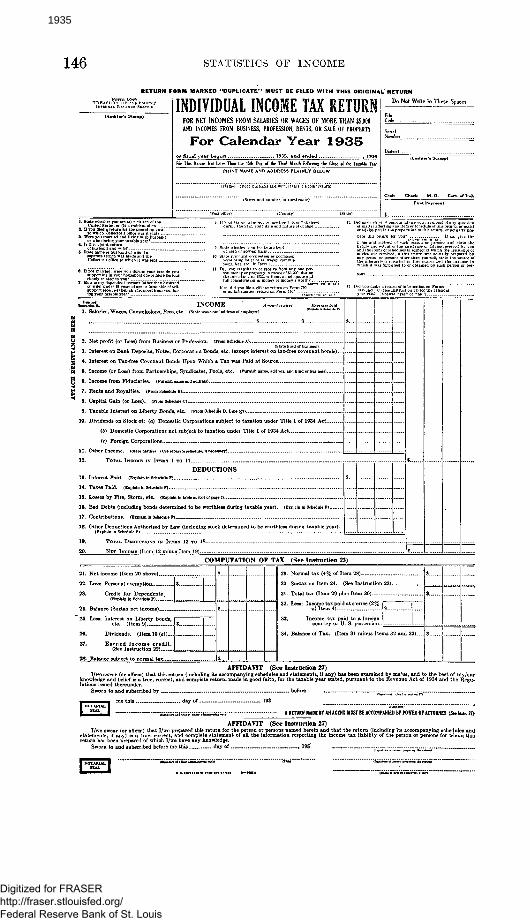

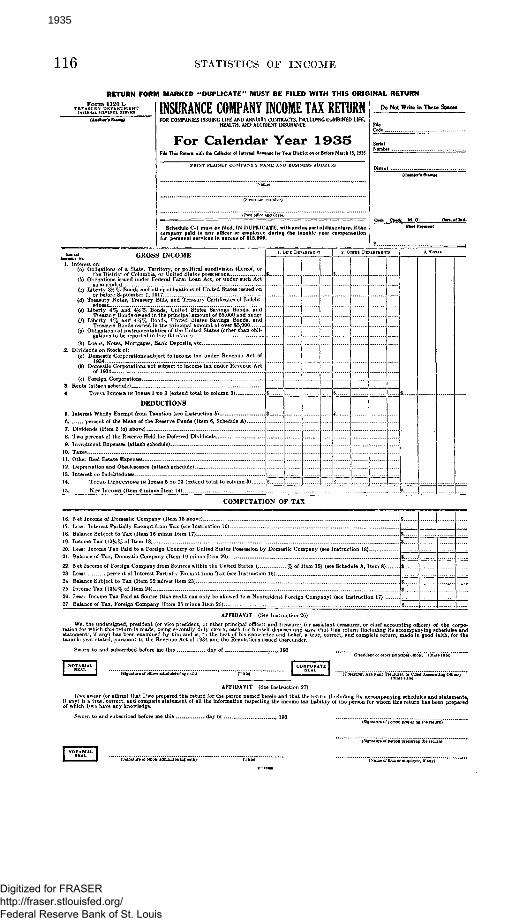

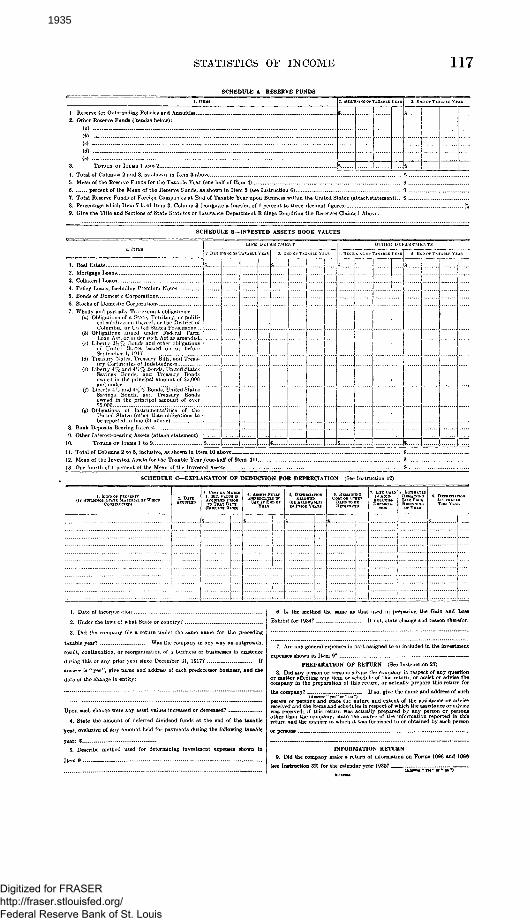

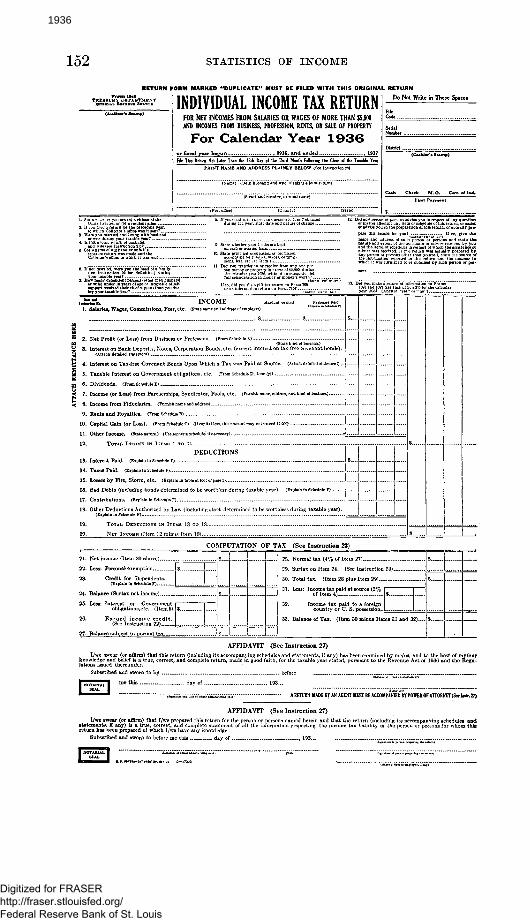

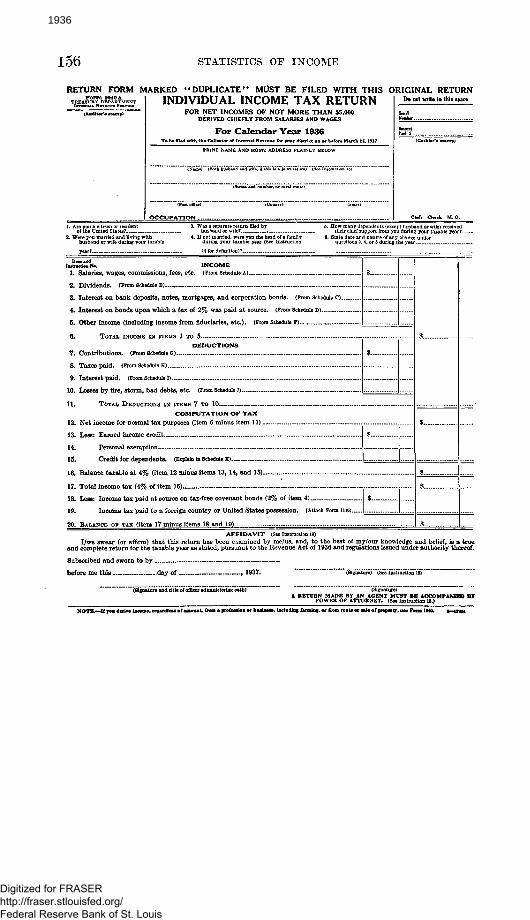

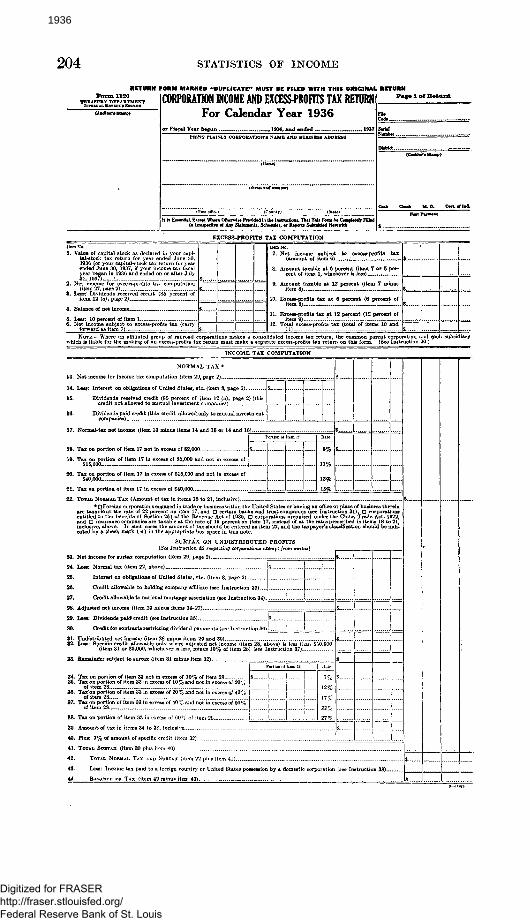

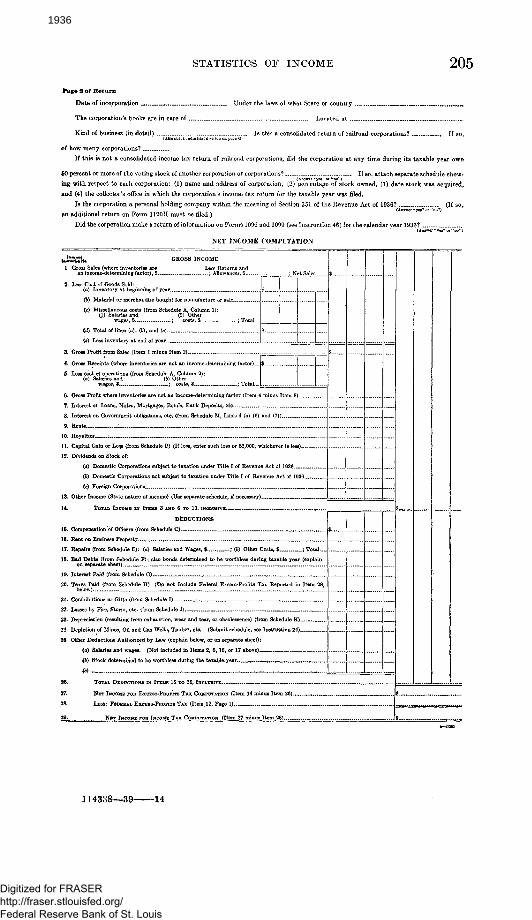

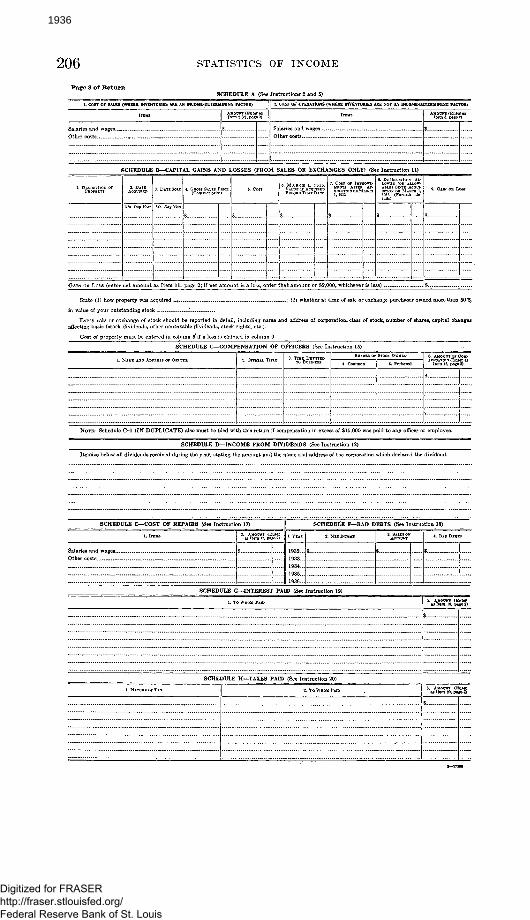

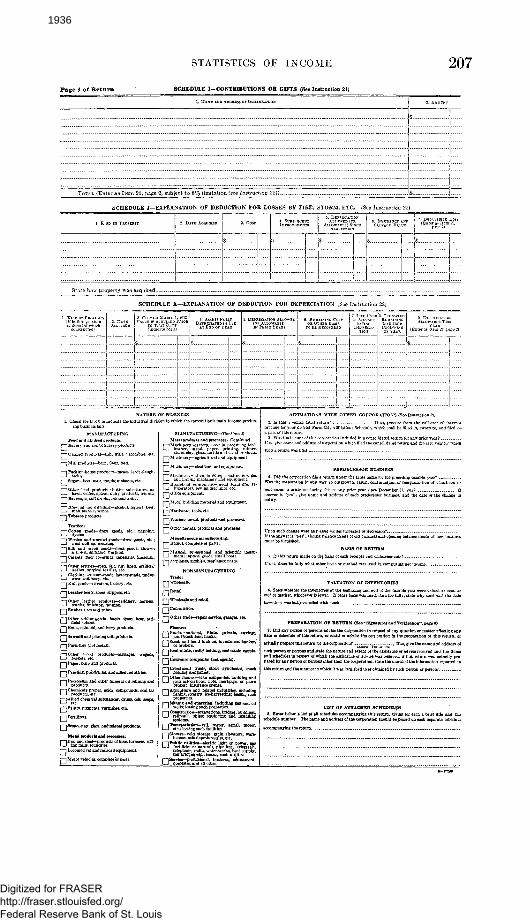

146 STATISTICS OF IXCOME TREASl (A RETURN F uditor'. SUmp) INDIVIDUAL INCOME TAX RETURN FOR NET INCOMES FROM SALARIES OR WAGES OF MORE THAN $5000 AND INCOMES FROM BUSINESS, PROFESSION, RENTS, OR SALE OF PROPERTY For Calendar Year 1935 or fiscal y e a r b e j u n , 1935, and ended , 1936 File Tbii Return Nol Uler Than lit 15th Day of tbe Third Month Folloiring the Close of the Taxable Year PRINT NAME AND ADDRESS PJ_AINLY BELOW (Name) (Doth husband and wifo, if this is a joint return) if^toS^ " iCounty) " --<SU«r" L RETURN Do Not Write In These Spaces File Code Serial Number v .. District (C h.«. Stamp) C».h Chwk M.O. C.rt.oflru) $ pporting in } Ing your taxable yearT . bM?*. INCOME Amourtrva.* Erptns,, void 1. Salaries, Wages, Commissions, Fees, etc. (State name ond address of employer) (ErtA« ufctaduur) $ $ . 2. Net profit (or Loss) from Business or Profession. (From Schedule A) 3. Interest on Bank Deposits, Notes, Corporation Bonds, etc. (except interest on tax-free covenant bonds)... 4. Interest on Tax-free Covenant Bonds Upon Which a Tax was Paid at Source 5. Income (or Loss) from Partnerships, Syndicates, Pools, etc. (Furnish name, address, and kind of business) 7. Rents and Royalties. (From Schedule B) 8. Capital Gain (or Loss). (From Schedule C) .... 9. Taxable Interest on Liberty Bonds, etc. (From Schedule D, Line (g)) 10. Dividends on Stock of: (a) Domestic Corporations subject to taxation under Title I of 1934 Act (6) Domestic Corporations not subject to taxation undei Title I of 1934 Act _ 12. TOTAL INCOME IN ITEMS 1 TO 11 _ _ DEDUCTIONS 13. Interest Paid. (Explain In Schedule T) „ 14. Taxes Paid. (Explain in Schedule F) 16. Bad Debts (including bonds determined to be worthless during taxable year). (Explain in Schedule F) 17. Contributions. (Explain In Schedule F) 18. Other Deductions Authorized by Law (including stock determined to be worthless during taxable year). S $ 19 TOTAL DEDUCTIONS IN ITEMS 13 TO 18. 20. NET INCOME (Item 12 minus Item 19) - $ $ COMPUTATION OF TAX (See Instruction 23) 21. Net income (Item 20 above) 22. Less: Personal exemption 23. Credit for Dependents, (Explain in Schedule F) '. 24. Balance (Surtax net income) etc. (Item 9) 26. Dividends. (Item 10 (a)) 27. Earned income credit. (See Instruction 22) $ $ 28. Balance subject to normal tax $.... $ 29. Normal tax (4% of Item 28) 30. Surtax on Item 24. (See Instruction 23) 3i. Total tax (Item 29 plus Item 30) 32. Less: Income tax paid at source (2% of Item 4) 33. Income tax paid to a foreign country or U. S. possession.. 34. Balance of Tax. (Item 31 minus Itei $ na 32 and 33) $ $ S AFFIDAVIT (See Instruction 27) I/we swear (or affirm) that this return (including its accompanying schedules and statements, if any) has been knowledge and belief is a true, correct, and complete return, made in good faith, for the taxable year stated, pursui lations issued thereunder. Sworn to and subscribed by - ........... .. «... before ........ ... ie this .. .. day of.. ..... 192 f s - j 5i.-i-^.-urJu.-i-:Ei--i£ii;-;« A RETURN MADE BY AN AGENT MUST BE ACCOMPANIED BY POWER OF ATTORNEY (Set Inslr. 27> AFFIDAVIT (See Instruction 27) I/we swear (or affirm) that I/we prepared this return for the person or persons named herein and that the return (including its accompanying schedules and statements, if any) is a true, correct, and complete statement of all the information respecting the income tax liability of the p ' ' return has been prepared of which I/we have any knowledge. Sworn to and subscribed before me this day of , 195 „ :. >r persons r whom this Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis 1935

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

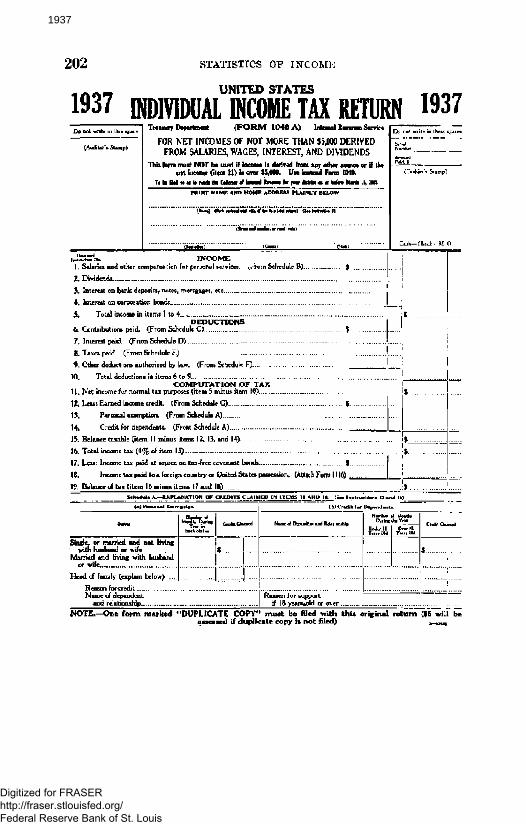

146 STATISTICS OF IXCOME

