ICP 22A: Introduction to Derivatives Basic-level Module A Core Curriculum for Insurance Supervisors

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ICP 22A:Introduction toDerivatives

Basic-level Module

A Core Curriculum for Insurance Supervisors

Copyright © 2006 International Association of Insurance Supervisors (IAIS).All rights reserved.

The material in this module is copyrighted. It may be used for training by competent organi-zations with permission. Please contact the IAIS to seek permission.

This module was prepared by Robert Sharkey. Mr. Sharkey is senior vice president at Sun Life insurance company, and his experience within the company spans 28 years. He is director and secretary-treasurer of the Actuarial Foundation of Canada as well as director of the board of trustees for the Actuarial Foundation in the United States. Prior to this, he was director of the board of the Canadian Institute of Actuaries from 1996 to 1999. He is an actuary with qualifi-cations from the Society of Actuaries (FSA), the Canadian Institute of Actuaries (FCIA), and the American Academy of Actuaries (MAAA) and holds memberships in numerous profes-sional organizations.

The module was reviewed by Tomoko Amaya and Antoine Mantel. Ms. Amaya has been director for international insurance services at the Financial Services Agency (FSA), Japan, since July 2002, where she is in charge of international aspects of insurance regulation and supervision. She chairs the Accounting Subcommittee of the International Association of In-surance Supervisors (IAIS) and has been an active member of many working parties. She has experience in the regulation and supervision of the securities and banking sectors. Antoine Mantel is a civil servant and an actuary with 16 years experience in insurance supervision at French Insurance Supervision Authority (‘Autorité de contrôle des assurances et des mutu-elles’). He is now responsible for a team in charge of supervision of around 80 French insur-ance companies or groups.

iii

Contents

About the Core Curriculum . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

Note to learner . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vii

A. Introduction to derivatives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

B. Standard types of derivatives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

C. Derivative risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

D. References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Appendix I. ICP 22 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Appendix II. Glossary of key terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Appendix III. Answer key . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

FiguresFigure 1: Profile of the call option payoff . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Figure 2. Profile of the put option payoff . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Figure 3. Interest rate or equity swap . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Figure 4. Credit default and total return swaps . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

v

About theCore Curriculum

A financially sound insurance sector contributes to economic growth and well-being by supporting the management of risk, allocation of resources, and mobilization of long-term savings. The insurance core principles (ICPs), developed by the International As-sociation of Insurance Supervisors (IAIS), are key international standards relevant for sound financial systems.

Effective implementation of the ICPs requires skilled and knowledgeable insurance supervisors. Recognizing this need, the World Bank and the IAIS partnered in 2002 to develop a “core curriculum” for insurance supervisors. The Core Curriculum Project, funded and supported by various sources, accelerates the learning process of both new and experienced supervisors. The ICPs provide the structure for the core curriculum, which consists of a set of modules that summarize the most relevant aspects of each topic, focus on the practical application of supervisory concepts, and cross-reference existing literature.

The core curriculum is designed to help those studying it to:

• Recognize the risks that arise from insurance operations• Know the techniques and tools used by private and public sector professionals• Identify, measure, and manage these risks• Operate effectively within a supervisory organization• Understand the ICPs and other IAIS principles, standards, and guidance• Recommend techniques and tools to help a particular jurisdiction observe the

ICPs and other IAIS principles, standards, and guidance• Identify the constraints and identify and prioritize supervisory techniques and

tools to best manage the existing risks in light of these constraints.

vii

Note to learner

Welcome to the ICP 22A: Introduction to derivatives. This is a basic-level module on derivatives that does not require specific prior knowledge of this topic. The module should be useful to either new insurance supervisors or experienced supervisors who have not dealt extensively with the topic or are simply seeking to refresh and update their knowledge.

Start by reviewing the objectives, which will give you an idea of what a person will learn as a result of studying the module. Then proceed to study the module either on an independent, self-study basis or in the context of a seminar or workshop. The amount of time required to study the module on a self-study basis will vary, but it is best addressed over a short period of time, broken into sessions on sections if desired.

To help you engage and involve yourself in the topic, we have interspersed the module with a number of hands-on activities for you to complete. These exercises are intended to provide a checkpoint from time to time so that you can absorb and under-stand the material more readily and can apply the material to your local circumstances. You are encouraged to complete each of these activities before proceeding with the next section of the module. If you are working with others on this module, develop the an-swers through discussion and cooperative work methods. An answer key in appendix III sets out some of the points that you might consider when tackling the exercises and suggests where you might look for the answers.

As a result of studying the material in this module, you will be able to do the fol-lowing:

• Explain financial derivatives and their relationship to securities

Insurance Supervision Core Curriculum

viii

• Describe options and futures and illustrate the difference in their payoff pro-files

• Describe the differences between exchange-traded and over-the-counter-deriv-atives and explain how these differences affect credit, legal, and liquidity risks

• Explain the function of derivative exchanges and clearinghouses• Enumerate and illustrate the different types of risks that may arise in connection

with derivatives.

�

ICP 22A:Introduction to Derivatives

Basic-level Module

A. Introduction to derivatives

Derivatives are financial contracts that change in value in response to changes in the value, or a component of the value, of one or more of the following: underlying assets (security or commodity), indexes, currency rates, or interest rates. Most derivatives fall into four classes: foreign exchange, interest rate, equity, and commodity. Derivatives can be based on underlying insurance, on catastrophe-loss and property indexes, and on climatic, geological, or physical conditions (see ICP 22, explanatory note 1). For a discussion of catastrophe insurance options, see Chicago Board of Trade (1996).

The derivative contract usually specifies a “notional amount” of the underlying asset, index, or currency that is used to determine the amount that the purchaser will pay to the seller of the derivative. The purchaser does not have to invest or receive the notional amount initially or at maturity. Derivatives that do not have a notional amount specify cash payments. Derivatives may or may not require payments initially, during the term of the contract, or at termination of the contract. Derivatives are often settled at maturity through an exchange of cash rather than the physical delivery of an underly-ing asset.

Insurance company supervisors, boards, and senior management should chal-lenge whether the use of derivatives is suitable and justified. It cannot be presumed that cash-market alternatives do not exist or are more costly or less effective. These deter-minations are matters of fact that can only be determined by comparing the costs and effectiveness of using derivatives to those of using the best cash-market solution. Before using a derivative, cash-market alternatives should be understood thoroughly, and the reasons for adopting a derivative solution should be clear. Supervisors should ensure

Insurance Supervision Core Curriculum

�

that this type of review process is in place and that the rationale for derivative strategies is clear, understood, and documented.

Cash-market alternatives often are available, but they may not meet the precise need. Often the risk exposures of financial intermediaries arise in retail markets, and derivatives can be used cost-effectively to manage those risks, because the supply-de-mand forces shaping wholesale markets are quite different from those shaping retail markets.

Exchange-traded versus over-the-counter derivatives

An exchange is a market mechanism that facilitates the exchange of offsetting contracts, thereby enabling derivative contracts to settle on a net or cash basis without exchange of the underlying asset. Derivatives may be transacted either on exchanges (be “exchange listed”) or off exchanges (“over-the-counter”). Exchange-listed contracts have standard terms and conditions, whereas over-the-counter contracts have customized terms and conditions. Exchange-traded derivatives are inflexible, since the exchange determines the choice of the underlying asset (or index), the maturity, the size of the contract, terms of delivery, and other conditions of the contract. Exchange-traded transactions provide only a limited array of derivative types and contract terms, which may not fully meet hedging requirements as to timing and amount. A large exchange-traded derivative transaction may be difficult to execute, while a smaller one is usually easy to execute.

