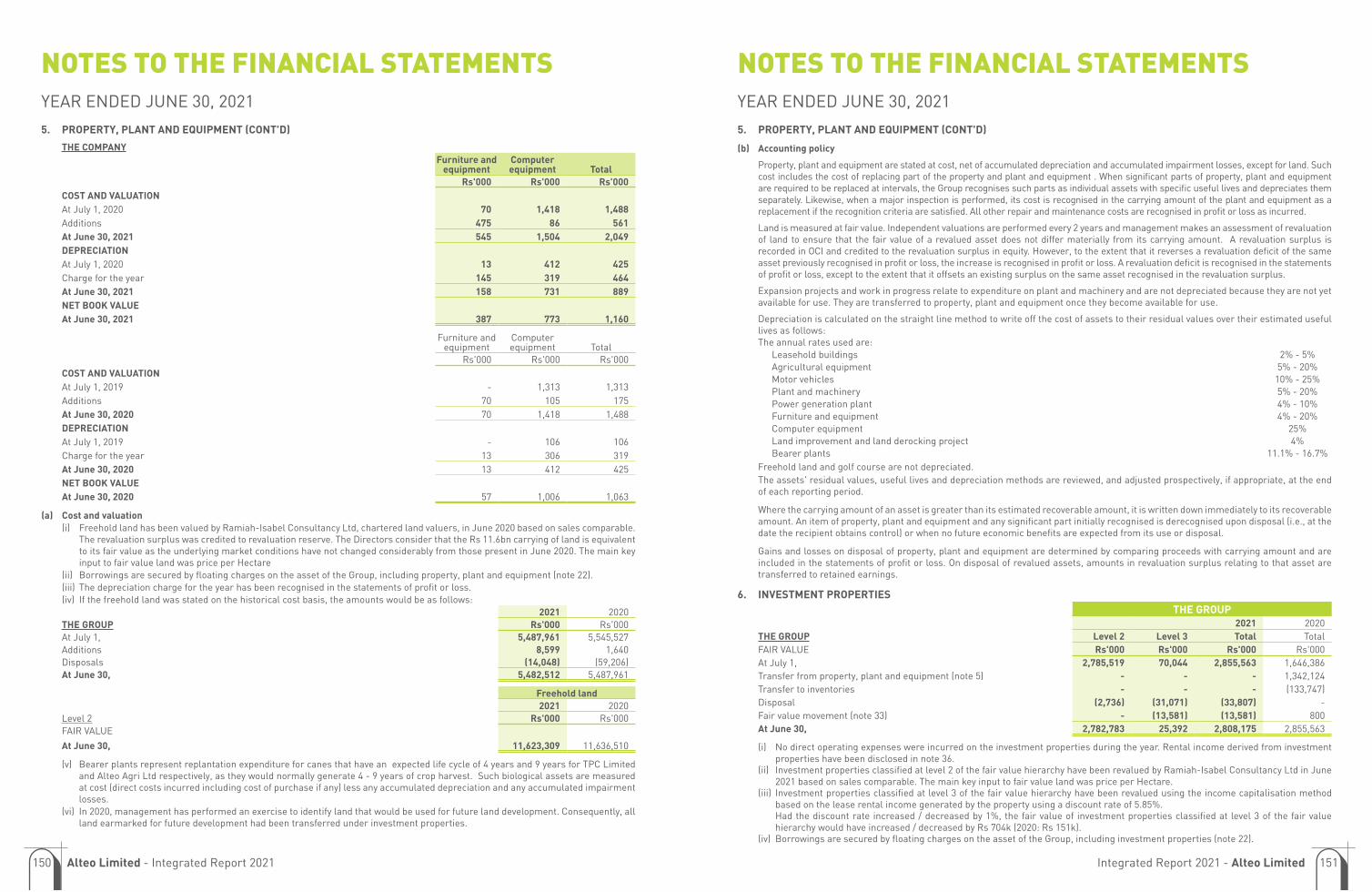

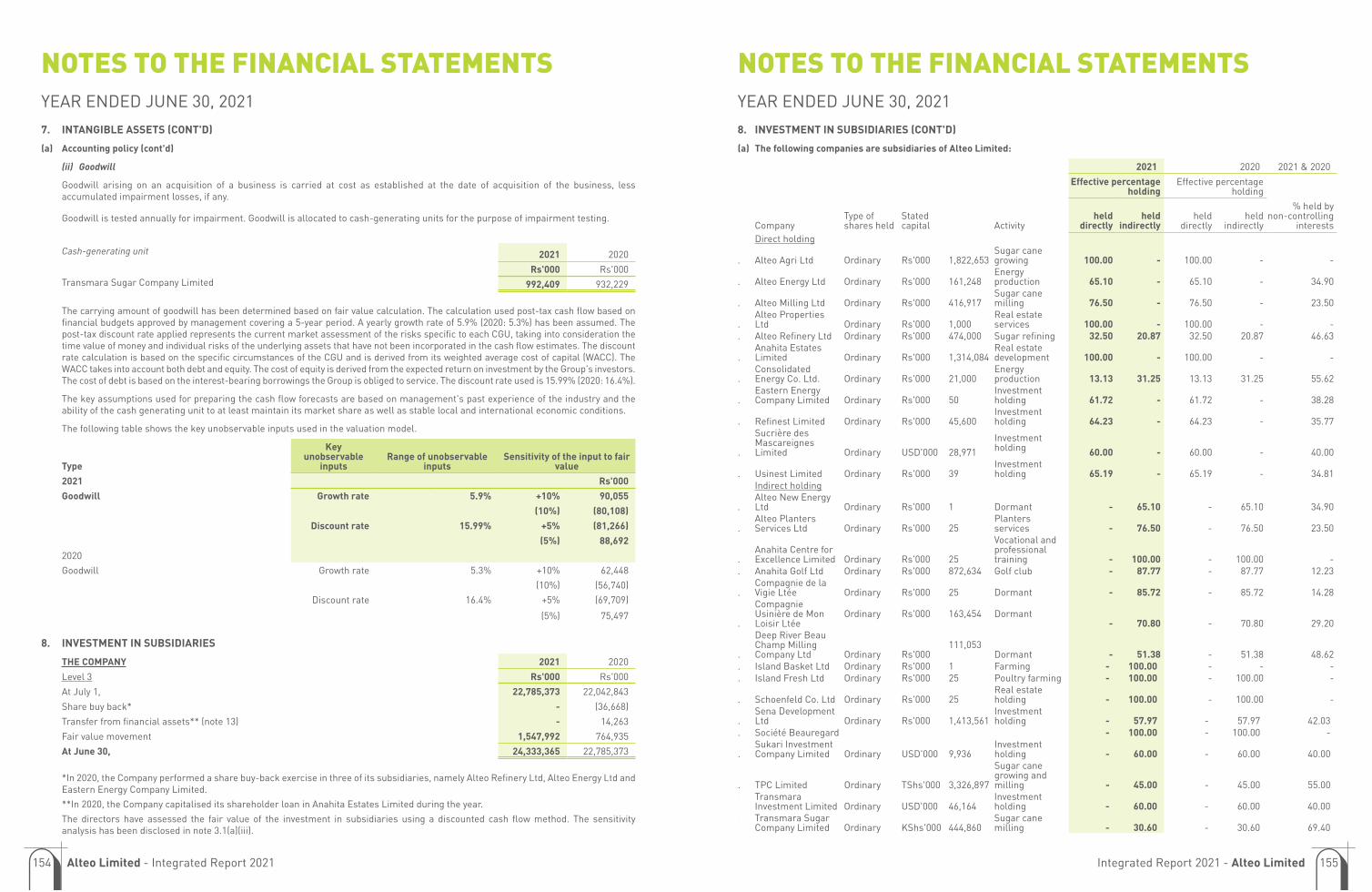

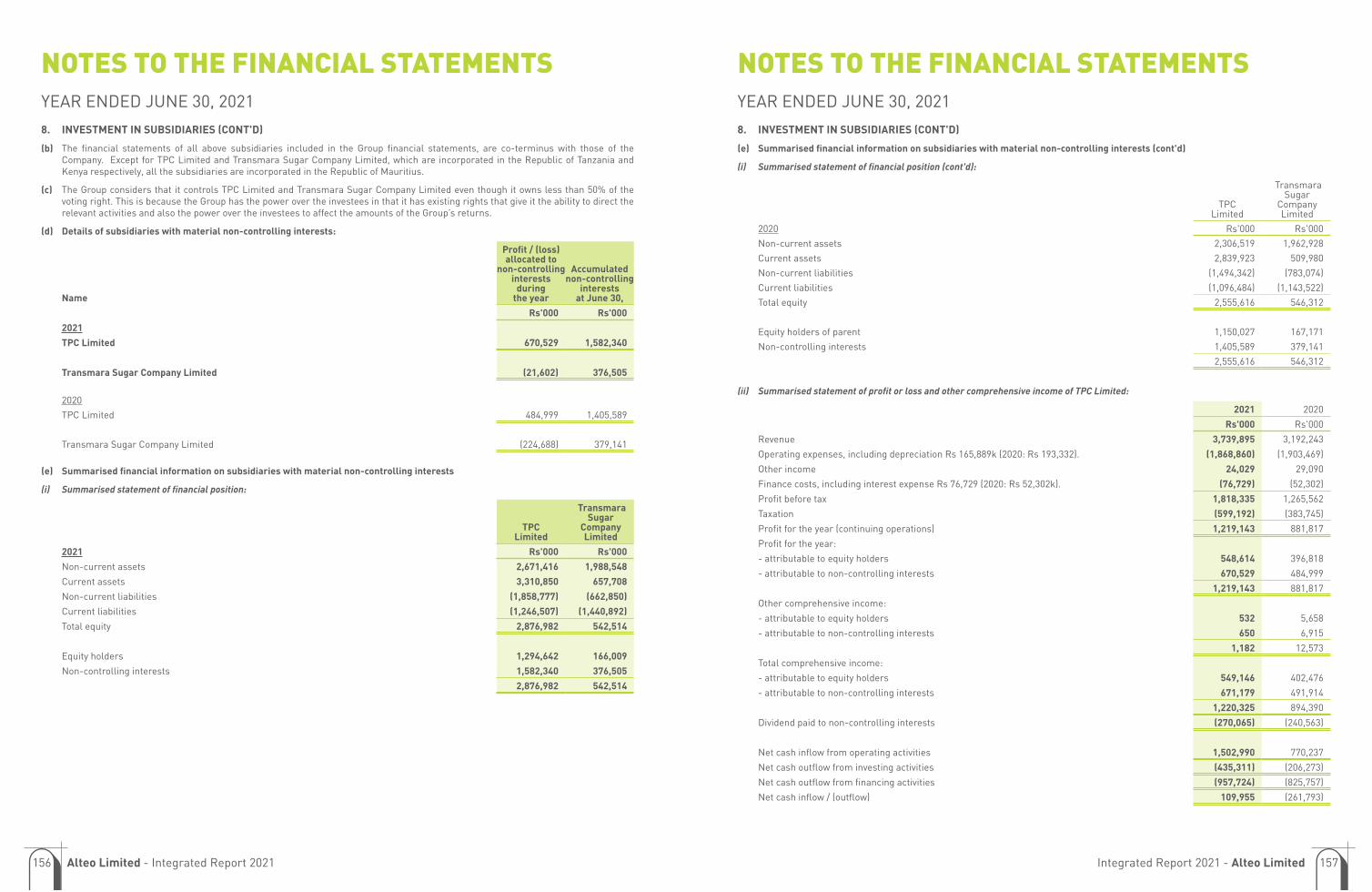

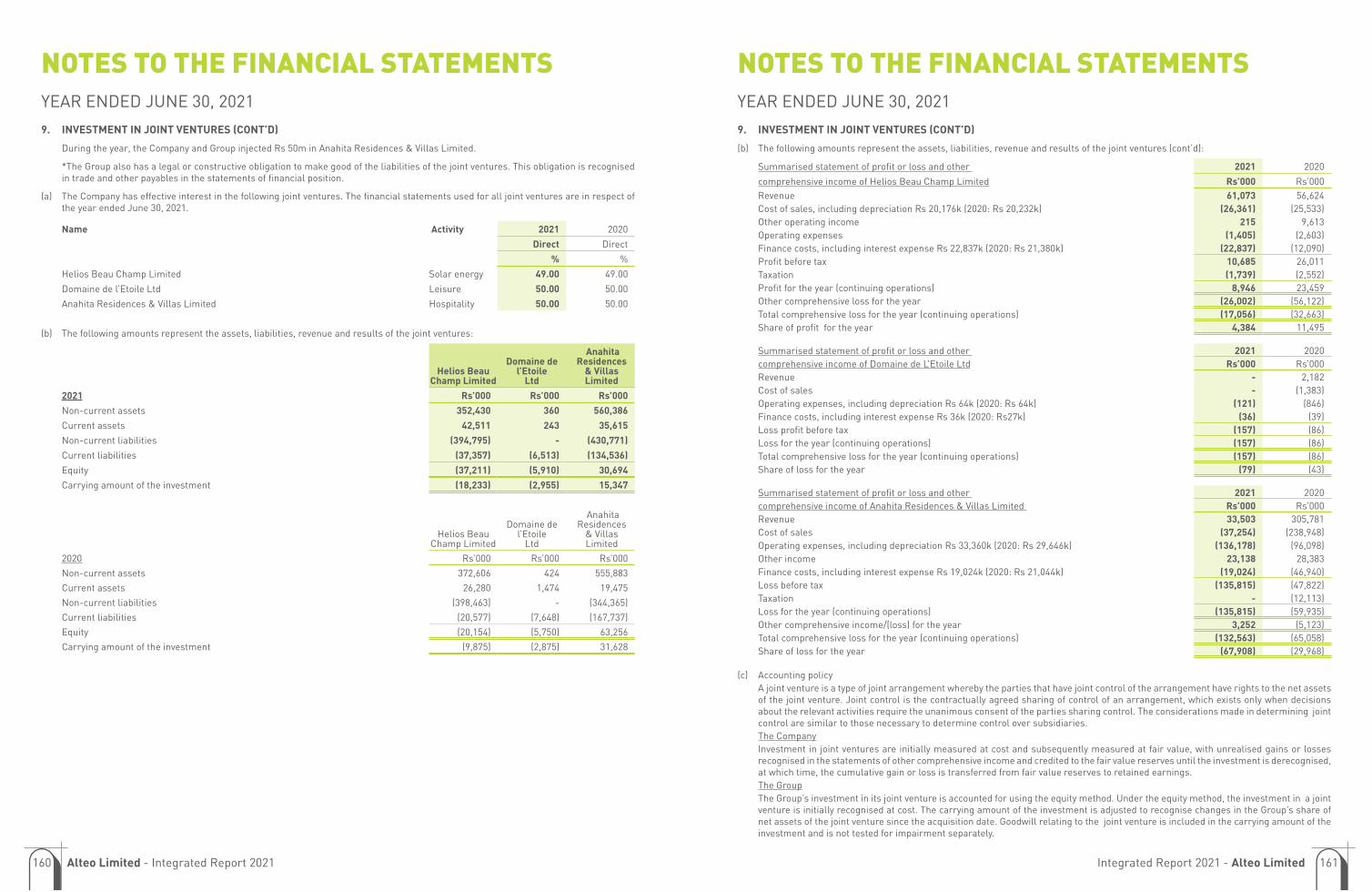

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INTEGRATED

REPORT

2021

Vision in Motion

Dear Shareholder,

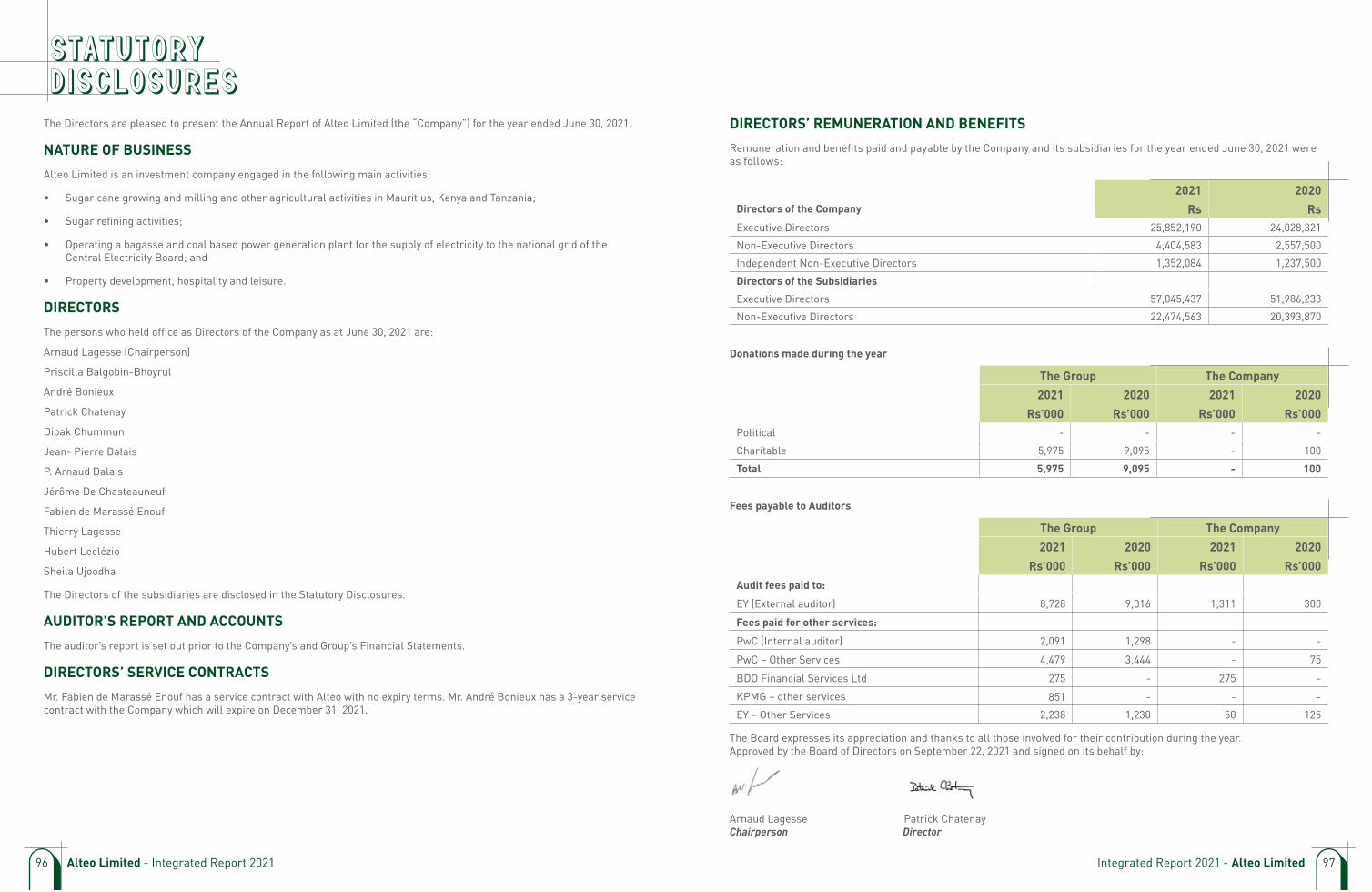

The Board of Directors of Alteo Limited (“Alteo” or the “Company”) is pleased to present to you the Annual Report of the Company for the fi nancial year ended June 30, 2021.

On behalf of the Board of Directors of Alteo, I would like to invite you to join us at the Annual Meeting of the Company.

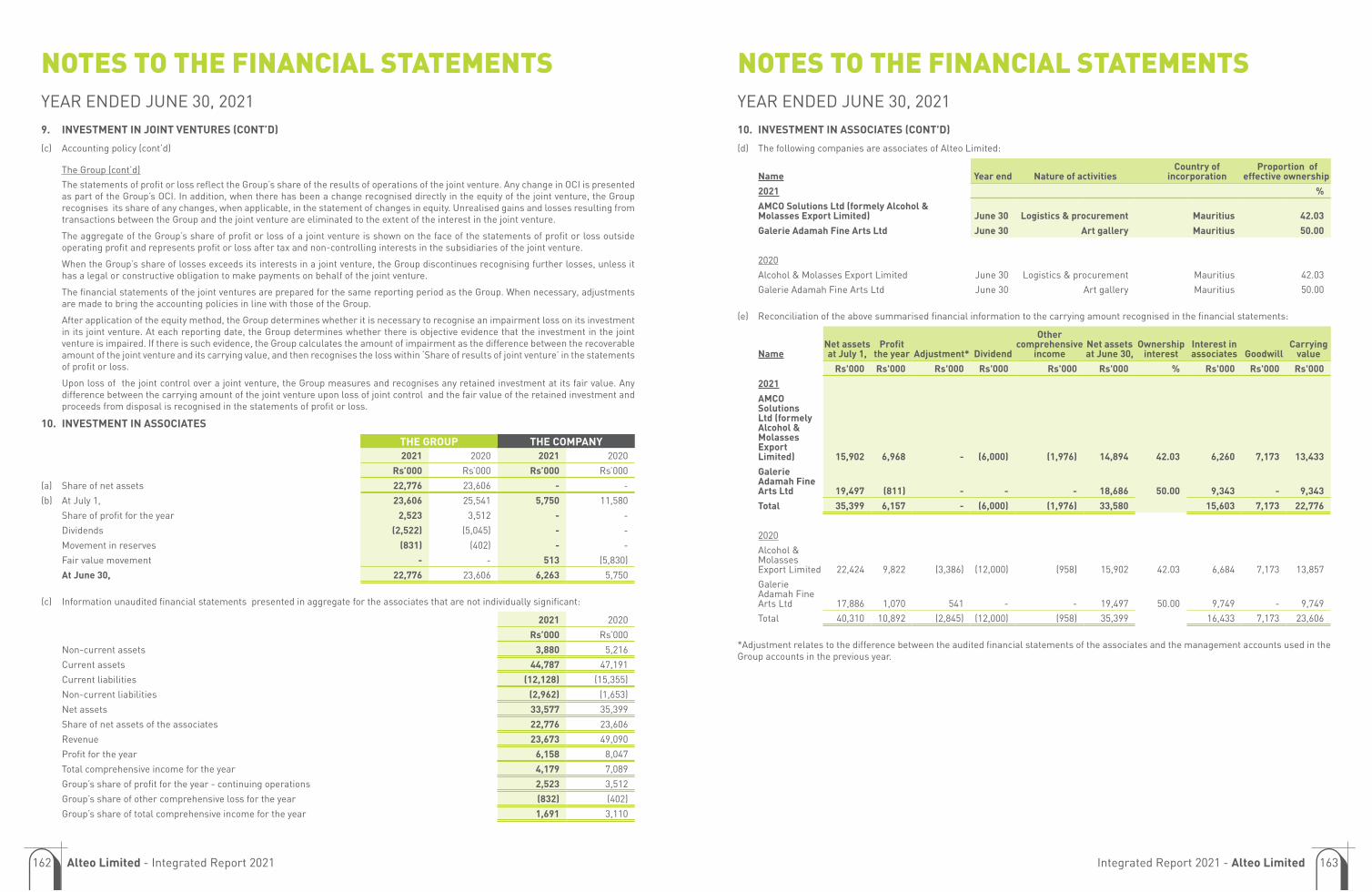

Date: December 10, 2021

Time: 10:00 a.m.

Place: Alteo Limited Vivéa Business Park Saint Pierre 81430 Mauritius

We look forward to seeing you.

Yours sincerely,

Arnaud Lagesse

Chairperson

Vision, Mission & Values 05 Alteo’s Profile 06 Corporate Information 07 Simplified Group Structure 08 Chairman’s Statement 12 Directors 16 CEO’s Report 18 Executives 22

Sugar 26 Energy 40 Property Development 46

Statutory Disclosures 96 Secretary’s Certificate 102

Independent Auditor’s Report to the Members 106 Statements of Financial Position 112 Statements of Profit or Loss 113 Statements of Other Comprehensive Income 114 Statements of Changes in Equity 115 Statements of Cash Flows 117 Notes to the Financial Statements 118

02

24

58

100

GROUP HIGHLIGHTS

OUR CLUSTERS

CORPORATE GOVERNANCE

FINANCIAL STATEMENTS

SCOPE, BOUNDARY AND REPORTING CYCLE

Alteo Limited’s Integrated Report 2021 provides material information relating to our strategy and business model, operating context, material risks, performance, prospects and governance. All performance data relates to the 12-month period ended June 30, 2021.

REPORTING PRINCIPLES

Alteo has applied the principles contained in the International Financial Reporting Standards (IFRS), the National Code of Corporate Governance for Mauritius 2016 and the Stock Exchange of Mauritius Listing Rules. This report has been prepared in accordance with the GRI Standards and the International <IR> Framework of the International Integrated Reporting Council (IIRC) has been used as reference.

The presentation of the group's key capitals as well as its business model are available on Alteo's website: http://www.alteogroup.com

MATERIALITY PROCESS

A materiality exercise and a stakeholder engagement were conducted in 2020 and 2021 to review the material topics under the GRI standards. The resulting report is available on Alteo’s website: http://www.alteogroup.com

EXTERNAL AUDIT

The annual independent statutory audit of the Group’s consolidated financial statements was performed by Ernst & Young.

Alteo Limited - Integrated Report 20212 3Integrated Report 2021 - Alteo Limited

4 Alteo Limited - Integrated Report 2021

To be a sustainable regional leader in sugarcane, renewable energy and property development

To responsibly create value through people development, strategic partnerships, innovative thinking, market focus and operational excellence

RESPECTCreate the right environment to nurture respect in each other

INTEGRITYBe our highest possible selves in everything we say or do

