Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and the Securities and Futures Commission take no responsibility for the contents of this Application Proof, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this Application Proof. Application Proof of In-Tech Holdings (Cayman) Limited (incorporated in the Cayman Islands with limited liability) WARNING The publication of this Application Proof is required by The Stock Exchange of Hong Kong Limited (the “Stock Exchange”) and the Securities and Futures Commission (the “Commission”) solely for the purpose of providing information to the public in Hong Kong. This Application Proof is in draft form. The information contained in it is incomplete and is subject to change which can be material. By viewing this document, you acknowledge, accept and agree with In-Tech Holdings (Cayman) Limited (the “Company”), its sponsor, advisers or members of the underwriting syndicate that: (a) this document is only for the purpose of providing information about the Company to the public in Hong Kong and not for any other purposes. No investment decision should be based on the information contained in this document; (b) the publication of this document or any supplemental, revised or replacement pages on the Stock Exchange’s website does not give rise to any obligation of the Company, its sponsor, advisers or members of the underwriting syndicate to proceed with an offering in Hong Kong or any other jurisdiction. There is no assurance that the Company will proceed with the offering; (c) the contents of this document or any supplemental, revised or replacement pages may or may not be replicated in full or in part in the actual final listing document; (d) the Application Proof is not the final listing document and may be updated or revised by the Company from time to time in accordance with the Rules Governing the Listing of Securities on the Stock Exchange; (e) this document does not constitute a prospectus, offering circular, notice, circular, brochure or advertisement offering to sell any securities to the public in any jurisdiction, nor is it an invitation to the public to make offers to subscribe for or purchase any securities, nor is it calculated to invite offers by the public to subscribe for or purchase any securities; (f) this document must not be regarded as an inducement to subscribe for or purchase any securities, and no such inducement is intended; (g) neither the Company nor any of its affiliates, advisers or underwriters is offering, or is soliciting offers to buy, any securities in any jurisdiction through the publication of this document; (h) no application for the securities mentioned in this document should be made by any person nor would such application be accepted; (i) the Company has not and will not register the securities referred to in this document under the United States Securities Act of 1933, as amended, or any state securities laws of the United States; (j) as there may be legal restrictions on the distribution of this document or dissemination of any information contained in this document, you agree to inform yourself about and observe any such restrictions applicable to you; and (k) the application to which this document relates has not been approved for listing and the Stock Exchange and the Commission may accept, return or reject the application for the subject public offering and/or listing. No offer or invitation will be made to the public in Hong Kong until after a prospectus of the Company has been registered with the Registrar of Companies in Hong Kong in accordance with the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Chapter 32 of the Laws of Hong Kong). If an offer or an invitation is made to the public in Hong Kong in due course, prospective investors are reminded to make their investment decisions solely based on a prospectus of the Company registered with the Registrar of Companies in Hong Kong, copies of which will be made available to the public during the offer period.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and the Securities andFutures Commission take no responsibility for the contents of this Application Proof, make no representation as toits accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from orin reliance upon the whole or any part of the contents of this Application Proof.

Application Proof of

In-Tech Holdings (Cayman) Limited(incorporated in the Cayman Islands with limited liability)

WARNING

The publication of this Application Proof is required by The Stock Exchange of Hong Kong Limited (the “StockExchange”) and the Securities and Futures Commission (the “Commission”) solely for the purpose of providinginformation to the public in Hong Kong.

This Application Proof is in draft form. The information contained in it is incomplete and is subject to change whichcan be material. By viewing this document, you acknowledge, accept and agree with In-Tech Holdings (Cayman)Limited (the “Company”), its sponsor, advisers or members of the underwriting syndicate that:

(a) this document is only for the purpose of providing information about the Company to the public in Hong Kongand not for any other purposes. No investment decision should be based on the information contained in thisdocument;

(b) the publication of this document or any supplemental, revised or replacement pages on the Stock Exchange’swebsite does not give rise to any obligation of the Company, its sponsor, advisers or members of theunderwriting syndicate to proceed with an offering in Hong Kong or any other jurisdiction. There is noassurance that the Company will proceed with the offering;

(c) the contents of this document or any supplemental, revised or replacement pages may or may not be replicatedin full or in part in the actual final listing document;

(d) the Application Proof is not the final listing document and may be updated or revised by the Company fromtime to time in accordance with the Rules Governing the Listing of Securities on the Stock Exchange;

(e) this document does not constitute a prospectus, offering circular, notice, circular, brochure or advertisementoffering to sell any securities to the public in any jurisdiction, nor is it an invitation to the public to make offersto subscribe for or purchase any securities, nor is it calculated to invite offers by the public to subscribe foror purchase any securities;

(f) this document must not be regarded as an inducement to subscribe for or purchase any securities, and no suchinducement is intended;

(g) neither the Company nor any of its affiliates, advisers or underwriters is offering, or is soliciting offers to buy,any securities in any jurisdiction through the publication of this document;

(h) no application for the securities mentioned in this document should be made by any person nor would suchapplication be accepted;

(i) the Company has not and will not register the securities referred to in this document under the United StatesSecurities Act of 1933, as amended, or any state securities laws of the United States;

(j) as there may be legal restrictions on the distribution of this document or dissemination of any informationcontained in this document, you agree to inform yourself about and observe any such restrictions applicableto you; and

(k) the application to which this document relates has not been approved for listing and the Stock Exchange andthe Commission may accept, return or reject the application for the subject public offering and/or listing.

No offer or invitation will be made to the public in Hong Kong until after a prospectus of the Company has beenregistered with the Registrar of Companies in Hong Kong in accordance with the Companies (Winding Up andMiscellaneous Provisions) Ordinance (Chapter 32 of the Laws of Hong Kong). If an offer or an invitation is madeto the public in Hong Kong in due course, prospective investors are reminded to make their investment decisionssolely based on a prospectus of the Company registered with the Registrar of Companies in Hong Kong, copies ofwhich will be made available to the public during the offer period.

If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

In-Tech Holdings (Cayman) Limited精達控股有限公司

(incorporated in the Cayman Islands with limited liability)

[REDACTED]

Number of [REDACTED] : [REDACTED] Shares (subject to the[REDACTED])

Number of [REDACTED] : [REDACTED] Shares (subject toreallocation)

Number of [REDACTED] : [REDACTED] Shares (subject toreallocation and the [REDACTED])

Maximum [REDACTED] : HK$[REDACTED] per [REDACTED], plusbrokerage fee of 1%, SFC transactionlevy of 0.0027%, Stock Exchange tradingfee of 0.005% and FRC transaction levyof 0.00015% (payable in full onapplication in Hong Kong dollars andsubject to refund)

Nominal Value : HK$0.01 per ShareStock Code : [REDACTED]

Sole Sponsor

[REDACTED]

Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibilityfor the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arisingfrom or in reliance upon the whole or any part of the contents of this document.

A copy of this document, having attached thereto the documents specified in “Documents Delivered to the Registrar of Companies and Available for Inspection in HongKong” in Appendix VI to this document, has been registered by the Registrar of Companies in Hong Kong as required by Section 342C of the Companies (WUMP). TheSecurities and Futures Commission and the Registrar of Companies in Hong Kong take no responsibility for the contents of this document or any other document referredto above.

The [REDACTED] is expected to be fixed by agreement between the [REDACTED] (for itself and on behalf of the [REDACTED]) and us on the [REDACTED]. The[REDACTED] is expected to be on or about [REDACTED] and, in any event, unless otherwise announced, not later than [REDACTED]. The [REDACTED] will be nomore than HK$[REDACTED] and is currently expected to be no less than HK$[REDACTED] unless otherwise announced. Investors applying for the [REDACTED] mustpay, on application, the maximum [REDACTED] of HK$[REDACTED] for each [REDACTED] together with a brokerage fee of 1%, SFC transaction levy of 0.0027%,Stock Exchange trading fee of 0.005% and FRC transaction levy of 0.00015%, subject to refund if the [REDACTED] as finally determined is lower thanHK$[REDACTED]. If, for any reason, the [REDACTED] is not agreed between the [REDACTED] (for itself and on behalf of the [REDACTED]) and us on or before[REDACTED], unless otherwise announced, the [REDACTED] will not proceed and will lapse.

