Impairment of Assets: IAS 36 Wiecek and Young IFRS Primer Chapter 16

Impairment of Assets: IAS 36 Wiecek and Young IFRS Primer Chapter 16.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Impairment of Assets:IAS 36

Wiecek and Young

IFRS PrimerChapter 16

2

Impairment of Assets

Related standards IAS 36 Current GAAP comparisons IFRS financial statement disclosures Looking ahead End-of-chapter practice

Related Standards

FAS 157 Fair value measurements FAS 144 Accounting for the impairment or

disposal of long-lived assets FAS 142 Goodwill and other intangible

assets FAS 141 Business combinations

3

Related Standards

IFRS 3 Business combinations IAS 16 Property, plant and equipment IAS 17 Leases IAS 27 Consolidated and separate financial

statements IAS 28 Investments in associates IAS 31 Interests in joint ventures IAS 38 Intangible assets IAS 40 Investment property

4

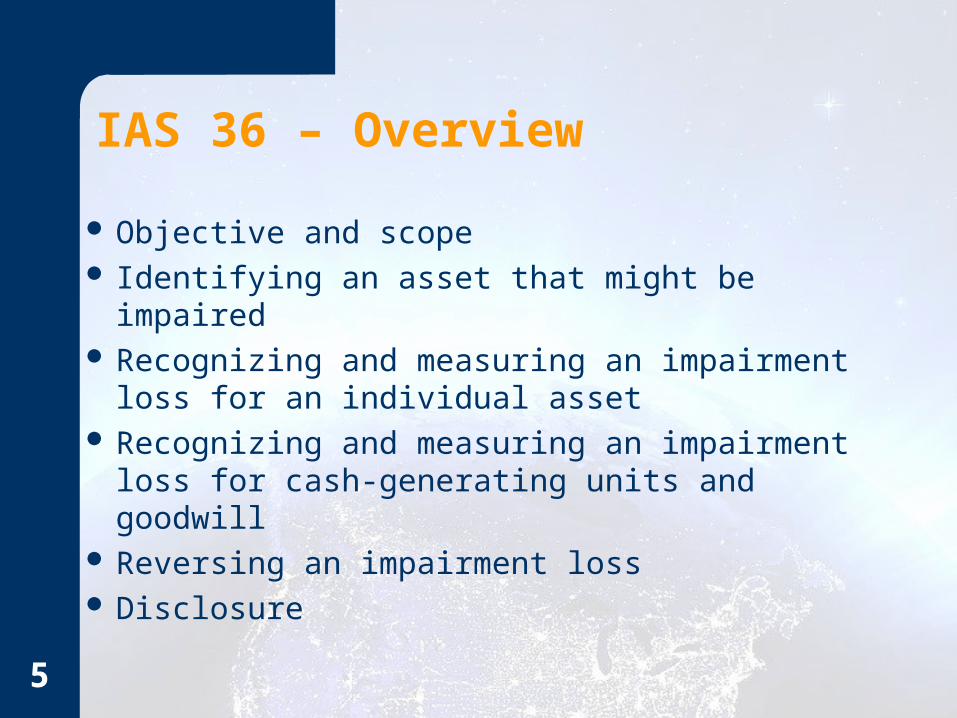

IAS 36 – Overview

Objective and scope Identifying an asset that might be impaired Recognizing and measuring an impairment

loss for an individual asset Recognizing and measuring an impairment

loss for cash-generating units and goodwill Reversing an impairment loss Disclosure

5

IAS 36 – Objective and Scope

IAS 36 ensures that assets are reported on the statement of financial position at no more than the entity can recover from their use or sale.

May be an impairment loss—“the amount by which the carrying amount of an asset or a cash-generating unit (CGU) exceeds its recoverable amount”

