IDC Results 2004/05 Geoffrey Qhena Chief Executive Officer 26 October 2005

IDC Results 2004/05 Geoffrey Qhena Chief Executive Officer 26 October 2005.

Jan 01, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

IDC Results 2004/05

Geoffrey QhenaChief Executive Officer

26 October 2005

Mission

“To be the primary driving force of commercially sustainable industrial

development and innovation to the benefit of South Africa and the rest of

the African continent”

• Contribute to the generation of balanced, sustainable economic growth in South Africa and Africa

• Economically empower the South African population

• Promote entrepreneurship through the building of competitive industries and enterprises based on sound business principles

2004/05 Highlights• For the 9-month period up to

31 March 2005:— Anticipated creation of more than 16 700

jobs;— Further investments of R3,8 billion

approved;— 70% of the number and 83% of the value

of financing approvals towards black economic empowerment, up from 53% and 35% respectively in 2004;

— More than 100 approvals for finance to small and medium enterprises;

— Numerous awards for the IDC-funded films; and

— Top Development Financier at the 2005 BusinessMap Business Report Black Economic Empowerment awards.

Transition from“Strategy for Growth” to “Leadership in Development”

IDC’s Investment Activity

Net Value and Number of Approvals

0

1

2

3

4

5

6

7

8

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05*

Val

ue

(R'b

n)

0

100

200

300

400

500

600

700

800

Nu

mb

er

Value of approvals (R'bn)

Number of approvals

Mozal I

Mozal II

• Approvals of more than R46 billion over the 10 year period, involving more than 3 300 deals;

* 9 month period

Shaded areas indicate annualised figures

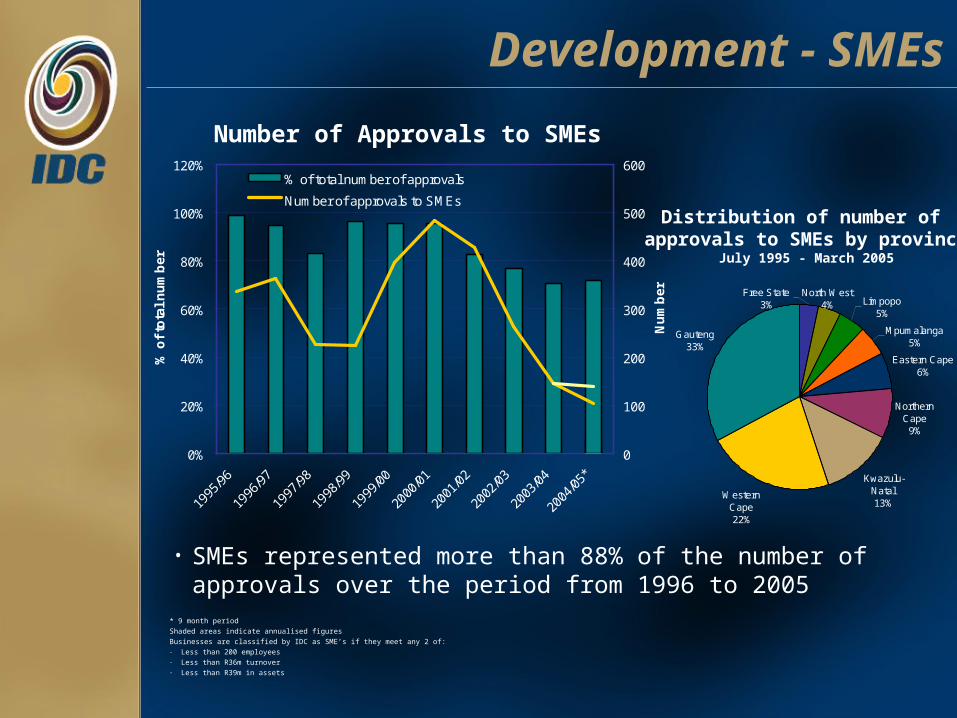

Development - SMEs

0%

20%

40%

60%

80%

100%

120%

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05*

% o

f to

tal

nu

mb

er

0

100

200

300

400

500

600

Nu

mb

er

% of total number of approvals

Number of approvals to SMEs

Number of Approvals to SMEs

• SMEs represented more than 88% of the number of approvals over the period from 1996 to 2005