Over-the-counter instruments are custom designed to meet the precise usage re-quired. Typically, there is more flexibility as to the financial terms, such as size and length of time to maturity, and the underlying asset or index than is available from exchange-traded instruments. Over-the-counter arrangements can fit hedging require-ments more precisely and can benefit from the advice and expertise of the market mak-er. A large over-the-counter derivative transaction is usually possible, but a smaller one may be difficult to execute.

Pricing

Over-the-counter arrangements can be more cost-effective. Current market prices are generally readily available for exchange-traded derivatives, since obtaining and dis-seminating this information is a responsibility of the exchange. In contrast, market prices for over-the-counter derivatives may be difficult to obtain. The standard nature of exchange-traded contracts can make them highly liquid and price competitive. The unique terms and conditions of over-the-counter derivatives may make them less liquid and less competitively priced than exchange-traded derivatives. However, liquidity and price competitiveness vary by the type of contract; moreover, some exchange-traded

ICP ��A: Introduction to Derivatives

�

derivatives are quite illiquid and have low volume, while some over-the-counter deriva-tives are quite liquid and competitively priced.

Over-the-counter derivatives are less competitively priced than exchange-traded derivatives to the extent that the over-the-counter derivative is complex, unusual, or innovative and consequently only available from a single or limited number of coun-terparties. Dealers charge handsomely for innovation, for the capacity to dynamically manage, measure, and monitor complex risks, and for the probability that capital will be put at risk during the life of the contract.

credit, legal, and liquidity risks

Credit, legal, and liquidity risks differ in important ways between exchange-traded and over-the-counter derivatives.

Credit risk applies to derivatives, in that the counterparty may not make good on the full financial terms of the contract. There is minimal credit risk from derivatives transacted on major exchanges. Exchange-traded derivatives are guaranteed by the exchange. The total capital of the exchange and the total margin on deposit with the exchange back this guarantee. Moreover, the members of the exchange will supply ad-ditional capital to support the guarantee, so long as it is in their interests to keep the exchange operational. Finally, potential credit exposure is minimized by requirements to mark exchange-traded derivatives to market each day. Insurance supervisors should recognize, nonetheless, that credit risk applies to derivative exchanges with minimal capital, margin requirements, and profitability to members.

Over-the-counter derivatives have credit risk, since not all market makers have adequate capital for the risks they underwrite and not all manage their risks effectively. Inadequate capital and mismanagement of risk can cause bankruptcy. Credit risk can be mitigated by mark-to-market settlement arrangements, by the provision of collateral, and by guarantees provided by a parent or other institutions with a high credit rating.

Regulators can restrict the list of derivative counterparties with which insurers are permitted to transact in order to ensure that counterparties are adequately capitalized and have adequate risk management expertise and processes. In addition, supervisors should be concerned about insurers who have significant exposures to counterparties with low credit ratings or do not make effective use of risk mitigation strategies: mark-to-market arrangements, provision of collateral, and provision of guarantees.

The legal documentation governing an exchange-traded derivative is provided by the rules and regulations of the exchange and any contract with the broker. Exchanges are subject to extensive regulatory oversight and legal requirements. Supervisors should ensure that insurers have appropriate processes for reviewing the legality of over-the-counter-derivative contracts, since the contract signed by the counterparties (usually a master agreement from the International Swaps and Derivatives Association) provides the legal documentation for over-the-counter derivatives. Over-the-counter markets

Insurance Supervision Core Curriculum

�

are largely unregulated and involve a higher degree of legal risk than exchange-traded vehicles.

Margin deposits and mark-to-market cash settlement on exchange-traded instru-ments require a liquidity account; they may contribute to increased earnings volatility and have adverse tax consequences. These can be largely avoided with over-the-counter contracts, but such contracts entail higher cost and credit risk.

The regulator should be concerned about the liquidity of large, long-term, com-plex, or unusual over-the-counter derivatives, especially if their price is volatile. Their liquidity can be limited, since the ability to transact is not guaranteed, as it is with exchange-traded derivatives. The potential size of the “premium” charged to unwind a derivative may be prohibitive, even though it is risky not to do so. A large premium may be charged if the derivative is unusual, complex, or long term or if markets are volatile and chaotic. Usually, liquidity evaporates in adverse circumstances, so that the deriva-tive cannot be unwound in a timely fashion, and the price continues to deteriorate. In the extreme, the original counterparty may not be prepared to unwind the contract at any price. Where liquidity is an issue, the right and even the price to unwind the con-tract should be negotiated and documented in the original contract. This concern is especially critical for derivatives with high price volatility.

Exercises

1. Whatarethefourmainclassesofderivativecontracts?

2. Whatisthepurposeofthe“notionalamount”inaderivativecontract?

3. Whyareexchange-tradedderivativeslessflexiblethanover-the-counterderivatives?

4. Describetheroleofexchangesastheyrelatetoexchange-tradedderivativetransactions.

5. Whatfactorsaffectthepricingofover-the-counterderivatives?

6. Explainwhyover-the-counterderivativeshavecreditrisk.Explainhowthiscreditriskcanbemitigated.

7. Whatgeneralcharacteristicsofover-the-counterderivativesrequirespecialattentionfromsupervisors?

8. Whatcharacteristicsofspecificover-the-counterderivativetransactionsrequirespecialattentionfromsupervisors?

9. Whyshouldsupervisorsbeconcernedabouttheilliquidityofover-the-counterderivatives?

10.Whatcharacteristicsofover-the-counterderivativescanmakethemilliquid?

ICP ��A: Introduction to Derivatives

�

B. Standard types of derivatives

This section introduces the standard types of derivatives—futures, options, and swaps—and their major variants; explains, compares, and contrasts the key characteristics, risks, and payoff profile of each type of derivative; and describes the terms and conditions of contracts and key terminology. It also presents the market context by describing futures exchanges and clearinghouses and notes the risk considerations that are important to supervisors and insurers. After finishing this section, you should have a basic knowl-edge of the derivatives most widely used by insurers and an appreciation of their market context.

Derivative contracts are of two basic types: forward-type contracts and option-type contracts. Forward-type contracts include forwards, futures, and swaps. Option-type contracts include options, caps, floors, collars, and options on forward-type contracts. The change in value of a forward-type contract is roughly proportional to the change in value of the underlying asset or index, whereas the change in value of an option-type contract is not. These two types of contracts are the building blocks from which all de-rivatives are constructed.

Futures and forward contracts

A futures contract is an exchange-traded, highly standardized contract obliging a buyer and a seller to trade a fixed amount of a specified commodity, currency, financial asset, or index at a set price on a future date during a specified delivery period. The set price is the price to be paid at maturity in exchange for the asset or index. The future is a price-fixing contract, because the purchaser has effectively bought the underlying asset at a fixed price set at the purchase date. The buyer takes on the financial consequences of owning the asset or index as soon as the future is purchased and, as the owner of the future, must absorb all price changes in the underlying asset or index from the future purchase date until the future is sold or settled.

The standard terms and conditions of a futures contract make it liquid and trad-able. Contracts with the same maturity, amount, and underlying asset or index are iden-tical and consequently are traded anonymously. The purpose of futures contracts is generally to capture the change in market value of the underlying asset or index, not to secure delivery of it.

The theoretical strike price of a future equals the current price of the underlying asset being bought forward plus the cost of financing its purchase until the delivery date less the return, if any, earned on the underlying asset during the period. Financial futures have a strike price lower than the current spot price, if the short-term borrowing cost is less than the return on the underlying asset. Supply-demand expectations can cause the price of a commodity future to be less than the current spot price of the com-modity, even though there is no earned income to reduce the financing costs.

