McGraw-Hill/Irwin Copyright © 2008, The McGraw-Hill Companies, Inc. All rights reserved. Welcome to “Income from House Property” Chapter 8

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

McGraw-Hill/Irwin Copyright © 2008, The McGraw-Hill Companies, Inc. All rights reserved.

Welcome to “Income from House

Property”

Chapter8

Group Name-Drinking Star

2-2

Name ID Md. Mizanur

Rahman11202073

Md.Dipu Hossain 12102461

Arifa Akter Pepasha

12102508

The concept of income from house property

• “Income from House Property “is the third head of income among the seven heads mentioned in section 20 of the ITO, 1984. According to section 24 and 25 of the ITO, 1984, annual value of property consisting of any building or lands appurtenant thereto of which the assesse is the owner, is chargeable to tax under this head of income after claiming deduction under sec. 25.

2-3

The concept of income from house property

Income Tax Ordinance, 1984, the following incomes are to be considered under the head “Income from House Property”.•Annual value of property, whether used for commercial or residential purposes, consisting of any building, furniture, fixture, fittings etc. Or lands appurtenant thereto, of which the assesse is the owner. [Section-24(1)].

2-4

The concept of income from house property

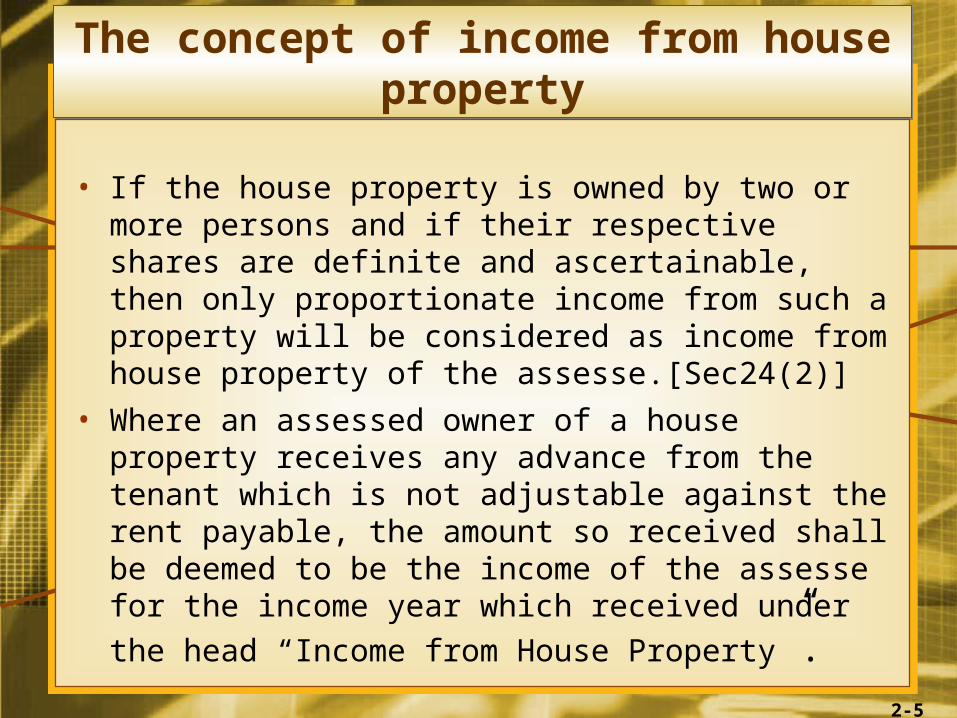

• If the house property is owned by two or more persons and if their respective shares are definite and ascertainable, then only proportionate income from such a property will be considered as income from house property of the assesse.[Sec24(2)]

• Where an assessed owner of a house property receives any advance from the tenant which is not adjustable against the rent payable, the amount so received shall be deemed to be the income of the assesse for the income year which received under the head “Income from House Property”.

