Income and Expense Effective date July 1997 Section 3400.1 Traditional ratio and peer earnings analyses are not relevant at a branch because earnings are largely influenced by the role of the branch within the foreign banking organization (FBO). Some FBOs maintain a U.S. presence to meet certain global portfolio considerations. As a result, their U.S. operations may likely engage in a wide range of activities similar to those of U.S. domestic banks. Other FBOs may have different objectives in establishing a U.S. pres- ence, such as to provide funding and clearing services. A branch may also benefit from unique relationships that have a positive effect on its earnings, such as interest free funds, advances from the head office or managing assets not reflected on its books. Therefore, earnings should be evaluated primarily against budgeted num- bers, which should be based on the branch’s strategic plan. The examiner should also deter- mine the role that the earnings and revenue structure plays in the context of the overall U.S. operations and objectives of the FBO. Com- ments may be warranted as to the adequacy of such results. In establishing the budget, management should assess the broad range of financial and opera- tional risk exposures, which are encompassed in the strategic plan. Projections should take into account not only the composition, quality, and risk structure of branch assets but also the internal control environment under which the assets are booked. Further, management’s abil- ity to prepare realistic budgets and meet bud- geted projections would indicate some measure of effective planning and control over the branch’s activities. To maximize effectiveness, budget projections should be periodically reviewed and updated as conditions change throughout the fiscal year. Actual results should be periodically compared to budget and material variances identified and reviewed by management. GENERAL EXAMINATION APPROACH Earnings are not a rated component of the branch rating system, although the level of earnings or absence of earnings may affect rating components. The review of earnings also provides important information on the nature and efficiency of the branch’s operations. The evaluation of earnings will consider, primarily, the effectiveness of a branch’s comprehen- sive risk management procedures as it affects budgetary performance. Accordingly, variances to budgets should be reviewed. Persistent variances or exceptions may indicate poor planning or unrealistic projections, barring changes in economic and market conditions and other external factors or influences from the head office, which are beyond the branch’s control. The accuracy and integrity of earnings pre- sented in risk management reports should be evaluated. For instance, reported earnings that do not properly reflect potential losses in the branch’s credit risk exposures or accrued income on nonperforming loans may raise questions about the effectiveness of financial and account- ing controls. The examiner should keep in mind, however, that the consolidated benefits derived by the FBO, as a result of maintaining a market presence to facilitate a global banking service network, may offset any earnings deficiencies or continued loss operations. Accordingly, the branch’s strategic plan and function within the FBO and standards used by the head office to evaluate earnings performance must be ascer- tained and analyzed. Examining the changes in earnings over time (a trend analysis) is a fundamental method for evaluating earnings. The trend in overall earnings and trends in earnings components should be reviewed to the extent that the branch’s strategic plan has not changed significantly. Any significant changes or variances in profits or any of the components of income and expense should be investigated. Improving, deteriorating, and even flat earnings can be the result of not only changes in economic conditions but also of management’s actions or influence over earn- ings through intrabank transactions. Some prof- itability ratios have been used, including net interest income/average assets (net interest margin) and net operating income/average assets, to make such an assessment. While providing a basis for analysis, particularly in year-to- year comparisons, earnings ratios can vary significantly among branches, depending on the nature of branch activity and the degree of support or influence exerted by head office. Branch and Agency Examination Manual September 1997 Page 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Income and ExpenseEffective date July 1997 Section 3400.1

Traditional ratio and peer earnings analysesare not relevant at a branch because earningsare largely influenced by the role of thebranch within the foreign banking organization(FBO).

Some FBOs maintain a U.S. presence to meetcertain global portfolio considerations. As aresult, their U.S. operations may likely engage ina wide range of activities similar to those ofU.S. domestic banks. Other FBOs may havedifferent objectives in establishing a U.S. pres-ence, such as to provide funding and clearingservices. A branch may also benefit from uniquerelationships that have a positive effect on itsearnings, such as interest free funds, advancesfrom the head office or managing assets notreflected on its books. Therefore, earnings shouldbe evaluated primarily against budgeted num-bers, which should be based on the branch’sstrategic plan. The examiner should also deter-mine the role that the earnings and revenuestructure plays in the context of the overall U.S.operations and objectives of the FBO. Com-ments may be warranted as to the adequacy ofsuch results.

In establishing the budget, management shouldassess the broad range of financial and opera-tional risk exposures, which are encompassed inthe strategic plan. Projections should take intoaccount not only the composition, quality, andrisk structure of branch assets but also theinternal control environment under which theassets are booked. Further, management’s abil-ity to prepare realistic budgets and meet bud-geted projections would indicate some measureof effective planning and control over thebranch’s activities. To maximize effectiveness,budget projections should be periodicallyreviewed and updated as conditions changethroughout the fiscal year. Actual results shouldbe periodically compared to budget and materialvariances identified and reviewed bymanagement.

GENERAL EXAMINATIONAPPROACH

Earnings are not a rated component of thebranch rating system, although the level ofearnings or absence of earnings may affectrating components. The review of earnings also

provides important information on the natureand efficiency of the branch’s operations. Theevaluation of earnings will consider, primarily,the effectiveness of a branch’s comprehen-sive risk management procedures as it affectsbudgetary performance. Accordingly, variancesto budgets should be reviewed. Persistentvariances or exceptions may indicate poorplanning or unrealistic projections, barringchanges in economic and market conditions andother external factors or influences from thehead office, which are beyond the branch’scontrol.

The accuracy and integrity of earnings pre-sented in risk management reports should beevaluated. For instance, reported earnings thatdo not properly reflect potential losses in thebranch’s credit risk exposures or accrued incomeon nonperforming loans may raise questionsabout the effectiveness of financial and account-ing controls. The examiner should keep in mind,however, that the consolidated benefits derivedby the FBO, as a result of maintaining a marketpresence to facilitate a global banking servicenetwork, may offset any earnings deficiencies orcontinued loss operations. Accordingly, thebranch’s strategic plan and function within theFBO and standards used by the head office toevaluate earnings performance must be ascer-tained and analyzed.

Examining the changes in earnings over time(a trend analysis) is a fundamental method forevaluating earnings. The trend in overallearnings and trends in earnings componentsshould be reviewed to the extent that the branch’sstrategic plan has not changed significantly. Anysignificant changes or variances in profits or anyof the components of income and expense shouldbe investigated. Improving, deteriorating, andeven flat earnings can be the result of not onlychanges in economic conditions but also ofmanagement’s actions or influence over earn-ings through intrabank transactions. Some prof-itability ratios have been used, including netinterest income/average assets (net interestmargin) and net operating income/average assets,to make such an assessment. While providing abasis for analysis, particularly in year-to-year comparisons, earnings ratios can varysignificantly among branches, depending onthe nature of branch activity and thedegree of support or influence exerted by headoffice.

Branch and Agency Examination Manual September 1997Page 1

PROFIT CENTERS AND COSTCENTERS

Generally, branches will function as profit cen-ters or cost centers. As an independent profitcenter, a branch will likely have a broad earningasset base and could have substantial off-balance-sheet activities. The branch would likely offer abroad array of products and services. Thus,earning assets and fee-based services would beprimary sources of income. Examiners shouldconsider the income distribution and the relativeprofitability and stability of the various sourcesof income.

As a cost center, the branch would serve amore narrowly defined central purpose of eitherproviding a service to the head office or theFBO’s customer network, such as a provider offunds to other bank offices. As such, the branchwould likely offer only a limited number ofproducts or services. Earnings at such officeswill generally be less than robust.

Accordingly, profitability as a factor in evalu-ating the branch is diminished. In these instancestraditional ratio and trend analysis is not rel-evant and alternate analysis techniques shouldbe employed. The examiner should determinethe standards that head office management usesin evaluating the branch’s performance. Thisanalysis will focus on the branch’s strategic planor primary function, for example, to serve as asource of liquidity for the head office or otherbranches, to service the FBO’s trade-relatedbusiness or to give the FBO a presence in aparticular geographic location as part of itsglobal banking network.

FACTORS AFFECTING EARNINGS

The Mission of the Office

The level of earnings would generally be drivenby the branch’s mission. In this context, internalfactors could significantly influence earnings tothe extent that a branch’s earnings are essen-tially managed by the head office. To make thisdetermination, examiners should carefully evalu-ate reported income for unusually high or lowprofit margins. For example, a branch may haveancillary functions from which it incurs addi-tional expense or receives supplementary income,such as managing an offshore book or providingmanagement or technical services to other offices

in a regional office function. If the fees for theseservices are not directly related to or based onthe fair value of goods and services received, thebranch’s earnings can be affected. Services couldinclude electronic data processing, audit andcredit review, credit management, and foreignexchange and correspondent banking services.

