II: Portfolio Theory I 2: Measuring Portfolio Return 3: Measuring Portfolio Risk 4: Diversification

II: Portfolio Theory I 2: Measuring Portfolio Return 3: Measuring Portfolio Risk 4: Diversification.

Dec 28, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

II: Portfolio Theory I

2: Measuring Portfolio Return

3: Measuring Portfolio Risk

4: Diversification

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

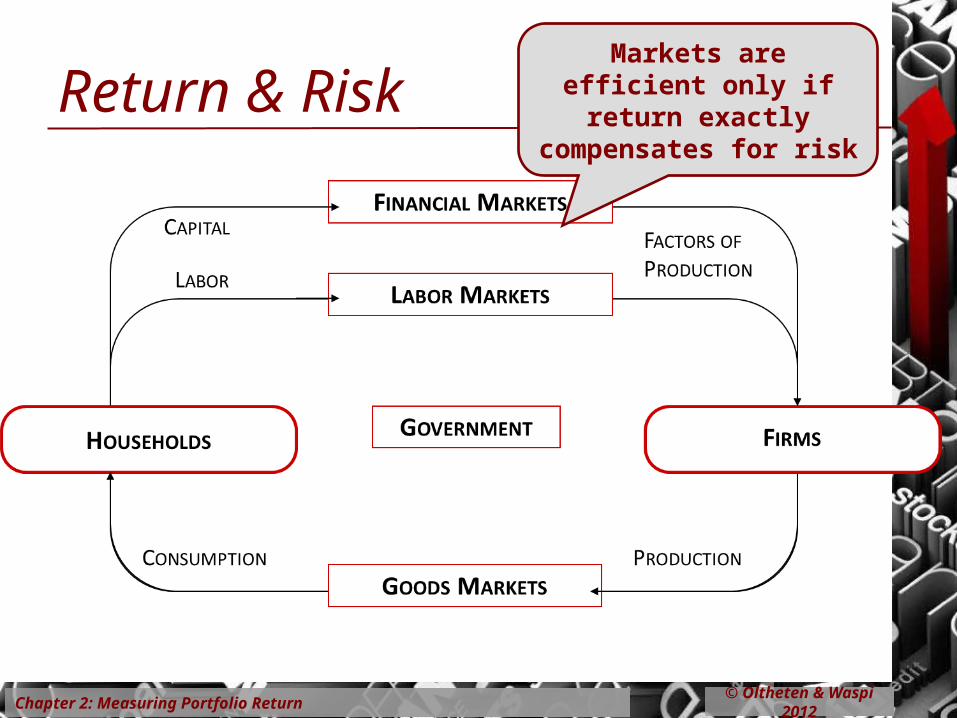

Return & RiskMarkets are efficient only if return exactly compensates

for risk

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Measuring Portfolio Return

Holding Period Return Cash Flow Adjusted Rate of Return Time Weighted versus Statistical Rates of

Return Internal Rate of Return

Chapter 2: Measuring Portfolio Return

Holding Period Return

$2,400,000 = $1.20 = $1 + 20%$2,000,000

$1,600,000 = $0.80 = $1 - 20%$2,000,000

For every $ you started with you now have $1.20

$ you started with

+ 20%

For every $ you started with you now have only $0.80

$ you started with

- 20%

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

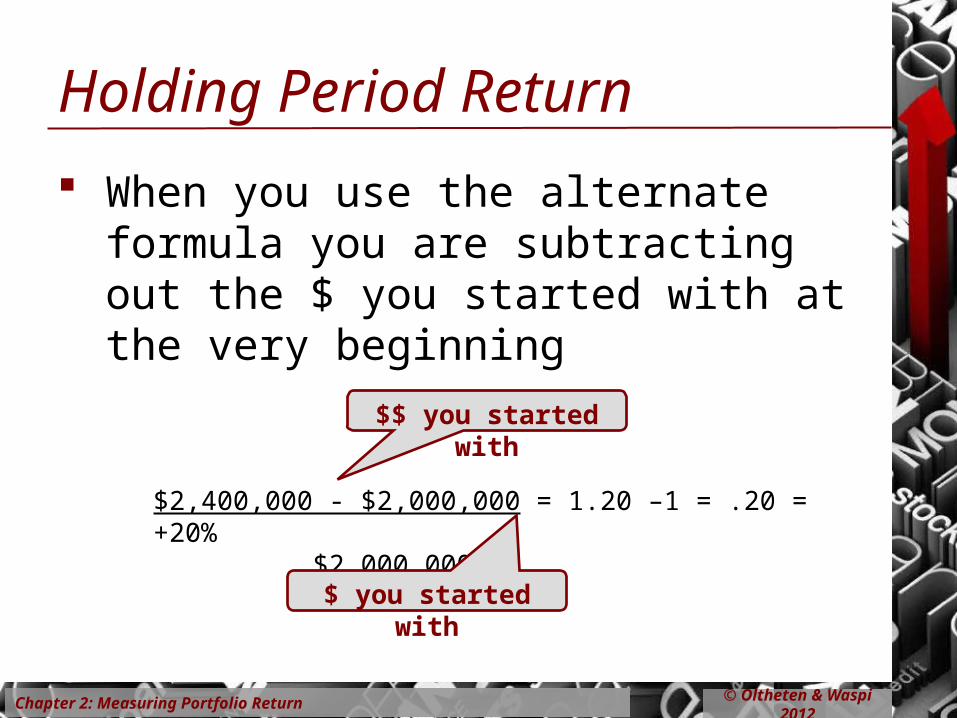

Holding Period Return

When you use the alternate formula you are subtracting out the $ you started with at the very beginning

