IMPACT OF MICROFINANCE IN GRASSROOT DEVELOPMENT BY WELI, CHISONMA IBELEMA Being an Empirical Research Project Submitted To the INSTITUTE OF FINANCIAL AND INVESTMENT ANALYSTS, NIGERIA (IFIAN) In Partial Fulfillment of the Requirements for certification as an Associate Member of the CHATTERED INSTITUTE OF FINANCIAL AND INVESTMENT ANALYSTS, NIGERIA (CIFIAN) (C) WELI, Chisonma Ibelema 0

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

IMPACT OF MICROFINANCE IN GRASSROOT DEVELOPMENT

BYWELI, CHISONMA IBELEMA

Being an Empirical Research Project

Submitted To the

INSTITUTE OF FINANCIAL AND INVESTMENT ANALYSTS,

NIGERIA (IFIAN)

In Partial Fulfillment of the Requirements for

certification as an

Associate Member of the

CHATTERED INSTITUTE OF FINANCIAL AND INVESTMENT

ANALYSTS, NIGERIA (CIFIAN)

(C) WELI, Chisonma Ibelema0

All Rights Reserved

2014

INSTITUTE OF FINANCIAL AND INVESTMENT

ANALYSTS, NIGERIA (IFIAN)

Empirical Research Project on

“IMPACT OF MICROFINANCE IN GRASSROOTDEVELOPMENT”

BY

WELI, CHISONMA IBELEMA (MRS.)

1

CHATTERED INSTITUTE OF FINANCIAL AND

INVESTMENT ANALYSTS, NIGERIA (CIFIAN)

NOVEMBER, 2014.

CERTIFICATION

This is to certify that I, Weli Chisonma Ibelema, am

responsible for this work. That this work is my

original contribution to the body of knowledge, except

as specified in the acknowledgement and references. I

also declare that this entire project or any part of it

has not been submitted by me or any other person in any

institution for the award of any degree or

certification .

2

WELI, CHISONMA IBELEMA ______________________

_________

(STUDENT)

SIGNATURE DATE

DEDICATION

This work is dedicated to god Almighty who generously

gave me the strength, health and resources to

successfully accomplish this research amid competing

demands.

3

AKNOWLEDGEMENT

4

My sincere and profound gratitude first and foremost

goes to my Father- the Lord God almighty for His love

and mercies that have brought me thus far.

I also wish to acknowledge the efforts and

contributions of my lecturers in the cause of this

certification program to enable me acquire relevant

knowledge in this field.

My heartfelt gratitude goes to my wonderful family who

gave me all the support I needed in the course of this

program. I specially thank my loving husband- Ruwhuoma

for his support, encouragement and understanding. I

also appreciate our God given children- Oke and Izi;

and my entire household.

5

TABLE OF CONTENT

Title Page Declaration Certification Abstract Acknowledgement Table of Content List of TablesChapter One: Introduction

1.1. Background to the Study1.2. Statement of the problem1.3. Purpose of the study1.4. Research Questions1.5. Hypotheses1.6. Definition of terms1.7. Significance of the study1.8. Scope of the study1.9. Limitations to study1.10. Organization of the study

Chapter two: Literature Review

2.0. Introduction

Chapter three: Research Methodology

3.1. Research Design

3.2. Population of Study

6

3.3. Data collection

3.4. Operational Measures of Variables

3.5. Data analysis technique

3.6. Test of Hypothesis

Chapter four: Presentation and Analysis of Data

Chapter five: Discussion, Conclusion, and Recommendation

5.1. Discussion

5.2. Conclusion

5.3. Recommendations

Bibliography

Appendix

LIST OT TABLES

Table 2.1 Ownership of informal enterprises by sector in Nigeria

Table 2. 2. Participatory distribution of Sectors for which MFBs give account of Micro-credit

activities

Table 4.1: Descriptive statistics of percentage growth rate of Variables- Micro Finance

Banks (MFB) operations and Grass root development (1992-2013).

Table A. 1: MFB operations and Development indices

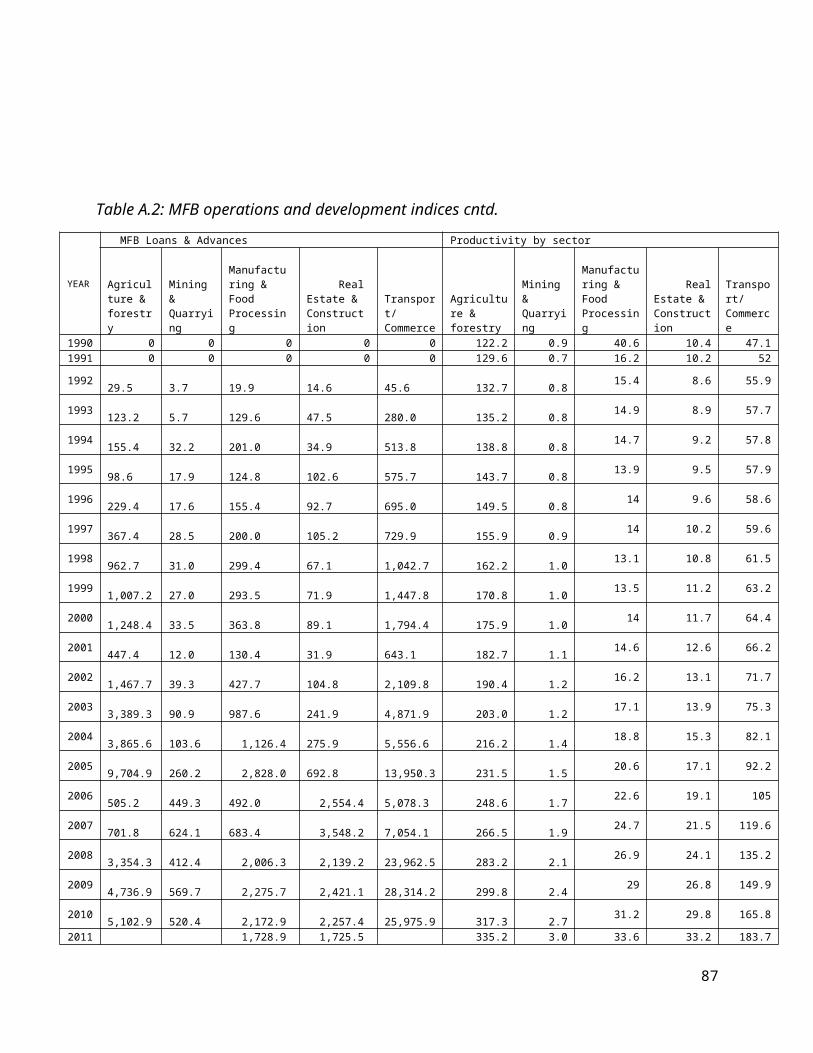

Table A.2: MFB operations and development indices cntd.

Table A. 3: Regression analysis: Beta coefficient

Table A. 4: Coefficient of Determination (R-Squared)

Table A. 5: Z-test at 5% level of significance- critical value

7

LIST OF FIGURES

Figure 2. 1 Ownership distribution of informal enterprises by sector in Nigeria

Figure 2.2: Ownership of informal enterprises by sector in Nigeria for which MFBs give account

of Micro-credit activities

Figure 4.1: Comparison of MFB average apportioning of credit to sectors and thesector’s aggregate productivity.

8

ABSTRACT

This study investigated the impact of micro finance operations on grassroot development, by analyzing its effect on factors that define the majorcharacteristic of the grass root which is poverty. It was identified fromliterature that low productivity and employment are the major causes ofpoverty, and all strategies that fail to address their increase cannot bringabout development at the grass roots. Based on this assumptions asrooted in the micro finance classical theory, this study raised eighteenhypothesis which were tested through multiple regression analysis. Data

9

was gathered from secondary sources of the Central Bank, World BankData base, and the National Bureau of statistics. Micro finance operationswas proxied by Micro finance Banks (MFB) Micro- credit, Micro- depositsand size of the industry; while grass root development was proxied by rateof employment and aggregate productivity in sectors where the grass rootis economically active. The results revealed that Micro- credit did not haveany significant impact on employment or any of the sectors’ productivity,but had the potential of increasing employment, and productivity inagriculture. Micro- savings was found to have a significant but negativeimpact on productivity in agriculture. The results also showed thatalthough it had no significant impact on the other sectors, yet it had thepotential to increase productivity in the manufacturing andtransport/commerce sectors of the economy. The size of the micro financeindustry had a significant and positive impact on employment rate; but anegative yet significant impact on productivity in the real estate/construction sector. The insignificant impact of micro finance operationsand its rather negative impact on most of the sectors which was contraryto our a-priori expectations could be explained by the prevalent problemsof funds diversion of MFB clients to consumption expenditures rather thaninvestment, which most often brings them into a debt trap, and most oftendeath of such enterprises. Therefore the study recommended that MFBsintroduce and priorities as part of its services, training and informativesessions to educate its clients on the potentials of funds being invested intobusinesses; priorities its functioning of monitoring and corporategovernance in cases of lending, and extend more of its credit facilities tothe agricultural sector. It also recommended that the government enhanceits provision of basic infrastructure to ease operational difficultiesencountered by these firms.

10

CHAPTER 1

INTRODUCTION

1.1. Background to the Study

In every society no matter how advanced, the system stratifies

different levels of power, resources, and status among

inhabitants; determining distribution pattern of these benefits

and control over the distribution process. At the bottom of the

distribution process lies those considered as the grass-root of

the society. According to Pilisuk, McAllister and Rothman (1996),

individuals with high socio-economic status, also considered as

the elite are better positioned to exploit both persons and

environments for their benefits, as they have greater share of

powers and control over resources. On the other hand, the grass-

root are those with less power and fewer resources; they are the

common or ordinary people, especially as contrasted with the

leadership; the society at a local level rather than at the

center of major political activity, and are mostly found in the

agricultural, rural, and sub-urban areas of a country

(Dictionaty.com, 2014). Pilisuk, McAllister and Rothman (1996),

described them as those who most often lack the most basic of

human necessities for housing, employment, food, health-care,

education, and a clean and safe environment. They are the

ordinary citizens and in particular the poor.

11

In developing countries like Nigeria, majority of their

population fall under this description in contrast with what

obtains in developed countries like America, where very few

persons fall into this category. Therefore, the challenge for

most developing countries has been the need to reduce the

percentage of persons that fall into this category through grass

root development. According to the US- ADF (1998), grassroots

development is promotion in people’s well-being and empowering of

persons and groups such that they can expand and make their own

choices and bring about change. It centers on poverty alleviation

and socio- economic empowerment of poor and vulnerable. Various

measures have been employed including reforms in government and

political structure (like, creation of districts and Local

Governments); introduction of several government policies and

programs like provision of public goods at the grass-root by the

various tiers of government and their parastatals, and

involvement of public-private partnership projects. According to

Amsden (2011) the problem has been that these remedies to reduce

poverty at the grass-root do not address the causes of poverty

which is unemployment. Grass-roots poverty alleviation measures

in Africa have been exclusively designed and targeted to make

job-seekers more capable (healthy, educated, mobile), although no

jobs are available. She further stated that poverty persists from

low productivity which gives room for lack of employment; and to

create employment requires capital investments to expand

entrepreneurial opportunities and increase productive jobs. Going

12

by Schumpeter’s theory, development can only be achieved when

financial institutions are present to act as catalysts in the

system. They function to provide financial resources through

intermediation in form of capital accumulation for innovative

entrepreneurs to invest, taking advantage of opportunities and

thereby creating a whole cycle of increased productivity and

employment which leads to development. Unfortunately, due to

peculiar characteristics of individuals and entrepreneurs at the

grass root, these ones have been faced with financial exclusion

from the formal financial sector. In a bid to provide these

desirable services to the grass roots, micro financing was

created formally and has evolved informally in other to boost the

productive capacity of these impoverished persons. Micro-finance

means small-scale transactions of credit and savings, and it

sometimes offers skill-based training to augment productivity or

organizational support and consciousness-raising training to

empower the poor (Khander, 2003). Therefore, it is to a large

extent, meant to meet the needs of the ‘active poor’- small,

medium, and micro-scale producers and businesses, and the

vulnerable populace like women. This expectation has drawn much

debate. Proponents insist that microfinance reduces poverty

through increased productivity, higher employment and higher

incomes; while critics argue that it rather drives poor

households into a debt trap as money from loans are often spent

on consumption instead of being used for productive investments,

and therefore does not improved income or standard of living -

13

health or education (Baidoo, 2014). Khander (2003) in same light

hypothesized that since micro finance supports mainly informal

activities that often have low market demand, aggregate poverty

impact of microfinance in an economy would be unsustainable, low

or non-existent in most developing countries. Most studies

investigating impact of micro financing on development have often

used survey designs that only showed their short run relationship

as they use cross-sectional survey, and therefore fail to measure

its sustainable impact where it exists. Posner, cited in Nicholas

(2011) found that microfinance success had been more of a case-

by-case truth than a universal one. Most studies on micro finance

impact have more often looked at the individual or small group

level (case-by –case), only a hand full have assessed if these

claimed successes at the grass roots have such desired impact at

the aggregate level. In Nigeria, micro financing has existed

informally for decades, but was formally introduced under the

regulation of the Central Bank from 1992. This study seeks to add

to the body of knowledge in finance by investigating the

aggregate impact micro finance may have on grass-root development

in Nigeria over time, considering the root causes of poverty

being low productivity and employment.

