IBISWorld Industry Report 45391 Pet Stores in the US February 2012 Caitlin Moldvay /XFN\ GRJ 3HW RZQHUV ZLOO LQYHVW LQ SUHPLXP SURGXFWV DV GLVSRVDEOH LQFRPH ULVHV 2 About this Industry 2 Industry Definition 2 Main Activities 2 Similar Industries 2 Additional Resources 3 Industry at a Glance 4 Industry Performance 4 Executive Summary 4 Key External Drivers 5 Current Performance 8 Industry Outlook 11 Industry Life Cycle 13 Products & Markets 13 Supply Chain 13 Products & Services 14 Demand Determinants 15 Major Markets 16 International Trade 17 Business Locations 19 Competitive Landscape 19 Market Share Concentration 19 Key Success Factors 20 Cost Structure Benchmarks 21 Basis of Competition 22 Barriers to Entry 23 Industry Globalization 24 Major Companies 24 PetSmart Inc. 25 PETCO Animal Supplies Inc. 28 Operating Conditions 28 Capital Intensity 29 Technology & Systems 29 Revenue Volatility 30 Regulation & Policy 30 Industry Assistance 31 Key Statistics 31 Industry Data 31 Annual Change 31 Key Ratios 32 Jargon & Glossary www.ibisworld.com | 1-800-330-3772 | info @ ibisworld.com

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

WWW.IBISWORLD.COM Pet Stores in the US February 2012 1

IBISWorld Industry Report 45391Pet Stores in the USFebruary 2012 Caitlin Moldvay

2 About this Industry2 Industry Definition

2 Main Activities

2 Similar Industries

2 Additional Resources

3 Industry at a Glance

4 Industry Performance4 Executive Summary

4 Key External Drivers

5 Current Performance

8 Industry Outlook

11 Industry Life Cycle

13 Products & Markets13 Supply Chain

13 Products & Services

14 Demand Determinants

15 Major Markets

16 International Trade

17 Business Locations

19 Competitive Landscape19 Market Share Concentration

19 Key Success Factors

20 Cost Structure Benchmarks

21 Basis of Competition

22 Barriers to Entry

23 Industry Globalization

24 Major Companies24 PetSmart Inc.

25 PETCO Animal Supplies Inc.

28 Operating Conditions28 Capital Intensity

29 Technology & Systems

29 Revenue Volatility

30 Regulation & Policy

30 Industry Assistance

31 Key Statistics31 Industry Data

31 Annual Change

31 Key Ratios

32 Jargon & Glossary

www.ibisworld.com | 1-800-330-3772 | [email protected]

WWW.IBISWORLD.COM Pet Stores in the US February 2012 2

The primary activities of this industry areRetailing pets

Retailing pet food and supplies

Providing pet grooming and boarding services

54194 Veterinary Services in the USEstablishments in this industry provides veterinary services.

81291 Pet Grooming & Boarding in the USOperators in this industry provide pet grooming and boarding services.

45411a E-Commerce & Online Auctions in the USBusinesses in this industry retails pet foods and pet supplies via the internet.

45411b Mail Order in the USEstablishments in this industry retail pet foods and pet supplies via mail-order or catalogs.

Industry Definition

Main Activities

Similar Industries

Additional Resources

About this Industry

For additional information on this industrywww.americanpetproducts.org/ American Pet Products Association

www.petage.com Pet Age Magazine

www.petbusiness.com Pet Business

www.hsus.org The Humane Society of the United States

The major products and services in this industry areLive animals

Pet food

Pet services

Pet supplies

WWW.IBISWORLD.COM Pet Stores in the US February 2012 3

Mill

ions

210

140

150

160

170

180

190

200

1703 05 07 09 11 13 15Year

Number of pets (cats and dogs)

