REPORT TO THE JOINT LEGISLATIVE AUDIT AND REVIEW COMMISSION Impact Assessment of State-Level Economic Development Grants NICOLE GAFFEN XINGCHEN WANG JARED WILKERSON DECEMBER 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

REPORT TO THE

JOINT LEGISLATIVE AUDIT AND REVIEW COMMISSION

Impact Assessment of State-Level

Economic Development Grants

NICOLE GAFFEN XINGCHEN WANG

JARED WILKERSON DECEMBER 2011

1

ACKNOWLEDGEMENTS:

Dr. Greg Rest and Massey S. J. Whorley, JLARC

Professor Eric Jensen and Professor David Finifter, College of William & Mary,

Course Instructors

Professor Elaine McBeth and Professor John McGlennon, College of William & Mary,

Faculty Advisors

Rui Pereira, College of William & Mary, assistance with IMPLAN

Any opinions expressed here are those of the authors and not Joint Legislative Audit

and Review Commission staff. Any errors or omissions are the sole responsibility of

the authors.

2

TABLE OF CONTENTS

I. EXECUTIVE SUMMARY ............................................................................................................................ 5

II. INTRODUCTION ..................................................................................................................................... 6

A. Directive from the General Assembly ............................................................................................... 6

B. Overview of JLARC Special Report on Development Grants ............................................................. 7

1. Key Findings and Recommendations ............................................................................................. 7

C. Non-Grant Economic Development Incentives ................................................................................. 8

1. Tax Incentives ................................................................................................................................ 9

2. Technology Zones .......................................................................................................................... 9

3. Financial Assistance ....................................................................................................................... 9

4. Managing and Technical Support ................................................................................................ 10

D. Economic Development Grants ...................................................................................................... 10

1. Governor’s Opportunity Fund (GOF) ........................................................................................... 10

2. Virginia Investment Partnership (VIP) Grant ............................................................................... 11

3. Major Eligible Employer (MEE) Grant .......................................................................................... 12

4. Virginia Economic Development Incentive Grant (VEDIG) .......................................................... 12

5. Clean Energy Manufacturing Incentive Grant (CEMIG) ............................................................... 12

6. Virginia Jobs Investment Program (VJIP) ..................................................................................... 13

7. Economic Development Access Program (EDAP) ........................................................................ 13

8. Rail Industrial Access Program (RIAP) .......................................................................................... 13

9. Transportation Partnership Opportunity Fund (TPOF) ................................................................ 14

10. Tobacco Region Opportunity Fund (TROF) ................................................................................ 14

III. EVALUATION OF JOB CREATION ........................................................................................................ 15

A. Rationale ......................................................................................................................................... 15

B. Methodology ................................................................................................................................... 15

1. Job Projections Database ............................................................................................................ 16

2. Job Creation Database ................................................................................................................. 16

C. Job Creation ..................................................................................................................................... 18

1. Evaluation Conducted on Original Data ...................................................................................... 19

2. Evaluation Conducted under Bracketing System ........................................................................ 20

D. Job Creation by Sector .................................................................................................................... 24

3

1. Performance of Manufacturing Sectors ...................................................................................... 25

2. Performance of White Collar Sectors .......................................................................................... 26

3. Average Salary by Sector ............................................................................................................. 26

4. Sector Economic Multipliers ........................................................................................................ 28

IV. STATE-LEVEL GRANT EXPENDITURES & TAX REVENUES .................................................................... 30

A. State-Level Grant Expenditures....................................................................................................... 30

1. Aggregate Grant Awards ............................................................................................................. 30

2. Aggregate Grant Expenditures .................................................................................................... 32

B. State-Level Tax Revenues ................................................................................................................ 34

1. Using IMPLAN to Estimate State-Level Tax Revenues ................................................................. 34

2. Sector-Level Analysis of State-Level Tax Revenues ..................................................................... 36

C. Comparison of State-Level Expenditures and Revenues ................................................................. 37

V. CYCLICAL AND COUNTER-CYCLICAL TRENDS ....................................................................................... 39

A. Effect of Business and Election Cycles on Job Projections .............................................................. 39

B. Effect of Business and Election Cycles on Grant Awards ................................................................ 41

VI. CASE STUDIES ..................................................................................................................................... 43

A. Goodyear Automotive Service ........................................................................................................ 43

B. STIHL, Incorporated ......................................................................................................................... 44

C. Barber & Ross Company .................................................................................................................. 45

D. Eli Lilly and Company....................................................................................................................... 46

VII. Recommendations for Further Evaluation ....................................................................................... 48

A. Limitations to Using Input-Output Software ................................................................................... 48

B. Considerations for Current Development Incentive Policies .......................................................... 50

VIII. Conclusion ....................................................................................................................................... 52

APPENDIX 1: GRANT PROGRAM GUIDELINES ............................................................................................. 55

APPENDIX 2: ANNUAL JOBS COMPARISON TABLES .................................................................................... 60

APPENDIX 3: JOB PROJECTIONS AND CREATION BY SECTOR...................................................................... 78

APPENDIX 4: STATE-LEVEL GRANT EXPENDITURES AND REVENUES BY SECTOR ........................................ 87

APPENDIX 5: TOTAL EFFECT ON EMPLOYMENT AND OUTPUT BY SECTOR ................................................ 90

APPENDIX 6: METHODOLOGY OF USING IMPLAN ...................................................................................... 98

References ................................................................................................................................................ 100

4

LIST OF TABLES

TABLE III-A: AVERAGE ANNUAL RATIOS OF JOB CREATION ................................................................................. 18

TABLE III-B: JOB CREATION PERFORMANCE WITHIN FIVE YEARS OF PROJECT ANNOUNCEMENT ..................... 20

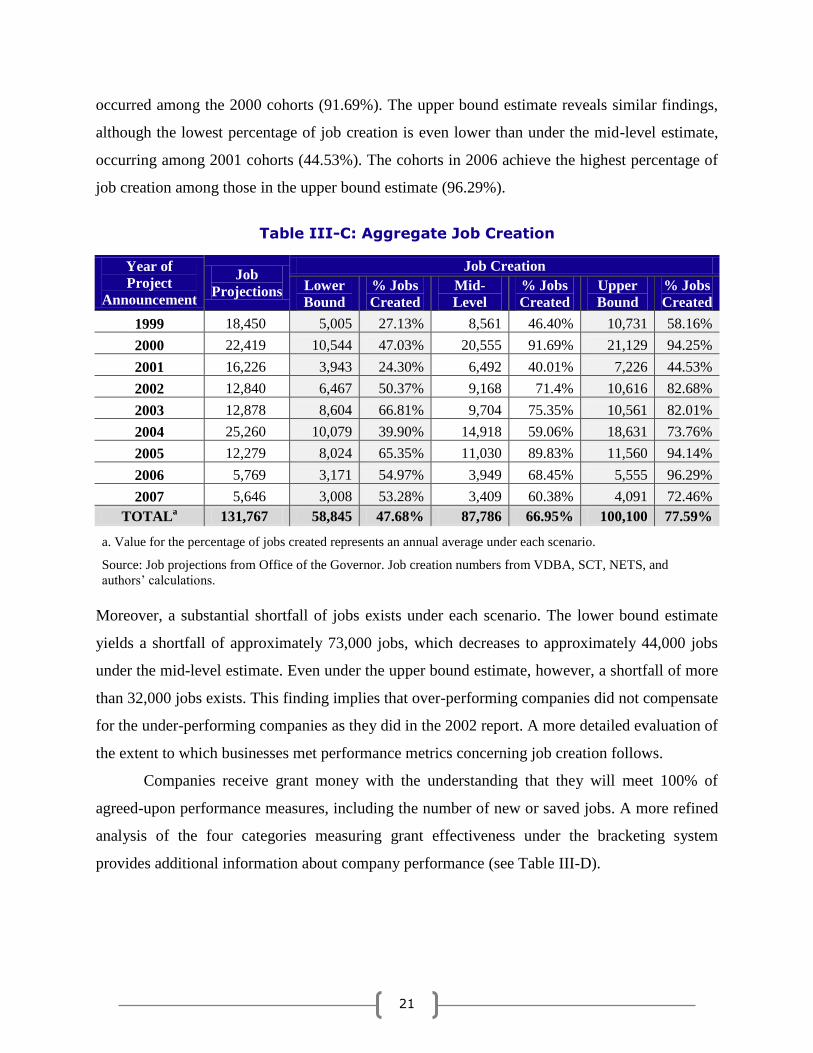

TABLE III-C: AGGREGATE JOB CREATION .............................................................................................................. 21

