IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH ‘A’, NEW DELHI BEFORE SHRI I.C. SUDHIR, JUDICIAL MEMBER AND SHRI J. SUDHAKAR REDDY, ACCOUNTANT MEMBER ITA No. 6059/Del/2013 AY: 2009-10 Amserve Consultants Ltd. vs. ADIT, Circle 2(1) 1 st floor, Elegance Tower, Plot no.8 International Taxation Non Hierarchical Commercial Centre New Delhi Jasola New Delhi 110 025 PAN: AAECA 8626 K A n d ITA No. 6090/Del/2013 AY: 2009-10 Amsure Insurance Agency Ltd. vs. ADIT, Circle 2(1) New Delhi International Taxation New Delhi (Appellant) (Respondent) Appellant by : Sh. C.S.Agarwal, Sr.Adv. And Sh. R.P.Mall, Adv. Respondent by : Sh. Ravi Jain, CIT, D.R. ORDER PER J. SUDHAKAR REDDY, ACCOUNTANT MEMBER Both these appeals are filed by the Assessees against the order of Ld.CIT(A)-IV, New Delhi dated 26.8.2013 and 13.9.2013 for the Assessment Year (hereinafter referred to as the A.Y.) 2009-10.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH ‘A’, NEW DELHI

BEFORE SHRI I.C. SUDHIR, JUDICIAL MEMBER AND SHRI J. SUDHAKAR REDDY, ACCOUNTANT MEMBER ITA No. 6059/Del/2013 AY: 2009-10

Amserve Consultants Ltd. vs. ADIT, Circle 2(1) 1st floor, Elegance Tower, Plot no.8 International Taxation Non Hierarchical Commercial Centre New Delhi Jasola New Delhi 110 025 PAN: AAECA 8626 K

A n d

ITA No. 6090/Del/2013 AY: 2009-10 Amsure Insurance Agency Ltd. vs. ADIT, Circle 2(1) New Delhi International Taxation New Delhi (Appellant) (Respondent)

Appellant by : Sh. C.S.Agarwal, Sr.Adv. And Sh. R.P.Mall, Adv.

Respondent by : Sh. Ravi Jain, CIT, D.R.

ORDER PER J. SUDHAKAR REDDY, ACCOUNTANT MEMBER

Both these appeals are filed by the Assessees against the order of

Ld.CIT(A)-IV, New Delhi dated 26.8.2013 and 13.9.2013 for the

Assessment Year (hereinafter referred to as the A.Y.) 2009-10.

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

2

As the issues arising in both these appeals are common, for the sake

of convenience they are heard together and are disposed of by way of this

common order.

2. Facts in brief:- M/s Amserve Consultants Ltd. (‘Amserve’ for short) is

a company and derives income from the business of providing advisory and

consulting services to companies engaged in the business of general

insurance and life assurance. It filed its return of income on 29.10.2009

declaring income of Rs.5,61,56,010/-. The Assessing Officer (hereinafter

referred to as the AO) passed an order u/s 143(3) of the Income Tax Act,

1961 (hereinafter referred to as ‘the Act’) determining the total income at

Rs.20,00,13,880/- inter alia making a disallowance u/s 40A(2)(b) of the Act

of data processing charges paid to M/s Amway India Enterprises Pvt.Ltd.

(Amway for short).

2.1. M/s Amsure Insurance Agency Ltd. (‘Amsure’ for short) is a company

which derives income from the business of providing services as a corporate

insurance agency. This Company filed its return of income on 29.10.2009

declaring income of Rs.3,61,16,150/-. The assessment was completed u/s

143(3) of the Act on 30.12.2011 determining total income at

Rs.34,43,66,150/- inter alia making a disallowance u/s 40A(2)(b) of the Act

on payment made for data base charges paid to M/s Amway India

Enterprises Pvt.Ltd. (‘Amway’ for short).

3. Aggrieved both the assesses are in appeal. The A.O. has made a

disallowance u/s 40A(2)(b) of the Act for the following reasons.

i. That a substantial portion of the revenue is being passed on to

their sister concern, which is not commensurate with the services

rendered.

ii. The manpower and infrastructure has been created by Amway, is

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

3

for the purpose of its own business but it is providing the same

manpower and infrastructure to Amserve and providing services

as per their agreement. However, it may be noted that it is not

incurring any additional expenditure in creating and maintaining

this infrastructure.

iii. In the absence of break-up of data processing services,

infrastructure services and customer facilitation services, it is not

possible to ascertain as to what extent the resources of Amway

were utilized in providing the services.

iv. Comparison with similar transaction in respect of some unrelated

parties is not possible.

v. That Amway has been paying taxes on the amount received does

not give unfettered rights to the assessee to make payments to its

related party at its sweet will.

vi. The contention that for invoking section 40A(2)(b) of the Act,

learned AO has to look at the fair market value of the goods and

services, legitimate business needs and benefit derived by the

assessee is though correct in principle but is immaterial in the

facts of the instant case.

vii. Whether or not employees or other resources were being used

exclusively for the purpose of providing services to Amserve; this

results in a scenario where it is also not possible even to

approximate the cost in the hands of Amway, not to mention the

impossibility of arriving at any certain figure in this respect.

viii. Alternatively, where there are no exclusive employees or resources

of Amway utilized in processing services to Amserve, the

attributable costs should be reduced by Amway from its own

expenses for arriving at its true profits.

