HOW TO EXPORT GUIDE: VIETNAM All rights reserved to The Blue Ocean Vietnam Business Consulting and Ventures - Prepared for Brazilian Embassy November 2021

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

HOW TO EXPORT GUIDE:

VIETNAM

All rights reserved to The Blue Ocean Vietnam Business Consulting and Ventures -

Prepared for Brazilian Embassy

November 2021

HOW TO EXPORT GUIDE: VIETNAM

1 | Page

TABLE OF CONTENTS

TABLE OF CONTENTS ....................................................................................................... 1

LIST OF TABLES ................................................................................................................. 4

LIST OF FIGURES ............................................................................................................... 6

LIST OF CHARTS ................................................................................................................ 8

ABBREVIATIONS ................................................................................................................ 9

INTRODUCTION ................................................................................................................ 10

WHY VIETNAM? ............................................................................................................... 11

PART 1: VIETNAM OVERVIEW...................................................................................... 14

1.1. Country Profile .............................................................................................................. 14

1.1.1. Geography of Vietnam .............................................................................................. 14

1.1.2. The government organization .................................................................................... 19

1.1.3. The Vietnamese people ............................................................................................. 22

1.1.4. Transformation of Vietnam ....................................................................................... 25

1.1.5. The opening of Vietnam ............................................................................................ 27

1.2. Vietnamese Foreign Policy ........................................................................................... 29

1.2.1. Vietnam's External Relations ................................................................................... 29

1.2.2. General aspects of Vietnam's international policy...................................................... 32

1.3. The Vietnamese Economy ............................................................................................. 37

1.3.1. Main Macroeconomic Indicators ............................................................................... 38

1.3.2. Vietnam Social - Economic Development Strategy ................................................... 45

1.3.3. Vietnam Trade .......................................................................................................... 47

1.3.4. Commercial Disputes ................................................................................................ 54

1.3.5. Currency and Finance ............................................................................................... 56

1.4. Understanding the Vietnamese Consumer ................................................................... 61

1.4.1. A growing middle class ............................................................................................. 62

1.4.2. Consumer segments .................................................................................................. 63

1.4.3. Consumer standard.................................................................................................... 66

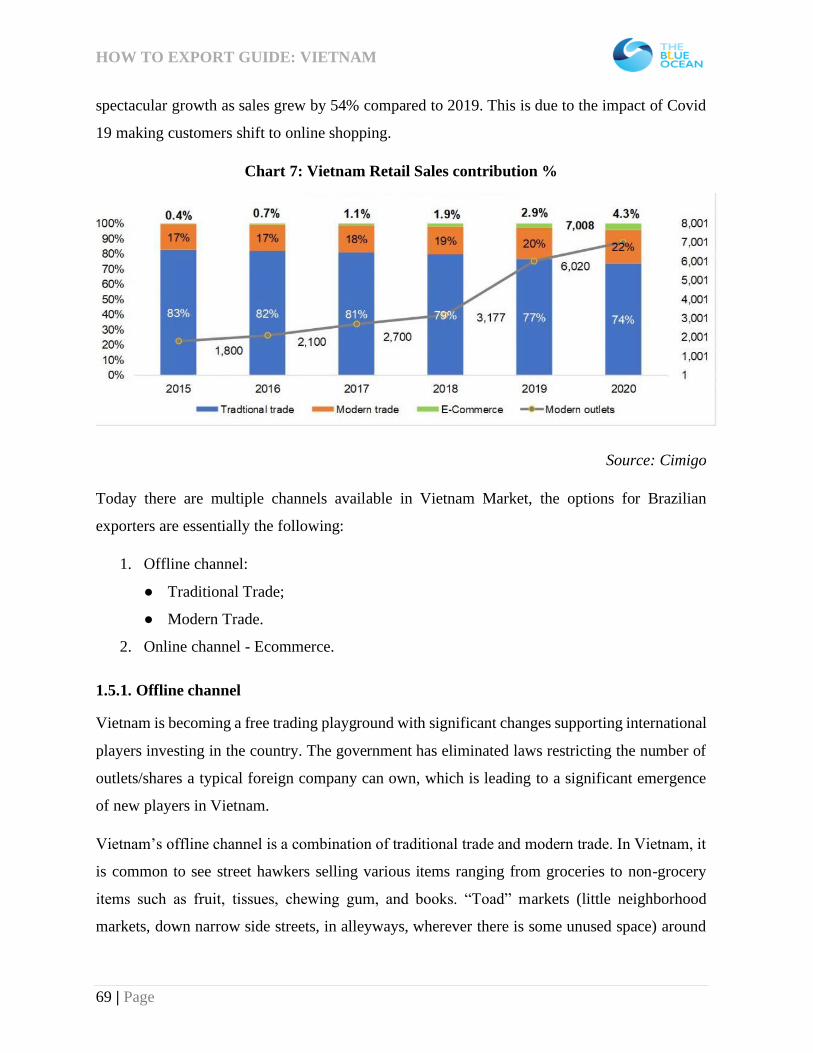

1.5. Vietnam Channels landscape ........................................................................................ 68

PART 2: VIETNAM AND BRAZIL ................................................................................... 81

HOW TO EXPORT GUIDE: VIETNAM

2 | Page

2.1. Relationship between Brazil and Vietnam ................................................................... 81

2.1.1. Relationship between Brazil and Asian countries ...................................................... 81

2.1.2. Bilateral Diplomatic Relationships between Vietnam and Brazil ............................... 83

2.1.3. Bilateral Trade .......................................................................................................... 85

2.1.3. Bilateral Investments................................................................................................. 90

2.1.4. Institutions for export promotion ............................................................................... 92

2.2. Opportunities and Challenges in Vietnam ................................................................... 93

2.2.1. Opportunities ............................................................................................................ 94

2.2.2. Challenges .............................................................................................................. 103

PART 3: HOW TO EXPORT TO VIETNAM ................................................................. 106

3.1. Common Route-to-market of Brazilian exporters in Vietnam .................................. 106

3.2. How to export to Vietnam ........................................................................................... 109

3.2.1. Exporting/Selling directly to customers in Vietnam (Direct commerce)................... 109

3.2.2. Exporting through a Vietnamese intermediary ......................................................... 111

3.2.3. Exporting through a Brazilian commercial presence in Vietnam .............................. 112

3.3. Payment terms ............................................................................................................. 129

3.4. Selling to the Vietnamese Consumer .......................................................................... 132

3.4.1. Distribution strategies ............................................................................................. 132

3.4.2. Highlighted challenges in the Vietnam market ........................................................ 136

3.4.3. Transport options .................................................................................................... 138

3.4.4. Advertising ............................................................................................................. 147

3.5. Dealing with Government ........................................................................................... 154

3.5.1. Customs .................................................................................................................. 154

3.5.2. Import Policies and Regulation ............................................................................... 166

3.5.3 Intellectual Property ................................................................................................. 168

PART 4: HOW TO INVEST IN VIETNAM .................................................................... 176

4.1. Investment Environment ............................................................................................. 176

4.1.1. Highlight project in 2020: ....................................................................................... 182

4.1.2. Some major projects in the 6 months of 2021: ......................................................... 183

4.1.3. The Government orientation in the next five years (2021 – 2025):........................... 184

4.1.4. Case study............................................................................................................... 185

4.2. Investment sectors ....................................................................................................... 197

HOW TO EXPORT GUIDE: VIETNAM

3 | Page

4.2.1. The manufacturing and processing sectors .............................................................. 197

4.2.2. The electricity production and distribution sector: ................................................... 198

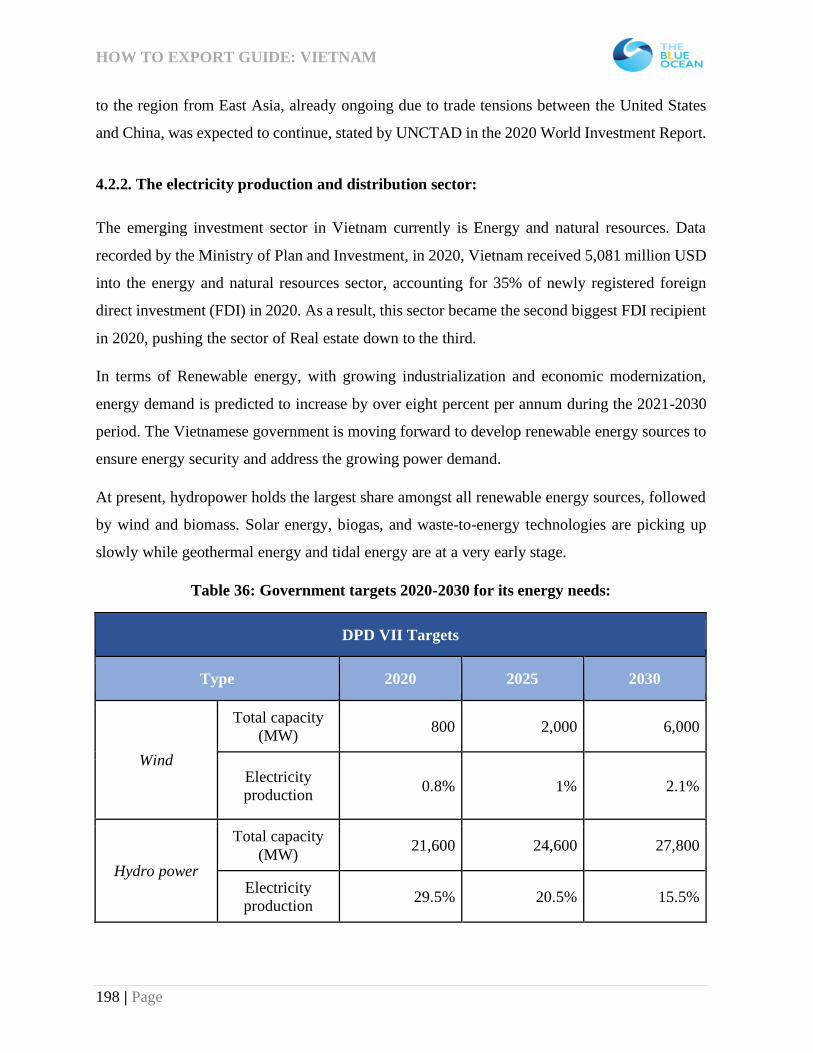

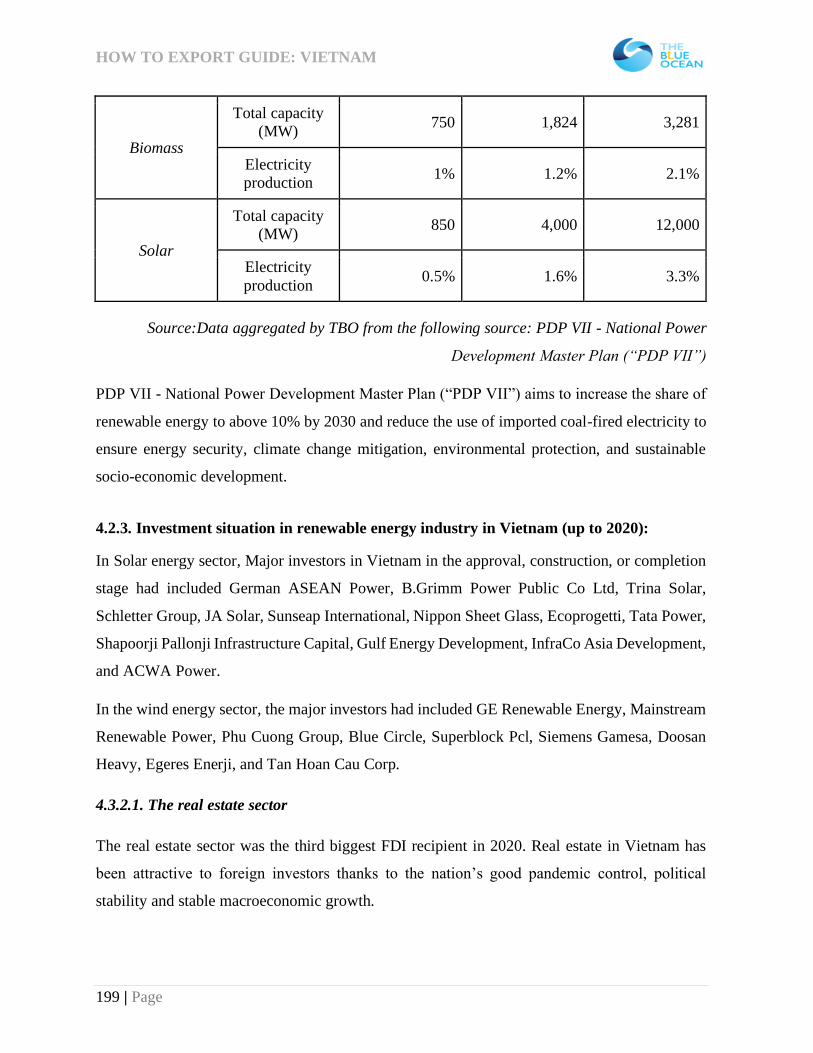

4.2.3. Investment situation in renewable energy industry in Vietnam (up to 2020): ........... 199

4.3. Geographical Considerations ...................................................................................... 202

4.3.1. FDI situation across Vietnam: ................................................................................. 204

4.3.2. Other types of Economic zone in Vietnam: ............................................................. 205

4.4. State agencies related to Investment ........................................................................... 206

4.5. Main tax policies .......................................................................................................... 212

4.5.1. License tax (license fee) .......................................................................................... 212

4.5.2. Value Added Tax: ................................................................................................... 214

4.6. Human resources in Vietnam...................................................................................... 223

4.6.1. Human Resource Policies:....................................................................................... 227

4.6.2. Recruitment channels .............................................................................................. 231

PART 5. DOING BUSINESS IN VIETNAM .................................................................... 234

5.1. Common business customs in Vietnam ...................................................................... 234

5.2. A Typical Vietnamese Business Meeting .................................................................... 238

5.3. Trading techniques ...................................................................................................... 242

APPENDIX 2: .................................................................................................................... 247

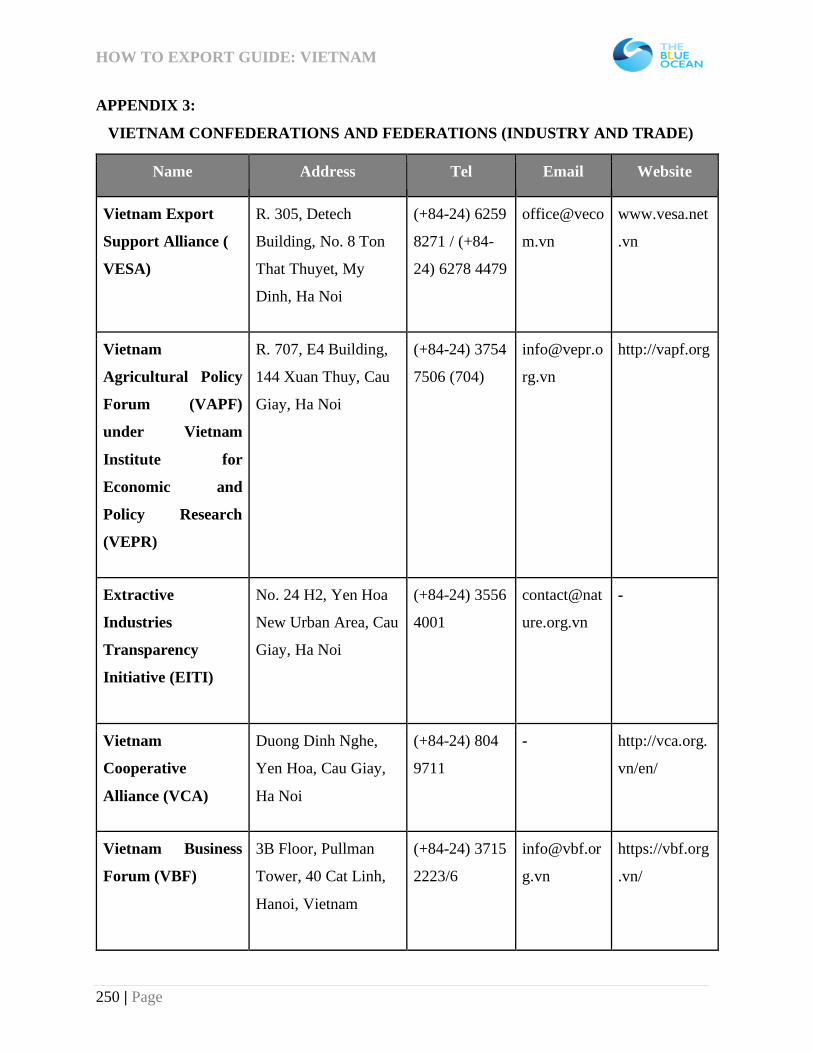

APPENDIX 3: .................................................................................................................... 250

APPENDIX 4: .................................................................................................................... 252

APPENDIX 5: .................................................................................................................... 255

APPENDIX 6: .................................................................................................................... 259

HOW TO EXPORT GUIDE: VIETNAM

4 | Page

LIST OF TABLES

Table 1: Vietnam Overview ................................................................................................... 15

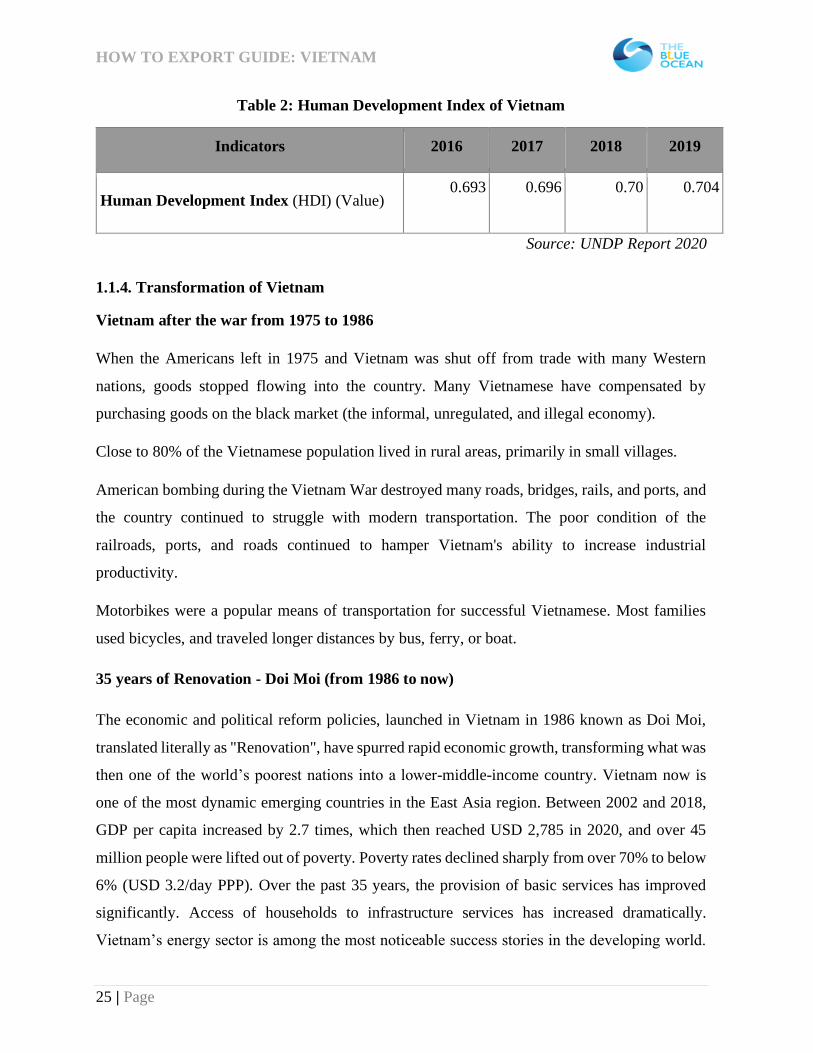

Table 2: Human Development Index of Vietnam .................................................................... 25

Table 3: Summary of Vietnam's FTAs as of May 2021........................................................... 33

Table 4: Number of free trade agreements in effect, which Vietnam has joined, by type ......... 37

Table 5: Main indicators......................................................................................................... 39

Table 6: Vietnamese inflation Rate by years(%) ..................................................................... 40

Table 7: Vietnamese Interest rate by years (%) ....................................................................... 40

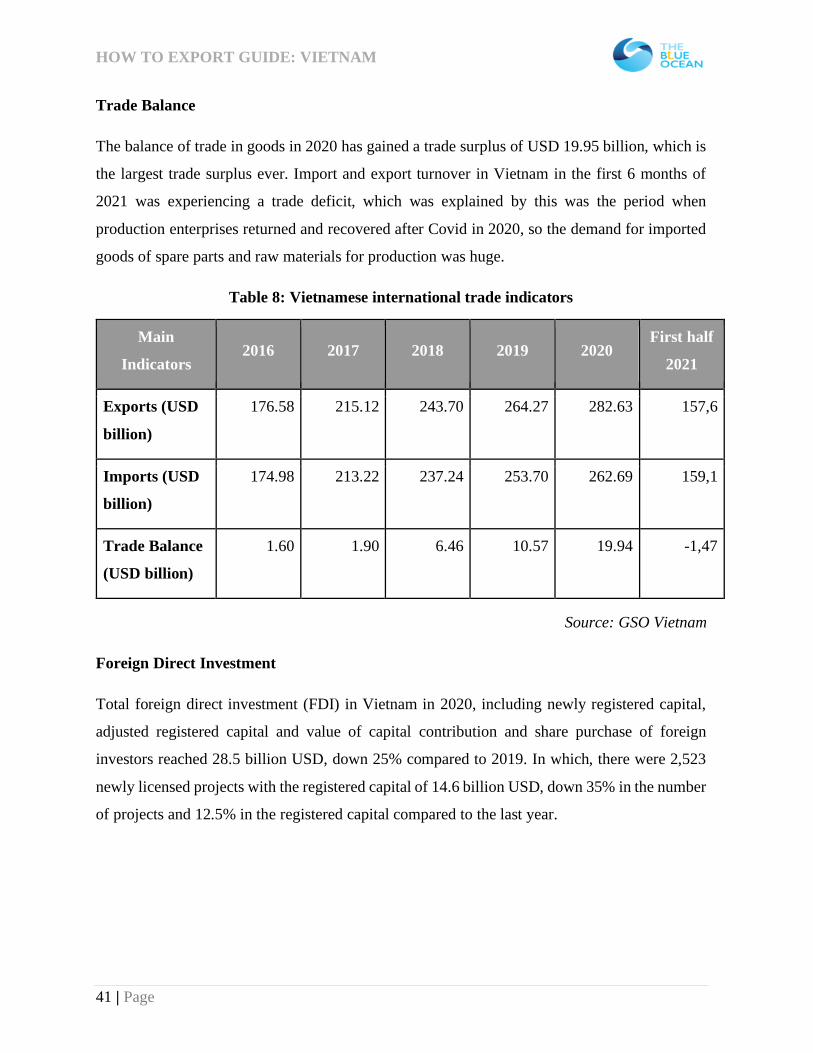

Table 8: Vietnamese international trade indicators ................................................................. 41

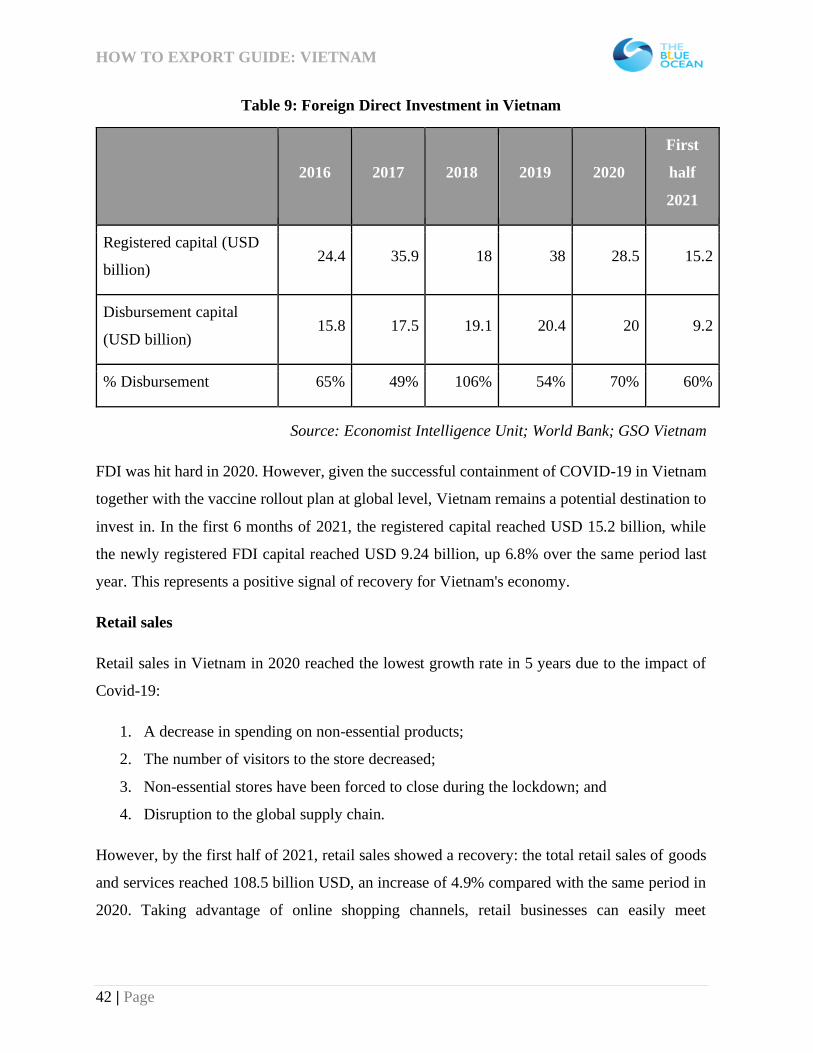

Table 9: Foreign Direct Investment in Vietnam ...................................................................... 42

Table 10: Retail industry in Vietnam (annual) ........................................................................ 44

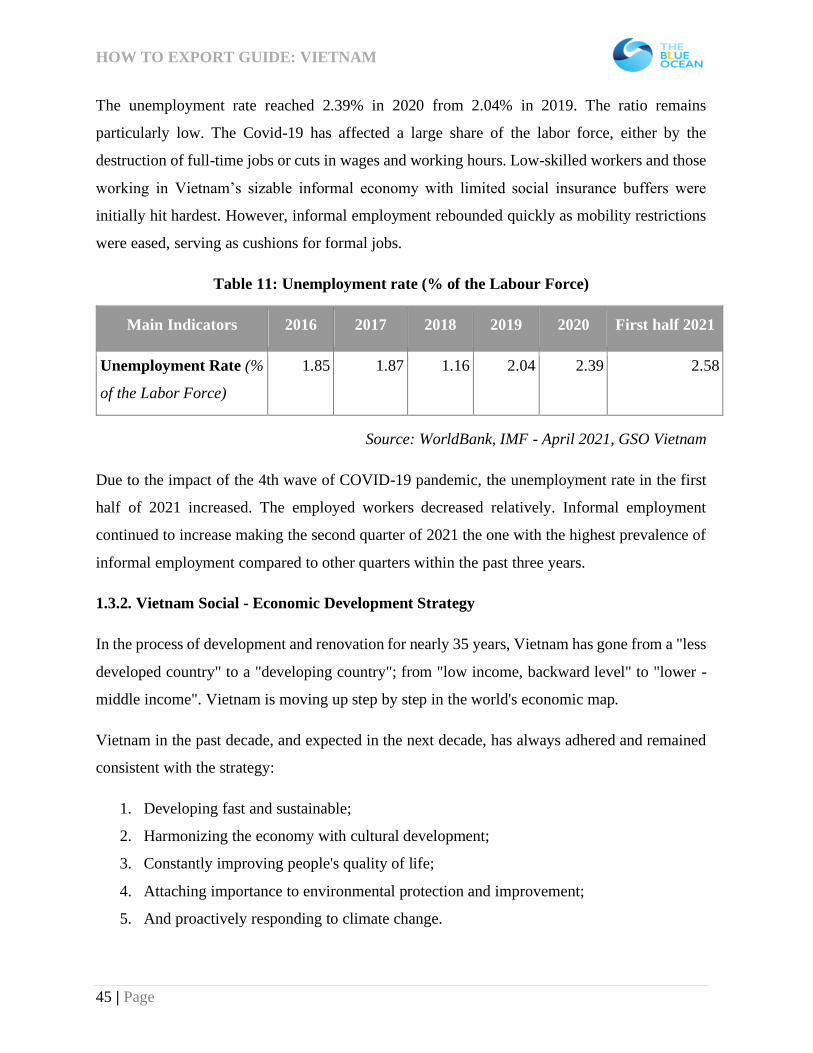

Table 11: Unemployment rate (% of the Labour Force) .......................................................... 45

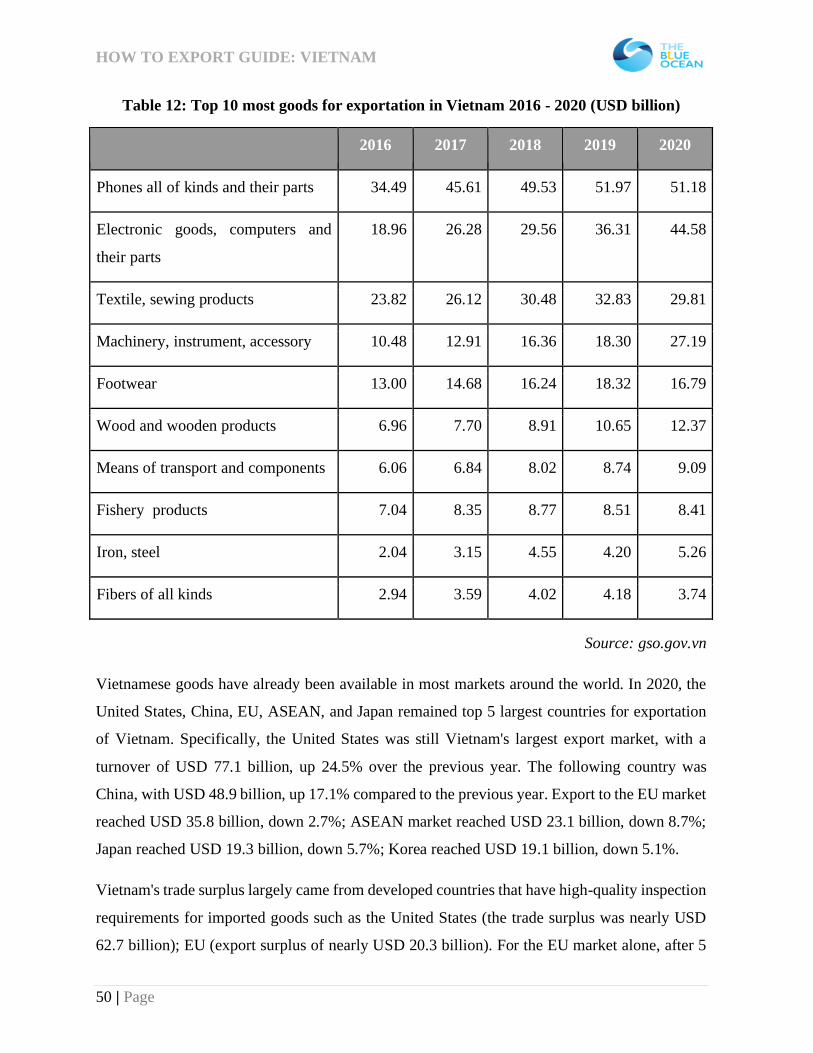

Table 12: Top 10 most goods for exportation in Vietnam 2016 - 2020 (USD billion) ............. 50