TABLE III-D: JOB CREATION PERFORMANCE (PROJECTS MEETING LESS THAN 75% OF PROJECTIONS) ....... 22

TABLE III-E: JOB CREATION PERFORMANCE (PROJECTS MEETING BETWEEN 75 AND 99.99% OF

PROJECTIONS) ................................................................................................................................................... 23

TABLE III-F: JOB CREATION PERFORMANCE (PROJECTS MEETING OR EXCEEDING PROJECTIONS) .................. 24

TABLE IV-A: AGGREGATE GRANT AWARDS AND PLEDGES .................................................................................... 30

TABLE IV-B: AGGREGATE GRANT EXPENDITURES FOR QUANTIFIED GRANTS ..................................................... 33

TABLE IV-C: AGGREGATE GRANT EXPENDITURES.................................................................................................. 34

TABLE IV-D: STATE AND LOCAL TAX REVENUES ................................................................................................... 36

TABLE IV-E: STATE-LEVEL EXPENDITURES AND REVENUES ................................................................................. 37

TABLE V-A: BUSINESS CYCLES, 1999-2007 ....................................................................................................... 40

TABLE V-B: STATE-WIDE ELECTION CYCLES, 1999-2007 ................................................................................ 41

TABLE 3A: JOBS COMPARISON (SECTORS EXCEEDING JOB CREATION PROJECTIONS) ..................................78

TABLE 3B: JOBS COMPARISON (SECTORS MEETING STANDARD GRANT REPAYMENT CUTOFF) ......................79

TABLE 3C: JOBS COMPARISON (SECTORS MEETING BETWEEN 50-74.99% OF PROJECTIONS) ...................80

TABLE 3D: JOBS COMPARISON (SECTORS MEETING LESS THAN 50% OF JOB CREATION PROJECTIONS) .....81

TABLE 3E: ECONOMIC MULTIPLIERS BY SECTOR ...........................................................................................82

TABLE 3F-1: HIGHEST PERFORMING DEVELOPMENT PROJECTS (JOB CREATION RATIO) ...............................83

TABLE 3F-2: HIGHEST PERFORMING DEVELOPMENT PROJECTS (NET JOBS) .................................................84

TABLE 3G: AVERAGE HOURLY WAGE BY SECTOR ..........................................................................................85

TABLE 3H: GRANT AWARDS BY SECTOR........................................................................................................86

LIST OF FIGURES

FIGURE III-A: JOBS COMPARISON .…………………………………………………………………………………………………20

FIGURE V-A: BUSINESS AND ELECTION CYCLE TRENDS (JOB CREATION PROJECTIONS) …………………………40

FIGURE V-B: BUSINESS AND ELECTION CYCLE TRENDS (GRANT AWARDS)……………………………………………42

5

I. EXECUTIVE SUMMARY

Virginia offers numerous economic development incentives to

businesses contemplating relocation to or expansion within the state. A

report on the effectiveness of these grant programs conducted by JLARC

in 2002 followed the results of development projects announced in 1997

and 1998. The report revealed that over-performing companies

compensated for both under-performing and non-performing companies in

terms of job creation. Additionally, these jobs produced individual income

tax revenues that allowed the state to recover the costs of GOF and

workforce service training grants within two and a half years.

The current update examines development projects announced

over nine years (1999-2007), which includes periods of recession and

expansion, as well as Republican and Democrat control of the

governorship. Job projections resulting from the development projects

exceeded 131,000. A bracketing system was applied to projects for which

data could not be obtained, resulting in job creation estimates ranging

from approximately 58,845 to 94,825 – a finding notably distinct from the

result of the 2002 report. If the indirect and induced effects of direct job

creation are factored in, however, projections are well exceeded.

Manufacturing companies tended to come closest to meeting metrics

established in performance agreements, while companies creating non-

manufacturing jobs brought the highest net number of jobs to the state.

The state promised $346.32 million in quantifiable grants to the

490 development projects announced within this timeframe. Estimated

expenditures ranged from $204.27 million under the lower bound of the

bracketing system to $234.93 million under the upper bound. Despite the

lower rate of job creation than present in the 2002 report, however,

estimated state-level tax revenues more than matched grant expenditures.

Revenues were estimated for jobs created by direct, indirect, and induced

effects over a two to three year period; as a result, estimates are likely low.

Even so, tax revenues significantly exceed expenditures – estimated state

collections range from $460.52 million under the lower bound to $1.11

billion under the upper bound.

Incentive grants appear to be a revenue-enhancing policy that

provides added benefits for the state in terms of lower unemployment and

the maintenance of a highly ranked business climate. It is in Virginia’s

best interest to maintain these grant programs to more effectively compete

with regional and national competitors. There is room, however, for a

thorough re-evaluation of the policies governing grant programs.

Additionally, the state should consider targeting grants to sectors that tend

to meet performance metrics (briefly examined in this study).

STUDY HIGHLIGHTS

Timeframe: 1999-2007

Development Projects:

490

Total Job Projections:

131, 767

Estimated Job Creation:

Lower Bound - 58,845

Mid-Level - 87,787

Upper Bound - 94,825

Total Grant Awards:

$346.32 million

Total Grant

Expenditures:

Lower- $238.79 million

Mid- $268.61 million

Upper- $275.51 million

State-Level Tax Revenue:

Lower- $460.52 million

Mid- $1,081.08 million

Upper- $1,110.45 million

Net State Revenue: Lower- $78.75 million

Mid- $695.41 million

Upper- $723.55 million

Projects Exceeding Job

Projections: 112

Projects Achieving Job

Projections: 20

6

II. INTRODUCTION

The effects of the most recent recession are still being felt in Virginia, particularly for the

nearly 300,000 unemployed who comprise a ―jobs gap‖ between pre-recession and post-

recession employment levels.1 While economic development incentives cannot alone bridge the

gap, effective programs can bring high-paying jobs to localities and needed employment to areas

of economic decline, such as Southwestern Virginia. Consequently, the Virginia General

Assembly has directed that a study be undertaken to evaluate the effectiveness of current grant

incentive programs – this study provides an initial examination of the program policies, the

resulting impacts of economic development supported by grants, and avenues of future

consideration for the year-long study to be conducted by the Joint Legislative Audit and Review

Commission (JLARC).

A. Directive from the General Assembly

In February 2011, the General Assembly directed JLARC to evaluate the effectiveness of

state-level economic development grants. Senate Joint Resolution 329 noted the substantial

increase in funds such programs have received over the past decade, in addition to an increase in

the number of programs themselves (such as the establishment of the Clean Energy

Manufacturing Incentive Grant in 2011). An important aspect of evaluating program

effectiveness is whether, in light of other factors impacting company decisions to locate or

expand in the Commonwealth, economic development grants provide Virginia with an advantage

over competing states.2

The legislature mandated that the report include three elements. First, identify grant

programs currently offered by Virginia and the extent to which businesses make use of these

incentives. Second, evaluate the extent to which each grant program fulfills the public policies

―for which the grant programs were established.‖3 Third, recommend a method for conducting

ongoing analysis of the effectiveness of these incentive programs.4 The present study will focus

on the first and third elements, providing an update to JLARC’s 2002 Special Report, ―State

Business Incentive Grant Programs.‖ This report will first provide a broad overview of economic

development incentives, as well as a detailed examination of the major development grants

7

offered by the State of Virginia. Following is an analysis of the effectiveness of major economic

development grant programs in Virginia based on job creation performance. A cost-effectiveness

analysis is also conducted, weighing grant expenditures against state-level tax revenues. For both

of these measures of effectiveness, a sector-level analysis is also conducted, revealing which

industry sectors are highest performing. Next, an examination of business and election cycles

reveals whether there are cyclical or counter-cyclical effects on employment or grants. This

report then discusses four specific development projects in-depth, providing additional insight

into why certain projects are more successful than others. Finally, this report provides

recommendations for future evaluation of development grants and suggests several policies that

should be re-examined in light of the findings.