SPIRIT OF ENTREPRENEURSHIPHave the audacity to think big and the dare to act

EXCELLENCEOutperform to reach beyond the expected

Integrated Report 2021 - Alteo Limited 5

With a turnover of MUR 9,549 M in 2021 and a capitalisation of MUR 8.2 Bn (USD 195M) on 30 June 2021, Alteo is a key regional player in sugar, energy and property development.

Listed on the Official Market of the Stock Exchange of Mauritius (SEM), Alteo is the largest sugar producer in Mauritius and has a strong foothold in Africa with cane growing in Tanzania and sugar factories in Kenya and Tanzania. In 2020-2021, the Group produced 297,900 tonnes of raw sugar and 65,000 tonnes of premium special sugars.

In addition to its sugar activities, Alteo owns and operates three power plants (two in Mauritius, one in Tanzania) that exported 204.9 GWh to the national grids in 2020-2021. One of the Group’s core objectives is to increase its activities in the energy sector and to become an important player in renewable energy in Mauritius and Africa.

With 15,000 ha of freehold land in Mauritius, Alteo also has extensive experience in the property development sector. The group developed Anahita – a world-renowned luxury residential and golf estate – and launched several successful property developments aimed at the local market. Alteo now focuses on its strategic master plan aimed at creating value from its substantial land asset base through the development of a variety of innovative real estate projects in the east of Mauritius.

exported to the national grids in 2020-2021

tonnes of special sugars

power plants (two in Mauritius, one in Tanzania)

of freehold land in Mauritius

Alteo Limited - Integrated Report 20216

NAME OF COMPANYAlteo Limited

BUSINESS REGISTRATION NUMBERC17150285

REGISTERED OFFICEVivéa Business Park

81430 Saint Pierre, Mauritius

Tel: +230 402 9050

Fax: +230 432 0729

Email address: [email protected]

Website: www.alteogroup.com

EXTERNAL AUDITORSErnst & Young, Ebène, Mauritius

INTERNAL AUDITORSPricewaterhouseCoopers, Mauritius

COMPANY SECRETARYIntercontinental Secretarial Services Ltd

Level 3, Alexander House

35 Cybercity, Ebene 72201, Mauritius

Tel: +230 403 0800

Fax: +230 403 0801

BANKERSAfrAsia Bank Limited

Absa Bank Mauritius Limited

Bank One Limited

SBM Bank (Mauritius) Ltd

The Mauritius Commercial Bank Ltd

LEGAL ADVISERSENSafrica Mauritius

De Speville – Desvaux Chambers

Ahnee-Duval, Law Firm

SHARE REGISTRY & TRANSFER OFFICEMCB Registry & Securities Limited

Sir William Newton Street

Port-Louis, Mauritius

Tel: +230 202 5000

Fax: +230 208 1167

SUGARAlteo Agri Ltd / Alteo Milling Ltd

Union Flacq 41903, Mauritius

Tel: +230 402 33 00/ 650 34 00

Fax: +230 413 2699

Email: [email protected]

Website: www.alteogroup.com

ENERGYAlteo Energy Ltd

Union Flacq 41903, Mauritius

Tel: +230 402 33 00/ 650 34 00

Fax: +230 413 2699

Email: [email protected]

Website: www.alteogroup.com

PROPERTYAnahita Estates Limited

Vivéa Business Park

St Pierre 81430, Mauritius

Tel: +230 402 90 50

Fax: +230 432 0729

Email: [email protected]

Website: www.alteogroup.com

Anahita Residences & Villas Limited/ Anahita Golf Ltd

Beau Champ G.R.S.E. Mauritius

Tel: +230 402 2200

Fax: +230 402 2220

Email: [email protected]