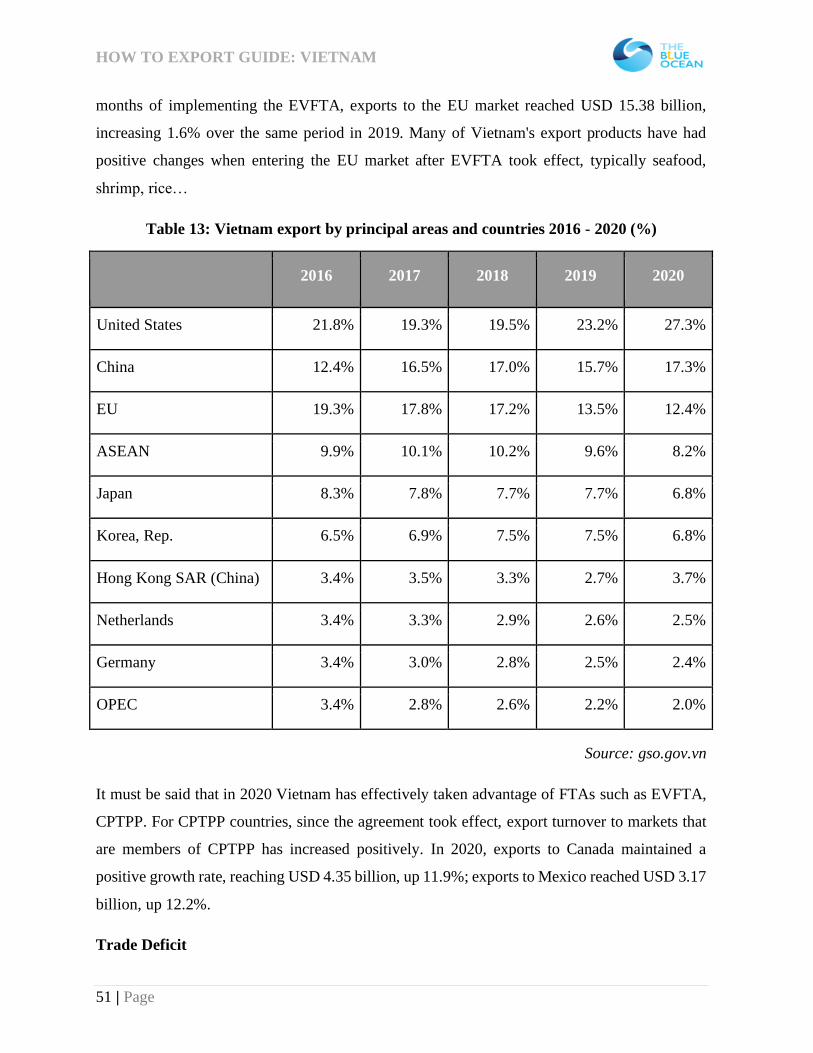

Table 13: Vietnam export by principal areas and countries 2016 - 2020 (%) ........................... 51

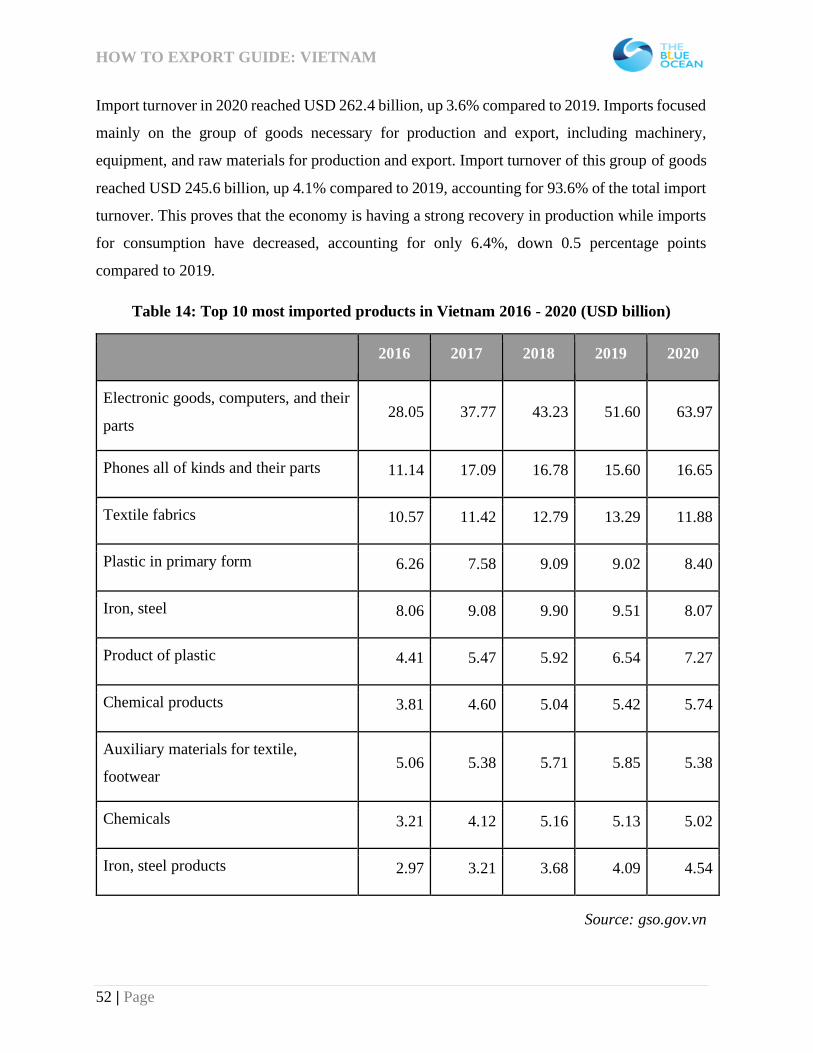

Table 14: Top 10 most imported products in Vietnam 2016 - 2020 (USD billion) .................. 52

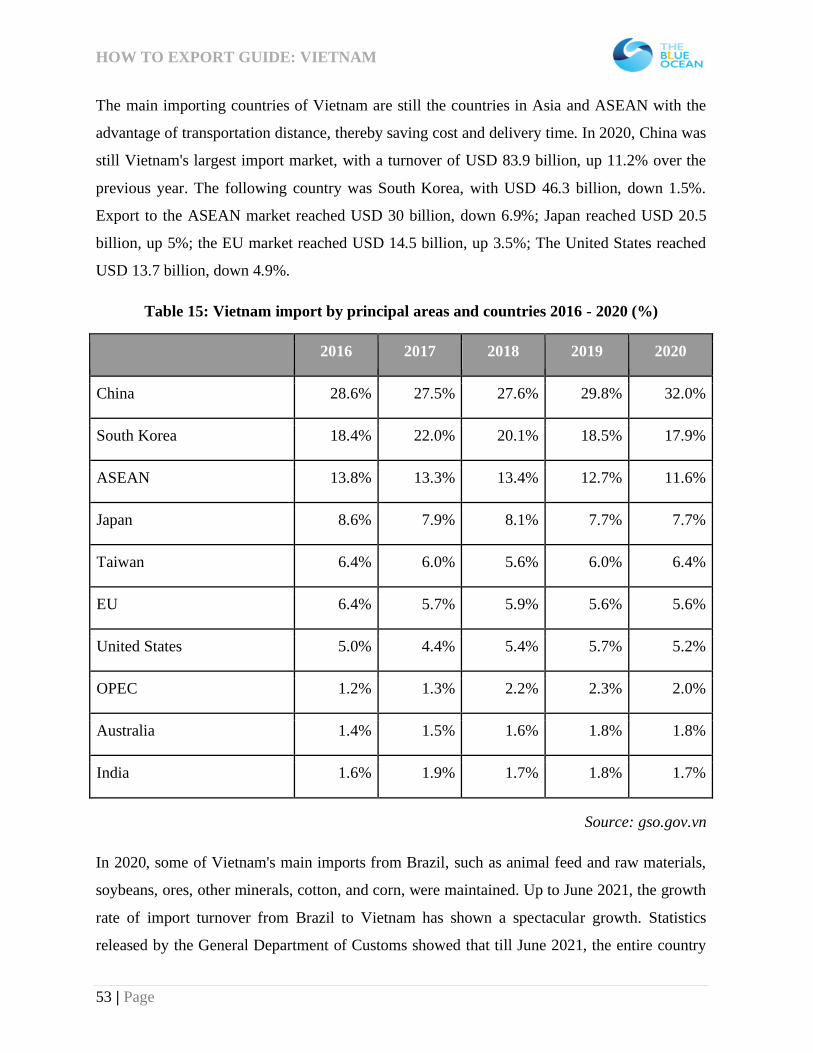

Table 15: Vietnam import by principal areas and countries 2016 - 2020 (%) .......................... 53

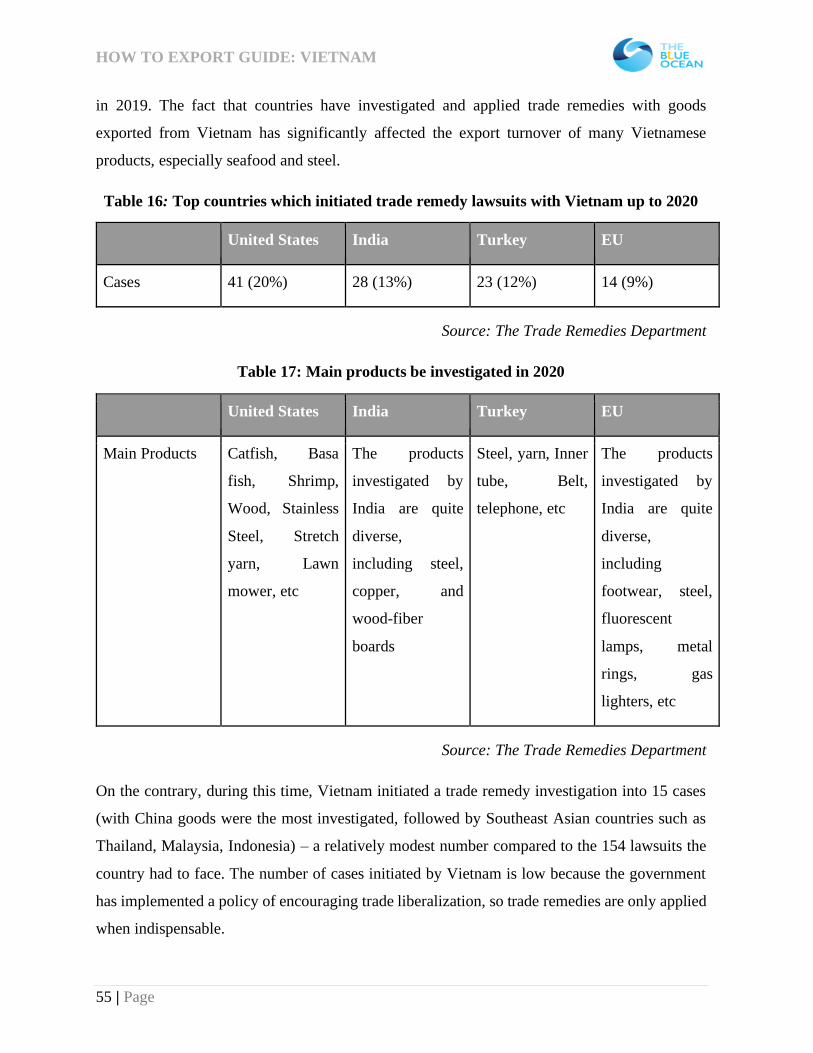

Table 16: Top countries which initiated trade remedy lawsuits with Vietnam up to 2020 ....... 55

Table 17: Main products be investigated in 2020 .................................................................... 55

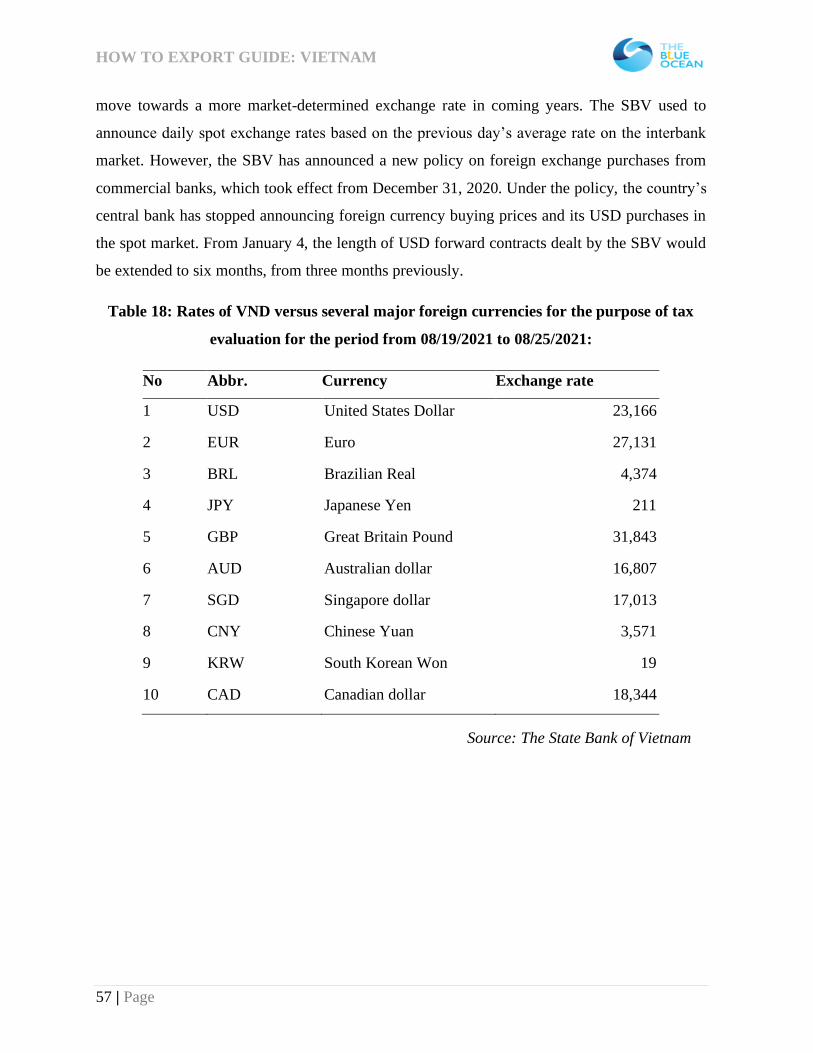

Table 18: Rates of VND versus several major foreign currencies for the purpose of tax evaluation

for the period from 08/19/2021 to 08/25/2021: ....................................................................... 57

Table 19: Consumer group impacts ........................................................................................ 66

Table 20: Bilateral conventions signed between Vietnam and Brazil ...................................... 83

Table 21: Institutions for export promotion ............................................................................ 92

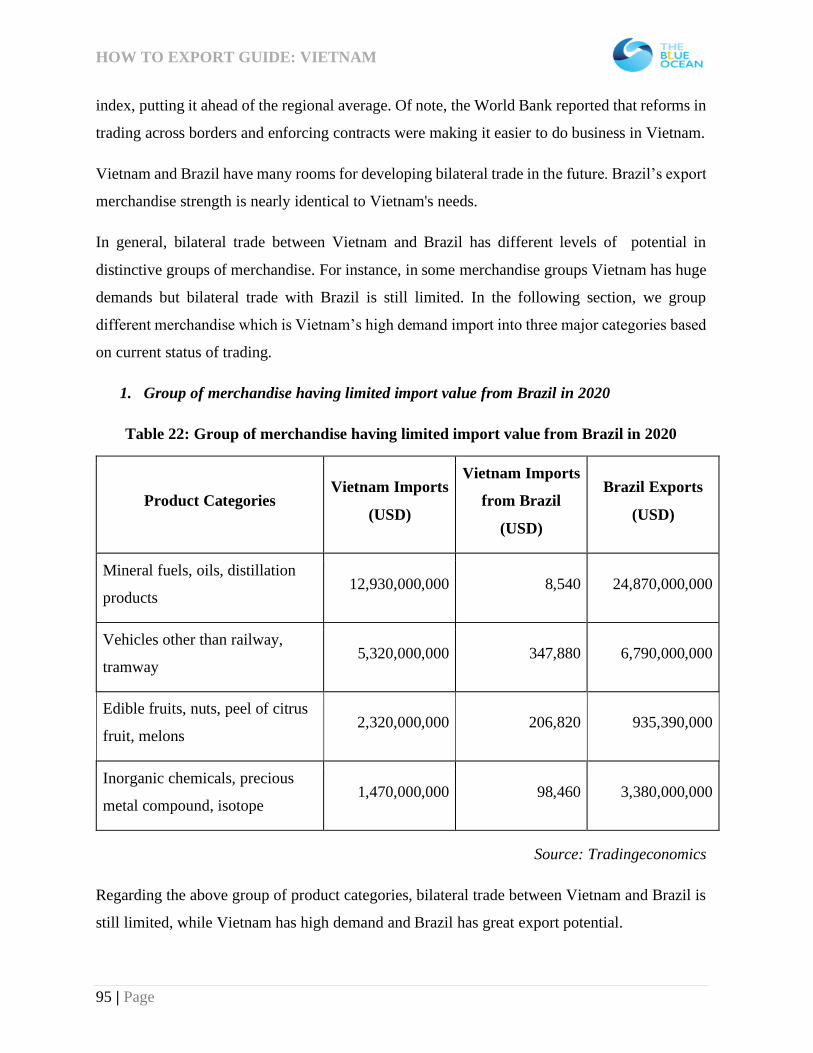

Table 22: Group of merchandise having limited import value from Brazil in 2020 ................. 95

Table 23: Group of merchandise having potential import value from Brazil in 2020 ............... 97

Table 24: Group of merchandise having high import value from Brazil in 2020 ..................... 99

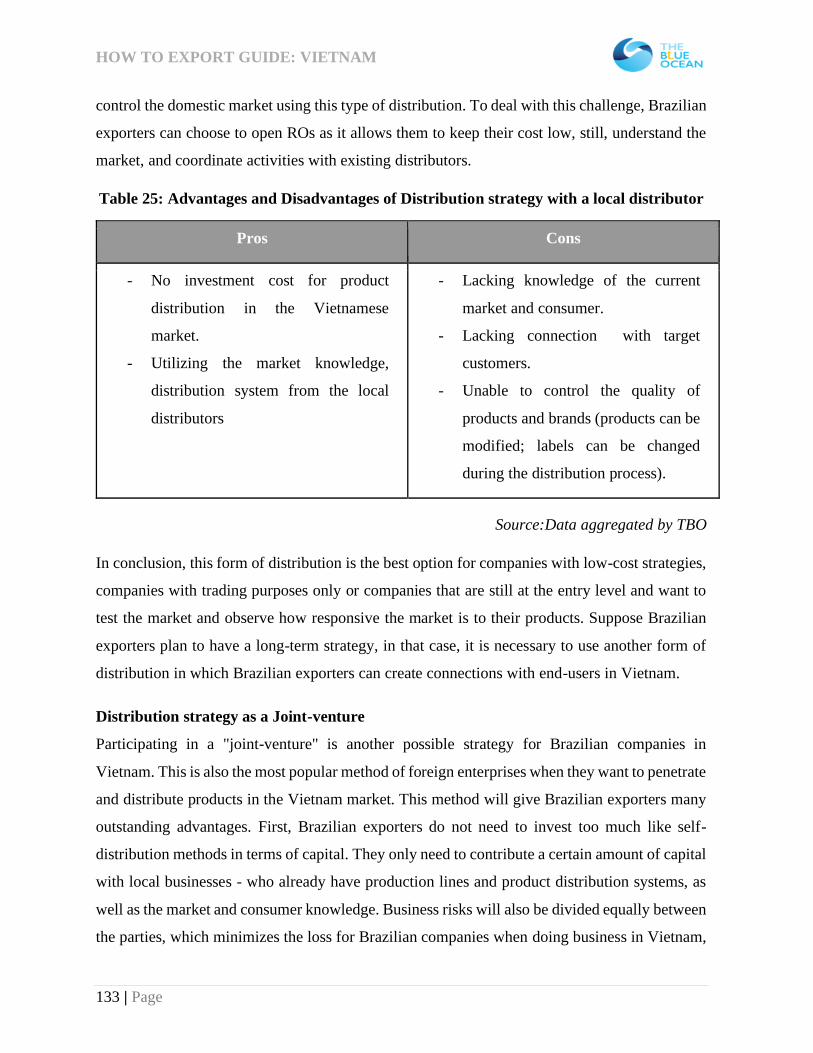

Table 25: Advantages and Disadvantages of Distribution strategy with a local distributor .... 133

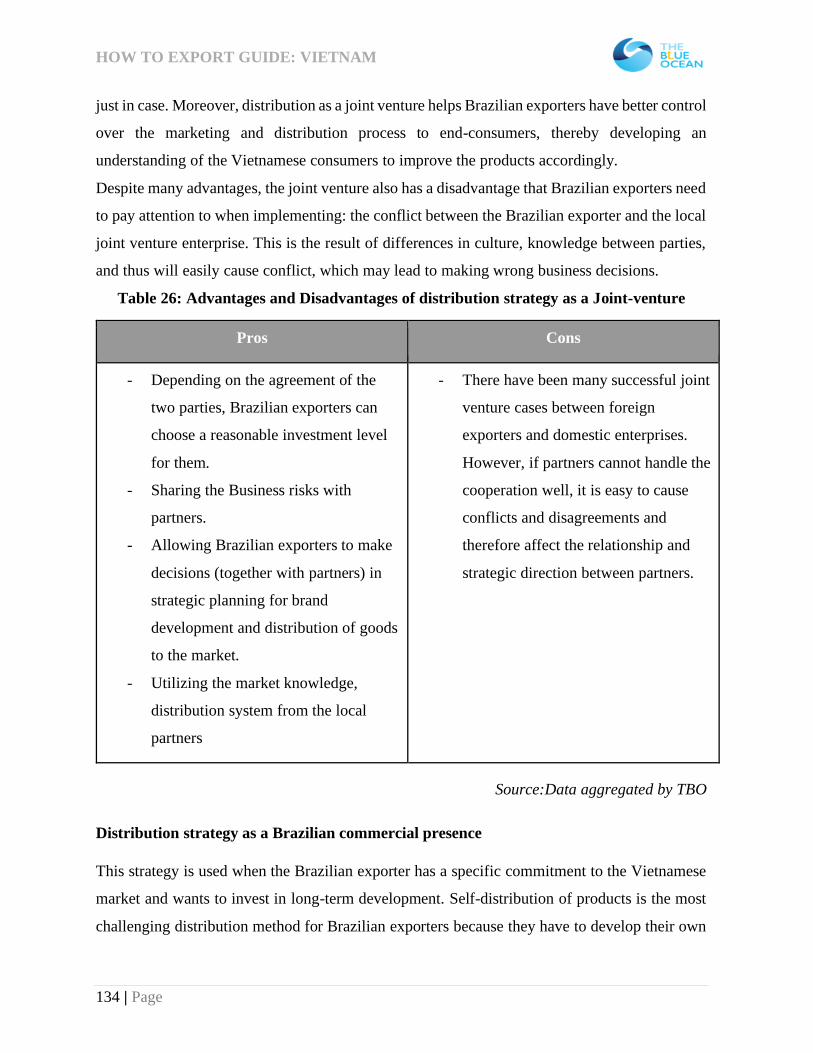

Table 26: Advantages and Disadvantages of distribution strategy as a Joint-venture ............. 134

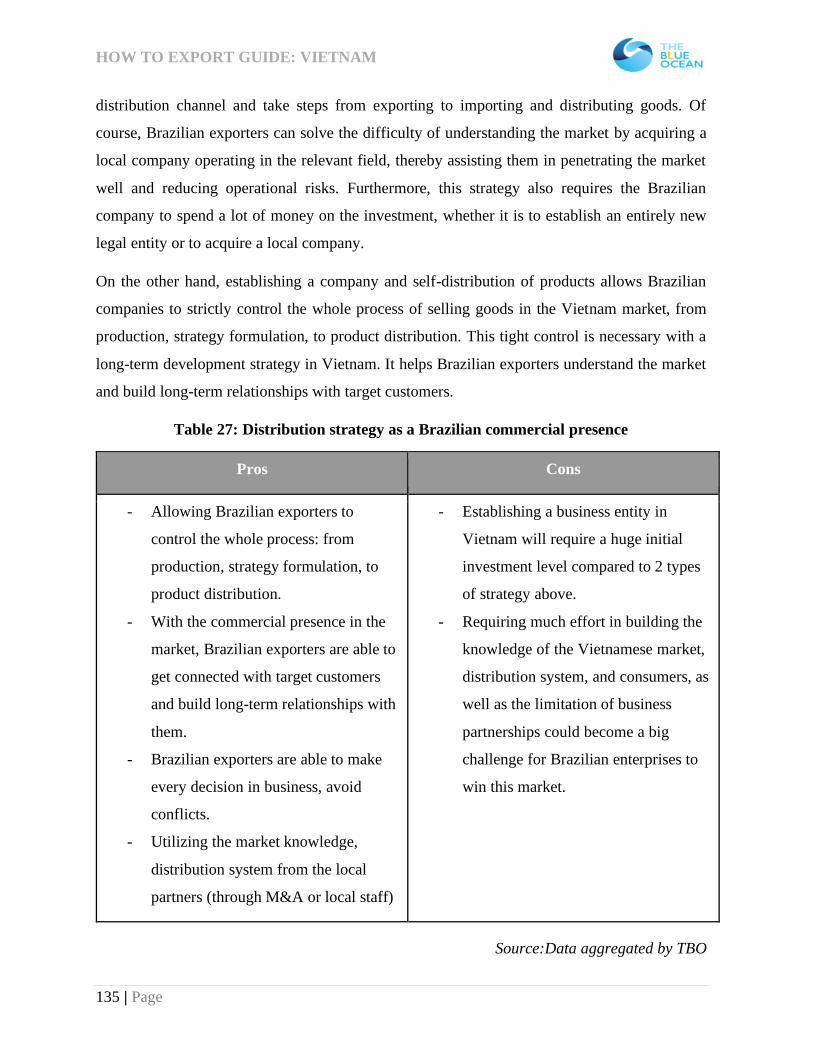

Table 27: Distribution strategy as a Brazilian commercial presence ...................................... 135

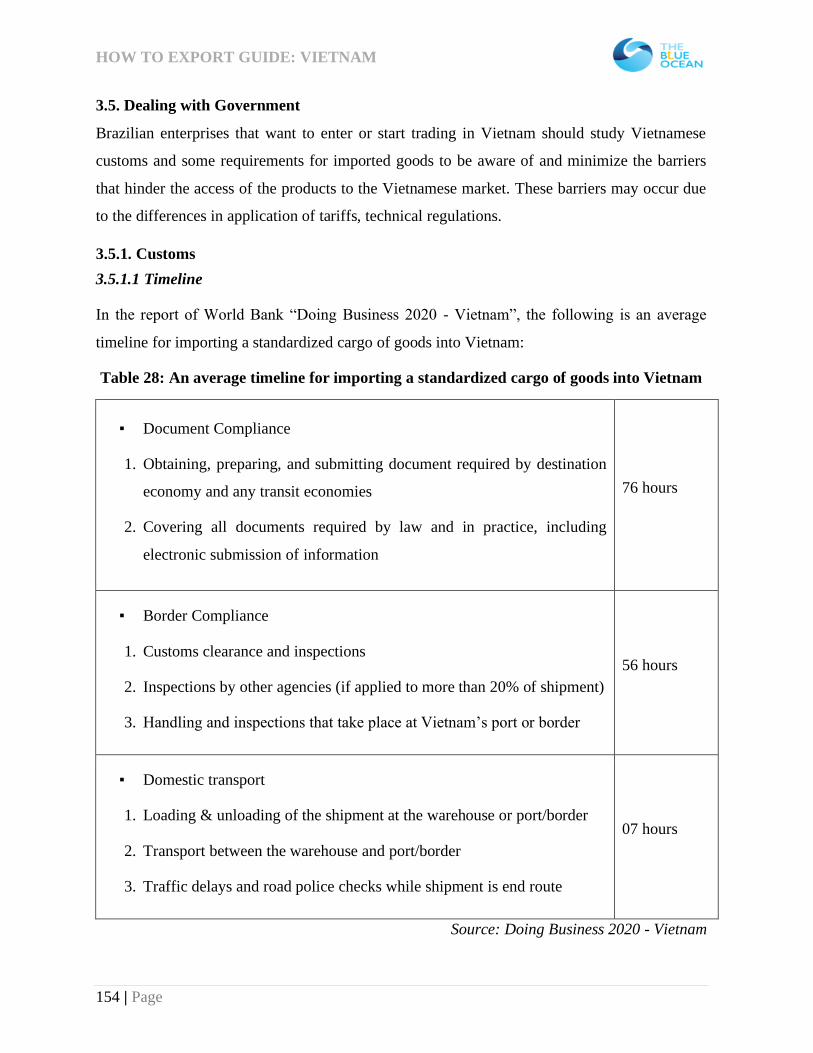

Table 28: An average timeline for importing a standardized cargo of goods into Vietnam .... 154

