ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS COPY RIGHT © 2011 Institute of Interdisciplinary Business Research 834 SEPTEMBER 2011 VOL 3, NO 5 The impact of regulatory framework and bank initiatives on the adoption of internet banking in Iran Mahmoud Manafi Department of management and accounting, Marvdasht Branch, Islamic Azad University, Marvdasht, IRAN Mehrdad Salehi MBA student, MSU, Faculty of Management Roozbeh Hojabri DBA student, MMU, Faculty of Management Reza Gheshmi Department of management and accounting, Marvdasht Branch, Islamic Azad University, Marvdasht, IRAN Darioush Jamshidi MBA student, MMU, Faculty of Management Pagah Khatabi MBA Student MMU, Faculty of Management Abstract This quantitative research attempts to measure the impact of important factors on Trust and also Adoption on Internet Banking. The motivation for this study is the belief that the poor response to Internet banking in Iran springs from an inadequate Regulatory Framework for customer protection and the lack of initiatives on the part of the banks in promoting this new delivery channel. In an attempt to find support for this belief, data was also collected from three cities (Tehran, Shiraz, and Isfahan) in Iran. Key words: Trust, Interface design, Regulators and risk, Role of government, Regularity controls, Bank initiative, Promotion and marketing, Value added, and Adoption on Internet Banking 1. Introduction In recent years, by developing the telecommunication and technology data, the banking industries got many changes. Nowadays, most of the customers are interested on using ATM machines for their needs such as witch drawls, transfers, balance inquiries and other conveniences. As a matter of fact, based on the beliefs of Guru et al. (2000), although internet banking has too many advantages, but the adoption of the customers both in terms of

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

834

SEPTEMBER 2011 VOL 3, NO 5 The impact of regulatory framework and bank initiatives on the

adoption of internet banking in Iran Mahmoud Manafi

Department of management and accounting, Marvdasht Branch,

Islamic Azad University, Marvdasht, IRAN

Mehrdad Salehi

MBA student, MSU, Faculty of Management

Roozbeh Hojabri

DBA student, MMU, Faculty of Management

Reza Gheshmi

Department of management and accounting, Marvdasht Branch, Islamic Azad University,

Marvdasht, IRAN

Darioush Jamshidi

MBA student, MMU, Faculty of Management

Pagah Khatabi

MBA Student MMU, Faculty of Management

Abstract

This quantitative research attempts to measure the impact of important factors on Trust and

also Adoption on Internet Banking. The motivation for this study is the belief that the poor

response to Internet banking in Iran springs from an inadequate Regulatory Framework for

customer protection and the lack of initiatives on the part of the banks in promoting this new

delivery channel. In an attempt to find support for this belief, data was also collected from

three cities (Tehran, Shiraz, and Isfahan) in Iran.

Key words: Trust, Interface design, Regulators and risk, Role of government, Regularity

controls, Bank initiative, Promotion and marketing, Value added, and Adoption on Internet

Banking

1. Introduction

In recent years, by developing the telecommunication and technology data, the banking

industries got many changes. Nowadays, most of the customers are interested on using ATM

machines for their needs such as witch drawls, transfers, balance inquiries and other

conveniences. As a matter of fact, based on the beliefs of Guru et al. (2000), although internet

banking has too many advantages, but the adoption of the customers both in terms of

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

835

SEPTEMBER 2011 VOL 3, NO 5 financial loss and individual problems which stemming from the internet had not undergone

well in worldwide. The first issue may be happened because of the robberies from the bank or

other risk such as frauds and forgeries. . According to this issue, Iranian bank are going to

guarantee their customers deposits. The second issue is considered as the same protection

couldn’t be able to afford to those internet banking accounts.

However, internet banking has too many advantages. (Littler and locket, 1997)Such as 24

hours services,(pikkaranen et al. 2004) reduce cost of the bank and help the bank to use their

expenses on other business (buyers and lederer, 2001; Alstad, 2002; Pyun et al.2002 ).

Obviously, despite the availability of all these continence but only 2% of the customers in

IRAN used internet banking. So much so, the first problem statement coming in the mind is:

1: is the law covering of internet banking and financial transactions electronically are

adequate and sufficient?

2: are the banks in IRAN are going to do their role to instill trust and confidence for the

customers to get their satisfaction to accept internet banking comfortably?