TREASl

(A

RETURN F

uditor'. SUmp)INDIVIDUAL INCOME TAX RETURN

FOR NET INCOMES FROM SALARIES OR WAGES OF MORE THAN $5000

AND INCOMES FROM BUSINESS, PROFESSION, RENTS, OR SALE OF PROPERTY

For Calendar Year 1935or fiscal y e a r b e j u n , 1935, a n d e n d e d , 1936

File Tbii Return Nol Uler Than lit 15th Day of tbe Third Month Folloiring the Close of the Taxable Year

PRINT NAME AND ADDRESS PJ_AINLY BELOW

(Name) (Doth husband and wifo, if this is a joint return)

i f ^ t o S ^ " iCounty) " - -<SU«r"

L RETURN

Do Not Write In These Spaces

FileCode

Serial

Number v . .

District

(C h . « . Stamp)

C».h Chwk M.O. C.rt.oflru)

$

pporting in }

Ing your taxable yearT .

b M ? * . INCOME Amourtrva.* Erptns,, void1. Salaries, Wages, Commissions, Fees, etc. (State name ond address of employer) (ErtA« u fctaduu r)

$ $ .

2. Net profit (or Loss) from Business or Profession. (From Schedule A)

3. Interest on Bank Deposits, Notes, Corporation Bonds, etc. (except interest on tax-free covenant bonds)...

4. Interest on Tax-free Covenant Bonds Upon Which a Tax was Paid at Source

5. Income (or Loss) from Partnerships, Syndicates, Pools, etc. (Furnish name, address, and kind of business)

7. Rents and Royalties. (From Schedule B)

8. Capital Gain (or Loss). (From Schedule C) ....

9. Taxable Interest on Liberty Bonds, etc. (From Schedule D, Line (g))

10. Dividends on Stock of: (a) Domestic Corporations subject to taxation under Title I of 1934 Act

(6) Domestic Corporations not subject to taxation undei Title I of 1934 Act _

12. TOTAL INCOME IN ITEMS 1 TO 11 _ _

DEDUCTIONS

13. Interest Paid. (Explain In Schedule T) „

14. Taxes Paid. (Explain in Schedule F)

16. Bad Debts (including bonds determined to be worthless during taxable year). (Explain in Schedule F)

17. Contributions. (Explain In Schedule F)

18. Other Deductions Authorized by Law (including stock determined to be worthless during taxable year).

S

$

19 TOTAL DEDUCTIONS IN ITEMS 13 TO 18.

20. NET INCOME (Item 12 minus Item 19) -

$

$

COMPUTATION OF TAX (See Instruction 23)

21. Net income (Item 20 above)

22. Less: Personal exemption

23. Credit for Dependents,(Explain in Schedule F) '.

24. Balance (Surtax net income)

etc. (Item 9)

26. Dividends. (Item 10 (a))

27. Earned income credi t .(See Instruction 22)

$

$

28. Balance subject to normal tax

$....

$

29. Normal tax (4% of Item 28)

30. Surtax on Item 24. (See Instruction 23)

3i. Total tax (Item 29 plus Item 30)

32. Less: Income tax paid at source (2%of Item 4)

33. Income tax paid to a foreigncountry or U. S. possession..

34. Balance of Tax. (Item 31 minus Itei

$

na 32 and 33)

$

$

S

AFFIDAVIT (See Instruction 27)I/we swear (or affirm) that this return (including its accompanying schedules and statements, if any) has been

knowledge and belief is a true, correct, and complete return, made in good faith, for the taxable year stated, pursuilations issued thereunder.

Sworn to and subscribed by - . . . . . . . . . . . . . « . . . before ... . . . . . . . .

ie this . . . . day of.. . . . . . 192

f s - j 5 i . - i - ^ . - u r J u . - i - : E i - - i £ i i ; - ; « A RETURN MADE BY AN AGENT MUST BE ACCOMPANIED BY POWER OF ATTORNEY (Set Inslr. 27>

AFFIDAVIT (See Instruction 27)I/we swear (or affirm) that I/we prepared this return for the person or persons named herein and that the return (including its accompanying schedules and

statements, if any) is a true, correct, and complete statement of all the information respecting the income tax liability of the p ' 'return has been prepared of which I/we have any knowledge.

Sworn to and subscribed before me this day of , 195 „ : .

>r persons r whom this

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

1935

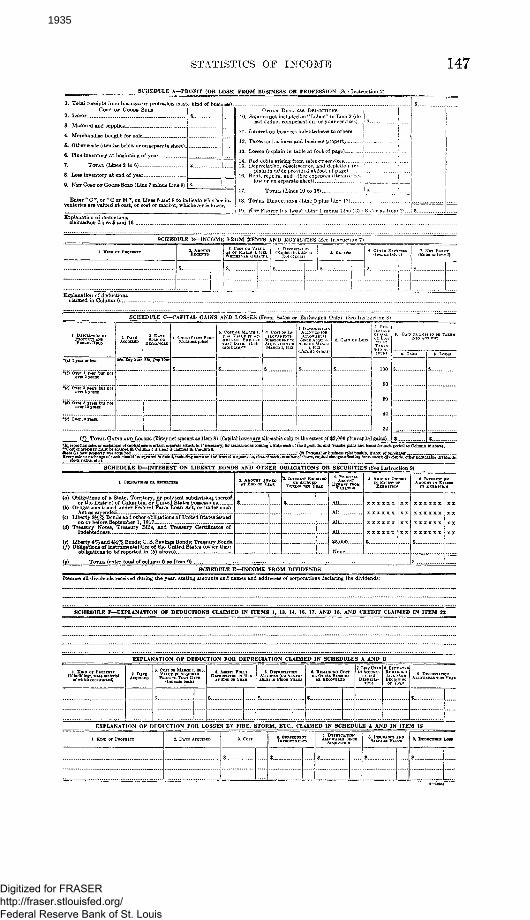

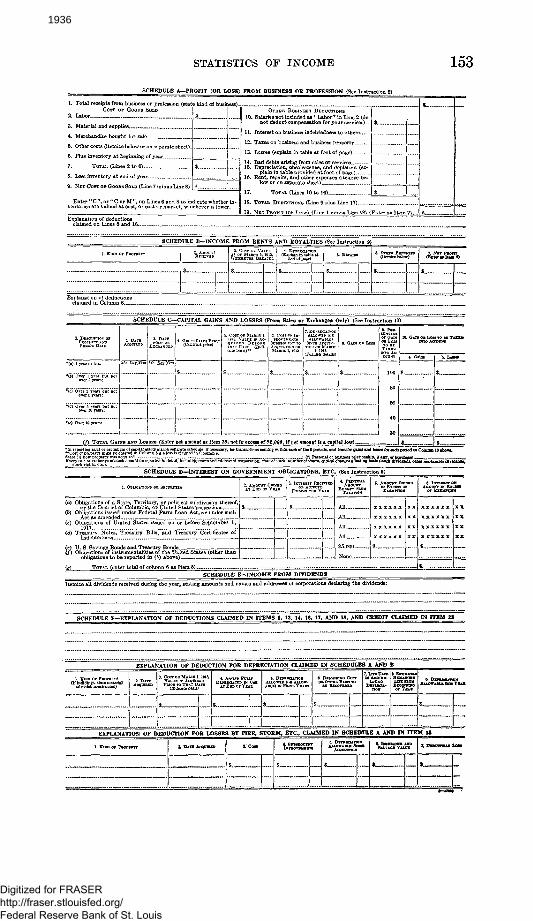

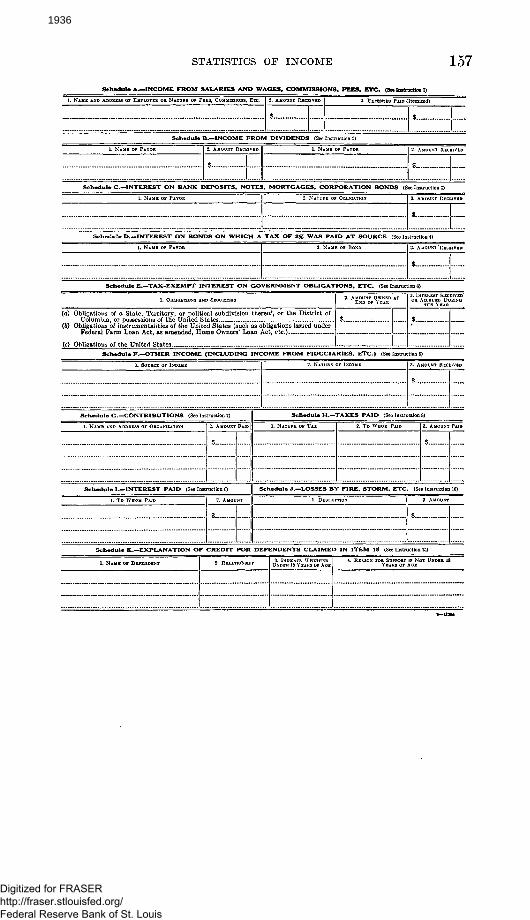

STATISTICS OF INCOME 147SCHEDULE A—PKOF5T (OR LOSS) FROM BUSINESS OR PROFESSION (See Inatruction 2)

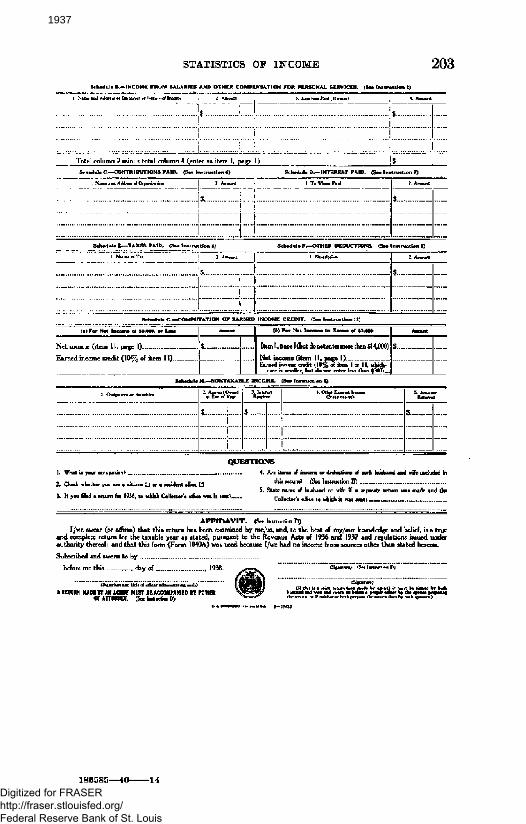

1. Tetal receipts <roCOST C

2. Labor

w or profession (state kind of business)...

