BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 1 BEFORE THE BIHAR ELECTRICITY REGULATORY COMMISSION VIDYUT BHAWAN –II, PATNA Petition For Determination of Annual Revenue Requirement (ARR) and Transmission Tariff for FY 2017-18 For Bihar Grid Company Limited (BGCL) Patna General Manager 2 nd Floor, Alankar Place Boring Road Patna – 800 001 January 13, 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 1

BEFORE

THE BIHAR ELECTRICITY REGULATORY COMMISSION

VIDYUT BHAWAN –II, PATNA

Petition

For

Determination of Annual Revenue Requirement (ARR)

and Transmission Tariff for FY 2017-18

For

Bihar Grid Company Limited

(BGCL)

Patna

General Manager

2nd Floor, Alankar Place

Boring Road

Patna – 800 001

January 13, 2017

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 2

BEFORE, THE BIHAR ELECTRICITY REGULATORY COMMISSION,

IN THE MATTER OF

Filing of the Petition for Determination of Annual Revenue Requirement (ARR) and

Tariff for FY 2017-18 under BERC (Terms and Conditions for Determination of Tariff)

Regulations, 2007 along with the other guidelines and directions issued by the BERC

from time to time and under Sections 61, 62, and 64 of the Electricity Act, 2003 read

with the relevant guidelines.

AND

IN THE MATTER OF

BIHAR GRID COMPANY LIMITED (hereinafter referred to as “BGCL” or ‘’Petitioner”

which shall mean for the purpose of this Petition, the Licensee), having its registered

office at 2nd Floor, Alankar Place, Boring Road, Patna - 800001.

The Petitioner respectfully submits as under:

1. BGCL is filing this Petition for Determination of Annual Revenue Requirement

and Tariff for FY 2017-18 as per procedures outlined in Sections 61, 62 and 64 of

the Electricity Act, 2003, and the governing Regulations thereof.

2. The Business Plan Petition of BGCL for FY 2014-15 to FY 2016-17 was filed before

the Hon’ble Commission on October 21, 2013. The Hon’ble Commission had

duly approved the Business Plan vide Order dated January 4, 2014 in Case No.

20 of 2013.

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 3

3. This instant Petition is being filed before the Hon’ble Commission for

determination of Annual Revenue Requirement (ARR) and Tariff for FY 2017-18.

4. This Petition has been prepared in accordance with the provision of Sections 61,

62 and 64 of the Electricity Act, 2003 and taking into consideration the provisions

of Chapter 6 Multi-Year Tariff of the BERC (Terms and Conditions for

Determination of Tariff) Regulations, 2007 as amended time to time by the

Hon’ble Commission.

5. BGCL along with this Petition is submitting the regulatory Formats with

relevant data and information to the extent applicable and would make

available any further information/additional data required by the Hon’ble

Commission during the course of the proceedings.

Prayers to the Commission:

The Petitioner respectfully prays that the Hon’ble Commission may:

a) Admit this Petition;

b) Examine the proposal submitted by the Petitioner in the enclosed Petition for

a favourable dispensation;

c) Approve the proposed Annual Revenue Requirement (ARR) for FY 2017-18

and recovery of ARR through the mechanism proposed in the Petition;

d) Condone any inadvertent omissions, errors, short comings and permit BGCL

to add/ change/ modify/ alter this filing and make further submissions as

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 4

may be required at a future date; and

e) Pass such Order as the Hon’ble Commission may deem fit and appropriate

keeping in view the facts and circumstances of the case.

Dated: January 13, 2017 T. Pandey

General Manager

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 5

Table of Contents

1 Introduction ...................................................................................................................... 9

1.1 Background ............................................................................................................... 9

1.2 Main Functions and Duties of BGCL .................................................................. 11

1.3 Profile of BGCL ....................................................................................................... 12

1.4 Current Petition ...................................................................................................... 13

1.5 Contents of the Petition ......................................................................................... 14

2 Approach for filing the Petition ................................................................................... 15

3 Determination of ARR for FY 2017-18 ........................................................................ 16

3.1 Introduction ............................................................................................................ 16

3.2 Transmission Loss .................................................................................................. 16

3.3 Capital Investment Plan ........................................................................................ 17

3.4 Capitalisation .......................................................................................................... 19

3.5 Gross Fixed Assets ................................................................................................. 20

3.6 Depreciation ............................................................................................................ 24

3.7 Interest on Loan ...................................................................................................... 26

3.8 Operation and Maintenance Expenses ................................................................ 28

3.8.1 Employee Expenses ................................................................................................... 28

3.8.2 Repairs and Maintenance (R&M) Expenses ........................................................... 30

3.8.3 Administration & General Expenses ....................................................................... 31

3.8.4 Summary of O&M Expenses .................................................................................... 32

3.9 Interest on Working Capital ................................................................................. 33

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 6

3.10 Return on Equity .................................................................................................... 34

3.11 Non-Tariff Income .................................................................................................. 35

3.12 Transmission ARR for the Financial Year 2017-18 ........................................... 35

4 Methodology for Recovery of ARR ............................................................................. 37

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 7

List of Tables Table 1-1: Power Transformer Capacity (in MVA) .......................................................... 13

Table 1-2: Transmission Line Length (in Ckm) ................................................................ 13

Table 3-1: Transmission Loss Trajectory ............................................................................ 17

Table 3-2: Total Capital Expenditure to be incurred (Rs. Crore) .................................... 18

Table 3-3: Capitalisation as approved in Business Plan Order (Rs. Crore) ................... 20

Table 3-4: Revised Capitalisation Estimate (Rs. Crore) .................................................... 20

Table 3-5: Gross Fixed Assets (Rs. Crore) .......................................................................... 23

Table 3-6: Depreciation for FY 2017-18 (Rs. Crore) .......................................................... 25

Table 3-7: Calculation of Weighted avg. Rate of Interest ................................................ 26

Table 3-8: Interest on Loan for FY 2017-18 (Rs. Crore) ................................................... 27

Table 3-9: Projected Employee Expenses for FY 2017-18 (Rs. Crore) ............................ 29

Table 3-10: Normative R&M Expenses allowed in other States ..................................... 30

Table 3-11: Projected R&M Expenses for FY 2017-18 (Rs. Crore) .................................. 31

Table 3-12: Projected A&G Expenses for FY 2017-18 (Rs. Crore) .................................... 32

Table 3-13: Projected O&M Expense (Rs. Crore) .............................................................. 32

Table 3-14: Norms for Working Capital Requirement .................................................... 33

Table 3-15: Projected Interest on Working Capital (Rs. Crore) ....................................... 33

Table 3-16: Computation of Return on Equity (Rs Crore) ............................................... 34

Table 3-17: Projected Annual Fixed Charges/ARR (Rs. Crore) ..................................... 35

Table 4-1: Illustrative Fixed Charge (Rs. Crore) ............................................................... 42

Table 4-2: ARR Recovery (Rs. Crore) ................................................................................. 43

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 8

List of Annexures

Sl. No. Annexure

1 Audited Accounts for FY 2015-16

2 Trial Balance for FY 2016-17 (Apr-Nov’16)

3 Abstract of Board Resolution regarding award of projects

4 REC Loan Details

5 Shareholder Agreement between BSP(H)CL and PGCIL

6 ‘Implementation and Transmission Services Agreement’ signed

between BSP(H)CL and BGCL

7 Scheme diagram

8 ARR Forms

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 9

1 Introduction

1.1 Background

In order to develop the Intra-State Transmission System in the State of Bihar, it was

agreed between Bihar State Power Holding Company Limited (BSP(H)CL) and Power

Grid Corporation of India Limited (POWERGRID) to form a 50:50 Joint Venture

Company in the name of Bihar Grid Company Limited under the provisions of the

Companies Act, 1956. The Company will Build, Own and Operate (BOO) the

transmission system and it will be a transmission licensee duly authorised by the

Hon’ble BERC.

Bihar Grid Company Limited was registered on January 4, 2013 under the Companies

Act, 1956 with the objective of providing transmission facilities to the State

distribution companies and any other transmission system users. BGCL also fulfils the

responsibility of planning, developing and coordinating with the intra-State

transmission system user (STU) of the State of Bihar.

Considering the rapid load growth and the upcoming generating stations in the State

of Bihar in the next 5-6 years, a comprehensive study was carried out by POWERGRID

in 2011-12 in association with the then Bihar State Electricity Board (BSEB) and Central

Electricity Authority (CEA). As per the study, the following mentioned future

transmission Schemes, which also include strengthening of existing system were

planned, which are to be covered under the XIIth Plan and assigned to BGCL by

BSP(H)CL. The schemes were divided into three parts as indicated below:

Part-1: Bihar Sub-Transmission Phase-II extension scheme

Part-2(a): Strengthening scheme: Phase-1: Schemes identified for year 2012-13,

2013-14 and 2014-15 under Phase-III

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 10

Part-2(b): Strengthening Scheme: Phase-2: Schemes identified for year 2015-16

& additional strengthening for year 2016-17 under Phase-IV

Part-3: Generation Linked Scheme: Transmission System for evacuation of

power from Lakhisarai, Pirpainti and Buxar generation projects (identified for

year 2016-17) under Phase-V.

However, works under Part-1 and Part-2(a) were undertaken by BSPTCL on priority

basis. Therefore, BGCL is implementing works under Part-2(b) of the above

mentioned schemes and Detailed Project Report (DPR) for the same has been

approved by the Hon'ble Commission vide Order dated January 4, 2014 and July 22,

2015 in Case No. 20 of 2013 and Case No. 14 of 2015, respectively.

The Hon’ble Commission vide its Order dated April 29, 2013, in Case No. 7 of 2013

granted Transmission Licence to Bihar Grid Company Limited (BGCL) and stipulated

as follows:

“Therefore, the application of the Bihar Grid Company Limited for grant of licence to the

applicant BGCL for transmission of electricity as a transmission licensee in the State of Bihar

is approved. After compliance of conditions laid down in the Regulations 13, 14 and 15 of

BERC (Licencing for Transmission of Electricity) Regulations, 2007 by the Bihar Grid

Company Limited, the Commission would issue the Licence. The BGCL shall pay the initial

and annual licence fee to the Bihar Electricity Regulatory Commission in accordance with

BERC (Fees, Fines and Charges) Regulations, 2006.

The licence shall be issued for 25 (twenty five) years with effect from the date of issue of the

licence. Bihar Grid Company Limited shall submit requisite documents as specified in

Regulations 13, 15 and 16 of the BERC (Licencing for Transmission of Electricity)

Regulations, 2007. Bihar Grid Company Limited shall abide by all terms and conditions of the

licence and any other terms and conditions which Commission considers necessary to remove

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 11

the difficulty in giving effect to any of the provision of the BERC (Licencing for Transmission

of Electricity) Regulations, 2007.”

The Transmission Licence was issued to BGCL on June 21, 2013 vide Letter No.

BERC/Case No.7/2013-792-01-Tr.L.

1.2 Main Functions and Duties of BGCL

The main functions and duties of BGCL are as follows:

(a) To undertake planning and coordination activities in regard to Intra-State

Transmission, works connected with the inter-State Transmission System in the

State of Bihar, to introduce open access in transmission on payment of transmission

charges. To ensure development of an efficient, coordinated and economical system

of Intra-State Transmission lines for smooth flow of electricity from a generating

station to load centres and to provide non-discriminatory open access as per

requirement. Other functions as may be assigned to the company by law or

otherwise by Government or Government Authority concerning the operation of the

Power System.

(b) To plan, acquire, develop, establish, built, take over, erect, lay, operate, run, manage,

renovate, modernize, electrical transmission lines and/or networks through various

voltage lines and associated sub-stations, including cables, wires, meters, computers

and materials connected with transmission, ancillary services, telecommunication

and tele-metering equipment etc.

(c) To make available the entire transmission capacity of the Project to BSP(H)CL on a

commercial basis subject to the conditions laid down in the Inter-State Transmission

Services Agreement (ITSA).

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 12

(d) To derive its revenue by recovery of transmission charges from transmission system

users. The Company shall be primarily in the business of transmission of electricity

and it shall be vested with the transmission assets, interest in property, rights and

liabilities. The Company shall act as a Transmission Licensee under the Provisions

of Section 14 of the Electricity Act, 2003.

(e) To define its own ‘Safety policy’ keeping in view the motto of ‘ZERO ACCIDENT

GOAL’.

(f) To adopt the Environmental Social Policy and Procedure (ESPP) and also the

Corporate Social Responsibility (CSR) in line with POWERGRID’s established

Policy and Procedure and will make a sincere contribution towards the under

privileged community by supporting a wide range of educational initiatives so as

to make a positive difference in their lives.

(g) As a part of energy conservation programme, to contribute towards energy

conservation by spreading awareness amongst the people and adopt energy

efficient state of the art technology.

