How Common Foreign Currency Transactions by a Multinational's "Treasury Center" CFC Can Give Rise to Unfavorable Subpart F Whipsaws Michael Farber Davis Polk & Wardwell LLP L.G. “Chip” Harter PricewaterhouseCoopers LLP Yaron Z. Reich Cleary Gottlieb Steen & Hamilton LLP Danielle Rolfes U.S. Treasury, International Tax Counsel International Tax Institute July 18, 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

How Common Foreign Currency Transactions by a Multinational's "Treasury Center" CFC Can Give Rise

to Unfavorable Subpart F Whipsaws

Michael Farber Davis Polk & Wardwell LLP

L.G. “Chip” Harter

PricewaterhouseCoopers LLP

Yaron Z. Reich Cleary Gottlieb Steen & Hamilton LLP

Danielle Rolfes

U.S. Treasury, International Tax Counsel International Tax Institute

July 18, 2013

1

Agenda

I. Overview of key concepts

II. Fact pattern 1: back-to-back loans

III. Fact pattern 2: QBU hedges

IV. Fact pattern 3: Hoover hedges

2

Overview of key concepts: Section 988 transactions

Section 988 governs the treatment of non-functional foreign currency (“FC”) gain or loss on “Section 988 transactions”

Section 988 transactions include:

Acquisition or issuance of FC debt

Accrual of FC income or expense

Acquisition of FC forward contracts, options or similar financial instruments

Disposition of FC

3

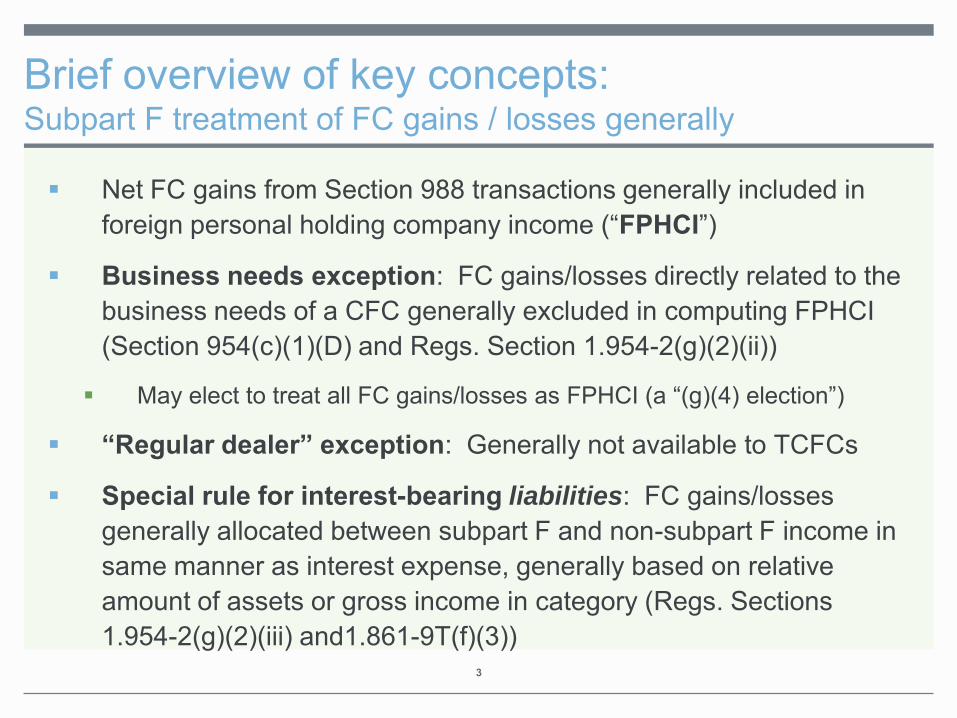

Brief overview of key concepts: Subpart F treatment of FC gains / losses generally

Net FC gains from Section 988 transactions generally included in foreign personal holding company income (“FPHCI”)

Business needs exception: FC gains/losses directly related to the business needs of a CFC generally excluded in computing FPHCI (Section 954(c)(1)(D) and Regs. Section 1.954-2(g)(2)(ii))

May elect to treat all FC gains/losses as FPHCI (a “(g)(4) election”)

“Regular dealer” exception: Generally not available to TCFCs

Special rule for interest-bearing liabilities: FC gains/losses generally allocated between subpart F and non-subpart F income in same manner as interest expense, generally based on relative amount of assets or gross income in category (Regs. Sections 1.954-2(g)(2)(iii) and1.861-9T(f)(3))

