IFRS 9 – Implementation Insights Challenges and Impact Analysis

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

IFRS 9 – Implementation InsightsChallenges and Impact Analysis

1. Preface

Implementing IFRS 9 by January 2018 is one of the most critical challenges financial institutions currently face. IFRS 9 requires Finance and Risk functions to improve their collaboration. Many financial institutions have almost finalized their analysis and design phase and have

started the implementation of their IFRS 9 solution. While our first Point of View IFRS 9 – Financial Instruments ‘Road to a successful implementation of the new requirements’ mainly emphasized the new regulations and project approach as well as implementation aspects, this paper

highlights the challenges and discussion items Capgemini Consulting faces in their IFRS 9 projects. A high-level impact analysis on KPIs, data and processes is also described.

IFRS 9 – Implementation Insights2

3

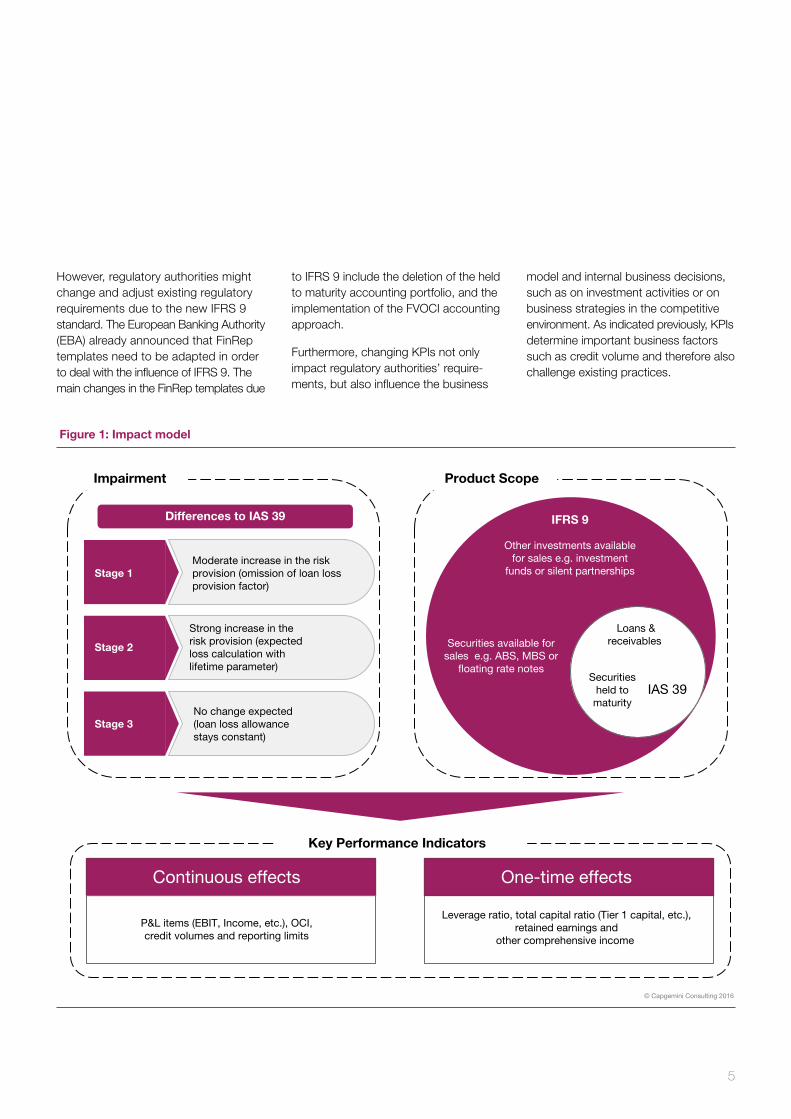

An important area that banks and financial institutions need to consider are impacts on the key performance indicators (KPIs) due to the new IFRS 9 impairment model. The KPIs with interrelations to other report- ing requirements such as Basel III and Financial Reporting (FinRep), are of special interest.

In general, it is important to differentiate between two main novelties of IFRS 9, which will impact the KPIs. First, the scope of the financial assets where credit losses must be reported is broader than under IAS 39 (e.g. assets classified as FVOCI). A risk provision needs to be recognized for those assets. This leads to significant effects on the Profit and Loss (PnL) as well as retained earnings in the first period.

Additionally, the new expected credit loss (ECL) models under which expected losses have to be recognized and credit losses are recorded, are required at an earlier point in time. This means a 12-month expected credit loss has to be determined and posted into the accounts directly after initial recognition of the finan-

cial instrument. IFRS 9 also requires the consideration of forward-looking informa- tion, e.g. macroeconomic factors, leading to an expected increase of risk provision.

Depending on the business model (hold or hold & sell), financial assets are either measured by the amortized cost (AC) method or the fair value other compre- hensive income (FVOCI) approach. An expected credit loss has to be calculated for both classification and measurement types. A higher volatility and an increase in credit loss provision is expected follow- ing early adoption. Finally, the FVOCI measurement requires the recognition of unrealized fair value gains and losses within the other comprehensive income (OCI) that will directly impact the banks’ equity position.

