The Hunter Economy: Carpe Diem! Alan Rai, HRF Principal Economist

Hunter economic update - May 2015

Jul 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Hunter Economy:

Carpe Diem!

Alan Rai, HRF Principal Economist

PRESENTATION OUTLINE

• ‘Pulse check’ of the local economy

– Still trying to rebalance away from mining

– Unemployment remains high

• Future opportunities and threats

– Free trade agreements

– The need to ‘think global, act local’

• Future of Professional Services

– SWOT analysis of three sectors:

• Financial services

• Legal, HR and real estate

• Engineering & technical services

HUNTER ECONOMY’S PERFORMANCE

• Still feeling the effects of

end of mining boom

– Unemployment remains high

– Weak business confidence

• (Weak) green shoots exist

– Lower A$: boosts our exporters

– Record low interest rates (good for borrowers)

– Low petrol prices: boost for consumers (e.g. households)

• Improving household confidence

– But will it translate into higher spending?

REGIONAL ECONOMYA ‘pulse check’

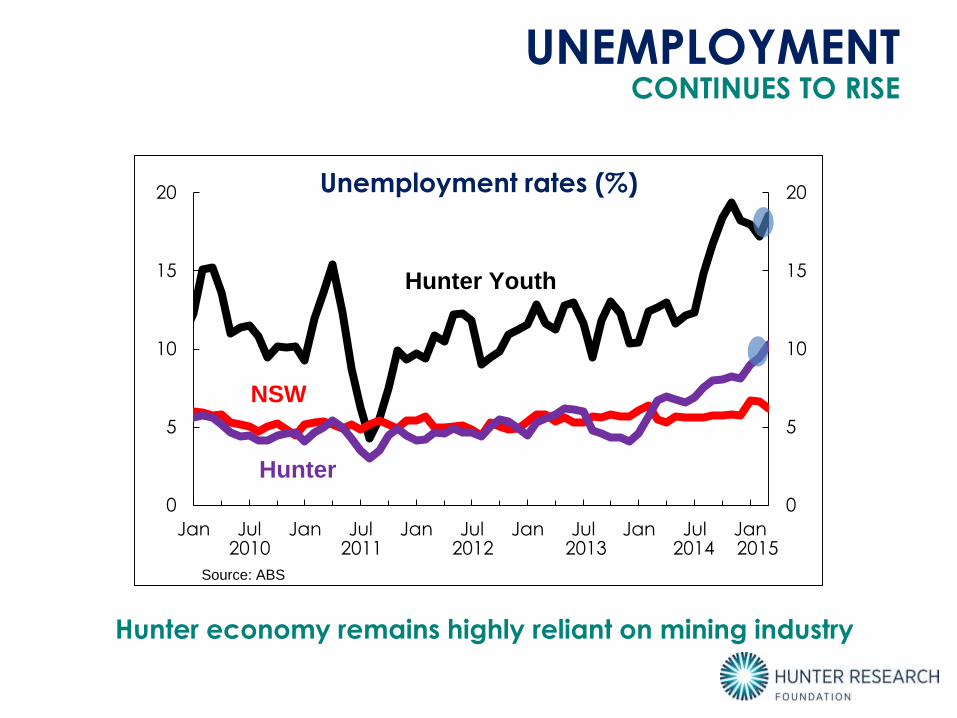

UNEMPLOYMENT

Hunter economy remains highly reliant on mining industry

CONTINUES TO RISE

0

5

10

15

20

0

5

10

15

20

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan

Unemployment rates (%)

Hunter Youth

Hunter

Source: ABS

NSW

2010 2011 2012 2013 2014 2015

Time for audience

participation!

ECONOMIC CHILLS

0

2

4

6

8

10

0

2

4

6

8

10

2011 2012 2013 2014 2015 2016

Growth in real GDP (% p.a.)

?

Australia

Dec 2014

forecast

April 2015

forecast

WHEN CHINA SNEEZES WE…?ECONOMIC GROWTH: COOLING

0

2

4

6

8

10

0

2

4

6

8

10

2011 2012 2013 2014 2015 2016

Growth in real GDP (% p.a.)

