in Asia, Africa and the Middle East Annual Report and Accounts 2008-2009 Leading the way

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

in Asia, Africa and the Middle East

Annual Report and Accounts 2008-2009

Leading the way

Leading the way“2008 was a year of extraordinary dislocationand disruption in financial markets. Bankscollapsed or were rescued by governments,markets fell precipitously and economic growthstalled. Given our conservative business model,our clear strategy and our focus on the basics,Standard Chartered has weathered the stormrelatively well. We have not been unscathedbut we have continued to be open for businessfor customers and once again deliveredrecord profits.”Peter SandsGroup chief executive3 March 2009

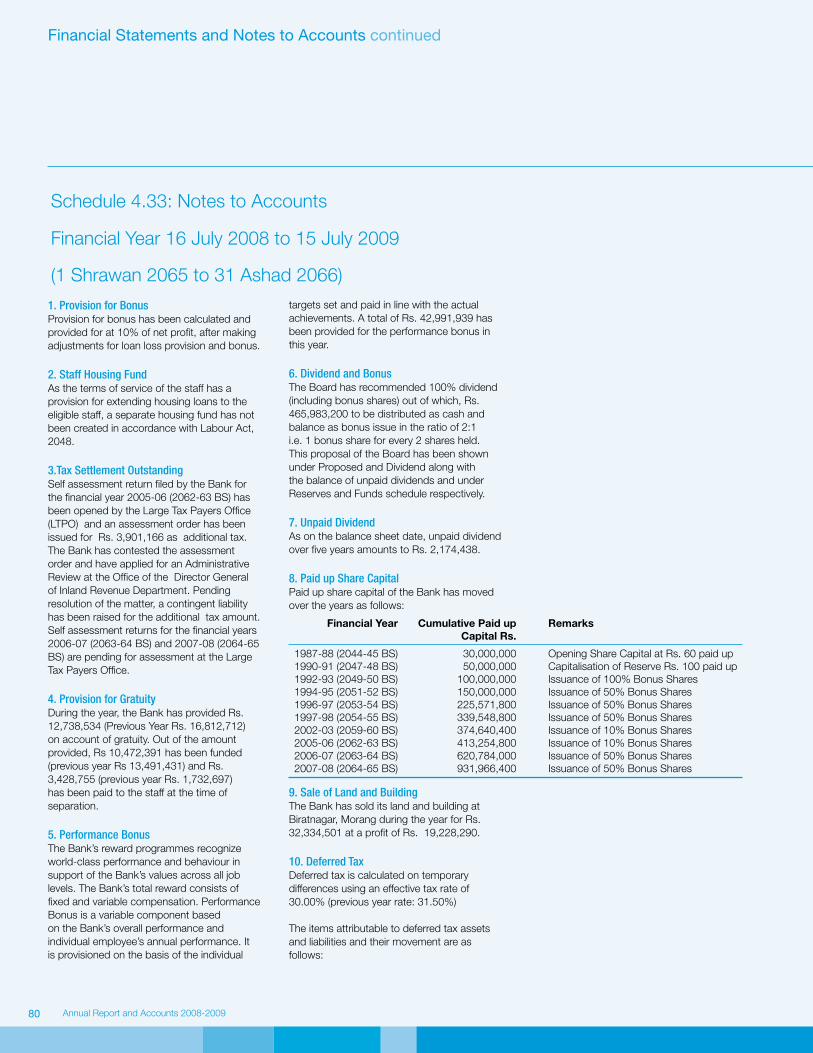

www.standardchartered.com

Standard Chartered PLC is headquartered in London where it is regulated by the UK’s Financial Services Authority. The Group’s head office providesguidance on governance and regulatory standards. Standard Chartered PLC stock code: 02888.

Note: Within this document ‘the Bank’ and ‘the Group’ refer to Standard Chartered PLC together with its subsidiary undertakings. The Hong Kong Special Administrative Regionof the People’s Republic of China is referred to as Hong Kong and includes Macau; India includes Nepal; The Republic of Korea is referred to as Korea or South Korea; Middle Eastand Other South Asia (MESA) includes, amongst others: Afghanistan, Bahrain, Bangladesh, Egypt, Jordan, Lebanon, Oman, Pakistan, Qatar, Sri Lanka, United Arab Emirates (UAE);and Other Asia Pacific includes, amongst others: Australia, Brunei, Cambodia, China, Indonesia, Japan, Laos, Mauritius, the Philippines, Taiwan, Thailand and Vietnam.

AsiaAfghanistanAustraliaBangladeshBruneiCambodiaChinaHong KongIndiaIndonesiaJapanKazakhstanLaosMacauMalaysiaMauritiusNepalPakistan

PhilippinesSingaporeSouth KoreaSri LankaTaiwanThailandVietnam

AfricaBotswanaCameroonCôte d’IvoireGhanaKenyaNigeriaSierra LeoneSouth AfricaTanzaniaThe GambiaUgandaZambiaZimbabwe

The Middle EastBahrainEgyptJordanLebanonOmanQatarUAE

EuropeAustriaFranceGermanyGuernseyIrelandItalyJerseyLuxembourgMonacoPolandRomaniaRussiaSpainSwedenSwitzerlandTurkeyUKUkraine

The AmericasArgentinaBahamasBrazilCanadaCayman IslandsChileColombiaFalkland IslandsMexicoPeruUruguayUSVenezuela

Our markets

Design by Black Sun Plc

Printed by Park Communications

Printed by Park Communications on FSC certifiedpaper. Park is a CarbonNeutral company and itsEnvironmental Management System is certified toISO14001:2004. 100% of the electricity used isgenerated from renewable sources, 100% of the inksused are vegetable oil based, 95% of press chemicalsare recycled and on average 99% of any wasteassociated with this production will be recycled.

This document is printed on Revive 50:50. Revive50:50 contains 50% recycled waste and 50% virginfibre and is fully recyclable, biodegradable, ElementalChlorine Free (ECF) and contains fibre from wellmanaged forests.

The laminate consists of cellulose acetatebiodegradable film made of wood pulp, also fromsustainable managed forests.

This document is fully recyclable.

© Standard Chartered PLC. All rights reserved.The STANDARD CHARTERED word mark, its logodevice and associated product brand names areowned by Standard Chartered PLC and centrallylicensed to its operating entities. Registered Office:1 Aldermanbury Square, London EC2V 7SB.Telephone +44 (0) 20 7885 8888. Principal place ofbusiness in Hong Kong: 32nd Floor, 4-4A Des Voeux Road,Central, Hong Kong. Registered in England No. 966425.