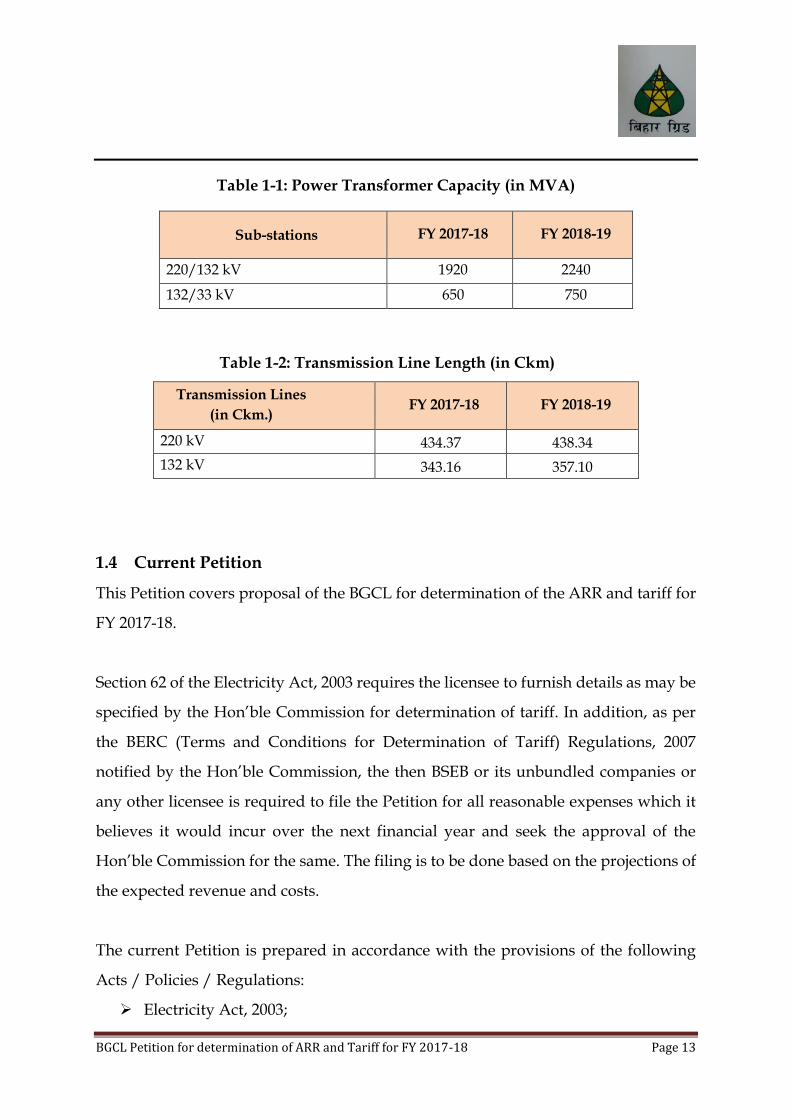

1.3 Profile of BGCL

Primarily, the transmission of power will take place at 220 kV and 132 kV voltage

levels. The total proposed capacity in the transmission system once all the projects

attain COD is provided in the table below:

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 13

Table 1-1: Power Transformer Capacity (in MVA)

Sub-stations FY 2017-18 FY 2018-19

220/132 kV 1920 2240

132/33 kV 650 750

Table 1-2: Transmission Line Length (in Ckm)

Transmission Lines

(in Ckm.) FY 2017-18 FY 2018-19

220 kV 434.37 438.34

132 kV 343.16 357.10

1.4 Current Petition

This Petition covers proposal of the BGCL for determination of the ARR and tariff for

FY 2017-18.

Section 62 of the Electricity Act, 2003 requires the licensee to furnish details as may be

specified by the Hon’ble Commission for determination of tariff. In addition, as per

the BERC (Terms and Conditions for Determination of Tariff) Regulations, 2007

notified by the Hon’ble Commission, the then BSEB or its unbundled companies or

any other licensee is required to file the Petition for all reasonable expenses which it

believes it would incur over the next financial year and seek the approval of the

Hon’ble Commission for the same. The filing is to be done based on the projections of

the expected revenue and costs.

The current Petition is prepared in accordance with the provisions of the following

Acts / Policies / Regulations:

Electricity Act, 2003;

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 14

National Electricity Policy;

Tariff Policy;

BERC (Terms and Conditions for Determination of Tariff) Regulations, 2007, as

amended time to time

BGCL has made genuine efforts for compiling all relevant information relating to the

ARR Petition as required by the Regulations issued by the Hon’ble Commission and

has also made every effort to ensure that information provided to the Hon’ble

Commission is accurate and free from material errors.

However, there may be certain deficiencies / infirmities in the Petitions owing to the

different aspects related with the operations of Transmission Company on

independent basis. Hence, BGCL prays to the Hon’ble Commission that the

information provided be accepted for the current filing and deficiencies if any, may

please be condoned. BGCL assures the Hon’ble Commission that appropriate

measures have been taken to improve the management information system for

improved data collection.

1.5 Contents of the Petition

The present petition comprises of main section namely:

Determination of ARR & Tariff for FY 2017-18; and

Proposed revenue recovery mechanism.

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 15

2 Approach for filing the Petition

The Hon’ble Commission in the Order dated January 4, 2013 in Case No. 20 of 2013 in

the matter of ‘Approval on Business Plan of Bihar Grid Company Limited (BGCL) for

the Control Period from FY 2014-15 to FY 2016-17 had stated the following:

“In view of the above, the Commission approves the Business Plan submitted by the petitioner

BGCL with the following conditions:

(1) The Business Plan will be implemented as per the cost estimate, investment schedule

and time schedule indicated in the Business Plan.

(2) The ARR of BGCL for FY 2015-16 and FY 2016-17 shall be computed after the

execution of the project based on the parameters specified in BERC (Terms and

Conditions for Determination of Tariff) Regulations, 2007 as amended from

time to time…”

BGCL is proposing to capitalise assets worth Rs. 35.31 Crore in FY 2016-17. The

remaining assets will be capitalised in FY 2017-18 and FY 2018-19, with majority of

capitalisation taking place in FY 2017-18.

In line with the above, BGCL is filing the present Petition for Determination of tariff

for FY 2017-18 in accordance with in BERC (Terms and Conditions for Determination

of Tariff) Regulations, 2007 read with its second amendment made in the year 2014.

As BGCL is the second Intra-State Transmission Licensee in Bihar, whose area of

operation overlaps with BSPTCL, the Petitioner has also proposed the methodology

for recovery of its Annual Revenue Requirement.

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 16

3 Determination of ARR for FY 2017-18

3.1 Introduction

The instant Petition relates to the approval of the Annual Revenue Requirement (ARR)

and Tariff for FY 2017-18. The ARR for FY 2017-18 has been prepared based on the

Business Plan approved by the Hon’ble Commission in Case No. 20 of 2013 vide Order

dated January 4, 2014, actual expenses incurred upto November 2016 and expected

commissioning of assets in February 2017. BGCL would like to inform the Hon’ble

Commission that assets worth Rs. 35.31 Crore will be commissioned in February 2017.

BGCL would approach the Hon’ble Commission at the appropriate time for seeking

approval for recovery of costs pertaining to such assets for FY 2016-17.

The methodology for recovery of Transmission Charges for FY 2017-18 have been

proposed in Chapter 4.

3.2 Transmission Loss

As per Regulation 92(d) of BERC (Terms and Conditions for determination of Tariff)

Regulations, 2007 as reproduced below, BGCL is required to file a loss reduction

trajectory for each year of the Control Period.

“(d) Loss reduction: The Licensees are required to file a loss reduction trajectory for

each year of the Control Period with upper and lower limits to enable fixation of incentives

/ penalties by the Commission. Reduction of transmission / distribution losses below the

approved range shall earn an incentive and such incentive shall be added to the ARR relating

to the subsequent control period. Similarly, lower beyond the approved range shall attract a

penalty to be deducted from the ARR of the subsequent control period. It would be desirable

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 17

that the levy of penalties is limited to 10% of the return on equity. The licensees shall comply

with the ‘Standards of Performance’ approved by the Commission.”

The current MYT Control Period spans from FY 2016-17 to FY 2018-19. BGCL is

expected to start only a part of its operation in February, 2017, however, more than

90% of its assets will be capitalised in FY 2017-18. As at this instant, BGCL is not

handling any energy, it is difficult to propose any Transmission Loss trajectory for

remaining years of the Control Period, i.e., for FY 2017-18 and FY 2018-19. Besides, all

the transmission lines will be commissioned in FY 2017-18, hence, BGCL can propose

transmission loss only from FY 2017-18 onwards. Therefore, BGCL requests the

Hon’ble Commission to approve the same trajectory for BGCL as proposed by

BSPTCL in their Tariff Petition for FY 2017-18. Any variation vis-à-vis the actual losses

can be reviewed at the time of truing up when actual data will be available.

Table 3-1: Transmission Loss Trajectory

Particulars FY 2017-18

(Expected)

FY 2018-19

(Expected)

Transmission Loss 4.89% 4.89%

3.3 Capital Investment Plan

The Petitioner had submitted the Capital Investment Plan of Rs. 1699.36 Crore in the

Business Plan Petition submitted before the Hon’ble Commission. The Hon’ble

Commission vide its Order dated January 4, 2014 in Case No. 20 of 2013 had duly

approved the Business Plan submitted by BGCL.

As per the approved Business Plan Order, BGCL was expected to incur capital

expenditure of Rs. 1699.36 Crore upto FY 2015-16, and all the assets were supposed to

be capitalised in FY 2015-16. However, against the Original Plan, BGCL is proposing

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 18

to capitalise assets worth only Rs. 35.31 Crore in FY 2016-17. The remaining assets will

be capitalised in FY 2017-18 and FY 2018-19, with majority capitalisation taking place

in FY 2017-18. BGCL would further like to submit that the delay in capital expenditure

is on account of the following main reasons:

i. Delay in equity infusion by promoters;

ii. Delay in handing over of land for sub-stations;

iii. Due to delay in equity infusion, there was delay in drawing of loan. The first

loan from REC was drawn on February 19, 2015;

iv. Scarcity of construction material, viz., fine aggregates in the State of Bihar due

to certain policy measures of Govt. of Bihar;

v. Delay in obtaining Right of Way (ROW) from local landowners and villagers;

vi. Delay in construction due to frequent bandh calls given by Naxalites; and

vii. Severe floods in 2016.

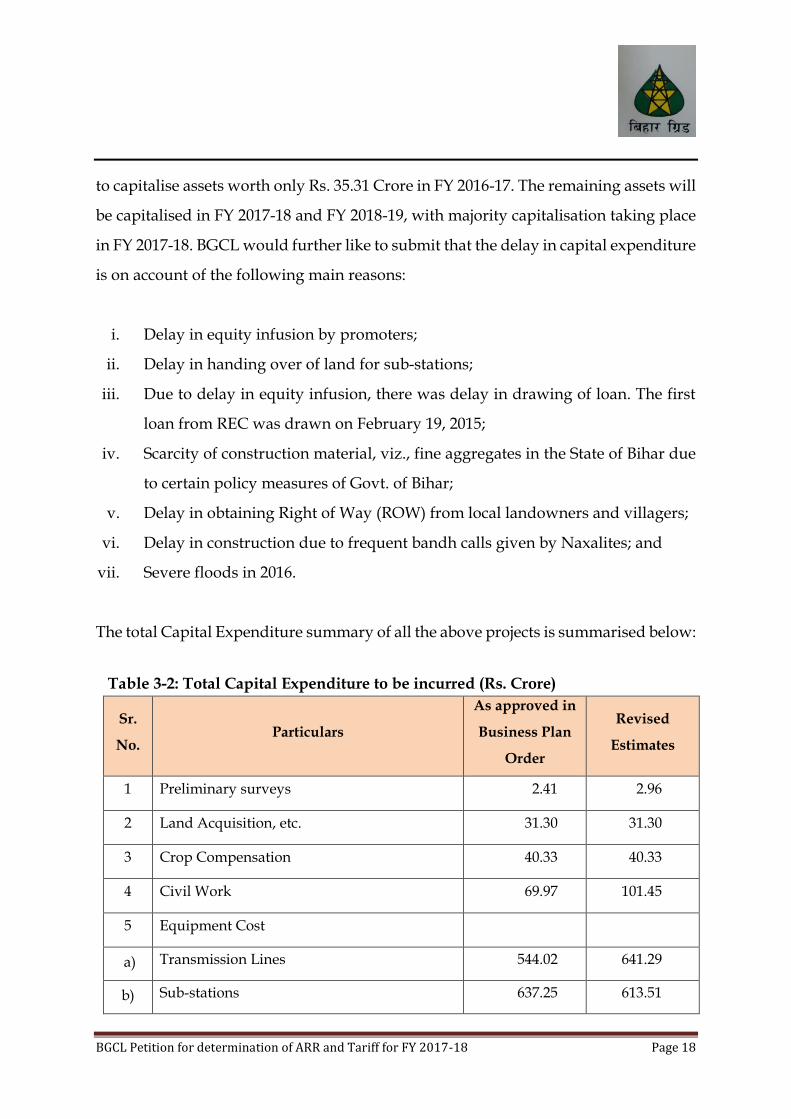

The total Capital Expenditure summary of all the above projects is summarised below:

Table 3-2: Total Capital Expenditure to be incurred (Rs. Crore)

Sr.

