ICICI Group: Performance & Strategy November 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ICICI Group: Performance

& Strategy

November 2014

2

Certain statements in these slides are forward-looking statements.

These statements are based on management's current expectations and

are subject to uncertainty and changes in circumstances. Actual results

may differ materially from those included in these statements due to a

variety of factors. More information about these factors is contained in

ICICI Bank's filings with the US Securities and Exchange Commission.

All financial and other information in these slides, other than financial

and other information for specific subsidiaries where specifically

mentioned, is on an unconsolidated basis for ICICI Bank Limited only

unless specifically stated to be on a consolidated basis for ICICI Bank

Limited and its subsidiaries. Please also refer to the statement of

unconsolidated, consolidated and segmental results required by Indian

regulations that has, along with these slides, been filed with the stock

exchanges in India where ICICI Bank’s equity shares are listed and with

the New York Stock Exchange and the US Securities and Exchange

Commission, and is available on our website www.icicibank.com

3

Agenda

Performance highlights

Strategy & outlook

4

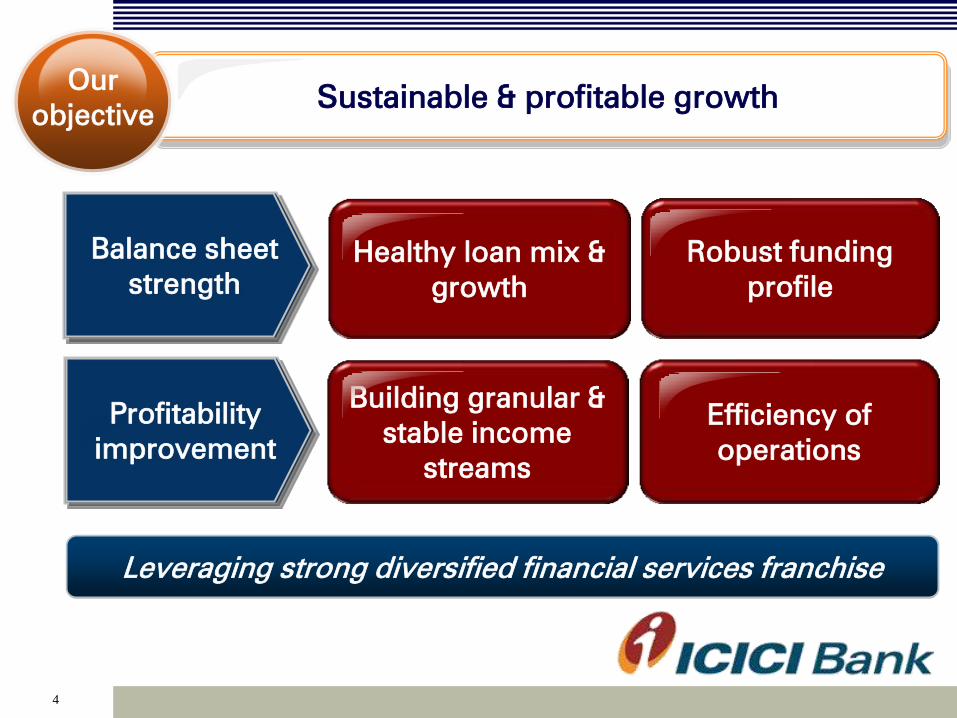

Healthy loan mix &

growth

Robust funding

profile

Building granular &

stable income

streams

Efficiency of

operations

Sustainable & profitable growth Our

objective

Profitability

improvement

Balance sheet

strength

Leveraging strong diversified financial services franchise

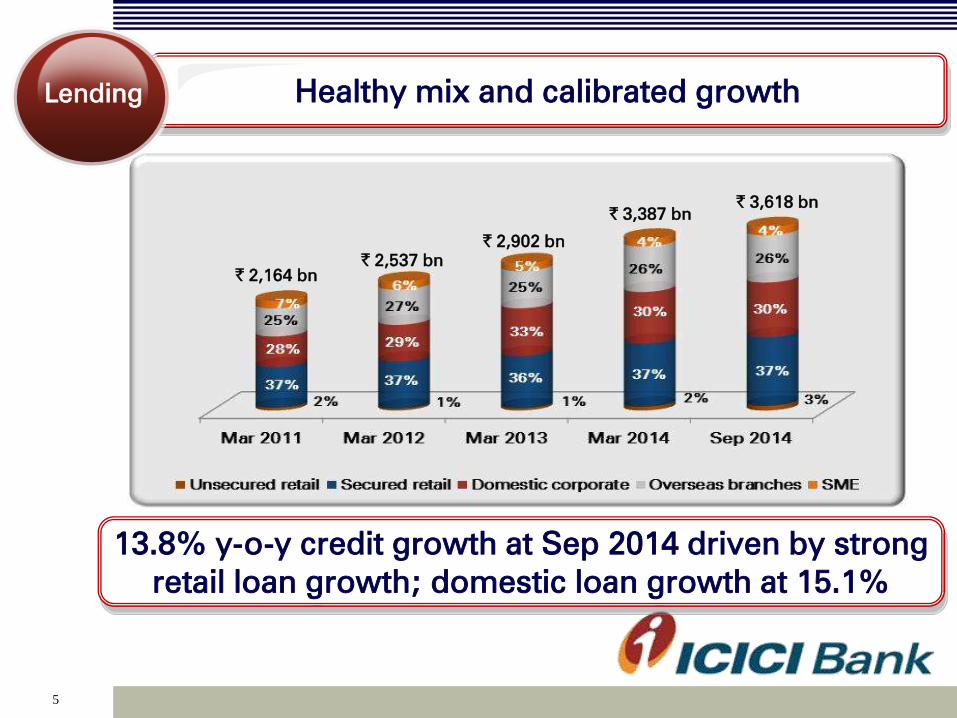

Healthy mix and calibrated growth

13.8% y-o-y credit growth at Sep 2014 driven by strong

retail loan growth; domestic loan growth at 15.1%

5

Lending

` 2,164 bn ` 2,537 bn

` 2,902 bn

` 3,387 bn ` 3,618 bn

Along with healthy growth in rural loans

Secured lending driving 20%+ portfolio growth

6

Retail

lending

Sep 2013 Sep 2014

Home loans

Auto loans

Sep 2013 Sep 2014

Business banking

Sep 2013 Sep 2014

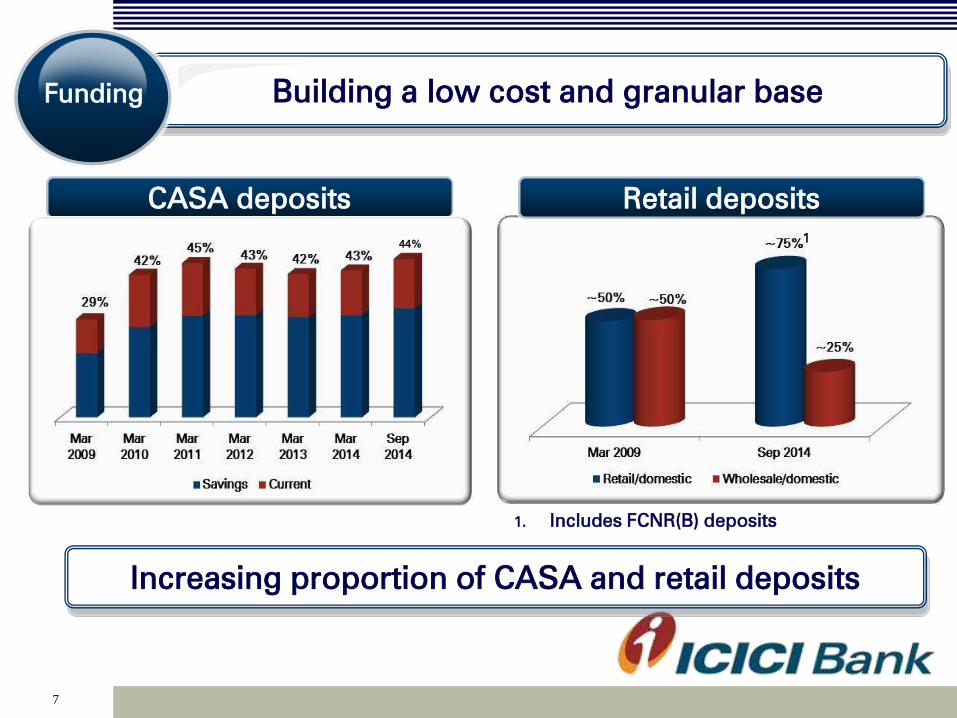

Building a low cost and granular base Funding

Increasing proportion of CASA and retail deposits

7

CASA deposits Retail deposits

1

1. Includes FCNR(B) deposits

44%

8

Growth driven by retail deposit franchise Funding

Sep 2013 Sep 2014

CASA deposits

Retail deposits

Sep 2013 Sep 2014

Driven by continued investments in physical and

technological infrastructure

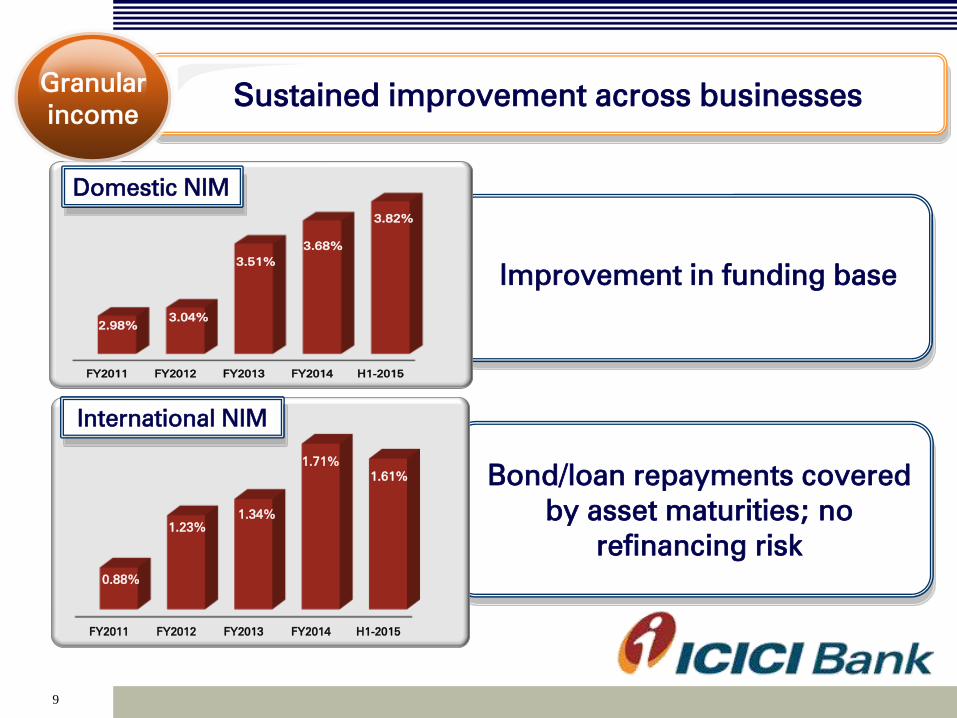

Bond/loan repayments covered

by asset maturities; no

refinancing risk

FY2011 FY2012 FY2013 FY2014 H1-2015

0.88%

1.23%

1.34%

1.71%

1.61%

Improvement in funding base

FY2011 FY2012 FY2013 FY2014 H1-2015

2.98%

3.04%

3.51%

3.68%

3.82%

9

Sustained improvement across businesses Granular

income

Domestic NIM

International NIM

