At a Glance IMAP BUSINESS... ACCELERATING

IMAP at a Glance Low resolution

Aug 07, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

At a GlanceIMAP

BUSINESS...ACCELERATING

3

A team that is based on values

will outperform a team based on interests.

Excellence

Global Reach

Integrity

Leadership

Sector Expertise

Teamwork

Truly Local

Trust

Long-term Relationships

Our values

4

Contents/ Foreword Gilberto Escobedo 06

/ About IMAP 10

/ Sector expertise 15 Automotive 18 Chemicals 19 High Technology 20 Pharmaceuticals 21

/ Global Reach 23 China 26 Czech Republic & Slovakia 28 Germany 30 India 32 Japan 34 Mexico 38 Russia 40 Spain & Portugal 42 Turkey 44 United Kingdom 46 USA 48

/ Why IMAP 51

/ Video compilation 52

5

Excellence

99% is as good as Zero

Excellence means giving your 100%

nothing less!

66

7

As we look ahead almost 6 years after the financial crisis, it is clear that the trends that started to take shape in and

before 2008 – namely a re-composition of the global economic order, with many emerging economies having clearly “emerged” and taking centre stage – continue to forge the path of global integration along with a new local de-globalization.

Companies that do not take advantage of moving into, or expanding their presence within, the growing economies will lose the edge to the ones that do. Even when we have seen a difficult recovery of global M&A activity from the pre-crisis levels at IMAP we believe that the years ahead will be interesting to say the least. Our philosophy has always been to put our clients’ interests first, and, in keeping with this, IMAP has remained by their side during the prolonged downturn, preparing the terrain, analyzing trends and opportunities, in order to help our clients make their move when the time is right.

OutlOOk The fact is that while there are still strong headwinds and challenges going forward, such as central bank policy uncertainty, stubbornly high unemployment rates, depressed salaries, and sluggish growth in Europe and the US, there are many other positive signs, which point to growth in the M&A market over the next few years. Let us name a few:

Gilberto Escobedo

8

Multinational companies have large reserves of cash in their war chests and Private Equity funds have impressive amounts of un-invested capital. Interest rates are at historic lows. There are opportunities in emerging markets, with favorable demographics and growth prospects. There is also a great deal of pent up demand, and decreasing uncertainty in the business world. Geographically, M&A looks to be robust in the USA, followed by the EU and Asia.

In spite of the uncertainty in the macroeconomic picture, which has never been a deciding feature or obstacle to acquisition or exit strategies, one of the key success factors in M&A has always been the well-executed integration plan. Good times always come back, but proper integration will determine positioning when they do. Seamless integration and, of course, realistic deal valuations is what clients seek most, whether economic conditions are optimal or challenging.

Growth motivates deals, and companies are driven by three things in the M&A market: a desire to grow the customer base, expansion across geographies, and entering new business lines.

Going forward, the middle-market, IMAP’s strong suit, is where the game will be played, rather the blockbuster deal. Challenges ahead, indeed, but expansion

areas abound for those who work them, especially in Technology, Media and Telecommunications, Industrials, as well as Pharmaceuticals and Life Sciences, followed by Financials and Energy.

Our values-based teams, cross-border reach, sector expertise and entrepreneurial spirit with hands-on partner involvement will be key to meeting the challenges and opportunities ahead.

IMAPAs the President of IMAP - the international firm of firms - I cannot stress too forcefully the things that make IMAP agile and alert. Is it because we are both a cross-border organization with the watch-work cohesion of a unified organization bound by excellence, shared values, professional respect and sector expertise - Or is it because we have the independence that many of our competitors might lack because of their chronic conflicts of interest?

We can do the seamless cross-border deals because our senior partners are always directly involved and not mere supervisors. Deals are conceived by putting ourselves in our clients’ shoes. How we rank is important, and we are up there, but sector expertise, independence, integrity and excellence got us there and have given us our momentum.

9

We know our sectors from the inside, as our professionals are people who came from technical backgrounds and were transformed by the power inherent in the IMAP entrepreneurial spirit.

I recommend you have a look at IMAP at a Glance, as it will cover some relevant sectors, illustrated by MIKO, showcasing our cross-border capacity and pro-activeness. Examples like these abound in IMAP. In short, a lot depends on the ability to seize an opportunity, and precision in execution.

This document highlights our geographic reach across vast continental territories, as well as our presence in smaller geographic units. See how we can make a broad global presence click with intense involvement in local markets.

We share with you in this book our Values, those of the firm and its people. We have intercalated them throughout the text, instancing them through videos and testimonials, to show you who we are: the seasoned professional enthusiastic about deal making and excellence, or the young professionals drawn to IMAP for accelerated learning and experience.

Successful teams are made up of people with shared values. What will you feel when you see these values illustrated by individuals?

Well, just that at IMAP there are great people to work with; how comfortable they are with each other and their professions. That’s what makes our clients happy to work with us!

Let’s work together!