The aim of this paper is to cover an investigation about the influence of the bank imitative on

adoption of internet banking in IRAN. Based on this study, it's all about the interest of the

customers to accept internet banking according to their trust and confidence .to this regard, it

can be followed as:

1: all the issues and factors that influence on internet banking in IRAN.

2: psychological or behavioral factors that affecting on trust when they keen on adopts

internet banking or on their attitudes while they are doing risks.

3: figure out the differences between the influence of design and value with together at the

time of adoption of internet banking and awareness.

2. Literature review

The aim of this chapter is to review all the factors from the literature that influence on

internet banking.

For the technology acceptance that effect on individual's behavior, three theory of reasoned

action (TRA), technology acceptance model (TAM) and planned behavior (TPB) are figured

out.

The first theory (TRA) is generally consisting of four steps mentioned as subjective norms,

behavioral attitudes, intention and actual usage. Refer to Ajzen 1985) ,he developed TRA by

introducing another factor named as controlling of perceiving behavior that could be able to

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

836

SEPTEMBER 2011 VOL 3, NO 5 forecast behavioral aims and intention .this model is mentioned as planned behavior theory

(TPB). After that another researcher, Davis (1989) extended another theory of (TAM)

technology acceptance model. Usefulness and ease of used that perceived in TAM are the

basic features of these perceptions. The definition of useful perception is the level of

individual's beliefs when using a particular technology which is covering the job performance

.on the other hand, ease of used defined as the level of free using of IT (Davis et el. 1989).

Usefulness which is perceived is highly contributed to the productivity. For instance, using

computers can be the feature to increase job performance, job performance and effectiveness.

But despite the fact, Legris et al. (2003) postulated that TAM researches and studies are not

clear and not be the summery of too many factors that explain adoption. Tan and Teo (2000)

mentioned that one of the reason that theoretical models has been extended is all because in

internet banking the actual usage behavior cannot be measured in service environment of

internet banking where a lot of internet banking users is lacking. Guru et al. (2000) examined

the electronic banking in IRAN, particularly, examined lots of electronic channel using by

local banks .they mentioned that internet banking was not then existence in IRAN because of

sufficient legal framework and security issues are not available in IRAN.

Stoakes (1999) mentioned that internet banking can be just like a nightmare as Mark Lewis

stated that "more that 200 legal systems can be available to comply with internet banking

transaction". Overcoming all the barriers of legal internet banking are the most important

factors for those who want to use the e internet banking.

Role of regularity: Regard to this issue, the role of regularity which is concerned as the duty

is to make effective guidelines to regulate all the industries and environment.

2.1. Regulators and risk

One of the basic reasons of regulation is to mitigate the risks. Nsouli and Schaechter (2002)

believed that all the changes in financial points make new challenges for the managers of

bank ,regulatory and supervisors to form legal and regular ,reputational and operational risk.

2.2. Role of government

We can state that government can play an important role of adoption of consumers toward

internet banking. Tan and Teo (2000) postulated that government can be as a leadership in the

feature of innovation. They also figured out that the support of the government can be the

significant issue that can impact on adoption of internet banking. Hoppe et al. (2001) also

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

837

SEPTEMBER 2011 VOL 3, NO 5 mentioned that the perception of each person or individuals was useful for measuring the

degree of the government support to accept the internet banking by each consumer.

2.3. Regularity controls:

This is defined as enhancement of integrity of e _banking. Lee and Turban (2001) all of

integrity of online and internet banking are depends on the context of the regulatory controls.

When one customers use internet banking they receive the confidence in regularity control in

cyberspace (Clay and Strauss, 2000). Lee et al. 2001 ; Novak et al. 1999 ;Ackerman et

al.1999 believed that without the existence of the sufficient control of regulation personal

information of each customers may be used without the knowledge of navigations.

2.4. Bank initiative:

One of the striking roles of initiative of the bank is the time when the bank is introducing the

new products and services to their customers. Particularly, when banks encourage their

customers to adopt internet baking and accept their new products and services among their

promotions, communications and efforts of marketing.

2.4.1. Promotion and marketing:

Tan and Teo (2000) believed that banks should encourage their customers by offering them to

use internet banking to promote their services. Due to this fact, banks should use marketing

and promotions of their products and services. Obviously, effective and good promotion and

marketing will improve marker share of each company or a firm. Storey and Easingwood

(1996) postulated that marketing of each product and each support that give to each product

can develop the performance of new products.

