Hyundai Merchant Marine Co., Ltd. Company overview May 2010

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1Hyundai Merchant Marine Co.,Ltd.

Hyundai Merchant Marine Co., Ltd.

Company overview

May 2010

HYUNDAI MERCHANT MARINE Co.,Ltd.

Important Notice

This presentation contains “forward-looking statements”, that are based on Hyundai Merchant

Marine’s current expectations, prospects, assumptions, market view and strategies. These

statements are subject to risks and uncertainties as various factors may cause actual results to

differ materially. We undertake no duty to update or revise any forward–looking statements,

whether as a results of new information, future events, or otherwise.

Ⅰ. Company Overview

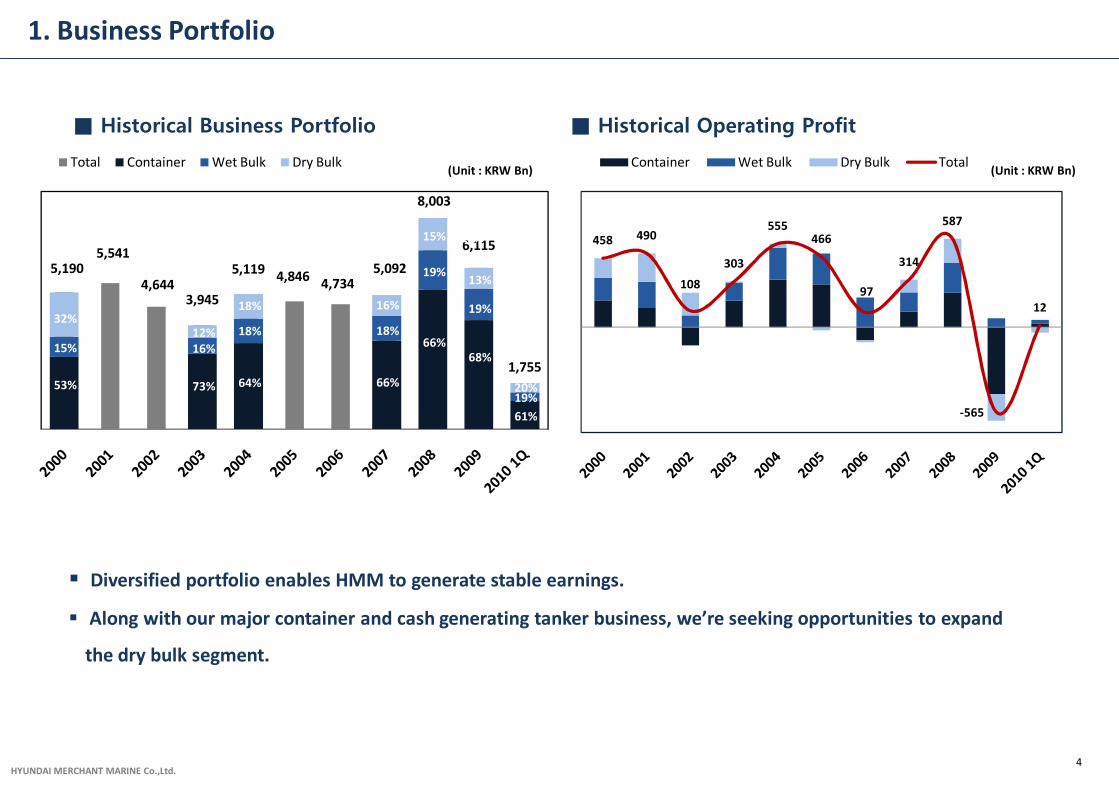

1. Business Portfolio

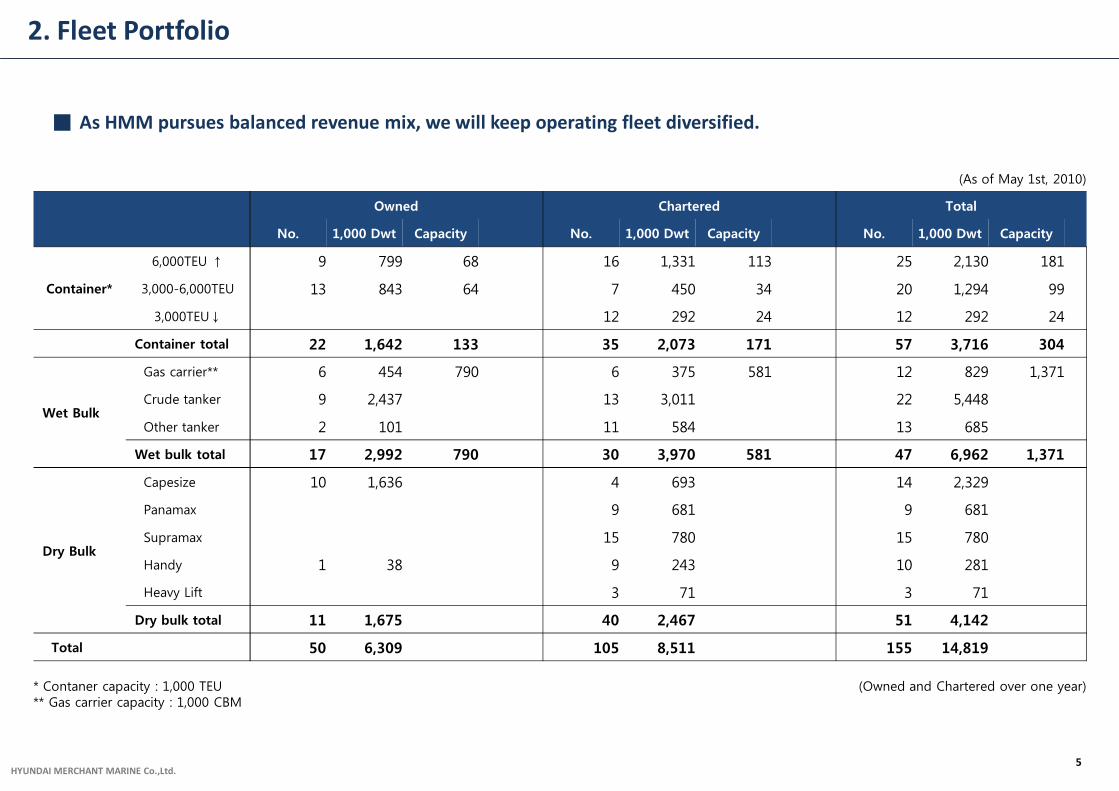

2. Fleet Portfolio

3. Fleet Expansion Plan

4. HMM’s Competitiveness

5. Overall Result

6. 2010 Market Outlook

7. 2010 Guidance

Ⅱ. Divisional Data

Table of Contents

3

HYUNDAI MERCHANT MARINE Co.,Ltd.