4. On appeal the First Appellate Authority upheld the order of the A.O.

At Para 5.6 he held as follows.

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

4

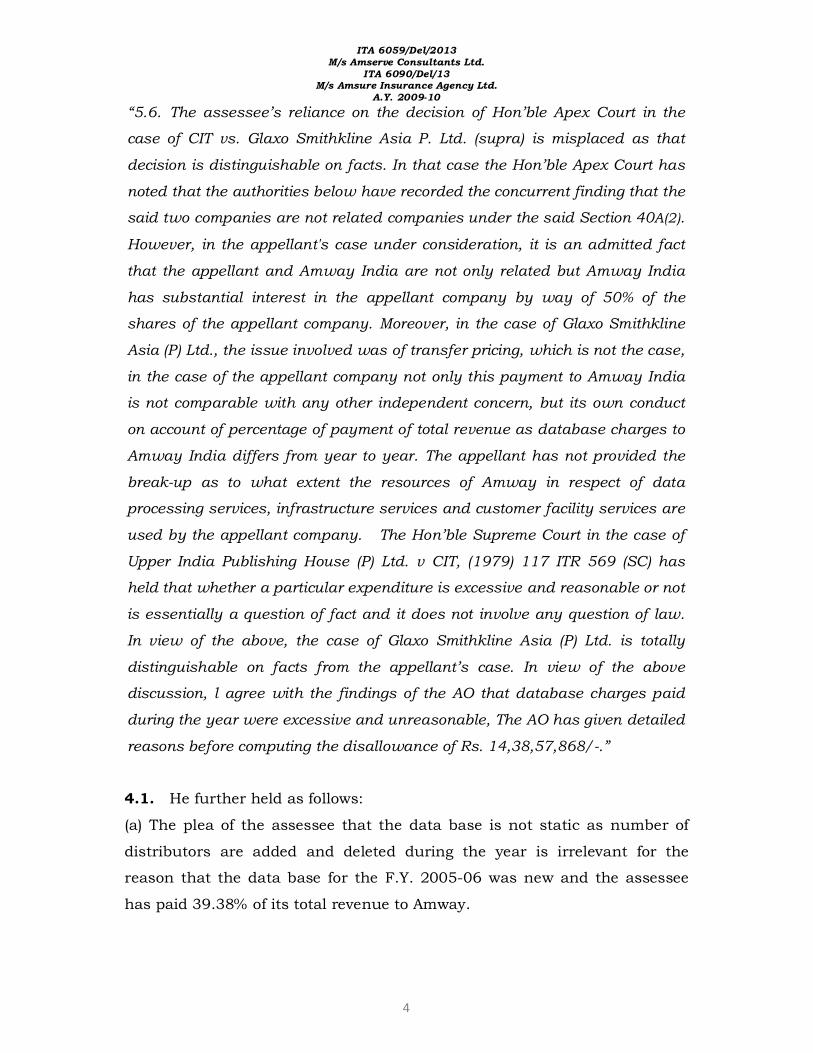

“5.6. The assessee’s reliance on the decision of Hon’ble Apex Court in the

case of CIT vs. Glaxo Smithkline Asia P. Ltd. (supra) is misplaced as that

decision is distinguishable on facts. In that case the Hon’ble Apex Court has

noted that the authorities below have recorded the concurrent finding that the

said two companies are not related companies under the said Section 40A(2).

However, in the appellant's case under consideration, it is an admitted fact

that the appellant and Amway India are not only related but Amway India

has substantial interest in the appellant company by way of 50% of the

shares of the appellant company. Moreover, in the case of Glaxo Smithkline

Asia (P) Ltd., the issue involved was of transfer pricing, which is not the case,

in the case of the appellant company not only this payment to Amway India

is not comparable with any other independent concern, but its own conduct

on account of percentage of payment of total revenue as database charges to

Amway India differs from year to year. The appellant has not provided the

break-up as to what extent the resources of Amway in respect of data

processing services, infrastructure services and customer facility services are

used by the appellant company. The Hon’ble Supreme Court in the case of

Upper India Publishing House (P) Ltd. v CIT, (1979) 117 ITR 569 (SC) has

held that whether a particular expenditure is excessive and reasonable or not

is essentially a question of fact and it does not involve any question of law.

In view of the above, the case of Glaxo Smithkline Asia (P) Ltd. is totally

distinguishable on facts from the appellant’s case. In view of the above

discussion, l agree with the findings of the AO that database charges paid

during the year were excessive and unreasonable, The AO has given detailed

reasons before computing the disallowance of Rs. 14,38,57,868/-.”

4.1. He further held as follows:

(a) The plea of the assessee that the data base is not static as number of

distributors are added and deleted during the year is irrelevant for the

reason that the data base for the F.Y. 2005-06 was new and the assessee

has paid 39.38% of its total revenue to Amway.

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

5

(b) The argument that despite payment of Rs.34.25 crores during the year

under consideration the assessee earned higher margins than in the

industry, does not help in supporting the reasonableness of payment u/s

40A(2) of the Act. The assessee has paid only Rs.29.39 crores in the next

F.Y.