Funding Sources

A branch that is funded through borrowingsfrom related entities may have its cost of fundsadjusted above or below market rates or evenpriced below the FBO’s cost of funds. The headoffice might also provide an interest free capitalallocation, or fund the branch’s reserves at nocost. In these ways, the head office can eithersubsidize or reduce the branch’s net interestincome.

Transfer of Assets

The FBO may also transfer assets to or from abranch’s books, which also will affect earnings.The transfer of nonperforming and other prob-lem loans from the branch to the head office oranother branch of the FBO will improve abranch’s earnings and, conversely, negativelyaffect the earnings of any branch designated bythe FBO as a workout branch. Low quality loansmaintained on a branch’s books would reduceinterest income to the extent that full interestpayments are not received. The transfer of suchassets from the books of a branch would improvethe quality of its assets, support its net interestincome, and reduce its need for loan loss provi-sions and charge-offs. High quality earningassets may also be transferred to a branch’sbooks from the head office. This may occur withstart-up offices or branches that cannot other-wise generate earning assets at a level to sustainoperations and fund the cost of doing business.

Accounting Considerations

Earnings at a branch may also be distorted tosome extent because of the effect of homecountry accounting standards, administrative,tax, or other external influences. Accordingly, inreviewing earnings, the examiner should adjustbranch income and expense statements to cor-respond with U.S. generally accepted accounting

3400.1 Income and Expense

September 1997 Branch and Agency Examination ManualPage 2

principles. If statements cannot be adjusted, theexaminer’s written analysis must take into con-sideration major accounting aberrations. Morecommonly seen accounting exceptions mayinclude:

• Recognizing interest income on loans, which,according to U.S. standards, should be placedon nonaccrual status.

• All U.S. offices of a foreign bank may becombined for income tax purposes; accord-ingly, taxes might be calculated by a regionaloffice and the branch may not accrue for taxes.

• Failure to record unrecognized gains and losseson trading assets and certain off-balance sheetcontracts in accordance with FASB 115 andFIN 39 can affect both asset valuations andearnings.

ANALYTICAL REVIEW

Interest Income

Recognizing that branch earnings are primarilyevaluated against budgeted numbers, a compari-son of detailed balances on a period-to-periodbasis also should be performed to assess trendsin account balances. Such a review also wouldprovide the examiner with an understanding ofbranch operations and help to identify potentialproblem situations. The analysis of net interestincome will give an indication of management’sability to borrow at attractive rates and investthose funds with maximum profitable results.The level and trend of net interest incomeshould be established and evaluated. As withany financial institution, the composition of netinterest income should be reviewed for qualityand stability.

In analyzing net interest income, the compu-tation of net interest margin (interest incomeminus interest expense, divided by average earn-ings assets) is helpful, although the potentialdistortion of net interest income through inter-office transactions can limit the usefulness of theratio. When discussing growth in earnings, theexaminer should clearly differentiate betweenincreases due to rates or yields versus volumesof earning assets. An improvement in net inter-est income, as a percentage of earning assets,may reflect favorably on management’s abilityto invest its funds at favorable yields or itsability to find less expensive sources of funds.However, it also may reflect changes in rates on

interoffice transactions. The management ofinterest rate risk also can affect earnings. Anaggressive or speculative funding policy, wherebythe branch is permitted to maintain large interestrate sensitivity gaps, could result in materialincreases or decreases in margins.

Asset Yields

An analysis of asset yields should provide ameasure of the branch’s ability to invest funds inearning assets that provide a rate of return overthe cost of funds. The analysis of asset yieldsand cost of funds should include whether marketrates are paid for funds borrowed from theinterbank markets and the level and cost ofinteroffice funding activities. If market rates ofinterest are not charged on interoffice borrow-ings or paid on interoffice placements, net inter-est income can be materially distorted. Forexample, if a branch is a net user of head officeor interoffice funds, rates on intrabank borrow-ings could be adjusted upward or downward toincrease or reduce the branch’s cost of funds,which would flow through to net interest income.A branch that is a net provider of funds to thebank may be required to charge below marketrates to other offices of the FBO. This situationwould have an adverse affect on gross interestincome and apply downward pressure to the netinterest margin.

The level of nonperforming assets would alsoadversely affect net interest income. Nonper-forming and renegotiated credits either provideno income or provide a reduced rate of incometo the extent that the assets are no longerprofitable relative to the cost of funds and thecost of doing business.

Reserves

Regulatory agencies have long recognized thatan allowance for loan loss reserves is onlymeaningful for the bank as a whole and not on abranch by branch basis. Accordingly, branchesof FBOs are not required to establish separateloan loss reserves on the books of each branch,but may do so voluntarily, or to meet localrequirements. Provisions for loan loss reservesmay either be transferred to the branch from thehead or regional office, or may be directlycharged against the branch’s earnings. However,unlike at stand-alone operations that are sepa-

Income and Expense 3400.1

Branch and Agency Examination Manual September 1997Page 3

rately capitalized, concerns arising from inad-equate loan loss reserves are not key issues at abranch.

Other Income and Expenses

Examiners should analyze the composition, level,and trend of other income and expenses. Non-interest income would include trading commis-sions and fees, deposit service charges, andletter of credit fees, among other items. Nonin-terest expense includes personnel and occu-pancy expense, and other operating expensesthat arise from the normal activities of thebranch. An analysis of these components wouldbe especially valuable when evaluating a limitedpurpose branch or a branch that is sufferingoperating losses. Fees for intrabank servicesprovided or received from related entities shouldalso be reviewed. Earnings can be materiallydistorted if market rates are not charged forthese services.

Extraordinary Gains or Losses

Extraordinary gains or losses result from any-thing outside the normal operations of a branchand should be analyzed carefully for their effecton earnings. Generally, extraordinary gains orlosses result from the sale or disposal of assetsand because of accounting changes. Examiners

should note that ‘‘extraordinary’’ as used in thecontext of the examination report is not the sameas defined in U.S. generally accepted accountingprinciples.

Offshore Shell Branches

Earnings for offshore shell branches should bemaintained separately from those of the U.S.branch. As such, report comments should belimited to the income and expenses of the U.S.branch. Earnings for the offshore branch arefrequently commingled in the U.S. branch’smanagement reports. The U.S. branch mayabsorb the offshore shell branch’s indirectexpenses, such as personnel expenses, withoutcharging a fee. The significance of these indirectexpenses varies depending upon the relationshipof the U.S. branch to the offshore shell branch.However, because the allocation of these expensesare ultimately under the direction of head officemanagement, exception should not be taken tothis practice. Also, examiners, generally shouldnot question the tax implication to the U.S.branch if the branch and the offshore shellbranch file a combined federal income tax return.However, expenses between a branch and arelated U.S. banking subsidiary of the foreignbanking organization should be properly allo-cated and in accordance with applicable lawsand regulations.

3400.1 Income and Expense

September 1997 Branch and Agency Examination ManualPage 4

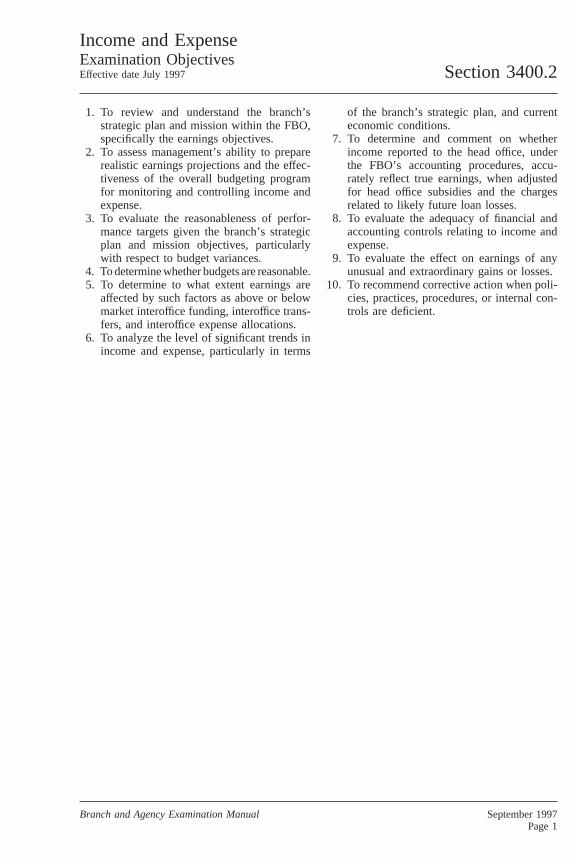

Income and ExpenseExamination ObjectivesEffective date July 1997 Section 3400.2

1. To review and understand the branch’sstrategic plan and mission within the FBO,specifically the earnings objectives.

2. To assess management’s ability to preparerealistic earnings projections and the effec-tiveness of the overall budgeting programfor monitoring and controlling income andexpense.