Gilberto Escobedo

10

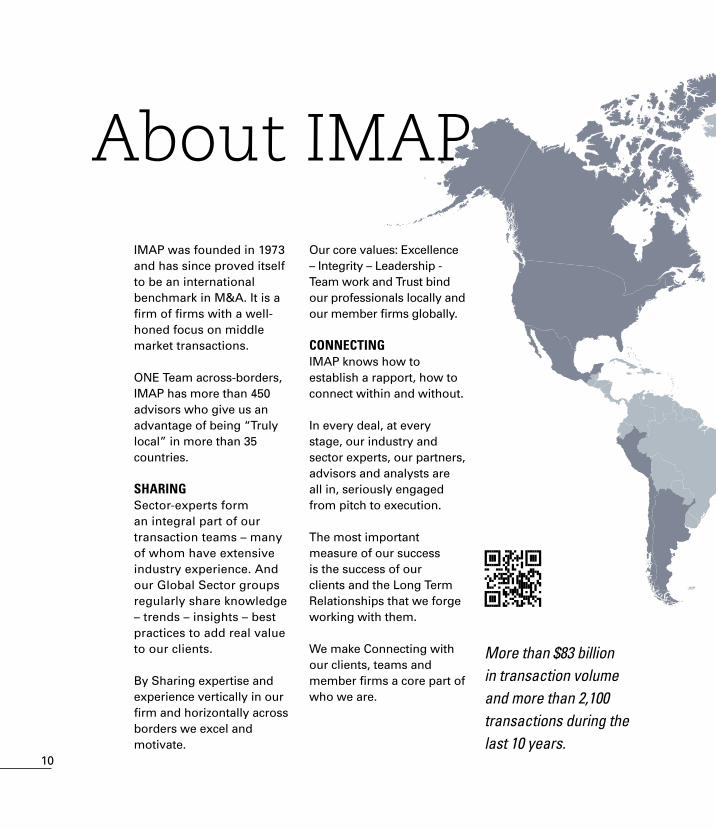

IMAP was founded in 1973 and has since proved itself to be an international benchmark in M&A. It is a firm of firms with a well-honed focus on middle market transactions.

ONE Team across-borders, IMAP has more than 450 advisors who give us an advantage of being “Truly local” in more than 35 countries.

ShArIng Sector-experts form an integral part of our transaction teams – many of whom have extensive industry experience. And our Global Sector groups regularly share knowledge – trends – insights – best practices to add real value to our clients.

By Sharing expertise and experience vertically in our firm and horizontally across borders we excel and motivate.

Our core values: Excellence – Integrity – Leadership - Team work and Trust bind our professionals locally and our member firms globally.

COnneCtIngIMAP knows how to establish a rapport, how to connect within and without.

In every deal, at every stage, our industry and sector experts, our partners, advisors and analysts are all in, seriously engaged from pitch to execution.

The most important measure of our success is the success of our clients and the Long Term Relationships that we forge working with them.

We make Connecting with our clients, teams and member firms a core part of who we are.

About IMAP

More than $83 billion in transaction volume and more than 2,100 transactions during the last 10 years.

11

IMAP AdvISoRS ARe loCATed THRoUGHoUT NoRTH ANd SoUTH AMeRICA, eASTeRN ANd WeSTeRN eURoPe ANd ASIA.

Argentina

Belgium

Bosnia and herzegovina

Canada

Chile

China

Croatia

Czech republic

Denmark

egypt

Finland

France

germany

hungary

India

Ireland

Italy

Japan

Mexico

netherlands

norway

Peru

Poland

Portugal

russia

Serbia

Slovenia

Spain

Sweden

Switzerland

turkey

united kingdom

united States

Vietnam

every business day - somewhere in the world - an IMAP advisor is closing an M&A transaction!

12

IMAP HISTORY TIMELINE

Founding of IMAP by a group of US-based M&A Practitioners under the acronym

NAMAC

Merger of two US-based M&A advisory

organizations (IN-TERMAC and IMAP)

into one.

Presence in UK, France, Germany Spain and Italy.

Merger of Central and Eastern European

organizations (MACEE) into IMAP.

1973 1993 1999 2005

Source: Thomson Reuters

gLObAL PERfORMANcE 2011-2013

Rank financial Advisor

1 KPMG

2 PricewaterhouseCoopers

3 Ernst & Young LLP

4 Rothschild

5 Goldman Sachs & Co

6 IMAP7 Deloitte

8 Lazard

9 Morgan Stanley

10 BDO

undisclosed Values & Values up to $500 million(Based on number of transactions)

in the world in the number of closed transactions valued up to

US$500 million

6th

13

Consolidation of cross-bordercollaboration.

IMAP adds more global locations.

IMAP adds Peru, Norway, Vietnam and

in talks to incorpo-rate more LatAm and

Asia locations.

2008 2010 2014

gLObAL PERfORMANcE 2011-2013

in the world in the number of closed transactions valued up to

Source: Thomson Reuters

US$200 million

Rank financial Advisor1 PwC

2 KPMG

3 Ernst & Young LLP

4 IMAP5 Deloitte

6 Rothschild

7 BDO

8 Lazard

9 M&A International

10 Goldman Sachs & Co

undisclosed Values & Values up to $200 million(Based on number of transactions) 4th

Integrity

IMAP will never compromise standards

in order to get a transaction done

either from a timing perspective or by violating

any confidentiality or legal requirements…

Even if it means losing our fees

Sector expertiSe

“We speak your language”