Website: www.anahita.mu

Integrated Report 2021 - Alteo Limited 7

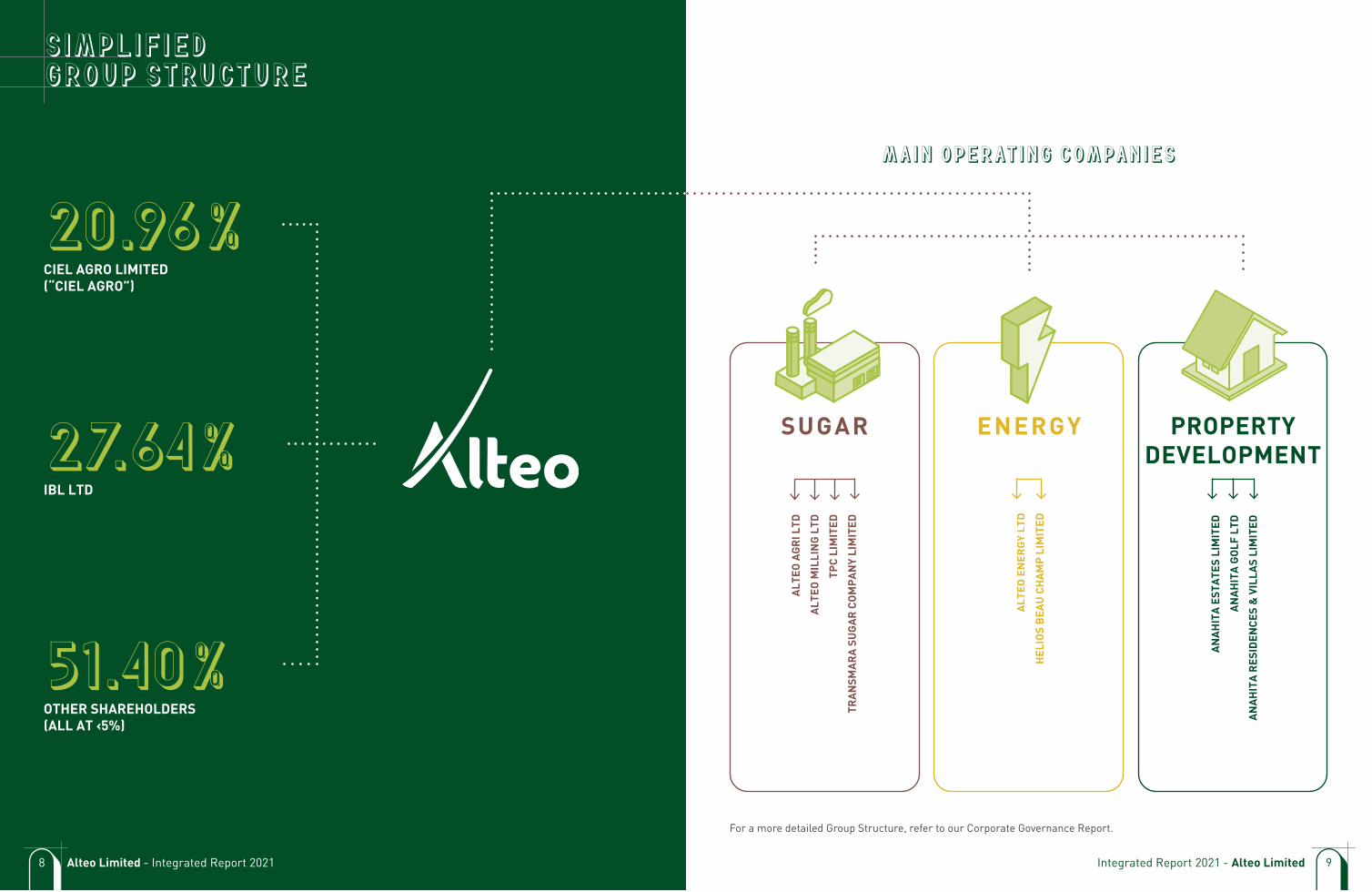

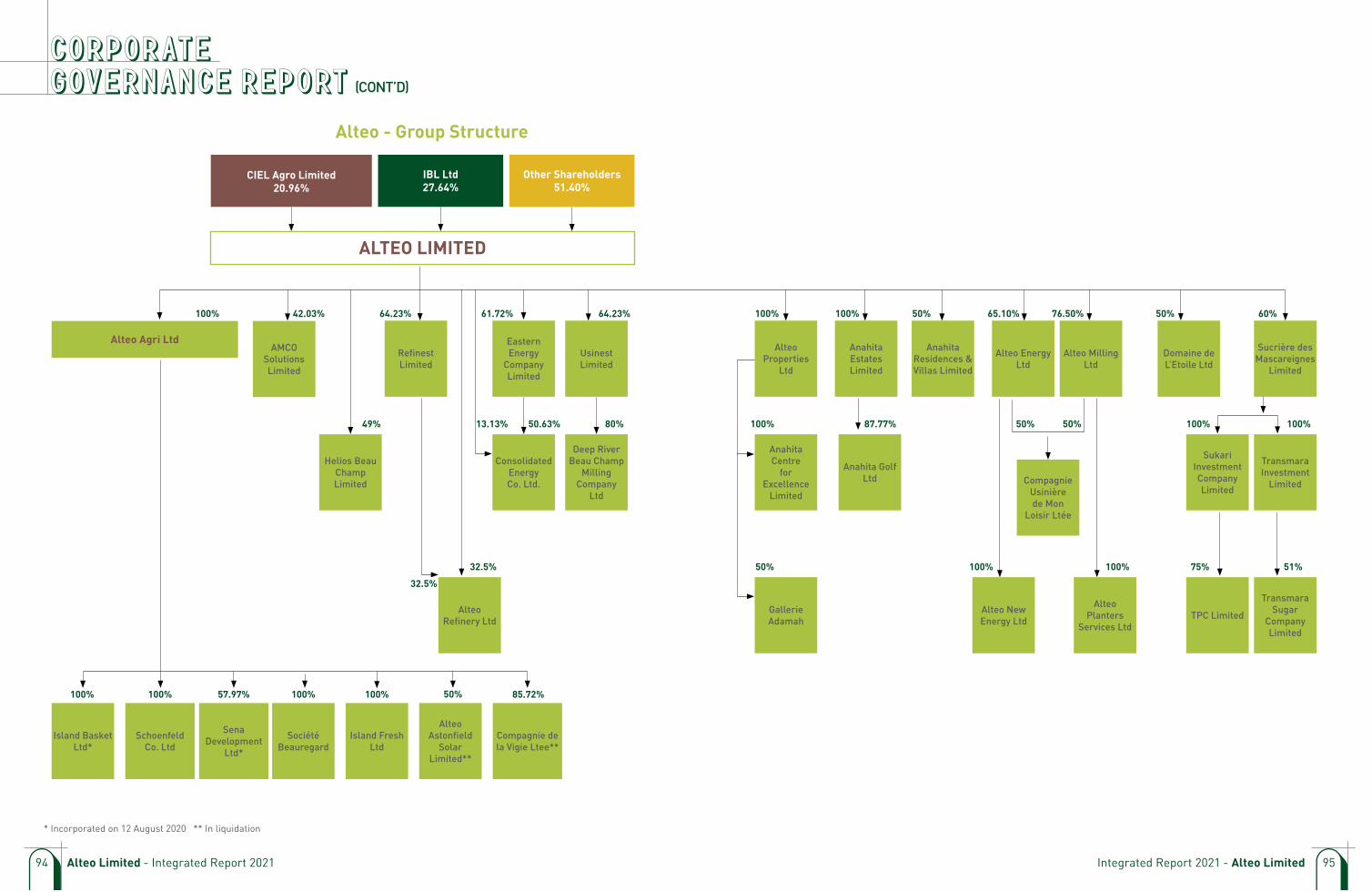

CIEL AGRO LIMITED (“CIEL AGRO”)

IBL LTD

OTHER SHAREHOLDERS (ALL AT ‹5%)

8 Alteo Limited - Integrated Report 2021

PROPERTY DEVELOPMENT

AN

AH

ITA

EST

ATE

S LI

MIT

ED

AN

AH

ITA

GO

LF L

TD

AN

AH

ITA

RES

IDEN

CES

& V

ILLA

S LI

MIT

ED

ALT

EO A

GR

I LTD

ALT

EO M

ILLI

NG

LTD

TPC

LIM

ITED

TRA

NSM

AR

A S

UG

AR

CO

MP

AN

Y LI

MIT

ED

ALT

EO E

NER

GY

LTD

HEL

IOS

BEA

U C

HA

MP

LIM

ITED

For a more detailed Group Structure, refer to our Corporate Governance Report.

SUGAR ENERGY

Integrated Report 2021 - Alteo Limited 9

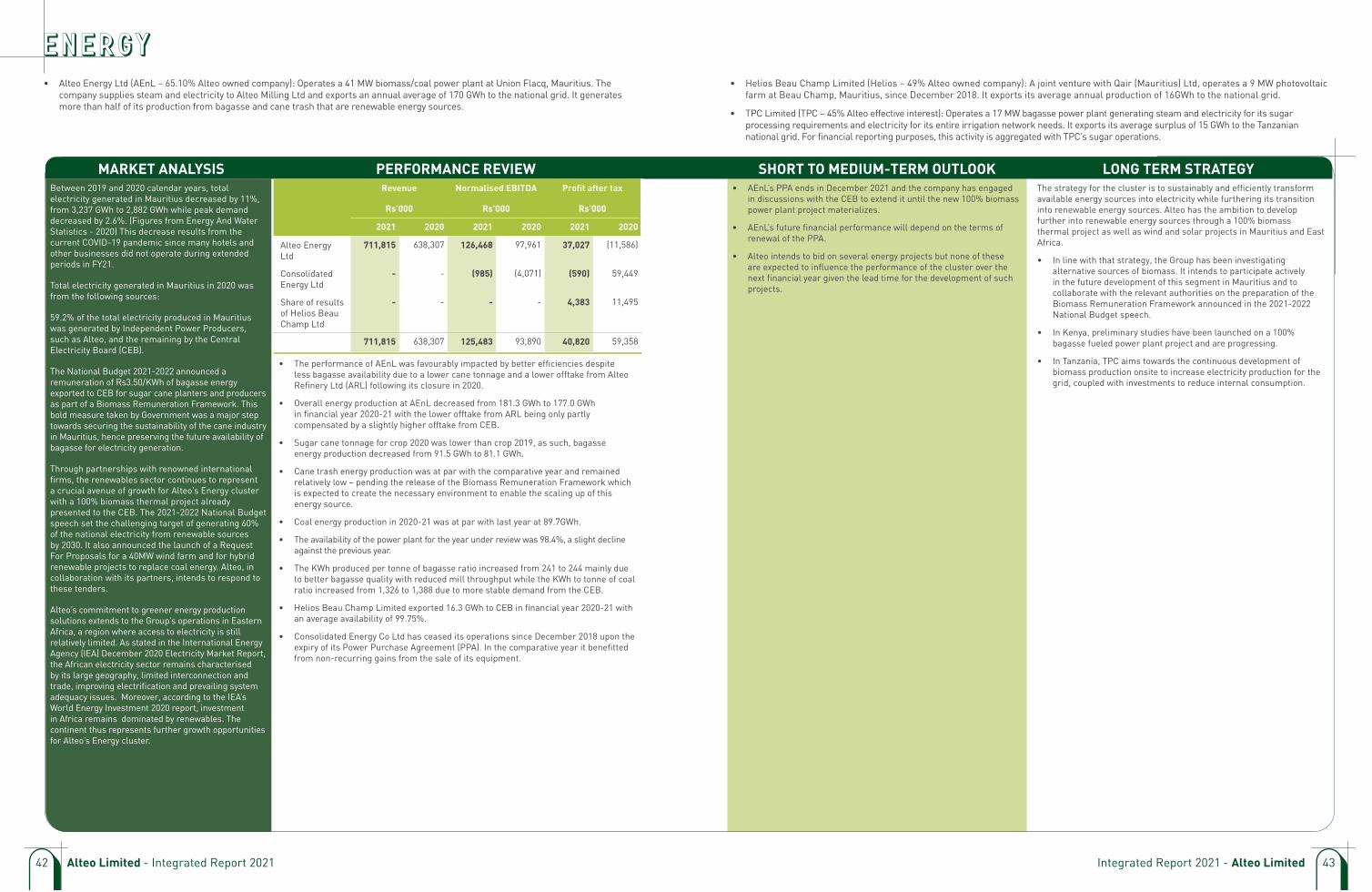

Our Sugar cluster had an excellent year, with improved results in all countries of operations.

12 Alteo Limited - Integrated Report 2021

Dear Shareholder,

On behalf of the Board, I am pleased to present Alteo’s very first Integrated Report for the financial year ended June 30, 2021.

This report condenses our performance and charts our achievements during a challenging year where we strived to achieve our ambitious objectives despite a constantly evolving socio-economic landscape.

Operating Context and Performance

In a difficult context still deeply marred by the ongoing pandemic, our group managed an even better performance than during the previous exercise mostly thanks to a rejuvenated sugar cluster, a declining interest rate environment and a depreciated Rupee. We thus noted significant improvements in our group revenue (+15%), normalised EBITDA (+82%), profit after tax (8 fold) as well as earnings per share (12 fold) for this financial year, despite an under-par performance from several activities.

Our Sugar cluster had an excellent year, with improved results in all countries of operations. Our Mauritian activities largely benefitted from the strengthening of sugar prices – resulting from an increased global sugar deficit coupled to tighter management costs, the depreciation of the Mauritian Rupee versus the Euro and the US Dollar – as well as from an increase in the production and sale of special sugars. This links directly to the bold strategy adopted by Alteo in recent years to revamp its Mauritian sugar operations with radical cost reductions and a refocusing on high value-added products. In Tanzania, our operations improved on last year’s already good performance with even higher profits that can be explained by a higher production of sugar, better prices on the domestic market as well as a favourable consumable biological asset fair value movement compared to FY20. Better domestic prices also benefitted our Kenyan operations where the factory reliability improved and sugar cane availability stabilised, leading to higher production and sales volumes.

The performance of our Energy cluster was positively impacted by better efficiencies despite a lower offtake for the second year running – the increased demand from the Central Electricity Board (CEB) was offset by the lower exports resulting from the closure of Alteo Refinery Ltd in 2020. Moreover, the cluster’s profit after tax showed a year on year decrease since the FY20 figure included a one-off gain from the sale of Consolidated Energy Co. Ltd’s equipment.

