Impact of Repo Rate on Bank‘s lending 2013-14 2014 Sudheer Parashar 5/5/2014

Impact of Repo Rate on Bank Lending-2014

Jul 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Impact of Repo Rate on

Bank‘s lending 2013-14

2014

Sudheer Parashar

5/5/2014

Amity Business School Page 1

DISSERTATION REPORT ON

“IMPACT OF REPO RATE ON BANK LENDINGS”

FOR THE PARTIAL FULFILLMENT OF THE REQUIREMENT

FOR THE AWARD OF

MASTERS IN BUSINESS ADMINISTRATION

OF AMITY UNIVERSITY

SUBMITTED BY:

SUDHEER PARASHAR

(MBA-3rd

SEM.)

UNDER THE GUIDANCE OF:

Dr. NUPUR AGARWAL

AMITY UNIVERSITY, RAJASTHAN

Amity Business School Page 2

DECLARATION

I, hereby, declare that this research report entitled ―Analysis of Impact of

Repo Rate on Bank Lending‖ submitted in partial fulfillment for the

award of Master of Business Administration in Amity University,

Rajasthan is a record of independent work carried out by me under the

guidance of Dr. NUPUR AGRAWAL (Faculty member), AMITY

BUSINESS SCHOOL, AUR.

I, also declare that this report is a result of my own effort and has not

been submitted earlier for the award of any degree or diploma of

AMITY UNIVERSITY and other Universities.

Place: Jaipur Name: Sudheer Parashar

Date: - MBA 4th

Semester

Amity Business School Page 3

Abstract

Changes in Repo rate affect the cost of borrowing of Banks, which

shows that RBI plays a very important role in supply of money in the

market.

This paper examines the recently impact of raise the repo rate on

banking lending from the period of September-till now, it also explain

what is the scenario of lending behavior towards personal loan and

corporate loan.

I have done recent theoretical and empirical work that relates to the

―lending‖ channel of monetary policy transmission and Monetary Policy

and Long-Term Real Rates, Investigate the efficiency level of repo rate

among the all monetary tools.

This study aims to find out at what level the impact repo rate on deposit

and loan, what should be investment strategy of general public towards

change in it.

Inflation beyond the threshold level makes growth costly and calls for

policy change. As a result of increasing rate for control inflation, the

cost of borrowing has been higher.

Amity Business School Page 4

Table of Content

1 Introduction 1.1 Background of Study 7

1.2 Impact of Repo Rate 8-10

2 Lending View 2.1 Concept of Lending 12

2.2 Sources of Fund 12-14

2.3 Use of Fund 15-16

2.4 Lending Segment of Banks 19-23

2.5 Key Driver in Lending Rate 23-27

2.6 Indian Prime Lending Rate 28

3 Repo Policy 3.1 Monetary Policy 30

3.1.1 Monetary Instrument 32

3.2 Inflation vs. Interest rate 33

4 Literature Review

5 Research Methodology

5.1 Research Methodology 44

5.2 Problems of Study 44

5.3 Objective of Study 45

5.4 Importance of Study 45

5.5 Hypothesis of Study 45

5.6 Sample of Study 46

5.7 Sample 46

5.8 Size of Data 46

5.9 Limitation 47

Amity Business School Page 5

6 Analysis

& Interpretation

47-52

7 Banking Sector 53-65

8 Conclusion 66-67

9 Reference 68-69

Amity Business School Page 6

1 Introduction

Amity Business School Page 7

Introduction

1.1 Background of Study

The inflation is continuously increasing which are the bad for Indian economy.

Goal of Indian government is growth that is likely to lose the quantum in Q3 of

2013-14, with industrial activity in contractionary mode, mainly on account of

manufacturing.

The current account deficit for 2013-14 i s now expected to be below 2.5

percent of GD P as compared with 4.8 per cent i n 2012-13. Reserves have been

rebuilt since September, and are expected to increase.

And oil companies are buying foreign exchange for paying to RBI.

Retail inflation, as measured by the consumer price index, eased to a two-year low

of 8.10% in February from 8.79% in January, having touched a high of 11.24% in

November. Inflation based on the wholesale price index fell to a nine-month low of

4.68% in February on the back of a drop in food and fuel prices, having been at

5.05% in January. But data from Barclay‘s shows inflationary expectation is

running at 12%, the highest in recent memory.

The hailstorm is likely to result in an estimated crop failure of about Rs 12,000

crore (0.1% of the full year GDP) and this could reverse the recent downtrend in

retail price inflation

Monetary authorities may also wait for signals from the new government that will

present a full budget once it takes office in May. How quickly rate cuts may begin

will also depend a lot on how efficient the new government will be in managing its

finances.

Although the continued tapering of bond purchases by the Federal Reserve is

having little impact on India, international factors such as Ukraine, or a shakeup in

the US markets could adversely affect the outlook on rates.

Amity Business School Page 8

1.2 Impact of Repo Rate

We all Indian read and watch in newspapers, magazine and TV about the Reserve

Bank of India changing Repo Rate and other monetary instrument. Debt markets

affected by the change in ”Repo Rate and Reverse Repo Rate”. Banks decide their

lending rates on the basis of change in Repo Rate, Reverse Repo Rate and other

monetary instrument. RBI hikes repo rate by 25 bps to 8% in January`2014 credit

policy.

This is the third time that Governor of RBI, Rajan has raised rates after taking over

as governor in September 2013 last year an increase of 75 basis points from 7.25%

to 8% in four months. The move is unlikely to have an impact on rates charged by

banks

In a surprise move, the Reserve Bank of India release its third quarter monetary

policy increased the short term lending rate or repo rate to 8 per cent from the

existing 7.75 per cent. This move see as a surprise to most financial experts as it

was announced despite the lower inflation rates released in December. While RBI

justified the revision saying it is an essential option to bring down retail inflation,

in point view of business leaders, this move is disappointing.

Let us take a look at how RBI‘s repo rate policy impacts loans, fixed deposits and

other areas of life for the common man.

Before getting into the reasons why the increase in repo rates may be bad news for

the common man with increased loan EMIs, it is essential to understand what repo

rates are and how they impact the banking system. In a layman‘s term, Repo rate is

the rate at which the Reserve Bank of India lends money to commercial banks. The

increase in repo rates for 7.75% to 8% would mean that the RBI would charge a

higher rate of interest for all money given out to various commercial banks. The

bank in turn would be forced to charge its customers a higher rate of interest when

it comes to home and auto loans to offset the higher interest rate.

Amity Business School Page 9

1.2.3 Impact on Deposit and Lending Rates:

Most financial experts are of the opinion that the immediate impact of the increase

in repo rates may not necessarily get translated into higher deposit and lending

rates offered by the banks. The banks already fighting a weak loan growth rate due

to a sluggish real estate sector are unlikely to pass on the increased rates to the

customers immediately. Depending on the liquidity condition of the banks, the

changed interest and deposit rates may be passed on once banks analyze their cost

of funds over the next few days.

1.2.3 Increase EMIs:

Once the banks analyze their cost of funds and their overall liquidity condition, the

higher interest rates would have to be passed on to the end user or the retail

customer. This would effectively mean higher EMIIs on home loans, auto loans as

well as personal loans.

The home loan segment is likely to face the brunt of this increase in repo rate.

Financial experts believe that since the car loan market is dominated by various

schemes, financers are likely to absorb the rate hike by increasing discount offers.

Majority of car loans are on fixed rate basis compared to home loans with majority

offered on floating rate basis. Any rate impact due to the repo rate increase would

not necessarily impact the auto loan market as much as it would impact the home

loan segment. Real estate companies and developers already facing the brunt of

sluggish sales are disappointed with this rate hike as it is likely to dampen interest

in the real estate segment.

Amity Business School Page 10

1.2.3 Impact on Loans:

The question as to whether banks would actually increase the lending rates amid

the hike in the repo rates remains an open one. Once done with analyzing their

costs of funds and bank liquidity conditions, the banks would have no option but to

increase their interest rates

For example, assuming the interest rate on a 20 year housing loan of Rs 75 Lakh is

increased from 11 to 11.25 %, it will translate into an increase of approximately Rs

1279 per month in the EMI

1.2.4 Impact on Fixed Deposits:

The short term impact of such a hike is does not augur well for investors parking

their money in fixed deposits. Being an election year, the banks may reduce retail

deposit rates only slightly for below one-year fixed deposits simply to keep their

margins intact. The long term policy of the RBI is now aimed at fighting retail

inflation. Once the inflation rates are substantially lowered, the prospect of

investing in fixed deposit over the long term offers lucrative gains. The immediate

impact on small fixed deposits may be a damper but banks are unlikely to lower

interest rates across the board as of now giving relief to a vast section of fixed

deposit account holders.

The unexpected hike in the benchmark lending rate came despite lower inflation

rates in December. India‘s wholesale inflation rate eased to a five-month low of

6.16% last month while retail inflation — a more realistic index as it captures

shop-end prices — grew at a three-month low rate of 9.87% compared to 11.16%

the previous month as fresh seasonal arrivals pushed down vegetable prices.

Amity Business School Page 11

2

Lending View

Amity Business School Page 12

2.1 Concept of Lending in India

Banks make generally commercial loans designed to meet the specific needs of a

borrower. They also make standardized loans as in the case of mortgage and credit

card loans which can be packaged into securitized loans and sold in pools in the

secondary markets. Banks which are uniquely qualified to make, monitor and

collect commercial loans as well as standardized loans however face competition

from insurance companies, Unit Trust and non-bank finance companies.

Borrower‘s especially large corporates also have choice to raise funds directly in

the primary market by issue of shares and debentures and public fixed deposits and

in the money market through issue of commercial paper. The competition from

other types of lenders and direct financing by prospective borrowers has reduced

the profitability of banks. To offset lower profits banks abroad have shifted some

of their loans to higher yielding and higher risk real estate loans and loans to

emerging countries. The crash in real estate values and large scale defaults on

LDCs debts in 1980s and 1990s has highlighted the tradeoff between risk and

return.