2-5

The conditions of income under the head “Income from House

Property”

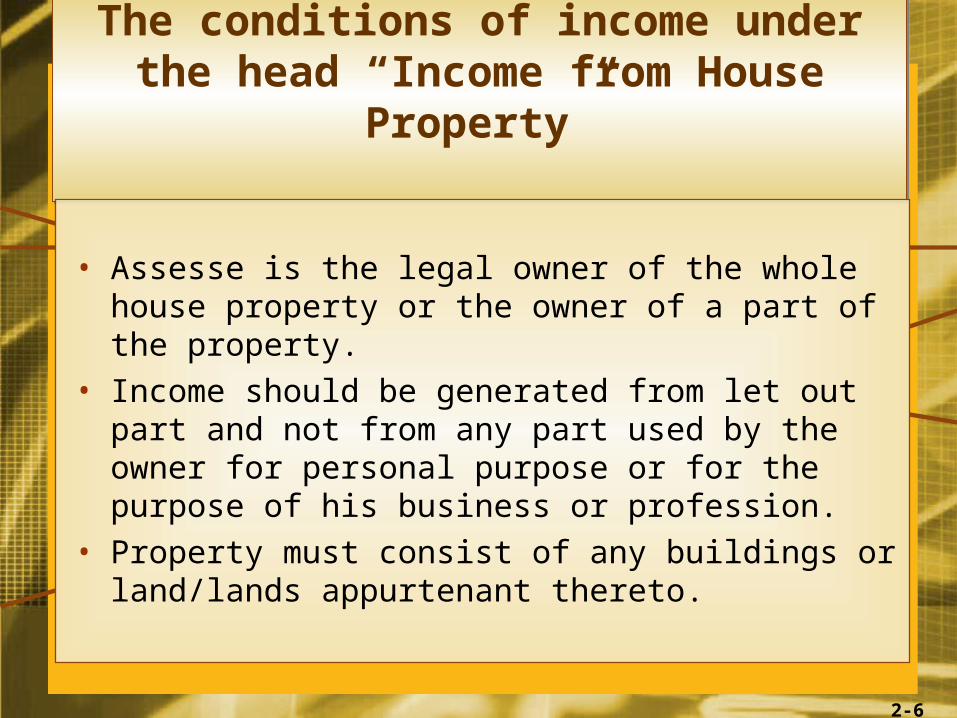

• Assesse is the legal owner of the whole house property or the owner of a part of the property.

• Income should be generated from let out part and not from any part used by the owner for personal purpose or for the purpose of his business or profession.

• Property must consist of any buildings or land/lands appurtenant thereto.

2-6

The conditions of income under the head “Income from House

Property”

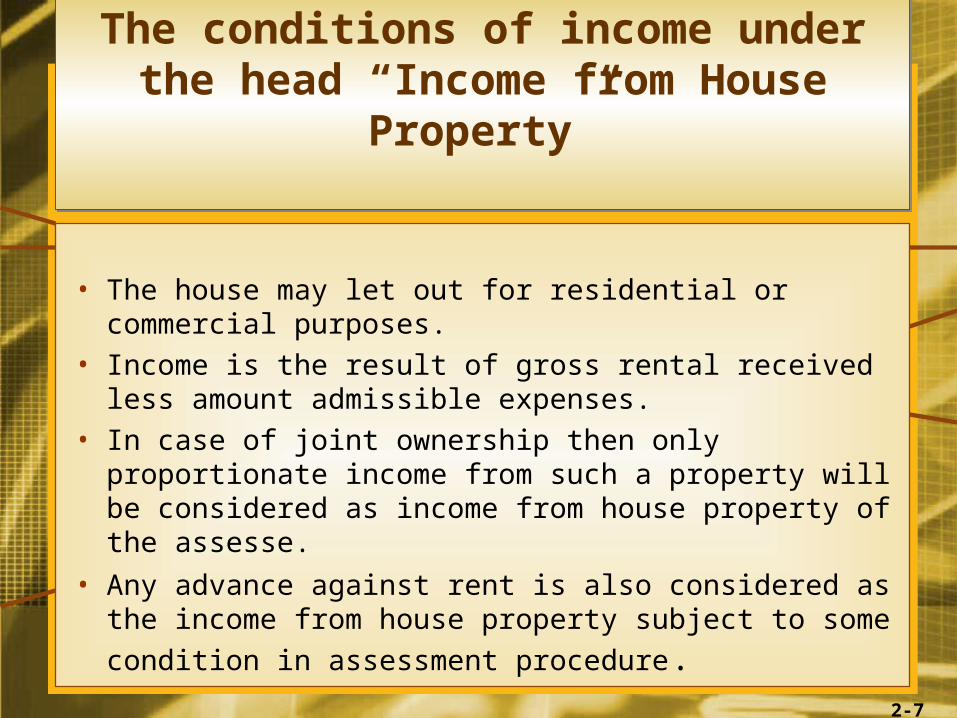

• The house may let out for residential or commercial purposes.