Contents

Business Review

6 Chairman’s Statement

12 CEO & Director’s Report

16 Our Approach to Corporate Responsibility

22 Our people, Our Strength

26 Our Approach to Corporate Governance

34 Additional Information

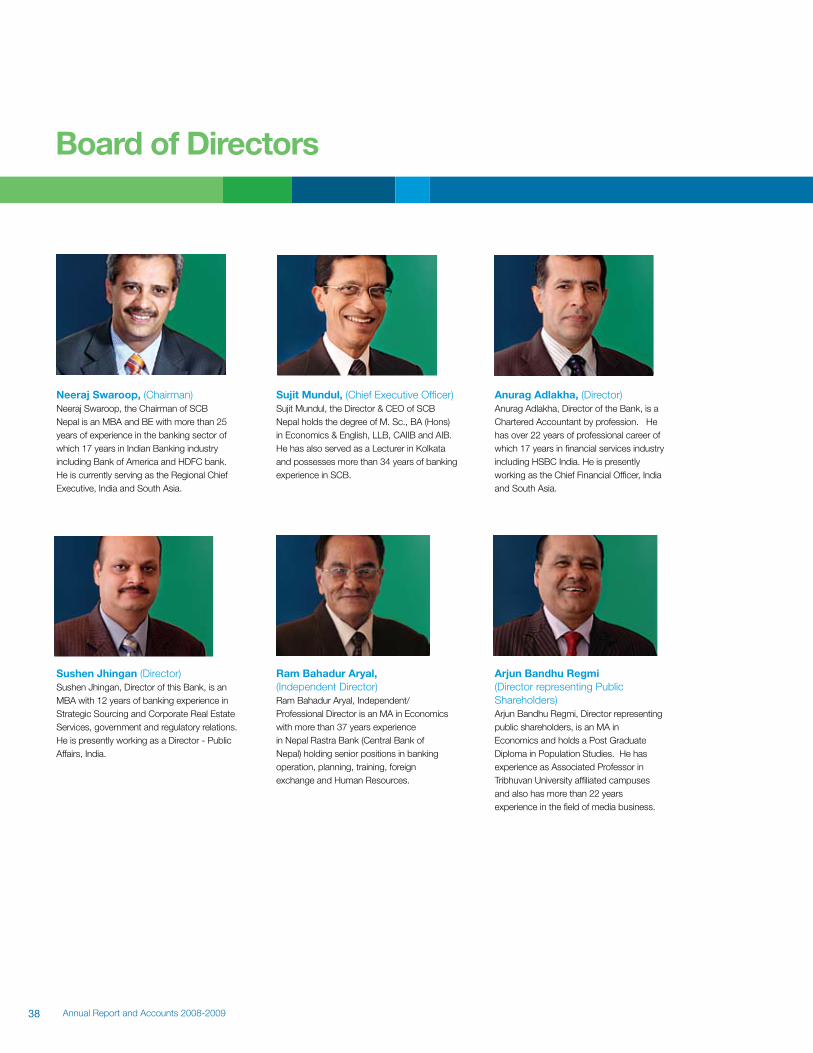

38 Board of Directors

39 Management Team

42 Branches and ATM’s

Financial Statements and Notes to Accounts

43 Auditor’s Report

44 Balance Sheet

45 Profit & Loss Account

46 Profit & Loss Appropriation Account

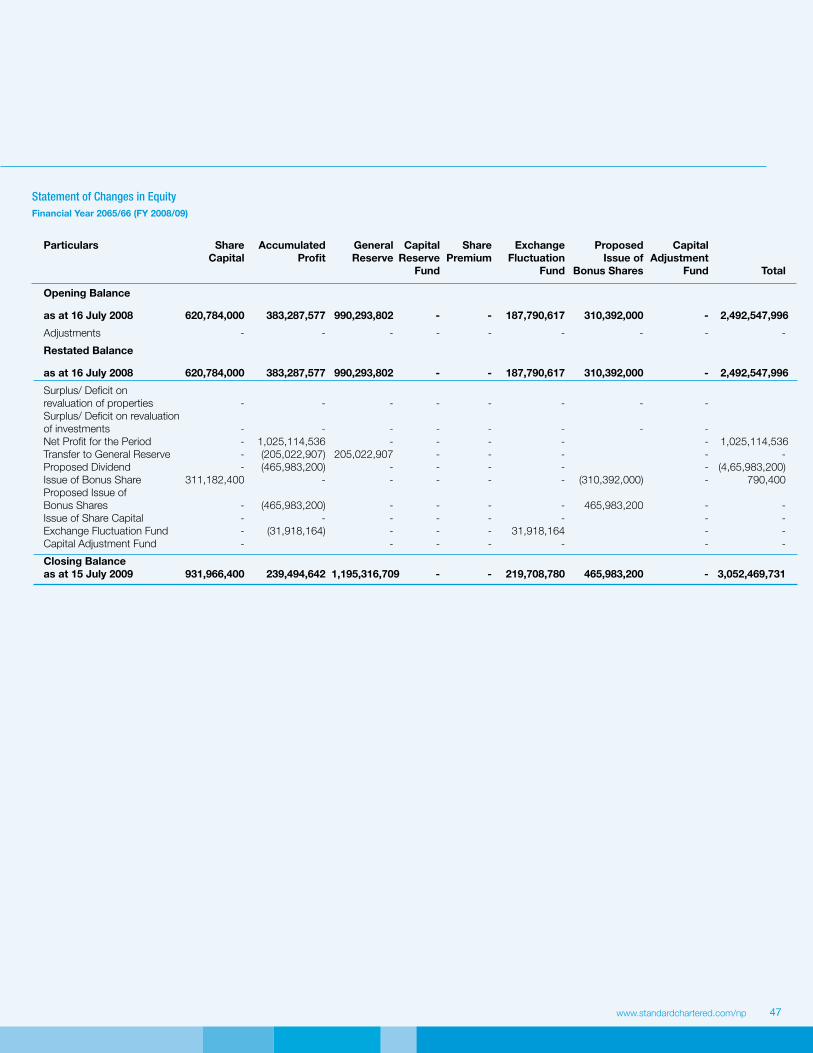

47 Statement of Changes in Equity

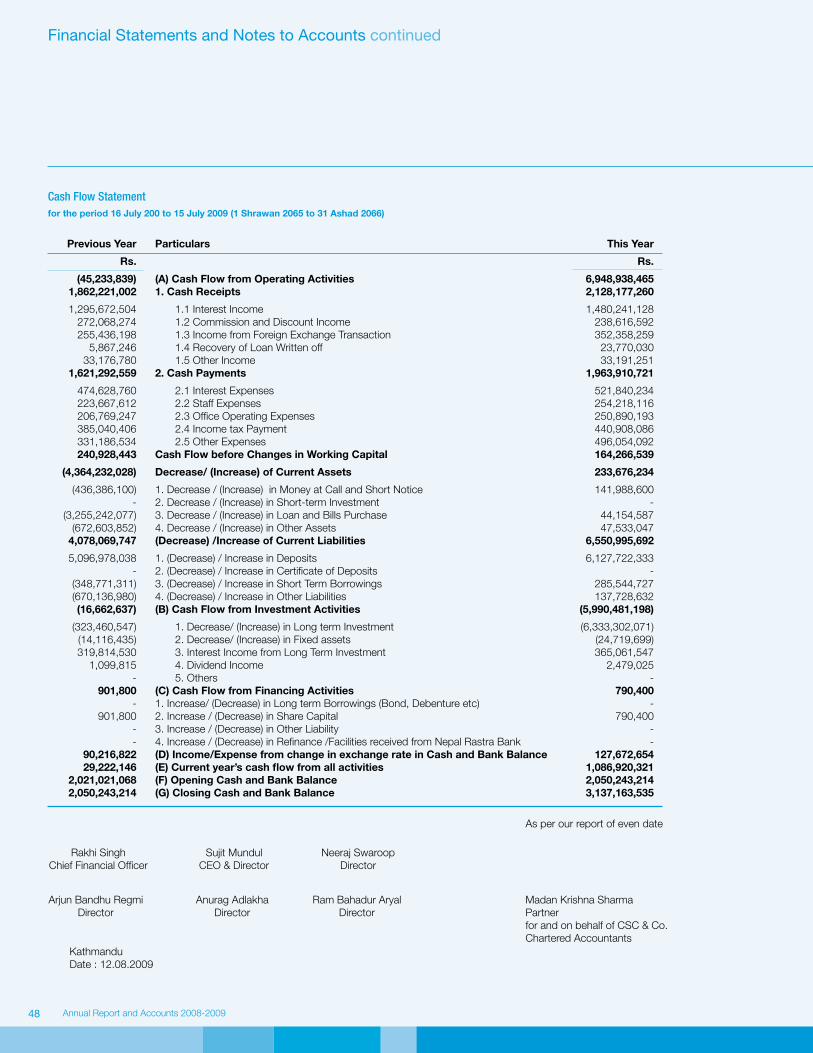

48 Cash Flow Statement

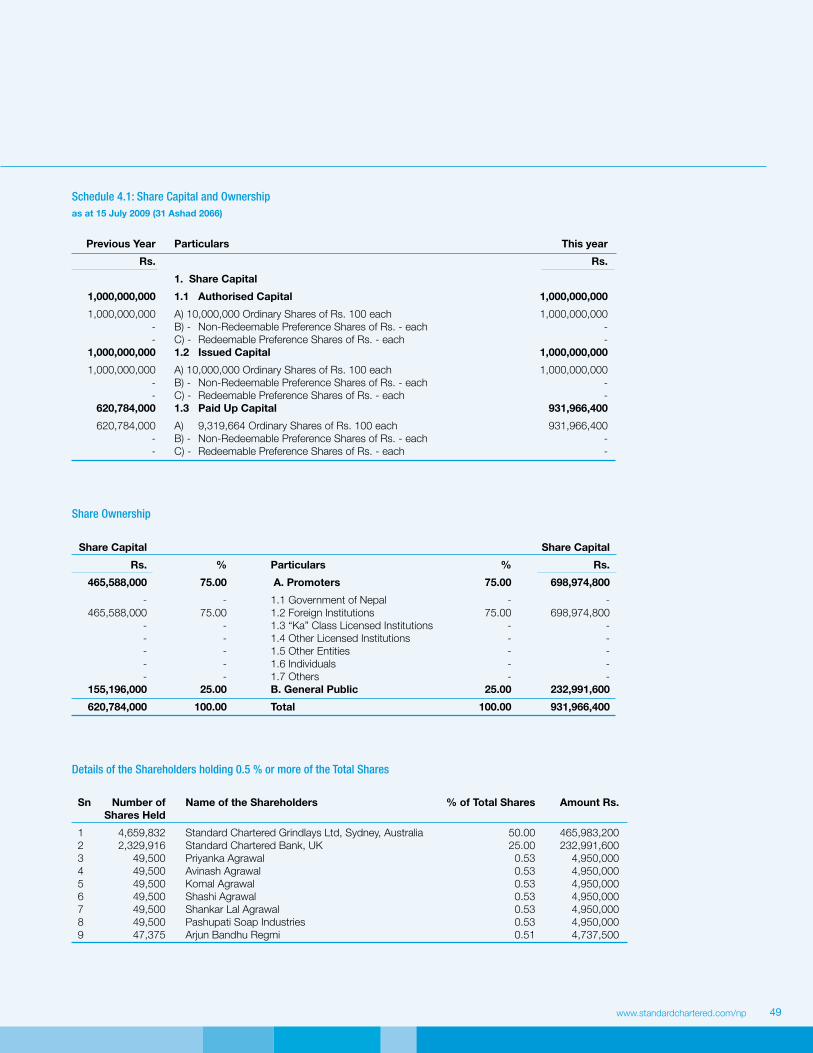

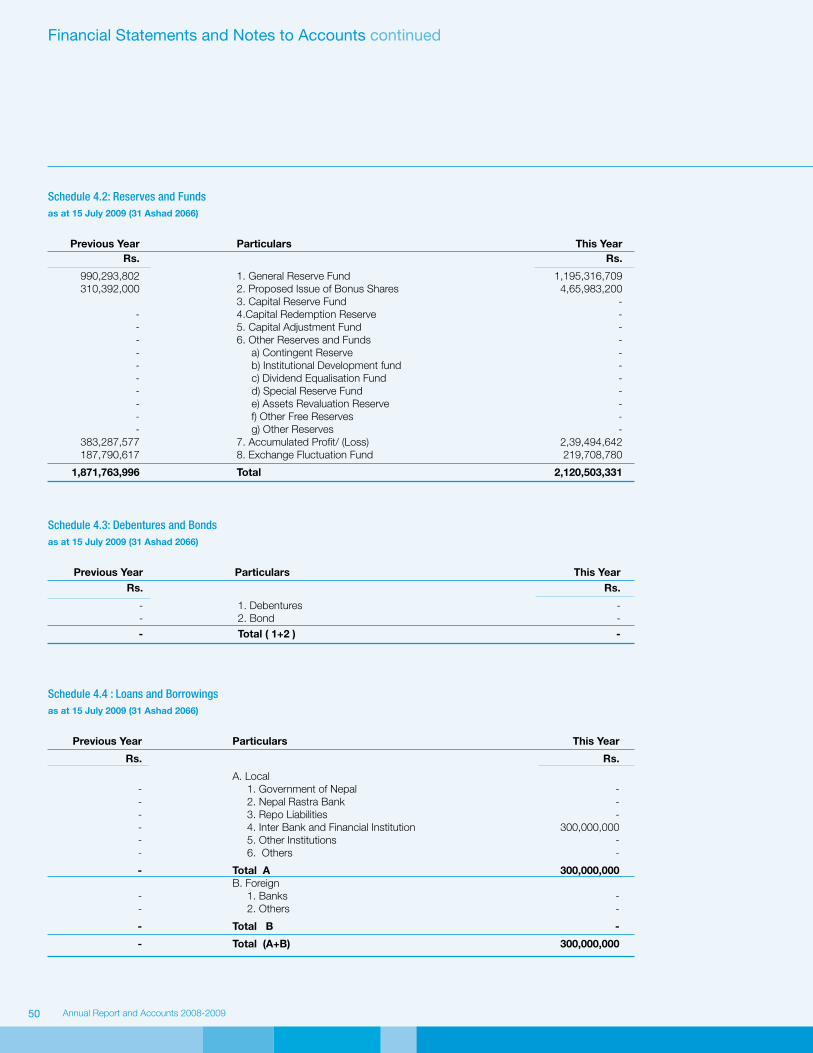

49 Schedules

78 Significant Accounting Policies

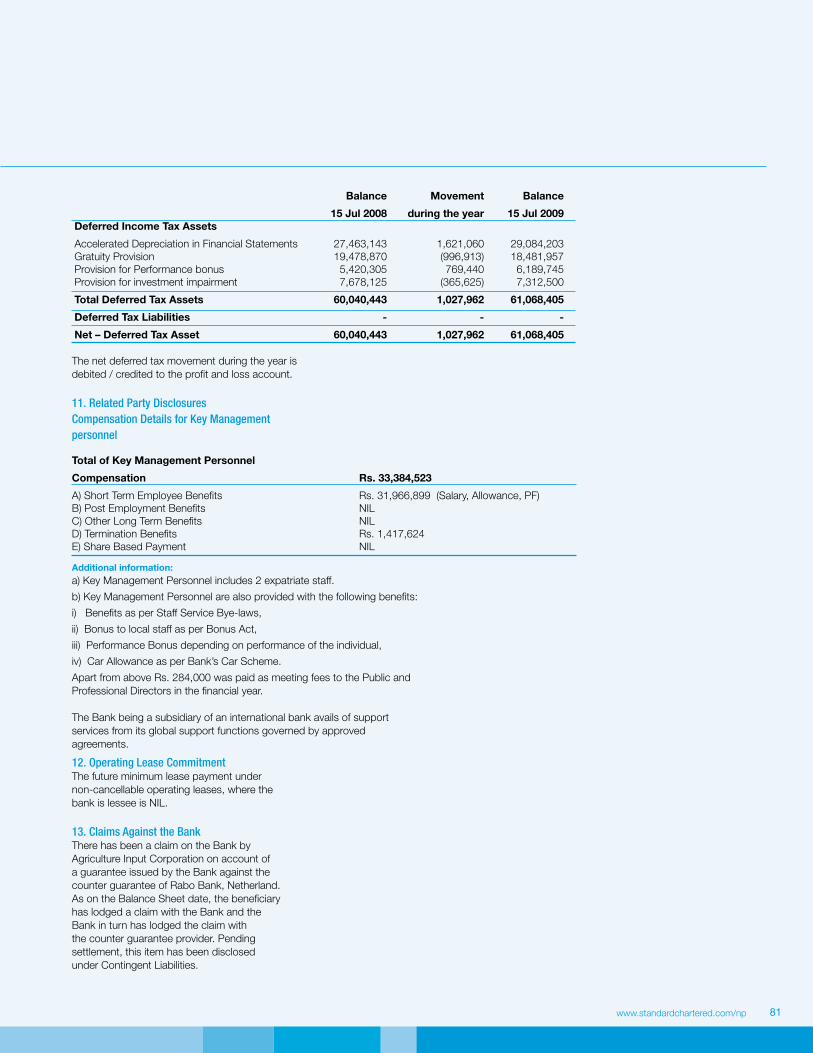

80 Notes to Accounts

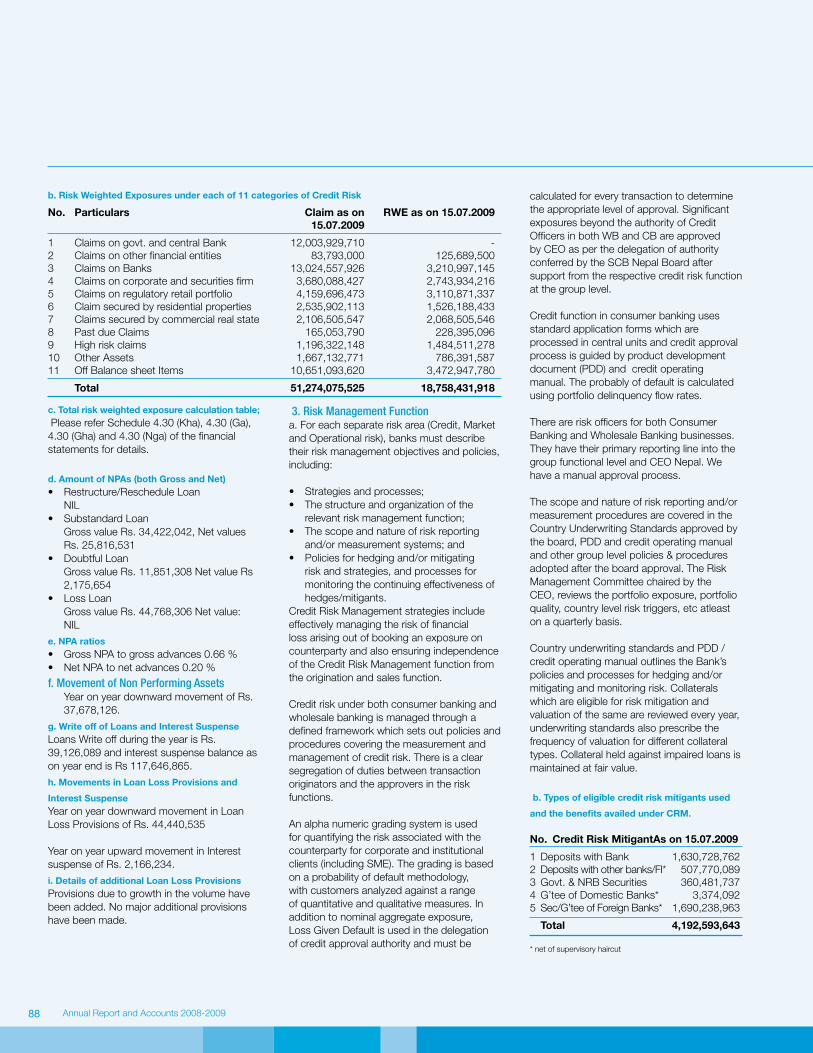

86 Disclosure as per Bank’s disclosure policy under the

Basel –II Capital Accord of Nepal Rastra Bank

89 Nepal Rastra Bank’s Approval and Directions

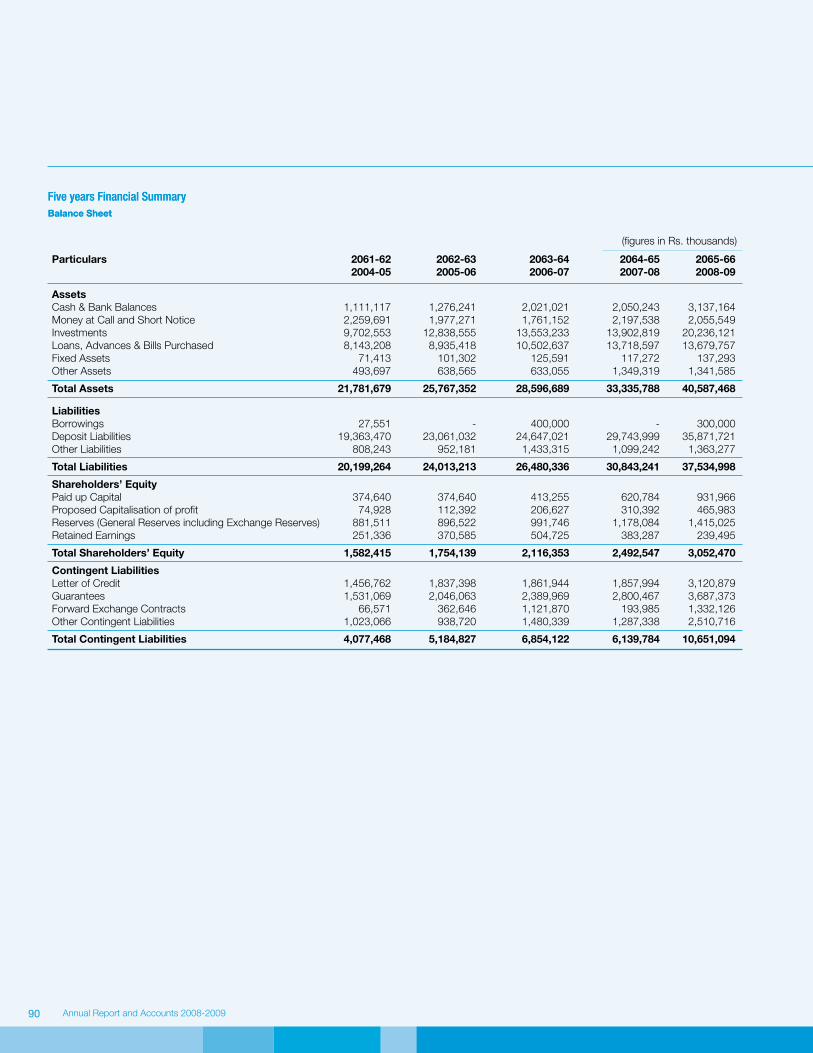

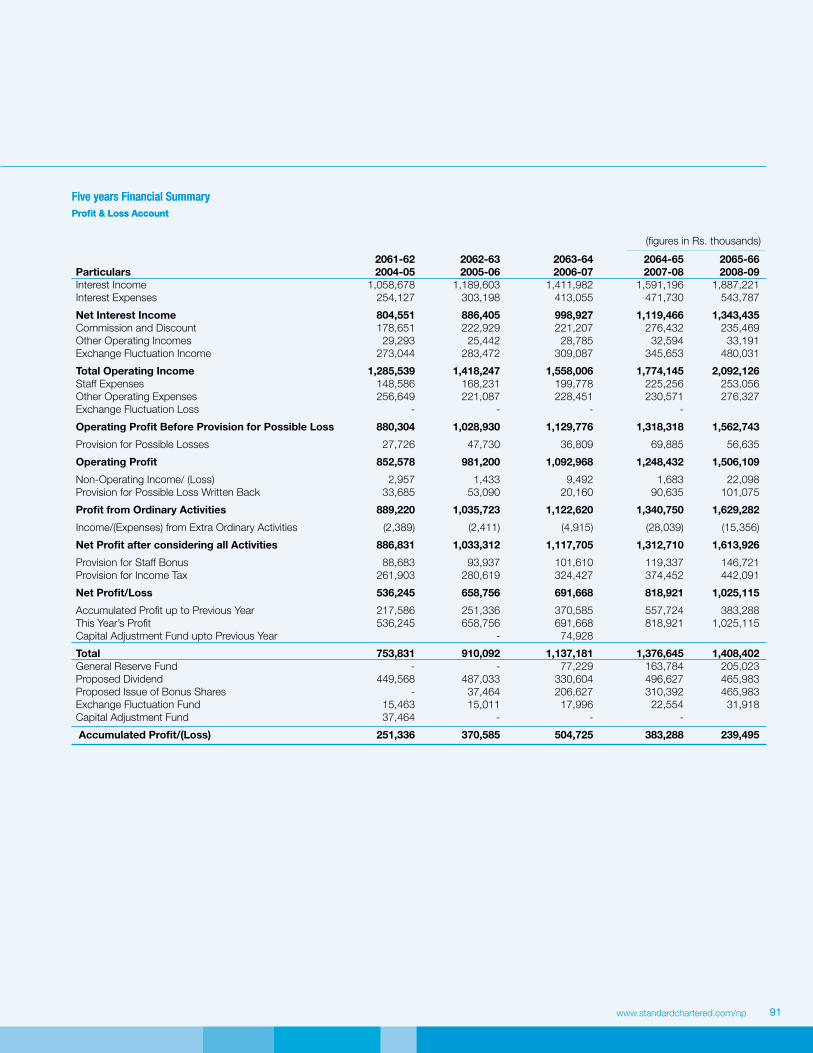

90 Five Years Financial Summary

Get more on LinePlease visit us on line at www.standardchartered.com/np for more information on the Bank and its full range of banking services.

Our performance

Financial highlights

FYE 2008/09

Non-financial highlights

Operational highlights

2092m

14.70%

1506m

39217

33.58%

40,587m

100%

Operating Income

(in NPR where applicable)

Points of representation

Capital Adequacy

Operating Profit

Employees

Return on equity

Total Assets

Dividend

Strong Income Growth

Strong Profit Growth

Robust balance sheet

Sound capital base

Solid deposit growth

Sustainable business

(Including Bonus Shares)

4 Standard Chartered 2008

Our approachWe have operated for over 150 years in some of theworld’s most dynamic markets, leading the way in Asia,Africa and the Middle East.

Group overview Our business

Standard Chartered PLC, listed on both the London and Hong Kong stock exchanges, ranks among thetop 25 companies in the FTSE 100 by market capitalisation. The Bank has grown substantially in recentyears, primarily as a result of organic growth, supplemented by acquisitions.

Standard Chartered aspires to be the best international bank for its customers. The Bank derives morethan 90 per cent of its operating income and profits from Asia, Africa and the Middle East, generatedfrom its Wholesale and Consumer Banking businesses. The Group has over 1,600 branches and outletslocated in over 70 countries.

Our business

Leading by example to be the right partner for its stakeholders, the Group is committed to building asustainable business over the long term that is trusted worldwide for upholding high standards of corporategovernance, social responsibility, environmental protection and employee diversity. It employs over 70,000people, nearly half of whom are women. The Group’s employees are of 125 nationalities, of which 68 arerepresented among senior management.

Our principles

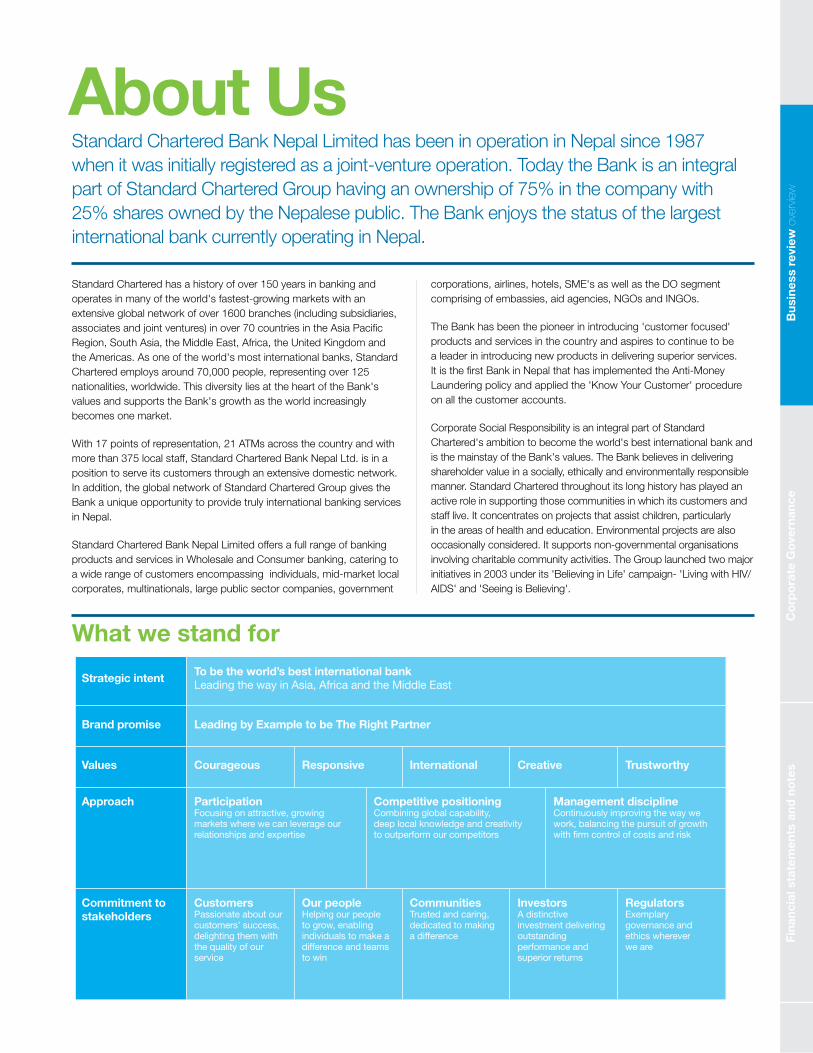

What we stand for

Brand promise

Approach

Commitment tostakeholders

Values

Strategic intent

Leading by Example to be The Right Partner

ParticipationFocusing on attractive, growingmarkets where we can leverage ourrelationships and expertise

CustomersPassionate about ourcustomers’ success,delighting them withthe quality of ourservice

Our peopleHelping our peopleto grow, enablingindividuals to make adifference and teamsto win

CommunitiesTrusted and caring,dedicated to makinga difference

InvestorsA distinctiveinvestment deliveringoutstandingperformance andsuperior returns

RegulatorsExemplarygovernance andethics whereverwe are

Competitive positioningCombining global capability,deep local knowledge and creativityto outperform our competitors

Management disciplineContinuously improving the way wework, balancing the pursuit of growthwith firm control of costs and risk

ResponsiveCourageous International TrustworthyCreative

To be the world’s best international bankLeading the way in Asia, Africa and the Middle East

Bus

ines

s re

view

ove

rvie

wC

orp

ora

te G

ove

rnan

ceFi

nanc

ial s

tate

men

ts a

nd n

ote

sB

usin

ess

revi

ew o

verv

iew

Co

rpo

rate

Go

vern

ance

Fina

ncia

l sta

tem

ents

and

no

tes

About UsStandard Chartered Bank Nepal Limited has been in operation in Nepal since 1987 when it was initially registered as a joint-venture operation. Today the Bank is an integral part of Standard Chartered Group having an ownership of 75% in the company with 25% shares owned by the Nepalese public. The Bank enjoys the status of the largest international bank currently operating in Nepal.