4

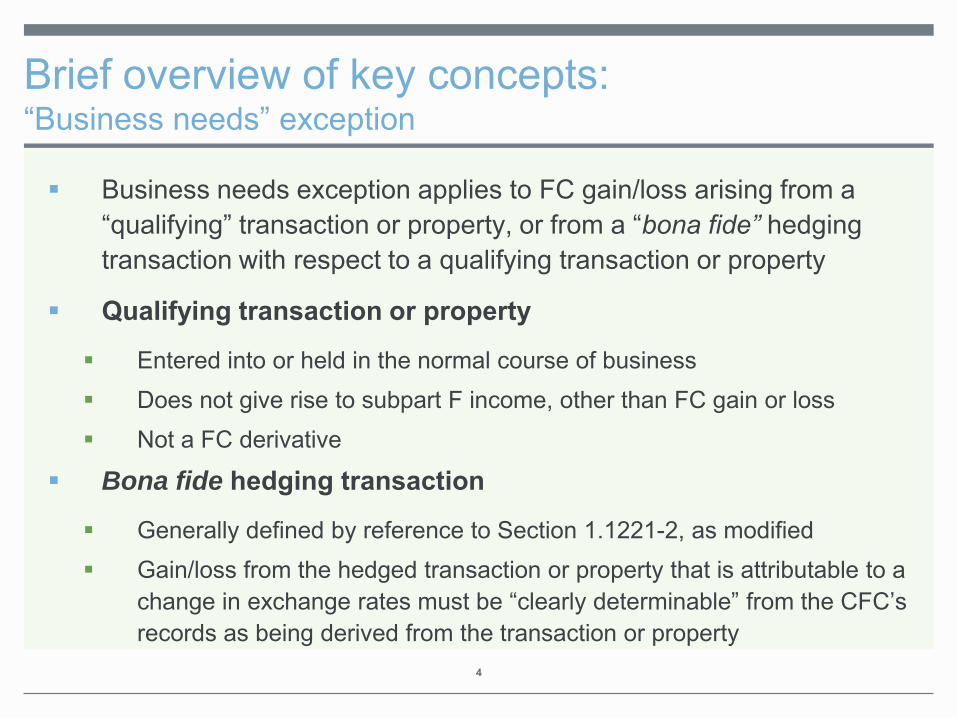

Brief overview of key concepts: “Business needs” exception

Business needs exception applies to FC gain/loss arising from a “qualifying” transaction or property, or from a “bona fide” hedging transaction with respect to a qualifying transaction or property

Qualifying transaction or property

Entered into or held in the normal course of business Does not give rise to subpart F income, other than FC gain or loss Not a FC derivative

Bona fide hedging transaction

Generally defined by reference to Section 1.1221-2, as modified Gain/loss from the hedged transaction or property that is attributable to a

change in exchange rates must be “clearly determinable” from the CFC’s records as being derived from the transaction or property

5

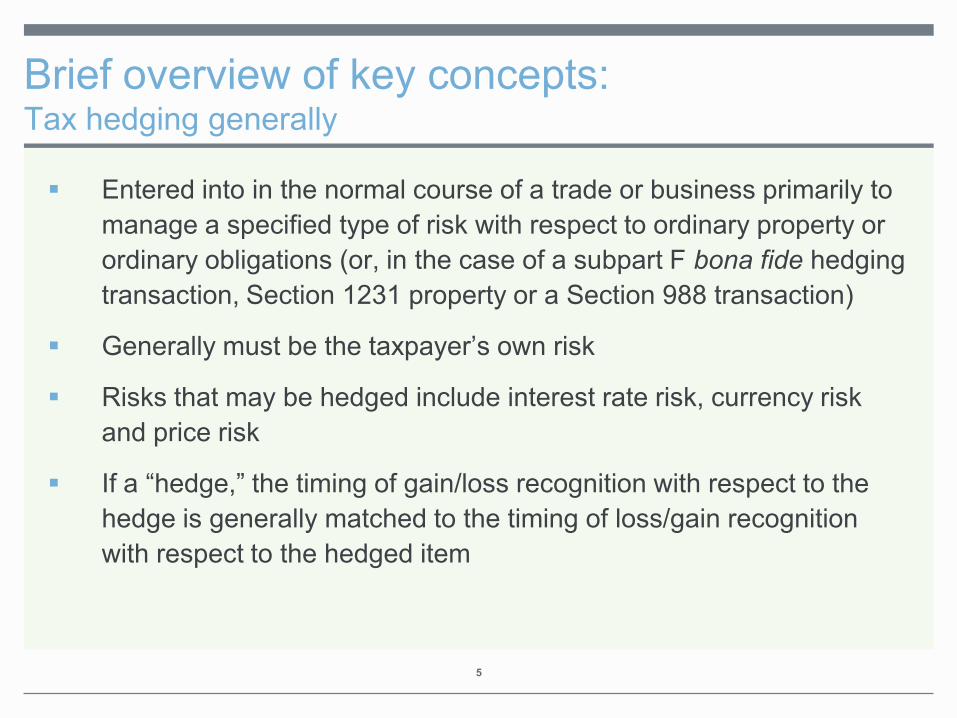

Brief overview of key concepts: Tax hedging generally

Entered into in the normal course of a trade or business primarily to manage a specified type of risk with respect to ordinary property or ordinary obligations (or, in the case of a subpart F bona fide hedging transaction, Section 1231 property or a Section 988 transaction)

Generally must be the taxpayer’s own risk

Risks that may be hedged include interest rate risk, currency risk and price risk

If a “hedge,” the timing of gain/loss recognition with respect to the hedge is generally matched to the timing of loss/gain recognition with respect to the hedged item

6

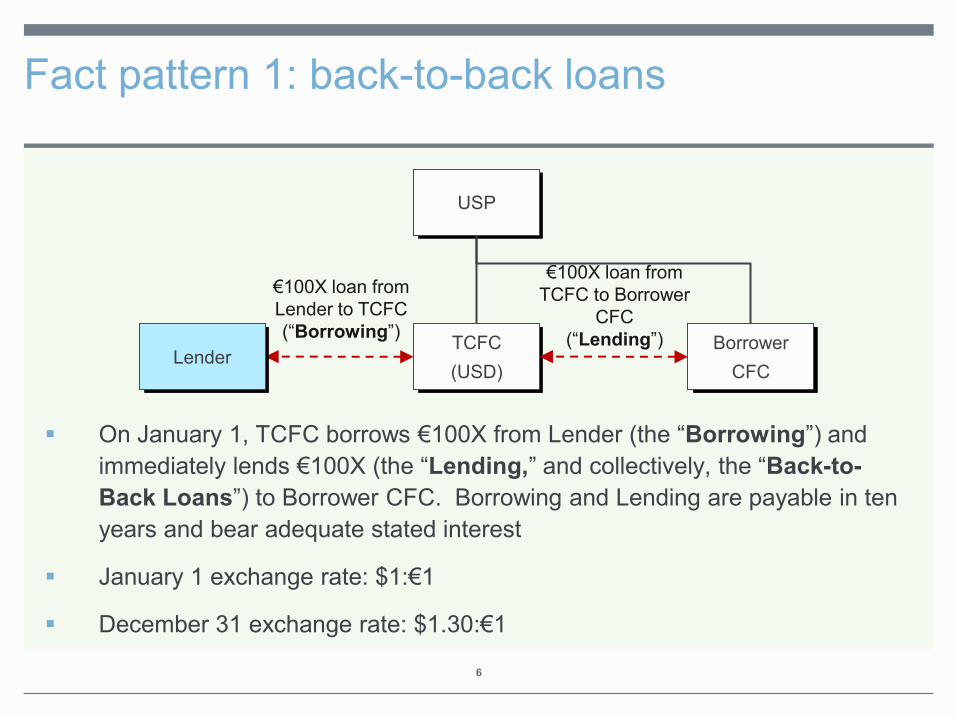

Fact pattern 1: back-to-back loans

On January 1, TCFC borrows €100X from Lender (the “Borrowing”) and immediately lends €100X (the “Lending,” and collectively, the “Back-to-Back Loans”) to Borrower CFC. Borrowing and Lending are payable in ten years and bear adequate stated interest