The [REDACTED] (for itself and on behalf of the [REDACTED]) may, where considered appropriate, reduce the indicative [REDACTED] range below that which isstated in this document at any time on or prior to the morning of the last day for lodging applications under the [REDACTED]. In such a case, an announcement will bepublished on the websites of the Stock Exchange at www.hkexnews.hk and of our Company at http://www.in-tech.com.hk not later than the morning of the day whichis the last day for lodging applications under the [REDACTED]. For further information, see “Structure of the [REDACTED]” and “How to Apply for [REDACTED]”in this document.

Prior to making an investment decision, prospective investors should consider carefully all of the information set out in this document and the [REDACTED], includingthe risk factors set out in “Risk Factors” in this document.

The obligations of the [REDACTED] under the [REDACTED] to subscribe for, and to procure applicants for the subscription for, the [REDACTED] are subject totermination by the [REDACTED] (for itself and on behalf of the [REDACTED]) if certain grounds arise prior to 8:00 a.m. on the [REDACTED]. Such grounds are setout in “[REDACTED] – [REDACTED] and Expenses – [REDACTED] – Grounds for termination” in this document. It is important that you refer to that section for furtherdetails.

The [REDACTED] have not been, and will not be, registered under the US Securities Act or with any securities regulatory authority of any state of the United States,and may not be offered or sold within the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the USSecurities Act. The [REDACTED] will be offered and sold only outside the United States in reliance on Regulation S.

[REDACTED]

IMPORTANT

[REDACTED]

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

[REDACTED]

IMPORTANT

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

[REDACTED]

EXPECTED TIMETABLE(1)

– i –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

[REDACTED]

EXPECTED TIMETABLE(1)

– ii –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

[REDACTED]

EXPECTED TIMETABLE(1)

– iii –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

[REDACTED]

EXPECTED TIMETABLE(1)

– iv –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

IMPORTANT NOTICE TO INVESTORS

This document is issued by us solely in connection with the [REDACTED] and does

not constitute an offer to sell or a solicitation of an offer to buy any securities other than

the [REDACTED] offered by this document pursuant to the [REDACTED]. This

document may not be used for the purpose of, and does not constitute, an offer or

invitation in any other jurisdiction or in any other circumstances. No action has been

taken to permit a [REDACTED] of the [REDACTED] in any jurisdiction other than

Hong Kong and no action has been taken to permit the distribution of this document in

any jurisdiction other than Hong Kong. The distribution of this document for purposes of

a [REDACTED] and the [REDACTED] and sale of the [REDACTED] in other

jurisdictions are subject to restrictions and may not be made except as permitted under

the applicable securities laws of such jurisdictions pursuant to registration with or

authorisation by the relevant securities regulatory authorities or an exemption therefrom.

You should rely only on the information contained in this document and the GREEN

Application Forms to make your investment decision. We have not authorised anyone to

provide you with information that is different from what is contained in this document.

Any information or representation not contained nor made in this document and the

[REDACTED] must not be relied on by you as having been authorised by us, the Sole

Sponsor, the [REDACTED], the [REDACTED], the [REDACTED], the

[REDACTED], any of our or their respective directors, officers, employees, agents or

representatives or any other parties involved in the [REDACTED].

Page

EXPECTED TIMETABLE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [i]

CONTENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [v]

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [1]

DEFINITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [27]

GLOSSARY OF TECHNICAL TERMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [40]

FORWARD-LOOKING STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [50]

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [52]

INFORMATION ABOUT THIS DOCUMENT ANDTHE [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [83]

CONTENTS

– v –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DIRECTORS AND PARTIES INVOLVED IN THE [REDACTED] . . . . . . . . . . . [89]

CORPORATE INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [93]

INDUSTRY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [95]

REGULATORY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [118]

HISTORY, REORGANISATION AND CORPORATE STRUCTURE . . . . . . . . . . [147]

BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [164]

RELATIONSHIP WITH CONTROLLING SHAREHOLDERS . . . . . . . . . . . . . . [279]

DIRECTORS AND SENIOR MANAGEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . [283]

SUBSTANTIAL SHAREHOLDERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [297]

SHARE CAPITAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [298]

FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [302]

FUTURE PLANS AND USE OF [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . [357]

[REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [367]

STRUCTURE OF THE [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [379]

HOW TO APPLY FOR [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . [391]

APPENDIX I – ACCOUNTANT’S REPORT . . . . . . . . . . . . . . . . . . . . . . I-1

APPENDIX II – UNAUDITED PRO FORMA FINANCIALINFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-1

APPENDIX III – PROPERTY VALUATION REPORT . . . . . . . . . . . . . . . III-1

APPENDIX IV – SUMMARY OF THE CONSTITUTION OF THECOMPANY AND CAYMAN COMPANY LAW . . . . . IV-1

APPENDIX V – STATUTORY AND GENERAL INFORMATION . . . . . V-1

APPENDIX VI – DOCUMENTS DELIVERED TO THE REGISTRAROF COMPANIES AND AVAILABLE ON DISPLAY . VI-1

CONTENTS

– vi –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

This summary aims to give you an overview of the information contained in this

document. Since this is a summary, it does not contain all the information that may be

important to you. You should read the whole document, before you decide to invest in the

[REDACTED]. There are risks associated with any investment. Some of the particular

risks in investing in the [REDACTED] are set forth in the section headed “Risk Factors”

in this document. You should read that section carefully before you decide to invest in the

[REDACTED].

OVERVIEW

We are a specialised end-to-end electronics development and manufacturing services

provider focused on customised IoT and jointly-developed products for demanding customers

across the world, particularly those in specialised and highly-regulated industries such as the

automotive, aerospace, medical, marine, banking, security and wireless communication

network industries. As an electronic manufacturing services (“EMS”) provider, we provide our

customers integrated product design and development, manufacturing and validation solutions

for electronic products and sub-assemblies. We work in close collaboration with our customers

at all stages of the product cycle to deliver customised end-to-end solutions for complicated

projects.

We offer a comprehensive range of services including initial product specification and

development, hardware and mechanical product design, selection of components, sub-supplier

management, performance testing of parts and products and product certification. In particular,

our on-site accredited laboratory in Dongguan allows for real time product and part verification

and validation and environmental testing under “one roof” and can help increase process

efficiency and minimise our customers’ time to market.

We develop and produce electronics products, including complete electronic products,

sub-assemblies and assembled PCBs, in response to specific customer requests for customers

in a variety of different industries. Examples of products we produced during the Track Record

Period include power management systems for commercial aircraft, marine navigational

systems, intelligent driver surveillance systems, ultra low power IoT utility meters and IoT

devices and monitoring systems for elderly persons, among many others.

We are often actively involved in the early stages of product conceptualisation and

development for our customers. As such, our research and development capabilities are key to

our success. In the context of our business model and consistent with other EMS providers,

R&D does not generally relate to the invention of new technologies, but primarily to skilful

application of the latest technologies in the pursuit of product engineering, development and

approval of new products, development of new product concepts and other product engineering

activities such as the development of specific test and production processes. As at 31 March

2022, we had over 300 engineers carrying out our R&D activities. These engineers cover a

variety of relevant fields, including electrical hardware engineering, software engineering,

SUMMARY

– 1 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

mechanical engineering and information technology. According to the Frost & Sullivan Report,

our ratio of R&D expenses to revenue (5.3%, 4.2% and 4.4% in FY2020, FY2021 and FY2022,

respectively) indicates a higher focus on R&D and new product development capabilities than

other leading EMS providers in the specialised electronics segment, who generally have R&D

expenses to revenue ratios ranging from 1% to 2%. We expense all of our R&D expenses as

staff costs and they are recognised in our consolidated income statement under cost of sales or

administrative expenses.

