How Europe Ended Up Someplace Else Ashoka Mody EuroTragedy: A Drama in Nine Acts New York: Oxford University Press, June 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

How Europe Ended Up Someplace Else

Ashoka Mody

EuroTragedy: A Drama in Nine Acts

New York: Oxford University Press, June 2018

Thesis: monetary union would lead Europe into political union.

Early warnings it would not.

• Nicholas Kaldor, March 1971:

o Single currency would amplify economic divergence, and

o A house “divided against itself cannot stand.”

• Robert Marjolin, crucial catalyst of Treaty of Rome, in the 1970s:

o Political efforts to counteract economic divergence would be

impeded by the sovereignty barrier:

o European leaders “obviously not ready” to give up core

sovereign functions;

o Change required was “too profound.”

A flawed euro, which the French desperately wanted, on German terms.

• Chancellor Helmut Kohl—despite

severe initial misgivings—pushed the

euro, overriding German public’s

deep opposition to giving up the

deutsche mark

• Seeking the Bundestag’s

authorization on April 24, 1998, he

twice said:

• “According to the treaty rules, the

community shall not be liable for the

commitments of the member states

and there are no additional financial

transfers.” Translation: Germany will

not pay the bills of other member

countries.

• Kohl’s mantra: euro would ensure

Europe’s peace.

But there was no conception of what the end goal was

…and, hence, no idea of how Europe would get there.

“If you don’t know where you are

going,

You'll end up someplace else.”

Yogi Berra

The tragedy: the euro inevitably

pushed Europe into a “someplace”

else that was not good.

Kaldor’s ghost stalks:

The euro divides Europe

The great divergence in euro-area incomes and employment.

Per capita incomes

(In thousands of US dollars, corrected

for purchasing power parity)

Unemployment rates

(Percent)

Sources: Conference Board, “Total Economy Database (Adjusted Version),” http://www.conference-

board.org/data/economydatabase/; IMF, World Economic Outlook Database,

https://www.imf.org/external/pubs/ft/weo/2017/01/weodata/index.aspx.

34

36

38

40

42

44

46

48

50

2003 05 07 09 11 13 15

Germany

France

Italy

4

5

6

7

8

9

10

11

12

13

2003 05 07 09 11 13 15

Italy

France

Germany

The euro-area north-south divergence: public debt and youth distress. Public debt Youth unemployment and inactivity

Source: IMF, World Economic Outlook Database; Eurostat (edat_lfse_20). Note: Countries on the left side

correspond to the countries on the right side. The “unemployed” are those who are looking for a job but are unable

to find one; the “inactive” are not looking for a job and neither are they in an educational or training program. The

sum of the unemployed and inactive is known as “neither in employment, education or training” (NEET).

0 50 100 150 200

2017Netherlands 2007

2017Germany 2007

2017Austria 2007

2017Finland 2007

2017Portugal 2007

2017France 2007

2017Spain 2007

2017 Greece 2007

2017 Italy 2007

Public debt as a

percentage of GDP

0 5 10 15 20 25

20162007

20162007

20162007

20162007

20162007

20162007

20162007

20162007

20162007

Percentage of population

15 to 29 years old

Inactive Unemployed

Divergence was predictable, not an accident: southern euro area suffers

from weak governance and institutions, which weaken growth potential:

The euro is cruel on countries with low growth potential.

Source: World Bank, Worldwide Governance Indicator. Note: The overall index presented is an average of

measures of government effectiveness, regulatory quality, rule of law, and control of corruption. Each individual

measure is normally distributed, with a mean of zero, a standard deviation of 1, and an approximate range of –2.5

to 2.5. Larger values indicate better governance.

0,0 0,5 1,0 1,5 2,0 2,5

2015Netherlands 1998

2015Germany 1998

2015Austria 1998

2015Finland 1998

2015Portugal 1998

2015France 1998

2015Spain 1998

2015 Greece 1998

2015 Italy 1998

Better governance

and institutions

Poorer long-term growth prospects a trap: persistently low R&D rates in

the euro-area periphery, hence persistently low growth potential.

(R&D as a percentage of GDP, 2016 versus 1997)

Source: OECD Statistical Database.