Standard Chartered has a history of over 150 years in banking and operates in many of the world's fastest-growing markets with an extensive global network of over 1600 branches (including subsidiaries, associates and joint ventures) in over 70 countries in the Asia Pacific Region, South Asia, the Middle East, Africa, the United Kingdom and the Americas. As one of the world's most international banks, Standard Chartered employs around 70,000 people, representing over 125 nationalities, worldwide. This diversity lies at the heart of the Bank's values and supports the Bank's growth as the world increasingly becomes one market.

With 17 points of representation, 21 ATMs across the country and with more than 375 local staff, Standard Chartered Bank Nepal Ltd. is in a position to serve its customers through an extensive domestic network. In addition, the global network of Standard Chartered Group gives the Bank a unique opportunity to provide truly international banking services in Nepal.

Standard Chartered Bank Nepal Limited offers a full range of banking products and services in Wholesale and Consumer banking, catering to a wide range of customers encompassing individuals, mid-market local corporates, multinationals, large public sector companies, government

What we stand for

corporations, airlines, hotels, SME's as well as the DO segment comprising of embassies, aid agencies, NGOs and INGOs.

The Bank has been the pioneer in introducing 'customer focused' products and services in the country and aspires to continue to be a leader in introducing new products in delivering superior services. It is the first Bank in Nepal that has implemented the Anti-Money Laundering policy and applied the 'Know Your Customer' procedure on all the customer accounts.

Corporate Social Responsibility is an integral part of Standard Chartered's ambition to become the world's best international bank and is the mainstay of the Bank's values. The Bank believes in delivering shareholder value in a socially, ethically and environmentally responsible manner. Standard Chartered throughout its long history has played an active role in supporting those communities in which its customers and staff live. It concentrates on projects that assist children, particularly in the areas of health and education. Environmental projects are also occasionally considered. It supports non-governmental organisations involving charitable community activities. The Group launched two major initiatives in 2003 under its 'Believing in Life' campaign- 'Living with HIV/AIDS' and 'Seeing is Believing'.

Annual Report and Accounts 2008-20096

Chairman’s Statement

Building strong foundations“Our deep understanding of this market, ability to quickly adapt to the changing scenario and the aptitude of our management to execute the Bank’s strategy are continuously propelling our intent to garner a balanced and sustainable growth.” – Neeraj Swaroop, Chairman

It is my pleasure to report that Standard Chartered Bank Nepal Limited has been able to successfully maintain its record of consistent performance and delivered robust financial results for the fiscal year ended 15 July 2009. Our results clearly demonstrate the underlying strength of our businesses and the overall resilience of the Bank. We have been consistent in our strategy, carrying out business in the areas of our strength and with products of our expertise. To deliver record results in this exceptional environment is a great achievement. Full credit goes to the Nepal Team for having achieved this feat in the backdrop of global

7www.standardchartered.com/np

Bus

ines

s re

view

ove

rvie

wC

orp

ora

te G

ove

rnan

ceFi

nanc

ial s

tate

men

ts a

nd n

ote

s

“We continued to show restraint while leading the best practices for the industry, be it in the area of products sold to customers or in the quality of services rendered to them.”

economic melt down coupled with challenging political and economic environment within the country itself.

Some improvement in the underlying security and political situation has paved way for the Bank to consider investment in footprint expansion and in launching innovative products. These have had a positive effect in the Bank’s performance as evidenced by our FYE 2008/09 numbers. We continued to show restraint while leading the best practices for the industry, be it in the area of products sold to customers or in the quality of services rendered to them. Our deep understanding of this market, ability to quickly adapt to the changing scenario and the aptitude of our management to execute the Bank’s strategy

are continuously propelling our intent to garner a balanced and sustainable growth. Throughout our presence, we have lived our commitment in being the right partner to our people, customers, regulators, industry and the community. This is a firm foundation which prepares us to seize the opportunities even as the business environment becomes increasingly challenging. Our brand is the most valuable asset which is at the heart of our strategic intent i.e, to be the world’s best international Bank, leading the way in Asia, Africa and the Middle East. Standard Chartered is the best brand in this market and we are committed to maintain this position in the future as well.