Areas in which we have developed particular proficiency include development and

manufacture of IoT devices and design, verification and production of rugged products that

need to be sealed from and operate reliably in harsh external environments, including products

that require waterproofing and protection from dust and other solid objects or which will

operate in conditions of extreme temperatures and/or humidity. See “Business – Our Core

Technological Competencies” for details. In particular, we believe our in-house development

of IoT solutions provides us with a competitive edge in this growing market, particularly in

niche product segment areas which require real-time and accurate information. We have the

ability to develop and to demonstrate total solutions for new innovative IoT applications to

potential customers. In FY2020, FY2021 and FY2022, revenue from IoT devices and modules

represented approximately 39.8%, 58.6% and 59.4%, respectively, of our total revenue for the

year, and we plan to continue to invest further in our IoT capabilities to facilitate growth of

revenue from this sector.

COMPETITIVE STRENGTHS

We believe the following competitive strengths contribute to our success and differentiate

us from our competitors: (i) we have comprehensive solutions spanning the development,

testing, verification and manufacturing stages of complex projects for highly-regulated

industries; (ii) we have strong long-term relationships with customers spanning multiple key

specialised industry sectors; (iii) we have strategically-located, top-tier facilities; (iv) we are

well-positioned to benefit from growth in the electronics industry, in particular with respect to

RF/IoT related electronic applications in various industries; and (v) we have stable,

experienced management team with deep industry knowledge and technical knowhow who has

established a strong corporate culture. See “Business – Our Competitive Strengths” for further

details.

OUR BUSINESS STRATEGIES

We aim to strengthen our position in the market for providing development and

manufacturing services for the industrial electronics sector by increasing our scope and

enhancing the quality of our services. We aim to achieve these objectives through the following

principal business strategies: (i) increase our IoT business capabilities and market presence;

(ii) increase our production capacity and upgrade our production facilities; (iii) invest in

sustainable manufacturing capabilities; and (iv) expand our operations into new jurisdictions

through acquisition. See “Business – Our Business Strategies” for further details.

SUMMARY

– 2 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

OUR BUSINESS MODEL

Our revenue is derived from assembling and manufacturing products for sale to ourcustomers, as well as from the fees that we charge for our value-added product developmentservices. We generally price our products, inclusive of manufacturing services, on a “cost-plus”basis agreed between us and our customers.

Our customers typically engage us on a Joint Development or OEM basis. For JointDevelopment Projects, we engage in hardware, mechanical and software design for the projectin conjunction with our customer’s in-house design team and/or take a major role in productand component validation services. For OEM projects, our customers provide the key elementsof hardware, mechanical and software design for the project and lead the validation activities.However, even on projects for which we are not engaged to develop a product, we offer a rangeof ancillary services to support the process. Many of our major OEM customers still use ourengineers to manage the design of production and test equipment as well as manage localsuppliers. Such activities include supplier sourcing and tooling bring-up and will also ask usto carry out product and component validation work. For all projects, we will engage with ourcustomer’s engineering teams to carry out Design for Manufacturing, Design for Assembly andDesign for Test reviews to ensure the products are able to be produced without major yieldissues or inefficient procedures. See “Business – Our Business Model” for a description of theactivities we carry out throughout the design and production process when engaged on a jointdevelopment or OEM basis.

The following table sets forth a breakdown of our revenue by business model for the yearsindicated:

Business Model FY2020 FY2021 FY2022HK$’000 % HK$’000 % HK$’000 %

Joint Development 594,682 42.6 989,745 54.9 995,048 47.6OEM 800,379 57.4 811,925 45.1 1,093,727 52.4

Total 1,395,061 100.0 1,801,670 100.0 2,088,775 100.0

The following table sets forth a breakdown of our gross profit margin by business modelfor the years indicated:

Business Model FY2020 FY2021 FY2022% % %

Joint Development 16.3 14.0 14.8OEM 20.7 19.2 17.1

Overall Gross Profit Margin 18.8 16.3 16.0

SUMMARY

– 3 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

OUR PRODUCTION FACILITIES

As at the Latest Practicable Date, we had production plants in two locations: one plant in

Dongguan, the PRC and two plants in Penang, Malaysia. Our production facilities in Dongguan

and Penang are fully-functional and are equipped with a wide range of advanced automated

machinery and equipment for our production processes, including SMT assembly, wave

soldering and aqueous cleaning, in addition to testing and laboratory capabilities. We also have

offices and a workshop in Hong Kong providing product refurbishment and repair services. We

have office premises located in Xili, Shenzhen, the PRC, which acts as our operations centre

to carry out a range of services, including R&D services, engineering, purchasing, sales and

marketing, IT, finance and human resources management.

We relocated and expanded our production facilities during the Track Record Period. In

FY2020 we relocated our PRC production facilities from leased premises in Shenzhen to new,

larger premises we constructed in Dongguan. We acquired the land for our Dongguan site in

May 2018, began setting up production lines there in October 2019 and commenced production

in December 2019. We continued to gradually relocate our production and equipment from

Shenzhen to Dongguan through March 2020, at which time we vacated the premises and the

land upon which the Shenzhen production facilities were located was returned to the landlord.

This migration did not result in any suspension of operation or adversely affect our revenue.

Since that time, our production facilities in Dongguan have served as our main production

facilities. Over the Track Record Period, we incurred capital expenditure of RMB123.3 million

(equivalent to HK$139.2 million) for construction of our Dongguan production facilities.

In order to expand our production capacity and diversify our operations given the

unpredictable nature of recent global events, in particular growing Sino-US trade tensions and

announcement of US tariffs on certain types of goods exported from the PRC, we commenced

operations in our production facilities in Penang, Malaysia in 2019. In February 2019, we

leased a site with GFA of 6,038 sq.m, and leased a second site with GFA of 5,888 sq.m. in

September 2020 to further expand the scope of our business operations in Penang. In order to

further expand our production facilities in Penang and consolidate them in a single location,

in January 2021, we purchased a larger third site with a GFA of 32,702 sq.m. at consideration

of MYR31.8 million (equivalent to HK$58.8 million). We commenced operations at this third

site in March 2022 and expect to complete migration of all equipment and operations to the site

by the end of 2022, at which point it will function as our sole operational location in Penang.

This third site will provide enough space to absorb the operations of our first two Penang sites

as well as provide significant room for future expansion. We ceased operations at our first

Penang production site following commencement of operations at our new third Penang site in

March 2022.

The expansion and relocation of our production facilities have impacted our consolidated

income statements, consolidated statements of financial position, and consolidated statements

of cash flows for the Track Record Period in a number of ways, including (i) significant cash

outflows for purchases of property, plant and equipment amounting to approximately

HK$144.2 million, HK$118.3 million and HK$46.1 million in FY2020, FY2021 and FY2022,

SUMMARY

– 4 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

respectively, most of which related to our new production facilities in Dongguan and Penang,

(ii) payment of severance compensation to redundant employees with respect to our closure of

our site in Shenzhen and relocation of our production facilities to Dongguan, which contributed

to net operating cash outflow of approximately HK$17.6 million in FY2020, (iii) additional

bank borrowings to finance such expansion and (iv) increased depreciation expenses relating

to our property, plant and equipment and right-of-use assets. See “Financial Information –

Factors Affecting our Financial Results – Expansion and relocation of our production

facilities”.