3. Material and oupplies

4. Merchandise bought for sale ,..

5. Other cost* (itemize below or on separata sheet)

6. Plus inventory at beginning of year...

7. TOTAL (lines 2 to 6)

8. Less inventory at end of year

9. NET COST or GOODS SOLD (Lino 7 minus Line 8}

ventories are valued at cost, or cost or market, whicheyer is lo

10. Salaries not included

not deduct compensation for your services)...

11. Interest on business indebtedness to others

12. Taxes on business and business property

13. Losses (explain in table at foot of page)

14. Bad debts arising from Bales cr services15. Depreciation, obsolescence, and depletion (ex-

plain id t&blQ providt'Ci st foot of pajjo)16. Rent, rcp&irs, &HQ otnsf expenses (iteiiiizo be-

low or on separate sheet) .*17. TOTAL (Lines 10 to 16) . - U _

(Line 1 minus Lino IS) (Er.te19. NET Pnonr (ox L

SCHEDULE B--INCOME FROM: RENTS^ND ROYALTIES (Sea Instruction 7)

• ( • ) I year or loss:

•(6) Ovor 1 year bat not

•(<) Over 5 yean bnt notover 10 yoara:

•(«) Ovor )0 yean:

(/) TOTAL GAI

SCHI

ElCHAJiOiD

-CAPITAL GAINS

$

N8 AND LOSSES (Enter net amotBt as Item 8

AND LOSSES(

eato baste) ••

$_

) (Capital losses are

Von

i

illon

Sa!oa or

r^iolr'o™

-able only t

Exchanges (

JiliFurnish dela.ls)

D the extent of

8. 0*1

|!2,000

1

pluses

is;rL

. . . .

ction S

COUNT

100

80

gains)._

— —

,0. O^ontos

8. Gains

.$

s

«™NTE T A ™

b. Losses

S

$

*In reporting sales en eichangas of capita] assets attach separate schedule. If neoes&iry, for transactions coming w]

^Coat of property must be eatored in Coluiaa 6 if a losa is cUlmed in Column 8.gas of capitantered la C

k a h l d ' bfltato (Ij how propOTty was aoquirea

Colnmis 10 above.

pontoYfibTe di video ds,

—

(o) Obligations of a State, Territory, or political mibdmsiou thereol,or tho District of Columbia cr United States possessions

(&) Obligations isaued under Federal Fann Loan Act, or under such

(c) Liberty Z}{ % Bonda and other obligations of United Statea issued

(d) Treasury Notes, Treasury Bills, and Treasury Certificates ofIndebtedness

(e) Liberty 4% and i%% Bonds; U. S. Savings Bonds; Treasury Bonds.(/) Obligations of instrumentalities of the United States (other than

obligations to be" reported in (6) above) .

$

3. IHTXSEST RlCDTID

$

S^o'iSr

All

All

All

All

$5,000

None

(l) TOTAL (enter total of column 6 as Item 9)

xxxxxx

$

X X

9)

xxxxxx

$

S.

SCHEDULE E—INCOME FROM DIVIDENDS

Itemize all dividends received during the year, stating amounts and names and addresses of corporations declaring the dividenc

SCHEDULE F—EXPLANATION OF DEDUCTIONS CLAIMED IN ITEMS 1, 13, 14, 16, 17, AND 18, AND CREDIT CLAIMED IN ITEM 23

Of buildings, state materialof which constructed)

EXPLANATION OF DEDUCTION FOR DEPRECIATION CLAIMED IN SCHEDULES A AND

2. D A T E3. COST OE MARCH 1,1913,

PRIOR TO THAT D A T E

$

4. A8SET3 FlOLTDEPRECIATED IN U3S

AT E N D or Y K A B

$

5. DirSTCIATIOKALLOWED (OR ALLOW-

ABLE) IN PRIOR Y E A E S

$

«. REMAININO COSTo s OTHER BASIS TO

$

7. LITE U S E D

B

w 9. DEPRECIATION

$

EXPLANATION OF DEDUCTION FOR LOSSES BY FIRE. STORM, ETC., CLAIMED IN SCHEDULE A AND IN ITEM 15

. . ^ O E P B O P E R T , ,DATEAC Q D IRE D 3.COST

s

4. STJBSEQBEUT

s „

5. DEPRECIATION

$

6siLVAOENvlLUKD

$

7. DEDUCTIBLE LOSS

$

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

1935

148 STATISTICS OF INCOME

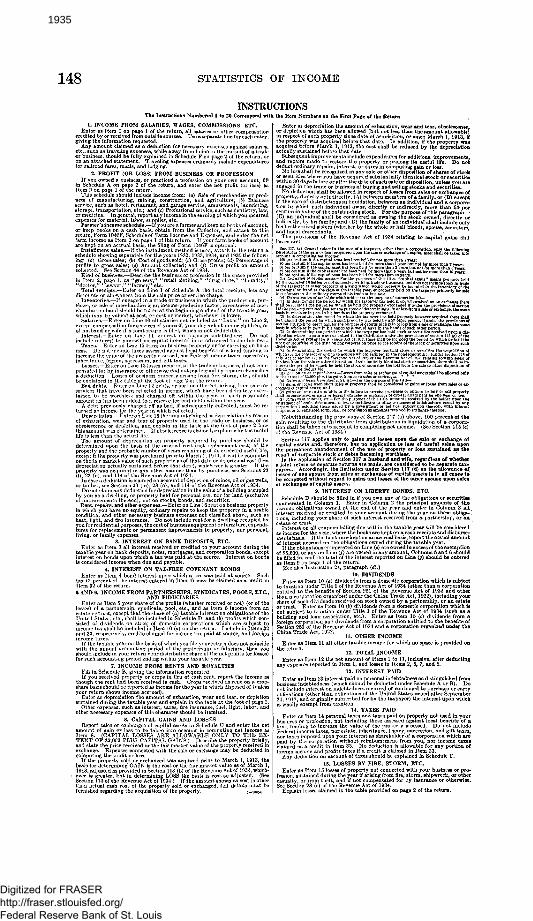

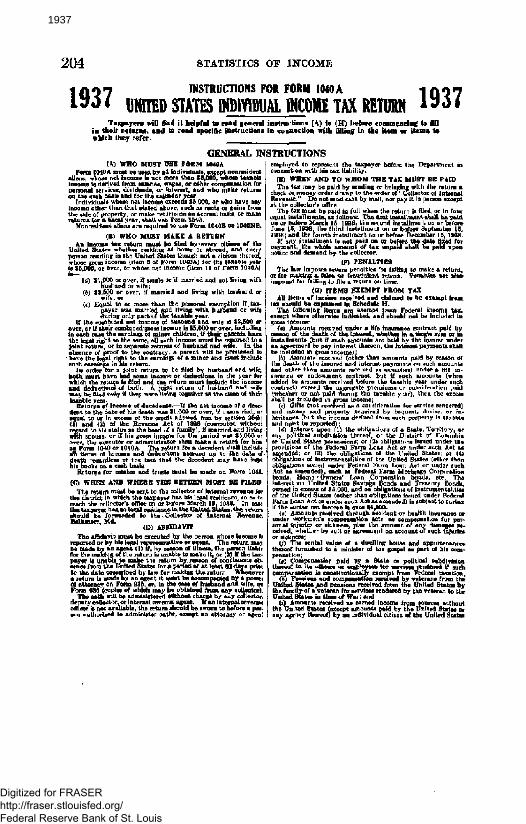

INSTRUCTIONSThe Instructions Numbered 1 to 20 Correspond with the Item Numbers on the First Page of the Return

ri other coseparate line for

I. INCOME FROM SALARIES, WAGES, COMMISSIONS, ETC.Enter as Item 1 on page 1 of the return, all salari

credited by or received from outside source Ugiving the information requested.

Any amount claimed as a deduction for necessary expenses against salaries,etc., such as traveling expenses, while away from home in the pursuit of ft tradeor business, should be fully explained in Schedule F on page 2 of the return, oron an attached statement. Traveling expenses ordinarily include expendituresfor railroad fares, meals, and lodging.

2. PROFIT (OR LOSS) FROM BUSINESS OR PROFESSIONd bIf you owne

n Schedule AItem 2

This

A on page 2- ,_age 1 of the r«hedule should in. me from: (a) Sale of merchandise or prod-

cts ui uuuiumtuinug, mining, construction, and agriculture; (6) Businessservice, such as hotel, restaurant, and garage service, amusements, laundering,storage, transportation, etc.; and (c) Professional service, such as dentistry, law,or medicine. In general, report any income in the earning of which you incurredexpenses for material, labor, supplies, etc.

Farmer's income schedule.—-If you are a farmer and keep no books of account,or keep books on a cash basis, obtain from the Collector, and attach to thisreturn, Form 1040F, Schedule of Farm Income and Expenses, and enter the netfarm income as Item 2 on page 1 of this return. If your farm books of account

instailmen^sales.—If the'installment method is used" attacMo the return aschedule showing Eeparatelv for the years 1932, 1933, 1934, and 1935 the follow-ng: (a) Gross sales; (6) Cost of goods sold; (c) Gross profits; (d) Percentage of

fit t l ( ) A n t l l t d d (/) G fit tR

s; (d) Pers profit o

Item 2, pagdoctor," "laT t l i

profits to gross sales; (e) Amount collected; and (f)collected. See Section 44 of the Revenue Act of 1934.

ind of buswess.—-Describe the business or profession in the space provided"grocery," "retail clothing," "drug store," "laundry,"

•eTpts.—Eiiter on t ine 1 of Schedule A the total receipts, less anydiscounts or allowances from the sale price or service charge.

Inventories.—If engaged in a trade or business in which the production, pur-chase, or sale of merchandise is an income-producing factor, inventories of mer-chandise on hand should bo taken a t the beginning and end of the taxable year,which may be valued a t cost, or cost or market, whichever is lower.

Salaries.—Enter on Line 10 all salaries not included as "Labo r " on Line 2,except compensation for services of yourself, your dependent minor children, orof husband or wife if a joint return is filed, which is not deductible.

Interest.—Enter o n ' l i n e 11 interest on business indebtedness. Do notinclude interest to yourself on capital invested in or advanced to the business.

Taxes.—Enter on Line 12 taxes on business property or for carrying on busi-ness. Do not include taxes assessed against local benefits of a kind tending toincrease the value of the property assessed, nor Federal income taxes, nor estate,inheritance, legacy, succession, and gift taxes.

Losses.—Enter on Line 13 losses incurred in the trade or business, if not com-pensated for by insurance or otherwise and not made good by repairs claimed asa deduction. Losses of business property arising from fire, storm, etc., shouldbe explained in the table at the foot of page 2 of the return.

Bad debts.—Enter on Line 14 debts, or portions thereof, arising from sales orservices that have been reflected iu income, which have been definitely ascer-tained to be worthies.-1, and charged oft' within the year, or such reasonableamount as has been added to a reserve for bad debts within the year.

A debt previously charged off as bad, if subsequently collected, must be re-turned as income for the year in which collected.

Depreciation.—Enter on Line 15 the amount claimed as depreciation by reasonof exhaustion, wear and tear of property used in the trade or business, or asobsolescence or depletion, and explain in the table at the foot of page 2 howthis amount v.as determined. If obsolescence is claimed, explain why the usefullife is less than the actual life.

The amount of depreciation on property acquired by purchase should bedetermined upon the'basis of the original cost (not replacement cost) of theproperty and the probable number of years remaining of its expected useful life,except it the property was purchased prior to March 1, 1913, it will be computedon the fair market value of such property as of that date or its original cost (lessdepreciation actually sustained before that date), whichever is greater. If theproperty was acquired in any other manner than by purchase, see Sections 23(1), 23 (n), and 114 of the Revenue Act of 1934.

In case a deduction is claimed on account of depletion of mines, oil or gas wells,or timber, see Sections 23 (m), 23 (n), and 114 of the Revenue Act of 1934.

Do not claim any deduction for depreciation in the value of a building occupiedby you as a dwelling, or property held for personal use, nor for land (exclusiveof improvements thereon), nor on stocks, bonds, and securities.

Rent, repairs, and other expenses.—Enter on Line 16 rent on business property* which you have no equity, ordinary repairs to keep the propei ' * " ' '*

ped byexpendi-ersonal

heat, light, and fire .you for residential purposes, the cost of business equipment or f uraitures for replacements or permanent improvements to property, nor personal,living, or family expenses.