3. To evaluate the reasonableness of perfor-mance targets given the branch’s strategicplan and mission objectives, particularlywith respect to budget variances.

4. To determine whether budgets are reasonable.5. To determine to what extent earnings are

affected by such factors as above or belowmarket interoffice funding, interoffice trans-fers, and interoffice expense allocations.

6. To analyze the level of significant trends inincome and expense, particularly in terms

of the branch’s strategic plan, and currenteconomic conditions.

7. To determine and comment on whetherincome reported to the head office, underthe FBO’s accounting procedures, accu-rately reflect true earnings, when adjustedfor head office subsidies and the chargesrelated to likely future loan losses.

8. To evaluate the adequacy of financial andaccounting controls relating to income andexpense.

9. To evaluate the effect on earnings of anyunusual and extraordinary gains or losses.

10. To recommend corrective action when poli-cies, practices, procedures, or internal con-trols are deficient.

Branch and Agency Examination Manual September 1997Page 1

Income And ExpenseExamination ProceduresEffective date July 1997 Section 3400.3

1. Determine to what degree the branch is aprofit center. If it is a profit center, calculatethe net interest margin and review the trend.Consider the following:a. To what degree does the agency raise its

own funds and set its own cost of funds?b. How is the pricing of loans and funds

determined? Is it market driven or con-trolled by other factors?

c. Are transfer costs to affiliates reasonable,in relation to the services provided?

d. To what extent do transfer costs/benefitsaffect net earnings?

2. Determine if any significant changes haveoccurred in:a. The branch’s operations.b. Accounting practices in U.S. or home

country.c. The branch’s financial reporting.d. General business conditions in U.S. or

home country.e. Tax codes in the U.S. or home country.

3. Obtain current financial statements, internaloperating reports, interim financial state-ments, reports filed with the Federal Reserve,daily statements of assets and liabilities, andother available financial information. Lookfor the development or continuation ofadverse trends and other significant or unusualtrends or fluctuations. Primary considerationsshould include whether:a. Significant structural changes are occur-

ring in the branch that may affect theearnings stream.

b. The branch is making use of tax carry-backs or carryforwards.

c. Earnings are static or declining, as apercentage of total resources.

d. Income before securities gains and losses,is decreasing as a percentage of totalrevenues.

e. The ratio of operating expense to operat-ing revenue is increasing.

f. Income and expense trends are inconsistent.g. The spread between interest earned and

interest paid is decreasing.h. Loan losses are increasing.i. Provisions for loan losses, if applicable,

are sufficient to cover loan losses andwhether overall reserves at an adequatelevel.

j. There is evidence that sources of interestand other revenues have changed since theprior examination.

k. There are any differences between branchaccounting practices and U.S. regulatoryaccounting standards and generallyaccepted U.S. accounting principles.

4. Obtain and review planning procedures, profitplans, budgets, mid-and long-range financialplans, economic advisory reports, and anyrelated progress reports and:a. Compare actual results to budgeted

amounts.b. Determine the impact of specific goals

that have been set.c. Determine the frequency of planning

revisions.d. Determine how planning revisions are

triggered.e. Determine who initiates plan revisions.f. Determine whether explanations are

required for significant variations andwhether causes are ascertained to imple-ment corrective action.

g. Determine the sources of input for fore-casts, plans, and budgets.

5. Review ledger accounts for unusual entries.Examples of such items include:a. Significant deviations from the normal

amounts of recurring entries.b. Unusual debit entries in income accounts

or unusual credit entries in expenseaccounts.

c. Significant entries from an unusual source,such as a journal entry.

d. Significant entries in other income orother expense, which may indicate fees orservice losses on an off-balance-sheetactivity (i.e., financial advisory or under-writing services).

6. Investigate conditions of interest dis-closed by the procedures in the precedingsteps by:a. Discussing exceptions or questionable

findings with the examiner responsible forconducting those aspects of the examina-tion that are most closely related to theitem of interest to determine if a satisfac-tory explanation already has been obtained.

Branch and Agency Examination Manual September 1997Page 1

b. Reviewing copies of workpapers preparedby internal auditors or management thatexplain account fluctuations from priorperiods or from budgeted amounts.

c. Discussing unresolved items withmanagement.

d. Reviewing underlying supporting data andrecords, as necessary, to substantiateexplanations advanced by management.

e. Performing any other procedures consid-ered necessary to substantiate the authen-ticity of the explanations given.

f. Reaching a conclusion as to the reason-ableness of any explanations offered by

other examiners or management, anddeciding whether extensions of examina-tion or verification procedures arenecessary.

7. Review with officers and prepare, in appro-priate report format, listings of deficienciesin and deviations from policies, practices,procedures, internal controls, and adversetrends.

8. Prepare a complete set of workpapers tosupport examiner conclusions and discuss allmaterial findings with management.

3400.3 Income And Expense: Examination Procedures

September 1997 Branch and Agency Examination ManualPage 2

Management Information SystemsEffective date July 1997 Section 3410.1

Management information systems (MIS) shouldgather, interpret, and communicate informationregarding the branch’s business activities andtheir inherent risks. Accurate, informative, andtimely MIS are essential to the prudent opera-tion of any branch office. In fact, the examiner’sassessment of the quality of the MIS is animportant factor in the overall evaluation of therisk management process, which is discussed inthe ROCA Rating System section of this manual.

In the evaluation of MIS, examiners shoulddetermine the extent to which the risk manage-ment function monitors and reports the branch’srisk exposures to local and head office manage-ment.1 Risk exposure levels and other signifi-cant measures such as profit and loss statementsshould be reported to managers who supervisebut do not, themselves, have operational respon-sibilities in the area of activity. Frequent reportsshould be made as warranted by the activity andtype of risk. Reports to head office managementmay occur less frequently, but examiners shoulddetermine whether the frequency of reporting issufficient for head office to maintain properoversight over the branch’s activities.

The form and content of the MIS will relate tothe branch’s operations and organization, poli-cies and procedures, and management reportinglines. Examiners will find that the form ofbranch management information systems willvary substantially with no particular structureshown to be optimum. MIS, however, generallytake two forms: computing systems with busi-ness applications and management reporting.For branches with extensive lending or tradingoperations, a computerized system should be inplace. For branches with more limited opera-tions in terms of risk and size, an elaboratecomputerized system may not be cost effective.

Not all management information systems arefully integrated within the branch or within theFBO. Generally, this aspect should be evaluatedbased on the complexity and degree of risk inthe branch’s activities.

Examiners should expect to see varyingdegrees of manual intervention and should deter-mine whether the integrity of the data is pre-served through proper controls, which will fac-tor into the overall assessment of the branch’s

operational controls. The examiner should reviewand evaluate the sophistication and capability ofthe branch’s computer systems and software,which should be capable of supporting, process-ing, and monitoring the branch’s changing riskprofile. Generally, in evaluating the individualbranch management information system, theexaminer should focus on its overall effective-ness in monitoring the branch’s level of riskwithin established parameters rather than itsform.

Other considerations in evaluating the MISinclude:

• Whether reports are presented in a format thatis easily read and understood by seniormanagement;

• Whether the branch has personnel with suffi-cient expertise to maintain MIS;

• Whether reports are updated and customizedto reflect changes in the business environmentor management’s requirements;

• Whether an adequate reconcilement procedureis in place to ensure the integrity of datainputs; and

• Whether the system is independently auditedby internal and external personnel with suffi-cient expertise to perform a comprehensivereview of management reporting, financialapplications, and systems capacity.

Management reporting summarizes thebranch’s day-to-day operations, including riskexposure. Reports also serve to provide manage-ment with an overall view of business activityfor strategic planning. Reporting may be con-ducted via telephone, computer, correspon-dence, meetings, periodic management reports,audits, and examination reports. Examinersshould evaluate the reporting process to deter-mine whether it is sufficiently comprehensivefor sound decision-making both on a day-to-daylevel and for future planning. To the extent thatproblems in specific areas of the branch mayrelate to inaccurate or inadequate reporting, theexaminer also should review results and com-ments from other areas of the examination.

