HSAs Set Sail forRapid Growth in 2017 What we have learned over 13 years Presented by Paula Weber, GBA Agency Partner, Vice President Group Service

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

HSAs Set SailforRapid Growth in 2017

What we have learned over 13 years

Presented by Paula Weber, GBAAgency Partner, Vice President Group Service

Today’s Agenda:

• HSA’s yesterday, today and tomorrow

• Employer plan administration twists and turns

• The key! Employee education and engagement

HSA Basics—Yesterday & Today• HSA’s became available in 2004 as the 1st attempt by Congress to control costs

through consumer-directed health plans (CDHP).• Devenir currently projects that by the end of 2018, the HSA market will

exceed $50 billion in HSA assets held in almost 30 million accounts.

HSA’s 101

• History• Basic structure• Contribution increase trends

4

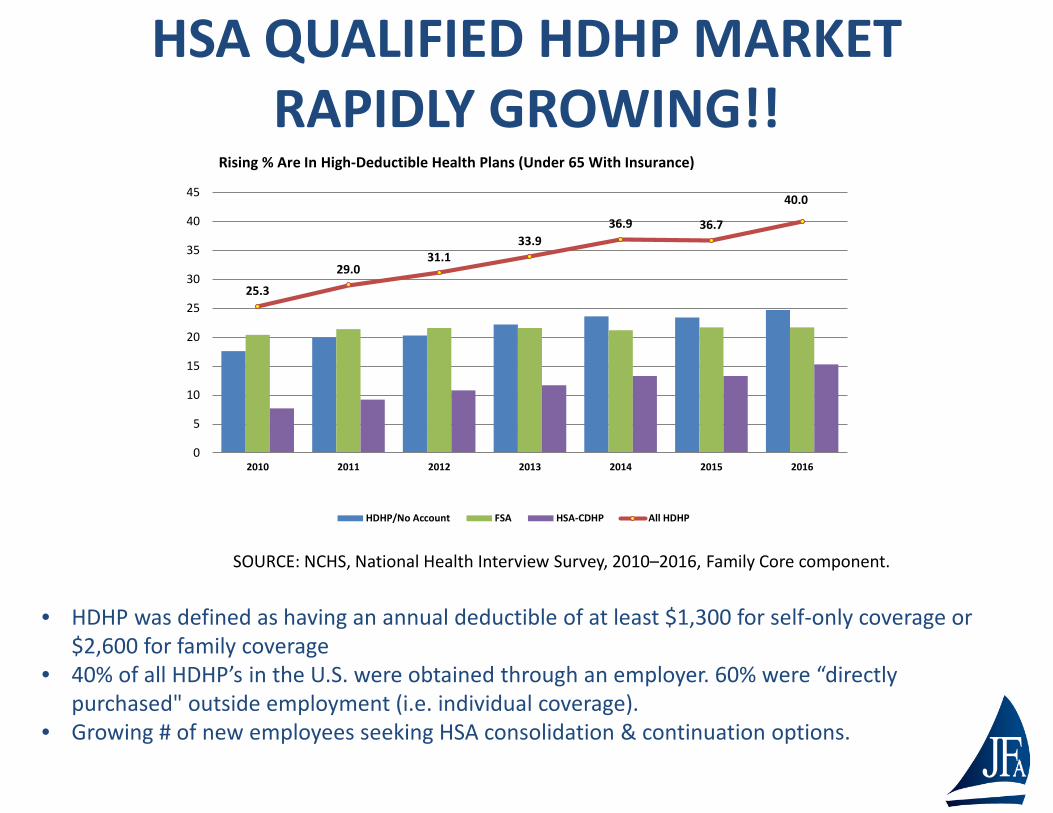

HSA QUALIFIED HDHP MARKET RAPIDLY GROWING!!

SOURCE: NCHS, National Health Interview Survey, 2010–2016, Family Core component.

• HDHP was defined as having an annual deductible of at least $1,300 for self-only coverage or $2,600 for family coverage

• 40% of all HDHP’s in the U.S. were obtained through an employer. 60% were “directly purchased" outside employment (i.e. individual coverage).

• Growing # of new employees seeking HSA consolidation & continuation options.

