equipment shall be determined in accordance with Article 25 of the

Proclamation and Chapter Two of Part Five of these Regulations on the basis

that:

a) the rental building is a depreciable asset being a structural

improvement to immovable property; and

b) any furniture and equipment leased with the building are

depreciable assets.

24. Rental Income Losses

1/ If the total rental income for a tax year of a taxpayer keeping records is

exceeded by the deductions allowed to the taxpayer under Article

15(7)(c) of the Proclamation for the tax year, the amount of the excess

shall be treated as a rental loss for the year.

2/ Article 26 of the Proclamation and Article 42 of these Regulations

shall apply to a taxpayer who has a rental loss for a tax year on the

basis that the reference in those Articles to a “loss” is a reference to a

“rental loss”.

25. Foreign Rental Income

1/ If a resident taxpayer has foreign rental income for a tax year on which

the taxpayer has paid foreign income tax, the taxpayer shall be allowed

a tax credit of an amount equal to the lesser of:

a) the foreign income tax paid; or

b) the rental income tax payable in respect of the foreign rental

income of the taxpayer calculated by applying the average rate

of rental income tax applicable to the taxpayer to the net

foreign rental income of the taxpayer for the tax year.

2/ Article 45(3), (4), and (5) of the Proclamation shall apply for the

purposes of the tax credit allowed under this Article on the basis that

the reference to “business income tax” is a reference to “rental income

tax”.

3/ In this Article:

a) “Average rate of rental income tax”, in relation to a resident of

Ethiopia for a tax year, means the percentage that the rental

income tax payable by the resident for the year, before the

FITR/Bochu/8/5/2017

12

allowance of any tax credit, is of the taxable rental income of

the resident for the year;

b) “Foreign income tax” means income tax, including withholding

tax, imposed by the government of a foreign country or a

political subdivision of a government of a foreign country, but

does not include a penalty, additional tax, or interest payable in

respect of such tax;

c) “Foreign rental income” means foreign income taxable under

Schedule „B‟; and

d) “Net foreign rental income”, in relation to a resident taxpayer

for a tax year, means the total foreign rental income of the

taxpayer for the year reduced by the deductions allowed under

Article 15(7) of the Proclamation that relate to the derivation of

that income.

26. Rental Building Notification

For the purpose of Article 17(1) of the proclamation, at the earlier of the time

construction of a rental building completed or when the building is rented, the

owner of the building and the builder shall notify the kebele administration or

local administration in which the building is located about the completion and

the name, address and TIN of the person liable for rental income tax with

respect to the building.

PART FIVE

SCHEDULE ‘C’ INCOME

CHAPTER ONE

DEDUCTIONS

27. Payments of Employment Income to Relatives

1/ a deduction shall be allowed for employment income paid by the

employer to a relative to the extent only that the amount of the

employment income paid is consistent with the value of the services

rendered by the relative and the qualifications of the relative for the

position held.

2/ An amount shall not be included in the employment income of an

employee to the extent that the employer has been denied a deduction

for the payment of the employment income under sub-article (1).

3/ The mode of application of this article shall be determined by a directive

to be issued by the Authority.

28. Representation Expenditures

FITR/Bochu/8/5/2017

13

For the purposes of Article 27(1)(i) of the Proclamation, “representation

expenditures” shall mean hospitality expenditures incurred by an employee in

receiving guests from outside the business for the purposes of promoting and

enhancing the business.

29. Deductibility of Interest Paid to a Foreign Bank

Interest paid to a foreign bank referred to in Article 23(2)(a)(2) of the

Proclamation shall be deductible only if the foreign bank has provided the

Authority with a copy of the National Bank of Ethiopia authorisation for the

loan.

30. Medical Expense Incurred for Employees’

Medical expense incurred by an employer for his employee including

premium payments made under employees‟ health insurance scheme shall be

deducted in accordance with Article 22(1)(a) of the Proclamation.