2.2 Source of Banking Fund

The money that a bank raises to lend is often called the capital. So, how does banks

raise capital is something that has to be understood in this background. Banks have

to raise money from sources in order to have it with them to be lent to customers,

from whom they charge a rate of interest that is higher than that at which they

borrow. This accounts for their profit. Since capital is one of the critical

components of a banking business, it is important to understand where all and how

to banks raise capital.

As mentioned before, banks basically make money by lending money at rates

higher than the cost of the money they lend. More specifically, banks collect

interest on loans and interest payments from the debt securities they own, and pay

interest on deposits, CDs, and short-term borrowings. The difference is known as

the "spread," or the net interest income, and when that net interest income is

divided by the bank's earning assets; it is known as the net interest margin.

Amity Business School Page 13

2.2.1 Deposits

The largest source by far of funds for banks is deposits; money that accounts

holders entrusts to the bank for safekeeping and use in future transactions, as well

as modest amounts of interest. Generally referred to as "core deposits," these are

typically the checking and savings accounts that so many people currently have.

In most cases, these deposits have very short terms. While people will typically

maintain accounts for years at a time with a particular bank, the customer reserves

the right to withdraw the full amount at any time. Customers have the option to

withdraw money upon demand and the balances are fully insured, up to $250,000,

therefore, banks do not have to pay much for this money. Many banks pay no

interest at all on checking account balances, or at least pay very little, and pay

interest rates for savings accounts that are well below U.S. Treasury bond rates.

2.2.2 Wholesale Deposits

If a bank cannot attract a sufficient level of core deposits, that bank can turn to

wholesale sources of funds. In many respects these wholesale funds are much like

interbank CDs. There is nothing necessarily wrong with wholesale funds, but

investors should consider what it says about a bank when it relies on this funding

source. While some banks de-emphasize the branch-based deposit-gathering

model, in favor of wholesale funding, heavy reliance on this source of capital can

be a warning that a bank is not as competitive as its peers.

Investors should also note that the higher cost of wholesale funding means that a

bank either has to settle for a narrower interest spread, and lower profits, or pursue

higher yields from its lending and investing, which usually means taking on greater

risk.

Amity Business School Page 14

2.2.3 Share Equity

While deposits are the primary source of loanable funds for almost every bank,

shareholder equity is an important part of a bank's capital. Several important

regulatory ratios are based upon the amount of shareholder capital a bank has and

shareholder capital is, in many cases, the only capital that a bank knows will not

disappear.

Common equity is straight forward. This is capital that the bank has raised by

selling shares to outside investors. While banks, especially larger banks, do often

pay dividends on their common shares, there is no requirement for them to do so.

Banks often issue preferred shares to raise capital. As this capital is expensive, and

generally issued only in times of trouble, or to facilitate an acquisition, banks will

often make these shares callable. This gives the bank the right to buy back the

shares at a time when the capital position is stronger, and the bank no longer needs.

Equity capital is expensive, therefore, banks generally only issue shares when they

need to raise funds for an acquisition, or when they need to repair their capital

position, typically after a period of elevated bad loans. Apart from the initial

capital raised to fund a new bank, banks do not typically issue equity in order to

fund loans.

2.2.4 Debt

Banks will also raise capital through debt issuance. Banks most often use debt to

smooth out the ups and downs in their funding needs, and will call upon sources

like repurchase agreements or Repo market, to access debt funding on a short term

basis.

There is frankly nothing particularly unusual about bank-issued debt, and like

regular corporations, bank bonds may be callable and/or convertible. Although

debt is relatively common on bank balance sheets, it is not a critical source of

Amity Business School Page 15

capital for most banks. Although debt/equity ratios are typically over 100% in the

banking sector, this is largely a function of the relatively low level of equity at

most banks. Seen differently, debt is usually a much smaller percentage of total

deposits or loans at most banks and is, accordingly, not a vital source of loanable

funds.

2.3 Use of Fund

2.3.1 Loans

For most banks, loans are the primary use of their funds and the principal way in

which they earn income. Loans are typically made for fixed terms, at fixed rates

and are typically secured with real property; often the property that the loan is

going to be used to purchase. While banks will make loans with variable or

adjustable interest rates and borrowers can often repay loans early, with little or no

penalty, banks generally shy away from these kinds of loans, as it can be difficult

Part and parcel of a bank's lending practices is its evaluation of the credit

worthiness of a potential borrower and the ability to charge different rates of

interest, based upon that evaluation. When considering a loan, banks will often

evaluate the income, assets and debt of the prospective borrower, as well as the

credit history of the borrower. The purpose of the loan is also a factor in the loan

underwriting decision; loans taken out to purchase real property, such as homes,

cars, inventory, etc., are generally considered less risky, as there is an underlying

asset of some value that the bank can reclaim in the event of nonpayment.

As such, banks play an under-appreciated role in the economy. To some extent,

bank loan officers decide which projects, and/or businesses, are worth pursuing

and are deserving of capital.

Amity Business School Page 16

2.3.2 Consumer Lending

Consumer lending grew at a higher rate in 2013 than in 2012 and in 2011. This was

despite negative economic sentiment in terms of low growth, high inflation and

high interest rates. The high growth was partly due to smart positioning of products

by banks, such as pushing credit cards, housing loans and auto loans to self-

employed individuals and partly it was because the impact of recession was less on

individuals compared to the corporate segment. Not only growth was higher in

2013, but bad assets were also on the lower side than in previous years.

Sentiment remained negative in Indian economy in 2013

The overall sentiment remained negative in the Indian economy through 2013. The

growth in gross domestic product was a fraction of its peak level in 2007. Inflation

continued to remain high in certain pockets, as the price of vegetables soared. The

Indian rupee depreciated significantly throughout the year. Reserve Bank of India

– the apex body – did not find conditions conducive to cutting key rates. In the

absence of rate cuts, banks were not in a position to cut lending rates, which was

considered important to boost credit growth. The only silver lining was that the

retail side of lending performed better than the corporate side, giving breathing

space to all financial institutions

Scheduled commercial banks continue to lead consumer lending in 2013

Banks such as State Bank of India, Punjab National Bank, ICICI Bank Ltd, HDFC

Bank Ltd, Bank of India, Bank of Baroda and Axis Bank Ltd continued to

dominate consumer lending in 2013. These entities fall under scheduled

commercial banks (SCBs). The reason that these entities dominated was their

decades-long experience in the Indian market, huge capital bases and wide branch

networks. Apart from banks, several non-banking financial companies (NBFCs)

were also a part of consumer lending. Such entities were smaller in scale than

banks because they could not raise money through savings and current deposits.

NBFCs had to raise money from money markets and, therefore, they operate on a

much smaller scale than banks. Apart from NBFCs, several microfinance

institutions (MFIs) also operated in this business. SCBs, NBFCs and MFIs

continued to attempt to reduce the share of informal money lenders in 2013.

Card lending witnesses fastest growth in 2013

Credit card outstanding balance witnessed the fastest growth in 2013. This was

because retail banking consumers continued to report significant growth in

disposable incomes. Based on this, banks felt assured of their creditworthiness and

Amity Business School Page 17

focused more on credit cards in 2012 and 2013. Banks realised that the slowdown

affected the corporate segment more than retail consumers. This was because a

very small fraction of Indians worked in the corporate sector. A large part of the

population continued to be self-employed in small businesses. Such consumers

continued to post growth in their income and bankers realised their continued

creditworthiness. Therefore banks targeted such individuals to grow their credit

card portfolios.

Consumer lending expected to post strong growth over the forecast period

Consumer lending is expected to see continued strong growth in outstanding

balance in constant value terms over the forecast period. This will be due to rising

disposable incomes, the growth of banks and other financial institutions and

increasing financial inclusion. More consumers will come under the ambit of

organised means of financing, rather than informal money lenders, who generally

charge exorbitant rates of interest.

Amity Business School Page 18

2.4 Impact of Repo on lending segment

Date Repo

Rate

Borrowings

from RBI

Balances

with

Reserve

Bank

Investments

in

Government

and other

approved

securities

Bank

credit

Food

credit

Non-

food

credit

1/10/2014 8% 414.28 3205.14 22255.25 57718.72 1137.08 56581.64

1/24/2014 8% 298.04 3233.33 22107.91 57757.35 1117.74 56639.61

2/7/2014 8% 406.39 3151.89 22308.84 58355.48 1107.09 57248.39

2/21/2014 8% 405.04 3120.05 22369.84 58458.33 1065.67 57392.66

3/7/2014 8% 311.04 3216.77 22374.97 59372.49 1000.30 58372.19

3/21/2014 8% 416.13 3163.44 22216.53 60130.85 984.77 59146.08

4/4/2014 8% 371.88 3265.98 22715.64 60868.81 896.13 59972.68

4/18/2014 8% 318.69 3266.24 22726.38 60360.83 926.90 59433.93

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0

10000

20000

30000

40000

50000

60000

70000

1 2 3 4 5 6 7 8

Impact on Lending Segment

Borrowings from RBI

Balances with Reserve Bank

Investments in Governmentand other approved securities

Bank credit

Food credit

Non-food credit

Repo Rate

Amity Business School Page 19

2.4.1 Types of Loans

Auto Loan

Most of the banks provide car loans. Car loan also termed as Auto Loan. One can

get car loan up to 85% of ex-showroom price of the car with some amount of

processing fee.

Education Loan

Education Loan is also termed as Student Loan.

Educational loan is offered to the students, who are having brilliant academic

records, studying at recognized colleges/universities in India or abroad.

Educational loan is generally offered to meet the expenses on tuition fees, books

and other educational related cost.