$2,400,000 - $2,000,000 = 1.20 –1 = .20 = +20% $2,000,000

$$ you started with

$ you started with

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Cash Flow Adjusted Rate of Return

We want to measure investment returns We adjust so that the rate of return is not

distorted by cash flows over which the investment manager has no control.

flow cash*

dateV

flow cash*date

VrR

3030

301

0

1

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

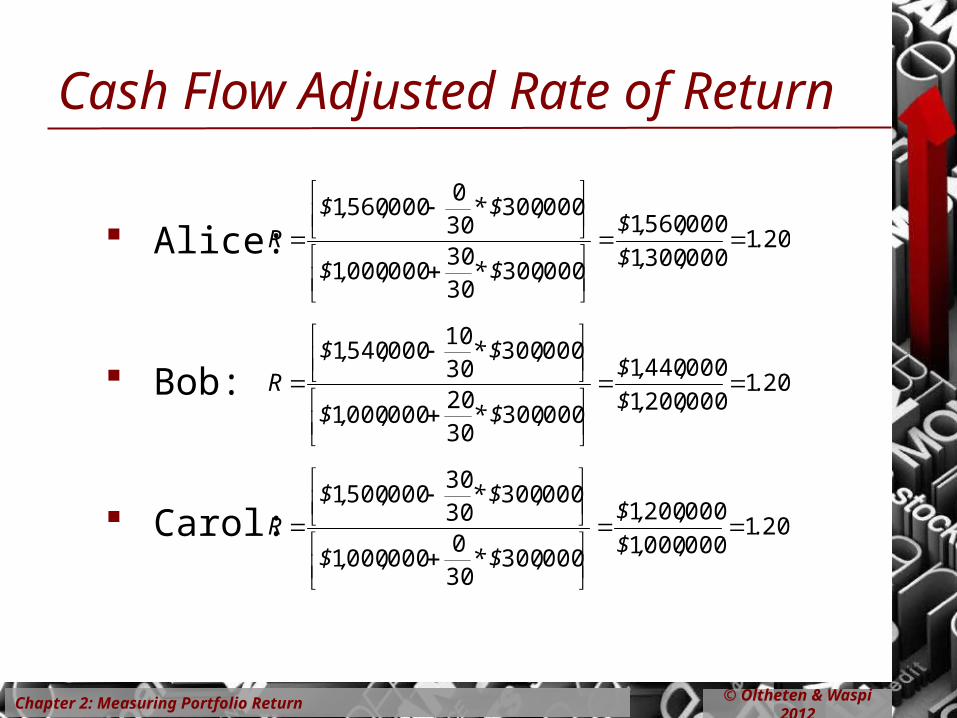

Cash Flow Adjusted Rate of Return

Each Investment Manger began the month of September with $1million. At the end of the month Alice: $1m to $1.56 million Bob: $1m to $1.54 million Carol: $1m to $1.50 million

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Cash Flow Un-adjusted

0 5 10 15 20 25 30$1.00m

$1.10m

$1.20m

$1.30m

$1.40m

$1.50m

$1.60m

Alice (56%)

Bob (54%)

Carol (50%)

