MANAGING GROWTH, SCALE AND COMPLEXITY Douglas Flint Group Finance Director CLSA Conference – Hong Kong - September 2006

HSBC Managing Growth, Scale and Complexity

Aug 08, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MANAGING GROWTH, SCALE AND COMPLEXITY

Douglas FlintGroup Finance Director

CLSA Conference – Hong Kong - September 2006

XGS4354

2

Forward-looking statements

This presentation and subsequent discussion may contain certain forward-looking statements with respect to the financial condition, results of operations and business of the Group. These forward-looking statements represent the Group’s expectations or beliefs concerning future events and involve known and unknown risks and uncertainty that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Additional detailed information concerning important factors that could cause actual results to differ materially is available in our Annual Report.

XGS4354

3

Tegucigalpa

Bogotá

SanSalvador

San Jose

Managua

To be added with Grupo Banistmo S.A.

In 76 countries and territoriesWith 9,500 offices

XGS4354

4

Changed and expanded Group profile

Staff (FTE) 101,000 284,000 10%

Customers 25m > 100m 15%

RWAs US$ 225bn US$ 873bn 14%

HSBC’s market cap US$ 40bn US$ 202bn 17%

HSBC’s dividend yield – 31 Aug 2006 4.1%

1995 1H06 CAGR%

XGS4354

5

HSBC – record of growthDividends per share / earnings per share

0

20

40

60

80

100

120

140

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

DPS EPS

(US cents)

UK GAAP (excl goodwill amortisation) IFRS

XGS4354

6

Geographic coverage and scale

BULL

Investor reactions to HSBC core values

BEAR

• Too many moving parts?

• Hard to see what drives performance

• Is it manageable?

• Cross border differentiation

• Cost synergies

• Development opportunities for human talent pool

XGS4354

7

Change in geographic composition of group pre-tax profit has been dramatic• The source of profits is much broader and better balanced

• Contribution in 2005 from business outside three major markets similar size to those major markets in 2000

• Increased the contribution from emerging markets

(1) 2000 figures, UK GAAP excluding goodwill amortisation

21.6%

20.4%

34.5%

23.5%

HK UK US Rest of Group

2005 2000*

35.8%

7.4%

26.4%

30.4%

US$4,517m

US$757mUS$4,280m

US$4,935m

US$7,234m

US$2,724m

US$3,127m

US$3,692m

US$20,966m US$10,300m*2000 figures, UK GAAP excluding goodwill amortisation

XGS4354

8

Emerging market potential

BULL

Investor reactions to HSBC core values

BEAR

• Not as leveraged as pure plays

• Absence of consolidation premium

• Combination of emerging markets and developed economies offers powerful synergies

• Best positioned in China

XGS4354

9

Strong growth in emerging markets

Argentina 112 154 244 58Brazil 208 281 406 44China -26 32 334 944India 87 178 212 19Indonesia 70 76 113 49Malaysia 116 214 236 10Mexico 9 774 923 19Saudi Arabia 30 122 236 93South Korea 65 89 94 6Taiwan 45 107 68 -36Turkey 59 142 265 87UAE 130 192 308 60Total 905 2,361 3,439 +46

(US$ millions) 20001 2004 2005 % change 2004/2005

(1) 2000 figures, UK GAAP excluding goodwill amortisation

XGS4354

10

Which continues into 2006

Mexico 428 515 +20Middle East 204 378 +85Mainland China 161 280 +74Brazil 185 251 +36India 108 215 +99Saudi Arabia 128 181 +41Malaysia 103 128 +24Turkey 133 120 -10Argentina 165 83 -50South Korea 55 48 -13Philippines 19 43 +126Indonesia 55 27 -51Thailand 31 24 -23Taiwan 48 (43) n/aTotal 1,823 2,250 +23

Profit before tax (US$ millions) 1H05 1H06 % change

XGS4354

11

Capital strength

BULL

Investor reactions to HSBC core values

BEAR

• Reflects discipline

• Source of advantage if there are stresses

• Opportunity to leverage returns

• A drag on returns

XGS4354

12

Return on average invested capital – 1998 to 2005

0

5

10

15

20

1998 1999 2000 2001 2002 2003 2004 20050

20,000

40,000

60,000

80,000

100,000

Average Invested Capital (RHS) Return on Average Invested Capital (LHS)

(%) (US$m)