Results – A Synopsis

Financial Highlights Net Profit after tax rose by 25.18 percent to

Rs.1.025 billion compared to Rs. 818.92 million in the previous year

Earnings per share is lower by Rs. 21.93 due to increase in the number of shares last year

Risk Assets decreased by less than a percent to Rs.13.88 billion

Deposits increased by 20.60 percent to Rs. 35.87 billion

A Consistent PerformanceThe Bank has been continuously delivering on its promises year on year. As a result of another exceptional year, the Bank continues to be one of the highest contributors to the Government Exchequer by contributing Rs. 443 million as compared to Rs. 381 million last year on account of Corporate tax.

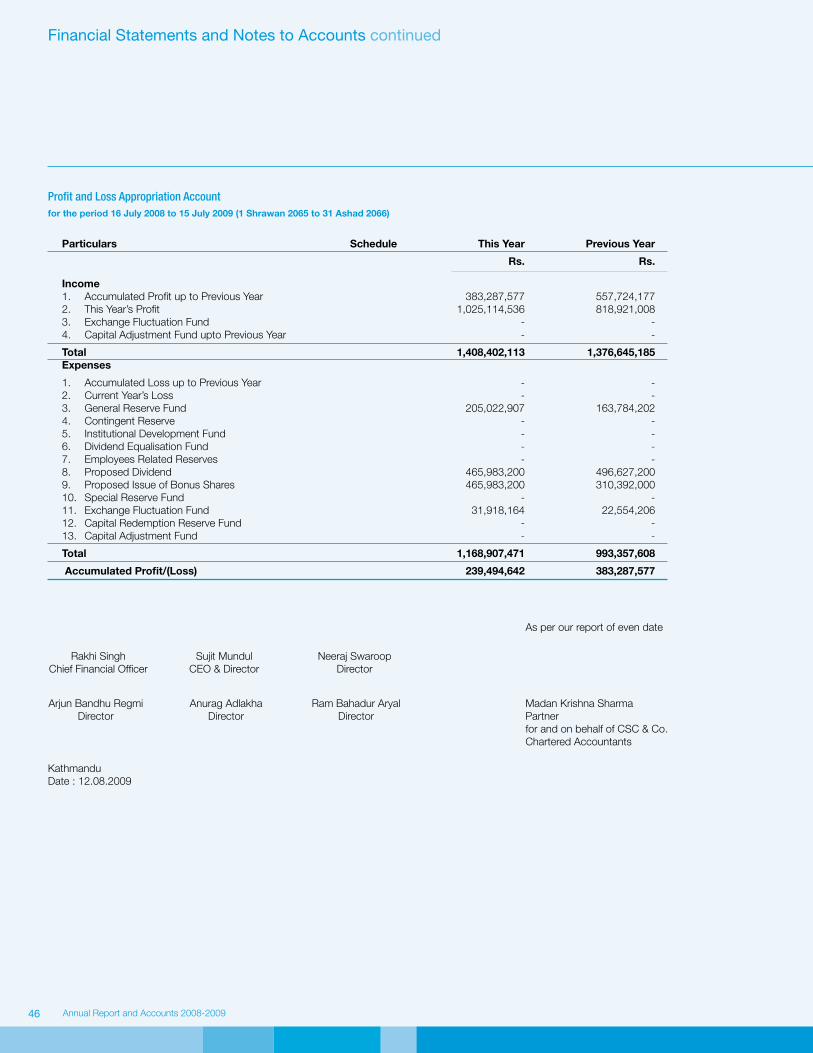

In accordance with the statutory requirements, the Board recommends a transfer of Rs. 31,918,164 to Exchange Fluctuation Reserve from current year’s profits and the statutory transfer of Rs. 205,022,907 into General Reserve Fund. In congruence with the revised capital requirements as stipulated by the Central Bank, the Board has proposed to increase the capital by issuing 50 percent Bonus shares for which Rs. 465,983,200 has been allocated from current year profit.

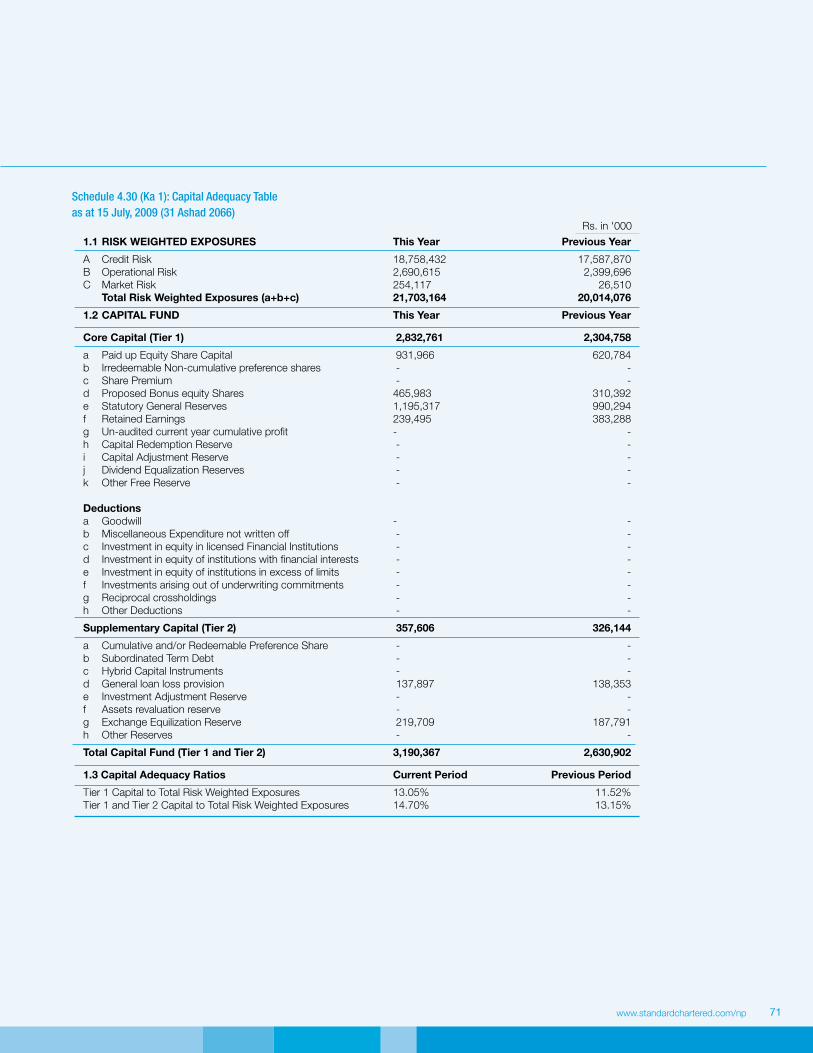

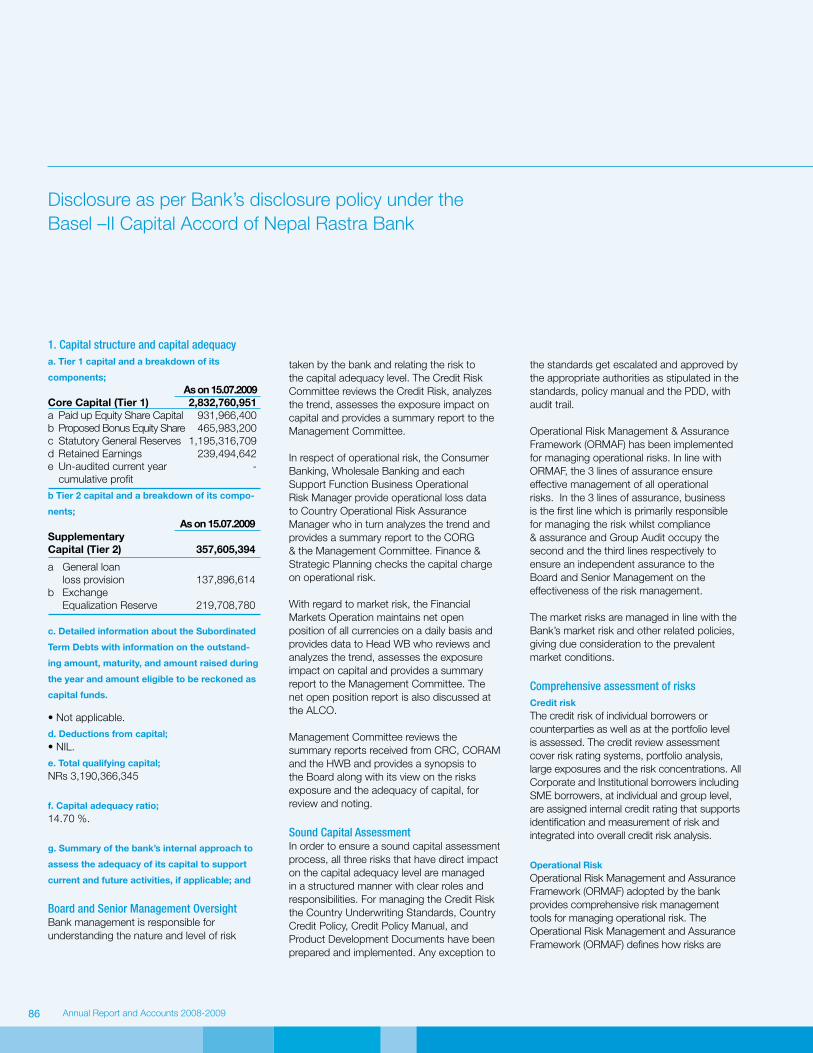

Our Tier 1 and Tier 2 Capital Adequacy Ratios were 13.05 percent and 1.65 percent respectively with an overall ratio of 14.70 percent. Our capital position is more than adequate and exceeds the current Nepal Rastra Bank’s capital adequacy requirement under the new Basel II capital accord of 10.00 percent and also exceeds the international norms.

536

659 692

819

1,025

2004

-05

Profit After Tax In NPR Mn

2005

-06

2006

-07

2007

-08

2008

-09

2,345

3,775

5,900

6,830

6,010

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

Market value per share In Rs.

Annual Report and Accounts 2008-20098

A Challenging EnvironmentIt appears that the worst of the global financial crisis is mostly over but its effects may remain for quite sometime. Markets seem to be quite cautious about the perplexing turning points of economies as there can be conflicting economic data failing to clearly justify if an economy has hit the bottom and turning around.

The obvious is that the last quarter of 2008 and the first quarter of 2009 were appalling, as exports slumped, inventories were cut and spending plans were put on hold. While many indicators were still poor in the second quarter of 2009, there were signs of improvement. Asia is leading this rebound and even the economies hit hard by the collapse in exports are starting to recover. Latest data suggests that it should become even more apparent and widespread as we progress into the second half of the year.

This year was even more challenging for Nepal in both political and economic fronts as the country transitioned into a republic state. Difficult labor relations and continuous power crisis were the major issues in the manufacturing sector. Poor monsoon hit hard on the agriculture as well. Growth in Remittance remained a major driver in holding the economy.

In FYE 2008/09, Nepal’s GDP growth is expected around 4 percent. During the year, agriculture sector is estimated to have grown by 2.2 percent compared to a growth of 4.7 percent in the previous year.

The growth in non-agricultural sector is estimated at 4.8 percent compared to a growth of 5.6 percent in the previous year.

The government revenue increased by 32.1 percent to Rs. 142.2 billion in FY 2008/09 compared to a growth of 22.7 percent in the previous year. Similarly government expenditure rose by 32.4 percent to Rs. 213.6 billion. Such expenditure had increased by 20.8 percent in the comparable period of the preceding year. The budget deficit amounted to Rs 36.8 billion during the period under review compared to the budget deficit of Rs 21.20 billion in the same period of the preceding year.

The annual average consumer inflation is expected to soar to 13 percent compared to a rise of 7.7 percent in the previous year. The upsurge in inflation was mainly driven by the power cuts, supply disturbances and poor labor relations resulting in low outputs.

The performance of export sector was relatively satisfactory against the backdrop of the global economic crisis. The total export grew by 19.8 percent in the first ten months of FY2008/09 compared to decline of 2.4 percent in the previous year. Likewise total imports increased significantly by 25.4 percent compared to a growth of 16.8 percent in the previous year.

Increased inflow from remittances which grew by 51 percent helped expand country’s total gross foreign exchange reserves to USD 3.59 billion as of mid June 2009. This is sufficient to cover import of merchandise and services for 9.6 months.

In line with the depreciation of the Indian Rupees against the US dollar, the Nepalese Rupee also recorded a weakening trend against USD and depreciated by 14.6 percent during FY 2008/09. Nepalese Rupee has a fixed parity of 1:1.6 with the Indian Rupee.

Outlook for 2009/10The government holds firm plans to attain high growth rate in the economy and contract the double digit inflation rate. However, achievement of such an augmentation will, to a great extent, depend upon the political stability in the country and provision of adequate security. The nation, thus, optimistically awaits the government’s efforts to implement its plans and resuscitate the economy.

Agriculture sector, which is largely dependant on the weather conditions, is expected to witness a depressed momentum. Arrival of late monsoon is likely to have a negative impact this year. However, improvement in the rural security situation is expected to expand cultivation area, enhance distribution of inputs and services, and raise farm productivity. Likewise, the industrial sector is also estimated to grow at a mediocre pace of 4-5 percent in the coming FY. The government’s focus to increase infrastructural expenditure and improve the operating condition in manufacturing sector coupled with a consistent remittance-driven consumer spending are likely to provide stability in the economy.

Service sector growth is likely to remain around 5 percent stemming mainly from higher tourism related activities. Investment in infrastructural projects by private sector is also expected to grow. However, labor and industrial security issues would be key factors to build investors’ confidence. Giving credence to these factors, an overall economic growth of 4% is considered achievable in the coming year.

Chairman’s Statement continued

“ Markets seem to be quite cautious

about the perplexing turning points of

economies as there can be conflicting

economic data failing to clearly justify if an economy has hit the bottom and turning

around. ”

9www.standardchartered.com/np

Bus

ines

s re

view

ove

rvie

wC

orp

ora

te G

ove

rnan

ceFi

nanc

ial s

tate

men

ts a

nd n

ote

s

143.14

175.84167.37

131.92

109.99

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

Earning Per Share In Rs.