Since Tier 1 capital is a basis for many KPIs and regulatory requirements, any change in retained earnings and OCI is visible. For example, Basel III demands that banks maintain a minimum total capital ratio of 8% and a minimum lever- age ratio of 3% - both ratios are based

on the Tier 1 capital. Another factor that influences these ratios is the increase in credit risk which impacts the risk weighted assets (RWA). When the Tier 1 capital decreases and RWA increase, these ratios will decrease; however, the level of impact is difficult to determine and is challenging in planning scenarios. Simulation models, test cases or a parallel run can help to identify estimate implementation effects. An overview of the impacts related to the introduction of IFRS 9 is illustrated in Figure 1.

Moreover, financial institutions under IFRS 9 are obliged to report loans which are higher than 10% of their equity. In addi- tion, the credit volume allowed is also determined by the equity.1 If the equity declines, banks will have to report more loans and then face the need for sophisti- cated forecasts due to the uncertainty of the impacts on financial ratios, representing a significant challenge for financial institutions.

2. Key Performance Indicators & Regulatory Requirements

1 According to the “Groß- und Millionenkreditverordnung” (GroMiKV) credit value is limited to 25% of the equity.

IFRS 9 – Implementation Insights4

However, regulatory authorities might change and adjust existing regulatory requirements due to the new IFRS 9 standard. The European Banking Authority (EBA) already announced that FinRep templates need to be adapted in order to deal with the influence of IFRS 9. The main changes in the FinRep templates due

to IFRS 9 include the deletion of the held to maturity accounting portfolio, and the implementation of the FVOCI accounting approach.

Furthermore, changing KPIs not only impact regulatory authorities’ require- ments, but also influence the business

model and internal business decisions, such as on investment activities or on business strategies in the competitive environment. As indicated previously, KPIs determine important business factors such as credit volume and therefore also challenge existing practices.

Figure 1: Impact model

© Capgemini Consulting 2016

Impairment

Leverage ratio, total capital ratio (Tier 1 capital, etc.),retained earnings and

other comprehensive income

Key Performance Indicators

Continuous effects

P&L items (EBIT, Income, etc.), OCI,credit volumes and reporting limits

One-time effects

Product Scope

IAS 39

IFRS 9

Stage 1 Moderate increase in the risk provision (omission of loan lossprovision factor)

Stage 2

Stage 3

Loans &receivables

Securitiesheld tomaturity

Securities available forsales e.g. ABS, MBS or

�oating rate notes

Other investments availablefor sales e.g. investment

funds or silent partnerships

Differences to IAS 39

Strong increase in therisk provision (expectedloss calculation withlifetime parameter)

No change expected(loan loss allowancestays constant)

5

IFRS 9 – Implementation Insights6

3. Data Model & IT Infrastructure

The implementation of IFRS 9 poses signifi- cant challenges to banks and financial institutions from data models and IT infra- structure perspectives as well. In particular, the new expected credit loss approach requires both new data attributes and large amounts of data that have not historically been sourced for accounting and risk purposes, e.g. date of inception. Identifying and integrating those attributes in the respective systems represents a considerable challenge for financial institu- tions, because the expansion and intro- duction of source systems are associated with high costs.

Besides data availability and quality, various systems have to be adjusted and expanded to include new data feeds and data attributes ensuring an IFRS 9 compli- ant expected credit loss calculation.

A large amount of transaction data needs to be traced and archived for the appro- priate usage of ECL models for financial instruments. In contrast to IAS 39, IFRS 9 requires additional information for the new impairment approach, e.g. significant deterioration triggers or lifetime probability of default, which are currently not captured and maintained as requested in existing systems. As a consequence, a high level of default values and approximations have to be integrated for existing financial contracts. In addition, the data granularity under IFRS 9 for the ECL models repre- sents a new challenge for financial institu- tions, because a significant amount of data at the individual asset level has to be collected and processed. The global scope of data collection from various source systems also adds additional complexity.

Nevertheless, the high data requirements for IFRS 9 encourage the harmonization of finance and risk data, which also has to comply with BCBS 239. Simultaneously, the available IT systems must be capable of handling extensive granular data requirements for providing accurate and complete ECL calculations in order to meet accounting and disclosure requirements. Comprehensive data management must be established to ensure all required data is available. Data governance structures and controls must also be in place because the required data is often sourced from various IT systems and may have quality issues.

7

4. Processes & Control Framework

In addition to the data and system chal- lenges during implementation, IFRS 9 also impacts several processes, recon- ciliations and controls. Ensuring compli- ance with IFRS 9, financial institutions must also implement robust processes including a flexible control framework in order to fulfill the new disclosure requirements. For this purpose, the existing credit risk models (e.g. incurred loss model) have to be adjusted and a new end-to-end process has to be designed.

The current business state for many banks and financial institutions is that the impair- ment processes differ by business unit and/ or location. This means various processes, e.g. risk assessment, postings and local solutions have to be revised or changed.