Insurance Supervision Core Curriculum

�

Owning a future or forward contract creates the same market risk-return trade-offs as owning the underlying asset or index. The contract owner suffers a loss (gain) at expiry if the value of the underlying asset is less (greater) than the strike price, since the owner must pay the strike price for an asset whose value is less than the strike price. This loss (gain) is dollar for dollar the same as the loss (gain) that would be experienced by the owner of the underlying asset as its value drops (rises) further and further below (above) the strike price.1 The maximum potential loss equals the strike price. This loss occurs when the underlying asset or index has lost all its value and the owner is obliged to pay the strike price in exchange for an asset that has no value. The maximum poten-tial gain is unlimited.

The seller of a future suffers a loss (gain) at expiry if the value of the underlying asset is greater (less) than the strike price, since the seller must provide the underlying asset in exchange for payment of the strike price, which is less than the value of the asset. There is no maximum potential loss from selling a future, since the value of the underlying asset can increase without limit. The maximum potential gain is the strike price.

Futures exchanges and clearinghouses

A futures exchange is a central marketplace where futures contracts are bought and sold competitively and openly. The exchange specifies all of the terms and conditions of the contract, except the price. The exchange establishes and enforces trading rules and collects and publishes market information. A centralized clearinghouse records, registers, and administers all contracts until they are closed out or until delivery. The clearinghouse guarantees each contract, eliminating the individual management of credit lines and counterparty risk. The mechanics of the clearinghouse differ slightly from exchange to exchange. For information on the Chicago Mercantile Exchange, see http://www.cme.com/clr/clring/securtyfut/clearinfo1508.html; for information on the London Clearing House, see http://www.liffe.com/access/trading/.

Initial and variation margin and accounting for futures contracts. At the time the futures position is established, the exchange requires the investor to put up collateral or margin equal to a small, specified percentage, such as 3 percent, of the contract’s face amount. This margin is a good-faith deposit and not a down payment. The exchange defines the amount of this “initial margin.” Every day thereafter, the investor pays or receives a “variation margin” equal to the change in price of the underlying asset or index times the face amount of the contract. This daily settlement means that the differ-ence between the price of the underlying asset or index at initiation and maturity of the contract will be paid over the life of the contract.

1. As a matter of convenience, all references to currency amounts use “dollars.” Of course, derivatives are also transacted in many other currencies.

ICP ��A: Introduction to Derivatives

�

The clearinghouse is responsible for collecting margin deposits and settling gains and losses. The clearinghouse acts as the buyer to every seller and the seller to every buyer. It guarantees payment on every transaction in the event of a default by one of the parties to the futures contract and also assigns deliveries. The margin, along with the capital and support provided by members of the exchange, gives the clearinghouse the financial resources to provide the guarantee and ensures the financial integrity of the clearinghouse.

The value of the asset underlying a futures contract is not reported on the balance sheet in financial statements. The initial margin continues to be owned by the company and is shown as a company asset. The securities underlying future margin receipts pro-vided to the clearinghouse are shown as company assets. Variation margin payments are recognized as accounting gains or losses in a fashion consistent with the related investment.

Settlement of futures contracts. A buyer who holds a futures contract until expiry is obligated to accept delivery of the underlying asset or index. The seller is commit-ted to making delivery during the delivery period. Most futures contracts are settled in cash by extinguishing the contract prior to commencement of the delivery period rather than by exchanging the futures price for the underlying asset. A futures contract is extinguished by buyers selling and sellers buying exactly offsetting contracts from the exchange. In the case of futures on indexes, cash settlement is the only means of settle-ment.

Consider the 10-year Government of Canada bond futures contract (CGB) traded on the Montreal Exchange. The trading unit is $100,000 of a notional 9 percent coupon Canada bond. Any government of Canada bond with at least $3.5 billion outstanding and 6.5–10 years remaining on the term can be used in delivery.

The price for any delivery bond is calculated using a conversion factor designed to bring all deliverable bonds to a common basis for delivery. The conversion factor is the price at which the delivered bond with $1 par value with the same maturity and coupon would be sold to yield 9 percent on the first day of the delivery month (less accrued interest). The Montreal Exchange publishes a list of conversion factors. The delivery settlement amount is the accrued interest plus the futures settlement price times the conversion factor times 1,000. The seller selects which bond to deliver.

Forward contracts

A forward contract is an over-the-counter future with a specific company. Contract terms and conditions are negotiated with this company and therefore are more flexible than exchange-traded future contracts. Normally, there is no initial or variation mar-gin. Cash changes hands only at maturity, when the buyer pays the forward price and receives the asset or cash settlement of the difference between the asset and the forward

Insurance Supervision Core Curriculum

�

price. Consequently, both parties have credit exposure to each other for the term of the contract. To reduce credit risk, collateral may be posted at the outset or when an adverse market move exceeds a predetermined threshold. A forward contract on a share usually has physical settlement. Forward contracts are executed over the phone; subsequently, written confirmations and signed contracts are exchanged.

Forward rate and Forward currency agreements

One of the most common types of forward contracts is a forward rate agreement (FRA). The parties to the FRA contract agree to exchange the amount of notional principal times the difference between a fixed rate agreed to on the purchase date and the mar-ket rate of an index, such as the six-month interbank rate, on the contract settlement date—for example, two months from the purchase date of the FRA. The purchaser ben-efits from rate increases, and the seller benefits from rate decreases. FRAs are referred to in terms of the number of months to the beginning and end of the interest period. An FRA on the six-month LIBOR starting two months forward is a 2 X 8 FRA.

The most common forward contract is the forward currency agreement (FCA). Currencies are regularly bought and sold up to one year forward, while major cur-rencies can usually be bought and sold at least five years forward without difficulty. Usually no money changes hands prior to maturity. The FCA fixes an exchange rate for exchanging currencies on the settlement date. Settlement may be by an actual exchange of currencies, but it usually involves a cash payment equal to the value of the difference between the exchange rate fixed by the contract and the spot exchange rate at the time of settlement.

risks associated with Future and Forward contracts

The greatest concern of supervisors and insurers should be to avoid speculative uses of futures. When futures are not used to hedge or manage portfolios, the risks can be substantial. By depositing a small initial margin, futures can oblige the insurer to make payments that may be many times larger. However, supervisors and insurers should be concerned about the risks associated with futures, even when their stated purpose is to hedge or to manage portfolios. Calling something a hedge or a tool for portfolio man-agement does not make it one.

The supervisor and insurer should be aware of several concerns that arise where hedging strategies are not perfect. There may be considerable “basis” or “timing” risk between the hedged position and the hedging future. Basis risk arises in the absence of a perfect correlation between the change in value of the hedged position and that of the hedging future. Timing risk arises when the hedging future does not expire at exactly the same time as the risk being hedged. Timing risk can be substantial, where short-

ICP ��A: Introduction to Derivatives

�

dated futures are used to “hedge” long-term exposures. This latter strategy is used with the expectation that new short-dated futures will be purchased to replace the short-dated futures prior to their expiry.

The supervisor and insurer must be satisfied that the hedge position is actively monitored and rebalanced to ensure that the objectives of the hedge are achieved over time and not just initially. No matter how effective the hedge, interest rate movements can result in margin calls to cover contract losses or the receipt of cash from contract gains, and the number of contracts in the hedging position may have to be adjusted to reflect the change in cash position.

The supervisor and insurer must be satisfied that the exposure to changes in the value of the underlying assets from the future position are no greater than those appro-priate for direct investments in the underlying asset. If the future is bought or sold as an alternative to prudent cash-market transactions, then the insurer faces the same risk-return trade-offs as when buying or selling the underlying asset in the cash market.

Option contracts

An option is a contract in which the buyer pays a fee (called a premium) in exchange for the right, but not the obligation, to buy (a call option) or sell (a put option) a fixed amount of a specific commodity, currency, swap, futures contract, financial asset, or market index at a set (strike) price within, or at, a specified time. With option-type con-tracts, the insurer must not only decide the amount, timing, and duration of the hedge, as with forward-type contracts, but also decide the appropriate set of option features, chief among which is the strike price.