• Income is the result of gross rental received less amount admissible expenses.

• In case of joint ownership then only proportionate income from such a property will be considered as income from house property of the assesse.

• Any advance against rent is also considered as the income from house property subject to some condition in assessment procedure.

2-7

Income from partly let out house property

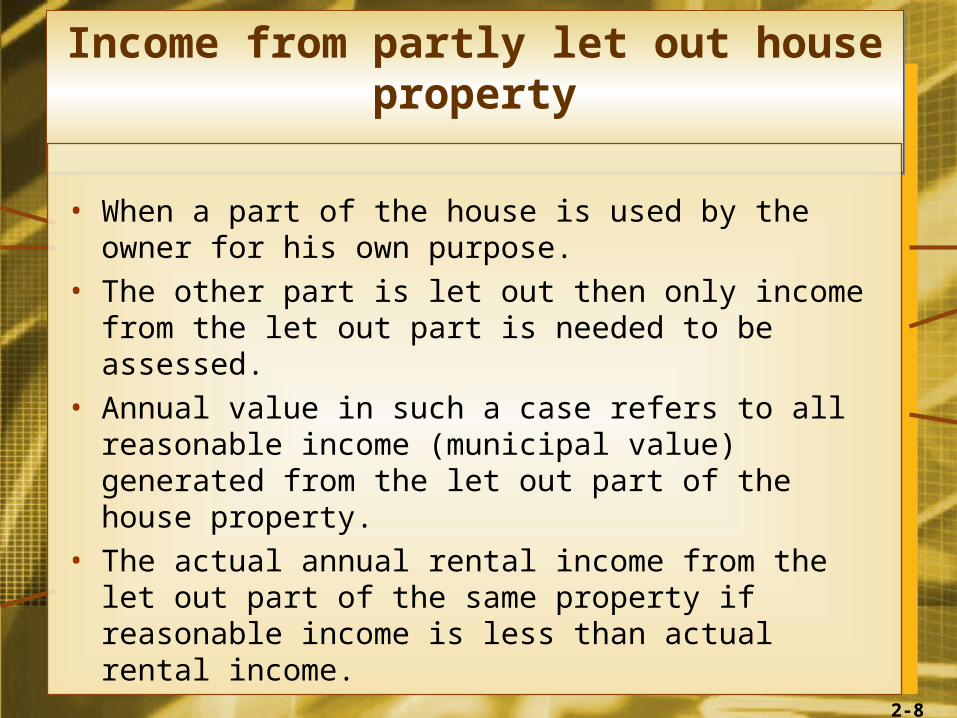

• When a part of the house is used by the owner for his own purpose.

• The other part is let out then only income from the let out part is needed to be assessed.

• Annual value in such a case refers to all reasonable income (municipal value) generated from the let out part of the house property.

• The actual annual rental income from the let out part of the same property if reasonable income is less than actual rental income.