No. Particulars

As approved in

Business Plan

Order

Revised

Estimates

1 Preliminary surveys 2.41 2.96

2 Land Acquisition, etc. 31.30 31.30

3 Crop Compensation 40.33 40.33

4 Civil Work 69.97 101.45

5 Equipment Cost

a) Transmission Lines 544.02 641.29

b) Sub-stations 637.25 613.51

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 19

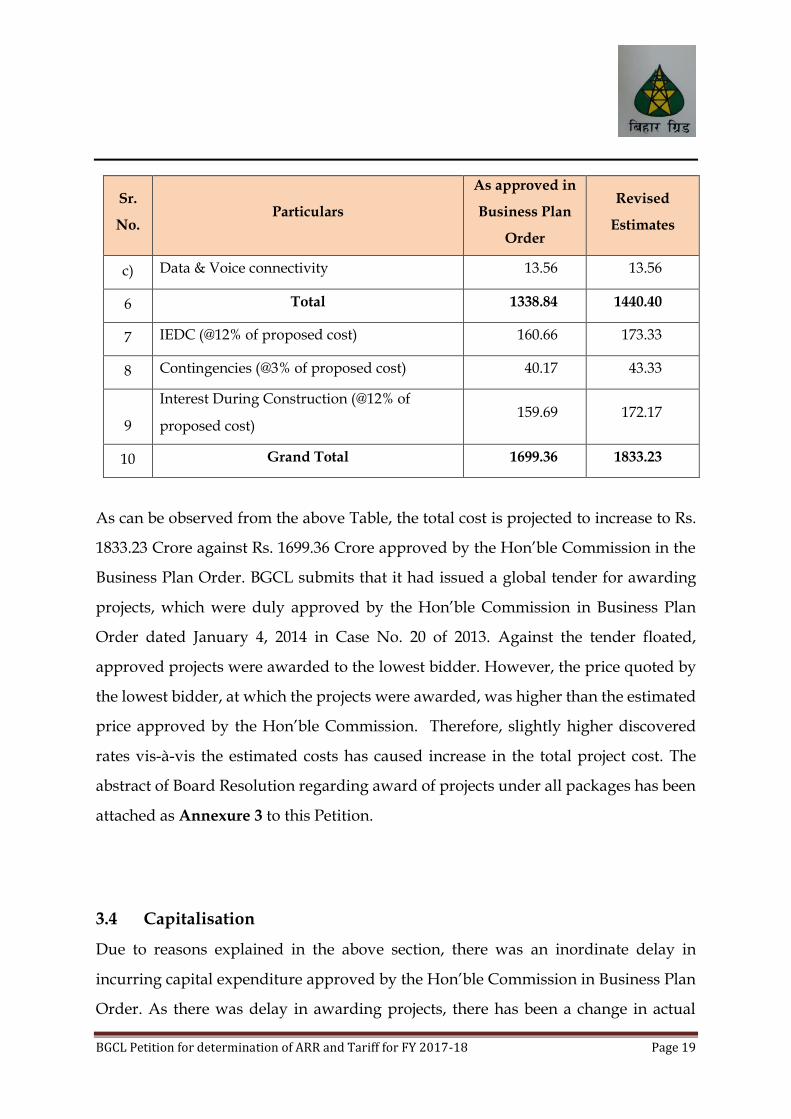

Sr.

No. Particulars

As approved in

Business Plan

Order

Revised

Estimates

c) Data & Voice connectivity 13.56 13.56

6 Total 1338.84 1440.40

7 IEDC (@12% of proposed cost) 160.66 173.33

8 Contingencies (@3% of proposed cost) 40.17 43.33

9

Interest During Construction (@12% of

proposed cost) 159.69 172.17

10 Grand Total 1699.36 1833.23

As can be observed from the above Table, the total cost is projected to increase to Rs.

1833.23 Crore against Rs. 1699.36 Crore approved by the Hon’ble Commission in the

Business Plan Order. BGCL submits that it had issued a global tender for awarding

projects, which were duly approved by the Hon’ble Commission in Business Plan

Order dated January 4, 2014 in Case No. 20 of 2013. Against the tender floated,

approved projects were awarded to the lowest bidder. However, the price quoted by

the lowest bidder, at which the projects were awarded, was higher than the estimated

price approved by the Hon’ble Commission. Therefore, slightly higher discovered

rates vis-à-vis the estimated costs has caused increase in the total project cost. The

abstract of Board Resolution regarding award of projects under all packages has been

attached as Annexure 3 to this Petition.

3.4 Capitalisation

Due to reasons explained in the above section, there was an inordinate delay in

incurring capital expenditure approved by the Hon’ble Commission in Business Plan

Order. As there was delay in awarding projects, there has been a change in actual

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 20

capitalisation schedule vis-à-vis the capitalisation schedule approved. As is evident

from the Tables shown below, the entire capital expenditure of Rs. 1699.33 Crore was

supposed to be capitalised in FY 2015-16. However, as per the revised schedule, assets

will be capitalised over a period of three years from FY 2016-17 to FY 2018-19, where

a major portion of assets will get capitalised in FY 2017-18.

BGCL submits that assets worth Rs. 35.31 Crore are expected to get capitalised in FY

2016-17. Further, in FY 2017-18 approximately all the assets will be capitalised by the

end of 1st quarter. Therefore, IEDC and IDC have been computed accordingly and it

might vary vis-à-vis the revised estimates submitted. Actual expenses will be known

only after assets are commissioned and the same will be submitted before the Hon’ble

Commission at the time of truing up for respective years.

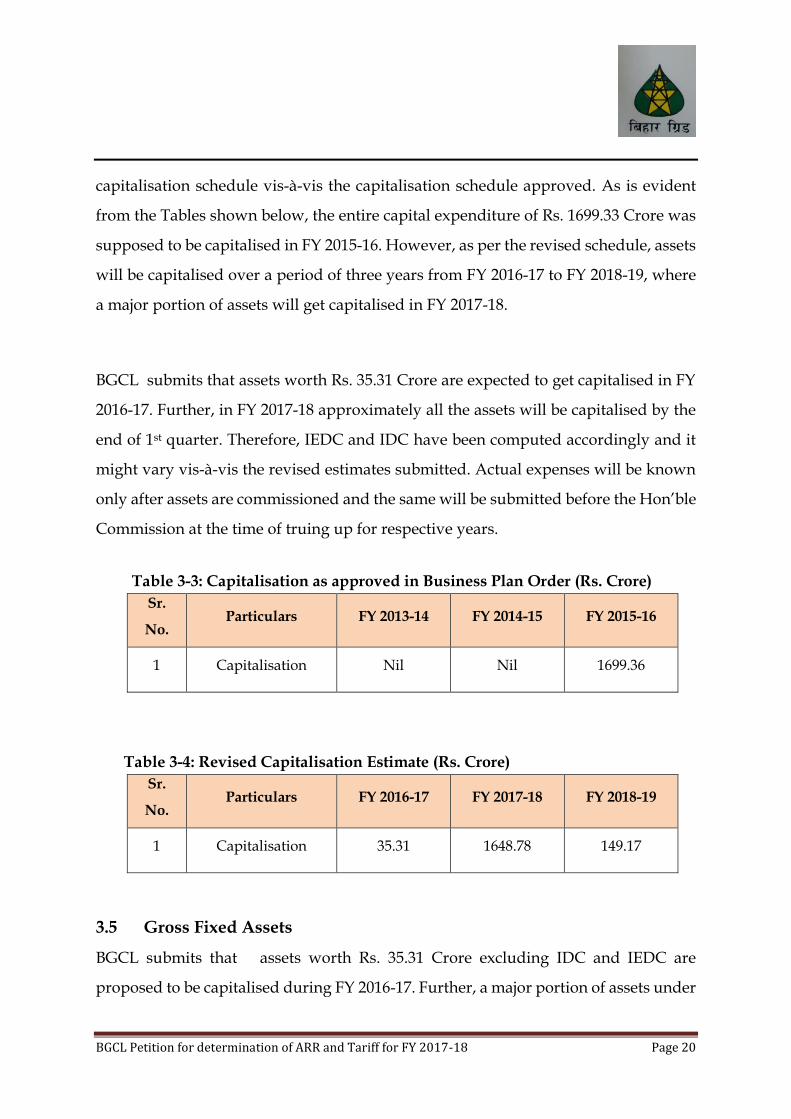

Table 3-3: Capitalisation as approved in Business Plan Order (Rs. Crore)

Sr.

No. Particulars FY 2013-14 FY 2014-15 FY 2015-16

1 Capitalisation Nil Nil 1699.36

Table 3-4: Revised Capitalisation Estimate (Rs. Crore)

Sr.

No. Particulars FY 2016-17 FY 2017-18 FY 2018-19

1 Capitalisation 35.31 1648.78 149.17

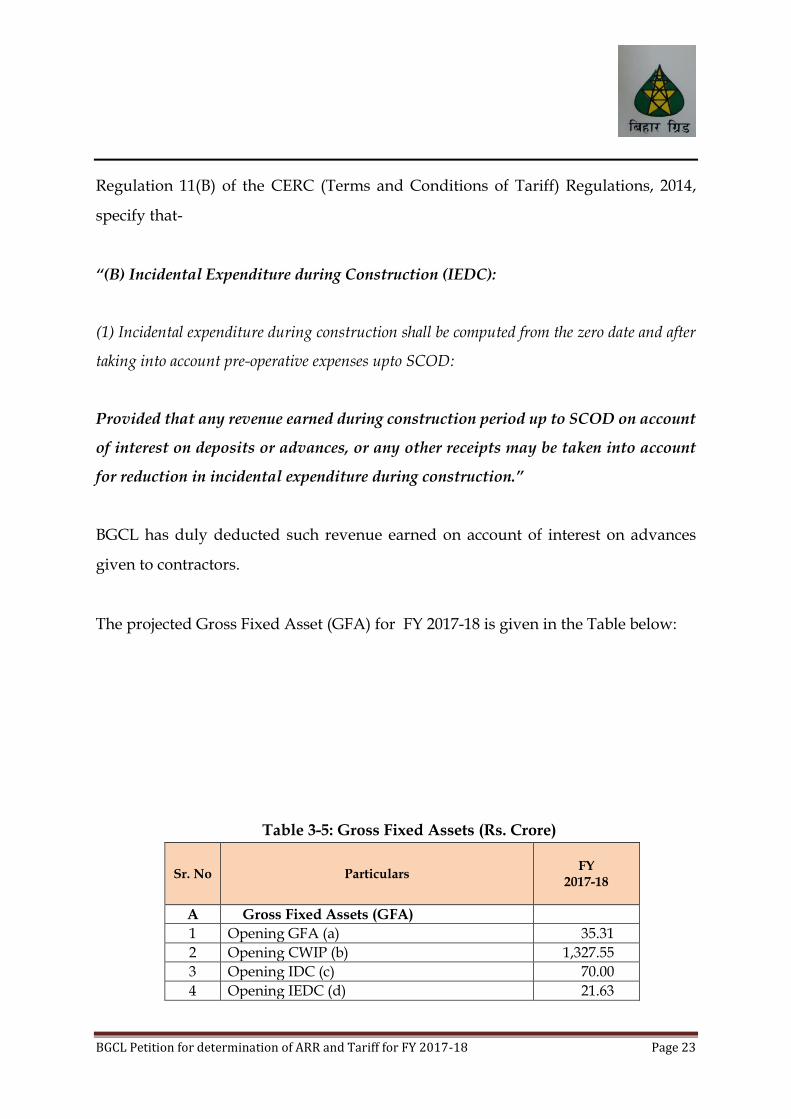

3.5 Gross Fixed Assets

BGCL submits that assets worth Rs. 35.31 Crore excluding IDC and IEDC are

proposed to be capitalised during FY 2016-17. Further, a major portion of assets under

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 21

construction will be commissioned by the end of first quarter of FY 2017-18. Therefore,

the Petitioner has projected GFA for FY 2017-18 including IDC and IEDC for assets

getting capitalised in FY 2017-18, excluding for the assets which will be capitalised in

FY 2016-17.

BGCL further submits that as per the approved Business Plan, it is implementing

projects, the purpose of which is to strengthen the existing network of BSPTCL. The

assets being constructed by BGCL are connected to BSPTCL system at 220 kV, 132 kV

and 33 kV. Therefore, BGCL is acting like an additional link between Generation,

Transmission and Distribution Company, as BGCL will evacuate power from Central

and State Generating Stations and feed it into the State’s Transmission system.

As BGCL will connect the Generating Stations and Distribution Companies to Intra-

State Transmission system, in the absence of downstream assets (which are to be built

by BSPTCL and Discoms), there is a possibility that despite being commissioned,

BGCL’s asset might not be put to use. To prevent any Transmission Licensee from

such unforeseen contingencies, the Hon’ble Central ERC in Regulation 4(3)(ii) of the

CERC (Terms and Conditions of Tariff) Regulations, 2014 has specified as under:

“4. Date of Commercial Operation: The date of commercial operation of a generating station

or unit or block thereof or a transmission system or element thereof shall be determined as

under:

…

…

(3) (ii) in case a transmission system or an element thereof is prevented from regular service

for reasons not attributable to the transmission licensee or its supplier or its

contractors but is on account of the delay in commissioning of the concerned generating

station or in commissioning of the upstream or downstream transmission system, the

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 22

transmission licensee shall approach the Commission through an appropriate

application for approval of the date of commercial operation of such transmission

system or an element thereof.” (emphasis added)

Similarly, the Hon’ble Maharashtra ERC in Regulation 2.1(23)(c) of the MERC (Multi

Year Tariff) Regulations, 2015, has provided for necessary relief against such

contingency, as reproduced below:

“(23) “Date of Commercial Operation” or "COD" means –

…

…

…

c. in case of a transmission system, the date declared….