Driven by profit and

margin focus across

domestic and international

businesses

FY2011 FY2012 FY2013 FY2014 H1-2015

2.64%

2.73%

3.11%

3.33%

3.41%

10

Substantial increase in NIMs Granular

income

~77 bps improvement in overall NIM since FY2011

Overall NIM

11

Granular

income

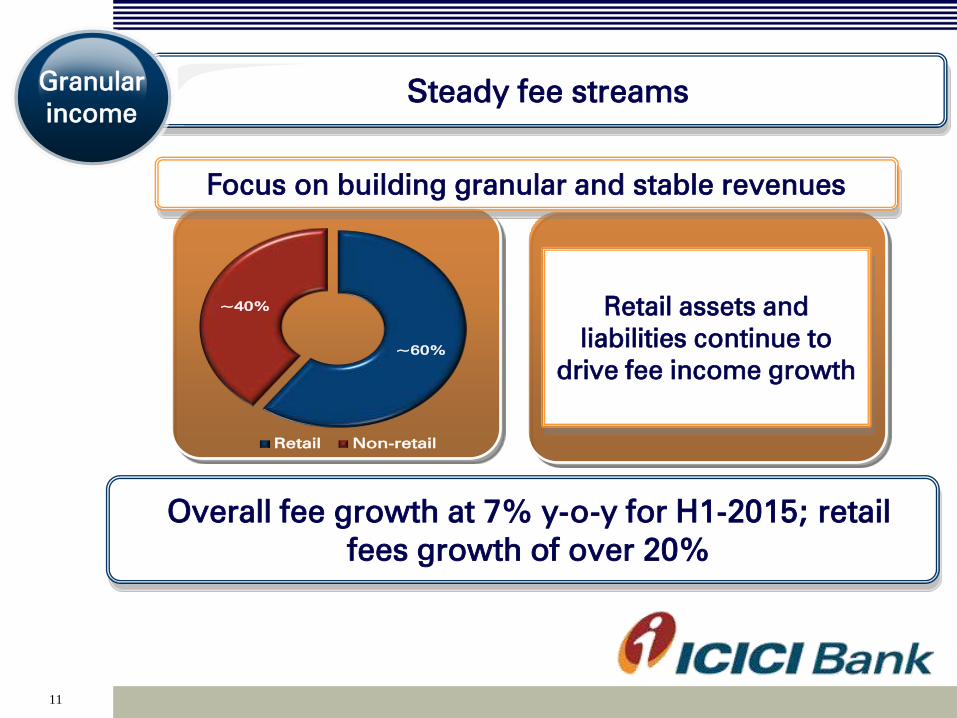

Steady fee streams Granular

income

Overall fee growth at 7% y-o-y for H1-2015; retail

fees growth of over 20%

Focus on building granular and stable revenues

Retail assets and

liabilities continue to

drive fee income growth

~60%

~40%

Retail Non-retail

Diversified financial services

franchise yielding high returns

12

Strong dividend income Granular

income

FY2010 FY2014 FY2013

Contributing to increase in non-interest income

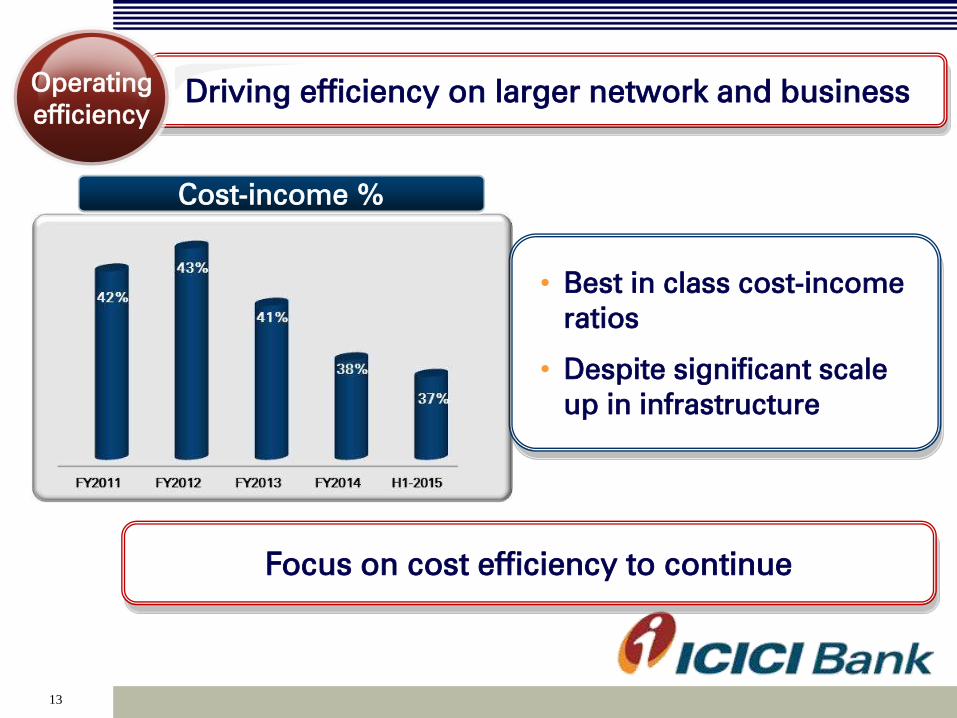

• Best in class cost-income

ratios

• Despite significant scale

up in infrastructure

13

Driving efficiency on larger network and business Operating

efficiency

Focus on cost efficiency to continue

Cost-income %

14

Asset quality impacted by operating environment Asset

quality

Net NPA ratio

• Net restructured loans at

` 110.20 billion at

September 30, 2014

• Provisions to average

loans at 91 bps in H1-

2015

Asset quality reflecting impact of slowdown in economy on SME

& corporate loans

Healthy growth in operating profits giving the ability to absorb

impact of higher credit costs

About 80 bps improvement

over FY2009

15

Consistent delivery against stated objectives Return

profile

Standalone RoA

1.66%

FY2013

1.76%

FY2014

1. annualised

1.82%

H1-20151

<1.0%

FY2009

16

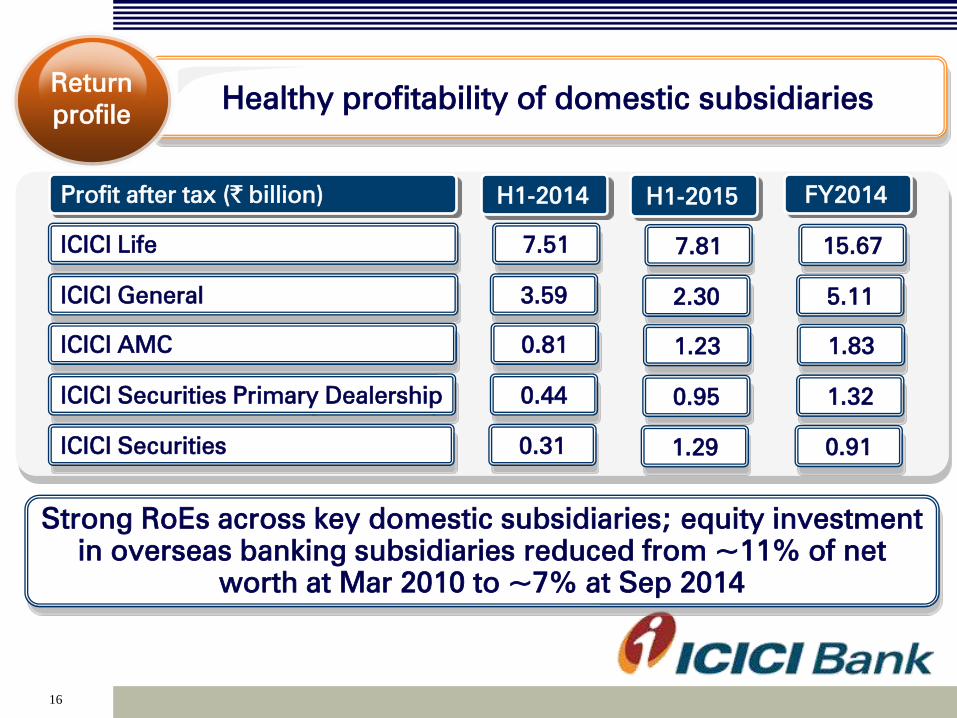

Healthy profitability of domestic subsidiaries Return

profile

15.67 ICICI Life

H1-2014

7.51

H1-2015

7.81

FY2014 Profit after tax (` billion)

5.11 ICICI General

3.59 2.30

1.83 ICICI AMC

0.81 1.23

1.32 ICICI Securities Primary Dealership

0.44 0.95

0.91 ICICI Securities

0.31 1.29

Strong RoEs across key domestic subsidiaries; equity investment

in overseas banking subsidiaries reduced from ~11% of net

worth at Mar 2010 to ~7% at Sep 2014

Near doubling of

consolidated RoE since

FY2009

17

Sustained consolidated returns Return

profile

Consolidated RoE

<8.0%

FY2009

14.7%

FY2013 14.9%

FY2014

1. annualised

14.9%

H1-20151

18

Agenda

Performance highlights

Strategy & outlook

19

Investments in

distribution

network

•Largest branch network among private

sector banks supplemented with large

ATM network

•Leadership in leveraging technology

Strong capital

position

Strong capital base with CAR of 17.41%1

with Tier 1 ratio of 12.75%1 at September

30, 2014

Diversified

business lines

Continued focus on sustaining and

enhancing franchise across financial

service businesses

Well positioned for recovery in

economic activity

Key

strengths

1. Including profits for H1-2015

20

Strong franchise across segments (1/2)