If the branch has extensive reporting require-ments, it is not necessary to review each report.Instead the examiner should summarize themonitoring process in each area, giving onlysuch information as is needed to justify theevaluation.

1. FBOs with multiple U.S. offices may establish an inter-mediate or regional U.S. reporting line. Such a reporting lineshould be evaluated to ensure that proper oversight by headoffice management is achieved.

Branch and Agency Examination Manual September 1997Page 1

Formal management reports will usually begenerated by control personnel within the branch,independent from line management. Where linemanagers have input, the senior managers shouldbe well aware of potential weaknesses in thedata provided. Risk reporting should be assessedand performed independently of line manage-ment to ensure objectivity and accuracy and

to prevent manipulation or fraud. For branchesoperating in a less automated environment, reportpreparation should be evaluated in terms oftimeliness and data accuracy. Cross checkingand sign off by the report preparer and reviewerwith appropriate authority promote a properoperational controls environment.

3410.1 Management Information Systems

September 1997 Branch and Agency Examination ManualPage 2

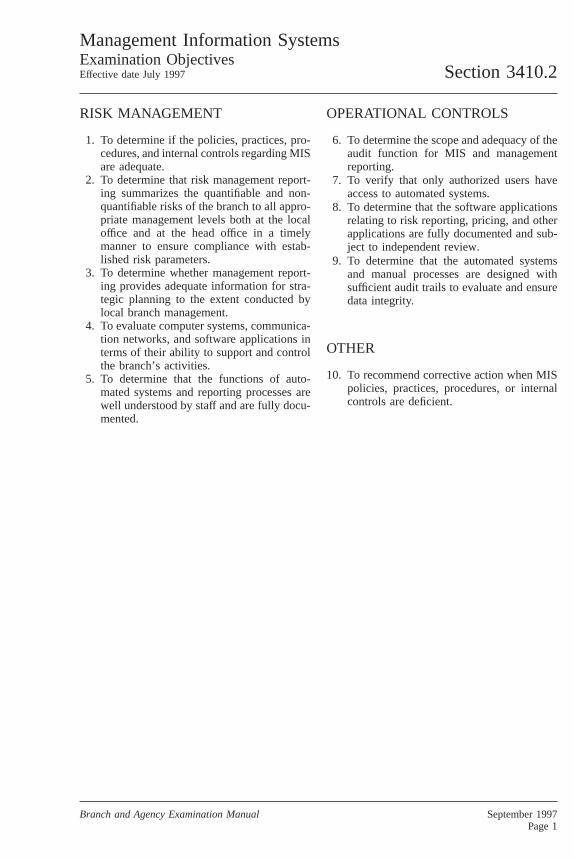

Management Information SystemsExamination ObjectivesEffective date July 1997 Section 3410.2

RISK MANAGEMENT

1. To determine if the policies, practices, pro-cedures, and internal controls regarding MISare adequate.

2. To determine that risk management report-ing summarizes the quantifiable and non-quantifiable risks of the branch to all appro-priate management levels both at the localoffice and at the head office in a timelymanner to ensure compliance with estab-lished risk parameters.

3. To determine whether management report-ing provides adequate information for stra-tegic planning to the extent conducted bylocal branch management.

4. To evaluate computer systems, communica-tion networks, and software applications interms of their ability to support and controlthe branch’s activities.

5. To determine that the functions of auto-mated systems and reporting processes arewell understood by staff and are fully docu-mented.

OPERATIONAL CONTROLS

6. To determine the scope and adequacy of theaudit function for MIS and managementreporting.

7. To verify that only authorized users haveaccess to automated systems.

8. To determine that the software applicationsrelating to risk reporting, pricing, and otherapplications are fully documented and sub-ject to independent review.

9. To determine that the automated systemsand manual processes are designed withsufficient audit trails to evaluate and ensuredata integrity.

OTHER

10. To recommend corrective action when MISpolicies, practices, procedures, or internalcontrols are deficient.

Branch and Agency Examination Manual September 1997Page 1

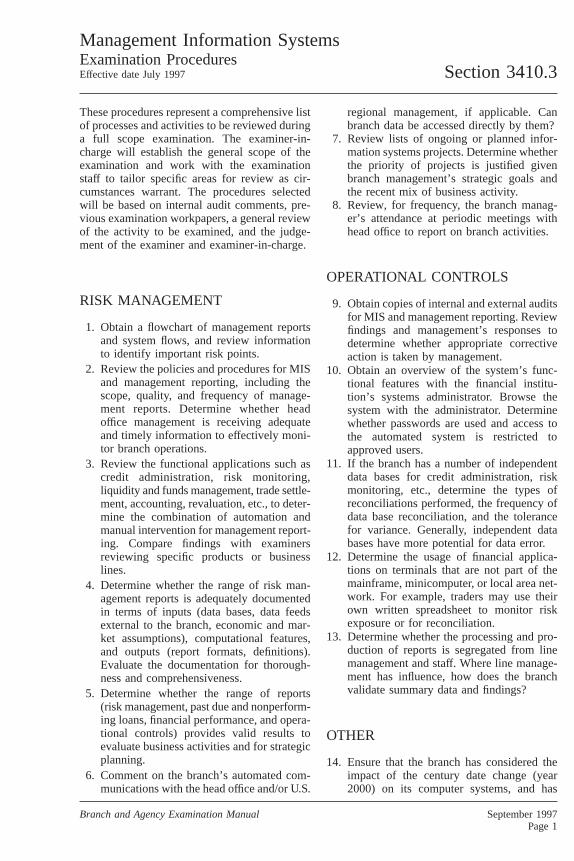

Management Information SystemsExamination ProceduresEffective date July 1997 Section 3410.3

These procedures represent a comprehensive listof processes and activities to be reviewed duringa full scope examination. The examiner-in-charge will establish the general scope of theexamination and work with the examinationstaff to tailor specific areas for review as cir-cumstances warrant. The procedures selectedwill be based on internal audit comments, pre-vious examination workpapers, a general reviewof the activity to be examined, and the judge-ment of the examiner and examiner-in-charge.

RISK MANAGEMENT

1. Obtain a flowchart of management reportsand system flows, and review informationto identify important risk points.

2. Review the policies and procedures for MISand management reporting, including thescope, quality, and frequency of manage-ment reports. Determine whether headoffice management is receiving adequateand timely information to effectively moni-tor branch operations.

3. Review the functional applications such ascredit administration, risk monitoring,liquidity and funds management, trade settle-ment, accounting, revaluation, etc., to deter-mine the combination of automation andmanual intervention for management report-ing. Compare findings with examinersreviewing specific products or businesslines.

4. Determine whether the range of risk man-agement reports is adequately documentedin terms of inputs (data bases, data feedsexternal to the branch, economic and mar-ket assumptions), computational features,and outputs (report formats, definitions).Evaluate the documentation for thorough-ness and comprehensiveness.

5. Determine whether the range of reports(risk management, past due and nonperform-ing loans, financial performance, and opera-tional controls) provides valid results toevaluate business activities and for strategicplanning.

6. Comment on the branch’s automated com-munications with the head office and/or U.S.

regional management, if applicable. Canbranch data be accessed directly by them?

7. Review lists of ongoing or planned infor-mation systems projects. Determine whetherthe priority of projects is justified givenbranch management’s strategic goals andthe recent mix of business activity.

8. Review, for frequency, the branch manag-er’s attendance at periodic meetings withhead office to report on branch activities.

OPERATIONAL CONTROLS

9. Obtain copies of internal and external auditsfor MIS and management reporting. Reviewfindings and management’s responses todetermine whether appropriate correctiveaction is taken by management.

10. Obtain an overview of the system’s func-tional features with the financial institu-tion’s systems administrator. Browse thesystem with the administrator. Determinewhether passwords are used and access tothe automated system is restricted toapproved users.

11. If the branch has a number of independentdata bases for credit administration, riskmonitoring, etc., determine the types ofreconciliations performed, the frequency ofdata base reconciliation, and the tolerancefor variance. Generally, independent databases have more potential for data error.

12. Determine the usage of financial applica-tions on terminals that are not part of themainframe, minicomputer, or local area net-work. For example, traders may use theirown written spreadsheet to monitor riskexposure or for reconciliation.

13. Determine whether the processing and pro-duction of reports is segregated from linemanagement and staff. Where line manage-ment has influence, how does the branchvalidate summary data and findings?