January 1 exchange rate: $1:€1

December 31 exchange rate: $1.30:€1

USP

TCFC (USD)

Lender Borrower

CFC

€100X loan from TCFC to Borrower

CFC (“Lending”)

€100X loan from Lender to TCFC (“Borrowing”)

7

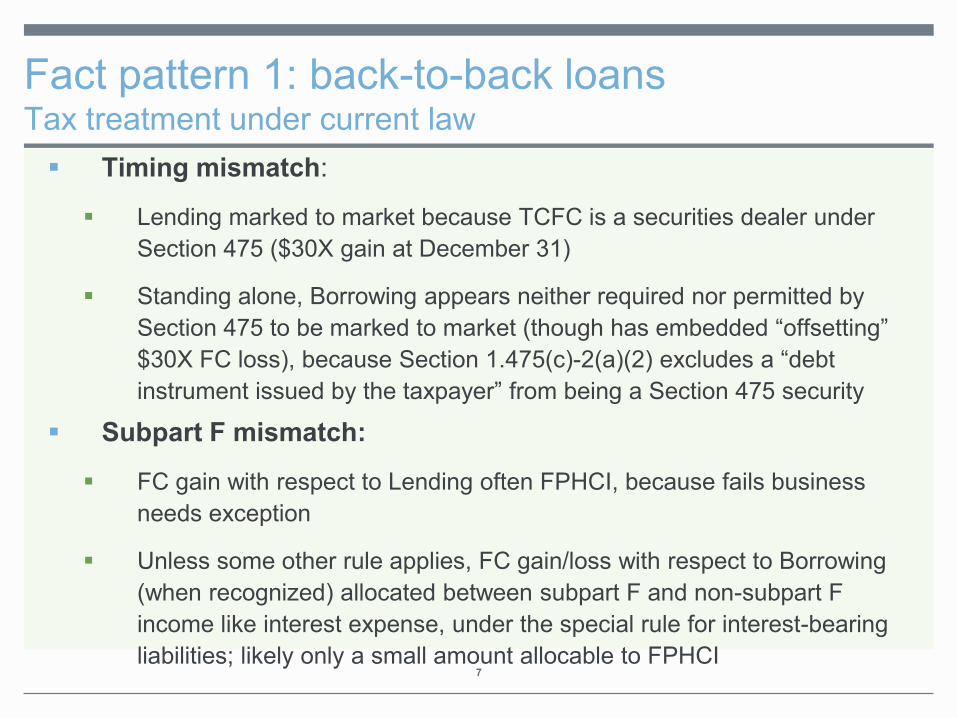

Fact pattern 1: back-to-back loans Tax treatment under current law Timing mismatch:

Lending marked to market because TCFC is a securities dealer under Section 475 ($30X gain at December 31)

Standing alone, Borrowing appears neither required nor permitted by Section 475 to be marked to market (though has embedded “offsetting” $30X FC loss), because Section 1.475(c)-2(a)(2) excludes a “debt instrument issued by the taxpayer” from being a Section 475 security

Subpart F mismatch:

FC gain with respect to Lending often FPHCI, because fails business needs exception

Unless some other rule applies, FC gain/loss with respect to Borrowing (when recognized) allocated between subpart F and non-subpart F income like interest expense, under the special rule for interest-bearing liabilities; likely only a small amount allocable to FPHCI

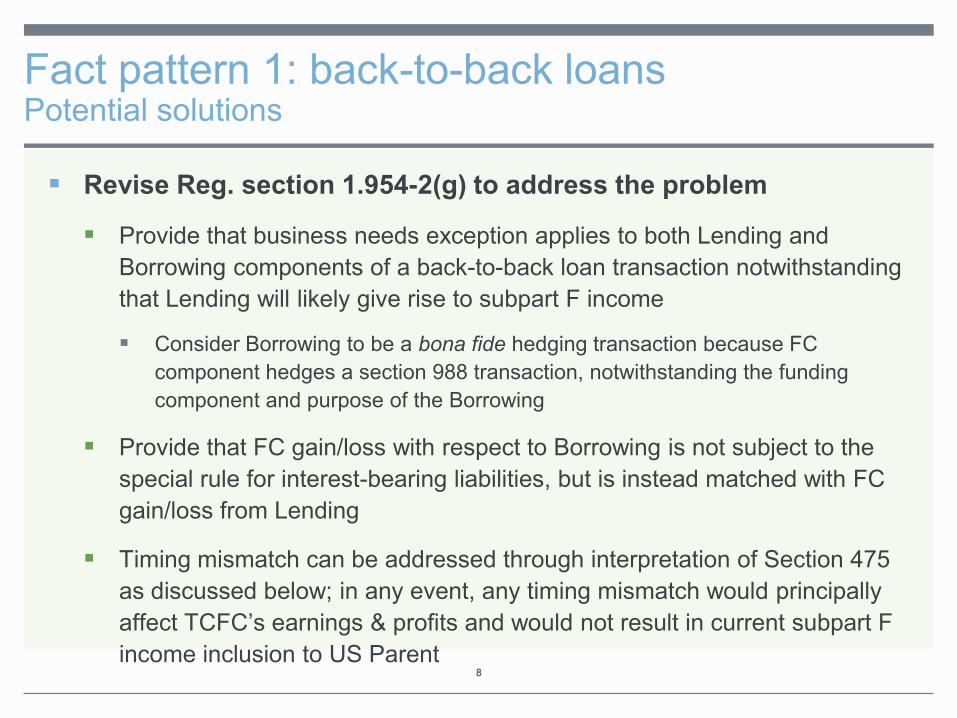

Fact pattern 1: back-to-back loans Potential solutions

Revise Reg. section 1.954-2(g) to address the problem

Provide that business needs exception applies to both Lending and Borrowing components of a back-to-back loan transaction notwithstanding that Lending will likely give rise to subpart F income