UK GAAP (excl goodwill amortisation) IFRS

XGS4354

13

Improving capital efficiency

70

80

90

100

1H04 2H04 1H05 2H05 1H065

10

15

20

Average invested capital employed (US$bn) Return on invested capital (%)

US$102bn

US$84bn

US$93bn

Generated 24% annualised return from additional US$9bn of capital

Tier 1 ratio (%)

Return on invested capital (%)

XGS4354

14

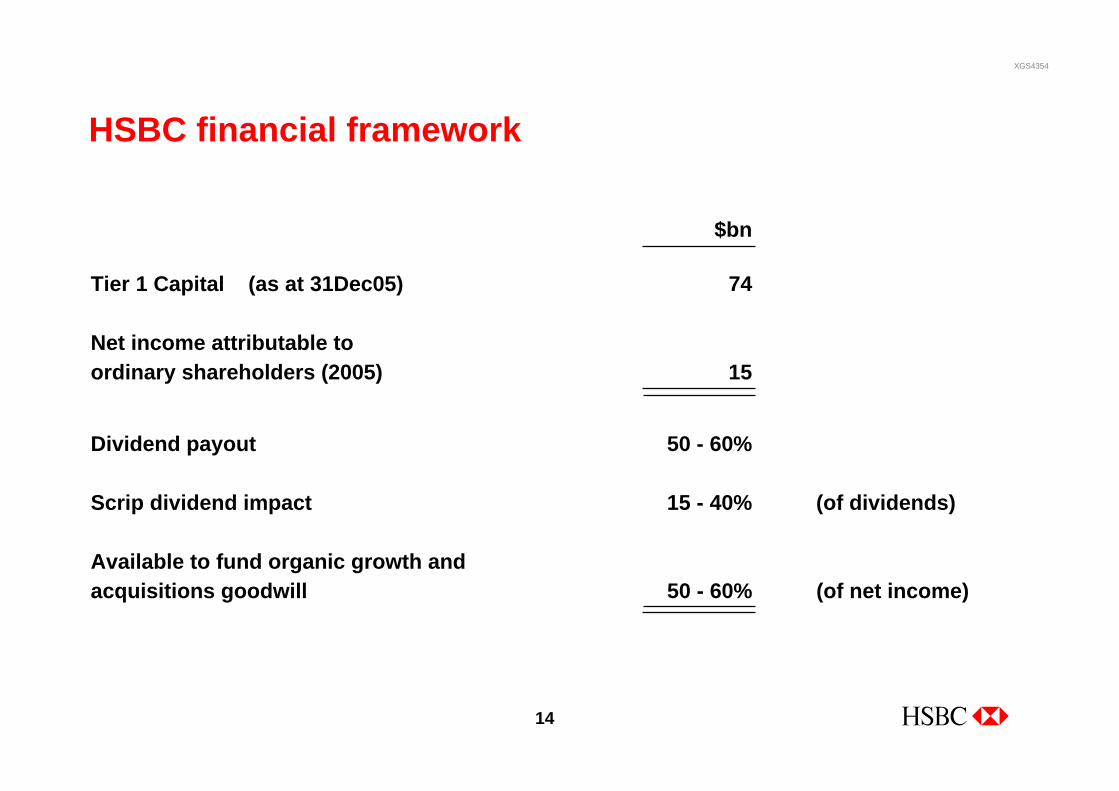

HSBC financial framework

$bn

Tier 1 Capital (as at 31Dec05) 74

Net income attributable to ordinary shareholders (2005) 15

Dividend payout 50 - 60%

Scrip dividend impact 15 - 40% (of dividends)

Available to fund organic growth and acquisitions goodwill 50 - 60% (of net income)

XGS4354

15

HSBC – profit before tax by main country – 2005

United StatesHong KongUnited Kingdom

US$4-5bn

MexicoFranceCanada

US$500m – 1bn

BrazilMainland ChinaSingaporeSwitzerlandMalaysiaUAEIndiaSaudi ArabiaArgentinaTurkeyGermanyBermudaIndonesiaMalta

US$100m – 500m

South KoreaAustraliaThailandTaiwanRep. of IrelandEgypt Qatar

US$50 – 100m

Personal Financial Services

Commercial Banking

Denotes significant acquisition in the last 10 years

ConsumerFinance

Private Banking

Corporate, Invest. Banking

& Markets

XGS4354

16

Longer term the recycling of capital through New York or London will diminish ‘South-North’ and ‘South-South’ investment flows increasingly important