Call options are not securitized, so they can be sold without the seller owning the underlying asset or index. This distinguishes a call from a warrant, which is a securi-tized call that can only be sold if the seller owns the actual security. The warrant, being a physical security, must be physically settled.

Consider a call option on 100,000 shares of a specific company at a strike price of $30 exercisable on or before March 31. If the share price is $32 when the option is exer-cised, the buyer will receive $2 from the seller for each share, since the $32 share price exceeds the $30 strike price by $2. The total amount paid to the call owner is $200,000, $2 for each of the 100,000 shares. If the share price is less than $30 on March 31, the call option expires worthless.

A call or put option is said to be “at-the-money” if the strike price equals the cur-rent value of the underlying asset. A call (put) is “in-the-money” if the strike price is less (greater) than the current value of the underlying asset. A call (put) is “out-of-the-money” if the strike price is greater (less) than the current value of the underlying asset. A call option with a strike price of $30 is at-the-money, in-the-money, or out-of-the-money if the share price is $30, greater than $30, or less than $30, respectively. A call (put) is “deep-in-the-money” or “deep-out-of-the-money” if it is in or out of the money,

Insurance Supervision Core Curriculum

�0

respectively, and the difference in strike price and the current value of the underlying asset is large.

If an out-of-the-money call option is purchased to partially “hedge” a position, the hedger can lose the option premium plus the difference between the current share price and the strike price.

Stock option contracts and the rules of option exchanges usually immunize coun-terparties against stock splits, stock dividends, rights issues, and other similar actions. Options terminate through their exercise, expiration, or an offsetting option purchase or sale (closing transaction). Options settle on exercise through delivery of the underly-ing asset or index or through cash settlement of the difference between the strike price and the asset value. Options on indexes almost always specify cash settlement. Options on single stocks usually specify physical settlement.

Dividends on individual stocks and coupon payments on individual bonds that are received during the option term usually are not paid or due to the owner of the call option. The option is on the underlying asset or index itself. The call (put) option price is higher (lower) in the event that such payments are to be paid. For options on total return indexes, these payments are taken into account indirectly.

exchange-traded and over-the-counter oPtions

An option may be exchange-traded, with standard terms, or over-the-counter, with terms negotiated directly between the two parties. The amount that can be purchased or sold by exercising the option is the “face amount” of the contract. The premium paid is usually a small fraction of the face amount. Exchange-traded option prices are quoted in cash terms. If the price of an over-the-counter option is expressed as a percentage, the insurer must be clear as to whether the percentage applies to the strike price or the value of the underlying asset (if they differ). Prices quoted in percentage terms are not sensitive to changes in the price of the underlying asset and may continue to apply even if the market has moved. For information on options markets, see Cox and Rubenstein (1995).

tyPes oF oPtions

A European-style option is one that can be exercised only on the expiration date. An American-style option is one that can be exercised at the owner’s choice, any time prior to expiration. Transatlantic-style options can be exercised before maturity, but only at specific times on specific dates (once a week, once a month, and so forth). An option is path dependent if its value depends on the value of the underlying asset or index at more than one time. A European option is not path dependent, whereas American and transatlantic options are.

ICP ��A: Introduction to Derivatives

��

A wide variety of exotic options are available from most dealers. The fact that an option is labeled exotic does not mean that it cannot be simple to understand or useful in risk and portfolio management. Exotic options may be referred to as second-gen-eration or nonstandard options. Exotic options are “exotic” from the market maker’s perspective, since they usually require sophisticated hedging and pricing techniques, are difficult to trade and manage, and place more capital at risk. For these reasons, they may be expensive.

oPtion Premiums and Pricing

If the probability distribution for the price of the underlying asset or index at option expiration is known, the value of a European option can be calculated as the sum of the present value of the probability-weighted option values at expiry based on this distribu-tion. The distribution is often taken to be log normal, with mean and volatility equal to the current forward price and current volatility of the underlying asset, respectively. The option premium thus depends on the time to expiry (which affects both the breadth of the distribution and the impact of present valuing), the price volatility of the underlying asset (which affects the breadth of the distribution), the strike price (which affects the option value at expiry at any point on the distribution), the current forward price for the underlying (which affects the mean of the distribution), and current interest rates (which are used in determining the present value).

A broader distribution and, consequently, a higher premium arise the longer the time to option expiry and the greater the price volatility of the underlying asset. The option tends to lose value as time passes, because the distribution of outcomes at op-tion expiry narrows with the passage of time. Call (put) option premiums increase (de-crease), the higher the current stock or bond price, the lower the strike price, the higher the current interest rates, and the lower the expected dividends or interest payments. The Black-Scholes option-pricing model was developed in 1973 and remains the indus-try standard for pricing European stock options.

Much of the innovation and complexity of option-type contracts is a result of ef-forts to reduce costs, while providing the end user with the flexibility to choose precisely how much upside potential to retain. To reduce the cost, the strike price of a call (put) can be increased (decreased). While reducing the cost, this also means that a greater loss must be absorbed before the protection of the option kicks in. The option premium often is not paid up-front but may be paid instead at the exercise date or in the form of an annuity or a contingent annuity. Sometimes the premium paid is reduced by the premium for an option that the purchaser sells to the counterparty.

Insurance Supervision Core Curriculum

��

Figure 2. Profile of the put option payoff

Figure 1: Profile of the call option payoff

one-sided PayoFF ProFile

When the value of the asset is less than the strike price, the call option expires worthless and the payoff is a loss equal to the premium paid. When the value of the asset exceeds the strike price, the payoff is the gain in value of the asset over the strike price (dollar for dollar) less the premium paid. The payoff profile is one-sided, since the downside is truncated (see figure 1).

When the value of the underlying asset is greater than the put strike price, the put option expires worthless and the payoff is a loss equal to the premium paid. When the value of the underlying asset is less than the put strike price, the payoff is the amount by which the value of the underlying asset has dropped below the put strike price (dollar for dollar) less the put premium paid. The put payoff profile is one-sided, since down-side losses are truncated (see figure 2).

Figure 1. Profile of the call option payoff

Profit

CallPremium

Asset Value

StrikePrice

0

Loss

Figure 2. Profile of the put option payoff

Profit

PutPremium

Asset Value

StrikePrice

0

Loss

ICP ��A: Introduction to Derivatives

��

Supervisors and insurers need to understand the very different risks involved in purchasing or writing calls. Option buyers take relatively little risk, since they cannot lose more than their option premium. Losses to call writers can be substantial, depend-ing on whether the calls are “covered” or “naked.” A written call (put) option is “cov-ered” if the writer owns the underlying asset or an offsetting call (holds cash or an offsetting put) in an amount equal to the amount of the option written. The cost of covered call writing is one of opportunity, and the risks are relatively minor. A written option is “naked” if it is not covered. The potential loss is unlimited on a naked call and 100 percent of the strike price on a naked put. Thus supervisors should pay close atten-tion to naked call writing.

intrinsic value and time value oF oPtions

The intrinsic value of an option is the difference between the current price of the un-derlying asset or index and the option strike price for in-the-money options; it is zero for options not in-the-money. The difference between the total option value (premium) and the intrinsic value is the time value of the option. While time value increases with time to expiration of the option, it also increases with price volatility and the cost of carry. The time value is greatest when the option is at-the-money and decreases as the difference between the strike price and the current asset price increases.

Exercises

11.Aportfoliomanagerowns$30millioninastockwithacurrentstockpriceof$30.Themanagerconcludesthatallofthestockshouldbesoldifitspriceincreasesto$32andafurther$30millionshouldbeboughtifitspricedropsto$28.Moreover,themanagerbelievesthestockisstuckinatradingrangebetween$28and$32.Constructastrategyinvolvingthesaleofcallsandputsonthestockthatallowsthemanagertoearnrelativelygreaterreturnsnomatterhowthestockpricechanges.