Provided that, in case a transmission system or an element thereof is prevented from

regular service for reasons not attributable to the Transmission Licensee or its

suppliers or contractors but on account of the delay in commissioning of the

concerned generating Station or the upstream or downstream transmission system or

distribution system, the Transmission Licensee may seek approval of the Commission

of the date of commercial operation of such transmission system or an element

thereof;” (emphasis added)

Therefore, the Petitioner submits before the Hon’ble Commission that it shall

approach the Hon’ble Commission through an appropriate application for approval

of the date of commercial operation of its transmission system or an element thereof.

Based on the approved date of COD, the Hon’ble Commission may provide necessary

relief in case BGCL’s assets are not put to use for reasons not attributable to BGCL,

even after commissioning of such assets.

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 23

Regulation 11(B) of the CERC (Terms and Conditions of Tariff) Regulations, 2014,

specify that-

“(B) Incidental Expenditure during Construction (IEDC):

(1) Incidental expenditure during construction shall be computed from the zero date and after

taking into account pre-operative expenses upto SCOD:

Provided that any revenue earned during construction period up to SCOD on account

of interest on deposits or advances, or any other receipts may be taken into account

for reduction in incidental expenditure during construction.”

BGCL has duly deducted such revenue earned on account of interest on advances

given to contractors.

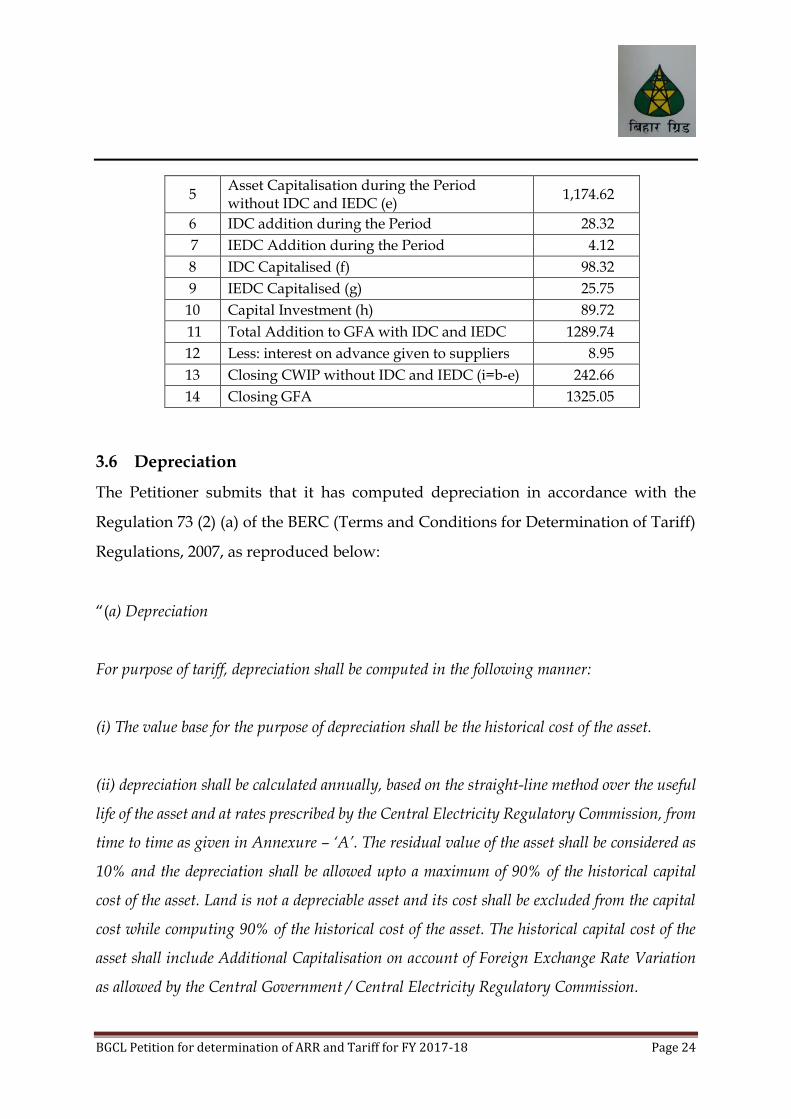

The projected Gross Fixed Asset (GFA) for FY 2017-18 is given in the Table below:

Table 3-5: Gross Fixed Assets (Rs. Crore)

Sr. No Particulars FY

2017-18

A Gross Fixed Assets (GFA)

1 Opening GFA (a) 35.31

2 Opening CWIP (b) 1,327.55

3 Opening IDC (c) 70.00

4 Opening IEDC (d) 21.63

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 24

5 Asset Capitalisation during the Period without IDC and IEDC (e)

1,174.62

6 IDC addition during the Period 28.32

7 IEDC Addition during the Period 4.12

8 IDC Capitalised (f) 98.32

9 IEDC Capitalised (g) 25.75

10 Capital Investment (h) 89.72

11 Total Addition to GFA with IDC and IEDC 1289.74

12 Less: interest on advance given to suppliers 8.95

13 Closing CWIP without IDC and IEDC (i=b-e) 242.66

14 Closing GFA 1325.05

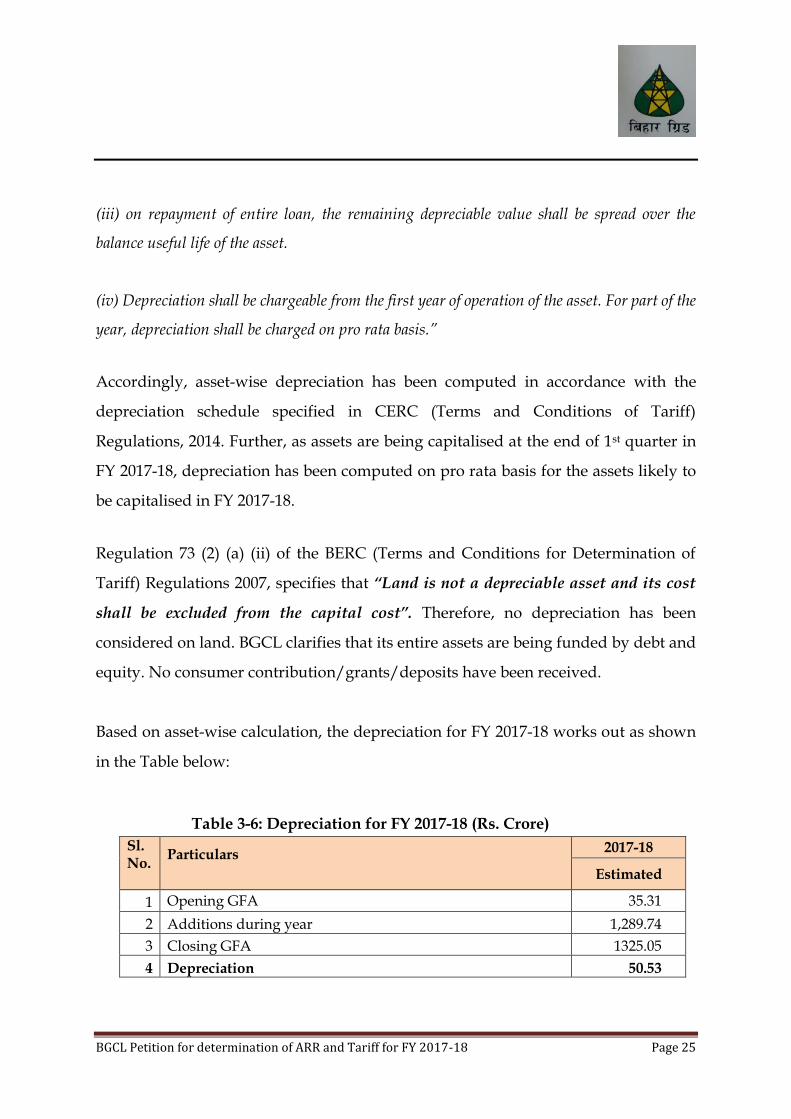

3.6 Depreciation

The Petitioner submits that it has computed depreciation in accordance with the

Regulation 73 (2) (a) of the BERC (Terms and Conditions for Determination of Tariff)

Regulations, 2007, as reproduced below:

“(a) Depreciation

For purpose of tariff, depreciation shall be computed in the following manner:

(i) The value base for the purpose of depreciation shall be the historical cost of the asset.

(ii) depreciation shall be calculated annually, based on the straight-line method over the useful

life of the asset and at rates prescribed by the Central Electricity Regulatory Commission, from

time to time as given in Annexure – ‘A’. The residual value of the asset shall be considered as

10% and the depreciation shall be allowed upto a maximum of 90% of the historical capital

cost of the asset. Land is not a depreciable asset and its cost shall be excluded from the capital

cost while computing 90% of the historical cost of the asset. The historical capital cost of the

asset shall include Additional Capitalisation on account of Foreign Exchange Rate Variation

as allowed by the Central Government / Central Electricity Regulatory Commission.

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 25

(iii) on repayment of entire loan, the remaining depreciable value shall be spread over the

balance useful life of the asset.

(iv) Depreciation shall be chargeable from the first year of operation of the asset. For part of the

year, depreciation shall be charged on pro rata basis.”

Accordingly, asset-wise depreciation has been computed in accordance with the

depreciation schedule specified in CERC (Terms and Conditions of Tariff)

Regulations, 2014. Further, as assets are being capitalised at the end of 1st quarter in

FY 2017-18, depreciation has been computed on pro rata basis for the assets likely to

be capitalised in FY 2017-18.

Regulation 73 (2) (a) (ii) of the BERC (Terms and Conditions for Determination of

Tariff) Regulations 2007, specifies that “Land is not a depreciable asset and its cost

shall be excluded from the capital cost”. Therefore, no depreciation has been

considered on land. BGCL clarifies that its entire assets are being funded by debt and

equity. No consumer contribution/grants/deposits have been received.

Based on asset-wise calculation, the depreciation for FY 2017-18 works out as shown

in the Table below:

Table 3-6: Depreciation for FY 2017-18 (Rs. Crore)

Sl. No.

Particulars

2017-18

Estimated

1 Opening GFA 35.31

2 Additions during year 1,289.74

3 Closing GFA 1325.05

4 Depreciation 50.53

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 26

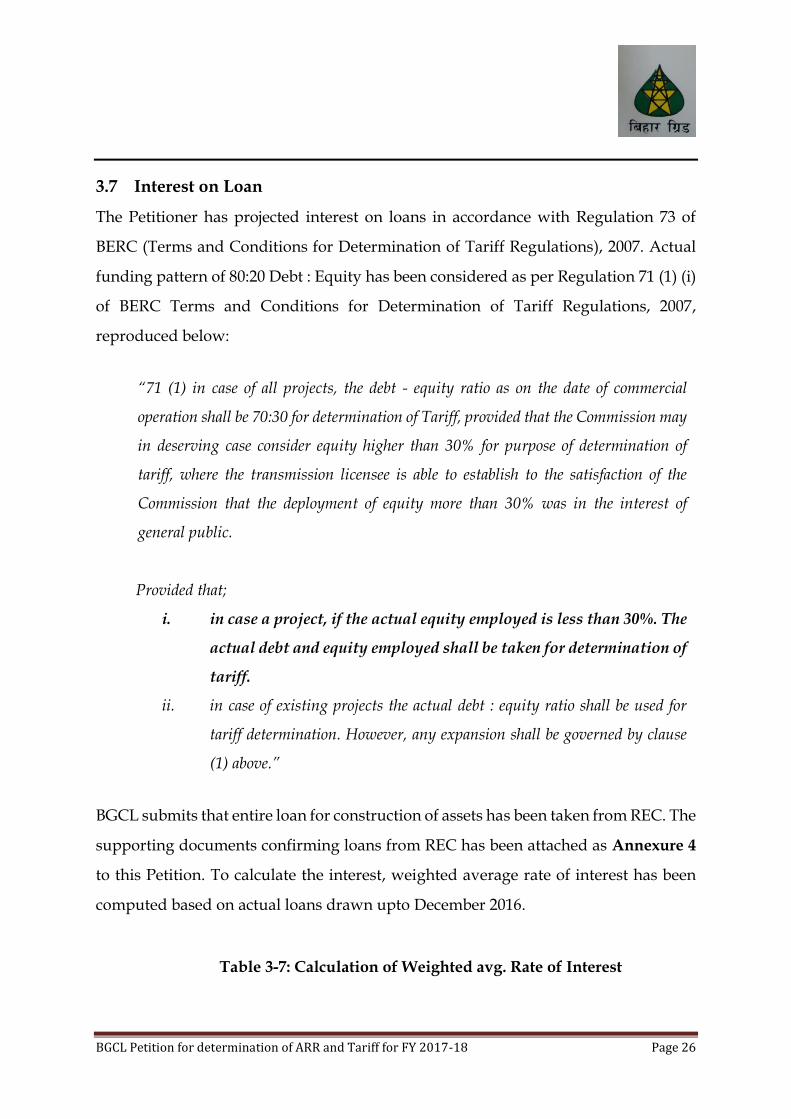

3.7 Interest on Loan

The Petitioner has projected interest on loans in accordance with Regulation 73 of

BERC (Terms and Conditions for Determination of Tariff Regulations), 2007. Actual

funding pattern of 80:20 Debt : Equity has been considered as per Regulation 71 (1) (i)

of BERC Terms and Conditions for Determination of Tariff Regulations, 2007,

reproduced below:

“71 (1) in case of all projects, the debt - equity ratio as on the date of commercial

operation shall be 70:30 for determination of Tariff, provided that the Commission may

in deserving case consider equity higher than 30% for purpose of determination of

tariff, where the transmission licensee is able to establish to the satisfaction of the

Commission that the deployment of equity more than 30% was in the interest of

general public.