16

We bring to the table strong Sector Expertise

who share thanks to our global sector-groups

Knowledge - trends - best practices

Many of our professionals have strong hands-on

experience and insights into the industry

17

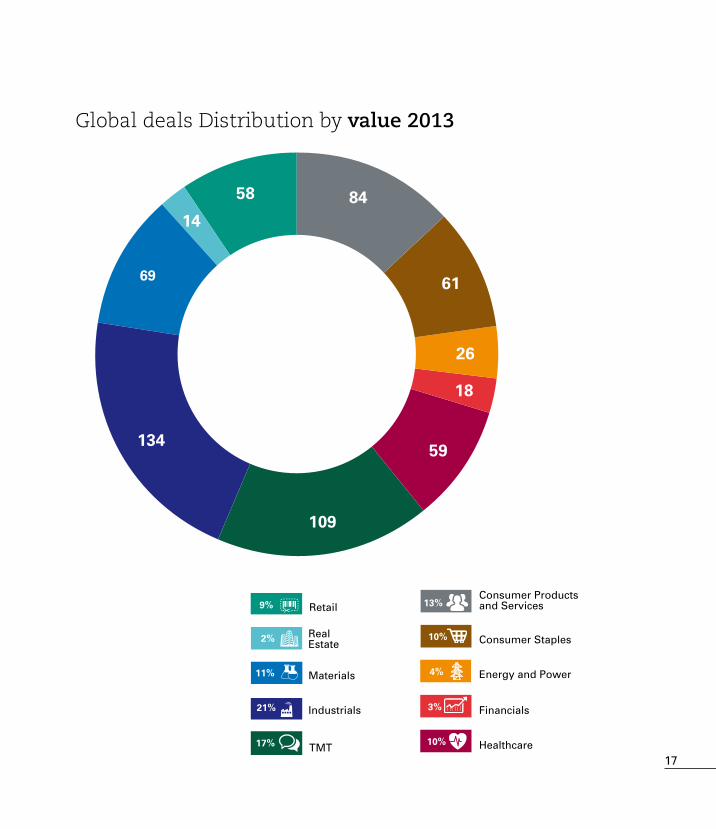

Global deals Distribution by value 2013

84

61

26

18

59

109

134

69

14

58

TMT

Industrials

Materials

Real Estate

Retail9%

2%

11%

21%

17%

Consumer Products and Services

Consumer Staples

Energy and Power

Financials

Healthcare

13%

10%

10%

4%

3%

18

In 2008 and 2009 a dramatic decline in the production volume of vehicles shocked everyone, as it was almost unheard of in the automotive industry. Rates of decline on this scale could only be found as far back as the Great Depression in the US. This crisis impacted every industry player, from Tier 3 suppliers to General Motors, who had to be bailed out with government funds.

Since 2010 the sector has been experiencing a slow, steady growth - especially in the emerging economies, although somewhat uneven across the board. In the case of the BRICS, not all are growing at the same rate.

China is the main driver in the automotive sector, outpacing the rest. Currently producing 11 million vehicles per year, the number is expected to grow to 35 million by 2020.

India and Russia are growing at a slower pace while Brazil has stagnated. The players from the mature markets, such as the U.S. and Western Europe, see their growth coming from enhanced sales in China. The MINT countries (Mexico, Indonesia, Nigeria, Turkey) are, on the other hand, starting to out-produce the BRICS (and in some cases also outsell them), together with Vietnam and Malaysia.

OEMs are now in the process of reducing the number of their Tier 1 suppliers. This could start knocking over the dominoes, given that Tier 1 providers are in turn forced to shed suppliers. Moreover, both OEMs and Tier 1 want global suppliers, which is starting to drive M&A in the sector, leading to both sector consolidation and stimulation of local company acquisition

in markets where a lack of presence is manifest.

The environmental regulatory context is also impacting M&A. Vehicle weight is becoming critical to CO2 emissions compliance and manufacturers know this. They now need to incorporate lighter materials, and increase the proportion of aluminum and plastics, which involves a technological shift.

Therefore, companies must either invest in R&D or acquire companies with this know-how.

We expect steady growth in the automotive sector for the next 10 years.

Automotive is not a sector with 12-14 times EBITDA multiples. Although in emerging markets you can find EBITDA X 8 multiples, 5-6 is the norm. While interest in investing in Western Europe is generally waning, there is some interest in Eastern Europe (Czech Republic, Poland) and some other markets. But it is in Mexico, China and India where the highest EBITDA multiples are being hit.

Automotive

José-María Alberú, Spain

19

In M&A activity, Private Equity has always displayed a tremendous interest in chemicals, particularly in the USA and Europe.

One of the drivers for the Chemicals market has been increasing Private Equity appetite, especially of large multinationals, for non-core assets.

Another key factor driving M&A in Chemicals is the huge development of Oil & Gas in North America. Energy costs have declined and raw materials are increasingly available to the chemical industry. This tandem of bountiful supply at lower cost is becoming a key driver in re-setting the market dynamics in the chemical industry, thus contributing to a significant degree of repatriation of production from emerging economies.

North America is beginning to satisfy its own demand in the chemical market (availability of raw

Constantine Biller, UK

materials in the value chain). We could also see this phenomenon emerge elsewhere, specifically in the UK.

Agrochemicals and crop chemicals are two more M&A drivers, unleashing positive dynamics due to the rising demand for high quality food. Moreover, certain world regions are fast becoming more developed and experiencing stiffer demand.

Another M&A market driver today is made up of pharmaceutical ingredients to tend to aging populations in certain parts of the world and the concomitant swelling demand for high quality healthcare.There has also been a major increase in personal care and households products.

Chemicals

The global High-Technology sector, spanning industries in e-commerce, computers and peripherals, software, internet software (such as mobile applications) and services, is fast-paced and scoring tremendous growth-rates over the past few years.

Technology is playing a critical role in many industries since machines and products are getting smarter (production 4.0) and intelligent networks coordinating the efficient use of resources are developing rapidly. An innovation-driven high-tech industry will be an engine for sustainable

High Technology

growth across a wide range of industries going forward.