HOW TO EXPORT GUIDE: VIETNAM

5 | Page

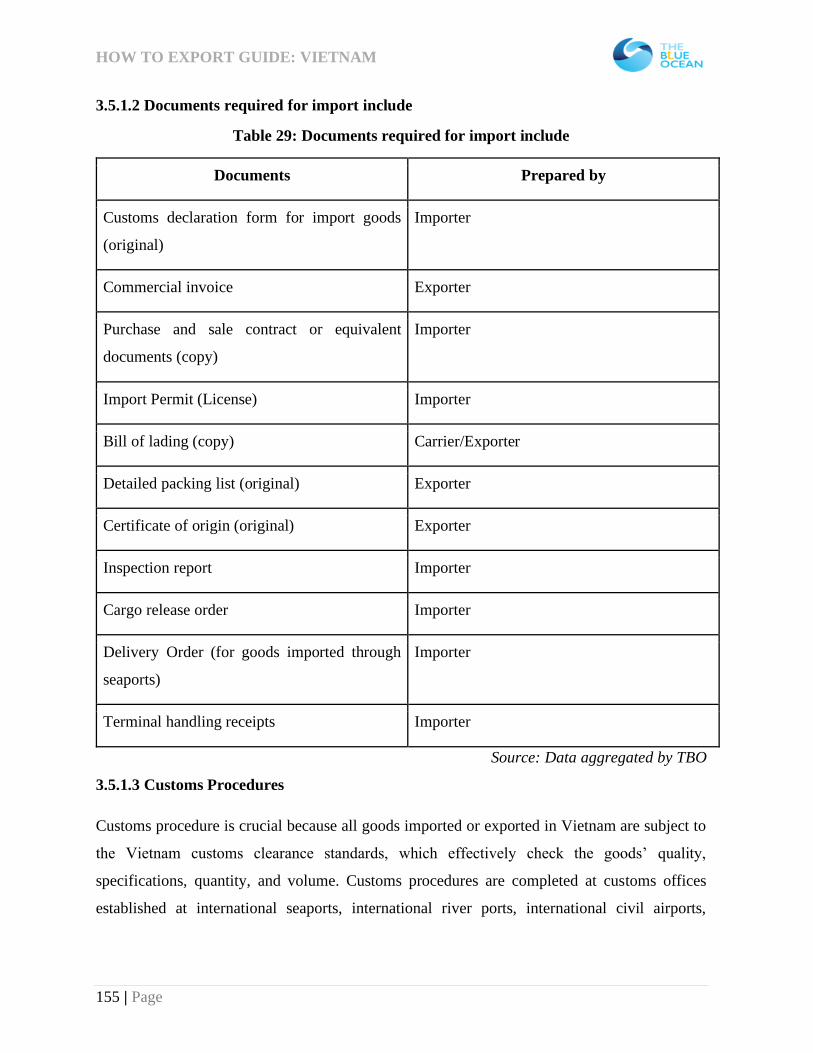

Table 29: Documents required for import include ................................................................. 155

Table 30: Common tariffs of imported goods in Vietnam ..................................................... 163

Table 31: Taxes are eligible to Group of merchandise having potential and high import value

from Brazil ........................................................................................................................... 164

Table 32: Group of merchandise having high import value from Brazil ................................ 165

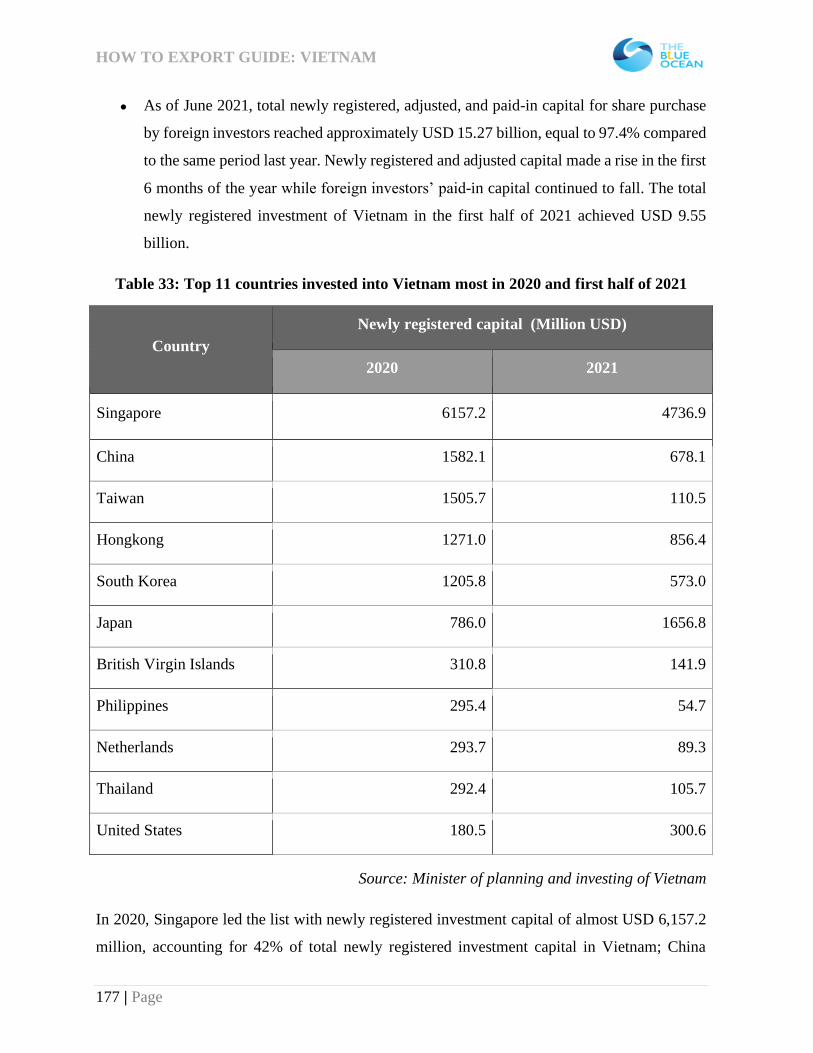

Table 33: Top 11 countries invested into Vietnam most in 2020 and first half of 2021 ......... 177

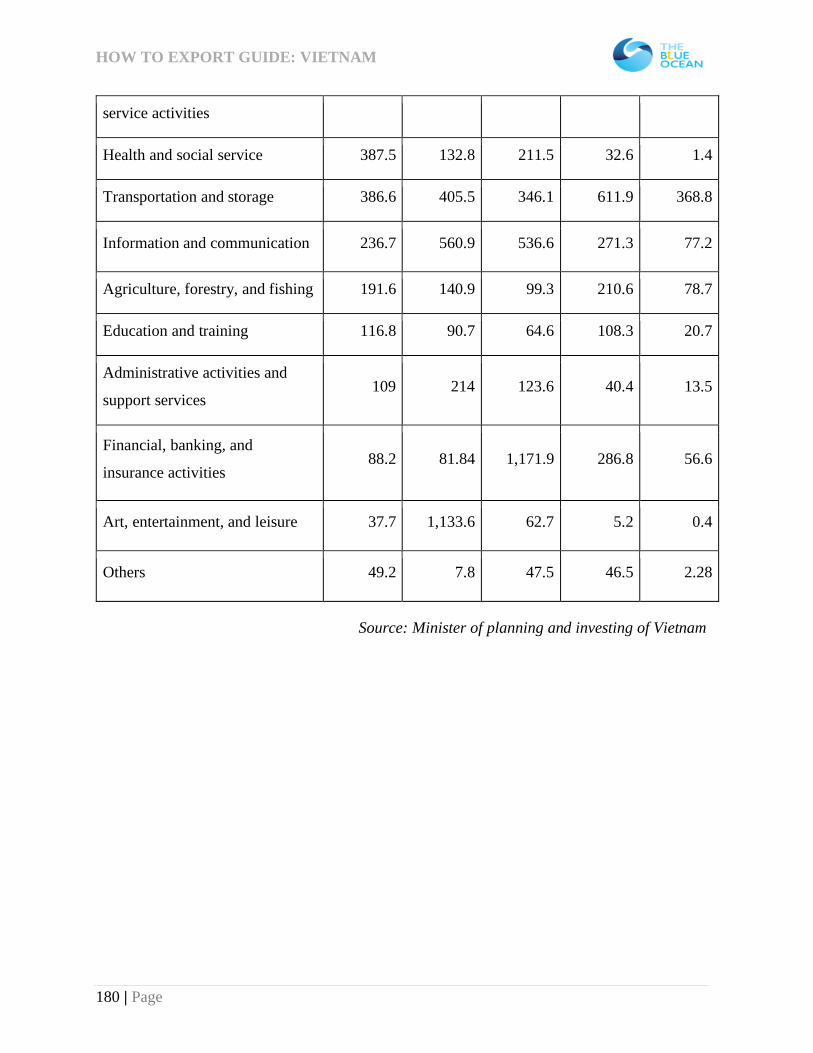

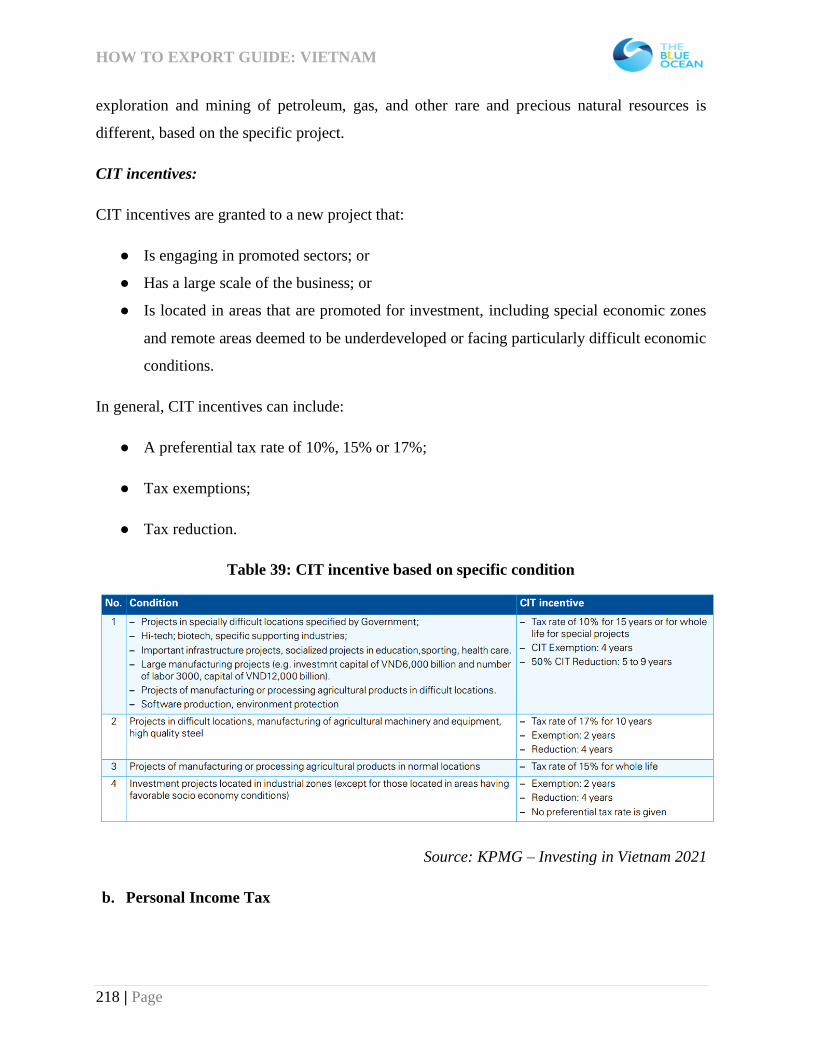

Table 34: Total foreign direct investment inflow by sectors in Vietnam from 2017 - 2020 & First

half of 2021 (Million USD) .................................................................................................. 179

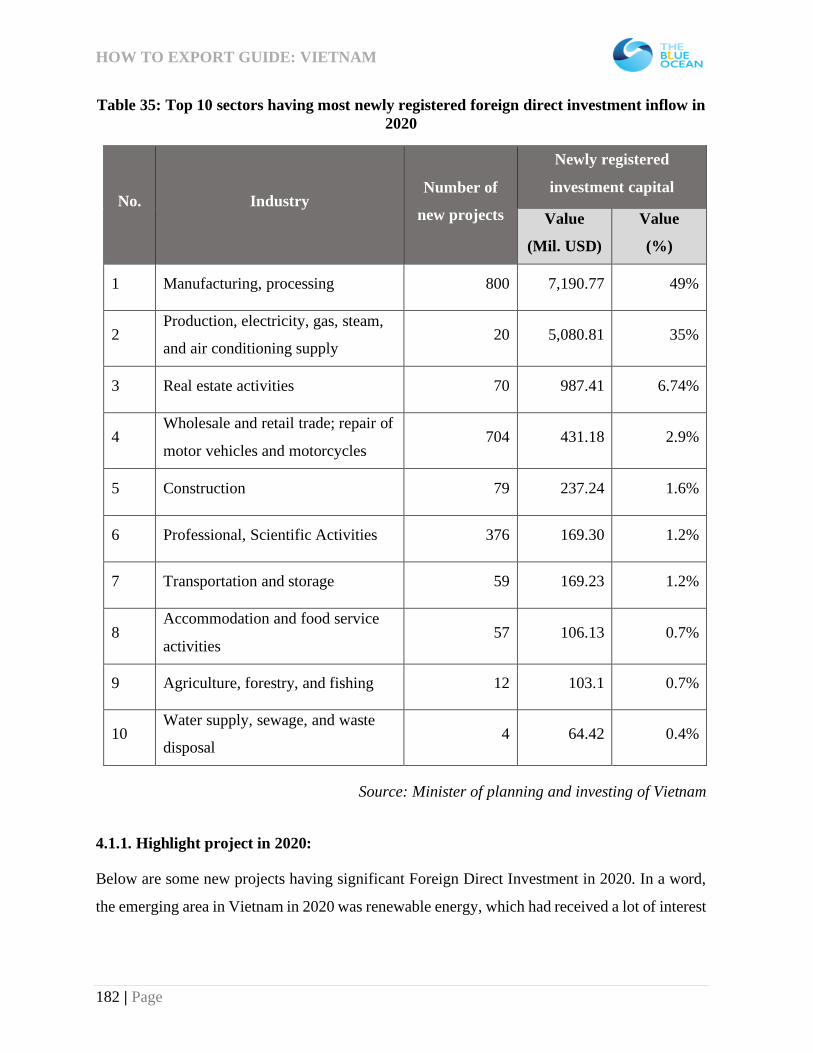

Table 35: Top 10 sectors having most newly registered foreign direct investment inflow in 2020

............................................................................................................................................ 182

Table 36: Government targets 2020-2030 for its energy needs:............................................. 198

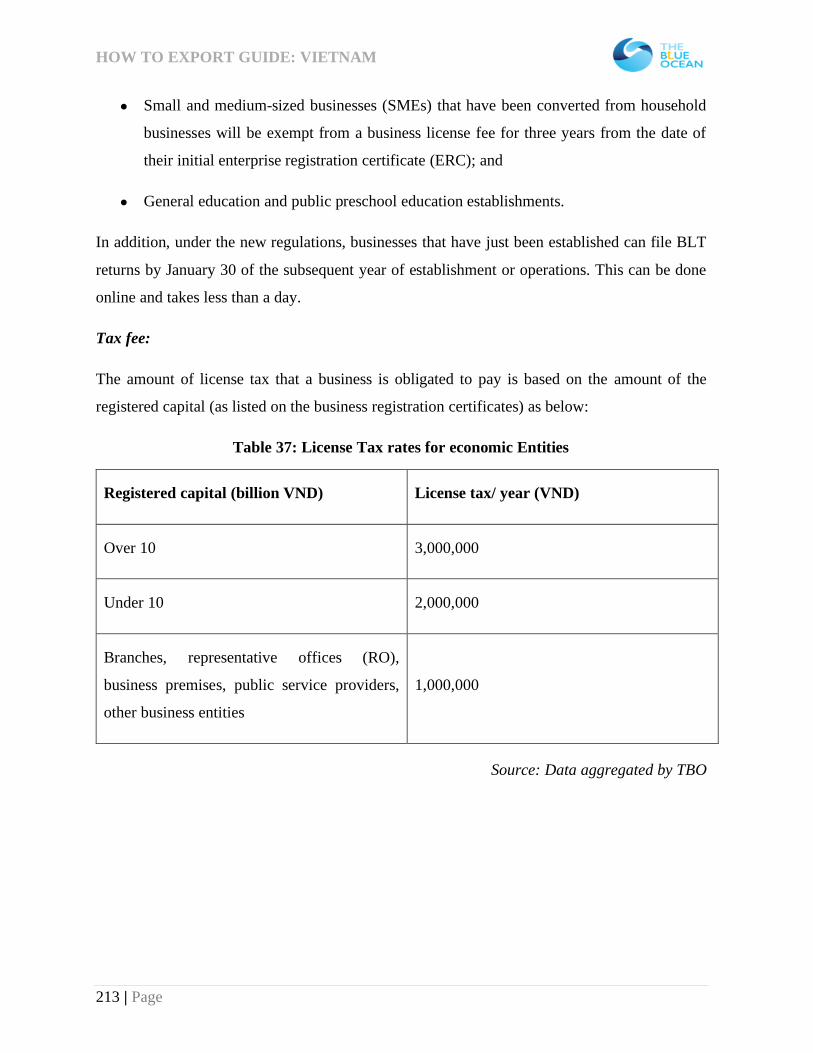

Table 37: License Tax rates for economic Entities ................................................................ 213

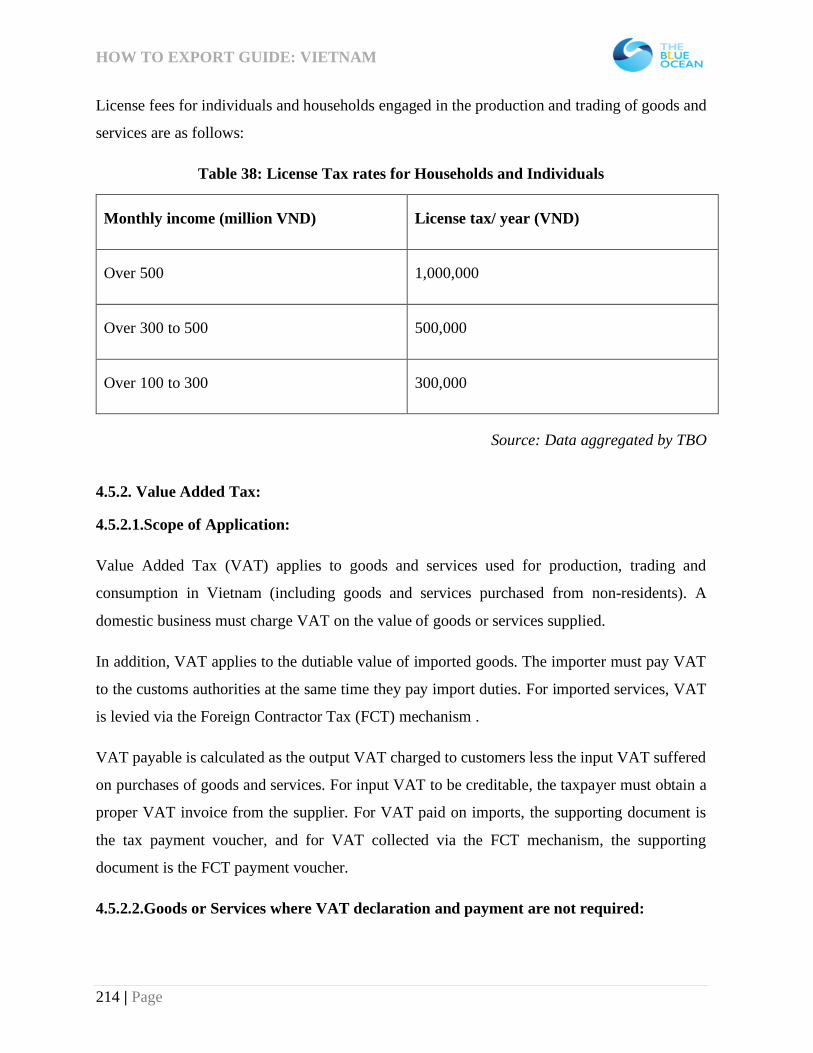

Table 38: License Tax rates for Households and Individuals ................................................ 214

Table 39: CIT incentive based on specific condition ............................................................. 218

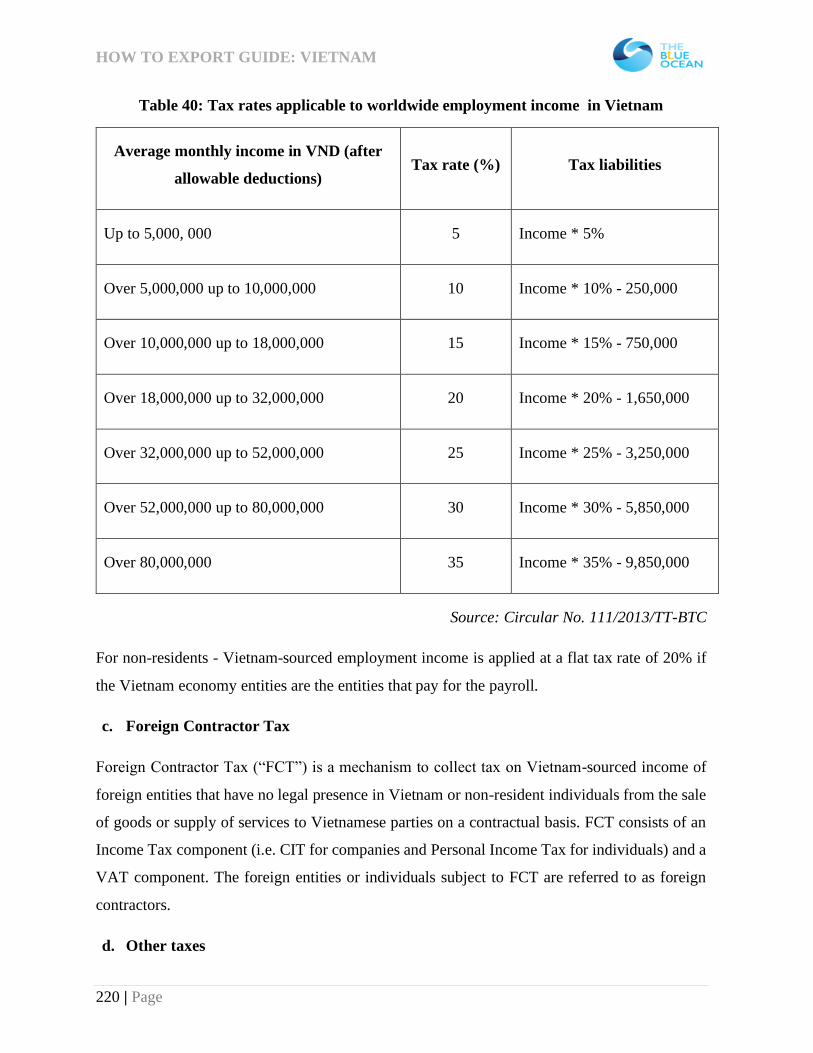

Table 40: Tax rates applicable to worldwide employment income in Vietnam ..................... 220

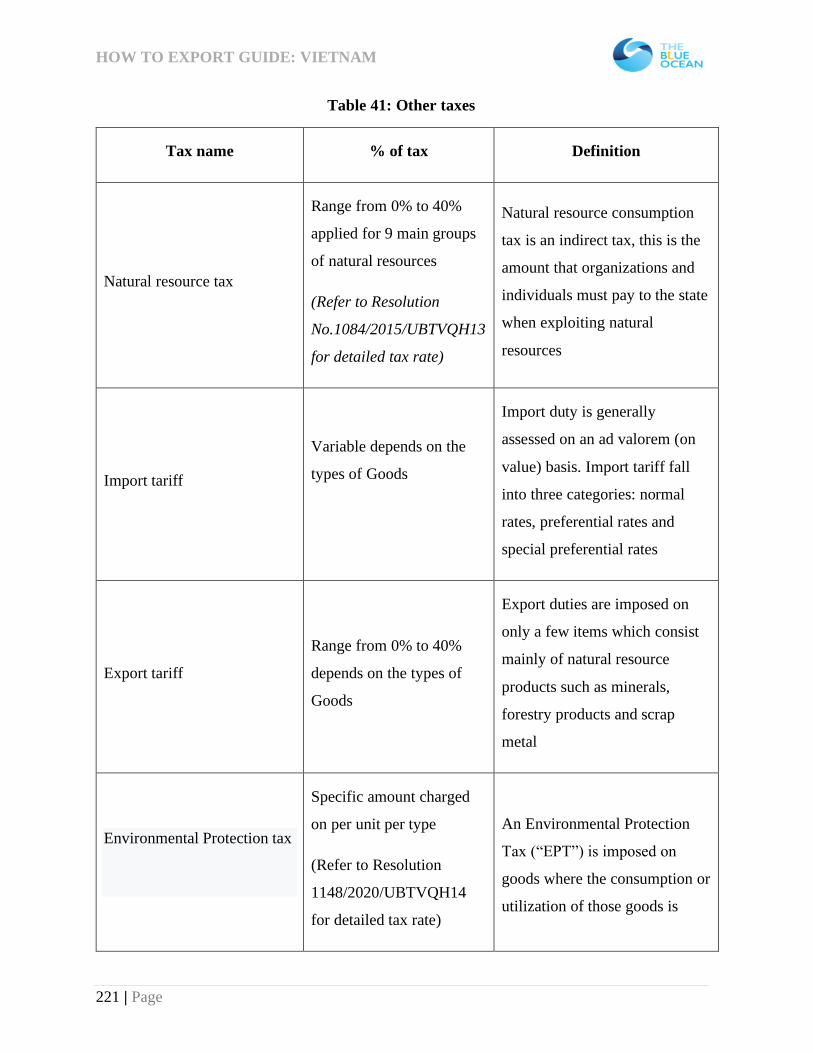

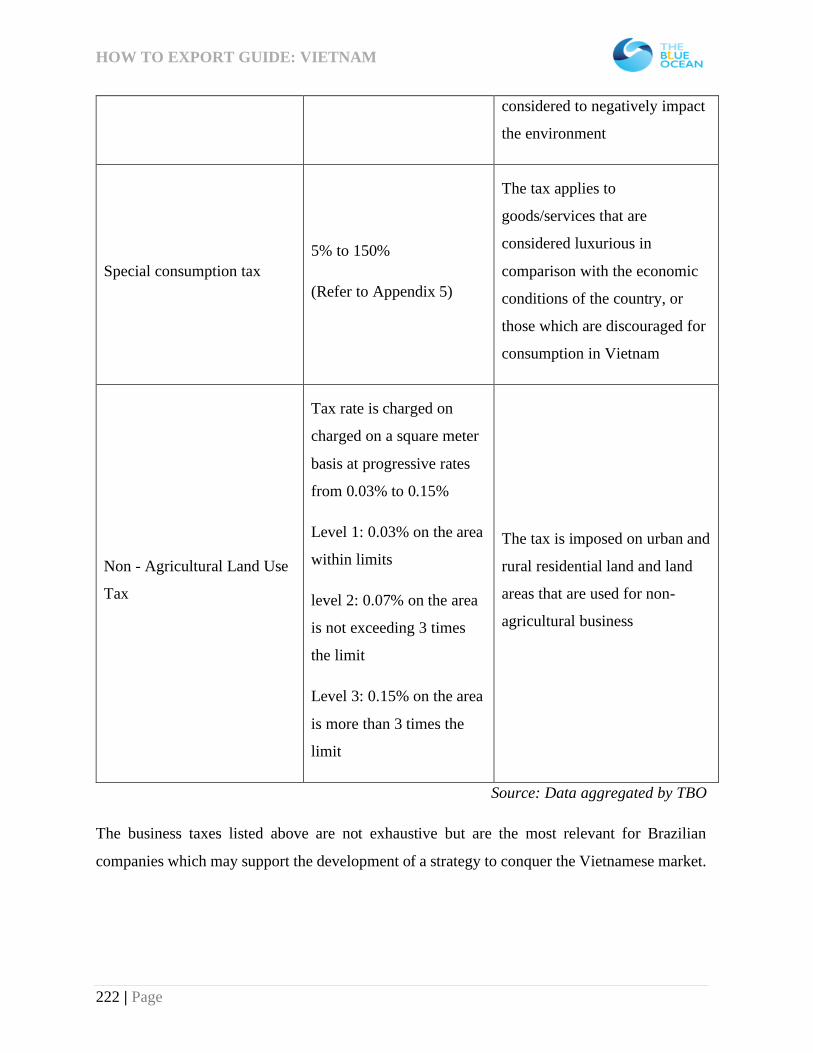

Table 41: Other taxes ........................................................................................................... 221

Table 42: Overtime rates in Vietnam .................................................................................... 228

Table 43: Holiday Calendar in Vietnam ............................................................................... 238

HOW TO EXPORT GUIDE: VIETNAM

6 | Page

LIST OF FIGURES

Figure 1: 8 geographical regions of Vietnam .......................................................................... 17

Figure 2: Vietnamese political system .................................................................................... 21

Figure 3: Timeline of Vietnam’s Major Economic Reforms Since 1986 ................................. 28

Figure 4: Vietnam Exports and Imports of Goods Overview 2020 .......................................... 48

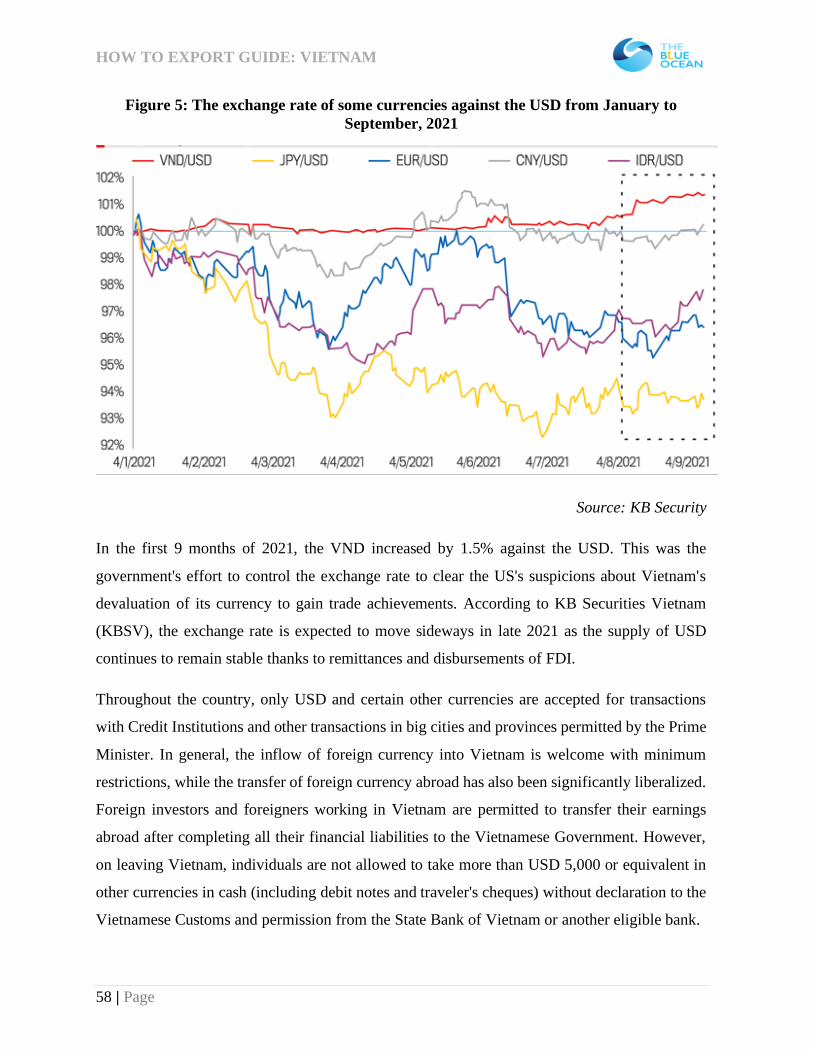

Figure 5: The exchange rate of some currencies against the USD from January to September,