12.Aportfoliomanagerowns$10millionofaparticularbondcurrentlytradingat7percent.Themanager’sviewisthatthebondwilltradeatyieldsofbetween6.80and7.20percent;therefore,thebondwillbeovervaluedandall$10millionshouldbesoldifratesdropto6.80percent,andthebondwillbeundervaluedandafurther$10millionshouldbeboughtifratesincreaseto7.20percent.Constructastrategyinvolvingthesaleofcallsandputsonthebondthatallowsthemanagertoearnrelativelygreaterreturnsnomatterhowthebondyieldchanges.

Insurance Supervision Core Curriculum

��

Contrasting the two-sided payoff profile of forwards with the one-sided profile of options

Supervisors need to understand the differences in the payoff profile between futures and options. Any position or risk can be hedged or managed using either forward-type or option-type contracts. The market risk of a forward-type contract is measurable us-ing symmetric measures of risk, such as standard deviation, in much the same way as the underlying asset or index. However, an option-type contract truncates the return distribution (see figures 1 and 2), and asymmetric measures of market risk are required (for example, semi-variance and shortfall risk).

The forward-type contract requires the hedger to forgo the upside potential of the hedged position. The option-type contract is a more costly form of hedging, but it al-lows the hedger to keep the upside potential of the hedged position. The future-type contract is used in “market-neutral” hedging. An option-type contract might be chosen if the hedger is prepared to pay the price for the opportunity to hedge against the down-side without giving up the upside.

Forward-type contracts involve bilateral credit risk. Both buyer and seller can be exposed to credit risk depending on the price movement of the underlying asset. Op-tion-type contracts create unilateral credit risk. The seller is not exposed to credit risk, since the only obligation of the purchaser is to pay the premium, which usually occurs at inception of the contract. For a tutorial on options and futures, see Clarke (1992).

interest rate and equity swaPs

An interest rate swap is an exchange of one or more payments between two counterpar-ties, at specified times and for a specified period of time. The payments are calculated as a percentage of a principal amount according to the swap agreement. The principal amount is not an obligation of either party. It is simply the basis on which payments are calculated. At the end of the swap term, payments simply cease. Since the principal amount typically is not exchanged, this amount is referred to as the notional principal amount. Since swaps are over-the-counter instruments, they can be designed exactly to fit the needs of the user.

In a typical interest rate swap, counterparty A agrees to make periodic floating-rate payments to counterparty B based on market index rates on the payment date for the term of the swap in return for the receipt from B of periodic fixed-rate payments (see figure 3). The market index rate might be one-, three-, or six-month interbank market rates on the payment date. Refer to the subsection on forward rate and forward cur-rency agreements for an example in which an interest rate swap is a package of FRAs, one for each floating-rate reset date.

In a typical equity swap, counterparty A agrees to make periodic payments to counterparty B of the return on an equity index for the term of the swap in return for

ICP ��A: Introduction to Derivatives

��

receiving periodic fixed- or floating-rate interest payments. An equity swap to pay float-ing-rate interest and to receive a stock index return modifies the risk profile. A company retains its upside stock exposure, while eliminating its downside stock exposure.

varieties oF interest rate swaPs

Floating payments are made at the end of each period using the floating rate at the be-ginning or end of the period. In a constant maturity swap, the floating rate can be paid every six months, say, using a five-year government bond index. The floating rate can be based on more than one index (greater, average, or lesser of two). In a semi-fixed swap, fixed payments use more than one fixed rate. The lower of the fixed rates might be paid if the floating rate is below a certain rate; otherwise, the higher fixed rate is paid.

In a basis swap, one counterparty pays a floating-rate index in exchange for anoth-er floating-rate index in the same currency. A yield-curve swap is a basis swap in which floating indexes based on different points in the yield curve are exchanged. Counter-party A could agree to pay counterparty B the two-year constant maturity rate in return for receiving the five-year constant maturity rate. An accrual interest rate swap involves the payment of a floating rate in exchange for the floating rate plus a spread, which only accrues on days in which the floating rate is between an upper and lower bound. A “diff ” swap involves the exchange of floating-rate payments based on two floating indexes denominated in different currencies.

Fixed-rate payments may be made semi-annually, and floating-rate payments may be made quarterly. In a zero-coupon swap, one counterparty makes periodic payments throughout the life of the swap and receives a single predetermined payment at incep-tion of the swap or maturity. In the extreme, a single payment is exchanged at maturity, representing the net economic value of the fixed and floating cash-flow streams. Mis-matched payment swaps are uncommon, since they involve greater credit risk and may have adverse tax consequences for foreign counterparties.

An index-amortizing swap has a notional amount that decreases with the level of the floating rate. Usually, the amortization schedule slows down (speeds up) as rates rise (fall). Such swaps have interest rate sensitivity similar to mortgage-backed securities that are subject to prepayment risk. An accreting (step-up) swap has a notional amount that increases according to a preset schedule or predefined formula.

Figure 3. Interest rate or equity swapFigure 3. Interest rate or equity swap

Counterparty A FLOATING

FIXED

Counterparty B

Insurance Supervision Core Curriculum

��

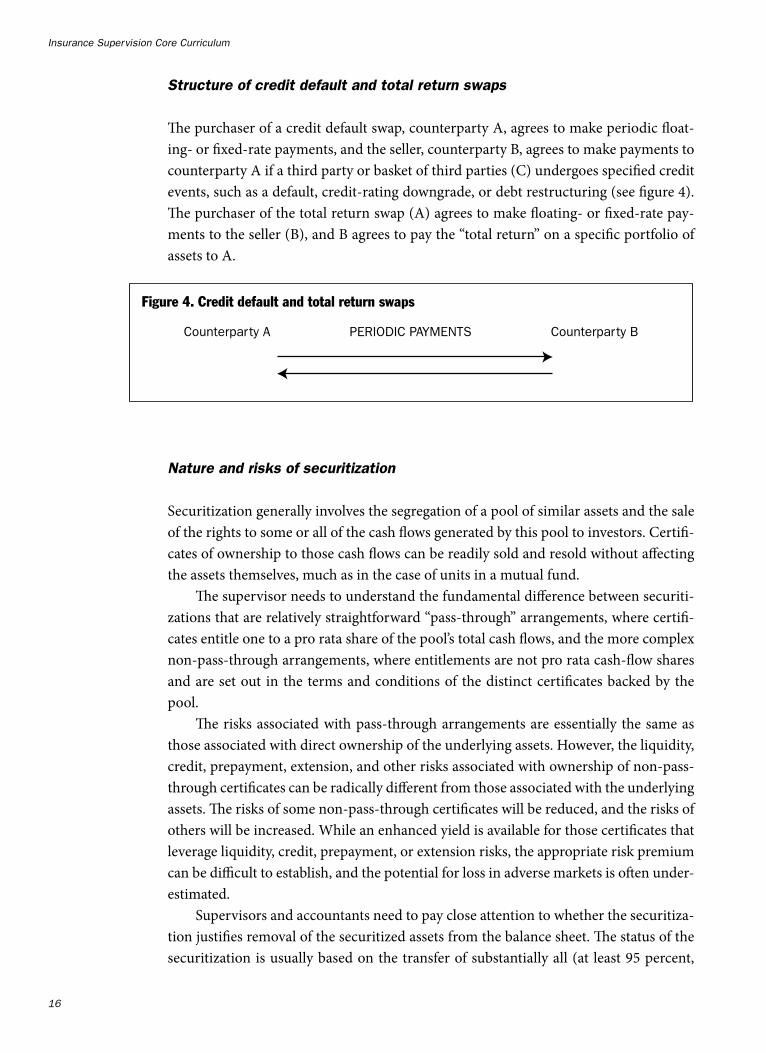

Structure of credit default and total return swaps

The purchaser of a credit default swap, counterparty A, agrees to make periodic float-ing- or fixed-rate payments, and the seller, counterparty B, agrees to make payments to counterparty A if a third party or basket of third parties (C) undergoes specified credit events, such as a default, credit-rating downgrade, or debt restructuring (see figure 4). The purchaser of the total return swap (A) agrees to make floating- or fixed-rate pay-ments to the seller (B), and B agrees to pay the “total return” on a specific portfolio of assets to A.