458 490

108

303

555 466

97

314

587

-565

12

-700

-500

-300

-100

100

300

500

700

900

Container Wet Bulk Dry Bulk Total

5,190 5,541

4,644 3,945

5,119 4,846 4,734 5,092

8,003

6,115

1,755

Total Container Wet Bulk Dry Bulk

53%

15%

32%

73%

16%12%

66%

15% 15%

61%

19%

13%

66%

18%

16%

1. Business Portfolio

4

§ Diversified portfolio enables HMM to generate stable earnings.

§ Along with our major container and cash generating tanker business, we’re seeking opportunities to expand

the dry bulk segment.

■ Historical Operating Profit■ Historical Business Portfolio

(Unit : KRW Bn)(Unit : KRW Bn)

64%

18%

18%

19%

68%

19%

13%

19%20%

HYUNDAI MERCHANT MARINE Co.,Ltd.

2. Fleet Portfolio

5

■ As HMM pursues balanced revenue mix, we will keep operating fleet diversified.

(As of May 1st, 2010)

Owned Chartered Total

No. 1,000 Dwt Capacity No. 1,000 Dwt Capacity No. 1,000 Dwt Capacity

Container*

6,000TEU ↑ 9 799 68 16 1,331 113 25 2,130 181

3,000-6,000TEU 13 843 64 7 450 34 20 1,294 99

3,000TEU↓ 12 292 24 12 292 24

Container total 22 1,642 133 35 2,073 171 57 3,716 304

Wet Bulk

Gas carrier** 6 454 790 6 375 581 12 829 1,371

Crude tanker 9 2,437 13 3,011 22 5,448

Other tanker 2 101 11 584 13 685

Wet bulk total 17 2,992 790 30 3,970 581 47 6,962 1,371

Dry Bulk

Capesize 10 1,636 4 693 14 2,329

Panamax 9 681 9 681

Supramax 15 780 15 780

Handy 1 38 9 243 10 281

Heavy Lift 3 71 3 71

Dry bulk total 11 1,675 40 2,467 51 4,142

Total 50 6,309 105 8,511 155 14,819

* Contaner capacity : 1,000 TEU** Gas carrier capacity : 1,000 CBM

(Owned and Chartered over one year)

HYUNDAI MERCHANT MARINE Co.,Ltd.

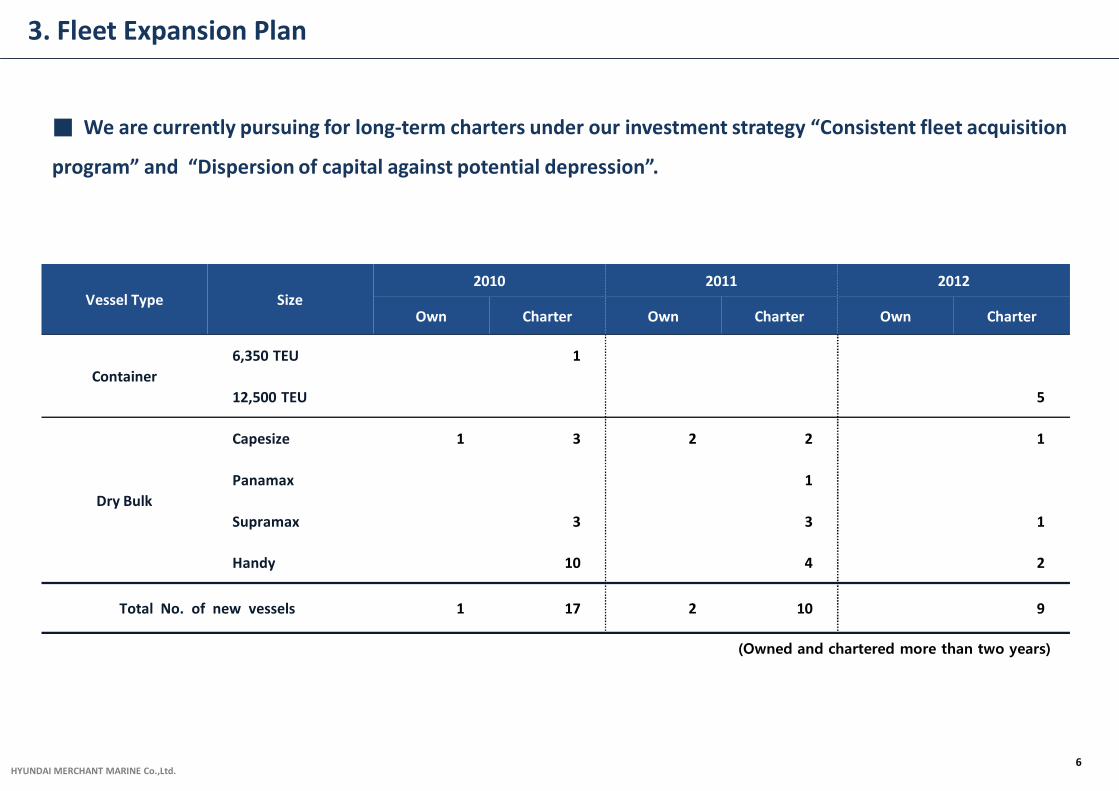

3. Fleet Expansion Plan

(Owned and chartered more than two years)

Vessel Type Size2010 2011 2012

Own Charter Own Charter Own Charter

Container

6,350 TEU 1

12,500 TEU 5

Dry Bulk

Capesize 1 3 2 2 1

Panamax 1

Supramax 3 3 1

Handy 10 4 2

Total No. of new vessels 1 17 2 10 9

6

■ We are currently pursuing for long-term charters under our investment strategy “Consistent fleet acquisition

program” and “Dispersion of capital against potential depression”.

HYUNDAI MERCHANT MARINE Co.,Ltd.