B. Overview of JLARC Special Report on Development Grants

The 2002 JLARC report examined economic development projects announced over a two

year period, 1997-1998. All eighty-nine projects received incentive grants from the

Commonwealth; their record of job creation was tracked for five years following the

announcement. Over the course of the report, JLARC implemented two fundamental

assumptions: (1) but for the promised grants, Virginia would not have received the investment of

companies to whom the grants were promised, and (2) all jobs created following the

announcement of a development project could be attributed to the initial promise of grant funds.5

This study continues to rely on those assumptions. This study will also evaluate current findings

against those contained in the 2002 report to assess whether program effectiveness remained

constant over the past decade.

1. Key Findings and Recommendations

A principal finding of the original report revealed that while many companies did not

create the number of jobs promised, those that exceeded performance agreements created enough

jobs to meet the total of annually announced projections.6 Several over-performing companies

created as many as three to four times the number of jobs initially projected, thereby

compensating for under-performing or non-performing companies. This study will examine

certain characteristics of over-performing companies that may allow state officials to better

8

target grant funds. Recommendations following from this analysis may allow the state to better

target grant awards to businesses that are more likely to meet performance metrics.

JLARC also found that estimated individual income tax revenues collected from jobs

directly created by development projects outweighed grant expenditures within three years of the

project announcement.7 Such an estimate was conservative because it did not include increased

revenue from other state-level taxes (such as corporate or sales taxes), leading to greater

certainty that financial benefits outweighed program costs. Consequently, JLARC recommended

that the two major grant programs, GOF and Workforce Services, remain functional - a

recommendation based on the conclusion that negative long-term consequences would result if

Virginia eliminated these programs. Among these negative impacts would be the creation of

fewer new jobs due to businesses deciding to locate in competing states. In the two or three years

following such a cut, ―the State’s resulting loss of individual income tax revenues would likely

be more than the amount that was saved by cutting these programs.‖8 This study will conduct a

similar cost-effectiveness analysis, although it makes use of a different method to estimate tax

revenue that more broadly reflects overall revenues collected by the state. Such a method will

provide a more detailed measure of the extent to which grant programs are revenue-enhancing

for the state.

There was a negative finding of the special report, however: some grant recipients may

pose risks that outweigh the positive impacts of job creation and capital investment.9 Such

impacts include undesirable business practices, which result in negative externalities for the state

and its citizens.A

Consequently, JLARC concluded that additional screening should be

implemented before the state awards grant funds.10

The case studies presented within this report

also examine the likelihood of local or state-level economic development officials detecting risks

before grants are awarded.

C. Non-Grant Economic Development Incentives

Virginia offers a wide variety of incentives targeted at businesses locating or expanding

in the state in an effort to successfully compete nationally and internationally. As development

A Examples of negative externalities include pollution and health-related impacts. Additionally, the 2002 report

uncovered a telemarketing firm that engaged in deceptive trade practices – before Virginia awarded the business

grant money, approximately twenty states initiated legal proceedings against it.

9

grants are just one of the Commonwealth’s many economic enticements, this section frames the

broad incentives available to qualifying businesses by briefly introducing non-grant incentives.

1. Tax Incentives

Virginia offers three types of tax incentives: corporate income, property, and sales and

use. Corporate income tax credits are not targeted towards all businesses; rather, they incentivize

certain behaviors. Thus, credits are available for businesses that create green jobs or a significant

number of new jobs, manufacturers purchasing recycling equipment, businesses that retrain

workers or invest in research and development, entities that increase their port volume, and

companies that use rail or barges instead of highways to transport goods.11

Property tax incentives are implemented solely at the local level. Localities have the

option to fully or partially waive taxes for property such as recycling equipment, rehabilitated

real estate, solar energy devices, and environmental restoration sites. Furthermore, localities can

reduce tax rates on items such as research and development property, semiconductor

manufacturing machinery, clean-fuel vehicles, and energy-efficient buildings.12

Finally, Virginia offers sales and use tax exemptions for the purchase or lease of certain

goods, such as semiconductor clean rooms, internet access charges, custom computer software,

and certain utilities.13

2. Technology Zones

Technology zones are created by local ordinances to attract technology-oriented

businesses. Qualifying businesses in these zones may receive fee waivers, local tax incentives,

and exemption from ordinances.14

3. Financial Assistance

The Virginia Small Business Financing Authority, a branch of the Virginia Department

of Business Assistance (VDBA), provides programs to make capital available to expanding

businesses and communities. These programs include the issuing of industrial development

bonds, guaranteeing loans to small businesses, and subsidizing loan portfolio insurance to

business-lending banks.15

10

4. Managing and Technical Support

The Center for Innovative Technology (CIT) provides two service lines to aid small

companies when accessing investment opportunities. First, CIT Entrepreneur connects

innovative companies with early-stage investors. Second, CIT R&D helps researchers transition

federally-funded and other research projects into commercial products and, ultimately, into

businesses or licensing opportunities. Additionally, the Virginia Small Business Development

Center Network, the Virginia Economic Development Partnership (VEDP)’s Division of

International Trade, and the Virginia Leaders in Export Trade program all assist their target

constituencies in achieving goals by strengthening small businesses and increasing international

trade.16

These diverse economic incentives often work in tandem with the subject of this report,

economic development grants, to encourage businesses to locate or expand in Virginia.

D. Economic Development Grants

The state offers a number of grant programs – some are available to any company that

can meet eligibility requirements based on capital investment and job creation, while others are

highly specialized and only offered to companies providing certain services or belonging to

specific industries. This section outlines ten major development programs; of these, the

Governor’s Opportunity Fund and Virginia Jobs Investment Partnership are the largest in terms

of both the number and size of grants awarded.

1. Governor’s Opportunity Fund (GOF)

The Virginia General Assembly established the GOF as a ―deal closer‖ that

provides performance grants to relocating or expanding businesses

deciding between several competing states.17

The governor exercises

discretion when offering funds to businesses, although recipients must meet

eligibility requirements, and projects must ―bring additional income into

the Commonwealth.‖18

The governor also maintains final approval of the

amount of the grant itself, considering recommendations made by VEDP

and negotiations conducted by the Secretary of Commerce and Trade with

the prospective recipient.19

11

The grant is given to localities—which provide matching funds—and then

applied towards site preparation, the expansion of utilities, and

infrastructure development.20

VEDP gives priority to projects in localities

with high unemployment rates, which must receive at least one-third of

total funds.21

The limit on grant payments per development project is $1.5

million, although the governor may approve a higher payout for projects

that ―are of statewide or regional interest.‖22

One vetting mechanism

applies to businesses that have ―closed, downsized, consolidated, or laid off

employees within the past 30 months‖ prior to applying for a grant,

although such actions do not necessarily preclude these businesses from

receiving funds.23

2. Virginia Investment Partnership (VIP) Grant

The General Assembly established VIP through the Virginia Investment

Partnership Act (VIPA) to benefit Virginia businesses maintaining at least

a five-year presence in the Commonwealth.24

Funds are intended for

manufacturing companies or associated research and development

operations to support increased production capacity and productivity,

facility modernization, and the development and implementation of

advanced technology.25

Grant payments per project are generally limited to

$3 million, subject to eligibility requirements (including a restriction on

receiving other state-level incentive grants). Grants of up to $5 million are

available for projects meeting more rigorous performance standards. An

increase in grant payments is also possible following the creation of new

jobs.26

VIP grant amounts are based on recommendations by VEDP and

negotiations conducted by the Secretary of Commerce and Trade, then

subject to final approval by the governor.27

Grants are paid with funds

appropriated by the General Assembly, and there is a program ceiling of $6

million in any given year.28

In FY 2010, four VIP

grants were awarded to

businesses, totaling $4.85

million. These businesses

announced new capital

investment of $500.5

million and the

anticipated creation of

681 new jobs and the

retention of 150 existing

jobs.

