1 © All rights reserved Please read Disclaimer on the back Impact of Interest Rate Changes on Banking Sector in Saudi Arabia Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

November 2015

1 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

November 2015

2 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

Contents

Executive Summary 4

Changes in interest rates and impact 5

Limited direct impact of Fed rate hike on Saudi economy 8

Impact on global economy could affect Saudi economy 8

Impact of rise in interest rates on treasury income, brokerage services, and investment banking income 12

Changes in interest rates to have mixed impact on business environment 14

APPENDIX 16

November 2015

3 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

List of FiguresFigure 1: GDP growth (developed markets) 5

Figure 2: GDP growth (emerging markets) 5

Figure 3: Unemployment rate (developed) 5

Figure 4: Unemployment rate (emerging) 5

Figure 5: Inflation (% chg.) (developed) 6

Figure 6: Inflation (% chg.) (emerging) 6

Figure 7: Different currencies versus USD (rebased to 100) 6

Figure 8: Interest (repo) rates (developed) 7

Figure 9: Interest (repo) rates (emerging) 7

Figure 10: Developed stock markets (rebased) 7

Figure 11: Emerging stock markets (rebased) 7

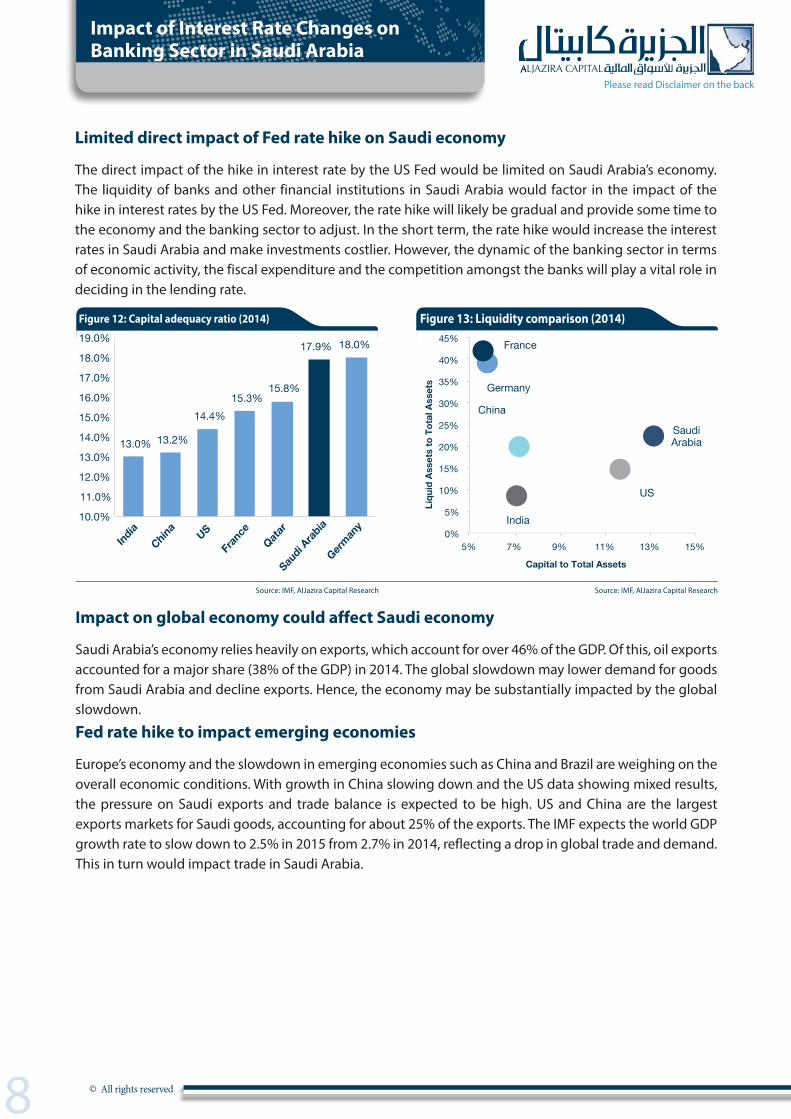

Figure 12: Capital adequacy ratio (2014) 8

Figure 13: Liquidity comparison (2014) 8

Figure 14: Saudi export share (2014) 9

Figure 15: GDP growth rates 9

Figure 16: Saudi Arabia exports 9

Figure 17: Saudi Arabia oil prices and budget 9

Figure 18: Saudi and US interest rates 10

Figure 19: Loan breakdown of Saudi banks as of 1H2015 10

Figure 20: Deposits breakdown of Saudi banks as of 1H2015 11

Figure 21: Loans-to-deposits ratio of Saudi banks 11

Figure 22: Investment banking and brokerage services income as % of income 12

Figure 23: Investment banking and brokerage services income as % of net income 12

Figure 24: Treasury income as % of total income 13

Figure 25: Treasury income as % of net income 14

Figure 26: Domestic credit to private sector (% of GDP) 14

Figure 27: Net FDI inflow (USD bn) 15

Figure 28: Net interest margin 15

November 2015

4 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

Executive Summary

• Economic developments across the globe have increased the need for sound domestic macroeconomic policies. This is important to avoid spillovers from policy decisions of advance economies such as the tapering of quantitative easing (QE) program by the US. After the closure of the QE program, the US is now expected to raise interest rates in the future, however judging the timing of the increase is dependent on a number of factors like inflation, unemployment rate, state of the economy and the geo political situation. Since the Saudi Arabian Riyal (SAR) is pegged against the US dollar (USD), the changes in the US interest rates will consequently result in parallel shift in the Saudi interest rates.

• Historically, interest rates have been used as a tool to influence various economic factors. For instance, by the beginning of 2009, major economies in the world were going through a recessionary phase. The GDP growth in all countries declined, while many countries witnessed high unemployment rate. Also, a few countries such as the US registered negative inflation (deflation). These factors forced the US government to cut down interest rates to boost economic growth, spur spending, reduce unemployment rates, and keep inflation at a reasonable level.

• The direct impact of the hike in interest rate by the US Fed would be limited on Saudi economy. The liquidity of banks and other financial institutions in Saudi Arabia would factor in the impact of the hike in interest rates by the US Fed. Moreover, the rate hike will likely be gradual and provide some time to the economy and the banking sector to adjust. However, in the short term, the rate hike would increase the interest rates in Saudi Arabia and make investments costlier.

• Saudi Arabia’s economy relies heavily on exports, which accounted for over 46% of the GDP (oil exports accounting for 38% of the GDP) in 2014. The decrease in oil prices and a global slowdown will impact the overall fiscal expenditure.

• As the US short-term interest rates are close to 0% since 2011 and long-term interest rates is at historical lows, SAIBOR and asset yield of the banks in Saudi Arabia have remained under pressure. Moreover, stiff competition in the country’s banking sector further constricted margins. However, due to the issue of the government bonds SAIBOR rates have started to rise. Along with that the rating cut by S&P (Standard and Poor) will put upward pressure on the discount rates, given the perceived higher risk profile of the company. We expect the banking sector’s asset yield to grow with the rate hike. Furthermore, banks with a higher share of corporate loans, high share or non-interest bearing deposits, and better liquidity would be benefitted to a greater extent.

• Although investment banking and brokerage services account for a lower share of income for the banking sector than other services, the segment would get impacted adversely through stock markets. The efficient treasury operations may negate the impact of the interest rate hike, however the challenge will be to manage the higher rate from foreign banks in light of the rating cut The bank’s income from fees could decline due to low transaction volumes.

• Changes in interest rates would have a mixed effect on the banking sector. The increase in interest rates would decrease domestic credit in the economy and reduce consumption and output, yet it would improve foreign investment and balance of trade. It is also expected to improve the net interest margins of banks. However, we believe that Saudi Arabian Monetary Agency (SAMA) would be cautious to respond to any such changes in interest rates, keeping in mind that the current decline in oil prices could weigh on the domestic economy.