45

34

0

1

2

3

4

5

6

7

8

9

10

0

50

100

150

200

2002 2003 2004 2005 2006 2007 2008 2009

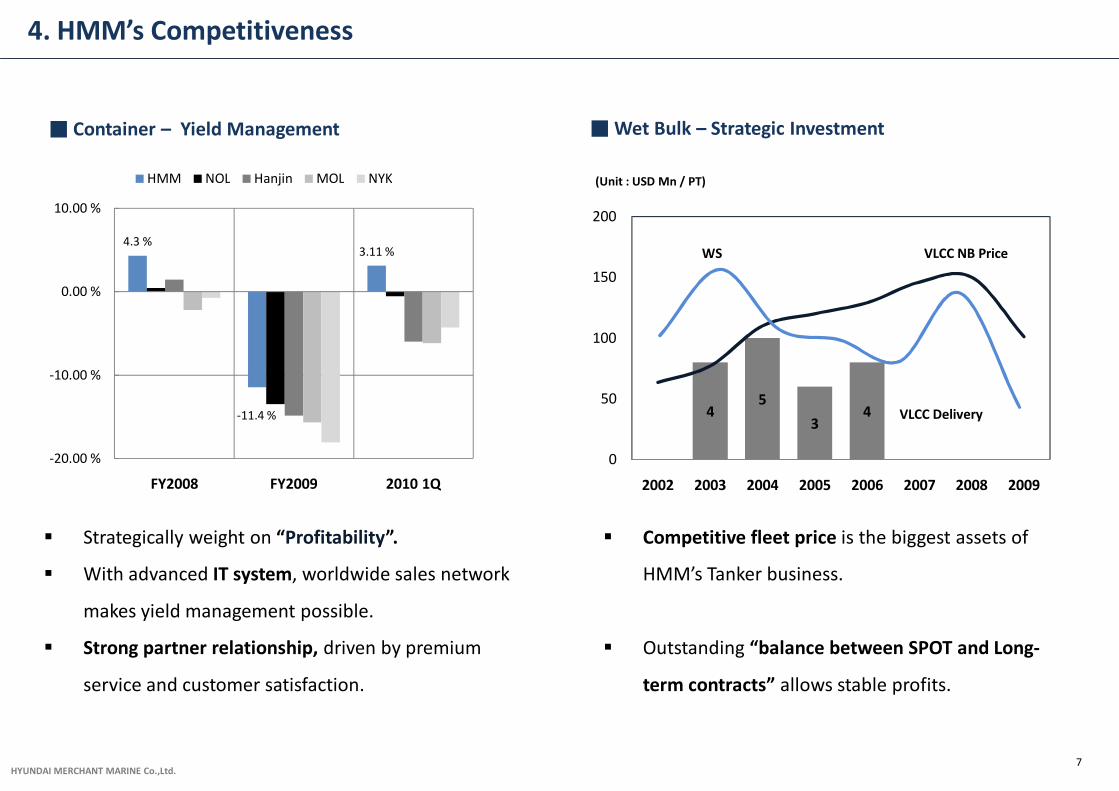

4. HMM’s Competitiveness

7

■ Container – Yield Management

§ Strategically weight on “Profitability”.

§ With advanced IT system, worldwide sales network

makes yield management possible.

§ Strong partner relationship, driven by premium

service and customer satisfaction.

(Unit : USD Mn / PT)

■ Wet Bulk – Strategic Investment

§ Competitive fleet price is the biggest assets of

HMM’s Tanker business.

§ Outstanding “balance between SPOT and Long-

term contracts” allows stable profits.

WS VLCC NB Price

VLCC Delivery

4.3 %

-11.4 %

3.11 %

-20.00 %

-10.00 %

0.00 %

10.00 %

FY2008 FY2009 2010 1Q

HMM NOL Hanjin MOL NYK

HYUNDAI MERCHANT MARINE Co.,Ltd.

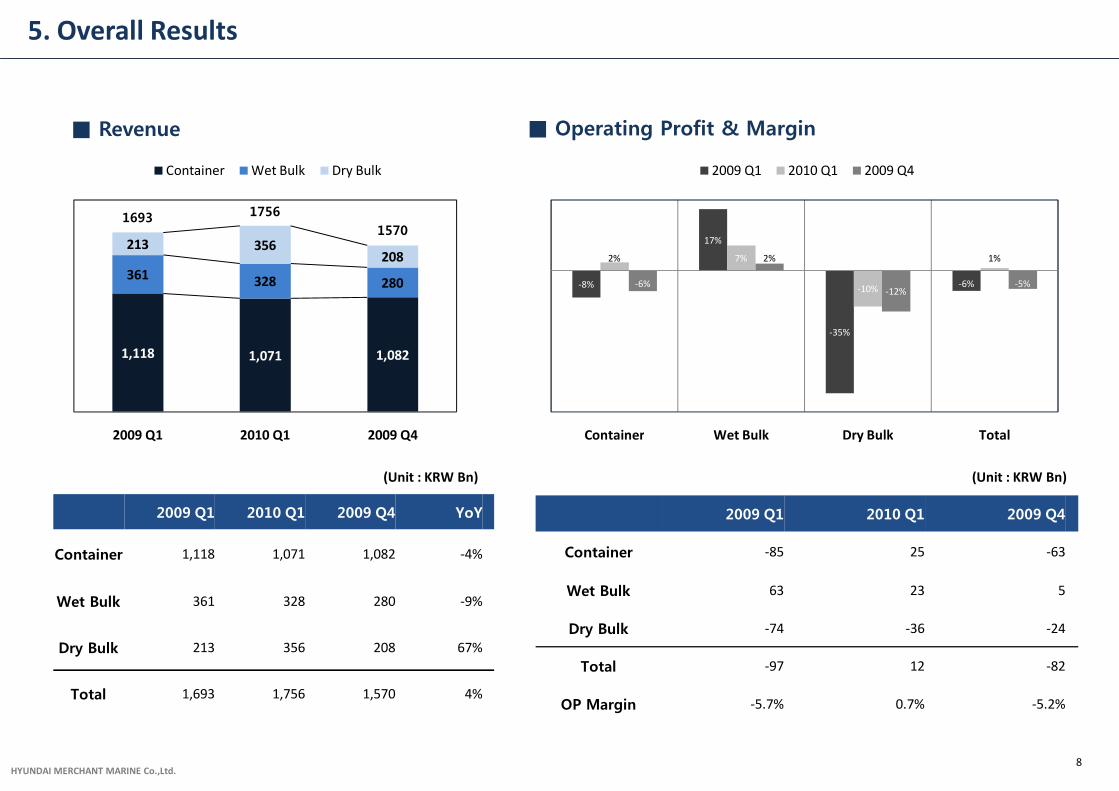

5. Overall Results

8

■ Revenue ■ Operating Profit & Margin

(Unit : KRW Bn)(Unit : KRW Bn)

1,118 1,071 1,082

361 328 280

213 356208

2009 Q1 2010 Q1 2009 Q4

Container Wet Bulk Dry Bulk

2009 Q1 2010 Q1 2009 Q4 YoY

Container 1,118 1,071 1,082 -4%

Wet Bulk 361 328 280 -9%

Dry Bulk 213 356 208 67%

Total 1,693 1,756 1,570 4%

1693 1756

1570

-8%

17%

-35%

-6%

2% 7%

-10%

1%

-6%

2%

-12%-5%

Container Wet Bulk Dry Bulk Total

2009 Q1 2010 Q1 2009 Q4

2009 Q1 2010 Q1 2009 Q4

Container -85 25 -63

Wet Bulk 63 23 5

Dry Bulk -74 -36 -24

Total -97 12 -82

OP Margin -5.7% 0.7% -5.2%

HYUNDAI MERCHANT MARINE Co.,Ltd.