Provided that;

i. in case a project, if the actual equity employed is less than 30%. The

actual debt and equity employed shall be taken for determination of

tariff.

ii. in case of existing projects the actual debt : equity ratio shall be used for

tariff determination. However, any expansion shall be governed by clause

(1) above.”

BGCL submits that entire loan for construction of assets has been taken from REC. The

supporting documents confirming loans from REC has been attached as Annexure 4

to this Petition. To calculate the interest, weighted average rate of interest has been

computed based on actual loans drawn upto December 2016.

Table 3-7: Calculation of Weighted avg. Rate of Interest

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 27

Loan Drawal Date Amount (Rs.) RoI (%)

19-02-15 49988447 11.50%

02-03-15 150000000 11.50%

27-03-15 185000000 11.50%

13-05-15 125000000 11.50%

01-07-15 291799604 11.10%

16-10-15 510000000 11.10%

30-11-15 205000000 10.75%

13-01-16 280000000 10.75%

17-02-16 203200000 10.75%

07-03-16 680400000 10.75%

28-03-16 283500000 10.75%

31-03-16 56370883 10.75%

11-04-16 204400000 10.75%

25-05-16 435300000 10.75%

17-06-15 340000000 10.75%

18-07-16 60000000 10.75%

18-07-16 440000000 10.75%

12-09-16 700000000 10.75%

20-10-16 1000000000 10.75%

21-12-16 1270000000 10.75%

Weighted Avg. RoI 10.84%

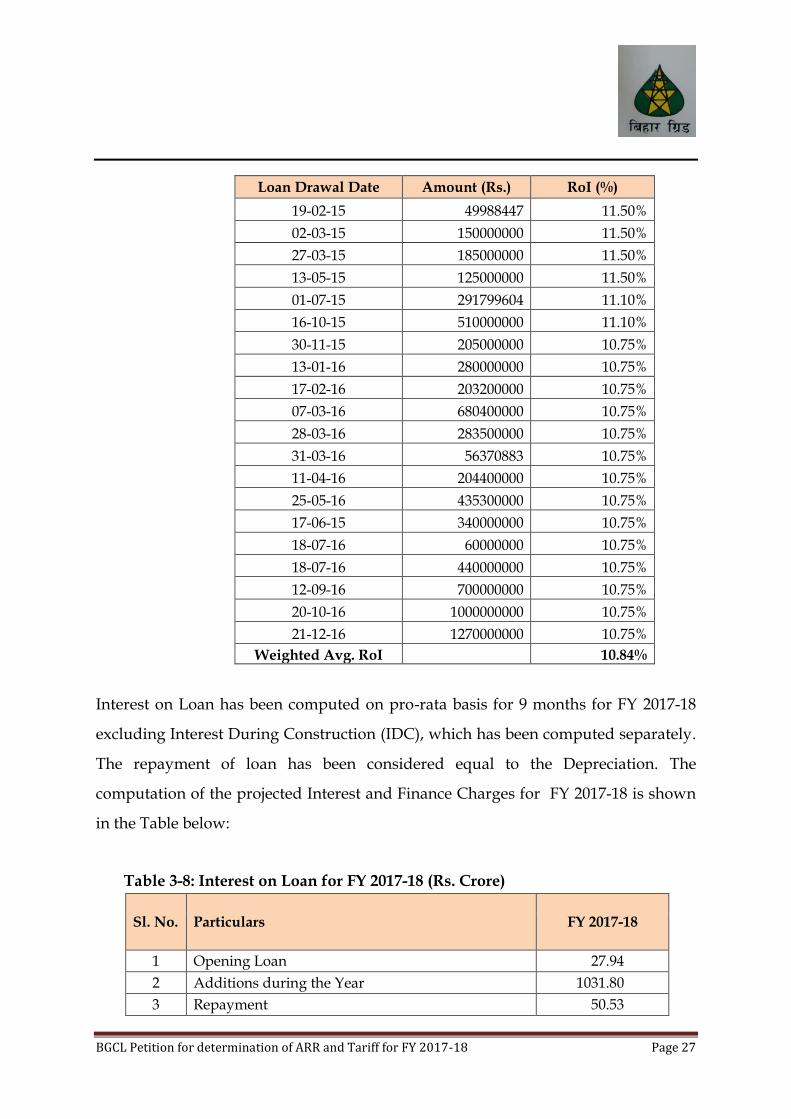

Interest on Loan has been computed on pro-rata basis for 9 months for FY 2017-18

excluding Interest During Construction (IDC), which has been computed separately.

The repayment of loan has been considered equal to the Depreciation. The

computation of the projected Interest and Finance Charges for FY 2017-18 is shown

in the Table below:

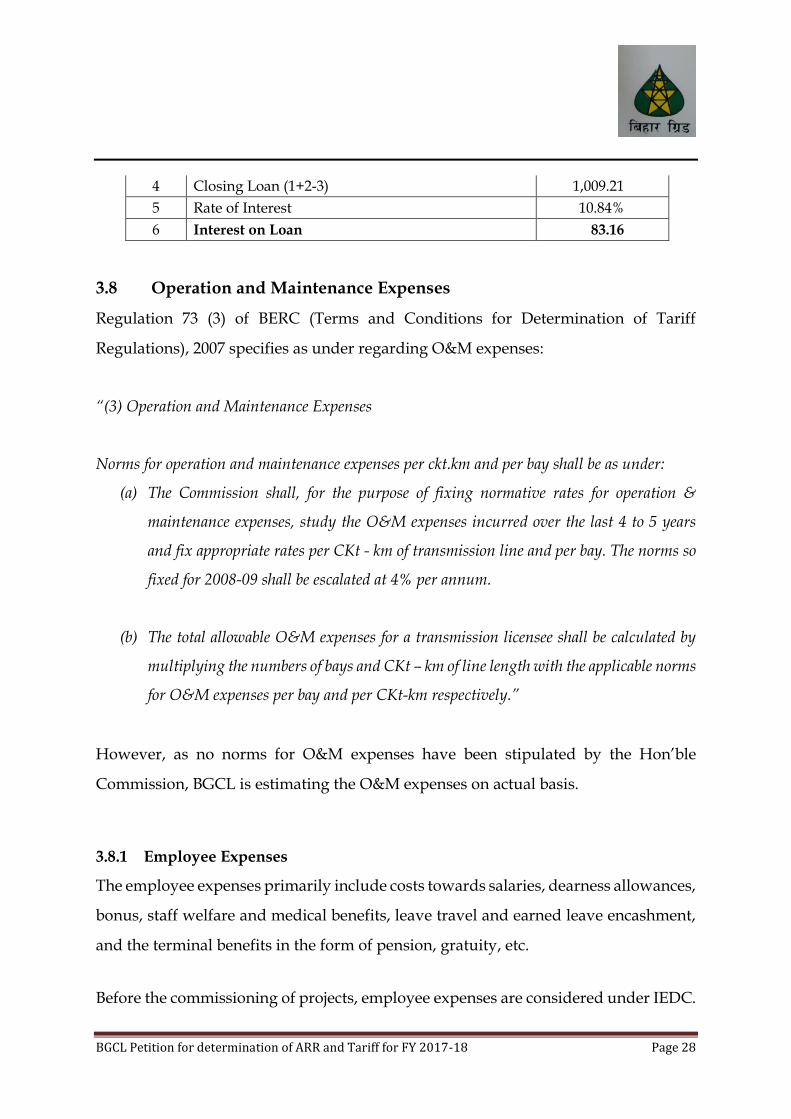

Table 3-8: Interest on Loan for FY 2017-18 (Rs. Crore)

Sl. No. Particulars FY 2017-18

1 Opening Loan 27.94

2 Additions during the Year 1031.80

3 Repayment 50.53

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 28

4 Closing Loan (1+2-3) 1,009.21

5 Rate of Interest 10.84%

6 Interest on Loan 83.16

3.8 Operation and Maintenance Expenses

Regulation 73 (3) of BERC (Terms and Conditions for Determination of Tariff

Regulations), 2007 specifies as under regarding O&M expenses:

“(3) Operation and Maintenance Expenses

Norms for operation and maintenance expenses per ckt.km and per bay shall be as under:

(a) The Commission shall, for the purpose of fixing normative rates for operation &

maintenance expenses, study the O&M expenses incurred over the last 4 to 5 years

and fix appropriate rates per CKt - km of transmission line and per bay. The norms so

fixed for 2008-09 shall be escalated at 4% per annum.

(b) The total allowable O&M expenses for a transmission licensee shall be calculated by

multiplying the numbers of bays and CKt – km of line length with the applicable norms

for O&M expenses per bay and per CKt-km respectively.”

However, as no norms for O&M expenses have been stipulated by the Hon’ble

Commission, BGCL is estimating the O&M expenses on actual basis.

3.8.1 Employee Expenses

The employee expenses primarily include costs towards salaries, dearness allowances,

bonus, staff welfare and medical benefits, leave travel and earned leave encashment,

and the terminal benefits in the form of pension, gratuity, etc.

Before the commissioning of projects, employee expenses are considered under IEDC.

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 29

Employee expenses for FY 2017-18 have been estimated on pro-rata basis for 9 months,

as assets are scheduled to be capitalised at the end of 1st quarter. While projecting

employee expenses for FY 2017-18, the Petitioner has factored in the impact which will

occur due to impending Pay Revision. The Govt. had provided a hike of 30% in

salaries on the basis of recommendations of the Pay Commission in 2007. Therefore,

while estimating salaries for Dec’16 to Mar’17, BGCL has considered an increase of

30% over the actual salary expenses in the first 8 months of FY 2016-17.

The actual employee expenses till Nov’16 and estimated expenses from Dec’16 to

Mar’17, together have been considered as base expenses for projecting employee

expenses for FY 2017-18. An escalation of 10% over the estimated employee expenses

for FY 2016-17, has been considered while projecting employee expenses for FY 2017-

18.

Further, BGCL intends to recruit seven employees in Grade E4, four Junior Engineers

and six technicians. Expenses on account of proposed hiring has been factored in

employee expenses for FY 2017-18. As total manpower available at BGCL is not

adequate to cater to the upcoming vast network of transmission assets, the Petitioner

is also planning to recruit manpower on contractual basis for O&M services. It is

estimated that contracting out services will cost BGCL approximately Rs. 3.40 Lakh

per month per sub-station. The cost estimate for contracting out services for first three

months has already been approved by the management.

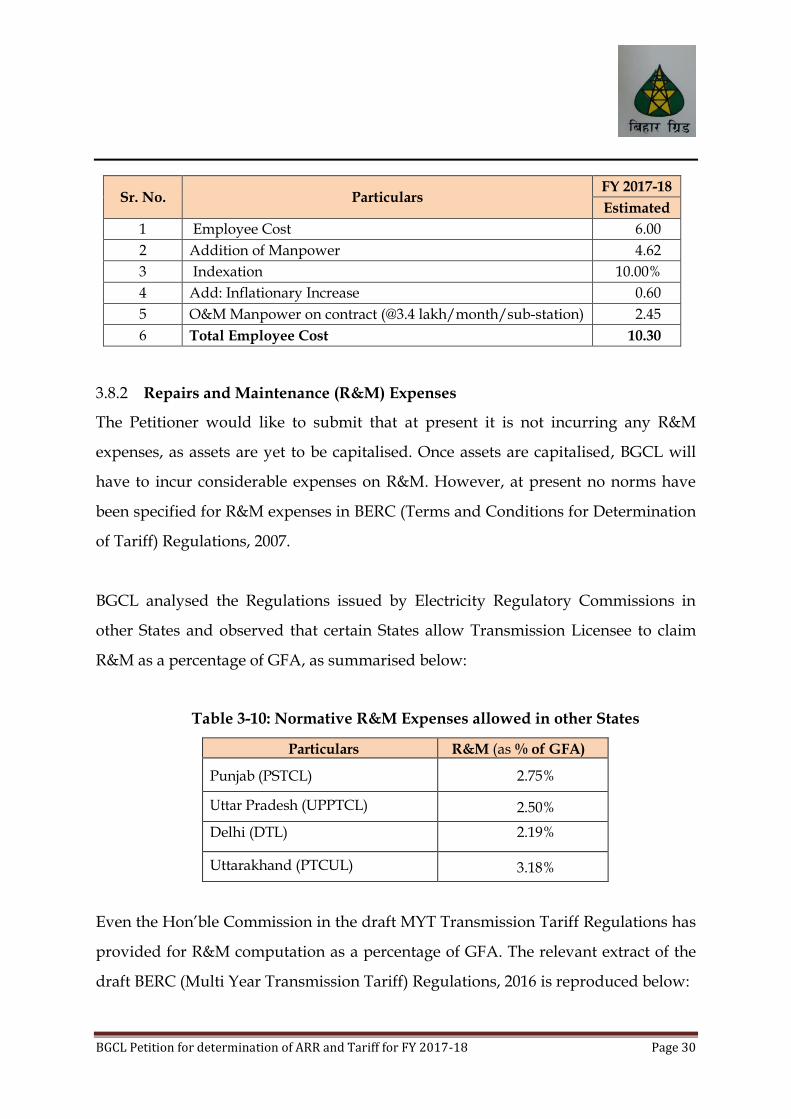

The Employee Expenses for FY 2017-18 as computed by the Petitioner is shown in the

Table below:

Table 3-9: Projected Employee Expenses for FY 2017-18 (Rs. Crore)

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 30

Sr. No. Particulars FY 2017-18

Estimated

1 Employee Cost 6.00

2 Addition of Manpower 4.62

3 Indexation 10.00%

4 Add: Inflationary Increase 0.60

5 O&M Manpower on contract (@3.4 lakh/month/sub-station) 2.45

6 Total Employee Cost 10.30

3.8.2 Repairs and Maintenance (R&M) Expenses

The Petitioner would like to submit that at present it is not incurring any R&M

expenses, as assets are yet to be capitalised. Once assets are capitalised, BGCL will

have to incur considerable expenses on R&M. However, at present no norms have

been specified for R&M expenses in BERC (Terms and Conditions for Determination

of Tariff) Regulations, 2007.