(c ) The argument that Amway India has a very different business of direct

selling and will not share its customers with everybody and that Amway

India is only 50% shareholder in the joint venture will not make any

difference.

(d) For the A.Ys 2006-07, 2007-08, 2008-09 and 2010-11, the amount paid

as data base charges range from 27.08% to 40% and whereas the charges

are as high as 59.63% of the total revenue during the year under

consideration and the assessee has not given any convincing argument to

hold that the AO’s action of allowing only 10% of the data base charges has

no justification, and

(e) That justice will be met if 35% of the data base charges are allowed, as

this is the average of three years.

5. Aggrieved the assessee is in appeal before us on the following

grounds.

(1). That on facts and in law, CIT(A) erred in upholding the disallowance of Data Processing Charges of Rs. 14,38,57,868/- paid by the appellant to M/s Amway India Enterprises.

(1.1) That on the facts and in law, the CIT(A) erred in upholding the action of AO in and applying the provisions of section 40A(2) of the Act to the facts of instant case.

(2) That on the facts and in law the AO/CIT(A) erred in holding:

(a) that the appellant received only Rs. 2,700/- per policy as service income but paid service processing charges of Rs. 3,288/- per policy to M/s Amway India Enterprises Private Limited.

(b) that the appellant has not provided any basis for payments made to M/s Amway India Enterprises Private Limited.

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

6

(c) that it was an after thought to decide as to how much payment was required to be made to M/s Amway India Enterprises Private Limited.

(3). That on facts and in law the AO/CIT(A) erred in ignoring the transfer

pricing report submitted by the appellant to justify the arm’s length nature of

the transaction for payment of Data Processing Charges to M/s Amway India

Enterprises

(4). That on facts and in law the orders passed by Assessing Officer {herein above referred to as the “AO”) and the Commissioner of Income Tax (Appeals) {herein above referred to as the “CIT(A)”} are void ab intio and bad in law.

(5). That the appellant craves for leave to add, alter, amend, vary, omit or substitute any of the aforesaid grounds of appeal at any time before or at the time of hearing of the appeal.

6. We have heard Shri C.S.Aggarwal, the Ld.Counsel for the assessee

and Shri Ravi Jain, Ld.CIT, D.R. on behalf of the Revenue.

7. The arguments of Shri C.S.Agarwal, the Ld.Sr.Advocate representing

the assessee are as follows.

i. That the Learned DCIT acted without jurisdiction for invoking the provisions

of section 40A(2)(a) of the Income Tax Act, 1961, a prerequisite, in the

complete absence of any valid material, for forming an “OPINION” that the

assessee has incurred an expenditure which is “excessive or unreasonable”

having regard to the fair market value of the goods, services or facilities.

ii. The burden lay on the AO to establish by leading positive material that the

expenditure incurred is an “excessive or unreasonable” having regard to the

fair market value of the database. There is no material with the A.O. in this

regard.

iii. Section 40A(2)(a) could not be invoked unless the expenditure has been

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

7

incurred with a motive of tax evasion and has resulted into or would even

result in a loss of revenue as laid down in CBDT Circular No.6-P dt.

6.7.1968.

iv. The Payee Company has paid taxes on substantially higher income and

thus there is no loss to revenue. Hence it is wrong to hold that there is

diversion of income to save tax. The transaction is tax neutral.

v. Without prejudice and even otherwise, unless there is a clear finding

supported by valid and tangible material that the fair market value of the

database taken from the sister-concern, is excessive when compared with

the expenditure incurred, there cannot be an occasion to apply the

disabling provisions of s. 40A(2).

vi. That the assessee otherwise to having let evidence to establish the fair

market value of database obtained was at arm’s length (TP report) no

disallowance is permissible in law. The disallowance thus made on ad-hoc

basis is highly arbitrary.

vii. No disallowance could be made by invoking the provisions of section

40A(2)(a) even on the assumption that by incurring such expenditure third

party has benefitted. Such a consideration is not a relevant consideration

for the purpose of section 40A(2) or even under section 37 of the IT Act.

The rendering of services are not in dispute.

viiii. The exercise of commercial and business prudency is within the exclusive

domain of the assessee and is not subjected to the scrutiny of the AO. In

any case no material has been brought on record that, the assessee did not

exercise such a commercial and business prudency or it was improper. The

expenditure was incurred for the purpose of business and on account of

commercial expediency and business prudence.

ix. The disallowance has been made on a highly hypothetical ground and is

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

8

without any basis. The disallowance so made is apparently based on

subjective basis unsupported by any valid and tangible material. Thus the

disallowance made of Rs. 30,82,50,000/- out of which disallowance

sustained of Rs. 14,14,60,000 out of expenditure incurred of Rs.

34,25,00,000 is not merely highly arbitrary but also lacks any judicial

acceptance.

x. Rule of Consistency has not been followed.

xi. Lastly the disallowance made has resulted in to double taxation for the

same very income -Once in the hands of the assessee and another in the

hands of its associate enterprise.

xii. He also relied on a number of case laws which we would be dealing during

the course of our findings as and when necessary.