Source: VEDP

The General Assembly has

appropriated more than

$216 million to the Fund

since its inception in

1992.

In FY 2010, sixteen GOF

grants were awarded to

businesses, totaling $6.37

million. These businesses

announced new capital

investments of $288.9

million and the

anticipated creation of

2,998 jobs.

Source: VEDP

12

3. Major Eligible Employer (MEE) Grant

VIPA also established the MEE program, a discretionary performance

incentive geared towards existing Virginia manufacturers and non-

manufacturing basic employers.29

Eligibility requirements are more

rigorous than with VIP, although recipients are also prohibited from

simultaneously receiving other state-level grants.30

The MEE grant award

is based on VEDP recommendations and negotiations led by the Secretary

of Commerce and Trade. The governor retains final approval of all

payments.31

Funds for MEE grants are subject to appropriations by the

General Assembly, and payments cannot exceed $25 million per project.

Businesses must complete capital investment and job creation within five

years, although extensions are possible.32

4. Virginia Economic Development Incentive Grant (VEDIG)

VEDIG was also established by VIPA.33

Funds are targeted towards

Virginia businesses seeking to locate ―significant headquarters,

administrative or service sector operations‖ in the state.34

The governor

reserves final approval of each grant awarded based on recommendations

made by VEDP and negotiations conducted by the Secretary of Commerce

and Trade.35

Eligibility requirements differ based on locality; businesses

are ineligible if they simultaneously benefit from other state grant programs

or receive VIP or MEE funds.36

The VEDIG program is limited to annual

payouts of $6 million, and aggregate outstanding awards may not exceed

$30 million.37

5. Clean Energy Manufacturing Incentive Grant (CEMIG)

The General Assembly established CEMIG in 2011; program funds are

subject to annual appropriations.38

CEMIG is targeted towards clean energy

manufacturers seeking to locate or expand their business in the

Commonwealth and is intended to improve business performance, not fund

initial site preparation or infrastructure development.39

CEMIG limits the

maximum grant awarded to $9 million for eligible businesses, although the

In FY 2010, no businesses

were awarded MEE

grants.

Source: VEDP

In FY 2010, VEDIG funds

were awarded to one

business, which

announced new capital

investment of $25 million

and the anticipated

creation of 1,200 jobs.

Source: VEDP

13

governor is able to authorize a higher payout ―for projects with significant

state or regional interest.‖40

6. Virginia Jobs Investment Program (VJIP)

VJIP provides partial reimbursement for customized recruiting and training

services to companies creating new jobs or experiencing technological

change.41

Eligibility requirements ensure that a company is for-profit and

pays a minimum wage of $10 per hour (this requirement may be waived in

some localities due to high unemployment rates). Additionally, only certain

businesses are eligible: manufacturers, distribution centers, corporate

headquarters, call centers, informational technology services, and research

and development facilities. VJIP offers three programs to better serve

businesses with different workforce training needs: the New Jobs Program,

the Small Business New Jobs Program, and the Retraining Program.42

7. Economic Development Access Program (EDAP)

EDAP is a state-funded program administered by the Virginia Department

of Transportation (VDOT) and allocated by the Commonwealth

Transportation Board (CTB). The program provides funds to localities for

road improvements needed for adequate access for new or substantially

expanding qualifying projects. The award amount is determined by the

eligible capital investment of the company and the estimated cost of the

access road.43

The maximum award for an economic development access

road is $0.5 million; however, an additional $0.15 million is available but

must be matched dollar-for-dollar by the locality.

8. Rail Industrial Access Program (RIAP)

Administrated by the Virginia Department of Rail and Public

Transportation, RIAP operates in a similar manner to EDAP—funds are

appropriated to construct railroad tracks for new or substantially expanding

industrial and commercial projects. Eligible localities can receive awards of

In FY 2010,721

businesses received funds

from VJIP to train or

retrain employees.

Workforce training

reimbursements totaled

nearly $7 million.

Source: VEDP

In FY 2010, five grants

were awarded for road

improvements, totaling

$2.65 million.

Source: VEDP

In FY 2010, six grants

were awarded for rail

improvements, totaling

$1.31 million.

Source: VEDP

14

up to $450,000 per fiscal year.44

Up to two-thirds of the grant payment can

be unmatched; the remainder must be matched dollar-for-dollar by the

recipient or from other non-program sources. Each application for funds

must be accompanied by a resolution from the local governing body

requesting an allocation.

9. Transportation Partnership Opportunity Fund (TPOF)

Although VDOT also administers TPOF, the governor awards payments in

the form of grants, revolving loans, or other financing tools and equity

contributions. TPOF can only be granted to supplement activities

associated with eligible transportation projects, which must meet the

minimum criteria established in the GOF Guidelines. Additionally, projects

must address the needs identified in the appropriate state, region or local

transportation plan.45

Once funded by TPOF and completed, transportation

development projects become or remain public property.

10. Tobacco Region Opportunity Fund (TROF)

Administered by the Tobacco Indemnification and Community

Revitalization Commission, TROF provides performance-based grants at

the Commission’s discretion to localities in the tobacco producing region

(thirty-four counties and seven cities located in Southside and

Southwestern Virginia). TROF grants support job creation and capital

investments associated with the establishment or expansion of a business.

The grant amount varies based on local unemployment rate, prevailing

wage rate, capital investment level, industry type, and other factors chosen

by the Commission.46

In FY 2010, one TPOF

grant was awarded to a

business, totaling $3

million.

Source: VEDP

In FY 2010, twenty-five

grants and loans from

TROF were provided to

businesses, totaling $4.86

million.

Source: VEDP

15

III. EVALUATION OF JOB CREATION

A. Rationale

Economic impact assessments often ―enumerate outcomes and . . . assume that any new

activities of assisted firms must be attributable to the economic development program.‖47

Although this study does not assess the impact that many other factors can exert on job creation

numbers (e.g., natural business expansion due to increased sales), and thus cannot determine

strict causation, such enumeration can provide general (although limited) insight into the

effectiveness of development grants. One method of evaluation revealing whether economic

development grants led to job creation is a comparison of the number of jobs projected by each

company and the number of jobs directly created. B

In this case, effectiveness was measured

according to the following categories:

1. Businesses exceeding projections within five years of a project’s announcement

2. Businesses meeting projections within five years

3. Businesses failing to meet projections but still created jobs

4. Businesses failing to meet projections and did not create any jobs

A thorough analysis of the results follows, which includes an examination of the number and

types of businesses that fall into each category.

B. Methodology

A comparison of the projected number of jobs and the actual number of jobs created by a

business resulted from the comparison of two unique databases developed for this report: one

containing job projections (―Job Projections database‖) and another containing the number of

jobs directly created (―Job Creation database‖). Both will be described in detail below.

Examining the performance of companies in meeting job creation projections provides a useful

measure of program effectiveness based upon the most fundamental intent of the grant programs

– to provide employment opportunities for citizens of the Commonwealth.

B Saved jobs were included in the total job projection and creation numbers because VDBA includes them when

making these calculations. Additionally, by saving jobs, the state ensures that employment and tax revenues remain

constant. All further mention of job projections and creation throughout the report will implicitly include the number

of jobs saved as well.

16

1. Job Projections Database

This database included information from press releases publicly announcing development

projects from the Office of Governor between January 1999 and December 2007.48

For each

project announcement, the following information was recorded: (1) the name of the grant

recipient and the location of the economic development, (2) the number of jobs projected to be

created or saved, (3) the value of each grant awarded or pledged, and (4) a description of the

industry in which the jobs would be created.

The press releases covered 497 project announcements between January 1999 and

December 2007, the years for which job creation data allowed an accurate assessment of both

short-term (one to two years following the announcement) and long-term (three to five years

following the announcement) job creation.C From this set of projects, seven were eliminated

because they were awarded to state agencies, did not project job creation, or were not promised

grant funds.D Thus, the final database contained 490 projects.