Home Loan

Hiking the key policy rate today will hit property sales, particularly in the

residential segment , real estate developers. Raised the key policy rat e by 0. 25

per cent to 8 percent in a bid to curb inflation, a move that may translate

into higher EMI s and push up the cost of borrowing f or the corporate,

There is already a slowdown in the property market and the overall

economy. So, there would not be much adverse impact on sales, make

corporate and retail loan more expensive. It may increase EMI burden on

common man

Personal Loan

Credit costs are lower in segments such as home loans, which are secured

loans, it may be possible to lower the rates in that segment Re- pricing in

loan rates might be seen i n segment s such as personal loans, which were

riskier than home loans

Amity Business School Page 20

The fact that most banks were consciously going slow on credit growth,

owing asset quality concerns, was another reason why arise in lending rates

was unlikely at this point

Impact of Repo on Bank’s Loan Segment

Date Repo Rate Personal Loans

Housing Loan

Vehicle Loans

Education Loans

2/21/2014 8 10,159.34 2,984.51 1,285.26 571.30

1/24/2014 8 10,091.32 2,974.58 1,274.37 570.48

12/27/2013 7.75 9,989.87 2,952.49 1,261.46 567.90

11/29/2013 7.75 9,843.87 2,945.91 1,240.36 564.74

10/18/2013 7.5 9,702.01 2,922.66 1,202.32 564.25

9/20/2013 7.5 9,652.79 2,909.59 1,185.79 558.04

8/23/2013 7.5 9,564.45 2,888.38 1,174.09 550.73

7/26/2013 7.25 9,423.13 2,873.54 1,167.62 544.76

6/28/2013 7.25 9,347.73 2,865.71 1,167.05 534.11

5/31/2013 7.25 9,272.94 2,833.56 1,167.02 530.97

4/19/2013 7.5 9,124.53 2,791.81 1,141.62 546.31

3/22/2013 7.5 8,975.84 2,672.03 1,110.89 526.12

2/22/2013 7.75 8,719.95 2,633.97 1,082.42 525.86

1/25/2013 7.75 8,658.81 2,623.32 1,063.21 523.46

6.8

7

7.2

7.4

7.6

7.8

8

8.2

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

1/1

/20

13

2/1

/20

13

3/1

/20

13

4/1

/20

13

5/1

/20

13

6/1

/20

13

7/1

/20

13

8/1

/20

13

9/1

/20

13

10

/1/2

01

3

11

/1/2

01

3

12

/1/2

01

3

1/1

/20

14

2/1

/20

14

Axi

s Ti

tle

Impact on Repo Rate

Personal Loans

Housing Loan

Vehicle Loans

Education Loans

Repo Rate

Amity Business School Page 21

2.4.2 Deposit Rates

In 2013-14 for many quarters, deposit rates have not changed. The reason is

deposit rates are linked to the rate of inflation. You should give positive returns to

your depositors. You should watch the trends in inflation and deposits, which

impact the cost of funds and lending rates.

While there is a need to retain deposit rates at these levels due to the high

inflation, banks also need to see if the increase can be passed on to borrowers. But

credit demand has not started picking up. So, if banks raise deposit rates, the cost

will have to be absorbed. Each bank‘s asset liability management committee will

meet and take a decision on whether to raise rates or not.

Though returns to depositors were negative because of the high inflation, banks

were unlikely to raise deposit rates, as that would impact their margins.

Reasons:

banks are comfortable on the liquidity front most have already made

provisions to address asset quality issues

There is no immediate requirement for funds it is unlikely they will

raise deposit rates immediately

Types of Deposit

1. Demand Deposits

Savings account deposits

Current account deposits

2. Term Deposits

3. Hybrid Deposits / Flexi Deposits

4. Non-Resident Accounts

Foreign Currency Non-Resident Account (FCNR)

Non-Resident External Rupee Account (NRE)

Non-Resident Ordinary Account (NRO)

Amity Business School Page 22

Impact of Repo rate on Demand deposit and Time deposit

Date Repo Rate Demand deposits Time deposits

4/18/2014 8% 7265.94 71433.72

4/4/2014 8% 7677.41 71633.63

3/21/2014 8% 7208 70185.85

3/7/2014 8% 7031.62 69891.5

2/21/2014 8% 6878.38 68887.71

2/7/2014 8% 6792.05 68921.38

1/24/2014 8% 6892.04 68353.06

1/10/2014 8% 6662.5 68565.79

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0

10000

20000

30000

40000

50000

60000

70000

80000

1 2 3 4 5 6 7 8

Axi

s Ti

tle

Demand and Time Deposits

Demand deposits

Time deposits

Repo Rate

Amity Business School Page 23

2.4.3 Loan Rate and Deposit Rate

The repo rate cut is unlikely to have any impact on the lending and deposit rates

immediately, say bankers as well as analysts. Says Clyton Fernandes, analyst,

Anand Rathi Financial Services Ltd, ―Banks are not expected to pass on the repo

rate cut benefit immediately as liquidity is still tight.

RBI will have to first improve liquidity in the markets and only then will the

benefits be passed to the consumers. Banks were earlier borrowing Rs.1 trillion,

now it has come down to Rs.85, 000 crore. Borrowing is expected to turn positive

in the open market. If this happens, banks will lower the lending rate. However,

this will take at least six months.‖

Agrees Abhishek Kothari, research analyst, Violet Arch Securities Pvt. Ltd, ―There

are two reasons for no immediate impact: tight liquidity and higher cost of funding

for banks. Only when cost of funding comes down banks will be able to reduce

rates.‖

Inflation has a major impact on deposit rates. With inflation at high levels, the real

rate of return will be close to negative. Hence, deposit rates will be subdued. Says

Fernandes, ―We expect inflation to be at 5% by March 2015. As long as inflation is

high, deposit rates will remain where they are. In case of a rate cut, first lending

rates will fall and then deposit rates will come down.‖

Amity Business School Page 24

So what about loan customers? Says Surya Bhatia, managing partner, Asset

Managers, ―Lending and deposit rates will not come down immediately. But

whenever it happens there will not be a big drop in deposit rates. In case of fall in

lending rates, floating rate consumers will benefit while those on fixed rate will

miss out.‖ Planners also advise caution. Says Suresh Sadagopan, ―Lock-in your

fixed deposits at current level even though rate will not come down immediately.

Overall we know that rates are falling and hence, after a period of time deposit

rates may fall.‖

Overall, the credit policy was largely a non-event. While markets would once

again look out for government action and global cues, if you were looking for

lowering your loan instalments, you would be disappointed as there is no change

expected in loan or deposit rates

Amity Business School Page 25

2.5 Key Driver of Fluctuation in Lending Rates

The rate of interest in general is the price we pay for borrowing money. It is the

price that the lender charges for taking the risk and investing in the money market.

If you borrow/ take a loan from the bank for personal requirements like buying a

house or car or starting a business, you will have to pay interest to the bank on

your loan. If you deposit money in a bank in the form savings or fixed or recurring

deposits, the bank pays you interest for the use of your money.

Banks use a formula to calculate the interest amount you will have to pay .

The standard formula for computing simple interest is - Principal x Rate of

interest x Time. If you borrow Rs. 10000 at an annual interest rate of 6% for a

period of 1 year, the interest amount you pay will be Rs. 600.

10000 (Principal balance) x 0.005

(Monthly interest rate) x 12 (no. of months)

The monthly interest rate is calculated as follows the decimal equivalent of 6%

is 0.06

0.06 is divided by 12 equal s which is 0.005.

So the total amount you pay back to the bank at the end of the y ear would be Rs.

10600 (principal + interest).

This is simple interest when the principal is paid all together at the end of the loan

period. The interest rate and the amount of total interest paid are usually higher

when the loan is paid in installments, in the form of EMI.

Amortization The gradual reduction of the loan balance through regular interest and principal

payments is Called ‗amortization‘.

The bank uses an amortization calculator to determine the amount of monthly

payment, so that each payment is the same amount.

Amity Business School Page 26

Interest on saving account and other deposits in bank

Compound interest is paid on our deposits with the bank. Interest on such

deposits is calculated using the same formula (as of simple interest), but it

is done according to a ―compounding‖ schedule, which can be daily , monthly ,

quarterly or annual l y . Compounding refers to the frequency with which the

bank calculates the interest on the deposits. The interest is then added to the

balance. A simple example- if you deposit Rs. 1000 with the bank at 10 %

interest rate maturing after 3 y ears , after one year i t becomes Rs . 1100.

Another Rs. 100

As interest will be added in the second year, and yet another in the third year. So

the amount you will receive on maturity will be a bigger amount- Rs. 1300.

2.5.1 Factors affecting Interest rate

Interest rate depends on the activities and fluctuations in the money market. It

depends on the demand and supply of money in the economy at a given time.

The three main economic factors that affect interest rates.

Policies of the Central bank- The apex bank or the central bank of the

country (RBI in India) is responsible for monetary stability in the country .

To achieve this objective an important function of the Central bank is credit

control. The apex bank controls the money supply in the economy through

measures like changing the Cash Reserve Ratio and the Repo Rate and Reverse

repo Rate.

The repo rate in common terms , is the interest rate at which the commercial

banks borrow from the RBI . When there is inflation and the central bank

wants to curb money supply and credit creation in the economy to check

inflation, it will raise the interest rate and CRR, thus making borrowing

costly . The commercial banks in turn pass on this increased rate to it ‘ s

customers . The reverse happens during recess i on. To boost the economy,

interest rate is lowered by the Central bank, thus making credit cheaper for

investment.

Amity Business School Page 27

Recession- During recession economic activities slow down. Expectation of

fall in profit margins discourages investment, reducing the demand for credit.

This results in fall in interest rate.

Inflation- Inflationary pressures tend to raise the market interest rates. This is

because, when prices are expected to rise considerably , the lender will be

reluctant to lend during that period, fearing a loss of purchasing power of

the loaned amount , on maturity . To compensate this loss, a higher interest rate

is charged.

State of the economy- When the economy is growing, the demand is also

growing with increased expectation of profit in the future. Hence there is more

deem and for credit for investment purpose, which raises the interest rate. The

opposite happens during recession.

Amity Business School Page 28

2.6 INDIA PRIME LENDING RATE

Bank Lending Rate in India remained unchanged at 10.25 percent in April of 2014

from 10.25 percent in March of 2014. Bank Lending Rate in India is reported by

the Reserve Bank of India. Bank Lending Rate in India averaged 14.08 Percent

from 1978 until 2014, reaching an all-time high of 20 Percent in October of 1991

and a record low of 8 Percent in July of 2010. In India, the prime lending rate is the

average rate of interest charged on loans by commercial banks to private

individuals and companies. This page provides - India

Prime Lending Rate - actual values, historical data, forecast, chart, statistics, economic calendar and news. 2014-04-26

ACTUAL PREVIOUS HIGHEST LOWEST FORECAST DATES UNIT FREQUENCY

10.25 10.25 20.00 8.00 10.15 | 2014/05 1978 - 2014 PERCENT MONTHLY

Amity Business School Page 29

3

Repo

Policy

Amity Business School Page 30

3.1 What is monetary policy?

The instruments of monetary policy used by the Central Bank depend on the level

of development of the economy, especially its financial sector.