Corporate GovernanceGovernance across the Bank is robust. As you can appreciate, banking is a relationship business. We highly value the relationships that we have with our people, regulators, clients and the other stakeholders and we would strive hard to remain The Right Partner for them.

We are committed to ensuring the integrity of governance. In addition to the established committees, we have committees on Diversity and Inclusion, Health and Safety, the Environment, Outserve Plus and Community Partnership. The initiatives taken by these committees have added value to our stakeholders and delighted them. We believe good governance provides clear accountabilities, ensures strong controls, instills the right behaviors and reinforces good performance.

Mr. Arjun Bandhu Regmi representing the public shareholders, Mr. Anurag Adlakha and Mr. Sushen Jhingan, nominated by the Standard Chartered Grindlays Australia and Mr. Ram Bd. Aryal as Professional/Independent Director continue to be in the Board of SCB Nepal Limited. I, Neeraj Swaroop and Mr. Sujit Mundul, continue to represent the Standard Chartered Group on the Board of Standard Chartered Bank Nepal Limited.

During the period, Standard Chartered Group nominated Peter Warbanoff and Aniruddha Bose as Alternate Director to Sushen Jhingan and Neeraj Swaroop respectively replacing Robert Green and Ranjan Ghosh respectively with effect from 1st February 2009. Rajeev Uberoi, Alternate Director to Anurag Adlakha, resigned from Standard Chartered Bank. We are delighted to have new Alternate Directors on our Board. I would like to thank Mr.

Robert Green, Mr. Ranjan Ghosh and Mr. Rajeev Uberoi for their contribution during their tenure as Alternate Directors of the Bank.

In Conclusion A review of the world economy reveals that the crisis is yet to be over. It is therefore important to look beyond the immediate future. While the near-term economic conditions have deteriorated, our markets mainly in Asia remain fundamentally strong and attractive. With the advent of growing middle class, rapid urbanization and continuing industrialization, our markets offer vast potential. We are in the right markets and will stay focused on them.

Nepal experienced a relatively stable condition during the downturn of the major global economies. Apparently, the Nepali financial market does not seem to have been directly impacted by the crisis due mainly to insignificant amount of foreign private capital inflows. However, the country has critical dependence on other larger economies both in terms of imports and exports including remittances. Therefore, the contagion effect of the global economies cannot be underestimated. For Nepal, tourism, foreign aid, big budget projects including FDIs, exports and remittances are areas which could prove to be vulnerable as a result of the global economic meltdown.

Against the backdrop of a difficult overall economic scenario, Nepal recorded a satisfactory growth during the review period as evidenced by FYE 2008/09 economic indicators. In line with this, the Bank was also able to achieve good results due mainly to the efforts, focus and commitment displayed by the management team in creating shareholders value.

The Bank has undertaken various initiatives to make it an employer of choice. Continuous focus is placed on staff’s learning and development. The Bank has embraced Work-life Balance by creating a conducive work environment which could fulfill the different needs of individuals. Ours is probably the only Bank in the country to introduce a five day week, which allows our people to stay on leave on alternate Sundays.

The Diversity and Inclusion Council in the Bank continued to address the different strands of diversity including women, and the differently-abled.

Ministry of Finance and the Central Bank have played important roles in driving the financial sector reforms in Nepal. We appreciate any initiatives that are aimed at driving reforms and strengthening the overall financial system in the country. Support and guidance received from our Regulators and the

“We are committed to ensuring the integrity of governance. In addition to the established committees, we have committees on Diversity and Inclusion, Health and Safety, the Environment, Outserve Plus and Community Partnership. ”

2.46

2.56

2.42

2.46

2.53

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

Return on Total Assets In Percent

1,5821,754

2,116

2,493

3,052

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

Total Shareholder Equity In NPR Mn

Annual Report and Accounts 2008-200910

Enterprise (SME) portfolio. We are happy the way we are growing and we want to maintain this momentum. We have taken a proactive approach towards managing risks for ensuring that we do not experience “any surprises” in both the businesses. In the meanwhile, we are keeping a firm grip on costs. As in the past, in the coming year, we will stick to our strategy and will continue to focus on deepening our relationships with our clients.

It has been more than a year that the country has seen in place an elected government. The successful holding of Constituent Assembly elections and the formation of an elected government has injected renewed hope for peace, security and economic progress after more than a decade long instability and strife. At this juncture, SCB Nepal intends to make meaningful contribution in accelerating the economic activities of the country and attaining a higher growth trajectory.

On behalf of SCB Nepal’s Board of Directors, I take this opportunity to thank all the stakeholders for being our Right Partner. I express my sincere appreciation to our valued customers and shareholders for guiding and supporting us in our journey. I would also like to express my deepest gratitude to our people for exhibiting their seamless engagement and commitment to take the Bank to insurmountable heights. I am sure we will deliver another year of record performance next year. Let me assure you that we are in a strong position to deal with the emerging challenges and opportunities on an ongoing basis.

Neeraj Swaroop Chairman

high level of governance of the Standard Chartered Group have been the cornerstones for us in consistently delivering good results, in maintaining exemplary governance standards and in providing superior products and services.

Continued support and trust received from our valuable customers, shareholders and other stakeholders has enabled us to remain the Best Bank in Nepal - Leading the Way. I sincerely appreciate their efforts to bestow us with their encouragement, trust and loyalty.

As a leading corporate citizen, our approach has been to take a long-term view of our actions and use our core skills and services to make a positive contribution to the society. Our `Sustainability’ agenda revolves around several pillars, including community investment, environment protection, financial inclusion, tackling financial crime and responsible selling and marketing. Building a sustainable business is an integral part of our long-term strategy to enhance shareholder value.

We are cautious in expanding our risk assets portfolio. Our asset quality is conservative, diverse and tightly secured. We are disciplined in the risks we take. Our Wholesale Banking business comprising of Origination & Client Coverage (OCC) and Financial Markets (FI) exhibited broad-based growth by continuing to benefit from the increasing market share. Consumer banking, on the other hand, also displayed strong growth in all fronts of Auto, Mortgage, Credit Card & Personal Loan including our recently introduced Small and Medium

“Our `Sustainability’ agenda revolves around several pillars, including community investment, environment protection, financial inclusion, tackling financial crime and responsible selling and marketing.”

Chairman’s Statement continued

Leading the way in helping realize

local dreams

Annual Report and Accounts 2008-200912

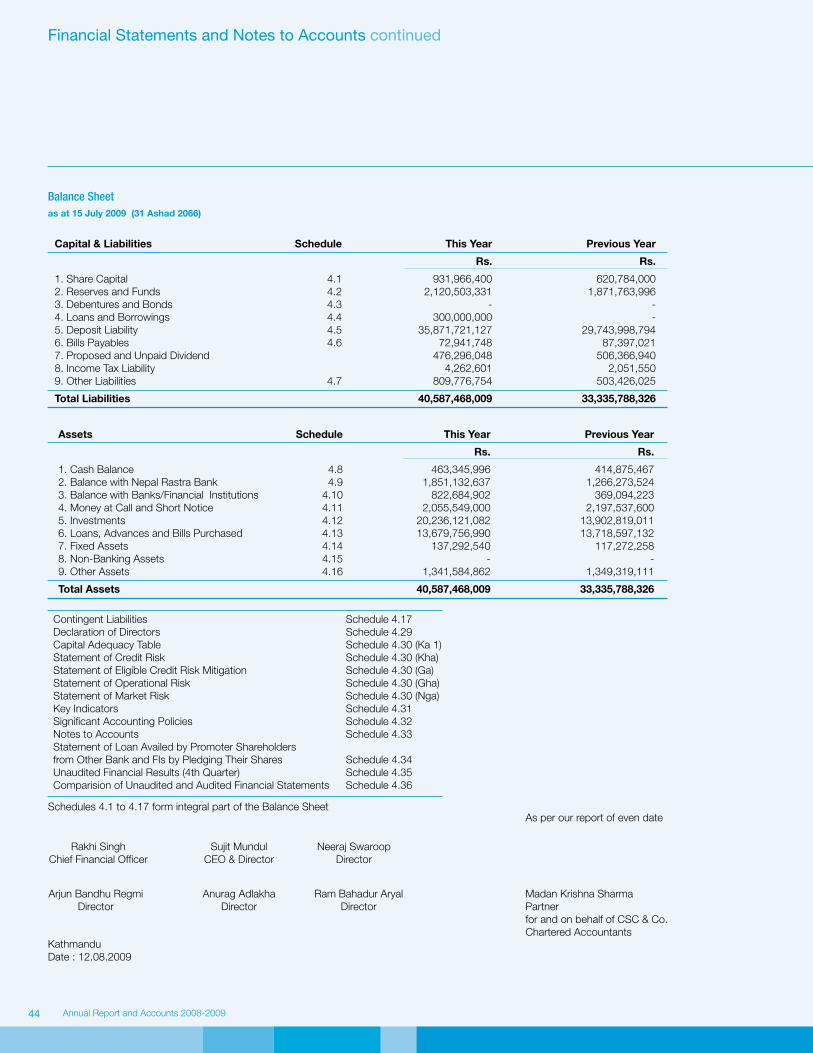

The CEO & Director presents this report together with the Balance Sheet and statement of Profit and Loss for the year ended 15 July 2009. The report is in conformity with the provisions of the Companies Act 2063 and Bank & Financial Institution Act 2063 including the directives issued by the Nepal Rastra Bank.

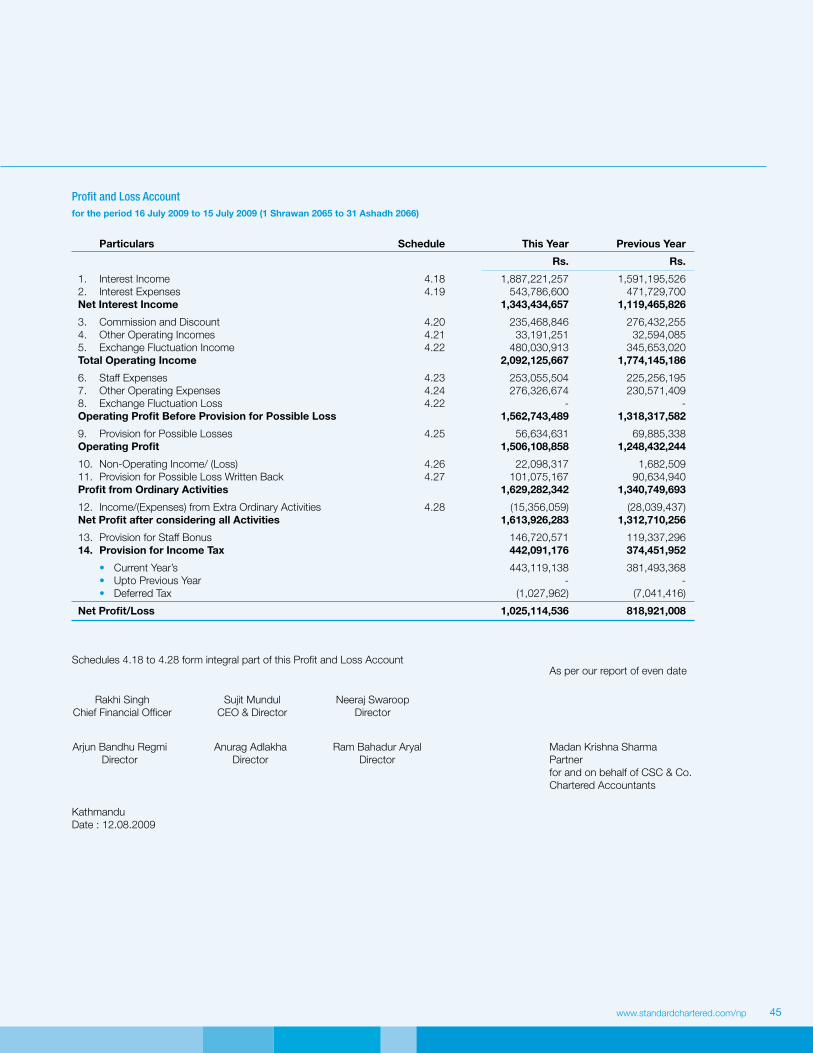

Standard Chartered Bank Nepal is in good shape and we continue to deliver strong financial performance. Through the disciplined execution of our strategy and the hard work of our team, we have delivered another set of strong results. An increase in the net profit after tax of 25.18 percent over last year to Rs. 1.03 billion is commendable in the backdrop of difficult economic and socio-political conditions. This has been achieved by relentless focus on cost and risk management while pursuing limited business growth.

There is a marginal decline in the volume of risk assets compared to the preceding year. The Bank has been able to manage the credit portfolio better as a result of which the loan loss provision balance has contracted to Rs. 201 million this year from Rs. 245 million last year. Similarly the ratio of Non-performing credit to Total credit has reduced from 0.92 percent to 0.66 percent. The provisions made are adequate to cover all the potential credit losses of the Bank as of the balance sheet date.

After transfer to general reserve Rs. 205.02 million, exchange fluctuation reserve Rs. 31.92 million, proposed dividend Rs. 465.98 million and bonus share Rs. 465.98 million, total retained earnings as at 15 July 2009 stood at Rs. 239.49 million. This performance reflects a very good momentum in the

CEO & Director’s Report

In Rs. ‘000s In Rs. ‘000s

15-Jul-09 16-Jul-08 % Change

Operating Profit 1,506,109 1,248,432 20.64%

Transfer to General Loan Loss Provision 56,635 69,885 (18.96)%

Provision for Tax 442,091 374,452 18.06%

Net Profit After Provision and Tax 1,025,115 818,921 25.18%

Issue of Bonus Shares 465,983 310,392 50.13%

Proposed Cash Dividend 465,983 496,627 (6.17)%

underlying businesses and disciplined management of risks and costs.

RepresentationAs at 15 July 2009, the Bank maintained seventeen points of representation which included thirteen branches and four extension counters. In addition to this, services were also extended to our customers through twenty one ATMs located at different parts of the country.

Wholesale BankingWholesale Banking (WB) business grew at an impressive rate with broad spectrum income stream - across the client base and product range. Given the challenging operating environment in terms of political uncertainties and global meltdown – maintaining the credit quality of the portfolio and at the same time supporting clients with enhanced credit facilities were the biggest challenges.

