February/March 2022

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

February/March 2022

Hystead Group

Hyprop PDI

Delta CityBelgrade

(Disposed)

Delta CityPodgorica

(Held-for-saleto 3rd party)

Hystead

SCM Retail

The Mall,Sofia, Bulgaria

City Center One East & City Center One West,

Croatia

Balkan Retail

Skopje City Mall,North Macedonia

2

40% dividend and asset management fee

Hystead shareholder arrangements

PDI

HysteadLimited

Guarantees =

€ 362 million (90%)

Equity debt providers

(RMB, Standard Bank,

Nedbank)Debt =

€ 402 million

Debt =

€ 384 million

In-country banks

Guarantee =

€ 40 million (10%)

40%

Back-to-back security = € 47.2 million (11.7%)

60% dividend and asset management fee

60% SHAREHOLDING

HypropInvestments

Limited

Guarantee Fee = 60% of the dividend on shareholding not guaranteed by PDI (60% x 18.3% = 11%)

3

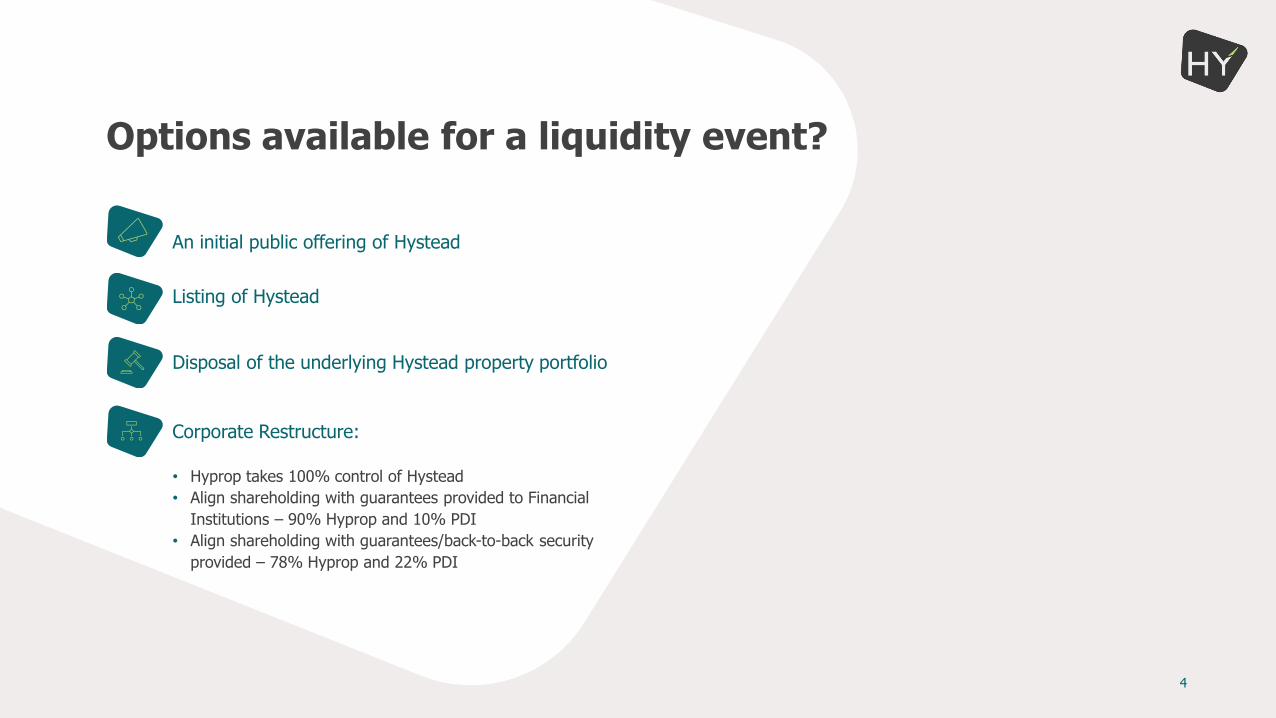

Listing of Hystead

Options available for a liquidity event?