China

Australia

Dec 2014

forecast

April 2015

forecast

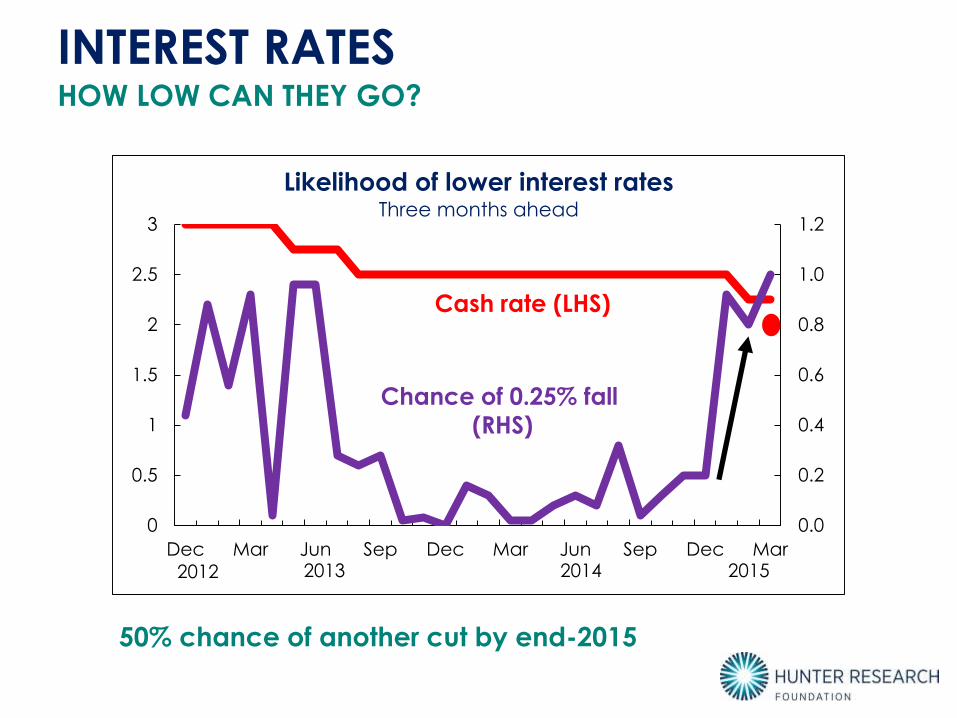

INTEREST RATES

50% chance of another cut by end-2015

HOW LOW CAN THEY GO?

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0

0.5

1

1.5

2

2.5

3

Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar

Likelihood of lower interest ratesThree months ahead

Chance of 0.25% fall

(RHS)

Cash rate (LHS)

2012 2013 2014 2015

Within two hours of here….

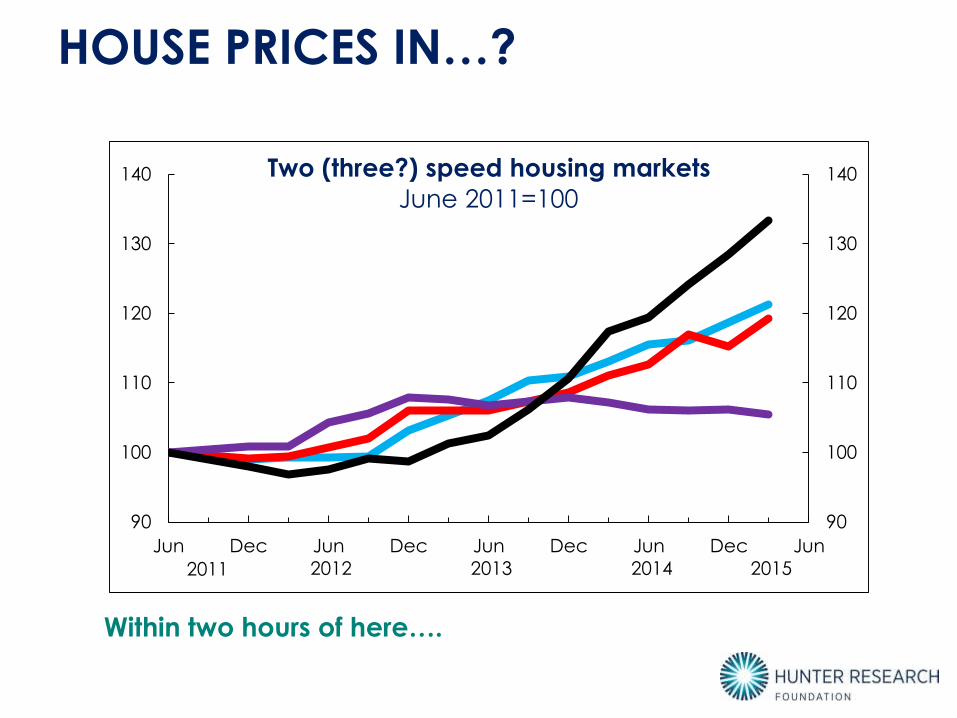

HOUSE PRICES IN…?