Reserve Requirement: The Central Bank may require Deposit Money Banks

to hold a fraction (or a combination) of their deposit liabilities (reserves) as vault

cash and or deposits with it. Fractional reserve limits the amount of loans banks

can make to the domestic economy and thus limit the supply of money. The

assumption is that Deposit Money Banks generally maintain a stable relationship

between their reserve holdings and the amount of credit they extend to the public.

Open Market Operations: The Central Bank buys or sells ((on behalf of the

Fiscal Authorities (the Treasury)) securities to the banking and non-banking public

(that is in the open market). One such security is Treasury Bills. When the Central

Bank sells securities, it reduces the supply of reserves and when it buys (back)

securities-by redeeming them-it increases the supply of reserves to the Deposit

Money Banks, thus affecting the supply of money.

Lending by the Central Bank: The Central Bank sometimes provide credit to

Deposit Money Banks, thus affecting the level of reserves and hence the monetary

base.

Interest Rate: The Central Bank lends to financially sound Deposit Money

Banks at a most favorable rate of interest, called the minimum rediscount rate

(MRR). The MRR sets the floor for the interest rate regime in the money market

(the nominal anchor rate) and thereby affects the supply of credit, the supply of

savings (which affects the supply of reserves and monetary aggregate) and the

supply of investment (which affects full employment and GDP).

Direct Credit Control: The Central Bank can direct Deposit Money Banks on

the maximum percentage or amount of loans (credit ceilings) to different economic

sectors or activities, interest rate caps, liquid asset ratio and issue credit guarantee

Amity Business School Page 31

to preferred loans. In this way the available savings is allocated and investment

directed in particular directions.

Moral Suasion: The Central Bank issues licenses or operating permit to Deposit

Money Banks and also regulates the operation of the banking system. It can, from

this advantage, persuade banks to follow certain paths such as credit restraint or

expansion, increased savings mobilization and promotion of exports through

financial support, which otherwise they may not do, on the basis of their risk/return

assessment.

Prudential Guidelines: The Central Bank may in writing require the Deposit

Money Banks to exercise particular care in their operations in order that specified

outcomes are realized. Key elements of prudential guidelines remove some

discretion from bank management and replace it with rules in decision making.

Exchange Rate: The balance of payments can be in deficit or in surplus and

each of these affect the monetary base, and hence the money supply in one

direction or the other. By selling or buying foreign exchange, the Central Bank

ensures that the exchange rate is at levels that do not affect domestic money supply

in undesired direction, through the balance of payments and the real 3exchange

rate. The real exchange rate when misaligned affects the current account balance

because of its impact on external competitiveness. Moral suasion and prudential

guidelines are direct supervision or qualitative instruments. The others are

quantitative instruments because they have numerical benchmarks

Amity Business School Page 32

3.1.1Instruments of monetary policy The RBI has numerous instruments of monetary policy at its disposal in order to

regulate the availability, cost and use of money and credit. Using these monetary

policy instruments, the RBI must walk a tightrope between trying to stimulate

growth while keeping inflation under control

Direct regulation:

Cash Reserve Ratio (CRR): Commercial Banks are required to hold a certain

proportion of their deposits in the form of cash with RBI. CRR is the minimum

amount of cash that commercial banks have to keep with the RBI at any given

point in time. RBI uses CRR either to drain excess liquidity from the economy or

to release additional funds needed for the growth of the economy.

For example, if the RBI reduces the CRR from 5% to 4%, it means that

commercial banks will now have to keep a lesser proportion of their total deposits

with the RBI making more money available for business. Similarly, if RBI decides

to increase the CRR, the amount available with the banks goes down.

Statutory Liquidity Ratio (SLR): SLR is the amount that commercial banks are

required to maintain in the form of gold or government approved securities before

providing credit to the customers. SLR is stated in terms of a percentage of total

deposits available with a commercial bank and is determined and maintained by

the RBI in order to control the expansion of bank credit. For example, currently,

commercial banks have to keep gold or government approved securities of a value

equal to 23% of their total deposits.

Indirect regulation:

Repo Rate: The rate at which the RBI is willing to lend to commercial banks is

called Repo Rate. Whenever commercial banks have any shortage of funds they

can borrow from the RBI, against securities. If the RBI increases the Repo Rate, it

makes borrowing expensive for commercial banks and vice versa. As a tool to

control inflation, RBI increases the Repo Rate, making it more expensive for the

banks to borrow from the RBI with a view to restrict the availability of money. The

Amity Business School Page 33

RBI will do the exact opposite in a deflationary environment when it wants to

encourage growth.

Reverse Repo Rate: The rate at which the RBI is willing to borrow from the

commercial banks is called reverse repo rate. If the RBI increases the reverse repo

rate, it means that the RBI is willing to offer lucrative interest rate to commercial

banks to park their money with the RBI. This results in a reduction in the amount

of money available for the bank‘s customers as banks prefer to park their money

with the RBI as it involves higher safety. This naturally leads to a higher rate of

interest which the banks will demand from their customers for lending money to

them.

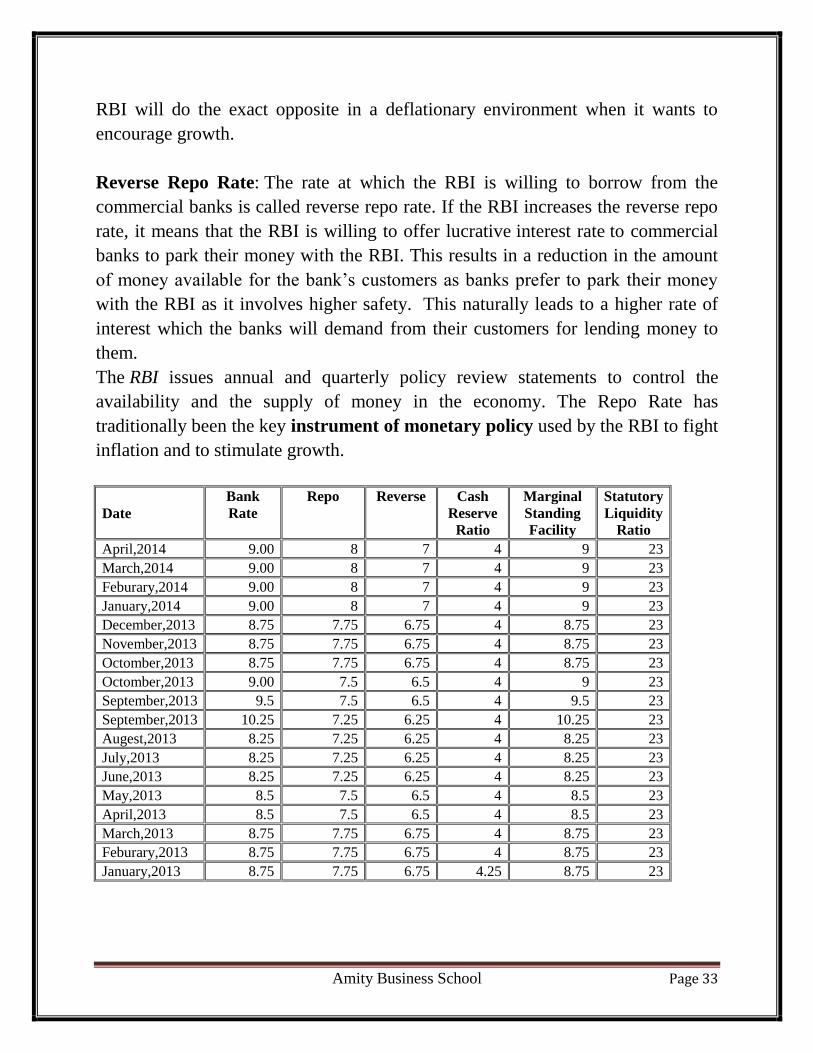

The RBI issues annual and quarterly policy review statements to control the

availability and the supply of money in the economy. The Repo Rate has

traditionally been the key instrument of monetary policy used by the RBI to fight

inflation and to stimulate growth.

Date

Bank

Rate

Repo Reverse Cash

Reserve

Ratio

Marginal

Standing

Facility

Statutory

Liquidity

Ratio

April,2014 9.00 8 7 4 9 23

March,2014 9.00 8 7 4 9 23

Feburary,2014 9.00 8 7 4 9 23

January,2014 9.00 8 7 4 9 23

December,2013 8.75 7.75 6.75 4 8.75 23

November,2013 8.75 7.75 6.75 4 8.75 23

Octomber,2013 8.75 7.75 6.75 4 8.75 23

Octomber,2013 9.00 7.5 6.5 4 9 23

September,2013 9.5 7.5 6.5 4 9.5 23

September,2013 10.25 7.25 6.25 4 10.25 23

Augest,2013 8.25 7.25 6.25 4 8.25 23

July,2013 8.25 7.25 6.25 4 8.25 23

June,2013 8.25 7.25 6.25 4 8.25 23

May,2013 8.5 7.5 6.5 4 8.5 23

April,2013 8.5 7.5 6.5 4 8.5 23

March,2013 8.75 7.75 6.75 4 8.75 23

Feburary,2013 8.75 7.75 6.75 4 8.75 23

January,2013 8.75 7.75 6.75 4.25 8.75 23

Amity Business School Page 34

Repo Rate vs. Reserve repo Rate Repo or repurchase option is a means of short-term borrowing, wherein banks sell

approved government securities to RBI and get funds in exchange. In other words,

in a repo transaction, RBI repurchases government securities from banks,

depending on the level of money supply it decides to maintain in the country's

monetary system.

Repo rate is the discount rate at which banks borrow from RBI. Reduction in repo

rate will help banks to get money at a cheaper rate, while increase in repo rate will

make bank borrowings from RBI more expensive. If RBI wants to make it more

expensive for the banks to borrow money, it increases the repo rate. Similarly, if it

wants to make it cheaper for banks to borrow money, it reduces the repo rate.