SOURCE: WWW.IBISWORLD.COM

% c

hang

e

10

!4

!2

0

2

4

6

8

1804 06 08 10 12 14 16Year

Revenue Employment

Revenue vs. employment growth

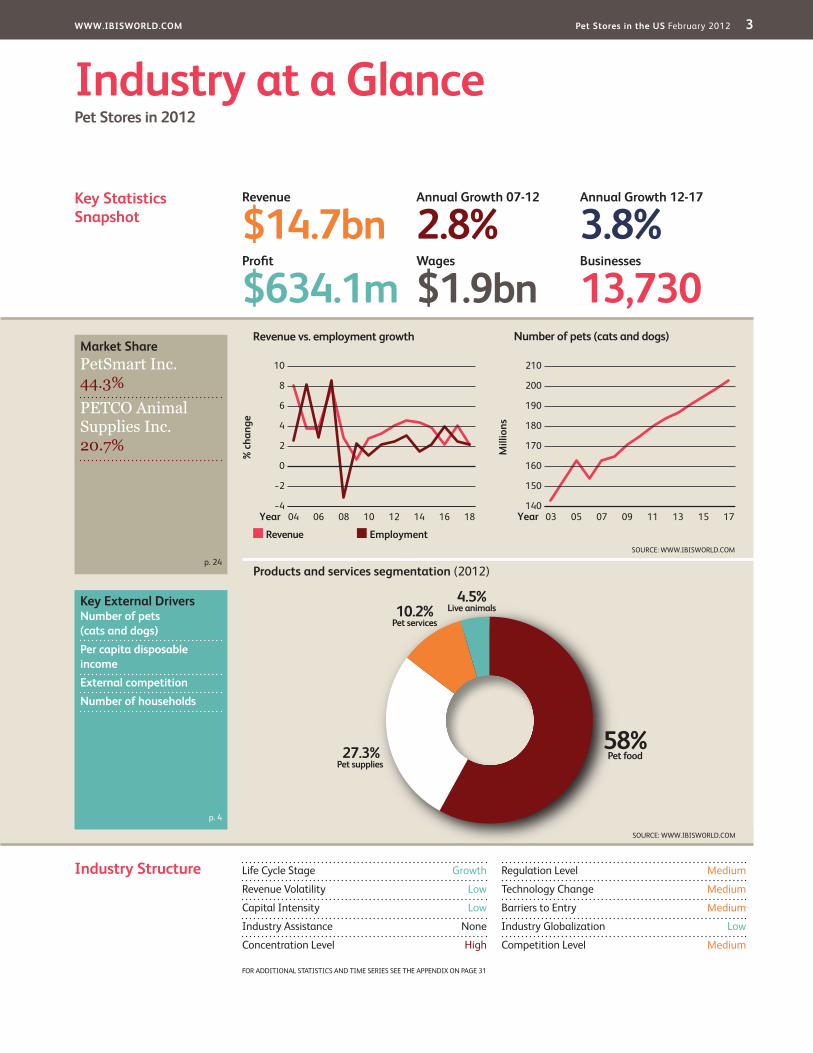

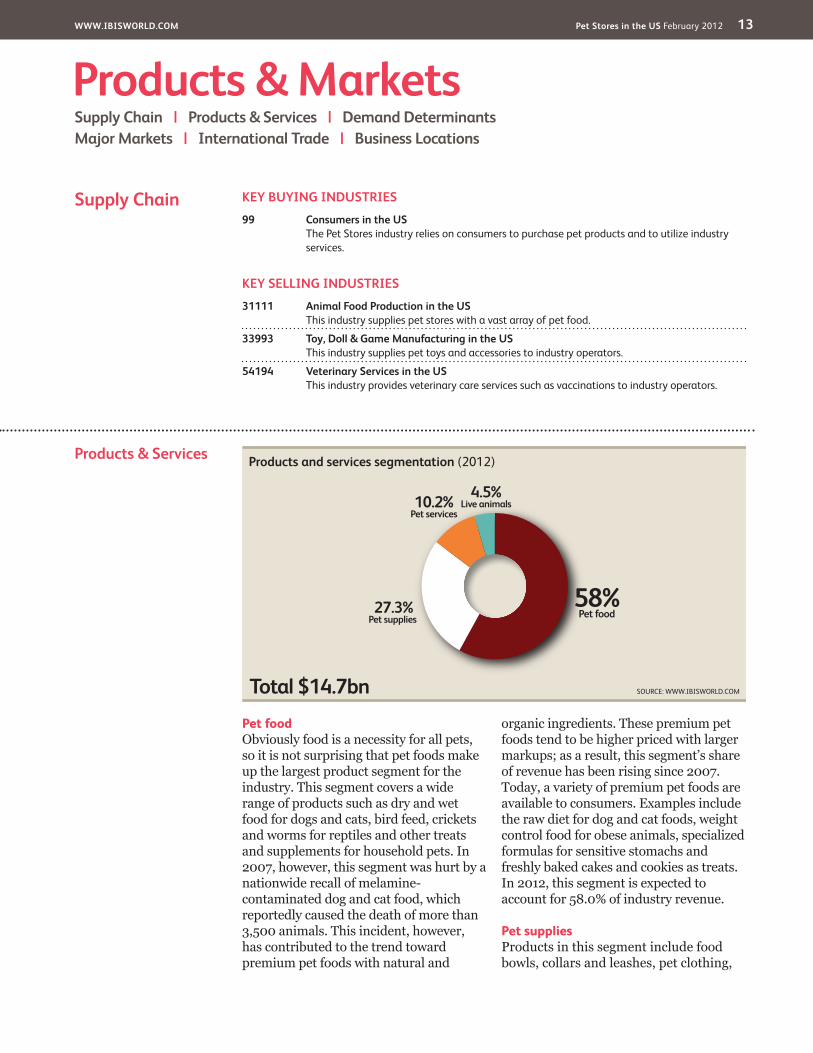

Products and services segmentation (2012)

58%Pet food27.3%

Pet supplies

10.2%Pet services

4.5%Live animals

SOURCE: WWW.IBISWORLD.COM

Key Statistics Snapshot

Industry at a GlancePet Stores in 2012

Industry Structure Life Cycle Stage Growth

Revenue Volatility Low

Capital Intensity Low

Industry Assistance None

Concentration Level High

Regulation Level Medium

Technology Change Medium

Barriers to Entry Medium

Industry Globalization Low

Competition Level Medium

Revenue

$14.7bnProfit

$634.1mWages

$1.9bnBusinesses

13,730

Annual Growth 12-17

3.8%Annual Growth 07-12

2.8%

Key External DriversNumber of pets (cats and dogs)Per capita disposable incomeExternal competitionNumber of households

Market Share

p. 24

p. 4

FOR ADDITIONAL STATISTICS AND TIME SERIES SEE THE APPENDIX ON PAGE 31

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Pet Stores in the US February 2012 4

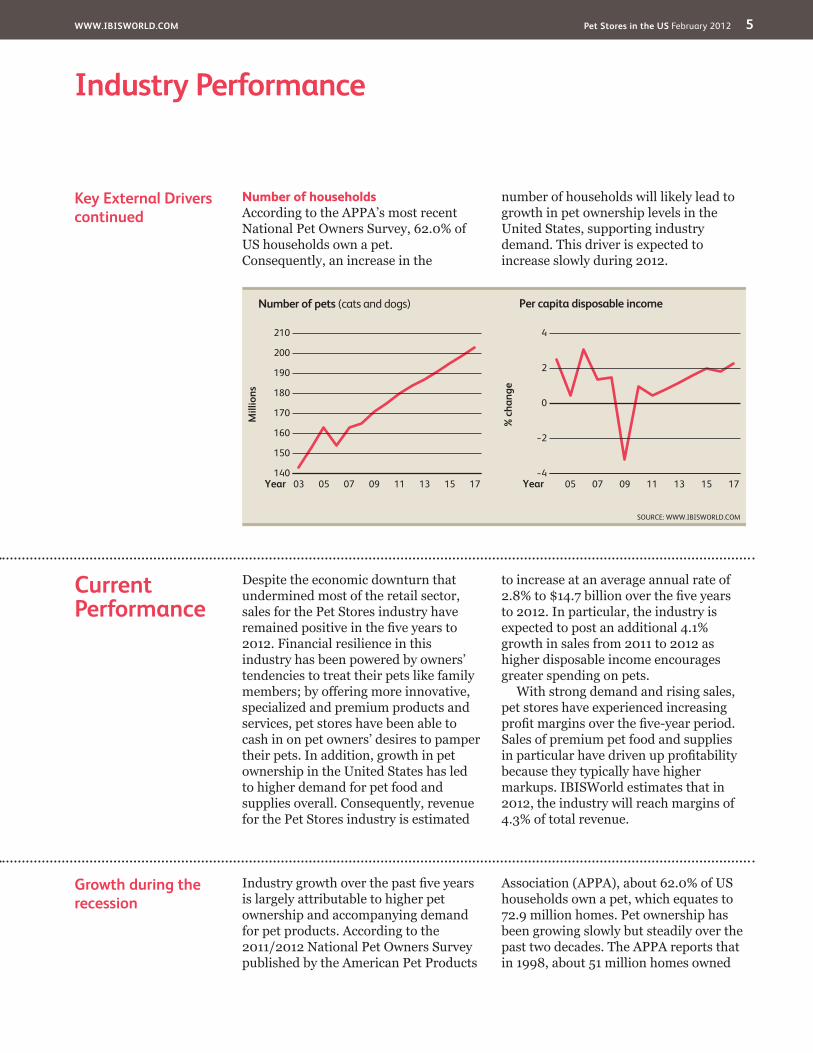

Key External Drivers Number of pets (cats and dogs)