6

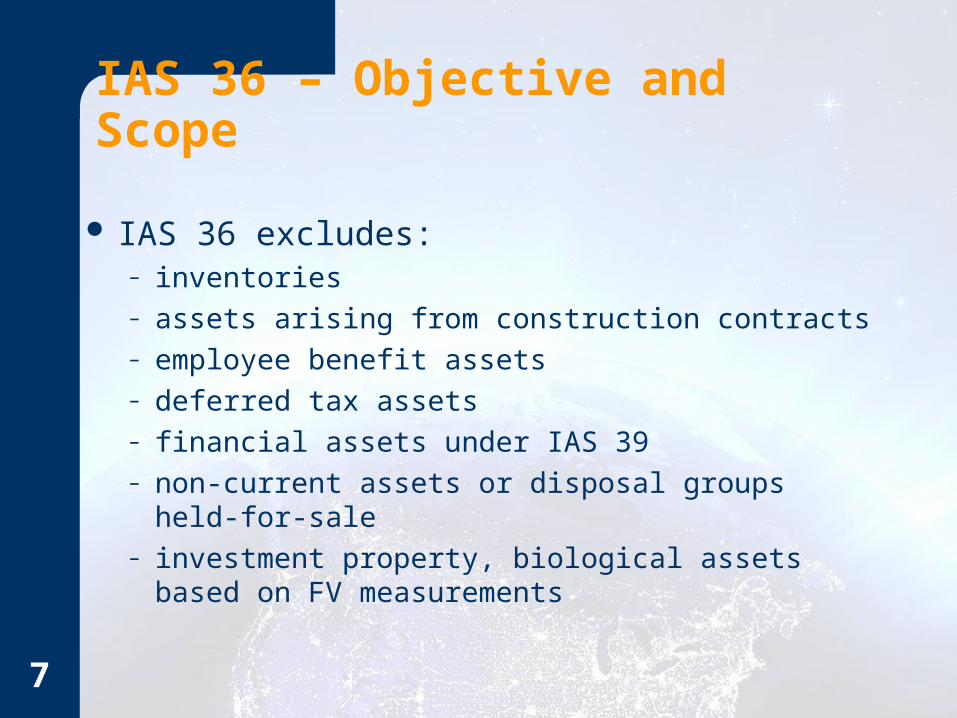

IAS 36 – Objective and Scope

IAS 36 excludes:– inventories– assets arising from construction contracts– employee benefit assets– deferred tax assets– financial assets under IAS 39– non-current assets or disposal groups held-for-sale– investment property, biological assets based on FV

measurements

7

IAS 36 – Objective and Scope

8

IAS 36 – Identifying an Asset that May Be Impaired

Assets– end of each reporting period– assess for indications of impairment– if indications of impairment, test for impairment

Intangibles with indefinite lives, those not yet ready for use, and goodwill– annually– test for impairment regardless of indications of

impairment

9

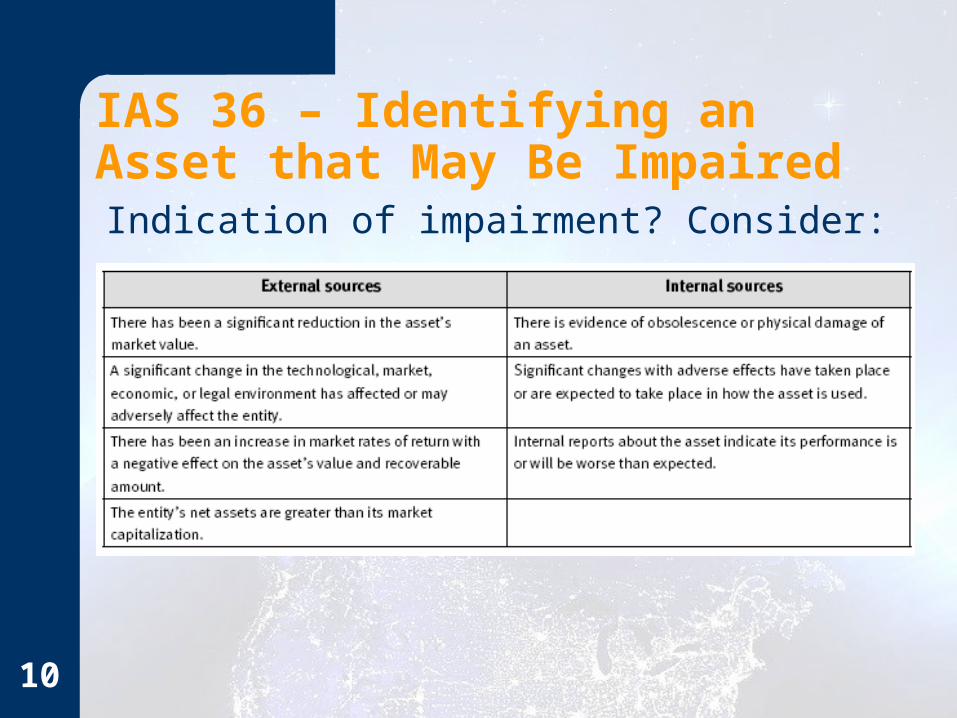

10

Indication of impairment? Consider:

IAS 36 – Identifying an Asset that May Be Impaired

IAS 36 – Identifying an Asset that May Be Impaired

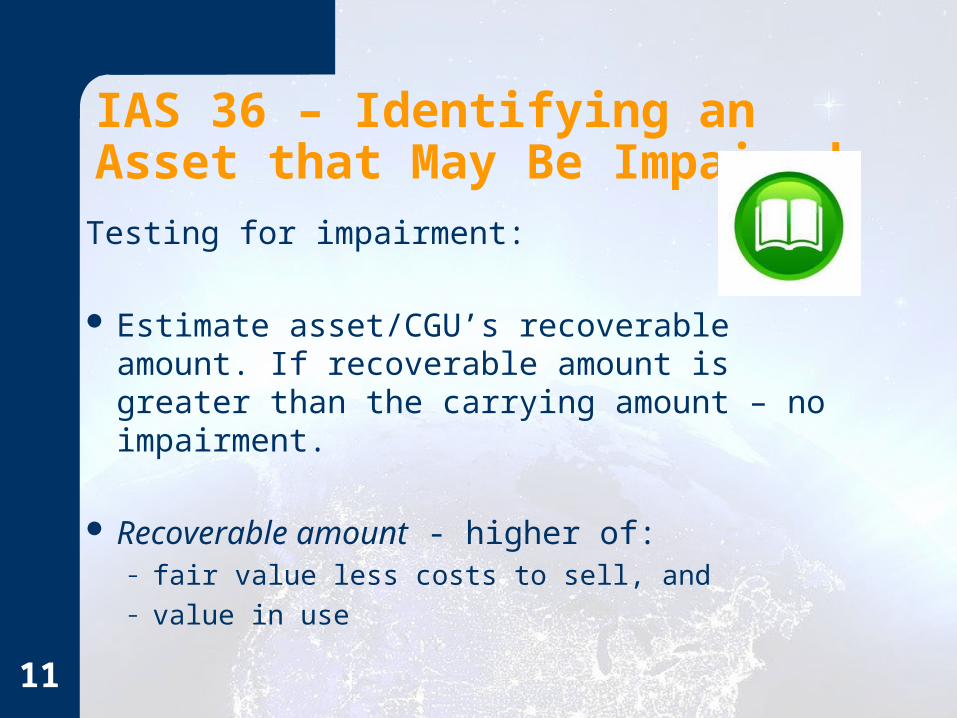

Testing for impairment:

Estimate asset/CGU’s recoverable amount. If recoverable amount is greater than the carrying amount – no impairment.

Recoverable amount - higher of:– fair value less costs to sell, and– value in use

11

For assets that do not generate independent cash flows on their own – group into cash-generating units (CGUs)

CGU – “the smallest identifiable group of assets that generates cash flows that are largely independent of the cash flows from other assets or groups of assets”

12

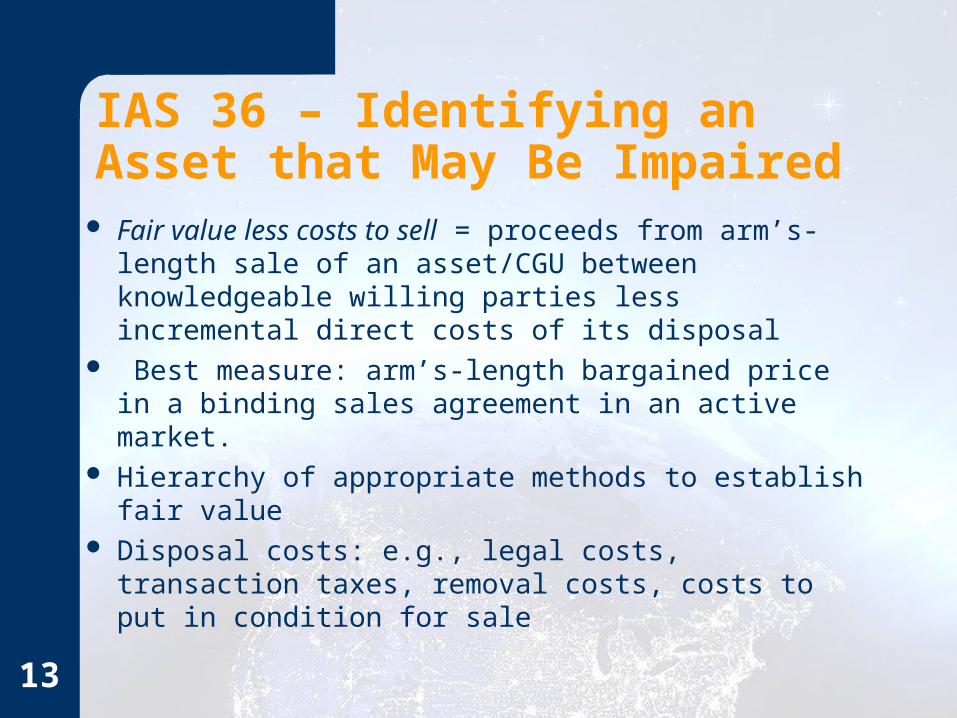

IAS 36 – Identifying an Asset that May Be Impaired

Fair value less costs to sell = proceeds from arm’s-length sale of an asset/CGU between knowledgeable willing parties less incremental direct costs of its disposal

Best measure: arm’s-length bargained price in a binding sales agreement in an active market.

Hierarchy of appropriate methods to establish fair value

Disposal costs: e.g., legal costs, transaction taxes, removal costs, costs to put in condition for sale