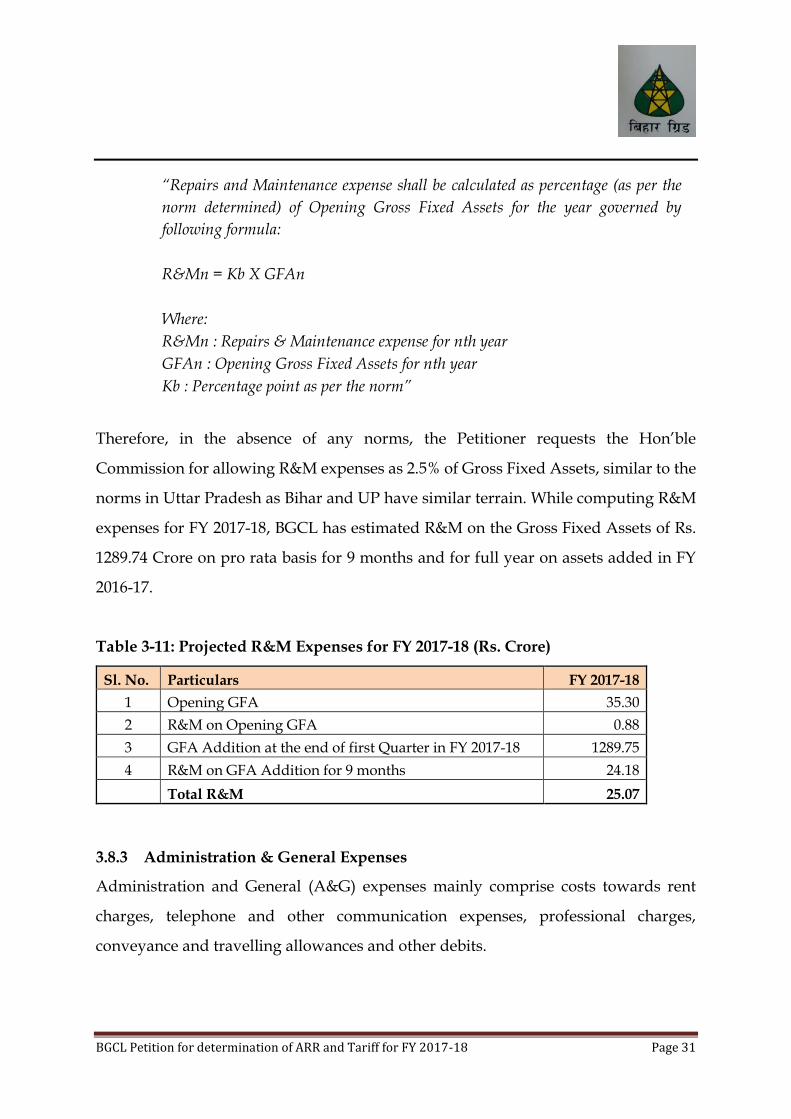

BGCL analysed the Regulations issued by Electricity Regulatory Commissions in

other States and observed that certain States allow Transmission Licensee to claim

R&M as a percentage of GFA, as summarised below:

Table 3-10: Normative R&M Expenses allowed in other States

Particulars R&M (as % of GFA)

Punjab (PSTCL) 2.75%

Uttar Pradesh (UPPTCL) 2.50%

Delhi (DTL) 2.19%

Uttarakhand (PTCUL) 3.18%

Even the Hon’ble Commission in the draft MYT Transmission Tariff Regulations has

provided for R&M computation as a percentage of GFA. The relevant extract of the

draft BERC (Multi Year Transmission Tariff) Regulations, 2016 is reproduced below:

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 31

“Repairs and Maintenance expense shall be calculated as percentage (as per the

norm determined) of Opening Gross Fixed Assets for the year governed by

following formula:

R&Mn = Kb X GFAn

Where:

R&Mn : Repairs & Maintenance expense for nth year

GFAn : Opening Gross Fixed Assets for nth year

Kb : Percentage point as per the norm”

Therefore, in the absence of any norms, the Petitioner requests the Hon’ble

Commission for allowing R&M expenses as 2.5% of Gross Fixed Assets, similar to the

norms in Uttar Pradesh as Bihar and UP have similar terrain. While computing R&M

expenses for FY 2017-18, BGCL has estimated R&M on the Gross Fixed Assets of Rs.

1289.74 Crore on pro rata basis for 9 months and for full year on assets added in FY

2016-17.

Table 3-11: Projected R&M Expenses for FY 2017-18 (Rs. Crore)

Sl. No. Particulars FY 2017-18

1 Opening GFA 35.30

2 R&M on Opening GFA 0.88

3 GFA Addition at the end of first Quarter in FY 2017-18 1289.75

4 R&M on GFA Addition for 9 months 24.18

Total R&M 25.07

3.8.3 Administration & General Expenses

Administration and General (A&G) expenses mainly comprise costs towards rent

charges, telephone and other communication expenses, professional charges,

conveyance and travelling allowances and other debits.

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 32

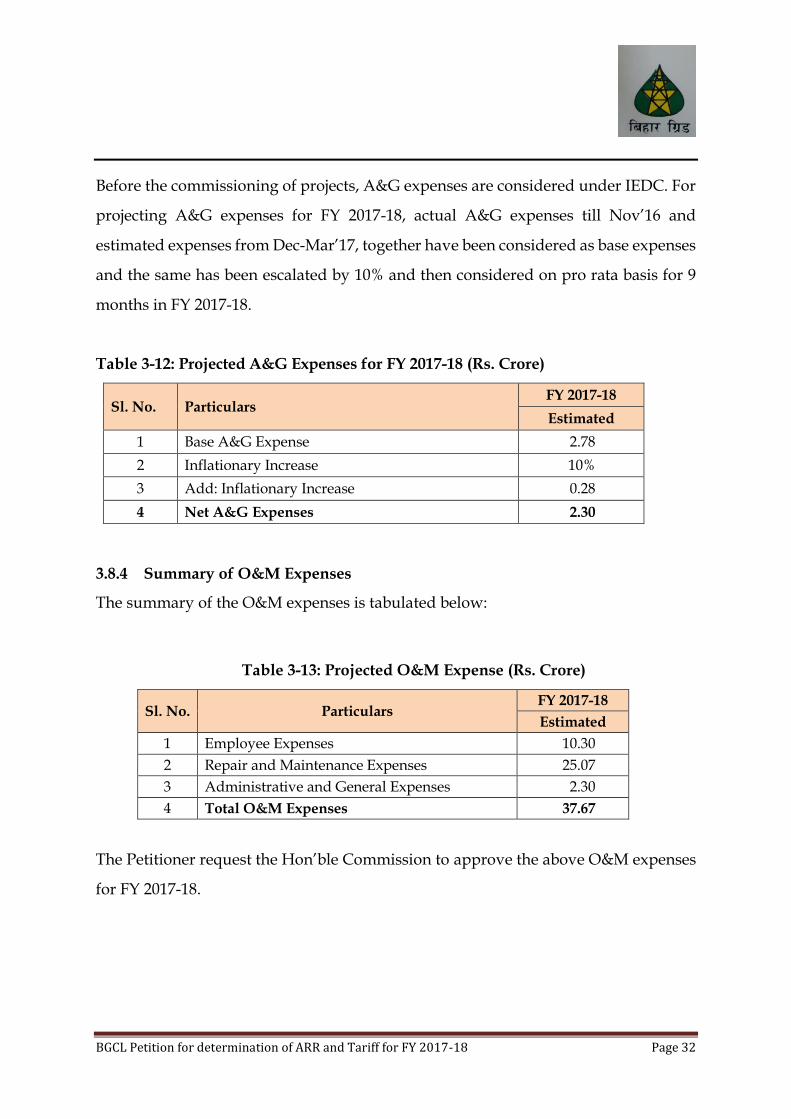

Before the commissioning of projects, A&G expenses are considered under IEDC. For

projecting A&G expenses for FY 2017-18, actual A&G expenses till Nov’16 and

estimated expenses from Dec-Mar’17, together have been considered as base expenses

and the same has been escalated by 10% and then considered on pro rata basis for 9

months in FY 2017-18.

Table 3-12: Projected A&G Expenses for FY 2017-18 (Rs. Crore)

Sl. No. Particulars FY 2017-18

Estimated

1 Base A&G Expense 2.78

2 Inflationary Increase 10%

3 Add: Inflationary Increase 0.28

4 Net A&G Expenses 2.30

3.8.4 Summary of O&M Expenses

The summary of the O&M expenses is tabulated below:

Table 3-13: Projected O&M Expense (Rs. Crore)

Sl. No. Particulars FY 2017-18

Estimated

1 Employee Expenses 10.30

2 Repair and Maintenance Expenses 25.07

3 Administrative and General Expenses 2.30

4 Total O&M Expenses 37.67

The Petitioner request the Hon’ble Commission to approve the above O&M expenses

for FY 2017-18.

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 33

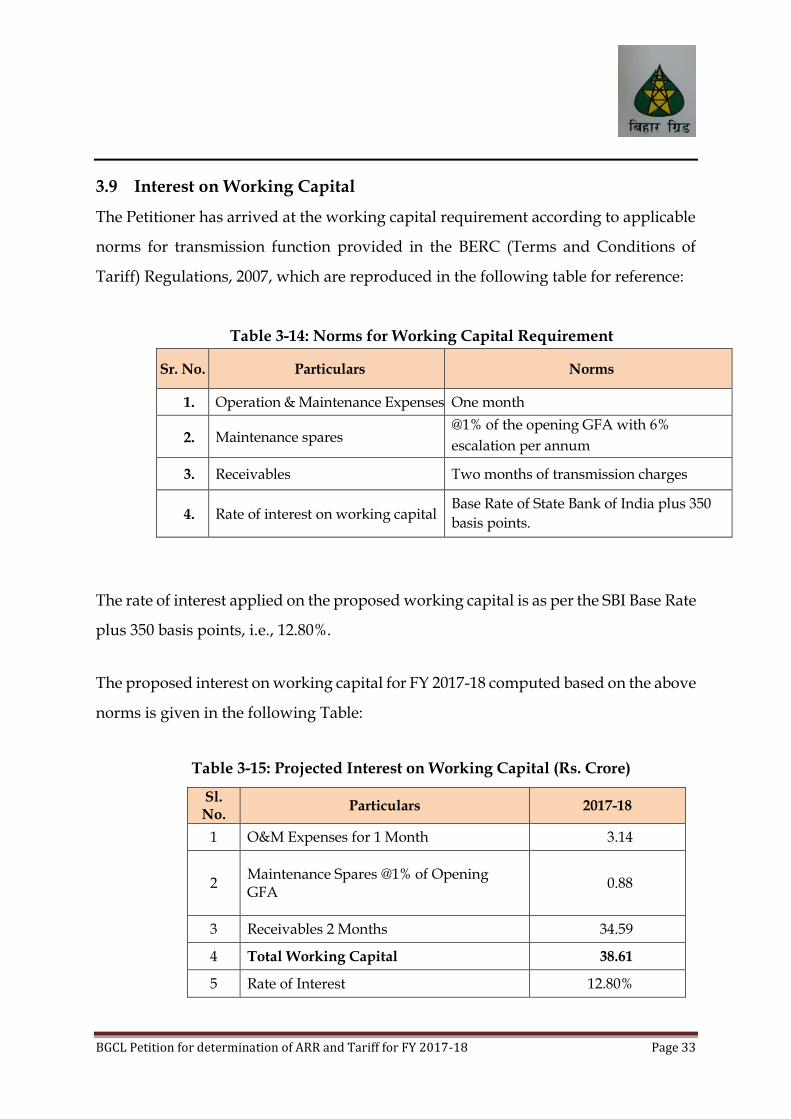

3.9 Interest on Working Capital

The Petitioner has arrived at the working capital requirement according to applicable

norms for transmission function provided in the BERC (Terms and Conditions of

Tariff) Regulations, 2007, which are reproduced in the following table for reference:

Table 3-14: Norms for Working Capital Requirement

Sr. No. Particulars Norms

1. Operation & Maintenance Expenses One month

2. Maintenance spares @1% of the opening GFA with 6%

escalation per annum

3. Receivables Two months of transmission charges

4. Rate of interest on working capital Base Rate of State Bank of India plus 350

basis points.