Reverse repo is the exact opposite of repo. In a reverse repo transaction, banks

purchase government securities form RBI and lend money to the banking

regulator, thus earning interest. Reverse repo rate is the rate at which RBI borrows

money from banks. Banks are always happy to lend money to RBI since their

money is in safe hands with a good interest.

Thus, repo rate is always higher than the reverse repo rate.

0.00

5.00

10.00

15.00

20.00

25.00

Mar

ch,2

014

Feb

ura

ry,2

01

4

Jan

uar

y,2

01

4

Dec

emb

er,2

013

No

vem

ber

,20

13

Oct

om

ber

,201

3

Oct

om

ber

,201

3

Sep

tem

ber

,20

13

Sep

tem

ber

,20

13

Au

ges

t,2

01

3

July

,20

13

Jun

e,20

13

May

,20

13

Ap

ril,

20

13

Mar

ch,2

013

Feb

ura

ry,2

01

3

Jan

uar

y,2

01

3

Ra

te

Monetary Policy Rate

Bank Rate

Repo

Reverse

Cash Reserve Ratio

Marginal Standing Facility

Statutory Liquidity Ratio

Amity Business School Page 35

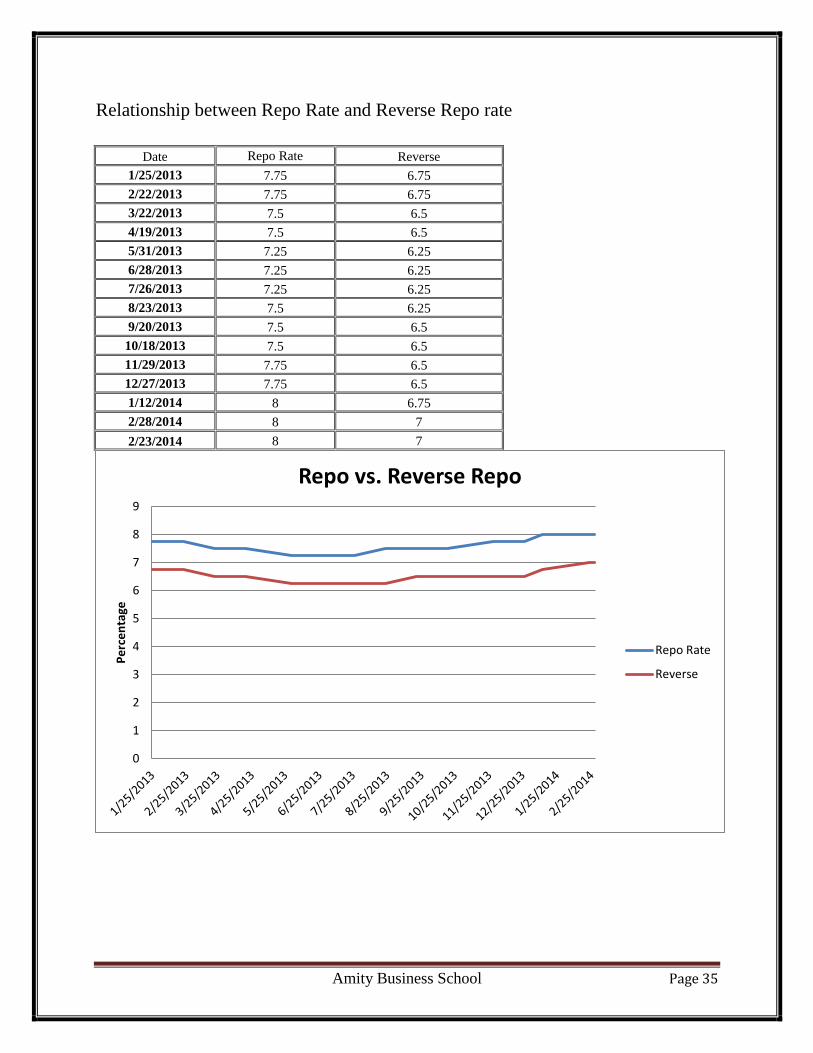

Relationship between Repo Rate and Reverse Repo rate

Date Repo Rate Reverse

1/25/2013 7.75 6.75

2/22/2013 7.75 6.75

3/22/2013 7.5 6.5

4/19/2013 7.5 6.5

5/31/2013 7.25 6.25

6/28/2013 7.25 6.25

7/26/2013 7.25 6.25

8/23/2013 7.5 6.25

9/20/2013 7.5 6.5

10/18/2013 7.5 6.5

11/29/2013 7.75 6.5

12/27/2013 7.75 6.5

1/12/2014 8 6.75

2/28/2014 8 7

2/23/2014 8 7

0

1

2

3

4

5

6

7

8

9

Pe

rce

nta

ge

Repo vs. Reverse Repo

Repo Rate

Reverse

Amity Business School Page 36

Repo rate vs. inflation

Inflation occurs due to excess of money in the market. So RBI uses repo rates and

reverse repo rates to control money in the market.

The rate at which RBI lends money to commercial banks is called Repo-rate.

When repo rates are increased, commercial banks have to return more money to

RBI thus banks lend less money from RBI as a result of which the money available

with banks is less to lend out in the market. Consequently, banks increase their

loan interest rate as they have less money to hand out in the market which

decreases amount of money in the market. Now, when people have less money

with them they spend less which decreases demand of products and as a result

prices go down.

However, when money in the market decreases, money available with industries

diminishes and as a result production decreases. The reduction in production leads

to soaring of prices of products which are in demand which can lead to further

inflation.

Therefore, high repo rates and low repo rates both are dangerous and RBI carefully

monitors and governs the repo rate to control the market.

Raghuram Rajan, the governor of RBI increased the interest rate of banks shortly

after he said that bank could loan 100% of their TIER-1 strength.

Policy repo rates for banks act as an instrument for controlling the short term

liquidity. Repo rates are defined as "The rate at which the RBI lends money to

commercial banks is called repo rate. It is an instrument of monetary policy.

Whenever banks have any shortage of funds they can borrow from the RBI."

Raghuram Rajan would have commented that bank could loan 100% of their

TIER-1 strength is a long term measure. Banks‘ lending 100% of the TIER-1

strength would be them being able to earn higher return and increase their Net

Interest Margins, Return on Equity and Return on Capital Employed.

So the comment and the policy change are inherently different because one is a

short-term measure and the other a long term. Now by changing the repo rates and

Amity Business School Page 37

the reverse repo rates, RBI indirectly affects the CALL MONEY Market rates,

these are market driven interbank short duration rates and mostly are in between

the Repo rate and the reverse repo rate.

No When RBI increases the Repo Rates and hence leading to an increase in the call

money market rates. The cost of short term funds for the banks increase and hence

in order to stay profitable they would be do the short term lending to the corporate

and individuals at a higher rate than before.

This makes the corporates and individuals to restrain excess spending and hence a

decrease in the demand. This cumulative decrease in demand leads to change in the

prices of goods as now supply is at the same level but the demand has decrease in

the short term. Hence a real decrease in prices leads to a reduction in inflation

Relationship between Inflation and Repo Rate

Period Inflation Repo Rate

May 2013 10.680 7.25

June 2013 11.058 7.25

July 2013 10.849 7.25

August 2013 10.748 7.25

September 2013 10.698 7.50

October 2013 11.060 7.50

November 2013 11.468 7.50

December 2013 9.132 7.50

January 2014 7.240 8.00

February 2014 6.726 8.00

Amity Business School Page 38

3.2 Relation between Inflation and Bank interest Rate

Now days, you might have heard lot of these terms and usage on inflation and the

bank interest rates. We are trying to make it simple for you to understand the

relation between inflation and bank interest rates in India.

Bank interest rate depends on many other factors, out of that the major one is

inflation. Whenever you see an increase on inflation, there will be an increase of

interest rate also

What is Inflation?

Inflation is defined as an increase in the price of bunch of Goods and services that

projects the Indian economy. An increase in inflation figures occurs when there is

an increase in the average level of prices in Goods and services. Inflation happens

when there are fewer Goods and more buyers; this will result in increase in the

price of Goods, since there is more demand and less supply of the goods

0.000

2.000

4.000

6.000

8.000

10.000

12.000

14.000

Ra

tio

Relationship between Inflation and Repo Rate

Inflation

Repo Rate

Amity Business School Page 39

Inflation causes increase of Interest

Inflation can be recognized as a combination of 4 factors:

The Supply of money goes up

The Supply of Goods goes down

Demand for money goes down

Demand for goods goes up

Our Indian government gets involved in it to control the inflation by adjusting the

level of money in our economic system. The most noticeable way to increase the

money flow in the system is to print more currency, and then the rupees will

become more relative to goods

Inflation and Global Liquidity

Factors like rates of import and export, the production cost of farms, value of

dollar, and price of oil (crude oil), market movements of other overseas markets

cause global liquidity. In India, we can also feel the effects of global liquidity. We

are not isolated from all these issues now. Due to the remarkable economic growth

of India over the recent years, increase in foreign currency inflow caused the

demand in multiples for many Merchandise and services in India. RBI (Reserve

Bank of India) needs to control this excess liquidity in our economic system. For

this, RBI increases the ―Repo rates‖ which makes ―Costly Credits‖ and thus

increases the CRR rate (Cash Reserve Ratio). This kind of measures by RBI can

only control the inflation to a certain extent only

Amity Business School Page 40

4

Review

Of

Literature

Amity Business School Page 41

Literature Review

In the development and developing countries, many studies have been conducted

to test the impact banking lending with respect to monetary policy announcements.

In India, only very few studies has been conducted. Some of the select studies

relevant to the present study are reviewed.