September

Slope of 50%

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

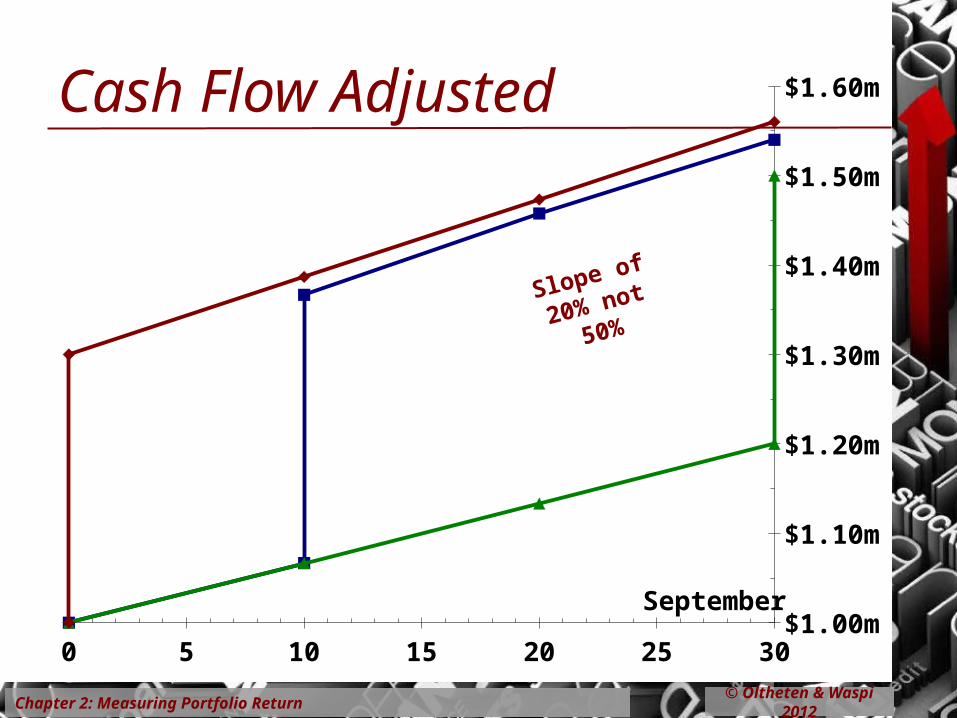

Cash Flow Adjusted

Each investment manager received an additional $300,000 from the client during the month Alice: before the open on the first Bob: on the tenth Carol: after the close on the thirtieth

Cannot measure as a rate of return any money that the investment manager did not generate.

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Cash Flow Adjusted Rate of Return

Alice:

Bob:

Carol:

2010003001

0005601

0003003030

0000001

000300300

0005601.

,,$

,,$

,$*,,$

,$*,,$R

2010002001

0004401

0003003020

0000001

0003003010

0005401.

,,$

,,$

,$*,,$

,$*,,$R

2010000001

0002001

000300300

0000001

0003003030

0005001.

,,$

,,$

,$*,,$

,$*,,$R

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

0 5 10 15 20 25 30$1.00m

$1.10m

$1.20m

$1.30m

$1.40m

$1.50m

$1.60m

September

Cash Flow Adjusted

Slope of 20%

not 50%

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Cash Flow Adjusted

December 31 Market Value: $34,978,567.03

January 3: Bond Income: $14,400.00

January 15: Pension contribution: $3,098.10

January 18: Bond Income: $600.00

January 21: Pension Payments - $9,879.20

January 22: Dividend received $1,700.00

January 31: Pension contribution $3,098.10

January 31 Market Value $34,993,897.09

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

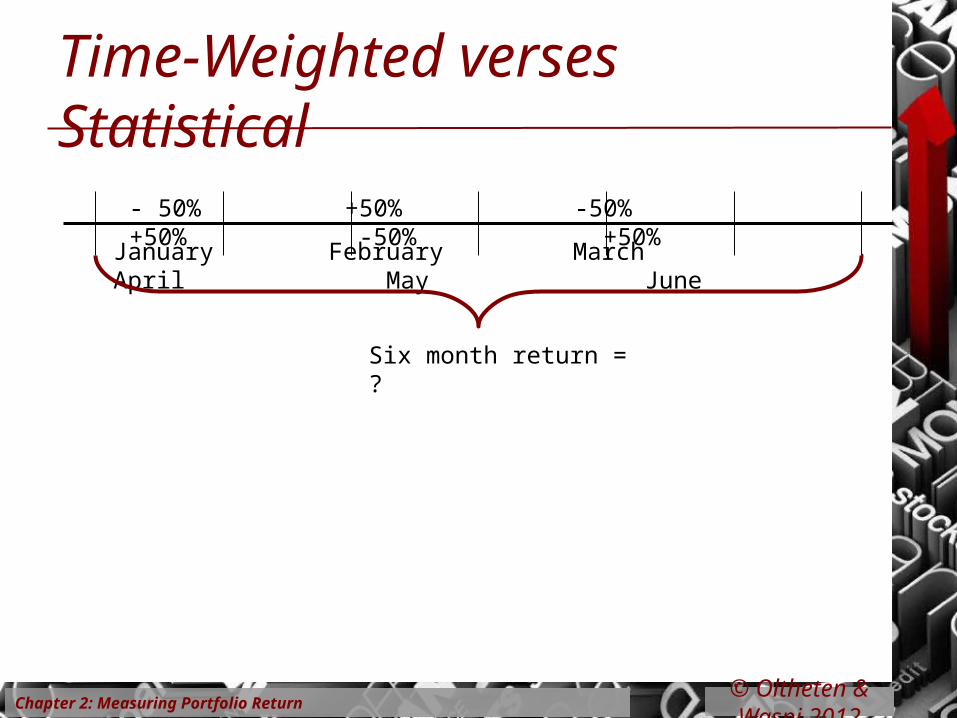

Time-Weighted verses Statistical

Time Weighted:combines time periods using Geometric totals and averages

Statistical: combines time periods using arithmetic totals and averages

Chapter 2: Measuring Portfolio Return

Time-Weighted verses Statistical

January February March April May June

- 50% +50% -50% +50% -50% +50%

Six month return = ?

© Oltheten & Waspi 2012

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Statistical

Total Return =

Average Return =

Variance =

Standard Deviation =

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Statistical

Statistical returns assume that the return in one month is independent of the returns of any other month.