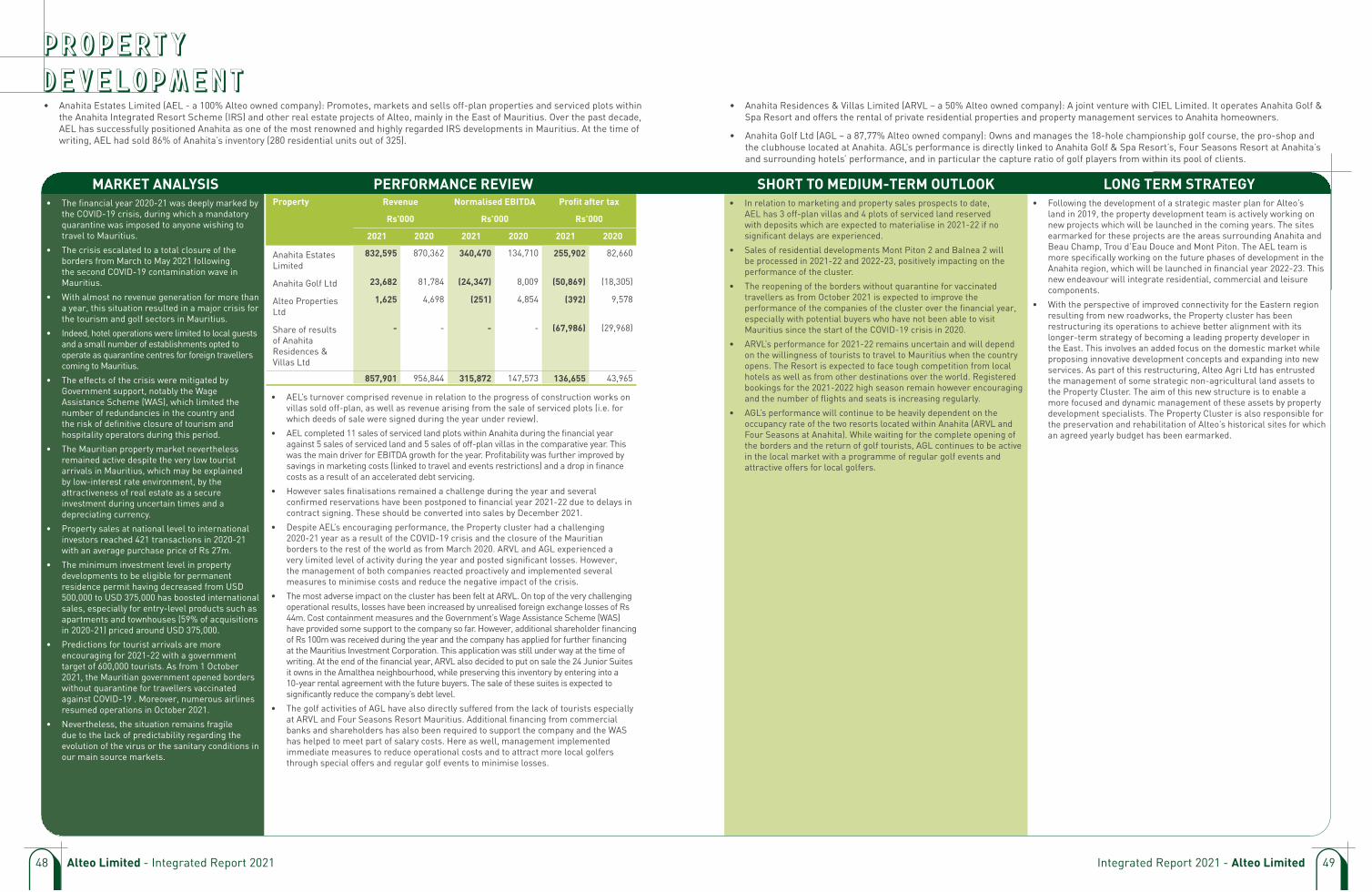

Our Property cluster was the most impacted by the ongoing COVID-19 crisis, with increased losses recorded by Anahita Golf & Spa Resort and Anahita Golf Club. Both entities logged negligible levels of activity during the year under review due to the lengthy border closure and the resulting absence of visitors. Thankfully, this situation was compensated by the sale of 11 serviced plots at Anahita which resulted in higher EBITDA generation.

Outlook

The COVID-19 pandemic will continue its disruptions around the world and our Property cluster will not be spared despite the recent reopening of Mauritian borders. We expect an uptick in activities at the Resort and the Golf in the coming months, but the impact of the last two years will not be easily erased from the books of these two entities. The forecast is brighter with regards to property development since reservations secured are expected to continue to help the cluster’s revenue for FY22.

The excellent performance of our Sugar cluster is expected to continue in the coming months, with stable prices in both Tanzania and Kenya. Regarding the latter, improved sugar cane availability and factory reliability are also inching us closer to the breakeven point.

In Mauritius, the recent announcement by the Government of the introduction of a Biomass Framework setting out a policy for remuneration of bagasse as a source of renewable energy has been met with widespread support. This mechanism was one of the industry’s main expectations and its implementation will be a major step for the future of the Mauritian sugar industry. Moreover, this bold move will not only strengthen the Sugar Industry, but it will also comfort Independent Power Producers (“IPP”) such as Alteo Energy Ltd that rely heavily on the availability of bagasse to produce electricity.

Integrated Report 2021 - Alteo Limited 13

Our Energy cluster’s performance for the next financial year will be dependent on the terms of renewal of the Power Purchase Agreement (“PPA”) between Alteo Energy Ltd and the CEB. Yet, thanks to the Biomass Framework, our cluster can now look to the future with bigger ambitions, such as the development of a 100% biomass power plant that would not only eclipse our venerable 35-year-old turbine’s efficiency, but also greatly contribute to the reduction of our country’s dependency on fossil fuels. Alteo has been committed to green energy for decades now and this commitment has only grown since the successful launch in 2018 of our Helios Beau Champ Photo Voltaic (“PV”) plant, in partnership with Qair. Our group is now looking forward to more investments in this sector, most notably with an additional PV plant as well as an ambitious project that will tap into the trade winds that blow across the east of our island.

Sustainability

Our move towards more renewables is not a passing fancy, it is part and parcel of our vision for the future: the creation of a sustainable Alteo. We have already taken the first steps on this journey – this Integrated Report is testament to that – and the materiality analysis conducted by our teams in Mauritius during FY21 has helped us better understand our value creation process and the impact of our activities on the communities we operate in, as well as on the environment. Much remains to be done, and our next milestone will be the creation of a materiality matrix for our African operations in the coming months. The sustainability agenda of our group is still in its infancy, but we are learning by doing and next year’s report will undoubtedly showcase more progress on this journey.

Acknowledgements

I would like to thank my fellow colleagues on the Board of Directors for their contribution throughout the year. I would specifically like to thank Jan Boullé and Amédée Darga, who both resigned from the Board during the year under review, and to welcome Priscilla Balgobin-Bhoyrul and Hubert Leclézio who graciously accepted to join our Board.

On behalf of Alteo’s Board of Directors, I would also like to express our gratitude to the people of Alteo. As was the case for countless businesses in Mauritius and around the globe, the past couple of years truly tested the mettle of our group and the value of our strategies, but our teams and management eagerly rose to the challenge under the leadership of our current Chief Executive Officer, André Bonieux. He will be leaving a more robust and resilient Alteo at the end of his contract in December 2021 and I wish to thank him for his hard work and dedication these past three years. Finally, it is my pleasure to officially welcome our new Chief Executive Officer, Fabien de Marassé Enouf, who will be taking the helm of Alteo as from January 1, 2022.

Arnaud LagesseChairperson

Alteo Limited - Integrated Report 202114

OUR MOVE TOWARDS MORE RENEWABLES IS NOT A PASSING FANCY, IT IS PART AND PARCEL OF OUR VISION FOR THE FUTURE: THE CREATION OF A

15Integrated Report 2021 - Alteo Limited

All profiles and full directorships can be viewed on: https://www.alteogroup.com/leadership

JEAN-PIERRE DALAISNon-Executive Director

JAN BOULLÉ Non-Executive Director

(Resigned on November 3, 2020)

PATRICK CHATENAYIndependent

Non-Executive Director

DIPAK CHUMMUNNon-Executive Director

ARNAUD LAGESSENon-Executive Chairperson

PRISCILLA BALGOBIN-BHOYRUL

Independent Non-Executive Director

(Appointed on December 11, 2020)

ANDRÉ BONIEUXExecutive Director

Alteo Limited - Integrated Report 202116

P. ARNAUD DALAISNon-Executive Director

JÉRÔME DE CHASTEAUNEUF

Non-Executive Director

AMÉDÉE DARGAIndependent Non-Executive Director

(Resigned on December 9, 2020)

THIERRY LAGESSENon-Executive Director

FABIEN DE MARASSÉ ENOUF

Executive Director

HUBERT LECLÉZIO(Appointed on November 25, 2020)

SHEILA UJOODHAIndependent Non-Executive

Director

Integrated Report 2021 - Alteo Limited 17

The ‘Alteo-nouveau’ is here: a leaner, meaner entity where strategy and activities have been through a wholesale rethinking.

18 Alteo Limited - Integrated Report 2021

Dear Shareholder, In my final report as Group CEO – I will be leaving at the end of my three-year contract on December 31, 2021 – I am happy to say that the ‘Alteo-nouveau’ is finally here: a leaner, meaner entity where strategy and activities have been through a wholesale rethinking. This has been a few years in the making, but I believe we are now primed for the future. How did we do it? I will get to it shortly.

The sugar prices were on the rise in FY20, and they are even better in FY21. The coming months are thus gearing up to be positive, but this is no surprise: the sugar industry evolves in a cyclic manner, with prices, demand and production rising and falling with almost clockwork-like regularity. We will profit from this positive phase and even expect prices to improve further, before inevitably falling again in the future. The difference now is that we are well and truly prepared to face tougher times. Benefitting from high prices is good, yet the ability to weather low returns and come out unscathed may be more important in the long run. This is what we believe has been achieved for our Mauritian sugar operations thanks to a combination of new strategy – cost-reduction exercises, a focus on special sugars production and a 100% mechanised agricultural production – and impactful public policy – the biomass remuneration framework announced by Government in July 2021.

Allow me here to go beyond FY21 and reflect on the past three years and the revamping of our local sugar operations. The restructuring of our agricultural activities with a focus on intensive mechanisation to drive costs down was not a simple exercise. For the past few years, we have progressively reduced the land under cane cultivation to focus only on areas that are mechanised and value creating. Yet, at the end of our derocking programme in a few years, we will be back to only 1,000 hectares less than in 2018, and all of it 100% mechanised, from plantation to harvest. Our agricultural operations will thus be much more productive - with less than 25% of the workforce it had in 2018 - and less costly too: since FY18, our production costs per ton of cane have dropped by 15 % (from USD 46 to USD 39) and it will drop further in the next five years. This is no mean feat, and it would never have been possible without the dedication and hard work of our teams. They showed grit and character, and for that they have my gratitude and my admiration. Hats off also to Arnaud d’Unienville who has been leading this major transformation.

On the sugar milling side, under the leadership of Sébastien Lavoipierre, we made the tough call to shift our strategy from refined sugar to special sugars. Sébastien and his team have managed the closure process and addressed the challenge of producing special sugars using the refinery’s infrastructure, enabling the group to significantly increase

WELCOME TO

Integrated Report 2021 - Alteo Limited 19

its special sugars production in a relatively short timeframe. This transition was made even more difficult by the nature of our milling operations where the costs are fixed and yet our cane volumes are falling. This is not a healthy model and it requires constant changes by the management.

Our African sugar operations are also on a positive trajectory. TPC Limited had a record breaking FY21, surpassing FY20’s already excellent performance thanks to the careful management of pests in the fields, a stable pricing environment, as well as significantly improved cane yields – a record productivity of 11.64 tonnes of cane per hectare per month. A special word here for our CEO in Tanzania, Marius Jacobs, who is setting the bar in only his first full year occupying this position.

Things are looking up too for Transmara Sugar Company Limited (TSCL), where a combination of stable prices, good weather, improved cane availability and better factory efficiency resulted in a significant increase in production and sales for FY21. Yet, it is safe to say that the past few years have been rough for our Kenyan sugar operations, and one of my focus areas as Group CEO was to help TSCL ‘weather the storm’. As such, the management team in Kenya led by Frederic North-Coombes and the executive team in Mauritius worked hand in hand to clearly define a way ahead and, to their credit, our colleagues in Kenya stuck with this plan through thick and thin. Thus, after three years, an aggressive capital expenditure programme, thousands of e-mails, meetings, and phone calls – production figures were closely monitored and discussed almost daily – I am happy to report that TSCL is now close to a break even, with a clear improvement in its short and medium-term outlook. Here again, I wish to express my appreciation for the hard work of our Kenya team. I have no doubt that a bright future lies ahead for them.

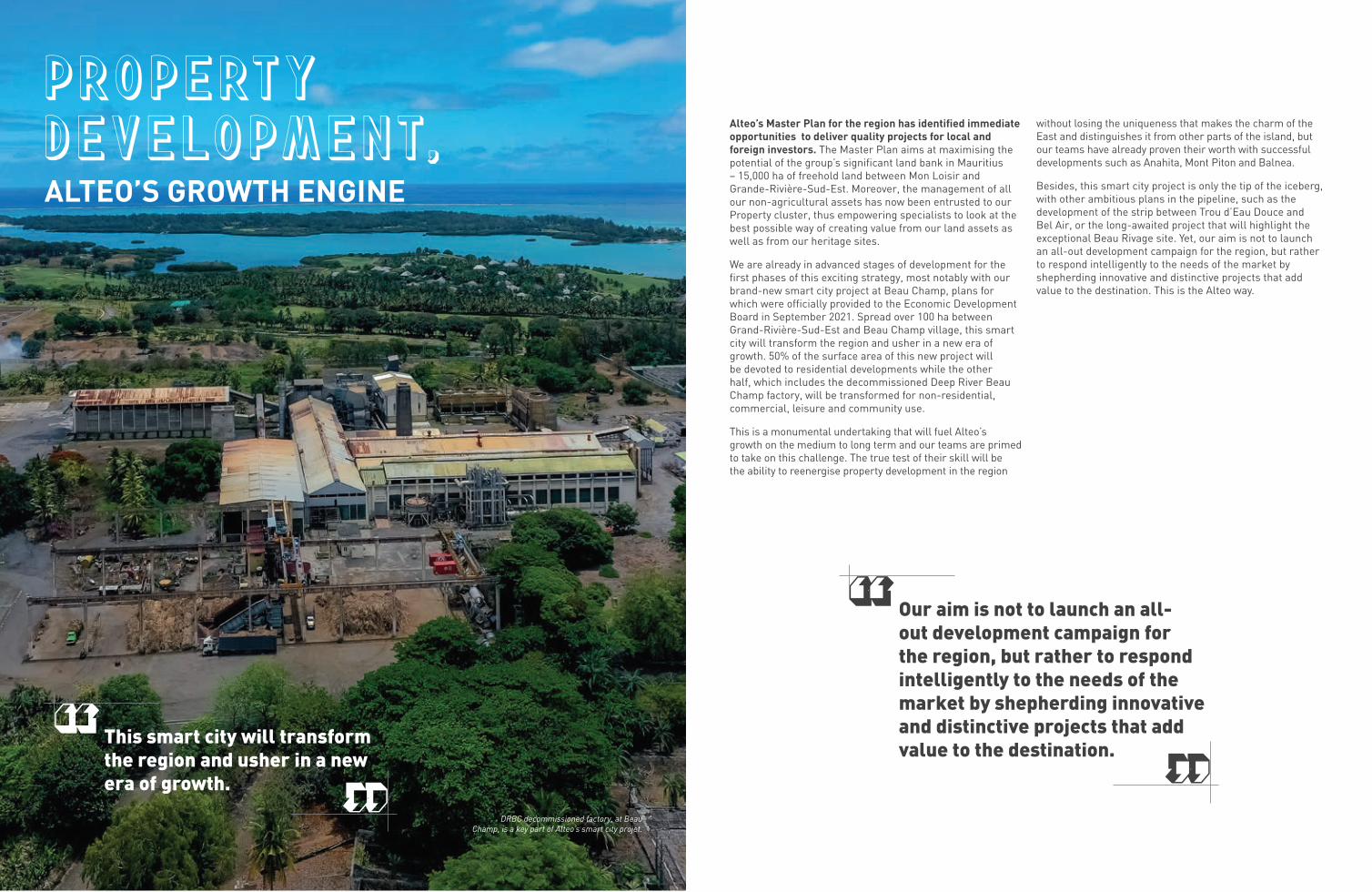

Such a prediction is also easy to make for our Property cluster even though it did not avoid repercussions from the COVID-19 pandemic. Our hotel and our golf suffered with little to no activity for almost two years but thanks to Government aids and investment from our shareholders, we managed to preserve all jobs as well as maintain the quality of our assets. With the full reopening of Mauritian borders in October 2021, we can look ahead with more confidence. Moreover, despite the circumstances, our property development initiatives have not slowed. Au contraire. The Master Plan for the development of our land asset base is ready and, to provide our teams with the means to achieve our ambitious objectives, we have been busy restructuring our cluster for the past few months. Thus, all the land and assets not under agricultural or industrial use is now under the aegis of our property experts who are already planning new projects and activities. These include an innovative smart city concept in the region of Beau Champ, between