OTHER

14. Ensure that the branch has considered theimpact of the century date change (year2000) on its computer systems, and has

Branch and Agency Examination Manual September 1997Page 1

taken steps to correct any problems. Deter-mine the extent of management’s:a. awareness and due diligenceb. risk assessmentc. solution implementation and testingd. contingency planning

15. Recommend corrective action when poli-cies, practices, procedures, internal controlsor MIS are deficient.

3410.3 Management Information Systems: Examination Procedures

September 1997 Branch and Agency Examination ManualPage 2

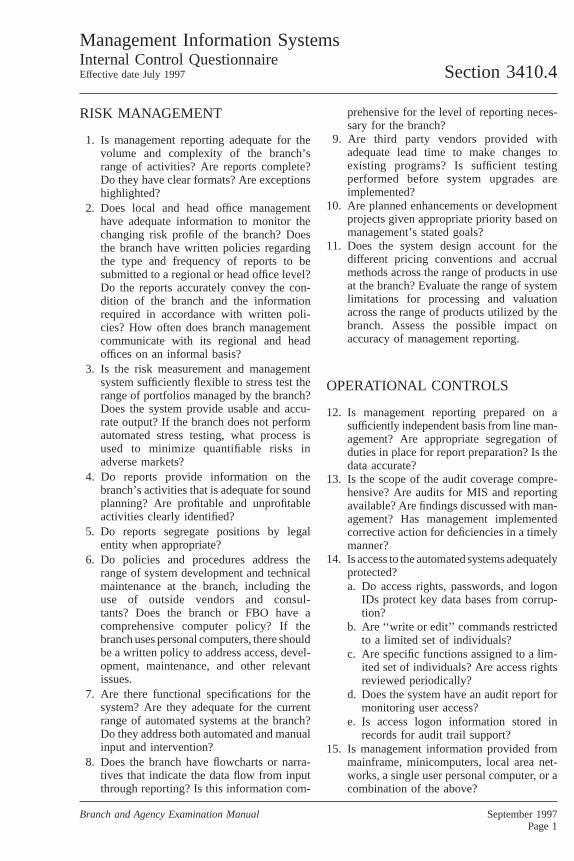

Management Information SystemsInternal Control QuestionnaireEffective date July 1997 Section 3410.4

RISK MANAGEMENT

1. Is management reporting adequate for thevolume and complexity of the branch’srange of activities? Are reports complete?Do they have clear formats? Are exceptionshighlighted?

2. Does local and head office managementhave adequate information to monitor thechanging risk profile of the branch? Doesthe branch have written policies regardingthe type and frequency of reports to besubmitted to a regional or head office level?Do the reports accurately convey the con-dition of the branch and the informationrequired in accordance with written poli-cies? How often does branch managementcommunicate with its regional and headoffices on an informal basis?

3. Is the risk measurement and managementsystem sufficiently flexible to stress test therange of portfolios managed by the branch?Does the system provide usable and accu-rate output? If the branch does not performautomated stress testing, what process isused to minimize quantifiable risks inadverse markets?

4. Do reports provide information on thebranch’s activities that is adequate for soundplanning? Are profitable and unprofitableactivities clearly identified?

5. Do reports segregate positions by legalentity when appropriate?

6. Do policies and procedures address therange of system development and technicalmaintenance at the branch, including theuse of outside vendors and consul-tants? Does the branch or FBO have acomprehensive computer policy? If thebranch uses personal computers, there shouldbe a written policy to address access, devel-opment, maintenance, and other relevantissues.

7. Are there functional specifications for thesystem? Are they adequate for the currentrange of automated systems at the branch?Do they address both automated and manualinput and intervention?

8. Does the branch have flowcharts or narra-tives that indicate the data flow from inputthrough reporting? Is this information com-

prehensive for the level of reporting neces-sary for the branch?

9. Are third party vendors provided withadequate lead time to make changes toexisting programs? Is sufficient testingperformed before system upgrades areimplemented?

10. Are planned enhancements or developmentprojects given appropriate priority based onmanagement’s stated goals?

11. Does the system design account for thedifferent pricing conventions and accrualmethods across the range of products in useat the branch? Evaluate the range of systemlimitations for processing and valuationacross the range of products utilized by thebranch. Assess the possible impact onaccuracy of management reporting.

OPERATIONAL CONTROLS

12. Is management reporting prepared on asufficiently independent basis from line man-agement? Are appropriate segregation ofduties in place for report preparation? Is thedata accurate?

13. Is the scope of the audit coverage compre-hensive? Are audits for MIS and reportingavailable? Are findings discussed with man-agement? Has management implementedcorrective action for deficiencies in a timelymanner?

14. Is access to the automated systems adequatelyprotected?a. Do access rights, passwords, and logon

IDs protect key data bases from corrup-tion?

b. Are ‘‘write or edit’’ commands restrictedto a limited set of individuals?

c. Are specific functions assigned to a lim-ited set of individuals? Are access rightsreviewed periodically?

d. Does the system have an audit report formonitoring user access?

e. Is access logon information stored inrecords for audit trail support?

15. Is management information provided frommainframe, minicomputers, local area net-works, a single user personal computer, or acombination of the above?

Branch and Agency Examination Manual September 1997Page 1

16. Identify the key data bases used for therange of management reports.a. Are direct electronic feeds from external

services, such as Reuters, Telerate, andBloomberg employed? How are incom-plete data feeds identified? Can marketdata be overridden by users? How doesthe branch ensure the data integrity ofdata feeds or manually input rates, yields,or prices from market sources?

b. Are standard instructions set within theautomated systems? Can these be over-ridden? Under what circumstances?

c. For merging and combining data bases,how does the branch ensure accurateoutput?

d. What periodic reconciliations are per-formed to ensure data integrity? Are

reconciliation personnel sufficientlyfamiliar with the information to identify‘‘contaminated’’ data?

17. Is the branch’s computer system capable ofhandling year 2000 calculations?

CONCLUSION

18. Is the information covered by this ICQadequate for evaluating internal controls inthis area? If not, indicate any additionalexamination procedures deemed necessary.

19. Based on the information gathered, evaluateinternal controls in this area (i.e. strong,satisfactory, fair, marginal, unsatisfactory).

3410.4 Management Information Systems: Internal Control Questionnaire

September 1997 Branch and Agency Examination ManualPage 2

Other Assets and Other LiabilitiesEffective date July 1997 Section 3420.1

OTHER ASSETS

The term ‘‘other assets,’’ as used in this section,includes all balance sheet asset accounts notcovered specifically in other areas of the exami-nation. Such accounts often may be quite insig-nificant to the overall size of the branch. How-ever, significant subquality assets may bediscovered in accounts of some branches lack-ing proper internal controls and procedures.

Types of Accounts

Types of other assets frequently found inbranches include the various temporary holdingaccounts such as suspense, teller, transit, andbookkeeping differences having debit balances.Those accounts should be used only for tempo-rary recording, until the offsetting entry isreceived or fully identified and posted to theappropriate account. Branches will also havemore permanent accounts recorded in otherassets such as premises and furniture, lease-hold improvements, purchased computer soft-ware, and deferred payment letters of credit.Nothing should be allowed to remain in thetemporary holding accounts (‘‘differenceaccounts’’) for any significant length of time,usually no more than a few business days.Branches should have written procedures toensure that difference accounts are reconciledand closed out on a timely basis. In any event,all difference accounts should be closed out atleast monthly.

General categories of other assets common tobranches on the accrual system are prepaidexpenses and income earned not collected.Prepaid expenses represent cash outlay for goodsand services, the benefits of which will berealized in future periods. Income earned andnot collected results from the differences betweenaccrual and cash-basis accounting.

There are an unlimited number of accounttitles that could be included in the other assetscategory, from bond coupons to art objects,antiques, and coin and bullion. The examinermust design specific procedures for review andtesting to fit the particular account and situationand must document the scope of the review inthe workpapers.

Scope of other assets review

Examiners assigned to review other assets mustobtain a detailed breakdown of such accounts,with a description of each account and the dateeach item was posted. Certain accounts, such asOther Real Estate Owned, may be reviewed byexaminers assigned to other areas of the branch.Refer to Section 3090 for information on otherreal estate owned. The remaining accountsshould be reviewed and evaluated by examinersassigned to this section.

The major factor in deciding which accountsare to be reviewed is materiality; however, evenaccounts with small balances may require atten-tion. Net balance accounts must be grossed up.The examiner should then evaluate whether toanalyze the nature and quality of each indivi-dual item based upon its impact on the overallsoundness or risk standing of the branch. In thisregard, it is important that the examiner verifythe existence of the asset, the proper valuation ofthe asset, the adequacy of the accounting anddisposition controls, and the quality of theasset.