Austria

Belgium

DenmarkFinland

France

Germany

GreeceIreland

Italy

Netherlands

Portugal

Spain

Sweden

United Kingdom

United States

0

0,5

1

1,5

2

2,5

3

3,5

0,0 0,5 1,0 1,5 2,0 2,5 3,0 3,5

R&

D/G

DP

rat

io (

per

cent)

in 2

016

R&D/GDP ratio (percent) in 1997

Predictably, German exporters shift their sights away from the euro area.

(Percent of total German exports to the various countries)

Source: IMF Data, http://data.imf.org/regular.aspx?key=61013712.

Undercuts the idea that the euro would promote trade and, hence,

growth.

United States

Italy

Czech Republic,

Hungary, and Poland

0

2

4

6

8

10

12

1999 2007 2016

France

China

Kaldor’s ghost stalks also the eurozone’s

politics

Italians lost trust in Europe: economic wounds left political scars. (Decrease in percentage of respondents who trust the European Union, 2016 relative to 2001)

Source: Standard Eurobarometer survey, available at http://zacat.gesis.org. Note: Respondents answered the

following question: “I would like to ask you a question about how much trust you have in certain institutions. For

each of the following institutions, please tell me if you (Tend to trust it; Tend not to trust it): The European Union.”

The chart presents the change in share of people who said they trusted the EU. For each year, 2001 and 2016,

responses for the two available quarters are averaged.

-40

-35

-30

-25

-20

-15

-10

-5

0

Italy France Germany

“European chancellor” Merkel held eurozone together:

Became polarizing force.

Between 2010 and 2016, Merkel

was de facto European

chancellor, a goal that Kohl had

dreamt of.

Ipso facto, she became a

politically polarizing figure,

dividing Europe.

• In Italy, February 2013 election:

o Rise of the anti-euro Five Star

Movement

o Silvio Berlusconi, whose party also

performed well, asked at his rallies,

“Do you want a government that that

is subject to the diktats of Europe?”

o Pro-European Mario Monti

electorally humiliated.

• In Germany, starting in 2012:

o Breakaway group from Merkel’s

Christian Democratic Party (CDU)

formed Alternative für Deutschland,

initially as an anti-euro party and

then as an anti-immigrant party.

Looking ahead:

The future ain’t what it used to be

For now, Greece has lost its democracy.

• Failure to provide substantial

and upfront debt relief implies

o Large primary surpluses

o Historically hard to

maintain

o Will constrain

government investment

o Keep growth low

• More seriously

o Greek parliament will

mainly rubber-stamp

decisions made in Berlin,

Brussels, and Frankfurt.

The ECB has reached its political limits

ECB tardy in initiating bond purchases:

Euro-area inflation rate began dropping in mid-2013, delivering the

lowflation wound. (Three-month moving average of “core” annual inflation rates, percent)

Source: Eurostat: “HICP—All Items Excluding Energy and Food”; St. Louis Fed, FRED: “Personal Consumption

Expenditures Excluding Food and Energy (Chain-Type Price Index).”

0,6

0,8

1

1,2

1,4

1,6

1,8

2

Jun

2012

Dec

12

Jun

13

Dec

13

Jun

14

Dec

14

Jun

15

Dec

15

Jun

16

Dec

16

Jun

17

Dec

17

Jun

18

United States

Euro Area

The ECB keeps forecasting a rise in inflation:

Inflation remains stubbornly low.

Sources: ECB’s Macroeconomic Projections made in March of the year,

https://www.ecb.europa.eu/pub/projections/html/index.en.html.

Note: 2018 core inflation is the average of months January to September 2018.

0,6

0,8

1,0

1,2

1,4

1,6

1,8

2012 13 14 15 16 17 18 19 20

2013 forecast

2014 forecast

2015 forecast

2016 forecast

2017 forecast

Solid line is

the actual

euro-area

core inflation

2018

forecast

The ECB lacked commitment to bond purchases, even more so than the

Bank of Japan.