13

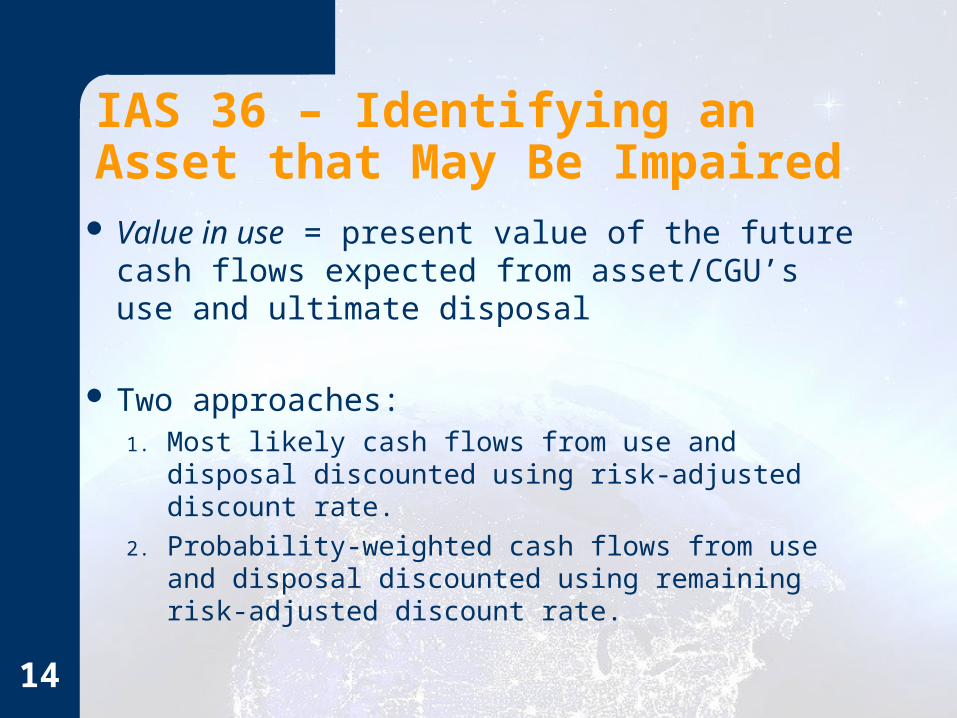

IAS 36 – Identifying an Asset that May Be Impaired

Value in use = present value of the future cash flows expected from asset/CGU’s use and ultimate disposal

Two approaches:1. Most likely cash flows from use and disposal

discounted using risk-adjusted discount rate.

2. Probability-weighted cash flows from use and disposal discounted using remaining risk-adjusted discount rate.

14

IAS 36 – Identifying an Asset that May Be Impaired

Estimated cash flows with a 40% probability they will be $120 and a 60% probability they will be $80. Value in use?

Method 1: Most likely cash flows = $80. This amount is discounted using a rate that takes into account all risks including the uncertainty of the cash flow amounts.

Method 2: Expected value of cash flows = (120 × 40%) + (80 × 60%) = $96. This amount is discounted using a rate that includes remaining risks.

15

IAS 36 – Identifying an Asset that May Be Impaired

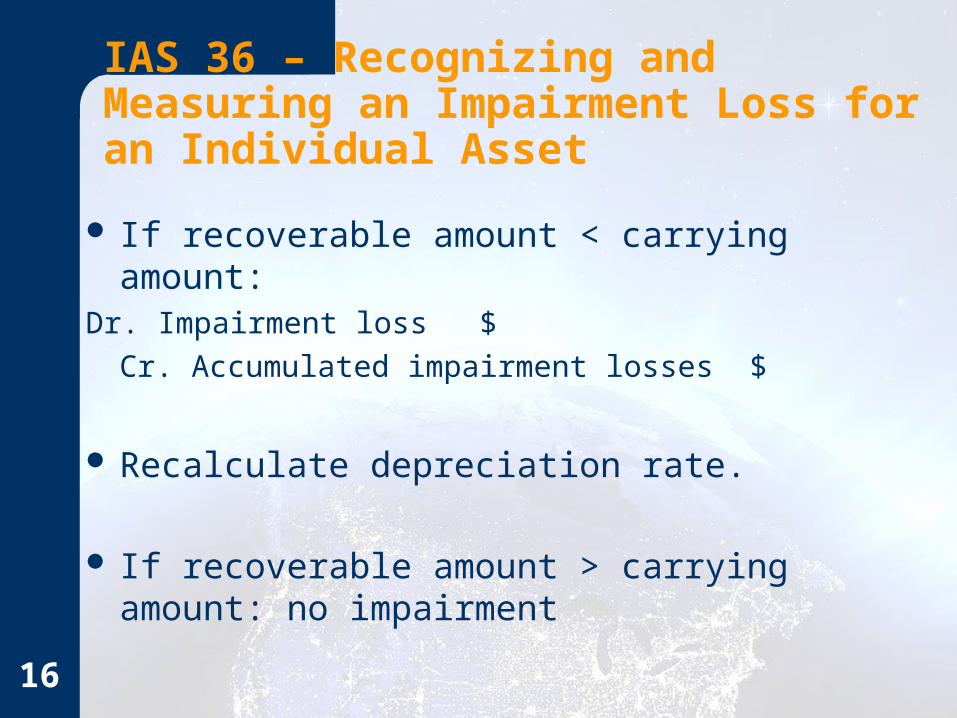

If recoverable amount < carrying amount:Dr. Impairment loss $

Cr. Accumulated impairment losses $

Recalculate depreciation rate.