Diversified

business

lines

• Leadership among private sector players

• Focus on strengthening franchise and profitability

• Renewed growth momentum

• Leadership among private sector players

• Healthy profitability

• Largest private sector bank in India

• Continued focus on enhancing retail franchise;

investing in semi-urban & rural markets

• Well established corporate franchise along with

overseas presence

21

• Increase in market share in broking

• Improvement in market conditions favourable for

business outlook

• Improved market position to second largest mutual

fund in India in terms of overall AUM

• Strong fund performance

Strong franchise across segments (2/2)

Diversified

business

lines

22

Significant scale up in branch & ATM network

•Network of 3,815 at Sep 2014;

largest in private sector banks

• Supplemented by ~11,700

ATMs

•Largest rural branch network

among private sector banks

• ~75% of branch additions

since March 2012 in rural and

semi-urban areas

Branch network

Investments in

distribution

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Sep-14

Metro Urban Semi Urban Rural

1,707

2,529

2,752

3,100

3,753 3,815

Supported by continued leadership

in technology platforms

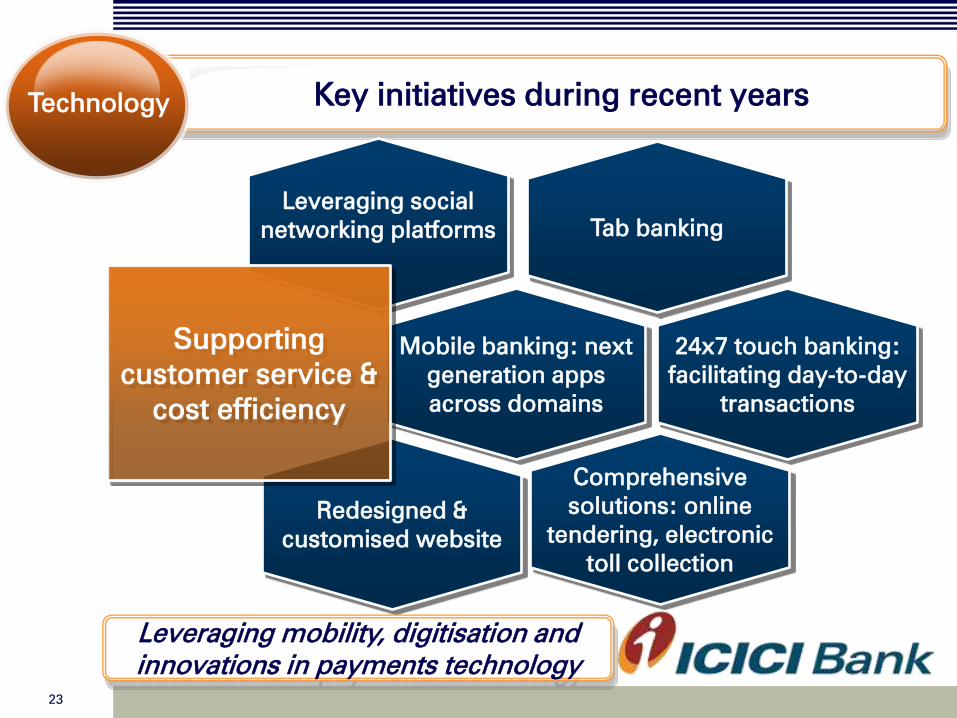

Key initiatives during recent years

23

Technology

Tab banking

Mobile banking: next

generation apps

across domains

24x7 touch banking:

facilitating day-to-day

transactions

Comprehensive

solutions: online

tendering, electronic

toll collection

Leveraging social

networking platforms

Redesigned &

customised website

Supporting

customer service &

cost efficiency

Leveraging mobility, digitisation and

innovations in payments technology

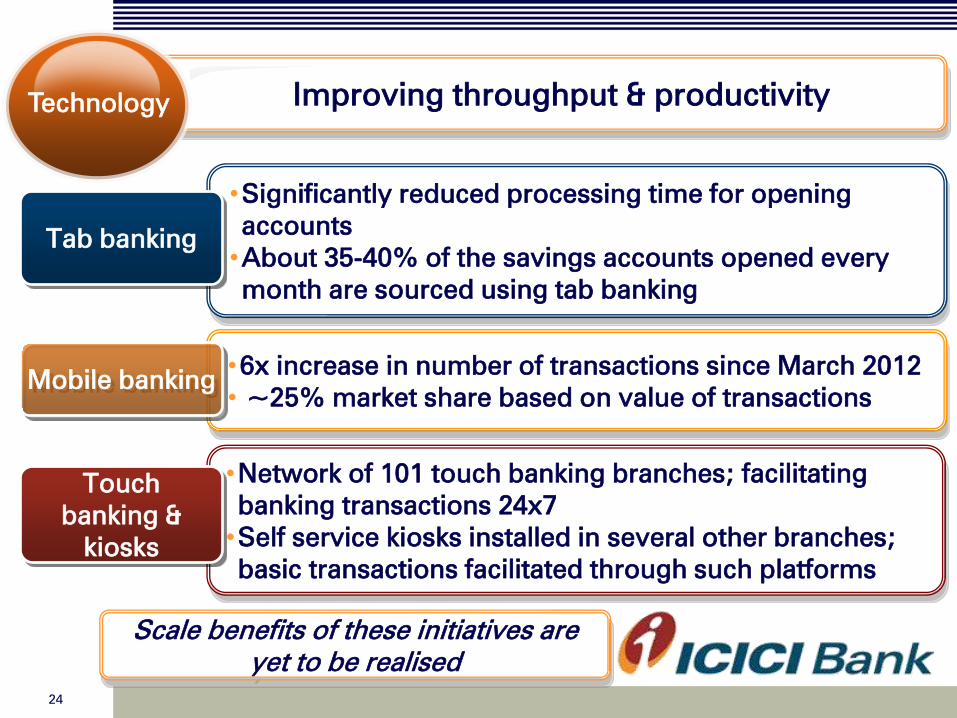

Improving throughput & productivity

24

Technology

•Network of 101 touch banking branches; facilitating

banking transactions 24x7

•Self service kiosks installed in several other branches;

basic transactions facilitated through such platforms

•6x increase in number of transactions since March 2012

• ~25% market share based on value of transactions

Mobile banking

Touch

banking &

kiosks

•Significantly reduced processing time for opening

accounts

•About 35-40% of the savings accounts opened every

month are sourced using tab banking

Tab banking

Scale benefits of these initiatives are

yet to be realised

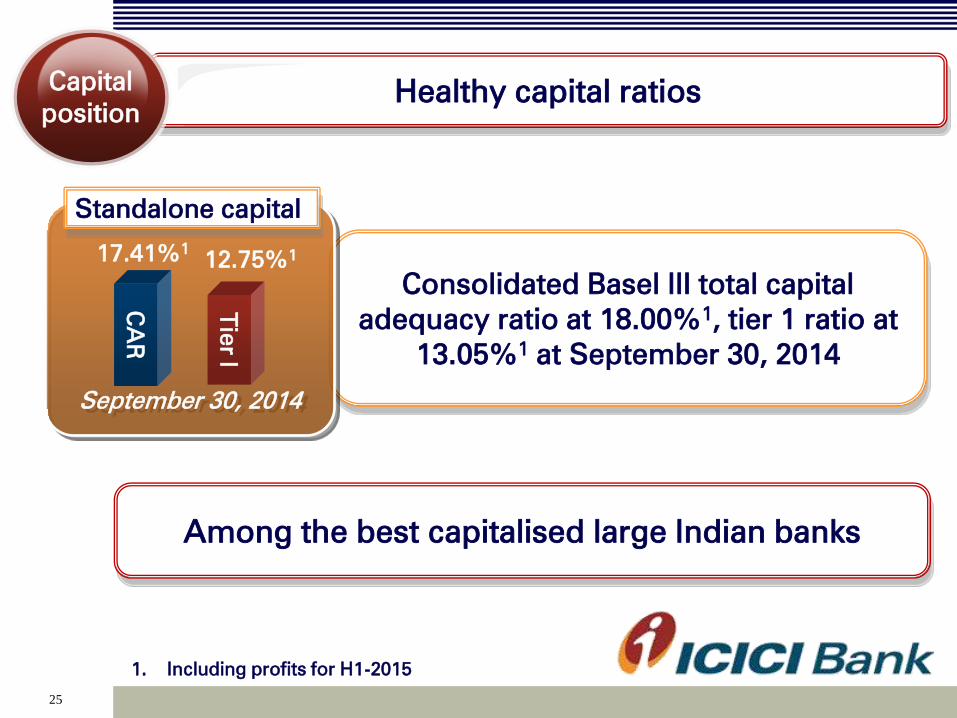

Consolidated Basel III total capital

adequacy ratio at 18.00%1, tier 1 ratio at

13.05%1 at September 30, 2014

25

Healthy capital ratios Capital

position

Among the best capitalised large Indian banks

September 30, 2014

Tier I

CA

R

17.41%1

12.75%1

Standalone capital

1. Including profits for H1-2015

26

Key priorities going forward

27

Key priorities Our

approach

We are targeting credit growth with focus on selected

areas; retail lending to be a key driver

We will continue to support this growth with a robust

funding profile

We will continue to focus on productivity & operating

efficiency as a profitability driver

28

Targeting healthy growth and mix Lending

Retail portfolio to continue to be the key driver for

growth

Growth in corporate (including overseas branches) &

SME portfolios to be calibrated to the environment

Targeting 2-4% higher than system domestic loan

growth

29

• Sustaining momentum in disbursements Home

loans

•Significant geographic expansion achieved;