The table below sets forth the utilisation rate of our SMT lines for the years indicated, as

well as our projected total production capacity in terms of maximum potential SMT run hours

for the years ending 31 March 2023, 2024 and 2025, respectively:

FY2020 FY2021 FY2022 FY2023 FY2024 FY2025

PRC Production 8.5 lines(4)(5) 8 lines(5) 8 linesTotal actual SMT run

hours 31,479 42,526 45,027Maximum potential SMT

run hours(1) 48,017(5) 45,192(5) 45,192Utilisation rate(2) 65.6% 94.1%(6) 99.6%

Penang Production 0.5 lines(4) 1.75 lines(4) 2 linesTotal actual SMT run

hours 1,257 4,929 6,265Maximum potential SMT

run hours(1) 2,825 9,886 11,298Utilisation rate(2)(3) 44.5% 49.9%(6) 55.5%

Total across PRC andPenang Production 9 lines 9.75 lines(4) 10 lines 10.5 lines(4) 11.5 lines(4) 12.75 lines(4)

Total actual SMT run

hours 32,736 47,455 51,292Maximum potential SMT

run hours(1) 50,841 55,078 56,490 59,315 64,964 72,025Utilisation rate(2) 64.4% 86.2%(6) 90.8%

Notes:

1. Assuming maximum operating time of 21 hours a day and 22 days a month across our PRC and Penang sites.

2. Based on total actual hours of operation divided by maximum potential hours of operation over the year.

3. The relatively low utilisation rates in our Penang production facilities over the Track Record Period werelargely the result of our Penang operations being in the initial set-up stage. See “Business – Our BusinessStrategies – Increase our production capacity and upgrade our production facilities – 2. Upgrade and expandfunctionality at our production facilities in Penang” for further details.

4. Partial lines are due to retirement/new purchase of SMT lines during the year.

SUMMARY

– 5 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

5. The decrease in the number of SMT lines in the PRC and the resulting decrease in maximum potential SMTrun hours in the PRC related to the retirement of one older SMT production line during FY2020.

6. The increase in utilisation rate in the PRC from 65.6% in FY2020 to 94.1% in FY2021 was due to increasedproduction in FY2021, in-line with total increase in our revenue from HK$1,395.1 million in FY2020 toHK$1,801.7 million in FY2021, on 0.5 fewer lines, as one older SMT production line was retired duringFY2020. Production increases in Penang were largely offset by introduction of one additional SMT line in the

first half of FY2021.

OUR CUSTOMERS

We have built strong, long-term relationships with reputable multi-national companies,

including global leaders in a wide range of demanding industries, including the automotive,

medical, aerospace, marine, insurance, banking and wireless communications network

industries. We focus on customers in industries that are highly regulated and require a high

degree of specialised technical knowledge and target customers who are undertaking

challenging tasks that EMS companies may not have the capability, or patience, to support.

Through providing end-to-end solutions and engineering services, we have developed strong

working relations with numerous teams throughout our customers’ company structure. Our

customers also typically make significant investments in time and resources to approve our

production processes and product-specific assembly and production test solutions. As a result,

we have generally retained our customers and have continued to work with them on an

on-going basis. Over the Track Record Period, 85.3% of our total revenue came from customers

with whom we had worked for over 10 years.

The following table sets out a breakdown of our revenue by our customers’ industry sector

for the years indicated:

Industry Sector FY2020 FY2021 FY2022HK$’000 % HK$’000 % HK$’000 %

Transportation(1) 483,645 34.7 392,485 21.8 485,411 23.2Medical/Assisted

Living/Wellness 354,850 25.4 406,954 22.5 591,302 28.3Smart Module/

Smart Device 260,576 18.7 644,104 35.8 635,779 30.5Communication/Postal 215,718 15.5 293,490 16.3 317,747 15.2Others(2) 80,272 5.7 64,637 3.6 58,536 2.8

Total 1,395,061 100.0 1,801,670 100.0 2,088,775 100.0

Notes:

1. Transportation primarily included the aerospace, marine and automotive industries.

2. Others primarily included other products, sub-assemblies and PCBAs, for industrial applications not includedin the above, such as commercial X-Ray machines and audio/video streaming equipment.

SUMMARY

– 6 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

The following table sets out a breakdown of our gross profit margin by our customers’

industry sector for the years indicated:

Industry Sector FY2020 FY2021 FY2022% % %

Transportation(1) 20.5 17.6 25.7Medical, assisted living, and wellness 16.9 17.7 10.0Smart module and smart device 16.3 12.3 11.2Communication and postal 20.5 20.4 20.1Others(2) 20.7 22.0 26.2

Overall Gross Profit Margin 18.8 16.3 16.0

Notes:

1. Transportation primarily included the aerospace, marine and automotive industries.

2. Others primarily included other products, sub-assemblies and PCBAs, for industrial applications notincluded in the above, such as commercial X-Ray machines and audio/video streaming equipment.

Gross profit margin by industry sector generally reflected the decreases exhibited by our

overall gross profit margin over the Track Record Period, as further discussed below. See “–

Summary Consolidated Financial Information”, “Financial Information – Principal Items in the

Consolidated Income Statements”.

In particular, gross profit margin from customers in the transportation industry sector

decreased from 20.5% in FY2020 to 17.6% in FY2021 as demand from aerospace, which was

particularly hit by COVID-related travel restrictions, decreased. As demand from customers in

the aerospace sector recovered in FY2022, gross profit margins from customers in the

transportation sector also increased to 25.7%.

Revenue contribution from customers in the smart module and smart device industry

sector increased significantly over the Track Record Period, from HK$260.6 million in FY2020

to HK$635.8 million in FY2022. Gross profit margins over the same period decreased, largely

due to the execution of large volume projects for Customer A, which due to their overall size

and batch size contributed to an increase in the revenue and gross profit generated from the

smart modules/smart devices industry from FY2020 to FY2022 and justified lower margins.

Gross profit margin from customers in the medical, assisted living and wellness industry

sector increased from 16.9% in FY2020 to 17.7% in FY2021. Gross profit margin decreased

to 10.0% in FY2022, largely due to product mix, as we sold a large amount of a lower-margin

product to a customer in this sector over the year.

SUMMARY

– 7 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Gross profit margin from customers in the communications and postal industry sector

remained relatively stable over the Track Record Period at 20.5% in FY2020, 20.4% in FY2021

and 20.1% in FY2022.

Our products are sold to customers throughout the world, primarily in North America,

Europe and Asia-Pacific (including Australia). The following table sets out a breakdown of our

revenue by geographical location for the years indicated:

GeographicRegion(1)

FY2020 FY2021 FY2022HK$’000 % HK$’000 % HK$’000 %

Europe 732,173 52.5 1,073,497 59.6 1,302,074 62.3North America 480,635 34.5 397,252 22.0 498,293 23.9Asia-Pacific 178,540 12.8 329,282 18.3 288,340 13.8Others(2) 3,713 0.2 1,639 0.1 68 0.0

Grand Total 1,395,061 100.0 1,801,670 100.0 2,088,775 100.0

Notes:

1. The breakdown is based on the location of the contracting party of our customers. Our customers, inparticular multinational corporations, may place purchase orders from various regional offices. Thelocations where our products are ultimately used may be different from the location of the contractingentity.

2. Others mainly includes locations in South America.

For FY2020, FY2021 and FY2022, the revenue attributable to our five largest customers

amounted to HK$699.2 million, HK$1,211.1 million and HK$1,354.1 million, representing

50.2%, 67.2% and 64.7%, respectively, of our total revenue for the year and the revenue

attributable to our largest customer amounted to HK$185.9 million, HK$575.9 million and

HK$548.0 million, representing 13.3%, 32.0% and 26.2%, respectively, of our total revenue for

the year. All of our five largest customers during the Track Record Period are Independent

Third Parties.