China is the largest high-technology market in the world (over €950bn in 2012 – followed by the United States with €840bn and Europe with €670bn). In M&A terms, there were nearly 5,000 transactions globally in Telecommunications and IT in 2013, with average EBIT- or EBITDA-Multiples ranging from 6.3 to 8.4.

Our outlook is that the M&A high-technology market will expand even more, especially due to the continuous development of cutting-edge technologies.

More and more key players are seeking to acquire competitors that have a remarkable, unique selling proposition. They are also looking for transactions with a game-changing impact. Other key market drivers include the growing demand for cloud-based technologies, new, innovative materials (e.g. RFID-chips in clothes)

or mobile products (e.g. Apps for mobile phones or “Internet of Things”), which still have swift market anticipation. Internet-based business models are also evolving over time and spreading to more and more diverse areas (virtual market places, advertising, social networking services, etc.). Therefore, in order to bolster market position or stay competitive in the future, companies must stay ahead of the market through innovation, partnerships, and decisive leadership.

We understand that innovation and creativity play an important role in the success of companies operating in such a challenging environment. IMAP is ranked among the top five M&A Advisors in this sector involving companies with revenues up to $200m. Therefore, over the past two years, IMAP and its dedicated, cross-border, sector-expert teams, has successfully advised on more than 50 High Technology transactions worldwide.

Dr. Heiko Frank, Germany

21

In the pharmaceutical industry, M&A activity shattered records in 2013 in terms of deal numbers. There were three major drivers responsible for this:

Valuations of companies with products in development spiked dramatically, a sign that large pharmaceutical companies are competing more fiercely than ever in terms of innovation, particularly in the highly coveted launches of drugs that treat rare (“orphan”) diseases.

A plethora of M&A deals were also tax-driven: American companies applied inversion in order to shift their tax base to Ireland. Transactions of this type prompted many of the heftier M&A deals in 2013.

More diversified groups such as Novartis, Merck, Sanofi, Baxter and Pfizer began to focus on selling or spinning off businesses.

Pharmaceuticals

Christoph Bieri, Switzerland

We expect the M&A market to cool over the next twelve months. Valuations of public, development-stage companies are already smarting from the pricing issues impacting some of the newest innovative drugs, such as Gilead’s Sovaldi (used to fight HCV). Moreover, the American government is eyeing regulatory changes for inversions. Nevertheless, the break-up of larger groups will spark substantial, large-transaction activity.

In China deal-making came to a stand-still because of the government inquiry into the marketing practices of multinational companies operating in the pharmaceutical market. Almost all major pharmaceutical companies in China fell under government scrutiny, which made planning impossible while jacking up acquisition risk. Now that most of the investigations have been

settled, we expect deal-making activity to reboot.

India remains a burgeoning pharmaceuticals market with exciting growth prospects. The recent manufacturing problems faced by Indian generic drug producers will certainly be worked out and inbound acquisitions will heat up as a result. We should also not fail to mention that the global aspirations of major Indian pharmaceutical groups have been escalating, which could lead to larger outbound transactions.

LeadershipIMAP is a leadership multiplier

not just because it ranks consistently

amongst the Top 5

in the Middle Market league tables

It is about how we do business

How our people are empowered

We live our values

excellence & integrity

forging long-term relationships

global reach

Since 1973,

IMAP has grown across different geographies

keeping in tune with our client’ needs

Already present in 35+ countries

we continue to grow our presence to ensure that we

serve our clients globally!

Cross border transaCtions and % of Cross border deals

40

35

30

25

202006 2007 2008 2009 2010 2011 2012 2013

% of Cross Border DealsTrend Line

26% 25%

30% 30%

33% 33%

28%29%

25

26

china

interChina (IMAP in China) is an M&A and strategy advisory firm founded in 1994

over the last 15 years, InterChina has become one of the leading boutique corporate advisors in China

interChina now employs more than 60 specialized advisors, with two offices in China (Beijing and Shanghai)

More than 150 transactions successfully closed, translating into $3.5 billion plus in overall deal value

chinainterChina

27

The Chinese economy continues to chalk up impressive growth rates. After hitting a soft patch in the first two quarters of 2013, it ended the year with 7.7% growth, practically the same rate as in 2012 (7.8%). High frequency indicators rebooted after the summer with a high degree of stability in the most commonly watched business barometers, with retail sales, industrial production and PMI all moving in a narrow range. Inflation remained relatively subdued throughout 2013, although it has edged up in recent months to 3%.

Nevertheless, there are rising concerns as the shift in the composition of demand away from investment and towards consumption, which we saw in 2012, made an about-face in 2013. Storm warnings have also appeared in the financial sector, which has experienced rapid credit expansion, and several recent spikes in inter-bank interest rates. Therefore, while high frequency indicators remain steady, and the short-term forecast is unchanged at 7.4% for both 2014 and 2015, significant risks are stalking China.

eduardo Morcillo Managing Director

28

since 1995, redbaenK has had a long record of accomplishments in the corporate finance field in the Czech and Slovak markets

ranking among the Top 3 in the Czech market

team of experts has gained extensive experience from successfully managing and closing transactions offering value to its clients

czech republic & SlovakiaiMaP in CzeCh rePubliC: redbaenK

29

richard KovárPartner

The Czech M&A market in 2013 strengthened both in deal volume and aggregate deal value. Once again the Czech Republic in 2013 was one of the hottest CEE markets for M&A. Two major transactions, such as the TELEFONICA divestment from the Czech market (e2.5bn) and the acquisition of Net4Gas – transmission systems operator sold by RWE (e1.2bn) represented the two largest transactions in the entire CEE. M&A activity in 2013 was mostly centred on energy, telecom, real estates and media.

