IFRS - Workshops Application of International Financial Reporting Standards Kontakt Warszawa Aleksandra Trych tel. +48 505 171 636 [email protected] Wrocław, Poznań Renata Michalak tel. +48 508 018 460 [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

IFRS - Workshops

Application ofInternational FinancialReporting Standards

KontaktWarszawaAleksandra Trychtel. +48 505 171 [email protected]

Wrocław, PoznańRenata Michalaktel. +48 508 018 [email protected]

Objectives and advantagesu To apply advanced accounting principles and techniques in a practical context.u To evaluate and apply various international standards.u To analyse, interpret and report on financial statements and related information to different user groups.u To ensure that preparers and users of financial statements are up-to-date with current amendments

and requirements of IFRS.

About Workshopu International Financial Reporting Standards is a programme covering existing International Accounting

Standards (IAS), International Financial Reporting Standards (IFRS) and IFRIC interpretations. Up to andincluding IFRS 15.

u Comprehensive course materials providedu Interactive training based on exercise solving and discussion of real-life scenariosu Progress tests throughout the programme to assess the knowledge of participantsu Diploma awarded upon completion of the programme and passing of the final exam

Each two-day module costs 1700 zł + 23% VAT.

Price – special offer

• Option 1 - 9100 zł + 23% VAT/per person.The course combines lectures, question and answersessions, practical exercises and examples

• Option 2 – 9250 zł + 23% VAT/per person.Addition, participants receive online tests to prepare forthe final exam

• Opcja 3 – 9900 zł +23% VAT/os.Addition, participants receive online tests to prepare forthe final exam, e-mail contact with the tutor and access to10 e-learning courses on the platform: http://e-learningacademyofbusiness.pl/archiwum/kategoria/58/mssf

IFRS - Workshop

PriceStructureThe course is composed of a mixture oflectures, question and answer sessions,practical exercises and illustrations as wellas home study.

The programme is divided into six modules,each consisting of two days of training withabout three weeks’ break between thecourse days. During the time betweencourses participants are expected to studyat home in their own time and solve tests.Tests are marked by the EY Academy ofBusiness team and sent back to participantstogether with the solutions.

An e-mail hot line is available to facilitatecontact with the tutor if any problems orquestions regarding homework assignmentsshould arise.

It is possible to participate in selectedmodules only.

Materials

Participants receive comprehensive course notes in Polish, which include a theoreticalcomponent summarizing the key elements of IFRS as well as practical tests and solutions.

It is also possible (only for course participants) to purchase the training materials in Englishat additional cost.

u 200 zł + 23% VAT - the cost of materials to the whole programme

Examination

The programme finishes with a two and a half hour written examination. After passing theexam with a positive result (at least 50% of the total marks), those students who haveattended the whole course receive an EY Academy of Business diploma.

The examination will cover only the topics discussed at the course.

"In my several-yearcareer, it was the bestorganized andconducted training.„

Danuta GorzkowskaKierownik Biura ControllinguAmica Wronki S.A.

Who is it for?Accountants, chief accountants, controllers and finance managerswho would like to understand, interpret and apply IFRS. The courseassumes knowledge of basic accounting procedures and double entrybookkeeping. No prior knowledge of accounting standards is required.

IFRS - Workshop

PROGRAMME

PROGRAMME – module I

Day 1 (A)

Introduction to International Financial ReportingStandards (IFRS)u Basic historical background to financial reporting and

accounting internationally.

u Structure of the International Accounting Standards Boardincluding current developments and discussion of the workof the International Financial Reporting InterpretationsCommittee.

u Role of International Financial Reporting Standards inEuropean Union countries and the United States.

u The Standard Setting process.

u IFRS Conceptual Framework with emphasis on basicaccounting concepts and the definitions of assets,liabilities, revenue, costs and equity.

Presentation of Financial Statementsu The current format of financial statements.

u The operating cycle relevant to specific business activitiesand the classification of assets and liabilities intocurrent/non current.

u Minimum requirements regarding the presentation of itemsin the income statement/statement of comprehensiveincome and statement of financial position/balance sheet;presentation of illustrative formats.

u Statement of changes in equity.

u Interim reporting.

Inventoriesu Measurement at recognition: purchase price, cost of

conversion, other costs included in the valuation ofinventory.

u Net realizable value – definition and practical examples ofvaluation.