If recoverable amount > carrying amount: no

impairment

16

IAS 36 – Recognizing and Measuring an Impairment Loss for an Individual Asset

IAS 36 – Recognizing and Measuring an Impairment Loss for CGUs and Goodwill

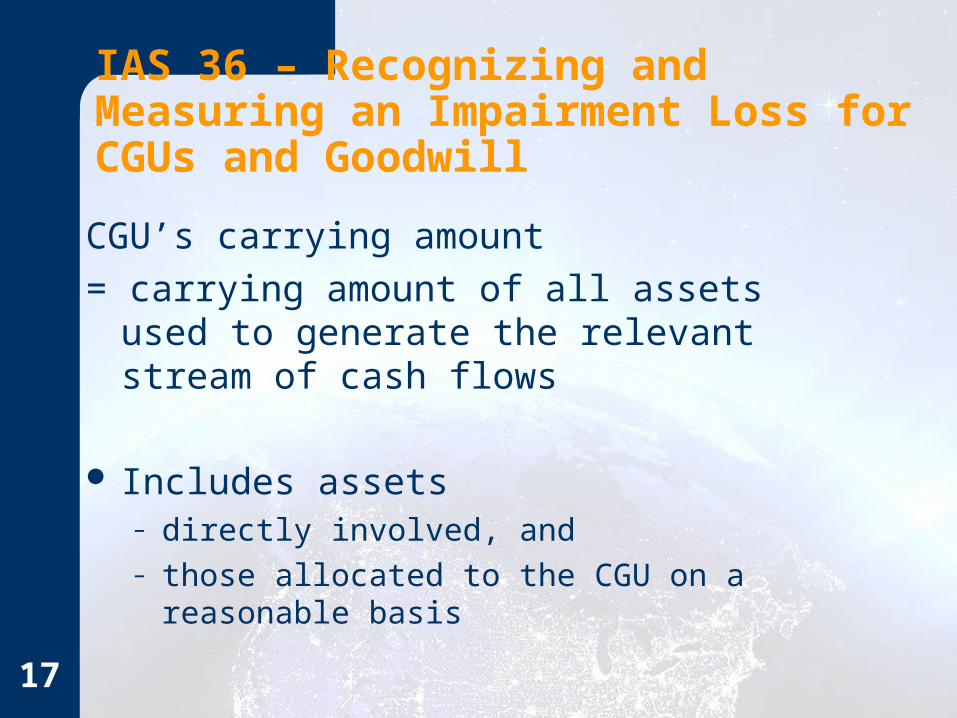

CGU’s carrying amount

= carrying amount of all assets used to generate the relevant stream of cash flows

Includes assets

– directly involved, and – those allocated to the CGU on a reasonable basis

17

Goodwill allocated to a CGU or group of CGUs not larger than an “operating segment” that is:– expected to benefit from synergies of a

combination– at lowest level in organization that manages the

goodwill– not on an arbitrary basis

18

IAS 36 – Recognizing and Measuring an Impairment Loss for CGUs and Goodwill

If part of CGU with allocated goodwill is sold:– allocate goodwill between portion sold and portion

remaining– base on relative value of the CGU sold to portion

retained

19

IAS 36 – Recognizing and Measuring an Impairment Loss for CGUs and Goodwill

Testing CGUs for impairment CGUs with related G/W not allocated

specifically:– Test when an indication of impairment– Loss = CGU carrying amount excluding G/W -

recoverable amount CGUs with G/W allocated to it

– Test at least annually– Loss = CGU carrying amount including G/W –

recoverable amount

20

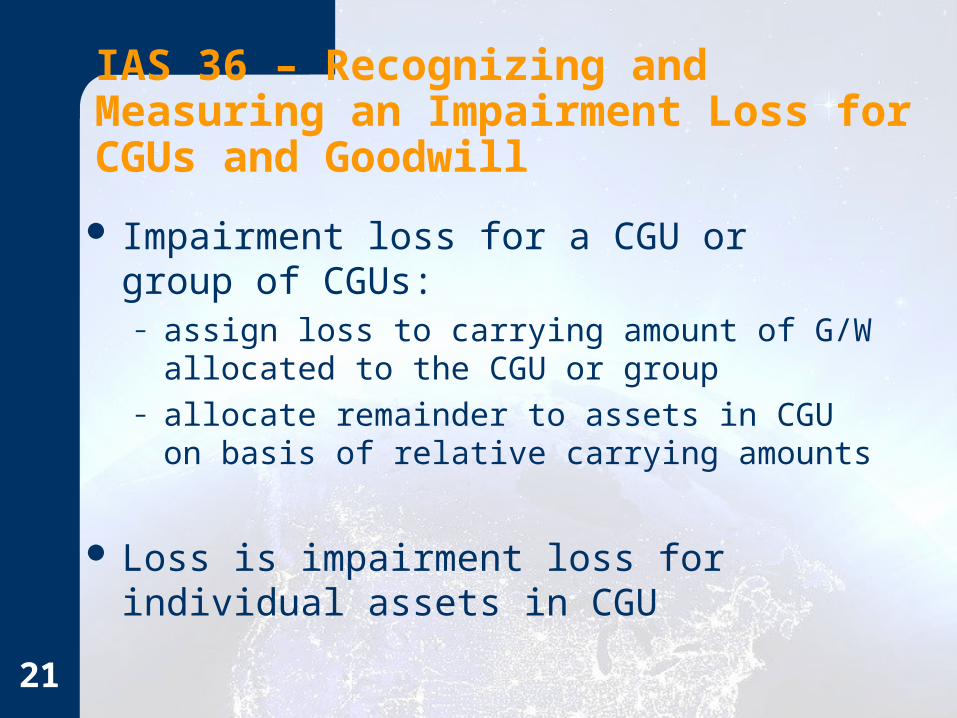

IAS 36 – Recognizing and Measuring an Impairment Loss for CGUs and Goodwill

Impairment loss for a CGU or group of CGUs:– assign loss to carrying amount of G/W allocated

to the CGU or group– allocate remainder to assets in CGU on basis of

relative carrying amounts

Loss is impairment loss for individual assets in CGU

21

IAS 36 – Recognizing and Measuring an Impairment Loss for CGUs and Goodwill

IAS 36 – Reversing an Impairment Loss

No reversal of impairment loss for G/W

For other assets, reversal permitted if estimates used to determine recoverable amount have changed