Nature and risks of securitization

Securitization generally involves the segregation of a pool of similar assets and the sale of the rights to some or all of the cash flows generated by this pool to investors. Certifi-cates of ownership to those cash flows can be readily sold and resold without affecting the assets themselves, much as in the case of units in a mutual fund.

The supervisor needs to understand the fundamental difference between securiti-zations that are relatively straightforward “pass-through” arrangements, where certifi-cates entitle one to a pro rata share of the pool’s total cash flows, and the more complex non-pass-through arrangements, where entitlements are not pro rata cash-flow shares and are set out in the terms and conditions of the distinct certificates backed by the pool.

The risks associated with pass-through arrangements are essentially the same as those associated with direct ownership of the underlying assets. However, the liquidity, credit, prepayment, extension, and other risks associated with ownership of non-pass-through certificates can be radically different from those associated with the underlying assets. The risks of some non-pass-through certificates will be reduced, and the risks of others will be increased. While an enhanced yield is available for those certificates that leverage liquidity, credit, prepayment, or extension risks, the appropriate risk premium can be difficult to establish, and the potential for loss in adverse markets is often under-estimated.

Supervisors and accountants need to pay close attention to whether the securitiza-tion justifies removal of the securitized assets from the balance sheet. The status of the securitization is usually based on the transfer of substantially all (at least 95 percent,

Figure 4. Credit default and total return swaps

Counterparty A PERIODIC PAYMENTS Counterparty B

ICP ��A: Introduction to Derivatives

��

say) of the asset’s risks and rewards rather than on criteria based on control of the eco-nomic benefits. For more on collateralized mortgage obligations and mortgage-backed securities, see Fabozzi (1992); Fabozzi, Ramírez, and Ramsey (1994).

Structured (hybrid) investments

Structured investments combine a cash-market security (debt or equity) with a deriva-tive. Structured notes embed a derivative in a bond. Callable, putable, exchangeable, and extendable bonds as well as convertible bonds, which give the option to the investor to convert into stock at a fixed conversion price, satisfy this definition but usually are not referred to as structured notes. A bond with fixed or floating semi-annual payments and a maturity value tied to an equity index, rather than to a fixed nominal amount as with standard bonds, is an example of a structured note.

A medium-term note is a structured note that provides return of principal or inter-est indexed to the change in or return from a given currency, commodity, market index, yield-curve, or interest rate relationship. Principal-guaranteed notes are medium-term notes, where a fixed amount of principal is paid at maturity along with an additional payment equal to the greater of zero and some participation percentage of the change in an equity index over the note term. For example, a note might mature in five years, at which time the owner is paid a principal amount of $100,000 plus 50 percent of $100,000 times the growth (zero, if growth is negative) of the equity index over the five years.

The participation percentage may be more or less than 100 percent. The note may provide for minimal periodic fixed-rate payments with a corresponding reduction in the participation percentage. The participation percentage may be greater for increases in the index beyond some specified level.

An equity-linked note consists of a bond with an embedded call option on a stock index. This note protects the owner from losses, should the index decline, but preserves the upside potential, although perhaps at less than 100 percent, should the index rise. The insurer has no downside equity risk but has taken on credit exposure to the coun-terparty. Thus the capital required for the equity note should be a function of the capital required for a credit exposure to the counterparty and not at all a function of the capital required for equity holdings. The equity-linked notes bring about a very real reduction in the risk-return profile, when contrasted with a direct equity holding.

Insurance Supervision Core Curriculum

��

Exercises

13.Whatarethetwobasictypesofderivativecontracts?

14.Isthechangeinvalueofbothtypesofderivativecontractsproportionaltothechangeinvalueoftheunderlyingassetorindex?

15.Whyisafuturescontractaprice-fixingcontract?

16.Explainwhythereisnomaximumgainfromowningafuturescontract.

17.Explainthemaximumlossfromowningafuturescontract.

18.Explaininitialandvariationmarginsforfuturescontracts.Explainhowtheyaffectderivativecreditrisk.

19.Whatisthefunctionofaclearinghouse?

20.Explainhowtheclearinghouseaffectsthecreditriskofexchange-tradedderivatives.Doclearinghouseseliminatecreditrisk?

21.Howaremostfuturescontractssettled?

22.Whatisa3x6FRA?

23.Whyshouldsupervisorsbeconcernedabouttheuseoffuturescontractstohedgerisk?

24.Whyshouldsupervisorsbeconcernedabouttheuseoffuturescontractsasasubstituteforcash-marketinvestments?

25.Whatarebasisandtimingrisksinafuturescontract,andwhyshouldtheybeofconcerntosupervisors?

26.Whatarethemainfactorsaffectingthepriceofanoption?

27.Howdoesthepassageoftimeaffectoptionprices?

28.Explainwhatismeantbysaying,“Optionshaveaone-sidedpayoffprofile,andfutureshaveatwo-sidedpayoffprofile.”

29.Howdoesriskoflossvarybetweenbuyingandsellingoptions?Whyshouldsupervisorsbeparticularlyconcernedaboutthesellingofnakedoptionsbyinsurers?

30.Explaintheriskdifferencesbetweensecuritizationsthatare“pass-through”arrangementsandsecuritizationsthatarenot“pass-through.”

31.Whyshouldsupervisorsbeconcernedaboutthesalestatusofsecuritizations?Howdoaccountantsassessthesalestatusofasecuritization?

ICP ��A: Introduction to Derivatives

��

C. Derivative risks

This section explains the major risks that derivative users must manage and under-stand, explains differences between the risk implications of different types of deriva-tives, and provides examples of special concern to supervisors and insurers. At the end of this section, you will have a basic understanding of the following: (a) derivative credit risk and how it differs among different types of derivatives, (b) some risks relating to model-based valuations, such as fraud, calibration, parameterization, assumption set-ting, programming errors, reporting, and controls, and (c) important aspects of liquid-ity, funding, operating, legal, settlement, systemic, and other derivative risks.

Credit risk

Derivative credit risk is the risk that loss will be incurred in consequence of a failure to receive full payments, when due, in accordance with the terms of the contract. An actual loss because of default depends on the financial distress of the counterparty. De-rivative credit risk primarily relates to over-the-counter derivatives, since exchange-traded derivatives on mature exchanges have the exchange as counterparty and can be regarded as a high AAA from a credit perspective.

current and Potential credit risk

It is vital for supervisors to understand that the current market value of a derivative portfolio may not indicate the potential credit exposure of the portfolio. Market value may greatly underestimate or greatly overestimate the credit exposure.

The current market value of cash-market investments gives a good indication of the potential loss that may be incurred as a result of owning the investment. The po-tential credit loss from a cash-market investment with a $100 million current market value is $100 million, whether the investment is a single investment or a portfolio of investments.

Potential credit loss is not an adequate measure of potential credit exposure for cash-market investments, because it does not take into account the likelihood that:

• A credit event will occur• Not all counterparties will default at the same time• There will be recoveries in the event of default.

For this reason, measures of credit risk exposure combine measures of potential credit loss with measures of credit quality and recovery rates after default.

Insurance Supervision Core Curriculum

�0

The current market value of a derivative is especially misleading as a measure of potential credit exposure. As with cash-market investments, information regarding po-tential credit loss must be combined with measures of credit quality and recovery rates after default to achieve a measure of potential credit risk.