1.2. Statement of the problem

Over time, Nigeria like most developing countries has

struggled with the issues of extreme poverty at its grassroots.

Several steps have been taken in direction of poverty alleviation

14

and development, one of such is formal micro-financing. Micro

finance banking was adopted by the Nigerian government as one of

its ‘bottom-up’ approaches to development- targeting the

grassroots, as recommended by international bodies like the World

Bank and evident in aiding poverty reduction in places like

India. A Policy Regulatory and Supervisory Framework for micro

finance banking was introduced in 2005 by the Central Bank of

Nigeria (CBN) to further strengthen the potentials of the

industry and aid government in using them as a tool to effect

development. This policy was later revised in 2011, to target at

the recognition of existing informal financial institutions and

bringing them within the supervisory purview of the CBN creating

a platform for the regulation and supervision of microfinance

banks. Since its formal introduction into the Nigerian banking

systems debates have been on about its efficacy as a tool for

necessary sustainable development at the grassroots. As at this

year, 2014, the World Bank ranked Nigeria as third country with

the largest number of poor people, and advised on the need to

complement development efforts to enhance growth with policies

that allocate more resources to the extreme poor like transfer

(Omoh, 2014). Gong by the World Bank development Indicators

(2013), 70% of Nigerians still live below $2 per day and are

therefore poor; and this index rather increased by 2.4% between

2004 to 2010, even though the number of Micro finance banks

increased by 6.4% within the same period. Babajide in 2011 from

her grass root study as obtains in most studies claimed that

15

micro financing significantly impacted positively on the

individual entrepreneur’s development in Nigeria. Given these

facts, the core problem here concentrates on questioning the

efficacy of micro finance banking as a potent tool for effecting

sustainable grass root development in Nigeria, such that it

reflects on aggregate indices. This study investigates this

problem empirically.

1.3. Purpose of the study

The objective of this study is to estimate the aggregate

impact of micro-finance on grassroots development. Based on this

the specific purpose is:

a. To ascertain the effect of micro financing on

productivity in sectors where the grass root is economically

active.

b. To identify the effect of micro financing on

employment.

1.4. Research Questions

To achieve the set out general and specific objectives of this

study, this research intends to provide empirical answers to the

following questions:

16

1. In what ways has micro-financing increased

productivity in sectors where the grass root is economically

active?

2. In what ways has micro financing impacted on

employment?

1.5. Hypotheses

To provide answers to our research questions and achieve our

study objectives, this study raised 15 hypothesis for the first

research question, and 3 others for the research question above.

Therefore we hypothesize thus:

H01: Micro-credit has no significant impact on productivity in

the agricultural sector of Nigeria.

H02: Micro-savings has no significant impact on productivity

in the agricultural sector of Nigeria.

H03: Size of the micro-finance industry has no significant

relationship with productivity in the agricultural sector of

Nigeria.

H04: Micro-credit has no significant impact on productivity in

the mining sector of Nigeria.

H05: Micro-savings has no significant impact on productivity

in the mining sector of Nigeria.

H06: Size of the micro-finance industry has no significant

relationship with productivity in the mining sector of Nigeria.

17

H07: Micro-credit has no significant impact on productivity in

the manufacturing sector of Nigeria.

H08: Micro-savings has no significant impact on productivity

in the manufacturing sector of Nigeria.

H09: Size of the micro-finance industry has no significant

relationship with productivity in the manufacturing sector of

Nigeria.

H010: Micro-credit has no significant impact on productivity

in the Real Estate/ Construction sector of Nigeria.

H011: Micro-savings has no significant impact on productivity

in the Real Estate/ Construction sector of Nigeria.

H012: Size of the micro-finance industry has no significant

relationship with productivity in the Real Estate/ Construction

sector of Nigeria.

H013: Micro-credit has no significant impact on productivity

in the Transport/ Commerce sector of Nigeria.

H014: Micro-savings has no significant impact on productivity

in the Transport/ Commerce of Nigeria.

H015: Size of the micro-finance industry has no significant

relationship with productivity in the Transport/ Commerce sector

of Nigeria.

H016: There is no significant relationship between micro-

credit and employment in Nigeria.

18

H017: There is no significant relationship between micro-

deposits and employment in Nigeria.

H018: There is no significant relationship between size of the

micro finance industry and employment in Nigeria.

1.6. Definition of terms

Micro Finance: is a source of financial services for

entrepreneurs and small businesses lacking access to banking and

related services.

Micro- financing: is the act of providing financial services to

the poor who do not qualify for conventional bank services, like

savings and credit extension.

Micro- credit: this is that aspect of micro-financing that deals

with extending micro- debt funds (money available for a person to

borrow) to micro- finance institution customers, usually at a

cost (interest payment) for a specific time frame.

Productivity: refers to output of a sector, and in this case the

increase or decrease in the volume of output.

Employment: This is having and occupation for which the person

is paid, otherwise known as work or job engagement. This could be

self-employment (a person works solely on his business activities

to generate enough funds to pay himself), or being employed by

19

another person or organization and paid for services rendered to

them.

Income: refers to all financial inflows accruing to a unit

(individual or group). In this case, we are referring to all

financial receipts accruing to the household, which could be

reflected by its total expenditure or receipts.

Poverty: this is a state of not having enough money to take care

of basic needs such as food, clothing, and housing.

Aggregate development: collective or sum value of an economic

growth indices; in this case, at the national level.

1.7. Significance of the study

With the grassroots constituting approximately 70% of

Nigerian’s population (Poverty headcount ratio at $1.25 a day (%

of population), NBS, 2012), the results of this study will

educate the Nigerian government and populace (especially the

active poor) on the efficacy or irrelevance of micro-financing in

the economic development process. The findings would also

instruct policy makers on areas where micro-financing can impact

on grassroots development, and suggest policy/ strategy

adjustments such that aggregate developmental goals can be

achieved.

1.8. Scope of the study

20

This study is carried out in Nigeria, and therefore

geographically restricted to the area. The Central bank of

Nigeria only began to give specific account of Micro-finance

activities from 1992, and reliable records necessary to cover all

variables and give balanced data are available up to 2013 for

now; therefore this study covers a twenty- one year period of

1992 to 2009; and is geographically restricted to Nigeria. The

study is restricted to examine the relationship between micro-

finance operations and aggregate grassroots development indices

in Nigeria within this given time frame.

1.9. Limitations to study

Analyzing development could take several dimensions, but most

of the data that reflect development especially at the grass root

are either incomplete, irregular or not up to date in Nigeria,

therefore this study centered on two groups of indices, as these

were data that where readily available and up to date. Of the two

groups of indices, data on employment by sector was not included

in the study, as their computation at the national level begun in

2004, which falls short of our study period.

1.10. Organization of the study

To effectively carry out this study, this paper is divided

into 5 sections. Section one is the introduction. Section two of

this study is the literature review, which is made up of the

theoretical framework and review of empirical literature. The

21

former work discusses theories that relate to finance and

development; while the second part reviews findings from

empirical studies on the subject matter. The third part of the

study suggests the methodology used in the study, while the

fourth section presents our data for the study, analyzes it and

interprets the results of our tests. The final section, which is

five, discusses the findings of our study, draws conclusion and

makes recommendations accordingly.

CHAPTER 2

LITERATURE REVIEW

2.0 Introduction

The previous chapter introduced the study, by providing the

background to the study giving a conceptual framework of the

study, as well as the research questions and hypotheses. This

chapter goes on in its first part to review literature on

theories that attempt to explain the nature of relationship that

exists between finance and development. The second part of this

chapter reviews empirical literature on micro-financing and

development.

22

2.1. Theoretical Framework

Grass roots development: this refers to the development of the

common man who exists at the lowest class of the social ladder.

This class is often characterized by poverty and general

deficiencies in basic areas of life. Therefore factors or

strategies that would impact on poverty level actually define

grass root development. Development can be defined within the

contexts of human development, capital development, or

environmental development, whichever form it takes, it is desired

at the grass root. Several literature and studies have suggested

measures/ indicators of development at the grass roots. These

include:

a. Poverty level- Human development index; poverty

head count; etc.

b. Unemployment

c. Income level/ Socio-economic status

d. Productivity- start up, expansion or

sustainability of micro enterprises that exist in that class

e. Health

f. Education

g. Productivity, etc.

According to Baidoo (2014), development in any setting depends on

the nature and level of economic activities in that society, and

this is defined by the economically active entrepreneurs; in this

case the active poor. At the grass roots they are found to be

either self-employed or employees of production units. In

23

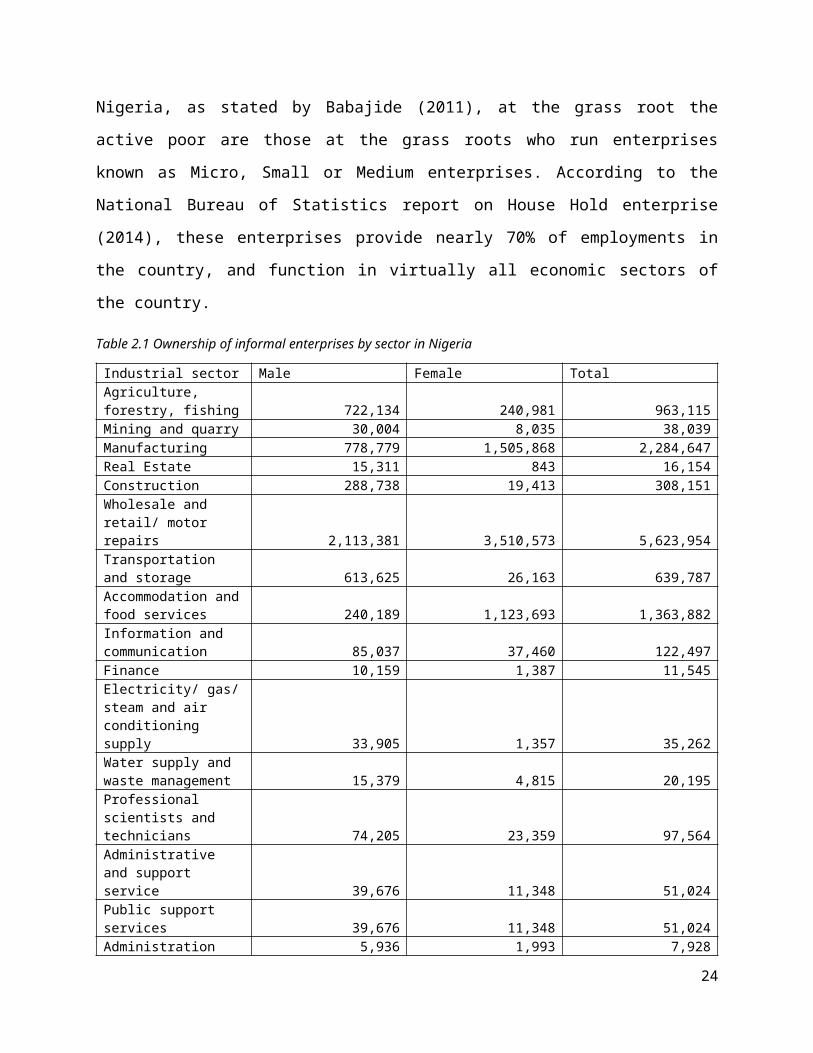

Nigeria, as stated by Babajide (2011), at the grass root the

active poor are those at the grass roots who run enterprises

known as Micro, Small or Medium enterprises. According to the

National Bureau of Statistics report on House Hold enterprise

(2014), these enterprises provide nearly 70% of employments in

the country, and function in virtually all economic sectors of

the country.