31. Food and beverage services provided by establishments engaged in the

provision of Food and Beverage Services

Expenditure incurred in the provision of food and beverage services by Hotels

, Restaurants and other similar establishments for their employees shall be

deducted in accordance with Article 22(1)(a) of the proclamation to the extent

allowed by a directive to be issued by the minister.

32. Business Promotion Expenditure

Expenses incurred locally or abroad in connection with the promotion of the

business shall be deductible in accordance with the limits set by the directive to be

issued by the Minister.

33. A lessee maintaining or repairing or improving a business asset at his own

Expense

Expenditure incurred by a lessee in the maintenance or repair or improvement of

the leased business asset in accordance with the contract concluded with the

lessor, shall be deducted from the business income of the lessee.

34. Charitable Donation

1. A deduction allowed under Article 24(1) of the proclamation for charitable

donations shall apply to expenses incurred by the tax payer in the management

of his own charitable activities.

FITR/Bochu/8/5/2017

14

2. For the purpose of Article 24(1) b of the proclamation, call by the government

means call by the federal government or a regional state and includes a call by

the Addis Ababa and Diredawa city administrations.

35. Deduction allowed for Business Asset held under a Hire Purchase

Agreement

Lease payment made for business asset held under a hire purchase agreement

is deductible business expenditure from gross business income. However, a

person realizing deduction under this article shall not be entitled to

depreciation on the asset.

CHAPTER TWO

DEPRECIATION

36. Depreciation of Depreciable Assets and Business Intangibles

1/ Subject to sub-article (2), a taxpayer may determine the depreciation

deduction allowed under Article 25(1) of the Proclamation according

to the straight-line method under Article 37 of these Regulations or the

diminishing value method under Article 38 of these Regulations

provided:

a) the taxpayer has used the same method of depreciation in its

financial accounts prepared in accordance with financial

reporting standards; and

b) the same method of depreciation is used by the taxpayer for all

depreciable assets owned by the taxpayer.

2/ The following assets shall be depreciated only under the straight-line

method:

a) a business intangible;

b) a structural improvement;

3/ For the purposes of calculating the depreciation deduction in relation

to a structural improvement, the cost of the structural improvement

shall not include the cost of the land on which the improvement is

situated.

4/ No depreciation deduction shall be allowed for the cost of a

depreciable asset or business intangible acquired by a taxpayer from a

related person (“transferor”) when the cost of the asset or intangible

had been fully depreciated by the transferor.

37. Straight-line Depreciation

FITR/Bochu/8/5/2017

15

1/ Subject to Article 25(3) and (4) of the Proclamation, the depreciation

deduction allowed to a taxpayer for a tax year in respect of a

depreciable asset or business intangible under the straight-line method

shall be calculated by applying the rate specified in Article 32 of these

Regulations against the cost of the asset.

2/ The total deductions allowed, or that would be allowed but for Article

25(4) of the Proclamation, to a taxpayer in respect of a depreciable

asset or business intangible to which this Article applies for the current

tax year and all previous tax years shall not exceed the cost of the

asset.

38. Diminishing Value Depreciation

1/ Subject to Article 25(3) and (4) of the Proclamation, the depreciation

deduction allowed to a taxpayer for a tax year in respect of a

depreciable asset under the diminishing value method shall be

calculated by applying the rate specified in Article 32 of these

Regulations against the net book value of the asset at the beginning of

the year.

2/ If Article 25(4) of the Proclamation applies to a depreciable asset for a

tax year, the net book value of the asset shall be calculated on the basis

that the asset has been used in that year solely to derive business

income.