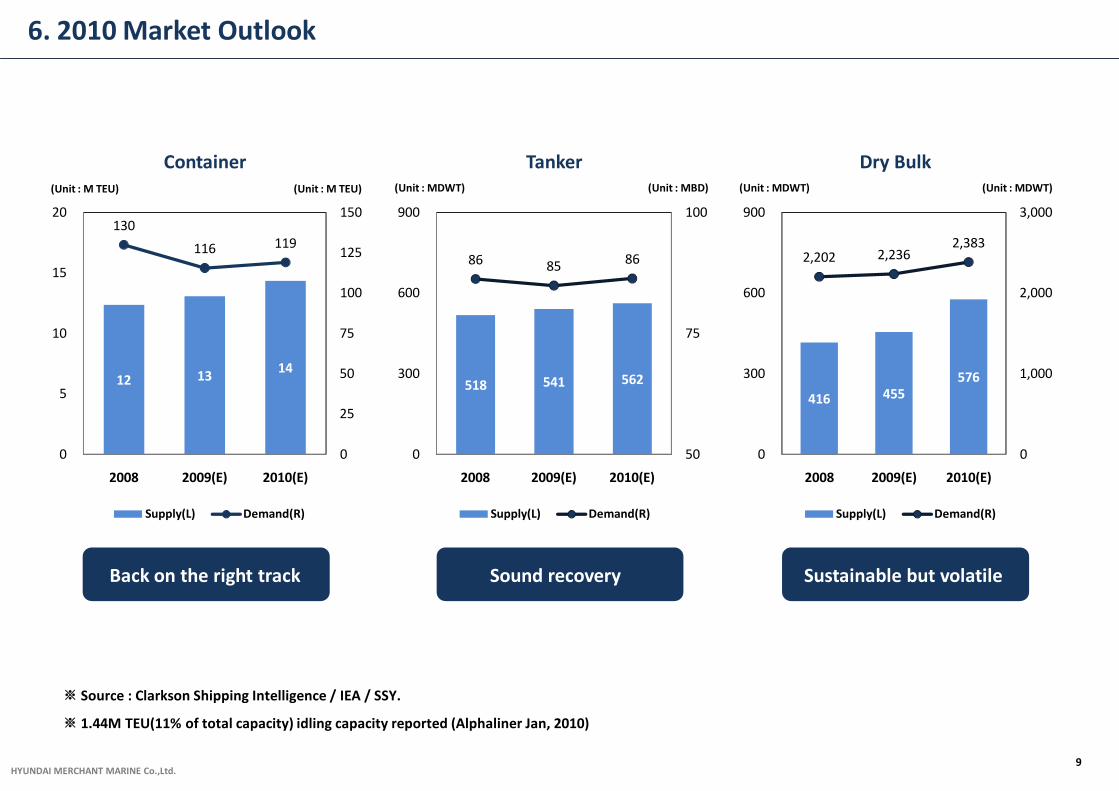

6. 2010 Market Outlook

9

Container Tanker Dry Bulk

※ Source : Clarkson Shipping Intelligence / IEA / SSY.

※ 1.44M TEU(11% of total capacity) idling capacity reported (Alphaliner Jan, 2010)

(Unit : M TEU) (Unit : M TEU) (Unit : MDWT) (Unit : MBD) (Unit : MDWT) (Unit : MDWT)

12 13 14

130

116 119

0

25

50

75

100

125

150

0

5

10

15

20

2008 2009(E) 2010(E)

Supply(L) Demand(R)

518 541 562

86 85 86

50

75

100

0

300

600

900

2008 2009(E) 2010(E)

Supply(L) Demand(R)

416 455 576

2,202 2,236 2,383

0

1,000

2,000

3,000

0

300

600

900

2008 2009(E) 2010(E)

Supply(L) Demand(R)

Back on the right track Sound recovery Sustainable but volatile

HYUNDAI MERCHANT MARINE Co.,Ltd.

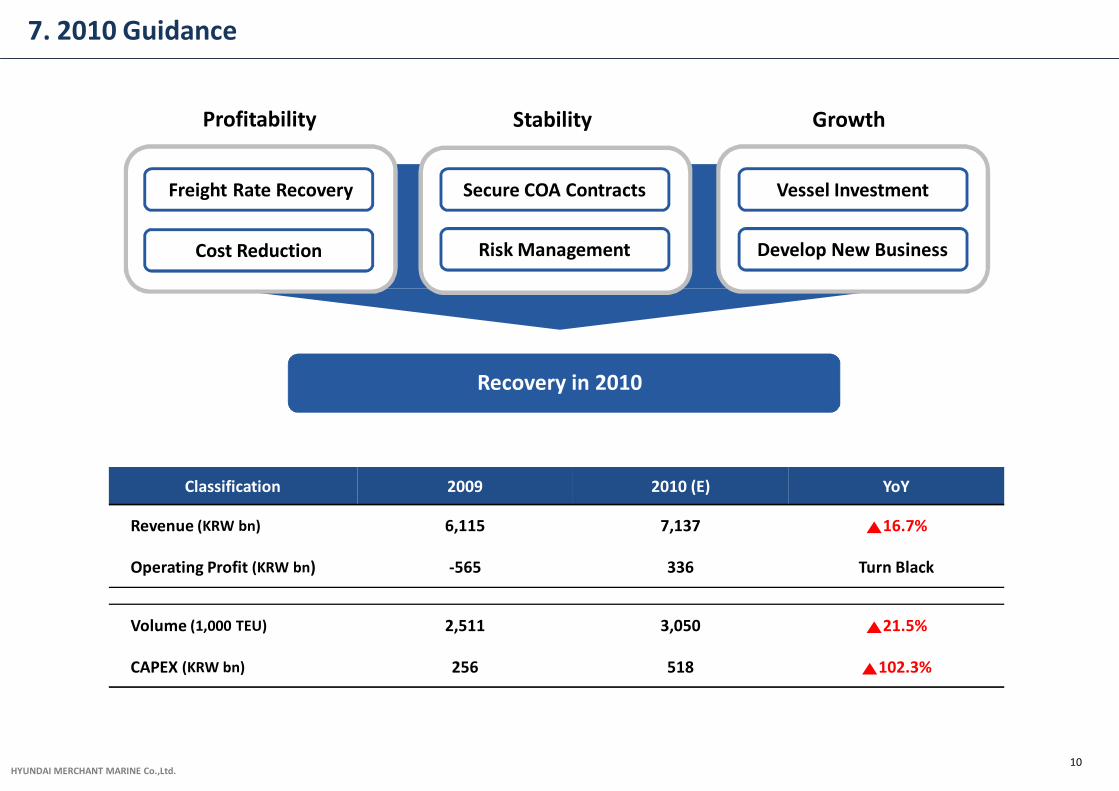

7. 2010 Guidance

10

Classification 2009 2010 (E) YoY

Revenue (KRW bn) 6,115 7,137 ▲16.7%

Operating Profit (KRW bn) -565 336 Turn Black

Volume (1,000 TEU) 2,511 3,050 ▲21.5%

CAPEX (KRW bn) 256 518 ▲102.3%

Freight Rate Recovery Secure COA Contracts Vessel Investment

Cost Reduction Risk Management Develop New Business

Profitability Stability Growth

Recovery in 2010

Ⅰ. Company Overview

Ⅱ. Divisional Data

1. Container

2. Wet Bulk

3. Dry Bulk

4. Summary Financial Statements

Table of Contents

11

HYUNDAI MERCHANT MARINE Co.,Ltd.