8. The Ld.CIT, D.R. Shri Ravi Jain on the other hand vehemently

opposed the contentions of the Ld.Counsel for the assessee. He made oral

as well as written submissions. The gist of his arguments is:

(a) A perusal of the agreements demonstrate that the assessee has been

granted license for use of the data base, only to promote and sell insurance

policies to its distributors and their customers, which is accessed by the

assessee on a real time basis. The assessee extracts the data on

weekly/daily basis, as per its need and solicit insurance business. In

addition to the use of the data base, the assessee was also entitled to make

available the insurance promotion technology to Amway Distributors and

their customers and also to participate in various Seminars and Conferences

organised by Amway for its distributors, and it was allotted time to talk

about various insurance products. This enabled the assessee to directly

interact with the prospective customers. This made it easy for the assessee

to sell insurance products because of the goodwill of M/s Amway India

P.Ltd. for which it charges a fee. For this, the assessee is paying

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

9

substantial payments to Amway India, year after year, for more or less the

same data base with only minor changes.

(b) A perusal of the agreement demonstrate that there is no exclusivity

Clause in the agreement between Amway and Amsure and Amway is free to

provide data base to any other third party.

(c) Amway had not incurred any additional cost for creating the data base.

Still huge amount is charged from Amsure on this account. No data or

break-up has been given by the assessee to prove the expenditure of use of

resources of Amway.

(d) The contention of the assessee that for invoking the provision of

S.40A(2)(b), the AO has to look at the fair market value of the goods and

services, legitimate business needs and benefits derived by the assessee,

though correct on principle, is immaterial in the case on hand, as it is

impossible to find comparables which could be taken up for the purpose of

ascertaining the market value of the goods and services.

(e) It can be seen that the payments made by Amsure to Amway do not

justify the legitimate business needs and benefits.

(f) The Circular of the CBDT relied upon by the assessee is not applicable to

the facts of the present case as payments made are unreasonable and

excessive.

(g) The case laws relied upon by the assessee relating to the Transfer Pricing

study cannot be made applicable as the transactions of the assessee are

domestic transactions undertaken in the F.Y. 2008-09 before the

introduction of T.P. provisions to specified domestic transactions by the

Finance Act, 2012. That burden to prove the genuineness of the

expenditure is on the assessee.

(h) Tax neutrality does not grant unfettered rights to the assessee to make

payments to its related enterprises at its sweet will. The cases relied upon

by the assessee are distinguishable as the payments made were

unreasonable or excessive considering the services availed by the assessee.

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

10

(i) Reliance was placed on the decision of CIT vs. NEPC India Ltd.

reported in 303 ITR 271 (Madras H.C.) and CIT vs. Shatrunjay

Diamonds (2003) 261 ITR 258 (Bombay H.C.).

9. He relied upon the order of the A.O. as well as that of the Ld.CIT(A)

and also relied on certain other case laws which we would be discussing as

and when necessary, during the course of our finding.

10. In response the Ld.Counsel for the assessee filed written submissions.

He argued that under the section a disallowance can be made only when

the A.O. is of the opinion that, the expenditure incurred is excessive or

unreasonable having regard to the fair market value of the goods, services or

facilities for which the payment is made. He submitted that, in the case on

hand the AO has not done such an exercise as admittedly there is no

comparative data available. He submitted that the disallowance was made

on an arbitrary basis. 90% of the expenses incurred were disallowed on

adhoc basis. He submitted that the A.O. ignored that the assessee

benefitted from, the goodwill, data and net work of Amway and the unique

features of the data base of Amway. He submitted that the A.O. ignored

and disregarded the evidence produced by the assessee and that the

payment is made in pursuance of an agreement and the genuineness of the

services is not doubted.

11. Rival contents heard. On a careful consideration of the facts and

circumstances of the case, orders of lower authorities and case laws cited,

we hold as follows.

12. The assessee company Amserve Consultants Ltd. was established in

the year 2004 as a joint venture between Amway India Enterprises P.Ltd.

and Poland Life Assurance Co.Ltd., South Africa with a 50:50 share holding

pattern. The assessee company is in the business of providing advisory,

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

11

consultancy and business support services to companies engaged in

insurance business. It earned income from service charges primarily from

collection of forms, data entry and quality check services etc. It was

engaged in policy processing and other related services for insurance

business of Max New York Life Insurance Co. Ltd.

Amserve had agreed to provide various data processing services to Max New

York Life Insurance Co. Ltd., and this included physical collection of

completed proposal forms from the corporate agencies, organising detailed

quality checks, data entry etc.

12.1. Amserve also entered into an agreement with Amway for data

processing services vide agreement dt. 25.11.2005. The assessee avails

data processing services from Amway India from 1st October, 2005 to 31st

March, 2007. This includes arrangement for physical collection of completed

proposal forms from corporate agencies of Max New York, preliminary

quality checks and data entry.

Thus for the F.Y. 2008-09 Amway which has offices in 45 localities

across India, render data processing services to Amserve.

12.2. Amsure is the corporate agency of Max Life Insurance Co.Ltd.

and Royal Sundaram Alliance Co.Ltd. for life insurance solutions. It

distributes life insurance projects, health insurance projects, motor

insurance products. It entered into an agreement with M/s Amway India

Enterprise Ltd. on 24.10.2005 for the period 1.10.2005 to 31.10.2007 for

the use of data base of Amway India Enterprises P.Ltd. which contain details

of Amways Distributors, their status etc. Under this agreement the assessee

Amsure was granted license by Amway for use of its data base for promotion

and sale of insurance policies to its distributors and their customers.