* 9 month period

Shaded areas indicate annualised figures

Businesses are classified by IDC as SME’s if they meet any 2 of:- Less than 200 employees- Less than R36m turnover- Less than R39m in assets

Limpopo 5%

Mpumalanga 5%

Eastern Cape 6%

Northern Cape

9%

Kwazulu-Natal 13%

Western Cape 22%

Gauteng 33%

North West 4%

Free State 3%

Distribution of number of approvals to SMEs by province

July 1995 - March 2005

Development - SMEs

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Electricity, gas & water supply

Construction

Hotels & restaurants etc

Transport, storage & communication

Healthcare, education, media, etc

Electrical & electronic products

Financial, insurance and business services

Mining & quarrying

Wood, paper & printing Furniture, jewellery and other manufacturing

Wholesale & retail trade

Clothing, textiles & leather products

Machinery & metals products

Food, beverages & tobacco

Chemicals & other mineral products

Agriculture, forestry & fishing

% of Total

% of Total Value

% of Total Number

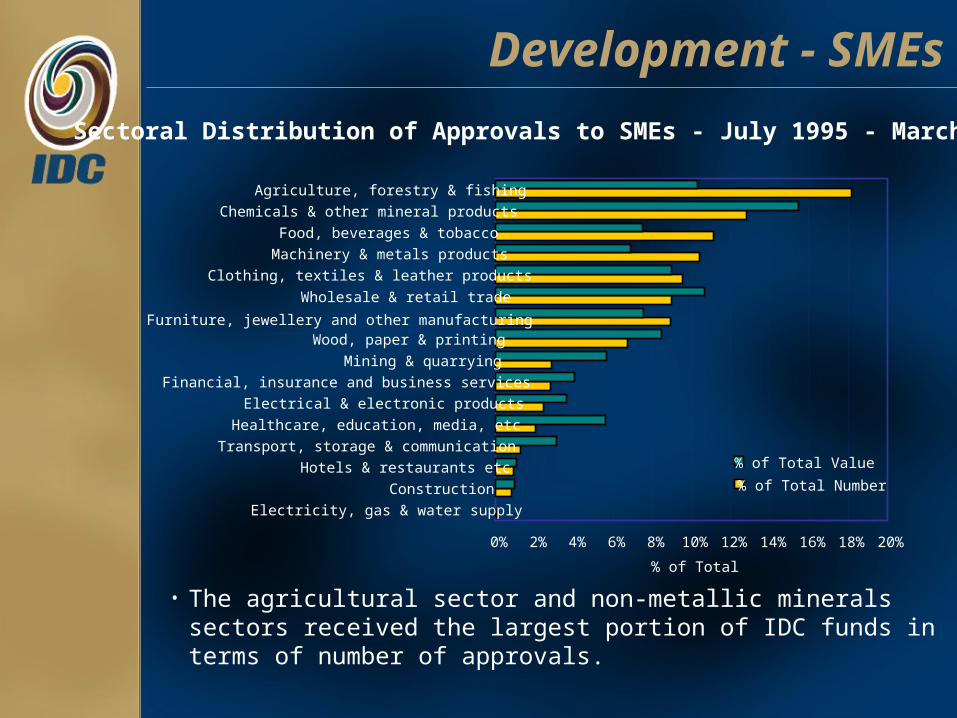

Sectoral Distribution of Approvals to SMEs - July 1995 - March 2005

• The agricultural sector and non-metallic minerals sectors received the largest portion of IDC funds in terms of number of approvals.

