Basel III - Implementation issues facing the Industry Patricia Jackson Head of Financial Regulation Advisory EMEIA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Basel III - Implementation issues facing the IndustryPatricia Jackson

Head of Financial Regulation Advisory EMEIA

Head of Financial Regulation Advisory EMEIAPage 2

Systemically Important Banks

► FSB paper on intensive supervision – Other elements are under discussion

– Contains a number of components:

SIFIs

Intensive supervision

Early Action

ResolutionBail -in/cocos

Higher Capital

Large exposures

SIFIs

Intensive supervision

Early Action

ResolutionBail -in/cocos

Higher Capital

Large exposures

National

discretion will

create unlevel

playing field

Mandatory

recovery and

resolution

planning

This will create pressures– global strengthening of regulatory regimes. Global

increase in focus on stress testing and governance.

Head of Financial Regulation Advisory EMEIAPage 3

Practical Implications - SIFIs, CoCo, Bail In, Resolution

The shareholder dynamic:

► CoCo layer held by hedge funds,

sovereign wealth funds, etc

► As bail in approaches so are bonds

► In the CoCo layer shareholder

dynamic shifts – authorities now

dealing with hedge funds.

Bail In – issues and challenges:

► Equity holders – are they wiped out

when bail in is triggered

► Scope ?

► All wholesale

► Senior bonds

► Derivatives

► How to execute recapitalisation –

determining haircuts for bail in, how

to allocate to creditors. Can it be

done over a weekend? Or is more

time required?

► Contracts – statutory classification

issues

► Linking bail in with resolution?

Bank can no longer operate

standalone below a level (eg A-)

– value unravels quickly due to

loss of swap rating,

counterparties step away, etc,

bank run

CoCo Layer

~7% capital trigger

Bail in –separate

from resolution

ResolutionOr Bail in linked to

resolution

Recovery

Remedial

actions

Recovery

actions

AA

AA-

A+

A

A-

Recovery

Bank unravels

Head of Financial Regulation Advisory EMEIAPage 4

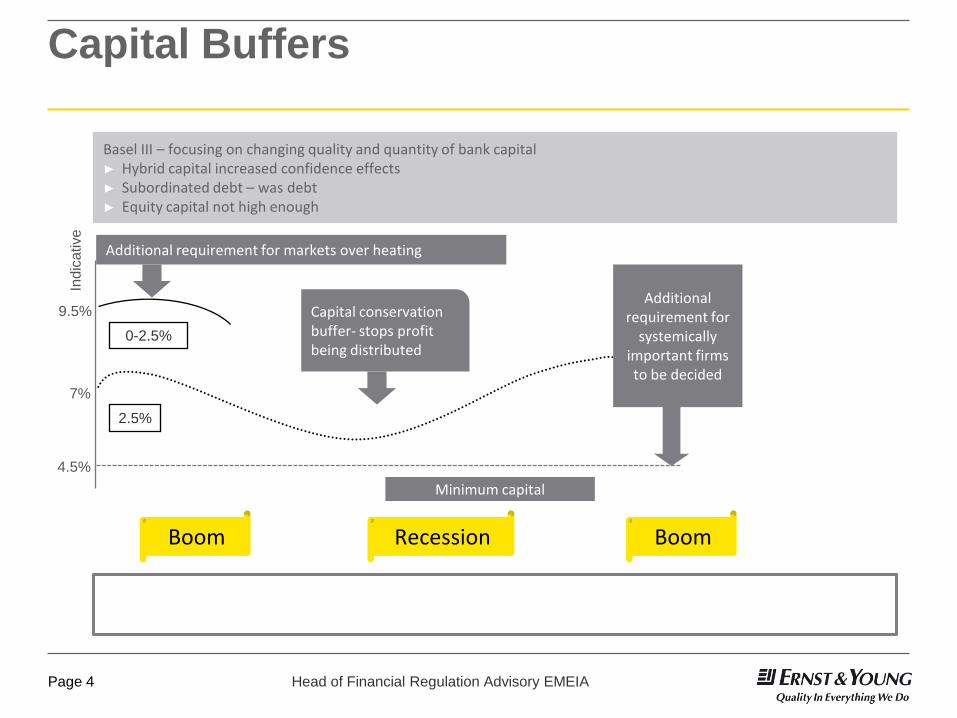

Capital Buffers

Basel III – focusing on changing quality and quantity of bank capital► Hybrid capital increased confidence effects► Subordinated debt – was debt► Equity capital not high enough