February April June

January March May

- 50%- 50%- 50%

+ 50% + 50% + 50%

$1,000,000

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Time-Weighted

Total Return =

Average Return =

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Time-Weighted

Time Weighted returns assume that returns in one month are reinvested in the following month

$421,875

$1,000,000

$500,000

$281,250

$750,000

$375,000

$562,500

January February March April May June

- 13.4%

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Time-Weighted = Holding Period

In the absence of excluded cash flows, time weighted returns equal holding period returns.

$421,875

$1,000,000

$500,000

$281,250

$750,000

$375,000

$562,500

January February March April May June

- 13.4%

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Internal Rate of Return

Internal rate of return (IRR) is the rate of return that renders the Net Present Value (NPV) equal to zero.

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

Internal Rate of ReturnDec 31, 2012 Dec 31, 2013 Dec 31, 2014 Dec 31, 2015 Dec 31, 2016

-$10,000 +$510 +$2,000 +$4,500 +5,000

IRR = 6%

Chapter 2: Measuring Portfolio Return © Oltheten & Waspi 2012

In Summary: Measuring Return

Holding Period Rate of Return Cash Flow Adjusted Rate of Return Time Weighted vs Statistical Rates of Return Internal Rate of Return

Chapter 3: Measuring Portfolio Risk © Oltheten & Waspi 2012

Measuring Risk

Risk versus Uncertainty Standard Deviation () Coefficient of Variation (CV) Beta (β)

Chapter 3: Measuring Portfolio Risk © Oltheten & Waspi 2012

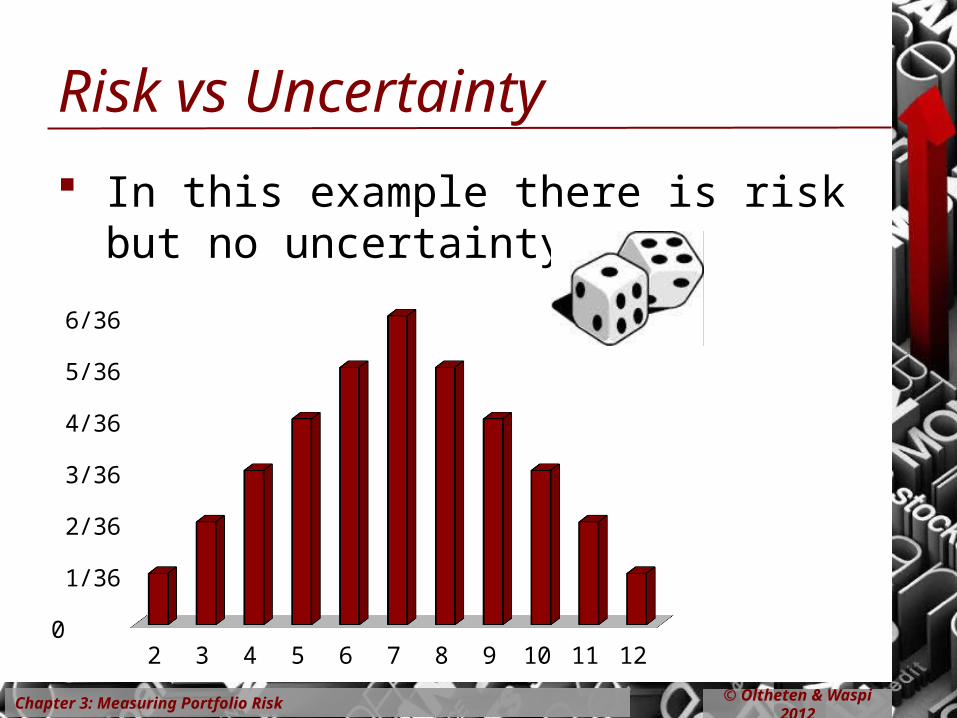

Risk vs Uncertainty

In this example there is risk but no uncertainty

2 3 4 5 6 7 8 9 10 11 120

1/36

2/36

3/36

4/36

5/36

6/36

Chapter 3: Measuring Portfolio Risk © Oltheten & Waspi 2012

-5 -4 -3 -2 -1 0 1 2 3 4 5

Risk vs Uncertainty

Stock returns are normally distributed (more or less) so there is risk, but there is still uncertainty…

5 sigma event

r~ N(0, 1)

Chapter 3: Measuring Portfolio Risk © Oltheten & Waspi 2012

In the normal distribution 99.74% of the observationsare within 3standard deviationsof the mean.