3. INTEREST ON BANK DEPOSITS, ETC.Enter as Item 3 all interest received or credited to your account during the

taxable year on bank deposits, notes, mortgages, and corporation bonds, exceptinterest on bonds upon which a tax was paid a t tho source. Interest on bondsis considered income when due and payable.

4. INTEREST ON TAX-FREE COVENANT BONDSis Item 4 bond interest upon which a tax was paid a t source. Such

ent of the interest entered in Item 4) may be claimed as a credit intax (2 percentItem 32 of the retur5 AND G. INCOME FROM PARTNERSHIPS, SYNDICATES, POOLS, ETC.,

AND FIDUCIARIESEnter as Item 5 your share of the profits (whether received or not) (or of the

losses) of a partnership, syndicate, pool, etc., and as Item 6 income from anestate or trust, except that the share of (a) taxable interest on obligations of theUnited States, etc., shall be included in Schedule D, and (6) profits which con-sisted of dividends on stock of domestic corporations which are subject toincome tax shall be included in Item 10 (a) on the return. Include in Items 32and 33, respectively, credits claimed for income tax paid a t source, and foreign

If the taxable year on the basis of which you file your return does not coincidewith the annual accounting period of the partnership or fiduciary, then youshould include in your return your distributive share of the net profits (or losses)for such accounting period ending within your taxable year.

7. INCOME FROM RENTS AND ROYALTIESFill in Schedule B, giving the information requested.If you received property or crop3 in lieu of cash rent, report the income as

though the rent had been received in cash. Crops received as rent on a crop-share basis should be reported as income for the year in which disposed of (unlessyour return shows income accrued).

Enter as depreciation the amount of exhaustion, wear and tear, or depletionsustained during the taxable year and explain in the table at the foot of page 2.

Other expenses, such as interest, taxes, fire insurance, fuel, light, labor, andother necessary expenses of this character should be itemized.

8. CAPITAL GAINS AND LOSSESReport sales or exchanges of capital assets in Schedule C and enter the net

Item 8. (CAPITAL LOSSES* A R E " ALLOWABLE ONLY TO T H E EX-T E N T OP $2,000 PLUS CAPITAL GAINS.) Describe the property briefly,and state the price received or the fair market value of the property received inexchange. Expenses connected with the sale or exchange may be deducted incomputing the profit or loss.

If the property sold or exchanged was acquired prior to March 1, 1913, thebasis for determining GAIN is the cost or the fair market value as of March 1,1913, adjusted as provided in Section 113 (b) of the Revenue Act of 1934, which-

• ever is greater, but in determining LOSS the basis is cost so adjusted. (SeeSection 113 of the Revenue Act of 1934.) If the amount shown as cost is otherthen actual cash cost of the property sold or exchanged, full details must befurnished regarding the acquisition of the property. 2—IOSM

Enter as depreciation the amount of exhaustion, wear and tear, obsolescense,or depletion which has been allowed (but not less than the amount allowable)in respect of such property since date of acquisition, or since March 1, 1913, ifthe property was acquired before that date. In addition, if the property wasacquired before March 1, 1913, the cost shall be reduced by the depreciationactually sustained before that date.

Subsequent improvements include expenditures for additions, improvements,and repairs made to restore the property or prolong its useful life. Do notdeduct ordinary repairs, interest, or taxes in computing gain or loss.

No loss shall be recognized in any sale or other disposition of shares of stockor securities where you have acquired substantially identical stock or securitieswithin 30 days before or after the date of such sale or disposition, unless you areengaged in the irade or business of buying and selling stocks and securities.

No deduction shall be allowed in respect of losses from sales or exchanges ofproperty, directly or indirectly, (A) between members of a family, or (B) exceptin the ca;:e of distributions in liquidation, between an individual and a corpora-tion in which euch individual owns, directly or indirectly, more than 50 percentum in value of the outstanding stock. For the purpose of this paragraph—(C) an individual shall be considered as owning the stock owned, directly orindirectly, by his family; and (D) the family of an individual shall include onlyhis brothers and sisters (whether by the whole or half blood), spouse, ancestors,

to

nd linTh

aal des

sistendant

The provisions of the Revenue Act of 1934 relating to capital gains a'

ruU.—Xn the case of a taxpayer, other than a corporation, only the followingor loss recocnized upon the sale or exchange of a capital asset shall bo taken intS

ir bat not for more than 2 years;t bes been held

(bp^niion ofnpuiVa] ses of this title, "capital assets" means pris trade or business), but does not Include sta r"""propeny"held by^the t ' l

^BEBvMf^iitho provisions of section

(2) I n d e t e r m i c i ^ t h ,CHJ Inclucieu the period fo. •• ^.^^ u-— j--..-,-^.-.j •• ^ .section 113, such property has^ for the purpose of deter

(3) In determining t: * ** l "nds as it would havor which the taxpay

ichanped.

• has held property however acquired there shalld by any other person, If under tbe provisions ofioing gain or ioss from a sale or exchange, thesamoin tho hands of such other person. k

• has held stoca or securities received upon a dis*

i tract or option quire which) resulted in the nondeductib

us to buy or sell property

>r tho purposes of this title, amounts roceived by the holder upon tDotes, or certificates or othn evidences of Indebtedness issued by a

of Section 117 (a) above, 100 percent of theom distributions in liquidation of a corpora-computing net income. (See Section 115 (c)

Notwithstanding the provisi.gain resulting to the distributetion shall be taken into accountof the Revenue Act of 1934.)

Section 117 applies only to gains and losses upon the sale or exchange ofcapital assets and, therefore, his no application t» loss of useful v&lne uponthe permanent abandonment of the use of property or loss sustained as theresult of corporate stock or debts becoming worthless.

In the application of Section 117 a husband and wife, regardless of whethera joint return or separate returns are made, are considered to be separate tax-payers. Accordingly, the limitation under Section 117 (d) on the allowance oftosses of one spouse from sales or exchanges of capital assets is in all cases to'be computed without regard to gains and losses of the other spouse upon salesor exchanges of capita) assets.

9. INTEREST ON LIBERTY BONDS, ETC.Schedule D should be filled in if you own any of the obligations or securities

enumerated in Column 1. Enter in Column 2 the principal amounts of the-various obligations owned at the end of the year and enter in Column 3 allinterest received or credited to your account during the year on these obliga-.'tions, including your share of such interest received from a partnership, or an '

Interest on all coupons falling due within the taxable year will be consideredas income for t&e year, where the books are kept on a cash receipts P-nd disburse-ments basis. If the books are kept on an accrual basis, report the actual amountof interest accrued on the obligations owned during the taxable year.

If the obligations enumerated on Line (e) are owned in excess of the exemption,f $5,000, or any on Line (f) are owned in any amount. Columns 5 and 6 shouldn any amount, Columns 5 and 6 should

reported on. Line (j) should be enteredof $5,000, or anj „, ..be filled in, and the total of the iras Item 9 on page 1 of the return.

(See also Instruction 24, paragraph (d).)

10. DIVIDENDSEnter as Item 10 (a) dividends from a domestic corporation 'which is subject

to taxation under Title I of the Revenue Act of 1934 (other than a corporationentitled to the benefits of Section 251 of the Revenue Act of 1934 and otherthan a corporation organized under the China Trade Act, 1922), including yourshare of such dividends received on stock owned by a partnership, or an estateor trust. Enter as Item 10 (6) dividends from a domestic corporation which ianot subject to taxation under Title I of the Revenue Act of 1934 (such as abuilding and loan association, etc.). Enter as Item 10 (c) dividends from aforeign corporation and dividends from a corporation entitled to the benefits ofSection 251 of the Revenue Act of 1934 and a corporation organized under theChina Trade Act, 1922.

s Item 11 all ( Jch no space is provided onEnter ithe return. ^ T Q T A L J N C O M E

Enter as Item 12 the net amount of Items 1 to 11, inclusive, after deductingany expenses reported in Item 1, and losses in Items 2, 5, 7, and 8.

13. INTEREST PAID

Enter as Item 13 interestbusiness indebtedness (which should be deducted under Schedule A or B). Donot include interest on indebtedness incurred or continued to purchase or carryobligations (ether than obligations of the United States issued after September24, 19!7, and originally subscribed for by the taxpayer) the interest upon whichis wholly exempt from taxation.

U. TAXES PAIDEnter as I tem 14 personal taxes and taxes paid on property not used in your

business or profession, not including those assessed against local benefits of akind tending to increase the value of the property assessed. Do not includeFederal income taxes, nor estate, inheritance, legacy, succession, and gift taxes,nor taxes imposed upon your interest as shareholder of a corporation which arepaid by the corporation without reimbursement from you, nor income taxesclaimed as a credit in Item 33. No deduction is allowable for any portion offoreign income and profits taxes if a credit is claimed in Item 33.

Any deduction on account of taxes should be explained in Schedule F .

15. LOSSES BY FIRE, STORM, ETC.Enter as Item 15 losses of property not connected with your business or pro-

fession, sustained during the year if arising from fire, storm, shipwreck, or othercasualty, or from theft, and if not compensated for by insurance or otherwise.See Section 23 (e) of the Revenue Act of 1934.

Explain losses claimed in the table provided on page 2 of the return.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

1935

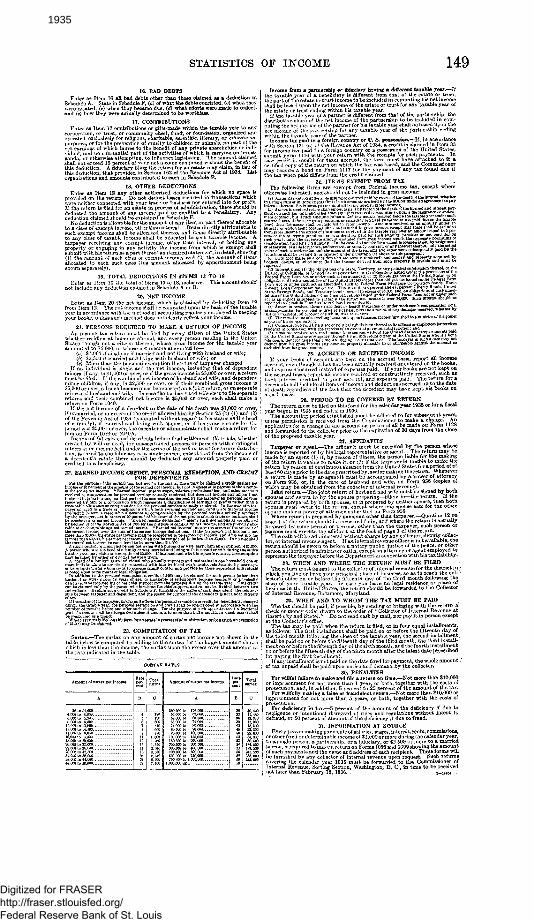

STATISTICS OF INCOME 14916. BAD DEBTS

Enter as Item 16 all bad debts- other than those okimed as a deduction inSchedule A. State in Schedule F, (a) of what the debts concisted, (6) when theywere created, (c) when they became due, (d) what effort* were made to collect,and 0) bow they were actually determined to ba worthless.

17. CONTRIBUTIONSEnter aa Item 17 contributions or gifts made within the taxable year to any

corporation, or trust, or community chest, fund; or foundation, organized andoperated exclusively for religious, charitable, scientific, literary, or educational

- ' - "- -' - - - - - '-children or animals, no part of theif any private shareholder or indi-

:>f which is carrying on propa-, - __„, ^r.lation. The amount claimed

shall not exceed 15 percent of your net income computed without the benefit ofthis deduction. A fiduciary filing ths return for an esUte may claim, in lieu ofthis deduction, that provided in Section 162 of the Revenue Act of 1934- Listorganizations and amounts contributed to each in Schedule F.

18. OTHER DEDUCTIONSEnter aa Item 18 any other authorized deductions for which no space is

provided on the return. Do not deduct losses incurred in transactions whichwere neither connected with your tr*da or busineffl nor entered into for profit.If the return is filed for an estate in process of administration, there should bededucted tho amount of any incoma paid or credited to a beneficiary. Anydeduction claimed should be explained in Schedule F.

No deduction i3 allowable for the amount of any item or part thereof allocableto a class of exempt income, other than interest. Itcm3 directly attributable tosuch exempt income shaU be allocated thereio. and items directly attributableto any class of taxable income shall be allocated to such taxable income. Ataxpayer receiving any exempt income, other than interest, or holding anyproperty or engaging in any activity the income from which ia exempt shallsubmit with his return as a part thereof an itemized statement, ia detail, showing(1) the nmount of each class of exempt income, and (2) the amount of itemsallocated to each such class (th« amount allocated by apportionment beingshown separately).

IS. TOTAL DEDUCTIONS IN ITEMS 13 TO 18Enter as Item 19 the total of Items 13 to IS, inclusive. This amount should

not include any deduction claimed in Schedule A or B.20. NET INCOfttE

m Itr in

b

Anht

"books, unless such method does not clearly reflecl

21. PERSONS REQUIRED TO MAKE A RETURN OF INCOMEin income tax return must be filed by every citizen of the TTnited States;ther residing at home or abroad, and every person residing in the United

crates though not a citizen thereof, whose e,Tcsa income for tho taxable yearamounted to $5,000, or whose net income amounted to—

(a) $1,000 if Eing!o or if married and not living with husband or wife;(bS $2,500 if married and living with husband or wife; or(c) More than the personal exemption if status of taxpayer changed.

If an individual is single and the net income, including that of dependentminors, if any, is SI ,000 or over, or if the gross income is 85,000 or over, a returnmust be filed. If the combined net income of husband and wife,- and dependentminor children, if any,_ is $2,500 or over, or if their_combined gross income isS5fCX)0 or over, s,ll such income must t)c reported on & "*oinfc return, or on scpttrst-creturns of husband and wife. In case the husband *.nd wife elect, to file separatereturns and theb combined net income is $5,(XX) cr over, each shall make a

If'the net income of a decedent to the date of his death was $1,000 or over,if unmarried, or in excels of the credit allowed him by Section 25 (b) (1) and (3)of the Revenue Act of 1934 (computed without regard to his status aa the headof s family), jf raf,rricd and living with epeuse, or if his gross.income for theperiod WHS $3,000 or over, the executor or administrator shall make a return for

Income of (a) estates of decedents before final settlement, (&) trusts, whethercreated by will or deed, for unascertained persons or persons with contingentinterests; or income held under the terms of the will or trust for future distribu-tion, is taxed to the fiduciary as a single person, except that from the income ofa deec-dent's estate there should be deducted any amount properly paid orcredited to a beneficiary.