November 2015

5 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

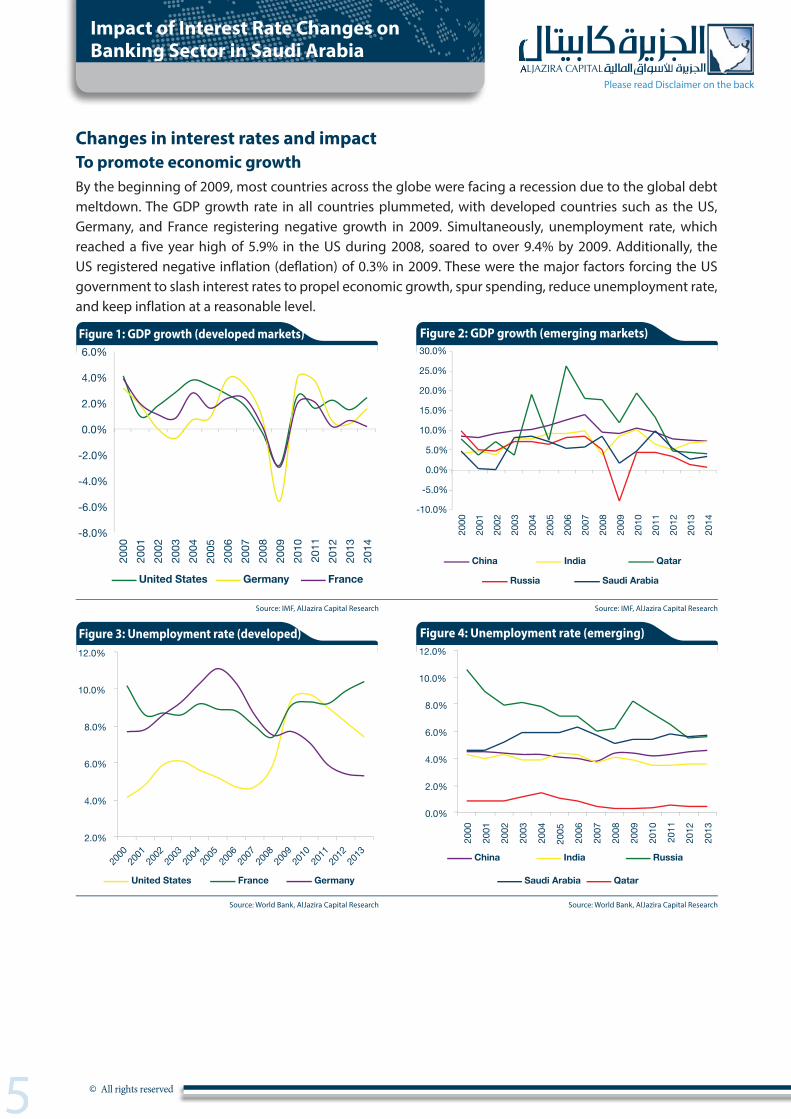

Changes in interest rates and impactTo promote economic growthBy the beginning of 2009, most countries across the globe were facing a recession due to the global debt meltdown. The GDP growth rate in all countries plummeted, with developed countries such as the US, Germany, and France registering negative growth in 2009. Simultaneously, unemployment rate, which reached a five year high of 5.9% in the US during 2008, soared to over 9.4% by 2009. Additionally, the US registered negative inflation (deflation) of 0.3% in 2009. These were the major factors forcing the US government to slash interest rates to propel economic growth, spur spending, reduce unemployment rate, and keep inflation at a reasonable level.

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2014

United States Germany France China India Qatar

Russia Saudi Arabia

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Figure 1: GDP growth (developed markets) Figure 2: GDP growth (emerging markets)

Source: IMF, AlJazira Capital ResearchSource: IMF, AlJazira Capital Research

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2000

20

01 20

02 20

03 20

04 20

05 20

06 20

07 20

08 20

09 20

10 20

11 20

12 20

13

United States France Germany

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

China India Russia

Saudi Arabia Qatar

Figure 3: Unemployment rate (developed) Figure 4: Unemployment rate (emerging)

Source: World Bank, AlJazira Capital ResearchSource: World Bank, AlJazira Capital Research

November 2015

6 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

Spillover of interest rate changes to currencies

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

EUR RUB CNY INR QAR SAR

Figure 7: Di�erent currencies versus USD (rebased to 100)

Source: Reuter Eikon, AlJazira Capital Research

-1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5%

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2014

United States Germany France

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

China India Qatar

Russia Saudi Arabia

Figure 5: In�ation (% chg.) (developed) Figure 6: In�ation (% chg.) (emerging)

Source: IMF, AlJazira Capital ResearchSource: IMF, AlJazira Capital Research

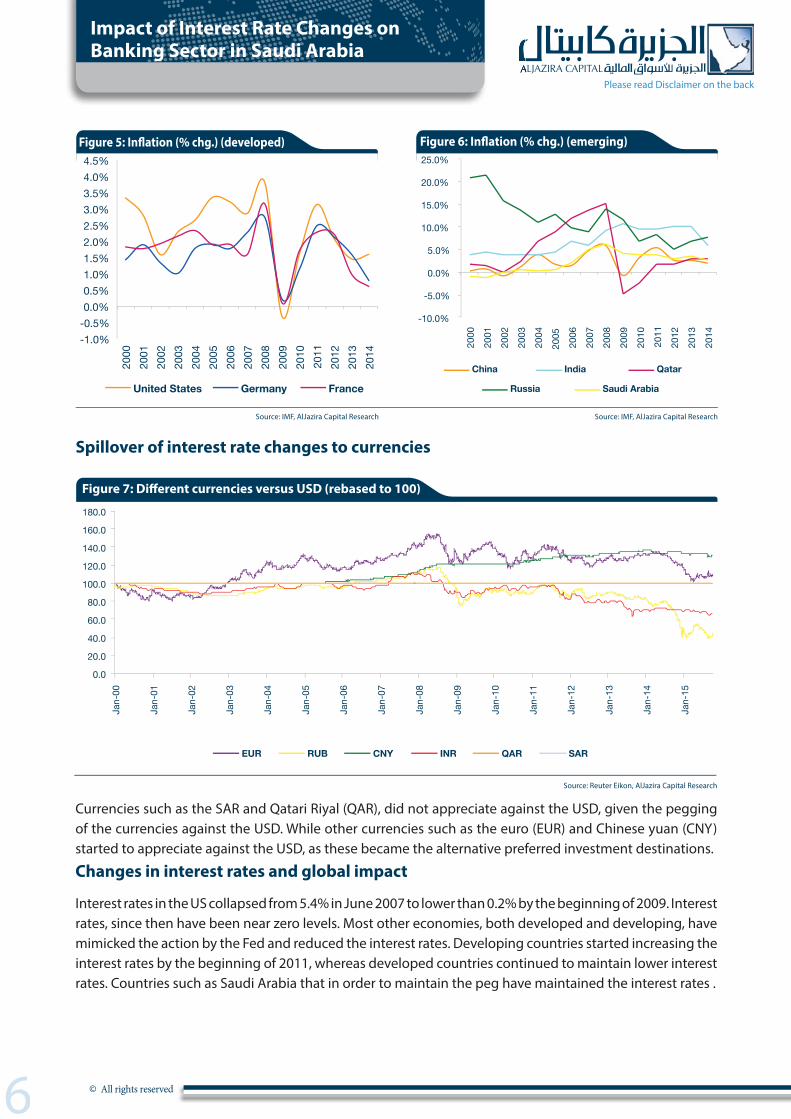

Currencies such as the SAR and Qatari Riyal (QAR), did not appreciate against the USD, given the pegging of the currencies against the USD. While other currencies such as the euro (EUR) and Chinese yuan (CNY) started to appreciate against the USD, as these became the alternative preferred investment destinations.