Corporate Restructure:

• Hyprop takes 100% control of Hystead

• Align shareholding with guarantees provided to Financial

Institutions – 90% Hyprop and 10% PDI

• Align shareholding with guarantees/back-to-back security

provided – 78% Hyprop and 22% PDI

Disposal of the underlying Hystead property portfolio

An initial public offering of Hystead

4

The Transaction

Once the Delta City Podgorica disposal is complete, Hystead only holds a Vendor Loan relating to Belgrade sale

Liquidity event via the disposal of underlying portfolio

Hyprop PDI

Delta CityBelgrade

(Disposed)

Delta CityPodgorica

(Held-for-saleto 3rd party)

Hystead

The Mall,Sofia, Bulgaria

City Center One East & City Center One West,

Croatia

Skopje City Mall,North Macedonia

SCM Retail Balkan Retail

5

• Signed SPA of €95 million for Delta City Podgorica • Purchase consideration of €95 million (the 30 June 2021 valuation €75.3 million)

• Sale is expected to complete Q1 2022

• Belgrade vendor loan• €10 million vendor loan to the purchaser of Delta City Belgrade

• Shareholders (PDI and Hyprop) will receive proceeds (interest and capital) as vendor loan is repaid over 7 years

What is remaining? (1 of 2)

6

What is remaining? (2 of 2)

• Hyprop is purchasing 100% of SCM Retail and Balkan Retail, holding Skopje City Mall,

The Mall Sofia, City Center One East and City Center One West respectively

• Total aggregate consideration: €193 million

• Estimated purchase consideration: €173 million

• Excluded claim to be settled by Balkan Retail no later than 31 May 2022: €20 million

• The purchase consideration payable is equal to the consolidated aggregate NAV of the target group

• Deferred tax treatment

• Hystead will use sale proceeds to settle equity debt

• Any profit/losses to be split between shareholders

7

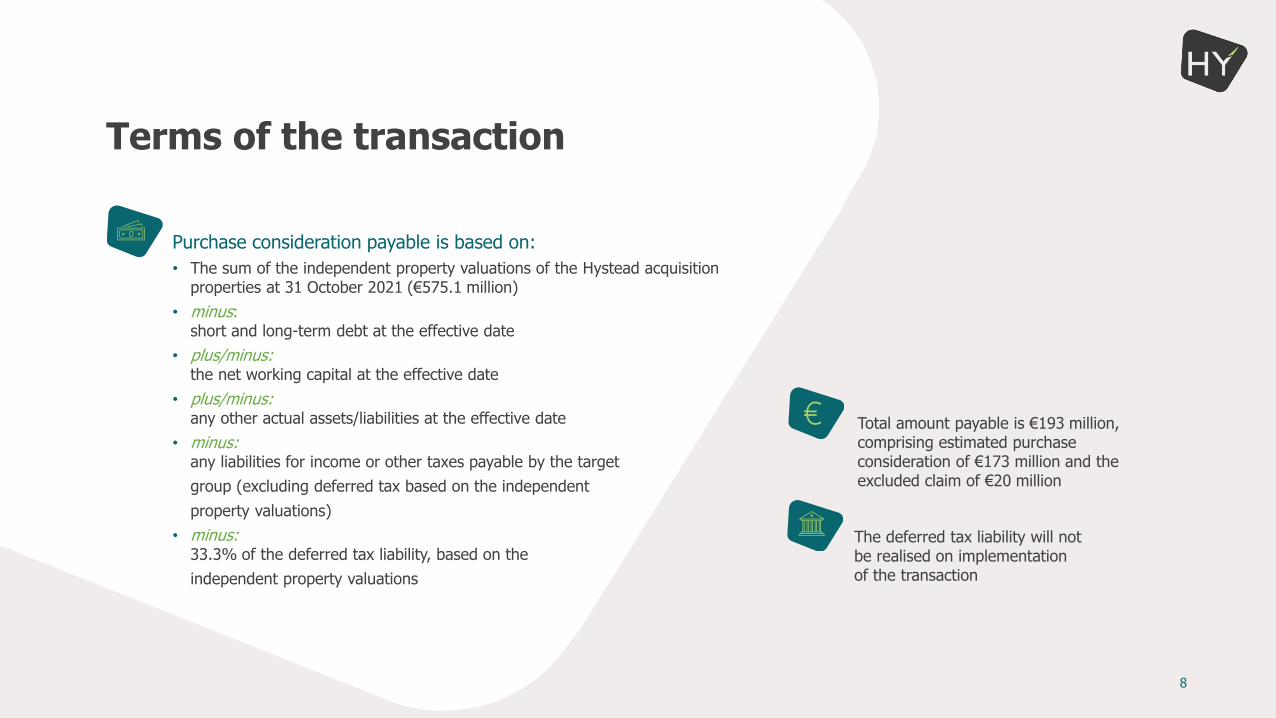

Total amount payable is €193 million, comprising estimated purchase consideration of €173 million and the excluded claim of €20 million