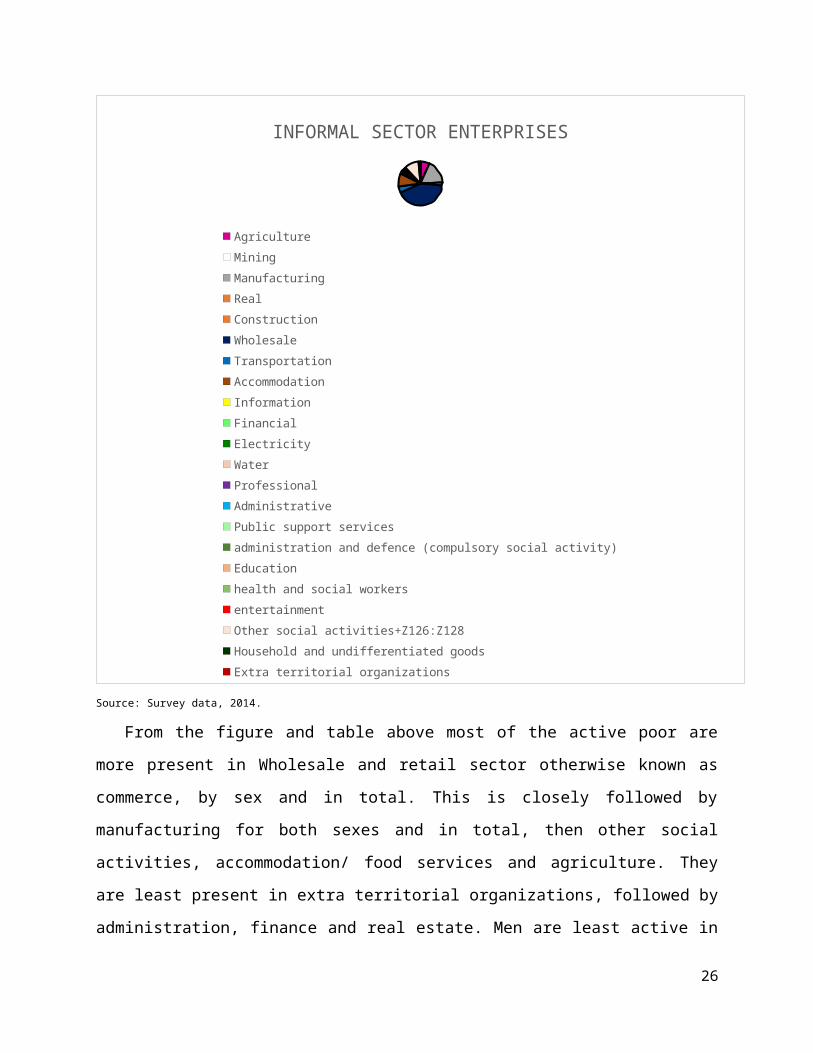

Table 2.1 Ownership of informal enterprises by sector in Nigeria

Industrial sector Male Female TotalAgriculture, forestry, fishing 722,134 240,981 963,115Mining and quarry 30,004 8,035 38,039Manufacturing 778,779 1,505,868 2,284,647Real Estate 15,311 843 16,154Construction 288,738 19,413 308,151Wholesale and retail/ motor repairs 2,113,381 3,510,573 5,623,954Transportation and storage 613,625 26,163 639,787Accommodation andfood services 240,189 1,123,693 1,363,882Information and communication 85,037 37,460 122,497Finance 10,159 1,387 11,545Electricity/ gas/steam and air conditioning supply 33,905 1,357 35,262Water supply and waste management 15,379 4,815 20,195Professional scientists and technicians 74,205 23,359 97,564Administrative and support service 39,676 11,348 51,024Public support services 39,676 11,348 51,024Administration 5,936 1,993 7,928

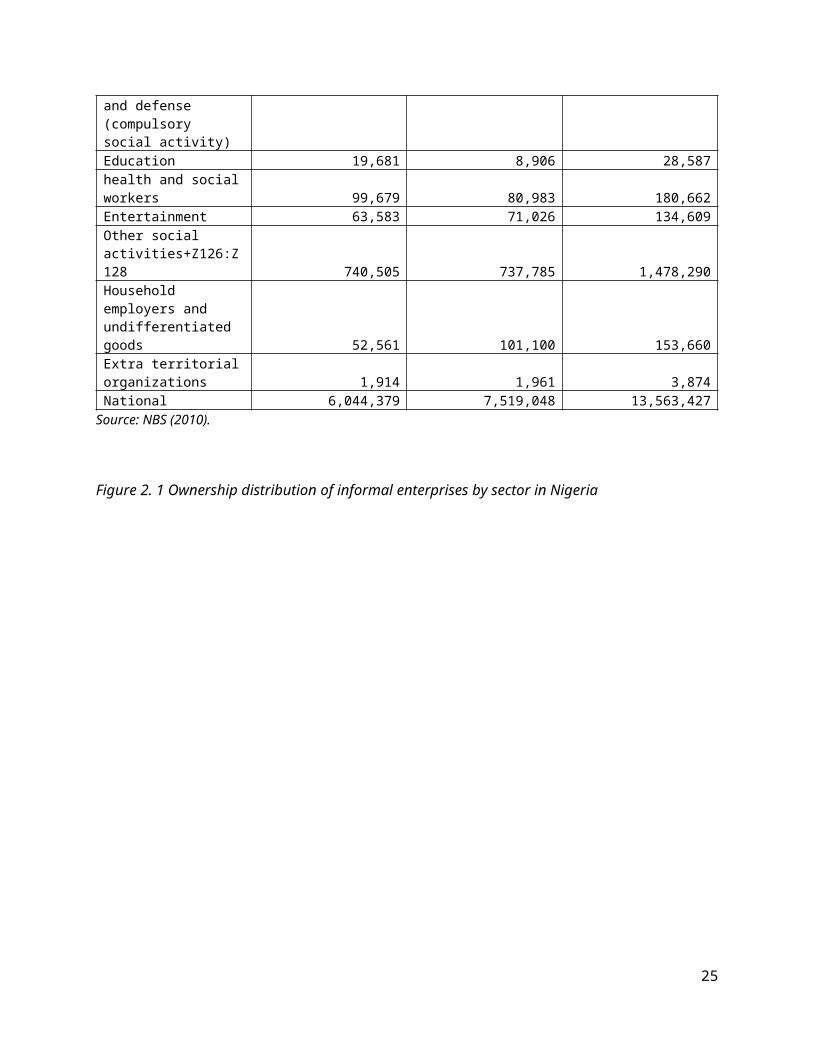

24

and defense (compulsory social activity)Education 19,681 8,906 28,587health and socialworkers 99,679 80,983 180,662Entertainment 63,583 71,026 134,609Other social activities+Z126:Z128 740,505 737,785 1,478,290Household employers and undifferentiated goods 52,561 101,100 153,660Extra territorialorganizations 1,914 1,961 3,874National 6,044,379 7,519,048 13,563,427

Source: NBS (2010).

Figure 2. 1 Ownership distribution of informal enterprises by sector in Nigeria

25

INFORMAL SECTOR ENTERPRISES

AgricultureMiningManufacturingRealConstructionWholesaleTransportationAccommodationInformationFinancialElectricityWaterProfessionalAdministrativePublic support servicesadministration and defence (compulsory social activity)Educationhealth and social workersentertainmentOther social activities+Z126:Z128Household and undifferentiated goodsExtra territorial organizations

Source: Survey data, 2014.

From the figure and table above most of the active poor are

more present in Wholesale and retail sector otherwise known as

commerce, by sex and in total. This is closely followed by

manufacturing for both sexes and in total, then other social

activities, accommodation/ food services and agriculture. They

are least present in extra territorial organizations, followed by

administration, finance and real estate. Men are least active in

26

extra territorial organizations; while women are least active in

the real estate sector. Nationally, more women than men make up

the population of the active poor, and this applies to 9 out of

the 23 sectors.

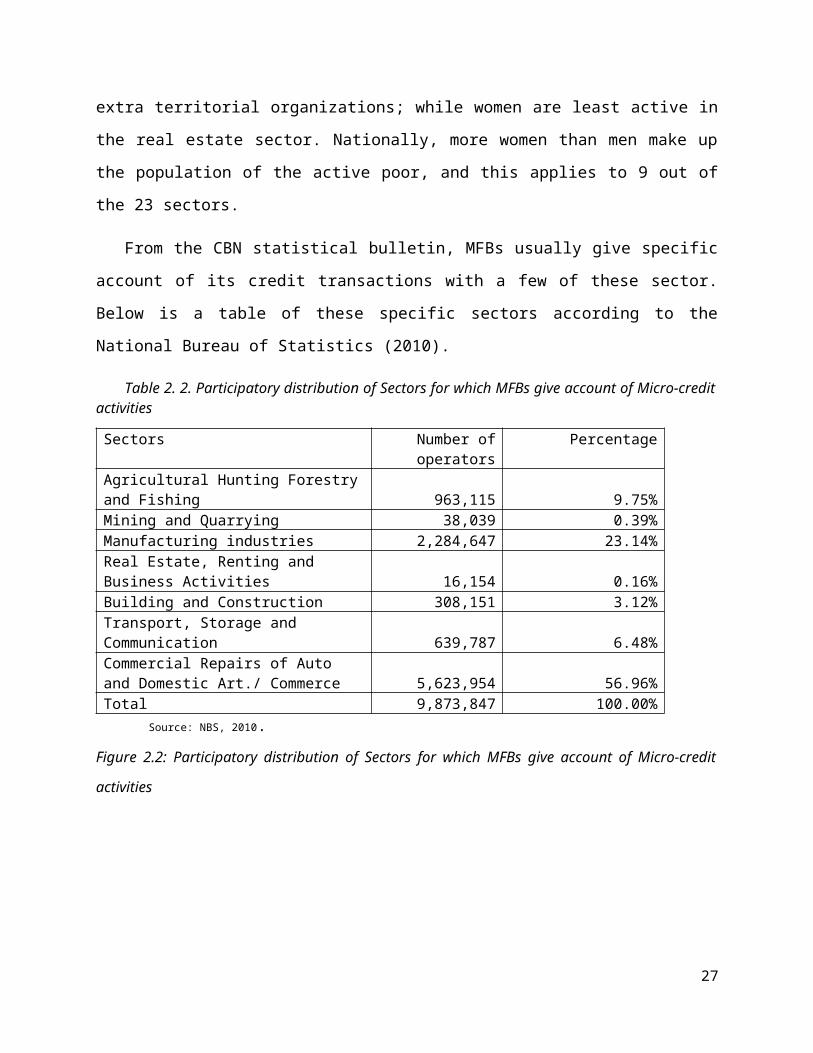

From the CBN statistical bulletin, MFBs usually give specific

account of its credit transactions with a few of these sector.

Below is a table of these specific sectors according to the

National Bureau of Statistics (2010).