2021 ....................................................................................................................................... 58

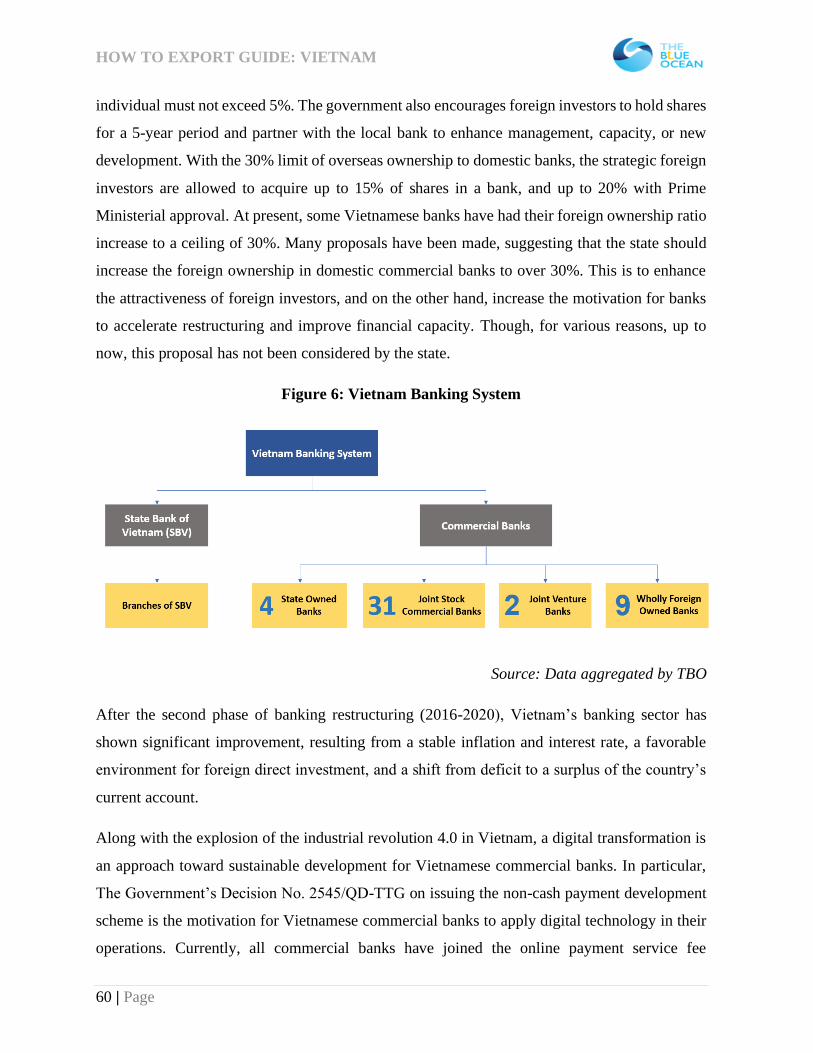

Figure 6: Vietnam Banking System ........................................................................................ 60

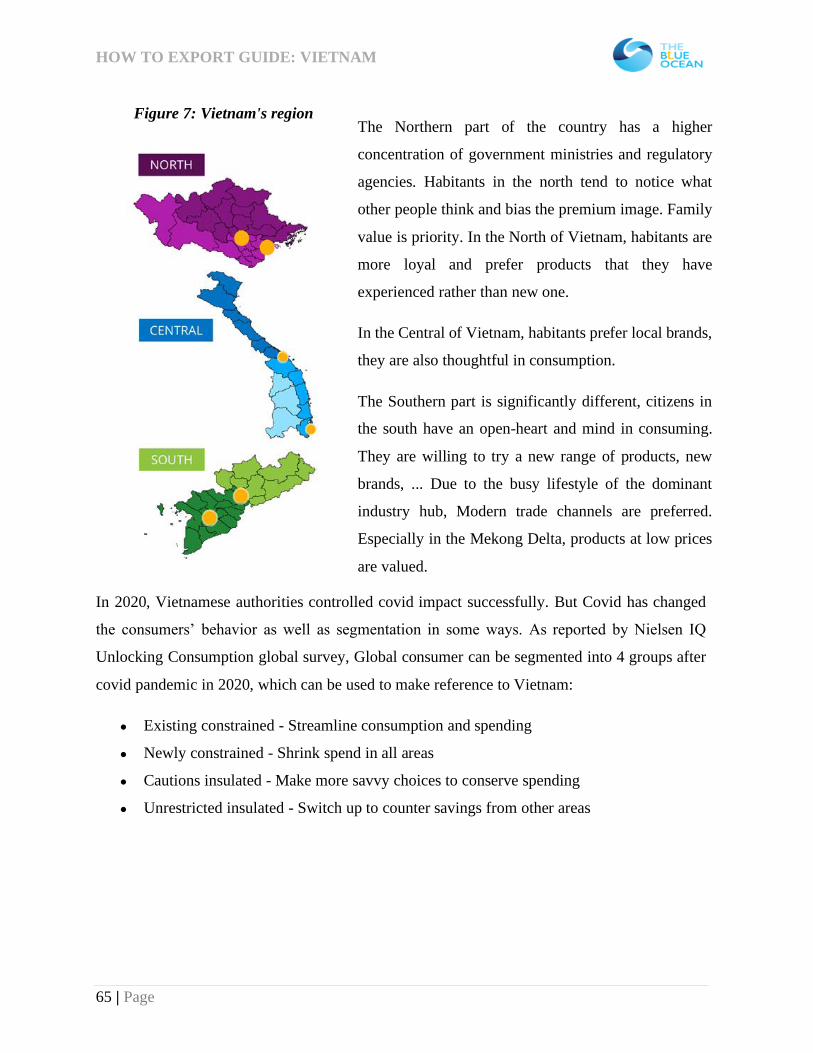

Figure 7: Vietnam's region ..................................................................................................... 65

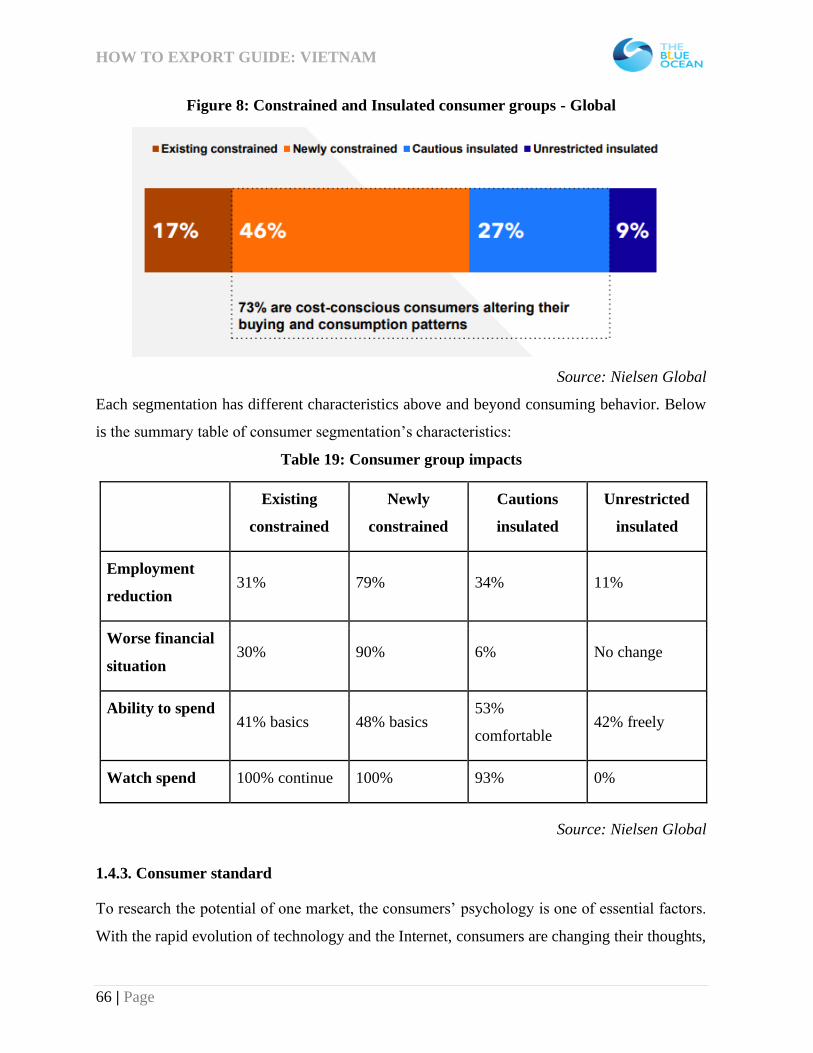

Figure 8: Constrained and Insulated consumer groups - Global .............................................. 66

Figure 9: Toad Market in Vietnam ......................................................................................... 70

Figure 10: Traditional Grocery in Vietnam ............................................................................. 71

Figure 11: One of the top Convenience Store in Vietnam - Circle K ....................................... 73

Figure 12: The biggest hypermarket chain in Vietnam GO! .................................................... 75

Figure 13: The leading local minimart chain - Bach Hoa Xanh ............................................... 76

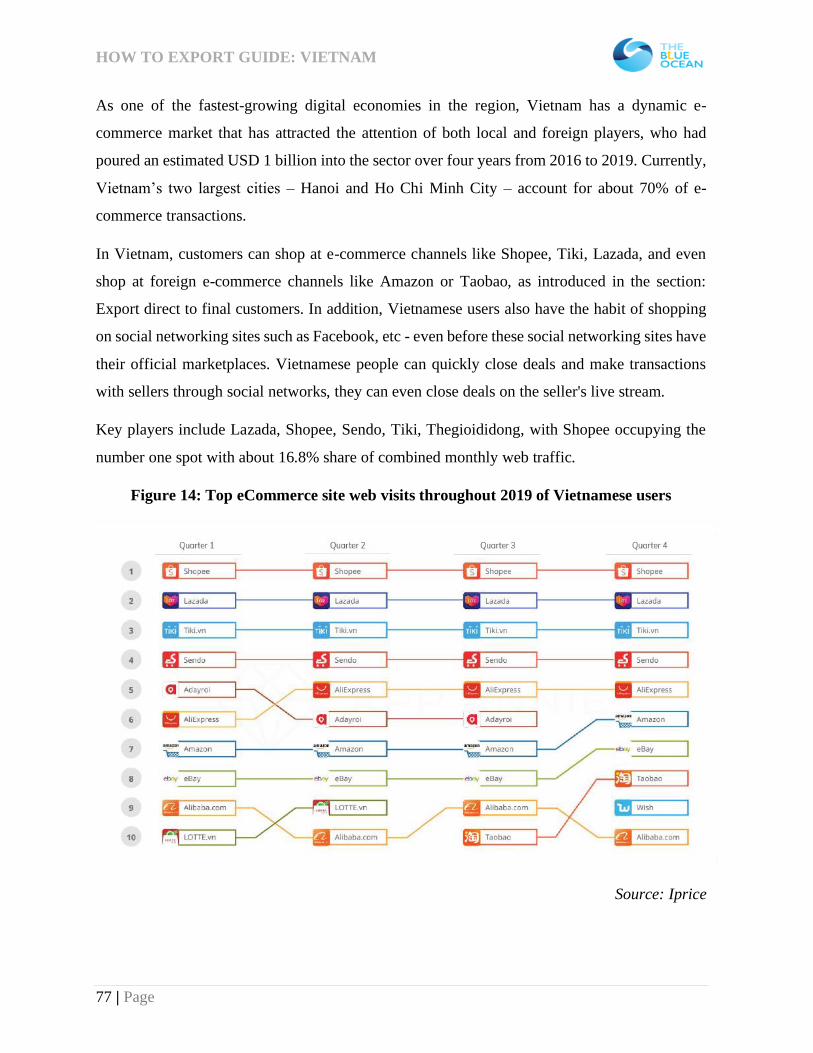

Figure 14: Top eCommerce site web visits throughout 2019 of Vietnamese users .................. 77

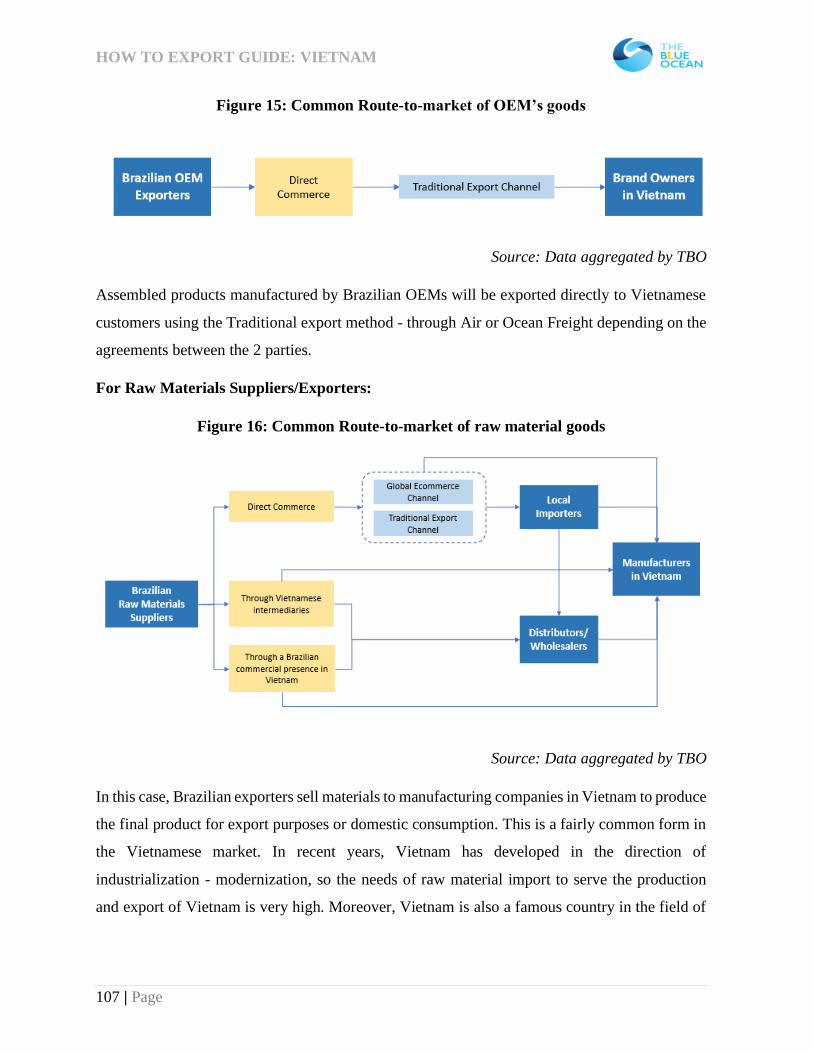

Figure 15: Common Route-to-market of OEM’s goods ........................................................ 107

Figure 16: Common Route-to-market of raw material goods ................................................ 107

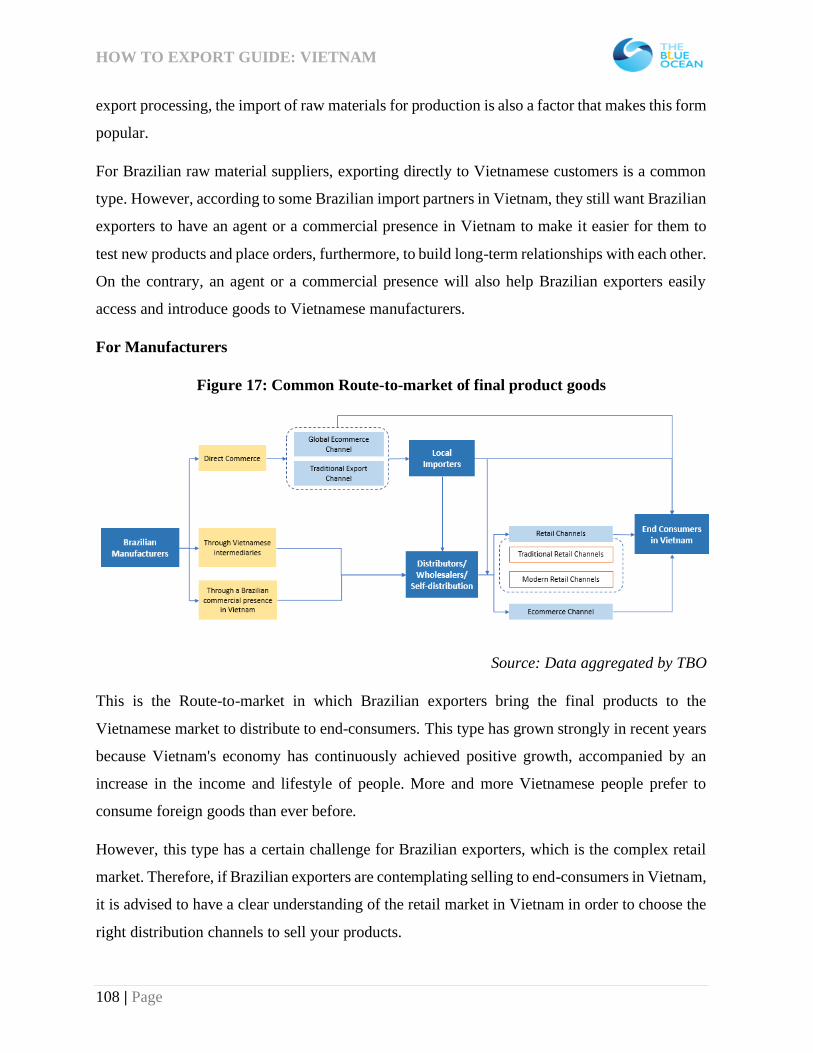

Figure 17: Common Route-to-market of final product goods ................................................ 108

Figure 18: Fado Vietnam ...................................................................................................... 111

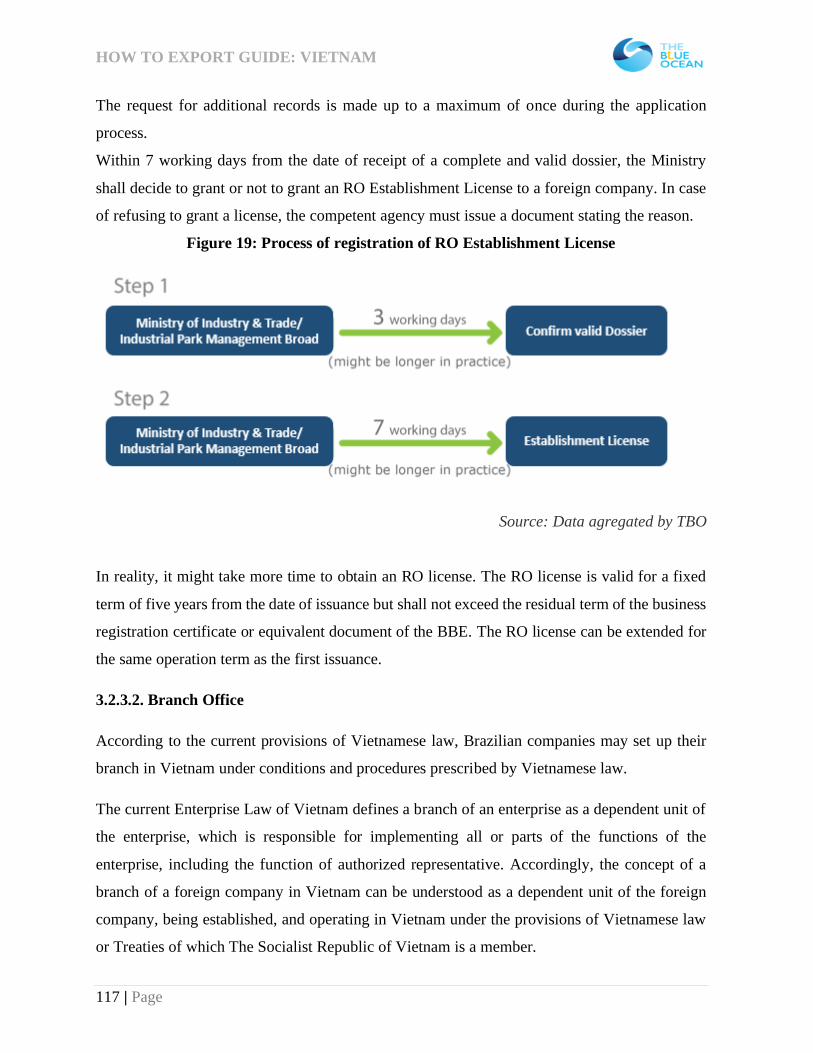

Figure 19: Process of registration of RO Establishment License ........................................... 117

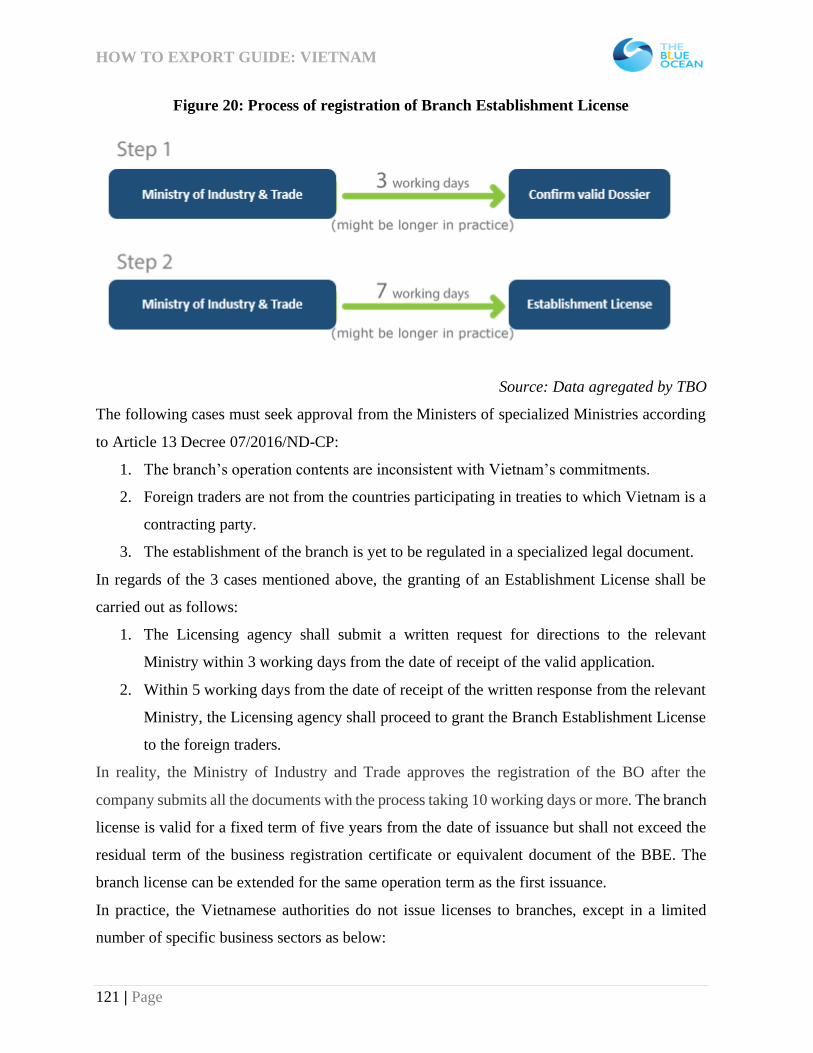

Figure 20: Process of registration of Branch Establishment License ..................................... 121

Figure 21: Road Transport in Vietnam ................................................................................. 139

Figure 22: Railway Transport in Vietnam ............................................................................. 139

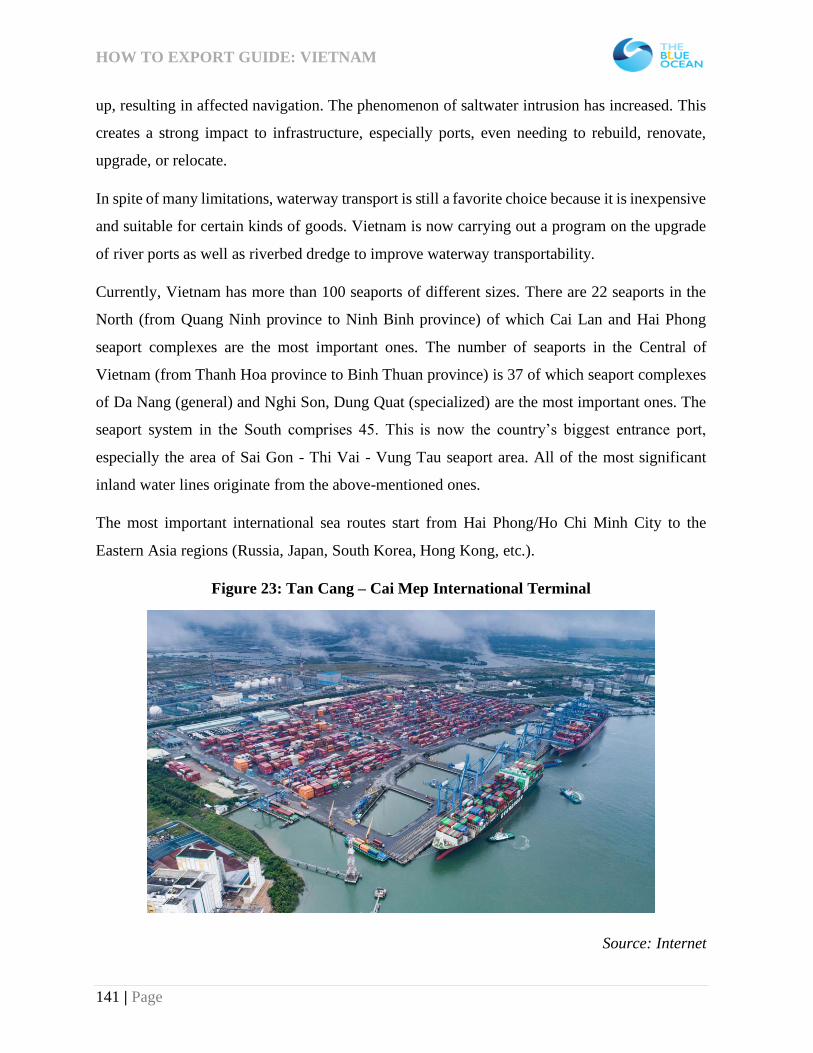

Figure 23: Tan Cang – Cai Mep International Terminal ........................................................ 141

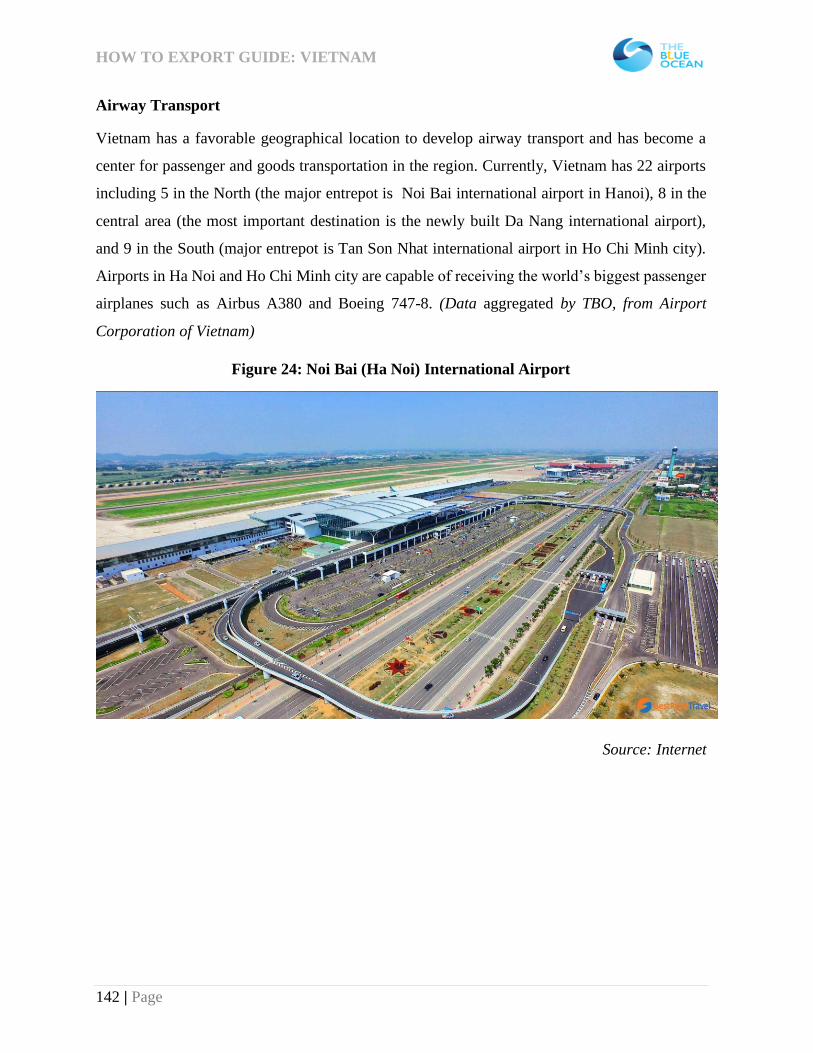

Figure 24: Noi Bai (Ha Noi) International Airport ................................................................ 142