The deferred tax liability will not be realised on implementation of the transaction

Terms of the transaction

Purchase consideration payable is based on:

• The sum of the independent property valuations of the Hystead acquisition properties at 31 October 2021 (€575.1 million)

• minus: short and long-term debt at the effective date

• plus/minus: the net working capital at the effective date

• plus/minus: any other actual assets/liabilities at the effective date

• minus: any liabilities for income or other taxes payable by the target

group (excluding deferred tax based on the independent

property valuations)

• minus: 33.3% of the deferred tax liability, based on the

independent property valuations

8

Fundamentals

Amounts in € million 2019 2020 COVID 2021 COVID Transaction

Portfolio

Initial Purchase

Price

Valuation31 Dec

2018

Valuation 31 Dec

2019

Valuation31 Dec

2020

Valuation31 Oct

2021

Skopje City Mall 92 93.7 95.2 90.7 91.3

The Mall, Sofia 179 186.6 186.8 178.6 179.1

City Center one East 315 153.2 153.7 146.9 148.4

City Center one West 162.3 162.4 157.2 156.3

TOTAL 586 595.8 598.1 573.4 575.1

• Sofia NOI normalised given the Hypermarket conversion only completed in June 2019

** As per Circular

Valuations

Purchase price €20 million below December 2019 Valuation

595.8 598.1 573.4 575.1

Dec 2018

Dec 2019

Dec 2020

Oct2021

AFS Dec 2019

AFS Dec 2020

AFS Dec 2021

BudgetJun 2023

NOI 46.3* 33.1 38.4 38.8

Yield 7.8% 5.5% 6.7% 6.8%

AFS Dec 2019

NOI 46.3

Yield 8.1%

**

*

**

9

Why are we doing it? (1 of 3)

• In line with Hyprop’s diversification strategy

• Understand the centres and have a 4-year history

• Retain competent asset management and property

management teams:

• Ensuring in-country know how; and

• Continuity

10

Why are we doing it? (2 of 3)

Upside on all centres: City Center One East & West

• Expansion opportunity due to tenant demand

The Mall of Sofia, Bulgaria

• Hyper conversion only completed 7 months before Covid

• Food court fully upgraded

• Revamp of bathrooms started

Skopje City Mall, North Macedonia

• Right sizing of tenants and strengthening of tenant mix

• Upgrade of food court and bathrooms

• Improvement of internal flow

• Upgrading of external restaurant and play area

11

Why are we doing it? (3 of 3)

• Solid base to grow the EE portfolio

• Optimise capital structure

• Restructure debt

• Create real Euro equity by investing circa €173 million

• Reducing Euro-denominated equity debt exposure

• Reducing the cross-currency risk/exposure

• Settle Hystead equity debt from sale proceeds

12

Capital profit/loss in Hystead

€ 789 million € 785 million +/- reserves

• Dividends payable per shareholder agreement

• Shareholders agreed to retain dividends during Covid

• Any profit/losses up to 31 May 2022:

Profit: 60% (Hyprop) / 40% (PDI)

Loss: 78% (Hyprop) / 22% (PDI)

• Any profit/loss after 31 May 2022:

In terms of actual shareholding

Delta City Belgrade€ 128 million

Delta City Podgorica€ 76 million

The Mall Sofia€ 179 million

Skopje City Mall€ 92 million

City Center One East & West€ 315 million

Delta City Belgrade€ 115 million

Accumulated reserves € ?

4 transaction properties€ 575 million

Delta City Podgorica€ 95 million

In-country and equity debt€ 786 million

Initial valuation on acquisition by Hystead

Current valuation based on Hyprop transaction and other sales

13

The financial implications

14

How will we fund it?