focus on improving profitability

Auto

loans

•Moderate growth given economic scenario CV

•Growth off low base with close monitoring of

asset quality trends; Significant proportion of

incremental lending to existing customers

Unsecured

loans

Focus on traditional segments to continue Retail

assets

30

New growth areas Retail

assets

• Small value and well collateralised lending to small

businesses

• Closely linked to current account deposits

• Building granular and diversified portfolio while

maintaining focus on portfolio asset quality

• Leveraging increase in geographical presence and larger

distribution to increase volumes

Small business loans

Rural markets

31

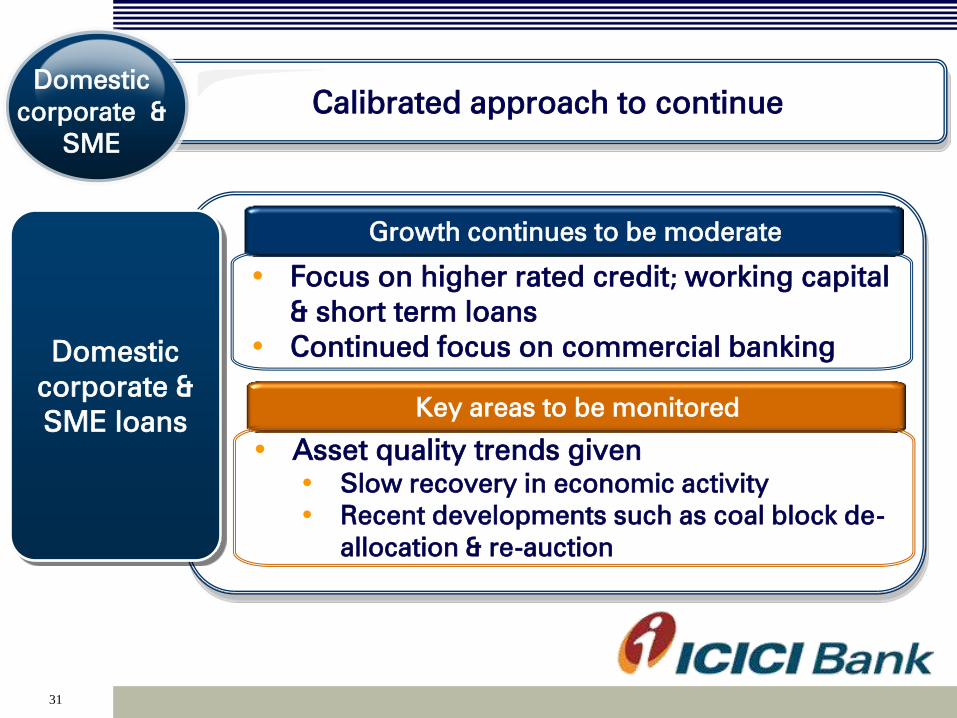

Domestic

corporate &

SME loans

Calibrated approach to continue

Domestic

corporate &

SME

Key areas to be monitored

• Asset quality trends given

• Slow recovery in economic activity

• Recent developments such as coal block de-

allocation & re-auction

Growth continues to be moderate

• Focus on higher rated credit; working capital

& short term loans

• Continued focus on commercial banking

32

•Growth calibrated to global funding

markets & Indian corporate credit demand

•Focus on commercial banking, including

working capital facilities for Indian

companies abroad and MNCs engaged in

trade with India

Branches

Lending primarily

to Indian

corporates

•Continued focus on optimising capital

•Focus on short term loans, working

capital lines, trade & transaction banking

products to MNCs, select local market

corporates & Indian companies abroad

Subsidiaries

•Regulatory

expectations

impacting

business model

•High capital levels

Focus on profitability and returns International

business

33

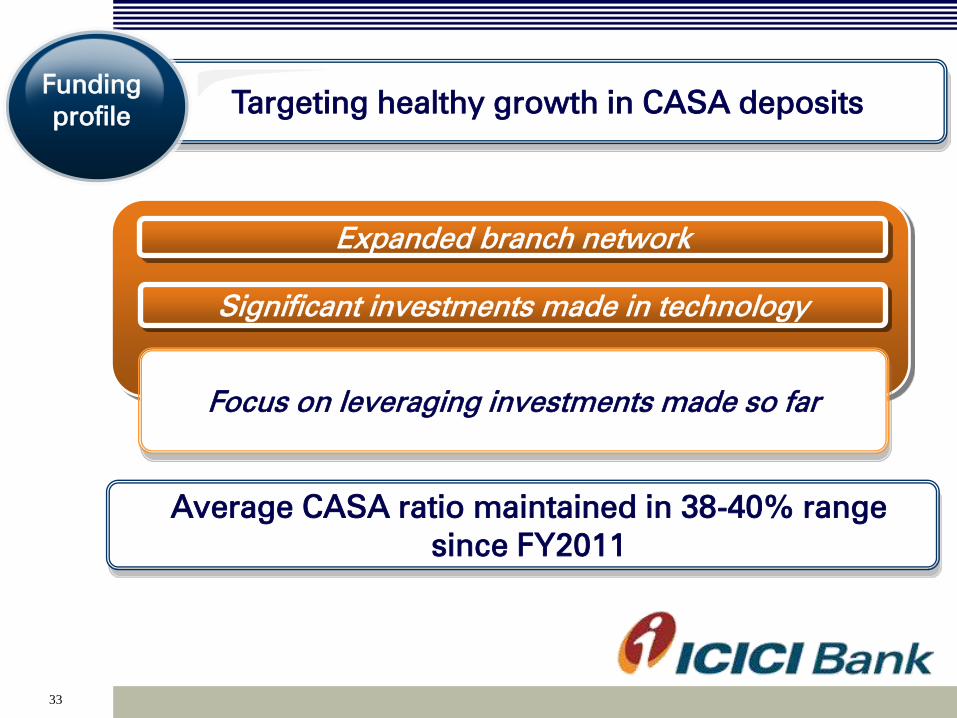

Targeting healthy growth in CASA deposits Funding

profile

Focus on leveraging investments made so far

Expanded branch network

Significant investments made in technology

Average CASA ratio maintained in 38-40% range

since FY2011

34

Sustained focus on strengthening franchise In

summary

2009 onwards

Driving

structural

improvements

Outlook going forward

Achieved

significant

improvement in

balance sheet &

operating

parameters Well-positioned

for economic

recovery

Focus on

profitable credit

growth;

enhancing

franchise

2011 onwards

Scaled up retail

business; continued

investments in

distribution &

technology

Focus on sustaining

profitability metrics

& leveraging growth

opportunities

35

Thank you

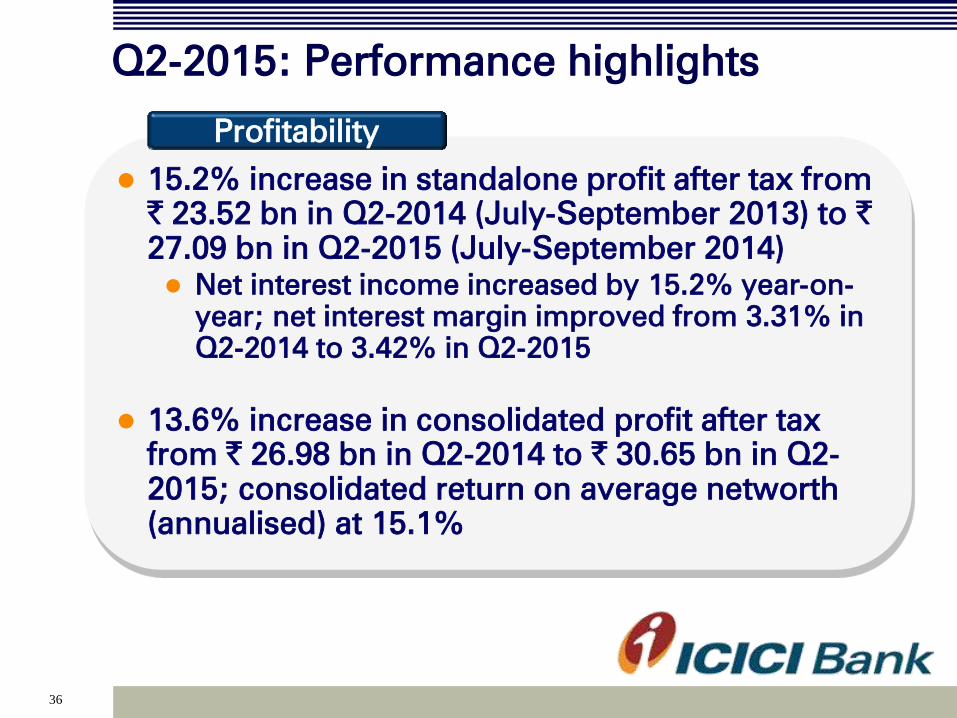

Q2-2015: Performance highlights

36

15.2% increase in standalone profit after tax from

` 23.52 bn in Q2-2014 (July-September 2013) to `

27.09 bn in Q2-2015 (July-September 2014)

Net interest income increased by 15.2% year-on-

year; net interest margin improved from 3.31% in

Q2-2014 to 3.42% in Q2-2015

13.6% increase in consolidated profit after tax

from ` 26.98 bn in Q2-2014 to ` 30.65 bn in Q2-

2015; consolidated return on average networth

(annualised) at 15.1%

Profitability

37

Advances increased by 13.8% year-on-year to `

3,617.57 billion at September 30, 2014

Retail advances growth at 25.2% year-on-year at

September 30, 2014

Period end CASA ratio at 43.7% at September

30, 2014 compared to 43.3% at September 30,

2013 and 43.0% at June 30, 2014

Average CASA ratio stable at 39.5% for Q2-2015

Net NPA ratio at 0.96% at September 30, 2014

(June 30, 2014: 0.87%; September 30, 2013:

0.73%)

Balance sheet

Q2-2015: Performance highlights

38

Standalone results

39

Profit & loss statement

1. Includes ` 2.22 billion, ` 1.03 billion and ` 1.65 billion of exchange rate gains on

repatriation of retained earnings from overseas branches in FY2014, Q1-2015 and Q2-