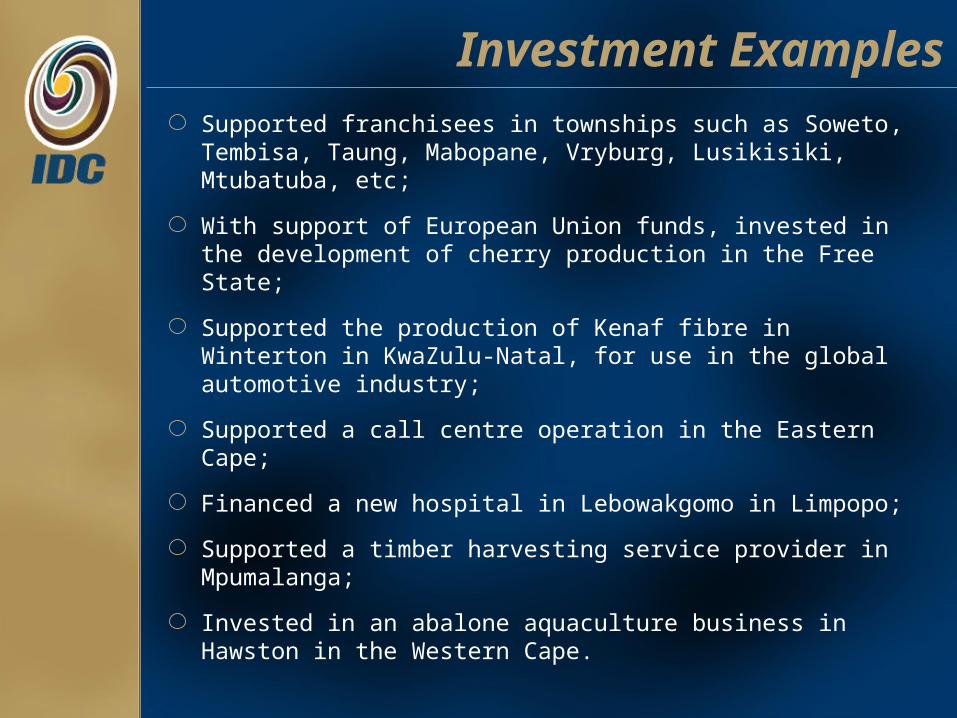

Investment Examples

Supported franchisees in townships such as Soweto, Tembisa, Taung, Mabopane, Vryburg, Lusikisiki, Mtubatuba, etc;

With support of European Union funds, invested in the development of cherry production in the Free State;

Supported the production of Kenaf fibre in Winterton in KwaZulu-Natal, for use in the global automotive industry;

Supported a call centre operation in the Eastern Cape;

Financed a new hospital in Lebowakgomo in Limpopo;

Supported a timber harvesting service provider in Mpumalanga;

Invested in an abalone aquaculture business in Hawston in the Western Cape.

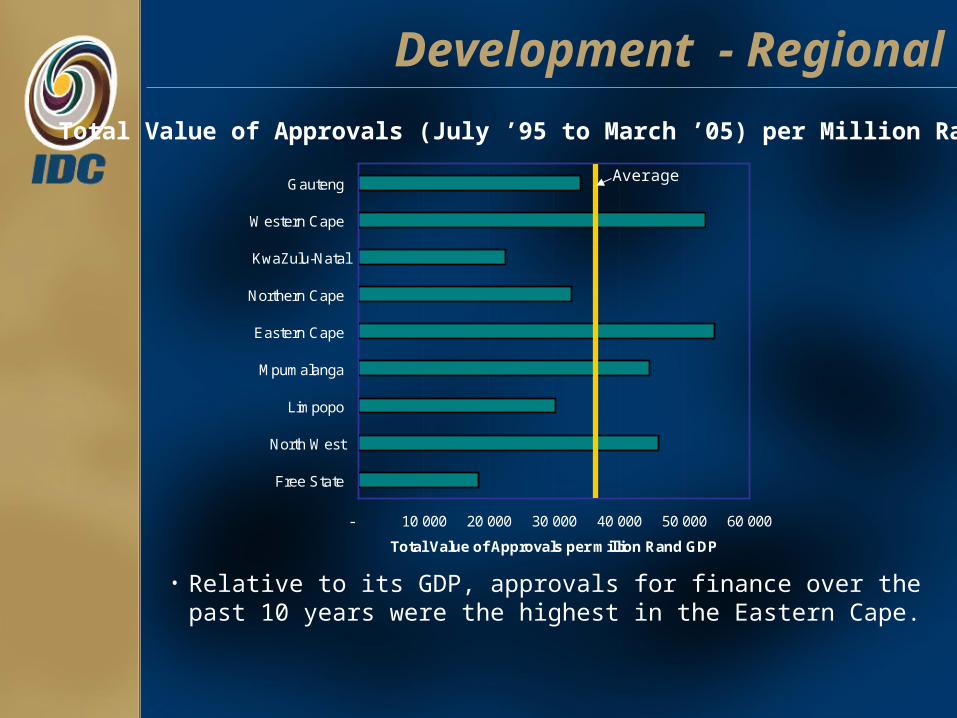

Development - Regional

• Relative to its GDP, approvals for finance over the past 10 years were the highest in the Eastern Cape.

