Evolution of Tax Structure

"How does your tax structure evolve with your business?" - Simon Davari SdM Accounting

Aug 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Evolution of Tax Structure

Agenda

1. Start-up phase

2. Incorporation and Holding companies

3. Expansion phase

4. Legal issues to consider

1-Development & Start-up

Pros• Losses are used against

other sources of income• Simpler to file• Lower cost for filing

Cons• Taxed at individual level• No benefit of incorporated

rates• Little or no opportunity for

SRED claim

Mr. A Mrs. Aor

Incorporated business

2- Benefits of incorporation

•Deferral of taxation

•Lower tax rate at corporate level▫CCPC status 19% in Quebec▫General rate 26.9% in Quebec

•Dividends are not taxable up to a certain threshold

•Changes to expect in 2017

•Legal protection

•Additional incentives available such as SRED

Cost benefit to consider

2- Benefits of incorporation (cont’d)

2- Growth

Pros• Lower corporate tax rate• Deferral of taxes• Access to 800K capital

gain exemption (“CGE”)• Access to SRED, if

applicable

Mr. A Mrs. Aor

OPco

100%

Cons• Distinct legal status• Requires accounting

process in place• More costly for

compliance

2 – Using a holding companyBenefits• Deferral of taxation

• Legal protection

• Can be used as an investment vehicle

• Income splitting opportunities

• Meet objectives of different shareholders

• Protects redundant assets

• Distribution of dividends from Opco without immediate taxation

• Allows to reinvest in other ventures

OPco Holdco

OPco

Mr. A Mr. AMr. B Mr. B

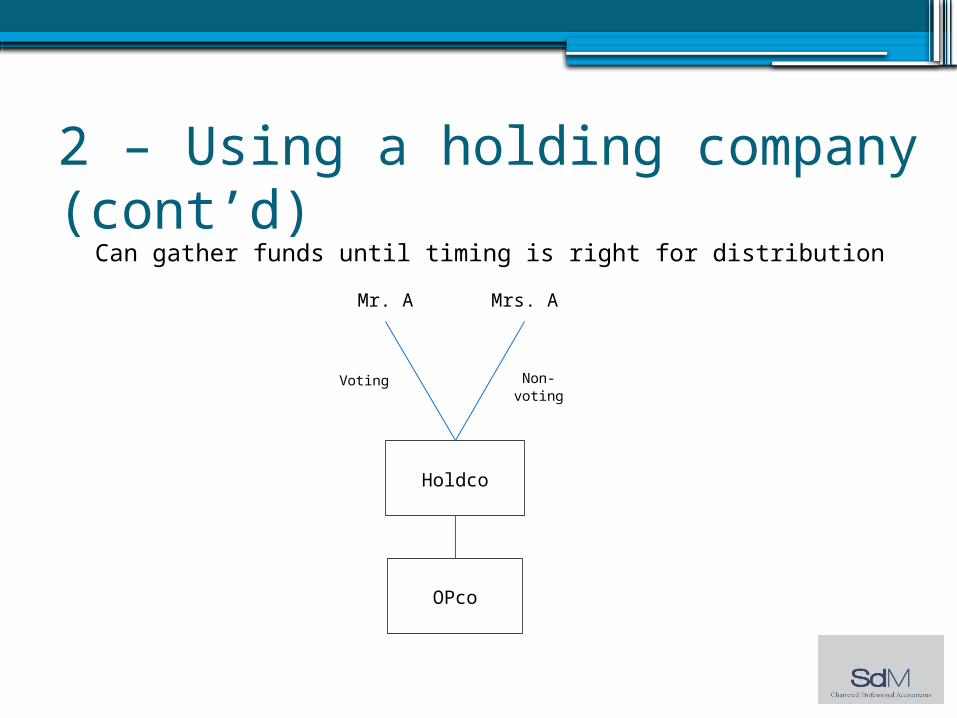

2 – Using a holding company (cont’d)

Holdco

Mr. A Mrs. A

OPco

Voting Non-voting

2 – Using a holding company (cont’d)

Can gather funds until timing is right for distribution

2 – Using a holding company (cont’d)

OPco

Holdco

Trust

Mr. A

Mrs. A

Others

Drawbacks

• May contaminate access to capital gain

exemption

• Must sell Holdco to access capital gain

exemption

• Higher compliance cost

• Another separate accounting

2 – Using a holding company (cont’d)