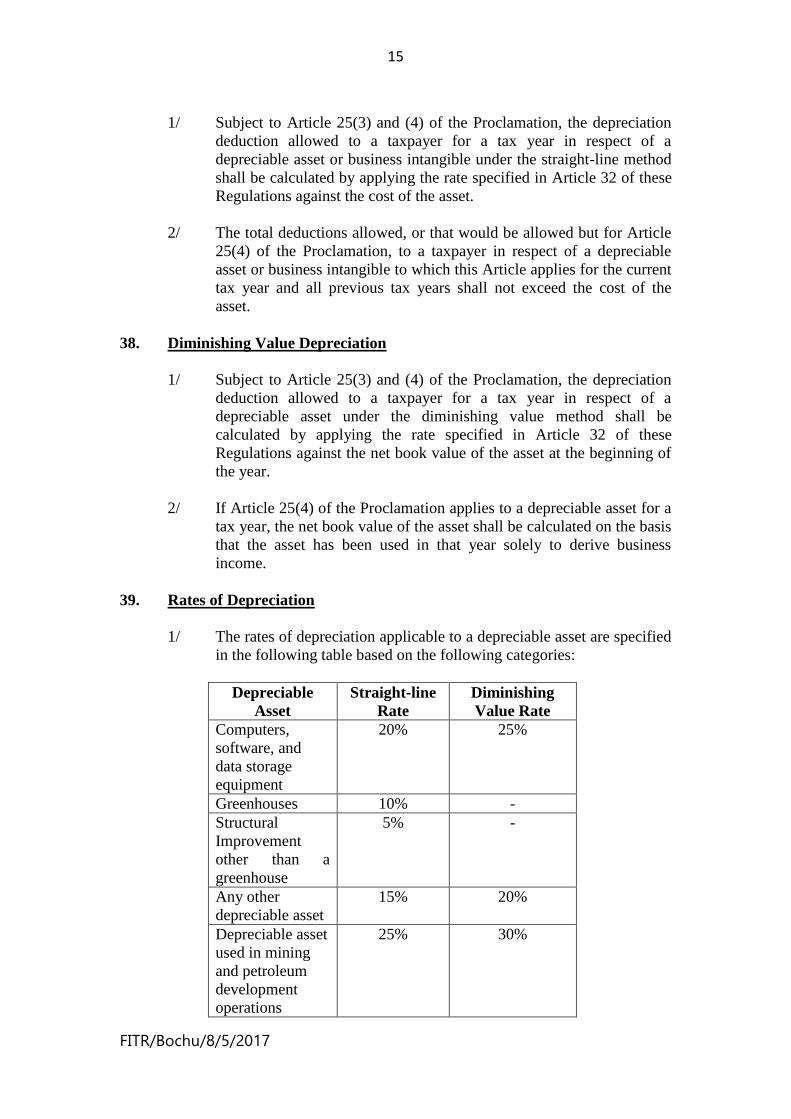

39. Rates of Depreciation

1/ The rates of depreciation applicable to a depreciable asset are specified

in the following table based on the following categories:

Depreciable

Asset

Straight-line

Rate

Diminishing

Value Rate

Computers,

software, and

data storage

equipment

20% 25%

Greenhouses 10% -

Structural

Improvement

other than a

greenhouse

5% -

Any other

depreciable asset

15% 20%

Depreciable asset

used in mining

and petroleum

development

operations

25% 30%

FITR/Bochu/8/5/2017

16

2/ The rate of depreciation applicable to a business intangible shall be:

a) for preliminary expenditure, 25%;

b) for a business intangible with a useful life of more than 10

years, other than a business intangible referred to in paragraph

(a), 10%; or

c) for any other business intangible, 100% divided by the useful

life of the intangible.

3/ In this Article, “preliminary expenditure” means expenditure referred

to in paragraph (4) of the definition of “business intangible” in Article

25(7)(a) of the Proclamation incurred by a taxpayer before the

commencement of a business.

40. Depreciation allowed on a Building used Partially as a Business Asset

Depreciation on a building used partially as a business asset shall be allowed

only in proportion to the portion of the property used as a business asset.

41. Repairs and Improvements

1/ Subject to sub-article (2), a taxpayer shall be allowed a deduction for a

tax year for the cost of a repair or improvement made to a depreciable

asset during the year.