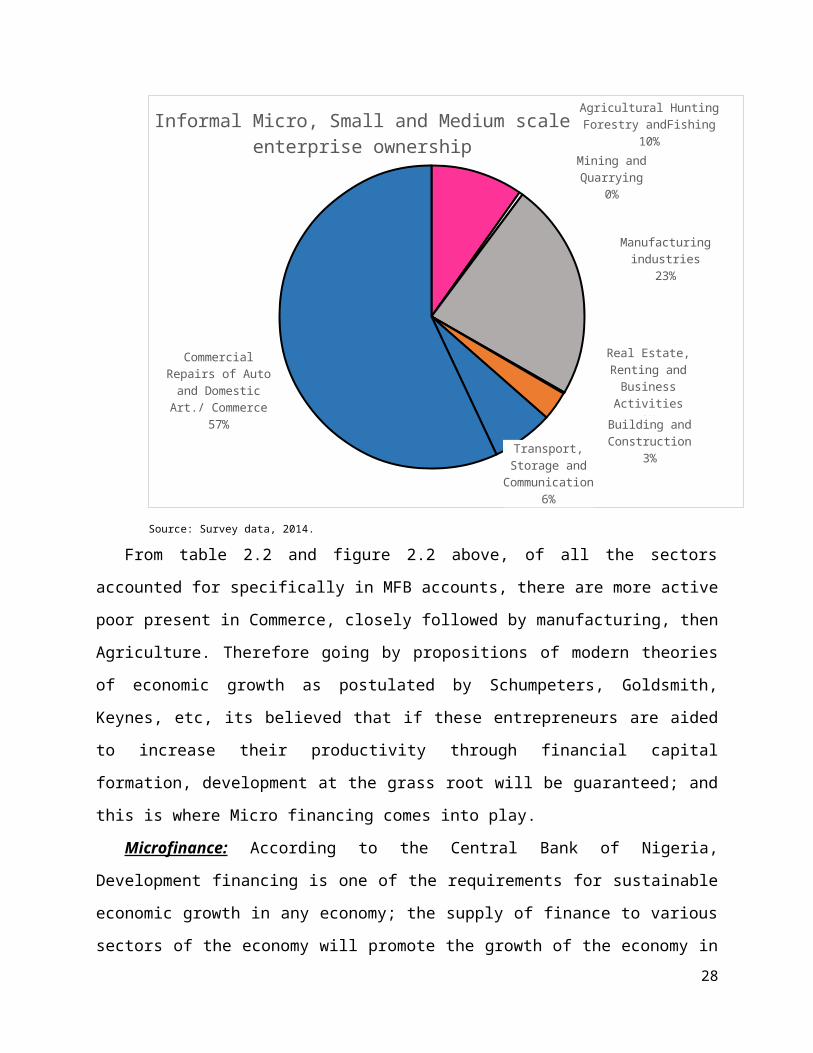

Table 2. 2. Participatory distribution of Sectors for which MFBs give account of Micro-creditactivities

Sectors Number ofoperators

Percentage

Agricultural Hunting Forestryand Fishing 963,115 9.75%Mining and Quarrying 38,039 0.39%Manufacturing industries 2,284,647 23.14%Real Estate, Renting and Business Activities 16,154 0.16%Building and Construction 308,151 3.12%Transport, Storage and Communication 639,787 6.48%Commercial Repairs of Auto and Domestic Art./ Commerce 5,623,954 56.96%Total 9,873,847 100.00%

Source: NBS, 2010.Figure 2.2: Participatory distribution of Sectors for which MFBs give account of Micro-credit

activities

27

Agricultural Hunting Forestry andFishing

10%Mining and Quarrying

0%

Manufacturing industries

23%

Real Estate, Renting and Business Activities

0%Building and Construction

3%Transport, Storage and Communication

6%

Commercial Repairs of Auto and Domestic Art./ Commerce

57%

Informal Micro, Small and Medium scale enterprise ownership

Source: Survey data, 2014.

From table 2.2 and figure 2.2 above, of all the sectors

accounted for specifically in MFB accounts, there are more active

poor present in Commerce, closely followed by manufacturing, then

Agriculture. Therefore going by propositions of modern theories

of economic growth as postulated by Schumpeters, Goldsmith,

Keynes, etc, its believed that if these entrepreneurs are aided

to increase their productivity through financial capital

formation, development at the grass root will be guaranteed; and

this is where Micro financing comes into play.

Microfinance: According to the Central Bank of Nigeria,

Development financing is one of the requirements for sustainable

economic growth in any economy; the supply of finance to various

sectors of the economy will promote the growth of the economy in28

a holistic manner and this, will make development, welfare

improvement to proceed at a faster rate. This line of thought has

given rise to several institutions in the financial service

industry to meet requirement of provision of finance to all

necessary sectors to further economic growth; one of such

institutions is the Micro finance Institutions. Armendariz (2013)

defined micro finance institution (MFI), as a “formal” financial

institution delivering credit and other financial services to

poor individuals without collateral at lower than usurious

interest rates and majorly through group lending under joint

responsibility. Therefore, micro finance or financing as defined

by Baidoo (2014), is the provision of financial services such as

savings, loans and insurance to poor in both urban and rural

settings who are unable to obtain such services from the formal

financial sector. The Central Bank of Nigeria (CBN, 2005) defines

microfinance as the provision of financial services to the

economically active poor and low income households. In other

words, microfinance is the act of providing micro- savings,

credit, insurance and other financial developmental services to

those who have been excluded from the formal banking system, by

special financial institutions called- micro finance institutions

(MFIs).

In Nigeria, the Central Bank classified MFIs as specialized

development institutions, and launched a policy on it in 2005 to

address problems of financial inclusion- to increase access of

the poor and low income earners to factors of production. EFInA

29

(2010) study on Nigeria revealed that five years after the launch

of the Micro Finance policy, those served by formal financial

market (including formal MFIs) only increased marginally by 1.3%

in 2010. It was noted that this percentage increased by 22.7%

when those serviced by the informal sector were included, which

was desirable; yet 39.2 million adult population were still

financially excluded. Against this backdrop and the need to

enhance financial services delivery, the 2005 Microfinance Policy

Regulatory and Supervisory Framework for Nigeria was Revised in

April, 2011, by the CBN in exercise of the powers conferred on

the it by the provisions of the laws- CBN act 1991 and BOFIA

1991. The revision of the policy was targeted at recognizing

existing informal financial institutions and bringing them within

the supervisory purview of the CBN creating a platform for the

regulation and supervision of microfinance banks (MFBs) through

specially crafted Regulatory Guidelines (CBN, 2014). This review

has led an increase in the number of formal MFIs, therefore

increasing possibilities of access to financial service even in

remote areas.

The reason for the evolution, creation, and reforms of MFIs is

strongly based on empirical and theoretical positions on the role

of finance and its special institutions in economic development.

Most theories of economic development all agree to the fact that

development is a function of increase in productivity, which is

highly dependent on availability and efficient use of factors of

production, of which capital - finance is one. Going by this,

30

sourcing of financial resources is as important as sourcing for

other necessary factors of production; but the modern schools of

thought argue that finance is a necessary resource as it could to

a great extent determine procurement of other resources. Sourcing

of financial resources therefore makes financial institutions an

important player in development process as they create avenues

for capital accumulation- providing savings or credit extension.

They act as funnels in the system (neoclassical model), catalysts

(credit creation theory), puppets for directed development

(regulation theory), and have the ability to lead investment and

economic growth as they develop (liberalization theory).

Classical microfinance theory as explained by Dunford (2012)

is centered on change. The theory holds that micro finance

institutions are the key to poverty alleviation, because it

guarantees change in the status of the poor. This is because they

exist to provide an avenue for the poor to raise financial

capital either through savings or loans for investment purposes

in microenterprises. The essence is to either start or expand a

microenterprise, which will in turn yield enough net revenue to

repay the loan (capital and interest), and increase personal or

household income enough to raise their standard of living. A

major assumption of this theory is that, the poor utilizing micro

financing follow these steps:

Step 1: Save with or access loan from a micro finance

institution;

31

Step 2: Invest funds in viable micro enterprise;

Step 3: Yield major returns on investment.

This theory relies on development or poverty alleviation

through access to micro financial services of savings and credit

extension; actual use of these funds for investment purpose; and

management of resources generated. Dunford criticized this

classical theory of micro financing based on what obtains in

reality as relates to these three points. He claims that this

theory of change doesn’t apply to a whole lot of poor people. On

access to financial services, with reference to the Global

Financial index developed by the World Bank, he states that

measures and indices available only tell about the percentage of

global adult population with bank accounts and those currently

borrowing. This analysis, does not show if people who did not

report ‘actual use’ of financial services of savings and credit,

really had a choice to use or not use—a microfinance institution

may not have been locally available; or if it was purely based on

choice of self-exclusion. Banerjee and Duflos as cited by

Dunford, reported from a research in Andra Pradesh that, “Even in

Hyderabad, where there are several competing MFIs, the sign-up

rate for any microcredit loan among families who were eligible to

borrow was only 27 percent, and only 21 percent of those who had

a small business had taken a microcredit loan”. This showed that

most poor people may not take loans from or save with

microfinance providers (both formal and informal) even when they

32

can; therefore this theory does not apply to all poor because so

many choose not to participate even when they can. On use of

funds for investment, Dunford argues that of those who use a

microfinance provider to obtain a “usefully large sum” of money,

how many actually invest the money in a real business. According

to Baidoo (2014) studies have shown that most funds accessed from

micro finance institutions have been diverted to other

unproductive uses such as purchase of durable consumer goods or

consumption instead. This goes to defy the stance of this theory

that funds accessed from the MFIs are solely used for investment

purposes, as people may for several reasons decide not to invest

funds but consume them. This rather drives households into a debt

trap. Concerning management of the resources to generate

sufficient net revenue, Dunford argues that in most developing

countries there are a lot of factors that could interfere with

the process and hinder the realization of such returns even when

funds have been invested in a viable business. Onugu (2005)

stated that micro enterprises profitability and survival are

hindered by internal (such as poor management, low

entrepreneurial skill, unavailability of skilled manpower and

efficient technology, poor record keeping, etc.) and external

(economic conditions in the country, power supply,

infrastructures, government policies, market size/ weak demand

for product, uneven competition with importers, etc.) factors.

According to him, these major factors can stall any micro

enterprise form generating revenues expected and may even drive

33

the borrower into debt and further poverty where the business

fails. Therefore the stance of this theory on the certainty of

change through micro- financing is still under strong debate till

date.

Other schools of thought on micro financing have also risen

along lines justifying the existence of the Micro- finance

institution. Armendariz (2013), stated that Micro finance

institutions have two contending objectives- of survival and

welfare. From our definition, MFIs evolved originally to provide

financial services to the poor, and therefore have and objective

of alleviating poverty; on the other hand, like every other

enterprise they have an objective of survival/ self-

sustainability. Advocates of the Welfare/ Subsidized Credit

delivery approach to micro financing, argue that the main essence

of micro financing is poverty alleviation, and therefore suggest

that the core poor qualify for grants not loans. They assume the

poor are typically unable to lend and save, and therefore are in

need of subsidized credit services (Appah, John and Soreh, 2012).

They kick against MFIs over-emphasizing self-sustainability and

growth, as this objective can make an MFI profit-seeking rather

than welfare-seeking, which would mean introduction of higher

charges further excluding the extreme poor. They argue that,

Micro finance institutions often receive subsidies, donations and

grants from NGOs, government and profit-organizations for on-

lending to the poor. These gifts serve as a form of equity, and

as such these donor can be seen as investors; only that rather

34

than seek monetary returns, they prefer intrinsic returns

(Baidoo, 2014). Therefore the essence of the MFIs existence

should be centered on providing inexpensive financial services

and cheap loans to the poor- providing subsidized credit

services. On the other hand, the Institutional/ Commercial

sustainable Microfinance approach advocates for self-

sustainability, and argue that MFIs should be able to cover their

costs with its revenues. They hold the opinion that, the poor can

and do save and repay their loans to a market-oriented interest

rate, but need secure financial institutions for doing this

(Appah et al., 2012). They criticize the welfare approach as they

believe that MFIs, can easily attain self – sustainability and

make profits and therefore do not need gifts (donations, grants

or subsidies). In defense against the claims of the welfare

approach that their approach will discriminate providing services

to the extreme poor, they posit that competition among

microfinance entrepreneurs will prevent for-profit MFIs to charge

astronomical interest rates (Armendariz, 2013). They state that

self-sufficiency leads to long-term sustainability for

Microfinance Institutions, which will facilitate greater poverty

alleviation in the long-term (Baidoo, 2014). According to Baidoo,

from empirical evidence MFIs which proved self-sufficient tended

to loan borrowers who were either slightly above or slightly

below the poverty line in their respective countries; and this

defeats the aim of reaching and developing the extreme poor of

the society. Also, empirical evidence has shown based on growth

35

estimates that, heavily subsidized MFIs remain at its infancy

(Armendariz, 2013). According to her, far less than expected

households have benefit from their products; they have been found

to not necessarily serve the core poor; they provide exceedingly

small micro savings and insurance; and suffer from a potential

mismatch between what the MFI offers and what the potential

client would prefer. Therefore there have been suggestions that

microfinance should move away completely from the “dual

objective”; while others advocate a balance be struck between

both objectives to properly position the MFI to reach its goal of

service provision and sustainability.