SUMMARY

– 8 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

The following table sets out a breakdown of our gross profit margin by geographical

location for the years indicated:

Geographic Region(1) FY2020 FY2021 FY2022% % %

Europe 15.6 14.0 12.4North America 22.2 20.3 23.8Asia-Pacific 23.0 19.3 18.8Others(2) 20.7 15.1 15.3

Overall Gross Profit Margin 18.8 16.3 16.0

Notes:

1. The breakdown is based on the location of the contracting party of our customers. Our customers, inparticular multinational corporations, may place purchase orders from various regional offices. Thelocations where our products are ultimately used may be different from the location of the contractingentity.

2. Others mainly includes locations in South America.

Gross profit margin by geographic location generally reflected the decreases exhibited by

our overall gross profit margin over the Track Record Period, as further discussed below. See

“– Summary Consolidated Financial Information”, “Financial Information – Principal Items in

the Consolidated Income Statements”.

Revenue contribution from orders placed by customers in Europe increased significantly

over the Track Record Period, representing 59.6% of total revenue in FY2021 and 62.3% of

total revenue in FY2022. Much of this growth was driven by customers in the smart modules

and devices industry sector. As a result gross profit margins for Europe decreased over the

Track Record Period.

Gross profit margin from orders placed by customers in North America decreased from

22.2% in FY2020 to 20.3% in FY2021, largely reflecting downturns in the aerospace and

commercial postal and printing industries. As demand, particularly from customers in the

aerospace industry recovered in FY2022, gross profit margins from customers in North

America also recovered to 23.8%.

Gross profit margin from orders placed by customers in Asia-Pacific decreased from

23.0% in FY2020 to 18.8% in FY2022, primarily due to the execution of a large scale project

for Customer E, which resulted in them being one of our five largest customers in FY2021 and

FY2022.

SUMMARY

– 9 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

OUR SUPPLIERS

During the Track Record Period, we purchased materials, components and parts

predominantly from the PRC, the United States, Europe, Hong Kong, Australia, Japan and

Taiwan and had over 700 suppliers in each of FY2020, FY2021 and FY2022. For FY2020,

FY2021 and FY2022, purchases from our five largest suppliers amounted to HK$236.6 million,

HK$455.2 million and HK$499.5 million, representing 26.1%, 37.2% and 30.5% of our total

purchases, respectively. In the same years, purchases from our largest supplier amounted

HK$105.1 million, HK$174.0 million and HK$198.2 million, representing 11.6%, 14.2% and

12.1% of our total purchases for the same years, respectively. All of our five largest suppliers

during the Track Record Period are Independent Third Parties.

MAJOR CUSTOMERS WHO WERE ALSO OUR SUPPLIERS

During the Track Record Period, to the best knowledge and belief of our Directors, four

of our major customers were also our suppliers with respect to certain purchases we made for

projects on which they were our customers. In FY2020, FY2021 and FY2022, purchases from

these four customers represented 0.3%, 0.2% and 1.4% of our total purchases for the year. The

reasons for these purchases generally related to situations in which the customer was better

able to procure needed materials, such as in cases of material shortages. Based on their

experience in the electronics manufacturing and development services market in the PRC, our

Directors note that the practice of purchasing materials, components and parts from customers

is commonly adopted in this market in the circumstances.

COMPETITIVE LANDSCAPE

According to the Frost & Sullivan Report, the specialised electronics sector of the EMS

market in the PRC is relatively fragmented with approximately over 600 industry players in

2021 and the top 10 EMS providers in the sector accounting for an aggregate market share of

approximately 59.5% in 2021. The high degree of fragmentation in the specialised electronics

sector of the EMS market is attributed to the wide variety of products and coverage of

industries, including but not limited to, industrial, automotive, medical, and other applications.

According to the Frost & Sullivan Report, based on the revenue generated from sales of

products manufactured in the PRC, it is estimated that we had a market share of approximately

0.1% and 0.2% in the overall EMS market and specialised electronics segment, respectively,

in the PRC in 2021.

SUMMARY CONSOLIDATED FINANCIAL INFORMATION

The following tables set forth a summary of our financial information for FY2020,

FY2021 and FY2022. The summary consolidated financial information has been prepared in

accordance with HKFRS. You should read this summary together with the consolidated

financial information as set forth in the Accountants’ Report in Appendix I to this document,

including the related notes, as well as the information set forth in “Financial Information” in

this document.

SUMMARY

– 10 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Summary consolidated income statements

FY2020 FY2021 FY2022HK$’000 HK$’000 HK$’000

Revenue 1,395,061 1,801,670 2,088,775Cost of sales (1,132,464) (1,507,434) (1,754,213)

Gross profit 262,597 294,236 334,562Administrative expenses (190,852) (189,133) (217,609)Distribution costs (5,783) (5,689) (5,830)Reversal of impairment

loss on financial assets, net 239 52 169Other income 9,688 7,631 3,574Other (losses)/gains, net (26,223) 23,371 16,023

Operating profit 49,666 130,468 130,889- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Finance income 1,007 509 2,576Finance costs (4,199) (10,883) (9,857)

Finance costs, net (3,192) (10,374) (7,281)- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Profit before income tax 46,474 120,094 123,608Income tax expense (13,888) (30,455) (28,828)

Profit for the year 32,586 89,639 94,780

SUMMARY

– 11 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Non-HKFRS Measure

To supplement our consolidated income statements which are presented in accordance

with HKFRS, we also use adjusted profit as an additional financial measure. We present this

financial measure because it is used by our management to evaluate our operating performance

as it excludes charges and gains our management do not expect to recur and thus provides

useful information on our on-going business. We believe that such non-HKFRS measure

provides useful information to investors in understanding and evaluating our results of

operations in the same manner as it helps our management and in comparing financial results

across accounting periods and to those of our peer companies.

Adjusted profit eliminates the effects of (i) [REDACTED] expenses and (ii) government

grants received. The term of adjusted profit is not defined under HKFRS. The use of adjusted

profit has material limitations as an analytical tool, as adjusted profit does not include all items

that impact our profit for the year. We compensate for these limitations by reconciling this

financial measure to the nearest HKFRS performance measure, which should be considered

when evaluating our performance. The following table reconciles our adjusted profit for the

year presented to profit for the year, the most directly comparable financial measure calculated

and presented in accordance with HKFRS:

FY2020 FY2021 FY2022HK$’000 HK$’000 HK$’000

Profit for the year 32,586 89,639 94,780Add:[REDACTED] expenses 885 825 14,430

Less:Government grants (9,045) (7,386) (3,341)

Adjusted profit (Non-HKFRS measure) 24,426 83,078 105,869

Our revenue in FY2020 was relatively low, primarily due to the outbreak of the

COVID-19 pandemic and measures taken in response to the pandemic which resulted in the

closure of our production facilities in the PRC from 18 January 2020 to 9 February 2020, and

in Penang from 18 March 2020 through 8 April 2020 and further closed down from 19 October

2021 to 27 October 2021 in order to prevent spreading of COVID-19 as stipulated by the

Malaysian government. Moreover, production in our PRC production facilities ramped up

gradually over the course of February 2020 and March 2020 as our workers, many who had

returned home for the Chinese New Year, returned back to work. Certain products originally

expected to launch in FY2020 were delayed until FY2021. The delivery of products accounting

for approximately HK$106.1 million of revenue originally scheduled to be made in FY2020

was postponed to FY2021 (of which approximately HK$58.8 million was due to component

shortages). Our revenue increased approximately 29.1% from FY2020 to FY2021, primarily

due to full operation of our production facilities and increased orders in FY2021. For FY2022,

our revenue increased approximately 15.9% as compared with the previous year, driven

primarily by increased sales and revenue from customers in the medical, assisted living and

SUMMARY

– 12 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

wellness and transportation industry sectors. To a lesser extent, the increase in revenuestracked increases in prices due to spot-buying of materials and components due to supplyconstraints stemming from the global shortages of IC components. Such spot buys are onlymade after our customer authorises such purchases and agrees that any increase in cost is alsoadded to the price of the product. Additional revenue and equivalent amounts of costs of salesfrom spot-buys increased from HK$6.2 million in FY2021 to HK$87.8 million in FY2022.