► But multiple buffers will add to complexity► Too much capital will drive disintermediation► Increase cost for industry - industry incentive to move to point in time models to offset buffers

Minimum capital

Additional requirement for

systemically important firms to be decided

Boom Recession

Additional requirement for markets over heating

Capital conservation buffer- stops profit being distributed

4.5%

7%

9.5%

Indic

ative

Boom

0-2.5%

2.5%

Head of Financial Regulation Advisory EMEIAPage 5

Changes to trading book treatments

Changes to the trading

book

Securitisation exposures in trading book

Revised specific risk charges for equity exposure

Stressed VaR

and EPE

New incremental risk

and CVA charges

Counterparty risk changes

magnify effect – capital now

rises 3 to 4 times particularly

because of CVA

These changes increase capital in trading books by 100%

Head of Financial Regulation Advisory EMEIAPage 6

Basel Committee Quantitative Impact study – capital impact relative to end 2009

Reduction

5.4

Percentage

points

Reduction

2.9

Percentage

points

5.7% Post-Basel III 7.8%

CETI 11.1% (Group 1) Pre-Basel III 10.7% (Group 2)

263 Banks – Across 23 countries

94 large/international ( Group 1)

169 others (Group2)

Head of Financial Regulation Advisory EMEIAPage 7

Overall additional capital required

50% raised already- but 50% still to raise

Over €400bn raised in past 2 years

Basel

QIS Sample

CET1

4.5%

CET1

7%

Shortfall end 2009

Group 1 €165bn €575bn

Group 2 €8bn €25bn

(10%)

(€825bn)

Overall private sector estimate for whole European banking

industry up to € 1 trillion more capital needed.

Head of Financial Regulation Advisory EMEIAPage 8

QIS results – liquid assets shortfall

Shortfall €1.73tr – end 2009

Group 1 Group 2

Retail/ SME 10% 18%

Corporate 16% 21%

Financial

Institution

28% 26%

Collateral 25% 11%

Derivative

payables

7% 13%

Stock of high quality liquid assets

Net cash outflows over a 30-day time

period

≥100%

Contributions to the shortfall- liability

structure/shocks

Head of Financial Regulation Advisory EMEIAPage 9

Strategic Issues

► Business focus will have

to change.

► Spreads will need to rise 1

-2.5 percentage points.

► Proprietary trading much

less profitable –trading

book capital 3-4 times

higher .

► Large corporate lending

will be difficult to

remunerate.

► Markets will have to

change – increased

collateralised faster close

out swaps.

Cost of more

capital – 40% to

100% more equity

Cost of the

liquid assets

buffer

Leverage

constraint

Three way constraint on strategy

Head of Financial Regulation Advisory EMEIAPage 10

ROE

Pre-Crisis 15%

Estimates of cut pre-mitigating actions –

reduction around 4 percentage points

Components of the reduction

Capital quality 0.8 percentage points

Capital increase 1.3

Leverage ratio 0.1

Liquid assets 0.6

Strategic issue for the banks – how much disclosure needed to convince

equity investors they are safer

Sourc

e: M

cK

insey,

Basel III and E

uro

pean b

ankin

g: Its im

pact, h

ow

banks

mig

ht re

spond, and the c

halle

nges o

f im

ple

menta

tion, P

hili

pp H

ärle

et al.