Note: Exchange rate for JPY/USD equals 100 on January 4, 2013 (date of the announcement of quantitative easing by the Bank of

Japan) and exchange rate for EUR/USD equals 100 on January 22, 2015 (date of the announcement of quantitative easing by the

ECB).

Source: For USD and Japanese Yen, https://www.investing.com/currencies, for USD and Euro rates ECB,

https://sdw.ecb.europa.eu/quickview.do?SERIES_KEY=120.EXR.D.USD.EUR.SP00.A&periodSortOrder=ASC.

80

90

100

110

120

130

140

150

-100 0 100 200 300 400 500 600 700 800 900 1000 1100 1200 1300 1400

Number of days from the quantitative easing announcement

JPY/USD

EUR/USD

Depreciation relative of the dollar

Start of quantitative easing

January 4, 2013: Bank of Japan

January 22, 2015: ECB

February 1, 2016

July 1, 2016

January 1, 2017 September 15, 2017

October 24, 2017: ECB begins tapering QE

Taper talk

Taper

talk

June 14, 2018: ECB announces

QE end date as end-2018

World trade rather than ECB’s bond purchases moves eurozone growth.

(Annual growth rates, percent; three-quarter moving averages)

Source: For world trade growth data World Trade Monitor, https://www.cpb.nl/en/data; for the industrial

production of Germany, France and Italy Eurostat, code [sts_inpr_m]. Note: The three-month average of growth

over the same three months in the previous year.

-1

0

1

2

3

4

5

6

7

Aug

2015

Nov

15

Feb

16

May

16

Aug

16

Nov

16

Feb

17

May

17

Aug

17

Nov

17

Feb

18

May

18

Aug

18

World trade

Germany industrial production

France industrial production

Italy industrial production

ECB bond purchases in

flow from March 2015, but

unable to raise economic

Italy: theater of EuroTragedy

Italy needed—and needs—the crutch of a depreciating

currency to offset its abysmal productivity growth. The depreciating lira

(Number of liras for one D-mark)

Italian productivity fell relative to German

(annual total factor productivity growth)

US Dollar/Euro exchange rate is back where it

began, 1999-2018

Italian productivity collapsed while even

German fell behind the U.S.

(annual total factor productivity growth)

Source: Top left panel: Banca d'Italia, https://tassidicambio.bancaditalia.it/timeSeries; top right

panel: ECB data warehouse

https://sdw.ecb.europa.eu/quickview.do?SERIES_KEY=120.EXR.D.USD.EUR.SP00.A&period

SortOrder=ASC; bottom left and right panels: The Conference Board, https://www.conference-

board.org/data/economydatabase/index.cfm?id=27762.