12.3. On these facts we should examine the correctness of disallowance

made u/s 40A(2) of the Act.

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

12

Sec.40 ‘A’ of the Income Tax Act reads as follows.

Expenses or payments not deductible in certain circumstances.

40A. (1) The provisions of this section shall have effect notwithstanding anything to the contrary contained in any other provision of this Act relating to the computation of income under the head "Profits and gains of business or profession".

(2)(a) Where the assessee incurs any expenditure in respect of which payment has been or is to be made to any personreferred to in clause (b) of this sub-section, and the [Assessing] Officer is of opinion that such expenditure is excessive or unreasonable having regard to the fair market value of the goods, services or facilities for which the payment is made or the legitimate needs of the business or profession of the assessee or the benefit derived by or accruing to him there from, so much of the expenditure as is so considered by him to be excessive or unreasonable shall not be allowed as a deduction.

12.4. The Central Board of Direct Taxes vide its circular no.6-B dated

6th July, 1968 at para 74 and 75 stated as follows.

74. It may be noted that the new provision is applicable to all categories of expenditure incurred in businesses and professions, including expenditure on purchase of raw materials, stores or goods, salaries to employees and also other expenditure on professional services, or by way of brokerage, commission, interest, etc. Where payment for any expenditure is found to have been made to a relative or associate concern falling within the specified categories, it will be necessary for the Income-tax Officer to scrutinize the reasonableness of the expenditure with reference to the criteria mentioned in the section. The Income-tax Officer is expected to exercise his judgment in a reasonable and fair manner. It should be borne in mind that the provision is meant to check evasion of tax through excessive or unreasonable payments to relatives and associate concerns and should not be applied in a manner which will cause hardship in bona fide cases. (Emphasis ours).

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

13

From this Circular of the CBDT, it is clear that the provision was made

specifically to check tax avoidance. Thus when there is no tax avoidance,

the applicability of this section would not be appropriate.

12.5. The Hon’ble Supreme Court in the case of CIT-IV, New Delhi vs.

M/s Glaxo Smithkline Asia P.Ltd. (supra) held as follows.

“The larger issue is whether Transfer Pricing Regulations should be limited to cross-border transactions or whether the Transfer Pricing Regulations be extended to domestic transactions. In domestic transactions, the under-invoicing of sales and over-invoicing of expenses ordinarily will be revenue neutral in nature, except in two circumstances having tax arbitrage such as where one of the related entities is (i) loss making or (ii) liable to pay tax at a lower rate and the profits are shifted to such entity; Complications arise in cases where the fair market value is required to be assigned to transactions between related parties u/s 40A(2). The CBDT should examine whether Transfer Pricing Regulations can be applied to domestic transactions between related parties u/s 40A(2) by making amendments to the Act. The AO can be empowered to make adjustments to the income declared by the assessee having regard to the fair market value of the transactions between the related parties and can apply any of the generally accepted methods of determination of arm’s length price, including the methods provided under Transfer Pricing Regulations. The law can also be amended to make it compulsory for the taxpayer to maintain Books of Accounts and other documents on the lines prescribed in Rule 10D and obtain an audit report from his CA that proper documents are maintained; Though the Court normally does not make recommendations or suggestions, in order to reduce litigation occurring in complicated matters, the question of extending Transfer Pricing regulations to domestic transactions require expeditious consideration by the Ministry of Finance and the CBDT may also consider issuing appropriate instructions in that regard.” (Emphasis ours).

The Hon’ble Apex Court has laid down that fair market value of a

transaction between associate domestic Enterprises can be determined by

using Transfer Pricing Methodologies and study.

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

14

12.6. The Hon’ble Bombay High Court in the case of CIT vs. Indo

Saudi Services (P) Ltd. (2009) 219 CTR 562 Bombay at para 4 held as

follows.

“4. We have heard the learned advocates appearing for both sides. W7e have also perused the order passed by the Tribunal dated 21st Oct., 1999 which is impugned by the Revenue in the present appeals. We find that the following facts were established before the Tribunal and the same have been accepted by the Revenue even before us. (i) That the assessee apart from paying handling charges @9 1/2 per cent to its sister concern, have paid handling charges at the same rate to other agents viz., M/s A.K.Travels, M/s Om Travels and M/s Jet Age Travels. (ii) For asst. yrs. 1986-87 and 1987-88 the assessee had paid the handling charges @ 10 per cent to the sister concern of the assessee and such charges paid were considered to be reasonable by the appellant. (iii) For asst.yrs. 1989-90 and 1990-91 the assessee had reduced the payment of handling charges to 9 1/2 per cent to its sister concern. The AO has considered the payment of commission to the sister concern in the asst. yr. 1989-90 and allowed the claim after due scrutiny. For asst. yr. 1990-91 also the claim of the assessee @9 1/2 per cent has been allowed though the same has not been dealt with by the AO specifically in the order. (iv) For asst.yrs. 1993-94 and 1994-95 the assessment has been made by the AO under section 143(3) and handling charges paid to the sister concern @ 9.5 per cent have been considered to be reasonable and allowed. (iv) The sister concern of the assessee M/s Middle East International is also assessed to tax and income assessed for the asst. yr. 1991-92 is Rs. 9,38,510 and for asst.yr. 1992-93 is Rs. 14,65,880 and the said assessment orders have been placed on record. (v) Under the CBDT Circular No. 6-P, dated 6th July, 1968 it is stated that no disallowance is to be made under section 40A(2) in respect of the payments -made to the relatives and sister concerns where there is no attempt to evade tax. 5. In view of the aforesaid admitted facts we are of the view that the Tribunal was correct in coming to the conclusion that the CIT(A) was wrong in disallowing half per cent commission paid to the sister concern of the assessee during the asst. yrs. 1991-92 and 1992-93. The ld.advocate appearing for the appellant was also not in a position to point out how the assessee evaded payment of tax by alleged payment of higher commission to its sister concern since the sister concern was also paying tax at higher rate and copies of the assessment orders of the sister concern were taken on