Statement of Cash Flowsu The need for a statement of cash flows and how it is

prepared from information contained in the incomestatement/statement of comprehensive income, balancesheet/statement of financial position and notes to thefinancial statements.

u Definition of cash and cash equivalents; examples of itemsclassified as both of the above.

u The indirect and direct methods of constructing the cashflow statement.

Day 2 (B)

Property, Plant and Equipmentu Measurement at recognition: costs to be capitalized at

initial recognition (purchase price, production cost, costs ofremoving the asset at the end of its useful economic life).

u Definition of depreciable amount; various depreciationmethods: straight-line, diminishing balance, sum of digits,units of production.

u Component accounting.

u Measurement after recognition: cost model and revaluationmodel.

u Accounting for revaluations and disposals of non currentassets.

u Changes in depreciation methods and revisions of usefullife.

u Presentation and disclosure of non current assets.

Borrowing Costs (loans, credits)u Definition of borrowing costs

u Accounting treatment of borrowing costs under the revisedIAS 23

u Key issues related to capitalization: qualifying assets,capitalization period and capitalization rate.

Government Grants and Disclosure of GovernmentAssistanceu Grants related to income and grants related to assets.

u Discussion of the two methods of accounting forgovernment grants recommended under IAS 20.

Investment Propertiesu Definition and measurement at recognition of investment

properties.u Criteria for classification as investment property;

reclassification rules.

u Valuation methods: cost model and fair value model;conditions for applying the fair value model, accounting forchanges in fair value.

Events after the Reporting Dateu Defining the period during which events after the reporting

date arise.

u Adjusting and non-adjusting events – practical examplesand accounting treatment.

Accounting Policies, Changes in Accounting Estimatesand Errorsu Hierarchy of sources for choosing accounting policies.

u Definition of past period errors and the accountingtreatment applied to correction of errors.

u Accounting estimates and their changes.

IFRS - Workshop

Day 1 (A)

IFRS 15 Revenue from Contracts with Customersu Scope of IFRS 15u Identifying the contract and modificationsu Identifying performance obligations: distinct goods or

services, promises in contracts with customers,principal vs. agent.

u Determining the transaction price: Variableconsideration, significant financing component,consideration payable to a customer.

u Allocating the transaction price to performanceobligations

u Satisfaction of performance obligations: over time orat a point in time

u Incremental costs of obtaining a contractu Effective date and transitionu Disclosures

Provisions, Contingent Liabilities and ContingentAssetsu Definitions of provisions, contingent liabilities and

contingent assetsu Obligating events: legal and constructive obligations

u Provisions for future operating losses and onerouscontracts.

u Measurement rules: defining the expenditure required tosettle the obligation, discounting and unwinding of thediscount.

u Conditions for recognizing provisions for restructuringexpenses.

u Discussion of criteria for recognition in the statement offinancial position or in the notes to the financialstatements.

Day 2 (B)

Introduction to Group Accountingu Methods of accounting for investments in individual

company accounts and their impact on consolidatedfinancial statements.

u When to use the various methods of consolidation.u Definitions of a subsidiary, associate, joint venture, control,

joint-control, significant influence and other definitionsrelating to group accounting.

Consolidated Statement of Financial Position andStatement of Comprehensive Incomeu Step by step guide to the preparation of the consolidated

statement of financial position based on discussion ofexamples.

u Goodwill and gain on bargain purchase.u Impairment of goodwill

u Revaluation of the assets and liabilities of a subsidiary tofair value.

u Non-controlling interests in the statement of financialposition.

u Consolidation adjustments eliminating:

§ equity and investments,

§ intra-group balances (trade, loans),§ unrealized profit on intra-group transactions arising

from the transfer of inventory and non-current assets(including the impact on depreciation),

§ Dividends.

u Step by step guide to the preparation of the consolidatedstatement of comprehensive income based on discussion ofexamples.

u Eliminating intra-group transactions from the perspectiveof the statement of comprehensive income (sales, cost ofsales, dividends).

u The impact of transactions on non-controlling interests.

Related Party Transactionsu Definition of related parties and the need to disclose

transactions and balances with related parties.

u Types of transactions requiring disclosure; discussion ofrequired level of detail of disclosures.