Anahita and the Deep River Beau-Champ factory, that will target different segments locally and overseas, and undoubtedly help the growth of Alteo and the development of the East. In addition, we are working on the third phases of our two successful morcellement projects, Mont Piton and Balnéa, both of which will be promoted during FY22. Our property teams are also the now responsible for the restoration and preservation of a significant number of Alteo’s historical and cultural heritage, most notably chimneys and buildings that are more than a century old. As such, I can say that the Property cluster has both the past and the future of Alteo in its hands, and I could not be more confident in the journey ahead.

Our Energy cluster also has an interesting few years to look forward to. We are currently working on the renewal of the Power Purchase Agreement between Alteo Energy Ltd and the Central Electricity Board and are convinced that we will find common ground in the coming months. Our partnership with Qair – with whom we launched our first solar farm in 2018 – is as strong as ever and, together, we are developing solar and wind powered projects for the short to medium term, in line with our vision and the Government’s aim to curb the use of fossil fuels for local electricity production. Yet, while turning our backs on fossil fuel makes perfect sense, and is the right approach to ensure the sustainability of our group, I must admit that it is also linked to the one regret of my tenure as CEO of Alteo: despite all our efforts, we are yet to launch a new power plant to replace our ageing Union Flacq turbines after dropping the coal-bagasse hybrid power plant project. We are now working on a 100% biomass power plant project that shall be more climate-friendly and it is something we will be proud of for decades. I cannot wait to see this project turn to reality.

Final thoughts

A company or group is nothing without its people and my most cherished memories of these past few years are undoubtedly the moments I spent discussing with colleagues from all levels of the company, in Mauritius, in Kenya or in Tanzania, listening to their stories and discovering their work. They showed me what Alteo is really about and for that I will be eternally grateful.

Our group is now embarking on a new leg of its journey in the capable hands of a young and dynamic CEO, and I trust that you, as a shareholder, will be along for the ride.

I will happily be watching and cheering you on from the sidelines.

André BonieuxCEO

Alteo Limited - Integrated Report 202120

AND MY MOST CHERISHED MEMORIES ARE THE MOMENTS I SPENT DISCUSSING WITH COLLEAGUES FROM ALL LEVELS OF THE COMPANY, IN MAURITIUS, IN KENYA OR IN TANZANIA.

A COMPANY OR GROUP IS NOTHING WITHOUT

Integrated Report 2021 - Alteo Limited 21

ANDRÉ BONIEUXGroup CEO of Alteo

(Until December 31st, 2021)

MARIUS JACOBSCEO of TPC Limited

FABIEN DE MARASSÉ ENOUF

Deputy Chief Executive Officer

(Group CEO of Alteo as from January 1st, 2022)

SÉBASTIEN LAVOIPIERRE

COO Industrial Activities

STÉPHANE ISAUTIER

Regional Development Executive

PATRICE LEGRISCOO of Property

Development

All profiles can be viewed on: https://www.alteogroup.com/leadership

22 Alteo Limited - Integrated Report 2021

JEAN-ROBERT LINCOLN

Group Agricultural Development Executive

FREDERICK NORTH-COOMBESCEO of Transmara Sugar

Company Limited

ARNAUD D’UNIENVILLECOO Agricultural Activities

SOPHIE STRAUSS Human Resources

Executive

DAVID MARTIALCommercial and Business Development Director of Anahita Estates Limited

23Integrated Report 2021 - Alteo Limited

OUR CLUSTERS

OUR CLUSTERS

MAURITIUS • Alteo Agri Ltd (AAL – 100% Alteo owned company): Owns a total of 15,218 hectares of land in the eastern region of Mauritius. The company cultivates sugar cane over 8,245 hectares of land including some 427 hectares leased from Ferney Ltd. Around 84% of the sugar cane produced by Alteo Agri Ltd is processed by Alteo Milling Ltd and the remaining is processed by Terra Milling Ltd.

MARKET ANALYSIS PERFORMANCE REVIEW SHORT TO MEDIUM-TERM OUTLOOK LONG TERM STRATEGYSugar prices have been heavily influenced by the coronavirus-induced volatility in global commodity markets over the past year which led to significant movements of crude oil prices as well as the Brazilian currency – two key factors for sugar price formation. As from mid-February 2020, sugar prices fell significantly to progressively recover to reach pre-Covid levels as from November 2020.

Since then, on the back of an anticipated global deficit of 3.8m tonnes in 2021-22 (ISO market outlook August 2021), coupled to change in sourcing habits from just in time to just in case, prices on the world market rose sharply to reach USD 20 cent/lb in August 2021.

Adverse weather conditions in the main beet growing regions during the European summer 2020 coupled with aphid infestations in France, where the use of neonicotinoids (a range of pesticides) had been banned, have affected yields substantially and impacted the European sugar market positively. As reported by the European Commission, EU average ex-work prices for sugar reached EUR397 per tonne in June 2021, rising steadily since January’s EUR388 per tonne.

The price in the southern deficit regions of Europe, where most of the Mauritian white refined sugar is sold, was relatively stable over the period and closed at EUR456 per tonne in June 2021.

The Mauritian sugar industry benefited from price recoveries on the world market and depreciation of the Rupee as mentioned above and its total sales revenue for 2020-21 was consequently enhanced compared to the previous campaign. The ex-MSS price for the 2020 crop (financial year 2020-21) was finalised at Rs 14,062 per tonne, a 23% rise over the preceding period when it reached Rs 11,383 per tonne.

Sugar Mauritius

Revenue Normalised EBITDA Profit after tax

Rs’000 Rs’000 Rs’000

2021 2020 2021 2020 2021 2020

Alteo Agri Ltd

853,517 832,680 339,597 (74,150) 438,509 (381,526)

Alteo Milling Ltd

586,179 477,249 123,271 44,633 127,775 90,297

Alteo Refinery Ltd

55,726 349,454 42,526 115,606 86,713 16,822

Others 104,205 101,696 3,645 (10,367) 86,533 (40,665)

1,599,626 1,761,079 509,039 75,722 566,464 (315,072)

• AAL’s and AML’s turnover increased mainly on the back of better prices achieved in FY21 as explained under the market analysis earlier.

• The area harvested by AAL was reduced from 8,829 hectares in FY20 to 8,439 hectares FY21, a 4.4% drop in line with AAL’s strategy to gradually cease the manual cultivation of sugar cane.

• The sugar productivity in fields of AAL was reduced from 7.94 Tonnes Sugar Hectare (TSH) in 2019-2020 to 7.13 TSH in 2020-21. A drop of 10.18% due to unfavourable climatic conditions and above average ratoons age. The crop 2020 was declared an event year.

• Significant costs reductions were achieved in 2020-21 through the ongoing restructuring of AAL’s operations.

• AAL’s EBITDA and profit after tax were further enhanced by a Rs 238m favourable movement in the fair value of consumable biological assets and a reversal of past impairment of bearer biological assets amounting to Rs234m.

• AML’s sugar production totalled 104,050 tonnes in the financial year under review, a decrease of 17,653 tonnes compared to last year.

• As mentioned above, poor agro-climatic conditions prevailing in 2020-21, coupled with cane attrition, resulted in a reduction of 217,754 tonnes in the supply of sugar cane to the mill. This was partly compensated by a higher recovery rate of 9.93% compared to 9.62% in the previous year

• 62,139 tonnes of special sugars were produced during the financial year under review, which was higher than last year by 14,737 tonnes. This growth in the volume of special sugars was a major driver of this year’s profitability.

• In FY21 both AAL and AML earned compensations from the Sugar Insurance Fund as the 2020 crop was declared an event year.

• ARL’s production reached only 15,597 tonnes of refined sugar this year as the operations stopped in August 2020. The results of the refinery were positively impacted by overprovisions linked to the closure of operations

• Results shown under ‘Others’ arose mainly from the operations of Island Fresh Ltd, a poultry farming business, Deep River Beau Champ Milling Company Ltd and Compagnie Usiniere de Mon Loisir Ltee, previously sugar milling businesses which are now dormant, and Alteo Limited, the Group holding company.

• Since June 2021, the world raw sugar price has been on a predominantly upward trajectory, with the August average leaping higher to near USD 20cent/lb. The market structure between futures contracts has an upward leg to the March 2022 No11 position, after which values weaken.

• Most analysts have maintained their bullish positioning in the sugar market, however, ISO outlook for prices remains neutral as fundamentals do not indicate either a lack of supply, an excess of demand or an absence of readily available stock. The current high price environment and costly freight situation is further adding to the global trade challenge.

• In the EU, the 2021-22 production is anticipated at some 15 million tonnes, a substantial improvement over the virus-yellows affected harvest of 2020-21. The rise in world market values after June 2021 could translate into a significant prices rise in 2022, once forward contracted tonnages are consumed.

• In Mauritius, the MSS has recently announced a price estimate of Rs 15,000 per tonne for crop 2021, an improvement over last year largely explained by the depreciation of the Rupee against the main hard currencies and the increase in the price of sugar on the world market, which stood approximately at USD 20cent/lb in September 2021.

• Mauritius has signed preferential agreements with China and India, which will benefit the MSS and the industry. The quotas will increase gradually over the next 5 years to reach 50,000 tons and 40,000 tons quotas respectively which should support growth in special sugar volumes.

• In the last National Budget, the Government announced the implementation the biomass framework with a bagasse remuneration of Rs3.5 per Kwh which is equivalent to Rs3,300 per ton sugar accruing to planters and producers. This policy is a bold move towards securing the sustainability of the cane industry in Mauritius and should favourably affect the revenues of AAL and AML as from the next financial year.

• The sugar productivity in our fields is expected to be higher than the previous crop, however accrued sugar production will be lower due to a reduction in the harvested area.

MAURITIUS

To ensure the long-term viability of its Mauritian sugar operations, Alteo Agri Ltd aims at increasing its productivity and enhancing its processes to reduce production costs. To achieve these objectives, the following initiatives are ongoing:

• Ceasing cane cultivation in low yielding manually planted, maintained, and harvested fields

• De-rocking and preparing 150 hectares of cultivable land for mechanisation every year

• Pursuing investments in the mechanisation of all agricultural activities and implementation of best management practices by means of precision farming

• Re-organising management structures and workforce to adapt to mechanisation strategy

• Developing agricultural diversification projects

• Prioritising the production of special sugars and developing further the range of value-added direct consumption sugars, including an organic sugars range

• Developing other derivatives from sugar cane by-products

• Reorganising procurement structures to source key field and factory consumables directly from manufacturers and reduce input costs

• Continued support to G2G preferential tariff and quota agreements to supply special sugars

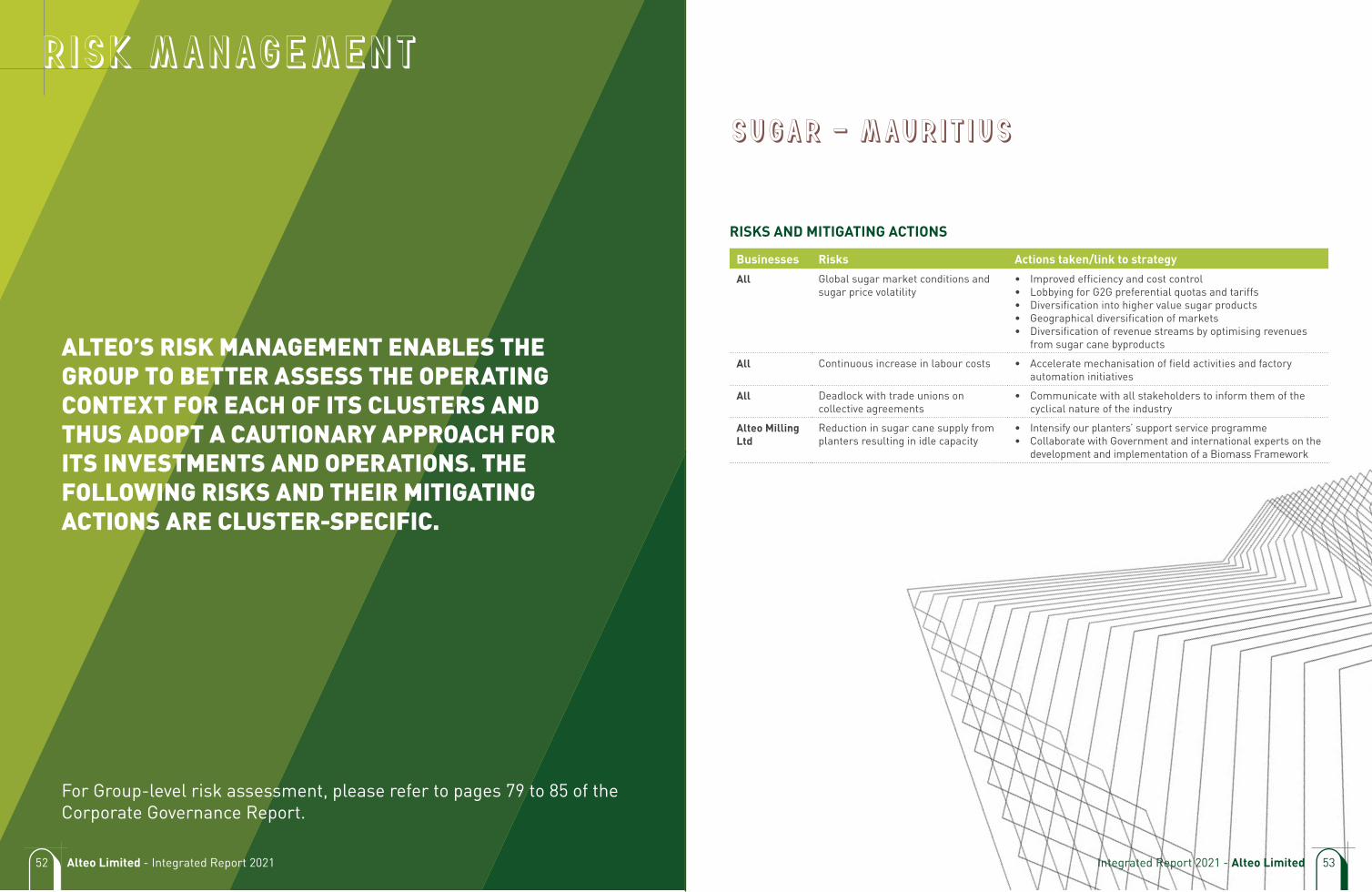

SUGAR CLUSTER (Mauritius, Tanzania, Kenya)