Consider Borrowing to be a bona fide hedging transaction because FC component hedges a section 988 transaction, notwithstanding the funding component and purpose of the Borrowing

Provide that FC gain/loss with respect to Borrowing is not subject to the special rule for interest-bearing liabilities, but is instead matched with FC gain/loss from Lending

Timing mismatch can be addressed through interpretation of Section 475 as discussed below; in any event, any timing mismatch would principally affect TCFC’s earnings & profits and would not result in current subpart F income inclusion to US Parent

8

9

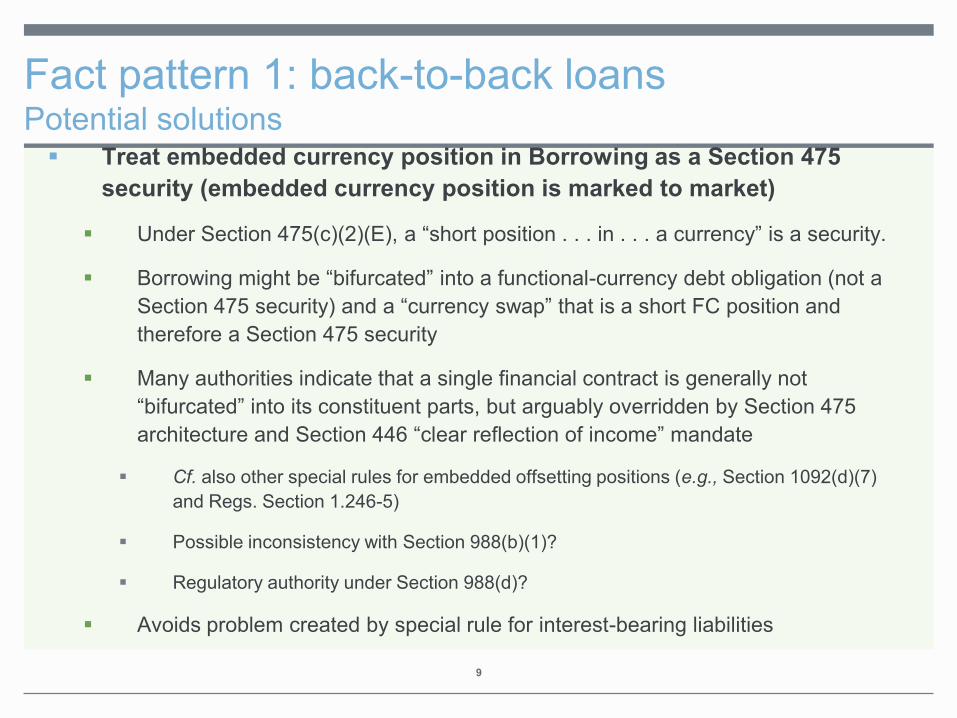

Fact pattern 1: back-to-back loans Potential solutions Treat embedded currency position in Borrowing as a Section 475

security (embedded currency position is marked to market)

Under Section 475(c)(2)(E), a “short position . . . in . . . a currency” is a security.

Borrowing might be “bifurcated” into a functional-currency debt obligation (not a Section 475 security) and a “currency swap” that is a short FC position and therefore a Section 475 security

Many authorities indicate that a single financial contract is generally not “bifurcated” into its constituent parts, but arguably overridden by Section 475 architecture and Section 446 “clear reflection of income” mandate

Cf. also other special rules for embedded offsetting positions (e.g., Section 1092(d)(7) and Regs. Section 1.246-5)

Possible inconsistency with Section 988(b)(1)?

Regulatory authority under Section 988(d)?

Avoids problem created by special rule for interest-bearing liabilities

10

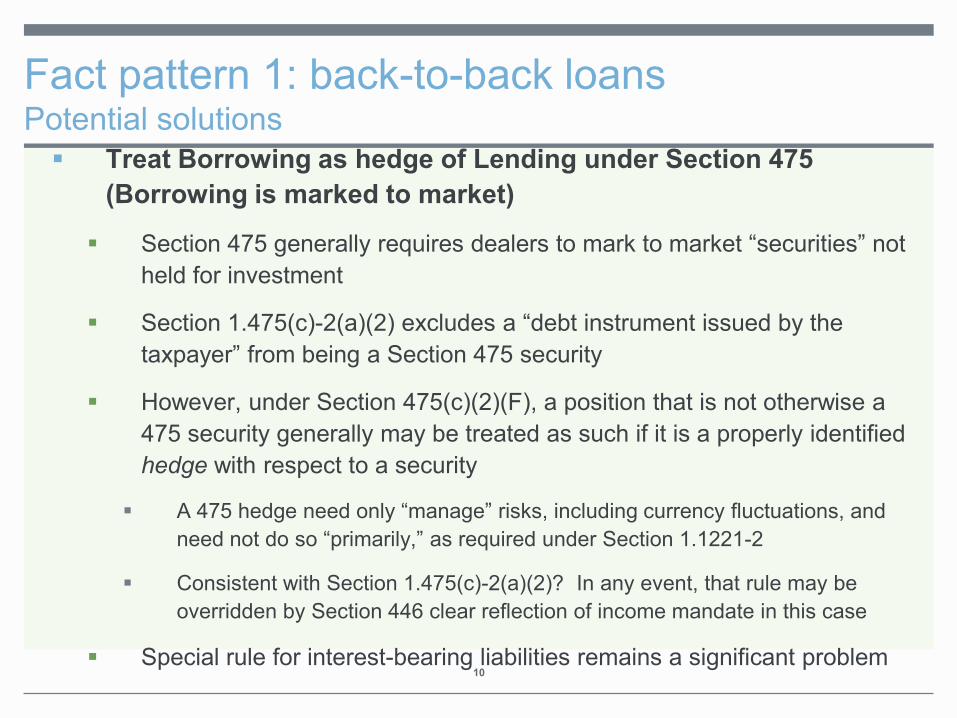

Fact pattern 1: back-to-back loans Potential solutions Treat Borrowing as hedge of Lending under Section 475