The purchase consideration: Funded from:

15

€ million R billion

Purchase Price 173 2.9

Excluded Claim 20 0.4

193 3.3

R billion

Cash 2.0

Bank Facilities 0.9

Excluded Claim 0.4

3.3

Undrawn Facilities 2.4

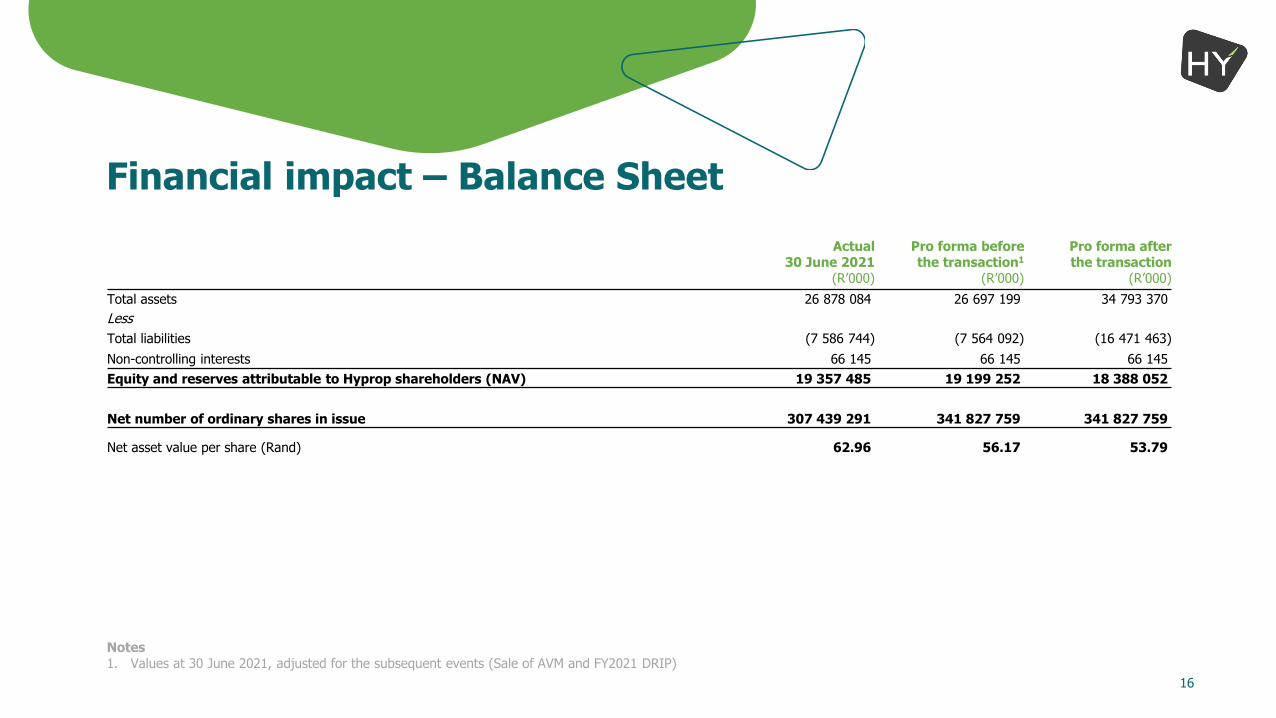

Financial impact – Balance Sheet

Actual30 June 2021

(R’000)

Pro forma beforethe transaction1

(R’000)

Pro forma afterthe transaction

(R’000)

Total assets 26 878 084 26 697 199 34 793 370

Less

Total liabilities (7 586 744) (7 564 092) (16 471 463)

Non-controlling interests 66 145 66 145 66 145

Equity and reserves attributable to Hyprop shareholders (NAV) 19 357 485 19 199 252 18 388 052

Net number of ordinary shares in issue 307 439 291 341 827 759 341 827 759

Net asset value per share (Rand) 62.96 56.17 53.79

Notes1. Values at 30 June 2021, adjusted for the subsequent events (Sale of AVM and FY2021 DRIP)

16

Notes1. At 30 June 2021, after adjusting for the sale of AVM and the FY2021 DRIP (“the subsequent events”)

Pro Forma Statement of Financial Position

Hyprop as at30 June 2021

Audited(R’000)

Hyprop as at30 June 2021

Pro forma 1

(R’000)

After the subsequent events and the

TransactionPro forma

(R’000)ASSETSNon-current assets 22 993 712 23 059 836 32 744 293

Investment property 21 831 329 21 831 329 31 618 324Property, plant and equipment 261 306 261 306 308 786Financial asset – Hystead 297 234 297 234 136 534Other non-current assets 603 843 669 967 680 496

Current assets 908 208 1 792 055 203 769Cash and cash equivalents 777 691 1 661 538 4 899Other current assets 130 517 130 517 198 870