0

200

400

600

800

1000

1200

1400

70 74 78 82 86 90 94 981970

0,0

0,5

1,0

1,5

2,0

2,5

1970-79 1980-89 1990-98

Italy Germany

0,8

0,9

1

1,1

1,2

1,3

1,4

1,5

1,6

99 02 05 08 11 14 171999

The euro's

starting

exchange

value

-0,8

-0,6

-0,4

-0,2

0,0

0,2

0,4

0,6

0,8

2008-08 2009-16

Italy Germany United States

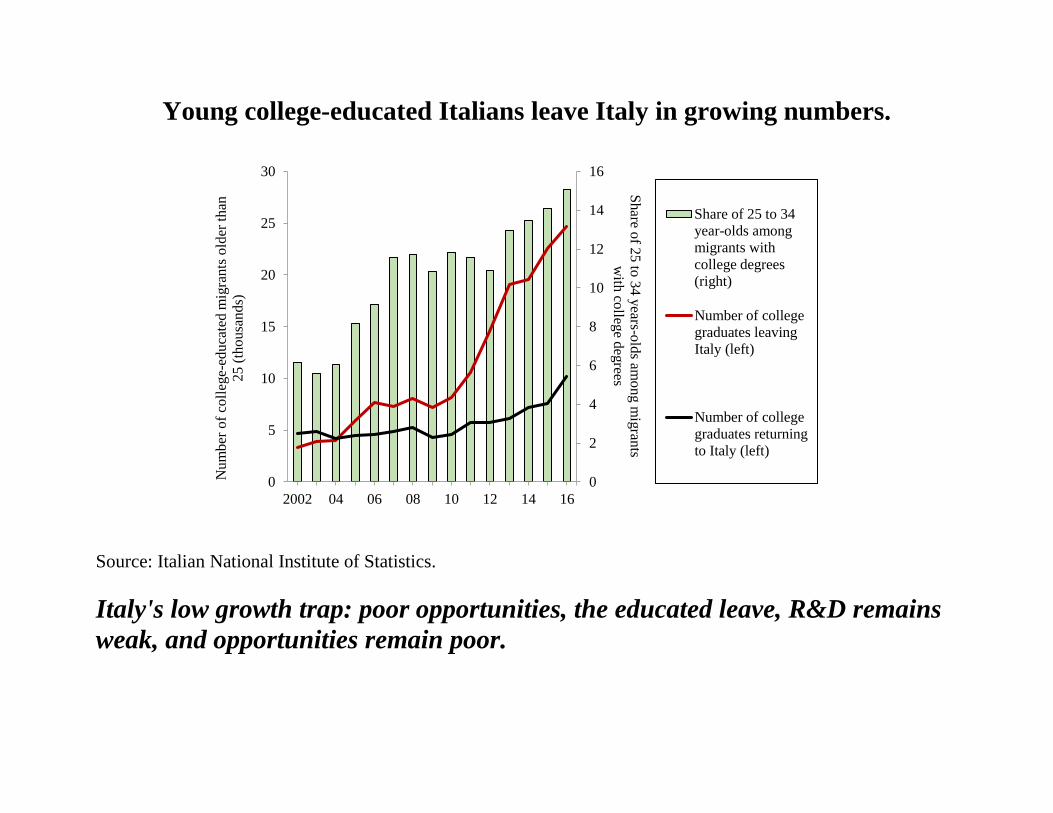

Young college-educated Italians leave Italy in growing numbers.

Source: Italian National Institute of Statistics.

Italy's low growth trap: poor opportunities, the educated leave, R&D remains

weak, and opportunities remain poor.

0

2

4

6

8

10

12

14

16

0

5

10

15

20

25

30

2002 04 06 08 10 12 14 16

Share o

f 25

to 3

4 y

ears-old

s amo

ng m

igran

ts

with

colleg

e deg

rees

Num

ber

of

coll

ege-

educa

ted m

igra

nts

old

er t

han

25 (

thousa

nds)

25-34

Number of college

graduates leaving

Italy (left)

Number of college

graduates returning

to Italy (left)

Share of 25 to 34

year-olds among

migrants with

college degrees

(right)

Italy’s financial problems:

The government-bank “doom loop,” always latent, has remerged.

Sources: FTSE Italia All-Share Financial Index: Global Financial Data, ticker IT8300 Index; FTSE Italia All-Share

Index: Global Financial Data, ticker FTSEMIB Index; Italy ten-year bond yield: Datastream International, code

S310DT. Notes: The graph presents the relative performance of financial stocks and the Italian 10-year bond yield

from 2 January 2015 to 18 September 2012. The relative performance of financial stocks for Italy is the ratio

between the FTSE Italia All-Share Financial Index and FTSE Italia All-Share Index.

0,8

0,9

1,0

1,1

1,2

1,5

2,0

2,5

3,0

3,5

4,0

Jan

2018

Feb

18

Mar

18

Apr

18

May

18

Jun

18

Jul

18

Aug

18

Sep

18

Oct

18

Government bond yield

(left, percent)

Financial sector performance

(right, index)