2.4.2. Communication:

As we mentioned above, good communication in marketing and promotion effort can refer to

the good performance of the product. Storey and Easingwood (1996) figured out that those

effects on performances of sale in new financial services are all about the successful

communications. Furthermore, they stated that the services which are financial (intangible),

promotion and marketing as the communication strategy should explain the effective benefits

of the products that consumers couldn’t be able to try the product before buying that product.

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

838

SEPTEMBER 2011 VOL 3, NO 5

2.4.3. Internal communication:

Internal communication also plays an important role like internal marketing in introducing

new services and products. Storey and Easingwood (1995) mentioned that internal marketing

is highly related to the support which is given to staff. Furthermore, Storey and Johne, stated

that front line professional and good communication are the basic features in developing of

services and marketing. Other factors , such as external communication, bank initiatives and

security risks ,the importance and dimension of trust ,perceived risk, customer's orientation

,reputation, trust and website contents and informal communication and security ,trust and

intuitional assurance, trust and risk attitudes, risk tolerance and personality traits are the

other factors that we are not going to go to the details of each one.

2.5. Value added:

Value added is the benefits that each customer will enjoy .Au and Enderwick (2000) figured

out that improving value, compatibility, benefits which perceived ,experience which is

adopted and commitment of suppliers impact the continues process which clarified the

intention toward the adoption of technology. The factors of value added can be figured out

from five steps of adoption of the website of the company which is stated by the Breitenbach

and Van doren (1998). The five steps are: interest, awareness, evaluation, adoption and trial.

Value added for each service and product can be in any form like meet all needs and wishes.

Birtch and young (1997) stated that the desire of the customers based on the financial

services is followed as:

Choice of selecting product and services , convenience ,the transaction which is basic to be

right ,reliable, effective ,good price and return which is highlighted as the financial value, the

provider should act like they know their clients and their circumstance, respect to the

customers and their situations, privacy contributed to their financial issues.

2.6. Interface design

Interface design is considered as the quality factors and transaction that happened among

computers and the users. Clark (2002) believed that if even one minimum mistake happened

in interface design it is contributed to the negative influence on the chances of success for

those projects that working on e business. So much so, the key factors that clarified by the

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

839

SEPTEMBER 2011 VOL 3, NO 5 Cox and Dale (2002) are mentioned as below: (1) Purpose, (2) speed and access to internet,

(3) design, (4) content, (5) customer relationship, and (6) customer service.

The other key quality factors for a web site are the ease of use, online resource, customer

confidence, relationship services. Jun and Cai (2001) stated these factors for the quality of

online system.

D'Angelo and Little (1998) mentioned that some of the factors, for example, visual and

navigational characteristics and practical consideration such as images, color, background,

sound, media, content, and video are the key important feature for website designing.

Spiller and Lohse (1999) postulated that some of the website characteristics of online

business including feedback and products bring about basic role in making sales.

Arnet and Liu (2000) highlighted four models as the fundamental keys for receiving to the

success of the website:

First System use, second information quality, third system design quality and last but not

least playfulness.

Sathye (1999) figured out that security and difficult problems in using the website are the

most important reasons to avoid the customers not to wait for the services.

Jayawardhena and Foley (2000) stated that speed o download, design, interactivity, content,

security and navigations are the features which are fundamental for improving the customer

satisfaction.

Regard to the protection of the customers, banks can use initiatives for supporting the

customers by controlling their information. Singh et al. (2006) postulated that, one of the

privacy jobs of the bank is to allow their customers to get affected like the time they

represented in the data of the bank particularly in their changes in their lifetime, relationship

and their residency.