EMPIRICAL LITERATURE

There have been several studies on the concept of micro-

financing as a strategy or tool for achieving development and

alleviating poverty globally, across countries, in a country,

state, district or settlements (like rural or urban areas). In

this section we discuss findings of such studies and attempt to

differentiate or associate these findings.

Most studies on the ‘discuss’ of micro financing are highly

concentrated in developing countries, especially in Asia and

Africa. Some studies have been carried out across countries or

even continents. Burne (2009) conducted a study empirically

comparing the impact of micro finance institutions on development

in some Asian and African countries. Data was gathered from

primary and secondary sources from Asia (6 MFIs in Cambodia and 3

36

in Philipines) and Africa (6 MFIS Ethiopia, and 5 in Uganda). The

study developed an econometric model to measure the relationship.

For development, he used average savings and loan balances per

clients as indicators; while the explanatory variables of micro

financing was proxied with size of the MFI (number of staff) and

experience (number of years in locality). The study results

revealed that micro finance had a significant positive

relationship with development; and that micro credit was the most

robust mechanism to boost development. He also found that MFI

size was irrelevant, but their level of experience positively

impacted on the amount of credit granted to the poor. Savings was

found to be the best estimator of development from the study. The

study also revealed that the number of personnel working with

microfinance institutions like in Uganda increased steadily over

time, and thus matched the development. There was found no

significant difference between marginal impact of microfinance

institutions based on geographical positioning between Asia and

Africa; but there was found an environment independent positive

impact of MFIs on development in low- income countries.

In Latin America and the Caribbeans, a study was carried out

by Nicholas (2011) to examine the effects of microfinance on

extreme poverty rates as defined by the poverty headcount ratio

at $2 a day and $1.25 a day, while controlling for structural

economic changes. His objective was to dispute critics who posit

that the costs of microfinance outweighs the benefits. They adopt

a panel-data analysis to capture effects over time and across

37

countries. The study spans over the time 1996 – 2008, and is

conducted in 17 countries from Latin America and the Caribbean

(Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica,

Dominican Republic, Ecuador, El Salvador, Guatemala, Honduras,

Mexico, Nicaragua, Panama, Paraguay, Peru, and Venezuela).

Secondary data was sourced from MIX Market which included total

borrowings, gross loan portfolio, number of active borrowers, and

the number of women borrowers for each of the countries listed

above. To control for other factors that may cause economic

growth, and thereby reduce the poverty head count ratios, the

study introduced to its model World Development Indicators: cost

to start a business (as a percent of GNI per capita), expenditure

on secondary education (as a percent of GDP per capita), female

labor participation rate (as a percent of the female population),

lending interest rate (as a percent), expenditure on research and

development (as a percent of GDP), time required to enforce a

contract (number of days) and the perception of crime as a

constraint to business (as a percent of managers surveyed). The

ordinary Least Square panel regression was the statistical tool

adopted for the study. The result findings did show that micro

finance had a statistically significant effect on reducing

poverty at both the $2 and $1.25 a day levels. It also revealed

that micro finance made a substantial contribution to decreasing

poverty when combined with other, more structural, contributors

to economic development. Coefficients of human capital variables

signaled a much larger effect on reducing poverty than the

38

different measures of microfinance. They conclude that as

microfinance continues to grow and reach more of the world’s

poor, it will give the poor the opportunity to take charge of

their own economic situation and work their way out of poverty.

For studies peculiar to an area or country, there are quite a

number. Khander (2003) studied impact of microfinance on poverty,

based on household survey data collected in 1991/92 and 1998/99

in Bangladesh. He hypothesized that micro finance had an

insignificant or non-existent impact on aggregate poverty

reduction since it mainly funds informal activities which have

low market demand. He used the panel survey method in other to

capture the long-term effect of the micro credit programs, since

they often take a long time to influence outcomes such as assets

or human capital investment- household or individual welfare. He

estimated the effects of micro-finance on consumption, poverty

and non-land assets for participants, non-participants, and an

average villager, assuming that micro-finance programs have

spillover (externality) effects. The study utilized secondary

data generated from a 2- period survey carried out by BIDS and

World Bank in 1991/92 and 1998/99 respectively; therefore the

study sample was restricted to households who formed the panel

during the two periods, 1638 households. His findings revealed

that micro financing programs contributed positively to raising

per capita consumption, mainly on non-food, as well as household

non-land asset. This he said increases the probability that the

program participants may be able to lift themselves out of

39

poverty. The findings also showed that micro-finance impacted

positively on welfare for all households, including non-

participants; which indicated that micro-finance programs were

helping the poor beyond income redistribution with contribution

to local income growth. The results showed that the micro finance

programs had spillover effects in local economies, thereby

increasing local village welfare, especially as it helped reduce

extreme poverty more than moderate poverty at the village level.

He also noted that the aggregate poverty reduction effects was

not quite substantial to have a large dent on national level

aggregate poverty. He recommended micro-finance should perhaps go

beyond the provision of financial services to finding ways to

improve the skills of its poor borrowers to improve their

productivity and income, so that MFIs can exhibit a stronger

impact on poverty reduction.

In Africa where nearly 100% of the countries are developing,

literature on micro financing seems to be more popular in

slightly advanced developing nations like South Africa, Kenya,

Nigeria, and Ghana. Some studies are area specific. In South

Africa, Sheraton (2004) carried out an analysis of the

effectiveness of microfinance with Western Cape as the case

study. The study focused on the investigating the extent to which

the UN/ OSCAL model of micro finance was being applied in South

Africa. Primary data was sourced from the views of community

members and groups (semi- formal lenders, savings clubs and

informal money lenders) collected through an interviewer-

40

administered questionnaire. The findings revealed that there was

large supply of semi-formal to formal micro lending institutions,

and micro lenders serves as a main source of credit. It also

showed that majority of loans disbursed were for consumption

purpose and to meet survival needs; and a large proportion of

micro lenders clients were recurring clients, making it a

potential source of poverty reinforcement. Micro lenders revealed

that small loans helped clients initially, but many ended up in a

debt spiral situation. The results also revealed a weak link

between microfinance and micro enterprise in the area. The

results further showed that although micro financing did assist

in consumption smoothening and emergency financing, and did

follow some of the principles of the model, yet it was not

sufficient to have a significant impact on poverty reduction.

They recommended ways in which the UN/ OSCAL model could be

incorporated into the reality of South Africa, for microfinance

to be more effective as a development tool.

In Nigeria, there have been some regional studies. In 2011,

Babajide studied the effect of micro financing (financing and

non-financing activities) on micro and small enterprises (MSEs)

in South- west Nigeria. The explanatory variable, Micro financing

was proxied by MFI activities- group membership, pre-loan

training, cross guaranteeship, loan size, technical and

managerial training; while the dependent variables included-

survival, growth, productivity and performance of Micro and Small

Enterprises, in Southwest Nigeria. Four hypotheses were

41

formulated based on theories of financial growth model, pecking

order theory, and contract theory; and tested at a 0.05

significant level, using the analytical tools of multiple

regression analysis and survival analysis (incorporating the Cox

Regression Analysis and Kaplan Meier Survival Analysis technique)

using SPSS statistical package version 15.1. Data was gathered

primarily through interviews and issuing of validated and

reliable questionnaires to 443 micro enterprises and 180 small

enterprises selected using multi-stage random sampling technique.

The study revealed that micro-financing enhanced survival of

MSEs, but was not sufficient for their growth and expansion; and

it had a positive impact on productivity and performance of local

entrepreneurs. It was revealed from the interviews that micro

financing was not effectively and substantially practiced in

Nigeria, as most MFBs granted more individual loans than group

based loans, thereby increasing their running cost and putting

their portfolio at risk. The study recommended as a critical

microfinance strategy - collective and cooperative support in the

form of solidarity groups at the local level; and at the national

and regional level; a networking of groups among operators of

MFBs for effectiveness and sustainability.

Similarly, Taiwo in 2012 conducted a study on the impact of

Microfinance (MF) on the welfare and poverty alleviation in

Southwest Nigeria. Three hypothesis were raised on mobilization

and dispersion of credit, standard of living, and growth of small

and medium scale enterprises in Nigeria. The study used

42

questionnaires to collect cross-sectional data from selected

respondents in selected areas of Lagos and Ogun States of Nigeria

respectively. The study used the multiple regression analysis of

the Ordinary Least Square (OLS) technique of estimation to make

tentative predictions concerning outcome variable, and the Linear

Probability Model was also adopted in the study. Findings showed

that Microfinance impacted the businesses and lives of the

beneficiaries (Microfinance Clients); and gave them access to

essential life-enhancing facilities and services. They

recommended that MFIs in Nigeria should seek long-term capital

from the Pensions and Insurance companies so they could grant

larger volumes of loans to greater number of their clients.

Appah, John and Soreh (2012) carried out an empirical analysis

of the relationship between Microfinance and poverty reduction in

Bayelsa state of Nigeria, with particular reference to all women

in small scale business in the area. The study raised four

hypothesis, and used a questionnaire titled ‘microfinance and

poverty’ to collect data from 400 entrepreneurs by stratified

random sampling, of which 286 were collected for analysis. The

chi-square, ANOVA and descriptive statistical tools were applied

to test data through the excel software and Statistical Package

for Social sciences (SPSS). It was found that microfinance had a

significant impact on poverty reduction. The results also showed

that there was a significant difference between microfinance and

the traditional savings rotating system in Bayelsa State. They

concluded that microfinance alone cannot reduce poverty in any

43

society where basic infrastructures like good roads, steady power

supply, good transportation system etc. are nearly not available.

The study recommended that the governments should provide the

basic infrastructural facilities to enable small business owners

grow; and the need for reduction in the interest rate of

microfinance institutions to minimize the level of poverty in

Nigeria.

Among studies specific to an area, some have also been gender

specific. Abdulkadir, Umar, Garba and Ibrahim (2010) empirically

investigated the impact of MFB on women entrepreneurial

development in Metropolis. Through the simple random sampling

technique, a sample population of 84 women who are members from

four different women associations in metropolis were selected;

and two women associations were selected from two microfinance

bank representing different areas within. Primary data was

gathered by issuing of questionnaire to the 24 women, of which 14

were returned. The study raised questions on awareness,

membership of groups and microfinance, loan collection,

sufficiency, and effect on business and socio-economic life.

Simple percentages were used in data analysis. The study found

that women entrepreneurs knew about MFBs existence; their level

of patronage was high. Also the results of the survey showed that

women entrepreneurs were generally satisfied with the credits

facilities and efficiency of MFB services. It was also found that

as MFBs increased their access to financial services, profits and

growth opportunities occurred in business and thus brought

44

positive changes in their socio-economic life. Also, MFBs

impacted positively in enhancing the socio-economic life of women

entrepreneurs. The study therefore, recommended that MFBs, should

come up with appropriate strategies to attract more investors and

women participation in entrepreneurial activities should also be

encourage for women self-reliance and financial sustainability in

the society.

In 2014, Alani and Sani studied the effect of microfinance

banks on rural dwellers in Kogi State of Nigeria. The study

sample constituted of 5 micro finance banks (MFBs) selected by

judgmental sampling. Data was generated through primary source of

interviews and handing out a total of 368 questionnaires to the

customers and staff of the selected banks. The Z – Test

statistical tool was used to test the 3 hypotheses formulated on

– savings mobilization and intermediation, provision of

affordable services, and provision of employment to the rural

dweller. Findings showed that establishment of microfinance banks

in the area, had a positive impact on the lives of the rural

dwellers, as MFBs mobilized savings for financial intermediation

and provided employment opportunities. They observed that due to

lack of training and exposure of the rural dwellers, the

potentials of MFBs for improving the economic potentials of the

active poor in the rural communities is not maximized. They

therefore recommended for training of rural dwellers on how best

to establish, manage, sustain and expand their businesses. They

also found that the CBN monetary policy rates affected the cost

45

of funds of the MFBs, and therefore recommended a reduction in

the rates.