In line with its vision to become a sustainable regional leader in the sugar cane industry, Alteo has adopted a strategy consisting of:

• The continuous improvement of the efficiency of its processes and operations to reduce production costs and gain competitiveness in increasingly volatile markets;

• Revenue diversification through the development of new revenue streams from sugar cane by-products and innovation towards new added value end-user products, including:

• Optimising the use of bagasse and cane trash as renewable energy sources and inputs for its Energy operations;

• Creating more value from the transformation of molasses into downstream products and;

• Moving towards more value-added products such as premium direct consumption sugars;

• Market diversification through investments in high potential growth markets; and

• Collaboration with national regulators to help shape policies that will ensure the regional sugar industry’s sustainability.

28 Alteo Limited - Integrated Report 2021

MARKET ANALYSIS PERFORMANCE REVIEW SHORT TO MEDIUM-TERM OUTLOOK LONG TERM STRATEGYSugar prices have been heavily influenced by the coronavirus-induced volatility in global commodity markets over the past year which led to significant movements of crude oil prices as well as the Brazilian currency – two key factors for sugar price formation. As from mid-February 2020, sugar prices fell significantly to progressively recover to reach pre-Covid levels as from November 2020.

Since then, on the back of an anticipated global deficit of 3.8m tonnes in 2021-22 (ISO market outlook August 2021), coupled to change in sourcing habits from just in time to just in case, prices on the world market rose sharply to reach USD 20 cent/lb in August 2021.

Adverse weather conditions in the main beet growing regions during the European summer 2020 coupled with aphid infestations in France, where the use of neonicotinoids (a range of pesticides) had been banned, have affected yields substantially and impacted the European sugar market positively. As reported by the European Commission, EU average ex-work prices for sugar reached EUR397 per tonne in June 2021, rising steadily since January’s EUR388 per tonne.

The price in the southern deficit regions of Europe, where most of the Mauritian white refined sugar is sold, was relatively stable over the period and closed at EUR456 per tonne in June 2021.

The Mauritian sugar industry benefited from price recoveries on the world market and depreciation of the Rupee as mentioned above and its total sales revenue for 2020-21 was consequently enhanced compared to the previous campaign. The ex-MSS price for the 2020 crop (financial year 2020-21) was finalised at Rs 14,062 per tonne, a 23% rise over the preceding period when it reached Rs 11,383 per tonne.

Sugar Mauritius

Revenue Normalised EBITDA Profit after tax

Rs’000 Rs’000 Rs’000

2021 2020 2021 2020 2021 2020

Alteo Agri Ltd

853,517 832,680 339,597 (74,150) 438,509 (381,526)

Alteo Milling Ltd

586,179 477,249 123,271 44,633 127,775 90,297

Alteo Refinery Ltd

55,726 349,454 42,526 115,606 86,713 16,822

Others 104,205 101,696 3,645 (10,367) 86,533 (40,665)

1,599,626 1,761,079 509,039 75,722 566,464 (315,072)

• AAL’s and AML’s turnover increased mainly on the back of better prices achieved in FY21 as explained under the market analysis earlier.

• The area harvested by AAL was reduced from 8,829 hectares in FY20 to 8,439 hectares FY21, a 4.4% drop in line with AAL’s strategy to gradually cease the manual cultivation of sugar cane.

• The sugar productivity in fields of AAL was reduced from 7.94 Tonnes Sugar Hectare (TSH) in 2019-2020 to 7.13 TSH in 2020-21. A drop of 10.18% due to unfavourable climatic conditions and above average ratoons age. The crop 2020 was declared an event year.

• Significant costs reductions were achieved in 2020-21 through the ongoing restructuring of AAL’s operations.

• AAL’s EBITDA and profit after tax were further enhanced by a Rs 238m favourable movement in the fair value of consumable biological assets and a reversal of past impairment of bearer biological assets amounting to Rs234m.

• AML’s sugar production totalled 104,050 tonnes in the financial year under review, a decrease of 17,653 tonnes compared to last year.

• As mentioned above, poor agro-climatic conditions prevailing in 2020-21, coupled with cane attrition, resulted in a reduction of 217,754 tonnes in the supply of sugar cane to the mill. This was partly compensated by a higher recovery rate of 9.93% compared to 9.62% in the previous year

• 62,139 tonnes of special sugars were produced during the financial year under review, which was higher than last year by 14,737 tonnes. This growth in the volume of special sugars was a major driver of this year’s profitability.

• In FY21 both AAL and AML earned compensations from the Sugar Insurance Fund as the 2020 crop was declared an event year.

• ARL’s production reached only 15,597 tonnes of refined sugar this year as the operations stopped in August 2020. The results of the refinery were positively impacted by overprovisions linked to the closure of operations

• Results shown under ‘Others’ arose mainly from the operations of Island Fresh Ltd, a poultry farming business, Deep River Beau Champ Milling Company Ltd and Compagnie Usiniere de Mon Loisir Ltee, previously sugar milling businesses which are now dormant, and Alteo Limited, the Group holding company.

• Since June 2021, the world raw sugar price has been on a predominantly upward trajectory, with the August average leaping higher to near USD 20cent/lb. The market structure between futures contracts has an upward leg to the March 2022 No11 position, after which values weaken.

• Most analysts have maintained their bullish positioning in the sugar market, however, ISO outlook for prices remains neutral as fundamentals do not indicate either a lack of supply, an excess of demand or an absence of readily available stock. The current high price environment and costly freight situation is further adding to the global trade challenge.

• In the EU, the 2021-22 production is anticipated at some 15 million tonnes, a substantial improvement over the virus-yellows affected harvest of 2020-21. The rise in world market values after June 2021 could translate into a significant prices rise in 2022, once forward contracted tonnages are consumed.

• In Mauritius, the MSS has recently announced a price estimate of Rs 15,000 per tonne for crop 2021, an improvement over last year largely explained by the depreciation of the Rupee against the main hard currencies and the increase in the price of sugar on the world market, which stood approximately at USD 20cent/lb in September 2021.

• Mauritius has signed preferential agreements with China and India, which will benefit the MSS and the industry. The quotas will increase gradually over the next 5 years to reach 50,000 tons and 40,000 tons quotas respectively which should support growth in special sugar volumes.

• In the last National Budget, the Government announced the implementation the biomass framework with a bagasse remuneration of Rs3.5 per Kwh which is equivalent to Rs3,300 per ton sugar accruing to planters and producers. This policy is a bold move towards securing the sustainability of the cane industry in Mauritius and should favourably affect the revenues of AAL and AML as from the next financial year.

• The sugar productivity in our fields is expected to be higher than the previous crop, however accrued sugar production will be lower due to a reduction in the harvested area.

MAURITIUS

To ensure the long-term viability of its Mauritian sugar operations, Alteo Agri Ltd aims at increasing its productivity and enhancing its processes to reduce production costs. To achieve these objectives, the following initiatives are ongoing:

• Ceasing cane cultivation in low yielding manually planted, maintained, and harvested fields

• De-rocking and preparing 150 hectares of cultivable land for mechanisation every year

• Pursuing investments in the mechanisation of all agricultural activities and implementation of best management practices by means of precision farming

• Re-organising management structures and workforce to adapt to mechanisation strategy

• Developing agricultural diversification projects

• Prioritising the production of special sugars and developing further the range of value-added direct consumption sugars, including an organic sugars range

• Developing other derivatives from sugar cane by-products

• Reorganising procurement structures to source key field and factory consumables directly from manufacturers and reduce input costs

• Continued support to G2G preferential tariff and quota agreements to supply special sugars

SUGAR CLUSTER (Mauritius, Tanzania, Kenya)

In line with its vision to become a sustainable regional leader in the sugar cane industry, Alteo has adopted a strategy consisting of:

• The continuous improvement of the efficiency of its processes and operations to reduce production costs and gain competitiveness in increasingly volatile markets;

• Revenue diversification through the development of new revenue streams from sugar cane by-products and innovation towards new added value end-user products, including:

• Optimising the use of bagasse and cane trash as renewable energy sources and inputs for its Energy operations;

• Creating more value from the transformation of molasses into downstream products and;

• Moving towards more value-added products such as premium direct consumption sugars;

• Market diversification through investments in high potential growth markets; and

• Collaboration with national regulators to help shape policies that will ensure the regional sugar industry’s sustainability.

• Alteo Milling Ltd (AML – 76.5% Alteo owned company): Operates a sugar mill with a crushing capacity of 8,500 tonnes of cane per day (TCD) equivalent to an annual crushing capacity of 1,450,000 tonnes. The mill sources sugar cane from AAL (50%), other corporate planters (20%) and small planters (30%) from its factory area. Out of an average annual sugar production of 105,000 tonnes, 40,000 tonnes come in the form of plantation white sugar for refining, while direct consumption sugars or special sugars account for 65,000 tonnes. The plantation white sugar is transferred by AML to Omnicane Operations Ltd.

• Alteo Refinery Ltd (ARL – 53.4% Alteo owned company): Closed its operations on 6 August 2020 as part of industry wide reform measures to address the declining trend in sugar cane production nationally and the resulting excess refining capacities. ARL currently rents its warehouse to the Mauritius Sugar Syndicate (MSS) for storage of plantation white sugar and its production equipment to AML for the production of special sugars.

29Integrated Report 2021 - Alteo Limited

Alteo embarked on an ambitious derocking exercise to annually transform 150 ha of ‘manual’ fields into 100% mechanised fields.

WITHIN OUR AGRICULTURAL ACTIVITIES

MAURITIUS

Trapped between the proverbial hammer and anvil, Mauritian sugar producers such as Alteo have been plagued for decades by high local production costs versus fluctuating prices on world and European markets. Alteo’s solution: “Doing more, with less.” While this may sound like a simple statement, it has become the mantra, the guiding principle of our agricultural operations in Mauritius for the past three years, helping us reduce drastically our costs while improving our productivity in a relatively short time span.

The efforts of our teams were vindicated when Alteo Agri recorded operational profits for FY21, a first since Alteo’s creation in 2012, all thanks to its two-pronged strategy: increasing our productivity and focusing on mechanised precision agriculture.

As a context, when this ambitious plan was put into motion during FY18, production cost was estimated at USD 46.6 per ton cane, with 1990 employees (including permanent and seasonal workers), 10,000 ha under cane production and less than half this area fully mechanised. What changed? First, all employees who wished to leave the company were provided with an optional voluntuntarily departure scheme that recognised their contribution to Alteo over the years. This allowed for a complete rethinking of our resource allocation and further motivated our full-on foray into mechanised precision agriculture since we were short of the number of employees needed to manage fields that required manual (and cost-intensive) intervention. At the same time, Alteo invested massively in new equipment to plant, maintain and harvest cane while also embarking on an ambitious derocking exercise: annually transforming 150 ha of ‘manual’ fields into 100% mechanised fields.

The results of this strategy cannot be understated: 960 permanent and seasonal workers are now employed by Alteo Agri Ltd, the area under cane has dropped to 8,000 ha (almost all of it fully mechanised) and, more importantly,

the cost of production has now reached USD 39.5, 15% less than in FY18. The endgame is to increase the area under cane cultivation while achieving a production cost of USD 30 by FY26, a 35% decrease since the start of the project, and the teams are well underway to reaching this target.

In time, this will make Alteo more competitive and allow us to weather significant price fluctuations on the world and European sugar markets. Yet, the ambitions of our agricultural teams do not stop there, for they have already set their sights on their next target: a strategic replantation campaign to improve yields. The transformation of Alteo is well and truly on track.

• TPC Limited (TPC – 45% Alteo effective interest): Cultivates sugar cane, produces and sells sugar, electricity, and molasses on the domestic market. TPC has leasehold rights on some 16,000 hectares of land, of which 8,000 hectares are under irrigated sugar cane cultivation. It operates a 4,800 Tons of cane per day (TCD) mill which sources its entire sugarcane supply from the estate. Further, TPC produces electricity to power its factory, operations, housing and irrigation networks, and exports the surplus to the grid.

TANZANIA

MARKET ANALYSIS PERFORMANCE REVIEW SHORT TO MEDIUM-TERM OUTLOOK LONG TERM STRATEGY• Sugar prices in Tanzania decreased slightly at the

start of the financial year but then recovered well as from December 2020 further increasing towards the end of the financial year. The result was that TPC achieved a marginal increase in the year-on-year average price. The stable supply of sugar in the market from improved local production coupled with appropriate amounts of imports to fill the gap sugar season, has continued to ensure this stable pricing environment. The stable Tanzanian Shilling has also played its role to support this low inflationary environment.

• As in the preceding three years, the sugar producers were tasked with importing sugar during the gap season. This year, licenses amounting to a total of 50,000 tonnes were issued by Government via the Sugar Board of Tanzania in the final quarter of the financial year.

• The Tanzanian market remained protected from the low world sugar prices as a result of the 35% import duty and controlled import volumes which were licensed by Government.

• The sustained market stability and Government investment drives has resulted in significant investments to increase local sugar production from both incumbent and new investors to the industry in Tanzania. These investments will likely result in Tanzania being self-sufficient in sugar in the medium to longer term resulting in a more competitive industry than has been the case before.

• The COVID-19 pandemic had a limited impact both on consumption and production in Tanzania as the country remained open as in the prior year with no enforced lockdowns during the pandemic.