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

15

record by the Tribunal.” (Emphasis ours). 12.7. The Jurisdictional High Court in the case of Hive

Communications P.Ltd. vs. CIT reported in 353 ITR 200 (Delhi) referred to

the CBDT Circular no.6P dated 6.7.1968 at para 11 as under.

“11. We may also refer to the scope of S.40A(2) as explained by CBDT in

Circular no.6P, dated 6.7.1968. The CBDT clarified that while examining the

reasonableness of expenditure the AO is expected to exercise his judgement in

a reasonable and fair manner. It should be borne in mind that the provision is

meant to check evasion of tax through excessive or unreasonable payments to

relatives and associate concerns and should not be applied in a manner

which will cause hardship in bona fide cases.”

Thereafter it was held as follows.

“7. The question whether the expenditure is excessive or unreasonable in a

given case has to be examined keeping in mind the services (with which we

are concerned in the present case) for which payment is made. In the process

the legitimate needs of the business or profession of the assessee or the

benefit derived by or accruing to the assessee from such services is also to be

kept in mind. After applying this test if it is found that the expenditure is

excessive or unreasonable excess, excess or unreasonable portion of the

expenditure is to be disallowed. We have also kept in mind the provisions of

sub Section 2 (b) of Section 40-A of the Act as per which the burden is upon

the assessee to establish that the price paid by it is not excessive or

unreasonable as in this case Mr.SushilPandit was holding substantial portion

of share namely 65 percent in the assessee company. When we apply the

aforesaid principle in the facts of this case, we find that the assessee has

been able to discharge the burden that the price paid by it to Mr. SushilPandit

is not excessive or unreasonable.

“12. It will also be useful to refer to the judgment of Allahabad High Court in

Abbas Wazir (P.) Ltd. v. CIT [2004] 265 ITR 77/[2003] 133 Taxman 702

wherein the High Court held that even while invoking the provisions of

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

16

section 40A(2) of the Act, the reasonableness of the expenditure for the

purpose of business has to be judged from the point of view of a

businessman and not that of the revenue. The approach has to be that of a

prudent businessman and the reasonableness must be looked into from

businessman point of view. Similar view is held by the Madras High Court in

CIT v. Computer Graphics Ltd. [2006] 285 ITR 84/155 Taxman 612.

In CIT v. Edward Keventer (P.) Ltd. [1972] 86 ITR 370 , the Calcutta High

Court considering identical provision in 1922 Act, it was held that the section

places two limitations in the matter of exercise of the power. The section

enjoins the Assessing Officer in forming any opinion as to the reasonableness

or otherwise of the expenditure incurred must take into consideration (i) the

legitimate business needs of the company and (ii) the benefit derived by or

accruing to the company. The legitimate business needs of the company must

be judged from the view point of the company itself and must be viewed from

the point of view of a prudent businessman. It is not for the Assessing Officer

to dictate what the business needs of the company should be and he is only

to judge the legitimacy of the business needs of the company from the point of

view of a prudent businessman. The benefit derived or accruing to the

company must also be considered from the angle of a prudent businessman.

The term "benefit" to a company in relation to its business, it must be

remembered, has a very wide connotation and may not necessarily be

capable of being accurately measured in terms of pound, shillings and pence

in all cases. Both these aspects have to be considered judiciously,

dispassionately without any bias of any kind from the view-point of a

reasonable and honest person in business.

The aforesaid judgment of Calcutta High Court was affirmed by the Apex

Court in CIT v. Edward Keventer (P.) Ltd. [1978] 115 ITR 149 . In the same

line is the judgment of Bombay High Court in the case of CIT v. Shatrunjay

Diamonds [2003] 261 ITR 258/ 128 Taxman 759.” (Emphasis ours).

12.8. In this judgement at para 7, the Jurisdictional High Court has

laid down that the burden is upon the assessee to establish that the price

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

17

paid to a related party by it, is not excessive or unreasonable. Thus the

argument of the Ld.Counsel for the assessee that this burden of proof is on

the Revenue is contrary to the propositions of law laid down by the

Jurisdictional High Court.

12.9. In the case on hand the Revenue does not dispute the fact that

M/s Amway India Enterprises as well as the assessee are both assessed at

the maximum marginal rate. The transaction is tax neutral. Under these

circumstances it has to be held on facts that this payment is not made with

an intention to evade tax. In fact the income of the Payee Company is much

more than that of the assessee. Thus the Circular No.6P dt. 6th July,1968

read with the decision of the Hon’ble Bombay High Court in the caseof Indo

Saudi Services (P) Ltd. (supra) apply to the facts of this case. What is the

amount that should have been paid for these services is to be decided by the

Assessing Officer by keeping in view the requirements of business and the

point of view of the business man.