Changes in interest rates and global impact

Interest rates in the US collapsed from 5.4% in June 2007 to lower than 0.2% by the beginning of 2009. Interest rates, since then have been near zero levels. Most other economies, both developed and developing, have mimicked the action by the Fed and reduced the interest rates. Developing countries started increasing the interest rates by the beginning of 2011, whereas developed countries continued to maintain lower interest rates. Countries such as Saudi Arabia that in order to maintain the peg have maintained the interest rates .

November 2015

7 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

United States Germany France

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

India China Russia

Qatar Saudi Arabia

Figure 8: Interest (repo) rates (developed) Figure 9: Interest (repo) rates (emerging)

Source: Bloomberg, AlJazira Capital ResearchSource: Bloomberg, AlJazira Capital Research

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

Oct

-00

Oct

-01

Oct

-02

Oct

-03

Oct

-04

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

NASDAQ DAX CAC40

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0 O

ct-0

0

Oct

-01

Oct

-02

Oct

-03

Oct

-04

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Nifty SSE MICEX

DSM TADAWUL

Figure 10: Developed stock markets (rebased) Figure 11: Emerging stock markets (rebased)

Source: Bloomberg, AlJazira Capital ResearchSource: Bloomberg, AlJazira Capital Research

As the investors looking for better returns moved to the emerging markets, the flow of foreign funds (debt and equity) into the developing markets such as India, Russia, and China increased. This is also evident from the fact that the developing markets have performed better and provided better returns than the developed markets. Markets in the GCC region too showcased good performance during the period.

Direct or indirect impact on banking sector Low interest rates prove beneficial to lenders for a short short span of time,given the higher lending activity. However the deposit rates are decreased at a much slower rate, as the banks try to attract more depositors, to take advantage of the high lending activity, consequently resulting in lower NIMs. This shrank the net interest margins (NIM) for banks in the US from around 4.0% in 2008 to around 3.2% in 2013. Countries such as Saudi Arabia and Qatar that have their currencies pegged against the USD are directly impacted by the changes in interest rates because these countries have very limited options and have to change interest rates in tandem with the US to maintain the currency peg. Consequently, the NIM in Saudi Arabia declined from 3.3% in 2008 to about 2.7% in 2013. The changes in the US interest rates do not impact the emerging economies (currencies are not pegged to the USD) directly, but it impacts indirectly through capital markets. As the interest rates in the US and other developed economies decrease, investors seeking higher returns move to the emerging markets. Furthermore, the NIM in different countries did not showcase any direct relation due to other factors such as competition among banks, different business models for banks, and proportion of interest income to the total income earned by banks.

November 2015

8 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

13.0% 13.2%

14.4% 15.3%

15.8%

17.9% 18.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

18.0%

19.0%

India

China

US

Fran

ce

Qatar

Saudi

Arabia

German

y India

China

US

France

Saudi Arabia

Germany

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

5% 7% 9% 11% 13% 15%

Liqu

id A

sset

s to

Tot

al A

sset

s

Capital to Total Assets

Figure 12: Capital adequacy ratio (2014) Figure 13: Liquidity comparison (2014)

Source: IMF, AlJazira Capital ResearchSource: IMF, AlJazira Capital Research

Impact on global economy could affect Saudi economy

Saudi Arabia’s economy relies heavily on exports, which account for over 46% of the GDP. Of this, oil exports accounted for a major share (38% of the GDP) in 2014. The global slowdown may lower demand for goods from Saudi Arabia and decline exports. Hence, the economy may be substantially impacted by the global slowdown.

Fed rate hike to impact emerging economies

Europe’s economy and the slowdown in emerging economies such as China and Brazil are weighing on the overall economic conditions. With growth in China slowing down and the US data showing mixed results, the pressure on Saudi exports and trade balance is expected to be high. US and China are the largest exports markets for Saudi goods, accounting for about 25% of the exports. The IMF expects the world GDP growth rate to slow down to 2.5% in 2015 from 2.7% in 2014, reflecting a drop in global trade and demand. This in turn would impact trade in Saudi Arabia.

Limited direct impact of Fed rate hike on Saudi economy

The direct impact of the hike in interest rate by the US Fed would be limited on Saudi Arabia’s economy. The liquidity of banks and other financial institutions in Saudi Arabia would factor in the impact of the hike in interest rates by the US Fed. Moreover, the rate hike will likely be gradual and provide some time to the economy and the banking sector to adjust. In the short term, the rate hike would increase the interest rates in Saudi Arabia and make investments costlier. However, the dynamic of the banking sector in terms of economic activity, the fiscal expenditure and the competition amongst the banks will play a vital role in deciding in the lending rate.

November 2015

9 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

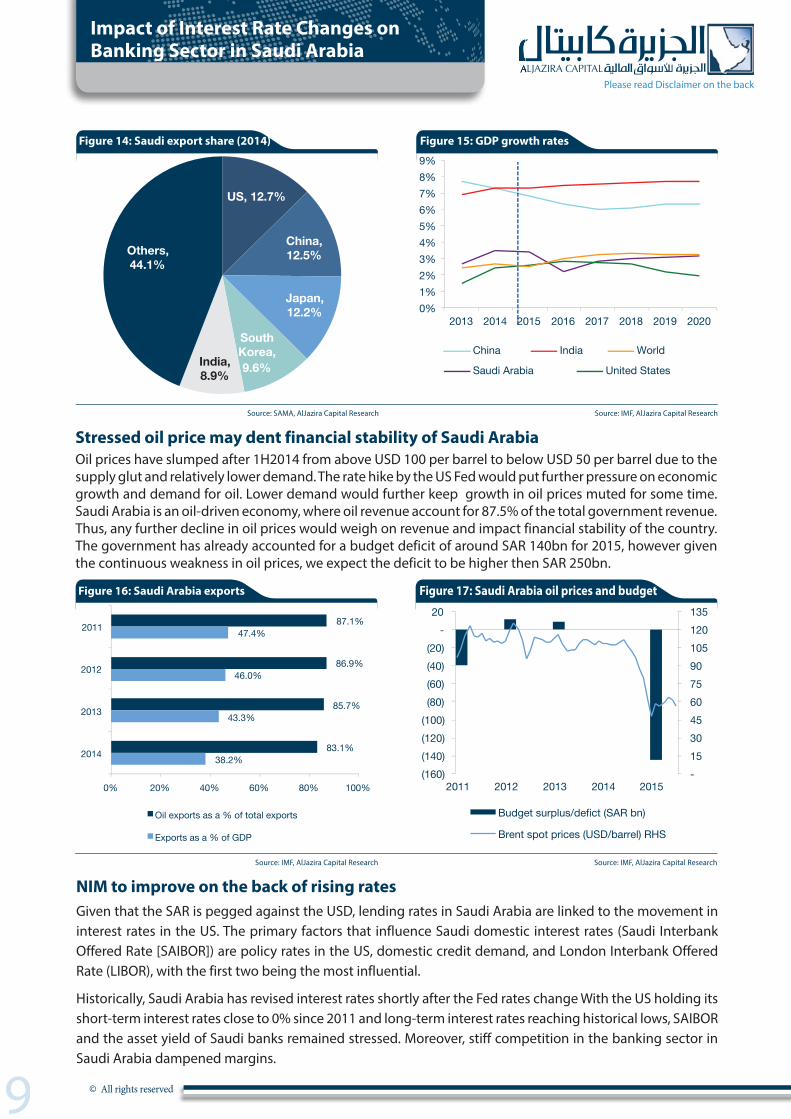

US, 12.7%

China, 12.5%

Japan, 12.2%

South Korea, 9.6% India,

8.9%

Others, 44.1%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

2013 2014 2015 2016 2017 2018 2019 2020

China India

Saudi Arabia United States

World

Figure 14: Saudi export share (2014) Figure 15: GDP growth rates

Source: IMF, AlJazira Capital ResearchSource: SAMA, AlJazira Capital Research

Stressed oil price may dent financial stability of Saudi ArabiaOil prices have slumped after 1H2014 from above USD 100 per barrel to below USD 50 per barrel due to the supply glut and relatively lower demand. The rate hike by the US Fed would put further pressure on economic growth and demand for oil. Lower demand would further keep growth in oil prices muted for some time. Saudi Arabia is an oil-driven economy, where oil revenue account for 87.5% of the total government revenue. Thus, any further decline in oil prices would weigh on revenue and impact financial stability of the country. The government has already accounted for a budget deficit of around SAR 140bn for 2015, however given the continuous weakness in oil prices, we expect the deficit to be higher then SAR 250bn.