2. Job Creation Database

Three data sources were used to estimate the number of jobs created or saved. The initial

data source for this study came from the National Establishment Time Series (NETS) database,

which annually tracks the number of employees at each business location in Virginia.49

Approximately half of development projects from the Job Projection Database remained without

employment information after importing the data, due primarily to an inability to find businesses

in the NETS database. Such gaps indicate the presence of a name discrepancy between the press

release and the NETS data or the failure of projects promising to create business locations in

Virginia. Other explanations include companies for which multiple business locations matched

the location given in the press releases, and subsidiaries or company mergers that were listed

under alternative names in NETS. All possible discrepancies were resolved but more than twenty

percent of projects were still without job creation information. Data from VDBA was later

incorporated; the agency provided information on job creation, grant expenditures, and hourly C Dropping 2008-2011 projects from this evaluation allows more accurate comparison among projects incorporating

both short-term and long-term effects. Projects from 2008 may have (at most) four full years of employment data,

depending on the month in which the project was announced – projects announced later have even fewer full years

of employment data. By standardizing the length of time encompassed by long-term effects to five years, direct

comparisons between job creation numbers become more reliable. D These projects are: eToys Inc. (August 23, 2000), DuPont (April 23, 2001), Leica Microsystems (April 25, 2001),

Port of Virginia (October 18, 2001), VEDP (May 27, 2003), Merck & Co., Inc. (February 4, 2005), and Indage

Group (April 25, 2007).

17

wages on companies for which VDBA has records of VJIP training reimbursements. The final

source of job creation data came from the Secretary of Commerce and Trade (SCT), which

provided employment numbers for projects receiving GOF grants.E

To correct for the problem of overlapping and contradictory data, the three data sources

were ranked to fill in job creation information: (1) VDBA (271 projects); (2) SCT (30 projects);

and (3) NETS (87 projects). VDBA data was seen as most reliable, since the information came

directly from the companies and was verified by the state. The same was true of SCT data,

although these reports did not divide job creation between the short- and long-term.F NETS data

often differed from the state data; however, the annual employment numbers provided a more

detailed picture of employment trends.G Using this system filled in job creation information for

388 of the 490 projects from the Job Projection database.

To correct for the problem of missing data for the remaining twenty-one percent of

projects, a bracketing system was applied (lower bound of job creation, mid-level, and upper

bound) to estimate job creation. Under the lower bound estimate – the worst-case scenario – the

condition was imposed that none of the remaining development projects created jobs. Under the

upper bound estimate – the best-case scenario – the condition was imposed that job projections

were fully met for each development project. Finally, under the mid-level estimate, the number

of jobs created for a particular project was assumed to be proportionate to the annual average

E SCT data came from the Secretary’s annual Reports on Business Incentives, 2004-2010. Each report tracks the

performance of GOF funded development projects based on job projections and job creation, in addition to tracking

grant promises, average salaries, and company performance on capital investment. The reports also included

information on projects receiving VIP grants; these employment numbers were not incorporated due to the

inconsistent timeframe over which job creation was measured. For example, Nylstar announced a development

project in April 2000 – the SCT data measures job creation from this point until fiscal year 2010, a nine-year

timeframe. On the other hand, Hershey Chocolate announced a development project in April 2007 – the SCT data

measures job creation from this point until fiscal year 2010, a three-year timeframe. To continue to maintain reliable

comparability between job creation numbers, this information was not included in the database. F These job creation numbers were classified as long-term, since the SCT reports were issued more than two years

after the development projects had been announced. G There is a noteworthy discrepancy between VDBA and NETS data on employment. VDBA data and NETS data

were both available for a total of 181 projects, associated with 43,113 job projections. Aggregating job creation

numbers among all these projects, VDBA data shows the creation of 33,772 jobs within five years, while only

11,192 jobs were created according to NETS. Consequently, we calculated the ratio of job projections to job

creation per project to be .78 from VDBA data and .26 from NETS data. By excluding outliers (where the job

creation to projection ratio is greater than 10 – over 1,000%), the average ratio becomes 0.97 from VDBA data and

0.44 from NETS. Although this gap is still substantial, we placed a floor (0 jobs) on the lowest employment values

that NETS provided for a project. Because NETS recorded negative employment values indicating lost jobs, and

VDBA only provided non-negative employment values, such action standardized the two data sources according to

the state agency data. Consequently, the two ratios of job creation to projections converge slightly: the ratio becomes

0.51 from NETS (after excluding outliers), while the VDBA ratio remains 0.97.

18

ratio of the number of jobs created and the number of jobs projected. Significant outliers were

dropped to maintain the most accurate ratio possible (see Table III-A).

Table III-A: Average Annual Ratios of Job Creation

Year of Project

Announcement

Ratio of Job Projections to

Job Creation

1999 0.655

2000a 0.958

2001 0.854

2002 0.840

2003 0.867

2004 0.636

2005b 0.922

2006c 0.687

2007d 0.637

a. Goodyear dropped; ratio was an extreme outlier (10.58)

b. STIHL Incorporated dropped; ratio was an extreme outlier (6.667)

c. MillerCoors dropped; ratio was an extreme outlier (20.25)

d. Progress Printing dropped; ratio was an extreme outlier (15.00)

Source: Authors’ calculations based on VDBA, SCT, and NETS data.

Examining these ratios reveals that both the lower and upper bounds may be too conservative. It

is highly unlikely that all projects for which VDBA, SCT, or NETS did not provide data created

no jobs. Internet searches revealed that several businesses are currently operating at the location

in which they promised to develop in the public project announcement, even though the number

of created jobs cannot concretely be determined. In the same vein, the high assumption does not

account for the possibility that companies may exceed performance measures, which occurred in

112 out of 490 projects. By using conservative brackets on both ends, however, the confidence in

the findings of this study is increased, particularly with respect to state-level tax revenues

(discussed in Section IV.B).

C. Job Creation

By comparing job creation projections with actual performance, it can be determined

whether each business created enough jobs to meet the performance metrics provided in the

19

public announcement of the development project. This evaluation was conducted both without

and with the bracketing system to ensure that results remained consistent across scenarios.

1. Evaluation Conducted on Original Data

Job creation projections were not met by businesses that announced development projects

within the nine year timeframe of this study (see Figure III-A). Performance ranged decidedly

among cohorts – projects announced during 2001 had the lowest overall rate of job creation

(29.78%), while projects announced during 2005 had the highest overall rate of job creation

(88.97%).

Figure III-A: Jobs Comparison

Source: VDBA, SCT, and NETS data.

Consequently, within no cohort did the job creation of over-performing companies fully

compensate for under-performing or non-performing companies—a far different conclusion from

JLARC’s 2002 report. A small number of individual projects were often responsible for the

drastic difference between projections and job creation – see Appendix 2 for project-specific

information among cohorts.

Additionally, examining the number of development projects within each of the four

categories described in the introduction to this section reveals both positive outcomes and areas

for improvement. Nearly thirty-five percent of projects exceeded initial job creation projections

within five years of the development project announcement (see Table III-B).

1999 2000 2001 2002 2003 2004 2005 2006 2007

Total job projections 12,75 11,96 13,24 9,624 11,60 17,65 9,019 4,637 5,016

Total job creation 5,005 10,54 3,943 6,467 8,604 10,07 8,024 3,171 3,008

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Nu

mb

er o

f J

ob

s

Year of Announcement

20

Table III-B: Job Creation Performance within Five Years of Project Announcement

Year of

Project

Announcement

Exceeded

Projections

Achieved

Projections

Failed to Meet Projections

TOTAL Created Jobs

Created No

Jobs

1999 8 0 23 4 35

2000 15 1 21 3 40

2001 9 2 16 3 30

2002 13 3 26 7 49

2003 23 3 25 7 58

2004 11 2 39 5 57

2005 15 7 24 5 51

2006 8 2 18 7 35

2007 10 0 15 8 33

Total 112 20 207 49 388

Source: Press releases from Office of the Governor; VDBA, SCT, and NETS data.

However, nearly two-thirds of development projects failed to achieve job creation projections.