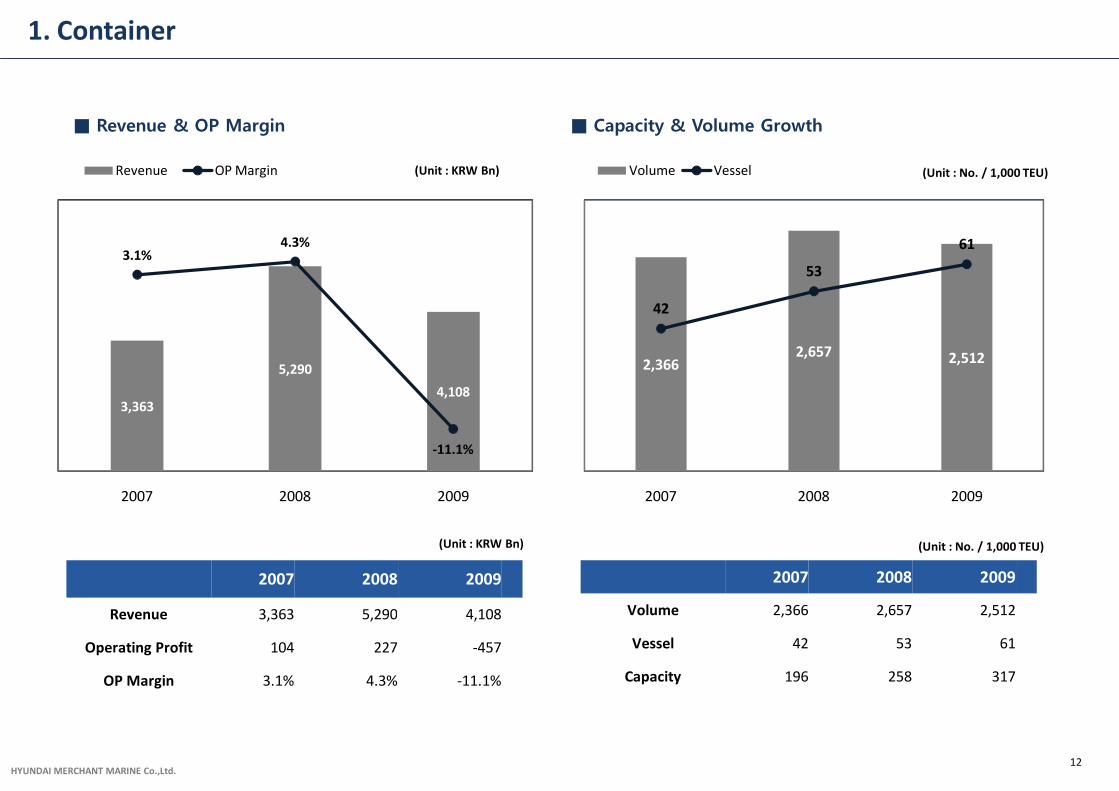

1. Container

■ Capacity & Volume Growth

12

■ Revenue & OP Margin

(Unit : No. / 1,000 TEU)(Unit : KRW Bn)

(Unit : No. / 1,000 TEU)(Unit : KRW Bn)

2,366 2,657 2,512

42

53

61

0

20

40

60

80

0

1,000

2,000

3,000

2007 2008 2009

Volume Vessel

2007 2008 2009

Revenue 3,363 5,290 4,108

Operating Profit 104 227 -457

OP Margin 3.1% 4.3% -11.1%

2007 2008 2009

Volume 2,366 2,657 2,512

Vessel 42 53 61

Capacity 196 258 317

3,363

5,290

4,108

3.1%4.3%

-11.1%-15%

-10%

-5%

0%

5%

10%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2007 2008 2009

Revenue OP Margin

HYUNDAI MERCHANT MARINE Co.,Ltd.

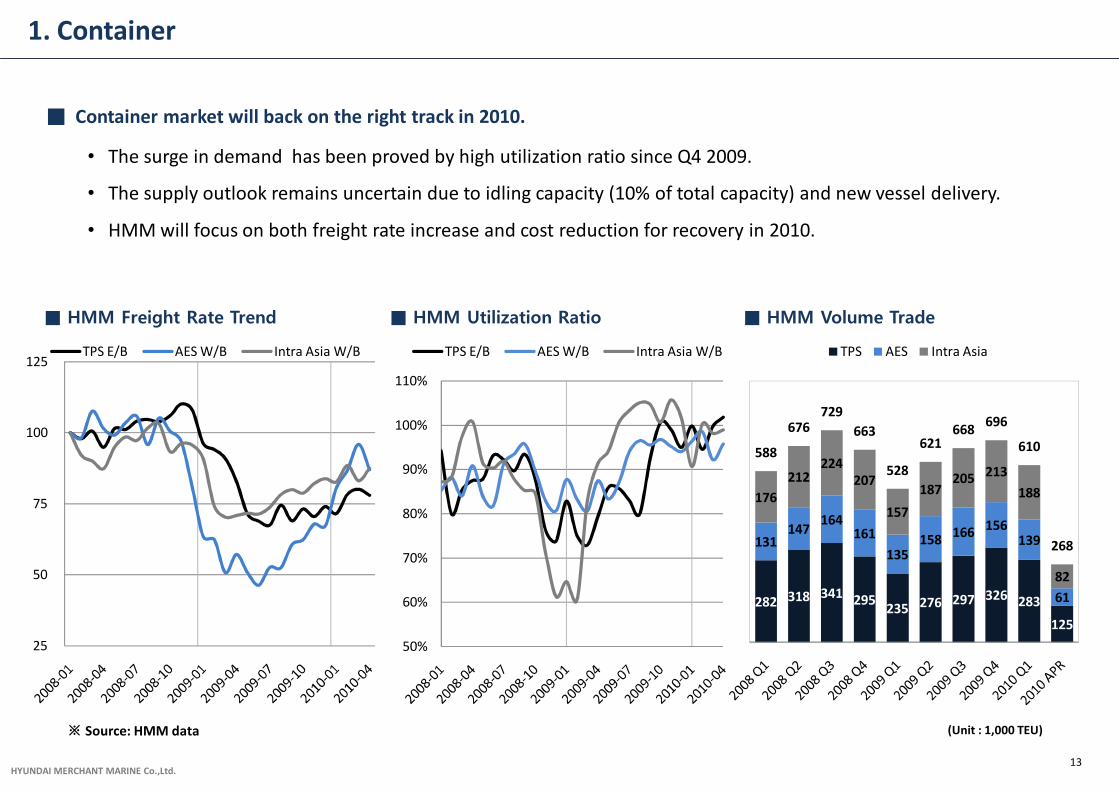

1. Container

■ HMM Freight Rate Trend ■ HMM Utilization Ratio

※ Source: HMM data

13

■ HMM Volume Trade

■ Container market will back on the right track in 2010.