The study ―The Effect of Monetary Policy on Bank Lending and Aggregate Output

(2005)‖ explains Asymmetries from Nonlinearities in the Lending Channel is also

reflects asymmetric effects of monetary policy on output and the role of bank-

lending behavior. This investigate whether contractionary and expansionary

policies have asymmetric impacts on bank loans, and whether there are further

differences in the response of small banks and big banks to policy actions. We also

investigate the link between changes in bank lending and aggregate economic

activity. Our goal is to simultaneously capture the existence of the lending view of

the monetary transmission mechanism, the strong relationship between loan

growth and output growth, and the asymmetric effect of monetary policy on

output. This study uses a nonlinear vector autoregressive approach to carry out our

analysis. Results show that asymmetry in the response of bank lending to monetary

policy is not a substantially contributing factor in explaining the different

responses of output to contractionary and expansionary policy.

―Monetary Policy and Long-Term Real Rates (July, 2012)‖ it document that

changes in the stance of monetary policy have surprisingly strong effects on very

distant forward real interest rates. Concretely, we show that a 100 basis-point (bop)

increase in the 2-year nominal yield on a Federal Open Markets Committee

(FOMC) announcement day—which we use as a proxy for changes in expectations

regarding the path of the federal funds rate over the following several quarters—is

associated with a 42 bps increase in the 10-year forward overnight real rate,

extracted from the yield curve for Treasury Inflation Protected Securities (TIPS).

―The Bank Lending Channel of Monetary Policy and Its Effect on Mortgage

Lending (May, 2010)‖ explains the bank lending channel suggests that banks play

a special role in the transmission of monetary policy. In this theory, monetary

policy has an effect on banks‘ cost of funds in addition to the change in the risk-

Amity Business School Page 42

free rate, leading to an additional response in bank lending. The supply of

intermediated credit therefore has a unique response to monetary policy. To

analyze the bank lending channel, the study the response of banks to monetary

policy in the context of mortgage funds and mortgage lending. We focus on

lending in subprime communities, because it is a form of information-intensive

lending which affects banks‘ choices in funding sources and their response to

changes in funding costs. Our paper helps explain how mortgage loan supply

responds to monetary policy by addressing the role of banks in the transmission of

monetary policy.

Amity Business School Page 43

5

Research

Methodology

Amity Business School Page 44

1.1 Research Methodology

1.2 Statement of the problem

Repo rate and other monetary ratio are important measures which control the

liquidity in the market. Changes in repo rate have direct impact on bank‘s cost of

borrowing. Aam Aadmi are interested to know the interest rate of loan and

deposit in banking sector during the change in reverse repo rate and other

monetary rate announcement period.

In the recent years small and medium scale investors in property market may

not aware about loan rate movements in banking sector after the announcement

of repo rate this change at what level affect their EMI. Hence, the present study

is an attempt to test the impact of rising repo rate on bank‘s lending.

1.3 1.4Objectives of the study

The following are the objectives of the study.

1. To analyze the impact of repo rate on bank‘s interest rate after announcement

period.

2. To test the relationship between repo rate and Inflation

3. Analysis the relationship between Interest rate and Inflation

1.4 Need of the study

The study aims to help investors and general person to making investment by

providing adequate information about impact of change in repo rate which help to

take making strategy for their EMI and Investment portfolio.

Amity Business School Page 45

1.5 Hypothesis of the study

The following hypotheses are tested in this study.

1. H0: There is significant impact of Repo Rate on Banking Interest Rate

2. H1: There is no significant impact of Repo Rate on banking Interest rate

1.6 Sample Selection

The sample selection for this study included Repo rate and reserve repo rate and

inflation and base rate data available on RBI website for the period 2013 to 2014.

1.7 Size of Data

The study shows the impact of rising repo rate on bank‘s lending from 2013 to

2014.

1.8 Source and collection of the data

The study used mainly contains secondary data. Information relating to inflation

and base rate data. The announcements of reverse repo rate and cash reserve

ratio change were collected from website www.rbi.org. The other related

sources were obtained from Books, Journals and websites

1.9 Period of the study

The present study is an attempt to test the impact of repo rate on the interest

rate of Indian Bank during the period from May 2013 to March 2014.

1.10 Tools

To test the impact of repo rate on interest rate of Indian Banks, the

following tools were used for study

Correlation

Regression Analysis

Amity Business School Page 46

1.11 Limitations

1. The report consider only Secondary data

2. This considers only the effect of repo rate on banking lending but does not

consider effect of CRR, SLR and Market operation.

3. Time period is short

Amity Business School Page 47

5 Analysis

&

Interpretation

Amity Business School Page 48

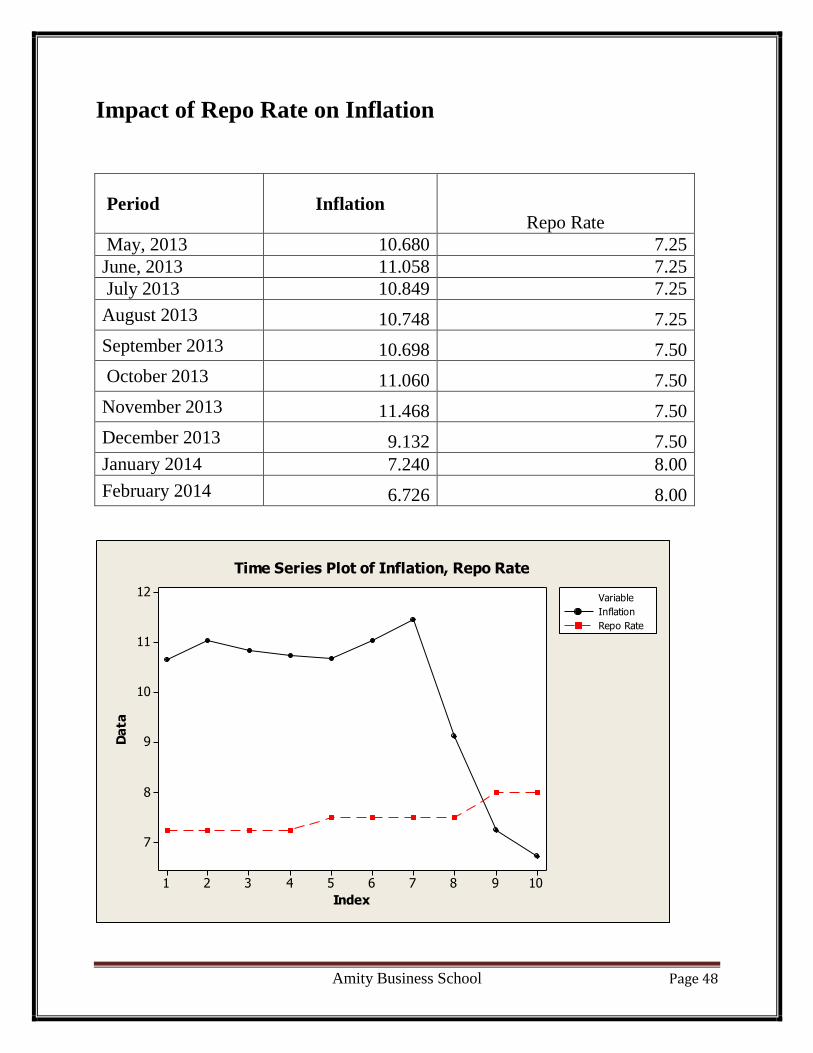

Impact of Repo Rate on Inflation

Period Inflation Repo Rate

May, 2013 10.680 7.25

June, 2013 11.058 7.25

July 2013 10.849 7.25

August 2013 10.748 7.25

September 2013 10.698 7.50

October 2013 11.060 7.50

November 2013 11.468 7.50

December 2013 9.132 7.50

January 2014 7.240 8.00

February 2014 6.726 8.00

10987654321

12

11

10

9

8

7

Index

Da

ta

Inflation

Repo Rate

Variable

Time Series Plot of Inflation, Repo Rate

Amity Business School Page 49

Data analysis

Correlation between Repo Rate and Inflation

Correlations: Inflation, Repo Rate Pearson correlation of Inflation and Repo Rate = -0.877

P-Value = 0.001

Fairly High degree of Correlation negative relationship

R (Pearson Correlation) = -0.877 indicates

There is negative correlation i.e. as the amount Repo increases the inflation

decreases.