One positive finding is that a significant majority (81%) of these unsuccessful development

projects did create jobs, even if not the number initially anticipated. On the other hand, nearly

fifty projects failed to create any jobs. Interviews conducted with several regional economic

development officials for the four case studies included in this report (see Section VI) may

provide limited insight into whether a stricter screening process is needed. Although beyond the

scope of this study, a more detailed examination of all forty-nine projects that did not manifest

may reveal whether a re-evaluation of existing screening procedures for grant applicants is

necessary.

2. Evaluation Conducted under Bracketing System

Applying the bracketing system revealed similar results; aggregate job projections were

not met by any cohort under any scenario (see Table III-C). Average job creation across cohorts

ranged from 47.68% under the lower bound estimate to 77.59% under the upper bound estimate.

There was a wide disparity among cohorts in terms of job creation performance, which remained

relatively consistent across the different scenarios. Under the lower bound estimate, job creation

ranged from a low of 24.30% among cohorts from 2001 to a high of 66.81% among 2003

cohorts. These percentages increased significantly under the mid-level estimate. The lowest

percentage of job creation occurred among the 1999 cohorts (46.40%), while the highest

21

occurred among the 2000 cohorts (91.69%). The upper bound estimate reveals similar findings,

although the lowest percentage of job creation is even lower than under the mid-level estimate,

occurring among 2001 cohorts (44.53%). The cohorts in 2006 achieve the highest percentage of

job creation among those in the upper bound estimate (96.29%).

Table III-C: Aggregate Job Creation

Year of

Project

Announcement

Job

Projections

Job Creation

Lower

Bound

% Jobs

Created

Mid-

Level

% Jobs

Created

Upper

Bound

% Jobs

Created

1999 18,450 5,005 27.13% 8,561 46.40% 10,731 58.16%

2000 22,419 10,544 47.03% 20,555 91.69% 21,129 94.25%

2001 16,226 3,943 24.30% 6,492 40.01% 7,226 44.53%

2002 12,840 6,467 50.37% 9,168 71.4% 10,616 82.68%

2003 12,878 8,604 66.81% 9,704 75.35% 10,561 82.01%

2004 25,260 10,079 39.90% 14,918 59.06% 18,631 73.76%

2005 12,279 8,024 65.35% 11,030 89.83% 11,560 94.14%

2006 5,769 3,171 54.97% 3,949 68.45% 5,555 96.29%

2007 5,646 3,008 53.28% 3,409 60.38% 4,091 72.46%

TOTALa 131,767 58,845 47.68% 87,786 66.95% 100,100 77.59%

a. Value for the percentage of jobs created represents an annual average under each scenario.

Source: Job projections from Office of the Governor. Job creation numbers from VDBA, SCT, NETS, and

authors’ calculations.

Moreover, a substantial shortfall of jobs exists under each scenario. The lower bound estimate

yields a shortfall of approximately 73,000 jobs, which decreases to approximately 44,000 jobs

under the mid-level estimate. Even under the upper bound estimate, however, a shortfall of more

than 32,000 jobs exists. This finding implies that over-performing companies did not compensate

for the under-performing companies as they did in the 2002 report. A more detailed evaluation of

the extent to which businesses met performance metrics concerning job creation follows.

Companies receive grant money with the understanding that they will meet 100% of

agreed-upon performance measures, including the number of new or saved jobs. A more refined

analysis of the four categories measuring grant effectiveness under the bracketing system

provides additional information about company performance (see Table III-D).

22

Table III-D: Job Creation Performance within Five Years of Project Announcement

(Development Projects Meeting Less Than 75% of Job Projections)

Estimate Percentage of

Job Creation

Total Jobs

Projected

Total Jobs

Created

Number of

Projects

Lower Bound

0.00% 49,688 0 151

0.01 – 10.00% 9,032 618 27

10.01 – 20.00% 7,950 1,227 15

20.01 – 30.00% 6,546 1,635 21

30.01 – 40.00% 4,459 1,547 23

40.01 – 50.00% 2,715 1,165 18

50.01 – 60.00% 7,747 4,360 30

60.01 – 70.00% 7,717 5,079 29

70.01 – 74.99% 2,287 1,632 6

TOTAL 320

Mid-Level

0.00% 13,708 0 49

0.01 – 10.00% 9,032 618 27

10.01 – 20.00% 7,950 1,227 15

20.01 – 30.00% 6,546 1,635 21

30.01 – 40.00% 4,459 1,547 23

40.01 – 50.00% 2,715 1,165 18

50.01 – 60.00% 7,747 4,360 30

60.01 – 70.00% 22,517 14,653 68

70.01 – 74.99% 2,287 1,632 6

TOTAL 257

Upper Bound

0.00% 13,708 0 49

0.01 – 10.00% 9,032 618 27

10.01 – 20.00% 7,950 1,227 15

20.01 – 30.00% 6,546 1,635 21

30.01 – 40.00% 4,459 1,547 23

40.01 – 50.00% 2,715 1,165 18

50.01 – 60.00% 7,747 4,360 30

60.01 – 70.00% 7,717 5,079 29

70.01 – 74.99% 2,287 1,632 6

TOTAL 218

Source: VDBA, SCT, NETS, and authors’ calculations.

Under all three estimates, a substantial number of companies failed to reach the standard

threshold to avoid grant re-payment (see Appendix 1 for additional information on grant

clawback policies for each program). Under the lower bound estimate, this number was inflated

due to the number of development projects for which no concrete employment information could

be obtained – the 151 projects in this category represents nearly half of all projects that failed to

reach the seventy-five percent threshold. The remaining categories contain a fairly even

23

distribution of projects, with two exceptions: projects creating between sixty and seventy percent

of projected jobs under the mid-level estimate and projects creating between seventy and

seventy-five percent under all estimates. The former can be explained by the average annual

ratios calculated for the 1999, 2004, 2006, and 2007 cohorts (see Table III-A). The latter is an

unexpected finding – a larger clustering of projects below seventy-five percent would be

expected, as businesses that did not meet projections attempt to avoid the clawback of grant

funds.

A more positive finding concerns the number of projects which met the repayment

threshold (see Table III-E).

Table III-E: Job Creation Performance

within Five Years of Project Announcement

(Development Projects Meeting Between 75% and 99.99% of Job Projections)

Estimate Percentage of

Job Creation

Total Jobs

Promised

Total Jobs

Created

Number of

Projects

Lower Bound

75.00 – 80.00% 5,409 4,076 12

80.01 – 90.00% 6,743 5,678 16

90.01 – 99.99% 2195 2,129 10

TOTAL 38

Mid-Level

75.00 – 80.00% 5,409 4,281 12

80.01 – 90.00% 13,613 11,489 49

90.01 – 99.99% 15,905 15,146 38

TOTAL 99

Upper Bound

75.00 – 80.00% 5,409 4,281 12

80.01 – 90.00% 6,143 5,678 16

90.01 – 99.99% 2,195 2,129 10

TOTAL 38

Source: VDBA, SCT, NETS, and authors’ calculations.

Approximately forty projects met this threshold under the lower and upper bound estimates – this

number increases to nearly one hundred under the mid-level estimates. Of note, however, is the

increased number of projects clustered above the seventy-five percent threshold (twelve)

compared with the number clustered below (six). Such a finding may substantiate the above

hypothesis and show that businesses are more successful at reaching such a threshold when job

creation approaches seventy-five percent.

Twenty projects met job creation projections under both the lower bound and mid-level

estimates (see Table III-F).

24

Table III-F: Job Creation Performance within Five Years of Project Announcement

(Development Projects Meeting or Exceeding Job Creation Projections)

Estimate Percentage of

Job Creation

Total Jobs

Promised

Total Jobs

Created

Number of

Projects

Lower Bound 100% 3,714 3,714 20

over 100% 15,565 25,780 112

TOTAL 132

Mid-Level 100% 3,714 3,714 20

over 100% 15,565 25,780 112

TOTAL 132

Upper Bound 100% 39,694 39,694 122

over 100% 15,565 25,780 112

TOTAL 234

Source: VDBA, SCT, NETS, and authors’ calculations.