22. EARNED INCOME CKEDIT, PERSONAL EXEMPTION, AND CREDITFOR DEPENDENTS

i© normal tax, but not for the surtax, there may be claimed a crodit &ffa!nst net

„ . ^ _ r salaries, professional fooa, and other Raouut^

or that part ol the compensation derived by the taij«yer for personal services

mpinafttop for theftj?reouai " " ° Dt l ° . - e a r n ° 5 S °-r ^ •• r a t - 1 W .

included in great income,nn er,.,_ jy.. m to t w

by thetai-ri

™^, , „ .... r JU SWTICOS actually rendered

by Section 23 ofche Revenue Act of 193* for tho purpose of computing net income, r.nd ftra properly allo-cable to or chBn;9able against earned Income. " Earned net Incoma mean? tha excess of the amount ofthe earned income over the sura of thd earned income deductions. If the taxpayer's net income ia not

, idlSh^f ,__ __„, r..__may be taken by either or dlvidod between tham. . . . .

A head of a family is an individual wao actually supports and nmiotains in ono household ono or

In addition to tho personal exemption, a credit of $400 may be claimed for each person (othor thanhusband or wife) under 18 years of ags, or inc&pabte of self-support because mentally or physically

ship batwoen taxpayer and dependent, and the reason for support if ttia depended ia not under 18 yearsof a«e.

If ths status of the taxpayer, insofar as it affects the personal exemption or cradi t for dependents, chacgodduring the taxable year, the personal exemption and credit shall bo apportioned in accordance with theDumber of months before and after such change. For the purpese of such apportionment a fractional

Whero a return h filed on this form for an estate in process of administration, or tor a trust, an exemption

23. COMPUTATION OF TAXSurtax.—The surtax on any amount of surtax net income not shown in the

table below ia computed by adding to the surtax for the largest amount shown

the rate indicated in the table.

A

8 &» to 20 000A) 06j to "2 1X0

B o

780

A

510 000 to 300 00T300009to «0C0n

1 000,000 up -

T

36

45

1

c

2S.00I2S oa

Income from a partnership or fiduciary hsrin* a different taxable year.—Uthe taxable year of a beneficiary is different from that of the estate or trust,the part of the estate or trust income to be included in computing his net incomeshall be baaed upon the net incomeof the estate or trust for any taxable year ofthe e3tate or trust ending within his taxable year.

If the taxable year of a partner ia different from that of the partnership, thedistributive share of the net income of the partnership to ba included in com-puting the net, income of the partner for his taxable year shall be based upon thenet income of the partrershlp for any taxable year of the partnership endingwithin the taxable year of the partner.

Income ttx paid to a foreign country or U. S. possession.—If, Ia accordancewith Section 131 (a) of the Revenue Act of 1934, a credit is claimed in Item 33for income tax paid to a foreign country or a possession of the United States,submit Form 1113 with your return with the receipts for such payments. Incase credit is sought for taxes accrued, the form must have attached to i t acertified copy of the return on which the tax was based, and the Commissionermay require a bond on Form 1117 for the payment of any tax found due iftho tax when paid differs from the credit claimed.

24. ITEMS EXEMPT FROM TAXThe following items are exempt from Federal income tax, except where

otherwise indicated, and should not be included in gross income:Aironnts raeo! vod under a life Insurant* contract raid by reason of the death of the labored, whether

ts pai'dly of the Inason ? m ! e death of t e s

T l d ' f h t h e r or not p

interest Day-

Mn?o'^e^^RaU)dpremfum3'cracoSlder r8tkin paid far such annuity (whether or not paid duringsuch y « / ) , until the aggregate amount excluded from gross income equals ths fijsresate premiums or

ams^t%^^M'aroi^iere.t^a'lac\wyliMt^n^9d) and°morieyPM<fproperty acquired by«t' doirisa, or inharitrace (but tho income derived from such propsrty Is taxable and must be

District of Columbia, or United Stiitaa possessions, or

Stated SavinM Bonds and Treasury t>ond^ owned in excess of $5,090, ani of tho'United Gtatas (otber than obligations ' >•—•-- "-•>—

r0"(£' Anouuts raoefvwiYhrowli ace'

is corapensatior. fcr porxraal injuries

U(J)°Th9 ren

Ut™-s'ElSe

a<jra dwelling t

^interest should be

lil-ance or under vcrortanen's compensatloD acts,

3e amount ot a n j damaees rooelved, whether by

fices thereof furnished to a minister of the goepel

icn thereof to its officers or employees for services

by tha Un:'"ed S'ites or any agency thereof) by aa individual ciUien of the United Stated who is a bonafide noni-oa'ident for more liisn e moi'ths during iLe t&iable year. Tbe tftipayer in such a case may notdeduct from his gross inooms any amount piopoiiy allocable to or cbargeablo against the amount 30

25. ACCRUED OR RECEIVED INCOMEIf your books of account are kept on the accrual basis, report all income

accrued, even though it has not been actually received or entered oa the books,and expenses incurred instead of expenses paid. If your books are not kept onthe accrual basis, report all income received or constructively received, such asbank interest credited to your account, and expenses paid. The return for adecedent rhall include all iterua of inoomo and deductions accrued up to the dateof death regardless of the fact that the decedent may have kept hi3 books on

26. PERIOD TO BE COVERED BY BETCKNThe return must be filed on this form for the calendar year 1935 or for a fiscal

year begue in 1935 and ended ia 1936.The accounting period established must be adhered to for subsequsnt years,

unless permission ia received from tho Commissioner to make a change. Anapplication for a change in tha accounting period shall be made on Form 1128and forwarded to the collector prior to the expiration of 30 days from the closeof the proposed taxable year.

27. AFFIDAVITSTaxpayer or agent—The affidavit must be executed by the person whose

income is reported or bv hia legal representative or agent. The return maybemade bv an agent (1) if, by reason of illness, the person liable for the makingof tha return is unable to make it, or (2) if the taxpayor is unable to make thereturn by reason of continuous absence from the United States for a period of atleast 00 days prior to tho date prescribed by Jaw for making tha return. Whenevera return is made by an agent it must bo accompanied by a power of attorneyon Form 935, or, in the cane of husband and wife, on Form 936 (copies ofwhich may be obtained from tha collector of internal revenue).

Joint retmiu—The joint return of husband and wife must be signed by bothspouse3 and sworn to by the spouse preparing—filling in—the return. If thereturn ia prepared by both spouses, or is prepared by neither spouse *"»<•" K"*h

si l ted oer.—Questi

tha otherepouso linder a power of attoi - _ -- -

Where return is prepared b7 someone other than taapay— .»page 1 of the return should ba answered fully, and where the return ia actuallyprepared by eome person or persona, other than tha taxpayer, such person ornsrsonfi must execute the affidavit at tha foot of page 1 of the return.

iU be administered without charge by any collector, deputy collec-Thtor, o

t

eed went. If ab f

grnal r

binternal revenue agent.

return should be sworn to before a notary public, justice of the peace, or otherperson authorised to administer oaths, except an attorney or agent employed torepresent the taxpayer before the Department in connection with his tax liability. .

28. WHEN AND WHERE THE RETURN MUST BE FILEDThe return must be sent to the collector of internal revenue for the district in •

which you live or have your principal place of business, so as to reach the col- •lector's ofSca on or before tho fifteenth day of the third month following theclose of your taxable year. In case vou have no legal residence or place ofbusiness in the United States, the return should be forwarded to the Collectorof Internal Revenue, Baltimore, Maryland.

20. WHEN AND TO WHOM THE TAX MUST BE PAIDThe tax should be paid, if possible, by sending or bringing with the return a

check or money order drawn to the order of "Collector of Internal Revenue at(insert city and State)." Do not send cash by mail, nor pay it in person exceptat the Collector's office.

The tax may be paid when the return is filed, or in four equal installments,as follows: Ths first installment shall be paid on or before the fifteenth day ofthe third month following the close of the taxable year, the second installment,shall be paid on or before the fifteenth day of the third month, the third install-ment on or before the fifteenth day of the sixth month, and the fourth installmenton or before the fifteenth day of the ninth month after the latest date prescribedfor paying the first installment.

If any installment is not paid on tho date fixed for payment, the whole amount .of tax unpaid shall be paid upon notice and demand by the collector.

30. PENALTIESFor willful failtire to make and file a return on time.—Not more than $10,000

or imprisonment for not more than 1 year, or both, together with the costs ofprosecution, and, in addition, 5 percent to 25 percent of the amount of the tax.

For wiUfully making a false or fraudulent return.—Not more than $10,000 orimprisonment for not more than 5 years, or both, together with the costs of.

For deficiency in tax.—5 percent of the amount of the deficiency if due tonegligence or intentional disregard of rules and regulations without intent todefraud, or 50 percent of amount of the deficiency if due to fraud.

31. INFORMATION AT SOURCEEvery person making payments of salaries, wages, interest, rents, commissions,

or other fixed or determinable income of $ 1,000 or more during the calendar year,to a single person, a partnership, or a fiduciary, or $2 500 or more to a marriedperson, is required to make a return on Forms 1096 and 1099 showing the amountof such payments and the name and address of each recipient. These forms willbe furnished by any collector of internal revenue upon request. Such returnscovering the calendar year 1935 must be forwarded to the Commissioner ofInternal Revenue, Sorting Section, Washington, D. C , in time to be receivednot later than February 15, 1936. . i-ieon *

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

1935

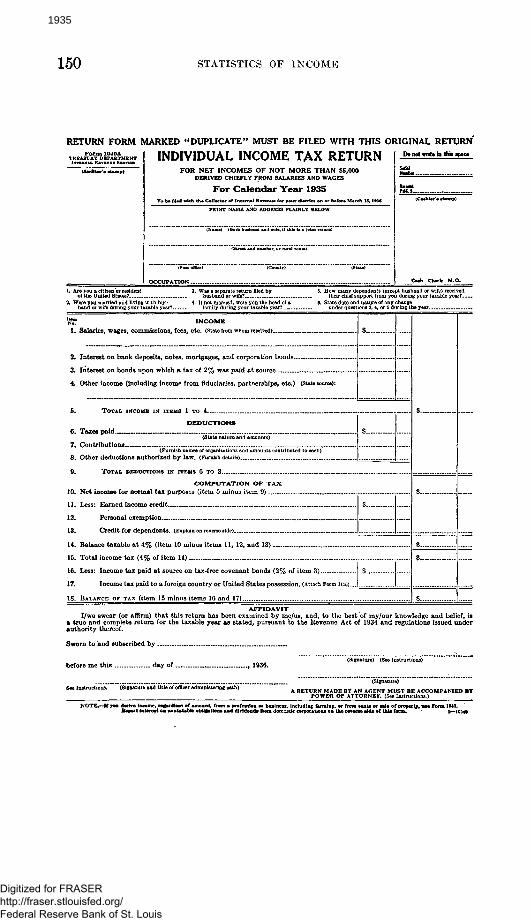

150 STATISTICS OF INCOME

RETURN FORM MARKED "DUPLICATE" MUST BE FILED WITH THIS ORIGINAL RETURNF o r m 1040A

TREASURY DEPARTMENT

OUdltor'. .ump)

INDIVIDUAL INCOME TAX RETURNFOR NET INCOMES OF NOT MORE THAN $5,000

DERIVED CHIEFLY FROM SALARIES AND WAGES

For Calendar Year 1935To be filed with t h . Collator of Internal Rrnnua for your dUtrict on or bo for. March 15,1938

PRINT NAME AND ADDRESS PLAINLY BELOW

(N«w) (Both "hu»b»nd end wife, it thL" U • joint return)

Otraet and number, or rural route)

(Post offioe) (County) (State)

OCCUPATION

Do not write in this space

SSLft*

(Cashier's .tamp)

Cadi Check M.O.

1. Are you a citizen or resident 3. Was a separate return filed byof the United States? husband or wife?

2. Were you married and living with hus- 4. If not married, were you the head of aband or wife during your taxable year? family during your taxable year?

5. How many dependents (except husband or wife) receivedtheir chief support from you during your taxable year? . . .

8. State date and nature of any changeunder questions 2, 4, or 5 during the year

'N£ INCOME1. Salaries, wages, commissions, fees, etc. (State from whom received)

2. Interest on bank deposits, notes, mortgages, and corporation bonds

3. Interest on bonds upon which a tax of 2% was paid at 6ourcc

4. Other income (including income from fiduciaries, partnerships, etc.) (State source):

$ .

5. TOTAL INCOME IN ITEMS 1 TO 4 -

DEDUCTIONS6 Taxes paid

(State nature and amounts)7 Contributions (Furnish names of organizations and amounts contributed to each)8. Other deductions authorized by law. (Furnish details)

9. TOTAL DEDUCTIONS IN ITEMS 6 TO 8

COMPUTATION OF TAX

10. Net income for normal tax purposes (item 5 minus item 0)

11. Less: Earned income credit

12 Personal exemption

1 3 . C r e d i t f o r d e p e n d e n t s . ( E x p l a i n o n r e v e r s e s i d e ) . . . . . .

$

$

14. Balance taxable at 4% (item 10 minus items 11, 12, and 13)

15. Total income tax (4% of item 14)

16. Less: Income tax paid at source on tax-free covenant bonds (2% of item 3)

17. Income tax paid to a foreign country or United Statea possession. (Attach Form me)

18. BALANCE or TAX (item 15 minus items 16 and 17)

$

$

S

$

$

$.....AFFIDAVIT

I/we swear (or affirm) that this return has been examined by me/us, and, to the best of my/our knowledge and belief, isa truo and complete return for the taxable year S3 8tated, pursuant to the Revenue Act of 1934 and regulations issued underauthority thereof.