Our focus continued to be on the Clients as we provided solutions under trade finance, cash management, foreign exchange and risk management products offering. Our strategy was to remain or become the core bank to our clients, deepen relationship with them and provide them with a broad range of products. The focused approach and client centric strategy enabled us to dominate our chosen areas of activity like Gold Sale, Trading in FCY and LCY, Structured Trade, Acquisition Financing and Investment Solutions. We continued to build scale cautiously - more so - in the cross border space and catered to client needs by offering sophisticated value added solutions.

Our uncompromising international standard of due diligence was appreciated by our clients as they understood the benefits it brought along. Especially the global financial crises made everyone alert and recognize risk which enabled us to tap the “flight to safety” of deposits. The bank adopted and successfully embedded the Basel II guidelines. It enabled us to effectively use collaterals in managing risk and reduce capital allocation. WB continued to monitor risk / reward using advanced tools and by introducing new parameters like RWA, etc. Booking and sell down of assets were initiated to enhance return for the shareholders. The merger of American

“ Standard Chartered Bank Nepal is in

good shape and we continue to deliver

strong financial performance. ”

– Sujit Mundul, CEO

CEO & Director’s Report

13www.standardchartered.com/np

Bus

ines

s re

view

ove

rvie

wC

orp

ora

te G

ove

rnan

ceFi

nanc

ial s

tate

men

ts a

nd n

ote

s

Express Bank Representative Office in Nepal with the Bank as part of our global acquisition was completed successfully.

Consumer BankingConsumer Banking priorities continue to be customer centric product innovation, service excellence, investment for the future and appropriate risk based pricing.

During FY 2008/09, despite a number of challenges posed by the political conundrum, coupled with sporadic shortage of fuel and acute load shedding, Consumer Banking fared pretty well in growing both quality assets and deposits.

We launched SME business with a focus to develop both asset and liability business in this segment, which is heading in the right direction.

In line with our commitment to expand at the right time and in the right place, we opened two more branches- one each in Narayangarh and Birgunj. With these two additional branches, our branch network has now reached seventeen.

Similarly for the ease of transactions, we installed four more ATMs- one each in Lazimpat, Naya Baneshwar, Narayangarh and Itahari. With these four additional ATMs, our total ATM network has now reached twenty one.

Our commitment to Treating Customers Fairly and our policies on Mis-selling and Mis- representation remain core to our values.

In order to simplify banking we are aggressively educating our customer base for Online Banking

which was launched last year and is now gaining momentum.

In order to enhance the plastic money culture in the country, our suite of plastic money –Rupee and USD Credit Card, Prepaid Rupee and USD Card and Proprietary ATM Cards have provided alternatives to Travellers Cheques and Cash.

The `Voice of Customer’ survey is an integral tool to gauge the level of satisfaction of our customers. The Mystery Shopping Concept that we conducted gave us significant insight into our business and customers’ perception. Further, our strategy to take direct feedback from customers on a regular basis has also helped us in enhancing the value to our customers. This is an ongoing journey and it is our commitment that we will continue to add value to our customers.

We have developed a system whereby each customer’s complaint/feedback gets captured and responses / resolution to each of these issues are provided within an agreed timeline.

In line with the customers’ feedback and our aspiration to extend footprints in the right places, we have plans to open two more branches in the year 2009/10.

Outserve Plus - Continuously Improving the Way We WorkIn line with the Bank’s strategic intent and our commitment to our stakeholders, the Bank has been successful in embedding a culture of continuous improvement to provide a differentiated, quality service to our customers. Continuous efforts in inculcating behavioral changes throughout the Bank

Market Extension: The Bank has launched SME Banking – Holistic Banking Solutions, targeting small and medium scale enterprises.

Branch Expansion Bank expanded its footprint by opening its Narayangarh Branch. Sujit Mundul, CEO, SCB Nepal inaugurated the Bank’s 13th branch located at Lion’s Chowk, Narayangarh, Chitwon.

Branch relocation The Bank has recently relocated its existing branch at Main Road Biratnagar to Hanumandas Road.

Annual Report and Accounts 2008-200914

have enabled our people to find ways for improving the way we work to achieve Operational Excellence.

We have an Outserve Council in the Bank to ensure that transformational agendas and improvement activities on service and processes are delivered to “delight customers”.

We treat all customer complaints as golden opportunities to better understand what is important to our customers and to drive service improvement priorities. We are working to make our complaint tracking system more effective to gauge our service quality and put in place corrective measures for meeting our customers’ needs and expectations.

We are freeing up capacity to support growth through simplification of processes and elimination of inefficient practices.

We have built a framework to ensure that the Bank’s transformational initiatives being driven by businesses and functions actually deliver on their promises of substantive changes and reasonable benefits.

Future PlansAs mentioned above, we intend to add two more branches in the year 2009/2010. As the political and economic landscape continues to be challenging and the impact of the global meltdown in Nepal particularly in respect of remittances is yet to be fully known, we will continue to be cautious in our approach. Any new investment will depend on how conducive the environment is. Hence our focus will continue to be in improvising on our existing products with focus on quality, customer service and returns for our stakeholders.

Despite a challenging environment from the Bank’s perspective - future holds opportunities. However, we will approach these opportunities with caution. Wholesale Bank will stick to its strategy of becoming the core bank to the existing clients by further deepening the relationships – offering new products and innovative solutions. We also intend to develop new relationships – though on a selective basis. Our differential capabilities stemming from the Group expertise vis-à-vis other players in the market enable us to anticipate and respond to the extraordinary changes that may take place in the future.

The objective is to add value to the client’s businesses at an acceptable risk.

Nepal, which holds a huge potential to become a popular tourist destination, has witnessed a rise in the flow of tourists into the country. This trend is likely to continue. Similarly, the steady economic growth of India and China is likely to offer significant opportunities for Nepal to act as a trade corridor. Appropriate policy decisions to capitalize on these opportunities are expected to have a positive impact in propelling the economic growth of the country and in transforming the lives of common people through their economic development. The formation of a stable government will provide the much needed impetus for economic growth.

The growing trend of inward remittances into the country is likely to play a pivotal role in expanding the consumer market.

CEO & Director’s Report continued

Enhancing plastic money culture With a view to enhance plastic money culture in Nepal, the Bank has since long been offering Credit, Debit and Prepaid cards to the market.

Broadening the market reach With a view to reach out to the Women segment in the market, the Bank has introduced Diva Account built-in with an attractive product packages.

Handling of complex FX transactions Bank has already built its capability to underwrite and manage customer transactions relating to Interest Rate and other Derivatives.

Wholesale trade of gold The Bank is `Leading the Way’ in Wholesale trade (import and sale) of physical gold in Nepal today. The Bank was one of the pioneers in introducing this product to the Nepalese market.

Home Remit SCB Nepal has established itself as a key player for remittance transactions emanating from the Middle East. ‘Standard Chartered Home Remit’ provides an easy solution to our customers in meeting their needs.

15www.standardchartered.com/np

Bus

ines

s re

view

ove

rvie

wC

orp

ora

te G

ove

rnan

ceFi

nanc

ial s

tate

men

ts a

nd n

ote

s

We are making continuous efforts to better our revenue streams through innovation as well as by introducing products which provide value added financial solutions to our customers. Our prime objective is to provide safety to our loyal depositor base by maintaining a healthy net-worth and liquidity position. As a Bank, we are resilient with a good appetite for acceptable risks as we have a strong balance sheet coupled with our expertise in striking a proper balance between risks and growth. We will combine our global capability, deep local knowledge and creativity to outperform the competition.

In line with our brand promise to be The Right Partner, we will continue to invest in our people, processes and systems so as to improve our quality of service for customer delight. For our communities we will endeavor to make a real difference. We will consciously drive and maintain our high level of governance. For our shareholders we shall strive to continue providing them with superior returns.

Credit EnvironmentThe last Financial Year remained very challenging in terms of risk management. Since the onset of the financial crisis about two years ago, there have been catastrophic effects in the major global economies with contraction in GDPs, bankruptcies of large number of corporates and financial institutions and sharply rising unemployment particularly in the developed western world. The instability and uncertainty in the global economy is not yet over. Though Nepal was relatively insulated from the global financial crisis, the sharp and sudden drop in commodity prices globally and severe fluctuations in exchange markets have had adverse impacts in the country’s corporate sector. The continued security concerns and political uncertainty in the country, very high inflation level, growing energy crisis, frequent industrial and transport strikes (bandhs) were some other key elements affecting the country’s credit environment in the last FY.

Unfavorable macroeconomic situation and tough competition in the banking industry also affected the credit environment. Industrial sector recorded a

declining trend. The overall business momentum in the country remained slow owing to the concerns in political stability, security situation, power supply, labour relations and the global economy. Nepal’s economic growth rate in last FY 2008/09 is estimated to have declined as the agriculture sector suffered from adverse weather conditions and non-agriculture sector also could not perform better due mainly to unstable socio-political situations.

Against the backdrop of a difficult economic and political environment, we have been able to maintain our credit quality owing to our robust risk management procedures. We continue to stick to the fundamentals of good banking. Clear strategy, broadening and deepening our relationships with existing clients, rigorous monitoring, debating on risk-return dynamics, etc are pivotal to our ongoing success in risk management.

AuditorCSC & Co; Chartered Accountants, were reappointed as Statutory Auditors for FY 2008/09 by the 22nd Annual General Meeting of the Bank held on 25th of November 2008. They are not eligible for reappointment as Auditors. We would like to thank them for their contribution made during their tenure as Auditors of the Bank. As per the recommendation of the Audit Committee, this meeting will decide on the appointment of the auditor for next year.

Proposed DividendThe 253rd meeting of the Board of Directors of the Bank has proposed dividend to the shareholders of the Bank for the year ended 15 July 2009 at the rate of 50% in cash and issue of bonus share of one for each two shares held.

Sujit MundulDirector and CEO

Outserve Plus- Striving for success Bank staff indulge in the morning or afternoon huddles/storming sessions and brainstorm to find ways to improve both service and product standards with a view of ‘Outserving’ its customers.

Online banking: Bank’s Online Banking has gained popularity in terms of reliability and security as an alternate banking channel. The Bank today has about 10,000 customers subscribing to this facility.

Annual Report and Accounts 2008-200916

In this context, we believe that our sustainability agenda must take into account the fundamental task of re-establishing confidence and trust in banks whilst continuing to maintain an unwavering focus on addressing the longer-term challenges that the world faces.

So our approach to sustainability focuses both on continuing to manage our core banking practices responsibly and on the seven specific areas which have been at the heart of our sustainability strategy for some years. These are outlined as below:

Access to financial servicesThe Bank is improving access to financial services to majority of population of Nepal and is committed to help bring who are not in realm of financial services into the mainstream economy. This is vital part of promoting economic growth and will help to bring people out of poverty.

The Bank considers that presence of an extensive network of micro finance institutions would, to a

The importance of taking a sustainable approach to businesses can be illustrated by the extraordinary dislocation and disruption in financial markets globally in 2008. Banks with unsustainable business models collapsed or were rescued by governments.

Our Approach to Corporate Responsibility

large extent, mitigate lack of credit delivery system to the unreached population of the country. The Bank’s association with this business has been for long in that SCB Nepal is the promoter of few rural development banks and Rural Microfinance Development Centre (RMDC). The Bank is represented in the Board of RMDC, an eminent wholesale lending micro finance entity. To facilitate onward lending to the rural population for the development of microfinance in Nepal, the Bank has been lending to rural development banks and NGO’s.

Sustainable financeThe world will need to generate twice the energy it does today but with half the carbon. The Bank believes in minimizing the environmental impact of whatever it does thereby influencing its customers and suppliers to do likewise through its sustainable lending practices and procurement processes.

The Bank has a policy in place on Environmental risk in lending since 1995. After 2003, Social and Ethical factors were also included in the policy where each credit application, regardless of its size is required to be identified, evaluated and if necessary, mitigate the Social and Environmental risks.

Tackling financial crimeTo effectively manage risks from financial crime and to minimise the risk of our products and services being used by money launderers, we use a multi-layered approach which starts with ‘Know Your customer’ (KYC)/ Customer Due Diligence (CDD) procedure from the time a customer opens an account. It also includes modern systems to screen suspicious transactions.

Responsible selling and marketingAs a result of the global financial crisis, many people have witnessed the value of their investments

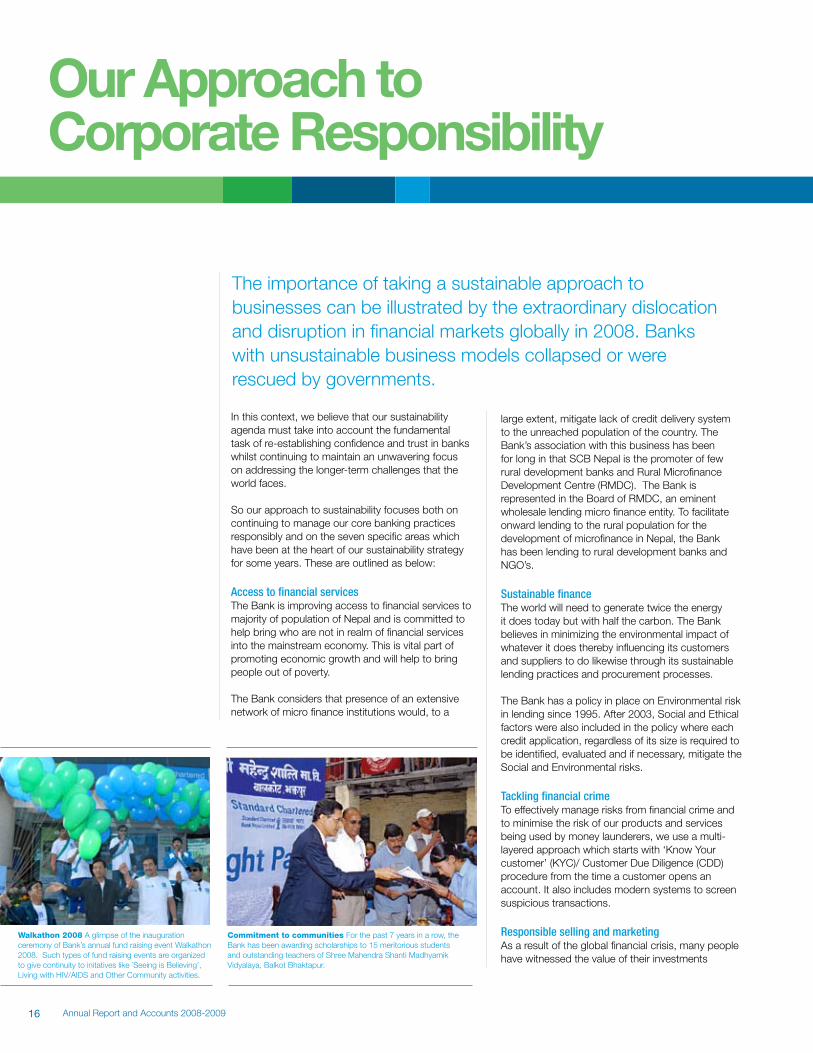

Walkathon 2008 A glimpse of the inauguration ceremony of Bank’s annual fund raising event Walkathon 2008. Such types of fund raising events are organized to give continuity to initatives like `Seeing is Believing’, Living with HIV/AIDS and Other Community activities.