Assets: held-for-sale 2 976 164 1 845 308 1 845 308Total assets 26 878 084 26 697 199 34 793 370EQUITY AND LIABILITIESEquity and reserves 19 291 340 19 133 107 18 321 907LIABILITIESNon-current liabilities 4 498 965 4 498 965 11 326 752

Borrowings 4 132 704 4 132 704 9 887 802Intercompany loans – Hystead - - 357 374Other non-current liabilities 366 261 366 261 1 081 576

Current liabilities 1 851 666 1 856 666 3 936 250Borrowings 1 281 593 1 281 593 3 186 686Other current liabilities 570 073 575 073 749 564

Liabilities: held-for-sale 1 236 113 1 208 461 1 208 461Total liabilities 7 586 744 7 564 092 16 471 463Total equity and liabilities 26 878 084 26 697 199 34 793 370

17

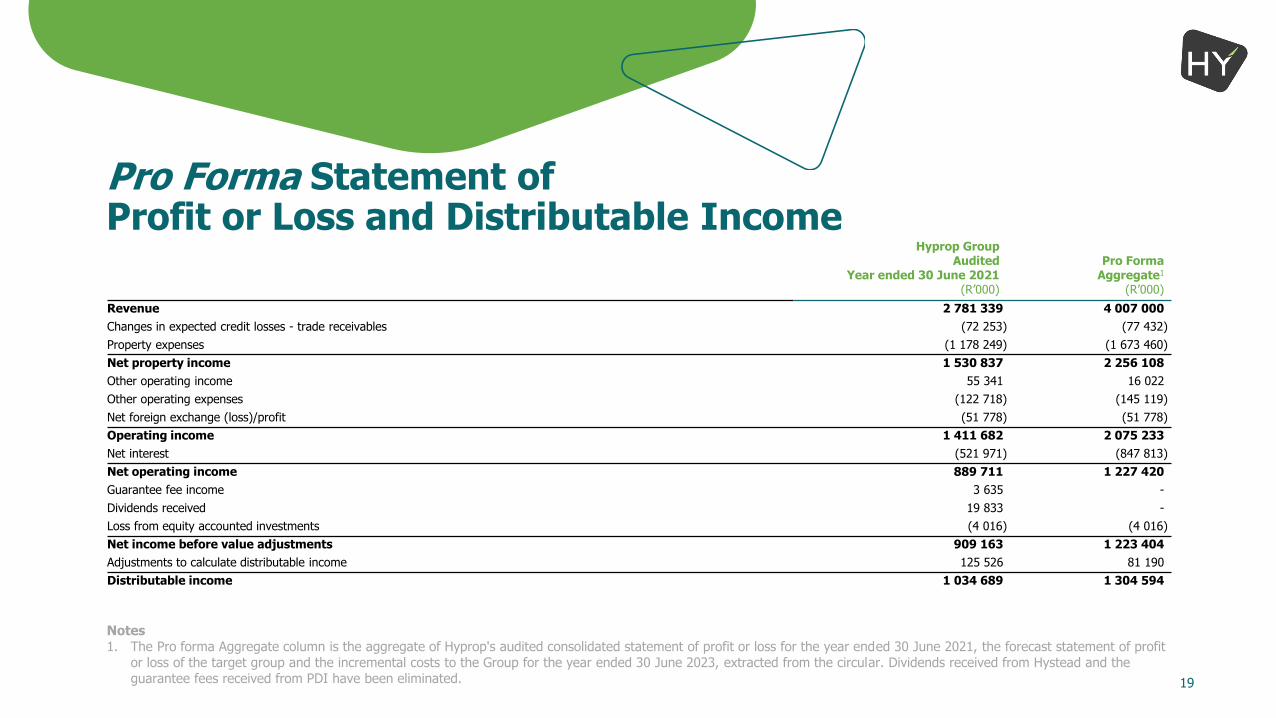

Financial Impact - Income Statement

ForecastYear ending

30 June 2022(R’000)

ForecastYear ending

30 June 2023(R’000)

Profit for the period/year of the target group 97 473 418 491

Incremental costs for the Group1 (47 557) (128 500)

Profit for the period/year for the Group attributable to the transaction 49 916 289 991

Adjustments to calculate distributable income 2 255 3 385

Distributable income for the period/year attributable to the transaction 52 171 293 376