2/ The amount of the deduction allowed under sub-article (1) shall not

exceed 20% of the net book value of the asset at the end of the tax

year.

3/ The amount of any excess under sub-article (2) shall be added to the

net book value of the asset.

CHAPTER THREE

LOSS CARRY FORWARD

42. Loss Carry Forward

1/ If a taxpayer has a loss carried forward under the Proclamation for

more than one tax year, the loss of the earliest year shall be deducted

first.

2/ A loss may be carried forward under the Proclamation only if the

taxpayer‟s books of account showing the loss are audited and

acceptable to the Authority.

FITR/Bochu/8/5/2017

17

3/ Despite sub-article (2), a taxpayer may carry a loss forward if:

a) the taxpayer has submitted books of account to the Authority

showing that the loss has been audited by external auditors; and

b) the Authority has failed to audit the taxpayer‟s books of

account before the due date for filing the taxpayer‟s tax

declaration for the next following tax year.

4/ Nothing in sub-article (3) prevents the Authority from subsequently

auditing the loss and serving the taxpayer with a notice of amended

assessment in relation to the loss in accordance with Article 28 of The

Federal Tax Administration Proclamation.

5/ In this Article, a reference to a loss carried forward means a loss

carried forward under Article 26, 38, or 46 of the Proclamation.

CHAPTER FOUR

FOREIGN CURRENCY EXCHANGE GAINS AND LOSSES

43. Foreign Currency Exchange Gains and Losses

1/ A foreign currency exchange gain derived by a taxpayer shall be

included in business income.

2/ Subject to sub-article (3), if a taxpayer incurred a foreign currency

exchange loss during a tax year, the loss shall be offset against a

foreign currency exchange gain derived by the taxpayer during the

year subject to the following:

a) the unused amount of a loss can be carried forward indefinitely

for offset against foreign currency exchange gains until fully

offset;

b) the taxpayer has substantiated the amount of the loss to the

satisfaction of the Authority.

3/ Sub-article (2) shall not apply to a foreign currency exchange loss

incurred by a financial institution and the amount of the loss shall be

allowed as a deduction provided the financial institution has

substantiated the amount of the loss to the satisfaction of the Authority.

4/ A taxpayer derives a foreign currency exchange gain or incurs a

foreign currency exchange loss when the gain or loss is realised.

5/ In determining whether a taxpayer has derived a foreign currency

exchange gain or incurred a foreign currency exchange loss in respect

of a foreign currency transaction, account must be taken of the

taxpayer‟s position under a hedging contract entered into by the

taxpayer or by a related person in relation to the transaction.

FITR/Bochu/8/5/2017

18

6/ In this Article:

a) “Debt obligation” means an obligation to make a payment of

money to another person, including accounts payable and the

obligations arising under promissory notes, bills of exchange,

and bonds;

b) “Foreign currency exchange gain” means a gain attributable to

currency exchange rate fluctuations derived in respect of a

foreign currency transaction;

c) “Foreign currency exchange loss” means a loss attributable to

currency exchange rate fluctuations incurred in respect of a

foreign currency transaction;

d) “Foreign currency transaction” means any of the following

transactions entered into in the conduct of a business to derive

business income:

(1) a dealing in a foreign currency;

(2) the issuing of, or obtaining a debt obligation,

denominated in foreign currency; or

(3) any other dealing in which foreign currency is

denominated;

e) “Hedging contract” means a contract entered into by a person

for the purpose of eliminating or reducing the risk of adverse

financial consequences that might result for the person under

another contract from currency exchange rate fluctuations.

CHAPTER FIVE

BANKS AND INSURANCE COMPANIES

44. Loss Reserve of Banks

A bank shall be allowed a deduction for a tax year for 80% of its loss reserve

for the year provided the amount of the reserve has been calculated in

accordance with the prudential requirements prescribed by the National Bank

of Ethiopia and is consistent with financial reporting standards.