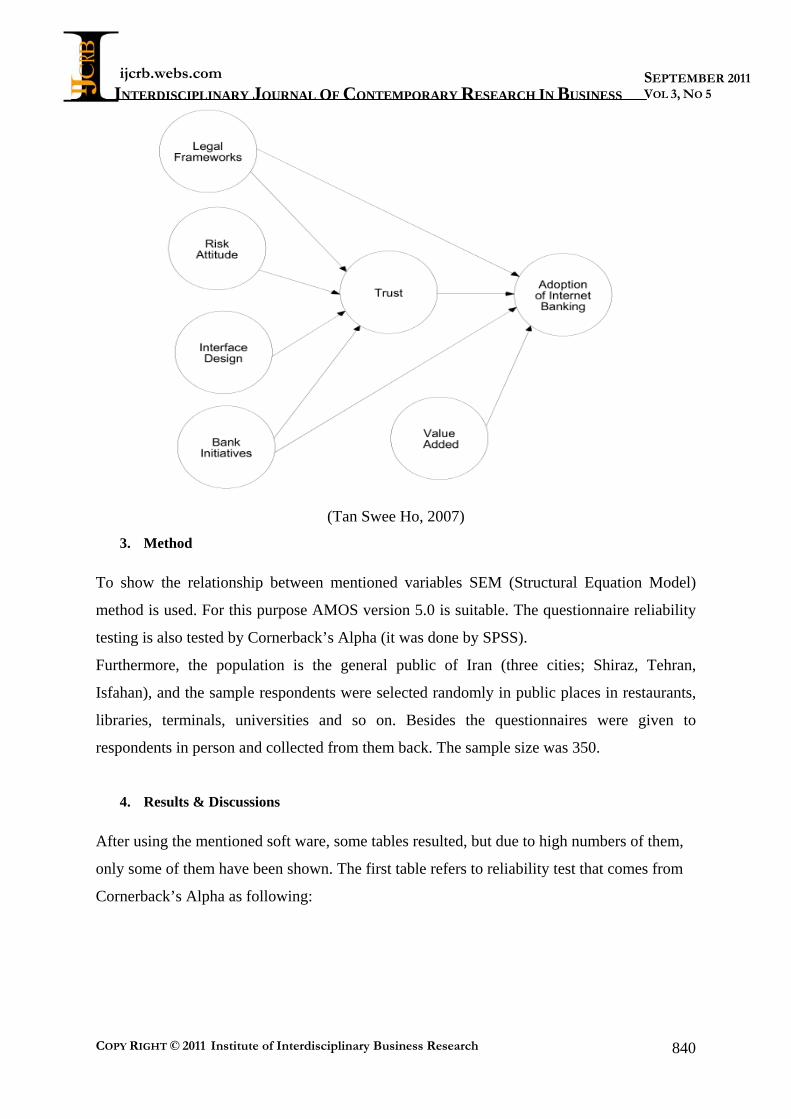

So the proposed framework is as following:

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

840

SEPTEMBER 2011 VOL 3, NO 5

(Tan Swee Ho, 2007)

3. Method

To show the relationship between mentioned variables SEM (Structural Equation Model)

method is used. For this purpose AMOS version 5.0 is suitable. The questionnaire reliability

testing is also tested by Cornerback’s Alpha (it was done by SPSS).

Furthermore, the population is the general public of Iran (three cities; Shiraz, Tehran,

Isfahan), and the sample respondents were selected randomly in public places in restaurants,

libraries, terminals, universities and so on. Besides the questionnaires were given to

respondents in person and collected from them back. The sample size was 350.

4. Results & Discussions

After using the mentioned soft ware, some tables resulted, but due to high numbers of them,

only some of them have been shown. The first table refers to reliability test that comes from

Cornerback’s Alpha as following:

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

841

SEPTEMBER 2011 VOL 3, NO 5

This table indicates that the six constructs have acceptable values in their original forms.

The next table shows the result of the validity test:

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

842

SEPTEMBER 2011 VOL 3, NO 5 According to above table, validity is acceptable.

The final result comes from following table that shows the relationship between different

variables (have been mentioned in the framework)

The theoretical framework analysis highlights that the magnitude of effect sizes of the

relationship of the constructs were mainly mixed as presented in this table.

In line with the foregoing discussion, the finding of this study will also be reported as

follows.

1) The impact of the legal framework on Customers’ trusting Behavior and Adoption of internet

Banking;

2) The impact of Bank initiatives on Customers’ trusting Behavior and Adoption of internet

Banking;

3) The impact of the Customers’ trust on their Trusting Behavior;

4) The impact of Interface Design on the Customers’ trusting Behavior;

5) The impact of the extent to which Internet banking adds value to the customer on the adoption

of Internet banking; and

6) The impact of Customers’ Risk Attitude on their Trusting Behavior.