25.3

29.031.1

33.936.9 36.7

40.0

0

5

10

15

20

25

30

35

40

45

2010 2011 2012 2013 2014 2015 2016

HDHP/No Account FSA HSA-CDHP All HDHP

Rising % Are In High-Deductible Health Plans (Under 65 With Insurance)

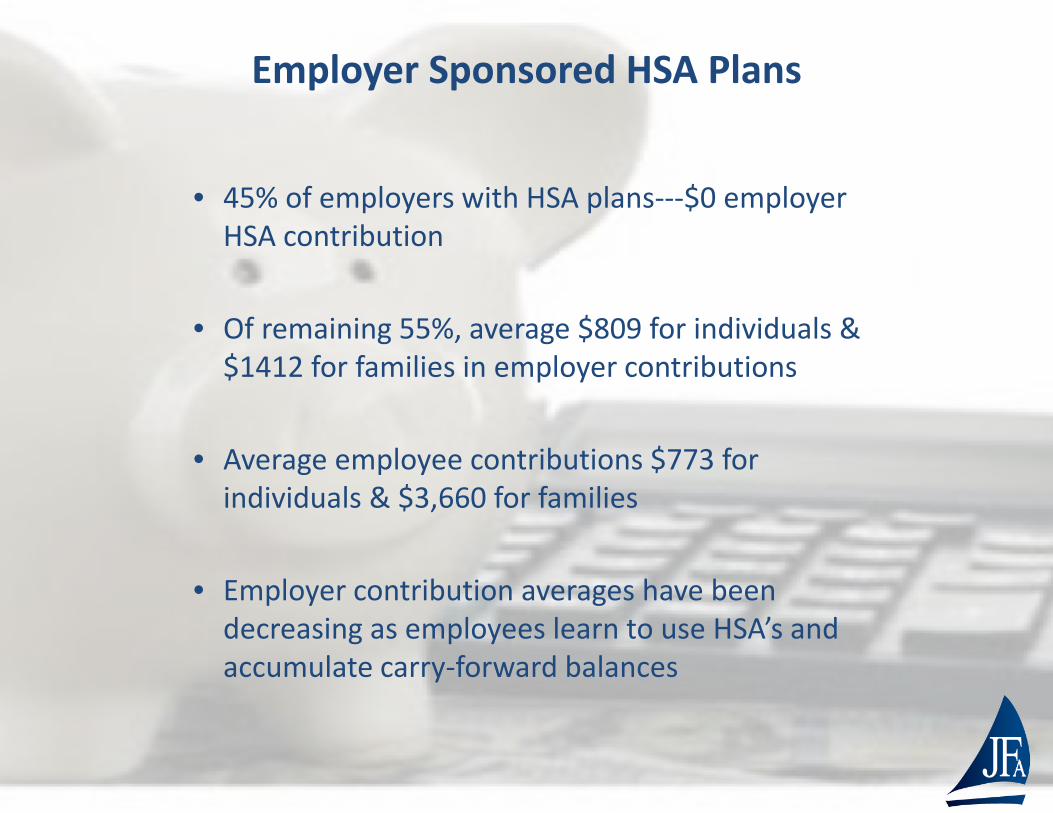

Employer Sponsored HSA Plans

• 45% of employers with HSA plans---$0 employer HSA contribution

• Of remaining 55%, average $809 for individuals & $1412 for families in employer contributions

• Average employee contributions $773 for individuals & $3,660 for families

• Employer contribution averages have been decreasing as employees learn to use HSA’s and accumulate carry-forward balances