Net number of ordinary shares in issue 341 827 759 341 827 759

Distributable income per share attributable to the transaction (cents) 15.26 85.832

Notes1. Incremental costs for the Group for the 3 months ending 30 June 2022 include the transaction costs of R12.3 million.2. Equivalent to 25% of Hyprop’s distributable income per share for the year ended 30 June 2021 of 336.5 cents per share. 18

Notes1. The Pro forma Aggregate column is the aggregate of Hyprop's audited consolidated statement of profit or loss for the year ended 30 June 2021, the forecast statement of profit

or loss of the target group and the incremental costs to the Group for the year ended 30 June 2023, extracted from the circular. Dividends received from Hystead and the guarantee fees received from PDI have been eliminated.

Pro Forma Statement of Profit or Loss and Distributable Income

Hyprop GroupAudited

Year ended 30 June 2021(R’000)

Pro FormaAggregate1

(R’000)

Revenue 2 781 339 4 007 000

Changes in expected credit losses - trade receivables (72 253) (77 432)

Property expenses (1 178 249) (1 673 460)

Net property income 1 530 837 2 256 108

Other operating income 55 341 16 022

Other operating expenses (122 718) (145 119)

Net foreign exchange (loss)/profit (51 778) (51 778)

Operating income 1 411 682 2 075 233

Net interest (521 971) (847 813)

Net operating income 889 711 1 227 420

Guarantee fee income 3 635 -

Dividends received 19 833 -

Loss from equity accounted investments (4 016) (4 016)

Net income before value adjustments 909 163 1 223 404

Adjustments to calculate distributable income 125 526 81 190

Distributable income 1 034 689 1 304 594

19

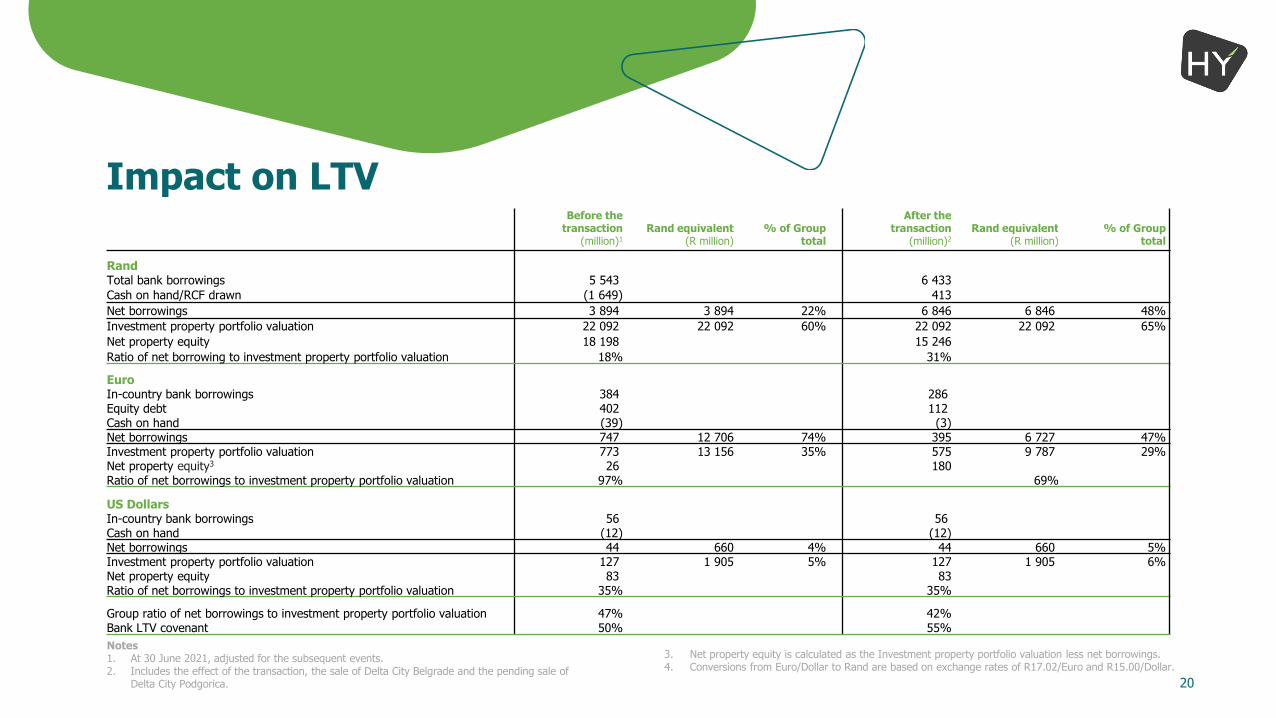

Impact on LTVBefore the

transaction(million)1

Rand equivalent(R million)