There is meaningful correlation between Repo and inflation

Regression

S = 0.861346 -Sq = 76.9% R R-Sq(adj) = 74.0%

Repo Rate -5.1343 0.9946 -5.16 0.001

S = 0.861346 R-Sq = 76.9% R-Sq(adj) = 74.0%

Analysis of Variance

Source DF SS MS F P

Regression 1 19.771 19.771 26.65 0.001

Residual Error 8 5.935 0.742

Total 9 25.706

Amity Business School Page 50

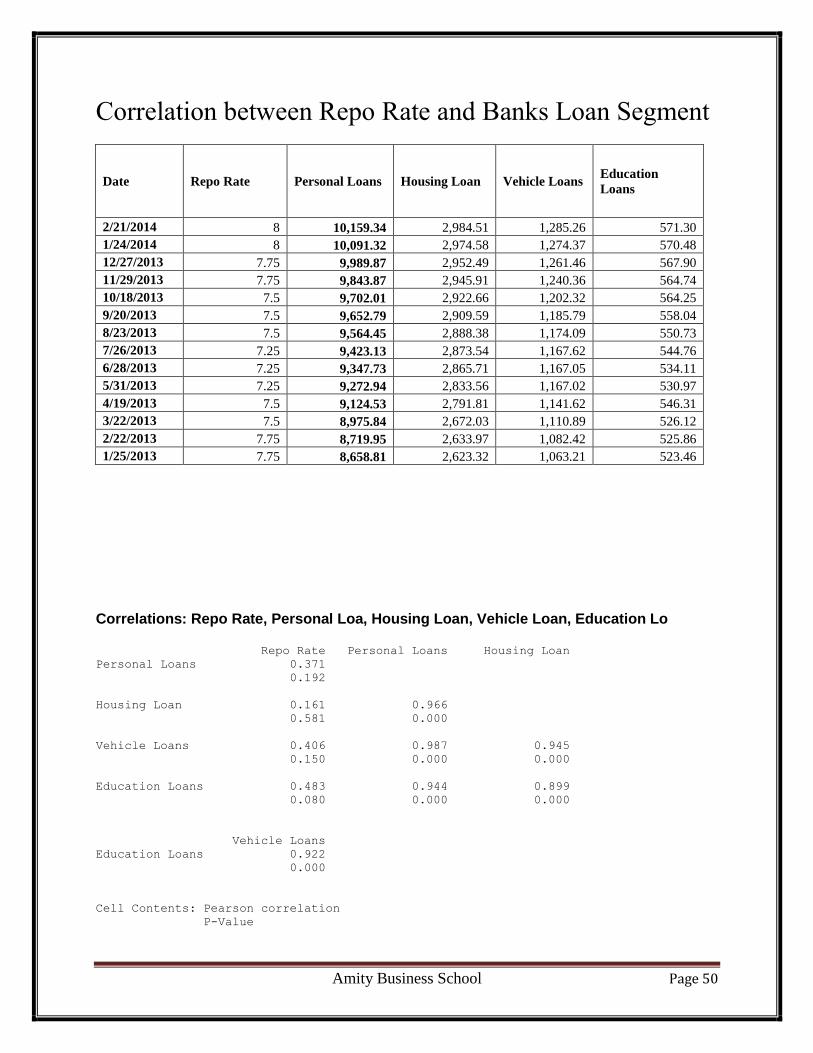

Correlation between Repo Rate and Banks Loan Segment

Date Repo Rate Personal Loans Housing Loan Vehicle Loans Education

Loans

2/21/2014 8 10,159.34 2,984.51 1,285.26 571.30

1/24/2014 8 10,091.32 2,974.58 1,274.37 570.48

12/27/2013 7.75 9,989.87 2,952.49 1,261.46 567.90

11/29/2013 7.75 9,843.87 2,945.91 1,240.36 564.74

10/18/2013 7.5 9,702.01 2,922.66 1,202.32 564.25

9/20/2013 7.5 9,652.79 2,909.59 1,185.79 558.04

8/23/2013 7.5 9,564.45 2,888.38 1,174.09 550.73

7/26/2013 7.25 9,423.13 2,873.54 1,167.62 544.76

6/28/2013 7.25 9,347.73 2,865.71 1,167.05 534.11

5/31/2013 7.25 9,272.94 2,833.56 1,167.02 530.97

4/19/2013 7.5 9,124.53 2,791.81 1,141.62 546.31

3/22/2013 7.5 8,975.84 2,672.03 1,110.89 526.12

2/22/2013 7.75 8,719.95 2,633.97 1,082.42 525.86

1/25/2013 7.75 8,658.81 2,623.32 1,063.21 523.46

Correlations: Repo Rate, Personal Loa, Housing Loan, Vehicle Loan, Education Lo Repo Rate Personal Loans Housing Loan

Personal Loans 0.371

0.192

Housing Loan 0.161 0.966

0.581 0.000

Vehicle Loans 0.406 0.987 0.945

0.150 0.000 0.000

Education Loans 0.483 0.944 0.899

0.080 0.000 0.000

Vehicle Loans

Education Loans 0.922

0.000

Cell Contents: Pearson correlation

P-Value

Amity Business School Page 51

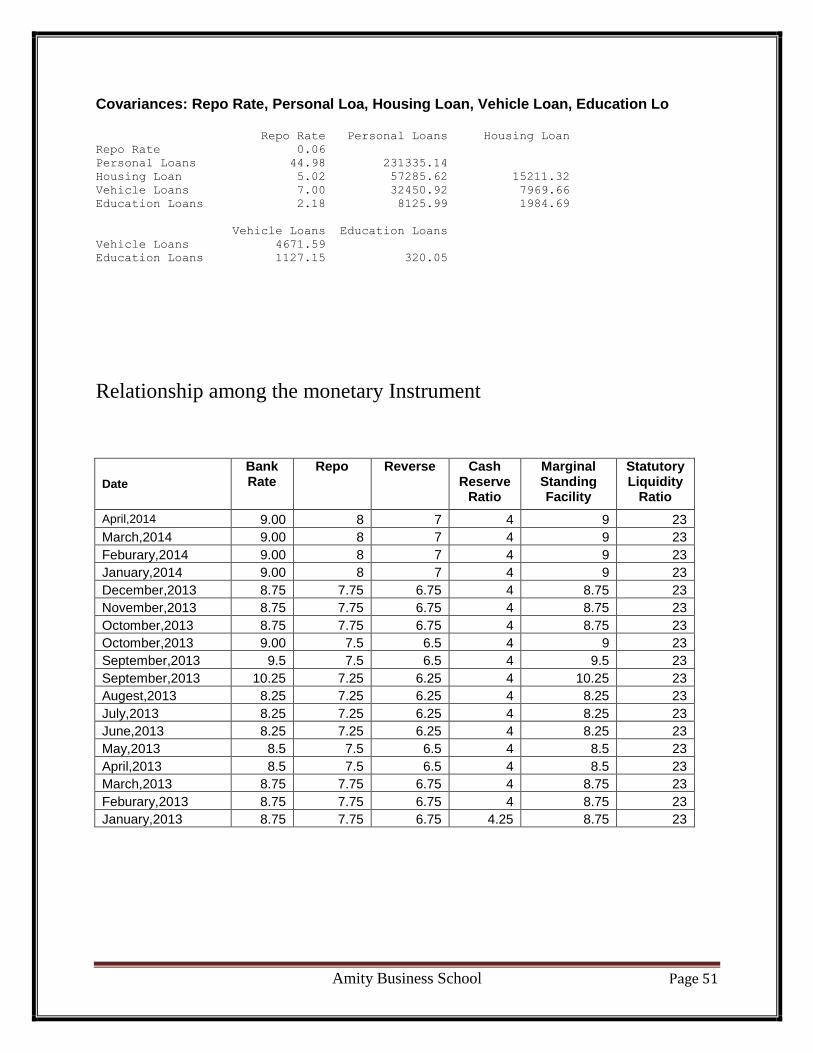

Covariances: Repo Rate, Personal Loa, Housing Loan, Vehicle Loan, Education Lo Repo Rate Personal Loans Housing Loan

Repo Rate 0.06

Personal Loans 44.98 231335.14

Housing Loan 5.02 57285.62 15211.32

Vehicle Loans 7.00 32450.92 7969.66

Education Loans 2.18 8125.99 1984.69

Vehicle Loans Education Loans

Vehicle Loans 4671.59

Education Loans 1127.15 320.05

Relationship among the monetary Instrument

Date

Bank Rate

Repo Reverse Cash Reserve

Ratio

Marginal Standing Facility

Statutory Liquidity

Ratio

April,2014 9.00 8 7 4 9 23

March,2014 9.00 8 7 4 9 23

Feburary,2014 9.00 8 7 4 9 23

January,2014 9.00 8 7 4 9 23

December,2013 8.75 7.75 6.75 4 8.75 23

November,2013 8.75 7.75 6.75 4 8.75 23

Octomber,2013 8.75 7.75 6.75 4 8.75 23

Octomber,2013 9.00 7.5 6.5 4 9 23

September,2013 9.5 7.5 6.5 4 9.5 23

September,2013 10.25 7.25 6.25 4 10.25 23

Augest,2013 8.25 7.25 6.25 4 8.25 23

July,2013 8.25 7.25 6.25 4 8.25 23

June,2013 8.25 7.25 6.25 4 8.25 23

May,2013 8.5 7.5 6.5 4 8.5 23

April,2013 8.5 7.5 6.5 4 8.5 23

March,2013 8.75 7.75 6.75 4 8.75 23

Feburary,2013 8.75 7.75 6.75 4 8.75 23

January,2013 8.75 7.75 6.75 4.25 8.75 23

Amity Business School Page 52

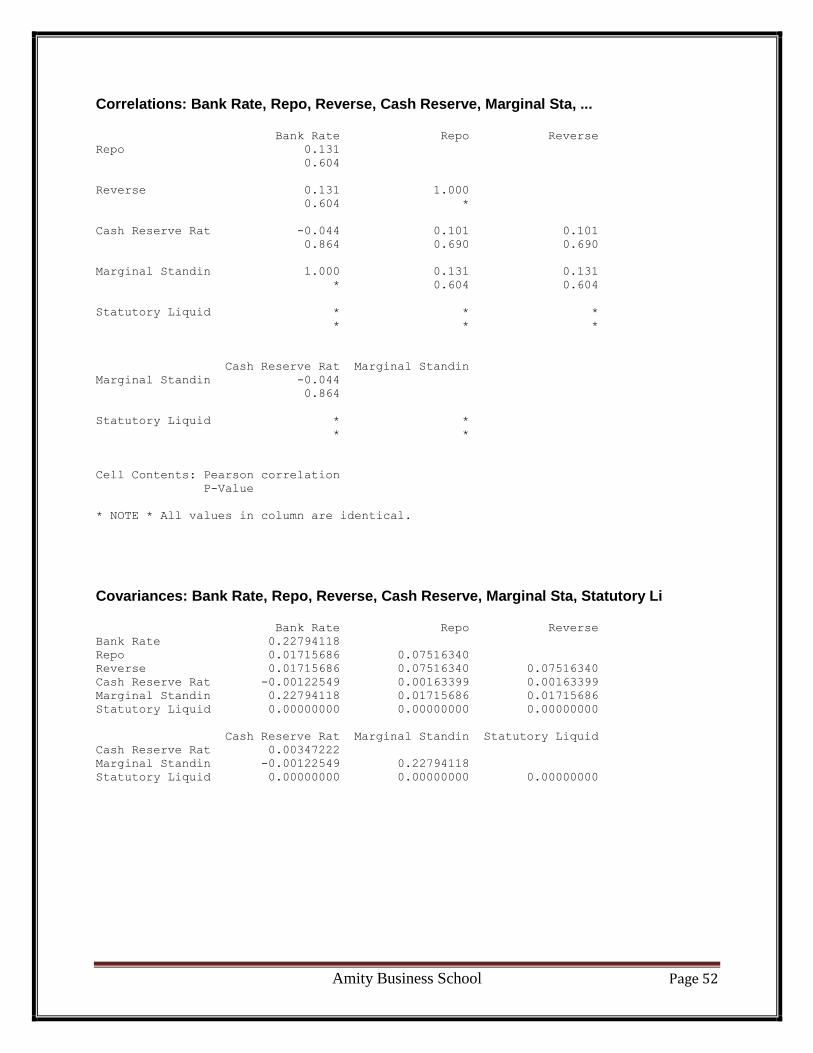

Correlations: Bank Rate, Repo, Reverse, Cash Reserve, Marginal Sta, ... Bank Rate Repo Reverse

Repo 0.131

0.604

Reverse 0.131 1.000

0.604 *

Cash Reserve Rat -0.044 0.101 0.101

0.864 0.690 0.690

Marginal Standin 1.000 0.131 0.131

* 0.604 0.604

Statutory Liquid * * *

* * *

Cash Reserve Rat Marginal Standin

Marginal Standin -0.044

0.864

Statutory Liquid * *

* *

Cell Contents: Pearson correlation

P-Value

* NOTE * All values in column are identical.