Program – moduł II

IFRS - Workshop

PROGRAMME – module II

Day 1 (A)

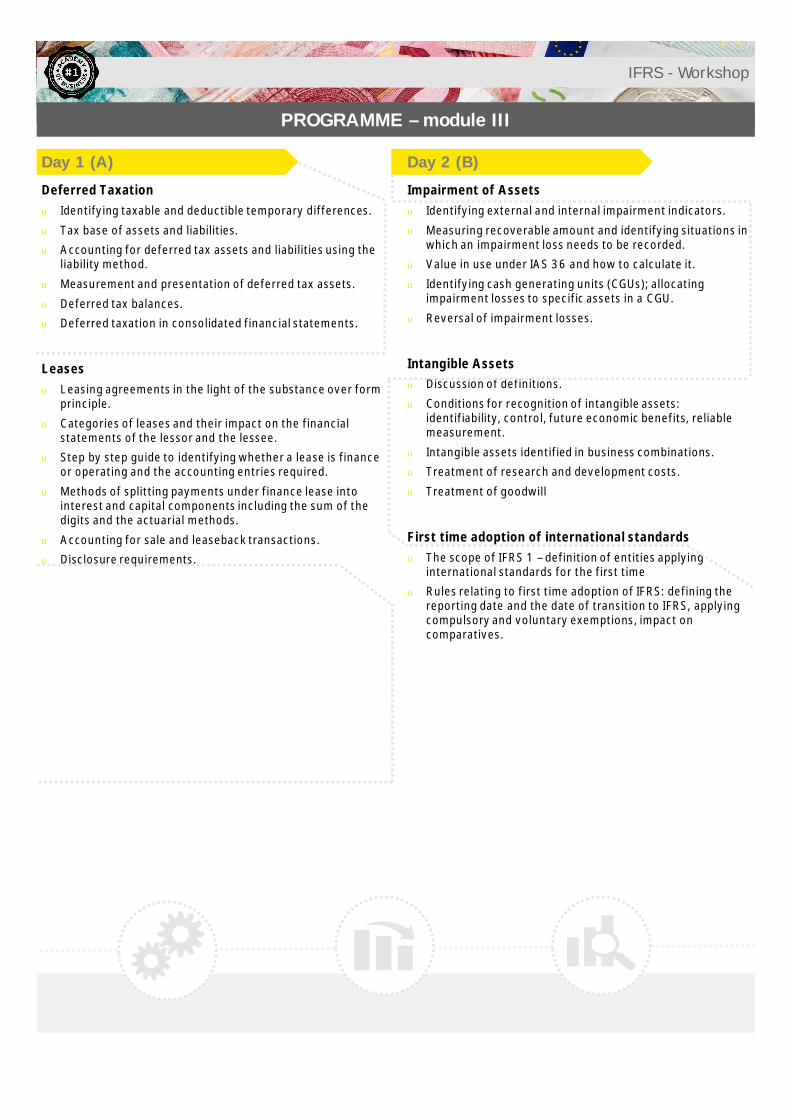

Deferred Taxationu Identifying taxable and deductible temporary differences.

u Tax base of assets and liabilities.u Accounting for deferred tax assets and liabilities using the

liability method.

u Measurement and presentation of deferred tax assets.

u Deferred tax balances.u Deferred taxation in consolidated financial statements.

Leasesu Leasing agreements in the light of the substance over form

principle.

u Categories of leases and their impact on the financialstatements of the lessor and the lessee.

u Step by step guide to identifying whether a lease is financeor operating and the accounting entries required.

u Methods of splitting payments under finance lease intointerest and capital components including the sum of thedigits and the actuarial methods.

u Accounting for sale and leaseback transactions.u Disclosure requirements.

Day 2 (B)

Impairment of Assetsu Identifying external and internal impairment indicators.

u Measuring recoverable amount and identifying situations inwhich an impairment loss needs to be recorded.

u Value in use under IAS 36 and how to calculate it.

u Identifying cash generating units (CGUs); allocatingimpairment losses to specific assets in a CGU.

u Reversal of impairment losses.

Intangible Assetsu Discussion of definitions.

u Conditions for recognition of intangible assets:identifiability, control, future economic benefits, reliablemeasurement.

u Intangible assets identified in business combinations.u Treatment of research and development costs.

u Treatment of goodwill

First time adoption of international standardsu The scope of IFRS 1 – definition of entities applying

international standards for the first timeu Rules relating to first time adoption of IFRS: defining the

reporting date and the date of transition to IFRS, applyingcompulsory and voluntary exemptions, impact oncomparatives.