For derivatives, the situation is much more complex, however. The current mar-ket value of a derivative can bear little or no relation to the future market value of the derivative and hence to potential credit loss. A small market value indicates nothing about potential credit risk, since the value of the underlying asset or index can shift unexpectedly.

Moreover, ownership of a derivative may be a liability to the owner rather than an asset. This means that a derivative with a market value of $10 million may represent obligations of the owner to the counterparty, whose market value is $10 million. Such an obligation does not involve any current credit exposure by the derivative owner to the counterparty. Indeed, there is nothing to prevent the same derivative from being a liability at one time and an asset at another, depending on changes in the market value of the underlying cash-market investments.

In a simple case, an insurer might have two offsetting derivatives with the same counterparty, each of whose market value is $10 million. The exposure of the insurer to the counterparty is zero rather than $20 million if the insurer has legally enforce-able netting arrangements with the counterparty. Doing more derivatives with the same counterparty can actually reduce credit risk exposure to that counterparty!

Finally, the potential credit exposure of two otherwise identical derivative portfo-lios can be radically different as a result of differences in the credit-enhancing features built into the derivative contracts. Use of collateral or frequent settlement of amounts owing, third-party guarantees, and termination features can materially reduce credit risk.

diFFerences in credit risk by tyPe oF derivative

Current and potential credit risk varies considerably among different types of deriva-tives. Forward-type contracts involve no, or very little, initial counterparty exposure, since they could be replaced at origin at no, or little, cost. Option-type contracts involve an initial counterparty exposure to the purchaser equal to the option premium. Struc-tured investments have an initial counterparty exposure similar to that of the cash-mar-ket instrument in which the option is embedded.

Forward-type contracts entail bilateral credit risk, since either party may be ex-posed to credit losses depending on movements in the price of the underlying asset or index. Options and floating-rate interest, commodity, and equity swaps entail one-sid-ed credit exposure of the option owner or floating-rate payer to the other counterparty. The potential exposure of a currency or equity swap is many times that of an interest rate swap with the same amount of notional principal.

ICP ��A: Introduction to Derivatives

��

credit exPosure across multiPle derivatives with the same counterParty

Potential aggregate exposure to a counterparty is likely to be considerably less than the sum of the potential exposures to each derivative. Some derivatives may have projected negative values if and only if others have projected positive values and vice versa. For example, the risk of same-term interest rate swaps with the same counterparty, one to pay a fixed rate and another to receive a fixed rate, is offsetting. Some derivatives have peak exposures at different times, as with interest rate swaps with different maturity dates. Price change correlations between derivatives also reduce projected aggregate credit exposure. Thus aggregate credit exposure should be measured on the entire port-folio of derivatives with each counterparty so that positive and negative exposures can be netted appropriately.

The supervisor should understand that current and potential credit exposure, where multiple transactions with the same counterparty are in place, depends on whether pay-ment netting applies on the settlement date and whether closeout netting applies on default or bankruptcy. Legally enforceable contractual netting agreements should be put in place for all derivatives.

Payment netting applies if same-currency payments on the same day are netted so that only one payment is made between the counterparties. If payment netting does not apply, there may be substantial settlement risk. Closeout netting provides that, on de-fault or other termination event, all derivatives are valued and netted and one payment is made between the counterparties to close out all derivative contracts. With a legally en-forceable bilateral closeout netting agreement, one counterparty cannot simultaneously default on derivative contracts under which it must make payments, while demanding payments on contracts under which it is to receive payments. If closeout netting does not apply, then current credit exposure is the sum of all individual positive exposures. If closeout netting applies, then current credit exposure is the sum of all positive and negative exposures. Netting of offsetting exposures to a counterparty is allowed in the Bank for International Settlements measure if contracts are subject to legally binding closeout netting. For more on credit risk for swaps, see Bollier and Sorensen (1994); Simons (1989).

Market risk

Market risk is the risk of loss arising from adverse movements in market prices for vola-tility, interest rates, exchange rates, equity, and commodity values, among others. Price changes of forward-type contracts are similar to price changes in the underlying asset or index, and so their market risk is similar to the market risk of the underlying asset or index. The market risks of option-type contracts are measured by delta, gamma, vega, theta, and rho, as defined in the glossary in appendix II, and their market risk may differ from that of the underlying asset or index.

Insurance Supervision Core Curriculum

��

Liquidity risk

Liquidity risk refers to the inability to unwind a position in an appropriate period of time without a loss of market value. The liquidity of a derivative is closely linked to the volume of transactions and the bid-ask spread of similar transactions. The high liquid-ity and ease of implementation of derivatives such as interest rate swaps make them at-tractive risk management tools. There is no delay in implementation, so unwanted risks can be eliminated immediately. See the subsection on differences in credit risk by type of derivative for a comparison of the liquidity of exchange-traded and over-the-counter derivatives.

A derivative is illiquid if a single dealer, or a limited number of dealers, is prepared to transact or if its size has a material impact on market prices. Wide bid-ask spreads are a reliable indication of illiquidity.

Liquidity risk is of special concern with complex, highly customized, long-dated derivatives and structured investments that have highly volatile prices. Such derivatives can be highly illiquid in abnormal or adverse markets, even if substantial liquidity exists in normal markets. Following a jump in the price or volatility of the underlying asset or index, derivative prices may be subject to discontinuities, prices may exceed their presumed theoretical values, bid-ask spreads may increase substantially, and it may not be possible to transact. The right to unwind such derivatives, and the terms, conditions, and pricing considerations involved in unwinding them, should be negotiated at the time the derivative is purchased. Understanding the cost of disposing of derivatives can be as important as understanding their initial costs.

Effective execution of a derivative strategy that requires “dynamic hedging” or con-tinuous rolling forward of derivatives may be impossible in the event of severe and un-expected changes in liquidity. Sudden market shifts in credit and risk assessments may deprive a company of access to derivative markets, or the availability of derivatives may become much less flexible and much more costly and uncertain. The ability to obtain additional credit support or to access alternative strategies should be considered before relying heavily on such strategies.

Funding risk

Funding risk is the risk that a company will be unable to make payments when due. Net cash flows from derivative portfolios should be projected regularly over short and near terms and under a range of likely and adverse market conditions to forecast the timing and size of net cash payments. Contingency plans should be established to deal with adverse or unexpected demands for cash flow. Collateral agreements requiring the pay-ment or receipt of cash or securities and events that trigger mark-to-market payments or contract termination should be reflected in these projections.

ICP ��A: Introduction to Derivatives

��

Reliance on swaps to manage interest rate risk requires additional vigilance with respect to cash management, since their extensive use can increase cash-flow mis-matches, even where the duration of the portfolios is closely matched. While an interest rate swap to make fixed payments and receive a three-month T-bill rate is equivalent in interest rate sensitivity to selling five-year bonds and holding three-month T-bills, it is not equivalent in cash-flow terms. A portfolio of illiquid five-year bonds (or mort-gages) combined with fixed-pay swaps may have similar interest-rate sensitivity to a portfolio of guaranteed investment contracts (GICs). This means that the market value of the combined bond and swap portfolio changes by amounts similar to changes in the market value of the portfolio of GICs in response to changes in interest rates. However, should a large volume of GICs be cashed out at maturity, there may be no matching-asset cash flows with which to fund the cash-outs. Further, it may not be possible to liquidate the bonds cost-effectively and expeditiously to fund these payments.

Basis or correlation risk

Basis or correlation risk arises because derivatives are not available on the precise underlying asset required for risk management. The efficacy of the risk management strategy depends on the extent of the correlation between changes in the value of the derivative and the market exposure being managed. If the value of the derivative and that of the managed position do not change in lockstep, because they are not perfectly correlated, the derivative may not satisfy the objectives of risk management. There is also the risk that the extent of correlation will change adversely. This risk of loss is called basis or correlation risk. This risk can be substantial, depending on the price volatility of the managed risk, the price volatility of the derivative, the correlation of their prices, the term of the derivative, and the factors causing the correlation.