Expected sources of FDI Latin America 2005-06 Expected sources of FDI Asia-Pacific 2005-06

Chinese outward direct investment Most attractive business locations for trans-national corporations 2005-06

Source: UNCTAD FDI Prospects 2005 Source: UNCTAD FDI Prospects 2005

Source: HSBC, CEIC Source: UNCTAD FDI Prospects 2005

0% 10% 20% 30% 40% 50% 60% 70%

US

China

Japan

Australia

India

0%

20%

40%60%

80%

100%

Chi

na

Indi

a

US

Rus

sia

Bra

zil

Mex

ico

Ger

man

y

UK

Thai

land

Can

ada

0

2,000

4,000

6,000

8,000

1991 1993 1995 1997 1999 2001 2003 2005

USDm

0% 10% 20% 30% 40% 50% 60% 70% 80%

US

Spain

Brazil

China

Canada

XGS4354

17

And scale allows us to think long term:Positioning for growth in Mainland China – patient money investment

Date Cost (US$m)

Market value (US$m)

2001 62

2002-5

2004

2004-5

Not listed

Not listed208

1.8bn 4.0bn

5.8bn2.2bn

XGS4354

18

Role of the centre – capital allocation

• Can we get scale?

• Have we comparative advantage and will it last?

• How consumptive of technology resource is it?

• How distracting will it be for existing management?

• How does the market value this business?

• Can we migrate the learning if successful?

XGS4354

19

Investment spend focused on higher growth markets

0

10

20

30

40

50

60

70

80

90

100-40 -30 -20 -10 0 10 20 30 40 50 60 70 80

Revenue growth1

Cos

t effi

cien

cy ra

tio1

48.8%2

12.5%2

Note: Size of circle represents profit contribution(1) Excluding Corporate, Investment Banking and Markets(2) Group average figure, excluding Corporate, Investment Banking and Markets

USUK

HongKong

Mainland ChinaFrance

Argentina Brazil

UAE

India

Mexico

Malaysia

Turkey

Canada

Re-engineer

Harvest

Invest

Grow

XGS4354

20

CIBM cost trends

Total cost growth has slowed

23.8%

12.5%

13.0%

17.2%

5.6%

6.5%

6.0%

0% 5% 10% 15% 20% 25% 30%

1H05 vs 1H04

2H05 vs 2H04

1H06 vs 1H05

2H04 vs 1H04

1H05 vs 2H04

2H05 vs 1H05

1H06 vs 2H05

% Change against comparable period

% Change against trailing half

0

2

4

6

8

10

12

14

16

18

20

2H04 vs 1H04

1H05 vs 2H04

2H05 vs 1H05

1H06 vs 2H05

% change

Jaws are positive

Revenue growth

Cost growth

XGS4354

21

Role of the centre – driving IT efficiencies from scale

Equipment/

tools

standardization

Best practice

and architecture

simplification

Application

consolidation

Geographical

& physical

consolidation

High

Cost savings

Low

Low Risk & difficulty to implement High

• Standardize applications used across the business

• Standardize business processes• Standardize Back office• Globalisation of customer base

• Elimination of excess overheads and fixed costs• Aggregation of demand, leverage economies of scale

• Multiple applications on a single partitioned server• Replace many low end servers with one high-end server• Enable ‘follow the sun’ support

• Advantages of skills transfer and Training• Increased purchasing leverage and Global best pricing

XGS4354

22

Technology

• Our customers are using technology in a transforming way:– 1.5 billion visits to HSBC websites in 2005, +48% on 2004– 25 million registered internet customers, +27% on 2004– High penetration in Commercial Banking with 950k registered internet banking

customers, around 40% of customer base– 271 million online transactions, +37% on 2004– 66% growth in online sales worldwide in 2005

• Constant drive to common architecture– HSBC Universal Banking (“HUB”)– Credit card system (WHIRL)– Bank on the internet - hsbc.com / HSBCnet

XGS4354

23

Role of the centre – examples of leveraging group skills• Mexico

• Internationality of Group key to ensuring success of acquisition– Influx of Group talent– Tightened controls (compliance and internal audit)– Installed new systems (treasury, branches, trade services and credit card)

• Leverage Mexico’s ATM capabilities – location selection, direct sales channel, charity donations

Rolling out the consumer finance model– Marketing skills Asia– Sophisticated analytics Mexico– Scaleable systems Brazil