The rate of interest applied on the proposed working capital is as per the SBI Base Rate

plus 350 basis points, i.e., 12.80%.

The proposed interest on working capital for FY 2017-18 computed based on the above

norms is given in the following Table:

Table 3-15: Projected Interest on Working Capital (Rs. Crore)

Sl. No.

Particulars 2017-18

1 O&M Expenses for 1 Month 3.14

2 Maintenance Spares @1% of Opening GFA

0.88

3 Receivables 2 Months 34.59

4 Total Working Capital 38.61

5 Rate of Interest 12.80%

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 34

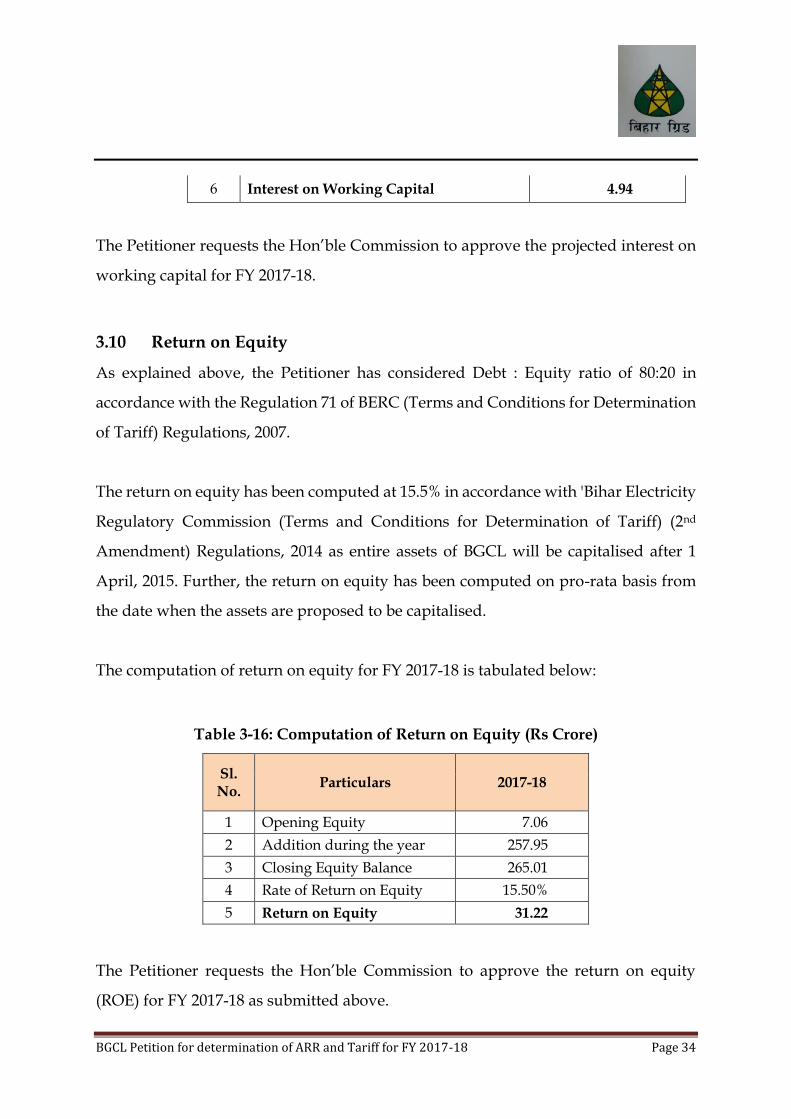

6 Interest on Working Capital 4.94

The Petitioner requests the Hon’ble Commission to approve the projected interest on

working capital for FY 2017-18.

3.10 Return on Equity

As explained above, the Petitioner has considered Debt : Equity ratio of 80:20 in

accordance with the Regulation 71 of BERC (Terms and Conditions for Determination

of Tariff) Regulations, 2007.

The return on equity has been computed at 15.5% in accordance with 'Bihar Electricity

Regulatory Commission (Terms and Conditions for Determination of Tariff) (2nd

Amendment) Regulations, 2014 as entire assets of BGCL will be capitalised after 1

April, 2015. Further, the return on equity has been computed on pro-rata basis from

the date when the assets are proposed to be capitalised.

The computation of return on equity for FY 2017-18 is tabulated below:

Table 3-16: Computation of Return on Equity (Rs Crore)

Sl. No.

Particulars 2017-18

1 Opening Equity 7.06

2 Addition during the year 257.95

3 Closing Equity Balance 265.01

4 Rate of Return on Equity 15.50%

5 Return on Equity 31.22

The Petitioner requests the Hon’ble Commission to approve the return on equity

(ROE) for FY 2017-18 as submitted above.

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 35

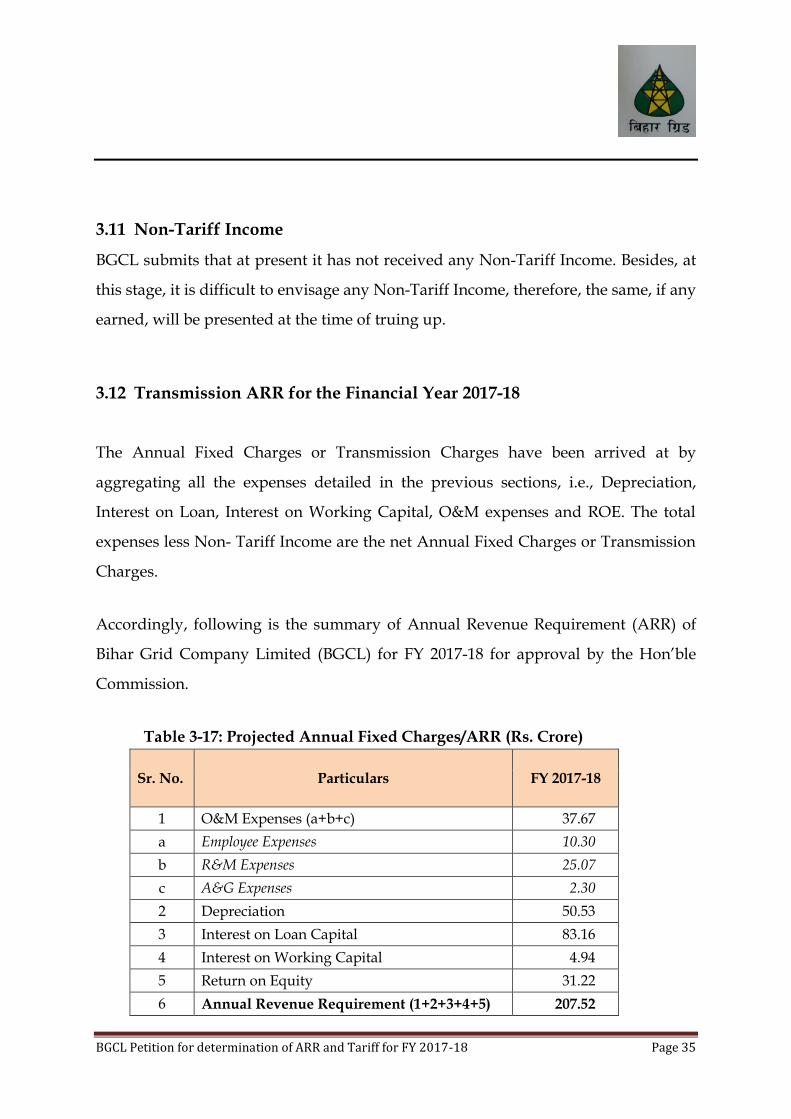

3.11 Non-Tariff Income

BGCL submits that at present it has not received any Non-Tariff Income. Besides, at

this stage, it is difficult to envisage any Non-Tariff Income, therefore, the same, if any

earned, will be presented at the time of truing up.

3.12 Transmission ARR for the Financial Year 2017-18

The Annual Fixed Charges or Transmission Charges have been arrived at by

aggregating all the expenses detailed in the previous sections, i.e., Depreciation,

Interest on Loan, Interest on Working Capital, O&M expenses and ROE. The total

expenses less Non- Tariff Income are the net Annual Fixed Charges or Transmission

Charges.

Accordingly, following is the summary of Annual Revenue Requirement (ARR) of

Bihar Grid Company Limited (BGCL) for FY 2017-18 for approval by the Hon’ble

Commission.

Table 3-17: Projected Annual Fixed Charges/ARR (Rs. Crore)

Sr. No. Particulars FY 2017-18

1 O&M Expenses (a+b+c) 37.67

a Employee Expenses 10.30

b R&M Expenses 25.07

c A&G Expenses 2.30

2 Depreciation 50.53

3 Interest on Loan Capital 83.16

4 Interest on Working Capital 4.94

5 Return on Equity 31.22

6 Annual Revenue Requirement (1+2+3+4+5) 207.52

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 36

The Petitioner would like to submit that the various costs have been estimated in

accordance with the regulatory norms, assumptions and detailed justifications

provided in this Petition. In view of the submitted facts and explanations, the

Petitioner humbly prays to the Hon’ble Commission for approval of the ARR for FY

2017-18 and resultant Transmission Charges to be recovered.

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 37

4 Methodology for Recovery of ARR

The Hon’ble Commission, vide its Order dated April 29, 2013, in Case No. 7 of 2013

had granted Transmission Licence to Bihar Grid Company Limited (BGCL).

The Transmission Licence was issued to BGCL on June 21, 2013 vide Letter No.

BERC/Case No.7/2013-792-01-Tr.L. Clause 8 of the Transmission Licence issued to

BGCL specifies that BGCL shall perform duties as stipulated in Section 40 of Electricity

Act, 2003, which is reproduced below:

“Section 40. (Duties of transmission licensees):

It shall be the duty of a transmission licensee -

(a) to build, maintain and operate an efficient, co-ordinated and economical inter-State

transmission system or intra-State transmission system, as the case may be;

(b) to comply with the directions of the Regional Load Despatch Centre and the State Load

Despatch Centre as the case may be;

(c) to provide non-discriminatory open access to its transmission system for use by-

(i) any licensee or generating company on payment of the transmission charges; or

(ii) any consumer as and when such open access is provided by the State Commission under

sub-section (2) of section 42, on payment of the transmission charges and a surcharge thereon,

as may be specified by the State Commission:

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 38

…

…

Provided also that such surcharge shall not be leviable in case open access is provided to a

person who has established a captive generating plant for carrying the electricity to the

destination of his own use.”

BGCL is a Joint Venture between PGCIL and BSP(H)CL where both Parties hold

shares in 50:50 ratio. Article 19.1 of the Shareholders Agreement signed on December

29, 2012, between PGCIL and BSP(H)CL stipulates that:

“19.1 The proposed company shall make available the entire transmission capacity

created by it to BSP(H)CL/Its subsidiaries and BSP(H)CL/Its subsidiaries would pay

the transmission charges as determined by BERC through appropriate orders.”

Clause 4.10. (Payment and Billing of Transmission Charges) of the ‘Implementation

and Transmission Services Agreement’ signed between BSP(H)CL and BGCL

stipulates that:

“4.10.2 BSP(H)CL shall pay Transmission Charges (“TC”) to BGCL, on monthly basis, from

the Commercial Operation Date until this Agreement is terminated, subject to the provisions

of this Section. Such monthly payment shall be termed as “Monthly TC Payment”.

4.10.3 The Monthly TC amount payable by BSP(H)CL to BGCL shall be calculated in

accordance with the provisions of BERC (Terms and Conditions for determination of Tariff)

Regulations, 2007, Chapter-4 “Intra State Transmission” or as amended from time to time.”

From the above Clauses, the following conclusions can be drawn:

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 39

a) BGCL is a JV between PGCIL and BSP(H)CL;

b) The Hon’ble BERC had granted Transmission Licence to BGCL on June 21,

2013;

c) By virtue of grant of licence, BGCL is the second intra-State Transmission

Licensee in Bihar and its area of operation overlaps with BSPTCL;

d) Being a Transmission Licensee, BGCL has to fulfil its duties as envisaged in

Electricity Act, 2003;

e) BGCL has to file Tariff Petition before the Hon’ble Commission for

determination of ARR and Transmission Charges in accordance with Section

62 of the Electricity Act, 2003, Clause 23 of the Transmission Licence conditions

issued by the Hon’ble Commission and Clause 4.10.3 of the ‘Implementation

and Transmission Services Agreement’ signed between BSP(H)CL and BGCL;

and

f) Pursuant to the Shareholders Agreement between PGCIL and BSP(H)CL,

BGCL shall duly recover the ARR and Transmission Charges determined by

the Hon’ble Commission from BSP(H)CL/Its subsidiaries.

Proposed Methodology

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 40

As BGCL and BSPTCL are two Intra-State Transmission Licensees in Bihar, BGCL is

proposing the revenue recovery methodology in line with the approach followed in

the State of Maharashtra. Maharashtra has seven Transmission Companies namely,

MSETCL, RInfra-T, TPC-T, JPTL, ATIL, MEGPTCL, VIPL-T and APTCL. Regulation

61 of MERC (Multi Year Tariff) Regulations, 2015, specifies that:

“61.1 The aggregate of the yearly revenue requirement for all Transmission Licensees shall

form the “Total Transmission System Cost" (TTSC) of the Intra-State transmission system,

to be recovered from the Transmission System Users (TSUs) for the respective year of the

Control Period, in accordance with the following Formula:

TTSC(t) = ∑𝑛𝑖=0 ARRi

Where,

TTSC(t) = Pooled Total Transmission System Cost of year (t) of the Control Period;

n = Number of Transmission Licensee(s);

ARRi = Yearly revenue requirement approved by the Commission for ith Transmission Licensee

for the yearly period (t) of the Control Period:

Provided that in case of transmission system projects undertaken in accordance with the

Guidelines for competitive bidding for transmission under Section 63 of the Act, the Annual

Revenue Requirement as per the annual Transmission Service Charges (TSC) quoted by such

projects, shall be considered, for aggregation under the TTSC.”