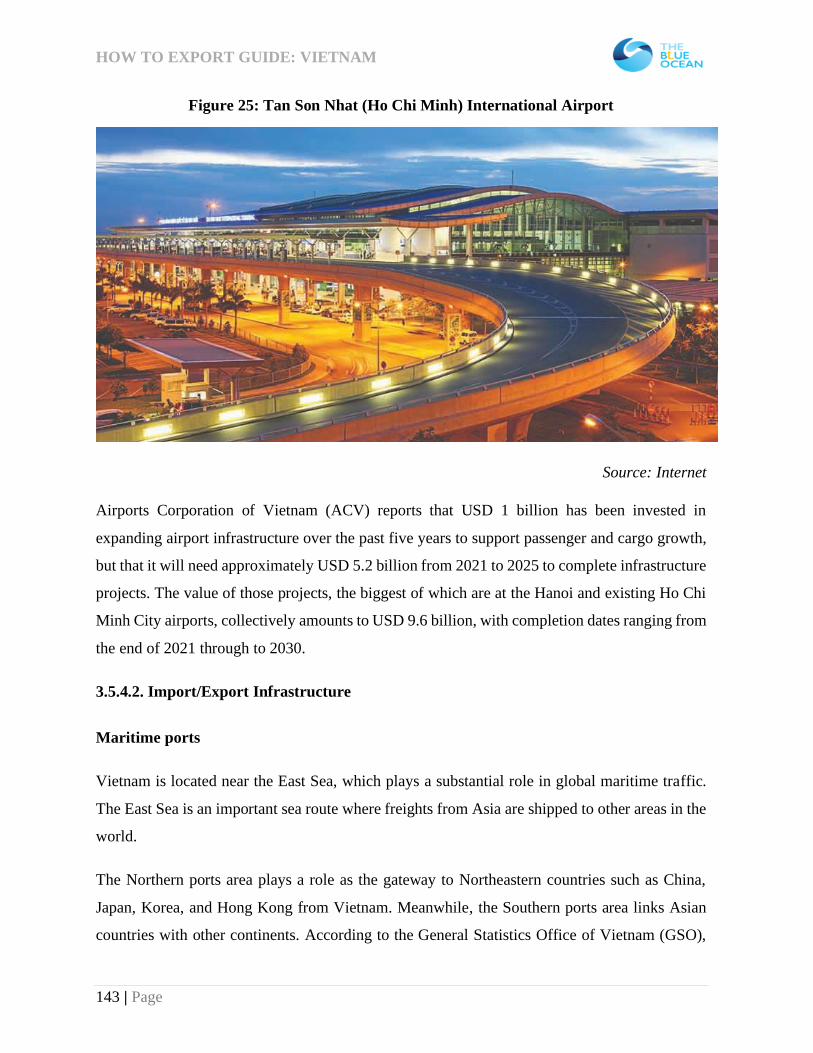

Figure 25: Tan Son Nhat (Ho Chi Minh) International Airport ............................................. 143

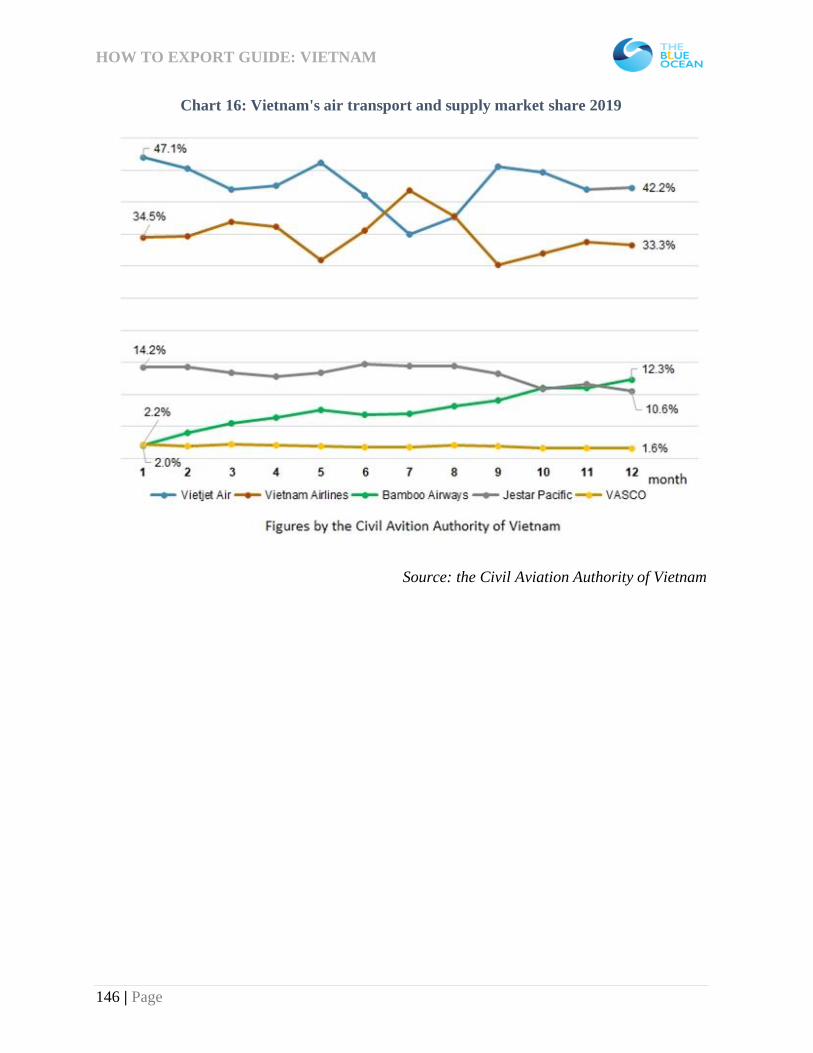

Figure 26: Airports and main flight routes in Vietnam .......................................................... 147

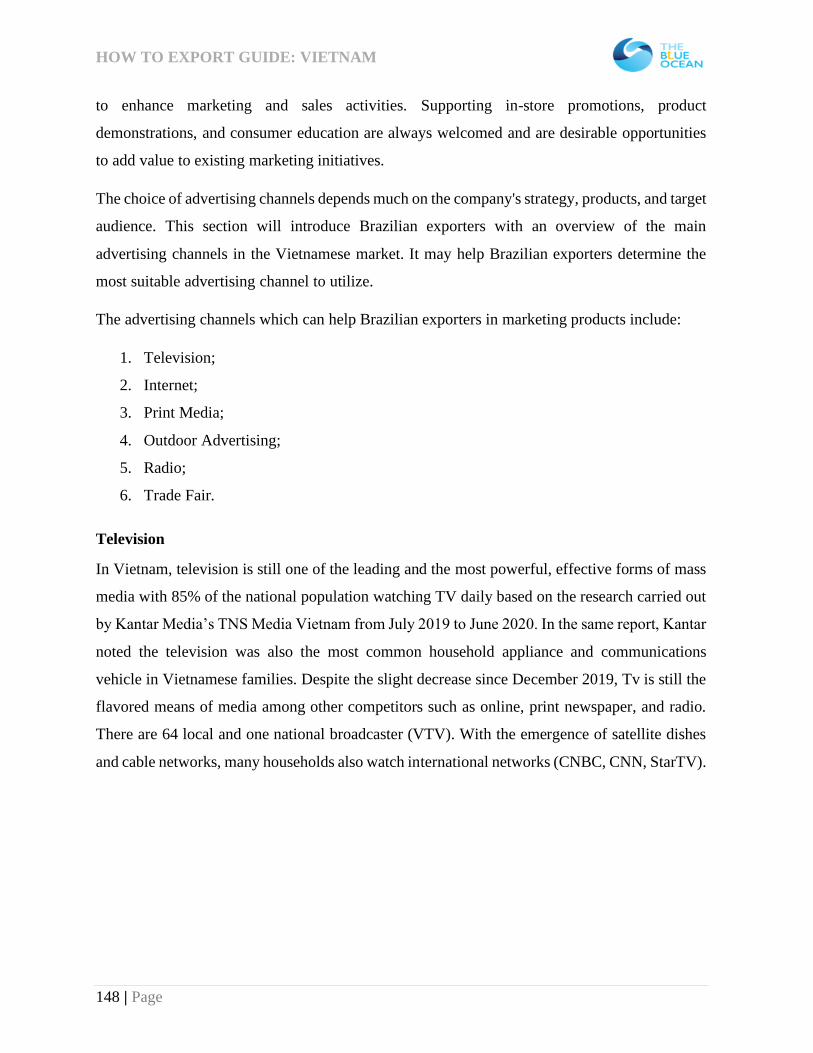

Figure 27: A broad picture of media landscape ..................................................................... 149

Figure 28: Vietnam top social media platform in 2020 ......................................................... 150

HOW TO EXPORT GUIDE: VIETNAM

7 | Page

Figure 29: Outdoor Advertising in Vietnam ......................................................................... 151

Figure 30: Digital Outdoor Advertising in Vietnam .............................................................. 152

Figure 31: Trade Fair in Vietnam ......................................................................................... 153

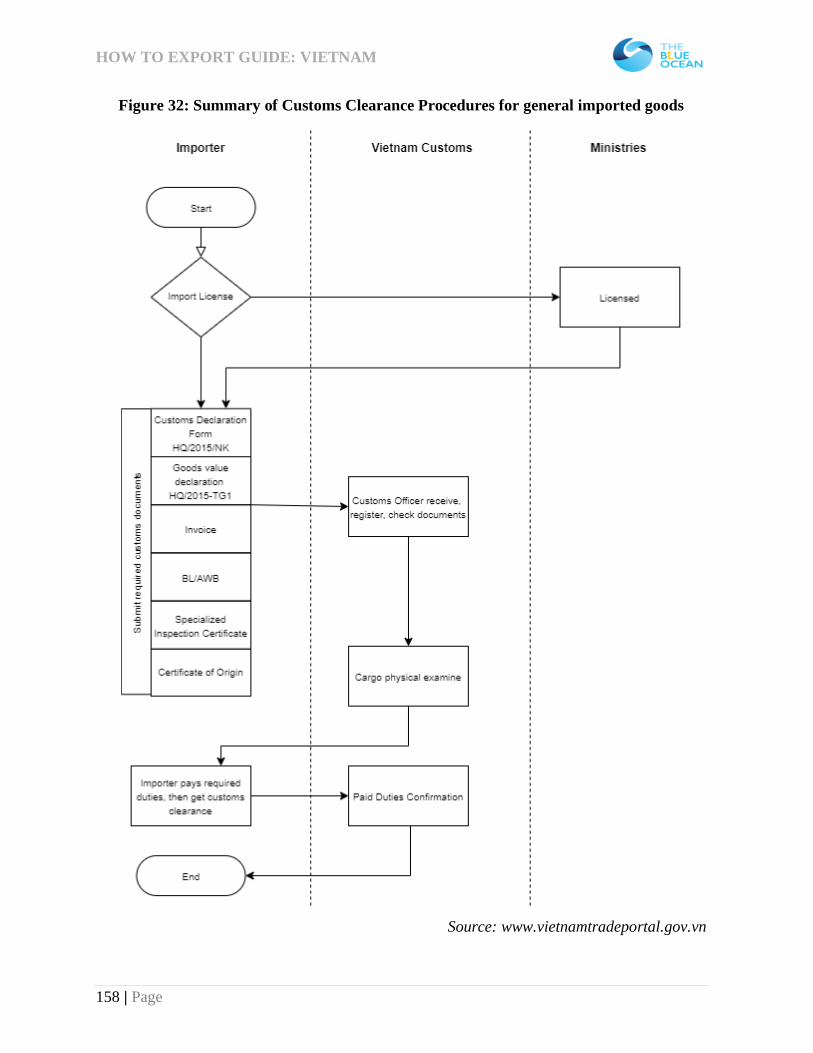

Figure 32: Summary of Customs Clearance Procedures for general imported goods ............. 158

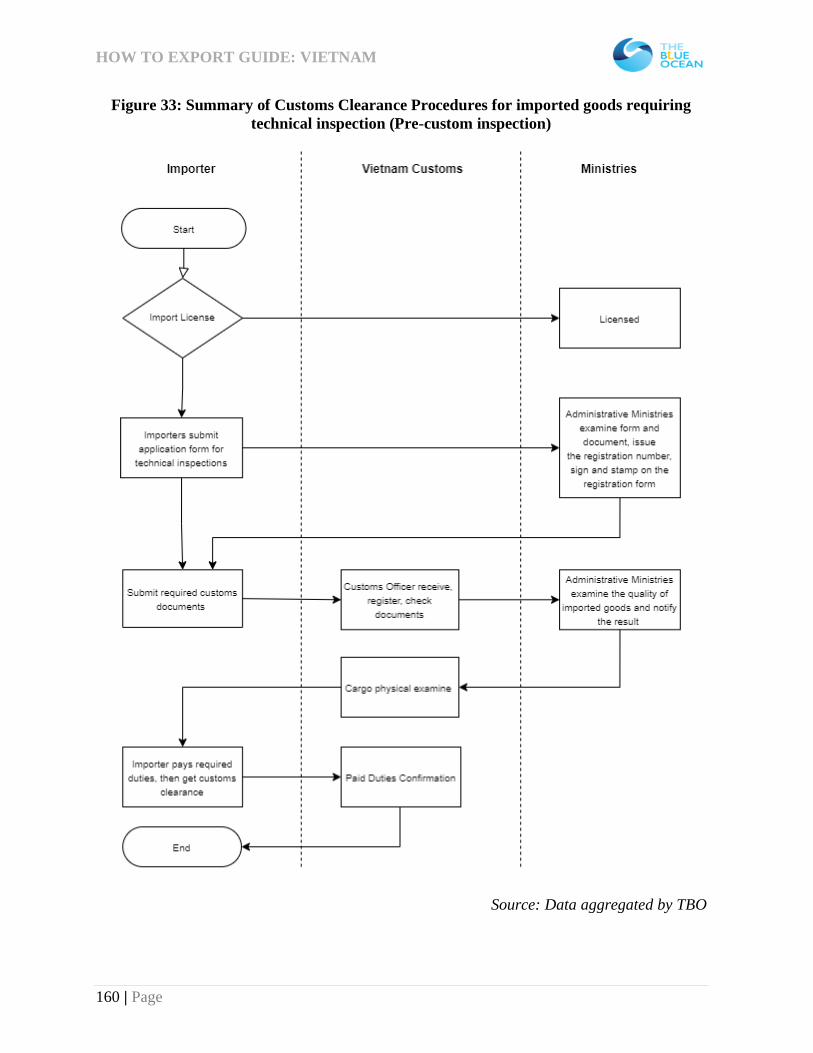

Figure 33: Summary of Customs Clearance Procedures for imported goods requiring technical

inspection (Pre-custom inspection) ....................................................................................... 160

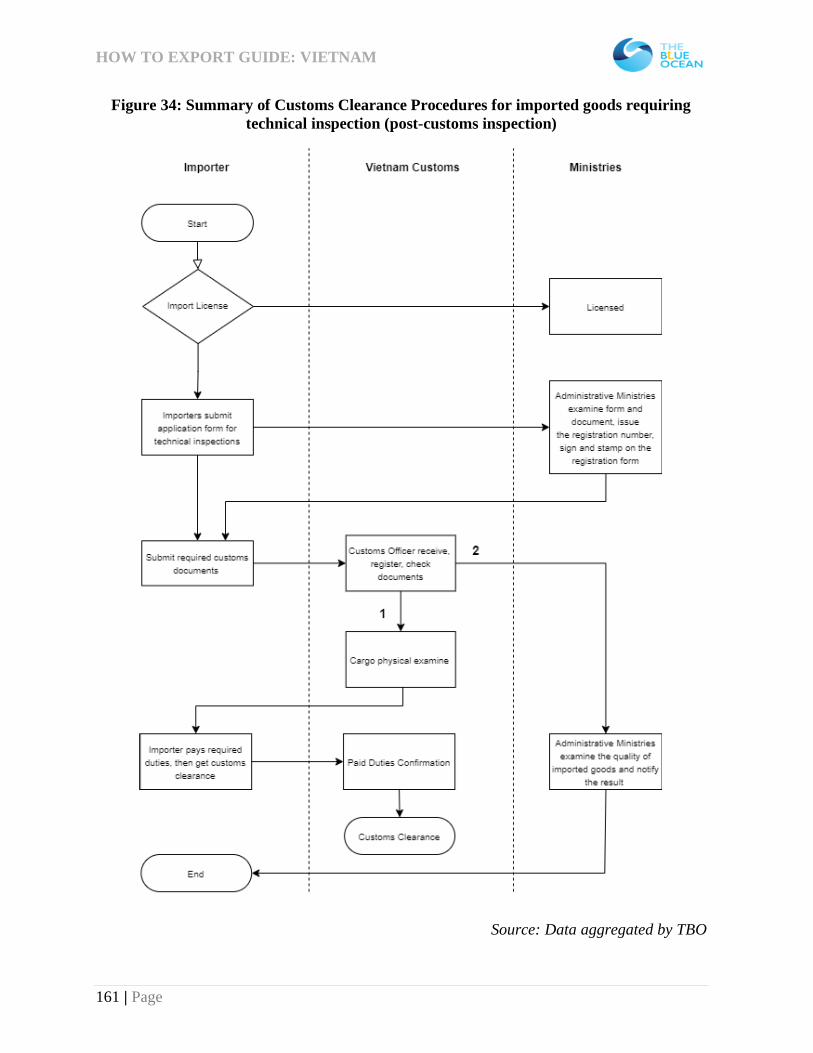

Figure 34: Summary of Customs Clearance Procedures for imported goods requiring technical

inspection (post-customs inspection) .................................................................................... 161

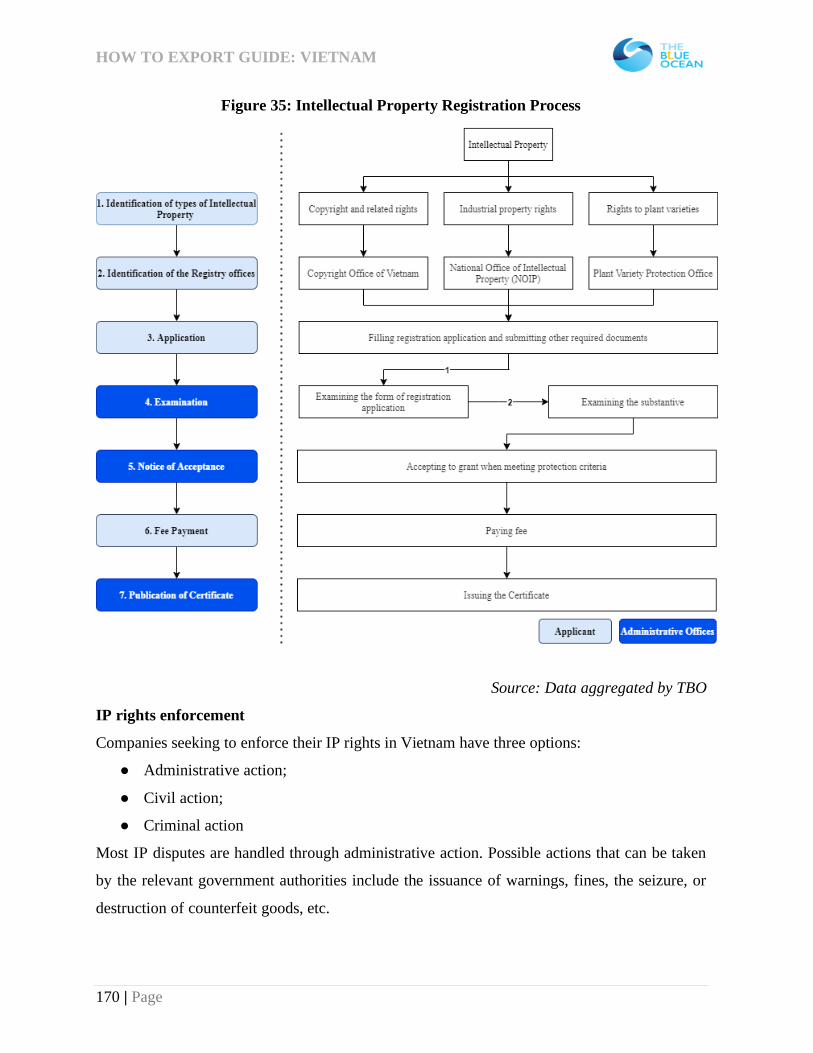

Figure 35: Intellectual Property Registration Process ............................................................ 170

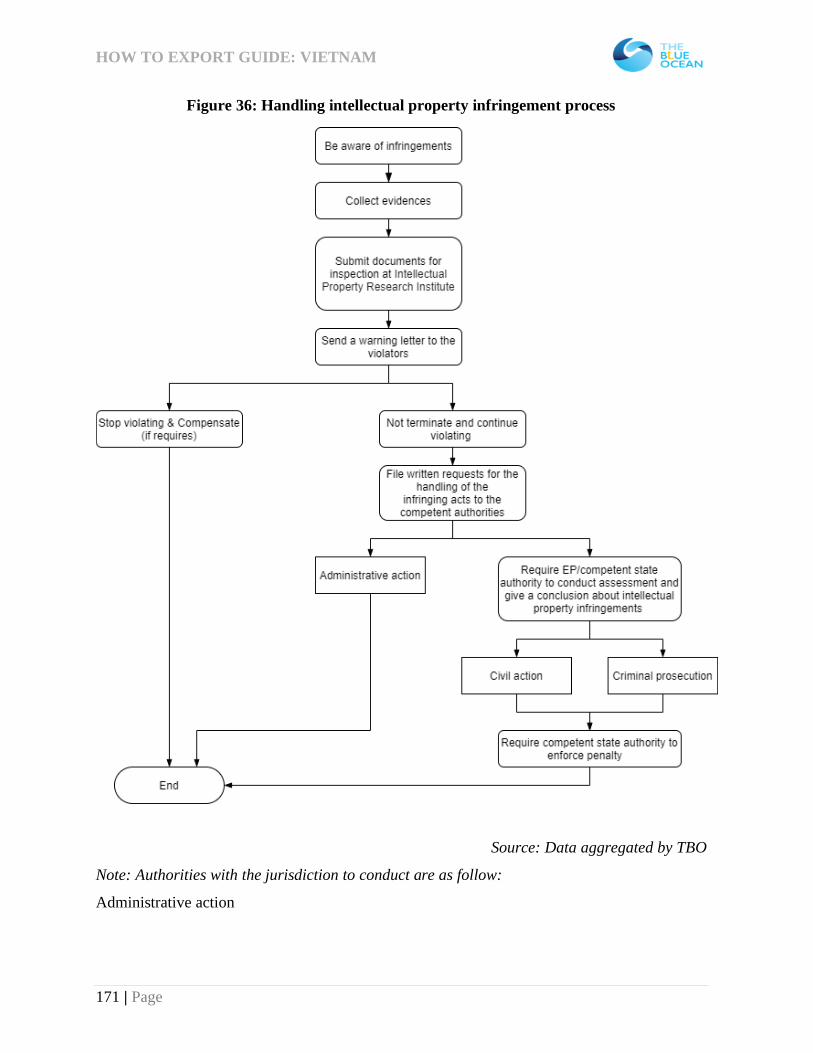

Figure 36: Handling intellectual property infringement process ............................................ 171

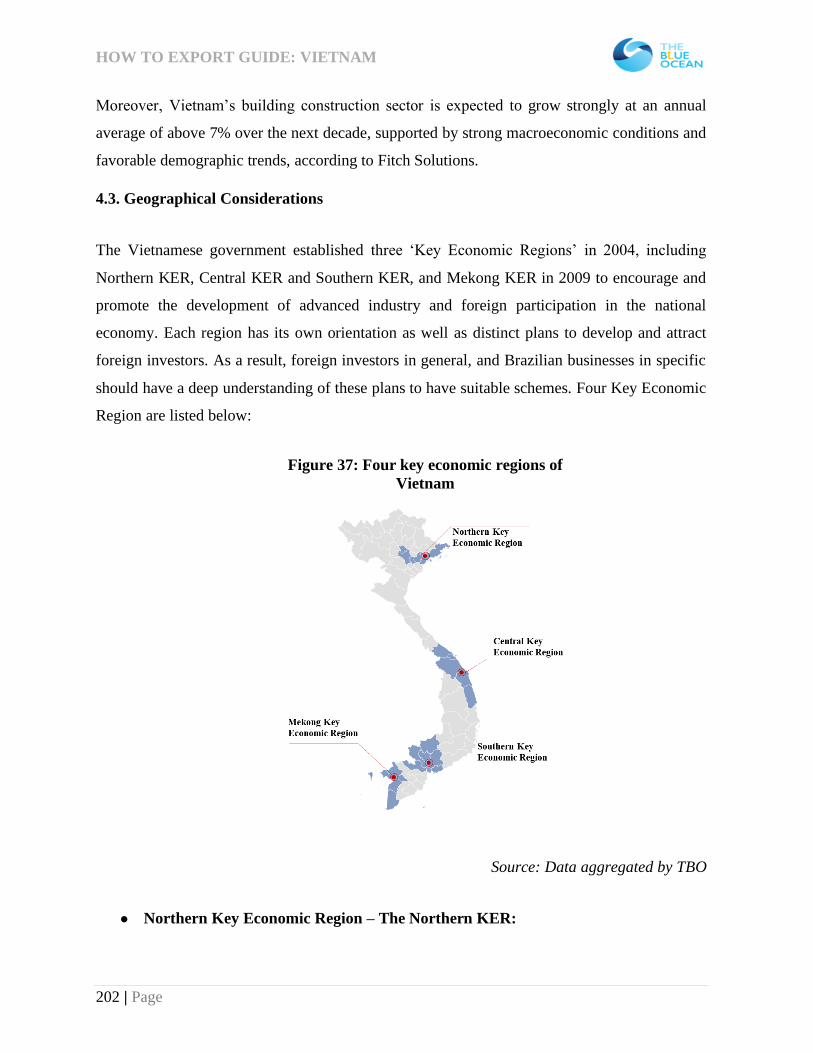

Figure 37: Four key economic regions of Vietnam ............................................................... 202

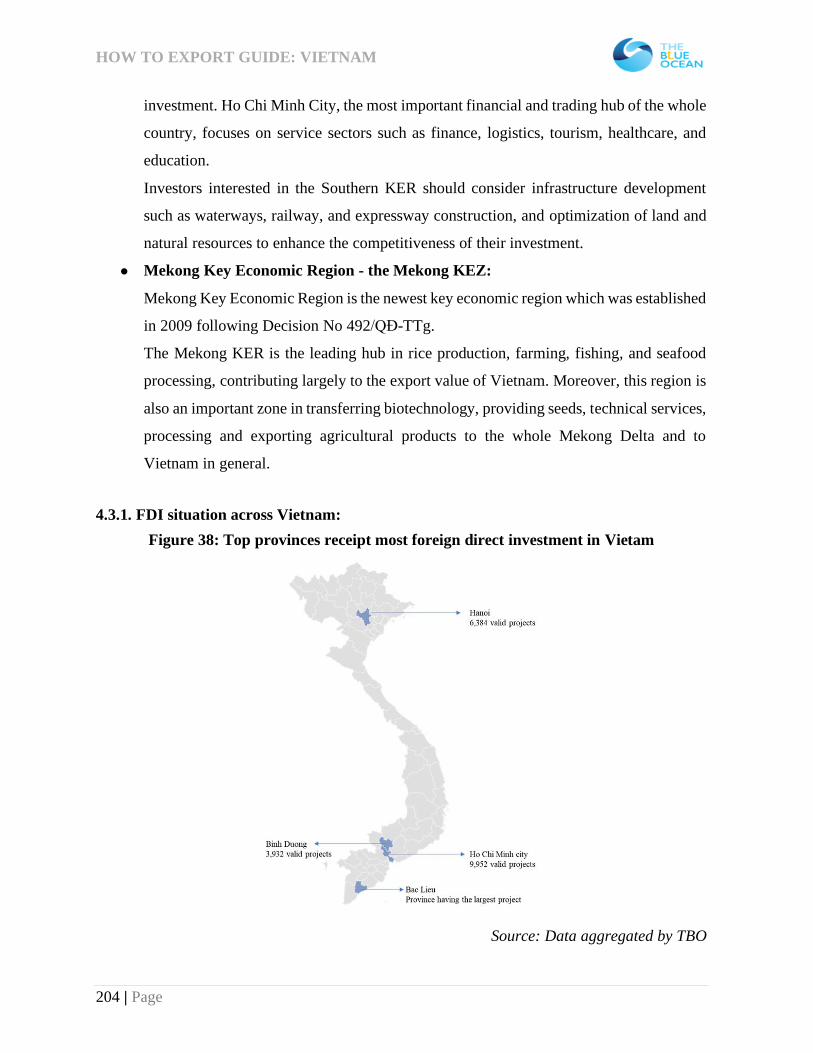

Figure 38: Top provinces receipt most foreign direct investment in Vietam .......................... 204

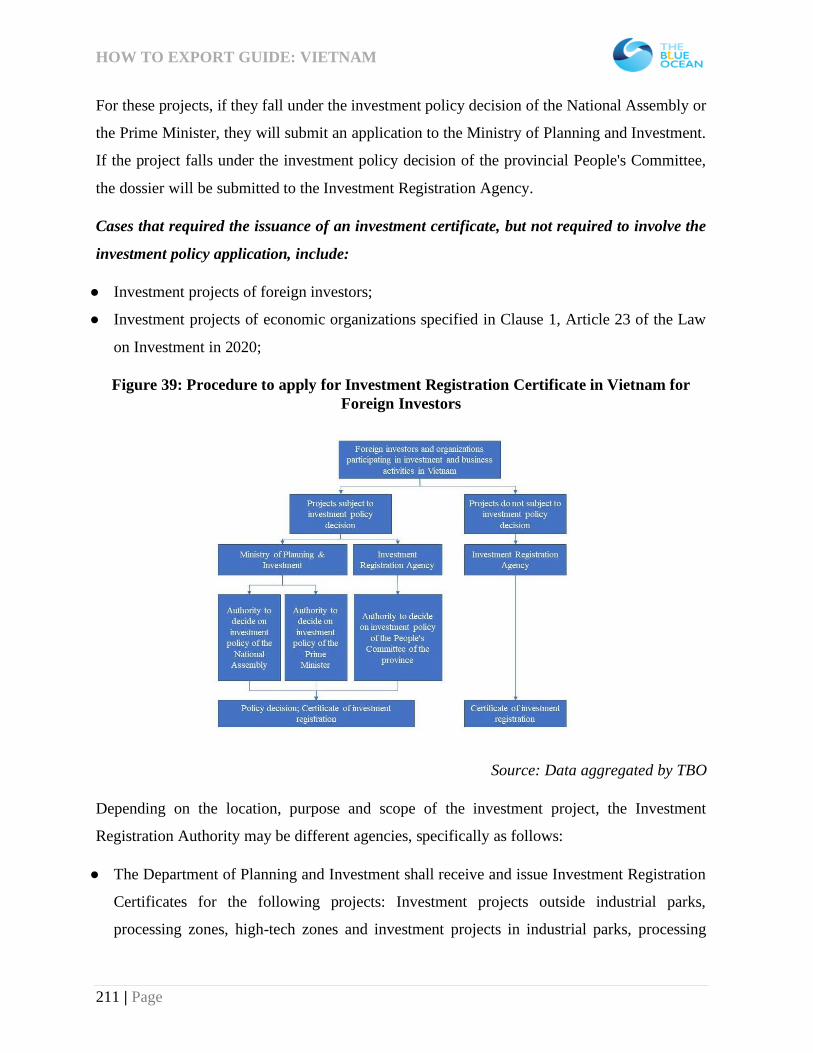

Figure 39: Procedure to apply for Investment Registration Certificate in Vietnam for Foreign