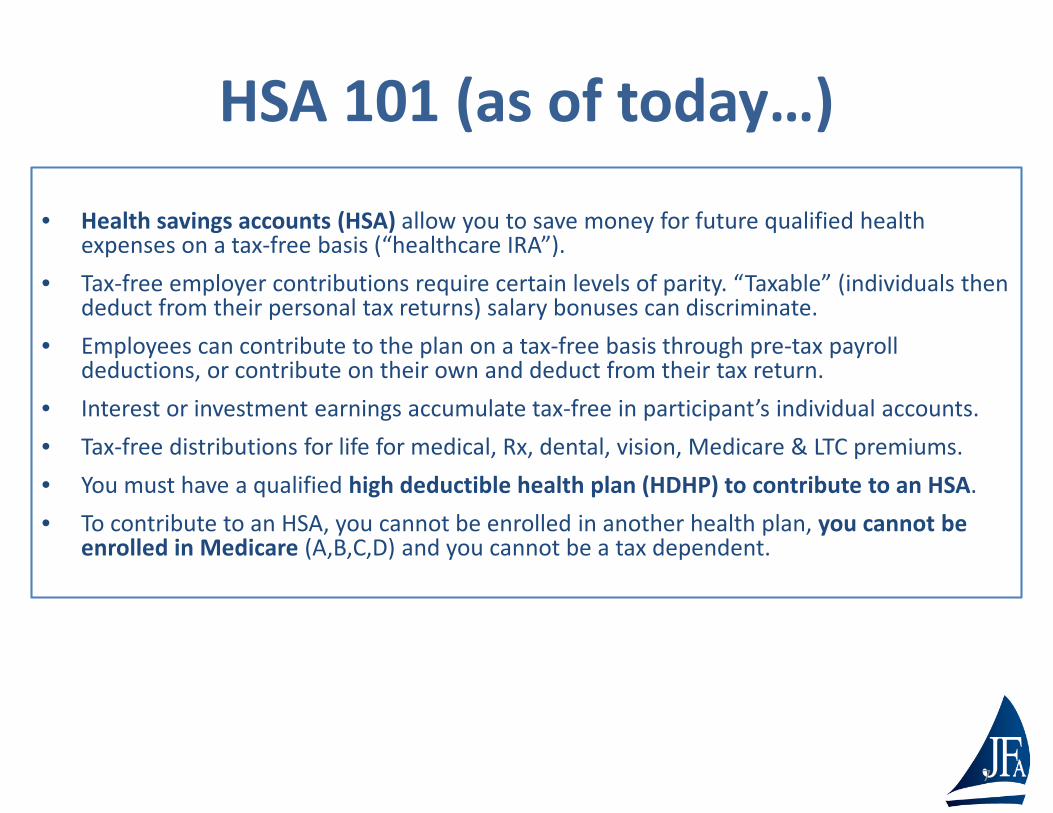

HSA 101 (as of today…)

• Health savings accounts (HSA) allow you to save money for future qualified health expenses on a tax-free basis (“healthcare IRA”).

• Tax-free employer contributions require certain levels of parity. “Taxable” (individuals then deduct from their personal tax returns) salary bonuses can discriminate.

• Employees can contribute to the plan on a tax-free basis through pre-tax payroll deductions, or contribute on their own and deduct from their tax return.

• Interest or investment earnings accumulate tax-free in participant’s individual accounts. • Tax-free distributions for life for medical, Rx, dental, vision, Medicare & LTC premiums. • You must have a qualified high deductible health plan (HDHP) to contribute to an HSA. • To contribute to an HSA, you cannot be enrolled in another health plan, you cannot be

enrolled in Medicare (A,B,C,D) and you cannot be a tax dependent.

7

HSA Recap (as of today…)

Consumer Owned

• Must be paired with a qualified high deductible health plan (HDHP)

• May pair with Limited Purpose FSA and/or HRA – Vision, dental

expenses only

Contributions

• Employer and/or consumer may contribute to the account

• Contributions made by payroll deduction, check, transfer

• IRS restrictions on annual contribution amount

Distributions

• No third party substantiation required –consumer responsible

• Internal Revenue Code §213(d) expenses may be reimbursed

• Funds may be withdrawn for non-qualified expenses with penalty

Account Balance

• Funds may carry over year to year

• Funds are portable

• Funds may be invested and earn interest for greater savings potential

Presenter

Presentation Notes

_______________________________________________________________________________ _______________________________________________________________________________ _______________________________________________________________________________ _______________________________________________________________________________

HSA Contribution Limits, Minimum Deductibles and Out-of-Pocket Maximums

Contribution and Out-of-Pocket Limitsfor Health Savings Accounts and High-Deductible Health Plans

For 2017 For 2016 ChangeHSA contribution limit Self-only: $3,400

Family: $6,750Self-only: $3,350

Family: $6,750Self-only: +$50

Family: no change

HSA catch-up contributions (age 55+) $1,000 $1,000 No change

HDHP minimum deductibles Self-only: $1,300Family: $2,600

Self-only: $1,300Family: $2,600

No change

IRS HDHP maximum out-of-pocket amounts (deductibles, co-payments, but not premiums)

Self-only: $6,550Family: $13,100

Self-only: $6,550Family: $13,100

No change

ACA HDHP maximum out-of-pocket amounts (deductibles, co-payments, but not premiums)

Self-only: $7,150Family: $14,300

Self-only: $6,850Family: $13,700

No change

HSA’s—TomorrowRapid expansion will continue

• HSA accounts now exceed 20 million. The number of HSA accounts rose to 20 million, holding almost $37 billion in assets, a year over year increase of 22% for HSA assets and 20% for accounts for the period of December 31st, 2015 to December 31st, 2016.