The number of transactions rose by approximately 50 per cent, and the main role is still played by local financial investors, such as PPF, EPH, KKCG or PENTA. This is in line with the general trend of the last few years in which local strategic and financial investors have dominated the Czech M&A market, which is driven by consolidation and the defensive strategies of various international

groups. Czech investors were also relatively active in neighbouring countries as EP Industries acquired Eastern European assets of the waste management company AVE. Growing cross border activity of Czech investors has consolidated a long-term process that is expected to continue.

2014 should bring growth again to the Czech economy. After two years of sliding GDP, the economy rebooted in Q4 2013. GDP is currently driven by stiff industrial production boosted by the depreciation of the Czech Crown in November 2013, which will have a positive impact on household and government spending. Optimistic forecasts for Czech market growth should enable foreign investors to become more valuation competitive. We therefore expect increased cross border transactions in 2014 and more transactions in sectors such as manufacturing, retail & distribution and healthcare.

The automotive industry is the backbone of the Czech economy and a strong connection to German automotive manufacturers provides relative stability to the Czech economy in a turbulent global environment. The lowest interest rates on record and easing bank financing terms cement the foundations for the next acceleration of M&A activity.

iMaP M&a Consultants AG is a full service M&A firm committed to providing unsurpassed M&A advisory services

independent Advisory firm offering financial services to the middle-market: mid-size companies, Subsidiaries, Holding companies & Family owned businesses

30

germanyiMaP in GerMany: iMaP M&a Consultants aG

31

2014 activity is driven by following factors:

Overall, the German economy is healthy.

Stock market valuations are high, perhaps too high for current earnings. But while earnings are rather robust, valuations may slip in the next consolidation. Therefore, stock assets have little room to advance further.

Interest rates have been at all time lows for several years. Accordingly, asset managers have a hard time making investment decisions.

Many family firms have re-directed their focus from low interest bonds to direct investment, i.e., private companies, and mezzanine and debt funds.

As a consequence, family firms and Private Equity groups are desperate to find businesses to invest in. However, these assets are not easy to find. IMAP helps family firms build their portfolio. The market has clearly shifted from a seller’s market to a buyer’s market. Most solid businesses,

across all sectors, are being approached even before they come to market.

Direct investment by family firms is in serious competition with classical Private Equity Funds. PE funds have slipped and more and more former PE specialists are now managing the direct investment by family businesses.

On the strategic side, people are still looking to the Far East. Anyone who wants to play a role in industrial markets in the future must be present in Asia, especially China, India, and the SEA. There is a lot of two-way activity – German companies investing in Asia and vice-versa. We have recently signed such a deal in the automotive industry. Industry consolidation is taking place mainly in two sectors: Automotive and Energy.

The Automotive industry as a whole is generating excellent results, although much of the growth is in Asia while Europe is declining. Tier 1 and Tier 2 suppliers are even being

forced to move into Asia, following their OEMs. Tier 2 and Tier 3 suppliers often do not have the financial and management capacity for this and are looking for integration into other structures in order to achieve critical mass. Anyone with revenues under €100M is going to find it hard to survive in the automotive sector, unless they have a technological niche.

The change in government energy policy has caused turmoil at all levels of the energy sector. Renewables relying on subsidies are under pressure and the big energy suppliers are suffering from the shutdown of nuclear power. The entire industry will be reconfigured, and, accordingly, there will be a lot of activity although deals will be difficult given all the uncertainty.

Karl fesenmeyer President

one of india’s leading advisory firms focussed on Investment banking, o3 Capital provides advice to its clients globally on a gamut of strategic transactions, including mergers, sell-side and buy-side advisory, leveraged buy-outs and other restructurings

iMaP in india: o3 CaPital

INDIa

o3 provides independent, research-driven advice to help clients glean the maximum value from their transactions

Bangalore

32

33

Gaurav Khungar Managing Director

restartinG the investMent CyCleIndustrial investment themes have historically rewarded investors only over specific parts of the investment cycle given that relative to other emerging markets the Indian economy has been more closed and insular.

Capital allocations by large conglomerates in India has been biased to overseas rather than Indian investment. It is now evident that the new Government will improve the investment cycle by consistently attracting Foreign Direct Investment, which will also stimulate domestic private sector capital expenditure. This investment upcycle should be visible in the latter part of the next 12 months and drive considerable cross border M&A whilst Indian demographics will continue to favour a steady growth in consumption. This is an enduring theme.

India will stimulate the economy by building infrastructure, enhancing banking systems and

lending to consumers. Learning from the past will result in a focus on domestic demand replacing the traditional reliance on international trade. Sectors that are expected to gain the most include Capital Goods, Construction and Materials, and Transportation. The anticipated number of skilled people joining the work force over the next 5 years offers investment opportunities in creating/expanding a services model catering to the clients of global conglomerates across the engineering goods sector – similar to the success of India in the Information Technology space. Over the next 5 years India will witness greater entrepreneurship and the clearest investment opportunities playing on the demographics in the healthcare and consumer space.

Pinnacle advises its clients in every step from strategy planning to transaction execution

Japana changing M&a marketplace

34

iMaP in JaPan: PinnaCle.