(Borrowing is marked to market)

Section 475 generally requires dealers to mark to market “securities” not held for investment

Section 1.475(c)-2(a)(2) excludes a “debt instrument issued by the taxpayer” from being a Section 475 security

However, under Section 475(c)(2)(F), a position that is not otherwise a 475 security generally may be treated as such if it is a properly identified hedge with respect to a security

A 475 hedge need only “manage” risks, including currency fluctuations, and need not do so “primarily,” as required under Section 1.1221-2

Consistent with Section 1.475(c)-2(a)(2)? In any event, that rule may be overridden by Section 446 clear reflection of income mandate in this case

Special rule for interest-bearing liabilities remains a significant problem

11

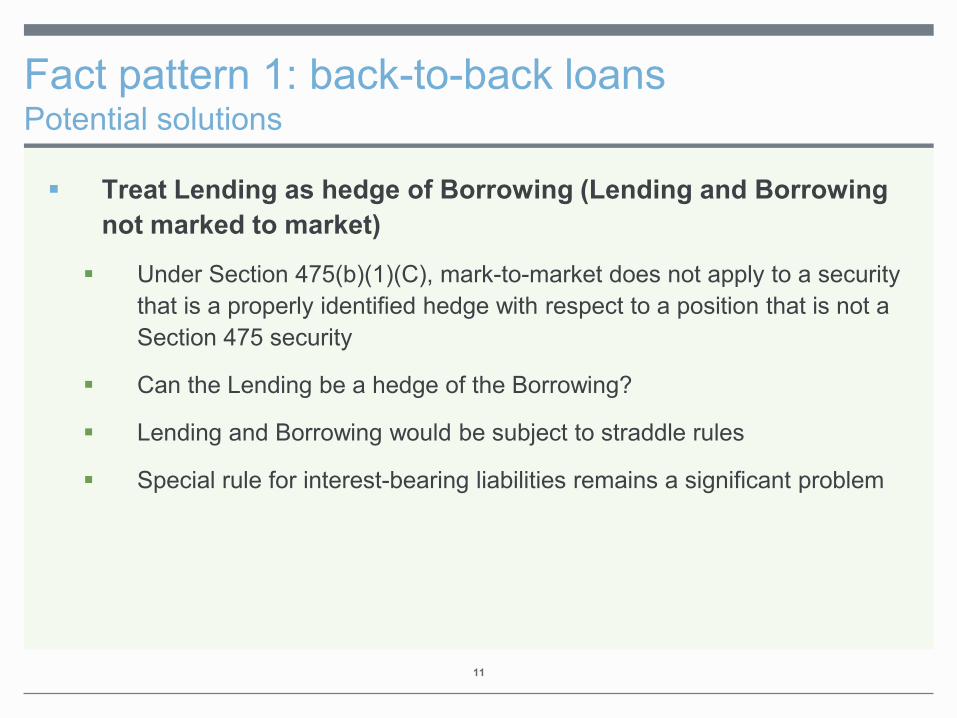

Fact pattern 1: back-to-back loans Potential solutions

Treat Lending as hedge of Borrowing (Lending and Borrowing not marked to market)

Under Section 475(b)(1)(C), mark-to-market does not apply to a security that is a properly identified hedge with respect to a position that is not a Section 475 security

Can the Lending be a hedge of the Borrowing?

Lending and Borrowing would be subject to straddle rules

Special rule for interest-bearing liabilities remains a significant problem

12

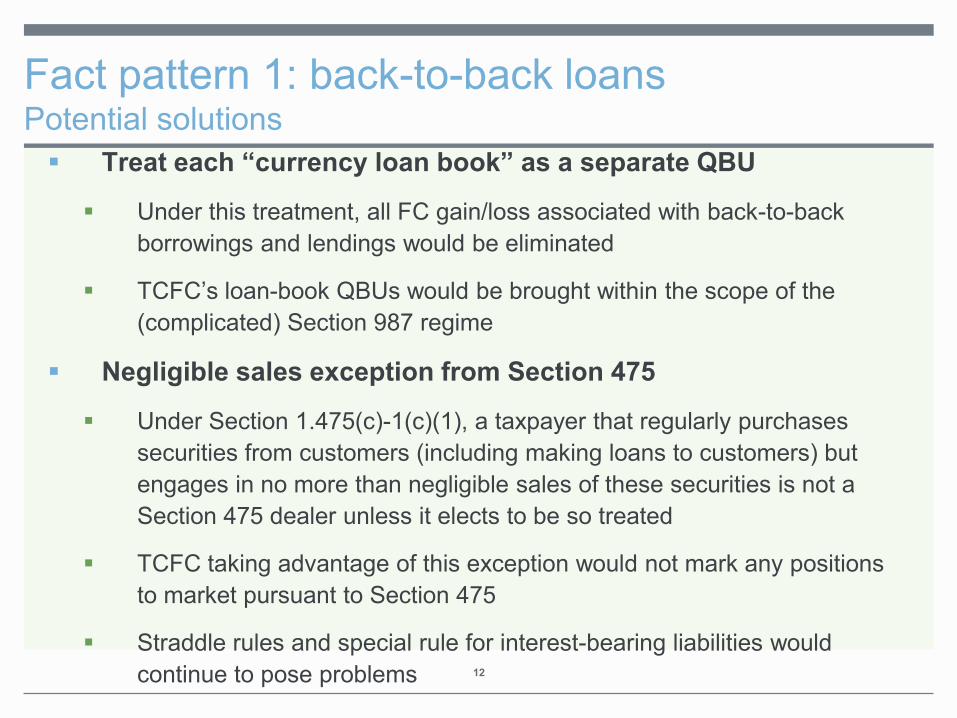

Fact pattern 1: back-to-back loans Potential solutions Treat each “currency loan book” as a separate QBU