2015 respectively

NII

Non-interest income

- Fee income

- Other income

- Treasury income

Total income

Operating expenses

Operating profit

` billion

164.75 40.44 78.64 44.92 46.57 91.49 15.2%

104.28 21.66 46.51 28.50 27.38 55.88 26.4%

77.58 19.94 37.87 19.36 21.03 40.39 5.5%

16.531

2.51 5.40 5.261

4.981

10.24 98.4%

10.17 (0.79) 3.24 3.88 1.37 5.25 -

269.03 62.10 125.15 73.42 73.95 147.37 19.1%

103.09 23.22 48.13 28.25 26.97 55.22 16.1%

165.94 38.88 77.02 45.17 46.98 92.15 20.8%

FY

2014

Q2-

2014

H1-

2014

Q1-

2015

Q2-

2015

H1-

2015

Q2-o-Q2

growth

40

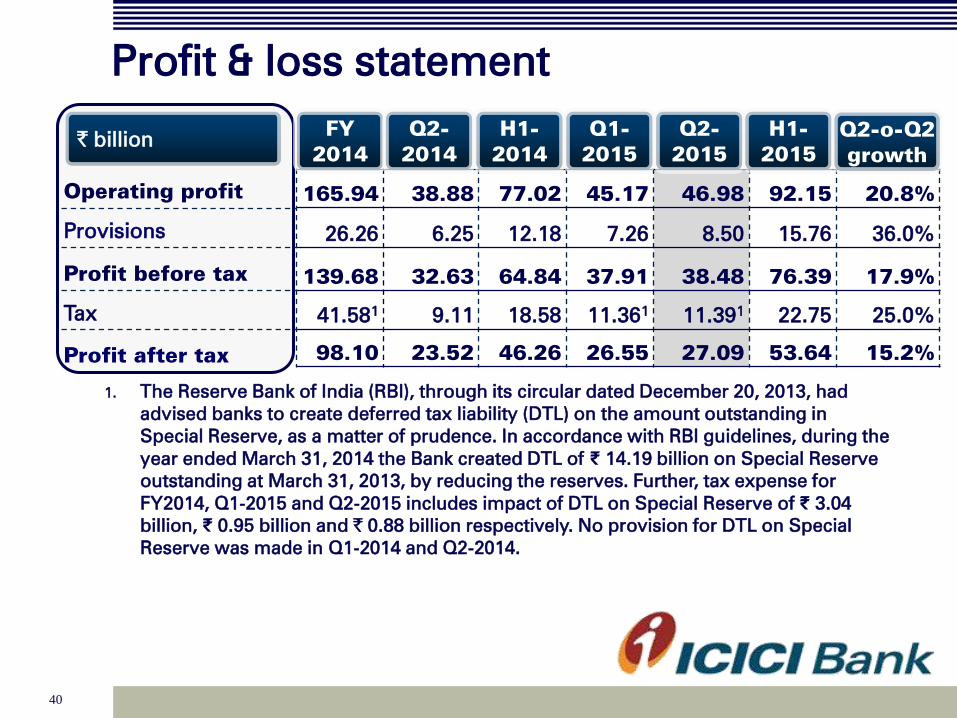

Profit & loss statement

1. The Reserve Bank of India (RBI), through its circular dated December 20, 2013, had

advised banks to create deferred tax liability (DTL) on the amount outstanding in

Special Reserve, as a matter of prudence. In accordance with RBI guidelines, during the

year ended March 31, 2014 the Bank created DTL of ₹ 14.19 billion on Special Reserve

outstanding at March 31, 2013, by reducing the reserves. Further, tax expense for

FY2014, Q1-2015 and Q2-2015 includes impact of DTL on Special Reserve of ₹ 3.04

billion, ₹ 0.95 billion and ` 0.88 billion respectively. No provision for DTL on Special

Reserve was made in Q1-2014 and Q2-2014.

Operating profit

Provisions

Profit before tax

Tax

Profit after tax

` billion

165.94 38.88 77.02 45.17 46.98 92.15 20.8%

26.26 6.25 12.18 7.26 8.50 15.76 36.0%

139.68 32.63 64.84 37.91 38.48 76.39 17.9%

41.581

9.11 18.58 11.361

11.391

22.75 25.0%

98.10 23.52 46.26 26.55 27.09 53.64 15.2%

FY

2014

Q2-

2014

H1-

2014

Q1-

2015

Q2-

2015

H1-

2015

Q2-o-Q2

growth

41

Key ratios

Yield on total interest earning

assets1

Cost of funds1

Net interest margin1

Movement in yield, costs &

margins (Percent)

Return on average networth1

Return on average assets1

Weighted average EPS1

Book value (`)

Fee to income

Cost to income

Average CASA ratio

Percent

8.92 8.86 8.89 8.90 8.93 8.92

6.21 6.13 6.22 6.19 6.16 6.18

3.33 3.31 3.29 3.40 3.42 3.41

FY

2014

Q2-

2014

H1-

2014

Q1-

2015

Q2-

2015

H1-

2015

13.7 13.0 13.2 14.3 13.9 14.1

1.76 1.70 1.72 1.82 1.82 1.82

85.0 80.8 80.0 92.2 92.9 92.6

634 633 633 657 682 682

28.9 32.1 30.3 26.4 28.4 27.4

38.2 37.3 38.4 38.4 36.5 37.5

39.4 40.3 39.6 39.5 39.5 39.5

FY

2014

Q2-

2014

H1-

2014

Q1-

2015

Q2-

2015

H1-

2015

1. Annualised for all interim periods

42

Balance sheet: Assets

Cash & bank balances

Investments

- SLR investments

- Equity investment in

subsidiaries

- RIDF and related

Advances

Fixed & other assets

Total assets

` billion

335.81 422.01 473.78 41.1%

1,688.29 1,701.53 1,735.91 2.8%

986.20 967.40 997.25 1.1%

120.23 120.23 120.23 -

229.40 241.20 240.89 5.0%

3,177.86 3,470.67 3,617.57 13.8%

433.12 289.34 284.17 (34.4)%

5,635.08 5,883.55 6,111.43 8.5%

September

30, 2013

June 30,

2014

September

30, 2014

Y-o-Y

growth

Net investment in security receipts of asset reconstruction companies

was ` 7.77 bn at September 30, 2014 (June 30, 2014: ` 9.25 bn)

1. Rural Infrastructure Development Fund

2. Including impact of exchange rate movement

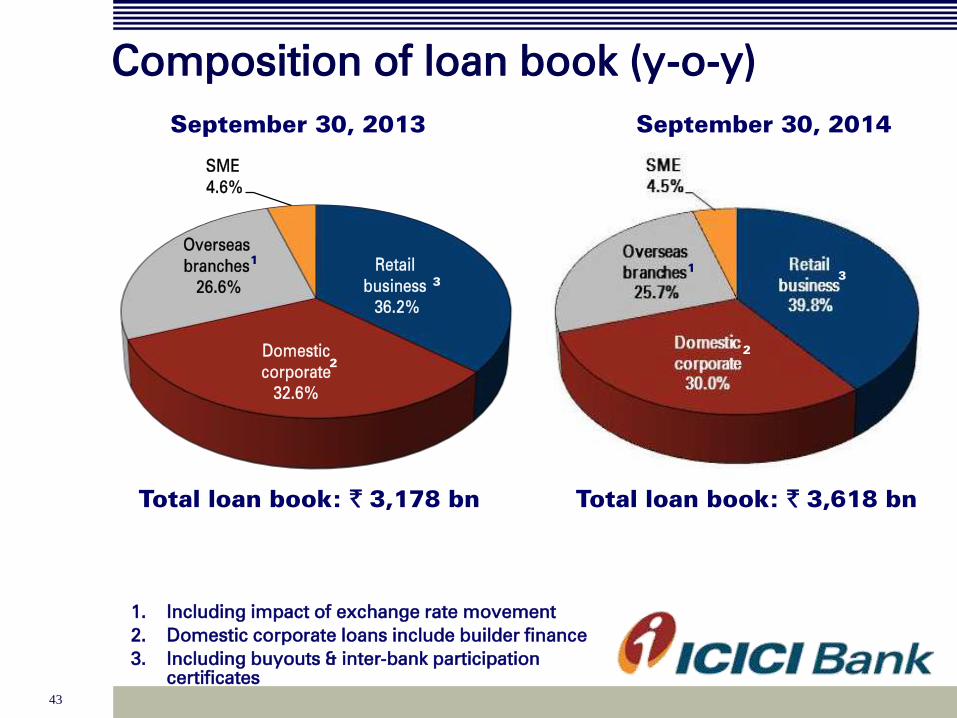

Retail

business

36.2%

Domestic

corporate

32.6%

Overseas

branches

26.6%

SME

4.6%

43

Composition of loan book (y-o-y)

September 30, 2014

Total loan book: ` 3,618 bn Total loan book: ` 3,178 bn

September 30, 2013

1. Including impact of exchange rate movement

2. Domestic corporate loans include builder finance

3. Including buyouts & inter-bank participation

certificates

1

2

3

1

2

3

44

Composition of retail loan book (y-o-y)

September 30, 2014

Total retail loan book: ` 1,441 bn Total retail loan book: ` 1,151 bn

September 30, 2013

• Total retail advances growth of 25.2%

1. September 30, 2013 :Vehicle loans includes auto

loans 10.5%, commercial business 11.7%

2. September 30, 2014: Vehicle loans includes auto

loans 11.6%, commercial business 7.7%

1 2

45

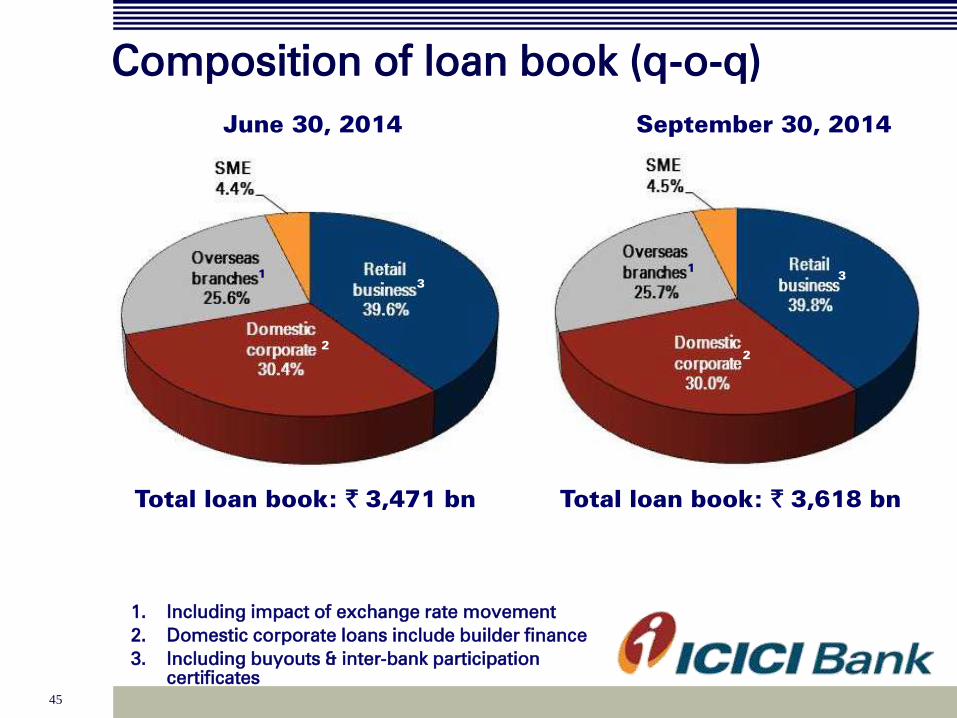

Composition of loan book (q-o-q)