The number of projects meeting this threshold under the upper level estimate is much higher

(112 projects) due to the condition of full job creation imposed on this scenario. A very positive

finding concerns the number of development projects exceeding initial

projections, however. Approximately twenty-three percent of all

development projects announced between 1999 and 2007 created more

jobs than initially anticipated, resulting in an additional 10,000 jobs

state-wide. While beyond the scope of this study, the state would benefit

from further analysis of the types of development projects that are high performing. The results

of such an analysis would allow the state to better target grants to businesses that will provide

added value in the form of additional jobs and tax revenues.

D. Job Creation by Sector

Examining sector-level output may provide beneficial guidelines as to which sectors

generally meet (or exceed) performance measurements and which offer the highest-quality jobs

for localities. These factors are important to consider when evaluating the effectiveness of

economic development grants. Additionally, knowledge about sector performance may help state

officials to target grants towards companies that are more likely to be successful, however that

term is defined.

Number of projects

exceeding job creation

projections: 112

Number of additional jobs

created: 10,215

25

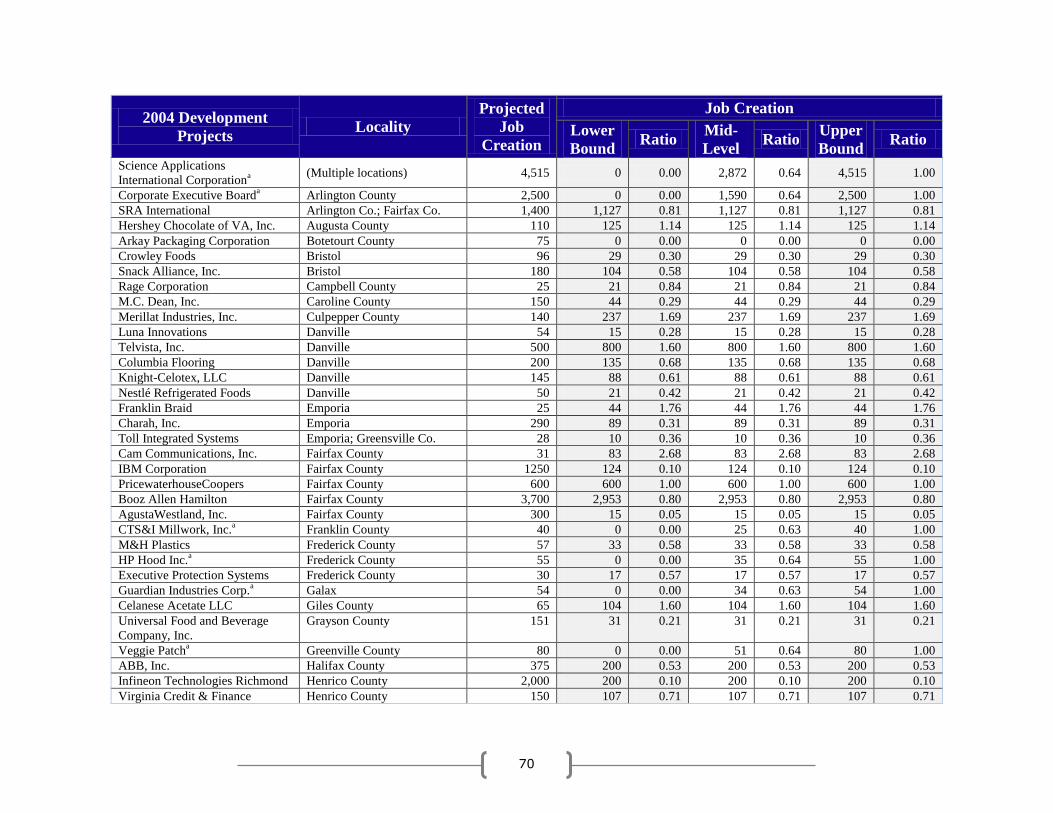

Ten sectors exceeded total job creation projections for the sector based on mid-level

estimates (see Appendix 3, Table 3A). These sectors represent seventy-eight development

projects projecting the creation of 8,645 jobs and directly creating 10,530 jobs. Several of these

sectors had a low number of projects (between one and three), indicating that a few over-

performing companies positively impacted the high ratio of job creation. Half of the sectors,

however, contained enough projects to be able to assert, with some degree of certainty, that they

represent a positive investment for the state; manufacturing is well-represented among these high

performers.

1. Performance of Manufacturing Sectors

Transportation Equipment Manufacturing (sector 336) contained the highest number of

development projects which exceeded 200% of job creation projections

– eight projects that originally projected 739 jobs but created 2,043 jobs

(see Appendix 3, Table 3F). Plastics and Rubber Products

Manufacturing (sector 326) contained six projects that also met this

threshold of job creation. The performance of one business heavily

influenced this outcome – Essel Propack America undertook four

development projects that anticipated creating 206 jobs but delivered

515 jobs.

The two most successful development projects over the nine year

timeframe of this study in terms of the ratio of projections to creation and the highest number of

net jobs exceeding projections belonged to manufacturing sectors (see

Appendix 3, Tables 3F-1 and 3F-2). The former belongs to Beverage and

Tobacco Product Manufacturing (sector 312). MillerCoors (then Coors

Brewing) announced a development project in 2006 projecting the

creation of eight jobs – within five years, 162 had been created. The

latter belongs to Machinery Manufacturing (sector 333). In 2005,

STIHL, Inc. projected the creation of 150 jobs through the course of

their development project. Job creation reached 1,000 jobs within five

years (see Section VI.B for a detailed case study of the 2005 STIHL

development project).

Highest Performing

Development Project

(Ratio of Projection to

Creation)

MillerCoors (2006)

Jobs Projected: 8

Jobs Created: 162

Ratio: 20.25

Highest Performing

Development Project

(Most Net Jobs

Exceeding Projections)

STIHL, Inc. (2006)

Jobs Projected: 150

Jobs Created: 1,000

Net Difference: 850

26

Such successes are positive for localities due to increased employment and economic

activity, and the state also benefits from increased tax revenues that are not counterbalanced by

additional grant expenditures. These high-performing projects offset to some degree the projects

that significantly underperformed or failed to create jobs; as discussed in Sections III.C.1 and

III.C.2, however, these projects could not fully compensate for the shortfalls in job creation.

2. Performance of White Collar Sectors

White collar sectors had the highest overall projections for job

creation, although their performances were often not as successful as that

of the manufacturing sectors discussed above. Development projects

initiated by businesses in Professional, Scientific, and Technical Services

(sector 541) projected overall job creation of 24,625 jobs (see Appendix

3, Table 3C). Under the lower bound estimate, these projects created

approximately 10,000 jobs – the highest net number of jobs among any

sector, even though this figure represents a forty percent job creation

rate. The upper bound reveals a more positive outcome: an eighty-one

percent job creation rate yields approximately 20,000 jobs under this scenario. Additionally,

these jobs are among the highest-paying with an average salary of $37.57 (see Appendix 3, Table

G).H

Telecommunications (sector 517) projected the second highest job creation among all

sectors - 12,718 jobs. The ratio of job creation was low, however, ranging from seventeen

percent under the lower bound to twenty-five percent under the upper bound. The poor

performance of this sector can be directly attributed to one development project, however:

WorldCom projected the creation of 8,000 jobs that never materialized due to the fraud-induced

bankruptcy of the company shortly after the December 2001 announcement of the development

project.

3. Average Salary by Sector

The state currently takes the average hourly wage of jobs created by development

projects into account when choosing grant recipients.I An analysis of the average hourly wage

H Expenditures, revenues, and hourly wages are calculated in 2008 dollars throughout the report.

I See individual program guidelines for eligibility requirements.