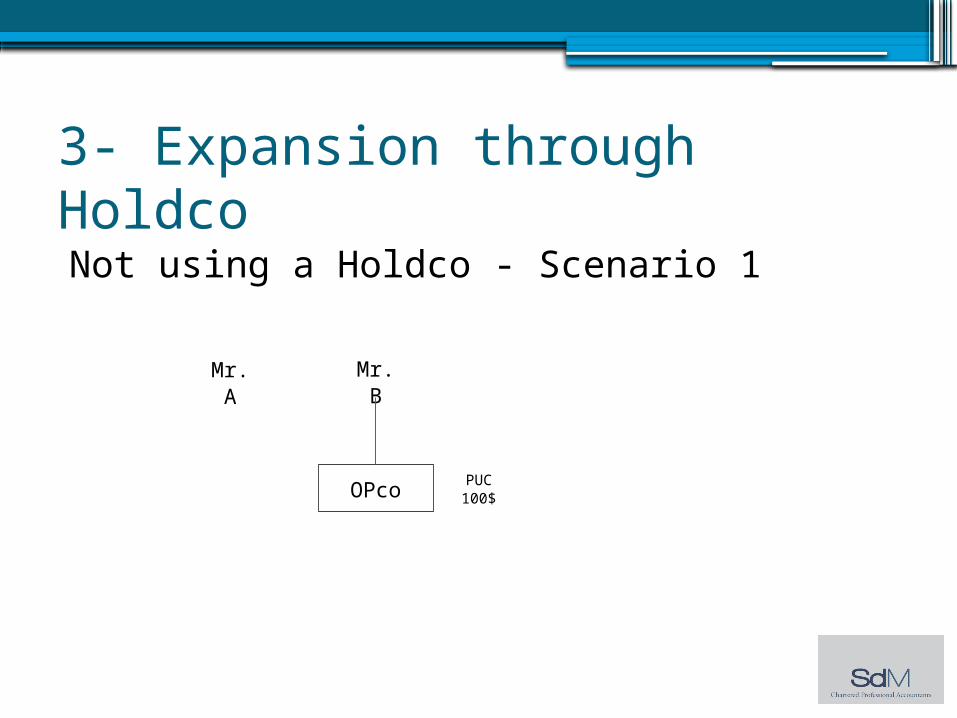

3- Expansion through Holdco

Not using a Holdco - Scenario 1

Mr. A Mr. B

OPco PUC 100$

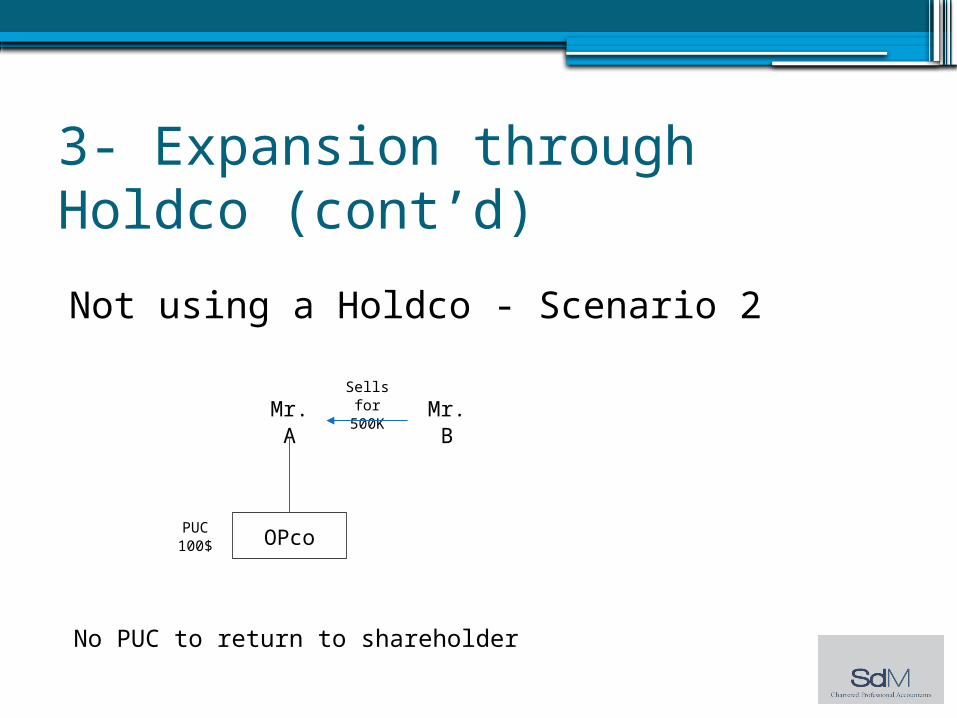

Not using a Holdco - Scenario 2

3- Expansion through Holdco (cont’d)