Head of Financial Regulation Advisory EMEIAPage 11

Basel III will change the shape of markets

UK US

Unsecured inter bank Secured inter bank

Derivatives exposures uncollateralised

Pressure under Basel to: i) increase term of wholesale funding

ii) collateralise exposures

Head of Financial Regulation Advisory EMEIAPage 12

Liquidity- challenges /improvements needed

Systems/ processes

governance

Intra-day liquidity tracking

Contingent commit-

ments

Funds transfer pricing

Enhanced analytic

capability

Collateral tracking systems

Better consolidat-ed/ group wide data

New data hubs

needed

Key concern -regulatory uncertainty

Head of Financial Regulation Advisory EMEIAPage 13

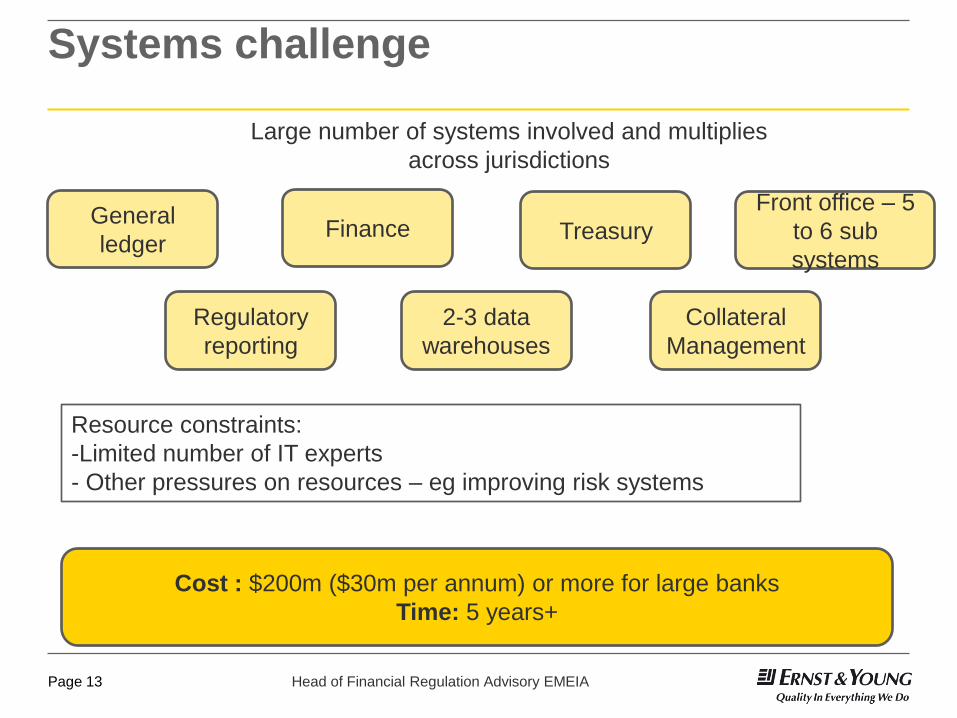

Systems challenge

Large number of systems involved and multiplies

across jurisdictions

General

ledger

Regulatory

reporting

Collateral

Management

2-3 data

warehouses

Finance Treasury

Front office – 5

to 6 sub

systems

Resource constraints:

-Limited number of IT experts

- Other pressures on resources – eg improving risk systems

Cost : $200m ($30m per annum) or more for large banks

Time: 5 years+

Head of Financial Regulation Advisory EMEIAPage 14

New Capital instruments

Issues

Uncertainty re allowable instruments

Large volume

(€250bn) of hybrid

maturing by 2018

Size of market for Cocos –

depends on clarity of triggers

Uncertainty about bail-in

Bank equity price

impacted by uncertainty

Could

take 4-5

years for

market

to build

Head of Financial Regulation Advisory EMEIAPage 15

Costs of regulatory compliance

Excluding enhancement of risk and

finance capabilities, capital, funding

and balance sheet management

Equivalent to 30%-50% of

Basel II costs

Regulatory compliance alone =

€45m - €70m per bank

Not

including

the large

systems

change

Head of Financial Regulation Advisory EMEIAPage 16

At the same time banks are running programmes to improve risk management

Head of Financial Regulation Advisory EMEIAPage 17

EY survey of risk management improvements/challenges

Areas of greatest progressAreas where more progress still needs to

be made

83%Increased board oversight of

risk78%

Revised compensation

schemes but only 40% are

close to completion of initial

changes

89%Strengthened the role of the

CRO 92%Increased attention on risk

culture, but only 23% report a

significant shift

65%Made adjustments to allocating

capital across business units 96%Increased focus on risk

appetite, but only 25% report a

link to business decisions

92%Changed approaches to

liquidity risk management, and

82% instituted more rigorous

internal pricing

59%Enhanced risk transparency,

but only 26% have yet made

significant changes

93%Implemented new stress

testing, but most firms continue

to see significant challenges

41%

48%

59%

65%

65%

76%

87%

Notional or gross positions

Valuation of uncertainty

Illiquidity

Stress VaR

Risks not in VaR

Counterparty risk

Stress testing

Areas of

increased

transparency

Related Documents