• The surge in demand has been proved by high utilization ratio since Q4 2009.

• The supply outlook remains uncertain due to idling capacity (10% of total capacity) and new vessel delivery.

• HMM will focus on both freight rate increase and cost reduction for recovery in 2010.

(Unit : 1,000 TEU)

50%

60%

70%

80%

90%

100%

110%

TPS E/B AES W/B Intra Asia W/B

282 318 341 295 235 276 297 326 283

125

131 147

164 161

135 158

166 156 139

61

176

212 224

207

157

187 205 213

188

82

588

676 729

663

528

621 668

696

610

268

TPS AES Intra Asia

25

50

75

100

125 TPS E/B AES W/B Intra Asia W/B

HYUNDAI MERCHANT MARINE Co.,Ltd.

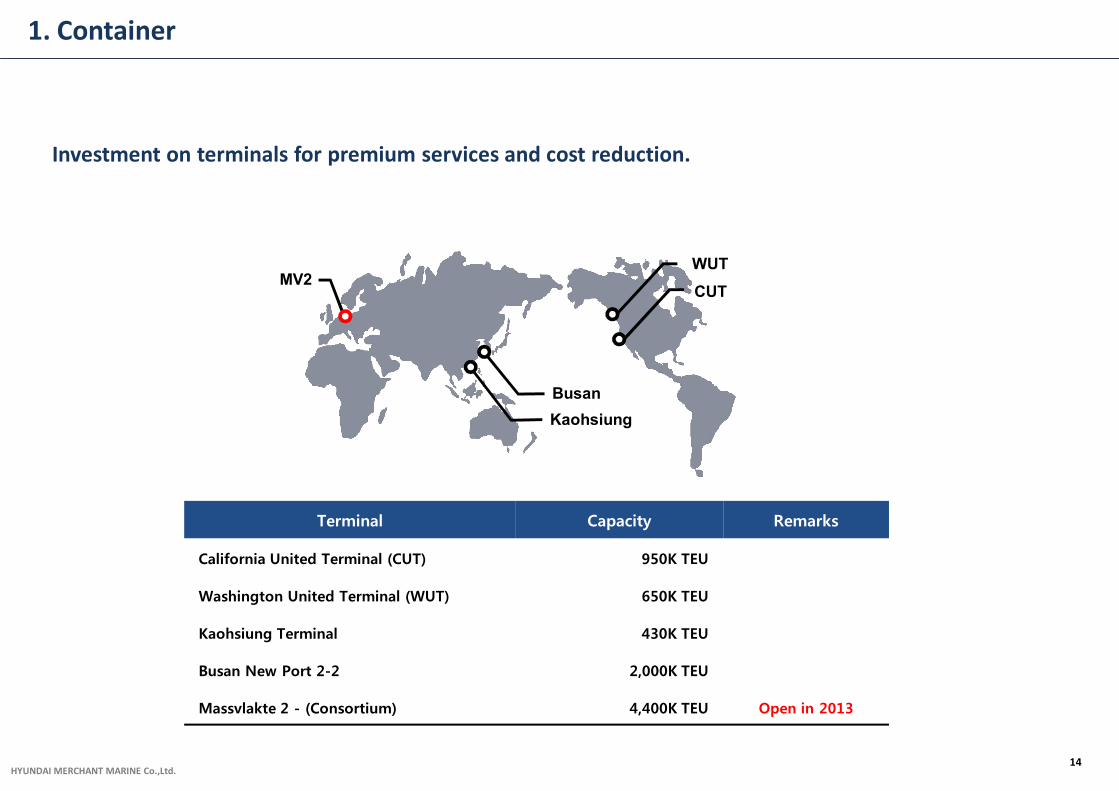

Investment on terminals for premium services and cost reduction.

Terminal Capacity Remarks

California United Terminal (CUT) 950K TEU

Washington United Terminal (WUT) 650K TEU

Kaohsiung Terminal 430K TEU

Busan New Port 2-2 2,000K TEU

Massvlakte 2 - (Consortium) 4,400K TEU Open in 2013

WUT

CUT

Busan

Kaohsiung

MV2

14

1. Container

HYUNDAI MERCHANT MARINE Co.,Ltd.

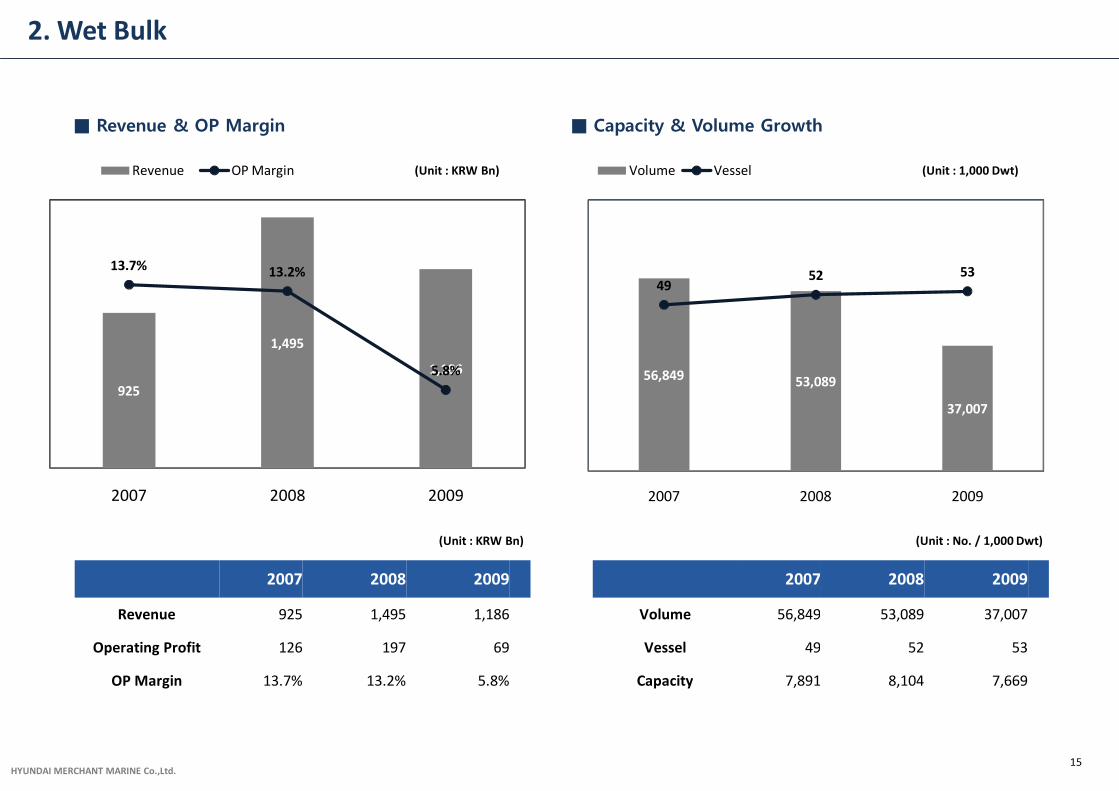

2. Wet Bulk

15

■ Capacity & Volume Growth■ Revenue & OP Margin

(Unit : 1,000 Dwt)(Unit : KRW Bn)