NIM to improve on the back of rising ratesGiven that the SAR is pegged against the USD, lending rates in Saudi Arabia are linked to the movement in interest rates in the US. The primary factors that influence Saudi domestic interest rates (Saudi Interbank Offered Rate [SAIBOR]) are policy rates in the US, domestic credit demand, and London Interbank Offered Rate (LIBOR), with the first two being the most influential.

Historically, Saudi Arabia has revised interest rates shortly after the Fed rates change With the US holding its short-term interest rates close to 0% since 2011 and long-term interest rates reaching historical lows, SAIBOR and the asset yield of Saudi banks remained stressed. Moreover, stiff competition in the banking sector in Saudi Arabia dampened margins.

87.1%

86.9%

85.7%

83.1%

47.4%

46.0%

43.3%

38.2%

0% 20% 40% 60% 80% 100%

2011

2012

2013

2014

Oil exports as a % of total exports

Exports as a % of GDP

- 15 30 45 60 75 90 105 120 135

(160) (140) (120) (100) (80) (60) (40) (20)

- 20

2011 2012 2013 2014 2015

Budget surplus/defict (SAR bn)

Brent spot prices (USD/barrel) RHS

Figure 16: Saudi Arabia exports Figure 17: Saudi Arabia oil prices and budget

Source: IMF, AlJazira Capital ResearchSource: IMF, AlJazira Capital Research

November 2015

10 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

We expect the asset yield from the banking sector in Saudi Arabia to grow with the Fed rate hike. However, the growth rate and the extent of benefits would depend on the following parameters:

• Bank’s loan mix

• Non-interest bearing (NIB) loans contribution

• Balance sheet liquidity

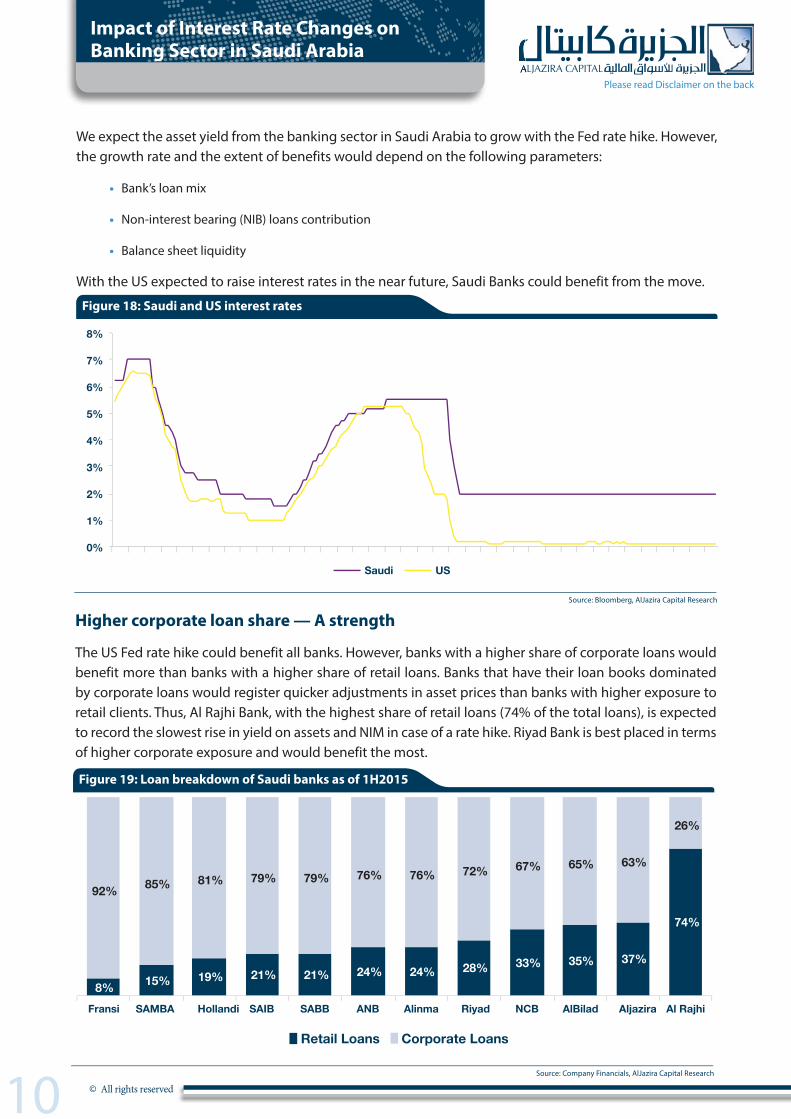

With the US expected to raise interest rates in the near future, Saudi Banks could benefit from the move.

Higher corporate loan share — A strength

The US Fed rate hike could benefit all banks. However, banks with a higher share of corporate loans would benefit more than banks with a higher share of retail loans. Banks that have their loan books dominated by corporate loans would register quicker adjustments in asset prices than banks with higher exposure to retail clients. Thus, Al Rajhi Bank, with the highest share of retail loans (74% of the total loans), is expected to record the slowest rise in yield on assets and NIM in case of a rate hike. Riyad Bank is best placed in terms of higher corporate exposure and would benefit the most.