Investors .............................................................................................................................. 211

HOW TO EXPORT GUIDE: VIETNAM

8 | Page

LIST OF CHARTS

Chart 1: Vietnam population pyramid by age in 2009 and 2019 (%) ....................................... 23

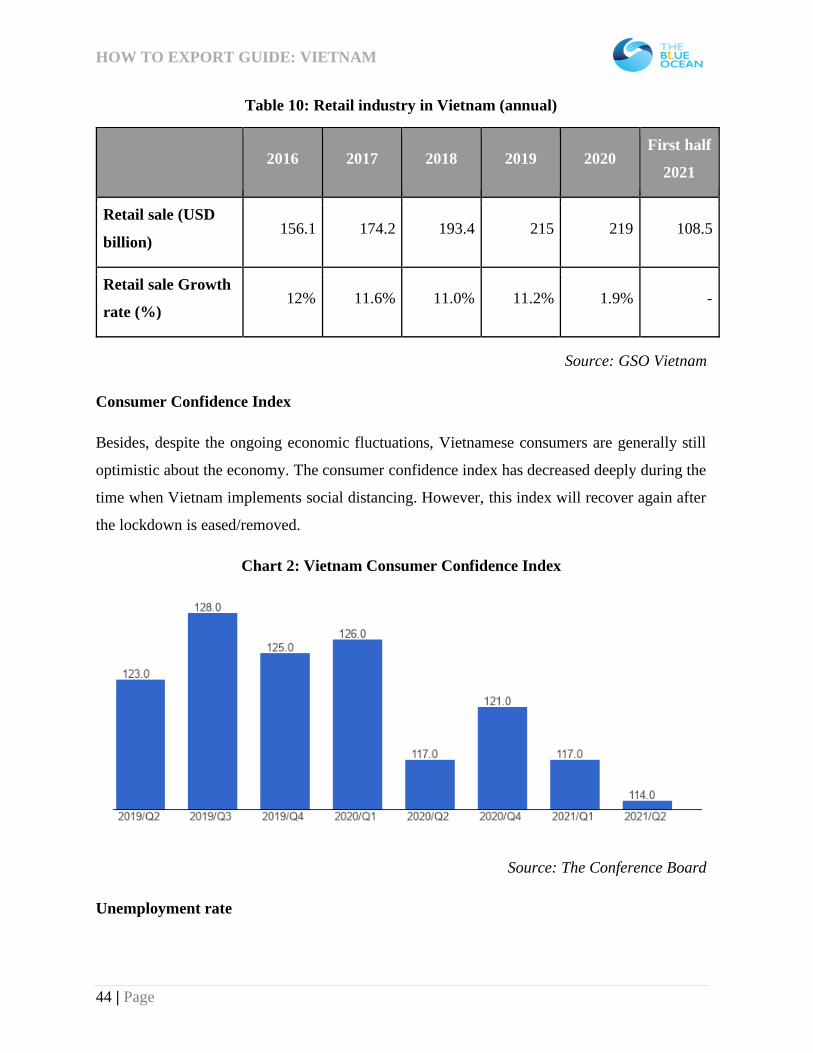

Chart 2: Vietnam Consumer Confidence Index ....................................................................... 44

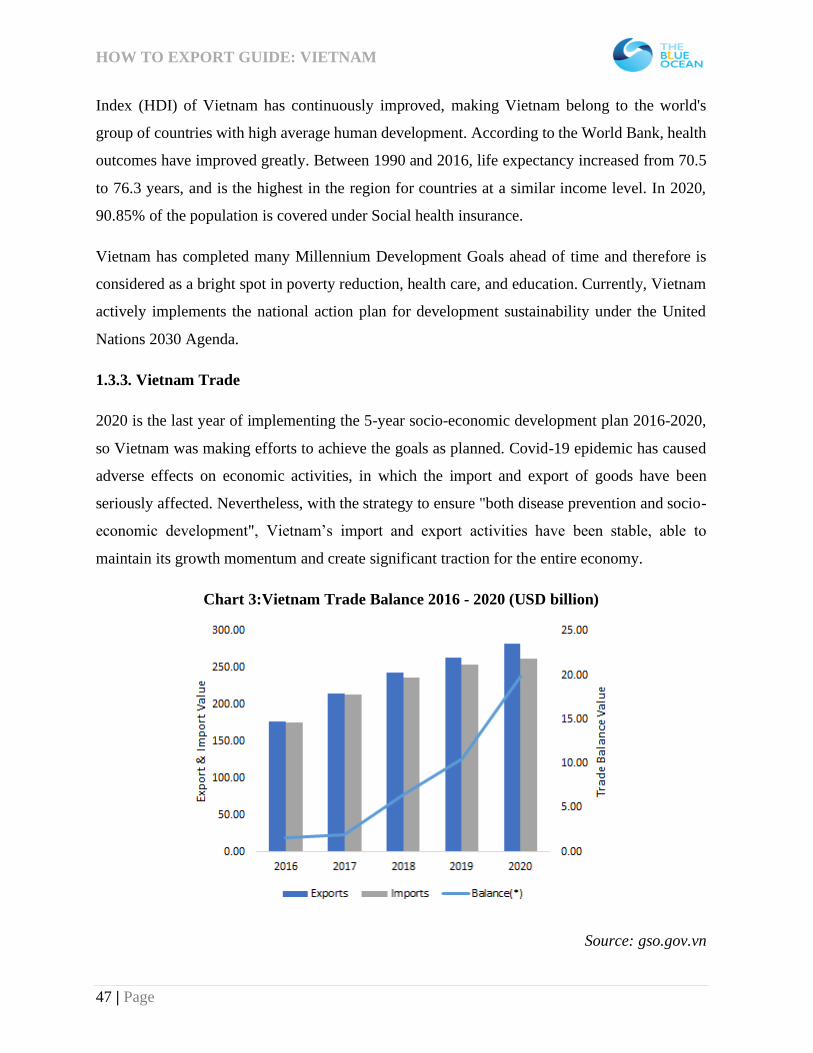

Chart 3:Vietnam Trade Balance 2016 - 2020 (USD billion) .................................................... 47

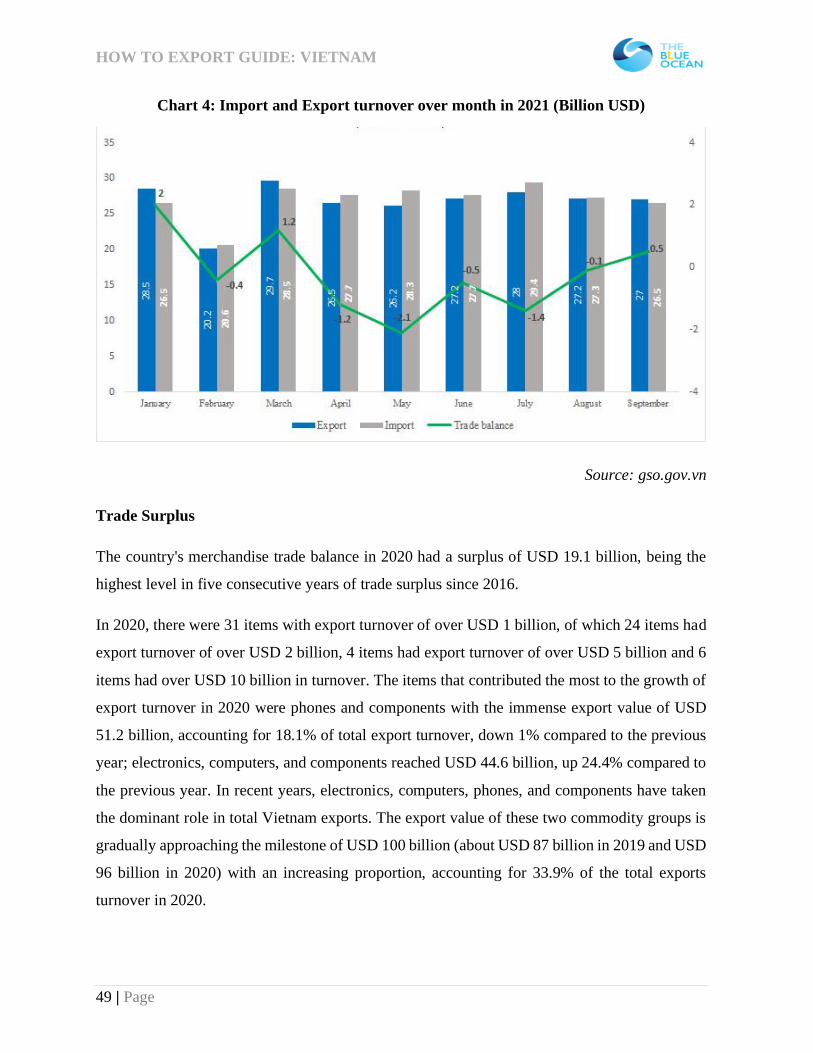

Chart 4: Import and Export turnover over month in 2021 (Billion USD)................................. 49

Chart 5: Economic class distribution ...................................................................................... 63

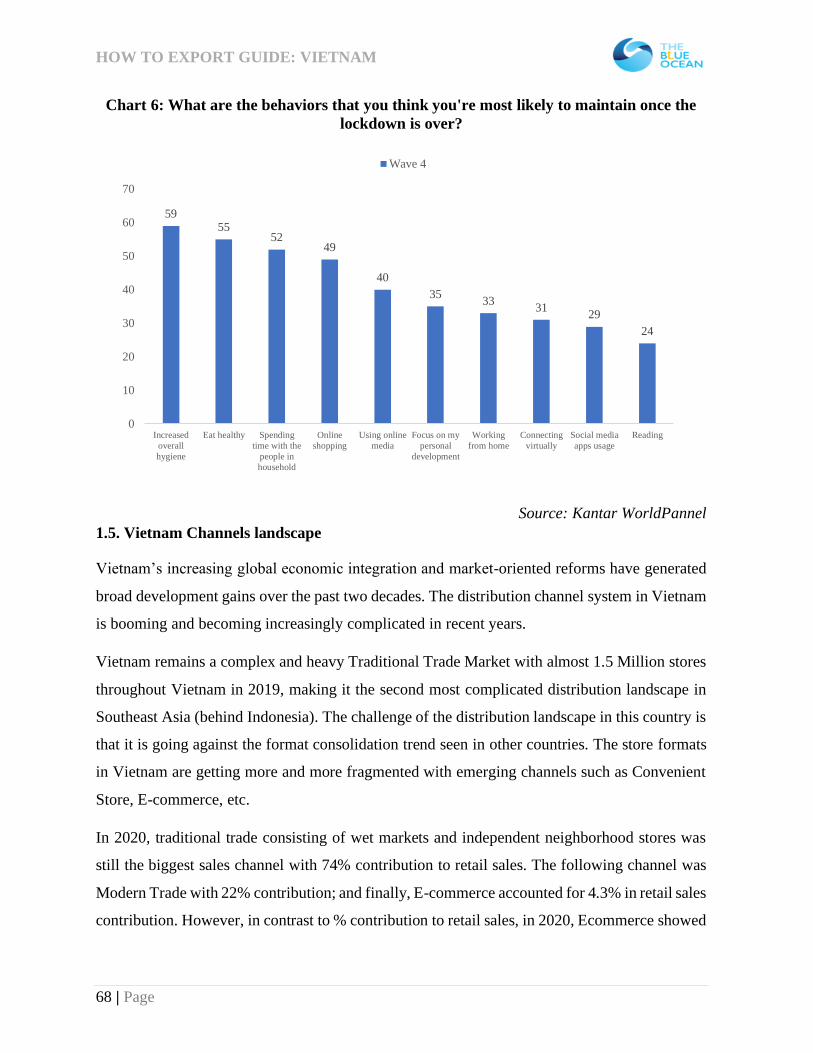

Chart 6: What are the behaviors that you think you're most likely to maintain once the lockdown

is over? .................................................................................................................................. 68

Chart 7: Vietnam Retail Sales contribution % ......................................................................... 69

Chart 8: Number of convenience stores by key players ........................................................... 72

Chart 9: Number of Hypermarkets and Supermarkets by key players ..................................... 74

Chart 10: Number of Minimart by key players ....................................................................... 74

Chart 11: Top 10 online shopping categories according to online shoppers in Vietnam in 2020

.............................................................................................................................................. 78

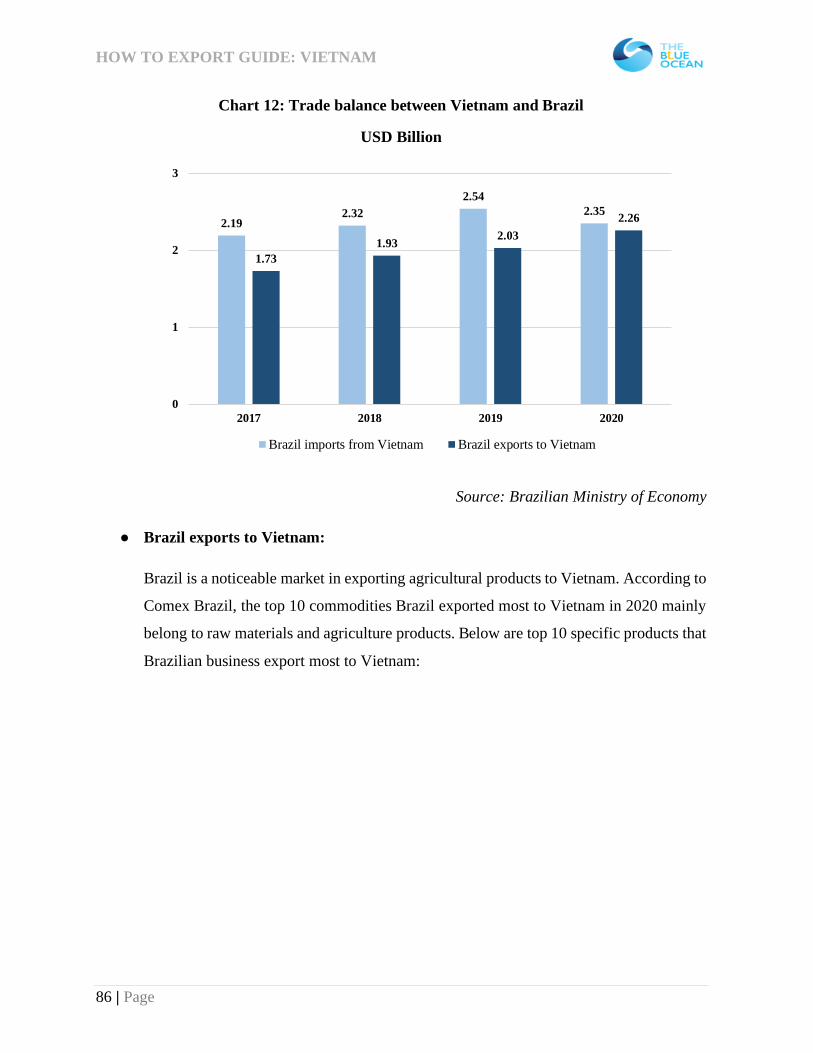

Chart 13: Trade balance between Vietnam and Brazil............................................................. 86

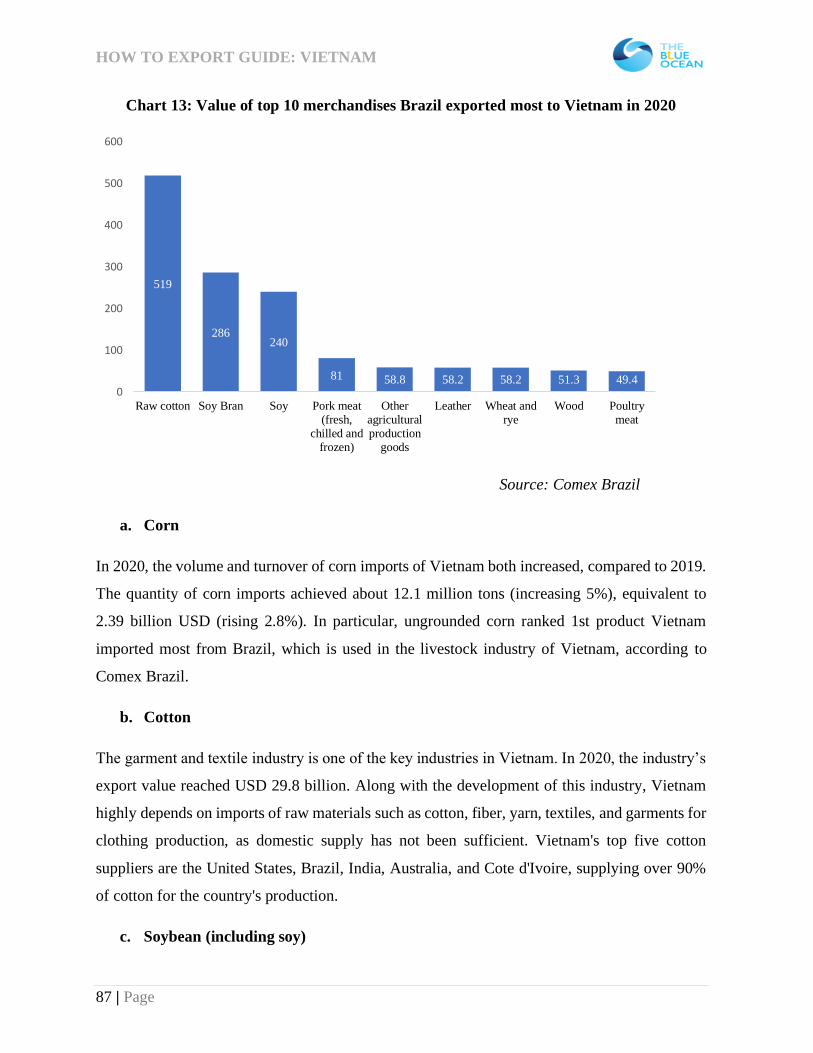

Chart 14: Value of top 10 merchandises Brazil exported most to Vietnam in 2020 ................. 87

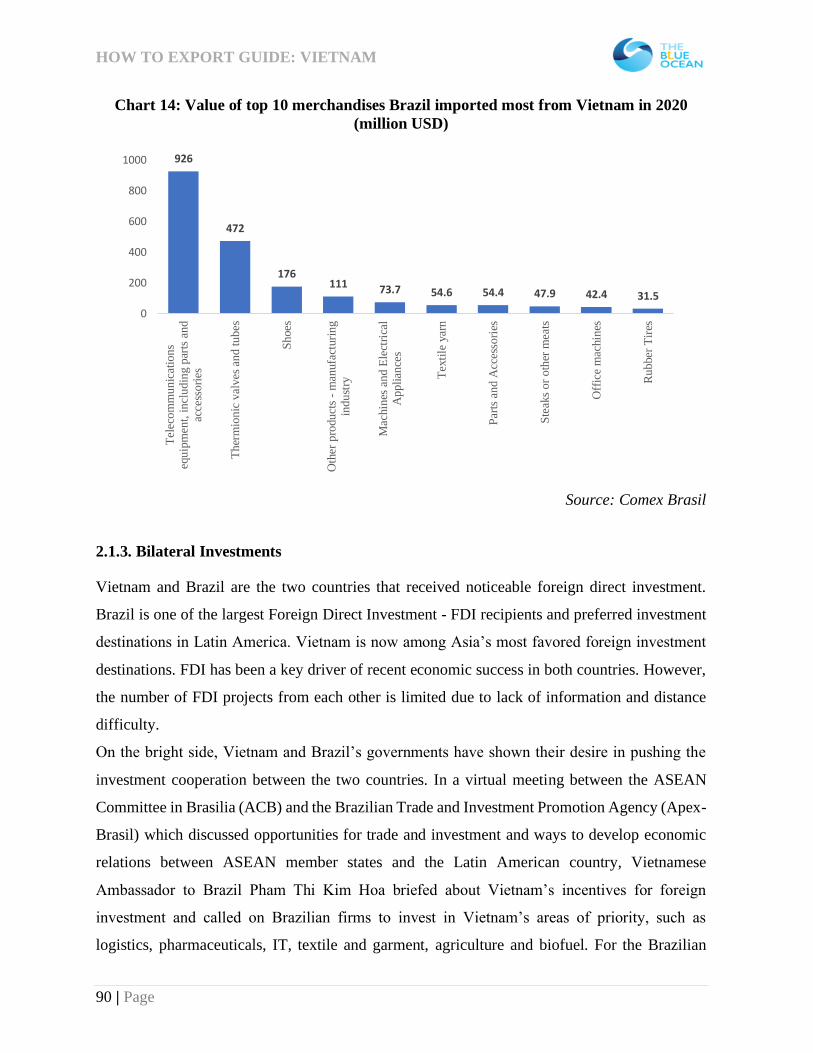

Chart 15: Value of top 10 merchandises Brazil imported most from Vietnam in 2020 (million

USD) ..................................................................................................................................... 90

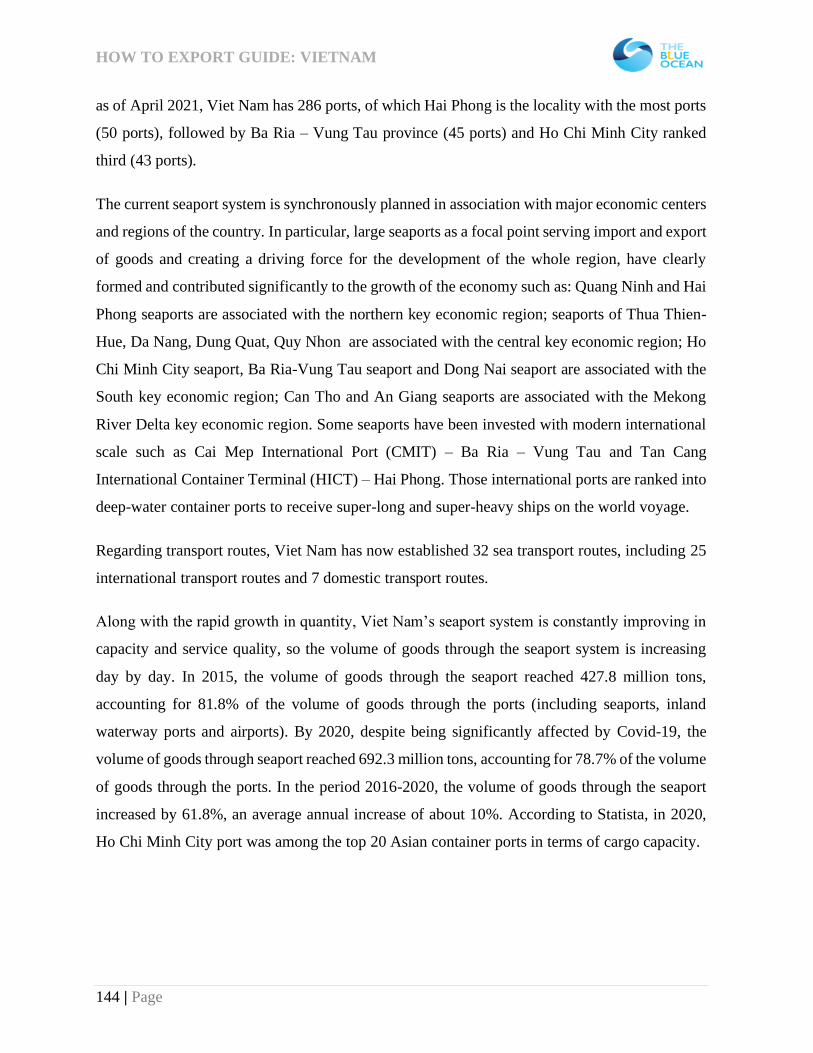

Chart 16: Volume of cargos across ports from 2015-2020 (Billion tons) ............................... 145

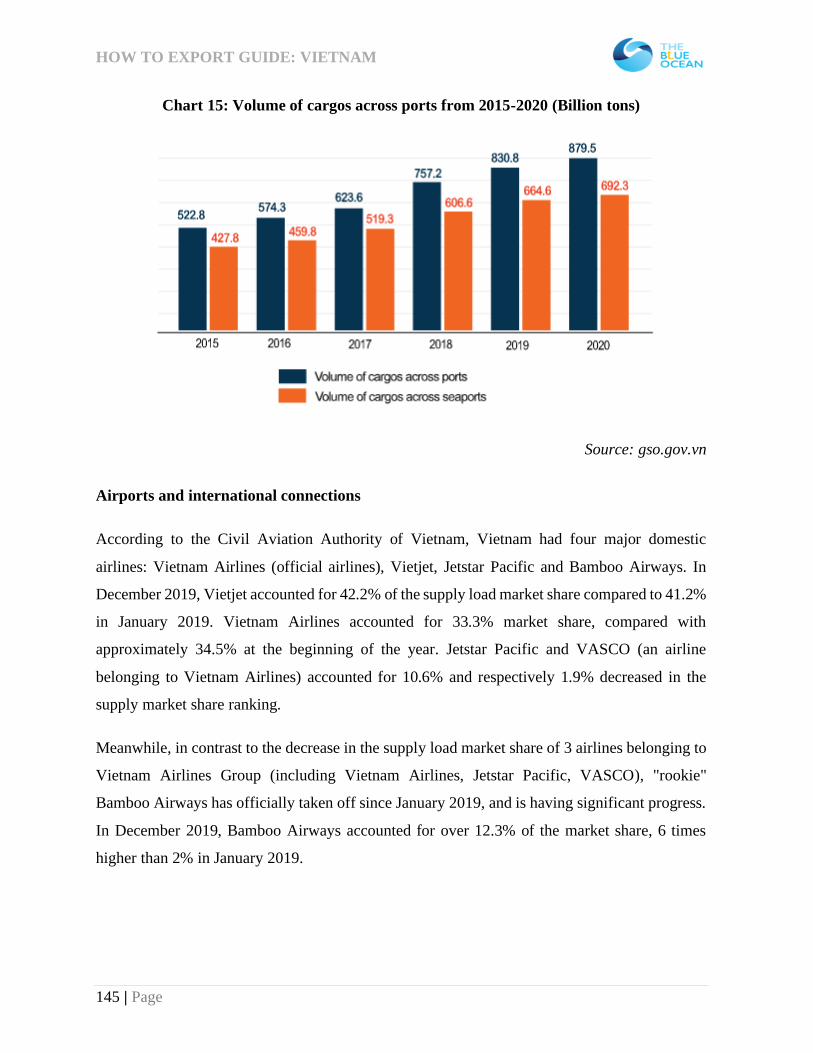

Chart 17: Vietnam's air transport and supply market share 2019 ........................................... 146

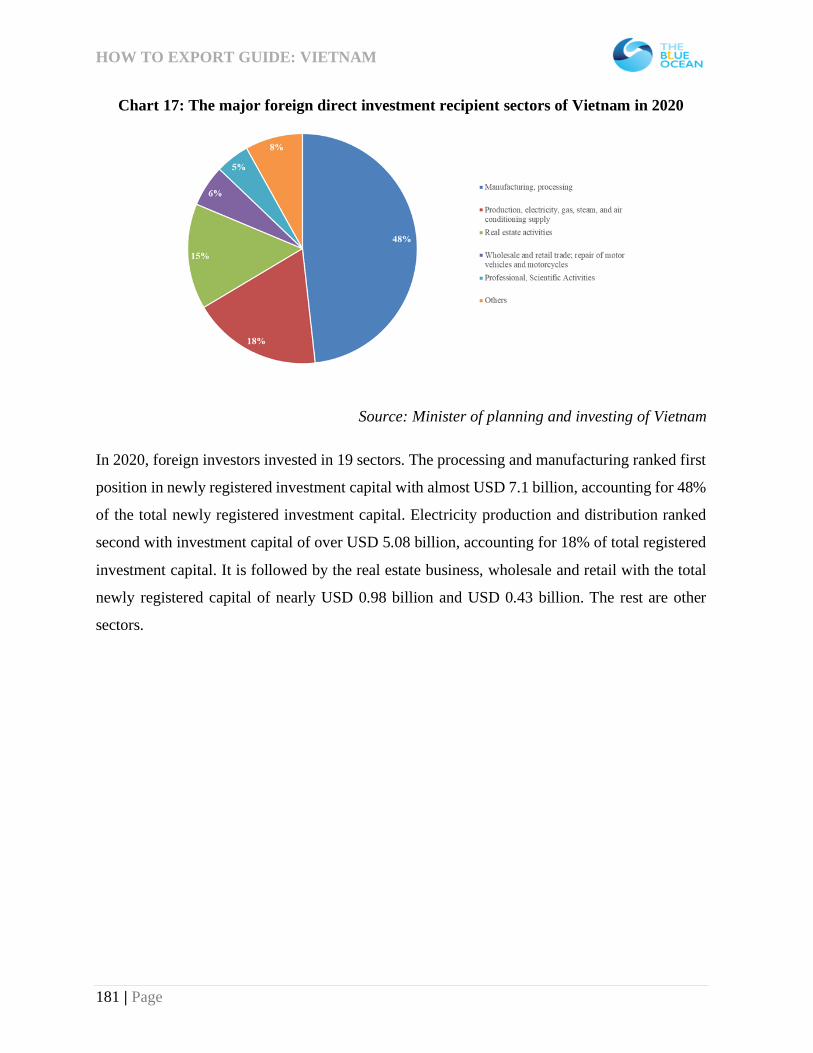

Chart 18: The major foreign direct investment recipient sectors of Vietnam in 2020............. 181

Chart 19: Number of people employed in thousand by sectors in Vietnam 2021 ................... 224

HOW TO EXPORT GUIDE: VIETNAM

9 | Page

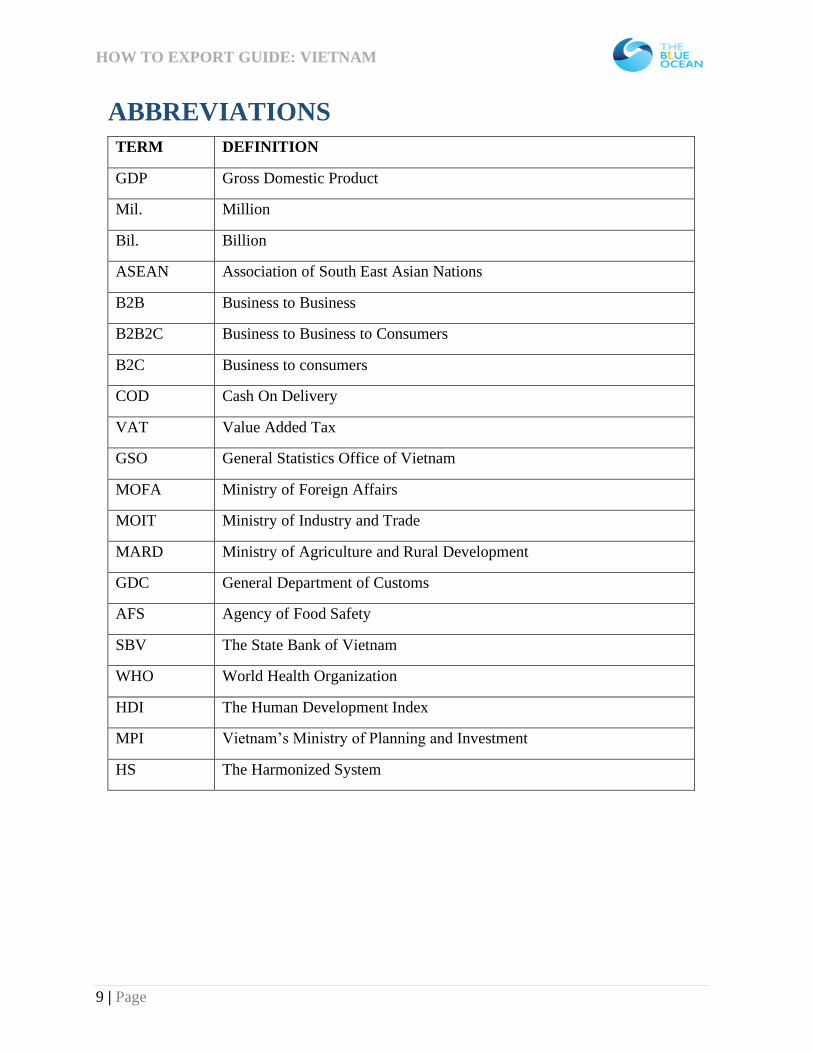

ABBREVIATIONS

TERM DEFINITION

GDP Gross Domestic Product

Mil. Million

Bil. Billion

ASEAN Association of South East Asian Nations

B2B Business to Business

B2B2C Business to Business to Consumers

B2C Business to consumers

COD Cash On Delivery

VAT Value Added Tax

GSO General Statistics Office of Vietnam

MOFA Ministry of Foreign Affairs

MOIT Ministry of Industry and Trade

MARD Ministry of Agriculture and Rural Development

GDC General Department of Customs

AFS Agency of Food Safety

SBV The State Bank of Vietnam

WHO World Health Organization

HDI The Human Development Index

MPI Vietnam’s Ministry of Planning and Investment

HS The Harmonized System

HOW TO EXPORT GUIDE: VIETNAM

10 | Page

INTRODUCTION

Brazil is one of Vietnam’s top partners in South America. The two countries have been

supporting each other to boost socio-economic development in each country and working closely

in international organizations and multilateral forums. Brazilian exports to Vietnam have

recorded steady growth in various product categories based on different degrees of

industrialization, with benefits for both Vietnamese importers and Brazilian suppliers.