Our cost of sales primarily includes cost of inventory sold and staff costs. For FY2020,FY2021 and FY2022, cost of inventory sold accounted for 78.6%, 82.9% and 82.9%,respectively, and staff costs accounted for 13.2%, 10.9% and 10.8%, respectively, of our totalcost of sales for the period.

The decrease of gross profit margin from 18.8% for FY2020 to 16.3% for FY2021 wasprimarily due to (i) increased depreciation expenses related to increased purchases of property,plant and equipment in connection with the opening of, and relocation of our operations to, ourproduction facilities in Dongguan, the PRC, and Penang, Malaysia, and (ii) a shift in productmix in FY2021, in particular as (a) revenue contribution and gross profit margin fromcustomers in the transportation industry sector decreased as demand from aerospace, whichwas particularly hit by COVID-related travel restrictions, decreased; and (b) revenuecontribution from customers in the smart module and smart device industry sector increasedsignificantly while gross profit margins decreased, largely due to execution of large volumeprojects, as further discussed below. Gross profit margin remained relatively stable at 16.3%in FY2021 and 16.0% at FY2022. There was an increase in spot-buys in FY2022, whichresulted in an additional HK$87.8 million in spot-buy premiums being added to both revenueand cost of sales in FY2022 (compared to HK$6.2 million in FY2021). Due to our customersagreeing to increase price to cover any increase in costs, this adjustment had no effect on ourgross profit but lowered gross profit margin for the periods.

Operating profit and profit for the year also decreased in FY2020 mainly attributable todecreased production and sales in FY2020 due to the effect of the COVID-19 pandemic as‘detailed above. In addition, the costs of commencing operations and transferring productionto Penang and Dongguan during FY2020 were significant. For example, they included the costof operation of a fully-loaded new factory in Penang while output was minimal. We alsoincurred additional costs in connection with shifting our production to new productionfacilities: from Shenzhen to Dongguan in the PRC and to Penang in Malaysia. All projectsbegun in, or moved to, such new production facilities and equipment installed needed to gothrough extensive validation and acceptance tests before mass production of any product couldbegin. Other costs during this time included the training of new staff in Penang, the travel ofstaff between Penang and Dongguan to facilitate the transfer of knowledge andtroubleshooting, and other duplicated cost of organisation associated with running multiplesites in parallel, which was not the case in FY2019. These costs adversely affected ouroperating profit and profit for the year in FY2020 and were only partly offset by governmentgrants and waiver of social insurance in FY2020. Operating profit remained relatively stableat HK$130.5 million for FY2021 and HK$130.9 million for FY2022. However, profit for theyear increased from FY2021 to FY2022 primarily due to a decrease in effective tax rate as wewere able to use previously unrecognised tax losses and there was no withholding tax ondividends as compared to withholding tax on dividends of HK$4.8 million in FY2021.

SUMMARY

– 13 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Summary consolidated statements of financial position

As at 31 March2020 2021 2022

HK$’000 HK$’000 HK$’000

Non-current assets 526,000 623,176 655,216Current assets 764,170 964,698 1,208,878Inventories 300,613 351,475 583,620Trade receivables 183,519 275,915 355,006Deposits, prepayments and other receivables 70,729 56,657 51,896Pledged deposits 9,316 70,735 9,070Cash and cash equivalents 198,640 206,285 204,839

Current liabilities 645,510 843,554 1,123,713Trade payables 221,689 310,862 401,606Other payables and accruals 255,417 326,817 335,701Income tax liabilities 8,508 899 14,083Bank borrowings 149,905 192,859 359,659Lease liabilities 9,991 12,117 12,131Provisions – – 533Net current assets 118,660 121,144 85,165Non-current liabilities 29,224 23,865 13,761Equity attributable to owners of the

Company 615,436 720,455 726,620

Our net current assets increased from HK$118.7 million as at 31 March 2020 to

HK$121.1 million as at 31 March 2021 primarily due to (i) an increase of HK$92.4 million in

trade receivables, (ii) an increase of HK$61.4 million in pledged deposits, and (iii) an increase

of HK$50.9 million in inventories. These increases in current assets in FY2021 were partly

offset by (i) an increase of HK$89.2 million in trade payables, (ii) an increase of HK$71.4

million in other payables and accruals, and (iii) an increase of HK$43.0 million in bank

borrowings, which were primarily used to fund our new production facilities in Dongguan and

Penang. Our net current assets decreased from HK$121.1 million as at 31 March 2021 to

HK$85.2 million as at 31 March 2022 primarily due to (i) an increase of HK$90.7 million in

trade payables, (ii) an increase of HK$166.8 million in bank borrowings, (iii) an increase of

HK$13.2 million in income tax liabilities and (iv) a decrease of HK$61.7 million in pledged

deposits, largely offset by (i) an increase of HK$79.1 million in trade receivables, and (ii) an

increase of HK$232.1 million in inventories.

SUMMARY

– 14 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Our equity attributable to the owners of the Company increased from HK$615.4 million

as at 31 March 2020 to HK$720.5 million as at 31 March 2021 primarily due to total

comprehensive income of HK$125.0 million in FY2021. Our equity attributable to the owners

of the Company remained relatively stable at HK$720.5 million as at 31 March 2021 and

HK$726.6 million as at 31 March 2022.

Summary consolidated statements of cash flows

FY2020 FY2021 FY2022HK$’000 HK$’000 HK$’000

Operating cashflows before movement in

working capital 103,222 170,011 160,718Changes in working capital (100,961) 45,420 (190,879)Income tax paid (19,890) (27,796) (12,356)Net cash (used in)/generated from operating

activities (17,629) 187,635 (42,517)Net cash used in investing activities (141,939) (117,763) (44,111)Net cash generated from/(used in) financing

activities 82,460 (69,152) 80,884

For FY2020, we recorded cash outflow from operating activities of approximately

HK$17.6 million. This was primarily due to the payment of severance compensation to

redundant employees pursuant to the closing of our previous production facility in Shenzhen

and relocation of our production facilities to Dongguan in FY2019. In respect of such

restructuring measures, we had made provisions amounting to HK$76.9 million as at 31 March

2019 and all such provisions were fully paid as at 31 March 2020, thereby contributing towards

a net operating cash outflow for FY2020. For FY2022, we recorded cash outflow from

operating activities of approximately HK$42.5 million. This was primarily due to an increase

in inventories of HK$221.5 million in FY2022. Such increase was primarily due to (i) an

increase in production activities and orders, (ii) shortages in certain electronic components

causing longer lead times and increased raw materials inventories while we waited for delivery

of electronic components, and (iii) some of our customers giving us binding commitments so

that we could commence purchase of electronic components earlier and stockpile such

components to mitigate the effect of any potential shortages or increase in delivery lead times.