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

843

SEPTEMBER 2011 VOL 3, NO 5 5. Conclusion

The major conclusions of this study can be illustrated via the tripartite model as following:

The successful adoption of Internet Banking or any electronic financial or banking innovation

depends on three parties namely Policy Makers, Banks and Customers. Policy Makers are

responsible for providing a safe environment for banks and customer to conduct their

business in today’s electronic era. One the part of banks, they should constantly carry out

research and development activities to ensure that customers get value and their interests are

adequately secure and protected. Customers should also play in active role in communicating

and providing feedback to Banks and Policy Makers. In this context, the importance of an

open and transparent channel for continues communication among the three can not

overemphasized.

5.1. Limitation of Study

Data gathering problem from three different cities and tendency of respondents to participate

is an old problem. Moreover, this study just concentrate on retail customers, but the corporate

customers and bankers have not been considered.

5.2. Future Study

Future researches and studies may consider corporate customers and bankers, and similar

research methodology including the Tripartite Concept can be applied to study other services

such as Mobile Banking, Credit Cards etc.

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

844

SEPTEMBER 2011 VOL 3, NO 5 References

Ackermann, E., 1995, "Issues ethical, legal, security, and social", Learning to Use The Internet, Franklin & Associates Inc. Wilsonville. Ackerman, M.S., Cranor, L.F., Reagle, J., 1999, "Beyond concern: understanding Net users' attitudes about online privacy", AT&T L Adams, D.A, Nelson, R.R, Todd, P.A., 1992, “Perceived usefulness, ease of use, and usage of information technology: a replication”, MIS Quarterly, 16, 2, 227-50. Ahire, S.L., Golhar, D.Y., and Waller, M.A., 1996, Development and Validation of TQM Implementation Construct. Decision Science. Atlanta, Winter, 27(1), pp23-56abs-Research, Shannon Laboratory. Al-Gahtani, S.S., King, M.,1999, "Attitudes, satisfaction and usage: factors contributing to each in the acceptance of information technology", Behaviour and Information Technology, Vol. 18 No.4, pp.277-97. AlibYakh lef, 2001 , “ Does the Internet compete with or complement brick and mortar bank branches”, International Journal of Retail & Distribution Management, 29, 6, 272-281. Altman, I., Taylor, D.A., 1973, Social Penetration: The Development of Interpersonal Relations, Holt Rinehart and Winston, New York, NY. Andaleeb, S.S., 1992, "The trust concept: research issues for channels of distribution", Research in Marketing, 11, 1-34. Anderson, J.C., Narus, J.A., 1990, "A model of distributor firm and manufacturer firm working partnerships", Journal of Marketing, 54. Au, A.K.M. and Enderwick, P., 2000 “A cognitive model on attitude towards technology adoption ” Jou rnal of Managerial Psychology, Volume 15 Number 4 pp. 266-282. Bailey, J.P., Bakos, Y., 1997, "An exploratory study of the emerging role of electronic intermediaries", International Journal of Electronic Commerce, 1, 3, 7-20. Bauer, R.A., 1960, "Consumer behavior at risk taking", Cox, D.F., Risk Taking and Information Handling in Consumer Behavior, Harvard University Press, Boston, MA, 23-33. Bauer, R.A., 1964, "Consumer Behaviour as Risk Taking", Dynamic Marketing for a Changing World, American Marketing Association Proceedings, 389-98. Beckett, A., Hewer, P., Howcroft, B., 2000, An exposition of consumer behaviour in the financial services International Journal of Bank Marketing, 18, 1, 15-26. Bejou, D., Ennew, C.T., Palmer, A., 1998, “Trust,ethics and relatio nship satisfaction”, International Journal of Bank Marketing,Vol 16, No. 4 pp. 170-175

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

845

SEPTEMBER 2011 VOL 3, NO 5 Bentler, P.M., Bonett, D.G., 1980, “ Significance tests and goodness of fit in the analysis of

covariance structures”, Psychological Bulletin, 88, 588-606.