• HSA investments see continued growth. HSA investment assets reached an estimated $5.5 billion in December, up 29% year over year. The average investment account holder has a $14,971 average total balance (deposit and investment account).

• Devenir currently projects that by the end of 2018 the HSA market will exceed $50 billion in HSA assets held among over 29+ million accounts.

Source: 2016 Year-End Devenir HSA Research Report

• 400+ healthcare bills in the 214th Congress

• Interesting proposals for 2017…

Allow expenses prior to establishment of HSA (60-day retro limit)

Permitting spouses to make catch-up contributions to 1 HSA

Allowing reimbursement of premiums for pre-65 retirees

Increasing the annual maximum contribution to match health plan OOP limits

Repeal the pre-65 early withdrawal tax penalty from 20% down to 10%

Repeal the limit on FSA contributions (Currently $2,550) after Dec. 31, 2017

Allowing OTC’s without a prescription

Making accounts available independent of HDHPs

HSA Expansion under theAmerican Health Care Act (Trumpcare)

Do HSA’s really work? We feel they do, but effort is required to assist consumers in understanding the plans and how they operate!

• Encourages consumerism. Reduce unnecessary claims and costs.

• It’s not just employees foregoing medical care that reduces costs. Employees are using providers, supplies and services cost comparison tools. Seeking alternatives.

• Reduce cost trends—both premiums and claims over time– The CDHP (Consumer Driven Health Plan - i.e. an HSA qualified plan)

population had rates of utilization 9%-13% lower than the non-CDHP population for all categories of health services outside of brand prescriptions

– The CDHP had average annual total spending (participant cost plus insurance plan cost combined) of $520 less per plan participant per year.

Source: Health Care Institute September 2016

12

Plan Administration Twists & Turns• Participation:

– Make enrolling easy with electronic or mobile platform (“responsive design” is the latest trend)

– FSA and/or HRA coordination--grace period or carry-forwards?

– Caution! Voluntary plans (accident, critical illness) or telemedicine plans knock outs?

– Caution! Medicare enrollment knock-outs

• Education:– Teach employees how to “say out loud” that they have a

HDHP when going to a provider’s office – Show employees how the deductible works and how they

can track their progress and expenses

13

Plan Administration Twists & Turns continued…

• Funding:– Funds are not available on the day they are taken from the

employee’s payroll– Annual contributions not available on Jan 1st

– Funding can be flexible—annual, monthly or quarterly but when will funds be needed by employees?

– Employer contributions—comparable (by tier or EE category)? 35% penalty for discrimination

– What happens when your health plan year is non-calendar and the HSA runs on a calendar year?

– Can employees make a full year contribution if they enroll in the health plan mid-year? Testing is required

– Strategic planning--is utilization data available? How can you track the individual accounts funding from year to year?

14

Employee Education & Engagement• Hit them any way you can—online, apps, videos• Frequent reminders of how the program works, tools available, etc.• Connection between claims and HSA accounts• Time heals all• Co-worker champions• Growth of transparency tools• Sharing nameless success stories• Overcoming financial literacy shortcomings• 401k & HSA contributions—thinking of them together, not separate• iPay, Google pay—will debit cards be obsolete?

Other helpful tools include health risk assessments, cost calculators, bill payment applications, online receipt storage, real-time claims transactions information, and information for financial planning.

15

Consumer-Initiated Payment

Consumers may send payment directly to the parties who need payment by requesting a check to reimburse themselves or to send directly to their provider

HSA eContributeConsumers may choose to have contributions set up from more than one bank account

Expense Tracking and Payment

Consumers may store expenses and receipts in the system to pay out of the HSA now, pay later, or simply store for their records

Convenient Self-Service Tools important for HSA success

Presenter

Presentation Notes

_______________________________________________________________________________ _______________________________________________________________________________ _______________________________________________________________________________ _______________________________________________________________________________

HSA Mobile App Mandatory for Millennials

Apps allow your employees to:• Check available balances• View account activity• Request distributions• Make contributions• Pay medical bills from your

smartphone• Upload receipts and EOB’s using

device’s camera• Access year-end tax data

Presenter

Presentation Notes

_______________________________________________________________________________ _______________________________________________________________________________ _______________________________________________________________________________ _______________________________________________________________________________

Related Documents