In the same light, some researches have investigated the

relationship between micro financing activities and economic

development especially in terms of developing the active poor

enterprises at the grassroots. Baidoo (2014) carried out a study

on impact of micro finance on grass root development in Ghana,

Kumasi. The study raised 3 research questions on access, role and

cost of micro-credit in grass root business operation. Using

simple random sampling, 10 respondents were selected; and primary

data was gathered from them through questionnaires, interview and

observations. Data was analyzed with simple descriptive

statistics. The results showed that MFIs assisted the grass root

businesses in raising additional capital requirement for the

expansion and development of their businesses. The process of

accessing loan facilities from MFBs was found to be slow. The

results showed that the charges for financial service (interest

rate) discouraged borrowings. He recommended that, MFIs should

endeavor to enhance their managerial skills among other factors.

Lloyd and Robbins (2014) conducted a study in Nigeria, to

examine the impact of the CBN’s Microfinance policy on credit

accessibility and financial inclusion on micro entrepreneurs, low

income household, and the economically active poor, already being

denied access to formal financial services. They used secondary

data sourced majorly from the CBN, and presented in bar charts

and statistically tables; and analyzed with descriptive

46

statistics tools. The study results revealed that only 35% of the

economically active poor had access to financial services. The

study revealed that the preceding finding was as a result of high

cost of accessing funds (the transmission effect of CBNs high

monetary policy rate on bank lending rates), and uneven spread of

micro finance institutions among the 6 geopolitical zones. The

study therefore recommended a reduction in the CBN’s monetary

policy rates from 12% to 9% to reduce cost of funds from micro

finance banks which stood as high as 19%, to enhance financial

inclusiveness and accessibility for the poor. They also

recommended the establishment of more MFIs in areas where they

were lacking, especially in the Northern region.

From the foregoing, most of the studies on micro financing and

the role it plays, relates more to- poverty, micro enterprising,

women and rural dwellings, which shows it is targeted at the

grass roots where the poor and vulnerable are. Most of these

studies differed in terms of geographical location, tools for

gathering data and data analysis techniques. The major tools for

obtaining data observed so far include questionnaires and

interviews which look at the impact of the subject matter on

individual bases and in a few communal bases. There are hardly

any study looking at the aggregate impact of micro financing

which has been adjudged as a necessary tool for development given

its impact on individuals or communities involved in it.

Therefore this gap in literature is what this study seeks to

47

fill; by investigating the aggregate impact of micro financing on

indices of grass root development.

48

CHAPTER THREE

RESEARCH METHODOLOGY

3.0. Introduction

The first chapter of this study dealt with the background of

the study, statement of the problem of the study as well as

hypotheses raised from the objectives and research questions of

the study. The immediate preceding chapter discussed literature

related to the problem and variables of the study. This chapter

discusses the research procedures adopted for this study, namely-

research design, population for the study, instruments for data

collection and data analysis techniques.

3.1 Research design

To achieve the objectives of this study as identified in

chapter one, it is necessary to articulate a research design. A

research design is defined by Barridam (2001) as a frame work or

plan that guides the collection and analysis of data for the

study. It is a model of proof that allows the researcher to draw

inferences concerning causal relations among the variables under

investigation (Nachimas and Nachimas, cited in Baridam, 2001).

There are basically two types of research design (Baridam, 2001)

49

or study research patterns (Nwankwo, 2010) - experimental and

quasi-experimental. According to Baridam (2001), the major

difference between them is that in the experimental design/

study, all the elements of the design are largely under the

control of the researcher- these include research setting,

explanatory variables, study subjects and their assignment to

different groups. He states that in quasi-experimental design/

study, the various elements of the design are not under the

control of the researcher. Nwankwo (2010) defined quasi-

experimental study as “a study in which some threats to internal

and external validity cannot be properly controlled because of

unavoidable situations associated with the study”. According to

Baridam (2001) the quasi-experimental design is often used in

social and administrative science research because the

relationship between variables involved is not subject to

manipulation. The current study on “Micro finance and grass root

development” is of administrative sciences and the relationship

between the variables to be studied is not subject to

manipulation, therefore this study is quasi-experimental.

3.2 Population of Study

The population of this study is made up of the 825 micro

finance bank- clients and staff in Nigeria.

3.3 Data Collection

Data in administrative science research can be obtained

through- survey of existing documents; questionnaire method

50

(personal interviews, telephone interviews, or mail survey); and

observation method (Baridam, 2001). Existing documents according

to him, play a significant role in all types of research, and can

be found in raw or tabulated forms. In their raw form, they are

basic documents or records originally designed as administrative

documents and not research instruments; however, it is often

possible to prepare statistical tabulation from them (raw data)

that can serve as meaningful, valid and reliable data for a

study. According to Baridam (2001) and Osaat (2009), the

tabulated data can be used as the major source of data or as

supplementary data in a research study. Often, available

statistical data such as produced by the Office of Statistics,

Census board, Central Bank, or Government Ministries, refer to

socio-economic information on a large scale (about demographics-

sex, age, etc; income, expenditure patterns, etc.) which provide

information which would normally be difficult to obtain by the

researcher. Considering the nature of factors to be investigated

in this study, it would prove difficult or impossible for the

researcher to generate data that will adequately represent these

factors through the other data collection methods; therefore,

this study adopts the method of ‘Survey of existing documents’

(secondary data), to determine the relationship between the

variables.

3.4 Operational Measures of the Variables

The key operational variables involved in this study include:

51

i. Grass root Development

ii. Micro finance operations

Grass root Development: For operational purpose, grass root

development is proxied by factors that cause and can influence

its major characteristic- poverty. These factors include:

Productivity: proxied by the gross domestic product of

sectors in which the grass root is economically active.

Unemployment: proxied by national rates of employment

Micro finance Operations: this is proxied by:

Total credit offered by MFBs;

Sectoral credit offerd by MFBs

Total deposits of MFBs;

Total number of MFBs in the country.

3.4 Data analysis technique

Osaat (2009), states that the identification of a data

analysis technique in every empirical study is very important, as

it primarily involves the researcher identifying the appropriate

statistics to be used for effective analysis of data gathered in

other to answer the research questions and test the null

hypotheses presented in chapter one of the study. The present

study raised two research questions and eighteen hypothesis, in

which relationship is being sort between variables relating to

Micro financing and indicators of grass root development. For

data analysis the multiple regression analysis is used to test

52

the hypothesis; and the coefficient of determination (r2) will

be used to measure the rate at which the dependent variable is

explained by independent variables. The analysis and model for

this study is therefore specified as follows:

Grass roots development = f (Micro finance operations)……………1

Considering the dimensions and measures of the variables, this

could otherwise be written as:

Productivity; employment = f (Micro-credit; micro-deposits;

Size of micro finance industry)

Model 1: for Hypothesis 1- 15

Productivity by sector (Agriculture, Mining, Manufacturing,

Real Estate, and Commerce) = f (Micro-credit to sector, micro-

deposits, Size of micro finance industry)

This relationship expressed above could be represented

functionally as:

PSn= f(MCSn, MCD; MFS)…………………………………………(1.

Equation one above could further be represented mathematically

as:

PSnit = α + β1 MCSnit + β2 MCDit + β3 MFSit …………………………….……..(2.

The econometric model for the relationships described in

equations 1 and 2 above is represented as:

PSnit = α β1 MCCSnit + β2 MCD it + β3 MFSit + eit; β1 > 0, β2 > 0, β3>

0……………(3.

53

Where:

PSnit = Productivity growth rate of the sector;

MCCSnit = Growth rate of Micro-credit allocated to the sector;

MCDit = Growth rate of Micro-deposits;

MFSit = Growth rate of number of micro finance banks- Size of

micro finance industry;

α = intercept;

β 1 = coefficient of the explanatory variable- MCCS

β2 = coefficient of the explanatory variable- MCD

β3 = coefficient of the explanatory variable- MFS

e = error term

n = Sectors under study which include – Agriculture, Mining,

Manufacturing, Real estate/ Construction, and Transport/

Commerce.

i = cross-sectional variable from 1,2, 3,…nth.

t = time series variable from 1, 2, 3...nth.

Apriori expectation β1 > 0, β2 > 0, β3> 0.

Model 2: for Hypothesis 16- 18

Employment = f (Micro-credit to sector, micro-savings, Size of

micro finance industry)

54

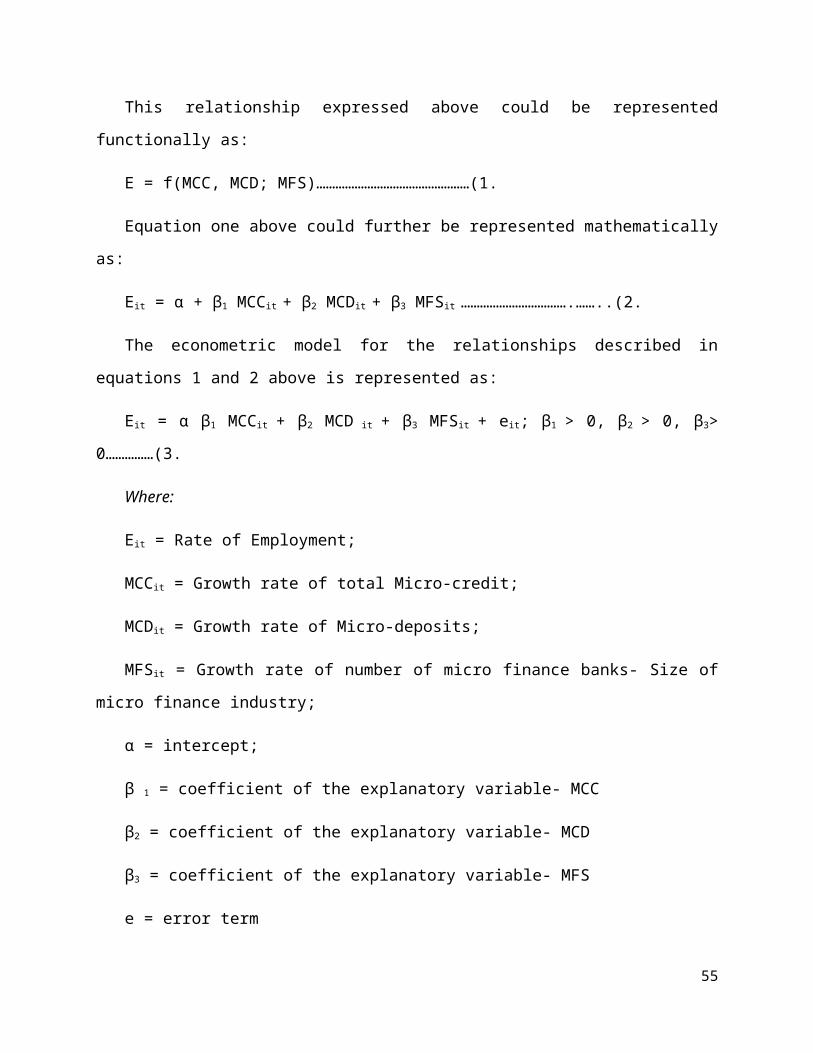

This relationship expressed above could be represented

functionally as:

E = f(MCC, MCD; MFS)…………………………………………(1.

Equation one above could further be represented mathematically

as:

Eit = α + β1 MCCit + β2 MCDit + β3 MFSit …………………………….……..(2.

The econometric model for the relationships described in

equations 1 and 2 above is represented as:

Eit = α β1 MCCit + β2 MCD it + β3 MFSit + eit; β1 > 0, β2 > 0, β3>

0……………(3.