90

100

110

120

130

140

90

100

110

120

130

140

Jun Dec Jun Dec Jun Dec Jun Dec Jun

Two (three?) speed housing markets

June 2011=100

2011 2012 2013 2014 2015

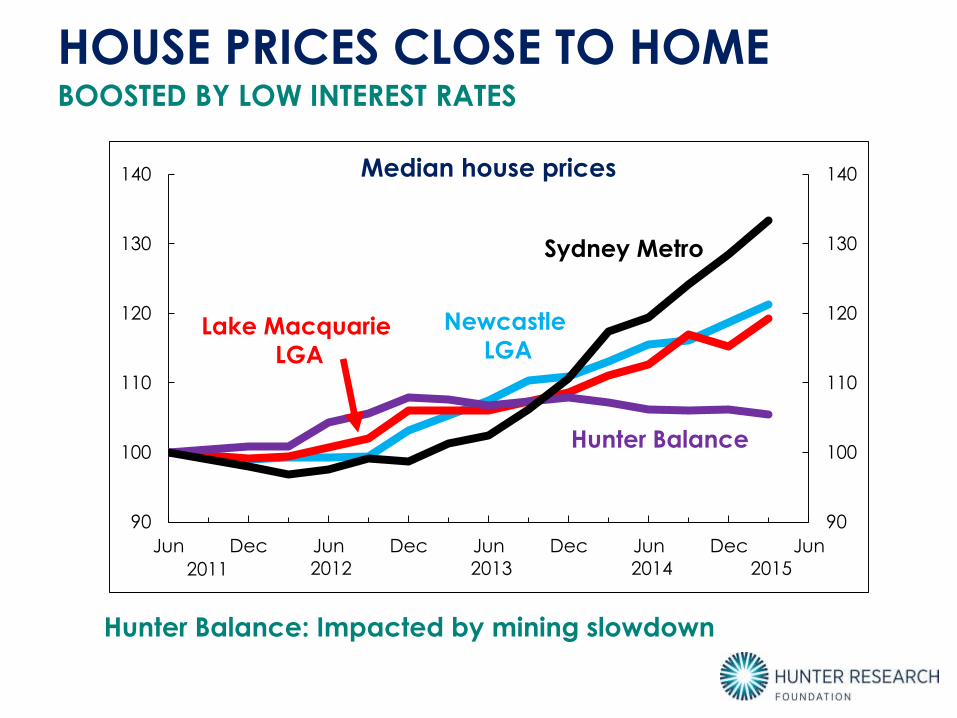

Hunter Balance: Impacted by mining slowdown

HOUSE PRICES CLOSE TO HOME

90

100

110

120

130

140

90

100

110

120

130

140

Jun Dec Jun Dec Jun Dec Jun Dec Jun

Median house prices

2011 2012 2013 2014 2015

Lake Macquarie

LGA

Newcastle

LGA

Hunter Balance

Sydney Metro

BOOSTED BY LOW INTEREST RATES

Time for audience

participation!