-3 -2 -1 0 1 2 3

68.27%

95.45%

99.73%

Standard Deviation

Chapter 3: Measuring Portfolio Risk © Oltheten & Waspi 2012

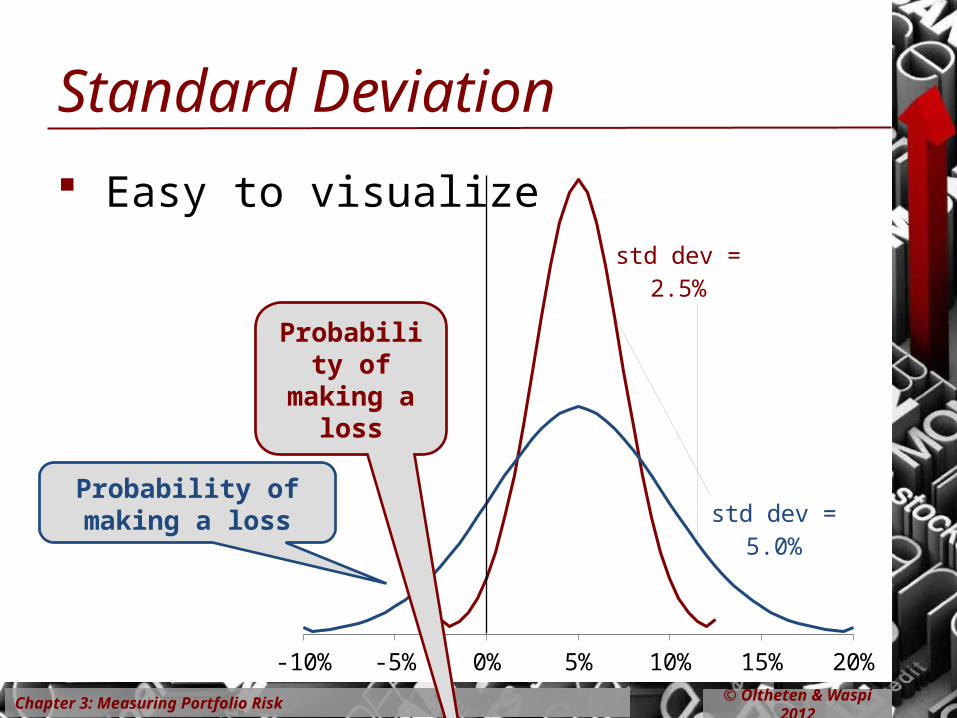

-10% -5% 0% 5% 10% 15% 20%

std dev = 5.0%

std dev = 2.5%

Standard Deviation

Easy to visualize

Probability of making a loss

Probability of making a loss

Chapter 3: Measuring Portfolio Risk © Oltheten & Waspi 2012

Coefficient of Variation

Risk per unit of Return CV = σ .

E[R]

Chapter 3: Measuring Portfolio Risk © Oltheten & Waspi 2012

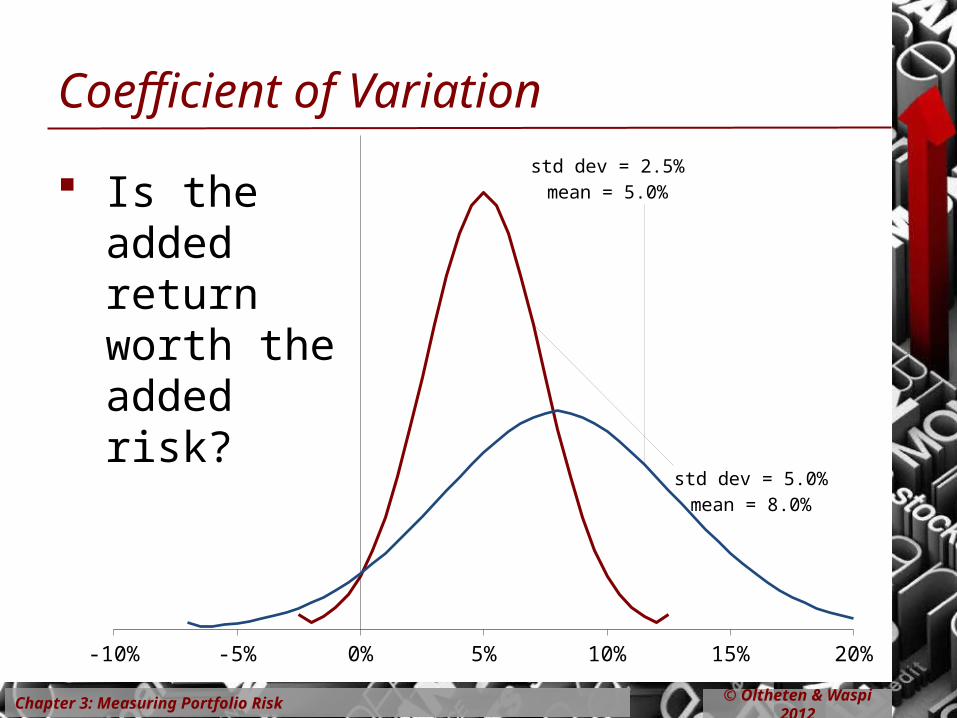

-10% -5% 0% 5% 10% 15% 20%

std dev = 5.0%mean = 8.0%

std dev = 2.5%mean = 5.0%

Coefficient of Variation

Is the added return worth the added risk?