Berger, W. and Wagner, H., 2002, “Spreading currency crises: the role of economic interdependence “, IMF working paper WP/02/144, International Monetary Fund, Washington, DC. Birch, D. and Young, M.A.,1997, “Financial services and the Internet - what does cyberspace mean for the financial services industry?:, Internet Research: Electronic Networking Applications and Policy Volume 7 Number 2 pp. 120-128. Bluhm, L.H., 1987, "Trust, terrorism and technology", Journal of Business Ethics, 6, 333-41. Breitenbach, C.S., Van Doren, C.S.,1998, “Value-added marketing in the digital domain: enhancing the utility of the Internet”, Jou rnal of Consumer Marketing, Vol. 15, No. 6, pp 558-575. Byrne, B.M., 1994, Structural Equation Modelling with EQS and EQS/Windows - Basic Concepts, Applications and Programming, Sage Publications, Thousand Oaks, CA. Choffee, S.H., McLeod, J.M., 1973, "Consumer decisions and information use", Ward, S., Robertson, T.S., Consumer Behavior: Theoretical Sources, Prentice-Hall In c., Englewood Cliffs, NJ, 385-415. Christopher Stoakes, Euromoney. London : August 1999, Iss. 364; pg.19 Clark, Lindsay, 2002, “ E- biz can be ruined by poor user interfaces”, Computer weekly, 5/23/2002, p18, 1p Item: 7049855 Cooper, R.G., 1976, "Introducing successful new products", European Journal of Marketing, 10, 6, 299- 329. Cooper, R.G., 1980, "Project NewProd: factors in new product success", European Journal of Marketing, 14. Crosby, L.A., Evans, K.R., Cowles, D., 1990, "Relationship quality in services selling: an interpersonal influence perspective", Journal of Marketing, 54, 68-81. Cunningham, S.M., 1967, "The major dimensions of perceived risk", Cox, D.F., Risk Taking and Information Handling in Consumer Behavior, Harvard University Press, Boston, MA, 82-108. Curall. S., and Judge, T., 1995, “Measuring Trust Between Organizational Boundary Role Persons,” organizational Behavior and Human Decision Processes (64), p.151-170. Daniel, E., 1999, "Provision of electronic banking in the UK and the Republic of Ireland", International Journal of Bank Marketing, 17, 2, 72-82 . Davis, F.D., Bagozzi, R.P., Warshaw, P.R., 1989, "User acceptance of computer technology: comparison of two theoretical models", Management Science , Vol. 35 No.8, pp.982-1003.

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

846

SEPTEMBER 2011 VOL 3, NO 5

Diacon, S.R., Ennew, C.T., 1996, "Ethical issues in insurance marketing in the UK", European Journal of Marketing, 30, 5, 67-80. Dixon, M., 1999, ".Com mad ness: 9 must-know tips for putting your bank online", America's Community Banker, 8, 6, 12-15. Easingwood, C.J., Storey, C., 1991, "Success factors for new consumer financial services", International Journal of Bank Marketing, 9, 1, 3-10. Edgett, S., Shipley, D., Forbes, G., 1992, "Japanese and British companies compared: contributing factors to success and failure in NPD", Journal of Product Innovation Management, 9, 3-10. Feldstein, M. (Ed.) 2003, Economic and Financial Crises in Emerginging Markets, University of Chicago Press, Chicago, IL. Frambach, R.T., Barkema, H.G., Nooteboom, B., Wedel, M., 1998, "Adoption of a service innovation in the business market: an empirical test of supply-side variables", Journal of Business Research, 41, 161-74. Garner, S.J., 1986, "Perceived risk and information sources in services purchasing", Mid-Atlantic Journal of Business, 24, 49-58. Gurbaxani, V., King, J. L., Kraemer, K.L., Jarman, S., Jason, D., Raman, K.S., and Yap, C.S.,1990, “Government as the Driving Force Toward the Information Society: Nation al Computer Policy in Singapore,” Information Society (7), pp 155-185. Heid er, F., 1958, The Psychology of Interpersonal Relations, John Wiley & Sons, New York, NY. Hines, W.W., Montgomery, D.C., 1990, Probability and Statistics in Engineering and Manag ement Science, John Wiley, New York, NY, 732. Jacoby, J., Kaplan, L., 1972, "The components of perceived risk", Venkatesan, M., Proceedings of 3rd Annual Conference, , 382-93. Jan Emblemsvåg,and Lars Endre Kjølstad, 2002, “Strategic risk analysis - a field version”, Management Decision, Volume 40 Number 9 2002 pp. 842-852. Jayawardhena, C., Foley, P., 2000, "Changes in the banking sector - the case of Internet banking in the UK", Internet Research: Electronic Networking Applications and Policy, 10, 1, 19-30. Jun, M., and Cai, S. 2001, “The key determinants of Internet banking service quality: a content analysis”, International Journal of Bank Marketing, Volume 19 Number 7 pp. 276-291. Kleijnen, M., Wetzels, M., de Ruyter, K., 2004, "Consumer acceptance of wireless finance", Journal of Financial Services Marketing, Vol. 8 No.3, pp.2 06-17.