22

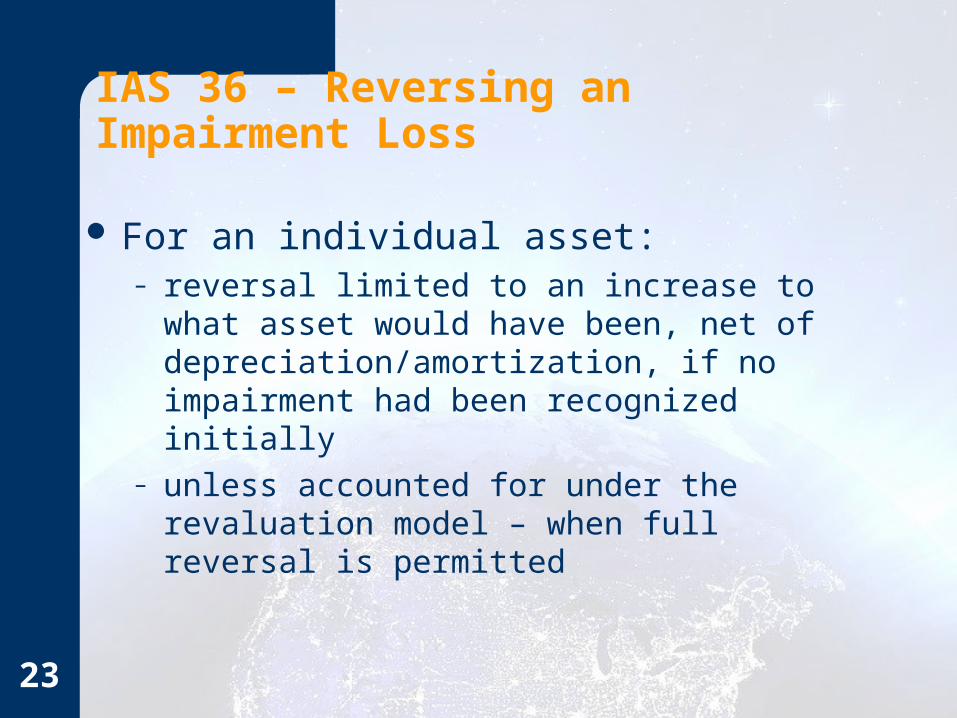

IAS 36 – Reversing an Impairment Loss

For an individual asset:– reversal limited to an increase to what asset

would have been, net of depreciation/amortization, if no impairment had been recognized initially

– unless accounted for under the revaluation model – when full reversal is permitted

23

For a CGU:– reversal is allocated to the assets of the unit,

excluding G/W– on basis of relative carrying amounts– restrictions on individual assets still apply

24

IAS 36 – Reversing an Impairment Loss

IAS36 – Disclosure

For each class of assets:– amount of impairment loss/loss reversals in P&L– line item where loss/reversal is reported– amount of impairment loss/loss reversals on