0%

1%

2%

3%

4%

5%

6%

7%

8%

Saudi US

Figure 18: Saudi and US interest rates

Source: Bloomberg, AlJazira Capital Research

8% 15% 19% 21% 21% 24% 24% 28% 33% 35% 37%

74%

92% 85% 81% 79% 79% 76% 76% 72% 67% 65% 63%

26%

Fransi SAMBA Hollandi SAIB SABB ANB Alinma Riyad NCB AlBilad Aljazira Al Rajhi

Retail Loans Corporate Loans

Figure 19: Loan breakdown of Saudi banks as of 1H2015

Source: Company Financials, AlJazira Capital Research

November 2015

11 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

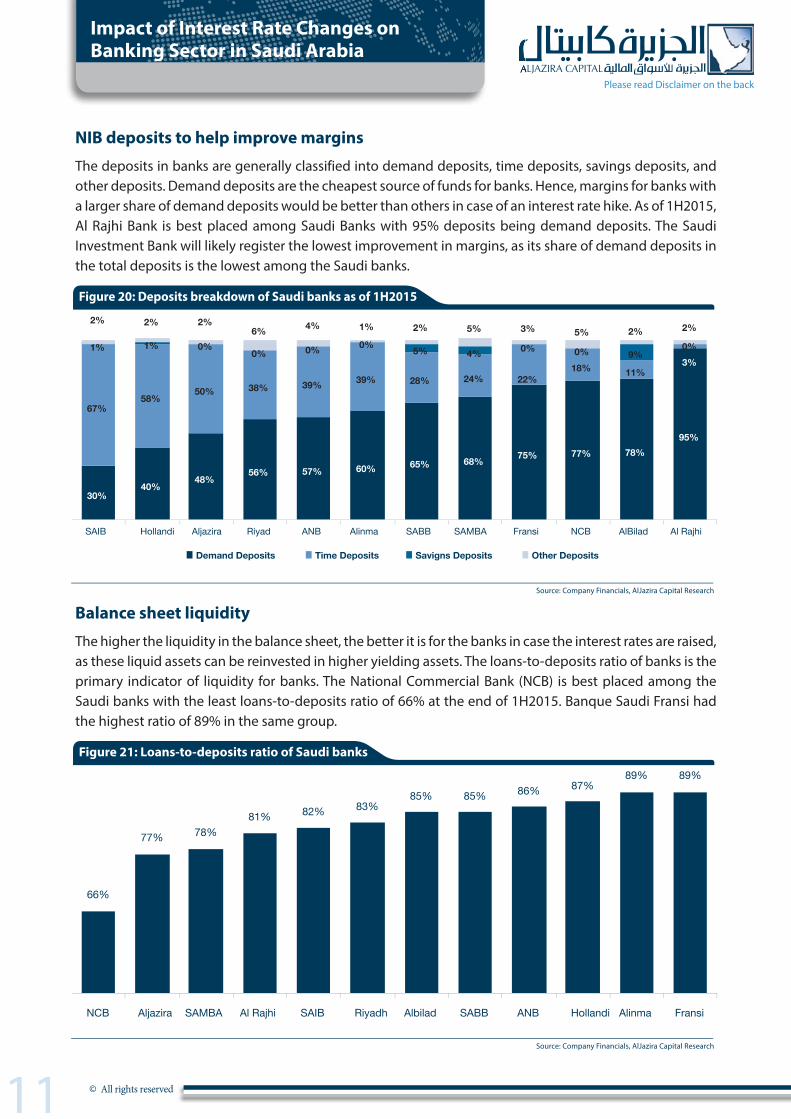

NIB deposits to help improve margins

The deposits in banks are generally classified into demand deposits, time deposits, savings deposits, and other deposits. Demand deposits are the cheapest source of funds for banks. Hence, margins for banks with a larger share of demand deposits would be better than others in case of an interest rate hike. As of 1H2015, Al Rajhi Bank is best placed among Saudi Banks with 95% deposits being demand deposits. The Saudi Investment Bank will likely register the lowest improvement in margins, as its share of demand deposits in the total deposits is the lowest among the Saudi banks.

30% 40%

48% 56% 57% 60% 65% 68% 75% 77% 78%

95%

67% 58%

50% 38% 39% 39% 28% 24% 22% 18% 11%

3% 1% 1% 0%

0% 0% 0% 5% 4% 0% 0% 9% 0%

2% 2% 2% 6% 4% 1% 2% 5% 3% 5% 2% 2%

SAIB Hollandi Aljazira Riyad ANB Alinma SABB SAMBA Fransi NCB AlBilad Al Rajhi

Demand Deposits Time Deposits Savigns Deposits Other Deposits

Figure 20: Deposits breakdown of Saudi banks as of 1H2015

Source: Company Financials, AlJazira Capital Research

Balance sheet liquidity

The higher the liquidity in the balance sheet, the better it is for the banks in case the interest rates are raised, as these liquid assets can be reinvested in higher yielding assets. The loans-to-deposits ratio of banks is the primary indicator of liquidity for banks. The National Commercial Bank (NCB) is best placed among the Saudi banks with the least loans-to-deposits ratio of 66% at the end of 1H2015. Banque Saudi Fransi had the highest ratio of 89% in the same group.

66%

77% 78% 81% 82% 83%

85% 85% 86% 87% 89% 89%

NCB Aljazira SAMBA Al Rajhi SAIB Riyadh Albilad SABB ANB Hollandi Alinma Fransi

Figure 21: Loans-to-deposits ratio of Saudi banks

Source: Company Financials, AlJazira Capital Research

November 2015

12 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

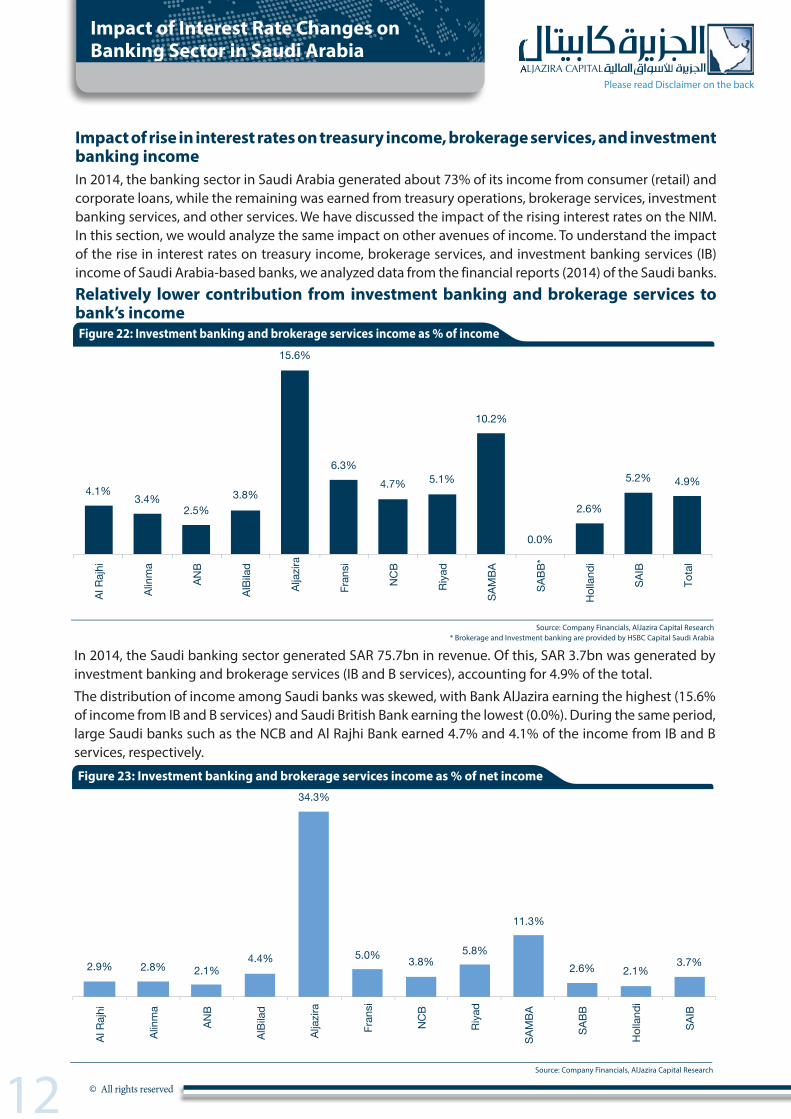

Impact of rise in interest rates on treasury income, brokerage services, and investment banking incomeIn 2014, the banking sector in Saudi Arabia generated about 73% of its income from consumer (retail) and corporate loans, while the remaining was earned from treasury operations, brokerage services, investment banking services, and other services. We have discussed the impact of the rising interest rates on the NIM. In this section, we would analyze the same impact on other avenues of income. To understand the impact of the rise in interest rates on treasury income, brokerage services, and investment banking services (IB) income of Saudi Arabia-based banks, we analyzed data from the financial reports (2014) of the Saudi banks.

Relatively lower contribution from investment banking and brokerage services to bank’s income

In 2014, the Saudi banking sector generated SAR 75.7bn in revenue. Of this, SAR 3.7bn was generated by investment banking and brokerage services (IB and B services), accounting for 4.9% of the total.

The distribution of income among Saudi banks was skewed, with Bank AlJazira earning the highest (15.6% of income from IB and B services) and Saudi British Bank earning the lowest (0.0%). During the same period, large Saudi banks such as the NCB and Al Rajhi Bank earned 4.7% and 4.1% of the income from IB and B services, respectively.