Per capita disposable income

External competition

Executive Summary

Industry PerformanceExecutive Summary | Key External Drivers | Current PerformanceIndustry Outlook | Life Cycle Stage

WWW.IBISWORLD.COM Pet Stores in the US February 2012 5

Industry Performance

Growth during the recession

Current Performance

Key External Driverscontinued

Number of households

% c

hang

e

4

!4

!2

0

2

1705 07 09 11 13 15Year

Per capita disposable income

SOURCE: WWW.IBISWORLD.COM

Mill

ions

210

140

150

160

170

180

190

200

1703 05 07 09 11 13 15Year

Number of pets (cats and dogs)

WWW.IBISWORLD.COM Pet Stores in the US February 2012 6

Industry Performance

Growth during the recessioncontinued

Part of the family

WWW.IBISWORLD.COM Pet Stores in the US February 2012 7

Industry Performance

Product innovation

Competition from bigger stores

WWW.IBISWORLD.COM Pet Stores in the US February 2012 8

Industry Performance

Industry Outlook

Competition from bigger storescontinued

% c

hang

e10

0

2

4

6

8

1804 06 08 10 12 14 16Year

Industry revenue

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Pet Stores in the US February 2012 9

Industry Performance

Industry Outlookcontinued

Changing competition

Premium products will remain popular

WWW.IBISWORLD.COM Pet Stores in the US February 2012 10

Industry Performance

Changing competitioncontinued

WWW.IBISWORLD.COM Pet Stores in the US February 2012 11

Industry PerformanceLife Cycle Stage

SOURCE: WWW.IBISWORLD.COM

30

25

20

15

10

5

0

–5

–10–10 100 20–5 155 25 30

% G

row

th o

f pro

fi t/G

DP

% Growth of establishments

DeclineCrash or Grow?

Potential Hidden GemsFuture Industries

Quality GrowthHigh growth in economic importance; weaker companies close down; developed technology and markets

Time WastersHobby Industries

MaturityCompany consolidation;level of economic importance stable

Shake-out

Shake-outQuantity GrowthMany new companies; minor growth in economic importance; substantial technology change

Key Features of a Growth Industry

Revenue grows faster than the economyMany new companies enter the marketRapid technology & process changeGrowing customer acceptance of productRapid introduction of products & brands

E-Commerce & Online Auctions

Animal Food ProductionMail Order

Toy, Doll & Game Manufacturing

Veterinary ServicesPet Stores

WWW.IBISWORLD.COM Pet Stores in the US February 2012 12

Industry Performance

Industry Life Cycle

This industry is Growing

WWW.IBISWORLD.COM Pet Stores in the US February 2012 13

Products & Services

Pet food

Pet supplies

Products & MarketsSupply Chain | Products & Services | Demand DeterminantsMajor Markets | International Trade | Business Locations

KEY BUYING INDUSTRIES99 Consumers in the US

The Pet Stores industry relies on consumers to purchase pet products and to utilize industry services.

KEY SELLING INDUSTRIES31111 Animal Food Production in the US

This industry supplies pet stores with a vast array of pet food.

33993 Toy, Doll & Game Manufacturing in the US This industry supplies pet toys and accessories to industry operators.

54194 Veterinary Services in the US This industry provides veterinary care services such as vaccinations to industry operators.

Supply Chain

Products and services segmentation (2012)

Total $14.7bn

58%Pet food27.3%

Pet supplies

10.2%Pet services

4.5%Live animals

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Pet Stores in the US February 2012 14

Products & Markets

DemandDeterminants

Pet ownership

Products & Servicescontinued

Services

Live animal purchases

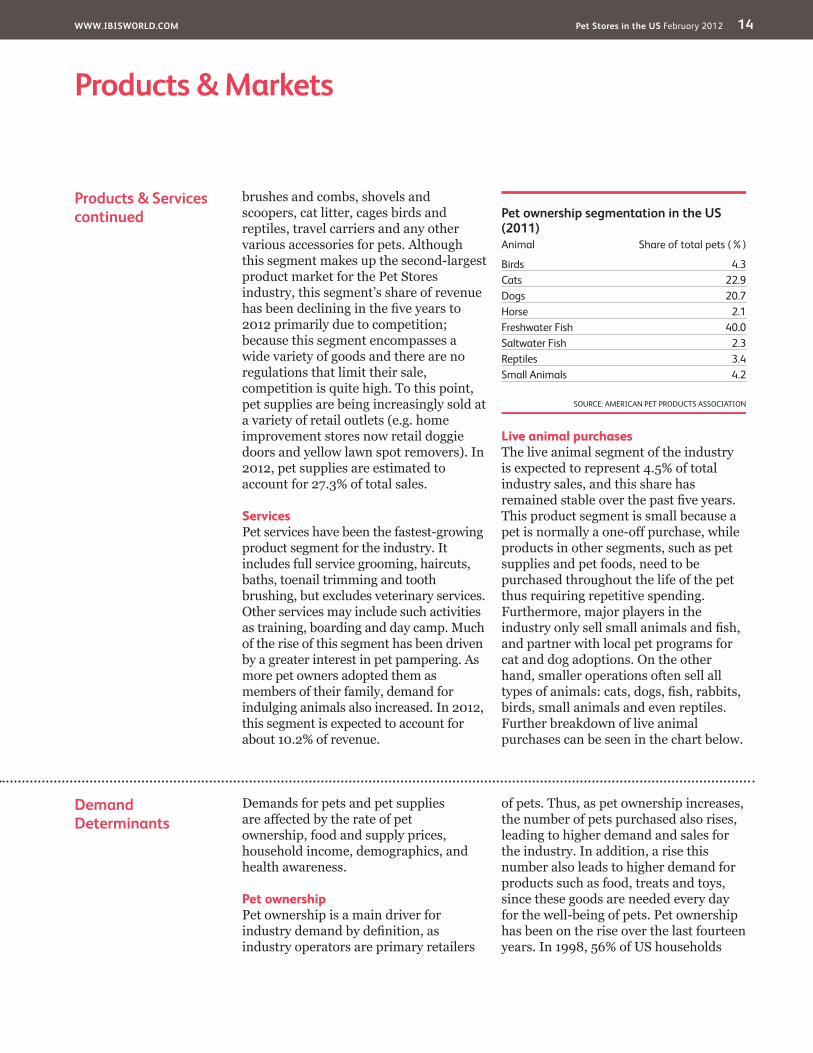

Pet ownership segmentation in the US (2011)Animal Share of total pets (%)