Vietnam and Brazil have much room for developing bilateral trade thanks to the similarities in

culture, geographical variety as well as climate and multiculturalism of the population. Yet, to

start doing business in Vietnam, Brazilians may need to understand various aspects of Vietnam,

which could be the major obstacle that many Brazilian businesses have to face due to the physical

and cultural distance. Understanding the differences between the way Vietnamese people and

Brazilians do business increases the opportunities for Brazilian exporters’ success in the

Vietnamese market.

This brief guide serves as an introduction to this market that is still so astonishing for many

Brazilians – you will find lots of helpful information which gives you an overview of the country,

the Vietnamese people, and the economy. Besides, the details on opportunities and challenges

consulted in this guide will help Brazilian businesses, as well as investors, understand and

prepare properly for a suitable way to enter the Vietnamese market.

Despite being called “Hoed to export guide - Vietnam” (title of the series of publications by the

Department of Trade Promotion and Investment of the Itamaraty on various markets), the guide

incorporates a fundamental chapter on “How to invest in Vietnam”, in order to subsidize

companies with an interest in the Vietnamese market.

The last section provides you with some indications and relevant contacts when doing business

in Vietnam which are essential for those who first explore this country’s market.

HOW TO EXPORT GUIDE: VIETNAM

11 | Page

WHY VIETNAM?

In the eyes of the foreigners, Vietnam is well-known as a country with a rich culture and history

spanning over 4,000 years. In the past, Vietnam’s economy was greatly affected by wars and

even embargoes from other countries. However, with the resilient nature of the Vietnamese

people and the continuous efforts of the Government, Vietnam has gradually re-integrated into

the world economy, and up to now, Vietnam is proud to be one of the stars of the emerging

markets universe.

Many years after the Renovation (Doi Moi) in 1986, Vietnam has changed in many aspects and

is now known as the country of dramatic development, the destination of foreign investors.

According to analysts from the World Bank and the think tank Brookings, Viet Nam’s economic

development can be explained by three main factors: “First, Vietnam has embraced trade

liberalization with gusto. Second, the country has complemented external liberalization with

domestic reforms through deregulation and lowering the cost of doing business. Finally, Vietnam

has invested heavily in human and physical capital, predominantly through public investments.”

The potential of the Vietnamese market is shown through the development of citizen’s living

standards, and the need of consumers is much higher than in the past. It is proven that Vietnamese

consumer spending is growing steadily from 2010 to 2020. Vietnam is currently categorized in

the group of lower-middle-income countries, according to the World Bank. This is the

opportunity for foreign companies to expand their business.

In addition, Vietnam is rising as a Foreign Direct Investment destination. Vietnam meets three

fundamental needs which every business always seeks when investing in one country are: Labour

force, socio-political stability, and legal system.

Firstly, Vietnam is now in a period of golden population structure – 68.94% of its population

were in working age, from 15 to 64 years old, in 2020, according to Statista. Besides, Vietnam

is strategically located in the center of Southeast Asia. It is also worth noting that Vietnam shares

borders with China. The country has a long coastline and is close to many international shipping

routes. These make Vietnam a prime location for trading. Additionally, Vietnam’s major cities

are also strategically located. Foreign businesses will find Hanoi - the capital, political and

HOW TO EXPORT GUIDE: VIETNAM

12 | Page

administrative hub in the north and Ho Chi Minh City - key economic hub of Vietnam in the

south. Having major cities on opposite ends of the country makes it easy to do business within

and outside the country. Furthermore, the country is a market economy, a member of the WTO,

and a party to multiple frameworks for international economic integration, including free trade

agreements with partners both within and outside the region. In particular, the country is part of

the Trans-Pacific Partnership negotiations. These factors all go some way to explaining why so

many choose to invest in Vietnam – and should draw in more foreign investors.

Secondly, Vietnam has been securing socio-political stability and is known to be one of the most

dynamic economies. Given its deep integration with the global economy, the Vietnamese

economy has been hit by the ongoing COVID-19 pandemic but has shown remarkable resilience.

GDP grew by 2.9% in 2020.

Last but not least, the Vietnamese government is committed to creating a fair and attractive

business environment for foreign investors, and constantly improving its legal framework and

institutions related to business and investment. The government has been working hard on

restructuring the economy and its model for growth, as well as enhancing national

competitiveness.

In the medium and long term, Vietnam will continue in its efforts to attract and use FDI inflows

to advance socio-economic development. The country will target “high quality” FDI inflows,

focusing on FDI projects that use advanced and friendly technologies, and use natural resources

in a sustainable way. It will also target projects with competitive products that could be part of

the global production network and value chain. This is an ample opportunity for Brazilian

businesses to consider when choosing to expand business abroad.

HOW TO EXPORT GUIDE: VIETNAM

13 | Page

PART 1: VIETNAM OVERVIEW

HOW TO EXPORT GUIDE: VIETNAM

14 | Page

PART 1: VIETNAM OVERVIEW

1.1. Country Profile

Vietnam is a rising country in Southeast Asia, witnessing significant GDP growth milestones,

especially when Vietnam's GDP receives positive growth in the context of the world economy

being stalled by Covid-19. Vietnam is undeniably an attractive destination for investors and

exporters from abroad, and Brazil is no exception.

Bilateral trade between Vietnam and Brazil has been growing since the two countries established

diplomatic relations in 1989. Brazil was the second largest exporter of soybeans and corn to

Vietnam in 2020. Major Brazil’s agricultural products exported to Vietnam include soybeans,

corn, wheat, timber, cotton, coffee, pepper, cashew nuts, tobacco, vegetables, fruits and products

originating from livestock. There are many similarities between Brazil and Vietnam: the natural

beauty, geographical variety, climate, and multiculturalism of the population. (Source: Vietnam

trade in 2020, the Ministry of Industry and Trade)

The relatively large distance that must be traveled for freight may have been the major

determinant of the level of trade between the two countries. However, these distances are no

greater than among many other trading partners.

There is potential for the current volume of trade between Vietnam and Brazil to be intensified,

especially given the encouragement of trade and the cooperation efforts between the Brazilian

and Vietnamese governments.

This first chapter will help Brazilian exporters have the most basic view of Vietnam: from basic

economic indicators to political institutions and the country's transformation after the war to the

present.

1.1.1. Geography of Vietnam

Officially named the Socialist Republic of Vietnam, Vietnam is located in the east of the

Indochina Peninsula in Southeast Asia. Vietnam lies in the tropical zone with a total area of

331,230 km2. The S-shaped country has a north-to-south distance of 1,650 kilometers and is

about 50 kilometers wide at the narrowest point. Vietnam is bordered by China to the north,

HOW TO EXPORT GUIDE: VIETNAM

15 | Page

Laos, and Cambodia to the west, the East Sea, and the Pacific Ocean to the east and south.

Vietnam's eastern border consists of over 3,444 km of beautiful coastline, which is ideal for the

development of maritime industries, trade and tourism and for its emergence as a shipping hub

for South East Asia and the world in general.

Table 1: Vietnam Overview

Official name Socialist Republic of Vietnam

Form of State One-party rule

Economic system Socialist-oriented market economy

Total Land area (sq. km) 331,230 sq. km

Local government 58 provinces and 5 centrally-controlled

municipalities

Total population (person) 97,338,583 (2020)

Climate Southern Vietnam has a tropical climate with 2

seasons (dry and rainy); while Northern

Vietnam (from Hai Van Pass onwards) has a

tropical monsoon climate, with 4 distinct

seasons (spring - summer - autumn - winter).

Main cities Hanoi (Capital), Ho Chi Minh City

(Commercial hub), Can Tho, Hai Phong, Da

Nang

Urbanization Urban population: 37.3% of total population

(2020)

Rate of urbanization: 2.98% annual rate of

change (2015-2020)

GDP (Nominal GDP) (2020) USD 271.2 billion

HOW TO EXPORT GUIDE: VIETNAM

16 | Page

GDP - composition, by sector (2020) Agriculture: 13.6%

Industry: 36.6%

Services: 38.7%

Labor force 56.5 million (2020)

Major export partners (2020) US, China, European Union (EU), ASEAN,

Japan, South Korea

Major import partners (2020) China, South Korea, ASEAN, Japan, Taiwan,

EU

Main exports (2020) Consumer electronics, machinery and

mechanical appliances, garments and

footwears

Main Agricultural products for 2020

exportation

Rice, coffee, rubber, tea, pepper, soybeans,

cashews, sugar cane, peanuts, bananas, pork,

poultry, seafood

Main Agricultural products for 2020

importation

Animal feed, Corn, Vegetables, Wheat,

Soybeans

Main imports (2020) Electronics, fuels, fabrics, plastics, chemical

products

Major sources of FDI Singapore, China, Taiwan, HongKong, South

Korea, Japan

Source: CEIC, WorldBank IMF World Economic Outlook Database (April 2021), Knoema,

GSO Vietnam

Data aggregated by TBO

HOW TO EXPORT GUIDE: VIETNAM

17 | Page

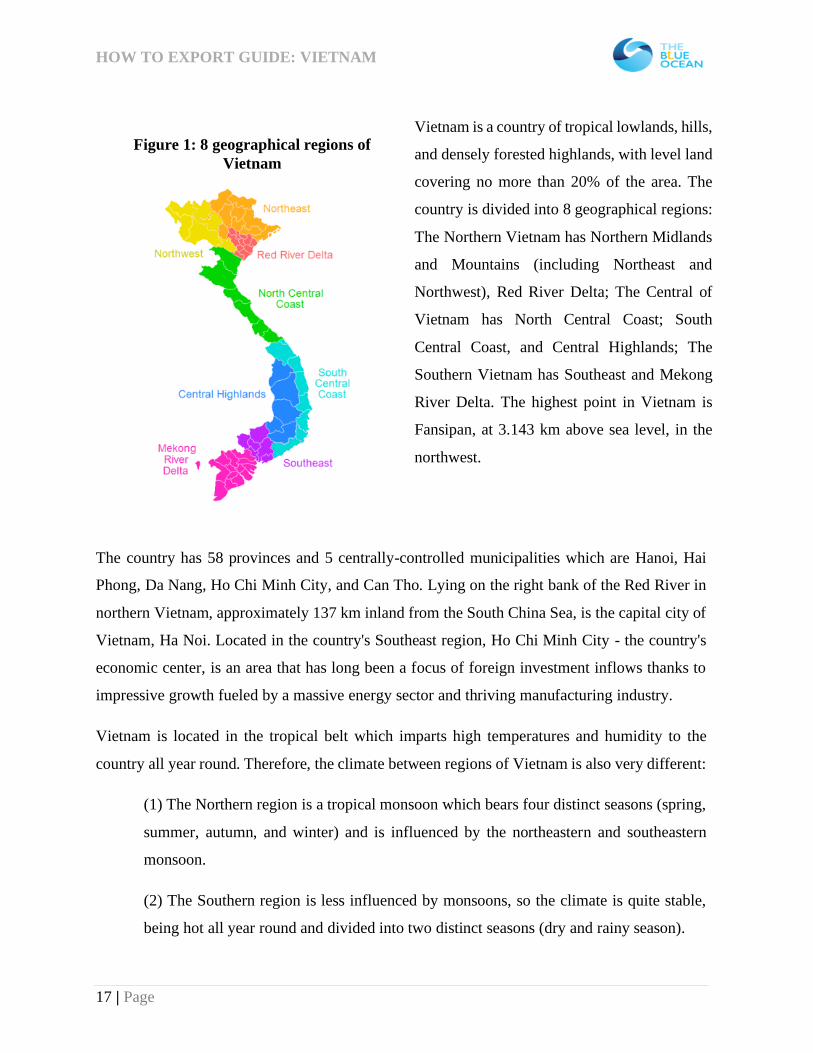

Figure 1: 8 geographical regions of

Vietnam

Vietnam is a country of tropical lowlands, hills,

and densely forested highlands, with level land

covering no more than 20% of the area. The

country is divided into 8 geographical regions:

The Northern Vietnam has Northern Midlands

and Mountains (including Northeast and

Northwest), Red River Delta; The Central of

Vietnam has North Central Coast; South

Central Coast, and Central Highlands; The

Southern Vietnam has Southeast and Mekong

River Delta. The highest point in Vietnam is

Fansipan, at 3.143 km above sea level, in the

northwest.

The country has 58 provinces and 5 centrally-controlled municipalities which are Hanoi, Hai

Phong, Da Nang, Ho Chi Minh City, and Can Tho. Lying on the right bank of the Red River in

northern Vietnam, approximately 137 km inland from the South China Sea, is the capital city of

Vietnam, Ha Noi. Located in the country's Southeast region, Ho Chi Minh City - the country's

economic center, is an area that has long been a focus of foreign investment inflows thanks to

impressive growth fueled by a massive energy sector and thriving manufacturing industry.

Vietnam is located in the tropical belt which imparts high temperatures and humidity to the

country all year round. Therefore, the climate between regions of Vietnam is also very different:

(1) The Northern region is a tropical monsoon which bears four distinct seasons (spring,

summer, autumn, and winter) and is influenced by the northeastern and southeastern

monsoon.

(2) The Southern region is less influenced by monsoons, so the climate is quite stable,

being hot all year round and divided into two distinct seasons (dry and rainy season).

HOW TO EXPORT GUIDE: VIETNAM

18 | Page

(3) The Central of Vietnam is surrounded by mountain ranges stretching from the west

to the east. For this position, the climate in Central Vietnam is harsher than that in

Northern Vietnam and Southern Vietnam. In winter the whole area is affected by cold

weather with rain. This is different from the dry weather in the Northern region. Another

characteristic feature of the central climate is the southwest monsoon (also known as Lao

wind). In summer, the southwest monsoon blows up, causing hot and dry weather. During

this time, the daily temperature can reach over 40 degrees Celsius while the air humidity

is very low.

The average temperature in Vietnam ranges from 21ºC to 27ºC and increases gradually from

north to south. In the summer, the average temperature is 25ºC (Hanoi 23ºC, Hue 25ºC, Ho Chi

Minh City 26ºC). Regarding winter in the North, the lowest temperature occurs in December and

January, at about 5ºC. In the northern mountainous areas (Sa Pa, Tam Dao, Hoang Lien Son)

temperatures can drop to 0ºC, with snowfall.

Vietnam absorbs large amounts of solar radiation with the amount of sunny time ranging from

1,400 to 3,000 hours per year. Humidity is approximately 80% or even increases to above 90%

in the rainy season and drizzly period.

The total annual rainfall of Vietnam is about 700 - 5,000mm which often falls into the range of

1,400 - 2,400mm. The monthly rainfall is unevenly distributed, mainly focusing on the rainy

season. In the North, the rainy season usually starts in April and ends in mid-October. In the

South, the rainy season lasts from early May to the end of November. Each year, particularly

from July to November, there is an average of 5-7 storms hitting Vietnam coastal areas, which

affect the lives and assets of Vietnamese people as well as their economic activities.

Although many westerners still imagine Vietnam through the lens of war, it is in reality a country

filled with captivating natural beauty and tranquil village life. Vietnam’s highlands and rainforest

regions, far from being devastated, continue to yield new species and team with exotic wildlife.

Its islands and beaches are among the finest in all of Southeast Asia. Those beautiful landscapes

make Vietnam an attractive destination to visit among Southeast Asian countries.

HOW TO EXPORT GUIDE: VIETNAM

19 | Page

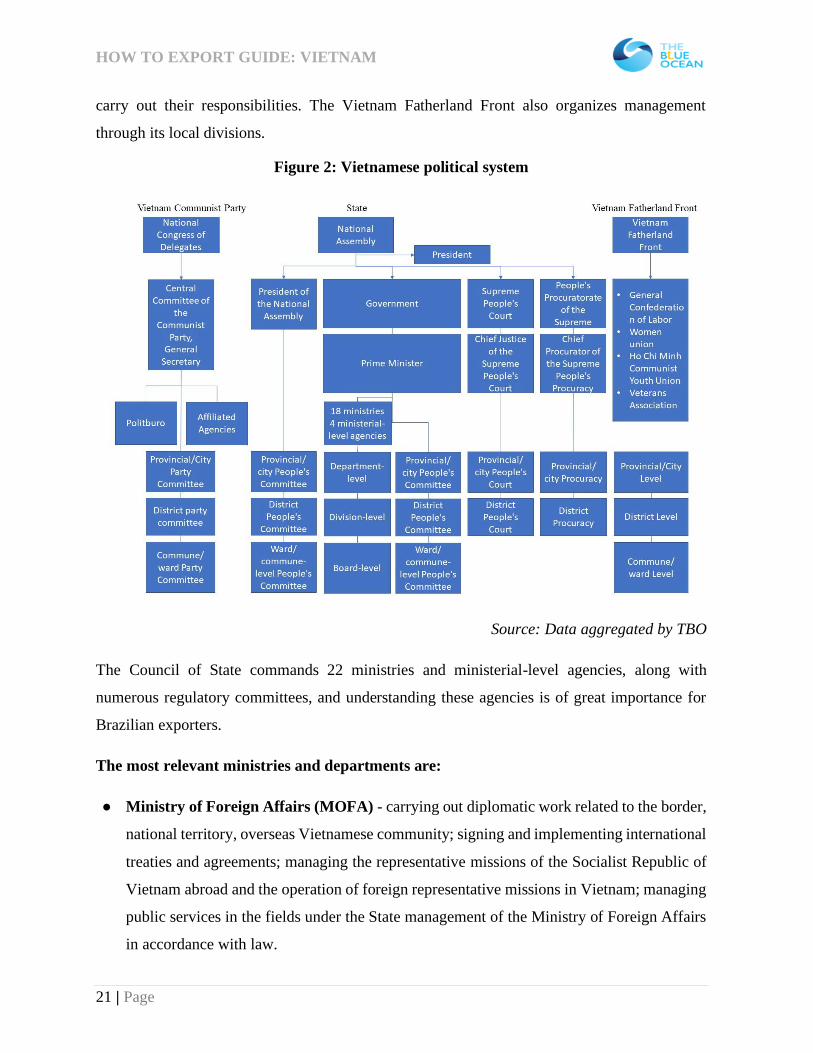

1.1.2. The government organization

The political structure of Vietnam consists of three main pillars:

The Vietnam Communist Party

Vietnam is a socialist country under the leadership of the Vietnam Communist Party. The Party

holds a National congress every five years to outline the country's overall direction and future

course as well as to formalize policies.

The most powerful body is the National Congress of Delegates. The National Congress of

Deputies is held every 5 years, during which the Party Central Committee will be elected and

the Central Committee will continue to elect the Politburo and General Secretary.

The Party Central Committee is responsible for organizing and directing the implementation of

the Political Platform, the Party Charter, and resolutions of the National Congress of Deputies;

deciding on guidelines and policies on domestic and foreign affairs, social work and party

building work; preparing the National Congress of Deputies for the next term, the Extraordinary

National Congress of Deputies (if any).

The General Secretary is the head of the Party Central Committee, presides over the work of the

Party Central Committee, the Politburo, the Secretariat and has other powers according to the

Party's regulations.

The Politburo's responsibilities are specified in Clause 2, Article 17 of the Party's Charter,

specifically as follows: "The Politburo leads, inspects and supervises the implementation of

resolutions of the National Congress, resolutions of the Central Executive Committee; decides

on matters on guidelines, policies, organization and personnel; decides to convene and prepare

the contents of meetings of the Central Committee; reports to the meeting of the Central

Committee or at the request of the Central Committee."

Under the management of the National Congress of Delegates is the Party Committee at the

provincial/city, district, commune/ward levels.

State – includes the National Assembly, the President, the Government, the Supreme People's

Court and the Supreme People's Procuracy.

HOW TO EXPORT GUIDE: VIETNAM

20 | Page

The National Assembly, which includes 498 members and is open to non-Party members, is the

supreme organ of state and the only body with constitutional and legislative power. The President

and the Prime Minister are elected by the National Assembly.

According to the Constitution of the Socialist Republic of Vietnam 2013, the President is the

Head of State and shall represent the Socialist Republic of Vietnam internally and externally.

The current President has been Nguyen Xuan Phuc since July 2021 and Secretary General has

been Nguyen Phu Trong since 23 October 2018.

The Government is the highest state administrative organ of the Socialist Republic of Vietnam,

exercising the executive power. The Prime Minister is the head of the Government. Below are

the Deputy Prime Ministers, the Ministers, and the Heads of ministerial-level agencies. The

current Prime Minister Pham Minh Chinh has served since July 2021. The Government manages

the country through the People's Committees at all levels. Ministers and Heads of ministerial-

level agencies perform their duties through their respective departments, divisions, and boards

corresponding to the province/city, district, commune/ward.

The Supreme People's Court, the local People's Courts established by law, are the judicial organs

of the Socialist Republic of Vietnam. Under special circumstances, the National Assembly may

decide to set up a Special Tribunal. At the grassroots, appropriate popular organizations shall be

set up to deal with minor offenses and disputes among the people according to the provisions of

the law.

The Supreme People's Procuracy supervises and controls obedience to the law by Ministries,

organ of ministerial rank, other organs under the Government, local organs of power, economic

bodies, social organizations, people's and armed units and citizens. It exercises the right to

initiate public prosecution, ensures a serious and uniform implementation of the law.

Vietnam Fatherland Front

The Vietnam Fatherland Front is an organization of political alliances which are the Ho Chi

Minh Communist Youth Union, the Labor Confederation, the Vietnam Women's Union, the

Vietnam Farmers' Union, Veterans Association, ... These organizations have local branches to

HOW TO EXPORT GUIDE: VIETNAM

21 | Page

carry out their responsibilities. The Vietnam Fatherland Front also organizes management

through its local divisions.

Figure 2: Vietnamese political system

Source: Data aggregated by TBO

The Council of State commands 22 ministries and ministerial-level agencies, along with

numerous regulatory committees, and understanding these agencies is of great importance for

Brazilian exporters.

The most relevant ministries and departments are:

● Ministry of Foreign Affairs (MOFA) - carrying out diplomatic work related to the border,

national territory, overseas Vietnamese community; signing and implementing international

treaties and agreements; managing the representative missions of the Socialist Republic of

Vietnam abroad and the operation of foreign representative missions in Vietnam; managing

public services in the fields under the State management of the Ministry of Foreign Affairs

in accordance with law.

HOW TO EXPORT GUIDE: VIETNAM

22 | Page

● Ministry of Industry and Trade (MOIT) - performing the function of State management

of industry, commerce and domestic commerce; import and export, border trade activities;

development of foreign markets; market management; trade promotion commercial

services; international economic integration; competition, consumer protection, trade

defense; public services in sectors and fields under the ministry's State management.

● Ministry of Agriculture and Rural Development (MARD)- performing the function of

State management in the following sectors and fields: Agriculture, forestry, salt production,

fisheries, irrigation, natural disaster prevention and control, rural development; performing

State management of public services in the branches and domains under the management of

the ministry in accordance with law; carrying out international cooperation and international

economic integration in the branches and domains under the ministry's State management

in accordance with law.

● General Department of Customs (GDC) - carrying out the inspection and supervision of

goods and means of transport; preventing and combating smuggling and illegal cross-border

transportation of goods; organizing the implementation of the tax law on imported and

exported goods; making statistics of exported and imported goods; proposing policies and

measures for State management of customs over export, import, exit, entry and transit

activities and tax policies for exported and imported goods.

● Agency of Food Safety (AFS) is a specialized department under the Ministry of Health,

performing the function of advising and assisting the Minister of Health in State

management and organizing law enforcement in the field of food safety under the

responsibility of the Ministry of Health as assigned nationwide.

● The State Bank of Vietnam (SBV) - acting as the Central Bank of the country, having the

same function as other central banks in countries around the world, influencing the entire

economy through the financial system.

1.1.3. The Vietnamese people

Vietnam today is experiencing rapid demographic and social change. The population reached

97.3 million in 2020 (up from about 60 million in 1986) and is expected to expand to 120 million

people by 2050. According to the 2019 Population Census Report, there was 55.5% of the

population in Vietnam under 35 years of age, with a life expectancy of 76 years, the highest

HOW TO EXPORT GUIDE: VIETNAM

23 | Page

among countries at similar income levels. Vietnam enjoys what is known as the “golden

population structure”, which means for every two people or more working, there is only one

dependent person. This demographic bonus provides Vietnam with a unique socio-economic

development opportunity to take advantage of the young labor force and push its economic

growth. And Vietnam’s emerging middle class, currently accounting for 13% of the population,

is expected to reach 26% by 2026. (Source: Worldbank)

Chart 1: Vietnam population pyramid by age in 2009 and 2019 (%)

Source: GSO Vietnam

Although witnessing a golden population period, Brazilian exporters should also pay attention

to the aging of Vietnam's population. With birth rates dropping and life expectancy rising,

Vietnam is among the world's most rapidly aging societies. The aging index in 2019 was 48.8%,

an increase of 13.3 percentage points compared to 2009. This shows that in the coming time, the

consumption trend of Vietnamese people will also change significantly. However, aging also

presents economic opportunities, as demographic shifts result in changing consumption patterns,

with services associated with the elderly offering avenues for market expansion. Observing this

point carefully will help Brazilian exporters planning well when entering Vietnam.

Health outcomes have improved in tandem with rising living standards. According to the World

Health Organization (WHO), in 2020, 90.85% of the population was covered under Social health

insurance - which is the main public financing method for healthcare in Vietnam. This is a

HOW TO EXPORT GUIDE: VIETNAM

24 | Page

remarkable number when compared to 2015 - when the revised Law on Health Insurance took

effect, only 76.5% of the population was covered under Social health insurance. The COVID-19

outbreak has proven that health is a priority for most Vietnamese. During Covid pandemic in

2020, many pharmaceutical companies registered positive results. Vietnam’s largest

pharmaceutical firm, DHG Pharmaceutical Joint Stock Company, had a USD 5 million profit,

which represented a 31% year-on-year increase. (Source: Worldbank)

Language and Religion

The national language is Vietnamese, which is widely spoken throughout the country. In 2018,

more than 95% of the Vietnamese population aged 15 and older was literate. English is the most

popular foreign language and is commonly used in major urban areas. English study is obligatory

in most schools. Other common foreign languages are French, Chinese, and Japanese. Vietnam’s

population practices a variety of religions. These include religions based on popular beliefs,

religions brought to Vietnam from other countries, and several indigenous religious groups.

Buddhism is the largest of the major world religions in Vietnam, followed by Protestantism,

Catholicism, Caodaism, Hoahaoism and others.

The Vietnamese living in the territory of Vietnam today are mainly Kinh people (87%) and 54

ethnic minority communities. The Kinh people are not a homogeneous ethnic community in

origin, but rather a collection of dozens of ethnic groups that have been assimilated since ancient

times of three major communities, but today all share a common identity.

Education and training

According to the results of the EPI survey conducted annually by EF, a multinational language

training company, which interviewed over 910,000 adults in 88 countries and territories that did

not use English as a native language, Vietnamese is in the group of moderately proficient English

users whose EPI reached 53.12/100, ranked 7/21 in Asia and 41/88 in the world.

The Human Development Index (HDI) of Vietnam has continuously improved, making Vietnam

belong to the world's group of countries with high average human development. Between 1990

and 2019, Viet Nam’s HDI value increased from 0.483 to 0.704, an increase of 45.8%.

HOW TO EXPORT GUIDE: VIETNAM

25 | Page

Table 2: Human Development Index of Vietnam

Indicators 2016 2017 2018 2019

Human Development Index (HDI) (Value) 0.693 0.696 0.70 0.704

Source: UNDP Report 2020

1.1.4. Transformation of Vietnam

Vietnam after the war from 1975 to 1986

When the Americans left in 1975 and Vietnam was shut off from trade with many Western

nations, goods stopped flowing into the country. Many Vietnamese have compensated by

purchasing goods on the black market (the informal, unregulated, and illegal economy).

Close to 80% of the Vietnamese population lived in rural areas, primarily in small villages.

American bombing during the Vietnam War destroyed many roads, bridges, rails, and ports, and

the country continued to struggle with modern transportation. The poor condition of the

railroads, ports, and roads continued to hamper Vietnam's ability to increase industrial

productivity.

Motorbikes were a popular means of transportation for successful Vietnamese. Most families

used bicycles, and traveled longer distances by bus, ferry, or boat.