4.1% 3.4%

2.5% 3.8%

15.6%

6.3% 4.7% 5.1%

10.2%

0.0%

2.6%

5.2% 4.9%

Al R

ajhi

Alin

ma

ANB

AlBi

lad

Alja

zira

Fran

si

NC

B

Riya

d

SAM

BA

SABB

*

Hol

land

i

SAIB

Tota

l

2.9% 2.8% 2.1% 4.4%

34.3%

5.0% 3.8% 5.8%

11.3%

2.6% 2.1% 3.7%

Al R

ajhi

Alin

ma

ANB

AlBi

lad

Alja

zira

Fran

si

NC

B

Riya

d

SAM

BA

SABB

Hol

land

i

SAIB

Figure 22: Investment banking and brokerage services income as % of income

Figure 23: Investment banking and brokerage services income as % of net income

Source: Company Financials, AlJazira Capital Research* Brokerage and Investment banking are provided by HSBC Capital Saudi Arabia

Source: Company Financials, AlJazira Capital Research

November 2015

13 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

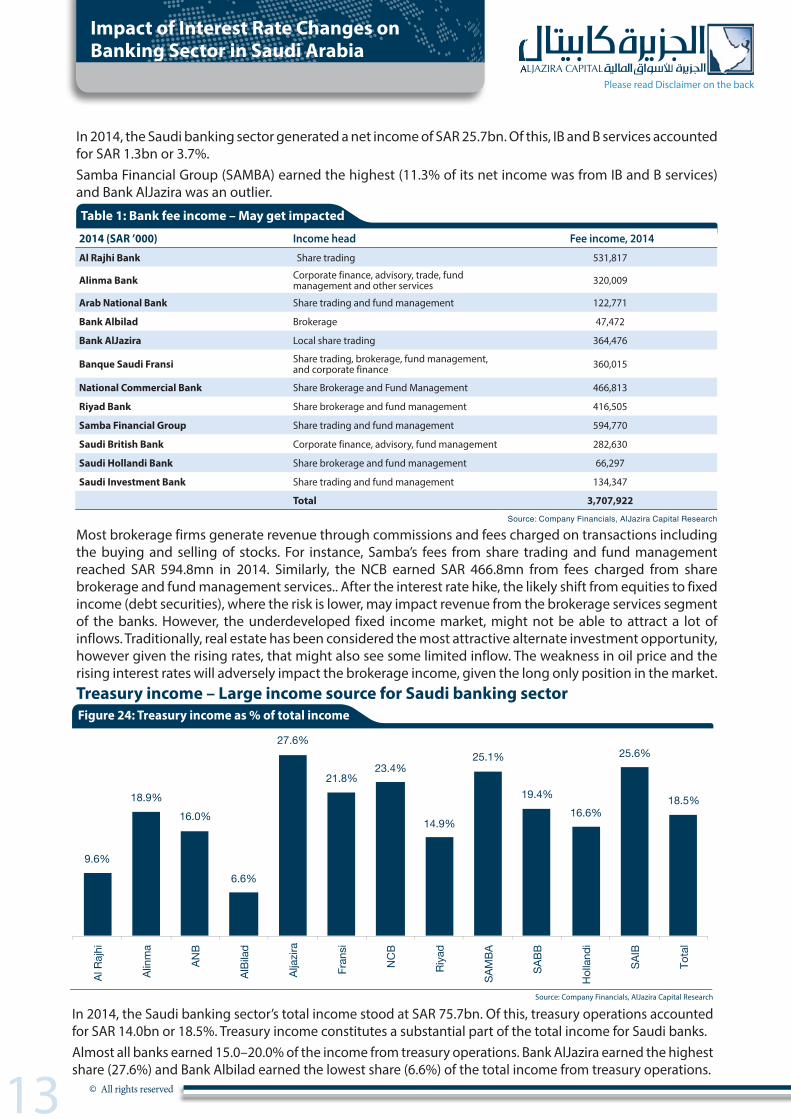

In 2014, the Saudi banking sector generated a net income of SAR 25.7bn. Of this, IB and B services accounted for SAR 1.3bn or 3.7%.Samba Financial Group (SAMBA) earned the highest (11.3% of its net income was from IB and B services) and Bank AlJazira was an outlier.

Most brokerage firms generate revenue through commissions and fees charged on transactions including the buying and selling of stocks. For instance, Samba’s fees from share trading and fund management reached SAR 594.8mn in 2014. Similarly, the NCB earned SAR 466.8mn from fees charged from share brokerage and fund management services.. After the interest rate hike, the likely shift from equities to fixed income (debt securities), where the risk is lower, may impact revenue from the brokerage services segment of the banks. However, the underdeveloped fixed income market, might not be able to attract a lot of inflows. Traditionally, real estate has been considered the most attractive alternate investment opportunity, however given the rising rates, that might also see some limited inflow. The weakness in oil price and the rising interest rates will adversely impact the brokerage income, given the long only position in the market.Treasury income – Large income source for Saudi banking sector

In 2014, the Saudi banking sector’s total income stood at SAR 75.7bn. Of this, treasury operations accounted for SAR 14.0bn or 18.5%. Treasury income constitutes a substantial part of the total income for Saudi banks.Almost all banks earned 15.0–20.0% of the income from treasury operations. Bank AlJazira earned the highest share (27.6%) and Bank Albilad earned the lowest share (6.6%) of the total income from treasury operations.

2014 (SAR ’000) Income head Fee income, 2014

Al Rajhi Bank Share trading 531,817

Alinma Bank Corporate finance, advisory, trade, fund management and other services 320,009

Arab National Bank Share trading and fund management 122,771

Bank Albilad Brokerage 47,472

Bank AlJazira Local share trading 364,476

Banque Saudi Fransi Share trading, brokerage, fund management, and corporate finance 360,015