35

Among the world’s leading economies, one of the most noteworthy shifts in economic and corporate outlook has occurred recently in Japan. Since Abe became Prime Minister in 2012, the Japanese economy as a whole and Japanese corporations have been driven by government reforms and export growth. These two policy “arrows” from Abe’s quiver have already hit some targets, while a third – private sector growth – is gradually being implemented. Both business optimism and land prices have been recovering.

But with a declining population, Japanese companies cannot rely on a domestic turnaround. Since 2009/2010 Japanese companies have been aggressively pursuing cross-border acquisitions. Outbound acquisitions are ascendant (and as a percentage of total acquisitions as well), buttressed by buoyant corporate balances (at a record high of $3 trillion at March 2014), as well as

increased bank lending, thanks to the BOJ.

We see Japanese companies taking on more challenging deals and not being afraid to fight for the deals they seek. In the large-cap company spectrum, for example, Softbank (Japan’s third-largest telecom group) acquired control of Sprint (US) in a $20bn+ deal. Suntory (a beverage group) acquired Beam (US) in a deal valued at some $16bn. Similar trends are seen in the M&A middle market as Japanese firms are

deal-making in emerging markets, especially in Southeast Asia.

In spite of the outbound M&A focus, in the last 12-18 months there also been increased interest in inbound M&A. A devalued yen (-20% since 2013) has sucked down acquisition costs. But even before this macro change, Pinnacle (IMAP Japan) witnessed a number of companies seeking a place in Japan’s large domestic markets where there is often no meaningful competition from foreign players.

36

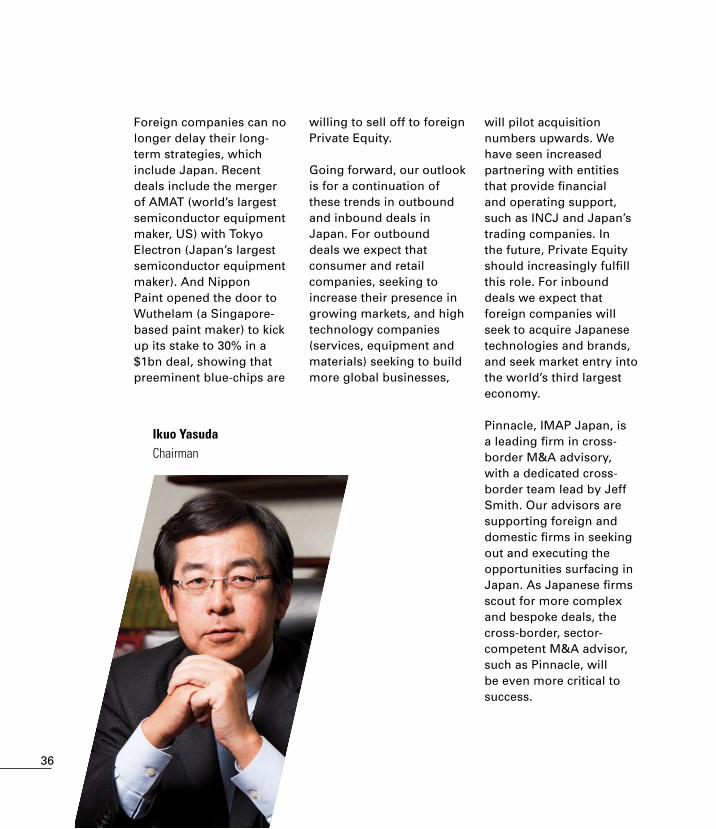

Foreign companies can no longer delay their long-term strategies, which include Japan. Recent deals include the merger of AMAT (world’s largest semiconductor equipment maker, US) with Tokyo Electron (Japan’s largest semiconductor equipment maker). And Nippon Paint opened the door to Wuthelam (a Singapore-based paint maker) to kick up its stake to 30% in a $1bn deal, showing that preeminent blue-chips are

will pilot acquisition numbers upwards. We have seen increased partnering with entities that provide financial and operating support, such as INCJ and Japan’s trading companies. In the future, Private Equity should increasingly fulfill this role. For inbound deals we expect that foreign companies will seek to acquire Japanese technologies and brands, and seek market entry into the world’s third largest economy.

Pinnacle, IMAP Japan, is a leading firm in cross-border M&A advisory, with a dedicated cross-border team lead by Jeff Smith. Our advisors are supporting foreign and domestic firms in seeking out and executing the opportunities surfacing in Japan. As Japanese firms scout for more complex and bespoke deals, the cross-border, sector-competent M&A advisor, such as Pinnacle, will be even more critical to success.

willing to sell off to foreign Private Equity.

Going forward, our outlook is for a continuation of these trends in outbound and inbound deals in Japan. For outbound deals we expect that consumer and retail companies, seeking to increase their presence in growing markets, and high technology companies (services, equipment and materials) seeking to build more global businesses,

ikuo yasudaChairman

37

Team Work

ONE Team

Working Together – Across Borders

38

With more than 20 years of experience in Corporate Finance Advisory, Serficor is the most effective independent investment bank in Mexico with a strong global reach

iMaP in MexiCo: serfiCor Partners

Mexico

39

Gabriel Millán Partner

In 2013 Mexico attracted $35 billion USD in Foreign Direct Investment, a record year. We expect this trend to continue in 2014 with an expected GDP growth of 3.5%. Expectations for 2014 include a lower inflation rate against those of other emerging economies, a strong Mexican Peso and stable interest rates.