35 years of Renovation - Doi Moi (from 1986 to now)

The economic and political reform policies, launched in Vietnam in 1986 known as Doi Moi,

translated literally as "Renovation", have spurred rapid economic growth, transforming what was

then one of the world’s poorest nations into a lower-middle-income country. Vietnam now is

one of the most dynamic emerging countries in the East Asia region. Between 2002 and 2018,

GDP per capita increased by 2.7 times, which then reached USD 2,785 in 2020, and over 45

million people were lifted out of poverty. Poverty rates declined sharply from over 70% to below

6% (USD 3.2/day PPP). Over the past 35 years, the provision of basic services has improved

significantly. Access of households to infrastructure services has increased dramatically.

Vietnam’s energy sector is among the most noticeable success stories in the developing world.

HOW TO EXPORT GUIDE: VIETNAM

26 | Page

Power losses in transmission and distribution were at or close to best-practice international

standards, and rates of consumers' access to electricity were almost 100% (World Bank 2019).

Rural household electrification increased from below 50% in 1990 to almost 100% today.

However, Vietnam’s rapid growth and industrialization have had detrimental impacts on the

environment and natural assets. Electricity consumption has tripled over the past decade,

growing faster than output. Given the increasing reliance of fossil fuels, the power sector itself

accounts for nearly two-thirds of the country’s greenhouse gas emissions. There is an urgent

need to accelerate the clean energy transition. Over the past two decades, Vietnam has emerged

as the fastest growing per-capita greenhouse gas emitters in the world – growing at about 5%

annually. Demand for water continues to increase, while water productivity is low, about 12%

of global benchmarks. Unsustainable exploitation of natural assets such as sand, fisheries, and

timber could negatively affect prospects for long-term growth. Compounding the problem is the

reality that much of Vietnam’s population and economy is highly vulnerable to climate impacts.

Urbanization and substantial economic and population growth are causing rapidly increasing

waste management and pollution challenges. Waste generation in Vietnam is expected to double

in less than 15 years. Linked to this is the issue of marine plastics. 90% of global marine plastic

pollution is estimated to come from just 10 in-land rivers, and the Mekong River is one of them.

Vietnam is among the 10 countries worldwide that are most affected by air pollution. Besides,

water pollution is also one of the top concerns in Vietnam, and it causes high costs on the

productivity of critical sectors and human health.

The government is working to lower the environmental footprint of the country’s growth and

effectively mitigate and adapt to climate change. Key strategies and plans to stimulate green

growth and sustainable use of its natural assets are in place.

Given its deep integration with the global economy, the Vietnamese economy has been hit by

the ongoing COVID-19 pandemic but has shown remarkable resilience. GDP grew by 2.9% in

2020. It was one of the few countries in the world to do so. However, the crisis also left a lasting

impact on households, with 45% of households reporting lower household income in January

2021 than in January 2020. Vietnam’s economy is expected to have a better recovery and grow

3.8% in 2021 in the context that COVID-19 still impacts worldwide.

HOW TO EXPORT GUIDE: VIETNAM

27 | Page

1.1.5. The opening of Vietnam

Since the late 1970s and mid-1980s, all socialist countries in general and Vietnam especially

have carried out the reforming, opening up and implemented policies that are suitable for the

development trend of humankind. Thus, has achieved many significant achievements in all fields

of politics, economy, culture, society, national defense, and other fields.

HOW TO EXPORT GUIDE: VIETNAM

28 | Page

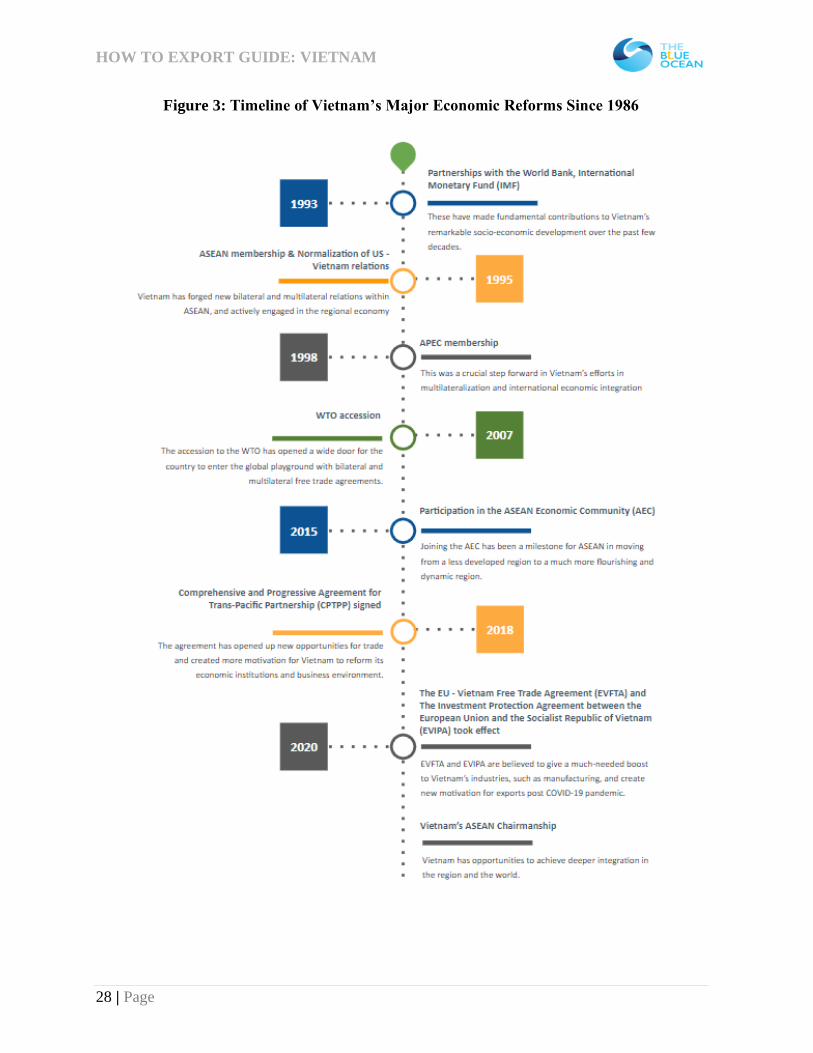

Figure 3: Timeline of Vietnam’s Major Economic Reforms Since 1986

HOW TO EXPORT GUIDE: VIETNAM

29 | Page

1.2. Vietnamese Foreign Policy

Vietnam is today a responsible member of the international community, it proved through

Vietnam’s proactiveness in contributing to global organizations. Vietnamese foreign policy is

aimed primarily at promoting economic development in the country. Vietnam today has

established diplomatic relations with nearly 189 countries, including all world great powers.

Vietnam has started trade relations with 221 countries and territories, signed trade agreements

with 76 countries and Most Favored Nation status with 72 countries and territories. Apart from

strengthening bilateral relations, Vietnam also continuously improves its relations with

international and regional organizations such as the United Nations, European Union, ASEAN,

APEC, and ASEM, thus making positive contributions to the activities of these organizations in

accordance with Vietnam's national strengths and interests.

1.2.1. Vietnam's External Relations

Vietnam is a country with a diverse international relationship which enhances Vietnam’s

international prestige.

In terms of foreign policy, Vietnam always aims to become a friendly and reliable partner of all

countries in the international community, to take part in international and regional cooperation

processes. The Vietnamese government has consistently implemented the foreign policy line of

independence, self-reliance, peace, cooperation and development, the foreign policy of openness

and diversification and multilateralization of international relations. Vietnam works toward

proactively and actively engaging in international economic integration while expanding

international cooperation in other fields.

In the current Covid context worldwide, Vietnam’s authorities have focused on the core line of

Foreign Policy, and taken flexible actions to overcome hard times:

- Firstly, Vietnam’s cooperation with other countries, especially with neighboring

countries and important partners, has been continuously strengthened and promoted.

Despite facing difficulties caused by the pandemic, Vietnam’s authorities still promoted

HOW TO EXPORT GUIDE: VIETNAM

30 | Page

many diplomatic exchanges and cooperation with other countries, especially online

exchanges at all levels.

- Secondly, the year 2020 made an important mark in promoting and raising the level of

Vietnam's multilateral foreign policy. Vietnam’s authorities took success on many

international responsibilities, including the 2020 ASEAN Chair and 41st General

Assembly of the ASEAN Inter-Parliamentary Assembly (AIPA-41), Non-Permanent

Member of the United Nations Security Council in the first year of the term 2020-2021.

- Thirdly, Vietnam’s international economic integration has achieved breakthrough

progress, creating an additional driving force for rapid and sustainable growth of the

economy. The effective implementation of many FTAs makes a significant contribution

to Vietnam’s achievement in maintaining one of the highest growth rates in the world. In

2020, Vietnam's export value increased by 6.5% compared to 2019. Vietnam has become

one of the potential destinations for investment in the world.

- Fourthly, the work on the border and territory demarcation had many positive results.

Vietnam and Cambodia exchanged ratification documents, including the approval of two

2019 Supplementary Treaty, and the Protocol on land border demarcation and marker

planting, recognizing 84% of the demarcation’s achievement. Vietnam and China

celebrated the 20th anniversary of Land Border Treaty signing and 10 years of

implementing 3 legal documents on land borders, which are Protocol on border

demarcation and marker planting, the Agreement on border management regulations, and

the Agreement on border gates and land border gate management regulations. These were

achievements of great significance, contributing to building a border line of peace,

friendship, cooperation, and development with neighboring countries.

- Fifthly, the work of cultural statecraft and foreign information were actively

implemented, especially the use of digital technology to promote Vietnam to the world

via many innovative products and ways.

The Vietnam Communist Party National Congress, held once every five years, is the biggest

exercise of collective policy-making, including foreign policy, in Vietnam. The latest national

congress - The 13th National party congress was held in Hanoi from January 25th to Feb 1st,

2021.

HOW TO EXPORT GUIDE: VIETNAM

31 | Page

After the 13th Congress, Vietnamese authorities have planned and unified the next priorities in

later years. According to the new Minister of Foreign Affairs Bui Thanh Son, Vietnam will

continue to have a foreign policy of independence, sovereignty, peace, cooperation and

development, diversification and multi-lateralization, proactive and active in-depth and

comprehensive international integration. Vietnam stands ready to be a trusted friend and partner

to all countries in the international community, with the spirit of cooperation, respect for

international law, fairness and win-win policies.

In the next few years, the Party’s foreign policy could be materialized into four priorities, as

below:

● Before all else, Vietnam focuses on deepening the relations with all important partners

of the country, especially neighboring countries, countries with which Vietnam’s

authorities have strategic partnership and comprehensive partnership, and traditional

friends. This priority is consistent with the government’s foreign policy so far.

● Next in order, Vietnamese authorities will focus on national development, also keep in

mind that political and cultural diplomacy, or overseas Vietnamese policies all serve the

goal of contributing to national development. Economic diplomacy will naturally be a

key pillar, attracting foreign resources to either add to or complement domestic resources

and factors. On the authority of this statement, Brazilian companies have so many

favorable conditions when doing business in Vietnam.

● Furthermore, Vietnam continues to proactively and actively participate in multilateral

forums and organizations, which will allow authorities to take part in the shaping and

development of rules. Also, as a responsible member of the international community,

Vietnam’s authorities would propose initiatives to help further promote the standing of

the country.

● In closing, the government considers citizen protection work a key task to maintain the

connection between overseas and the homeland. This is also the State’s policy towards

the Vietnamese overseas community. Vietnamese people have a high sense of national

pride, this is the noticeable characteristic that foreign investors should be aware of when

doing business with Vietnamese people.

HOW TO EXPORT GUIDE: VIETNAM

32 | Page

1.2.2. General aspects of Vietnam's international policy

Vietnam started focusing on breaking the embargo of Western countries, from after being unified

in 1975 up to 1990. The country at that time not only maintained relations with countries in the

socialist bloc but also gradually expanded economic cooperation to the outside. Typical events

may refer to as Vietnam opened an ODA with Japan, established diplomatic relations with many

countries, normalized and established relations with international economic organizations such

as the IMF, World Bank. In February 1994, the US announced its decision to lift the trade

embargo against Vietnam.

The year 1995 is considered an important milestone in the country's international integration

process. In July 1995, Vietnam officially became the seventh member of ASEAN. Joining

ASEAN was a historic and strategic decision, which created great benefits for Vietnam and made

an important contribution to the development of the bloc including expanding ASEAN into a 10-

nation bloc. Also in July 1995, the US and Vietnam announced their decision to normalize

diplomatic relations between the two countries. And in the same year, Vietnam signed a

Framework Agreement on Cooperation with the European Community in Belgium. Thus, in

1995, Vietnam simultaneously carried out three major external events, which opened the stage

of international integration.

In 2000, Vietnam and the US signed a Bilateral Trade Agreement (BTA) and had the first official

visit of the 42nd President of the United States - Mr. Bill Clinton.

In 2004, Vietnam was the host country of the Asia-Europe Meeting (ASEM) after participating

as a founding member for 8 years (1996). In 2006, Vietnam hosted the APEC Summit Week,

also 8 years after joining (1998). In 2007, Vietnam joined the World Trade Organization (WTO).

The years 2006, 2007 marked a higher stage of Vietnam's integration with the world.

International integration contributes to breaking the siege, embargo, and enhancing Vietnam's

position in the international arena. This is reflected in the fact that Vietnam has established

diplomatic, economic - trade relations with most countries, regions, and territories and has been

a member of many international organizations in the region and the world.

HOW TO EXPORT GUIDE: VIETNAM

33 | Page

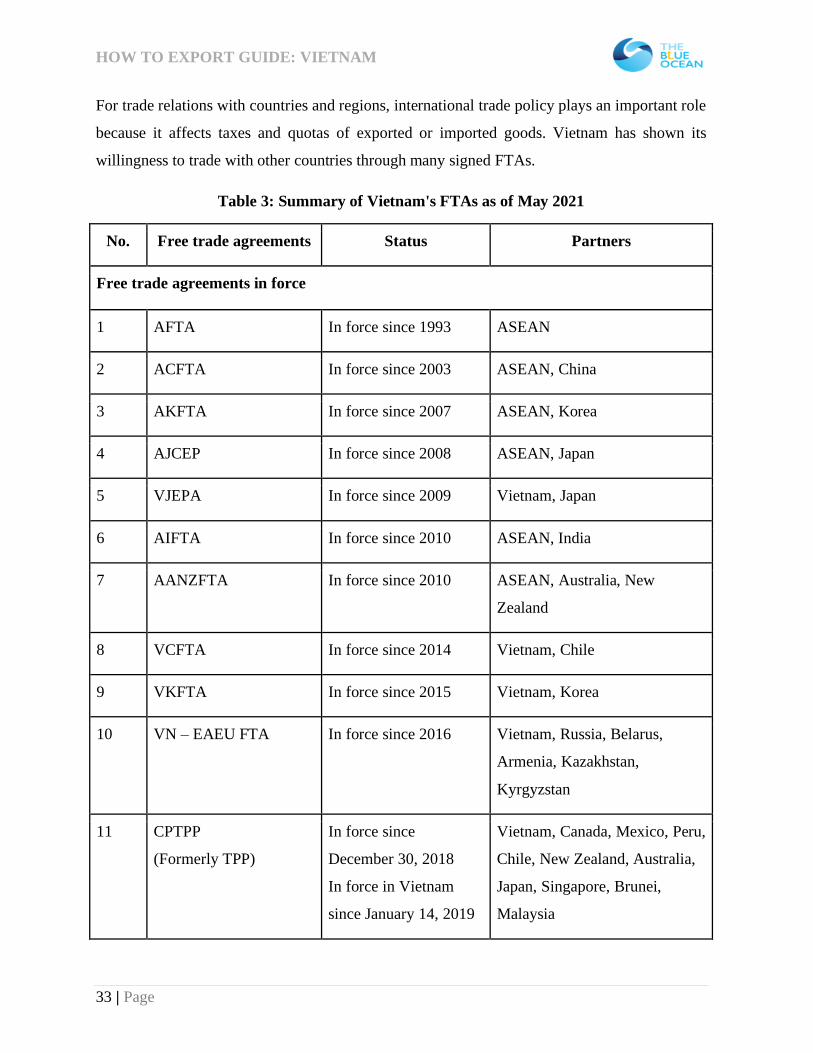

For trade relations with countries and regions, international trade policy plays an important role

because it affects taxes and quotas of exported or imported goods. Vietnam has shown its

willingness to trade with other countries through many signed FTAs.

Table 3: Summary of Vietnam's FTAs as of May 2021

No. Free trade agreements Status Partners

Free trade agreements in force

1 AFTA In force since 1993 ASEAN

2 ACFTA In force since 2003 ASEAN, China

3 AKFTA In force since 2007 ASEAN, Korea

4 AJCEP In force since 2008 ASEAN, Japan

5 VJEPA In force since 2009 Vietnam, Japan

6 AIFTA In force since 2010 ASEAN, India

7 AANZFTA In force since 2010 ASEAN, Australia, New

Zealand

8 VCFTA In force since 2014 Vietnam, Chile

9 VKFTA In force since 2015 Vietnam, Korea

10 VN – EAEU FTA In force since 2016 Vietnam, Russia, Belarus,

Armenia, Kazakhstan,

Kyrgyzstan

11 CPTPP

(Formerly TPP)

In force since

December 30, 2018

In force in Vietnam

since January 14, 2019

Vietnam, Canada, Mexico, Peru,

Chile, New Zealand, Australia,

Japan, Singapore, Brunei,

Malaysia

HOW TO EXPORT GUIDE: VIETNAM

34 | Page

12

AHKFTA

In force in Hong Kong

(China), Laos,

Myanmar, Thailand,

Singapore, and Vietnam

since June 11, 2019

ASEAN, Hong Kong (China)

13 EVFTA In force since August 1,

2020

Vietnam, EU (27 members)

14 UKVFTA In force since May 1,

2021

Vietnam, United Kingdom

FTA has not been ratified, coming into effect soon

15 RCEP Signed in November

15, 2020

ASEAN, China, Korea, Japan,

Australia, New Zealand

Free trade agreements in negotiation

16 Vietnam – EFTA FTA Commencement of

negotiations in May

2012

Vietnam, EFTA (Switzerland,

Norway, Iceland, Liechtenstein)

17 Vietnam - Israel FTA Commencement of

negotiations in

December 2015

Vietnam, Israel

Source: Vietnam Chamber of Commerce and Industry

Over the past time, Vietnam has joined many regional and bilateral Free Trade Agreements

(FTAs), such as signing FTAs between ASEAN and China (2004), ASEAN - Korea (2006),

ASEAN - Japan (2008), ASEAN - India (2010), ASEAN - Australia & New Zealand (2010).

Among them, the Comprehensive Economic Partnership Agreement with Japan has eliminated

tariffs on 1,261 lines of agricultural products from Vietnam by 2019. By the end of the roadmap

by 2026, Japan will have been committing to eliminating tariffs on 96.45% of the total tariff lines

HOW TO EXPORT GUIDE: VIETNAM

35 | Page

for Vietnamese goods (mainly agricultural products, seafood, textiles, footwear, and wooden

furniture, electronic components…).

Vietnam signed a bilateral FTA between Vietnam and Chile in 2011. This is Vietnam's first FTA

with a Latin - American country. This FTA includes commitments on goods and goods-related

issues, excluding commitments on services and investment... In terms of Mercosul countries,

Vietnam and this group of countries have shown interest in negotiating an FTA. An exploratory

dialogue on possible negotiations was finalized in 2020 with positive results. Currently, impact

studies and public consultations are ongoing in Mercosul countries on a possible FTA, and the

issue is expected to remain in the group's agenda.

Besides the ASEAN - Korea FTA (AKFTA), Vietnam also signed the Vietnam - Korea Free

Trade Agreement (VKFTA) in 2015, in which Korea gives more incentives in the fields of goods,

services and investment. VKFTA does not replace AKFTA, but both of these FTAs are in effect

and companies can choose to use the FTA which is more beneficial to them.

Free Trade Agreement Vietnam - Eurasian Economic Union (VN-EAEU FTA) which currently

includes the Russian Federation, the Republic of Belarus, the Republic of Kazakhstan, the

Republic of Armenia, and the Kyrgyz Republic, was signed on May 29, 2015 and took effect

from October 5, 2016. Through this agreement, Vietnam and the EAEU would increase the types

of commodities exported to one another market.

The Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP),

formerly known as the Trans-Pacific Partnership (TPP), was officially signed in March 2018 by

11 TPP member countries (excluding the US). The CPTPP was signed on March 8, 2018 in

Santiago, Chile, and officially entered into force on December 30, 2018 for the first group of 6

countries to complete the Agreement ratification procedures including Mexico, Japan,

Singapore, New Zealand, Canada and Australia. For Vietnam, the Agreement took effect on

January 14, 2019.

The EVFTA Agreement took effect on August 1st, 2020. As soon as the Agreement came into

effect, the EU eliminated import taxes on about 85.6% of tariff lines, equivalent to 70.3% of

Vietnam's export turnover to the EU. According to the Agreement, after 7 years from the date of

entry into force, the EU will eliminate import tax on 99.2% of tariff lines, equivalent to 99.7%

HOW TO EXPORT GUIDE: VIETNAM

36 | Page

of Vietnam's export turnover. For the remaining 0.3% of export turnover, the EU will allow a

tariff quota with an import tax within the quota of 0%.

The Free Trade Agreement between Vietnam and the United Kingdom (UKVFTA) was officially

signed in London on December 29, 2020. The Agreement took effect temporarily on January 1,

2021, and officially took effect from May 1, 2021.

The Regional Comprehensive Economic Partnership (RCEP - also known as ASEAN+6) was

signed by ASEAN, and six partners that already have FTAs with ASEAN including China,

Korea, Japan, India, Australia, and New Zealand. RCEP, which was signed on November 15,

2020, is the largest-scale free trade agreement (FTA) that Vietnam has participated in up to now.

RCEP covers 30% of the world's population, accounting for 32% of global GDP. This agreement

has not yet come into force, as it needs to be ratified by at least six ASEAN countries and three

outside the bloc. Just like the recently ratified EVFTA and the CPTPP, the RCEP will reduce

tariffs and set trade rules, and help link supply chains, particularly as governments grapple with

COVID-19 effects. The FTA is expected to cover all aspects of the business including trade,

services, e-commerce, telecommunications, and copyright though negotiations over some

aspects still need to be finalized. Tariffs are expected to be reduced within 20 years.

In addition, Vietnam is still making efforts in the process of negotiating other trade agreements.

The FTA between Vietnam and the EFTA bloc (including 4 countries Switzerland, Norway,

Iceland, Liechtenstein) started negotiations in May 2012. Currently, this FTA is still in the

negotiation process.

Regarding the FTA between Vietnam and Israel (VIFTA) and with the EFTA bloc: The Ministry

of Industry and Trade has coordinated with ministries and sectors to promote negotiations,

especially in key negotiation areas such as trade in goods and services, thereby creating a

favorable basis for promoting the negotiation process.

HOW TO EXPORT GUIDE: VIETNAM

37 | Page

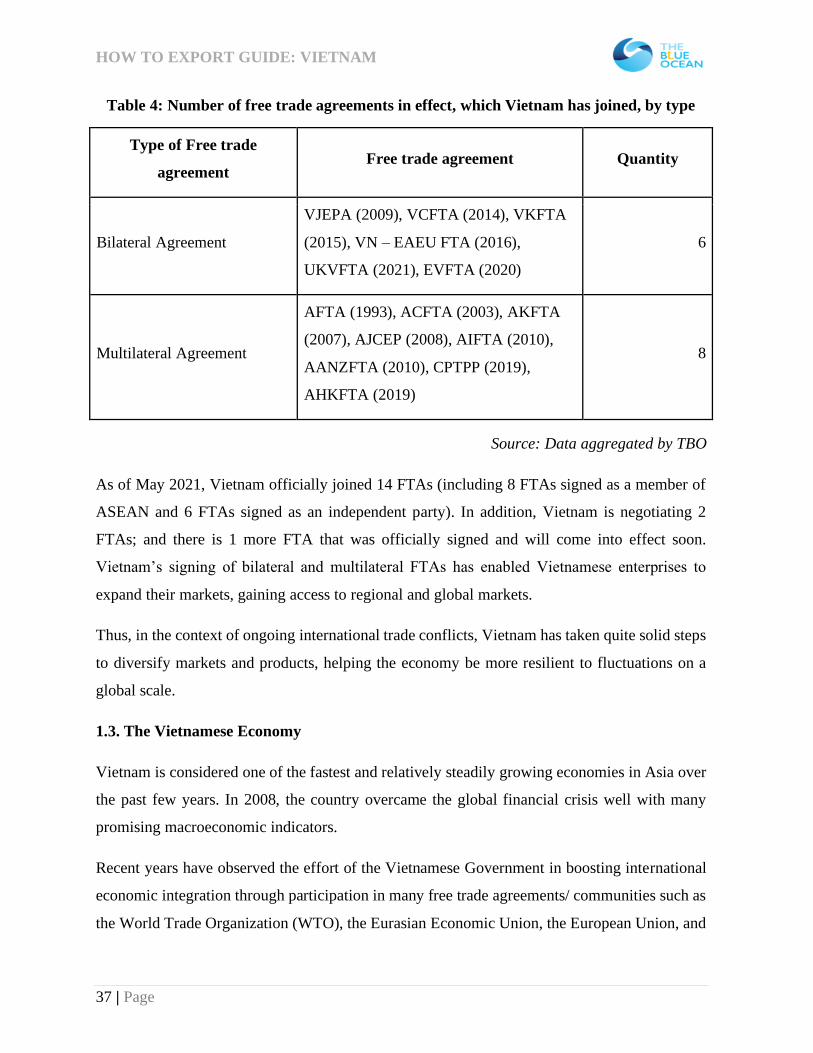

Table 4: Number of free trade agreements in effect, which Vietnam has joined, by type

Type of Free trade

agreement Free trade agreement Quantity

Bilateral Agreement

VJEPA (2009), VCFTA (2014), VKFTA

(2015), VN – EAEU FTA (2016),

UKVFTA (2021), EVFTA (2020)

6

Multilateral Agreement

AFTA (1993), ACFTA (2003), AKFTA

(2007), AJCEP (2008), AIFTA (2010),

AANZFTA (2010), CPTPP (2019),

AHKFTA (2019)

8

Source: Data aggregated by TBO

As of May 2021, Vietnam officially joined 14 FTAs (including 8 FTAs signed as a member of

ASEAN and 6 FTAs signed as an independent party). In addition, Vietnam is negotiating 2

FTAs; and there is 1 more FTA that was officially signed and will come into effect soon.

Vietnam’s signing of bilateral and multilateral FTAs has enabled Vietnamese enterprises to

expand their markets, gaining access to regional and global markets.

Thus, in the context of ongoing international trade conflicts, Vietnam has taken quite solid steps

to diversify markets and products, helping the economy be more resilient to fluctuations on a

global scale.

1.3. The Vietnamese Economy

Vietnam is considered one of the fastest and relatively steadily growing economies in Asia over

the past few years. In 2008, the country overcame the global financial crisis well with many

promising macroeconomic indicators.

Recent years have observed the effort of the Vietnamese Government in boosting international

economic integration through participation in many free trade agreements/ communities such as

the World Trade Organization (WTO), the Eurasian Economic Union, the European Union, and

HOW TO EXPORT GUIDE: VIETNAM

38 | Page

the ASEAN Economic Community (AEC), The EU - Vietnam Free Trade Agreement (EVFTA).

This led to a significantly increasing FDI year on year. With a stable political environment, low

labor and operating costs, as well as promising economic prospects, Vietnam is a dynamic

market and an attractive destination for both foreign and private investors to participate in the

economy.

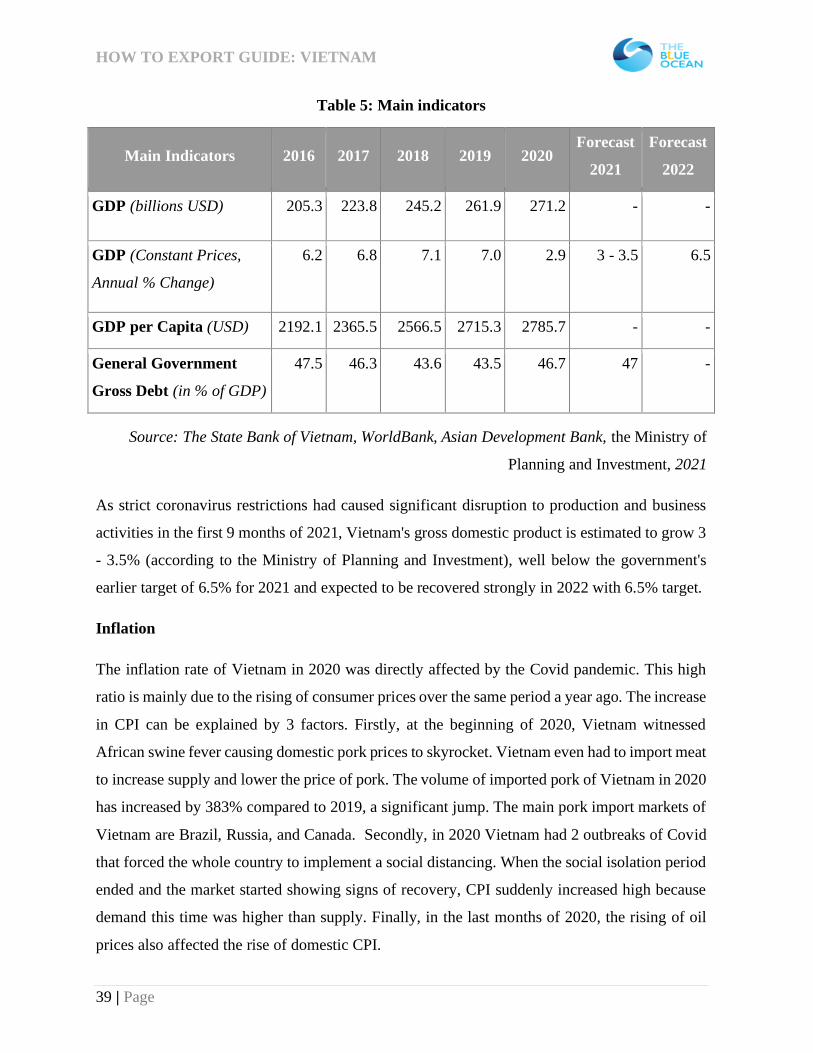

1.3.1. Main Macroeconomic Indicators

GDP

Vietnam’s real GDP achieved an average growth rate of 7.3% from 2005 to 2009 before

declining to 5.3% in 2009. The recovery began in 2012, with GDP growth gradually increasing

and reaching 6% in 2014. Despite the global trade recession and China’s economic growth