13. It is further found that, in the case of Amserve Consultants, the AO

chose to disallow 25% of the payments made for new policy business and

75% of payments made for renewal of policies. Similarly in the case of

Amsure Insurance Agency, the AO disallowed 90% of the data base charges

paid. Only 10% was allowed as reasonable. When the matter travelled to the

Ld.CIT(A) 35% of the data base charges were allowed and the balance 65%

was disallowed. No basis or factual justification whatsoever is given by the

revenue authorities in both these cases for this ad-hoc disallowance. The

factum of rendering of services is not in dispute. The requirement of

payment of fees is also not in dispute. Only on the quantum of charges,

the A.O. is of the view that it is excessive and unreasonable. No

comparative data or instance is available. No exercise is made to arrive at a

fair market price by the A.O. Those ad-hoc disallowances, in our view are

based on surmises and conjectures.

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

18

14. We now examine the legal position on this issue.

(i) The Hon’ble Delhi High Court in the case of CIT vs. B. Dalmia

Cement (P) Ltd., (2001) 254 ITR 377 (Del) at para 7 held as follows.

“7. It is to be noted that in the present case the question that has been raised by the Revenue is not one relating to the expenditure being not for the purposes of the business. It is an question of the appropriate amount which would have been paid as commission. In fact the Assessing Officer himself has allowed to the extent of Rs. 4,35,854 holding, inter alia, "the payment of Rs. 1.75 per M. T. to Cement Distributors Limited is very much on the excessive side". This in our view was impermissible within the framework of section 37 of the Act. The jurisdiction of the Revenue is confined to "deciding the reality of the expenditure", namely, whether the amount claimed as deduction was factually expended or laid down and whether it was wholly and exclusively for the purpose of the business. The reasonableness of the expenditure could be gone into only for the purpose of determining whether, in fact, the amount was spent. Once it is established that there was a nexus between the expenditure and the purpose of the business, the Revenue cannot justifiably claim to put itself in the armchair of a businessman or in the position of the board of directors and assume the said role to decide how much is a reasonable expenditure having regard to the circumstances of the case. We need not go into any hypothetical issue in this case in view of the accepted position that the factum of services rendered by the CDL has not been refuted by the Revenue. It needs no reiteration that the settled position in law is that no businessman can be compelled to maximise his profits. The obvious answer to the first question is in the affirmative, in favour of the assessee and against the Revenue.”

(ii) The Hon’ble Supreme Court in the case of CIT vs. Walchand and

Co. P.Ltd. 65 ITR 381 held that “In applying the test of commercial

expediency for determining whether expenditure was wholely and

exclusively laid out for the purpose of business, reasonableness of

the expenditure has to be adjudged from the point of view of the

business men and not of the Revenue.”

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

19

(iii) In the case of Principal CIT-II vs. Gujarat Gas Financial Services

Ltd. 233 Taxman 532 (Guj.) it is held as follows.

“13. As has been found by us in the preceding para of this judgement that

the respondent company as well as the parent company, both are assessed to

income tax at the maximum marginal rate and, therefore, it cannot be said

that the service charge is paid to the respondent company at an unreasonable

rate to evade income tax. Even the Ld.Counsel Mr.Bhatt for the revenue does

not dispute this fact.

14. We are in agreement with the observations made by the Tribunal as well

as the ratio laid down by the coordinate Bench of this Court in the case of

Enviro Contro Associated P.Ltd. (supra) Ashok J Patel and Indo Saudi Services

(Travel) P.Ltd.

15. It is pertinent to note that so far as the Circular dt. 6.7.1968 is

concerned, it makes clear that the provisions u/s 40A(2) and particularly with

regard to the transaction between the relatives and associates is concerned,

the same shall be treated as bona fide case unless the officer finds it that one

of them is trying to evade payment of tax.”

As already stated, in the case on hand, there is not even an allegation that

the assessee has evaded payment of tax.

(iv) In the case of Minda Acoustic Ltd. vs. ACIT (2015) 69 SOT 162 the

ITAT Delhi Bench at para 21 held as follows.

“21. We have heard the rival contentions, perused the material on record

and duly considered facts of the case in the light of the applicable legal

position. We find that the disallowance under section 40A(2)(a)/(b) can be

invoked when the A.O. is of the opinion that, inter alia, such expenditure is

"excessive or unreasonable having regard to the fair market value of the

goods, services or facilities for which the payment is made or the legitimate

needs of the business or profession of the assessee". In the present case, the

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

20

disallowance has been made on the ground that the payment is excessive or

unreasonable having regard to the fair market value and the services for

which the payment is made but then there is no finding by the A.O. as to what

according to him is fair market value of the services in question. A

disallowance under section 40A(2), on percentage basis, is inherently contrary

to the Act in as much as it is a condition precedent for invoking section 40A

that the benchmark to be set as to what is a fair market value of the services

question and then the expenditure in excess of the said benchmark is to be

disallowed but then such benchmark cannot be in terms of percentage of

payment by the assessee. For this reason alone, the impugned disallowance

indeed deserves to be disallowed. We have also noted that in the present

case, there is no dispute about the facts of service being rendered and there is

no benchmark set for as to what would constitute a fair market value of the

services in question. Unless there is a clear finding that the market value of

the services taken from the sister-concern is less than the price at which the

services are obtained, there cannot be an occasion to apply the disabling

provisions of s. 40A(2). This exercise, therefore, necessitates a finding about

the fair market value of such services. There is no such finding in the present

case. In these circumstances as also bearing in mind entirety of the case, we

are of the considered view that the disallowance made by the A.O. was

devoid of legally sustainable basis. The learned CIT(A) was thus quite

justified in deleting the same. Ground no.2 is thus dismissed.”