Program – moduł III

IFRS - Workshop

PROGRAMME – module III

Day 1 (A)

Earnings per Shareu Methods of calculating basic and diluted earnings per

share.

u Impact of issue of shares at full market price, share splits,bonus issues and rights issues on the weighted averagenumber of shares and comparatives.

u Treatment of potential ordinary shares: options,convertible preference shares, convertible loans andconvertible debentures.

u Determining the order in which potential dilutive factorsare included in the calculation of the weighted averagenumber of shares.

u Earnings per share for continuing operations.

Segment Reportingu The necessity for segment reporting.

u Definition of operating segment and Chief OperatingDecision Maker.

u Discussion on the criteria for presentation of separatesegments.

u Inter-segment transactions.

u Discussion on the changes required by IFRS 8: Operatingsegments.

Non-current Assets Held for Sale and DiscontinuedOperationsu Non-current assets held for sale – classification criteria.u Measurement of non-current assets held for sale at the

date of classification.

u Accounting for disposal groups.

u Discussion of when discontinued operations arise and thedisclosure requirements in IFRS 5.

u Accounting for discontinued operations in comparatives.

Day 2 (B)The Equity Methodu Accounting for associates in the standalone and

consolidated financial statements.u Discussion, based on an example, of the treatment of an

investment in the statement of financial position andstatement of comprehensive income under the equitymethod.

u Elimination of unrealized profits from transactions betweeninvestor and associate.

u Goodwill and gain on bargain purchase.

IFRS 11 Joint Arrangementsu Factors that influence the classification of joint

arrangements: legal form, contractual arrangements andother.

u Accounting for joint operations and joint ventures

u Numerical examples illustrating the principles

Business combinationsu Discussion of how the revised FRS 3 has changed

consolidation/group accounting.u Discussion of basic issues described in IFRS 10: new

definition of control, potential voting rights, de factocontrol, identification of relevant activities, protectiverights, continuous assessment.

u Deferred and contingent consideration.

u Re-measurement of assets, liabilities and contingentliabilities at fair value. Impact of remeasurement on thedate of acquisition in the consolidated statement offinancial position – fair value adjustments in subsequentyears.

IFRS 12 Disclosure of Interests in Other Entitiesu The purpose and scope of disclosures

u Disclosures required for significant interests in subsidiaries,joint arrangements and associates

u Other disclosures

Changes in Foreign Exchange Rates and Consolidationof Foreign Subsidiariesu Functional and presentation currencies.

u Criteria considered in selecting the functional currency.

u Accounting for foreign currency transactions on initialrecognition, settlement and balance sheet dates.

u Recognition of exchange differences.

u Translating the results and financial position of foreignsubsidiaries included in the consolidated accounts.

u Rules for applying foreign exchange rates to assets,liabilities, equity, income and costs.

u Recognition of exchange differences in consolidatedfinancial statements: share of group and non-controllinginterests.

u Elimination of balances and transactions with a foreignentity.

u Translation of goodwill.

Financial Reporting in Hyperinflationary Economiesu Criteria considered in assessing whether hyperinflation

exists.

u Financial statement items subject to adjustments due tohyperinflation.

Program – moduł IV

IFRS - Workshop

PROGRAMME – module IV

Day 1 (A)

Financial Instrumentsu How the standards on financial instruments have evolved:

IAS 32, IAS 39, IFRS 7 and IFRS 9

u Scope of standardsu Definitions of financial assets, liabilities and equity

u Classification of financial instruments under IFRS 9:financial assets at fair value through profit and loss, othercomprehensive income and amortised cost

u Fair value measurementu Amortised cost method using the effective interest rate

u Impairment of financial assets: expected losses modelunder IFRS 9

u Impairment of financial assets at amortised costu Impairment of financial assets at fair value

u Introduction to accounting for derivatives: presentation ofthe principles of forward, futures, options, swaptransactions

u Embedded derivativesu Hedge accounting

u Disclosures

Day 2 (B)

Group Statements of Cash Flowsu Dealing with the various issues that arise on preparation of

group statements of cash flows such as investments inassociates, dividends paid to non-controlling interests andthe acquisition and disposal of subsidiaries during theperiod.

u Preparing the consolidated statement of cash lows usingthe indirect method on the basis of information from theconsolidated statement of financial position, statement ofcomprehensive income and notes to the financialstatements.