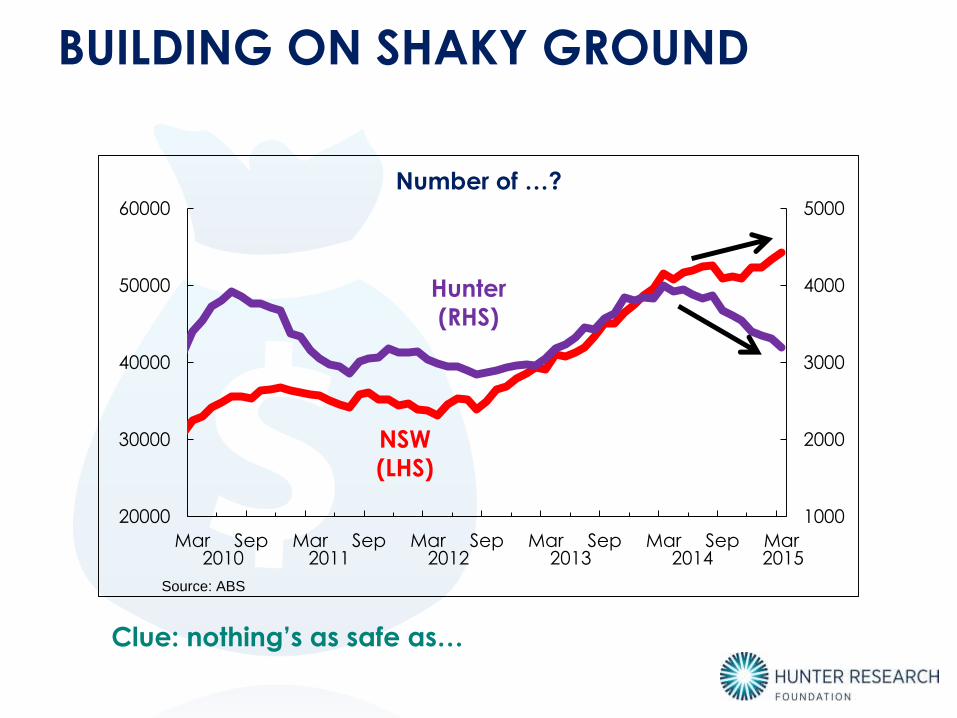

BUILDING ON SHAKY GROUND

Clue: nothing’s as safe as…

1000

2000

3000

4000

5000

20000

30000

40000

50000

60000

Mar Sep Mar Sep Mar Sep Mar Sep Mar Sep Mar

Number of …?

Source: ABS

NSW

(LHS)

Hunter

(RHS)

2010 2011 2012 2013 2014 2015

SYDNEY VS THE HUNTER

Less of a growth driver locally, due to high unemployment

1000

2000

3000

4000

5000

20000

30000

40000

50000

60000

Mar Sep Mar Sep Mar Sep Mar Sep Mar Sep Mar

Number of dwelling approvals (per annum)

Source: ABS

NSW

(LHS)

Hunter

(RHS)

2010 2011 2012 2013 2014 2015

SOMETHING TO DWELL ON

ECONOMIC OUTLOOK

Household confidence boosters: low interest rates and petrol prices

DIVERGING EXPECTATIONS

-0.2

-0.1

0

0.1

0.2

0.3

0.4

-0.2

-0.1

0

0.1

0.2

0.3

0.4

Mar Sep Mar Sep Mar Sep Mar Sep Mar Sep Mar

Economic outlook for the Hunter Next 12 months

Source: HRF

>0: improving, <0: worsening

Businesses

Households

2010 2011 2012 2013 2014 2015

MAY 2015 BUDGET

• What are its broad aims?

– Increase workforce

participation

– Boost employment and

investment

• Enabling policies– ‘Carrots’ for working mums; ‘sticks’ to stay-at-home

– Incentives to hire over-50s and under-25s

– Tax cut for SMEs; accelerated depreciation

• Are the policies a remedy for the current situation?

– Economy has excess labour supply, not labour demand

– Lack of sales is the major constraint….not higher taxes

– Lack of demand-boosting policies

ECONOMIC STRATEGY

SUMMING UP

• Suffering from the end of the

mining investment boom

– Unemployment remains high

– Weak business confidence

• (Weak) green shoots exist!

– Lower A$: boosts our exporters

– Record low interest rates (good for borrowers)

– Low petrol prices: boost for consumers (e.g. households)

• Improving household confidence

– May not lead to higher spending until unemployment falls

• Is the budget a remedy in the short-term? Unlikely

‘PULSE CHECK’ OF LOCAL ECONOMY

OPPORTUNITIES FOR THE REGIONPost mining boom

CONTEXTECONOMIC TRANSITIONS

• From high value mining to

lower value services:

– Australia-wide issue

– Transition can’t be avoided

– How to maintain the growth

during the mining boom?

• Services are not equally value-adding

– Professional services are highest value creators

– Finance; legal; HR; real-estate; and scientific services

• Global competition: an opportunity and a threat

– Competition will be spurred by recent FTAs

COMPARATIVE

ADVANTAGESWHERE DO OUR OPPORTUNITIES LIE?

• Comparative advantages:

– Energy (e.g. renewables)

– ‘Agritourism’, Wine, Equine

– Advanced manufacturing

• What are our comparative disadvantages?