Where:

Eit = Rate of Employment;

MCCit = Growth rate of total Micro-credit;

MCDit = Growth rate of Micro-deposits;

MFSit = Growth rate of number of micro finance banks- Size of

micro finance industry;

α = intercept;

β 1 = coefficient of the explanatory variable- MCC

β2 = coefficient of the explanatory variable- MCD

β3 = coefficient of the explanatory variable- MFS

e = error term

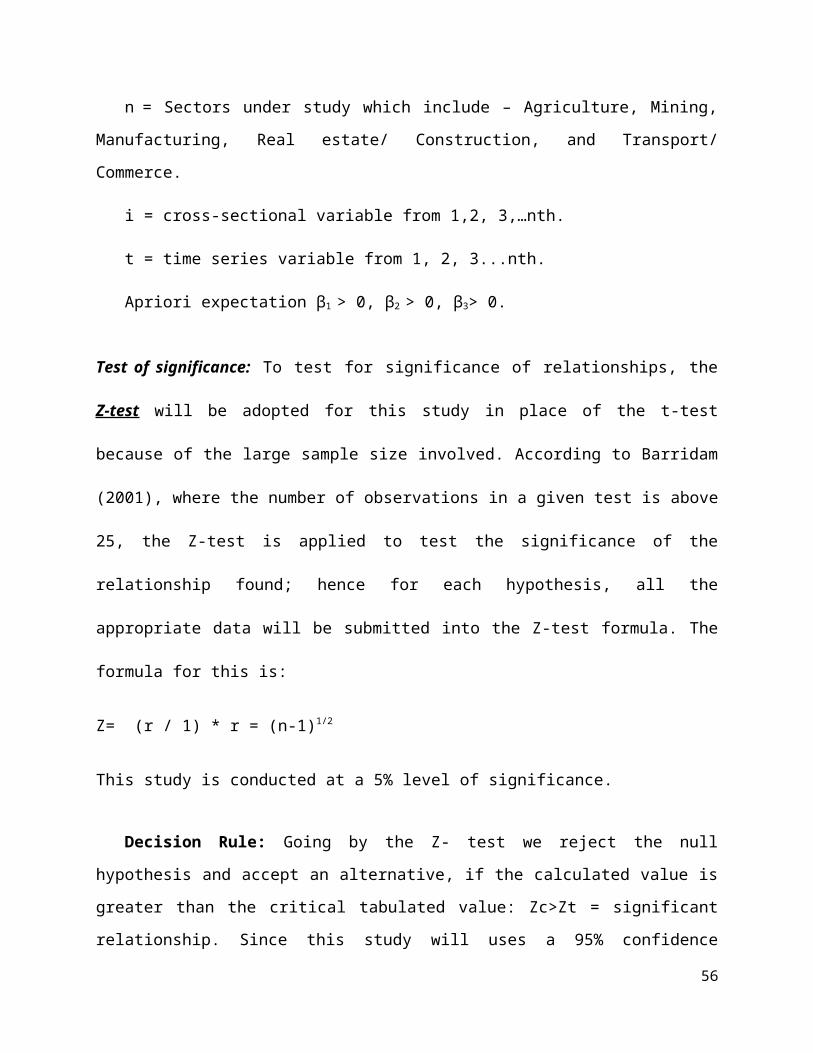

55

n = Sectors under study which include – Agriculture, Mining,

Manufacturing, Real estate/ Construction, and Transport/

Commerce.

i = cross-sectional variable from 1,2, 3,…nth.

t = time series variable from 1, 2, 3...nth.

Apriori expectation β1 > 0, β2 > 0, β3> 0.

Test of significance: To test for significance of relationships, the

Z-test will be adopted for this study in place of the t-test

because of the large sample size involved. According to Barridam

(2001), where the number of observations in a given test is above

25, the Z-test is applied to test the significance of the

relationship found; hence for each hypothesis, all the

appropriate data will be submitted into the Z-test formula. The

formula for this is:

Z= (r / 1) * r = (n-1)1/2

This study is conducted at a 5% level of significance.

Decision Rule: Going by the Z- test we reject the null

hypothesis and accept an alternative, if the calculated value is

greater than the critical tabulated value: Zc>Zt = significant

relationship. Since this study will uses a 95% confidence

56

interval; therefore the probability figure for the level of

significance of 0.05 is 1.64, which is our Zt. Therefore where

our Zc exceeds 1.64, the null hypothesis is rejected. This also

implies that if the Probability figure (Prob.) for our Zc exceeds

our 0.05 significance level, we reject the null hypothesis.

Therefore we state thus:

Reject null hypothesis when: Zc>Zt, or Prob. Value < significance value

CHAPTER 4

PRESENTATION AND ANALYSIS OF DATA

57

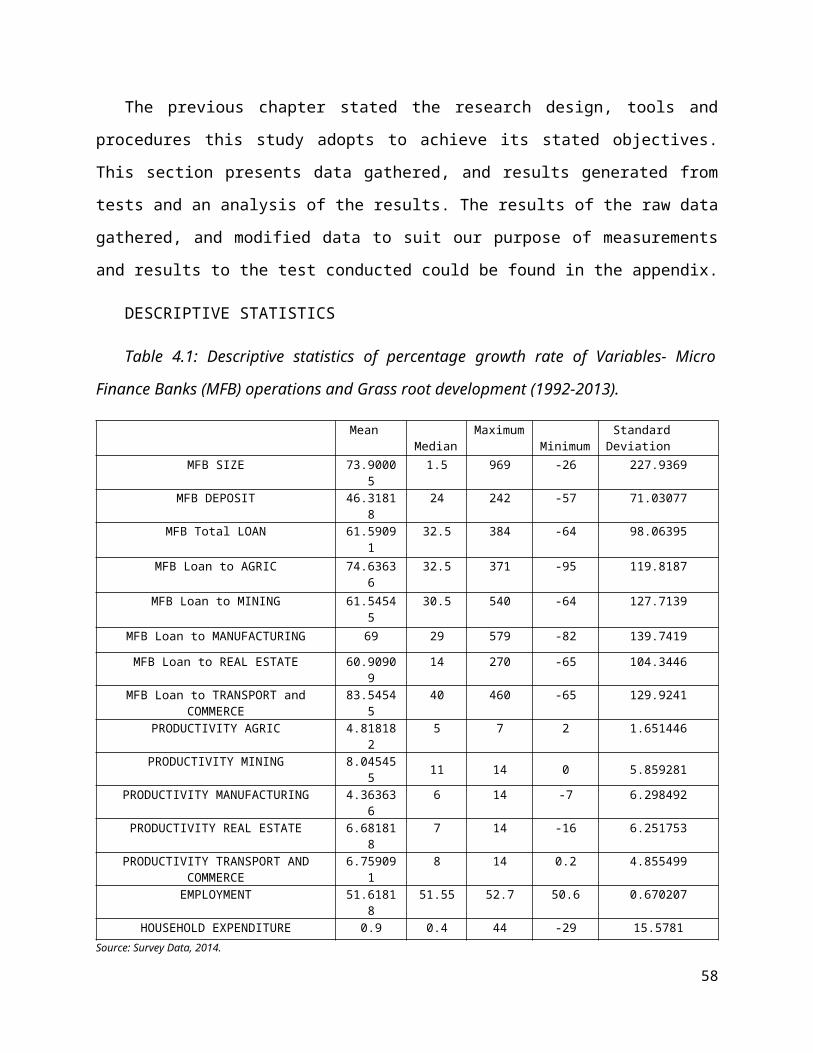

The previous chapter stated the research design, tools and

procedures this study adopts to achieve its stated objectives.

This section presents data gathered, and results generated from

tests and an analysis of the results. The results of the raw data

gathered, and modified data to suit our purpose of measurements

and results to the test conducted could be found in the appendix.

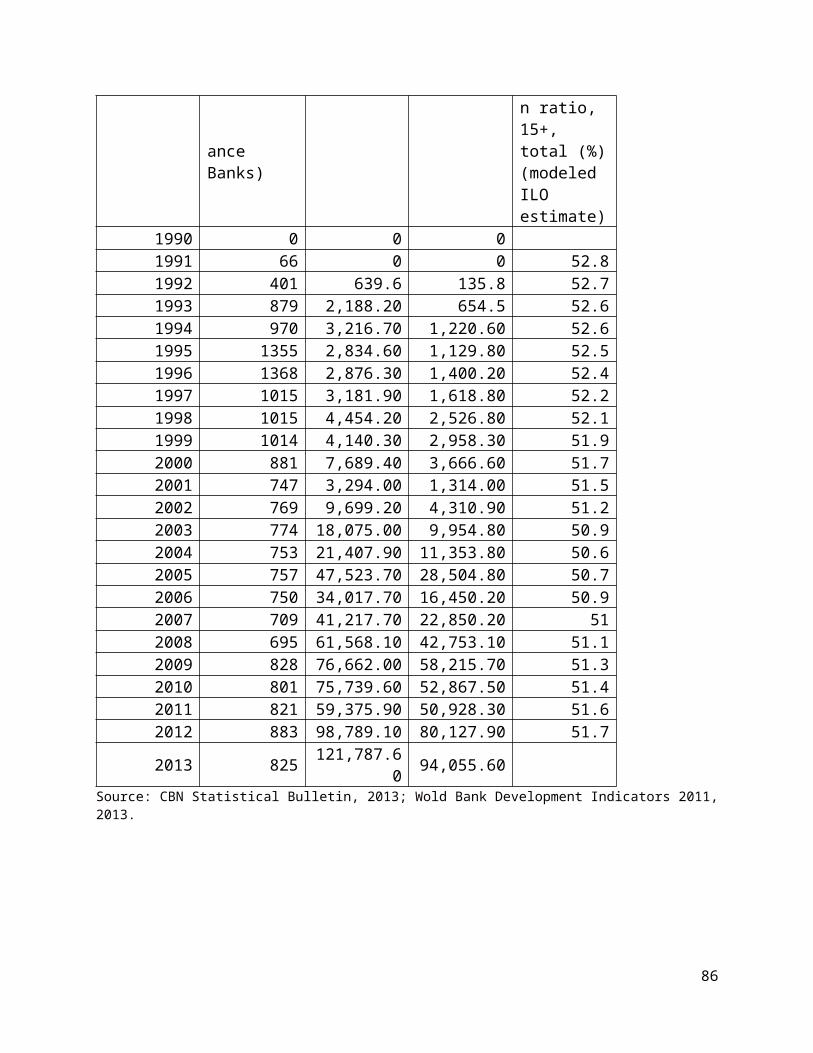

DESCRIPTIVE STATISTICS

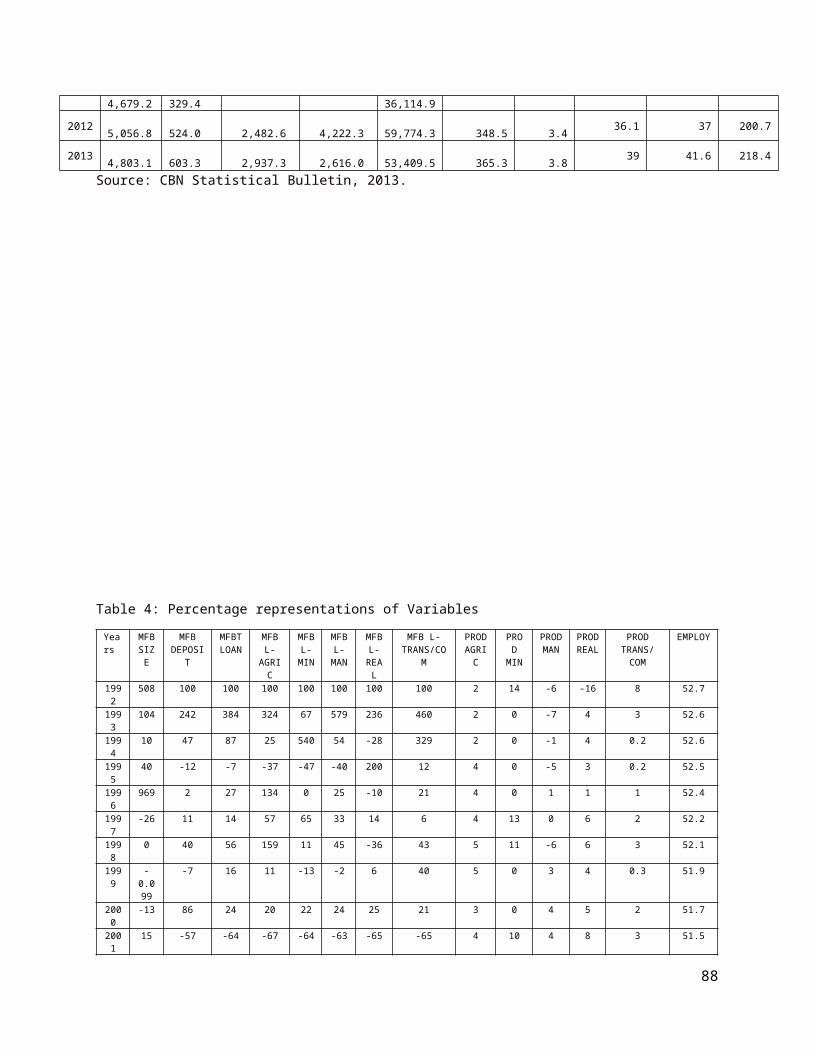

Table 4.1: Descriptive statistics of percentage growth rate of Variables- Micro

Finance Banks (MFB) operations and Grass root development (1992-2013).