Total Value of Approvals (July ’95 to March ’05) per Million Rand GDP

- 10 000 20 000 30 000 40 000 50 000 60 000

Free State

North West

Limpopo

Mpumalanga

Eastern Cape

Northern Cape

KwaZulu-Natal

Western Cape

Gauteng

Total Value of Approvals per million Rand GDP

Average

Provincial engagement initiatives

Initiated process of provincial engagement to support Provincial Growth and Development Strategies

Started with Limpopo Province: – Investment Conference; and– Memorandum of Understanding with LimDev

Following-up in current year:– Investment conferences in, and MOUs with, North

West, Free State and Mpumalanga (planned)– Meetings with Premiers and Executive Councils of

Eastern Cape and Northern Cape (planned)

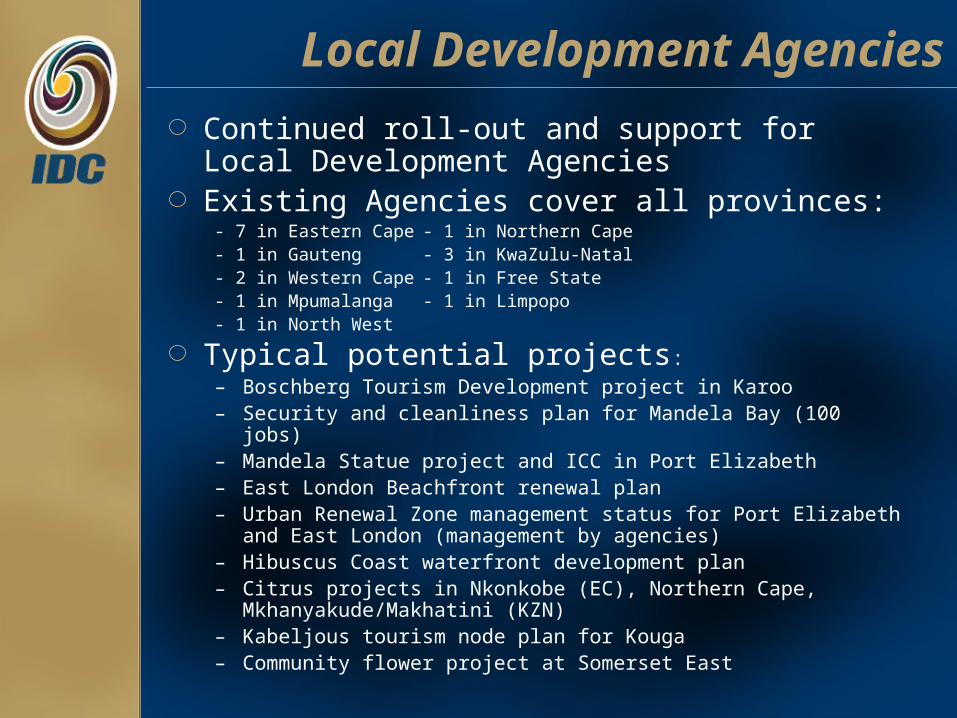

Local Development Agencies

Continued roll-out and support for Local Development AgenciesExisting Agencies cover all provinces:

- 7 in Eastern Cape - 1 in Northern Cape- 1 in Gauteng - 3 in KwaZulu-Natal- 2 in Western Cape - 1 in Free State- 1 in Mpumalanga - 1 in Limpopo- 1 in North West

Typical potential projects:– Boschberg Tourism Development project in Karoo– Security and cleanliness plan for Mandela Bay (100 jobs)– Mandela Statue project and ICC in Port Elizabeth– East London Beachfront renewal plan– Urban Renewal Zone management status for Port Elizabeth and East

London (management by agencies)– Hibuscus Coast waterfront development plan– Citrus projects in Nkonkobe (EC), Northern Cape,

Mkhanyakude/Makhatini (KZN)– Kabeljous tourism node plan for Kouga– Community flower project at Somerset East