– Unskilled, cheap labour• Mass production

• Standardised manufacturing

– Our high (labour) costs resemble the Germans & Swiss

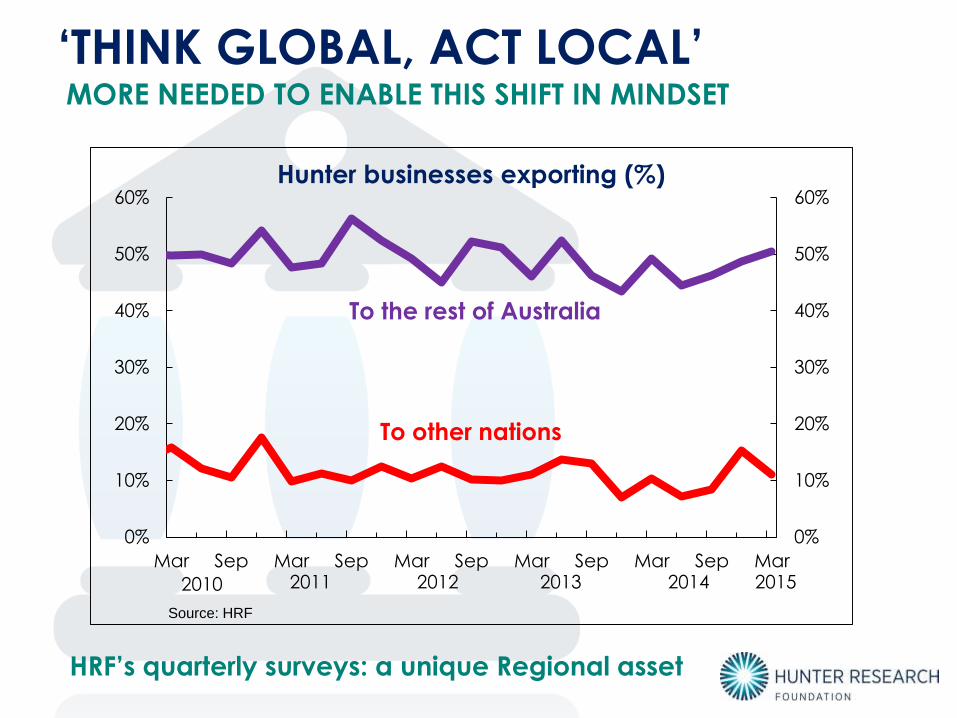

‘THINK GLOBAL, ACT LOCAL’MORE NEEDED TO ENABLE THIS SHIFT IN MINDSET

0%

10%

20%

30%

40%

50%

60%

0%

10%

20%

30%

40%

50%

60%

Mar Sep Mar Sep Mar Sep Mar Sep Mar Sep Mar

Hunter businesses exporting (%)