% of Grouptotal

After the transaction

(million)2

Rand equivalent(R million)

% of Grouptotal

RandTotal bank borrowings 5 543 6 433

Cash on hand/RCF drawn (1 649) 413

Net borrowings 3 894 3 894 22% 6 846 6 846 48%

Investment property portfolio valuation 22 092 22 092 60% 22 092 22 092 65%

Net property equity 18 198 15 246

Ratio of net borrowing to investment property portfolio valuation 18% 31%

EuroIn-country bank borrowings 384 286Equity debt 402 112Cash on hand (39) (3)Net borrowings 747 12 706 74% 395 6 727 47%Investment property portfolio valuation 773 13 156 35% 575 9 787 29%Net property equity3 26 180Ratio of net borrowings to investment property portfolio valuation 97% 69%

US DollarsIn-country bank borrowings 56 56Cash on hand (12) (12)Net borrowings 44 660 4% 44 660 5%Investment property portfolio valuation 127 1 905 5% 127 1 905 6%Net property equity 83 83Ratio of net borrowings to investment property portfolio valuation 35% 35%

Group ratio of net borrowings to investment property portfolio valuation 47% 42%Bank LTV covenant 50% 55%

Notes1. At 30 June 2021, adjusted for the subsequent events.2. Includes the effect of the transaction, the sale of Delta City Belgrade and the pending sale of

Delta City Podgorica.

3. Net property equity is calculated as the Investment property portfolio valuation less net borrowings.4. Conversions from Euro/Dollar to Rand are based on exchange rates of R17.02/Euro and R15.00/Dollar.

20

In closing

21

• In line with Hyprop’s diversification strategy

• Understand the centres and have a 4-year history

• Retain competent asset management and property management teams

• Upside on all centres

• Solid base to grow the EE portfolio

• Optimise capital structure

• Settle the remaining Hystead equity debt from sale proceeds

Our rationale

22

Q&A

23

Hyprop’s exposure and Hystead’s borrowings

€ millions %

Borrowings 786 100.0

In-country borrowing 384 48.9

Equity debt 402 51.1

The equity debt is guaranteed as follows:

Hyprop PDI Total

Guarantees issued to lenders 362.0 40.0 402.0

Back-to-back security from PDI (47.2) 47.2 -

Net exposure 314.8 87.2 402.0

% of total net exposure 78.3% 21.7%

24

Disclaimer

This presentation and any materials distributed in connection with this presentation may include certain forward-looking statements beliefs or opinions including statements with respect to the company’s business financial condition and results of operations. These statements which contain the words “will” “potential” “anticipate” “believe” “intend” “estimate” “expect” “forecast” and words of similar meaning reflect the directors’ beliefs and expectations and involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. No representation is made that any of these statements or forecasts will come to pass or that any forecast results will be achieved. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by these statements and forecasts. Past performance of the company cannot be relied on as a guide to future performance. Forward-looking statements speak only as at the date of this presentation and the company expressly disclaims any obligations or undertaking to release any update of or revisions to any forward-looking statements in this presentation. No statement in this presentation is intended to be a profit forecast. As a result, you are cautioned not to place any undue reliance on such forward-looking statements.

This document speaks as of the date hereof. No reliance may be placed for any purposes whatsoever on the information contained in this document or on its completeness accuracy or fairness. This information has not been audited or legally verified. The company, its advisers and each of their respective members, directors, officers and employees are under no obligation to update or keep current the information contained in this presentation to correct any inaccuracies which may become apparent or to publicly announce the result of any revision to the statements made herein except where they would be required to do so under applicable law and any opinions expressed in them are subject to change without notice. No representation or warranty express or implied is given by the company or any of its subsidiary undertakings or affiliates or directors, officers or any other person as to the fairness accuracy or completeness of the information or opinions contained in this presentation and no liability whatsoever for any loss howsoever arising from any use of this presentation or its contents otherwise arising in connection therewith is accepted by any such person in relation to such information.

25

v

26

Related Documents