Total loan book: ` 3,471 bn

June 30, 2014

1. Including impact of exchange rate movement

2. Domestic corporate loans include builder finance

3. Including buyouts & inter-bank participation

certificates

1

2

3

September 30, 2014

Total loan book: ` 3,618 bn

1

2

3

46

Composition of retail loan book (q-o-q)

Total retail loan book: ` 1,372 bn

June 30, 2014

1. June 30, 2014 :Vehicle loans includes auto loans

11.8%, commercial business 8.5%

2. September 30, 2014: Vehicle loans includes auto

loans 11.6%, commercial business 7.7%

1

September 30, 2014

Total retail loan book: ` 1,441 bn

2

47

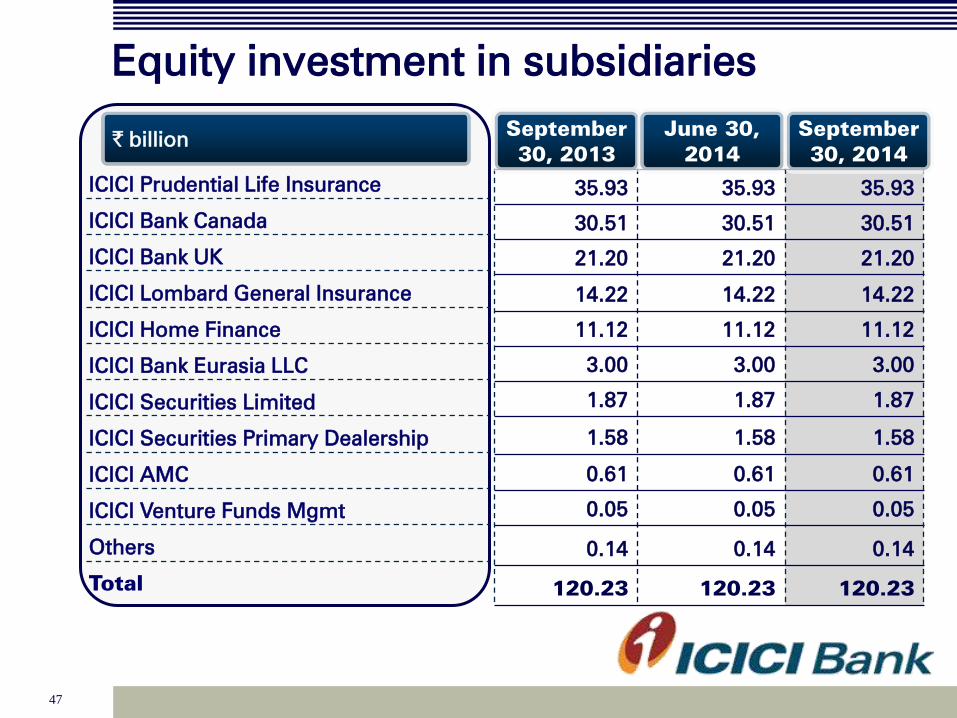

Equity investment in subsidiaries

ICICI Prudential Life Insurance

ICICI Bank Canada

ICICI Bank UK

ICICI Lombard General Insurance

ICICI Home Finance

ICICI Bank Eurasia LLC

ICICI Securities Limited

ICICI Securities Primary Dealership

ICICI AMC

ICICI Venture Funds Mgmt

Others

Total

` billion

35.93 35.93 35.93

30.51 30.51 30.51

21.20 21.20 21.20

14.22 14.22 14.22

11.12 11.12 11.12

3.00 3.00 3.00

1.87 1.87 1.87

1.58 1.58 1.58

0.61 0.61 0.61

0.05 0.05 0.05

0.14 0.14 0.14

120.23 120.23 120.23

September

30, 2013

June 30,

2014

September

30, 2014

48

Balance sheet: Liabilities

Net worth

- Equity capital

- Reserves1

Deposits

- Savings

- Current

Borrowings2,3

Other liabilities

Total liabilities

` billion

731.03 758.99 788.77 7.9%

11.54 11.56 11.57 0.3%

719.49 747.43 777.20 8.0%

3,090.46 3,357.67 3,520.55 13.9%

935.35 1,027.36 1,056.07 12.9%

403.73 416.78 481.18 19.2%

1,453.56 1,459.46 1,503.49 3.4%

360.03 307.42 298.62 (17.1)%

5,635.08 5,883.55 6,111.43 8.5%

September

30, 2013

June 30,

2014

September

30, 2014

Y-o-Y

growth

Credit/deposit ratio of 79.5% on the

domestic balance sheet at September 30,

2014

1. During the three months ended December 31, 2013, the Bank has created a DTL of ` 14.19 billion

on Special Reserve outstanding at March 31, 2013, by reducing the reserves

2. Borrowings include preference shares amounting to ` 3.50 bn

3. Including impact of exchange rate movement

49

Composition of borrowings

Domestic

- Capital instruments1

- Other borrowings

Overseas2

- Capital instruments

- Other borrowings

Total borrowings2

` billion

697.12 621.65 632.28

387.71 385.45 386.72

309.42 236.21 245.56

756.44 837.81 871.21

21.24 20.43 20.97

735.20 817.38 850.25

1,453.56 1,459.46 1,503.49

September

30, 2013

June 30,

2014

September

30, 2014

1. Includes preference share capital ` 3.50 bn

2. Including impact of exchange rate movement

Capital instruments constitute 61.2% of domestic borrowings

50

Capital adequacy

Total Capital

- Tier I

- Tier II

Risk weighted assets

- On balance sheet

- Off balance sheet

Standalone Basel III

881.29 17.00% 885.55 16.64%

634.18 12.23% 637.59 11.98%

247.11 4.77% 247.96 4.66%

5,184.02 5,321.74

4,055.52 4,200.23

1,128.50 1,121.51

June 30, 2014 September 30, 2014

1. In line with the applicable guidelines, the Basel III capital ratios reported by the Bank for

the interim periods do not include profits for the period

2. Capital ratios at June 30, 2014 and September 30, 2014 include the impact of credit value

adjustment on derivative exposures and capital charge required for borrowers with

unhedged foreign currency exposures, in accordance with the Reserve Bank of India