(Unit : No. / 1,000 Dwt)(Unit : KRW Bn)

56,849 53,089

37,007

4952 53

0

20

40

60

80

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2007 2008 2009

Volume Vessel

2007 2008 2009

Revenue 925 1,495 1,186

Operating Profit 126 197 69

OP Margin 13.7% 13.2% 5.8%

2007 2008 2009

Volume 56,849 53,089 37,007

Vessel 49 52 53

Capacity 7,891 8,104 7,669

925

1,495

1,186

13.7% 13.2%

5.8%

0%

5%

10%

15%

20%

0

200

400

600

800

1,000

1,200

1,400

1,600

2007 2008 2009

Revenue OP Margin

HYUNDAI MERCHANT MARINE Co.,Ltd.

2. Wet Bulk

Source: Clarkson YTD, HMM data

■ WS(Left) vs. HMM Tanker Index(Right)

(Unit : pt) (Unit : $/MT)

16

■ Wet Bulk market seems to recover after a challenging 2009.

• Increase in crude oil demand and S/H vessel phase outs could uphold recovery.

• However, excess supply will still remain as a task to challenge.

• HMM will keep optimal level of SPOT and COA/CVC proportion.

Source: 2009 HMM wet bulk revenue

■ SPOT vs. Fixed

Fixed68%

SPOT32%

KRW 1,189 Bn

0

10

20

30

40

50

0

50

100

150

200

250

WS Tanker(R)

HYUNDAI MERCHANT MARINE Co.,Ltd.