Source: HRF

To other nations

To the rest of Australia

2010 2011 2012 2013 2014 2015

HRF’s quarterly surveys: a unique Regional asset

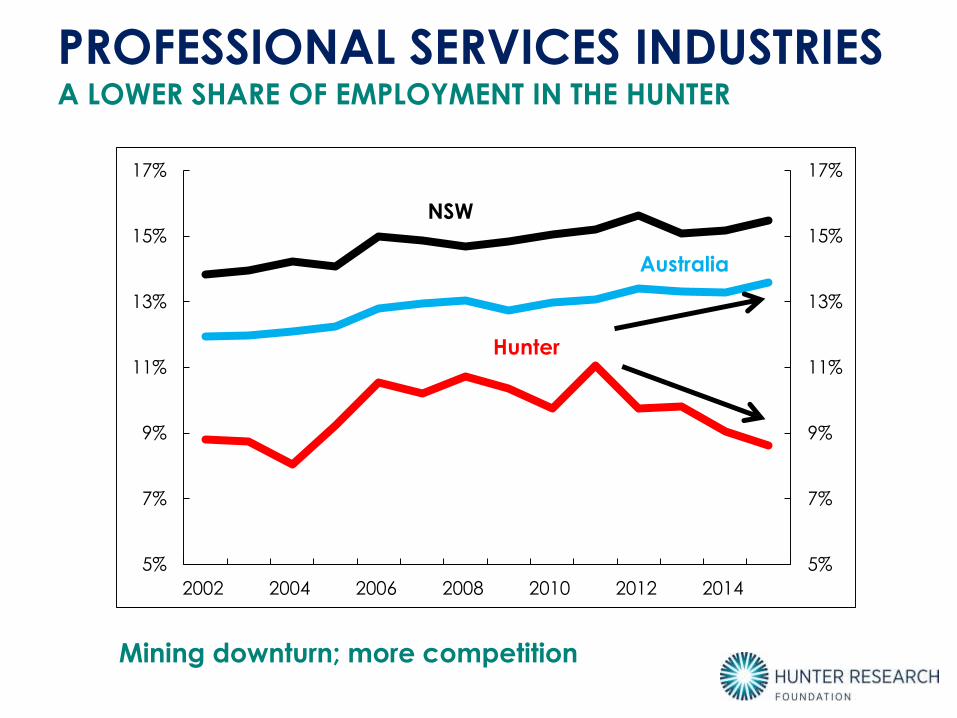

PROFESSIONAL SERVICES INDUSTRIES

5%

7%

9%

11%

13%

15%

17%

5%

7%

9%

11%

13%

15%

17%

2002 2004 2006 2008 2010 2012 2014

NSW

Australia

Hunter

Mining downturn; more competition

A LOWER SHARE OF EMPLOYMENT IN THE HUNTER

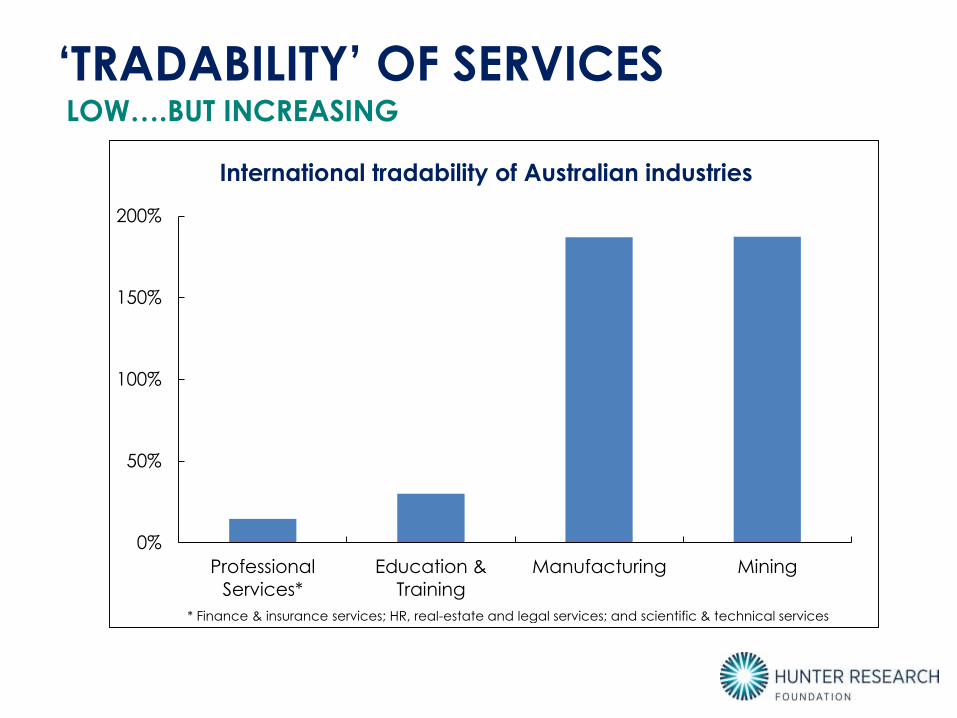

‘TRADABILITY’ OF SERVICESLOW….BUT INCREASING

0%

50%

100%

150%

200%

Professional

Services*

Education &

Training

Manufacturing Mining

International tradability of Australian industries

* Finance & insurance services; HR, real-estate and legal services; and scientific & technical services

HUNTER PROFESSIONAL SERVICESWays to enhance its global competitiveness

• What are the opportunities?

– Technology adoption

– Collaboration (are existing networks effective?)

– Export-oriented

• What are the constraints?

– Is lack of existing scale a barrier? How important are

economies of scale?

– Access to the right skills (especially in regional context)

– Funding/cashflow constraints for investment

HUNTER’S PROFESSIONAL

SERVICESRESEARCH QUESTIONS ADDRESSED

HUNTER’S PROFESSIONAL SERVICES

OUR RESEARCH AMBASSADORS

LESSONS LEARNTSTRATEGIC THINKING MUST

BE TOP OF MIND

• Manufacturing Our Future project

– What differentiates improving from

declining firms?

• What is the recipe for success?

– Formal strategic business planning

– Connect with global supply chains and networks

– Focus on high-value segments of the supply chain

– Innovative work processes and practices

– Culture change (less risk averse; globally-focused)

• ‘Ingredients’ also apply to professional services

CARPE FUTURUM!

• Hunter’s economic pulse is currently weak

• How can we remain economically vibrant?

– ‘Think global, act local’

– Focus on our comparative advantages

– What would John

Keating say?

LET’S MAKE OUR ECONOMY EXTRAORDINARY!

Source: http://theproactiveprofessional.com/tag/dead-poets-society/

Delivering insights that move the Hunter forward

Thank you

Related Documents