XGS4354

24

In Global Markets we have rolled out our Asian financing model with great success

• Hub and spoke management complemented by in-country coverage expertise

• Strong local distribution coupled with global emerging markets platform provides optimal execution for issuers

In Latin America

In the Middle East and North Africa

Mandates at bookrunner or equivalent

In Central and Eastern Europe

0

10

20

30

2002 2003 2004 2005

Mandates - Bonds Mandates - Loans

0

10

20

30

40

2002 2003 2004 2005

Mandates - Bonds Mandates - Loans

0

10

20

2002 2003 2004 2005

Mandates - Bonds Mandates - Loans

XGS4354

25

Diversified risk profile

BULL

Investor reactions to HSBC core values

BEAR

• Over-exposed to US consumer • Most diversified by geography, customer segment and risk type

• Consumer finance model transferable

XGS4354

26

Role of the centre – maintaining a consistent risk profileAs a % of average risk-weighted assets

0

1

2

3

4

5

6

7

8

9

10

2001 2002 2003 2004 2005

Credit Charges RevenuesNote: 2001-2003, UK GAAP; 2004-2005 IFRS

XGS4354

27

US residential first mortgages & 2nd lien lending market

Recent trends• Housing market showing signs of slowing. Increased loan impairment charges in 1H06 due to

deteriorating performance in the 2005 vintages within our wholesale/correspondent business• Overall, the first lien mortgage book shows stable credit

(1) Percentages are based on stated portfolio. Certain loans may be included in more than one classification.Interest rate only balances are included in adjustable rate balances.

US residential first mortgages & 2nd lien lending 112 118 126

(US$ billions) 1H05 2H05 1H06

Geographical and composition1 considerations at 30 June, 2006

California 19 14 16

New York 23 5 10

Florida 5 8 7

(%) of portfolio Consumer Overallby State Bank Finance portfolio

Total book (US$bn) 38 89

Adjustable rate 77% 27%

Interest only 24% 7%

Second lien 10% 18%

Composition Bank Consumer Finance

XGS4354

28

Real estate market – key actions

• Risk mitigation programs and efforts are underway including– Enhanced segmentation– Stress testing to evaluate difference scenarios– Enhanced pricing models– Proactively working with customers regarding ARM resets

• Increased collection capacity and enhanced strategies

• Ongoing reassessments of origination metrics impacting second liens and stated income volumes

XGS4354

29

Role of the centre – managing scale and complexity

• Tone from the top

• Collective management

• Rotation of senior management

• Training at all levels

• Reward mechanisms

XGS4354

30

Role of the centre – developing human capital

• Core values underpin corporate culture– Putting the team’s interests ahead of individuals– Individual accountability, aversion to committees and bureaucracy– Speed of decision making– Integrity– Reputation is paramount

• Talent Management

• Diversity and international experience

XGS4354

31

Tegucigalpa

Bogotá

SanSalvador

San Jose

Managua

To be added with Grupo Banistmo S.A.

Distribution remains the key competitive advantage –and therefore highlights the importance of the brandHSBC Group international network

XGS4354

32

HSBC brandMake HSBC one of the world’s leading brands for customer experience and corporate social responsibility

• 1998 Brand identity

• 2002 Brand identity with differentiated positioning

• 2005 Using the Brand for business growth

HSBC now ranked No. 28 by Interbrand(Highest mover in top 40. Absent from top 100 in 2002)

HSBC Amanah

HSBC Direct USA

HSBC France

XGS4354

33

Outlook

• HSBC’s unique international distribution footprint provides the platform for profitable growth

• The Group’s scale and breadth, together with financial strength (Tier 1 capital 9.4 per cent at 30Jun06) provides competitive advantage

• Strong opportunities for organic growth in Asia, Turkey, Mexico, Brazil and the Middle East

• Opportunities to strengthen our position in established franchises in the US, UK, Hong Kong and France

• Growing momentum in Corporate, Investment Banking and Markets

XGS4354

34

Distribution

TechnologyBrand

Customer

Culture

OrganisationDistribution

TechnologyBrand

Customer

Culture

Organisation

Our main focus going forward

XGS4354

35

Tegucigalpa

Bogotá

SanSalvador

San Jose

Managua

To be added with Grupo Banistmo S.A.

In 76 countries and territoriesWith 9,500 offices

Related Documents