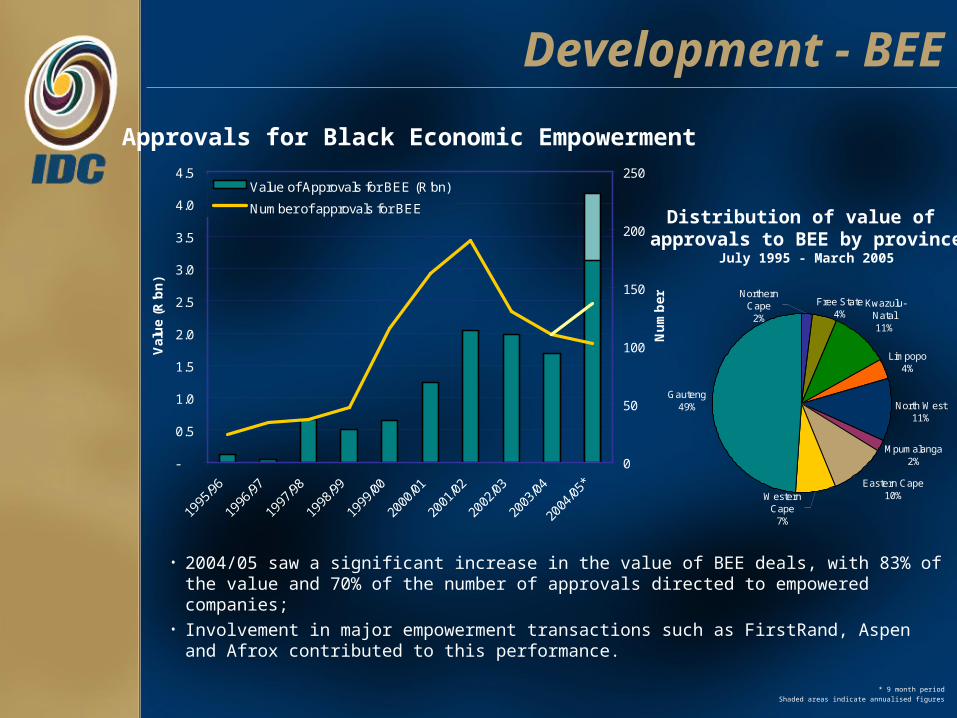

Development - BEE

Approvals for Black Economic Empowerment

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05*

Val

ue

(R'b

n)

0

50

100

150

200

250

Nu

mb

er

Value of Approvals for BEE (R'bn)

Number of approvals for BEE

• 2004/05 saw a significant increase in the value of BEE deals, with 83% of the value and 70% of the number of approvals directed to empowered companies;

• Involvement in major empowerment transactions such as FirstRand, Aspen and Afrox contributed to this performance.