Tanzania Revenue Normalised EBITDA Profit after tax

Rs’000 Rs’000 Rs’000

2021 2020 2021 2020 2021 2020

TPC Limited

3,739,895 3,192,243 2,126,806 1,506,288 1,219,142 881,817

SML & SIL - - 130,227 79,017 14,185 (20,759)

3,739,895 3,192,243 2,257,033 1,585,305 1,233,327 861,058

• Through the combined impact of a volume increase of 5% and a price increase of 2.3% in USD and a weaker Mauritian Rupee, the turnover of TPC increased substantially in financial year 2020-21.

• Sugar production increased as cane yields recovered from 119 tonnes per hectare in the prior year to 133 tonnes per hectare as a result of improved climatic conditions, resulting in a lower water table, and better treatment protocols of the Yellow Sugarcane Aphid (YSA) which had weighed negatively on the cane growth in the prior year. The achieved yields for the year reflected the best ever recorded yield productivity at 11.64 tonnes of cane per hectare per month.

• Cane yields have continued their strong performance at the start of the 2021-22 season with the best ever yields achieved as at the end of September 2021. The sustained investments in better irrigation, higher fertilisation and improved YSA controls bode well for the season although the lower rainfall during the long rains and prevalence of YSA may have adverse impacts later in the season.

• Cane quality and sucrose content have also been in line with high levels achieved in the financial year 2020-21 with the factory performing in line with expectations.

• As a result of the good start to the year, it is expected that sugar production will be higher in financial year 2021-22.

As Tanzania is likely to remain a deficit sugar market in the short term, Alteo’s strategy for its Tanzanian sugar business is to continue to grow its sugar supply to the domestic market, while creating further added value from sugar cane by-products. The cornerstone of its strategic priorities is the sustainable management of natural resources to ensure simultaneous business health and wellbeing of local communities living on the estate. These include:

• Sustained investment in water supply security with new boreholes to maintain and improve cane yields, while at the same time ensuring sustainable use of underground water resources;

• Sustained investment to convert flood irrigation areas to semi solid and drip irrigation systems to improve efficiency of water use (i.e, increased water productivity);

• Continued development of 440 hectares for new sugar cane cultivation through soil reclamation in regions of relatively high salinity and sodicity;

• Phased introduction of mechanical harvesting and evaluation of its impact on production costs and cane yields, in anticipation of rising labour costs and more stringent environmental legislation towards cane burning;

• Phased investments in the factory to stabilize crushing rate, improve efficiencies and treat effluents; and

• Continuing the feasibility study of an investment in a distillery to generate additional value from molasses to produce Extra Neutral Alcohol (ENA) for the domestic market.

32 Alteo Limited - Integrated Report 2021

• Sucrière des Mascareignes Limited (SML – 60% Alteo owned company) and Sukari Investment Company Limited (SIL – 60% Alteo effective interest): Alteo’s investment in TPC is held through SML, a management and intermediary holding company and SIL, an intermediary holding company.

MARKET ANALYSIS PERFORMANCE REVIEW SHORT TO MEDIUM-TERM OUTLOOK LONG TERM STRATEGY• Sugar prices in Tanzania decreased slightly at the

start of the financial year but then recovered well as from December 2020 further increasing towards the end of the financial year. The result was that TPC achieved a marginal increase in the year-on-year average price. The stable supply of sugar in the market from improved local production coupled with appropriate amounts of imports to fill the gap sugar season, has continued to ensure this stable pricing environment. The stable Tanzanian Shilling has also played its role to support this low inflationary environment.

• As in the preceding three years, the sugar producers were tasked with importing sugar during the gap season. This year, licenses amounting to a total of 50,000 tonnes were issued by Government via the Sugar Board of Tanzania in the final quarter of the financial year.

• The Tanzanian market remained protected from the low world sugar prices as a result of the 35% import duty and controlled import volumes which were licensed by Government.

• The sustained market stability and Government investment drives has resulted in significant investments to increase local sugar production from both incumbent and new investors to the industry in Tanzania. These investments will likely result in Tanzania being self-sufficient in sugar in the medium to longer term resulting in a more competitive industry than has been the case before.

• The COVID-19 pandemic had a limited impact both on consumption and production in Tanzania as the country remained open as in the prior year with no enforced lockdowns during the pandemic.

Tanzania Revenue Normalised EBITDA Profit after tax

Rs’000 Rs’000 Rs’000

2021 2020 2021 2020 2021 2020

TPC Limited

3,739,895 3,192,243 2,126,806 1,506,288 1,219,142 881,817

SML & SIL - - 130,227 79,017 14,185 (20,759)

3,739,895 3,192,243 2,257,033 1,585,305 1,233,327 861,058

• Through the combined impact of a volume increase of 5% and a price increase of 2.3% in USD and a weaker Mauritian Rupee, the turnover of TPC increased substantially in financial year 2020-21.

• Sugar production increased as cane yields recovered from 119 tonnes per hectare in the prior year to 133 tonnes per hectare as a result of improved climatic conditions, resulting in a lower water table, and better treatment protocols of the Yellow Sugarcane Aphid (YSA) which had weighed negatively on the cane growth in the prior year. The achieved yields for the year reflected the best ever recorded yield productivity at 11.64 tonnes of cane per hectare per month.

• Cane yields have continued their strong performance at the start of the 2021-22 season with the best ever yields achieved as at the end of September 2021. The sustained investments in better irrigation, higher fertilisation and improved YSA controls bode well for the season although the lower rainfall during the long rains and prevalence of YSA may have adverse impacts later in the season.

• Cane quality and sucrose content have also been in line with high levels achieved in the financial year 2020-21 with the factory performing in line with expectations.

• As a result of the good start to the year, it is expected that sugar production will be higher in financial year 2021-22.

As Tanzania is likely to remain a deficit sugar market in the short term, Alteo’s strategy for its Tanzanian sugar business is to continue to grow its sugar supply to the domestic market, while creating further added value from sugar cane by-products. The cornerstone of its strategic priorities is the sustainable management of natural resources to ensure simultaneous business health and wellbeing of local communities living on the estate. These include:

• Sustained investment in water supply security with new boreholes to maintain and improve cane yields, while at the same time ensuring sustainable use of underground water resources;

• Sustained investment to convert flood irrigation areas to semi solid and drip irrigation systems to improve efficiency of water use (i.e, increased water productivity);

• Continued development of 440 hectares for new sugar cane cultivation through soil reclamation in regions of relatively high salinity and sodicity;

• Phased introduction of mechanical harvesting and evaluation of its impact on production costs and cane yields, in anticipation of rising labour costs and more stringent environmental legislation towards cane burning;

• Phased investments in the factory to stabilize crushing rate, improve efficiencies and treat effluents; and

• Continuing the feasibility study of an investment in a distillery to generate additional value from molasses to produce Extra Neutral Alcohol (ENA) for the domestic market.

33Integrated Report 2021 - Alteo Limited

YEAR FOR TPC!A RECORD-BREAKING

The TPC Board approved a multiyear, multimillion-dollar project to improve drainage infrastructure.

The TPC Board approved

drainage infrastructure.

TPC’s sugarcane yields, historically the backbone of its strong financial results, made a strong recovery after a difficult 2019/20 season where a deadly combination of increasing Yellow Sugarcane Aphid (YSA) infestations and disruptively high rainfalls led to the lowest cane yields in six years. Whilst it remains difficult to assign the exact impact on yields for each of these two negative influences, it is thought that the exceptionally long rainy season led to record high water table across large parts of the estate. This meant that the cane was under stress for a significant part of the growing season and these stress conditions provided a fertile ground for the YSA pest to flourish and expand to unprecedented levels across the estate.

As the YSA pest was a relatively new challenge in Tanzania, and Alteo for that matter, management was researching, experimenting, and executing new and known measures at a rapid pace. Various consultants, industry contacts and experience from other parts of the world were considered. In the short term it was however clear that a targeted, chemical treatment campaign would be the only way to limit the damage whilst at the same time various longer term integrated pest management approaches were being studied. The adage of measuring that what you want to manage was no more visible than in this case. A substantial amount of work was invested in creating reliable and effective scouting procedures that ultimately went a long way to produce the required data to better understand the pest and the most effective treatment protocols. Whilst the final solution to eradicate the pest from TPC has not yet been found, great strides have been and are continued to be made in this regard.

It should however also be pointed out that the reduction in infestation levels would not have been as successful without the benefit of a drop in water table levels. Although the normalization of rainfall in the region resulted in this reduction, the importance of improving drainage infrastructures in and around the fields became extremely apparent. The last 5 years had seen annual flooding episodes as extreme weather conditions seemingly become the new normal. As a consequence, the TPC Board approved a multiyear, multimillion-dollar project to improve drainage infrastructure including, crucially, improvements of the river dike on the western boundary of TPC which had experienced multiple events of either overflowing or being breached in each of the last 5 years. During FY21, TPC decided to invest in the purchase of earth-moving equipment to enable the commencement of necessary drainage works on the high priority areas which had been identified in an in-depth study conducted by a specialized consultancy firm.

In the absence of disruptive rainfall events, the water table dropped to normal levels, resulting in lower YSA infestation levels and the stage was set for a return to ‘normalised’ TPC yields, thus improving profitability. FY21 did not disappoint in this regard and, in fact, led to numerous firsts with, most

importantly, the best ever cane productivity at 11.64 tons cane per hectare per month. With more cane and the second-best sucrose levels (over the same 6 years), the factory team was able to test the recent investments on the crushing capacity successfully at the designed capacity of 220 Tons Cane per Hour for short periods of time, reaching the highest ever season average of 197 TCH. With the increase in sugar production of more than 12%, a similar increase in sales of sugar followed. The resultant revenue increase, coupled with an increase in standing cane valuation (based on further increase in cane production foreseen in the following year) confirmed the significant impact of cane yields on TPC profitability as the company reached its highest ever Profit After Tax (in reporting currency of TZS).

Looking forward, the scope in maintaining and even improving such high cane yield seems daunting but at the same time exciting and achievable. With the last available horizontal expansion opportunity of 400 ha being completed within the next three years, the introduction of technological innovations such as precision farming in combination with even more investments in varietal improvements, efficient irrigation, integrated pest management activities, increased sustainable exploitation of the aquifer and the advancement of mechanized cane harvest, should bode well to offset the likely challenges of mother nature (more adverse weather and further expansion of pests such as YSA) and a reduction in surface water availability in the region.

TANZANIA

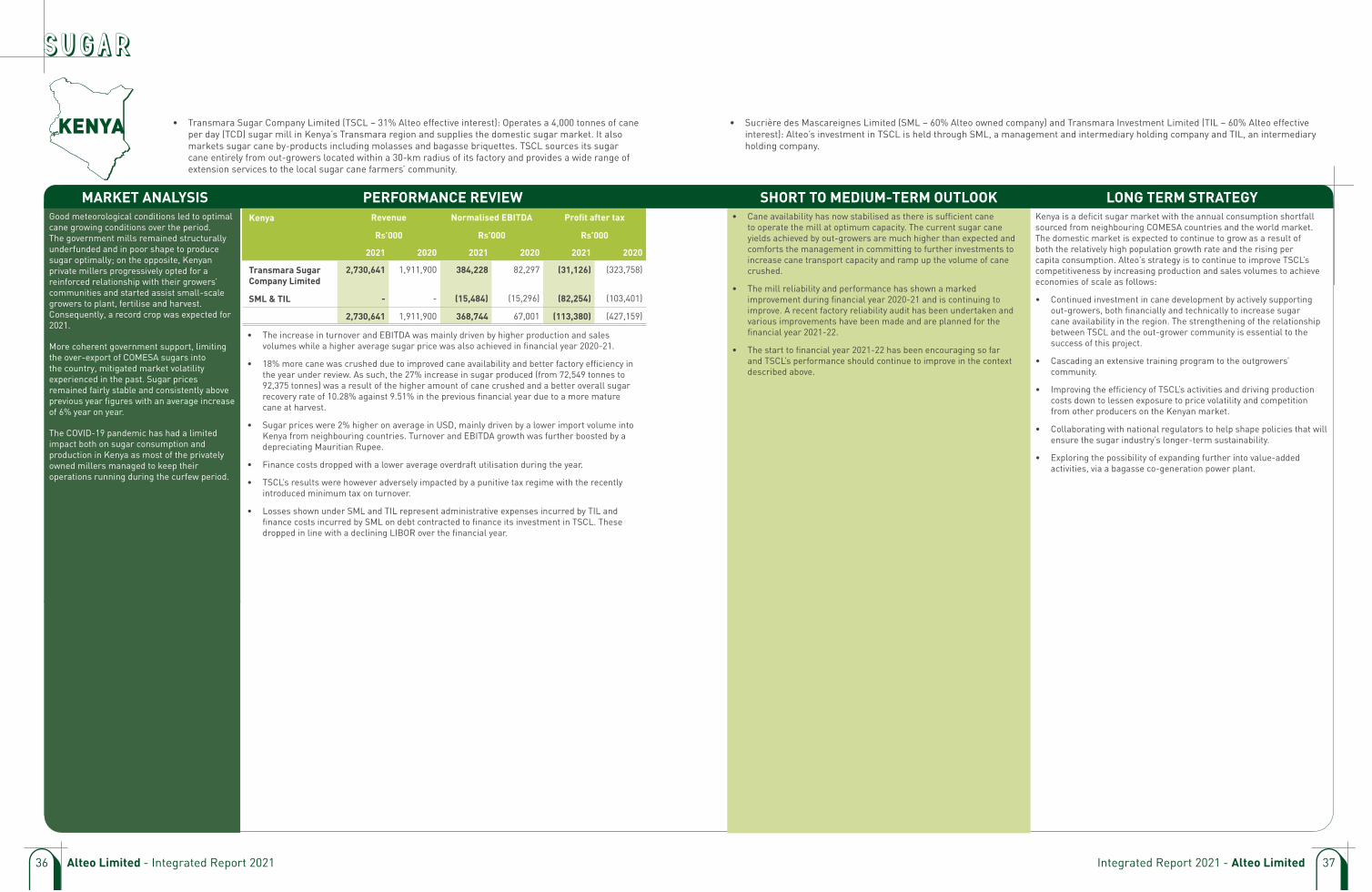

• Transmara Sugar Company Limited (TSCL – 31% Alteo effective interest): Operates a 4,000 tonnes of cane per day (TCD) sugar mill in Kenya’s Transmara region and supplies the domestic sugar market. It also markets sugar cane by-products including molasses and bagasse briquettes. TSCL sources its sugar cane entirely from out-growers located within a 30-km radius of its factory and provides a wide range of extension services to the local sugar cane farmers’ community.

KENYA

MARKET ANALYSIS PERFORMANCE REVIEW SHORT TO MEDIUM-TERM OUTLOOK LONG TERM STRATEGYGood meteorological conditions led to optimal cane growing conditions over the period. The government mills remained structurally underfunded and in poor shape to produce sugar optimally; on the opposite, Kenyan private millers progressively opted for a reinforced relationship with their growers’ communities and started assist small-scale growers to plant, fertilise and harvest. Consequently, a record crop was expected for 2021.