A future on a bond or stock index might be sold to manage excess exposure on a bond or stock portfolio, respectively, even though portfolio returns do not exactly replicate index returns. Basis risk from a futures position may involve no more than the potential widening or narrowing of fixed-income spreads between different fixed-in-come investments, different sectors, or different points on the yield curve. Risk manage-ment based on no more than “accidental,” historical correlations between the changes in value of the derivative and the risk being managed can be a form of speculation. In the absence of market inefficiencies, genuine risk management should provide no free lunches.

Operational risk

Operational risk is the potential for incurring material, unexpected losses due to inad-equate supervision and understanding on the part of management, systems, controls,

Insurance Supervision Core Curriculum

��

procedures, accounting, and reporting as well as errors. For the end user, the first step in managing operational risk arising from derivative activities is to integrate the man-agement oversight, control processes, risk measurement, management, and reporting of derivatives with those of cash-market investments. The complexity, diversity, and novelty of derivatives may lead to greater operational risks than cash-market invest-ments, in which case management oversight, control processes, and so forth may need to be strengthened.

Legal risk

To limit legal risks, legal counsel should be involved in developing policies and proce-dures to manage and limit legal risks and reviewing all arrangements, contracts, and addenda signed by the company. Care should be taken to ensure that payment and closeout netting and credit-enhancing features are legally enforceable. Contracts should be documented carefully and correctly.

A contract may not be valid because counterparties, such as local government authorities, pension plans, and mutual funds, may not have the authority to transact. Counterparty authorities might constrain the use of derivatives to particular uses only (for example, hedging or debt management). A contract might be unenforceable be-cause there was no authority to enter into it for the purpose to which it was put. There can be restrictions on the ability of certain counterparties to pledge collateral. In some countries, derivative contracts are not enforceable because they are classified as gam-bling activities.

The enforceability of multi-branch, cross-border closeout netting arrangements is especially unclear. Bankruptcy codes may suspend the contractual rights of secured creditors to foreclosure and setoff in bankruptcies and may provide for the “clawback” of property transferred within a certain period prior to the bankruptcy filing. Banks may be restricted in their ability to provide security for obligations, including deriva-tives.

Failure to act honestly and in good faith creates a risk that a market maker will lose existing clients and the ability to compete effectively for new clients. Moreover, legal li-ability may arise in any situation where a certain type of derivative is determined to be unsuitable for a client or a client’s accounts.

Accounting, tax, and regulatory risks

Accounting, tax, and regulatory issues may obstruct the effective use of derivatives. There can be uncertainty pertaining to the regulatory, accounting, and tax treatment of derivatives used in different ways. Inconsistencies between regulatory, accounting, and tax treatments of derivatives and the positions they “hedge” can create difficulties.

ICP ��A: Introduction to Derivatives

��

There may also be substantial risk of loss from changes in regulatory, tax, or accounting requirements or from unexpected interpretations or applications of existing require-ments. The full regulatory, accounting, and tax implications need to be examined prior to transacting.

Valuation risks associated with models

Supervisors need to understand that the ability to value derivatives in an objective and independent fashion is fundamental to prudent management of derivative risks for in-surers.

ICP 22, essential criterion g, states, “The supervisory authority requires that insur-ers have in place personnel with appropriate skills to vet models used by the front office and to price the instruments used and that pricing follows market convention.”

Reliance on internally developed models should be tempered by regular reality checks with the marketplace. Proprietary black boxes available from consultants may or may not produce more reliable prices, but they bring with them concerns that the consultant may have oversold the model and that the failure to understand the model fully may contribute to its misuse.

Unless justified by a well-understood cost-benefit analysis, end users should prefer cash-market alternatives to derivatives and simple derivatives to complex, innovative, and difficult-to-model derivatives. The time and effort required to model potential risk-return trade-offs of a derivative across a range of likely and unlikely market scenarios could be substantial. Developing the capability to price derivatives can be daunting, both intellectually and from a systems perspective. However, this effort is essential to ensure effective and prudent use of derivatives.

Supervisors should understand that derivative valuations are subject to risks, in-cluding fraud, foolhardiness, errors, lack of expertise and understanding, and limi-tations of the model used. They should be concerned about the independence of the derivative valuation function from those affected by valuations. For market makers, in-centive compensation makes the prospect of fraud a serious issue. For end users, fraud may arise in an attempt to cover up errors or to overstate hedging or risk management results. Several large derivative losses have involved fraud, ranging from cover-ups to more subtle forms such as using volatility and other inputs to produce above- or below-market prices. Short of outright fraud, there is room to calibrate models aggressively and to exercise judgment.

Models are prone to programming error and may involve unproven computer and information systems. Models may be relatively new and unseasoned, or they may be subjected to continuous “tinkering.” They may not yet have been subjected to vigorous audits, independent reviews, or systematic testing designed to uncover material errors. For these reasons, models should always be subjected to independent validation, both initially and periodically.

Insurance Supervision Core Curriculum

��

Models and derivative strategies based on them rely on simplified assumptions about markets: the continuous ability to measure risks based on market prices and vola-tilities and to trade in any volume at fair-market prices without price or volatility gaps. However, prices, volatilities, and bid-ask spreads can and do gap, and it is not always possible to transact, or at least to transact at what would normally pass for fair-market prices or presumed theoretical values. A number of unanticipated, model-based deriva-tive losses have been caused when a gap suddenly emerged between model and market pricing. Such gaps may result from simplistic assumptions, flaws in the model, or other causes whose importance only becomes apparent in abnormal markets.

Supervisors should understand that there is always some risk in using a model to derive an unknown price from a set of known prices, because the “extrapolated” price depends on such things as the choice of model, methodology, assumptions, sto-chastic process, and method of calibration. Derivative pricing models are market-con-sistent—that is, they are calibrated to replicate quoted market prices of specific assets and derivatives. In the absence of fraud, the risk that standard derivatives will be ma-terially mispriced is small, especially if the model is calibrated carefully and validated frequently. However, the risk that “market-consistent” models will price derivatives ma-terially differently increases the greater the difference between the instruments used to calibrate the model and the derivatives priced. Specifically, the accurate valuation of nonstandard derivatives may require the use of complex models, where model risk may be significant. When the pricing models of major derivative dealers are used to price complex or unusual derivatives, prices can differ materially.

It can be simplistic to speak of “market-consistent” pricing of complex, long-dated options embedded in insurance products that cannot be replicated by derivatives avail-able in the market. Here, market-consistent means no more than that a market-con-sistent model was used to do the pricing. If nothing similar to what is being priced is available in the market, then the extrapolated prices are not validated by the market.

Parameter values can change materially over time due to changing market condi-tions. Therefore, models should be validated and recalibrated regularly by comparing model values to quoted market prices. Some material derivative losses have been due to foolhardy reliance on model-based valuations in the face of lower market-based valu-ations that were presumed to be temporary aberrations but were, in fact, permanent adjustments to market forces.

No one model is likely to price all derivative instruments in all circumstances with a uniformly high degree of precision. The model may be fundamentally flawed, or it may have been pushed to value instruments beyond the point where it has validity. The ability to value derivatives using more than one model is a valuable check.

Sometimes end users use derivative valuation models for purposes other than pric-ing, such as to analyze projected future values, asset-liability management, and stress testing. For these purposes, models may be calibrated to historical experience. Param-eter values based on different historical periods can differ markedly. The values may have been selected to produce desired results or may have been derived from a period

ICP ��A: Introduction to Derivatives

��

that is too short or a period that is distorted by business and economic cycles or by po-litical and geopolitical events.