See “Risk Factors – Risks Related to our Business and our Industry – We had net operating cash

outflows for FY2020 and FY2022”

SUMMARY

– 15 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

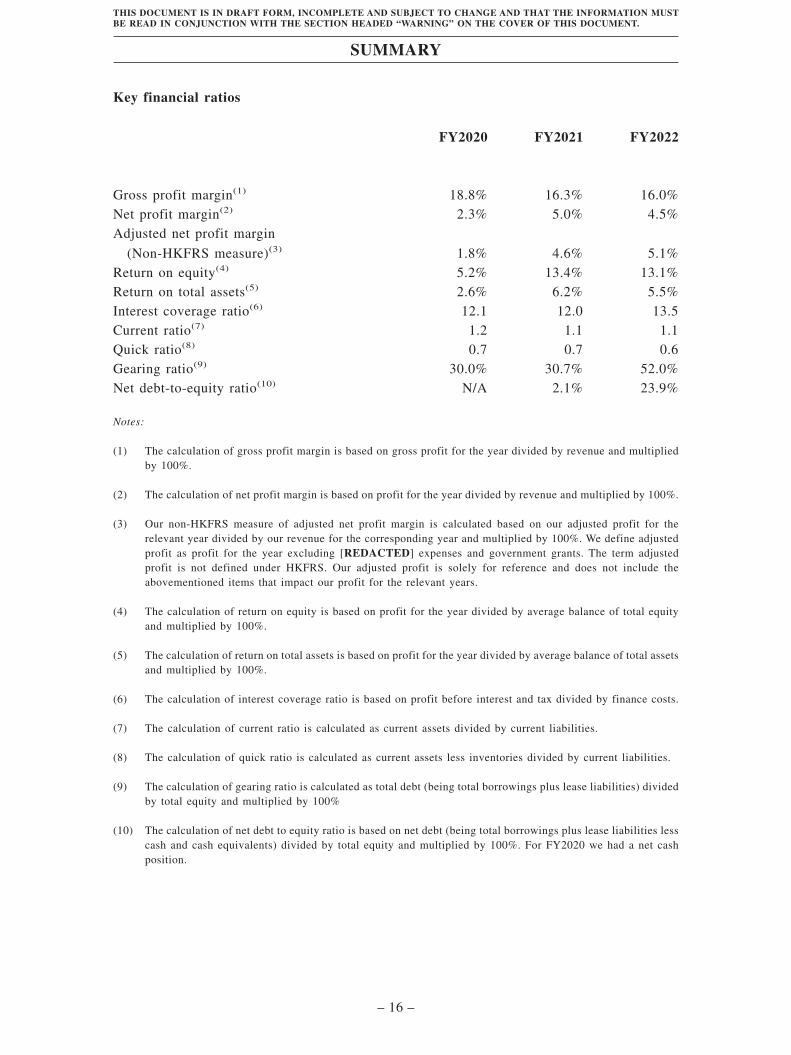

Key financial ratios

FY2020 FY2021 FY2022

Gross profit margin(1) 18.8% 16.3% 16.0%Net profit margin(2) 2.3% 5.0% 4.5%Adjusted net profit margin

(Non-HKFRS measure)(3) 1.8% 4.6% 5.1%Return on equity(4) 5.2% 13.4% 13.1%Return on total assets(5) 2.6% 6.2% 5.5%Interest coverage ratio(6) 12.1 12.0 13.5Current ratio(7) 1.2 1.1 1.1Quick ratio(8) 0.7 0.7 0.6Gearing ratio(9) 30.0% 30.7% 52.0%Net debt-to-equity ratio(10) N/A 2.1% 23.9%

Notes:

(1) The calculation of gross profit margin is based on gross profit for the year divided by revenue and multipliedby 100%.

(2) The calculation of net profit margin is based on profit for the year divided by revenue and multiplied by 100%.

(3) Our non-HKFRS measure of adjusted net profit margin is calculated based on our adjusted profit for therelevant year divided by our revenue for the corresponding year and multiplied by 100%. We define adjustedprofit as profit for the year excluding [REDACTED] expenses and government grants. The term adjustedprofit is not defined under HKFRS. Our adjusted profit is solely for reference and does not include theabovementioned items that impact our profit for the relevant years.

(4) The calculation of return on equity is based on profit for the year divided by average balance of total equityand multiplied by 100%.

(5) The calculation of return on total assets is based on profit for the year divided by average balance of total assetsand multiplied by 100%.

(6) The calculation of interest coverage ratio is based on profit before interest and tax divided by finance costs.

(7) The calculation of current ratio is calculated as current assets divided by current liabilities.

(8) The calculation of quick ratio is calculated as current assets less inventories divided by current liabilities.

(9) The calculation of gearing ratio is calculated as total debt (being total borrowings plus lease liabilities) dividedby total equity and multiplied by 100%

(10) The calculation of net debt to equity ratio is based on net debt (being total borrowings plus lease liabilities lesscash and cash equivalents) divided by total equity and multiplied by 100%. For FY2020 we had a net cashposition.

SUMMARY

– 16 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DIVIDENDS

Our Company has no fixed dividend policy specifying a dividend payout ratio. Any

amount of dividends we pay will be at the discretion of our Directors and will depend on our

future operations and earnings, capital requirements, contractual restrictions and others factors

which our Directors consider relevant. Any declaration and payment as well as the amount of

dividends will be subject to our constitutional documents and the Cayman Companies Act. Our

Shareholders in a general meeting may approve any declaration of dividends, which must not

exceed the amount recommended by our Board. No dividend shall be declared or payable

except out of our profits and reserves lawfully available for distribution. Our future

declarations of dividends may or may not reflect our historical declarations of dividends and

will be at the absolute discretion of the Board.

As at the Latest Practicable Date, no dividends had been declared or paid by our Company

since its incorporation. Pursuant to a directors’ resolution dated 17 June 2021, dividends of

HK$40 million were declared by In-Tech Investment, a company now comprising our Group,

to the equity holders of that company as at 31 March 2021. Such dividends were paid in cash

on 22 June 2021. Pursuant to a directors’ resolution dated 26 August 2021, dividends of HK$60

million were declared by In-Tech Investment to the equity holders of that company as at 31

March 2021. HK$4.5 million of such dividends were offset by the consideration of the disposal

of equity interests in a private company incorporated in the United Kingdom from our Group

to In-Tech Holdings on 30 September 2021, and the remaining HK$55.5 million were paid in

cash on 5 October 2021 using our internal resources. Pursuant to a directors’ resolution dated

31 May 2022, dividends of HK$125 million were declared by In-Tech Electronics HK to

In-Tech Electronics BVI, which in turn declared such dividends to its equity holders as at 31

March 2021. Pursuant to the resolution, such dividends are to be paid on or before 31

December 2022. As at 1 June 2022, none of such dividends have been paid.

CONTROLLING SHAREHOLDERS

Immediately following the completion of the Capitalisation Issue and the [REDACTED]

(assuming that the [REDACTED] is not exercised and without taking into account any Shares

to be issued upon exercise of any options which may be granted under the [REDACTED]

Share Option Scheme and the Share Option Scheme), In-Tech Holdings will be beneficially

interested in approximately [REDACTED]% of the issued share capital of our Company and

is accordingly entitled to exercise or control the exercise of 30% or more of the voting power

at general meetings of our Company. In-Tech Holdings is an investment holding company

owned as to 77.11% by Source Capital and 22.89% by Piggy Doggy. Source Capital is in turn

held by 15 shareholders. As these shareholders have decided to restrict their ability to exercise

control over In-Tech Holdings and thus our Company by holding their interests through a

common investment holding company, namely Source Capital, they are all presumed to be a

group of Controlling Shareholders, together with In-Tech Holdings and Source Capital. See

“Relationship with Controlling Shareholders” for further details.