Sworn to and subscribed by

beforo me this day of , 1936.(Signature) (See Instructions)

fioe Instructions. (Signature and title of officer administering oath)

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

1935

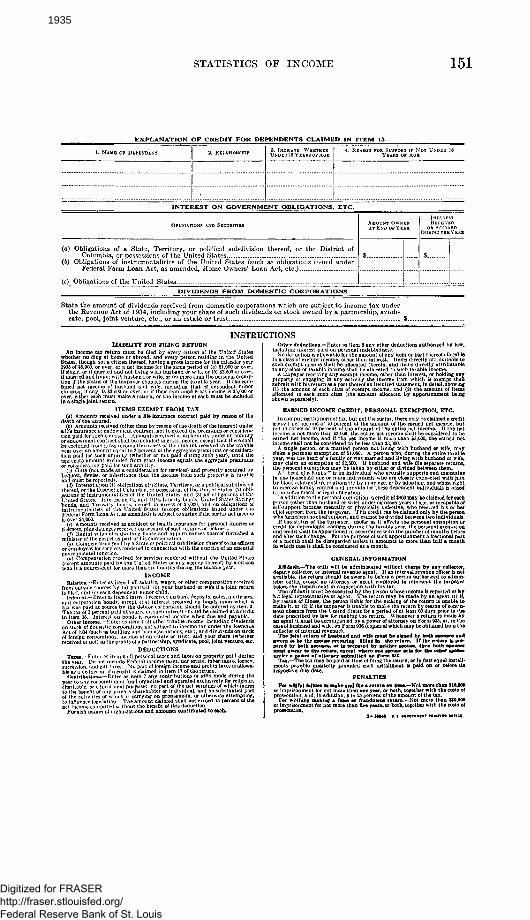

STATISTICS OF INCOME 151

EXPLANATION OF CREDIT FOR DEPENDENTS CLAIMED IN ITEM 13

1. NAME OF DEPENDENT

I N T E R E S T O N G O V E R N M E N T O B L I G A T I O N S . E T C .

(a) Obligations of a State, Territory, or politicnl subdivision thereof, or the District ofColumbia, or possessions of the United States

(b) Obligations of instrumentalities of the United States (such as obligations issued underFederal Farm Loan Act, as amended, Home Owners' Loan Act, etc.) .

(c) Obligations of the United States . .

AMOUNT OWNEDAT END OF YEAR

$

DBMNO'TUEYE.VB

$

DIVIDENDS FROM DOMESTIC CORPORATIONS

State the amount of dividends received from domestic corporations which are subject to income tax underthe Revenue Act of 1934, including your share of such dividends on stock owned by a partnership, syndi-cate, pool, joint venture, etc., or an estate or trust $..

INSTRUCTIONSLIABILITY FOR HUNG RETURN

An income tax Returnwhether residing at homiStates, though not a citizi1935 of $5,000, or over, orif single, or if married and not living

irried and living with husband

ust be filed byir abroad, and (thereof, having

ery citizen of the United States•y person residing in the United

g a gross income for the calendar yearthe same period of (a) $1,000 or over,

_ husband or wifo, or (6) $2,500 or over,ife, or (c) more than the personal exemp-

tion if the status of tho taxpayer changes during the taxable year. If the ©bined net income of husband and wife, including that of dependent miuurchildren, if any, is $2,500 or over, or if their combined gross income is $5,000 orover, either each must make a return, or the income of each must be includedin a single joint return.

ITEMS EXEMPT FROM TAX(a) Amounts received under a life insurance contract paid by reason of tha

death of the insured.(6) Amounts received (other than by reason of the death of the insured) uuder

.& life insurance or endowment contract, not to exceed the premiums or considera-tion paid for such contract. Amounts received as an annuity under an annuityor endowment contract shall be included in gross income; except that there shallbe excluded frois gross income the excess of tho amount received in the taxableyear ovor an amount equal to 3 percent of the aggregate premiums or considera-tion paid for such annuity (whether or not paid during such year), until thoaggregate amount excluded from gross income equals the aggregate premiumsor consideration paid for such annuity.

(c) Gifts (not made as a consideration for services) and property acquired bybequest, devise, or inheritance (but the income from such properly is taxableand must be reported).

(d) Interest upon (1) obligations of a State, Territory, or a political subdivisionthereof, or the District of Columbia, or possessions of the United States; (2) obli-gations of IUnited StaStates e % and 4)4bonds, and Treasury bonds, owned iinstrumentalities of the United StatFederal Farm Loan A< t, as amended) i

(e) Amounts received as accident orsickness, plus damages received on acco

(J) Rental value of a dwelling housminister of the gospel as part of his co

ental value ominister of the gospel p

(?) Compensation paid byor employees for services rend

gf hisS

, -j of $5,000, and o „! (except obligations issued under thosubject to surtax if the surtax net income

health insurance for personal injuries orint of such injuries or sickness.and appurtenances thereof furnished a

(ft) Compensation received for services rendered without the United Slates(except amounts paid by the United States or any agency thereof) by a citizenwho is a nonresident for more than six months during the taxable year.

INCOME

Salaries.—Enter as item 1 all salaries, wages, or other compensation receivedfrom outside sources by (a) yourself, (6) your husband or wife if a joint returnis filed, and (r) each dependent minor child.

Interest.—Knter as item 2 interest received on bank deposits, notes, mortgages,and corporation bonds, except that interest recoived on bonds upon which atax was paid at source by the debtor corporation should be entered as item 3.The tax of 2 percent paid at source on such interef t should be claimed as a creditin item 16. Interest on bonds is considered income when due and payablo.

Other income.—Enter as item 4 all other taxable income, including dividendsen stock of domestic corporations not subject to income tax under the RevenueAct of li)34 (such as building and loan associations, etc.), and dividanda on stockof foreign corporations, income of an estate or trust, and your share (whetherreceived or not) in tbe profits of a partnership, syndicate, pool, Joint venture etc.

DEDUCTIONS

Tues.—Kntcr os item C all personal taxes and taxes on property paid durinuthe year Do not include Federal income taxes, nor estate, inheritance, logacy,succession and gift luxes No part of foreign Income and profits taxes is allowa-ble as a deductiou if a credit is claimed in item 17 of the return.

Contributions.— Enter as item 7 any contributions or gifts made during theyear to any corporation or fund organized and operated exclusively for religious,charitable, or educational purposes, uo part of the net earnings of which inuresto the benefit of any private shareholder or individual, and no substantial partol tho activities of which is carrying on propaganda, or otherwise attempting,to influence legislation. The amount claimed -shall not exceed 15 percent of thonet income computed without tho benefit of tbb deduetlon.

Furnish names o( organizations and amounts oontributed to each.

Other deductions.—Enter ?s item 8 any other deductions authorized by law,including interest paid on personal indebtedness.

No deduction is allowable for the amount of any item or part thereof allocableto a class of exempt income, other than interest. Items directly attributable tosuch exompt income shall be allocated thereto, and items directly attributableto any class of taxable income shall bo allocated to such taxable income.

A taxpayer receiving any exempt income, other than interest, or holding anyproperty or engaging in any activity the income from which is exempt shallsubmit with his return as a part thereof an itemized statement, in detail, showing(1) the amount of each class of exempt income, and (2) the amount of itemsallocated to each such class (the amount allocated by apportionment beingshown separately).

EARNED INCOME CREDIT. PERSONAL EXEMPTION, ETC.

In computing tha normal tax, but not the surtax, there may be claimed a creditagainst net income of 10 percent of the amount of the earned net income, butnot in excess of 10 percent of the amount of the entire net income. If the netincome is not more than $3,000, the entire net income shall be considered to boearned net income, and if the net income is more than $3,000, the earned netincome shall not be considered to be less than $3,000.

A single person, or a married person not living with husband or wife, mnyclaim a personal exemption of $1,000. A person who, during the entire taxableyea/, was the head of a family or was married and living with husband or wife,may claim an exemption of $2,500. If husband and wife file separate returns,the personal exemption may be taken by either or divided between them.

A "head of a family" is an individual who actually supports and maintainsIn one household one or more individuals who are closely cocnected with himby blood relationship, relationship by marriage, or by adoption, ond whose r'ightto exercise family control und provide for these dependent individuals is based

1 n addition to the personal exemption, a credit of $400 may bo claimod for eachr-Tson (other than husband or wife) under eighteen years of age, or incapable ofself-support because mentally or physically defective, who received his or herchief support from the taxpayer. This credit can be claimed only by the personwlio furnishes the chief support, and cannot be divided between two individuals.

If the status of the taxpayer, insofar as it aftVcts the personal exemption orcredit for dependents, changes during the taxable year, the personal exemptionand credit shall be apportioned in accordance with the number of months beforeond after such change. For the purpose of such apportionment a fractional partof a month shall be disregarded unless it amounts to more than half a monthin which case it phftH be considered as a month.

GENERAL INFORMATION

Affldavit.-The onth will be administered without charge by any collector,deputy collector, or internal revenue agent. If an internal revenue officer is notavailable, the return should be sworn to before a person authorized to admin-ister oaths, except an attorney or agont employed to represent the taxpayerbefore the Department in connection with his tax.

The affidavit must be executed by the person whose income Is reported or byhis legal representative or agent. The return may be made by an agent (1) if,by reason of illness, the person liable for tho making of the return is unable tomake it, or (2) If the taxpayer is unable to make tho return by reason of contin-uous absence from the United States for a period of at least 60 days prior to thedate prescribed by law for making the return. Whenever a return is made byan agent it must be accompanied by a power of attorney on Form 635, or, in thecase of husband and wife, on Form 036 (copies of which may be obtained from thecollector of internal revenue).

The Joint return of husband and wife mnat be signed by both spooses and•worn to by the spouse preparing—filling In—the return. If the return is pre-pared by both spouses, or is prepared by neither spouse, then both spouse*must swear to the return, except where one spouse acts for the other spousaunder a power of attorney submitted on Form 936.

Tax.—The tax may be paid at time of filing the return, or In four equal Install-ments payable quarterly provided each installment is paid on or before itsrespective due date.

PENALTIES

For willful fallow, to make and file a return on tlme.-Not more than $10,000or Imprisonment for not more than one year, or both, together with the costs ofprosocutlon, and, in addition. 5 to 25 percent of tho amount of the tax.

For willfully making a false or fraudulent return.—Not more than $10,000or imprisonment for not more than five years,or both, together with the costs ofprosecution.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

1935

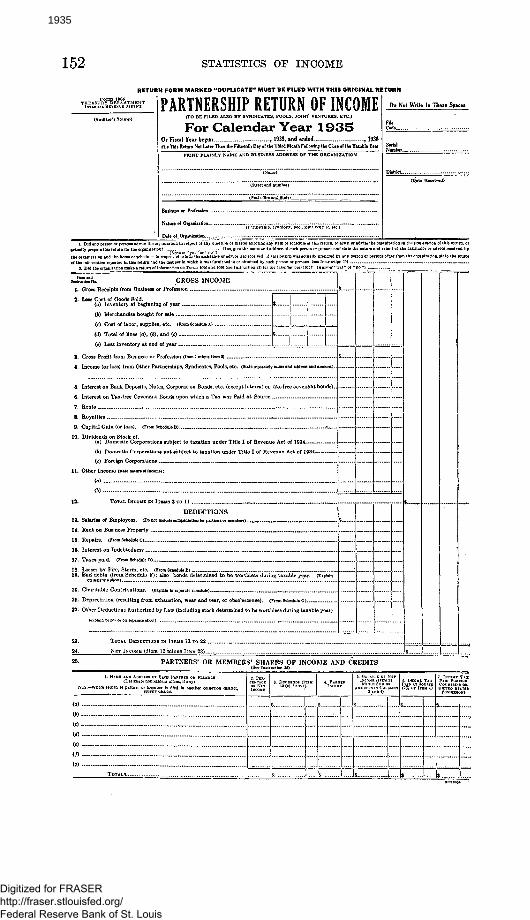

152 STATISTICS OF INCOME

RETURN FORM MARKED "DUPLICATE" MUST BE FILED WITH THIS ORIGINAL RETURN

TREASUK<YIDE1PARTME|NT

(Auditor's Stamp)

PARTNERSHIP RETURN OF INCOME(TO BE FILED ALSO BY SYNDICATES, POOLS, JOINT VENTURES, ETC.)

For Calendar Year 193SOr Fiscal Year begun , 1935, and ended ,-1936File This Return Not Later Than the Fifteenth Day of the Third Month Fallowing the Close of the Taxable Year

PRINT PLAINLY NAME AND BUSINESS ADDRESS OF THE ORGANIZATION

(Name)

(Street and number)

(Post office and State)

Business or Profession _

Nature of Organization

Do Not Write In These Spaces

FileCode

Serial

Number

District . — -

(Date Received)

actually prepare this return for t

the organization and the items c ectDofWwhich the as

give the name and address or such person or persons an

Imtruction No.