(Emphasis ours).

The proposition of law laid down by this Bench of the ITAT, when applied to

the facts of this case, we have to come to a conclusion that the disallowance

has to be deleted.

(v) The Hon’ble Gujarat High Court in the case of CIT vs. Enviro

Control Associated P.Ltd. (2014) 43 taxmann.com 291 (Guj.) at

para 12 held as follows.

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

21

“We are in complete agreement with the reasoning and observations

made by the learned CIT(A) confirmed by the learned ITAT. In absence

of any material before the Assessing Officer, such as comparative chart

etc. to suggest that any excessive payment was made to M/s. Pollucon

Engineers and the 10% ad hoc disallowance was made on the payment

made under Section 40A(2)(b) of the Act to M/s. Pollucon Engineers

solely on the ground that M/s. Pollucon Engineers to whom the payment

was made, was run by the wife of the Director of the assessee company

and therefore, there was an element of excessive claim, we are of the

opinion that the Assessing Officer was not justified in adopting

disallowance to the extent of 10% payment under Section 40A(2)(b) of

the Act . Under the circumstances, disallowance made by the Assessing

Officer is rightly deleted by the learned CIT(A) confirmed by the learned

ITAT.”

14.1. In the case on hand the adhoc disallowance made by the A.O.

in our view is arbitrary and without any basis. The A.O. has not given a

finding as to what as per him, is the fair market value. Even if it is

assumed that the payment made is excessive and unreasonable, such

arbitrary and baseless, adhoc disallowances cannot be upheld. On this

ground also the assessee has to succeed.

14.2. We now take up the issue as to whether the assessee has

discharged the burden of proof that lay on it that, the expenditure paid by

it to its sister concern, is not excessive or unreasonable. As already held,

the Hon’ble Delhi High Court in the case of Hype Communications P.Ltd.

(supra) has laid down that such burden is on the assessee. In this case the

assessee has filed Transfer Pricing Reports in both the cases justifying the

price paid by it for the services obtained, after conducting a Transfer

Pricing Study.

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

22

14.3. The Revenue authorities have not uttered a whisper as to why

the transfer pricing report is not acceptable. The methodology of

determining the ALP has been laid down in the Act and has been made

mandatory for international transactions with Associated Enterprises (A.E.).

Simply saying that these provisions do not apply to a domestic company

transactions with its A.Es. for this particular A.Y. does not suffice. When

the assessee has chosen to use these transfer pricing provisions to

demonstrate its claim that the expenditure in question is at arm’s length

and that the same is not excessive or unreasonable, the revenue authorities

are bound to rebut this claim of the assessee with reasons before coming to

a conclusion to the contrary. When these transfer pricing reports submitted

by the assessee are not rejected, we have to conclude that the assessee has

discharged the burden of proof that lay on it on this issue. On this ground

also the assessee succeeds.

14.4. In both the cases the assesses have filed detailed alternative

submissions in support of its contentions as to why the payment made to

Amway is reasonable and commensurate with the nature of services

provided by them and to demonstrate that the disallowance is bad in law.

15. The Ld.Sr.D.R. relied on the findings in the order of the

Ld.CIT(A) to rebut these alternative submissions. We do not propose to go

into these arguments for the reason that we have already come to a

conclusion that the disallowance is bad in law and the other contentions

would become academic in these cases on hand.

16. In view of the above discussion we allow the appeals of the

assessees in both the cases by deleting the disallowance made u/s 40A(2)(b)

of the Act for the reason that the assessee has proved that the price paid is

at arm’s length and not excessive or unreasonable and as the disallowance

ITA 6059/Del/2013 M/s Amserve Consultants Ltd.

ITA 6090/Del/13 M/s Amsure Insurance Agency Ltd.

A.Y. 2009-10

23

made on ad-hoc basis is arbitrary. There is no evasion of tax also

warranting invocation of S.40A(1) of the Act.

Hence we delete the disallowance in both the cases to the extent confirmed

by the Ld.CIT(A).

17. In the result both the appeals of the assesses are allowed.

Order pronounced in the Open Court on 29th June, 2016.

Sd/- Sd/- (I.C. SUDHIR) (J. SUDHAKAR REDDY)

JUDICIAL MEMBER ACCOUNTANT MEMBER

Dated: the 29th June, 2016

• Manga

Copy forwarded to: - 1. Appellant 2. Respondent 3. CIT 4. CIT(A) 5. DR, ITAT

TRUE COPY

By Order,

ASSISTANT REGISTRAR

Related Documents