An examiner should verify the existence ofthe assets selected by ensuring adequate support-ing documentation. The examiner should alsoverify that ownership of the asset rests with thebranch. The date the asset was acquired or firstposted also is important. Temporary accountssuch as suspense, should be cleared of staleitems.

Proper valuation and reporting of other assetaccounts is another potential area of concern forthe examiner. Assets are generally acquiredthrough purchase, trade, repossession, prepay-ment of expenses, or accrual of income. Gener-ally, assets purchased, traded, or repossessed aretransferred at their fair market value. Prepaidexpenses and income accrued are booked atcost. An examiner should be particularly alert inidentifying those assets that lose value over timeto ensure that they are appropriately depreciatedor amortized. All intangible assets should beregularly amortized, and management shouldhave a system in place to confirm the valuationof the remaining book balance of the intangibleassets. The examiner should ensure that thebook balance of key personnel life insurancepolicies owned by the branch value the surren-der charge, if any.

Branch and Agency Examination Manual September 1997Page 1

The examiner should assess the quality of theasset. Refer to Section 6010.1, Asset QualityClassifications, for information on the classifi-cation of assets.

The examiner should ensure that the controlsconcerning other assets protect the branch’sownership rights, that the accounts are properlyvalued and accurately reported, and that activityis monitored regularly by management. A branchwith good controls and review procedures willperiodically charge off all uncollectible orunreconcilable items. However, the examinermust frequently go beyond the general ledgercontrol accounts and scan the underlying sub-sidiary ledgers to determine that posting errorsand/or the common practice of netting certainaccounts against each other do not cause signifi-cant balances to go unnoticed because of thelack of proper detail.

OTHER LIABILITIES

‘‘Other liabilities,’’ as used in this section, includeall balance sheet liability accounts not coveredin other specific liability categories or in otherareas of the examination. The accounts oftenmay be quite insignificant to the overall size ofa branch. In some branches, specific accountsare established for control purposes and appearon the balance sheet as other liabilities. Forreporting, however, these accounts must beassigned to specific liability categories or nettedfrom related asset categories, as appropriate.

Types of Accounts

A general category of other liabilities commonto branches using accrual systems is expensesaccrued and unpaid. These accounts representperiodic charges to income based on anticipatedor contractual payments of funds to be made ata later date. The accounts include items such asinterest on deposits, taxes, and expenses incurredin the normal course of business. There shouldbe a correlation between the amount beingaccrued on a daily or monthly basis and theamount due on the stated or anticipated paymentdate.

The examiner should review other liabilityaccounts to determine that accounts, such asdeferred taxes (credit balance), are being prop-

erly recognized. This review should also deter-mine that matters, such as pending tax litigation,equipment contracts, and accounts payable, havebeen recorded properly and are being dischargedin accordance with their terms and requirements.

Various miscellaneous liabilities may be foundwithin the accounts, such as deferred credits,suspense, and other titles denoting pending sta-tus. The number of possible items that could beincluded are unlimited and the accounts shouldbe reviewed to determine that they are usedproperly and that all such items are clearing inthe normal course of business. Because of thevariety of such accounts, the examiner mustdevelop specific examination procedures to fitthe particular account and situation.

Scope of other liabilities review

Examiners assigned to review other liabilitiesare responsible for obtaining the branch’s break-down of those accounts and determining whenthey are to be reviewed under other sections ofthis manual. They must ensure that examiners incharge of those other sections receive the nec-essary information. The remaining accountsshould be reviewed and evaluated by examinersassigned to this section.

The major emphasis in examining this areashould be on the adequacy of the controls andprocedures employed by the branch in promptlyrecording the proper amount of liability. With-out proper management attention, these accountsmay be misstated, either advertently or inadvert-ently. For instance, fraudulent entries in sus-pense or interbranch accounts could be rolledover every other day to avoid stale dates causingshortages to be effectively concealed for indefi-nite periods of time.

Like other assets, other liability accounts withsmall balances may be significant and net bal-ance accounts should be grossed up. Scanningaccount balances may disclose a recorded liabil-ity but it does not aid in determining whetherliability figures are accurate. Therefore, it isimportant to review information obtained frombranch counsel handling litigation because thesedocuments might reveal a major understatementof liabilities. Determining accurate balances inother liability accounts requires an in-depthreview of source documents or other accountsfrom which the liability arose.

3420.1 Other Assets and Other Liabilities

September 1997 Branch and Agency Examination ManualPage 2

Other Assets and Other LiabilitiesExamination ObjectivesEffective date July 1997 Section 3420.2

1. To determine if policies, practices, proce-dures, and internal controls regarding otherassets and other liabilities are adequate.

2. To determine that branch officers andemployees are operating in conformance withestablished guidelines.

3. To evaluate the validity and quality of allother assets.

4. To determine that other liabilities are prop-erly recorded.

5. To evaluate the scope and adequacy of theaudit function.

6. To determine compliance with laws andregulations.

7. To recommend corrective action when poli-cies, practices, procedures, or internal con-trols are deficient or when violations of lawsor regulations have been noted.

Branch and Agency Examination Manual September 1997Page 1

Other Assets and Other LiabilitiesExamination ProceduresEffective date July 1997 Section 3420.3

1. Complete or update the Internal Con-trol Questionnaire, if selected forimplementation.

2. Based on the evaluation of internal controlsand the work performed by internal/externalauditors, determine the scope of theexamination.

3. Test for compliance with policies, practices,procedures, and internal controls in conjunc-tion with performing the remaining exami-nation procedures. Obtain a listing of anydeficiencies noted in the latest review byinternal/external auditors from the examinerassigned to Internal and External Audits,and determine if appropriate correctionshave been made.

4. Obtain a trial balance of other asset andother liability accounts and:a. Verify or reconcile balances to depart-

mental controls and general ledger.b. Review reconciling items for

reasonableness.5. Scan the trial balances for:

a. Obvious misclassifications of accountsand, if any are noted, discuss reclassifi-cation with appropriate branch personneland furnish a list to appropriate examin-ing personnel.

b. Large, old, or unusual items and, if anyare noted, perform additional proceduresas deemed appropriate being certain toappraise the quality of other assets.

c. Other asset items that represent advancesto related organizations, officers, employ-ees or their interests, and, if any arenoted inform the examiner assigned toCredit Risk Management.

6. Determine that amortizing other assetaccounts are being amortized over a reason-able period relative to their economic life.

7. If the branch has outstanding customerliabilities under deferred payment letters ofcredit, obtain and forward a list of namesand amounts to the examiner assigned toCredit Risk Management.

8. Review the balance of any other liabilitiesowed to officers or their interests and inves-tigate, by examining applicable supportingdocumentation, whether they have been usedto record unjustified amounts or amountsfor items unrelated to branch operations.

9. Develop and note in the workpapers anyspecial programs considered necessary toproperly analyze any remaining other assetsor other liabilities account.

10. Test for compliance with applicable federaland state laws and regulations.

11. For other asset items that are determined tobe stale, abandoned, uncollectible, or car-ried in excess of estimated values and forother liability items that are determined tobe improperly stated, request managementto make the appropriate entries on thebranch’s books after consulting with theexaminer-in-charge.

12. Prepare in appropriate report form and dis-cuss with appropriate officer(s):a. Violations of laws and regulations.b. Criticized other assets.c. The adequacy of written policies relating

to other assets and other liabilities.d. Recommended corrective action when

policies, practices, or procedures aredeficient.

13. Update the workpapers with any informa-tion that will facilitate future examinations.

Branch and Agency Examination Manual September 1997Page 1

Other Assets and Other LiabilitiesInternal Control QuestionnaireEffective date July 1997 Section 3420.4

Review the branch’s internal controls, policies,practices, and procedures concerning other assetsand other liabilities. The branch’s systems shouldbe documented in a complete and concise man-ner and should include, where appropriate, nar-rative descriptions, flow charts, copies of formsused, and other pertinent information.

1. Has the branch formulated written policiesand procedures governing both other assetand other liability accounts?

2. Does the branch maintain subsidiary recordsand supporting documentation of items com-prising other assets and other liabilities?

3. Is the preparation of entries and posting ofsubsidiary other asset and other liabilityrecords performed or tested by persons whodo not also have direct control, either physi-cal or accounting, of the supporting data orrelated assets?

4. Are the subsidiary records balanced at leastmonthly to the appropriate general ledgeraccounts by persons who do not also havedirect control, either physical or accounting,of the supporting data or related assets?