revalued assets in OCI

25

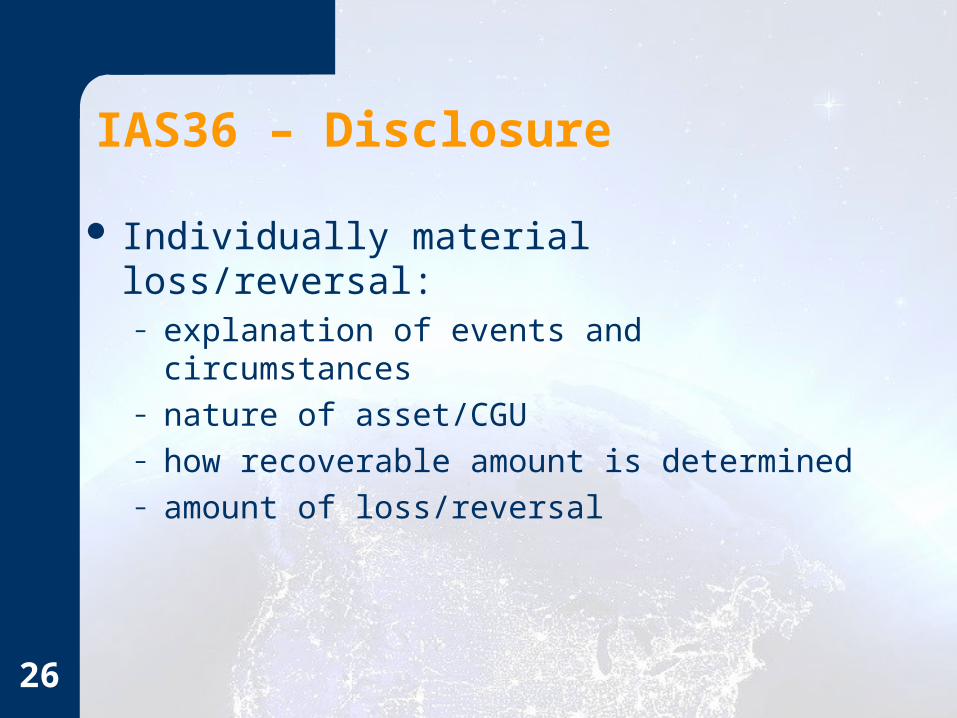

IAS36 – Disclosure

Individually material loss/reversal:– explanation of events and circumstances– nature of asset/CGU– how recoverable amount is determined– amount of loss/reversal

26

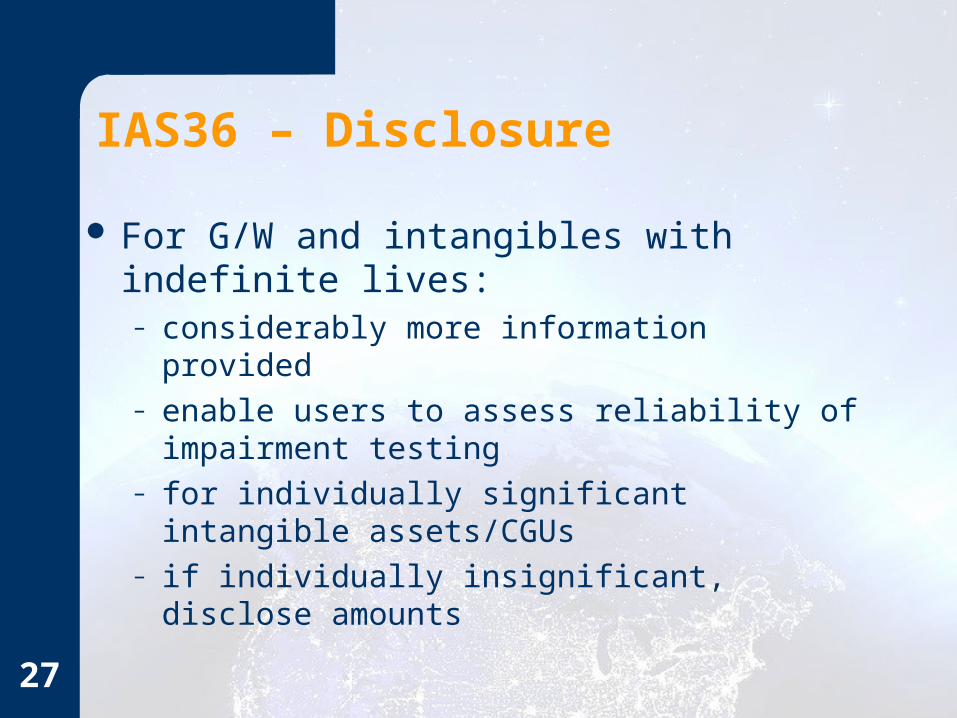

IAS36 – Disclosure

For G/W and intangibles with indefinite lives:– considerably more information provided– enable users to assess reliability of impairment

testing– for individually significant intangible assets/CGUs – if individually insignificant, disclose amounts

27

Current GAAP Comparisons

– Pages 19 to 20 of 49 of http://www.ey.com/Global/assets.nsf/International/IFRS_US_GAAP_vs_IFRS/$file/US_GAAP_vs_IFRS.pdf

– Pages 82 to 84 of 164 of http://www.kpmg.co.uk/pubs/IFRScomparedtoU.S.GAAPAnOverview(2008).pdf

28

IFRS Financial Statement Disclosures

Cadbury Schweppes plc– http://www.cadbury.com/Reports/2007AnnualRep

ort.pdf

Impairment policy note for goodwill and acquisition intangibles– Page 93 of 153

Goodwill Note 14– Page 104 of 153

29

Looking Ahead

IAS 36 – two recent revisions – resulting from project on business combinations – changes to IAS 27 and IFRS 3 – released in 2008– related to impairment test for goodwill

Impairment – part of longer term convergence– no short or medium term changes likely

30

End-of-Chapter Practice 16-1 Three years ago, Ace Airlines (AA) was granted

permission to schedule flights on the popular and profitable Newalta to Oldsford route, provided it also serviced Remoteville which is considerably further north than Oldsford. As a result, AA set up a facility in Oldsford and a small office and maintenance bay in Remoteville. Remoteville is sparsely populated and not accessible except by air. AA’s controller now wants to review the Remoteville assets for impairment due to the continuing losses on the Oldsford-Remoteville route, but is not familiar with IAS 36.