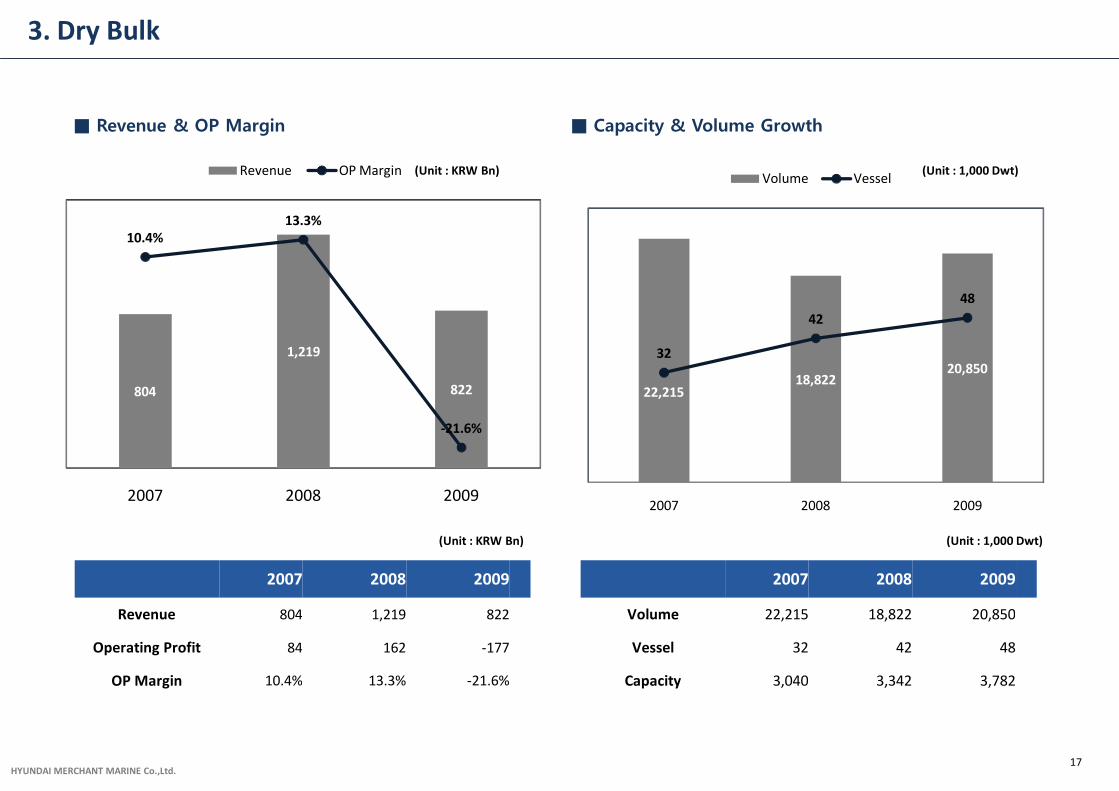

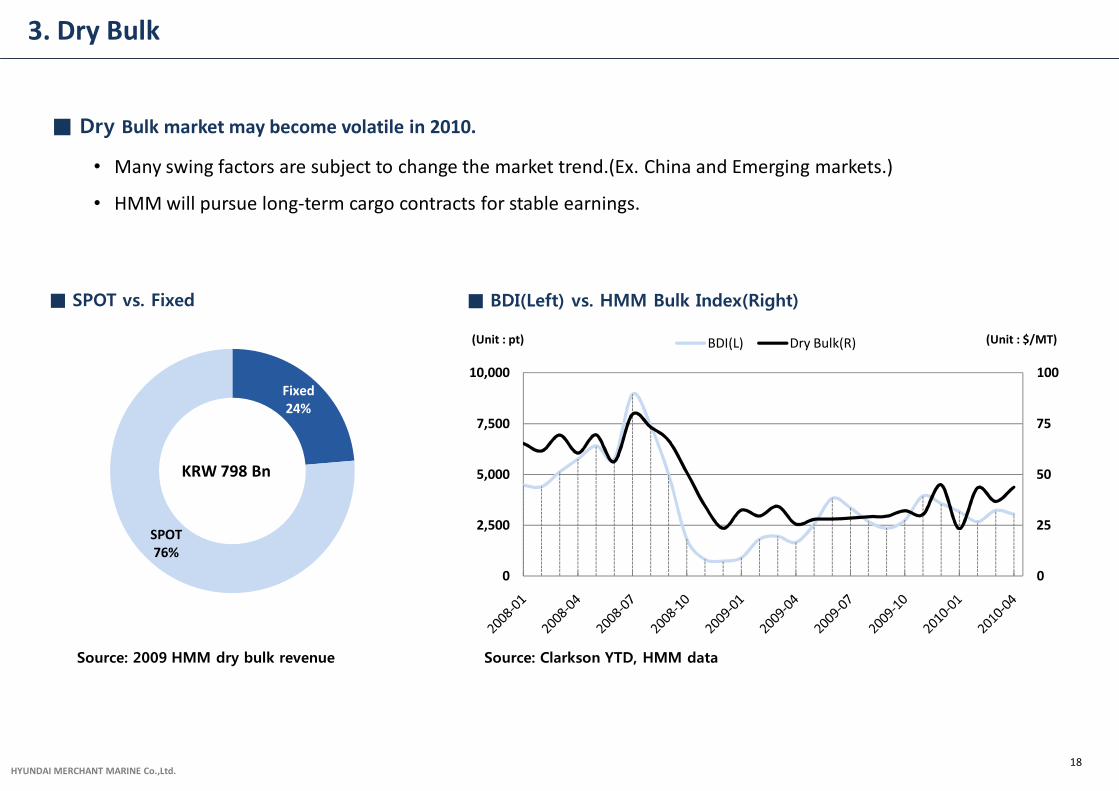

3. Dry Bulk

17

■ Capacity & Volume Growth■ Revenue & OP Margin

(Unit : 1,000 Dwt)(Unit : KRW Bn)

(Unit : 1,000 Dwt)(Unit : KRW Bn)

2007 2008 2009

Revenue 804 1,219 822

Operating Profit 84 162 -177

OP Margin 10.4% 13.3% -21.6%

2007 2008 2009

Volume 22,215 18,822 20,850

Vessel 32 42 48

Capacity 3,040 3,342 3,782

22,215 18,822

20,850 32

42

48

0

20

40

60

80

0

5,000

10,000

15,000

20,000

25,000

2007 2008 2009

Volume Vessel

804

1,219

822

10.4%13.3%

-21.6%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

0

200

400

600

800

1,000

1,200

1,400

2007 2008 2009

Revenue OP Margin

HYUNDAI MERCHANT MARINE Co.,Ltd.

Fixed24%

SPOT76%

3. Dry Bulk

■ BDI(Left) vs. HMM Bulk Index(Right)

(Unit : pt) (Unit : $/MT)

Source: Clarkson YTD, HMM data

18

■ Dry Bulk market may become volatile in 2010.

• Many swing factors are subject to change the market trend.(Ex. China and Emerging markets.)

• HMM will pursue long-term cargo contracts for stable earnings.

■ SPOT vs. Fixed

Source: 2009 HMM dry bulk revenue

KRW 798 Bn

0

25

50

75

100

0

2,500

5,000

7,500

10,000

BDI(L) Dry Bulk(R)

HYUNDAI MERCHANT MARINE Co.,Ltd.19

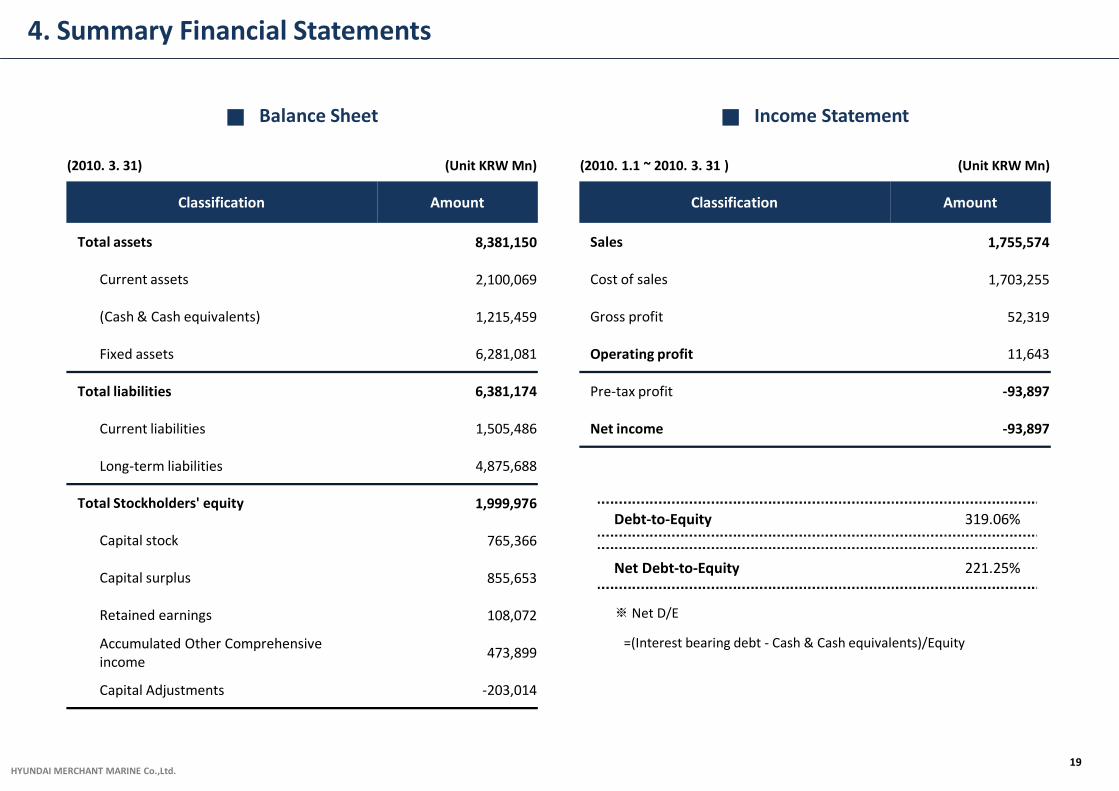

4. Summary Financial Statements

■ Balance Sheet ■ Income Statement

(2010. 3. 31) (Unit KRW Mn) (2010. 1.1 ~ 2010. 3. 31 ) (Unit KRW Mn)

Classification Amount Classification Amount

Total assets 8,381,150 Sales 1,755,574

Current assets 2,100,069 Cost of sales 1,703,255

(Cash & Cash equivalents) 1,215,459 Gross profit 52,319

Fixed assets 6,281,081 Operating profit 11,643

Total liabilities 6,381,174 Pre-tax profit -93,897

Current liabilities 1,505,486 Net income -93,897

Long-term liabilities 4,875,688

Total Stockholders' equity 1,999,976

Capital stock 765,366

Capital surplus 855,653

Retained earnings 108,072

Accumulated Other Comprehensive income

473,899

Capital Adjustments -203,014

Debt-to-Equity 319.06%

Net Debt-to-Equity 221.25%

※ Net D/E

=(Interest bearing debt - Cash & Cash equivalents)/Equity

HYUNDAI MERCHANT MARINE Co.,Ltd.

Investor Contact

HMM Investor Relations Contact

Sam Yoon +82-2-3706-5868 [email protected]

Ellie Jung +82-2-3706-5884 [email protected]

Bex Jung +82-2-3706-5879 [email protected]

Suk-Won Kang +82-2-3706-5872 [email protected]

Related Documents