SUMMARY

– 17 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

[REDACTED] SHARE OPTION SCHEME

Our Company has adopted the [REDACTED] Share Option Scheme on [●] 2022 and

granted options under the [REDACTED] Share Option Scheme to seven grantees, including

one Director and two senior management members, to subscribe for an aggregate of

[REDACTED] Shares, representing [REDACTED]% of the issued Shares immediately

following the completion of the Capitalisation Issue and the [REDACTED] (assuming no

exercise of the [REDACTED] or any options that may be granted under the [REDACTED]

Share Option Scheme or the Share Option Scheme). Assuming full exercise of the outstanding

options granted under the [REDACTED] Share Option Scheme, the shareholding of the

Shareholders immediately following completion of the Capitalisation Issue and the

[REDACTED] (assuming no exercise of the [REDACTED] or any options that may be

granted under the Share Option Scheme) will be diluted by approximately [REDACTED]% as

calculated based on [REDACTED] Shares then in issue. See “E. [REDACTED] Share Option

Scheme and Share Option Scheme – 1. [REDACTED] Share Option Scheme” in Appendix V

to this document for further details.

SHARE OPTION SCHEME

Our Company has conditionally adopted the Share Option Scheme on [●]. The principal

terms of the Share Option Scheme are set out in “E. [REDACTED] Share Option Scheme and

Share Option Scheme – 2. Share Option Scheme” in Appendix V to this document.

[REDACTED] EXPENSES

Assuming the [REDACTED] of HK$[REDACTED] per Share, being the mid-point of

the indicative range of the [REDACTED] stated in this document, and the [REDACTED] is

not exercised, the total amount of expenses in relation to the [REDACTED], including the

[REDACTED] commission, are estimated to be HK$[REDACTED] million (equivalent to

approximately [REDACTED]% of the expected gross [REDACTED]), of which (i)

[REDACTED] expenses (including but not limited to commissions and fees) amount to

HK$[REDACTED] million, and (ii) non-[REDACTED] expenses amount to

HK$[REDACTED] million, comprising fees and expenses of accountants of

HK$[REDACTED] million, fees and expenses of legal advisors of HK$[REDACTED]

million and other fees and expenses of HK$[REDACTED] million. Approximately

HK$[REDACTED] million of the total amount of expenses in relation to the [REDACTED]

is directly attributable to the [REDACTED] of the Shares to the public and will be accounted

for as a deduction from equity upon completion of the [REDACTED]. The remaining

estimated expenses in relation to the [REDACTED] of approximately HK$[REDACTED]

million was or will be charged to our profit or loss, of which approximately

HK$[REDACTED] million had been recorded in our consolidated income statements during

the Track Record Period, approximately HK$[REDACTED] million had been recorded in our

consolidated income statements during FY2019, and approximately HK$[REDACTED]

million is expected to be charged to our profit or loss for the year ending 31 March 2023.

SUMMARY

– 18 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

[REDACTED]

Based on theminimumindicative

[REDACTED] ofHK$[REDACTED]

per Share

Based on themaximumindicative

[REDACTED] ofHK$[REDACTED]

per ShareHK$ HK$

Market capitalisation upon completion of

the [REDACTED](2) [REDACTED] [REDACTED]Unaudited pro forma adjusted consolidated net tangible

assets per Share(3) [REDACTED] [REDACTED]

Notes:

1. All statistics in this table are based on the assumption that the [REDACTED] is not exercised. For details,please see “Appendix II – Unaudited Pro Forma Financial Information”.

2. The market capitalisation is calculated based on [REDACTED] Shares in issue immediately following thecompletion of the [REDACTED], which assumes that the [REDACTED] is not exercised and does not takeinto account any Shares which may be allotted and issued pursuant to the exercise of the options which maybe granted under the [REDACTED] Share Option Scheme and the Share Option Scheme.

3. The unaudited pro forma adjusted net tangible assets per Share is calculated after making the adjustments asset out in “Appendix II – Unaudited Pro Forma Financial Information” to this document and on the basis that[REDACTED] Shares are issued immediately following the completion of the Capitalisation Issue and the[REDACTED].

4. Save as disclosed above, no adjustment has been made to reflect any trading result or other transactions enteredinto subsequent to 31 March 2022.

(5) The unaudited pro forma adjusted consolidated net tangible assets of the Group does not take into account thedividend of approximately HK$125,000,000 declared by the Group on 31 May 2022. The unaudited pro formaadjusted consolidated net tangible assets per Share would have been HK$[REDACTED] andHK$[REDACTED] per Share based on the [REDACTED] of HK$[REDACTED] and HK$[REDACTED],respectively, after taking into account the declaration of dividend of HK$125,000,000.

SUMMARY

– 19 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

USE OF [REDACTED]

We estimate that the aggregate net [REDACTED] to us from the [REDACTED] (afterdeducting [REDACTED] fees and estimated expenses payable by us in connection with the[REDACTED], and assuming an [REDACTED] of HK$[REDACTED] per [REDACTED],being the mid-point of the indicative [REDACTED] range) will be approximatelyHK$[REDACTED] million, assuming that the [REDACTED] is not exercised. We currentlyintend to apply such net [REDACTED] in the following manner:

• approximately HK$[REDACTED] million, representing approximately[REDACTED]% of the net [REDACTED], will be used for increasing ourproduction capacity and upgrading our production facilities, including: (i)approximately HK$[REDACTED] million will be used for increasing ourproduction capacity, including: (a) approximately HK$[REDACTED] million willbe used for purchasing three SMT lines to replace existing SMT lines in ourDongguan facilities and purchasing three additional SMT lines and relatedequipment such as solder paste printers, inspection equipment, reflow ovens forPCB assembly, wave soldering machines, and AOI machines; and (b) approximatelyHK$[REDACTED] million will be used for additional component and producttesting facilities, including ICT and other testing stations and a new flying probetester, to increase our processing capacity to correspond with the additional SMTcapacity; and (ii) approximately HK$[REDACTED] million will be used forupgrading and expanding functionality at our production facilities, particularly inPenang, including: (a) approximately HK$[REDACTED] million will be used forrenovating our third site in Penang to bring it up to EMS standards; (b)approximately HK$[REDACTED] million will be used for the expansion andaccreditation of our reliability, environmental and product verification facilities; (c)approximately HK$[REDACTED] million will be used for hiring 21 additionalcustomer-facing engineers; and (d) approximately HK$[REDACTED] million willbe used for purchasing laboratory equipment related to new product introduction andlicencing;

• approximately HK$[REDACTED] million, representing approximately[REDACTED]% of the net [REDACTED], will be used for increasing our IoTbusiness capabilities and market presence, including: (i) approximatelyHK$[REDACTED] million will be used to invest in product development resourcesand equipment for IoT projects, including: (a) approximately HK$[REDACTED]million will be used for hiring an additional 21 engineers to handle the additionalproject volume, (b) approximately HK$[REDACTED] million will be used forpurchasing additional tools and equipment (including software development toolsand hardware validation equipment), and (c) approximately HK$[REDACTED]million will be used for funding of other project development expenses; and (ii)approximately HK$[REDACTED] million will be used for enhancing our B2B saleschannels and our global market presence by appointing six sales and marketingagents with technical backgrounds and relevant industry experience and increasingattendance at trade shows for relevant industries;

SUMMARY

– 20 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUSTBE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

• approximately HK$[REDACTED] million, representing approximately[REDACTED]% of the net [REDACTED], will be used for funding the acquisitionof an electronics product development and marketing company based in one of ourmajor markets;

• approximately HK$[REDACTED] million, representing approximately[REDACTED]% of the net [REDACTED], will be used for investing in sustainablemanufacturing capabilities in our production facilities in Dongguan and Penang,including: (i) approximately HK$[REDACTED] million will be used for purchasingand installing solar panels; and (ii) approximately HK$[REDACTED] million willbe used for developing and implementing our ongoing ESG initiatives,encompassing reduced water consumption, energy waste and usage of forestry;

• approximately HK$[REDACTED] million, representing approximately[REDACTED]% of the net [REDACTED], will be used for upgrading our ITcapabilities; and

• approximately HK$[REDACTED] million, representing approximately[REDACTED]% of the net [REDACTED], will be used for funding our generalworking capital.

RISK FACTORS