Chapter 3: Measuring Portfolio Risk © Oltheten & Waspi 2012

Beta

Captures Market Risk (Market Model)

We will generate the market model through our discussion of diversification

Chapter 3: Measuring Portfolio Risk © Oltheten & Waspi 2012

In Summary: Measuring Risk

Risk versus Uncertainty Standard Deviation Coefficient of Variation Beta

Chapter 3: Measuring Portfolio Risk © Oltheten & Waspi 2012

Risk Preferences

Risk Averse Investors accept risk only if they are compensated

Risk Neutral Investors are blind to risk and simply choose the

highest expected return

Risk Loving Investors actually derive utility from risky behavior

(like gambles)

Chapter 4: Diversification © Oltheten & Waspi 2012

Diversification

Diversification reduces risk exposure when returns are imperfectly correlated.

Covariance & Correlation (review)

Chapter 4: Diversification © Oltheten & Waspi 2012

Covariance

Expectations vs Actual

E[R] Boom Normal Bust

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

11%

28%

12%

-7%

7%

-3%

7%

17%

Stocks: =11%, =14.3062Bonds: =7%, =8.1650

Chapter 4: Diversification © Oltheten & Waspi 2012

Covariance

Deviations for the expected value

E[R] Boom Normal Bust

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

0%

17%

1%

-18%

0%

-10%

0%

10%

Stocks: =11%, =14.3062Bonds: =7%, =8.1650

Chapter 4: Diversification © Oltheten & Waspi 2012

Covariance

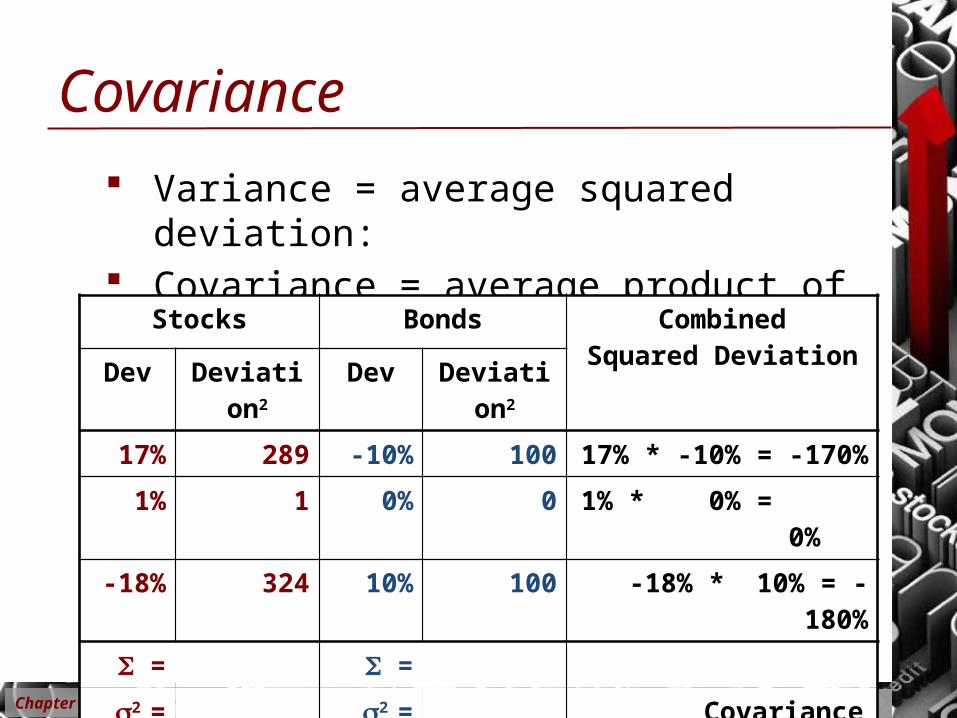

Variance = average squared deviation: Covariance = average product of the deviations:

Stocks Bonds CombinedSquared Deviation

Dev Deviation2 Dev Deviation2

17% 289 -10% 100 17% * -10% = -170%

1% 1 0% 0 1% * 0% = 0%

-18% 324 10% 100 -18% * 10% = -180%

= =

2 = 2 = Covariance =

= =

Chapter 4: Diversification © Oltheten & Waspi 2012

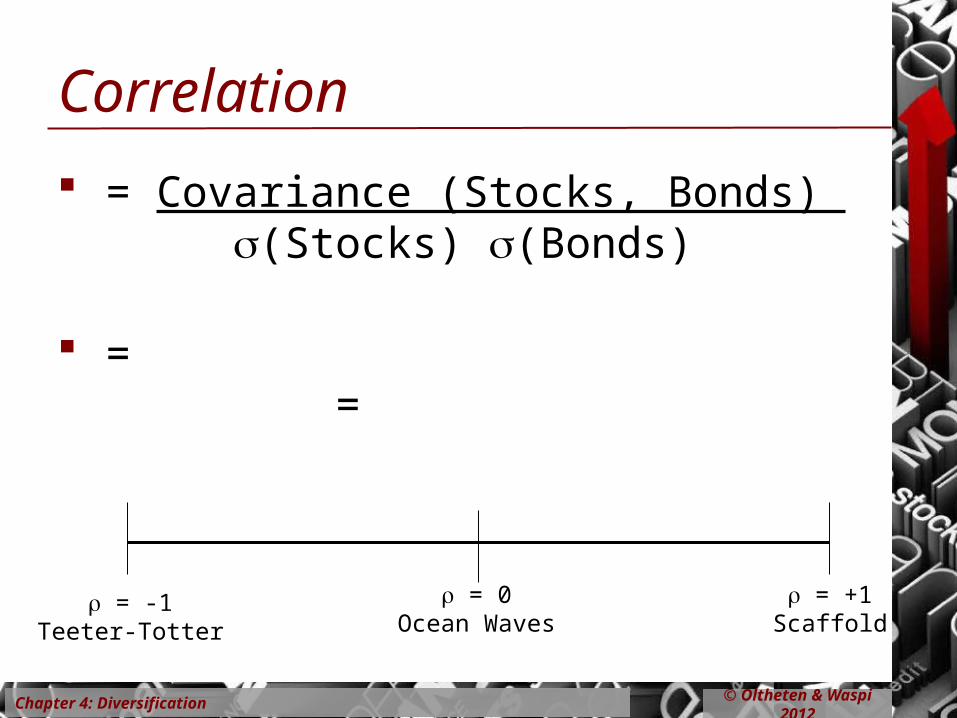

Correlation

= Covariance (Stocks, Bonds) (Stocks) (Bonds)