More complex consolidation techniquesu The impact of piecemeal acquisitions on goodwill

calculation.

u Accounting for disposals of all or part of a subsidiary:calculating the consolidated profit on disposal; accountingfor disposals resulting in a reduction of the shareholding,where a controlling interest remains, an associate orinvestment remains.

u Consolidation of groups, in which control is exercisedindirectly – vertical and mixed groups.

u Piecemeal acquisition under IFRS 10.

u The issues with acquiring and losing control.

u Group reorganisations including discussion on transactionsbetween entities under common control

Program – moduł V

IFRS - Workshop

PROGRAMME – module V

Day 1 (A)

Employee benefitsu Jubilee and retirement bonuses.

u Holiday pay accruals.u The operation of pension schemes.

u Defined benefit and defined contribution pension schemes.

u Disclosure requirements for employee benefits.

IFRS 13 Fair value measurementu Definition of fair value and related terms.

u Principal market and the most advantageous market.

u Transaction costs.u Highest and best use.

u Valuation techniques.

Share Based Paymentu Equity-settled and cash-settled share based paymentsu Definition of the grant date, vesting period and vesting

date.

u Accounting for market and non-market vesting conditions.

u Impact of modification, cancellation and cancellation withcompensation on accounting for equity-settledarrangements.

u Accounting for equity-settled transactions in situations,when the entity or counterparty have the choice ofwhether to settle in equity or cash.

Day 2 (B)

Revision of the most important issues in order toprepare for the final examination.

Program – moduł VI

Information

If you would like to receive moredetailed information, please call+48 22 579 8000 or e-mail us at:[email protected]

Information about the full range of ourcourses is available on our website at:www.academyofbusiness.pl

It is possible to organize in-companytraining at a customer’s individualrequest.

How to apply?

If you are interested in the IFRStraining programme pleasecomplete application by ourwebsite at least one week beforethe start of the course.

IFRS - Workshop

PROGRAMME – module VI

Jarek is graduate of the Poznań University of Economics. He is aMember of The Association of Chartered Certified Accountants(UK) since 1999. Since 2002 he is eligible to practise asChartered Certified Accountant in UK and as Biegły Rewident inPoland. He is also CFA Charter Holder and CIA title holder.In 1996 Jarek joined EY. He has got several years of trainingexperience.He specialises in International Financial Reporting Standards. Heis responsible for development and delivery of financial, in-house courses tailored to specific needs of diversified portfolioof clients. Jarek is Technical Director of postgraduate studiesconducted in cooperation with Warsaw School of EconomicsIn 2015-2017 a member of the PIBR Examination Commission.

Jarosław Olszewski FCCA, CFA, CIASenior Manager

Michał Błeszyński FCCA, CIAManager

Michał is a graduate of the Wrocław University ofTechnology, Faculty of Computer Science andManagement. He is a CIA (Certified Internal Auditor), ACCA(Association of Chartered Certified Accountants) member,and Polish Certified Auditor (biegły rewident). For over 5years he has been working in the Audit department inErnst & Young, he was responsible for auditing productioncompanies and capital groups operating in the real estatearea. He did educate new members of the Ernst& Youngteam on the external audit. Since 2008 he has beenworking as a trainer in Ernst & Young Academy ofBusiness, where he specializes in teaching courses on IFRS(International Financial Reporting Standards), finance fornon-finance managers, managerial accounting andpreparatory courses for CIA and ACCA exams.

Magdalena Burzyńska ACCASenior

Magdalena graduated in 1999 from the Warsaw School ofEconomics receiving the high score. Her first major wasFinances and Banking and the second one wasInternational Economic and Political Relations. Magdalenais a member of Association of Chartered CertifiedAccountants (ACCA) since 2003.Before joining Ernst & Young Academy of BusinessMagdalena used to work as a financial controller ininternational companies in FMCG sector, engineering andconstruction industry. She holds a vivid experience infinancial management in international companies,preparation of financial statements in accordance withInternational Financial Reporting Standards (IFRS),budgeting, cost control, management accounting andinternal reporting which was gained during 6 years whileworking in financial departments of many companies.

IFRS - Workshop

Trainers profiles

Related Documents