National Commercial Bank Share Brokerage and Fund Management 466,813

Riyad Bank Share brokerage and fund management 416,505

Samba Financial Group Share trading and fund management 594,770

Saudi British Bank Corporate finance, advisory, fund management 282,630

Saudi Hollandi Bank Share brokerage and fund management 66,297

Saudi Investment Bank Share trading and fund management 134,347

Total 3,707,922

Source: Company Financials, AlJazira Capital Research

Table 1: Bank fee income – May get impacted

9.6%

18.9% 16.0%

6.6%

27.6%

21.8% 23.4%

14.9%

25.1%

19.4% 16.6%

25.6%

18.5%

Al R

ajhi

Alin

ma

ANB

AlBi

lad

Alja

zira

Fran

si

NC

B

Riya

d

SAM

BA

SABB

Hol

land

i

SAIB

Tota

l

Figure 24: Treasury income as % of total income

Source: Company Financials, AlJazira Capital Research

November 2015

14 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

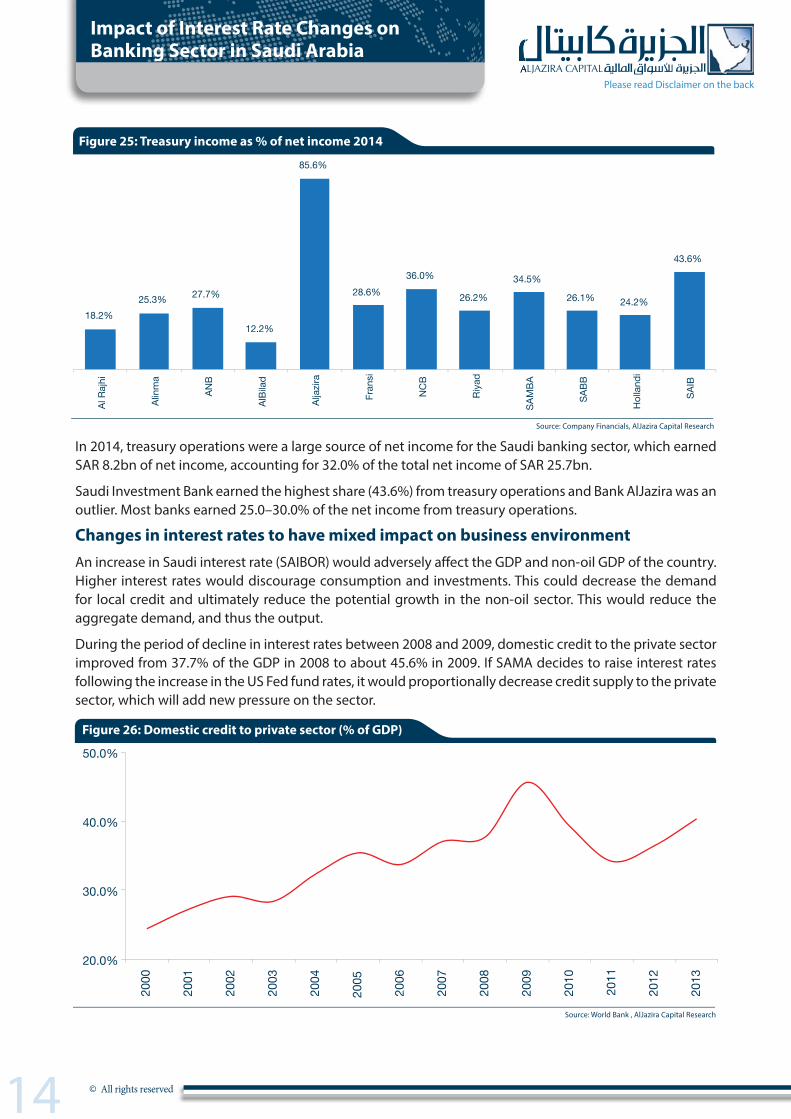

In 2014, treasury operations were a large source of net income for the Saudi banking sector, which earned SAR 8.2bn of net income, accounting for 32.0% of the total net income of SAR 25.7bn.

Saudi Investment Bank earned the highest share (43.6%) from treasury operations and Bank AlJazira was an outlier. Most banks earned 25.0–30.0% of the net income from treasury operations.

Changes in interest rates to have mixed impact on business environment An increase in Saudi interest rate (SAIBOR) would adversely affect the GDP and non-oil GDP of the country. Higher interest rates would discourage consumption and investments. This could decrease the demand for local credit and ultimately reduce the potential growth in the non-oil sector. This would reduce the aggregate demand, and thus the output.

During the period of decline in interest rates between 2008 and 2009, domestic credit to the private sector improved from 37.7% of the GDP in 2008 to about 45.6% in 2009. If SAMA decides to raise interest rates following the increase in the US Fed fund rates, it would proportionally decrease credit supply to the private sector, which will add new pressure on the sector.

18.2% 25.3% 27.7%

12.2%

85.6%

28.6% 36.0%

26.2%

34.5%

26.1% 24.2%

43.6%

Al R

ajhi

Alin

ma

ANB

AlBi

lad

Alja

zira

Fran

si

NC

B

Riya

d

SAM

BA

SABB

Hol

land

i

SAIB

Figure 25: Treasury income as % of net income 2014

Source: Company Financials, AlJazira Capital Research

20.0%

30.0%

40.0%

50.0%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Figure 26: Domestic credit to private sector (% of GDP)

Source: World Bank , AlJazira Capital Research

November 2015

15 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

On the positive side, higher interest rates would attract higher foreign investments (FDI) into the country. This can be affirmed from the fact that the lowering of the interest rate reduced the FDI in Saudi from USD 39bn in 2008 to about USD 8.9bn in 2013. As Saudi Arabia has an oil-driven economy and the majority of the revenue comes from oil exports, these revenues are in USD (as oil contracts are signed in USD). Higher interest rates would mean higher value for the USD earned. This in turn would help increase the trade balance of Saudi Arabia. It is evident from the fact that there was a sharp decline in the balance of trade from 28.1% of the GDP in 2008 to 9.1% of the GDP in 2009 (period when the interest rates declined). The increase in interest rates would also help improve the NIM of Saudi banks, which declined from 3.3% in 2008 to 2.7% in 2013.

The slow global recovery and falling import costs (ascribed to a strengthening USD) compels us to believe that the inflationary pressure would be muted by external influences and interest rate hikes would further pull down prices. However, we believe that SAMA would be cautious to respond to any such changes in interest rates, keeping in mind that the current decline in oil prices is likely to slow down the domestic economy.

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2000

20

01 20

02 20

03 20

04 20

05 20

06 20

07 20

08 20

09 20

10 20

11 20

12 20

13

2.5%

3.0%

3.5%

4.0%

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Figure 27: Net FDI in�ow (USD bn) Figure 28: Net interest margin

Source: Federal Reserve Bank of St. Louis, AlJazira Capital ResearchSource: World Bank, AlJazira Capital Research

November 2015

16 © All rights reserved

Please read Disclaimer on the back

Impact of Interest Rate Changes on Banking Sector in Saudi Arabia

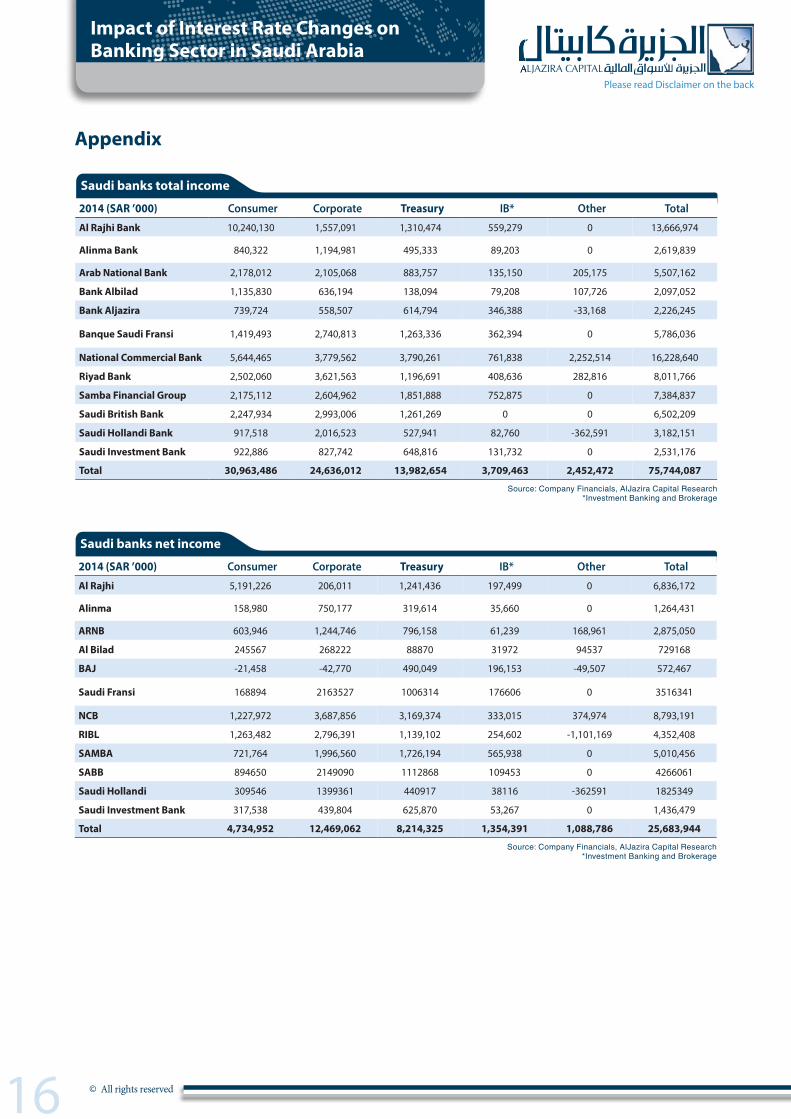

2014 (SAR ’000) Consumer Corporate Treasury IB* Other Total

Al Rajhi Bank 10,240,130 1,557,091 1,310,474 559,279 0 13,666,974

Alinma Bank 840,322 1,194,981 495,333 89,203 0 2,619,839

Arab National Bank 2,178,012 2,105,068 883,757 135,150 205,175 5,507,162

Bank Albilad 1,135,830 636,194 138,094 79,208 107,726 2,097,052

Bank Aljazira 739,724 558,507 614,794 346,388 -33,168 2,226,245

Banque Saudi Fransi 1,419,493 2,740,813 1,263,336 362,394 0 5,786,036

National Commercial Bank 5,644,465 3,779,562 3,790,261 761,838 2,252,514 16,228,640