45. Reserve for Unexpired Risks of General Insurance Companies

1/ Subject to sub-article (2), an insurance company carrying on the

business of general insurance shall be allowed a deduction for a tax

year of the balance of its reserve for unexpired risks as at the end of the

year provided the amount of the reserve has been calculated in

accordance with financial reporting standards.

FITR/Bochu/8/5/2017

19

2/ If an insurance company is a non- resident company carrying on

business through a permanent establishment in Ethiopia, the deduction

allowed under sub-article (1) shall be limited to the balance of the

company‟s reserve for unexpired risks in Ethiopia.

3/ The business income of an insurance company carrying on the

business of general insurance for a tax year shall include the amount of

the company‟s reserve for unexpired risks deducted in the previous tax

year under sub-article (1) or (2), as the case may be.

4/ In this Article, “General Insurance” means all insurance other than life

insurance as defined under Article 691 of the Commercial Code

Proclamation 1960.

46. Taxable Income from Life Insurance Business

1/ The taxable income of an insurance company from the conduct of the

business of life insurance for a tax year shall be calculated according to

the following formula:

(A + B + C + D) – (E + F + G + H)

where:

A is the life insurance premiums derived by the company during

year but not including premiums returned to policy holders

during the year;

B is investment income derived by the company during the year

relating to the business of life insurance;

C is the amount of any previously deducted reserves for life

policies cancelled during the year;

D is any other income derived by the company during the year

relating to the life insurance business;

E is underwriting expenses incurred by the company during the

year in the conduct of life insurance business, including

commissions paid, reinsurance premiums, risk analysis costs,

Government charges on the policy, and operating expenses;

F is the additions to life policy reserves, including the initial

reserve on new life policies issued during the year;

G is the amount of claim payments under life policies made in

excess of the sum of reserved amounts and income earned on

the reserved amounts in relation to life policies paid out during

the year; and

FITR/Bochu/8/5/2017

20

H is any other deductible expenditure incurred by the company

during the year in relation to the life insurance business.

2/ If a company conducts the business of life insurance and some other

business including the business of general insurance, the taxable

income of the company from the conduct of the life insurance business

shall be calculated separately from the taxable income from other

business of the taxpayer.

3/ In this Article, “Life Insurance” has the meaning in Article 691 of the

Commercial Code Proclamation 1960.

CHAPTER SIX

MICRO ENTERPRISES

47. Obligation of Micro Enterprises to maintain Books of Account

For the purpose of Article 82 of the proclamation, micro enterprises shall be

treated as individual.

CHAPTER SEVEN

CATEGORY ‘C’ TAXPAYERS

48. Presumptive Business Taxation of Category ‘C’ Taxpayers

1. The presumptive business tax to be paid by category “c” taxpayers shall

be calculated in accordance with the schedule attached to this

proclamation.

2. The annual taxable income of a tax payer shall be assessed in accordance

with the maximum annual turnover in the bracket within which the

annual gross income of the tax payer falls.

PART SIX

SCHEDULE ‘D’ INCOME

49. Income from Casual Rentals

For the purpose of Article 58 of the Proclamation “Income derived from

Casual rental of asset” means gross income derived by a person who is not

engaged in the regular business of rental of movable or immovable asset.

50. Repatriated Profit of a Permanent Establishment

1/ The tax under Article 62 of the Proclamation on the repatriated profit

of a non-resident body conducting business through a permanent

FITR/Bochu/8/5/2017

21

establishment in Ethiopia shall be imposed by reference to the body‟s

tax year.

2/ The repatriated profit of a body for a tax year shall be calculated in

accordance with the following formula:

A + (B - C) - D

where:

A is the total cost of assets, net of liabilities, of the permanent

establishment at the commencement of the tax year;

B is the net profit of the permanent establishment for the tax year

calculated in accordance with financial reporting standards;

C is the business income tax payable on the taxable income of the

permanent establishment for the tax year; and

D is the total cost of assets, net of liabilities, of the permanent

establishment at the end of the tax year.