To ease compliance with IFRS 9 regula- tions throughout all units, a centralized and fully integrated end-to-end impairment calculation and automated posting process would reduce the implementation effort involved. Otherwise every decentralized system components must be changed accordingly.

The idea of a centralized impairment pro- cess can be realized through the utilization of a strategic and centralized financial data warehouse. Centralized process implies a unified approach for impairment, which ensures a golden source of information for all impairment related queries by manage- ment and external authorities, and reduces reconciliation effort in the long run.

The central solution approach for IFRS 9 should consider all main process aspects such as ECL calculation, posting entries, disclosure/ reporting preparation and quality assurance for IFRS 9 figures. This enables the process to run in a stable and flexible environment. Major end-to-end process steps including governance aspects are highlighted in Figure 2.

When implementing a central IFRS 9 solution, it is crucial to create prerequi- sites for the decommissioning of local solutions or processes ensuring the targeted efficiency gains or unified approach for impairment.

A central IFRS 9 impairment approach poses new challenges to strict timing requirements for process operations in

financial reporting due to fixed publishing dates as well as integration into existing month-end closing procedure. Further- more, several reconciliation processes (e.g. IAS 39 vs. IFRS 9 comparisons or ECL result validations) could lead to significant adjustments depending on the materiality thresholds.

Additionally, the definition of governance aspects such as control framework, roles and responsibilities as well as organizational design must be able to identify potential amendments during the process design phase.

The consideration of dependencies on processes, such as credit risk manage- ment or RWA calculation, is crucial for IFRS 9 implementation to ensure consis- tent calculations, data flows and external reports.

A centralized IFRS 9 process ensures integrated risk and regulatory reporting, less implementation effort and greater efficiency.

Figure 2: Process and governance implication analysis

© Capgemini Consulting 2016

Classi�cationand

measurement

Inboundinterfaces

Stagedetermination

ECLdetermination

PnLdetermination

/ Posting

Input IFRS 9

Reporting andoutbound

Input Process Output

Data qualitymanagement

Controlframework

Exceptionmanagement

Accountingpolicy Annual review

Roles andresponsibilities

De�netimelines

Manage IFRS 9 End-to-End Process

High-Level IFRS 9 Impairment End-to-End Process and Affected Areas

IFRS 9 – Implementation Insights8

5. Conclusion & Outlook

Our experiences with running projects show financial institutions are faced with increasing implementation effort due to immense accounting requirements.

In this context implementing IFRS 9 requirements is complex due to:

• Intensive discussions among a huge number of stakeholders,

• Poor data availability and quality challenges

• Less flexible IT landscape and processes in Finance and Risk, e.g. modifications, forward-looking information, significant deterioration

To overcome these challenges developing a clear target picture for business and IT in order to guide implementation of a robust and efficient end-to-end process with regards to impairment is essential.

If you are faced with similar challenges, we offer consultation in all the areas mentioned and can share insights and propose carrying out a quick scan to assess your implementation status.

9

6. Authors

Joachim von Puttkamer

Vice President – Corporate Excellence &

Transformation

Daniel Biechele

Manager – Corporate Excellence &

Transformation

Dr. Ulrich Windheuser

Principal – Corporate Excellence &

Transformation

Ernest Roth

Consultant – Corporate Excellence &

Transformation

Patricia Sagert

Manager – Corporate Excellence &

Transformation

IFRS 9 – Implementation Insights10

7. Contacts

GlobalJean [email protected]

NorwayJon [email protected]

FranceStanislas de [email protected]

Germany/Austria/SwitzerlandChristian [email protected]

United StatesYves [email protected]

Belgium/LuxembourgRobert van der [email protected]

SpainDavid J [email protected]

United KingdomKevin [email protected]

AsiaFrederic [email protected]

NetherlandsFreek [email protected]

Sweden/FinlandJohan [email protected]

11

The information contained in this document is proprietary. ©2016 Capgemini.All rights reserved. Rightshore® is a trademark belonging to Capgemini.

About Capgemini Consulting Capgemini Consulting is the global strategy and transformation consulting organization of the Capgemini Group, specializing in advising and supporting enterprises in significant transformation, from innovative strategy to execution and with an unstinting focus on results. With the new digital economy creating significant disruptions and opportunities, the global team of over 3,000 talented individuals work with leading companies and governments to master Digital Transformation, drawing on their understanding of the digital economy and leadership in business transformation and organizational change.

Learn more about us at

www.de.capgemini-consulting.com

About CapgeminiWith more than 180,000 people in over 40 countries, Capgemini is a global leader in consulting, technology and outsourcing services. The Group reported 2015 global revenues of EUR 11.9 billion. Together with its clients, Capgemini creates and delivers business, technology and digital solutions that fit their needs, enabling them to achieve innovation and competitiveness. A deeply multicultural organization, Capgemini has developed its own way of working, the Collaborative Business ExperienceTM, and draws on Rightshore®, its worldwide delivery model.

Learn more about us at

www.de.capgemini.com

Rightshore® is a trademark belonging to Capgemini

Related Documents