Birds 4.3Cats 22.9Dogs 20.7Horse 2.1Freshwater Fish 40.0Saltwater Fish 2.3Reptiles 3.4Small Animals 4.2

SOURCE: AMERICAN PET PRODUCTS ASSOCIATION

WWW.IBISWORLD.COM Pet Stores in the US February 2012 15

Products & Markets

Major Markets

DemandDeterminantscontinued

IncomeDemographics and lifestyle

Major market segmentation (2012)

Total $14.7bn

28%Consumers 45 to

54 years old

7%Consumers over

65 years old

24%Consumers 35 to

44 years old

18%Consumers 25 to

34 years old

13%Consumers 55 to

64 years old

10%Consumers under

25 years old

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Pet Stores in the US February 2012 16

Products & Markets

International Trade

Major Marketscontinued

WWW.IBISWORLD.COM Pet Stores in the US February 2012 17

Products & Markets

Business Locations 2012

MO1.9

West

West

West

Rocky Mountains Plains

Southwest

Southeast

New England

Great Lakes

VT0.3

MA2.0

RI0.5

NJ3.3

DE0.5

NH0.7

CT1.5

MD1.9

DC0.1

1

5

3

7

2

6

4

8 9

Additional States (as marked on map)

AZ2.2

CA13.2

NV0.9

OR2.0

WA3.1

MT0.3

NE0.5

MN1.7

IA0.9

OH3.9 VA

2.7

FL7.7

KS0.9

CO2.6

UT0.7

ID0.5

TX5.6

OK0.9

NC2.5

AK0.2

WY0.3

TN1.5

KY0.7

GA2.2

IL4.1

ME0.6

ND0.2

WI1.9 MI

3.5 PA4.4

WV0.3

SD0.2

NM0.6

AR0.5

MS0.4

AL1.0

SC1.3

LA1.0

HI0.4

IN2.0

NY7.4 5

67

8

321

4

9

SOURCE: WWW.IBISWORLD.COM

Mid- Atlantic

Establishments (%)

Less than 3% 3% to less than 10% 10% to less than 20% 20% or more

WWW.IBISWORLD.COM Pet Stores in the US February 2012 18

Products & Markets

Business Locations

Southeast

West

Mid-Atlantic

Great Lakes

%

30

0

10

20

Sout

hwes

t

Wes

t

Gre

at L

akes

Mid

-Atla

ntic

New

Eng

land

Plai

ns

Rock

y M

ount

ains

Sout

heas

t

EstablishmentsPopulation

Establishments vs. population

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Pet Stores in the US February 2012 19

Key Success Factors Attractive product presentation

Experienced work force

Proximity to key markets

Economies of scope

Effective quality control

Market Share Concentration

Competitive LandscapeMarket Share Concentration | Key Success Factors | Cost Structure BenchmarksBasis of Competition | Barriers to Entry | Industry Globalization

Companies by employment sizeNo. of employees Share (%)

0-4 57.45-9 23.210-19 13.020-99 5.6100-499 0.6500+ 0.2

Statistics of US BusinessesSOURCE: US CENSUS BUREAU

Level Concentration in this industry is High

IBISWorld identifies 250 Key Success Factors for a business. The most important for this industry are:

WWW.IBISWORLD.COM Pet Stores in the US February 2012 20

Competitive Landscape

Cost Structure Benchmarks

Sector vs. Industry Costs

Profi t Wages Purchases Depreciation Marketing Rent & Utilities Other

Average Costs of all Industries in sector (2012)

Industry Costs (2012)

0

20

40

60

Perc

enta

ge o

f rev

enue

80

100 3.7

9.24.6 1.51.6

65.8

13.74.3

6.74.01.6

70.3

13.1

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Pet Stores in the US February 2012 21

Competitive Landscape

Basis of Competition Internal

Cost Structure Benchmarkscontinued

Level & Trend Competition in this industry is Medium and the trend is Increasing

WWW.IBISWORLD.COM Pet Stores in the US February 2012 22

Competitive Landscape

Barriers to Entry

Basis of Competitioncontinued

External

Barriers to Entry checklist LevelCompetition MediumConcentration HighLife Cycle Stage GrowthCapital Intensity LowTechnology Change MediumRegulation & Policy MediumIndustry Assistance None

SOURCE: WWW.IBISWORLD.COM

Level & Trend Barriers to Entry in this industry are Medium and Steady

WWW.IBISWORLD.COM Pet Stores in the US February 2012 23

Competitive Landscape

Industry Globalization

Barriers to Entrycontinued

Level & Trend Globalization in this industry is Low and the trend is Steady

WWW.IBISWORLD.COM Pet Stores in the US February 2012 24

Player Performance

Financial performance

Major CompaniesPetSmart Inc. | PETCO Animal Supplies Inc. | Other Companies

35.0%Other

PetSmart Inc. 44.3%

PETCO Animal Supplies Inc. 20.7%

SOURCE: WWW.IBISWORLD.COM

Major players(Market share)