5. Are the items included in suspense accountsaged and regularly reviewed for proprietyby responsible personnel?

6. Are receivables reviewed at least monthlyfor collectibility by someone other than theoriginator of the entry?

7. Is approval required to pay credit balancesin receivable accounts?

8. Do credit entries to receivables accounts,other than payments, require the approvalof an officer independent of the entrypreparation?

9. Does charge off of a nonamortizing otherasset initiate review of the item by a personnot connected with entry authorization orposting?

10. Are invoices and bills proved for accuracy,prior to payment? Who has the authority topay the invoices and up to what amount?

11. Are all payroll tax liabilities verified toappropriate tax returns and reviewed by anofficer to ensure accuracy?

CONCLUSION

12. Is the information covered by this ICQadequate for evaluating internal controls inthis area? If not, indicate any additionalexamination procedures deemed necessary.

13. Based on the information gathered, evaluateinternal controls in this area (i.e. strong,satisfactory, fair, marginal, unsatisfactory).

Branch and Agency Examination Manual September 1997Page 1

Other Assets and Other LiabilitiesAudit GuidelinesEffective date July 1997 Section 3420.5

1. Obtain or prepare detailed lists of other assetsand other liabilities, including a breakdownof subsidiary ledgers.

2. Within each category of other assets, use anappropriate sampling technique to select spe-cific items and:a. Where appropriate, verify the original bal-

ance of the item from an invoice or othersupporting document.

b. Examine documentation for additions toany given item since the previous audit.

c. Where amortization is applied to a givenitem, review the computations for theperiod since the previous audit to deter-mine mathematical accuracy and the rea-sonableness of estimated life.

d. Determine the reasonableness of the cur-rent balance by reviewing the remainingestimated life, collectibility, etc.

e. Prepare any special programs considerednecessary to properly analyze and testspecific accounts.

3. Determine that interbranch and affiliate trans-actions clear in the normal course of businessby actually reviewing the entries to theaccount for several days and examining thedebit and credit tickets. Special attentionshould be given to entry dates, authorizinginitials, and validity or reasonableness of theitem.

4. If a branch is on an accrual basis ofaccounting:a. Review the branch’s system of recording

liabilities for interest, taxes, and otherexpenses.

b. Review the balance of interest accrued tooutstanding interest-bearing liabilities forreasonableness.

c. Review the balance of the reserve for bothcurrent and deferred taxes for reasonable-ness by examining the worksheets andcomputations.

d. Review the reasonableness and complete-ness of the balance reflected for reservesfor other expenses.

5. Within each general category of other liabili-ties, use an appropriate sampling techniqueto select specific items for further review. Foreach item selected, determine that the bal-ance is reasonably stated by examining sup-porting documentation.

6. Review accounts not sampled, for items thatappear unusual in nature or amount andexamine supporting documentation.

7. Using an appropriate sampling technique,select expense checks issued since the exami-nation date and:a. Determine whether the expense was

incurred before or after the examinationdate by examining the vendor’s invoice orother supporting documentation.

b. For expenses incurred prior to the exami-nation, trace the amount to the detail listof other liabilities.

c. Discuss with appropriate branch officials,any significant items incurred prior to andrecorded after the examination date.

Branch and Agency Examination Manual September 1997Page 1

Private BankingEffective date July 1997 Section 3430.1

This section describes the activities of privatebanking services and provides insight intoadequate safeguards. The portions concerninghold mail, dormant accounts, and overdrafts arealso applicable to the Deposit Accounts sectionof this manual because they can affect all typesof accounts and account holders.

Private banking departments may offer a widearray of products and services to their clients,including, but not limited to, trust services (byreferral to or in association with an affiliatedtrust entity), investment advisory services, for-eign exchange trading, lending, letters of credit,bill paying, credit cards, and deposit services.Private banking generally markets its services tohigh net worth individuals and, if the client hasa business, may entice them to develop a cor-porate banking relationship. Private bankingaccounts may be opened in the name of anindividual, a commercial business, a trust, or aprivate investment corporation (PIC) registeredin offshore havens.

The relationship between the private bankerand the client is carefully cultivated by thebanker; therefore, it is common for clients tofollow private bankers to different financialinstitutions because of the level of trust that hasbeen developed. As a result, private bankingclients may delegate a significant amount ofdiscretionary financial authority to private bank-ers. Some private banking departments havesmall staffs that make the segregation of dutiesnormally found in banking activities difficult tomaintain. This combination of trust in the pri-vate banker and difficulty in segregating dutiesexposes private banking activities to possibleaccount manipulation. As a result, the privatebanking area must have compensating internalcontrols to ensure proper supervision and safe-guarding of client accounts.

Examiners should understand the nature andscope of the private banking activities. Addition-ally, examiners should carefully evaluate thepolicies, procedures, internal controls, creditreviews, and audits surrounding private bankingto ensure that internal controls exist to detectfraud and prevent losses to both the branchand/or customers. Internal and external auditsshould provide an excellent source of informa-tion concerning the adequacy of policies, proce-dures and controls of private banking. The lackof an internal audit of the private banking

department should be viewed as a serious weak-ness and criticized in the examination report.

REVIEW OF DEPOSIT ACCOUNTSAND REVIEW OF ACCOUNTDOCUMENTATION

Private banks often assist clients in formingshell corporations of PICs. PICs are generallyincorporated in bank secrecy (tax haven) coun-tries such as the Cayman Islands, Bahamas,British Virgin Islands, and Netherlands Antillesto maintain the clients’ confidentiality, and/orfor tax or trust related reasons. The beneficialowners of the shell corporations are typicallyforeign residents.

Reviewing the list of accounts for privatebanking clients may provide insight into someof the activities conducted by private banking.For instance, the review may reveal that thebranch allows accounts that disguise the trueidentity of the client through the use of fictitiousor code name accounts, accounts in the name ofa PIC, or blind/numbered trust accounts. Man-agement must be able to provide documentedfiles on the identity of the ultimate accountholder and details on the account relationship.Examiners should carefully scrutinize the rea-sons for these types of accounts and ensure thatthey do not compromise the institution’s com-pliance with the Financial Recordkeeping andReporting regulations, and the Federal Reserve’s‘‘Know Your Customer’’ guidelines.

Reviewing account documentation shouldreveal that the branch has an adequate qualitycontrol program in place for opening accountsthat includes a follow-up system for obtainingmissing or date-sensitive documents. Addition-ally, account documentation reviews should showhow the branch documents its client relation-ships and implements its "Know Your Cus-tomer" policy.

An integral part of an effective ‘‘Know YourCustomer’’ policy is a comprehensive knowl-edge of both the customer and the types oftransactions carried out by the customer. As ageneral rule, a financial institution should neverestablish a business relationship until the iden-tity of a potential customer is satisfactorilyverified. Accordingly, the ’’Know Your Cus-tomer’’ policy should clearly identify the type ofdocumentation needed before a relationship can

Branch and Agency Examination Manual September 1997Page 1

be formerly established. If a potential customerrefuses to produce any of the requested infor-mation, the relationship should not be estab-lished. Likewise, if requested follow-up infor-mation is not forthcoming, any relationshipalready begun should be terminated.

The purpose of the business relationshipshould also be identified. Incoming client fundsmay be used for various purposes such asestablishing deposits, funding investments,securitizing loans, paying bills, or establishingPICs or trusts. The ‘‘Know Your Customer’’procedures established by the institution allowfor the collection of sufficient information todevelop a ‘‘transaction profile’’ for each cus-tomer. The primary objective of such proceduresis to enable the institution to predict with rela-tive certainty the types of transactions in whicha customer is likely to engage. Internal systemsshould then be developed for monitoring trans-actions which are inconsistent with the custom-er’s transaction profile. The level, detail anddocumentation of ‘‘Know Your Customer’’information should be greater for customerswith larger balances and transaction volumes.(Examiners may refer to the Federal Reserve’sBank Secrecy Act Manual and other similarexamination material for more information).

HOLD MAIL

Private banking clients and in particular, inter-national private banking clients, are often pro-vided hold mail service. Hold mail clients electto have bank statements and other documentsmaintained at the institution rather than mailedto their home address. In most cases, this serviceis provided because the client’s country ofresidence has an unreliable or limited postalsystem or for security reasons. Controls overhold mail accounts should be carefully reviewedbecause the clients do not receive their state-ments promptly, and therefore, relinquished theirability to detect unauthorized transactions in atimely manner. One of the key controls thatshould be part of any hold mail operation is tohave a process for ensuring that the back officereceives customer account statements.

DORMANT ACCOUNTS

Accounts that are inactive for a prolonged periodof time could be subject to manipulation and

abuse by branch personnel. Examiners shouldcarefully review the policies, procedures, andcontrols over dormant accounts. Effective con-trols over dormant accounts should include:

• A specified period of time between the lastcustomer-originated activity and its classifica-tion as dormant.