guidelines Including the profits for H1-2015, the capital adequacy ratio for

the Bank as per Basel III norms would have been 17.41% and the

Tier I ratio would have been 12.75%

` bn % ` bn %

51

Asset quality and provisioning

Gross retail NPLs at ` 35.91 bn and net retail NPLs at ` 8.90 bn at

September 30, 2014 compared to ` 49.08 bn and ` 7.62 bn

respectively at September 30, 2013

Provisioning coverage ratio of 65.9% at September 30, 2014

computed in accordance with RBI guidelines

Net loans to companies whose facilities have been restructured

at ` 110.20 bn at September 30, 2014 compared to ` 112.65 bn at

June 30, 2014 and ` 68.26 bn at September 30, 2013

Outstanding general provision on standard assets: ` 21.30 bn at

September 30, 2014

Gross NPAs

Less: Cumulative provisions

Net NPAs

Net NPA ratio

` billion

100.78 110.01 116.95

73.71 75.27 76.99

27.07 34.74 39.97

0.73% 0.87% 0.96%

September

30, 2013

June 30,

2014

September

30, 2014

52

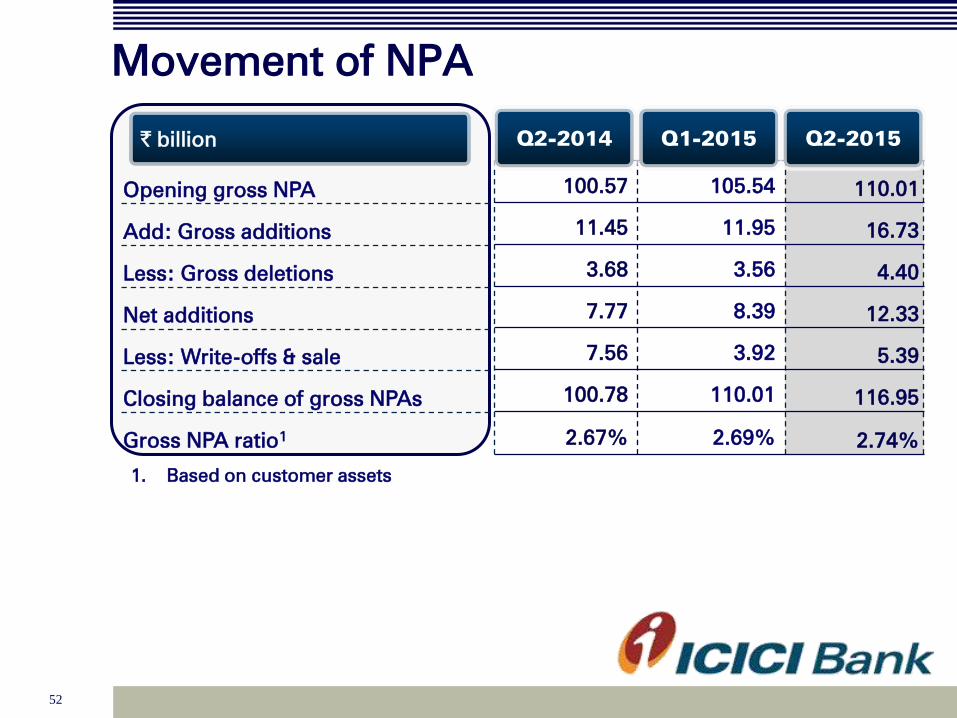

Movement of NPA

Opening gross NPA

Add: Gross additions

Less: Gross deletions

Net additions

Less: Write-offs & sale

Closing balance of gross NPAs

Gross NPA ratio1

` billion

100.57 105.54 110.01

11.45 11.95 16.73

3.68 3.56 4.40

7.77 8.39 12.33

7.56 3.92 5.39

100.78 110.01 116.95

2.67% 2.69% 2.74%

Q2-2014 Q1-2015 Q2-2015

1. Based on customer assets

53

Distribution network

Metro

Urban

Semi urban

Rural

Total branches

Branches

816 865 935 948 24.8%

720 782 865 887 23.3%

904 989 1,114 1,127 29.5%

312 464 839 853 22.4%

2,752 3,100 3,753 3,815 100.0%

9,006 10,481 11,315 11,739 -

At

March

31, 2012

At

March

31, 2013

At Sep

30, 2014

ATMs

Total ATMs

At

March

31, 2014

% of mix

at Sep

30, 2014

54

Consolidated results

55

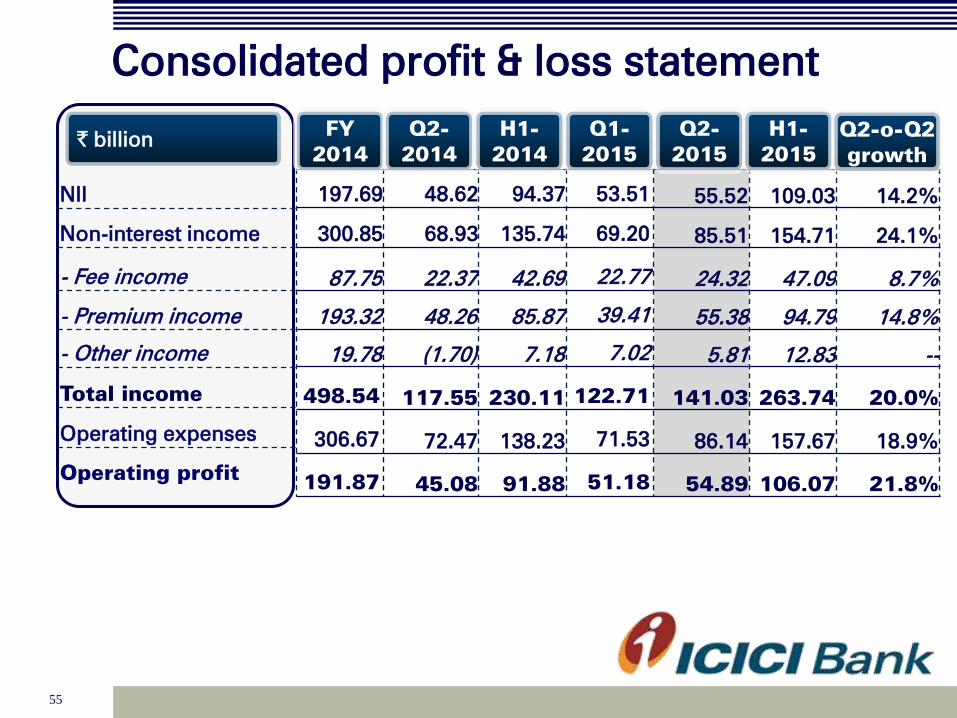

Consolidated profit & loss statement

NII

Non-interest income

- Fee income

- Premium income

- Other income

Total income

Operating expenses

Operating profit

` billion

197.69 48.62 94.37 53.51 55.52 109.03 14.2%

300.85 68.93 135.74 69.20 85.51 154.71 24.1%

87.75 22.37 42.69 22.77 24.32 47.09 8.7%

193.32 48.26 85.87 39.41 55.38 94.79 14.8%

19.78 (1.70) 7.18 7.02 5.81 12.83 --

498.54 117.55 230.11 122.71 141.03 263.74 20.0%

306.67 72.47 138.23 71.53 86.14 157.67 18.9%

191.87 45.08 91.88 51.18 54.89 106.07 21.8%

FY

2014

Q2-

2014

H1-

2014

Q1-

2015

Q2-

2015

H1-

2015

Q2-o-Q2

growth

56

Consolidated profit & loss statement

Operating profit

Provisions

Profit before tax

Tax

Minority interest

Profit after tax

` billion

191.87 45.08 91.88 51.18 54.89 106.07 21.8%

29.00 6.73 13.30 8.14 9.16 17.30 36.1%

162.87 38.35 78.58 43.04 45.73 88.77 19.2%

46.10 9.73 20.81 13.22 13.32 26.54 36.9%

6.36 1.64 3.32 1.50 1.76 3.26 7.3%

110.41 26.98 54.45 28.32 30.65 58.97 13.6%

FY

2014

Q2-

2014

H1-

2014

Q1-

2015

Q2-

2015

H1-

2015

Q2-o-Q2

growth

57

Consolidated balance sheet

Cash & bank balances

Investments

Advances

Fixed & other assets

Total assets

` billion

430.38 506.43 542.00 25.9%

2,560.41 2,668.17 2,769.01 8.1%

3,636.31 3,960.23 4,109.81 13.0%

501.51 356.95 363.53 (27.5)%

7,128.61 7,491.78 7,784.35 9.2%

759.64 794.52 827.56 8.9%

18.85 22.20 22.35 18.6%

3,378.84 3,639.17 3,790.15 12.2%

1,768.69 1,763.91 1,833.83 3.7%

684.63 801.98 846.83 23.7%

517.96 470.00 463.63 (10.5)%

7,128.61 7,491.78 7,784.35 9.2%

September

30, 2013

June 30,

2014

Y-o-Y

growth

September

30, 2014

Net worth

Minority interest

Deposits

Borrowings

Liabilities on policies in

force

Other liabilities

Total liabilities

58

Key ratios (consolidated)

Return on average networth1,2

(consolidated)

Weighted average EPS (`)1

Book value (`)

Percent

14.9 14.6 15.1 14.6 15.1 14.9

95.7 92.7 94.1 98.3 105.1 101.7

660 657 657 686 714 714

FY

2014

Q2-

2014

H1-

2014

Q1-

2015

Q2-

2015

H1-

2015

1. Based on quarterly average networth

2. Annualised for all interim periods

Total Capital

- Tier I

- Tier II

Consolidated Basel III (Percent)

17.57% 17.22%

12.52% 12.27%

5.05% 4.95%

June 30, 20141

September 30, 20141

1. In line with the applicable guidelines, the Basel III

capital ratios reported by the Bank for the interim

periods do not include profits for the period

Including the profits for H1-2015, the capital adequacy ratio on the

consolidated basis as per Basel III norms would have been 18.00% and

the Tier I ratio would have been 13.05%

59

Overseas subsidiaries

60

ICICI Bank UK asset profile

September 30, 2014

Total assets: USD 4.2 bn Total assets: USD 4.1 bn

June 30, 2014

1. Includes cash & advances to banks, T Bills

2. Includes securities re-classified to loans & advances

1

2

2

1

61

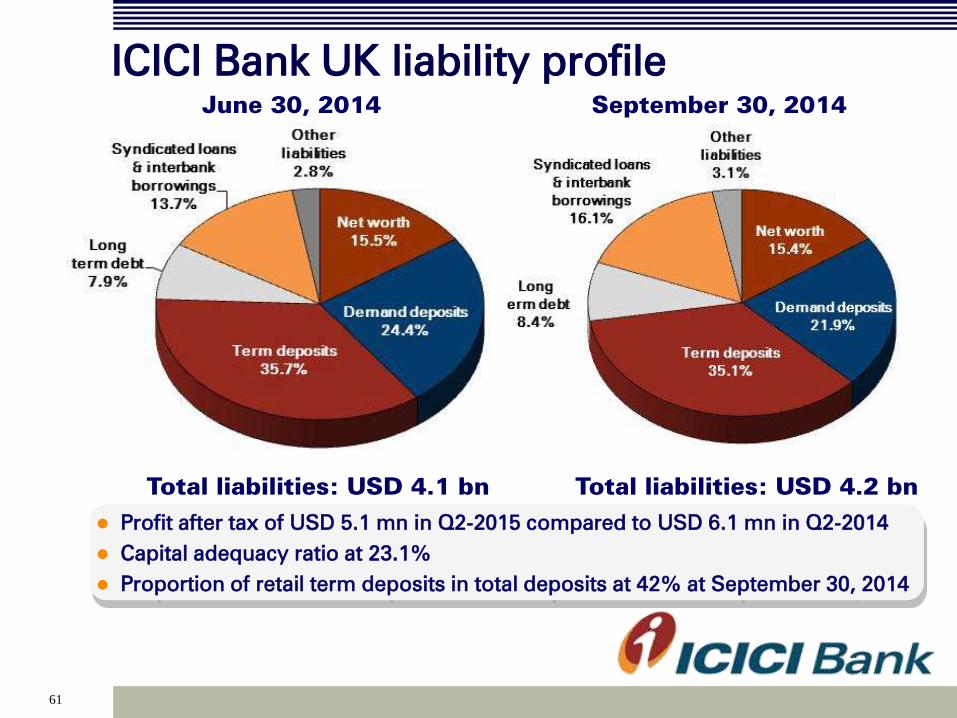

ICICI Bank UK liability profile

September 30, 2014

Total liabilities: USD 4.2 bn Total liabilities: USD 4.1 bn

June 30, 2014

Profit after tax of USD 5.1 mn in Q2-2015 compared to USD 6.1 mn in Q2-2014

Capital adequacy ratio at 23.1%

Proportion of retail term deposits in total deposits at 42% at September 30, 2014

62

ICICI Bank Canada asset profile

September 30, 2014

Total assets: CAD 5.5 bn Total assets: CAD 5.6 bn

June 30, 2014

1. Includes cash & advances to banks and government securities

2. Based on IFRS, securitised portfolio of CAD 2,035 mn and CAD 2,051 mn considered as

part of Insured mortgage portfolio at June 30, 2014 and September 30, 2014 respectively