PetSmart Inc. Market share: 44.3%

WWW.IBISWORLD.COM Pet Stores in the US February 2012 25

Major Companies

Player Performance

Player Performancecontinued

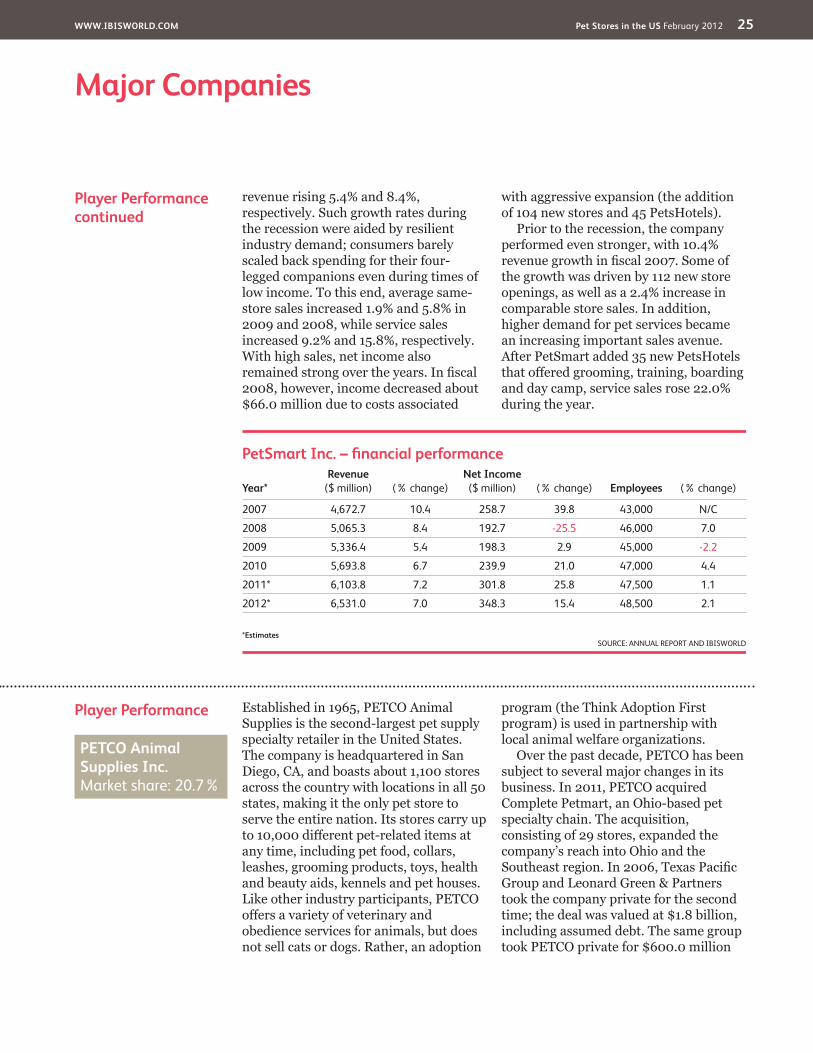

PetSmart Inc. – fi nancial performance

Year*Revenue

($ million) (% change)Net Income

($ million) (% change) Employees (% change)

2007 4,672.7 10.4 258.7 39.8 43,000 N/C

2008 5,065.3 8.4 192.7 -25.5 46,000 7.0

2009 5,336.4 5.4 198.3 2.9 45,000 -2.2

2010 5,693.8 6.7 239.9 21.0 47,000 4.4

2011* 6,103.8 7.2 301.8 25.8 47,500 1.1

2012* 6,531.0 7.0 348.3 15.4 48,500 2.1

*EstimatesSOURCE: ANNUAL REPORT AND IBISWORLD

PETCO Animal Supplies Inc. Market share: 20.7%

WWW.IBISWORLD.COM Pet Stores in the US February 2012 26

Major Companies

Other Companies Pet Supplies PlusEstimated market share: 3.6%

Player Performancecontinued

Financial performance

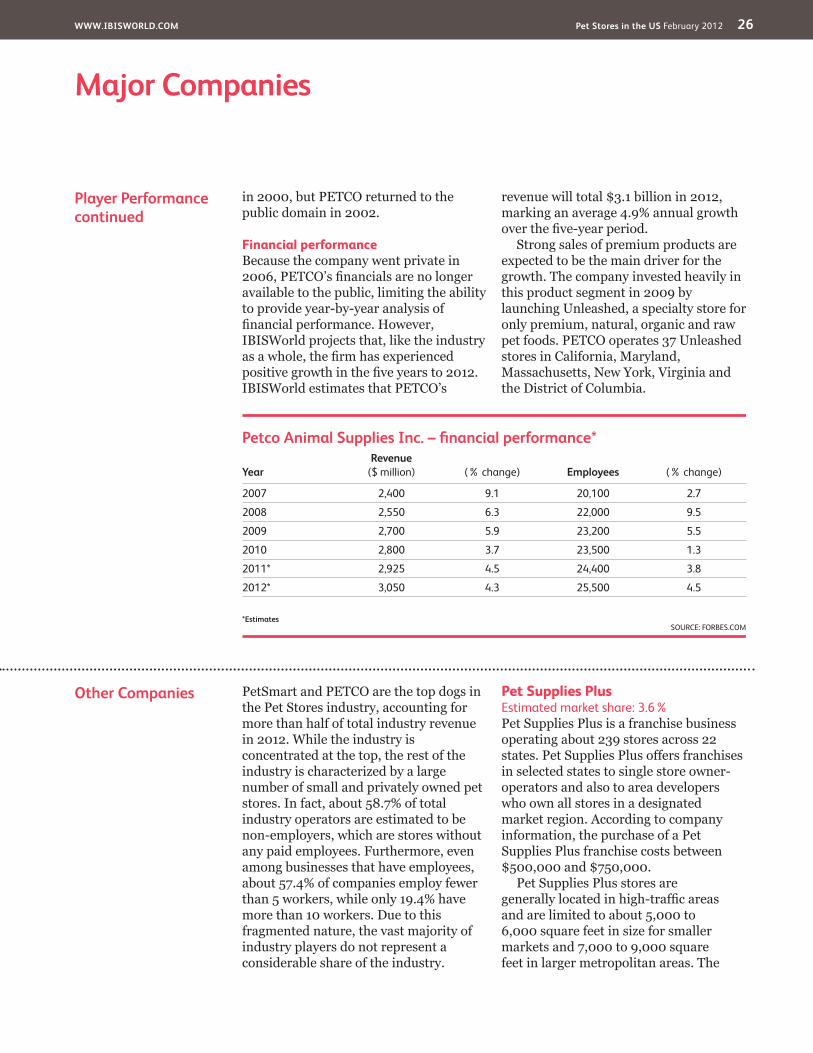

Petco Animal Supplies Inc. – fi nancial performance*

YearRevenue

($ million) (% change) Employees (% change)