Commitment to communities For the past 7 years in a row, the Bank has been awarding scholarships to 15 meritorious students and outstanding teachers of Shree Mahendra Shanti Madhyamik Vidyalaya, Balkot Bhaktapur.

Leading by touching lives

Annual Report and Accounts 2008-200918

drop. This has prompted increased customer and regulator awareness around the mis-selling of financial products and further highlights how responsible selling and marketing has to be at the heart of Banking.

Supporting our customers to make the right financial decisions sits at the core of our business. We have always taken the protection of customer’s funds seriously while endeavoring to match individual customer’s risk profiles to the products offered to them.

Great place to workOver the past five years, the number of our employees has substantially increased. We recognize that it is increasingly important to have a diverse, talented and engaged workforce to drive the growth opportunities we have in our markets. With rapid growth across our franchise and changing customer and employee demographics, the Bank believes that our innovative and sustainable approach to managing our people is a source of competitive advantage.

To sustain our success in future, along with the talents, diversity and values of our people, we refreshed awareness of our values as a guiding compass of responsible behaviors in 2008.

In 2007, we made good progress in three key areas as part of our approach to managing our people: Diversity and Inclusion (D&I), Employee Engagement and Health and Safety.

The Brand We place our brand, our most valuable asset, at the heart of our strategic intent to be the world’s best international Bank, leading the way in Asia, Africa and the Middle East. Our brand promise is to be the ‘Right Partner’ to our customers, communities, staff, stakeholders and regulators, and we practice

this through our businesses. To achieve our goal of continuing to be a truly a great brand in the market, we have invested strategically in our brand through various communication vehicles and community initiatives. Key sponsorships include Pro-Am event of the prestigious Surya Nepal Golf Tournament, Senior Nepal National Cricket Team, VOW Top 10 College Women Competition etc.

In line with sharing our best practices and being at the forefront of developing banking standards in the local market and our intent of partnering the regulators in the reform process/policy changes, the Bank sponsored a workshop on ‘World Financial Crisis and its impact in Nepal’ organized by Independent Business News (IBN).

Community InvestmentAs a leading corporate citizen with a responsibility to help ensure the country’s sustained growth and development, our approach is to take a long-term view of our actions and using our core skills and services to make a positive contribution to our society. Our work with local communities also helps

Our Approach to Corporate Responisbility continued

We recognize that it is increasingly

important to have a diverse, talented and

engaged workforce to drive the growth

opportunities we have in our markets.

Environment Day 2009 The Bank organized various programs to mark the World Environment Day 2009. Solar energy exhibition put-up by Environment Committee of the Bank in Naya Baneshwore and Lazimpat premises were major attractions.

Making a difference The Bank extended financial support to the Koshi Flood victims with a view to assist government in providing immediate relief measures. CEO Sujit Mundul handed over a cheque of NPR 500,001 to Finance Minister Baburam Bhattarai at his office in Singhadurbar.

Leading by touching lives SCB Nepal entered into an agreement with Tilganga Eye Centre (TEC) for sponsoring 600 cataract surgeries between period October 2008 to July 2009. Dr Sanduk Ruit, Director TEC and Sujit Mundul, CEO, SCB Nepal exchange agreement after signing the same.

We care With a view to assist Prayash Nepal, a drop-in centre for street children, SCB Nepal handed over a set of computer and stationery items for providing the children’s with an opportunity to learn and develop.

19www.standardchartered.com/np

Bus

ines

s re

view

ove

rvie

wC

orp

ora

te G

ove

rnan

ceFi

nanc

ial s

tate

men

ts a

nd n

ote

s

Go Greeen campaign Under the ‘Go Green’ campaign, SCB Nepal planted approximately 80 saplings of flowers and trees alongside Hariharbhawan Road in Lalitpur. The Executive Chief of Lalitpur Sub-Metropolitan City and Chief Executive Officer of SCB Nepal jointly inaugurated this initiative.

‘Sahayogi Haat Haru’ To assist Koshi Flood victims, the Bank partnered with Annapurna Post in their fund raising initiative `Sahayogi Haat Haru’. On behalf of the Bank, Diwakar Poudel, Head of Corporate Affairs handed over an additional financial assistance of NPR 200,000 under the initiative.

us to engage our employees, provide opportunities for product innovation and differentiate our brand.

With an objective to undertake various community initiatives in Nepal, SCB Nepal has constituted Standard Chartered Nepal Community Partnership Forum (SCNCPF) which has been registered with District Administration Office and has received affiliation from Social Welfare Council.

‘Seeing is Believing’ and ‘Living with HIV’ are the two major initiatives of the Bank under its ‘Believing in Life’ campaign launched in 2003.

Seeing is Believing (SiB)Seeing is Believing is our global programme to help tackle preventable and curable blindness. Launched in 2003, this programme has already reached over five million people in 17 countries, contributing to over two million sight restorations by the end of 2008.

Through the ‘Standard Chartered Nepal Walkathon’, the Bank provides a platform to engage cross sections of our community to raise funds. The Bank

has been conducting Walkathon –an annual fund raising event every year since 2003. Walkathon 2008 witnessed an active support and participation from all our stakeholders’ i.e. staff, vendors, customers and the community and made this event a great success. `Standard Chartered Nepal Walkathon’ continues to remain a signature event of the Bank.

Under the ‘Vitamin A Capsule distribution’ project, volunteers from SCB Nepal joined the teams from Helen Keller International (HKI) and the Nepal Technical Assistance Group (NTAG) to raise awareness and provide support to community health volunteers during the Nepal National Vitamin A Program’s distribution days on 19th & 20th April.

World Sight Day was celebrated on 12th of November 2008. An agreement was signed between the Bank and Tilganga Eye Centre (TEC) for conducting a minimum of 15 screening eye clinics with different community partners and for sponsoring 600 cataract surgeries. The Bank has been instrumental in restoring sights to more than

Vitamin A Capsule Distribution For the past 2 years, Standard Chartered Bank has been supporting Vitamin A Capsule distribution program in Kathmandu Valley through Helen Keller Nepal. The program supports feeding of Vitamin A Capsule to children between the age of 5-60 months.

Give blood... give life With the help of Blood Transfusion Centre, Nepal Red Cross Society, the Bank organized a blood donation camp at its premises in Naya Baneshwore. About 50 customers and staff members donated blood through this camp.

We have a vision- Seeing is Believing Patients after having undergone cataract surgery at a camp jointly organized by Tilganga Eye Centre and SCB Nepal.

Annual Report and Accounts 2008-200920

Our Approach to Corporate Responisbility continued

4,000 people till date. In FY 2008/09 alone, the Bank helped in restoration of sight to approximately 800 people. 25 Eye Clinics were conducted in different parts of the country through which ~ 9,000 underprivileged people in the community got an opportunity of treatment.

Under the Phase II program of SiB, SCB Group provided a financial assistance of USD 20,400 for procurement of the eye equipments to the Hetauda Community Eye Hospital, Hetauda.

Living with HIVLiving with HIV, is the Bank’s global HIV and AIDS education programme that aims to reduce the number of new HIV infections, reduce stigma associated with HIV, and meet our Clinton Global Initiative (CGI) commitment to educate one million people about HIV and AIDS by 2010.

Giving people the facts about HIV and AIDS enables them to avoid risky behavior and also dispels the myths that drive stigma. Education is part of our Group Policy on HIV. This takes place via face-to-face workshops and is supplemented by an online eLearning module. Education sessions are run by our own staff volunteers; who have undergone `Train the Trainers’ program and termed as “HIV Champions”.

The Bank extended support to Karuna Bhawan (a shelter home for the HIV infected women and children) by facilitating a skill learning training to help HIV infected women learn skills and generate income to support their livelihood.

Similarly, the Bank has been sponsoring the education and living expenses of two HIV- infected children from Maiti Nepal (MN) for three consecutive years.

Various activities were organized by SCB Nepal to mark the World AIDS Day 2008.

Our Focus on Youth, Health, Education and EnvironmentIn line with our effort to be ‘The Right Partner’ to the community where we operate, the Bank undertook various initiatives such as: Supported the Koshi flood victims by making

a contribution of NPR 500,001 to the Prime

Minister’s Relief Fund at a special ceremony held at Ministry of Finance.

Contributed NPR 200,001 in partnership with Annapurna Post (AP), a national daily in support of their initiative `Sahayogi Haat Haru’ as an immediate relief measure to Koshi flood victims. The assistance was channeled through Nepal Red Cross Society to the victims.

For the sixth consecutive year, the Bank continued its support to the deserving students of Shree Mahendra Shanti High School in Bhaktapur by providing incentives/scholarships through VISCOSS programme.

Organised a Blood donation camp with the technical assistance from Nepal Red Cross Society, Blood Transfusion Centre. More than 50 staff members and customers donated blood through this camp.

In the capacity of co-sponsor of Senior Nepal National Cricket Team, SCB Nepal branded the Team for ICC World Cricket League Div 5 Cricket Tournament held in Jersey and for the ACC Trophy held in Kuala Lumpur, Malaysia. The Bank has an exclusive right to brand the Senior National Cricket Team for its entire overseas matches. We are proud to be the co-sponsor of our National Team which has brought many glories to the nation. We are continuing with this sponsorship for year 2009/10 also.

Environment Environment being high on our agenda, the Bank has set up an Environment Committee which undertakes various initiatives for the Environmental conservation and awareness.

In our response to the growing environmental challenges, the Bank launched a Greenery project by planting 80 saplings alongside Hariharbhawan road in Kathmandu. It may be recalled that the Bank had planted 100 trees in Lakeside and New Road area of Pokhara in partnership with Green Pokhara in the year 2007/08.

To mark the Environment Day 2009, several activities were organized which included solar energy exhibition, vehicle de-carbonizing, wearing green, staff holding placards with environmental messages at the Bank’s entrance, car pooling, cycling to office, walking to office etc.

We care... Economic Journalist Gajendra Budathoki receiving a financial assistance of NPR 50,000 for his medical treatment from the CEO of SCB Nepal. Mr. Budathoki had earlier met with a fatal motorcycle accident.

Recognizing outstanding performance National Cricketer Mehboob Alam receiving a cash award of NPR 50,000 from Sujit Mundul, CEO SCB Nepal for his heroic 10 wicket haul in one innings in the ICC World Cup Division 5 Cricket Tournament against Mozambique. SCB Nepal is the sponsor of Senior Nepal National Cricket Team.

Leading with our sustainable

business strategy

Annual Report and Accounts 2008-200922

Our People, Our Strength

With an aspiration to start and grow their career with an organization that strives to be a Great Place to Work in, a total of 89 new joiners started their journey with the Bank in this fiscal year. As compared to last year, our staff strength was 392 as of July 15, 2009 against 377 full time equivalent staff in July 15, 2008. The current mix of male and female ratio is 62:38.A total of 3 ‘Right Start’ Induction Programs for the 68 New Joiners were conducted during the year. The program helps our new joiners make a great start with the Bank by enabling them to gain an overview of how the company works and also helps them become more quickly integrated into the organization. We believe that this program provides the new joiners the foundation that they need to build a wonderful career and perform at their best.

Driving performance through productivity and engagement Engaging employees is a key to retaining talent and helps to motivate them to ‘go the extra mile’, which is particularly important in today’s environment.

We genuinely believe that in the current challenging environment it is more important than ever to focus on our people. Establishing a strength based organization has been our priority where we know our people and help them to be at their best. We set clear performance expectations so that everyone knows what they are doing and how to perform at their best. We care about what happens to them, both in and outside work and inspire them to learn and grow.

We place particular importance on living the organization’s values embedded in our company culture. We believe that our behavior and culture which come from living our organization’s values are sources of our competitive advantage.

Keeping these priorities in mind the following initiatives/activities were conducted in the year under review:

Feel the Russh‘Feel the Russh’ workshop, which was originally rolled out a few years back was again conducted between 26-29 August for the staff who had not attended the workshop earlier. The workshop aimed at providing clarity to the Bank’s aspiration and strategy and boosting the passion and energy of individuals and teams to achieve the organizational mission.

Annual staff functionThe Bank recognizes the dedication, commitment and engagement of its people for its success and making it a Great Place to Work. Celebrating this at a function organized by the Bank staff members were honored for their dedicated 5, 10, 15 and 20 years of service to the Bank.

Living with HIV weekWe at Standard Chartered Nepal are committed to the pledge that SCB Group has made to the Clinton Global Initiative to educate one million people on HIV/AIDS by 2010.

Feel the Russh Staff actively participating in `Feel the Russh’ workshop organized by the Bank. The workshop was held with a view to provide clarity on SCB Group’s Vision and Strategy.

Diversity & Inclusion Female staff members greeted all their male counterparts in the Bank by presenting them with `palpali dhaka topi’ in celebration of Bhai Tika festival during ‘Tihar’.