Under this treatment, all FC gain/loss associated with back-to-back borrowings and lendings would be eliminated

TCFC’s loan-book QBUs would be brought within the scope of the (complicated) Section 987 regime

Negligible sales exception from Section 475

Under Section 1.475(c)-1(c)(1), a taxpayer that regularly purchases securities from customers (including making loans to customers) but engages in no more than negligible sales of these securities is not a Section 475 dealer unless it elects to be so treated

TCFC taking advantage of this exception would not mark any positions to market pursuant to Section 475

Straddle rules and special rule for interest-bearing liabilities would continue to pose problems

13

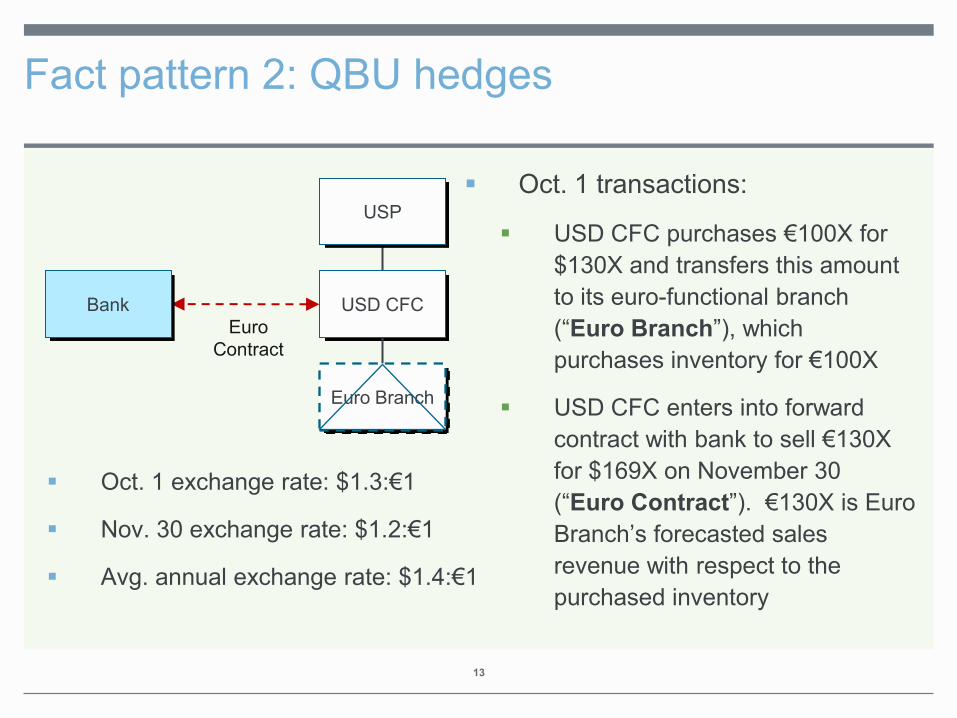

Fact pattern 2: QBU hedges

USP

USD CFC Bank Euro

Contract

Euro Branch

Oct. 1 transactions:

USD CFC purchases €100X for $130X and transfers this amount to its euro-functional branch (“Euro Branch”), which purchases inventory for €100X

USD CFC enters into forward contract with bank to sell €130X for $169X on November 30 (“Euro Contract”). €130X is Euro Branch’s forecasted sales revenue with respect to the purchased inventory

Oct. 1 exchange rate: $1.3:€1

Nov. 30 exchange rate: $1.2:€1

Avg. annual exchange rate: $1.4:€1

14

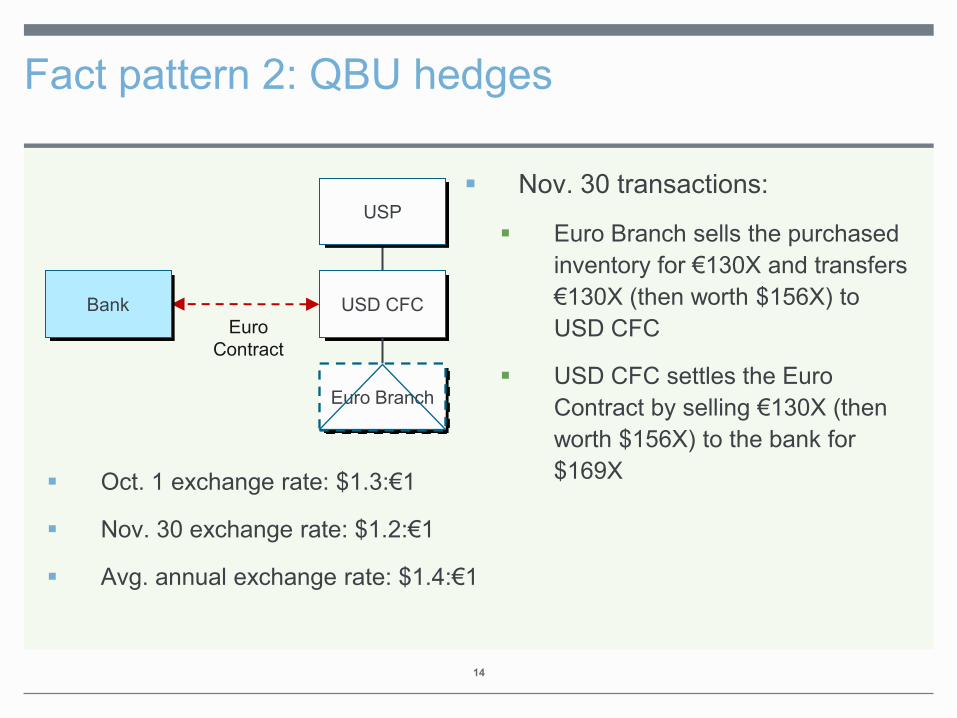

Fact pattern 2: QBU hedges

USP

USD CFC Bank Euro

Contract

Euro Branch

Nov. 30 transactions:

Euro Branch sells the purchased inventory for €130X and transfers €130X (then worth $156X) to USD CFC

USD CFC settles the Euro Contract by selling €130X (then worth $156X) to the bank for $169X

Oct. 1 exchange rate: $1.3:€1

Nov. 30 exchange rate: $1.2:€1

Avg. annual exchange rate: $1.4:€1

15

Fact pattern 2: QBU hedges

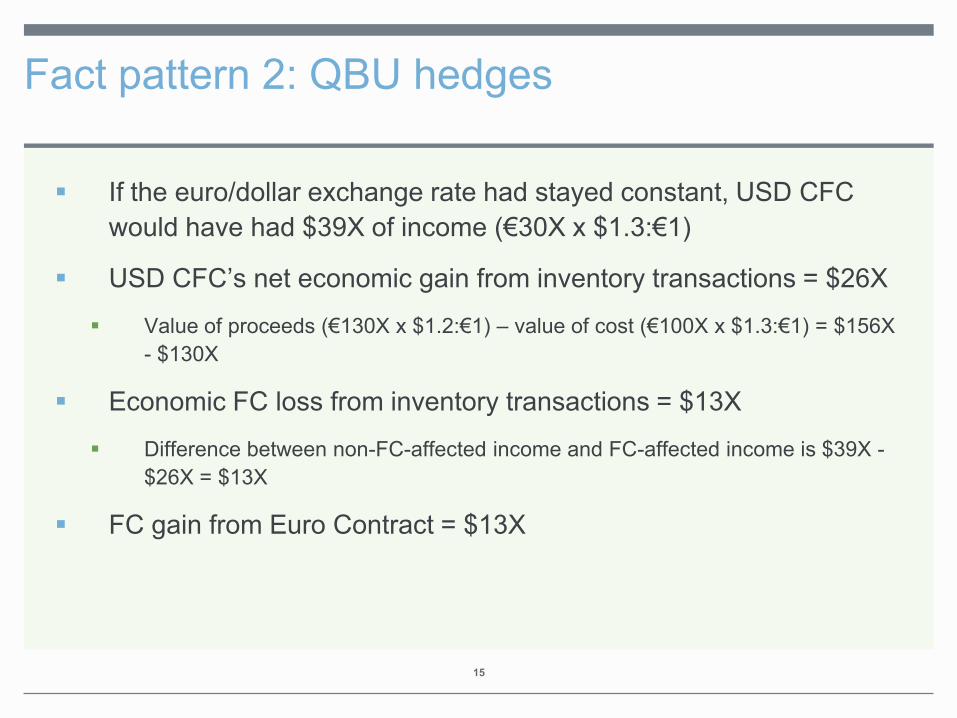

If the euro/dollar exchange rate had stayed constant, USD CFC would have had $39X of income (€30X x $1.3:€1)

USD CFC’s net economic gain from inventory transactions = $26X

Value of proceeds (€130X x $1.2:€1) – value of cost (€100X x $1.3:€1) = $156X - $130X

Economic FC loss from inventory transactions = $13X

Difference between non-FC-affected income and FC-affected income is $39X - $26X = $13X

FC gain from Euro Contract = $13X

16

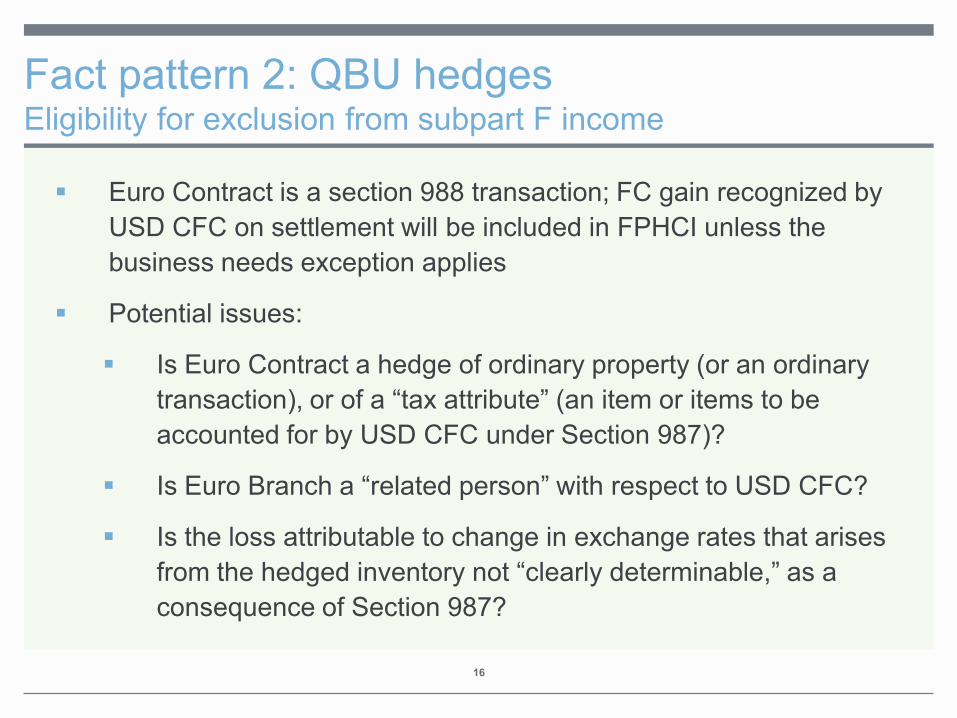

Fact pattern 2: QBU hedges Eligibility for exclusion from subpart F income

Euro Contract is a section 988 transaction; FC gain recognized by USD CFC on settlement will be included in FPHCI unless the business needs exception applies

Potential issues:

Is Euro Contract a hedge of ordinary property (or an ordinary transaction), or of a “tax attribute” (an item or items to be accounted for by USD CFC under Section 987)?