2007 2,400 9.1 20,100 2.7

2008 2,550 6.3 22,000 9.5

2009 2,700 5.9 23,200 5.5

2010 2,800 3.7 23,500 1.3

2011* 2,925 4.5 24,400 3.8

2012* 3,050 4.3 25,500 4.5

*EstimatesSOURCE: FORBES.COM

WWW.IBISWORLD.COM Pet Stores in the US February 2012 27

Major Companies

Other Companiescontinued

Pet Supermarket Inc.Estimated market share: 1.6%

Pet Food ExpressEstimated market share: Less than 1.0%

WWW.IBISWORLD.COM Pet Stores in the US February 2012 28

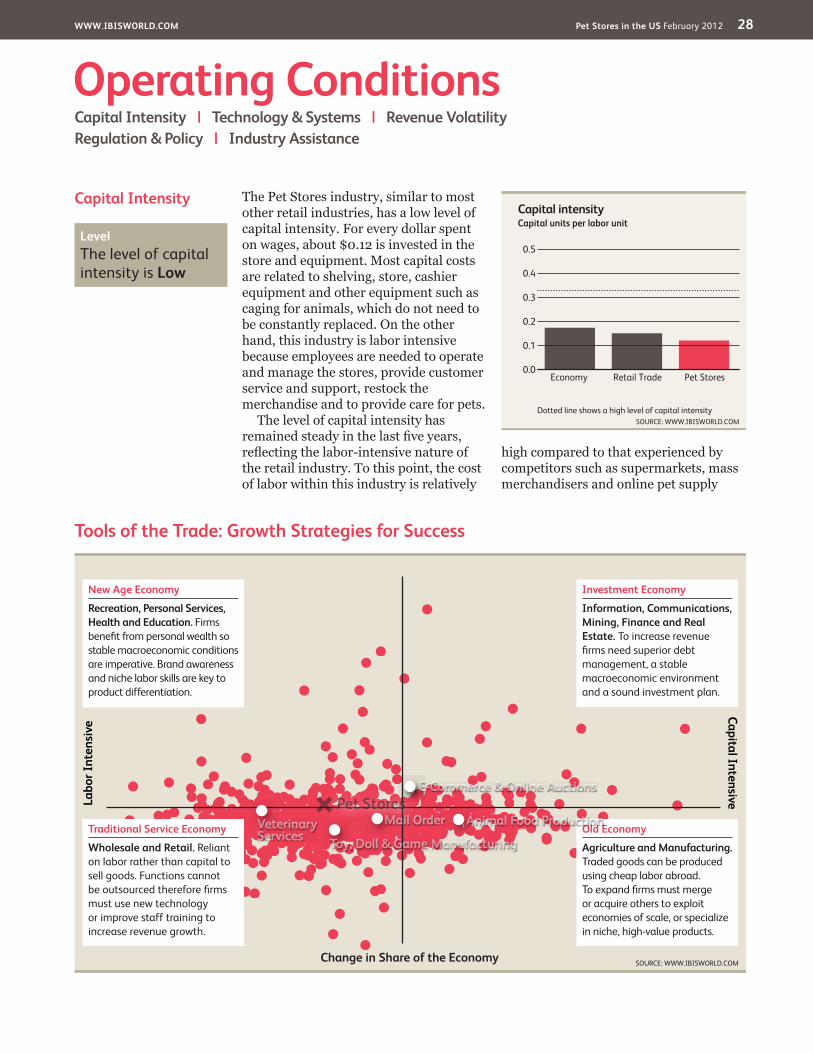

Capital Intensity

Operating ConditionsCapital Intensity | Technology & Systems | Revenue VolatilityRegulation & Policy | Industry Assistance

Tools of the Trade: Growth Strategies for Success

SOURCE: WWW.IBISWORLD.COM

Labo

r Int

ensiv

eCapital Intensive

Change in Share of the Economy

New Age EconomyRecreation, Personal Services, Health and Education. Firms benefi t from personal wealth so stable macroeconomic conditions are imperative. Brand awareness and niche labor skills are key to product differentiation.

Traditional Service EconomyWholesale and Retail. Reliant on labor rather than capital to sell goods. Functions cannot be outsourced therefore fi rms must use new technology or improve staff training to increase revenue growth.

Old EconomyAgriculture and Manufacturing. Traded goods can be produced using cheap labor abroad. To expand fi rms must merge or acquire others to exploit economies of scale, or specialize in niche, high-value products.

Investment EconomyInformation, Communications, Mining, Finance and Real Estate. To increase revenue fi rms need superior debt management, a stable macroeconomic environment and a sound investment plan.

E-Commerce & Online Auctions

Animal Food ProductionMail Order

Toy, Doll & Game ManufacturingVeterinary Services

Pet Stores

Capital intensity

0.5

0.0

0.1

0.2

0.3

0.4

SOURCE: WWW.IBISWORLD.COMDotted line shows a high level of capital intensity

Capital units per labor unit

Pet StoresRetail TradeEconomy

Level The level of capital intensity is Low

WWW.IBISWORLD.COM Pet Stores in the US February 2012 29

Operating Conditions

Revenue Volatility

Technology& Systems

Capital Intensitycontinued

Level The level of Technology Change is Medium

SOURCE: WWW.IBISWORLD.COM

Volatility vs Growth

Reve

nue

vola

tility

* (%

)

1000

100

10

1

0.1

Five year annualized revenue growth (%)–30 –10 10 30 50 70

Hazardous

Stagnant

Rollercoaster

Blue Chip

* Axis is in logarithmic scale

A higher level of revenue volatility implies greater industry risk. Volatility can negatively affect long-term strategic decisions, such as the time frame for capital investment.

When a fi rm makes poor investment decisions it may face underutilized capacity if demand suddenly falls, or capacity constraints if it rises quickly.

Pet Stores

Level The level of Volatility is Low

WWW.IBISWORLD.COM Pet Stores in the US February 2012 30

Operating Conditions

Industry Assistance

Regulation & Policy

Revenue Volatilitycontinued

Level & Trend The level of Regulation is Medium and the trend is Steady

Key tariffsGoods Low rate High rate

Saddlery and harness for any animal (excluding dogs – see above) 2.8 2.8Dog leashes, collars, muzzles, harnesses and similar 2.4 2.4Pet food 0.0 0.0