Covariances: Bank Rate, Repo, Reverse, Cash Reserve, Marginal Sta, Statutory Li Bank Rate Repo Reverse

Bank Rate 0.22794118

Repo 0.01715686 0.07516340

Reverse 0.01715686 0.07516340 0.07516340

Cash Reserve Rat -0.00122549 0.00163399 0.00163399

Marginal Standin 0.22794118 0.01715686 0.01715686

Statutory Liquid 0.00000000 0.00000000 0.00000000

Cash Reserve Rat Marginal Standin Statutory Liquid

Cash Reserve Rat 0.00347222

Marginal Standin -0.00122549 0.22794118

Statutory Liquid 0.00000000 0.00000000 0.00000000

Amity Business School Page 53

6 Indian

Banking Sector

Amity Business School Page 54

Management of Capital

Bank Capital

Banks hold capital to provide protection against unexpected losses. Traditionally

capital of a bank constitutes a very small fraction of its total assets. The leverage

ratio of banks is very small when compared to similar ratios of non-financial

institutions. Even the 8% ratio of capital to risk weighted assets does not aim at

protecting banks against losses. Provisions and reserves should take care of them.

Long-term Debt

Debentures and subordinated debt are sources of external funds. Debt is

―subordinated‖ because debt is second in priority to depositor claims in the event

of liquidation. Bank debt by and large is in the form of short and intermediate term

deposit and non-deposit funds derived from money market

Loss Reserve

There are two reserves that banks set aside. Loan loss reserve is set up to meet

anticipated loan losses. Earnings are set aside towards the provision for loan loss

(PLL). Tax burden is reduced when expensing PLL. When a loan defaults the loss

is deducted from the reserve account

Correction of Capital Deficiency

Capital requirements are used by regulators to control risk taking by bank. A bank

with abnormal risk level has to have capital in excess of minimum requirements.

Banks judged to be capital deficient need to take corrective action by

Change in the assets to capital ratio.

Change in the dividend payout ratio.

Change in profitability.

Employee stock ownership.

Raising funds from capital market.

Recapitalisation.

Mergers.

Amity Business School Page 55

Capital Issues

Banks may raise capital by issuing new securities, either equity or debentures.

Prior to July 1998, banks in private sector had to obtain prior approval of the

Reserve Bank for issue of all types of shares, public, preferential, rights/special

allotment to employees and bonus shares. After July 1998, private sector banks

whose shares are already listed can make further issues. The issue of bonus shares

requires prior approval

Refund of capital

The reduction in capital results in an improvement in earnings per share and helps

the concerned banks in better pricing of their share at the time of public issue.

Between 1995-96 and 2003-04, public sector banks have returned to Government

of India, paid-up capital aggregating Rs.1,303 crores.

Write off

Write off of accumulated losses against paid-up capital would enable public sector

banks to have Earning Per Share (EPS) at a higher level for public issues. Public

sector banks have been provided to write off losses of Rs.8,680 crores.

Recapitalization

Recapitalization involves a fundamental change in the ownership position of

shareholders. Through a large stock offering, or merger into another bank or

withdrawal of shares to reduce shareholders‘ equity, a bank in difficulties is

recapitalized

Amity Business School Page 56

Criteria for Evaluation: According to the Working Group the criteria for

evaluation of a bank are,

Capital adequacy ratio.

Coverage ratio.

Return on assets (ROA).

Net interest margin.

Ratio of operating profit to average working funds

Ratio of cost to income.

Ratio of staff cost to the net interest income plus all other income.

Rollover Loans and Flexi rates

To avoid interest rate risk in variability of future funding costs and loans at fixed

rate, the syndicated international loans were made at variable rates of interest

linked invariably to LIBOR and adoption of rollover loans. Rollover lending

involved the adjustment of assets in accordance with potential liabilities. Rollover

lending however, resulted in a shifting of risk to bank borrower who faced

additional uncertainty in managing cash flow and impairing his ability to service

the debt. While avoiding interest rate risk credit risk is created

Overall Risk of Banks

A bank‘s overall risk can be defined as the probability of failure to achieve an

expected value and can be measured by the standard deviation of the value. Banks

that manage their risks have a competitive advantage. They take risks consciously,

anticipate adverse changes and protect themselves from such changes.

The chart of check list for risk management compiled by Bank of Japan and quoted

by RBI in the Report on Trend and Progress of Banking in India, 1996-97 which is

quite comprehensive.

Amity Business School Page 57

Amity Business School Page 58

Interest Rate Risk

Net Interest Risk

Net interest income which is the difference between interest income and interest

expense is the principal determinant of the profitability of banks. Net interest

income is determined by interest rates on assets and paid for funds, volume of

funds and mix of funds (portfolio composition). Changes in interest rate affect the

net interest income. Whenever rate of interest conditions attaching to assets and

liabilities diverge, then changes in market interest rates will affect bank earning. If

a bank attempts to structure its assets and liabilities to eliminate interest rate risk,

the profitability of the bank would be impaired.

Mismatch of Assets and Liabilities

A bank may borrow short and lend long. The mismatch of assets and liabilities

gives rise to interest rate risk. In such a case a rise in interest rates can result in

losses for the bank.

Variable Interest Rate

Each bank through its choice from different types of assets and liabilities can alter

the structure of its balance sheet in order to increase or decrease interest rate

exposure

Yield Curve

Yield curve plays an important role in interest rate risk management. Banks accept

interest rate risk and maintain a slight liability sensitive position (rate sensitive

assets less than rate sensitive liabilities)

Maturity or Funding Gap

The interest sensitivity position of a bank is usually measured by its gap, which is

defined as the difference between the volume of interest sensitive assets and

liabilities. Interest sensitive

Amity Business School Page 59

Duration

Duration measures the interest rate risk of a financial instrument. It shows the

relationship between the change in value of a financial instrument and change in

the general level of interest rates

Modified Duration

Modified duration provides a standard measure of price sensitivity to calculate the

duration of the portfolio as the weighted average of the duration of its individual

components.

Future, option and Swap

These derivative instruments allow a bank to alter interest rate exposure and each

has advantages and disadvantages compared with the other. When taken together

they give a bank enormous flexibility in managing interest rate risk

Futures

A futures contract is a standardized agreement to buy or sell an asset on a specified

date in future for a specified price. The buyer agrees to take delivery at a future

date at today‘s determined price; and the seller agrees to make delivery at a future

date at today‘s established price.

Options on Futures Contracts

Interest rate risk may also be hedged through options on futures contracts. An

option provides the buyer with the right, but not the obligation, to buy or sell an

agreed amount of an underlying instrument (such as a T-bill futures contract) at an

agreed price. A call option gives the buyer the right but not the obligation to buy an

underlying instrument at a specified price, called exercise or strike price. A put

option gives the buyer the right (and not the obligation) to sell a specified

underlying security at the agreed price

Swaps

Swaps came into vogue in 1981. They are used widely by banks. At the end of

2004 outstanding (OTC) amount of interest rate swaps was $147 trillion. Swaps are

private arrangements to exchange cash flow in future according to a prearranged

formula.

Amity Business School Page 60

Interest Rate Swaps:

In an interest swap two parties, called counter parties, agree to exchange periodic

interest payments. The amount of interest payments exchanged is based on some

predetermined principal which is called the notional principal amount.

Types of Interest Rate Swaps

Fixed-for-Floating

Base Swaps (Floating-to-Floating Swaps

Zero Coupon for Floating Swap

Forward Swaps (or Delayed Rate Setting Swaps)

Rate Capped Swaps

Separation of Interest Rate Risk and Credit Risk

Banks do not want to make long-term loans at fixed rates of interest because of the

interest rate risk. Banks prefer the floating rate loan. With a swap, the borrower can

transform the floating rate loan to fixed rate and thus avoid the interest rate risk.

The swap allows the separation of interest rate risk from credit risk. The bond

market carries the former and the bank carries the later.

In pure interest rate swaps there is no exchange of notional or actual principal. If

the times of reciprocal interest payments coincide only the net difference is paid.

Pricing Interest Rate Swaps

Pricing covers relevant interest rates and interest payment schedules and fees for

swap dealer‘s services. The interest rates are set to provide a spread which runs

from 5 to 10 basis points. Interest rate swaps are standardized and do not generate

fee income.

Spreads on interest rate swaps are quite narrow reflecting low risks and the huge

and liquid financial markets. Narrow spreads provide an incentive to use interest

rate swaps

Amity Business School Page 61

REPOS REPO and reverse REPO operated by RBI in dated government securities and

Treasury bills (except 14 days) help banks to manage their liquidity as well as

undertake switch to maximize their return. REPOs are also used to signal changes

in interest rates. REPOs bridge securities and banking business.

A REPO is the purchase of one loan against the sale of another. They involve the

sale of securities against cash with a future buy back agreement.

They are well established in USA and spread to Euro market in the second half of

1980s to meet the trading demand from dealers and smaller commercial banks with

limited access to international interbank funding. REPOs are a substitute for

traditional interbank credit.

REPOs are part of open market operations. With a view to maintain an orderly

pattern of yields and to cater to the varying requirements of investors with respect

to maturity distribution policy or to enable them to improve the yields on their

investment in securities, RBI engages extensively in switch operations. In a

triangular switch, one institution‘s sale/purchase of security is matched against the

purchase/sale transaction of another institution by the approved brokers. In a

Amity Business School Page 62

triangular switch operation, the selling bank‘s quota (fixed on the basis of time and