Several key reforms have been implemented by the Mexican Government (Energy, Telecommunications, Tax law, Financial Services, Labor law, and Anti-Corruption initiatives). We expect that the effects of these reforms will initially materialize in the second half of 2014 and beyond.

The fine print on the regulations accompanying the reforms will be crucial in determining how much interest major players (financial and strategic) will have in investing in Mexico.

The Outlook for M&A in Mexico in 2014 and beyond is positive. We expect to see deal volume

pick up after the effects of the reforms are perceived. Deals could range from the tens of millions into the billions, considering that there are companies in Mexico offering value across all markets. We see the energy, distribution, healthcare, financial services, and retail and consumer sectors to be the most attractive with acquisition multiples similar to the past. The most attractive companies will command an acquisition premium.

40

russia

advance Capital is one of the leading providers of investment banking services in Russia and the CIS, with a focus on mid-cap companies

iMaP in russia: advanCe CaPital

41

at a slower pace than in the past, due to a weaker exchange rate. The current-account surplus is expected to gradually diminish by 2015.

evgeny antipovManaging Director

russia on the riGht PathRussia recovered briskly after the financial crisis of 2008-09, but the pace of growth has since slowed, reflecting both domestic and external weaknesses, such as the economy’s over-reliance on commodity exports, its low investment rate, and lagging competitiveness. GDP growth more than halved from 3.4% in 2012 to 1.3% in 2013, although is expected to rebound to 2.3% in 2014 and 2.7% in 2015. The 2014 outlook is for a moderate uptick in growth, reflecting both improving global prospects and upbeat domestic economy expectations – as measured by a rising composite Russian PMI (52.5 at December 2013, the highest level since March 2013).

Household consumption growth is expected to remain strong, while slowing due to a slightly negative trend in employment and an increasing household debt burden, which is squeezing real disposable

income. Government spending is expected to pick up slightly over the forecast horizon, spurred by government plans to boost infrastructure investment through public-private partnerships and financing from the National Welfare Fund.

A rebound in investment should be among the main drivers of GDP growth in 2014-15. Private investment is expected to return to positive territory as the temporary factors that were a drag on 2013 investment (completion of large one-off investment projects) are expected to taper off. Russia’s economy is widely considered to be running at close to capacity, which should underpin investment recovery, although this is expected to be gradual given vestigial frailties in the business climate. Export volume growth is expected to accelerate in 2014 and 2015, mirroring the anticipated recovery in the main export markets. Imports are set to pick up on the back of higher final demand, although

42

iMaP in sPain: ClearWater international iberiaSpain & Portugal

the firm has sector expertise in IT, Chemicals, Healthcare, Construction and Infrastructure, Clean Energy, Media and business process outsourcing

Clearwater international Iberia provides M&A, corporate finance and asset management services to mid-size companies in Spain and Portugal looking to expand their value through acquisitions, financing, and divestments

43

sPain is baCK!Spain’s incipient economic recovery is forecasted to consolidate in the coming quarters, backed by improved confidence and the easing of financing terms. While the Spanish economy is expected to continue rebalancing, the contribution to growth from external demand is expected to ebb. Employment is expected to begin to grow and the unemployment rate to retreat gradually, amidst continued moderation in unit labor costs. The budget deficit is set to narrow in 2014 although government debt will continue to expand.

Spain has returned to positive GDP growth since the third quarter of 2013, amidst improved confidence and some relaxation of financing terms.

Spain successfully exited the Financial Assistance Program for the Recapitalization of Financial Institutions while the Spanish financial markets continue to stabilize

now that sovereign-bond yields are bottoming at fresh lows. In general, financing conditions have improved, although they remain onerous for some borrowers, especially for SMEs. Despite these improvements, still elevated debt levels and high unemployment weigh on growth prospects and make Spain vulnerable to adverse shocks.

Javier Pérez-farguell Managing Director

david serra Managing Director

44

leadership position amongst financial institutions in Turkey in terms of number of deals closed

3 seas Capital Partners is the leading corporate finance house in Turkey in M&A

since its inception, the firm has completed 87 successful M&A transactions worth $.5 billion

TurkeyiMaP in turKey: 3 seas CaPital Partners

45

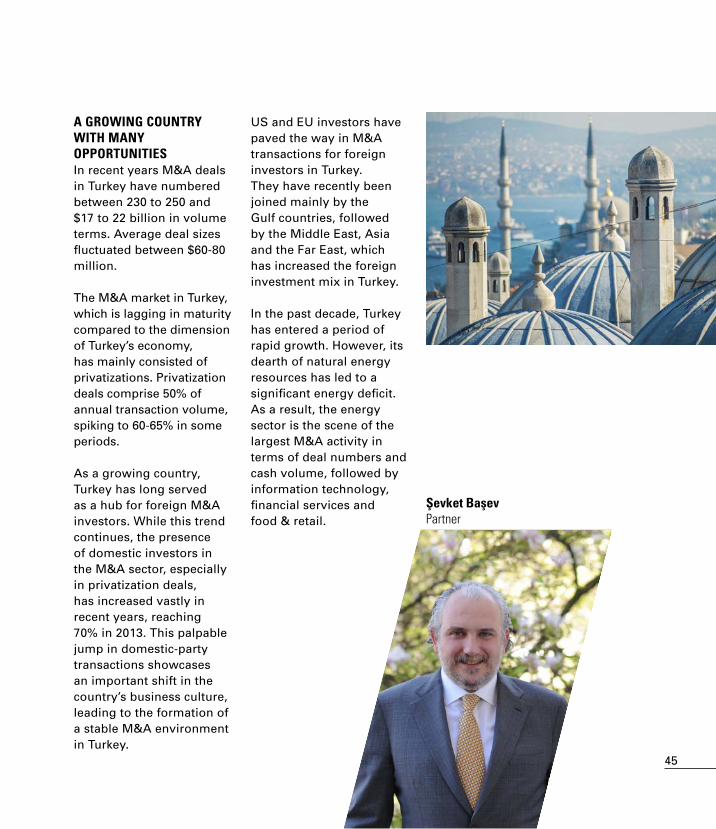

a GroWinG Country With Many oPPortunitiesIn recent years M&A deals in Turkey have numbered between 230 to 250 and $17 to 22 billion in volume terms. Average deal sizes fluctuated between $60-80 million.