SOURCE: USITC

Level & Trend The level of Industry Assistance is None and the trend is Steady

WWW.IBISWORLD.COM Pet Stores in the US February 2012 31

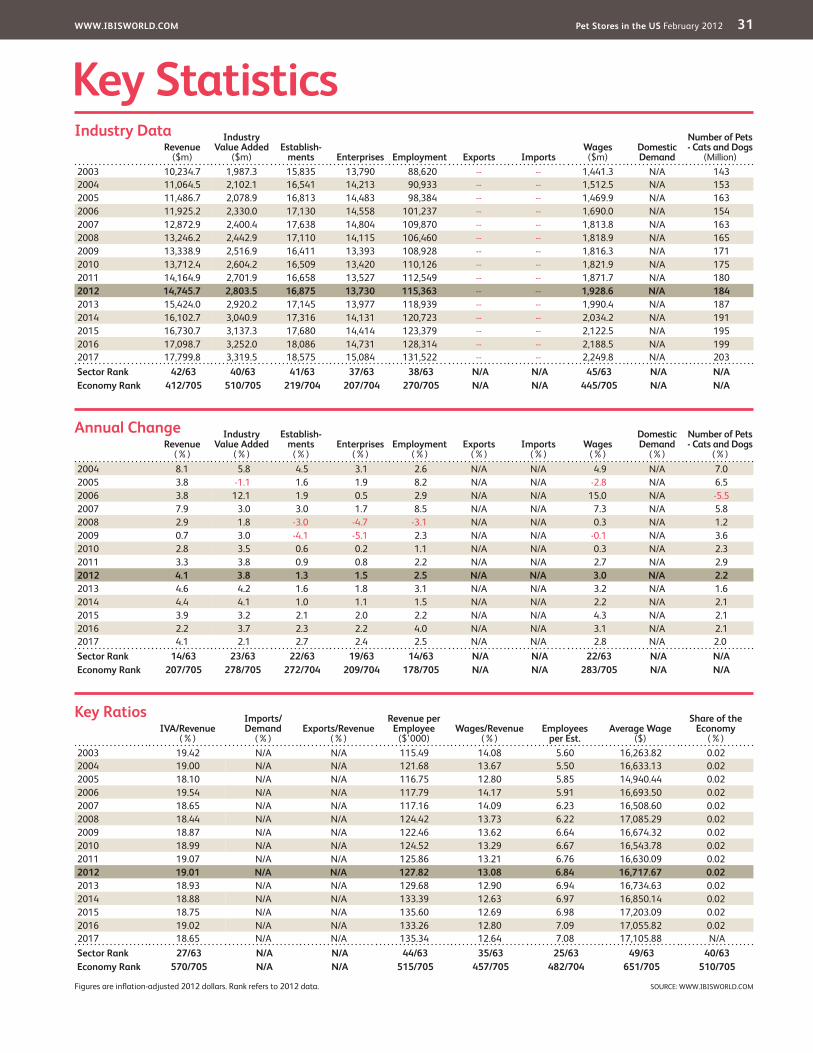

Key StatisticsRevenue

($m)

Industry Value Added

($m)Establish-

ments Enterprises Employment Exports ImportsWages ($m)

Domestic Demand

Number of Pets - Cats and Dogs

(Million)2003 10,234.7 1,987.3 15,835 13,790 88,620 -- -- 1,441.3 N/A 1432004 11,064.5 2,102.1 16,541 14,213 90,933 -- -- 1,512.5 N/A 1532005 11,486.7 2,078.9 16,813 14,483 98,384 -- -- 1,469.9 N/A 1632006 11,925.2 2,330.0 17,130 14,558 101,237 -- -- 1,690.0 N/A 1542007 12,872.9 2,400.4 17,638 14,804 109,870 -- -- 1,813.8 N/A 1632008 13,246.2 2,442.9 17,110 14,115 106,460 -- -- 1,818.9 N/A 1652009 13,338.9 2,516.9 16,411 13,393 108,928 -- -- 1,816.3 N/A 1712010 13,712.4 2,604.2 16,509 13,420 110,126 -- -- 1,821.9 N/A 1752011 14,164.9 2,701.9 16,658 13,527 112,549 -- -- 1,871.7 N/A 1802012 14,745.7 2,803.5 16,875 13,730 115,363 -- -- 1,928.6 N/A 1842013 15,424.0 2,920.2 17,145 13,977 118,939 -- -- 1,990.4 N/A 1872014 16,102.7 3,040.9 17,316 14,131 120,723 -- -- 2,034.2 N/A 1912015 16,730.7 3,137.3 17,680 14,414 123,379 -- -- 2,122.5 N/A 1952016 17,098.7 3,252.0 18,086 14,731 128,314 -- -- 2,188.5 N/A 1992017 17,799.8 3,319.5 18,575 15,084 131,522 -- -- 2,249.8 N/A 203Sector Rank 42/63 40/63 41/63 37/63 38/63 N/A N/A 45/63 N/A N/AEconomy Rank 412/705 510/705 219/704 207/704 270/705 N/A N/A 445/705 N/A N/A

IVA/Revenue (%)

Imports/Demand

(%)Exports/Revenue

(%)

Revenue per Employee

($’000)Wages/Revenue

(%)Employees

per Est.Average Wage

($)

Share of the Economy

(%)2003 19.42 N/A N/A 115.49 14.08 5.60 16,263.82 0.022004 19.00 N/A N/A 121.68 13.67 5.50 16,633.13 0.022005 18.10 N/A N/A 116.75 12.80 5.85 14,940.44 0.022006 19.54 N/A N/A 117.79 14.17 5.91 16,693.50 0.022007 18.65 N/A N/A 117.16 14.09 6.23 16,508.60 0.022008 18.44 N/A N/A 124.42 13.73 6.22 17,085.29 0.022009 18.87 N/A N/A 122.46 13.62 6.64 16,674.32 0.022010 18.99 N/A N/A 124.52 13.29 6.67 16,543.78 0.022011 19.07 N/A N/A 125.86 13.21 6.76 16,630.09 0.022012 19.01 N/A N/A 127.82 13.08 6.84 16,717.67 0.022013 18.93 N/A N/A 129.68 12.90 6.94 16,734.63 0.022014 18.88 N/A N/A 133.39 12.63 6.97 16,850.14 0.022015 18.75 N/A N/A 135.60 12.69 6.98 17,203.09 0.022016 19.02 N/A N/A 133.26 12.80 7.09 17,055.82 0.022017 18.65 N/A N/A 135.34 12.64 7.08 17,105.88 N/ASector Rank 27/63 N/A N/A 44/63 35/63 25/63 49/63 40/63Economy Rank 570/705 N/A N/A 515/705 457/705 482/704 651/705 510/705

Figures are inflation-adjusted 2012 dollars. Rank refers to 2012 data.