Sector with Highest Net

Job Creation

Professional, Scientific,

and Technical Services

Jobs Projected: 24,625

Jobs Created, Lower

Bound: 9,927

Jobs Created, Upper

Bound: 19,993

27

associated with each sector offers insight into the sectors that perform well in this aspect (see

Appendix 3, Table 3G). This analysis included 284 projects (representing forty-six out of the

fifty-nine sectors in this study) for which information on hourly wages was available.J The

average hourly wage for each sector was calculated based on project-

specific information and then creating a weighted average for each

sector.K

Of the forty-six sectors included in this analysis, six pay

average hourly wages that provide an annual salary higher than the

state-wide median income of $61,064 in 2008.50

The average hourly

wages of these sectors range from $31.48 for Textile Product Mills

(sector 314) to a high of $54.26 for Beverage and Tobacco Product

Manufacturing (sector 312). These six sectors had seventy-seven

development projects that anticipated the creation of approximately

28,000 jobs; applying the bracketing system estimates the creation of

between 13,000 and 24,000 jobs.

It is important to note that the average hourly wage of the two highest-paying sectors is

driven by two development projects: Philip Morris in Beverage and

Tobacco Product Manufacturing (sector 312), and Meristar

Hospitality in Accommodation (sector 721). The average hourly

wage at Philip Morris was $77.81 across 500 created jobs, increasing

the average salary of that sector significantly. Additionally, Meristar

was the only project in the Accommodation sector; the company paid

an average hourly wage of $43.29. In contrast, the average hourly

wage ($37.57) for the third highest paying sector, Professional,

Scientific, & Technical Services (sector 541), was based on the

hourly wages of 10,000 jobs across 59 development projects and is

J VDBA data provided hourly wage information for 240 projects. SCT provided salary information for twenty-four

additional projects, which was converted into hourly wages. In some sectors, no companies sought reimbursement,

so there is no estimate of an average salary. K The weighted average salary was created according to the following steps: (1) multiplying the average hourly

wage of each project by the total number of jobs created by that project (from VDBA, NETS, and SCT data); (2)

summing the average hourly wage of each project across the sector; and (3) dividing that number by the total

number of jobs created the companies for which hourly wage information existed in the sector.

Sectors with Highest Average

Hourly Wages

Beverage & Tobacco: $54.26

Accommodation: $43.29

Professional, Scientific, and

Technical: $37.57

Financial Investment: $36.61

Insurance: $32.76

Textile Mills: $31.48

Sectors with Lowest Average

Hourly Wages

Non-Store Retailers: $9.05

Administrative & Support

Services: $9.12

Paper Manufacturing: $10.27

Food & Beverage Stores:

$10.33

28

thus a more reliable estimate.

The five sectors with lower average hourly wages (ranging from $9.05 to $10.53) also

created fewer jobs compared to original job projections. Thirty-nine projects among these sectors

announced the expected creation of approximately 14,300 jobs. Between approximately 5,000

and 10,500 jobs were created under the lower and upper bound estimates. Thus, it appears that

the higher-paying sectors tend to have higher job creation performance than their lower-paying

counterparts. This finding offers one area in which the state can seek to improve strategies

concerning development grants. Although the state seeks to attract development projects that

create higher-paying jobs, a slight disconnect currently exists between outcomes and policy as

evidenced by the above results. A more detailed analysis of the location of the development

projects paying lower wages may reveal that they are located in southwestern Virginia. As

encouraging economic development in this region is a primary consideration for the state (and

thus high paying wages becomes a secondary consideration), these projects may require

additional assistance from the state in order to successfully perform. For example, it may be that

additional time is needed to meet performance metrics. Additionally, efforts to target businesses

within these higher-paying and -performing sectors should be increased.

4. Sector Economic Multipliers

A brief examination of the economic multipliers associated with each sector also provides

state officials with useful information to consider when weighing

between potential grant recipients (see Appendix 3, Table 3E).

Sectors with higher multipliers provide additional benefits for the

state in terms of jobs created through indirect and induced effects.

Higher total job creation leads to higher state and local tax revenues

in the form of income taxes, sales taxes, and other related taxes.

Many of these sectors with higher multipliers are manufacturing

sectors, which makes sense intuitively. Manufacturing firms require

inputs from many different industries, which in turn create additional

jobs. For example, the multiplier for the Beverage and Tobacco

Product Manufacturing sector (312) is 5.29, which indicates that for

every job directly created by a business in that sector, another 4.29

jobs are created throughout the local economy (in this case, the state of Virginia) through indirect

Sector with Highest Economic

Multiplier

Beverage & Tobacco Mfg

Multiplier: 5.29

Sectors with Lowest Economic

Multiplier

Nonmetallic Mineral Product

Manufacturing; Store Retailers

Multiplier: 1.16

29

and induced effects. Service-oriented industries, in contrast, rely heavily on the human capital of

their employees to provide a product to customers – fewer ancillary jobs are created as a result.

Consequently, Store Retailers (sector 453) have the lowest economic multiplier among sectors

with development projects examined in this study. Nonmetallic Mineral Product Manufacturing

also shares this low multiplier, although it represents the only manufacturing sector with a

multiplier below 1.5.

30

IV. STATE-LEVEL GRANT EXPENDITURES & TAX REVENUES

A. State-Level Grant Expenditures

1. Aggregate Grant Awards

Many grant awards are provided upfront to either the locality, through programs such as

GOF or TROF, or the business itself, through programs such as VIP (see Appendix 1). The

amount awarded through these programs was provided by the Office of the Governor and

incorporated in the Job Projections database.L However, grants requiring reimbursement, such as

VJIP, and those awarded from smaller grant programs, such as RIAP or EDAP, were generally

not quantified. The former issue was largely resolved through receipt of the VDBA data. The

state agency provided information on initial budget projections for the workforce training

programs, as well as the final reimbursement amount for many of the projects that had been

pledged VJIP funds. Expenditures related to the remaining projects without VJIP information, as

well as the smaller unquantified grants, will be discussed below in Section IV.A.2.a).

Within the nine year timeframe of this study, there existed substantial variation in annual

grant awards. These ranged from a high of $64.76 million in 2003 to a low of $16.85 million in

2007 (see Table IV-A).

Table IV-A: Aggregate Grant Awards

Year of Project

Announcement

Quantified Grant Awards

(in millions)

1999 $28.98

2000 $41.34

2001 $34.61

2002 $30.76

2003 $64.76

2004 $39.02

2005 $47.92

2006 $42.08

2007 $16.85

TOTAL $346.32

Note: Dollar amounts adjusted to 2008 USD.

Source: Grant projections are from the Office of the Governor and VDBA

budget estimates for VJIP grants.

L In addition to GOF, TROF, and VIP awards, as well as certain VJIP pledges, other quantifiable grants between

1999 and 2007 include five RIAP grants.

31

A more detailed analysis of grant awards and pledges according to projects and sectors will

reveal more information about the industries that are awarded the highest number of grants and

the most grant money.

a) Project-Level Analysis of Grant Awards

Only three development projects announced between 1999 and 2007 were awarded

incentive grants totaling more than $10 million. Philip Morris received the largest total grant

award over this timeframe for a 2003 development project in Henrico County - $3 million in

GOF grant money and $25 million in VIP grants. The company was also the recipient of another

significant payment in 2005 for a development project in the City of Richmond – a $3 million

GOF grant and $12 million in VIP funds. In 2008 dollars, grant payments to the tobacco

manufacturer totaled $49.30 million. Job creation for the 2003 project reached 500 within five

years, while the 2005 project created 450 jobs within five years – a 100% job creation rate for

the two projects combined. The other substantial grant award during this timeframe went to

WorldCom, which was pledged $11 million in VIP fund ($13.37 million in 2008 USD) in return

for job creation projections of 8,000 jobs. As discussed in Section III.D.2, however, the

WorldCom development project did not materialize.

b) Sector-Level Analysis of Grant Awards

The sector projecting the highest number of jobs created – Professional, Scientific, and

Technical Services (sector 541) – also received the highest total amount of grant awards and

pledges: $45.42 million (see Appendix 3, Table 3H). The sector also had the highest number of

development projects (fifty-seven) that received grant funds, however, resulting in an average

grant of $0.80 million per-project. Transportation Equipment Manufacturing (sector 336) had the

second highest number of development projects that received grant funds: thirty-one projects

received $23.83 million. As with Professional, Scientific, and Technical Services, however,

average per-project awards and pledges were low ($0.77 million).

Large aggregate grant awards and pledges were also given to several manufacturing