= =

= 0Ocean Waves

= +1Scaffold

= -1Teeter-Totter

Chapter 4: Diversification © Oltheten & Waspi 2012

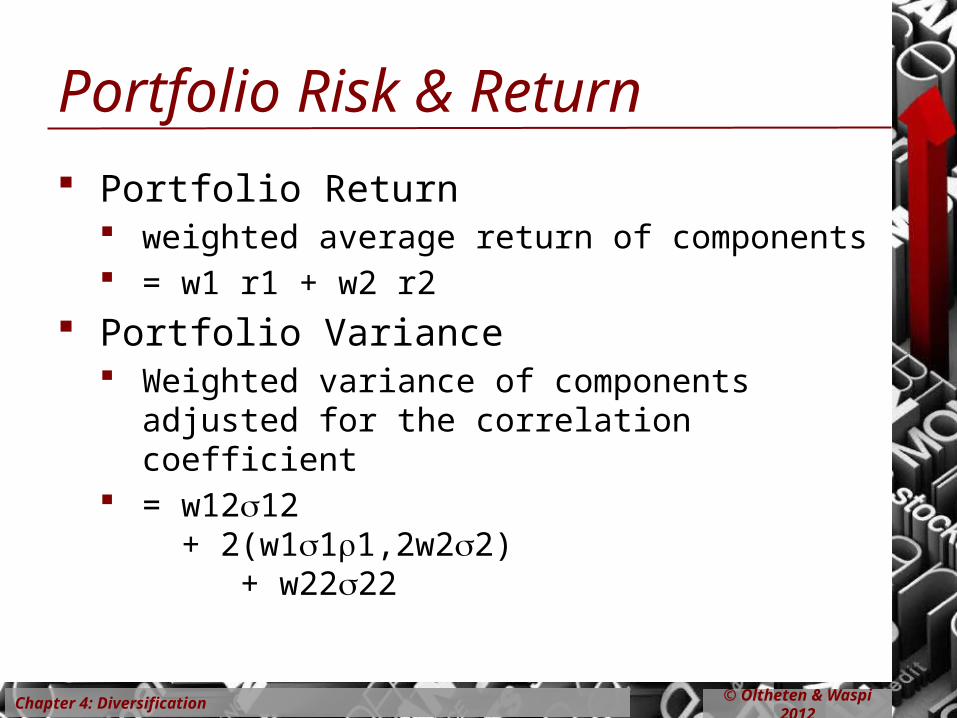

Portfolio Risk & Return

Portfolio Return weighted average return of components = w1 r1 + w2 r2

Portfolio Variance Weighted variance of components adjusted for

the correlation coefficient = w1212

+ 2(w111,2w22) + w2222

Chapter 4: Diversification © Oltheten & Waspi 2012

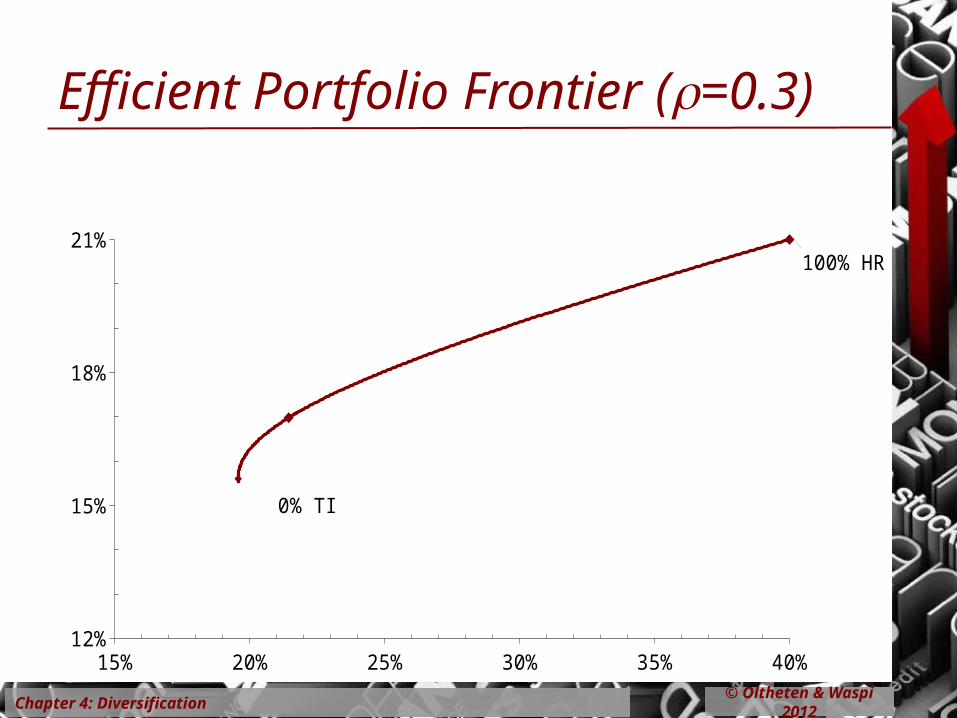

Portfolio Risk & Return: an example

A portfolio of two stocks Tardis Intertemporal

E[r] = 15% = 20% Hypothetical Resources

E[r] = 21% = 40% r = 0.30

Chapter 4: Diversification © Oltheten & Waspi 2012

Efficient Portfolio Frontier

10% 15% 20% 25% 30% 35% 40%12%

15%

18%

21%100% HR

100% TI

Chapter 4: Diversification © Oltheten & Waspi 2012

Efficient Portfolio Frontier (=0.3)

15% 20% 25% 30% 35% 40%12%

15%

18%

21%100% HR

100% TI

Chapter 4: Diversification © Oltheten & Waspi 2012

Efficient Portfolio Frontier

0% 5% 10% 15% 20% 25% 30% 35% 40%14%

15%

16%

17%

18%

19%

20%

21%

ρ=1

100% HR

ρ=-1ρ=0

ρ=0.3

100% TI

Chapter 4: Diversification © Oltheten & Waspi 2012

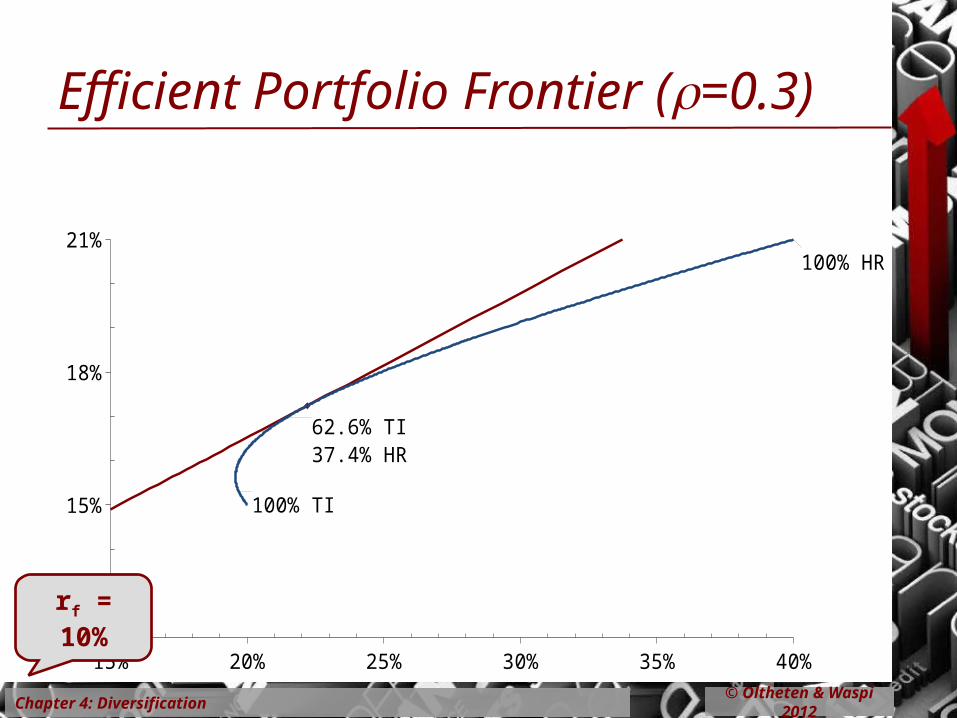

Efficient Portfolio Frontier (=0.3)

15% 20% 25% 30% 35% 40%12%

15%

18%

21%100% HR

62.6% TI37.4% HR

100% TI

rf = 10%

Chapter 4: Diversification © Oltheten & Waspi 2012

Limits of Diversification

Unsystematic Risk Industry or firm specific – can be diversified away

Systematic Risk Economy wide - cannot be diversified away

0 20 40

Systematic Risk

Unsystematic Risk

market portfolio

Number of Stocks in the portfolio

Sta

ndar

d D

evia

tion

II: Portfolio Theory I

Related Documents