1

2 2

1

63

ICICI Bank Canada liability profile

September 30, 2014

Total liabilities: CAD 5.5 bn Total liabilities: CAD 5.6 bn

June 30, 2014

Profit after tax of CAD 9.2 mn in Q2-2015 compared to CAD 12.9 mn in Q2-2014

Capital adequacy ratio at 34.0%

1. As per IFRS, proceeds of CAD 2,039 mn and CAD

2,069 mn from sale of securitised portfolio

considered as part of borrowings at June 30,

2014 and September 30, 2014 respectively

1 1

64

ICICI Bank Eurasia asset profile

September 30, 2014

Total assets: USD 114 mn Total assets: USD 127 mn

June 30, 2014

Total borrowings of USD 40 mn at September 30, 2014

Capital adequacy of 47.4% at September 30, 2014

Net profit of USD 0.7 mn in Q2-2015 compared to USD 1.1 mn in Q2-2014

1. Includes cash & call placements with banks,

balances with central bank, government

securities and nostro balances

1 1

65

Domestic subsidiaries

66

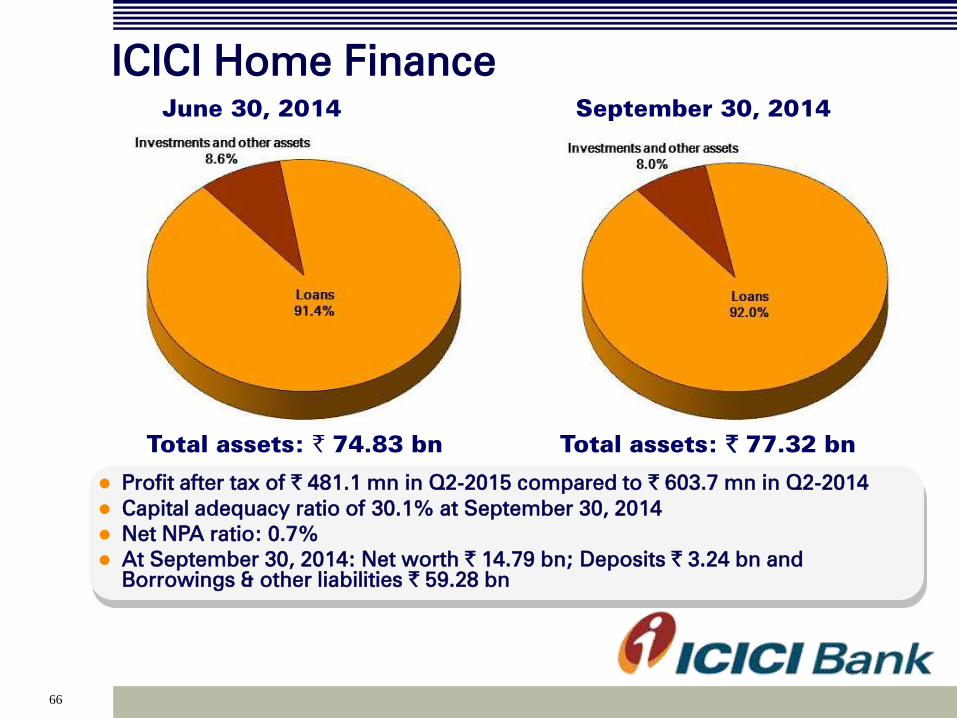

ICICI Home Finance

September 30, 2014

Total assets: ` 77.32 bn Total assets: ` 74.83 bn

June 30, 2014

Profit after tax of ` 481.1 mn in Q2-2015 compared to ` 603.7 mn in Q2-2014

Capital adequacy ratio of 30.1% at September 30, 2014

Net NPA ratio: 0.7%

At September 30, 2014: Net worth ` 14.79 bn; Deposits ` 3.24 bn and

Borrowings & other liabilities ` 59.28 bn

67

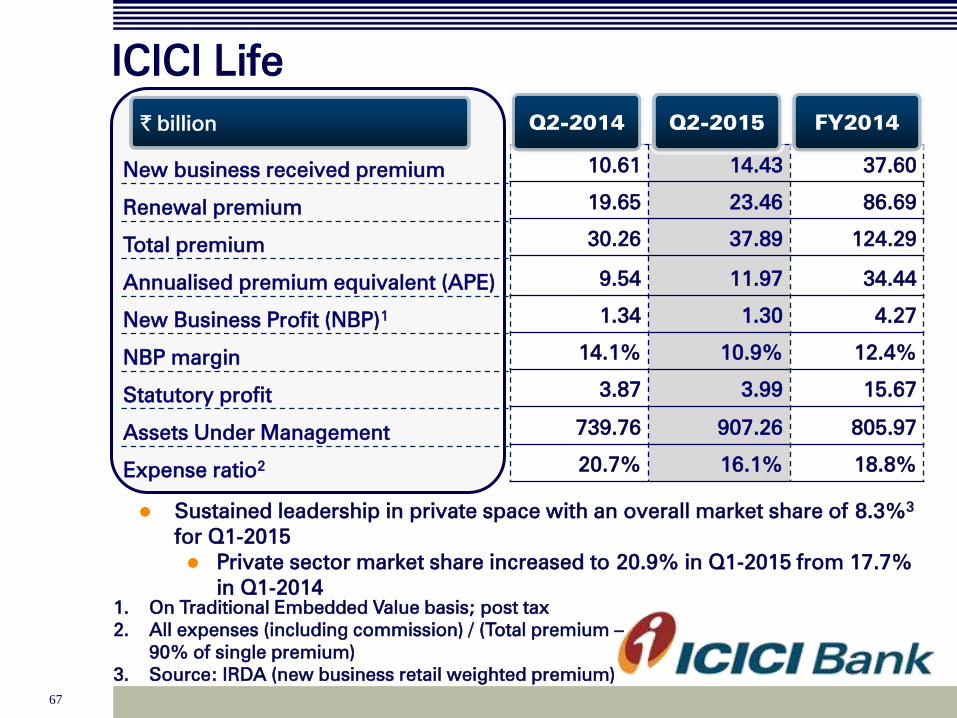

ICICI Life

New business received premium

Renewal premium

Total premium

Annualised premium equivalent (APE)

New Business Profit (NBP)1

NBP margin

Statutory profit

Assets Under Management

Expense ratio2

` billion

10.61 14.43 37.60

19.65 23.46 86.69

30.26 37.89 124.29

9.54 11.97 34.44

1.34 1.30 4.27

14.1% 10.9% 12.4%

3.87 3.99 15.67

739.76 907.26 805.97

20.7% 16.1% 18.8%

Q2-2014 Q2-2015 FY2014

Sustained leadership in private space with an overall market share of 8.3%3

for Q1-2015

Private sector market share increased to 20.9% in Q1-2015 from 17.7%

in Q1-2014

1. On Traditional Embedded Value basis; post tax

2. All expenses (including commission) / (Total premium –

90% of single premium)

3. Source: IRDA (new business retail weighted premium)

68

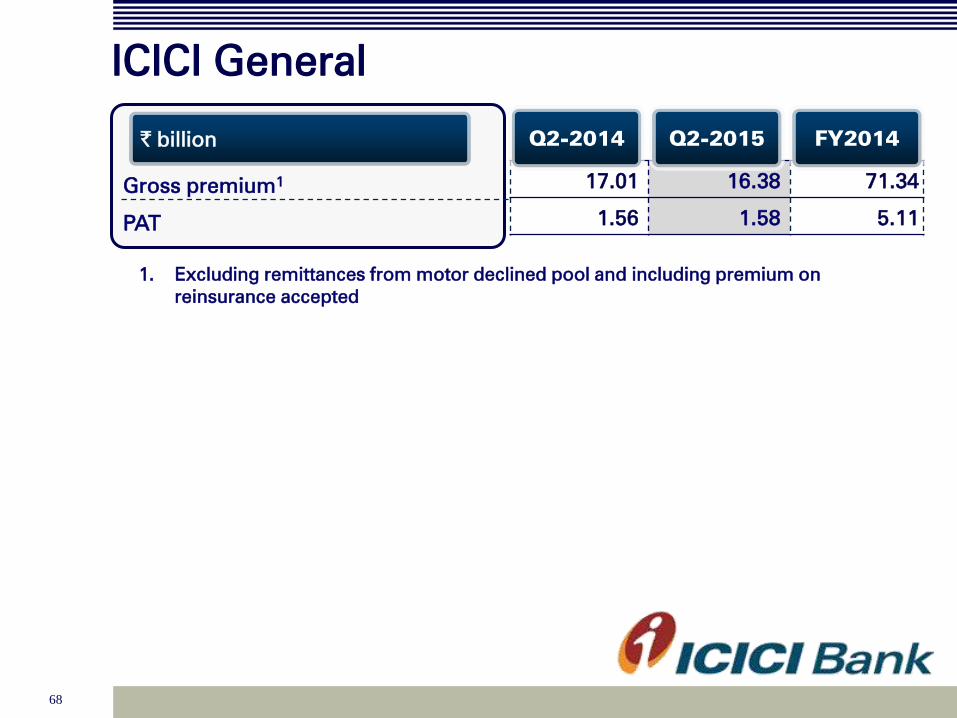

ICICI General

Gross premium1

PAT

` billion

17.01 16.38 71.34

1.56 1.58 5.11

Q2-2014 Q2-2015 FY2014

1. Excluding remittances from motor declined pool and including premium on

reinsurance accepted

69

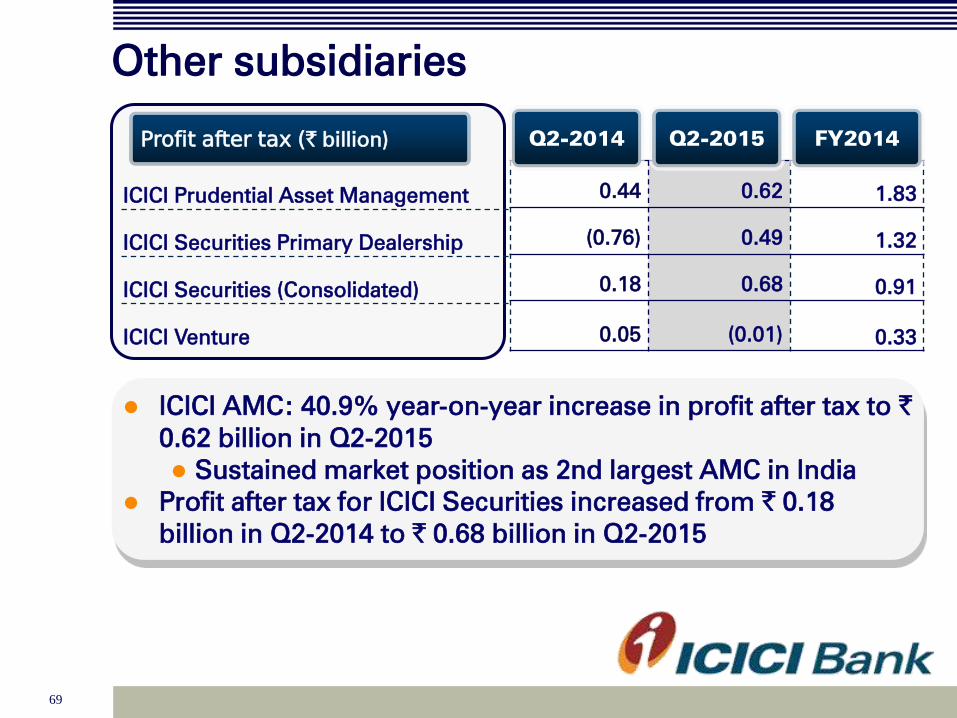

Other subsidiaries

ICICI Prudential Asset Management

ICICI Securities Primary Dealership

ICICI Securities (Consolidated)

ICICI Venture

Profit after tax (` billion)

0.44 0.62 1.83

(0.76) 0.49 1.32

0.18 0.68 0.91

0.05 (0.01) 0.33

Q2-2014 Q2-2015 FY2014

ICICI AMC: 40.9% year-on-year increase in profit after tax to ` 0.62 billion in Q2-2015

Sustained market position as 2nd largest AMC in India

Profit after tax for ICICI Securities increased from ` 0.18

billion in Q2-2014 to ` 0.68 billion in Q2-2015

Related Documents