Instructions

Write a short memo to AA’s controller, identifying how he should proceed in determining whether the Remoteville assets are impaired.31

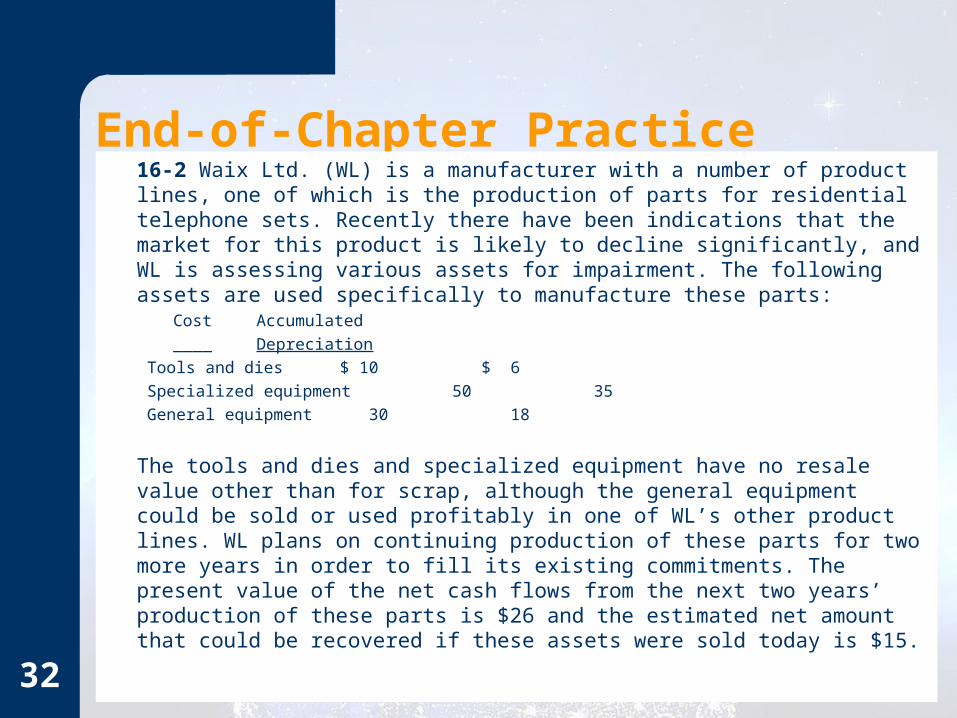

End-of-Chapter Practice16-2 Waix Ltd. (WL) is a manufacturer with a number of product lines, one of which is the production of parts for residential telephone sets. Recently there have been indications that the market for this product is likely to decline significantly, and WL is assessing various assets for impairment. The following assets are used specifically to manufacture these parts:

Cost Accumulated

____ Depreciation

Tools and dies $ 10 $ 6

Specialized equipment 50 35

General equipment 30 18

The tools and dies and specialized equipment have no resale value other than for scrap, although the general equipment could be sold or used profitably in one of WL’s other product lines. WL plans on continuing production of these parts for two more years in order to fill its existing commitments. The present value of the net cash flows from the next two years’ production of these parts is $26 and the estimated net amount that could be recovered if these assets were sold today is $15.

32

End-of-Chapter Practice

16-2 Instructionsa) Briefly discuss whether these assets should be assessed for

impairment individually or as part of a cash-generating unit.

b) Assuming the assets are allocated to a CGU made up of the three types of assets identified, determine whether an impairment loss needs to be recognized, and if so, in what total amount.

c) Prepare the entry needed to record any impairment loss indicated, assuming these assets are reported in separate asset classes.

33

End-of-Chapter Practice16-3 Firstall Corp. (FC) acquired four divisions of a competitor eight years ago in a business combination transaction, paying $25 more than the fair value of the identifiable assets acquired. The goodwill was determined to be 100% attributable to the operations of the East Division and the South Division. Although these two divisions are cash-generating units in their own right, there was no basis on which to allocate the goodwill between them. FC has identified the combined divisions as one CGU for assessing goodwill impairment on an annual basis. At the end of the most recent year, the following information is available:

Carrying Amount

East Division $ 75

South Division 125

Goodwill 25

FC has determined that the estimated recoverable value of the two divisions together is $215.

34

End-of-Chapter Practice

16-3 Instructionsa) Identify the asset, cash-generating unit, or group

of CGUs that FC should use to test for impairment.

b) Is there an impairment loss at the end of the current year? Explain how you determined your answer.

c) If applicable, indicate how any impairment loss should be accounted for. Be specific.

35

End-of-Chapter Practice

16-4 In this chapter, flag icons identify areas where there are GAAP differences between IFRS requirements and national standards.

Instructions

Access the website(s) identified on the inside back cover of this book, and prepare a concise summary of what the differences are that are flagged throughout the chapter material.

36

Copyright © 2010 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted

by Access Copyright is unlawful. Requests for further information should be addressed to the Permissions

Department, John Wiley & Sons Inc., 111 River Street, Hoboken, NJ 07030-5774, (201) 748-6011, fax (201) 748-6008, website

http://www.wiley.com/go/permissions. The purchaser may make back-up copies for his or her own use only and not for

distribution or resale. The author and the publisher assume no responsibility for errors, omissions, or damages caused by the

use of these programs or from the use of the information contained herein.

Related Documents