Sovereignty barrier remains as strong as

ever

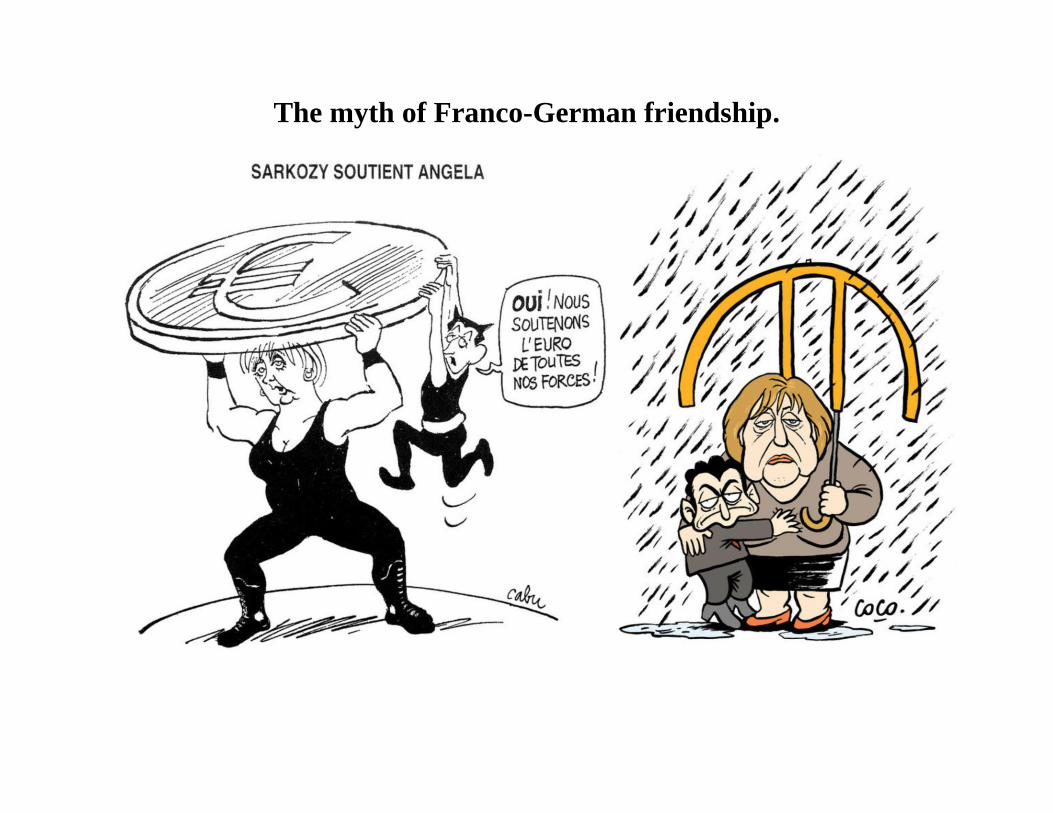

The myth of Franco-German friendship.

At the December 2012 European Council, Herman Von Rompuy proposed a

eurozone budget. Merkel asked, “Where will the money come from?” French

president François Hollande helpfully suggested to Merkel that she think of it as

a “solidarity fund.” Again, Merkel coldly asked, “And where will the money

come from?”

The search for a savior.

How the saviors fall:

Matteo Renzi and Emmanuel Macron approval ratings. (Approval ratings, percent)

Source: Ipsos polls for Matteo Renzi, www.ipsos.it; Ifop for Emmanuel Macron, https://www.ifop.com/wp-

content/uploads/2018/08/Indices-de-popularit%C3%A9-Ao%C3%BBt-2018.pdf.

Note: Percent "Don't know" excluded.

maj 2017 maj 2018 maj 2019 maj 2020 maj 2021

10

20

30

40

50

60

70

maj 2014 maj 2015 maj 2016 maj 2017 maj 2018

Matteo Renzi

Emmanuel Macron

There are no saviors.

Europe: a declining continent for over a century:

The future does not look much better, as Asia surges ahead.

(US patents granted annually to companies in different countries, numbers in thousands)

Source: World Intellectual Property Statistics Database, https://www3.wipo.int/ipstats/index.htm.

0

2

4

6

8

10

12

14

16

18

1995 97 99 01 03 05 07 09 11 13 15

Republic of Korea

Germany

China

France

Italy

The warnings were sounded. It

need not have been. It almost was

not. The rest followed. It could

get worse, a lot worse.

• The euro has hobbled many of

its member countries.

• It has created bitter political

division among Europeans.

• If Aristotle were alive today, he

would see how “eminently

good and just” men and women

enacted the EuroTragedy, “not

by vice or depravity,” but by

“error or frailty.”

Related Documents