Mean Median

Maximum Minimum

Standard Deviation

MFB SIZE 73.90005

1.5 969 -26 227.9369

MFB DEPOSIT 46.31818

24 242 -57 71.03077

MFB Total LOAN 61.59091

32.5 384 -64 98.06395

MFB Loan to AGRIC 74.63636

32.5 371 -95 119.8187

MFB Loan to MINING 61.54545

30.5 540 -64 127.7139

MFB Loan to MANUFACTURING 69 29 579 -82 139.7419

MFB Loan to REAL ESTATE 60.90909

14 270 -65 104.3446

MFB Loan to TRANSPORT andCOMMERCE

83.54545

40 460 -65 129.9241

PRODUCTIVITY AGRIC 4.818182

5 7 2 1.651446

PRODUCTIVITY MINING 8.045455 11 14 0 5.859281

PRODUCTIVITY MANUFACTURING 4.363636

6 14 -7 6.298492

PRODUCTIVITY REAL ESTATE 6.681818

7 14 -16 6.251753

PRODUCTIVITY TRANSPORT ANDCOMMERCE

6.759091

8 14 0.2 4.855499

EMPLOYMENT 51.61818

51.55 52.7 50.6 0.670207

HOUSEHOLD EXPENDITURE 0.9 0.4 44 -29 15.5781Source: Survey Data, 2014.

58

From the table above, MFB loans to Transport and Commerce

recorded the highest average growth rate of 83% within the

period, closely followed by MFB loan to Agriculture. House Hold

expenditure recorded the least average growth rate at 0.9%,

closely followed by Productivity in the Manufacturing sector out

of all our study variables. MFB size recorded the highest maximum

growth rate figure in the period among the variables. MFB size

recorded the most volatile growth rate of all the variable as

shown in its standard deviation figure; while employment rate

recorded the least deviations from its average.

Research Question 1: In what ways has micro financing increased

productivity in sectors where the grass root is economically active?

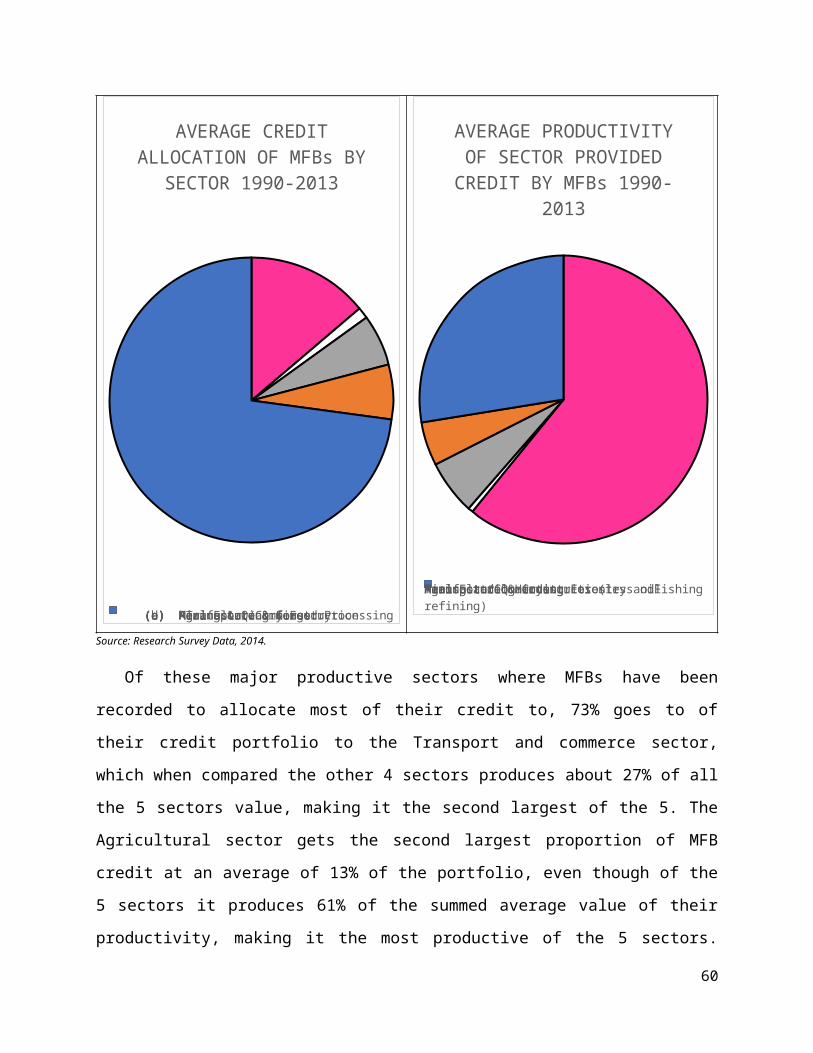

Figure 4.1: Comparison of MFB average apportioning of credit to sectors and thesector’s aggregate productivity.

59

AVERAGE CREDIT ALLOCATION OF MFBs BY

SECTOR 1990-2013

(a) Agriculture & forestry (b) Mining & Quarrying (c) Manufacturing & Food Processing (d) Real Estate & Construction (e) Transport/Commerce

AVERAGE PRODUCTIVITY OF SECTOR PROVIDED CREDIT BY MFBs 1990-

2013

Agricultural Hunting Forestry andFishingMining and QuarryingManufacturing industries (less oil refining)Real Estate & ConstructionTransport/Commerce

Source: Research Survey Data, 2014.

Of these major productive sectors where MFBs have been

recorded to allocate most of their credit to, 73% goes to of

their credit portfolio to the Transport and commerce sector,

which when compared the other 4 sectors produces about 27% of all

the 5 sectors value, making it the second largest of the 5. The

Agricultural sector gets the second largest proportion of MFB

credit at an average of 13% of the portfolio, even though of the

5 sectors it produces 61% of the summed average value of their

productivity, making it the most productive of the 5 sectors.

60

Mining gets the least proportion of MFBs credit of the 5 sectors

at 1.26%, and also produces only 0.44% of the summed average

value of the 5 sectors’ productivity. Manufacturing and Real

Estate/ Construction get average credit allocations of 5.9% and

6.23% respectively of the 5 sectors; and produce 6.15% and 4.96%

of the summed average value of the 5 sectors’ productivity.

Agricultural Sector and Micro finance:

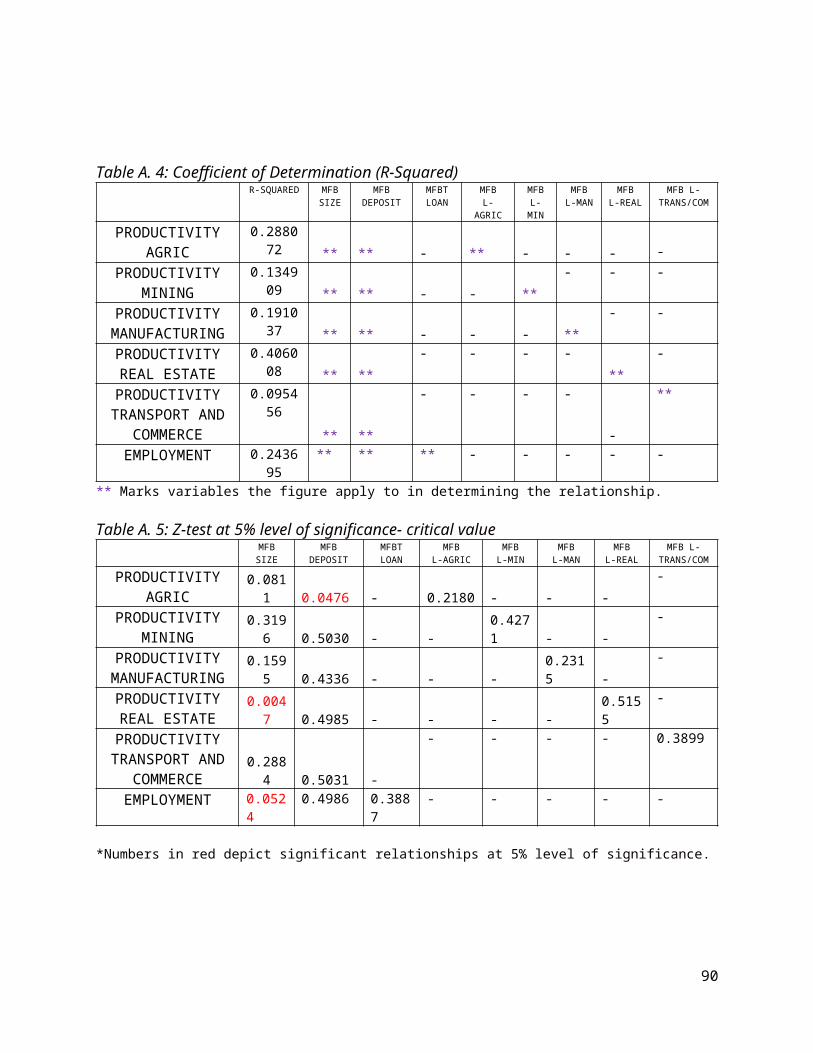

H01: Results from table A. 5 (Z test) showed that the Prob.

value of 0.218 which exceeds our critical value of 0.05. Going by

our decision rule, we accept the null hypothesis and state thus:

“Micro-credit has no significant impact on productivity in the

agricultural sector of Nigeria.”

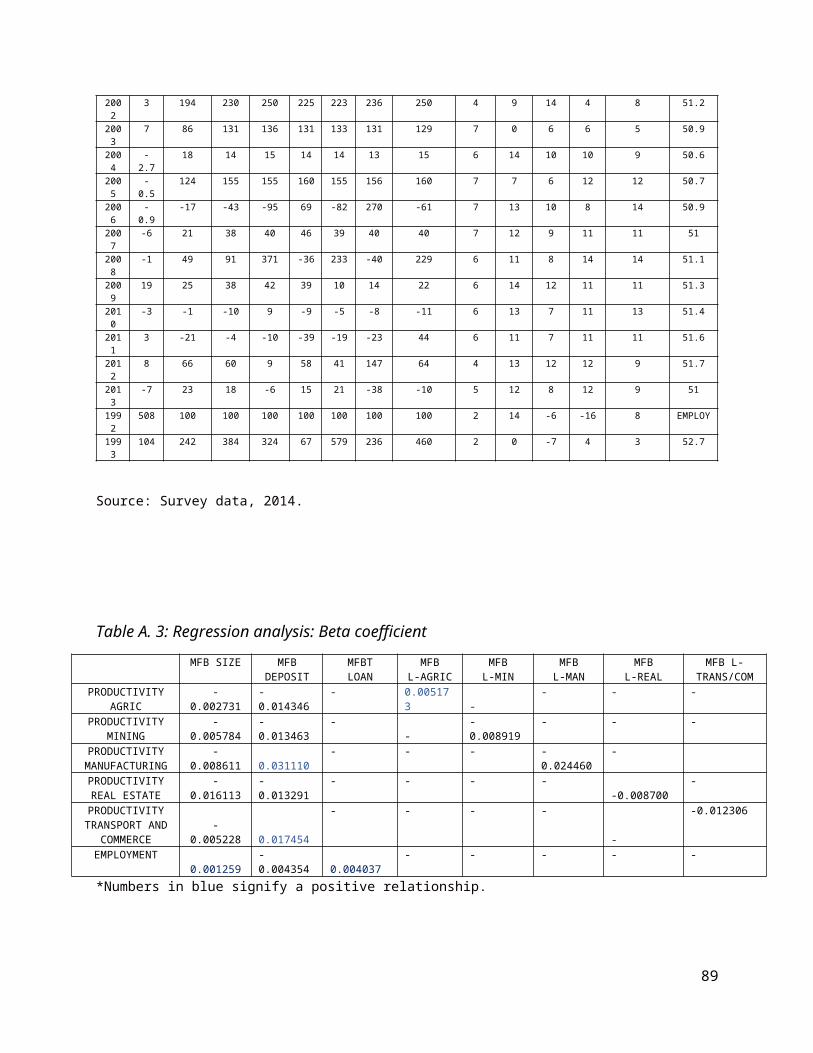

The regression analysis on Table A. 3 showed a Beta value of

0.005, which implies a positive relationship between Productivity

in Agriculture and MFB loans. This means that if MFB credit