3/ In calculating the repatriated profit of a permanent establishment for a

tax year, the total cost of assets of the permanent establishment at the

end of a tax year shall be the total cost of assets at the commencement

of the next following tax year.

51. The effect of Adjustment of Business Profit in accordance with a Tax

Audit on Tax paid on paid out Dividends

The fact of a business profit declared by a body being less than the adjusted

business profit of the body by the authority in accordance with the finding of a

tax audit, shall not affect the tax on dividend distributed to shareholders on the

basis of the profit declared by that body.

52. Capital gains tax payable on the disposal of certain investment assets by

Donation

1. For the purpose of Article 59 of the proclamation, tax payable on a capital

asset disposed by donation shall be calculated on the difference between the

original cost of the asset and the cost of the asset at the time of disposal by

donation.

2. The donee /receiver shall be liable to pay tax on a capital asset disposed by

donation.

FITR/Bochu/8/5/2017

22

PART SEVEN

EXEMPT INCOME 53. Exempt Income

1. The items of income listed below are exempt from tax.

a. the provision of food and beverage services by Hotels ,

Restaurants and other similar establishments for their

employees,

b. Membership contribution to non-profit entities

c. Income from employment received by unskilled employee

working for the same employer whether continuously or intermittently

for not more than thirty (30) days within any twelve month period,

provided however that the tax payable on income from employment

received by a casual employee working intermittently for the same

employer for more than thirty (30) days within twelve months period

shall be calculated only on the income received by that employee from

the last employment.

For the purpose of this exemption “unskilled employee” shall mean an

employee who has not received vocational training , does not use

machinery or equipment requiring special skill, and who is engaged by

an employer for a period aggregating not more than thirty(30)days

during a calendar year.

2. The exemption accorded under Article 65(1)( a) (1) of the

proclamation to an amount paid by an employer to cover the cost of

medical treatment of an employee shall include premium payments

made by an employer on behalf of an employee under employees‟

medical insurance scheme.

PART EIGHT

ASSETS

54. Disposal and Acquisition

Notwithstanding the provision of Article 1185 of the civil code, for the

purpose of depreciation and capital gain tax, when a registerable asset is

transferred by sale, exchange or gift, the transferor is treated as having

disposed of the asset and the transferee is treated as having acquired the

asset at the time the contract of sale, exchange or gift is registered by an

entity empowered to exercise the function of the notary.

55. Cost

FITR/Bochu/8/5/2017

23

1/ The cost of a class „A‟ taxable asset shall be adjusted for inflation as

determined under a Directive issued by the Minister.

2/ If the acquisition of an asset by a taxpayer is the derivation of an

amount that is:

a) included in the income of the taxpayer subject to tax under the

Proclamation, the cost of the asset is the amount so included

plus any amount paid by the taxpayer for the asset; or

b) exempt income, the cost of the asset is the exempt amount plus

any amount paid by the taxpayer for the asset.

PART NINE

ADMINISTRATIVE AND PROCEDURAL RULES

56. Books of Account to be kept by Category ‘B’ Taxpayers

The authority shall determine by directive the documents that category “B” tax payers

shall be required to submit together with their books of account.

57. Books of Account and Documents to be Kept by Category ‘C’ Taxpayers

1. For the purpose of Article 82(3) of the proclamation, category “C” tax

payers may keep book of accounts that category “B” tax payers are

required to maintain.

2. Notwithstanding the provision of sub article (1) of this article, a category

“C” tax payer employing a worker shall keep documents showing any

amount of employment income paid to the employee and any amount

withheld in tax from such income.

58. Payment of Tax by Category ‘C’ Taxpayers

For the purposes of Article 49 of the Proclamation, Category „C‟ taxpayers

shall pay tax in accordance with standard presumptive business tax and

indicator based presumptive business tax methods.