* 9 month period

Shaded areas indicate annualised figures

Kwazulu-Natal 11%

Limpopo 4%

North West 11%

Mpumalanga 2%

Eastern Cape 10%

Gauteng 49%

Western Cape

7%

Northern Cape

2%

Free State 4%

Distribution of value of approvals to BEE by province

July 1995 - March 2005

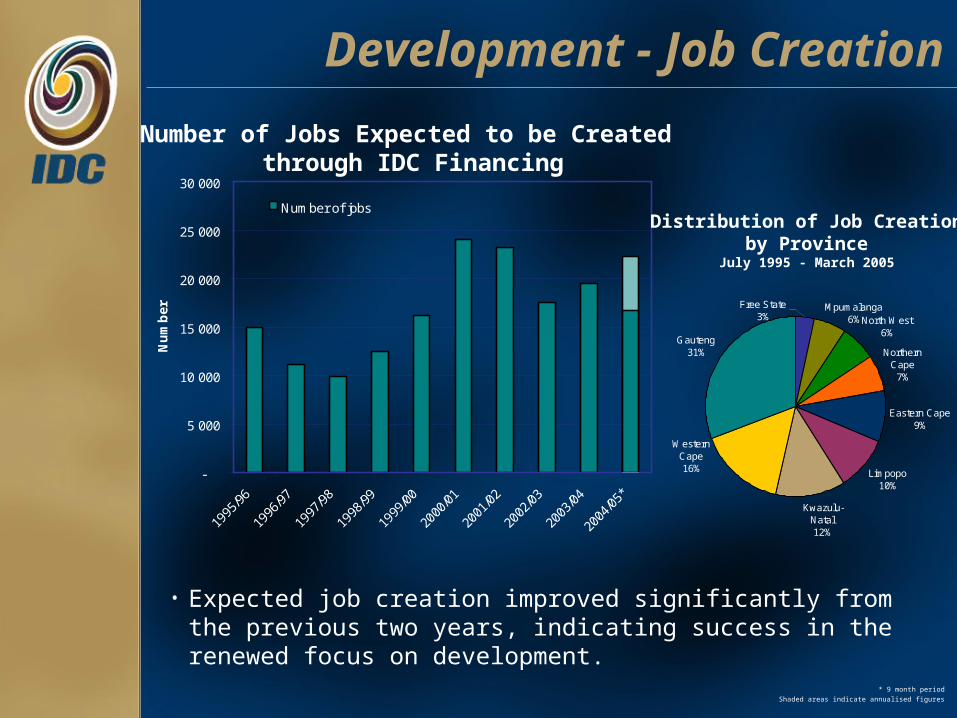

Development - Job Creation

Number of Jobs Expected to be Created through IDC Financing

-

5 000

10 000

15 000

20 000

25 000

30 000

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05*

Nu

mb

er

Number of jobs

• Expected job creation improved significantly from the previous two years, indicating success in the renewed focus on development.

* 9 month period

Shaded areas indicate annualised figures

North West 6%

Northern Cape

7%

Eastern Cape 9%

Limpopo 10%

Kwazulu-Natal 12%

Gauteng 31%

Mpumalanga 6%

Free State 3%

Western Cape 16%

Distribution of Job Creationby Province

July 1995 - March 2005

Development - Job Creation

- 10 20 30 40 50 60

Eastern Cape

Free State

Gauteng

KwaZulu-Natal

Limpopo

Mpumalanga

North West

Northern Cape

Western Cape

Number of IDC jobs per 1 000 people employed in the province

Number of IDC related jobs created per 1 000 people employed in each province

(July ’95 to March ’05)

Average

• Job creation in the Northern Cape benefited significantly over the past 10 years, through the implementation of high value added agricultural projects.

-0.5

-

0.5

1.0

1.5

2.0

2.5

3.0

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05*

Val

ue

(R'b

n)

Value of approvals (R'bn)

Involvement in Africa

Net Value of Approvals

• Approvals for investments in Africa vary depending on opportunities – with large transactions such as Mozal and infrastructure related investments leading to higher investments in 2001 and 2003

* 9 month period

Shaded areas indicate annualised figures

“Leadership in Development”

Job creation in priority areas through:

• Active identification and development of investment opportunities in targeted areas