Mr. A Mr. B

OPcoPUC 100$

Sells for 500K

No PUC to return to shareholder

3- Expansion through Holdco (cont’d)Using a Holdco for PUC preservation

OPco

Mr. A Mr. B

HoldcoSells for

500K

Injection of 500K

PUC 500K

PUC 100$

PUC can be returned tax-free to shareholder

Using a Holdco for debt pushdown – Step 1

3- Expansion through Holdco (cont’d)

OPco

Mr. A Bank

Holdco

Borrows 500KInterest

expenses

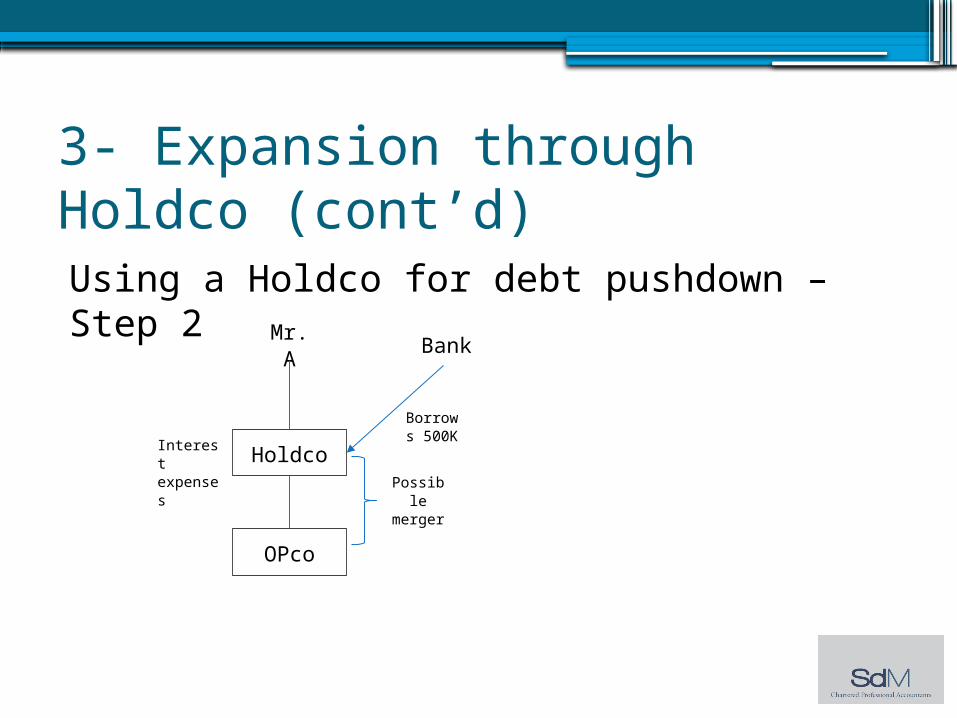

Using a Holdco for debt pushdown – Step 2

OPco

Mr. A Bank

Holdco

Borrows 500K

Interest expenses

Possible merger

3- Expansion through Holdco (cont’d)

3 - ExpansionCanada International

OPco

Holdco

ForeignCo

Shareholders

3 – Expansion (cont’d)

•Consider impact in foreign jurisdiction▫Capital contribution▫Legal status (branch vs. subsidiary)▫Cash repatriation

•Impact on CGE

3- Expansion (cont’d)Canada International

OPco

Holdco 1

ForeignCo

Shareholders

Holdco 2

Holdco 1 Sold to use up to 800K CGEHoldco 2 Sold without access to CGE

4 – Legal issues

•Holdco allows protection of assets accumulated against lawsuits at Opco level.

•In the case of a lawsuit, plaintiffs cannot access assets in trust.

Related Documents