• Segregation of signature cards for dormantaccounts.

• Blocking of the account so that entries cannotbe posted to the account without review bymore than one member of senior managementoutside of private banking.

OVERDRAFTS/EXTENSIONS OFCREDIT

Private banking clients often pledge their assets,including cash, mortgages, marketable securi-ties, land, and/or buildings to securitize loans.Loan proceeds are used for a variety of pur-poses, including, but not limited to, recapitaliz-ing the client’s business(s) or providing workingcapital. Branch management should demon-strate understanding of each specialty businessand should know what would affect the value ofany collateral or business being financed. Loansto private banking clients may not be of suffi-cient size to be covered during the review ofasset quality. However, it is important to ensurethat a sampling of private banking loans andcontingent liabilities are reviewed. In manyinstances, loans and other credit-related activi-ties for private banking clients are collateralizedby cash or marketable securities; therefore, creditunderwriting standards and procedures may notbe as complete or stringent as prudent bankingpractice would dictate.

Loans backed by cash or negotiable collateralare common in private banking. An extension ofcredit based solely on collateral, even if thecollateral is cash, does not guarantee repayment.There are at least three ways in which a branchcan lose its collateral: forfeiture through theseizure of assets by a government agency; theftor manipulation by a dishonest employee; anderrors such as the inadvertent release of collat-eral by an employee. While the collateralenhances the branch’s position, it should not beused as a substitute for regular credit analysesand prudent lending practices unless the branchmakes a separate determination of the creditwor-

3430.1 Private Banking

September 1997 Branch and Agency Examination ManualPage 2

thiness of the client. A client may be consideredcreditworthy if the branch performs its duediligence by adequately documenting that itsclient’s funds were derived from legitimatemeans and can verify that the use of the loanproceeds are for legitimate purposes.

Examiners should ensure that policies andprocedures for extending credit to private bank-ing clients are in place and are being followed.The branch’s credit review function should alsosample private banking loans and ensure com-pliance with established policies. Loan filesshould contain sufficient information to assessthe quality of the credit, the proper approvals,and the purpose and source of repayment. Dur-ing the review of private banking loans, exam-iners should ensure that loan files include docu-mented background information on the client’ssource of wealth and occupation, the purpose ofthe loan, and the source of repayment (otherthan collateral). Ambiguous purposes such aspersonal investments or working capital, andliquidation of cash collateral for source ofrepayment, are generally not acceptable. Weak-nesses in this area could result in noncompliancewith the Financial Recordkeeping and Reportingregulations (See the Federal Reserve’s BankSecrecy Act Manual and other similar examina-tion material for details).

Loans secured by cash or marketable securi-ties should have files containing pledge/assignment documents, which serve to perfectthe branch’s security interest. In addition, pro-cedures should be implemented to monitor anddocument the value of the collateral. Documen-tary exceptions should be listed as technicalexceptions.

Documented financial statements that supportcredit decisions and guarantees may be present.Financial statements should never be waivedmerely because the loan is secured by cash ormarketable securities.

BILL PAYING SERVICES

Private banking departments often provide billpaying services for their clients. If this service isprovided, examiners should ensure that an agree-ment between the customer and the client existsfor this service and that it has been reviewed bylegal counsel. Typically, a client might requestthat the branch debit a deposit account for creditcard bills, utilities, rent, mortgage payments, or

other monthly consumer charges. Policies, pro-cedures, and controls over this area should bereviewed to ensure that they are adequate andprotect the customer and the branch from fraudor abuse.

SALE OF NON-DEPOSITINVESTMENT PRODUCTS

Private banking departments are increasinglyoffering investment products to their clientsunder discretionary or nondiscretionary arrange-ments. In addition, private banking departmentsmay also offer treasury services, portfolio man-agement, financial planning advice and offshoreservices.

Although fiduciary and agency activities arecircumscribed by formal trust laws, clients maydelegate varying degrees of authority (discre-tionary versus nondiscretionary) over assetsunder management to the institution. In allcases, the terms under which the assets aremanaged are fully described in a formal agree-ment, also known as the ‘‘governing instru-ment’’, between the customer and the institu-tion. The agreement should address the dutiesthat a fiduciary is obliged to perform for itsbeneficiaries or customers, keeping the assets ofthe customers separate and distinct from thoseof the branch, and avoiding any circumstancesthat may conflict with the branch’s fiduciaryobligations. A client’s portfolio may consist of amixture of instruments bearing varying degreesof market and credit risk which should beappropriate to the client. Assets under manage-ment may include deposits, securities, loans,items held in safekeeping, and other products.

Examiners should determine, through discus-sions with private banking personnel, the typesof products being offered to clients. Clients maybe offered a wide range of products. Examinersshould also determine the level of discretionaryauthority delegated to private banking personnelin the management of these activities and thedocumentation required from customers toexecute transactions on their behalf. Privatebanking personnel should not be able to executetransactions on behalf of their clients withoutproper documentation from clients or indepen-dent verification of client instructions.

On February 16, 1994, federal and thriftregulatory agencies released a joint statement on

Private Banking 3430.1

Branch and Agency Examination Manual September 1997Page 3

retail sales of mutual fund and other non-depositinvestment products by federally insured insti-tutions. It reaffirms the agencies belief that retailcustomers must be fully informed about risksassociated with non-deposit investment products.Branches recommending or selling such prod-ucts should ensure that customers are fullyinformed that the products: (1) are not FDIC-insured; (2) are not deposits or other obligationsof the institution and are not guaranteed by theinstitution; and (3) involve investment risks,including possible loss of principal. Examinersshould refer to this statement for further guid-ance. While this statement addresses insured

branches, the premises in this statement areapplicable to uninsured branches.

Examiners should ensure that the branch hasagreements with customers covering the termsof any asset management or other servicesprovided, and that the agreements are on file. Anevaluation of private banking personnel’s abilityand competence to provide the services offeredshould also be assessed. If the branch executestransactions or performs back-office functions,the examiner should refer to the SecuritiesActivities section of this manual for furtherguidance.

3430.1 Private Banking

September 1997 Branch and Agency Examination ManualPage 4

Private BankingExamination ObjectivesEffective date July 1997 Section 3430.2

1. To determine if policies, practices, proce-dures, and internal controls covering privatebanking activities are adequate and are beingfollowed by branch personnel.

2. To determine the scope and adequacy of theaudit function.

3. To recommend corrective action when poli-cies, procedures, practices, or internal con-trols are deficient or when violations of lawsor regulations have been noted.

Branch and Agency Examination Manual September 1997Page 1

Private BankingExamination ProceduresEffective date July 1997 Section 3430.3

The examiner should refer to the sections of thismanual listed below as well as other applicablesupervisory agency manuals for further informa-tion on examination procedures:

• Deposit Accounts section for examinationprocedures covering deposit accounts, holdmail, dormant accounts and overdrafts.

• Credit Risk Management section for examina-tion procedures for extensions of credit.

• Federal Reserve’s Bank Secrecy Act Manualor other similar examination material forexamination procedures to check private bank-ing activities for compliance with the Finan-cial Recordkeeping and Reporting regulations.

The various state and federal agencies maydiffer in terms of specific practices and method-ologies used to implement the following guide-lines. For further guidance in this area, examin-ers should consult with their respective agencies.

1. If selected for implementation, complete orupdate the internal control questionnaire.

2. Review policies and procedural manuals, andinternal control activities to determine theiradequacy.

3. Assess the adequacy of the internal auditfunction as it relates to private banking.

4. Determine, through a discussion with man-agement, what types of products are offeredto private banking clients.

5. Review the agreements covering the prod-ucts offered by private banking to determinethat they adequately protect the branch andthe customer.

6. Assess private banking personnel’s level ofcompetency to provide the services beingoffered to clients, i.e., education, experience,licenses, and the branch’s training program.

Branch and Agency Examination Manual September 1997Page 1

Private BankingInternal Control QuestionnaireEffective date July 1997 Section 3430.4

POLICIES AND PROCEDURES

1. Does the branch have up-to-date policiesand procedures regarding private bankingactivities?

2. Do the policies and procedures cover thefollowing:a. Definition of the products offered.b. Client account opening procedures.c. Client background checking procedures.d. Account monitoring procedures.e. Token name account requirements.f. Account officer’s responsibilities.g. Documentation requirements.h. Segregation of duties.

OFFICE OF FOREIGN ASSETSCONTROL AND REGULATION