Riyad Bank 2,502,060 3,621,563 1,196,691 408,636 282,816 8,011,766

Samba Financial Group 2,175,112 2,604,962 1,851,888 752,875 0 7,384,837

Saudi British Bank 2,247,934 2,993,006 1,261,269 0 0 6,502,209

Saudi Hollandi Bank 917,518 2,016,523 527,941 82,760 -362,591 3,182,151

Saudi Investment Bank 922,886 827,742 648,816 131,732 0 2,531,176

Total 30,963,486 24,636,012 13,982,654 3,709,463 2,452,472 75,744,087

Source: Company Financials, AlJazira Capital Research *Investment Banking and Brokerage

2014 (SAR ’000) Consumer Corporate Treasury IB* Other Total

Al Rajhi 5,191,226 206,011 1,241,436 197,499 0 6,836,172

Alinma 158,980 750,177 319,614 35,660 0 1,264,431

ARNB 603,946 1,244,746 796,158 61,239 168,961 2,875,050

Al Bilad 245567 268222 88870 31972 94537 729168

BAJ -21,458 -42,770 490,049 196,153 -49,507 572,467

Saudi Fransi 168894 2163527 1006314 176606 0 3516341

NCB 1,227,972 3,687,856 3,169,374 333,015 374,974 8,793,191

RIBL 1,263,482 2,796,391 1,139,102 254,602 -1,101,169 4,352,408

SAMBA 721,764 1,996,560 1,726,194 565,938 0 5,010,456

SABB 894650 2149090 1112868 109453 0 4266061

Saudi Hollandi 309546 1399361 440917 38116 -362591 1825349

Saudi Investment Bank 317,538 439,804 625,870 53,267 0 1,436,479

Total 4,734,952 12,469,062 8,214,325 1,354,391 1,088,786 25,683,944

Source: Company Financials, AlJazira Capital Research *Investment Banking and Brokerage

Saudi banks total income

Saudi banks net income

Appendix

Asset Management | Brokerage | Corporate Finance | Custody | Advisory

Head Office: King Fahad Road, P.O. Box: 20438, Riyadh 11455, Saudi Arabia، Tel: 011 2256000 - Fax: 011 2256068

Aljazira Capital is a Saudi Investment Company licensed by the Capital Market Authority (CMA), license No. 07076-37

RESE

ARC

H D

IVIS

ION

RESE

ARC

H

DIV

ISIO

NRA

TIN

GTE

RMIN

OLO

GY

BRO

KERA

GE A

ND IN

VEST

MEN

T CE

NTER

S DI

VISI

ON

Disclaimer

AlJazira Capital, the investment arm of Bank AlJazira, is a Shariaa Compliant Saudi Closed Joint Stock company and operating under the regulatory supervision of the Capital Market Authority. AlJazira Capital is licensed to conduct securities business in all securities business as authorized by CMA, including dealing, managing, arranging, advisory, and custody. AlJazira Capital is the continuation of a long success story in the Saudi Tadawul market, having occupied the market leadership position for several years. With an objective to maintain its market leadership position, AlJazira Capital is expanding its brokerage capabilities to o�er further value-added services, brokerage across MENA and International markets, as well as o�ering a full suite of securities business.

1. Overweight: This rating implies that the stock is currently trading at a discount to its 12 months price target. Stocks rated “Overweight” will typically provide an upside potential of over 10% from the current price levels over next twelve months.

2. Underweight: This rating implies that the stock is currently trading at a premium to its 12 months price target. Stocks rated “Underweight” would typically decline by over 10% from the current price levels over next twelve months.

3. Neutral: The rating implies that the stock is trading in the proximate range of its 12 months price target. Stocks rated “Neutral” is expected to stagnate within +/- 10% range from the current price levels over next twelve months.

4. Suspension of rating or rating on hold (SR/RH): This basically implies suspension of a rating pending further analysis of a material change in the fundamentals of the company.

The purpose of producing this report is to present a general view on the company/economic sector/economic subject under research, and not to recommend a buy/sell/hold for any security or any other assets. Based on that, this report does not take into consideration the specific financial position of every investor and/or his/her risk appetite in relation to investing in the security or any other assets, and hence, may not be suitable for all clients depending on their financial position and their ability and willingness to undertake risks. It is advised that every potential investor seek professional advice from several sources concerning investment decision and should study the impact of such decisions on his/her financial/legal/tax position and other concerns before getting into such investments or liquidate them partially or fully. The market of stocks, bonds, macroeconomic or microeconomic variables are of a volatile nature and could witness sudden changes without any prior warning, therefore, the investor in securities or other assets might face some unexpected risks and fluctuations. All the information, views and expectations and fair values or target prices contained in this report have been compiled or arrived at by Aljazira Capital from sources believed to be reliable, but Aljazira Capital has not independently verified the contents obtained from these sources and such information may be condensed or incomplete. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on the fairness, accuracy, completeness or correctness of the information and opinions contained in this report. Aljazira Capital shall not be liable for any loss as that may arise from the use of this report or its contents or otherwise arising in connection therewith. The past performance of any investment is not an indicator of future performance. Any financial projections, fair value estimates or price targets and statements regarding future prospects contained in this document may not be realized. The value of the security or any other assets or the return from them might increase or decrease. Any change in currency rates may have a positive or negative impact on the value/return on the stock or securities mentioned in the report. The investor might get an amount less than the amount invested in some cases. Some stocks or securities maybe, by nature, of low volume/trades or may become like that unexpectedly in special circumstances and this might increase the risk on the investor. Some fees might be levied on some investments in securities. This report has been written by professional employees in Aljazira Capital, and they undertake that neither them, nor their wives or children hold positions directly in any listed shares or securities contained in this report during the time of publication of this report, however, The authors and/or their wives/children of this document may own securities in funds open to the public that invest in the securities mentioned in this document as part of a diversified portfolio over which they have no discretion. This report has been produced independently and separately by the Research Division at Aljazira Capital and no party (in-house or outside) who might have interest whether direct or indirect have seen the contents of this report before its publishing, except for those whom corporate positions allow them to do so, and/or third-party persons/institutions who signed a non-disclosure agreement with Aljazira Capital. Funds managed by Aljazira Capital and its subsidiaries for third parties may own the securities that are the subject of this document. Aljazira Capital or its subsidiaries may own securities in one or more of the aforementioned companies, and/or indirectly through funds managed by third parties. The Investment Banking division of Aljazira Capital maybe in the process of soliciting or executing fee earning mandates for companies that is either the subject of this document or is mentioned in this document. One or more of Aljazira Capital board members or executive managers could be also a board member or member of the executive management at the company or companies mentioned in this report, or their associated companies. No part of this report may be reproduced whether inside or outside the Kingdom of Saudi Arabia without the written permission of Aljazira Capital. Persons who receive this report should make themselves aware, of and adhere to, any such restrictions. By accepting this report, the recipient agrees to be bound by the foregoing limitations.

AGM - Head of ResearchAbdullah Alawi+966 11 [email protected]

Senior Analyst

Talha Nazar +966 11 [email protected]

AnalystSultan Al Kadi+966 11 [email protected]

Analyst

Jassim Al-Jubran +966 11 [email protected]

General manager - brokerage services and sales

Ala’a Al-Yousef+966 11 [email protected]

AGM-Head of international and institutional

brokerage

Luay Jawad Al-Motawa +966 11 [email protected]

AGM- Head of Western and Southern Region Investment Centers & ADC

Brokerage

Abdullah Q. Al-Misbani +966 12 6618400 [email protected]

AGM-Head of Sales And Investment Centers

Central Region

Sultan Ibrahim AL-Mutawa +966 11 [email protected]

AGM-Head of Qassim & Eastern Province

Abdullah Al-Rahit +966 16 3617547 [email protected]

AGM - Head of Institutional Brokerage

Samer Al- Joauni +966 1 225 6352 [email protected]

Related Documents