Therefore, based on the Regulation, the Hon’ble MERC pooled the ARR of all

Transmission Licensees and determined combined Transmission Charge of Rs. 483.79

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 41

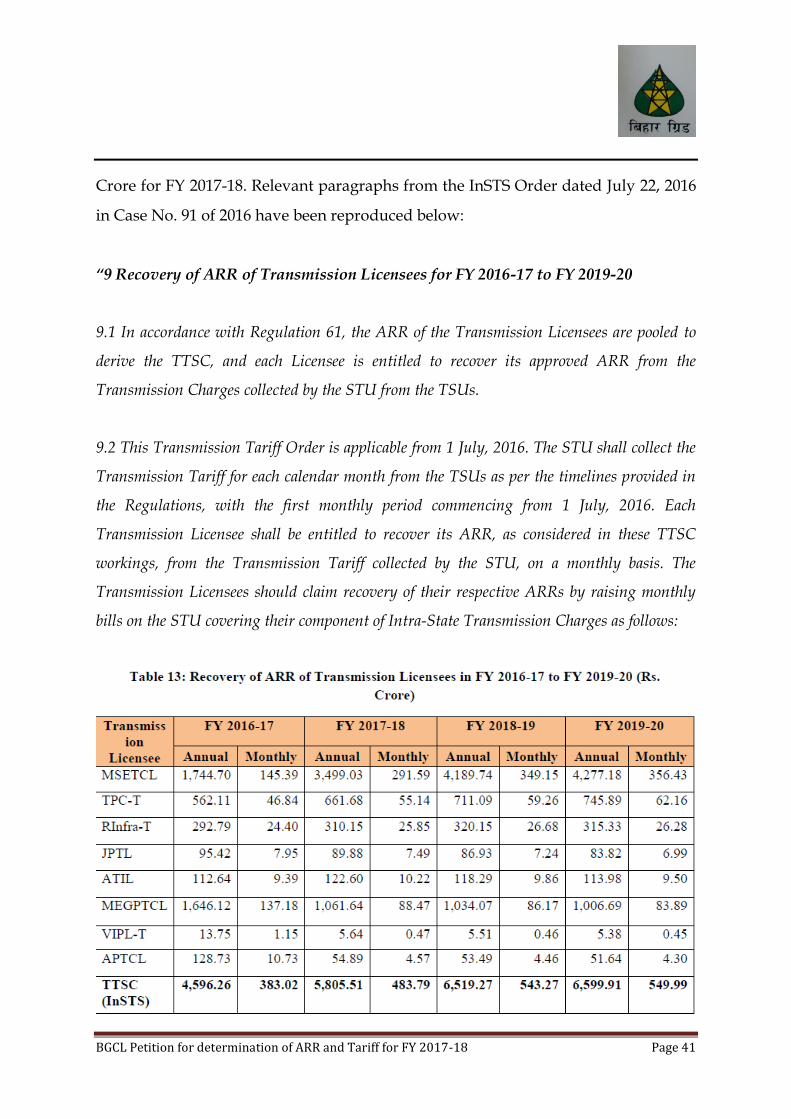

Crore for FY 2017-18. Relevant paragraphs from the InSTS Order dated July 22, 2016

in Case No. 91 of 2016 have been reproduced below:

“9 Recovery of ARR of Transmission Licensees for FY 2016-17 to FY 2019-20

9.1 In accordance with Regulation 61, the ARR of the Transmission Licensees are pooled to

derive the TTSC, and each Licensee is entitled to recover its approved ARR from the

Transmission Charges collected by the STU from the TSUs.

9.2 This Transmission Tariff Order is applicable from 1 July, 2016. The STU shall collect the

Transmission Tariff for each calendar month from the TSUs as per the timelines provided in

the Regulations, with the first monthly period commencing from 1 July, 2016. Each

Transmission Licensee shall be entitled to recover its ARR, as considered in these TTSC

workings, from the Transmission Tariff collected by the STU, on a monthly basis. The

Transmission Licensees should claim recovery of their respective ARRs by raising monthly

bills on the STU covering their component of Intra-State Transmission Charges as follows:

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 42

”

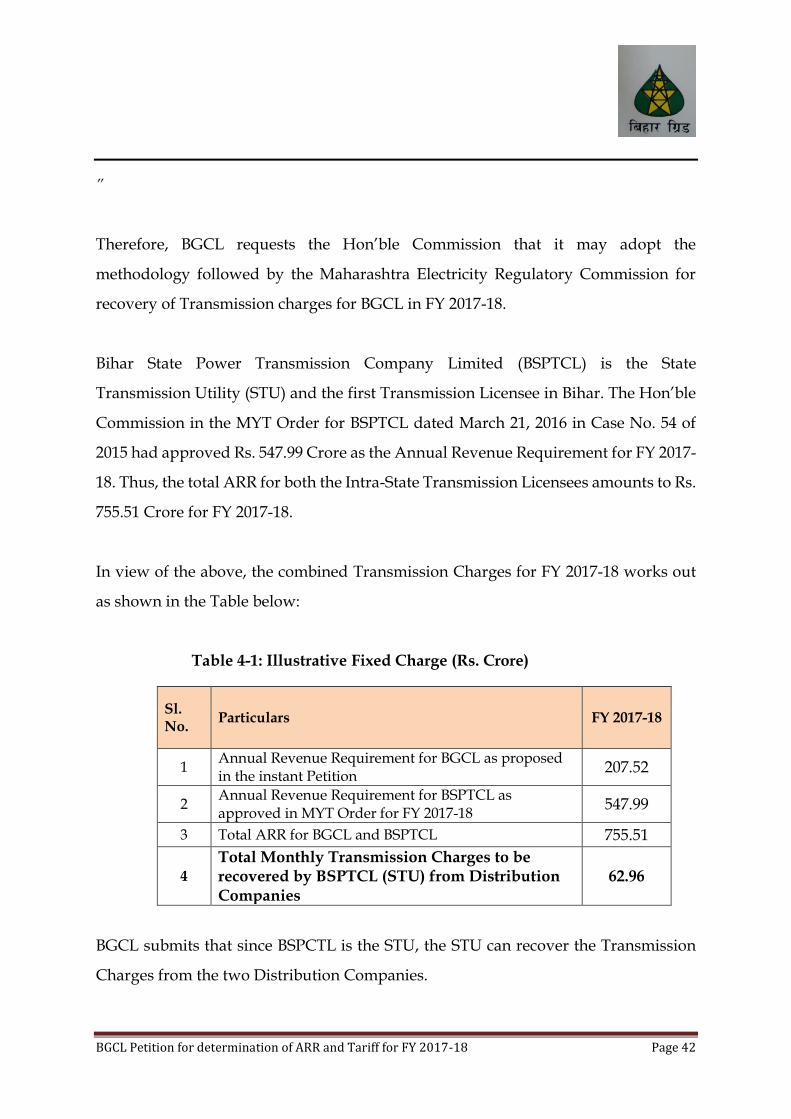

Therefore, BGCL requests the Hon’ble Commission that it may adopt the

methodology followed by the Maharashtra Electricity Regulatory Commission for

recovery of Transmission charges for BGCL in FY 2017-18.

Bihar State Power Transmission Company Limited (BSPTCL) is the State

Transmission Utility (STU) and the first Transmission Licensee in Bihar. The Hon’ble

Commission in the MYT Order for BSPTCL dated March 21, 2016 in Case No. 54 of

2015 had approved Rs. 547.99 Crore as the Annual Revenue Requirement for FY 2017-

18. Thus, the total ARR for both the Intra-State Transmission Licensees amounts to Rs.

755.51 Crore for FY 2017-18.

In view of the above, the combined Transmission Charges for FY 2017-18 works out

as shown in the Table below:

Table 4-1: Illustrative Fixed Charge (Rs. Crore)

Sl. No.

Particulars FY 2017-18

1 Annual Revenue Requirement for BGCL as proposed in the instant Petition

207.52

2 Annual Revenue Requirement for BSPTCL as approved in MYT Order for FY 2017-18

547.99

3 Total ARR for BGCL and BSPTCL 755.51

4 Total Monthly Transmission Charges to be recovered by BSPTCL (STU) from Distribution Companies

62.96

BGCL submits that since BSPCTL is the STU, the STU can recover the Transmission

Charges from the two Distribution Companies.

BGCL Petition for determination of ARR and Tariff for FY 2017-18 Page 43

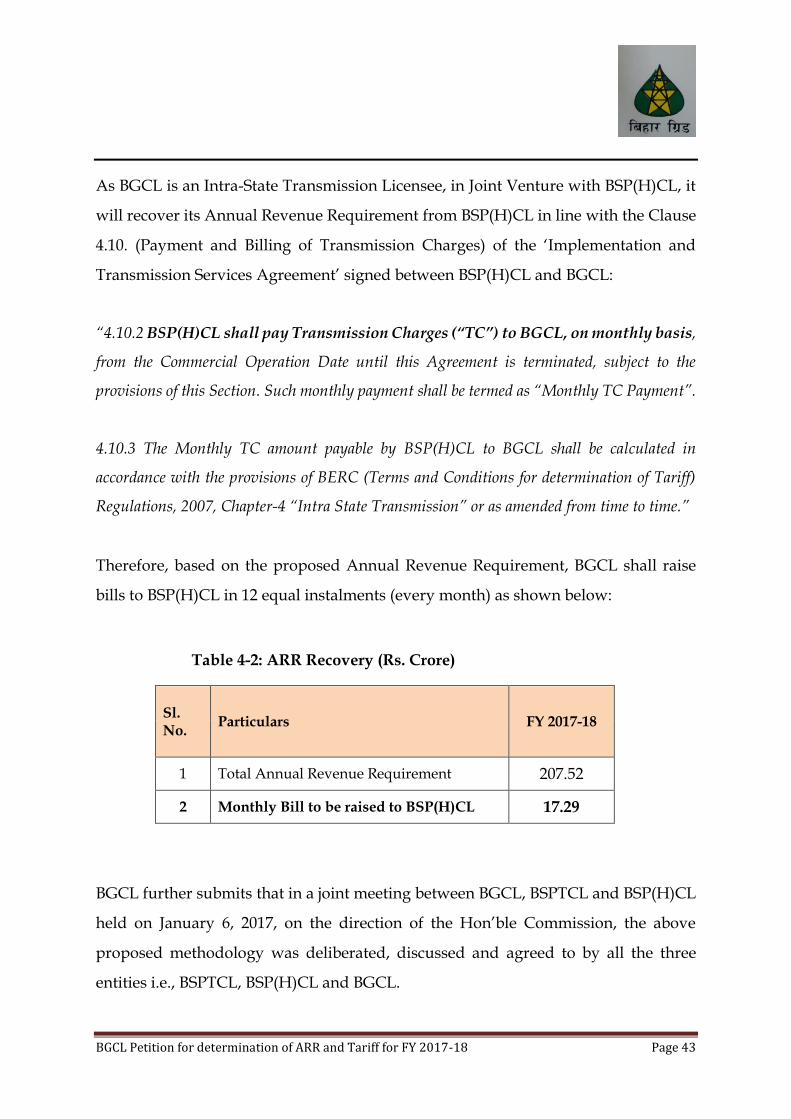

As BGCL is an Intra-State Transmission Licensee, in Joint Venture with BSP(H)CL, it

will recover its Annual Revenue Requirement from BSP(H)CL in line with the Clause

4.10. (Payment and Billing of Transmission Charges) of the ‘Implementation and

Transmission Services Agreement’ signed between BSP(H)CL and BGCL:

“4.10.2 BSP(H)CL shall pay Transmission Charges (“TC”) to BGCL, on monthly basis,

from the Commercial Operation Date until this Agreement is terminated, subject to the

provisions of this Section. Such monthly payment shall be termed as “Monthly TC Payment”.

4.10.3 The Monthly TC amount payable by BSP(H)CL to BGCL shall be calculated in

accordance with the provisions of BERC (Terms and Conditions for determination of Tariff)

Regulations, 2007, Chapter-4 “Intra State Transmission” or as amended from time to time.”

Therefore, based on the proposed Annual Revenue Requirement, BGCL shall raise

bills to BSP(H)CL in 12 equal instalments (every month) as shown below:

Table 4-2: ARR Recovery (Rs. Crore)

Sl. No.

Particulars FY 2017-18

1 Total Annual Revenue Requirement 207.52

2 Monthly Bill to be raised to BSP(H)CL 17.29

BGCL further submits that in a joint meeting between BGCL, BSPTCL and BSP(H)CL

held on January 6, 2017, on the direction of the Hon’ble Commission, the above

proposed methodology was deliberated, discussed and agreed to by all the three

entities i.e., BSPTCL, BSP(H)CL and BGCL.

Related Documents