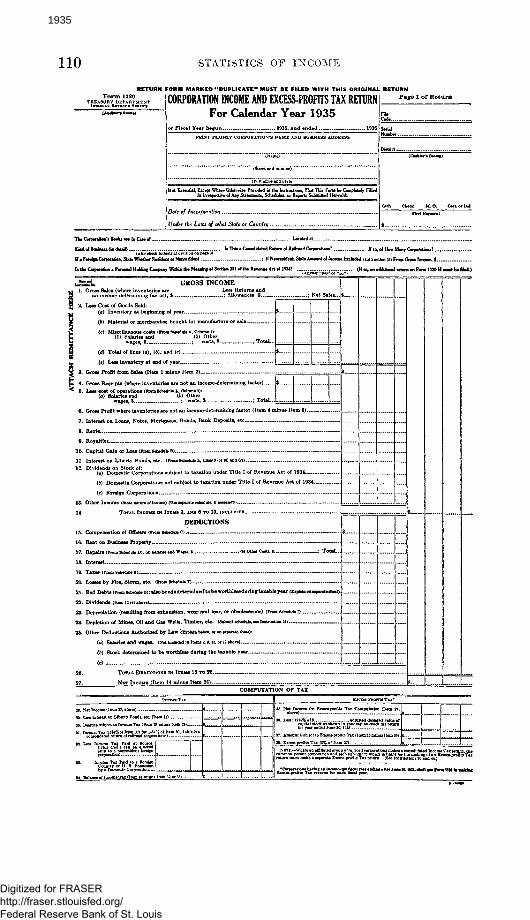

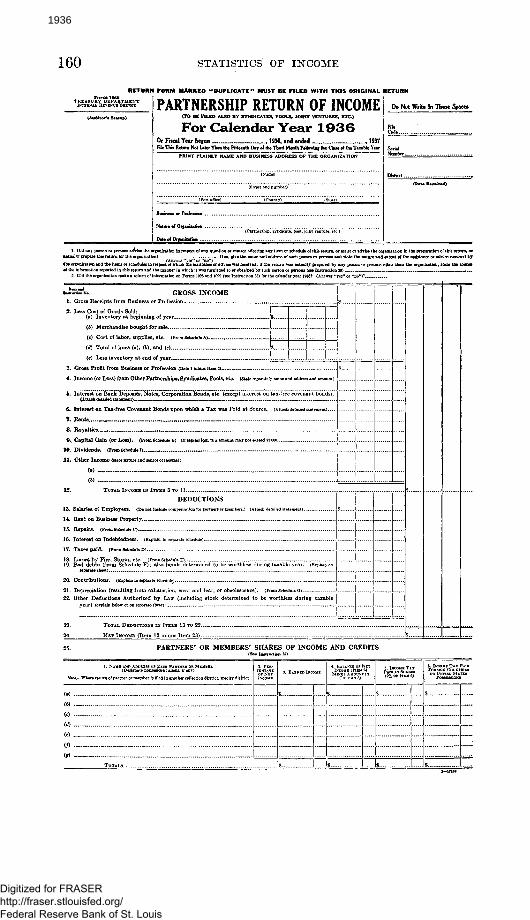

1. Groes Receipts from BusinessGROSS INCOME

r Profession _

(V) Merchandise bought for sale . . . . ,

(c) Cost Of labor, supplies, etc. (From Schedule A)

(d) Total of lines (a), (b), and (e)

(e) Less inventory at end of year _

3. Gross Profit from Business or Profession (Item l minus Item 2)

4. Income (or loss) from Other Partnerships, Syndicates, Pools, etc. (State separatel]

6. Interest on Bank Deposits, Notes, Corporation Bonds, etc. (except interest on tax-free covenant bonds).

6. Interest on Tax-free Covenant Bonds upon which a Tax was Paid at Source

8. Royalties

©. Capital Gain (or loss). (FromSc

(6) Domestic Corporations not subject to taxation u

(e) Foreign Corporations

11. Other Income (state nature of Income):

Bt of 1934—

e Act of 1934-

(o) ..

12. L I N S 3 TO 11

DEDUCTIONS13. Salaries of Employees. (Do not Include compensation for partners or me

14. Rent on Business Property _

15. Repairs. (From Schedule C) _

16. Interest on Indebtedness _

17. Taxes paid. (From Schedule B)

18. Looses by Fire, Storm, etc. (From Schedule E) _19. Bad debts (from Schedule F); also bonds determined to be worthless during taxable year.

20. Charitable Contributions. (Explain In soparate schedule) . _

21. Depreciation (resulting from exhaustion, wear and tear, or obsolescence). (From Schedule 0)

22. Other Deductions Authorized by Law (including stock determined to be worthless during taxable year)

(explain 1

TOTAL

N E T IN

UCTIONS IN ITEMS 13 TO 22 . .

E (Item 12 minus Item 23)...

(Designate nonresident aliens, if any)

«bl«.—Where return of partner or member is filed in another collection district,

( 0 )

(6)

(c)

(«) „

( / )

(?)

c?ici?if

TOTALS

$

s

$

* i 1$

8. INCOME TAX

!$

Pos?«asioAN3 *

$

- -

. . . . .

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

1935

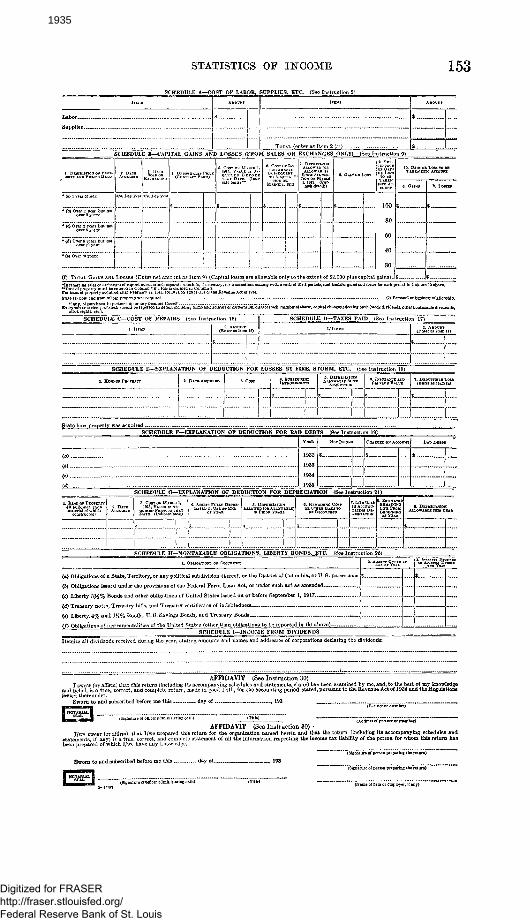

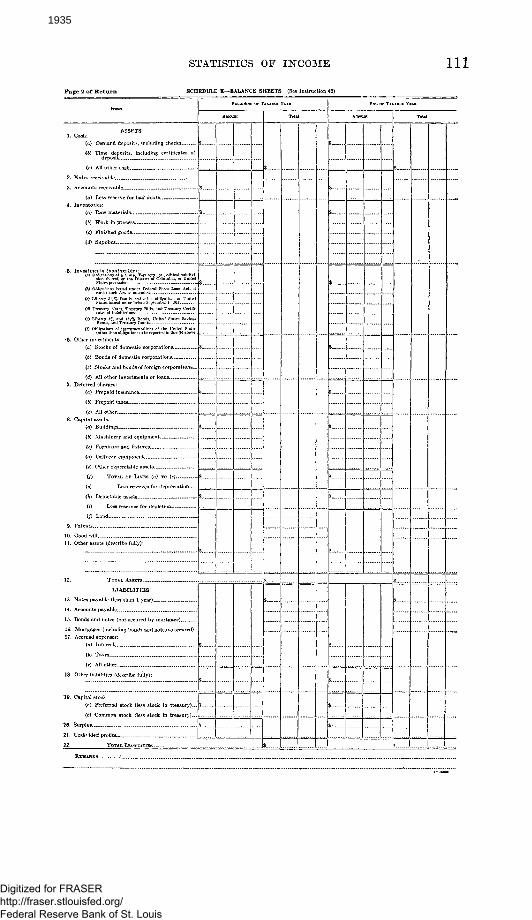

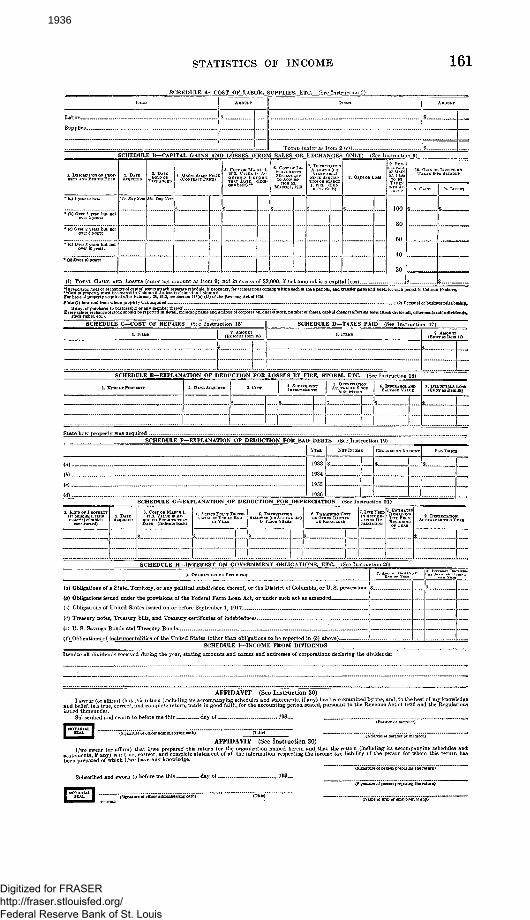

STATISTICS OF INCOME 153SCHEDULE A—COST OF LABOR, SUPPLIES, ETC. (See Instruction 2)

Labor _

Supplies _ _ - -

S

j

ii

.

ll ToTAL (enter as Item

I,EMS

2 (c))

AMOUNT

$

S , . „ .

I. DESCRIPTION or PBOP-

• (a) I year or less;

• (b) Over 1 year but not

• (o) Over 2 years but not

• (e) Over 10 years:

SCHEDULE B—CAPITAL GAINS AND LOSSES (FROM SALES OR EXCHANGES ONLY) (See Ir

£3*2,

Mo. BOD Year

•sssL

MU. / * „ V7«.r

TUAT D A T E ; ( Ini i -

$

™19?3R

(Fur-B

nlsb details)

of $

8. GAS; oa Loss

$

2,000 plus ca pital

structic

INT(?AC-

100

80

60

40

30'

gains).

nO)

a. <U«s

S

s

assb. LOSSES

•Inrejjortinc sales or exchangesof capital assetBattaeh^sepnreto schedule^ii necessa

- any, of purchaser to partnership or any member thereof _

Every sain or sxchanM of stock rnouM bo reportod in detail, inciudiag namo and addrosa of corstock rights, e t c i

- -o . . . . ; (2) Personal

of shares, capital changos affecting basis (stock dividends, other

relationship,

contaiabls dividends.

SCH :DULE C—COST OF REPAIRS

». ITEH3

(See In struction

cd•f

IS) I

15) fi|!

|

SCHEDULE I)—TAXES PAID

1/ITM.

(See Instruction

1t

17)

(ErSer UcmlT)

SCHEDULE E—EXPLANATION OF DEDUCTION FOR LOSSES HY FIRE, STORM, ETC. (See Instruction 18)

1 » « 1 « « - 1 3.COS*

I , .. ii " 1 J L ..-

i 1

7. DEDUCTIBLE LOSS(Enter as Item 18)

$

State how property was acquired ..

SCHEDULE F—EXPLANATION OF DEDUCTION FOB BAD DEBTS (See Inetructic

(a)

W)

YEAS

1932

1933

1934

NETIKCOME

$

n 19)

CHAEOEDO* ACCOST

1

B A D D E . T . '

$

—

SCHEDULE G—EXPLANATION OF DEDUCTION FOR DEPRECIATION (See Instruction 21)

' ( « buildinKE, statematerial of which hSSL

3. COST on MABCH 1,

DATI?D (Ind?cate>bIiste)

I!

i. ASSETS FTJILT D I ? E E -

~™ «?«,«=»

$

|

$

«. REMUNTNO COSTO B O T H I B B A S I O I O

s

T.LrjTETJsiDD

DEOmNINO

9. D E F R I C U T I O NAlXOWABLE THIS YEAn

$

SCHEDULE H—NQNTAXABLE OBLIGATIONS. LIBERTY BONDS, ETC. (See Instruction 26)

(a) Obligations of a State, Territory, or any poUtical subdivision thereof, or the District of Columbia, or U. S. possessions.

{&) Obligations issusd under the provisions of the Federal Farm Loan Act, or under such act as amended

(c) Liberty 3J^% Bonds and other obligations of United States issued oa or before September 1, 1917 _

[d) Treasury notes, Treasury bills, and Treasury certificates of indebtedness

(8) Liberty. 4% «nd 4,%% Bonds, TJ. S. Savings Bonds, and Treasury Bonds_ ^—

if) Obligations of instrumentalities of the United States (other than obligations to bo reported in (6) above)

SCHEDULE I—INCOME FROM DIVIDENDS

. . . . . .

$

Itemizo all dividends received during the year, B1 jnta and names and addresses of corporations declaring the dividends:

AFFIDAVIT (See Instruction 30)I swear (or affirm) that this return (including its accompanying schedules and statements, if any) has been examined by me, and, to the best of my knowledgo

and belief, is a true, correct, and complete return, made in good faith, for the accounting period eiated, pursuant to the Revenue Act of 1934 and the Regulationsissued thereunder.

Sworn to and subscribed before me this day of , 193

(Title

AFFIDAVIT (See Instruction 30) -I/we swear (or affirm) that I/we prepared this return for the organization named herein and that the return (including its accompanying schedules and

statements, if any) is a true, correct, and complete statement of all the information respecting the income tax liability of the person for whom this return hasbeen prepared of which I/we have any knowledge.

(Signature oJ person preparing tb

Sworn to and subscribed before me this day of... t 193

"(Slgnaturo ofofficer administering oath)

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

1935

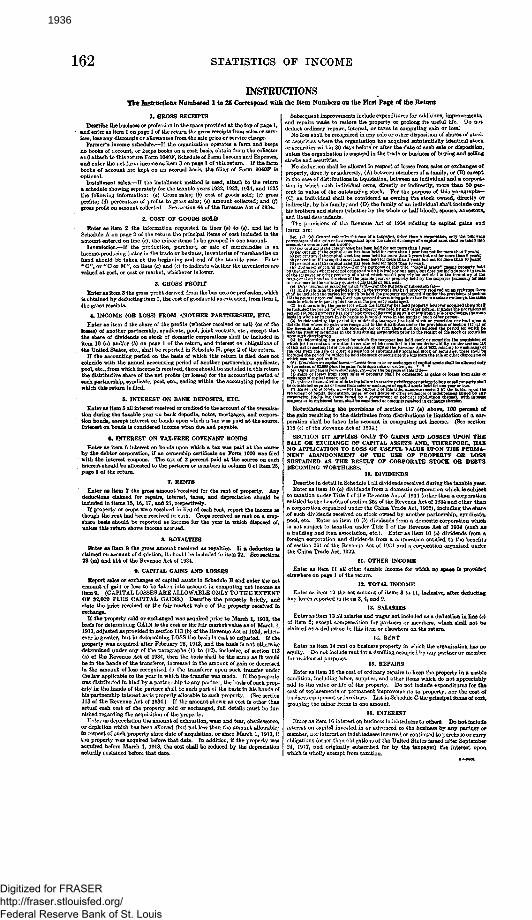

154 STATISTICS OF INCOME

INSTRUCTIONSThe Instructions Numbered 1 to 25 Correspond with the Item Numbers on the First Page of the Return

1. GROSS RECEIPTSDescribe the busim >r profession in the space provided at the top of page

• 1, and enter as item. 1 on page 1 of the return the gross receipts from sales orservices, less any discounts or allowances from the sale price or service charge.