Leading the way through our talented

and diverse team

Annual Report and Accounts 2008-200924

Our People, Our Strength continued

With the objective of educating, creating awareness and removing stigma around HIV/AIDS through our Living with HIV program both to internal and external stakeholders, we increased the number of HIV Champions who conducted many activities to celebrate the ‘Living with HIV Week’ starting from World AIDS Day, 1 December 2008.

Various activities like sharing stories, quotes, thoughts, creating the ambience in the work place was held throughout the week with a very high level of enthusiasm, creativity and engagement by all our people

Blood donation campWith very active participation of staff, a blood donation camp was organized by the Bank in collaboration with Nepal Red Cross Society on January 24, 2009 in the Bank’s Head Office premises.

International Women’s Day 2009 celebration With the objective to make our female colleagues feel special and to appreciate their contribution in the workplace, International Women’s Day 2009 was celebrated by organizing various engaging activities with a good level of cheer and participation of staff.

Vitamin A capsule distribution programTo get more closely associated with the Bank’s ‘Seeing is Believing’ initiative and to understand

more about Vitamin A capsule distribution program in the country which has received financial support from the SCB Group, 11 of our people volunteered to actively participate in this program in Kathmandu.

Wellness Week- May 10-15, 2009Wellness Week was observed in the Bank from May 10-15 with particular focus on Physical, Mental and Emotional Health.

Various activities were organized to mark the Wellness Week which generated a good level of interest and participation from our people in all the branches.

Other engagement programsOur people from various departments and branches participated in the “Soaltee Crowne Plaza Super Sixes Cricket Tournament – 2008” organized by Soaltee Crowne Plaza and in the “Inter Bank Volleyball Tournament 2009” organized by Nepal Rastra Bank (NRB) on the occasion of its 54th Anniversary.

We aim to create an inclusive workplace environment where everyone has the opportunity to maximise their potential and perform to their very best.

Handicraft exhibition Diversity & Inclusion (D & I) Committee put-up an exhibition of handicraft items under a program organized to mark International Women’s Day.

Jubilant after the training Members of staff in jubilant mood after undergoing `Great Managers’ training program organized by the Bank.

25www.standardchartered.com/np

Bus

ines

s re

view

ove

rvie

wC

orp

ora

te G

ove

rnan

ceFi

nanc

ial s

tate

men

ts a

nd n

ote

s

Learning and DevelopmentWe believe that development of our people is crucial for the growth and prosperity of the organization as they are one of the determining factors for the success of the company. We provide our diverse workforce with the skills needed to serve our customers and operate in an international environment. Number of learning opportunities - In-house trainings, Local programs by external trainers/organizations, Global trainings, Short term attachment programs in the Group, On the job learning inside and outside the country were given continuity during the year. A total of 1630 man-days were spent in learning and development programs during the review period.

Building great leadersOur strength based philosophy stands on our belief that we get the maximum contribution of our people by playing to their strengths. Ensuring that we get the best from our people is the responsibility of every leader in the Bank. For this purpose and in our continuous efforts to sharpen and enhance the leadership skills of our managers, the following Leadership Development Programs were conducted in this fiscal year:

• “LeadingTeamsEffectively”• “HowtoBuildaWinningTeam”• “GreatManagersProgram”

Diversity & InclusionIn today’s world the only thing that remains constant is change. Our markets, customer groups and talent pools are constantly changing. Our success depends on our ability to manage these changes, and our approach to Diversity and Inclusion (D&I). D&I lie in the heart of our Values. We focus on inclusion to ensure that each individual feels valued for what they bring to the Bank.

Our country D&I Committee along with the Group’s D&I Council are involved in driving D&I agenda across the Bank.

In addition to the cash rewards, our people’s extraordinary contributions are rewarded by excellence awards, appreciation letters and learning and development opportunities.

Ready for the tournament Members of SCB Nepal Volleyball Team that represented the Bank in Inter Bank Volleyball Tournament ogranised by Nepal Rastra Bank to mark its 54th anniversary.

After the training Participants of training program `How to influence others and win co-operation’ organized by the Bank.

Annual Report and Accounts 2008-200926

Our approach to corporate governance

A SynopsisDetails relating to steps taken by the management for strengthening Corporate Governance in the organisation.

The Board of Standard Chartered Bank is responsible and accountable to the shareholders and ensures that proper corporate governance standards are maintained.

The Audit Committee meets quarterly to review the internal and external inspection reports, control and compliance issues and provides feedback to the Board as appropriate.

The Manco (Management Committee) represented by all Business and Function Heads is the apex body managing the day to day operations of the Bank. Chaired by the CEO, it meets at least once a month for formulating strategic decisions.

The Annual General Meeting is used as an opportunity to communicate with all shareholders.

To ensure compliance with applicable laws, enhance resilience to external events and avoid reputational risk, the Board has adopted SCB Group policies and procedures.

Ultimate responsibility of effective Risk Management rests with the Board supported by Audit Committee, Manco, Country Operational Risk Group (CORG), Asset and Liability Committee (ALCO) and Credit Risk Management Committee (CRMC)

Embracing exemplary standards of governance and ethics wherever we operate is an integral part of our Strategic Intent. The Group Code

of Conduct is adopted to help us meet this objective by setting out the standards of behavior we must follow with each other and with our customers, communities, investors and regulators.

AnalysisThe Board of Standard Chartered Bank Nepal Limited is responsible for the overall management of the Company and for ensuring that proper corporate governance standards are maintained. The Board is also responsible & accountable to shareholders.

The report describes how the Board has applied the principles and provisions of the Nepal Rastra Bank directives on Corporate Governance and the provisions of Company Act, 2063 and Bank and Financial Institution Act, 2063 (the “Corporate Governance Code”). The directors confirm that: throughout FY 2065/066, the Company

complied with all the provisions of the Corporate Governance Code.

throughout FY 2065/066, the Company complied with the listing rules of Nepal Stock Exchange Limited.

throughout FY 2065/066, the Company complied with the Securities Registration and Issuance Regulation, 2065

the Company has adopted a code of conduct regarding securities transactions by directors on further terms no less than required by the Nepal Rastra Bank Directives and the Company Act and that all the Directors of the Bank complied with the Code of Conduct throughout FY 2065/066.

The BoardAs at the date of this report, the Board is made up of the Non-Executive Chairman, one Executive Director and four Non-Executive Directors of which one is professional /independent Director appointed as per the regulatory requirement and one Director, representing the public shareholders. The Board composition complied with the regulatory requirements. Four Directors including the Non-Executive Chairman are nominated by the SCB Group to represent it in the Board in proportion to its shareholding. The Board meets regularly and has a formal schedule of matters specifically reserved for its decision. These matters include determining and reviewing the strategy of the Company, annual

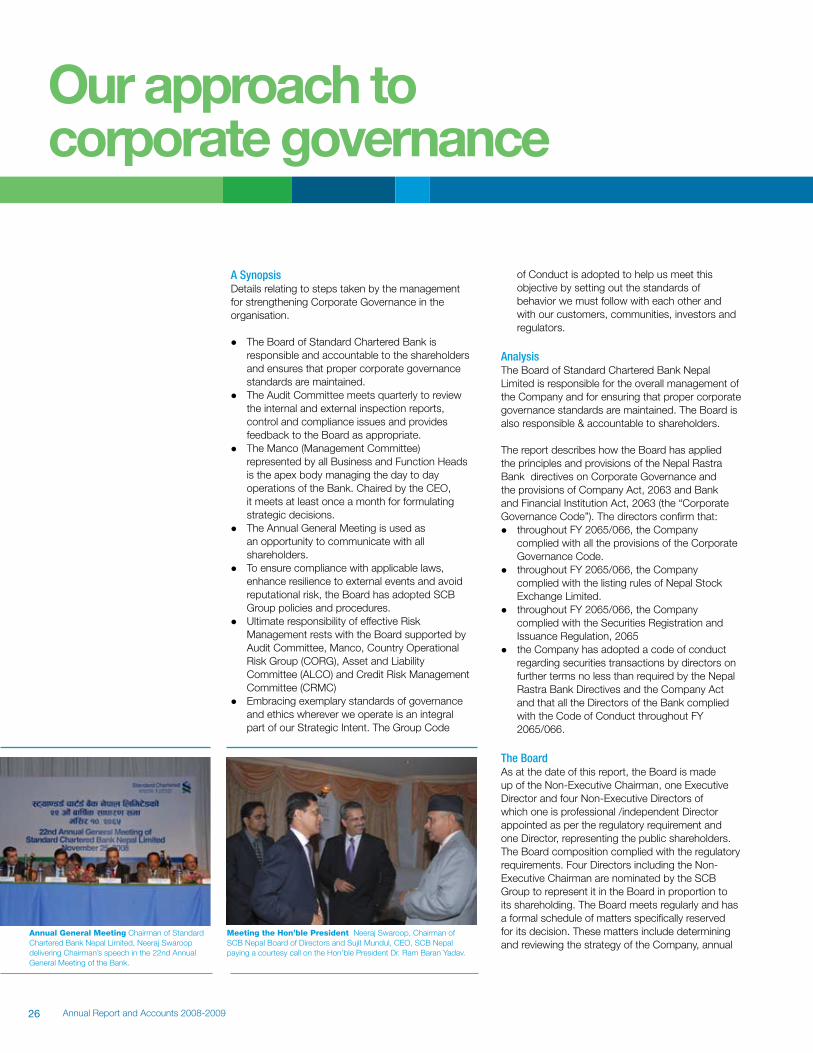

Annual General Meeting Chairman of Standard Chartered Bank Nepal Limited, Neeraj Swaroop delivering Chairman’s speech in the 22nd Annual General Meeting of the Bank.

Meeting the Hon’ble President Neeraj Swaroop, Chairman of SCB Nepal Board of Directors and Sujit Mundul, CEO, SCB Nepal paying a courtesy call on the Hon’ble President Dr. Ram Baran Yadav.

Leading the way through a

collective vision

Annual Report and Accounts 2008-200928

budget, overseeing statutory and regulatory compliance and issues related to the Company’s capital. The Board is collectively responsible for the success of the Bank.

During the year under review, the Board held 13 board meetings of which 4 were held by circulations. The Directors are given accurate, timely and clear information so that they can maintain full and effective control over strategic, financial, operational, compliance and governance issues.

The following table shows the number of Board and Audit Committee meetings held during the year:

Audit Board Committee

Number of meetings in FY 2065/066 13 4Neeraj Swaroop 7 -Anurag Adlakha* 8 -Sushen Jhingan* 12 -Sujit Mundul 13 -Ram Bahadur Aryal 13 4Arjun Bandhu Regmi 13 -

* Mr. Anurag Adlakha attended two Board meetings through his

alternate Director Mr. Rajeev Uberoi and Mr. Sushen Jhingan attended

one Board meeting through his alternate Director Mr. Peter Warbanoff.

Audit Committee As required by the local regulations, the Board has formed an Audit Committee with clear terms of reference. The Audit Committee meeting is normally held on a quarterly basis. The Committee reviews internal audit reports, Nepal Rastra Bank Inspection reports, Statutory Audit reports, Bank’s financial condition, internal audit/controls issues, compliance issues, etc. The Committee provides guidance/feedback to the Management through the Board of Directors as appropriate.

The Independent/Professional Director chairs the Committee for ensuring complete independence. The composition of the Audit Committee as on 15/07/2009 is as follows:

Ram Bahadur Aryal - Non Executive Director- Chairman

Anurag Adlakha - Director - Member Sushen Jhingan, Director - Member Gopi Krishna Bhandari - Member Kabir Tamrakar - Member Secretary

All members of the Audit Committee are either non-executive directors or independent of business. The responsibilities of the Committee are in congruence with the framework defined by the NRB Directives and the Company Act.

Management Committee (Manco)The Management Committee (Manco) represented by all Business and Function Heads of the Bank is the apex body that manages the Bank’s operation on a day to day basis. Manco meets formally at least once a month and informally as and when required. The strategies for the Bank are decided and monitored on a regular basis and decisions are taken jointly by this Committee. The CEO chairs the Manco.

As at the date of this report, the composition of the Manco was as follows:

Mr. Sujit Mundul, Chief Executive Officer Mr. Anurag Mishra, Head Wholesale Banking Ms. Anju Sharma, Head Consumer Banking Ms. Rakhi Singh, Chief Financial Officer Mr. Sudesh Khaling, Chief Information Officer Mr. Shobha Bd. Rana, Head Legal and Compliance

& Assurance Mr. Diwakar Poudel, Head Corporate Affairs Ms. Bina Rana, Head Human Resources Mr. Gopi Bhandari, Senior Manager Credit

The effectiveness of the Company’s internal control system is reviewed regularly by the Board, its committees, Management and Internal Audit.

Our Approach to Corporate Governance continued

29www.standardchartered.com/np

Bus

ines

s re

view

Co

rpo

rate

Go

vern

ance

Fina

ncia

l sta

tem

ents

and

no

tes

Relations with Shareholders The Board recognizes the importance of good communications with all shareholders. There are regular information, both financial as well as non-financial, published by the Company for shareholder’s information. The AGM is used as an opportunity to communicate with all the shareholders.

The notice of the AGM, as required by the Company Act, was sent to shareholders at least 21 days before the date of the meeting at their mailing addresses available in the Company’s records. In addition to that the notice and agenda of the AGM were also published twice in the national level daily newspaper for the shareholders information.

Internal ControlThe Board is committed to managing risks and to controlling its business and financial activities in a manner which enables it to maximize profitable business opportunities, avoid or reduce risks which can cause loss or reputational damage, ensure compliance with applicable laws and regulations and enhance resilience to external events. To achieve this, the Board has adopted the SCB Group policies and procedures of risk identification, risk evaluation, risk mitigation and control/monitoring.

The effectiveness of the Company’s internal control system is reviewed regularly by the Board, its committees, Management and Internal Audit. The Audit Committee has reviewed the effectiveness of the Bank’s system of internal control during the year and provided feedbacks to the Board as appropriate.

The Internal Audit monitors compliance with policies/standards and the effectiveness of internal control structures across the Company through its program of business/unit audits. The Internal Audit function is focused on the areas of greatest risk as determined by a risk-based assessment methodology. Internal Audit reports are periodically forwarded to the Audit Committee. The findings of all audits are reported to the Chief Executive Officer and Business Heads for immediate corrective measures.