2-8

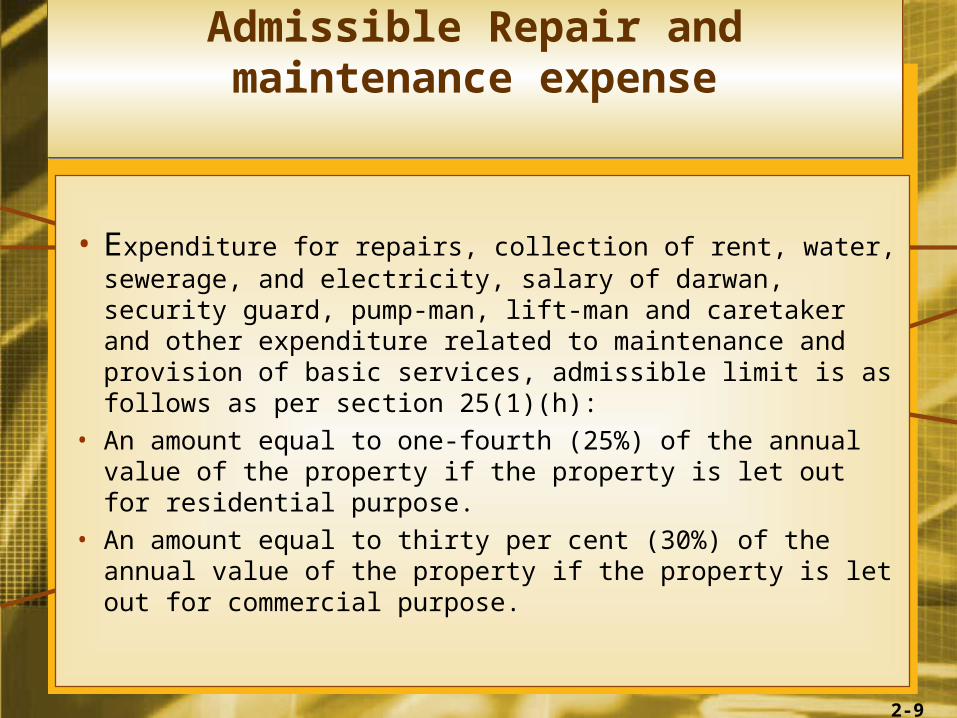

Admissible Repair and maintenance expense

• Expenditure for repairs, collection of rent, water, sewerage, and electricity, salary of darwan, security guard, pump-man, lift-man and caretaker and other expenditure related to maintenance and provision of basic services, admissible limit is as follows as per section 25(1)(h):

• An amount equal to one-fourth (25%) of the annual value of the property if the property is let out for residential purpose.

• An amount equal to thirty per cent (30%) of the annual value of the property if the property is let out for commercial purpose.

2-9

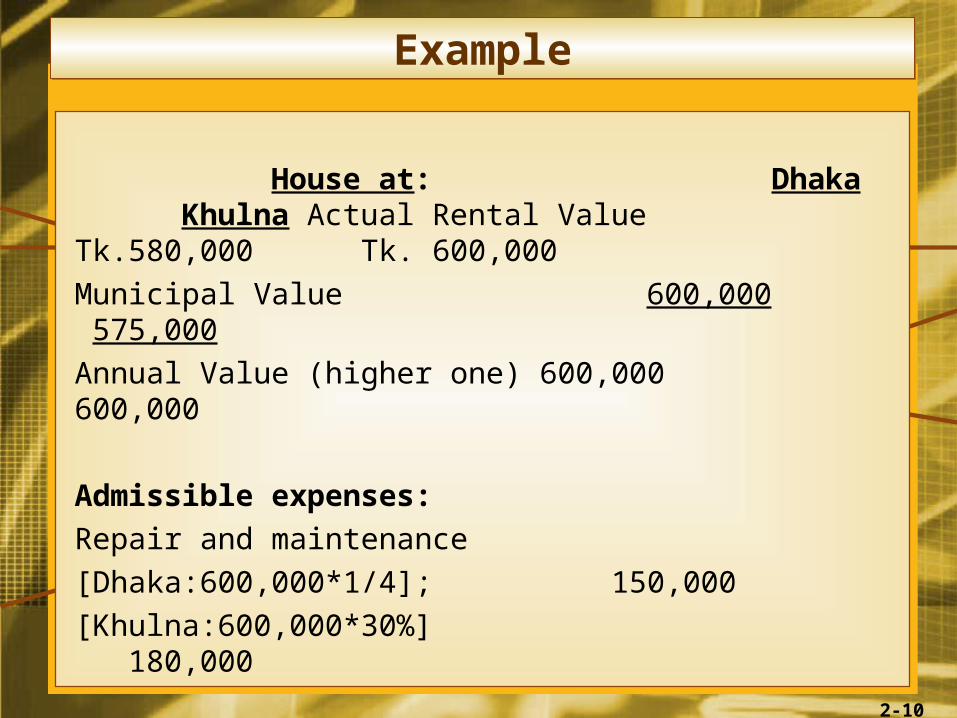

Example

House at: Dhaka Khulna Actual Rental Value Tk.580,000 Tk. 600,000Municipal Value 600,000 575,000Annual Value (higher one) 600,000 600,000

Admissible expenses:Repair and maintenance[Dhaka:600,000*1/4]; 150,000[Khulna:600,000*30%] 180,000

2-10

Broad Question:•Explain the concept of income from house property as per the ITO, 1984.Short Question:•Define income from partly let out house property.•Write down the condition of income under the head “Income from house property”.

Short note:• Admissible repair and maintenance expense.

2-11

Thanks toall

2-12

Related Documents