Farmer's income schedule.—If the organization operates a farm and keepsno books of account, or keeps books on a cash basis, obtain from the collectorand attach to this return Form 1040F, Schedule of Farm Income and Ex-penses, and enter the net farm income as item 3 on page 1 of this return. Ifthe farm books of account are kept on an accrual basis, the filing of Form1040F is optional.

Installment sales.—If the installment method is used, attach to the returna schedule showing separately for the taxable years 1933,1934,1935, and 1936the following information: (a) Gross sales; (b) cost of goods sold; (c) grossprofits; (d) percentage of profits to gross sales; (e) amount collected; and (/)gross profit on amount collected. See section 44 of the Revenue Act of 1936.

2. COST OF GOODS SOLDEnter as item 2 the information requested in lines (a) to (e), and list in

Schedule A on page 2 of the return the principal items of cost included in theamount entered on line (c), the minor items to be grouped in one amount.

Inventories.—If the production, purchase, or sale of merchandise is anincome-producing factor in the trade or business, inventories of merchandisen hand should be taken at the beginning and end of the taxable year. Enter

"C",valued at cost, or cost o arket, whichever is l

3. GROSS PROFITEnter as item 3 the gross profit derived from the business or profe on

•which is obtained by deducting item 2, the cost of goods sold as extended,from item 1, the gross receipts.

4. INCOME (OR LOSS) FROM ANOTHER PARTNERSHIP, ETC.Enter as item 4 the share of the profits (whether received or not) (or of the

losses) of another partnership, syndicate, pool, joint venture, etc., except th;the share of interest on obligations of the United States, etc., shall be reportedin Schedule H, page 2 of the return..

If the accounting period on the basis of which this return is filed does notcoincide "with the annual accounting period of another partnership, syndipool, etc., from which income is received, there should be included in thi return the distributive share of the net profits (or losses) for the accountingperiod of such partnership, syndicate, pool, etc., ending within the accountingperiod for which this return is filed.

5. INTEREST ON BANK DEPOSITS, ETC.Enter as item 5 all interest received or credited to the account of the organ

ization during the taxable year on bank deposits, notes, mortgages, and c rporation bonds, except interest on bonds upon which a tax wa id t tlsource. Interest on bonds is considered income when due and pa p

ble6. INTEREST ON TAX-FREE COVENANT BONDS

s paid aF 10

Enter as item 6 interest on bonds upon which pby the debtor corporation, if an ownership certificate on Form 1000 was filed•with the interest coupons. The tax of 2 percent paid at the source on suchinterest should be allocated to the partners or members in column oi tern25, page 1 of the return.

7. RENTSEnter sis item 7 tnc jross unmount TGCGIVGQ for tno rent of property* Any

deductions claimed for repairs," interest, -taxes, and depreciation should beincluded in items 15, 16, 17, and 21, respectively.

If property or crops were received in lieu of cash rent, report the income asthough the rent had been received in cash. Crops received as rent on a crop-share basis should be reported as income for the year in which disposed of,unless this return shows income accrued.

8. ROYALTIESEnter as item 8 the gross amount received as royalties. . If a deduction is

claimed on account of depletion, it should be included in item 22. See sections23 (m) and 114 of the Revenue Act of 1936.

9. CAPITAL GAINS AND LOSSESReport sales or exchanges of capital assets in Schedule B and enter the net

amount of gain or loss to be taken into account in computing net income asitem 9. (CAPITAL LOSSES ARE ALLOWABLE ONLY TO THE EXTENTOF $2,000 PLUS CAPITAL GAINS. THEREFORE, IF THE TOTALAMOUNT OF CAPITAL LOSSES IS IN EXCESS OF THE TOTALAMOUNT OF CAPITAL GAINS, THE AMOUNT TO BE ENTERED ASITEM 9 MAY NOT EXCEED $2,000.) Describe the property briefly, and

e the Tin exchange.

If the property sold or exchanged was acquired prior to March 1, 1913, thebasis for determining GAIN is the cost or the fair market value as of March 1,1913, adjusted as provided in section 113 (b) of the Revenue Act of 1936,•whichever is greater, but in determining LOSS the basis is cost so adjusted.If the property was acquired after February 28, 1913, and the basis is nototherwise determined under any of the paragraphs (1) to (12), inclusive, ofsection 113 (a) of the Revenue Act of 1936, then tie basis shall be the sameas it would be in the hands of the transferor, increased in the amount of gainor decreased in the amount of loss recognized to the transferor upon suchtransfer under the law applicable to the year m which the transfer was made.If the property was distributed in kind by a partnership to any partner, thebasis of such property in the hands of the partner shall be such part of thebasis in his hands of his partnership interest as is properly allocable to suchproperty. (See section 113 of the Revenue Act of 1936.) If the amountshown as cost is other than actual cash cost of the property sold or exchanged,full details must be furnished regarding the acquisition of the property.

Enter as depreciation the amount of exhaustion, wear and tear, obsolescence,or depletion which has been allowed (but not less than the amount allowable)in respect of such property since date of acquisition, or since March 1,1913, ifthe property was acquired before that date. In addition, if the property wasacquired before March 1, 1913, the cost shall be reduced by the depreciationactually sustained before that date.

Subsequent improvements include expenditures for additions, improve-ments, and repairs made to restore the property or prolong its useful life. Donot deduct ordinary repairs, interest, or taxes in computing gain or loss.

No loss shall be recognized in any sale or other disposition of shares ofstock or securities where the organization has acquired substantially identicalstock or securities within 30 days before or after the date of such sale or dis-position, unless the organization is engaged in the trade or business of buyingand selling stocks and securities.

No deduction shall be allowed in respect of losses from sales or exchangesof property, directly or indirectly, (A) between members of a family, or(B) except in the case of distributions in liquidation, between an individualand a corporation in which such individual owns, directly or indirectly, morethan 50 percent in value of the outstanding stock. For the purpose of thisparagraph—(C) an individual shall be considered as owning the stock owned,directly or indirectly, by his family; and (D) the family of an individual shallinclude only his brothers and sisters (whether by the whole or half blood),spouse, ancestors, and lineal descendants.

The provisions of the Revenue Act of 1936 relating to capital gains and

N w h t nding he p o o s of c on 117 (a) a o e 100 pe ent ofthe g n re ng to e b f m di tr b t on 1 on f opora on h 1 be taken n o ceo nt n comp y t n o e e e n hecase of amounts disti b ted in co p e e 1 q d on of a c rjo t ( ecsection 115 (c) of the Revenue Act of 1936.)

SECTION 117 APPLIES ONLY TO GAINS AND LOSSES UPON THESALE OR EXCHANGE OF CAPITAL ASSETS AND, THEREFORE, HASNO APPLICATION TO LOSS OF USEFUL VALUE UPON THE PER-MANENT ABANDONMENT OF THE USE OF PROPERTY OR LOSSSUSTAINED AS THE RESULT OF CORPORATE STOCK OR DEBTSBECOMING WORTHLESS.

10. DIVIDENDSEnter as item 10 the total of all dividends reported in Schedule I.

11. OTHER INCOMEEnter as item 11 all other taxable income for which no space is provided

elsewhere on page 1 of the return.

12. TOTAL INCOMEEnter as item 12 the net amount of items 3 to 11, inclusive, after deducting

any los reported in item 3, 4, a

13. SALARIESEnter as item 13 all salaries and wages not included as a deduction in line

(c) of item 2; except compensation for partners or members, which shall notbe claimed as a deduction in this item or elsewhere on the return.

14. RENTEnter as item 14 rent or>"business property in which the organization has no

equity. Do no'; include rent for a dwelling occupied by any partner or memberfor residential purposes.

15. REPAIRSEnter as item 15 the cost of ordinary repairs to keep the property in a

usable condition, including labor, supplies, and other items which do not ap-preciably add to the value or life of the property. Do not include expendituresfor the cost of replacements or permanent improvements to property, nor thecost of business equipment or furniture. List in Schedule C the principalitems of cost, grouping the minor items in one amount.

16. INTERESTEnter as item 16 interest on business indebtedness to others. Do not in-

clude interest on capital invested in or advanced to the business by anypartner or member, nor interest on indebtedness incurred or continued to ptir-- -chase or carry obligations (other than obligations of the United States issuedafter September 24, 1917, and originally subscribed for by the taxpayer) theinterest upon which is wholly exempt from taxation.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

1935

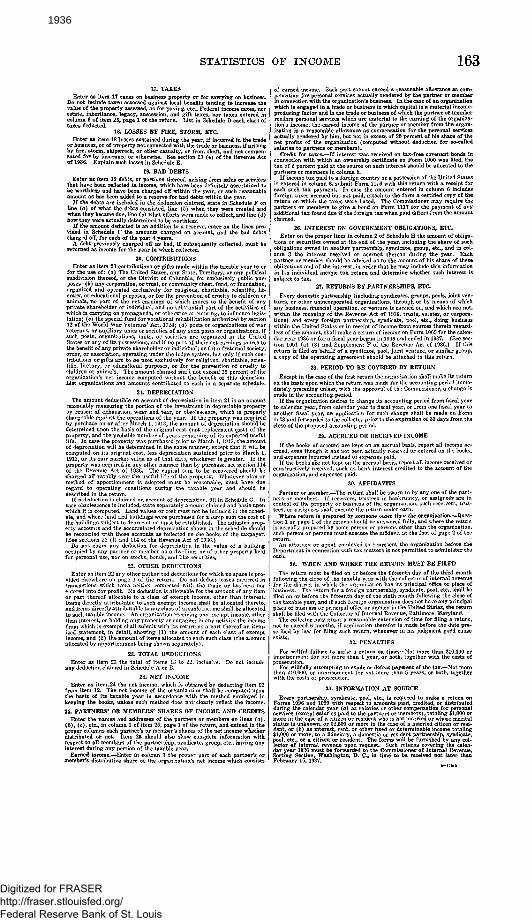

STATISTICS OF INCOME 15517. TAXES

Enter as item 17 taxes <n business property or for carrying on business. Donot include taxes assessed against local benefits tending to increase the value ofthe property assessed, as for paving, etc., Federal income taxes, nor estate,inheritance, legacy, succession, and gift taxes, nor taxes entered in column 7 ofitem 25, puga 1 of the return. List in Schedule D each class of taxes deducted.

18. LOSSES BY FIRE, STORM, ETC.Eater as item 18 losses sustained during the year, if incurred in the trade or

business, or of property not connected with the trade or business, if arising byfire, stonr>, shipwreck, or other casualty, or from theft, and not compensatedfor by insurance or otherwise. See section 23 (c) of the 'Revenue- Act of 1934.Explain such losses in Schedule E.

19. BAD DEBTSEnter as item 19 debts, or portions thereof, arising from sales or services that

have been reflected in income, which have been definitely ascertained to beworthless and have been charged off within the year, or such reasonable amountas ha/3 been added to a reserve for bad debts within the year.

If the debts are included in the deduction claimed, state in Schedule F onlice (a) of what the debts consisted, line (6) when they were created and whenthey became due, line (c) what efforts were made to collect, and line (d) howthey were actually determined to be worthless.

If the amount deducted is an addition to a reserve, enter en the lines providedin Schedule F the amounts charged on account, and the bad debts charged off,for each of the past 4 years.

A debt previously charged off as bad, if subsequently collected, must bereturned as income for the year in which collected.

20. CONTRIBUTIONSEnter as item 20 contributions or gifts made within the taxable year to any

corporation, or trust, or community chest, fund, or foundation, organized andoperated exclusively for religious, charitable, scientific, literary, or educationalpurposes, or for tbe prevention of cruelty to children or animals, no part of thenet earnings of which inures to the benefit of any private shareholder or indi-vidual, and no substantial part of the activities of which is carrying on propa-ganda, or otherwise attempting, to influence legislation. The amount claimedehall not exceed 15 percent of the organization's net income computed withoutthe benefit of this deduction. List organizations and amounts contributed toeach in a separate schedule.

21. DEPRECIATIONThe amount deductible on account of depreciation in item 21 is an amount

reasonably measuring the portion of the investment in depreciable property byreason of exhaustion, wear and tear, or obsolescence, which is properly chargeableagainst the operatic s of the year. If tho property was acqu'red by parchaseon or after March 1, 1913, the amount of depreciation should be determinedupon tTie basia of the original cost (not replacement co-it) of the property, andthe probable rumber of years remaining of its expected useful life. In case theproperty \va purchased prior to March 1, 1913, tne amount of depreciation willbe delr-rrcir.ed in the sajue manne-, except that it will be compute*.' on its originilcost, les dt preci ition. sustained prior to March 1, 1913, or its fair msrket valueas of that date, whichever is greater. If the property was acquired in aryother manner than by purchase, see section 111 of tho Revenue Ac*, of 1931.The capita sum to be recovered should be ch?.-p =d off ratably over the usefullife eZ the proptrty. Whatever plan or method of apportionment is adoptedmust be reasonable, must have due regard to operating co. ditions during thotaxable year and should be described in the return.

If a deduction is claimed on account of depreciation, fill in Schedule G. Incase obsolescence is included, etate separately amount cla;med and basis upenwhich it is computed. Land values or cost mvst cot be included in the schedule,and where I<,ri and buildings were purchased for a Tump sum the COS\J of thebuildirg subject to depreciation must be established. Th^ adjusted property

reconciled with, those account.? as relucted on the books of tho taxpayer. (Si eeectioLS 23 (1) and 114 of the Kcvenue Act o{ 1934.)