59. Services to which Withholding Tax shall not apply

For the purpose of Article 92 of the proclamation, the minister shall specify by

a directive the type of services to which withholding tax shall not apply.

60. Withholding of Tax from Domestic Payments

FITR/Bochu/8/5/2017

24

1/ A withholding agent required to withhold tax under Article 92 of the

Proclamation shall issue a serially numbered official receipt to the

recipient of the payment from which tax is to be withheld under that

Article.

2/ If the withholding agent is a Government agency, the receipts referred

to in sub-article (1) shall be authenticated by the Ministry.

3/ Article 19 of the Federal Tax Administration Proclamation shall apply

to receipts referred to in sub-article (1) issued by a withholding agent

other than a Government agency.

61. Requirement to provide Trade License to a Withholding Agent

The provision of article 92(4) of the proclamation shall apart from tax payers

failing to produce TIN, also apply to person not producing trade license.

62. The liability of a withholding agent

1. Article 97(3) of the proclamation shall not apply where a withholding agent

required to withhold and transfer tax to the authority under the proclamation

presents evidence to the tax authority that the principal tax payer has paid the

tax, notwithstanding that the withholding agent has failed to withhold and

transfer the tax.

2. The provision of sub article 1 of this article doesn‟t preclude the penalty

imposed under article of 106(1) of the Tax Administration Proclamation.

63. Delayed submission of Books of Account

1. Books of account shall not be rejected by reason of late submission.

2. The provision of sub article 1 shall not apply

a. Where the tax has been assessed by estimation because of non-filing of tax

return.

b. doesn‟t preclude the penalty imposed under article 102 of the Tax

Administration Proclamation.

PART TEN

TRANSITIONAL REGULATIONS

64. Pooled Depreciable Assets

1/ A taxpayer who has a positive balance in a depreciation pool at the

commencement of the Proclamation shall continue to depreciate the

balance of the pool in accordance with repealed Proclamation.

FITR/Bochu/8/5/2017

25

2/ If a taxpayer to whom sub-article (1) applies disposes of a depreciable

asset in a depreciation pool, the consideration for the disposal shall

reduce the depreciation base of the pool.

3/ If, as a result of a disposal a depreciable asset referred to in sub-article

(1), the depreciation base of a depreciation pool is a negative amount:

a) the negative amount is included in business income; and

b) the pool is treated as closed and any assets remaining in the

pool are treated as fully depreciated.

4/ A taxpayer who has acquired a depreciable asset on or after the

commencement of the Proclamation shall depreciate the asset in

accordance with Article 29 of these Regulations and the cost of the

asset shall not be added to a depreciation pool referred to in sub-article

(1).

65. Business Loss Carried Forward

1/ A taxpayer who has a business loss under the repealed Proclamation

that has not been fully deducted under the repealed Proclamation shall

continue to deduct the loss in accordance with the repealed

Proclamation.

2/ Any loss incurred under the repealed Proclamation shall not be taken

into account for the purposes of Article 26(4) of the Proclamation.

66. Exemptions under Directives

An exemption provided for in a Directive issued by the Minister prior to the

commencement of the Proclamation shall remain in force until the earlier of:

a) the date that the Directive lapses according to its terms; or

b) the date that the Minister withdraws the Directive.

PART ELEVEN

MISCELLANEOUS

67. Directives

The Minister may issue Directives for the proper implementation of these

Regulations.

68. Repealed and inapplicable laws

1/ The Income Tax Regulations No. 78/2002(as amended) are repealed

by these Regulations.

FITR/Bochu/8/5/2017

26

2/ The repealed Regulations shall continue to apply for tax years

preceding the effective date of these Regulations

69. Effective Date

This Regulation shall apply on income derived as of 8th

day of July, 2016.

Done at Addis Ababa, this….day of….., 2016.

Hailemariam Dessalegn

Prime Minister of the Federal Democratic

Republic of Ethiopia

Related Documents