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

847

SEPTEMBER 2011 VOL 3, NO 5 Kowert and Hermann, 1997, Who takes risks: Daring and caution in foreign policy making.

Journal of Conflict Resolution. 41(5), 611-637. Larzelere, R.E., Huston, T.L., 1980, "The dyadic trust scale: toward understanding in terpersonal trust in close relationships", Journal of Marriage and the Family, 42, 595-604. Leblanc, G., 1990, Customer motivations: use and non-use of automated banking, International Journal of Bank Marketing, 8, 4, 36-40. Lederer, A.L., Maupin, D.J., Sena, M.P., Zhuang, Y., 2000, "The technology acceptance model and the world wide web", Decision Support Systems, Vol. 29 No.3, pp.269-82. Legris, P., Ingham, J., Collerette, P., 2003, "Why do people use information technology? A critical review of the technology acceptance model", Information & Management, Vol. 40 pp.191-204. Li, D., Yadav, S.B., Lin, Z., 2001, "Explorin g the role of privacy programs on initial online trust formation", Texas Tech University, Lubbock, TX. Liao, S., Shao, Y., Wang, H., Chen, A., 1999, "The adoption of virtual banking: an empirical study", International Journal of Information Management, 19, 1, 63-74. Lohse, G.L., Spiller, P., 1999, "Internet retailer store design: how the user interface influences traffic and sales", Journal of Computer-mediated Communication, 5, 2, http://www.ascusc.org/jcmc/vol5/issue2/lohse.htm. MacCallum, R.C. & Austin, J.T.,2000, Application of Structural Equation Modeling in Psychological Research. Annual Review of Psychology. 51, 201-226. Malaga, R.A., 2001, "Web-based reputation management systems: problems and suggested solutions", Electronic Commerce Research, 1 , 403-17. Marr, N.E., Prendergast, G.P., 1993, "Consumer adoption of self service technologies in retail banking: is expert opinion supported by consumer research?", International Journal of Bank Marketing, 11, 1, 3-10. McDougall, G.H.G, Levesque, T.J, 1994, "Benefit segmentation using service quality dimensions: an investigation in retail banking", International Journal of Bank Marketing, 12, 2, 15-23. McKnight, D.H, Cummings, L.L, Chervany, N.L, 1998, "Initial tru st formation in new organizational relationships", Academy of Management Review, 23, 3, 473-90. Michalos, A.C., 1990, "The impact of trust on busin ess, international security and the quality of life", Journal Of Business Ethics, 9, 619-37. Milne, G.R. and Boza, M.E., 1999, “ Trust and concern in consumers’ perception of marketing information management practices”, Journal of Interactive Marketing, Vol. 13, No. 1, pp.5-24.

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

848

SEPTEMBER 2011 VOL 3, NO 5 Mols, N.P., 1998, "The behavioural consequences of PC banking", International Journal of