More coherent government support, limiting the over-export of COMESA sugars into the country, mitigated market volatility experienced in the past. Sugar prices remained fairly stable and consistently above previous year figures with an average increase of 6% year on year.

The COVID-19 pandemic has had a limited impact both on sugar consumption and production in Kenya as most of the privately owned millers managed to keep their operations running during the curfew period.

Kenya Revenue Normalised EBITDA Profit after tax

Rs’000 Rs’000 Rs’000

2021 2020 2021 2020 2021 2020

Transmara Sugar Company Limited

2,730,641 1,911,900 384,228 82,297 (31,126) (323,758)

SML & TIL - - (15,484) (15,296) (82,254) (103,401)

2,730,641 1,911,900 368,744 67,001 (113,380) (427,159)

• The increase in turnover and EBITDA was mainly driven by higher production and sales volumes while a higher average sugar price was also achieved in financial year 2020-21.

• 18% more cane was crushed due to improved cane availability and better factory efficiency in the year under review. As such, the 27% increase in sugar produced (from 72,549 tonnes to 92,375 tonnes) was a result of the higher amount of cane crushed and a better overall sugar recovery rate of 10.28% against 9.51% in the previous financial year due to a more mature cane at harvest.

• Sugar prices were 2% higher on average in USD, mainly driven by a lower import volume into Kenya from neighbouring countries. Turnover and EBITDA growth was further boosted by a depreciating Mauritian Rupee.

• Finance costs dropped with a lower average overdraft utilisation during the year.

• TSCL’s results were however adversely impacted by a punitive tax regime with the recently introduced minimum tax on turnover.

• Losses shown under SML and TIL represent administrative expenses incurred by TIL and finance costs incurred by SML on debt contracted to finance its investment in TSCL. These dropped in line with a declining LIBOR over the financial year.

• Cane availability has now stabilised as there is sufficient cane to operate the mill at optimum capacity. The current sugar cane yields achieved by out-growers are much higher than expected and comforts the management in committing to further investments to increase cane transport capacity and ramp up the volume of cane crushed.

• The mill reliability and performance has shown a marked improvement during financial year 2020-21 and is continuing to improve. A recent factory reliability audit has been undertaken and various improvements have been made and are planned for the financial year 2021-22.

• The start to financial year 2021-22 has been encouraging so far and TSCL’s performance should continue to improve in the context described above.

Kenya is a deficit sugar market with the annual consumption shortfall sourced from neighbouring COMESA countries and the world market. The domestic market is expected to continue to grow as a result of both the relatively high population growth rate and the rising per capita consumption. Alteo’s strategy is to continue to improve TSCL’s competitiveness by increasing production and sales volumes to achieve economies of scale as follows:

• Continued investment in cane development by actively supporting out-growers, both financially and technically to increase sugar cane availability in the region. The strengthening of the relationship between TSCL and the out-grower community is essential to the success of this project.

• Cascading an extensive training program to the outgrowers’ community.

• Improving the efficiency of TSCL’s activities and driving production costs down to lessen exposure to price volatility and competition from other producers on the Kenyan market.

• Collaborating with national regulators to help shape policies that will ensure the sugar industry’s longer-term sustainability.

• Exploring the possibility of expanding further into value-added activities, via a bagasse co-generation power plant.

36 Alteo Limited - Integrated Report 2021

• Sucrière des Mascareignes Limited (SML – 60% Alteo owned company) and Transmara Investment Limited (TIL – 60% Alteo effective interest): Alteo’s investment in TSCL is held through SML, a management and intermediary holding company and TIL, an intermediary holding company.

MARKET ANALYSIS PERFORMANCE REVIEW SHORT TO MEDIUM-TERM OUTLOOK LONG TERM STRATEGYGood meteorological conditions led to optimal cane growing conditions over the period. The government mills remained structurally underfunded and in poor shape to produce sugar optimally; on the opposite, Kenyan private millers progressively opted for a reinforced relationship with their growers’ communities and started assist small-scale growers to plant, fertilise and harvest. Consequently, a record crop was expected for 2021.

More coherent government support, limiting the over-export of COMESA sugars into the country, mitigated market volatility experienced in the past. Sugar prices remained fairly stable and consistently above previous year figures with an average increase of 6% year on year.

The COVID-19 pandemic has had a limited impact both on sugar consumption and production in Kenya as most of the privately owned millers managed to keep their operations running during the curfew period.

Kenya Revenue Normalised EBITDA Profit after tax

Rs’000 Rs’000 Rs’000

2021 2020 2021 2020 2021 2020

Transmara Sugar Company Limited

2,730,641 1,911,900 384,228 82,297 (31,126) (323,758)

SML & TIL - - (15,484) (15,296) (82,254) (103,401)

2,730,641 1,911,900 368,744 67,001 (113,380) (427,159)

• The increase in turnover and EBITDA was mainly driven by higher production and sales volumes while a higher average sugar price was also achieved in financial year 2020-21.

• 18% more cane was crushed due to improved cane availability and better factory efficiency in the year under review. As such, the 27% increase in sugar produced (from 72,549 tonnes to 92,375 tonnes) was a result of the higher amount of cane crushed and a better overall sugar recovery rate of 10.28% against 9.51% in the previous financial year due to a more mature cane at harvest.

• Sugar prices were 2% higher on average in USD, mainly driven by a lower import volume into Kenya from neighbouring countries. Turnover and EBITDA growth was further boosted by a depreciating Mauritian Rupee.

• Finance costs dropped with a lower average overdraft utilisation during the year.

• TSCL’s results were however adversely impacted by a punitive tax regime with the recently introduced minimum tax on turnover.

• Losses shown under SML and TIL represent administrative expenses incurred by TIL and finance costs incurred by SML on debt contracted to finance its investment in TSCL. These dropped in line with a declining LIBOR over the financial year.

• Cane availability has now stabilised as there is sufficient cane to operate the mill at optimum capacity. The current sugar cane yields achieved by out-growers are much higher than expected and comforts the management in committing to further investments to increase cane transport capacity and ramp up the volume of cane crushed.

• The mill reliability and performance has shown a marked improvement during financial year 2020-21 and is continuing to improve. A recent factory reliability audit has been undertaken and various improvements have been made and are planned for the financial year 2021-22.

• The start to financial year 2021-22 has been encouraging so far and TSCL’s performance should continue to improve in the context described above.

Kenya is a deficit sugar market with the annual consumption shortfall sourced from neighbouring COMESA countries and the world market. The domestic market is expected to continue to grow as a result of both the relatively high population growth rate and the rising per capita consumption. Alteo’s strategy is to continue to improve TSCL’s competitiveness by increasing production and sales volumes to achieve economies of scale as follows:

• Continued investment in cane development by actively supporting out-growers, both financially and technically to increase sugar cane availability in the region. The strengthening of the relationship between TSCL and the out-grower community is essential to the success of this project.

• Cascading an extensive training program to the outgrowers’ community.

• Improving the efficiency of TSCL’s activities and driving production costs down to lessen exposure to price volatility and competition from other producers on the Kenyan market.

• Collaborating with national regulators to help shape policies that will ensure the sugar industry’s longer-term sustainability.

• Exploring the possibility of expanding further into value-added activities, via a bagasse co-generation power plant.

37Integrated Report 2021 - Alteo Limited

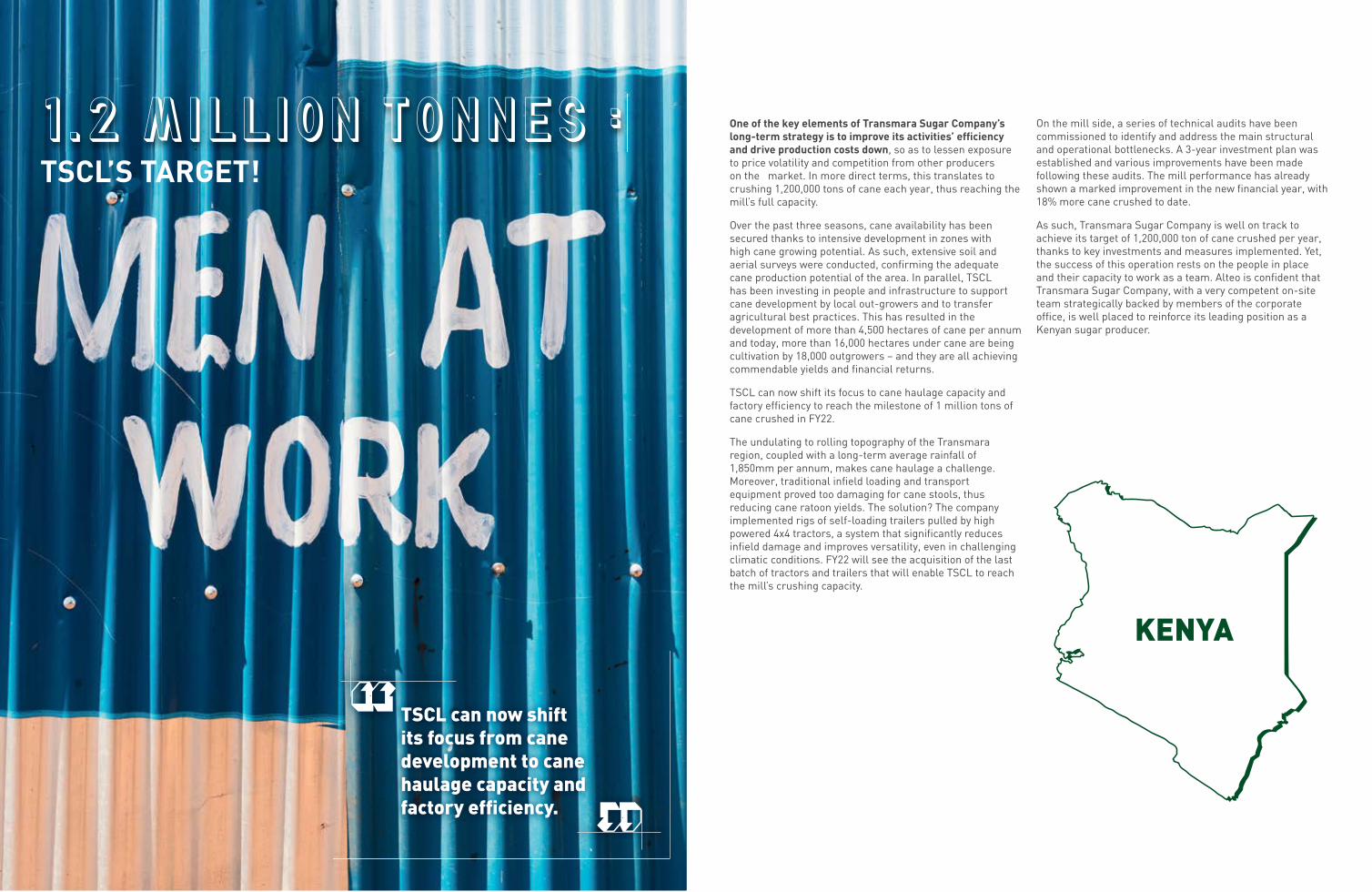

TSCL’S TARGET!

TSCL can now shift its focus from cane development to cane haulage capacity and factory efficiency.

One of the key elements of Transmara Sugar Company’s long-term strategy is to improve its activities’ efficiency and drive production costs down, so as to lessen exposure to price volatility and competition from other producers on the market. In more direct terms, this translates to crushing 1,200,000 tons of cane each year, thus reaching the mill’s full capacity.

Over the past three seasons, cane availability has been secured thanks to intensive development in zones with high cane growing potential. As such, extensive soil and aerial surveys were conducted, confirming the adequate cane production potential of the area. In parallel, TSCL has been investing in people and infrastructure to support cane development by local out-growers and to transfer agricultural best practices. This has resulted in the development of more than 4,500 hectares of cane per annum and today, more than 16,000 hectares under cane are being cultivation by 18,000 outgrowers – and they are all achieving commendable yields and financial returns.

TSCL can now shift its focus to cane haulage capacity and factory efficiency to reach the milestone of 1 million tons of cane crushed in FY22.

The undulating to rolling topography of the Transmara region, coupled with a long-term average rainfall of 1,850mm per annum, makes cane haulage a challenge. Moreover, traditional infield loading and transport equipment proved too damaging for cane stools, thus reducing cane ratoon yields. The solution? The company implemented rigs of self-loading trailers pulled by high powered 4x4 tractors, a system that significantly reduces infield damage and improves versatility, even in challenging climatic conditions. FY22 will see the acquisition of the last batch of tractors and trailers that will enable TSCL to reach the mill’s crushing capacity.

On the mill side, a series of technical audits have been commissioned to identify and address the main structural and operational bottlenecks. A 3-year investment plan was established and various improvements have been made following these audits. The mill performance has already shown a marked improvement in the new financial year, with 18% more cane crushed to date.

As such, Transmara Sugar Company is well on track to achieve its target of 1,200,000 ton of cane crushed per year, thanks to key investments and measures implemented. Yet, the success of this operation rests on the people in place and their capacity to work as a team. Alteo is confident that Transmara Sugar Company, with a very competent on-site team strategically backed by members of the corporate office, is well placed to reinforce its leading position as a Kenyan sugar producer.

KENYA

MARKET ANALYSIS PERFORMANCE REVIEW SHORT TO MEDIUM-TERM OUTLOOK LONG TERM STRATEGYBetween 2019 and 2020 calendar years, total electricity generated in Mauritius decreased by 11%, from 3,237 GWh to 2,882 GWh while peak demand decreased by 2.6%. (Figures from Energy And Water Statistics - 2020) This decrease results from the current COVID-19 pandemic since many hotels and other businesses did not operate during extended periods in FY21.

Total electricity generated in Mauritius in 2020 was from the following sources:

59.2% of the total electricity produced in Mauritius was generated by Independent Power Producers, such as Alteo, and the remaining by the Central Electricity Board (CEB).

The National Budget 2021-2022 announced a remuneration of Rs3.50/KWh of bagasse energy exported to CEB for sugar cane planters and producers as part of a Biomass Remuneration Framework. This bold measure taken by Government was a major step towards securing the sustainability of the cane industry in Mauritius, hence preserving the future availability of bagasse for electricity generation.

Through partnerships with renowned international firms, the renewables sector continues to represent a crucial avenue of growth for Alteo’s Energy cluster with a 100% biomass thermal project already presented to the CEB. The 2021-2022 National Budget speech set the challenging target of generating 60% of the national electricity from renewable sources by 2030. It also announced the launch of a Request For Proposals for a 40MW wind farm and for hybrid renewable projects to replace coal energy. Alteo, in collaboration with its partners, intends to respond to these tenders.