The M&A market in Turkey, which is lagging in maturity compared to the dimension of Turkey’s economy, has mainly consisted of privatizations. Privatization deals comprise 50% of annual transaction volume, spiking to 60-65% in some periods.

As a growing country, Turkey has long served as a hub for foreign M&A investors. While this trend continues, the presence of domestic investors in the M&A sector, especially in privatization deals, has increased vastly in recent years, reaching 70% in 2013. This palpable jump in domestic-party transactions showcases an important shift in the country’s business culture, leading to the formation of a stable M&A environment in Turkey.

US and EU investors have paved the way in M&A transactions for foreign investors in Turkey. They have recently been joined mainly by the Gulf countries, followed by the Middle East, Asia and the Far East, which has increased the foreign investment mix in Turkey.

In the past decade, Turkey has entered a period of rapid growth. However, its dearth of natural energy resources has led to a significant energy deficit. As a result, the energy sector is the scene of the largest M&A activity in terms of deal numbers and cash volume, followed by information technology, financial services and food & retail.

sevket basevPartner

46

United Kingdom

Clearwater international uK (iMaP uK) is a leading independent mid-market corporate finance advisory firm operating in the UK and internationally, with an exceptional track record of more than 400 completed transactions

through its four uK offices, Clearwater International UK advises on all aspects of corporate finance transactions including mergers and acquisitions, divestments and MBOs

Clients include large corporations, private equity firms, management teams, and owner-managers. The size of Clearwater International UK’s team and the deals on which it advises make the firm the most active, independent corporate finance house in UK

iMaP in uK: ClearWater international – uK

Michigan

47

stronG eConoMiC GroWth drives businessUK is the fastest growing economy in the G7. Expected GDP growth for 2014 comes in around 2.9%.

Keys to the UK recovery comprise a very effective use of QE by the Bank of England and appropriate public expenditure by the Government in transport and infrastructure.

Manufacturing is a real source for growth in the UK along with many government initiatives, such as tax incentives and a huge extensive training program, as well as repatriation from manufacturing. Because of debt market improvement, banks are much more receptive to providing funding opportunities, which is what’s driving private equity appetite.

Mike reevesCEO

48

USaaMherst Partners

founded in 1994, Amherst Partners is completely independent and one of the Midwest’s largest and most reputable boutique investment banking and restructuring & turnaround consulting firms

With offices in Birmingham and Ann Arbor (Michigan) and Chicago (Illinois), Amherst is focused on providing middle-market companies with financial advisory expertise for mergers and acquisitions, corporate restructurings and management consulting

a team of seasoned, hands-on problem solvers linked by our commitment to establishing a “trusted advisor” relationship with our clients and referral partners

49

the year that Wasn’tDespite a softer than expected 2013 with volumes at their lowest levels since 2009, we are encouraged by some year-end 2013 momentum and a very strong start in 2014. We also find it hard to ignore the supportive fundamentals that continue to exist in the M&A market today. The dynamics include strong corporate earnings and cash balances, receptive credit markets, attractive interest rates and record levels of investable funds held by Private Equity firms. As a result, we expect 2014 to see an uptick in dealmaking activity from 2013 levels.

The U.S. M&A market saw a decline in activity in 2013, with the total number of transactions announced (9,263) falling 11% from 2012 (10,419). Focusing on transactions with $25 million to $250 million of total transaction value, middle-market activity saw an even larger drop-off, falling 18% from 2012 levels (982 deals announced in 2013 versus 1,191 in 2012).

scott eisenbergManaging Partner and

Co-Founder

50

Trust We invest in

Trust based Relationships

with our clients…

For several years IMAP Belgium had been asking itself what its client, MIKO, needed. Various targets in Turkey and Central Europe turned out not to be the right fit. After the mandate came in, the IMAP network lit

MikoSuccess Story: MIKO

up and our Belgian and Danish professionals found the right targets and deals were signed.

Success was based on loyalty to client, long-term involvement and cross-border focus.

51

Why IMaP?

Connect and Share

For IMAP, strong long-term connections are thecornerstone of successful deal-making.

They motivate and lead the way!

And sharing takes us beyond what the individualprofessional and the member firm can do.

It is at the core of our team-making process!

By sharing we bring out theCross-border Excellence and Sector Expertise that can make or break a deal.

Connect & Share - a simple formula that is as basic asour values of Trust and Integrity.

Connect & Share - it is what our clients seek whenworking with us and it is how we work for them.

Let’s Work Together.

Video compilation

Corporate video

Sector Expertise

Cross Border

China

Excellence

Integrity

TeamWork

Trust

Miko

Why IMAP

53

54

©IMAP, Inc. 2014

IMAP, Inc. Av. Diagonal, 618 08021 Barcelona - Spain www.imap.com

Related Documents