Bank Marketing, 16, 5, 195-201. Mols, N.P., 2001, “Organising for the effective introduction of new distribution channels in retail banking, European Journal of marketing, Vol.36, No.5/6, 2001, pp661-686. Moorman, Zaltman, G.Z., Deshpande, R., 1992, "Relationship between providers and users of market research: the dynamics o f trust within and between organisations", Journal of Marketing Research, 29, 314- 328. Mukherjee A. and Nath P., 2003, “A model of trust in online relationship banking” , The International Journal of Bank Marketing, Vol. 21, No. 1 pp 5-15. National Office for the Information Economy (NOIE), 1999, "Banking on the Internet: a guide to personal Internet bank ing services", www.noie.gov.au/Projects/ecommerce/banking/personal_banking/banking_online.html. Nsouli, S.M. and Schaechter, A., 2002 , Finance and Deveopment, a quarterly magazine of IMF, Challenges of the "E-Banking Revolution" September 2002, Volume 39, Number 3 Nunnally, J.C., 1978, Psychometric Theory, New York: McGraw-Hill. Novak, T.P., Hoffman, D.L., Peralta, M., 1999, "Building consumer trust in online environments: the case for information privacy", Communications of the ACM, 40, 4, 80-5. Ong, H.B., Cheng M.Y., 2003, “Success factors in e-channels : the Malaysian banking scenario”, 2003, International Journal of Bank Marketing, 21, 6/7, 369-377. Pablo, A.L., Sitkin, S.B., Jemison, D.B., 1996, "Acquisition decision-making processes: the central role of risk", Journal of Management, 22, 723-4 7. Papadopoulou P., Andreou A., Kanellis P., Martakos D., 2001, trust and relationship building in electronic commerce, Internet Research: “Electronic Networking Applications and Policy” Volume 11 Number 4 , pp. 322-332. Patrick, A.S., Briggs, P., Marsh, S. Designing Systems That People will Trust in Cranor, L.F. and Garfinkel, S. eds. Security and Usability: Designing Secure Systems that People Can Use, O’reilly, Sebastopol, CA. 2005, 75-99. Pavlou, P.A., 2003, "Consumer acceptance of electronic commerce: integrating trust and risk in the technology acceptance model", International Journal of Electronic Commerce, Vol. 7 No.3, pp.101-34. Ratnasingham, P., 1998, “The importance of trust in electronic commerce”, Internet Research : Electronic Networking Applications and Policy, Vol. 8, No. 4 pp 313-32. Rigdon, E.E.,1998, Structural equation Modeling. In Modern methods for business research, G. A Marcoulides (editor). Mahwah, NJ: Lawrence Erlbaum Assocites. Publishers, pp.251-294 Ring, P.S., Van De Ven, 1994, "Developmental process of co-operative interrogational relationships", Academy of Management Review, 19, 1, 90-118.

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2011 Institute of Interdisciplinary Business Research

849

SEPTEMBER 2011 VOL 3, NO 5

Robinson, J.P.,P.R. Shaver, and L.S. Wrightsman,1991, “Criteria for Scale Selection and Evaluation,” in Measures of Personality and Social Psychological Attitudes, J.P. Robinson, P.R. Shaver, and L.S. Wrightsman (eds). San Diego, Calif.: Academic Press. Rogers, E.M., 1976, "New product adoption and diffusion", Journal of Consumer Research, 2, 4, 290-301. Rugimbana, R., 1995, "The relative importance of perceptual and demographic factors in predicting ATM usage patterns of retail banking customers", International Journal of Bank Marketing, 13, 4, 28-34. Suganthi, Guru, K., and Shanmugam, B., 2001, “Internet Banking Patronage : An Empirical Investigation of Malaysia “,Journal of Internet Banking and Commerce, Vol. 6, No.1, May. Sultan, F., Qualls, W., Urban, G.L., 1999, "Design and evaluations of a true based advisor on the Internet", Northeastern University, Boston, MA. Smeltzer, L.R., 1997, "The meaning and origin of trust in buyer-supplier relationships", International Journal of Purchasing and Materials Management, 40-8. Standards Australia, 1999, AS/NZS 43 60:1999 - Risk Management, Standards Australia, Sydney, 44. Strieter, J., Gupta, A.K., Raj, S.P., Wilemon, D., 1999, "Product management and the marketing of financial services", International Journal of Bank Marketing, 17, 7, 342-54. Taylor, J.W, 1974 , "`The role of risk in consumer behavior", Journal of Marketing, 38, 54-60. Toh, M. H., and Low, L., 1993, “ The Intelliegn City: Achieving the Next Lap”, Technology Analysis and Strategic management (5:2), pp 187-202. Venkatesh, V., 2000, "Determinants of perceived ease of use: integrating control, intrinsic motivation, and emotion into the technology acceptance model", Information Systems Research, Vol. 11 No.4, pp.342-65. Voss, C.A., 1985, "Determinants of success in the development of application software", Journal of Product Innovation Management, 2, 2, 122-9. Wang, Y.S.,Wang, Y.M., Lin, H.H., Tang, T.I., 2003, ”Determinants of user acceptance of Internet banking : an empirical study”, International Journal of Service Industry Management, 14, 5, 501-519. Zeithaml, V.A., Gilly, M.C., 1987, "Characteristics affecting the acceptance of retailing technologies: a comparison of elderly and non-elderly consumers", Journal of Retail Banking, 63, 1, 49-68. Zucker, L. 1986, “Production of Trust: Institution al sources of Economic Structure, 1840-1920” in research in Organizational Behaviour, B. Staw and L. Cummings (eds.), Greenwich, CT: JAI Press, pp 53-111.

Related Documents