• Sectoral development strategies

• Targeted pricing discounts

• Focused service delivery

• Supporting expansionary and broad-based BEE

• Providing support for entrepreneurs

• Providing support for community groups

• Expanding IDC’s reach/presence

• Leveraging outside resources

• Identification of opportunities arising from the Soccer World Cup 2010

• Expanding the role of the IDC Training Academy outside IDC

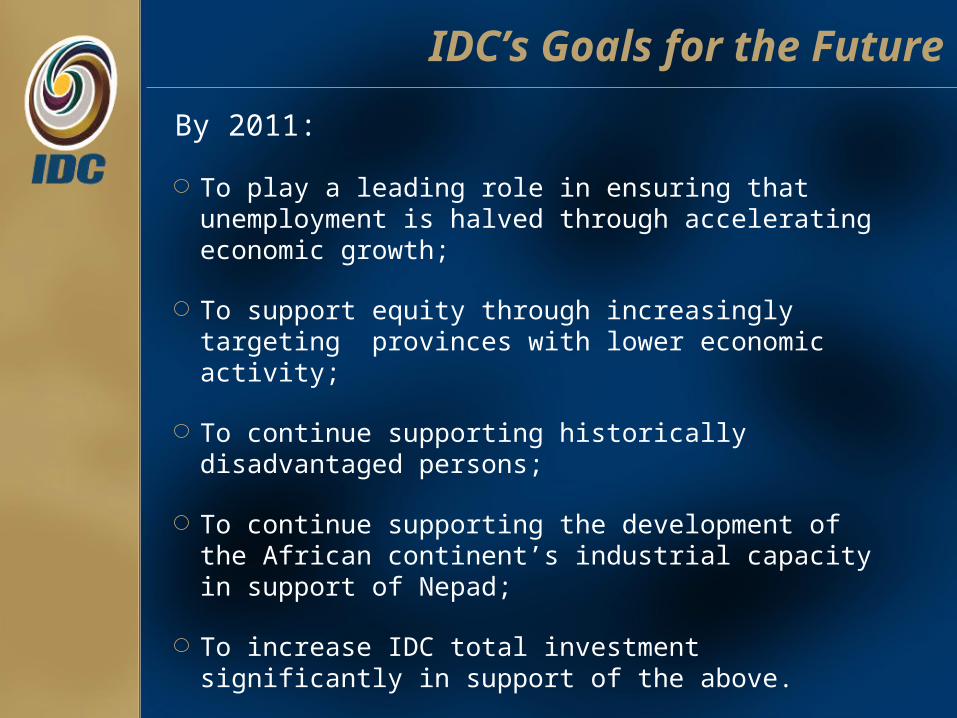

IDC’s Goals for the Future

By 2011:

To play a leading role in ensuring that unemployment is halved through accelerating economic growth;

To support equity through increasingly targeting provinces with lower economic activity;

To continue supporting historically disadvantaged persons;

To continue supporting the development of the African continent’s industrial capacity in support of Nepad;

To increase IDC total investment significantly in support of the above.

Thank You

Gert GouwsChief Financial Officer

2004/2005Financial Results

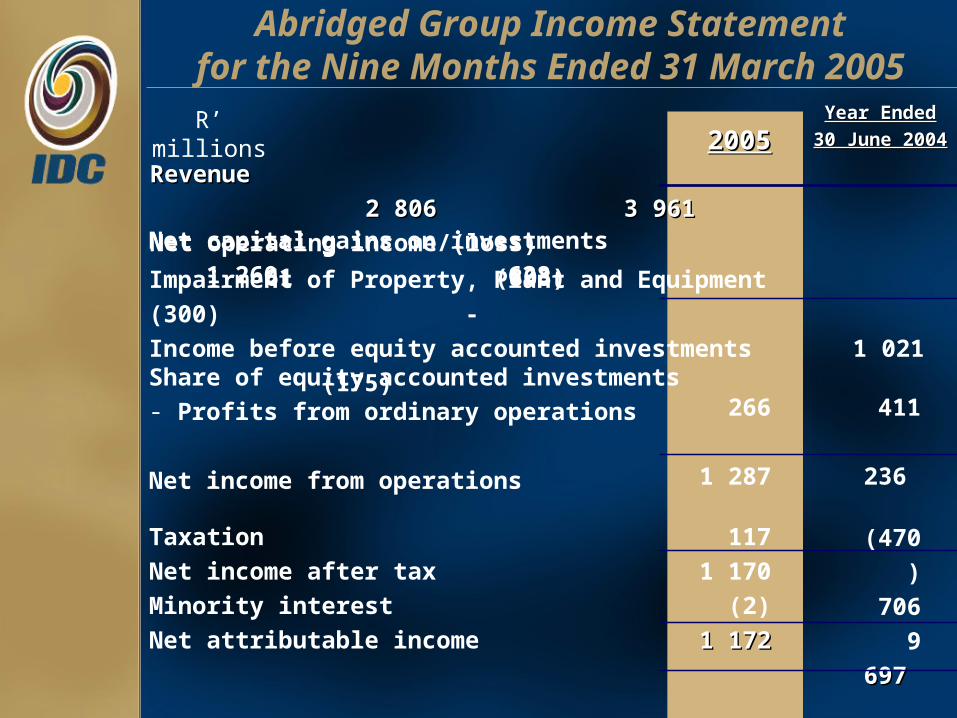

Abridged Group Income Statementfor the Nine Months Ended 31 March 2005

Share of equity accounted investments- Profits from ordinary operations

Net income from operations

266

1 287

411

236

20052005Year Ended Year Ended

30 June 30 June

20042004Revenue 2 806 Revenue 2 806

3 9613 961Net operating income/(loss) 61 (803)