Revenue (%)

Industry Value Added

(%)

Establish-ments

(%)Enterprises

(%)Employment

(%)Exports

(%)Imports

(%)Wages

(%)

Domestic Demand

(%)

Number of Pets - Cats and Dogs

(%)2004 8.1 5.8 4.5 3.1 2.6 N/A N/A 4.9 N/A 7.02005 3.8 -1.1 1.6 1.9 8.2 N/A N/A -2.8 N/A 6.52006 3.8 12.1 1.9 0.5 2.9 N/A N/A 15.0 N/A -5.52007 7.9 3.0 3.0 1.7 8.5 N/A N/A 7.3 N/A 5.82008 2.9 1.8 -3.0 -4.7 -3.1 N/A N/A 0.3 N/A 1.22009 0.7 3.0 -4.1 -5.1 2.3 N/A N/A -0.1 N/A 3.62010 2.8 3.5 0.6 0.2 1.1 N/A N/A 0.3 N/A 2.32011 3.3 3.8 0.9 0.8 2.2 N/A N/A 2.7 N/A 2.92012 4.1 3.8 1.3 1.5 2.5 N/A N/A 3.0 N/A 2.22013 4.6 4.2 1.6 1.8 3.1 N/A N/A 3.2 N/A 1.62014 4.4 4.1 1.0 1.1 1.5 N/A N/A 2.2 N/A 2.12015 3.9 3.2 2.1 2.0 2.2 N/A N/A 4.3 N/A 2.12016 2.2 3.7 2.3 2.2 4.0 N/A N/A 3.1 N/A 2.12017 4.1 2.1 2.7 2.4 2.5 N/A N/A 2.8 N/A 2.0Sector Rank 14/63 23/63 22/63 19/63 14/63 N/A N/A 22/63 N/A N/AEconomy Rank 207/705 278/705 272/704 209/704 178/705 N/A N/A 283/705 N/A N/A

Annual Change

Key Ratios

Industry Data

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Pet Stores in the US February 2012 32

Jargon & Glossary

BARRIERS TO ENTRY Barriers to entry can be High, Medium or Low. High means new companies struggle to enter an industry, while Low means it is easy for a firm to enter an industry.CAPITAL/LABOR INTENSITY An indicator of how much capital is used in production as opposed to labor. Level is stated as High, Medium or Low. High is a ratio of less than $3 of wage costs for every $1 of depreciation; Medium is $3 – $8 of wage costs to $1 of depreciation; Low is greater than $8 of wage costs for every $1 of depreciation.CONSTANT PRICES The dollar figures in the Key Statistics table, including forecasts, are adjusted for inflation using 2012 as the base year. This removes the impact of changes in the purchasing power of the dollar, leaving only the ‘real’ growth or decline in industry metrics. The inflation adjustments in IBISWorld’s reports are made using the US Bureau of Economic Analysis’ implicit GDP price deflator.DOMESTIC DEMAND The use of goods and services within the US; the sum of imports and domestic production minus exports.EARNINGS BEFORE INTEREST AND TAX (EBIT) IBISWorld uses EBIT as an indicator of a company’s profitability. It is calculated as revenue minus expenses, excluding tax and interest.EMPLOYMENT The number of working proprietors, partners, permanent, part-time, temporary and casual employees, and managerial and executive employees.ENTERPRISE A division that is separately managed and keeps management accounts. The most relevant measure of the number of firms in an industry.ESTABLISHMENT The smallest type of accounting unit within an Enterprise; usually consists of one or more locations in a state or territory of the country in which it operates.EXPORTS The total sales and transfers of goods produced by an industry that are exported.IMPORTS The value of goods and services imported with the amount payable to non-residents.

INDUSTRY CONCENTRATION IBISWorld bases concentration on the top four firms. Concentration is identified as High, Medium or Low. High means the top four players account for over 70% of revenue; Medium is 40 –70% of revenue; Low is less than 40%.INDUSTRY REVENUE The total sales revenue of the industry, including sales (exclusive of excise and sales tax) of goods and services; plus transfers to other firms of the same business; plus subsidies on production; plus all other operating income from outside the firm (such as commission income, repair and service income, and rent, leasing and hiring income); plus capital work done by rental or lease. Receipts from interest royalties, dividends and the sale of fixed tangible assets are excluded.INDUSTRY VALUE ADDED The market value of goods and services produced by an industry minus the cost of goods and services used in the production process, which leaves the gross product of the industry (also called its Value Added).INTERNATIONAL TRADE The level is determined by: Exports/Revenue: Low is 0 –5%; Medium is 5 –20%; High is over 20%. Imports/Domestic Demand: Low is 0 –5%; Medium is 5 –35%; and High is over 35%.LIFE CYCLE All industries go through periods of Growth, Maturity and Decline. An average life cycle lasts 70 years. Maturity is the longest stage at 40 years with Growth and Decline at 15 years each.NON-EMPLOYING ESTABLISHMENT Businesses with no paid employment and payroll are known as non-employing establishments. These are mostly set-up by self employed individuals.VOLATILITY The level of volatility is determined by the percentage change in revenue over the past five years. Volatility levels: Very High is greater than ±20%; High Volatility is between ±10% and ±20%; Moderate Volatility is between ±3% and ±10%; and Low Volatility is less than ±3%.WAGES The gross total wages and salaries of all employees of the establishment.

Industry Jargon

IBISWorld Glossary

HUMANIZATION A trend where pet owners treat pets as humans, providing them with services such as pet hotels and grief counseling.JUST-IN-TIME (JIT) A strategy implemented to improve profitability by reducing inventory and purchasing the raw materials that are needed for the immediate term only.

PET BOARDING AND DAY-CARE Long- and short-term options for owners who need assistance looking after their pets. Services include feeding, walking, grooming and lodging.PET PARENTS Pet owners who are enthusiastic about their pets and treat them as members of their family.

Disclaimer

This product has been supplied by IBISWorld Inc. (‘IBISWorld’) solely for use by its authorized licenses strictly in accordance with their license agreements with IBISWorld. IBISWorld makes no representation to any other person with regard to the completeness or accuracy of the data or information contained herein, and it accepts no responsibility and disclaims all liability (save for liability which cannot be lawfully disclaimed) for loss or damage whatsoever suffered or incurred by any other person resulting from the use

of, or reliance upon, the data or information contained herein. Copyright in this publication is owned by IBISWorld Inc. The publication is sold on the basis that the purchaser agrees not to copy the material contained within it for other than the purchasers own purposes. In the event that the purchaser uses or quotes from the material in this publication – in papers, reports, or opinions prepared for any other person – it is agreed that it will be sourced to: IBISWorld Inc.

Identify high growth, emerging & shrinking marketsArm yourself with the latest industry intelligenceAssess competitive threats from existing & new entrantsBenchmark your performance against the competitionMake speedy market-ready, profit-maximizing decisions

Who is IBISWorld?We are strategists, analysts, researchers, and marketers. We provide answers to information-hungry, time-poor businesses. Our goal is to provide real world answers that matter to your business in our 700 US industry reports. When tough strategic, budget, sales and marketing decisions need to be made, our suite of Industry and Risk intelligence products give you deeply-researched answers quickly.

IBISWorld MembershipIBISWorld offers tailored membership packages to meet your needs.

Copyright 2012 IBISWorld Inc

www.ibisworld.com | 1800-330-3772 | [email protected]

Related Documents