TaxationNet income after taxMinority interestNet attributable income

1171 170

(2)

1 1721 172

(470)

7069

697697

R’ millions

Net capital gains on investments 1 260 628 Impairment of Property, Plant and Equipment (300) -Income before equity accounted investments 1 021 (175)

Analysis of Income Statement Itemsfor the Nine Months Ended 31 March 2005

200200

55

Year Ended Year Ended

30 June 200430 June 2004

1 2601 372 174

2 8062 806

1 564

2 053

344

3 3

961961

RevenueRevenue

Financing Activities FoskorOther subsidiaries

R’ millions %%

7(11)(33)

(6)

(256)

218

- Net movement in Impairments

- After Impairment Provisions

20052005

474

Net Operating IncomeNet Operating Income

Financing Activities- Before Impairment Provisions

FoskorOther Subsidiaries

Analysis of Income Statement Itemsfor the Nine Months Ended 31 March 2005

R’ millions

(132)(25)

61

Year Year

ended ended

30 June 30 June

20042004

%%

408(803)

(395)

(410)2

(803)

5257

NMF

57NMF

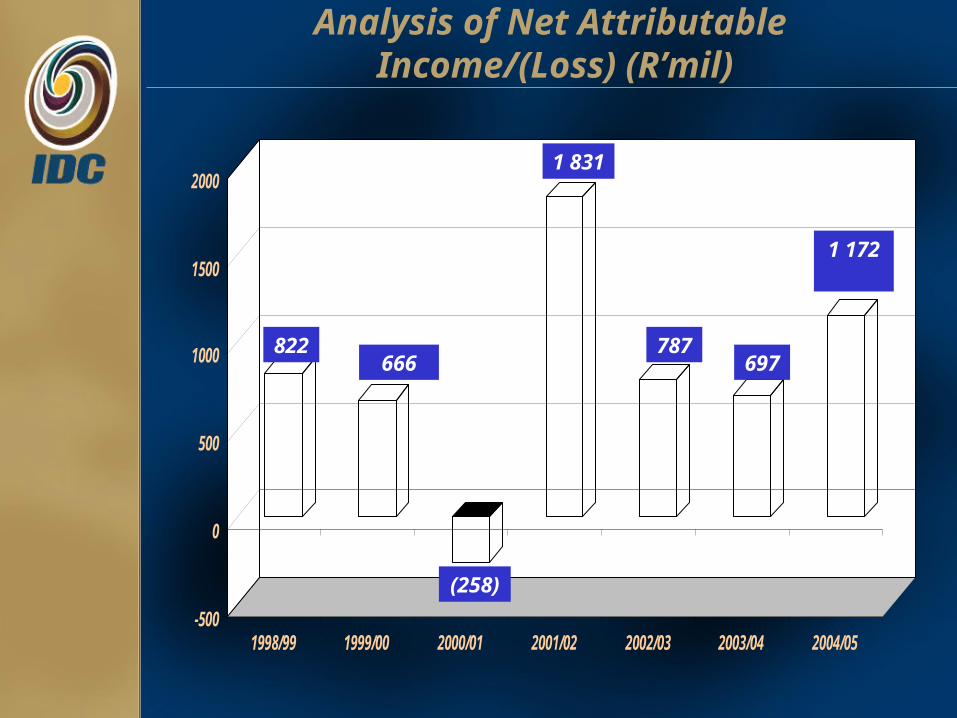

Analysis of Net Attributable Income/(Loss) (R’mil)

-500

0

500

1000

1500

2000

1998/99 1999/00 2000/01 2001/02 2002/03 2003/04 2004/05

1 172

822666

(258)

1 831

787697

Abridged Group Balance Sheetas at 31 March 2005

2005

2 08130

5922 7751 145

36 36

593593

1 666

25 059

3 1741 041

30 30

940940

AssetsAssets

Cash and cash equivalentsLoans, advances and investmentsProperty, plant & equipment & InventoriesOther assets

Debt/Equity Ratio 16%16% 21%21%

Equity and LiabilitiesEquity and Liabilities

Capital and reservesLong-term loansDeferred taxationOther liabilities

29 806

4 803643

1 341

36 36

593593

24

5415 038

-1 361

30 30

940940

30 June 30 June 20042004

R’ millions

Thank You

Related Documents