Is Euro Branch a “related person” with respect to USD CFC?

Is the loss attributable to change in exchange rates that arises from the hedged inventory not “clearly determinable,” as a consequence of Section 987?

17

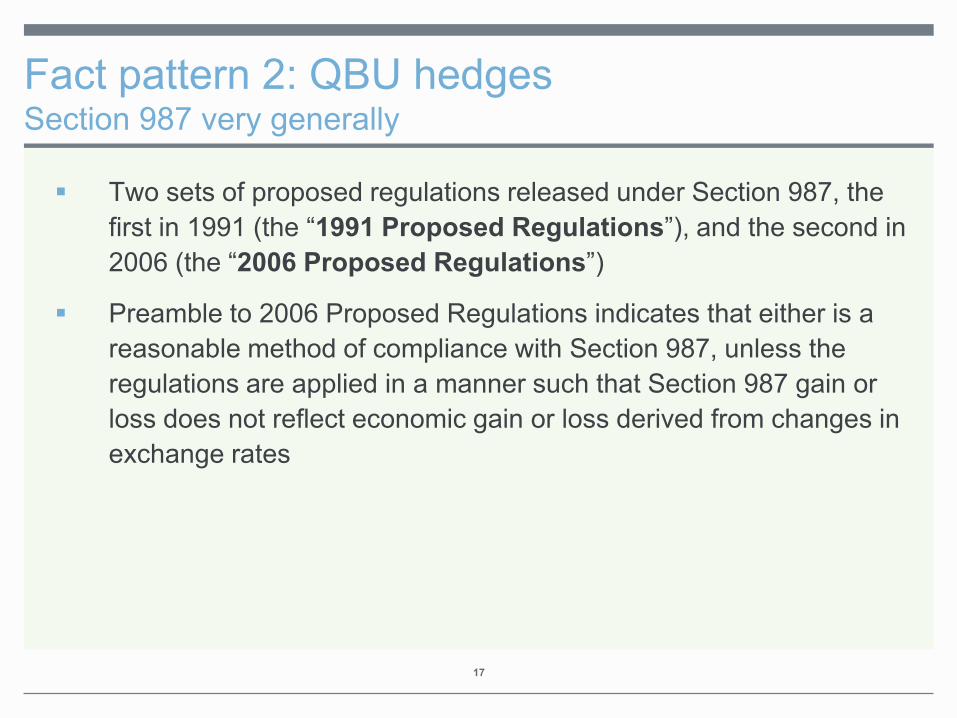

Fact pattern 2: QBU hedges Section 987 very generally

Two sets of proposed regulations released under Section 987, the first in 1991 (the “1991 Proposed Regulations”), and the second in 2006 (the “2006 Proposed Regulations”)

Preamble to 2006 Proposed Regulations indicates that either is a reasonable method of compliance with Section 987, unless the regulations are applied in a manner such that Section 987 gain or loss does not reflect economic gain or loss derived from changes in exchange rates

18

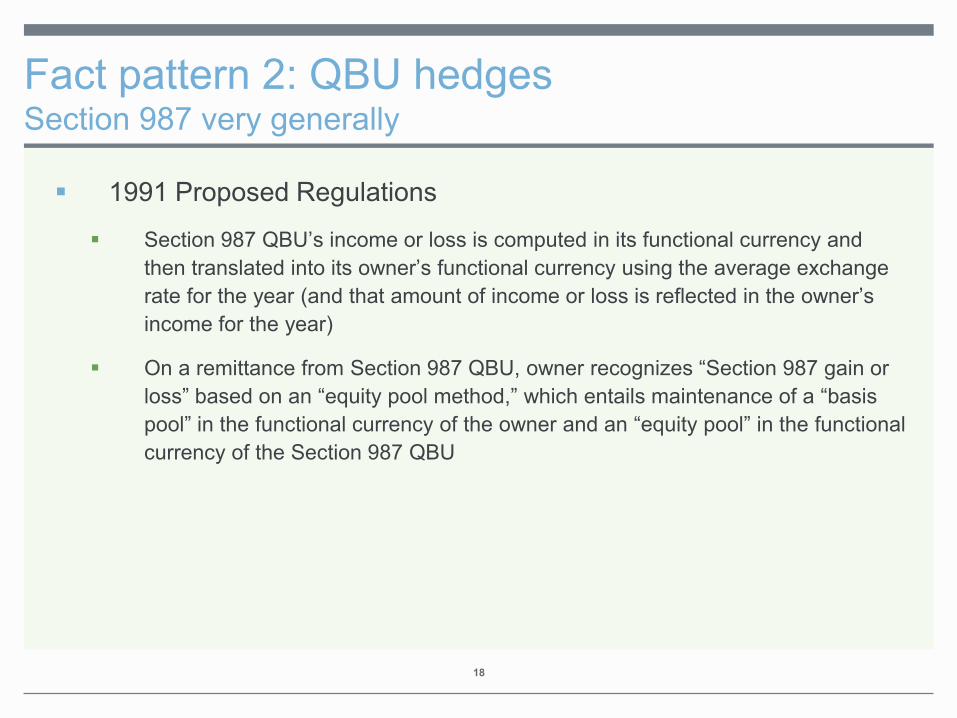

Fact pattern 2: QBU hedges Section 987 very generally

1991 Proposed Regulations

Section 987 QBU’s income or loss is computed in its functional currency and then translated into its owner’s functional currency using the average exchange rate for the year (and that amount of income or loss is reflected in the owner’s income for the year)

On a remittance from Section 987 QBU, owner recognizes “Section 987 gain or loss” based on an “equity pool method,” which entails maintenance of a “basis pool” in the functional currency of the owner and an “equity pool” in the functional currency of the Section 987 QBU

19

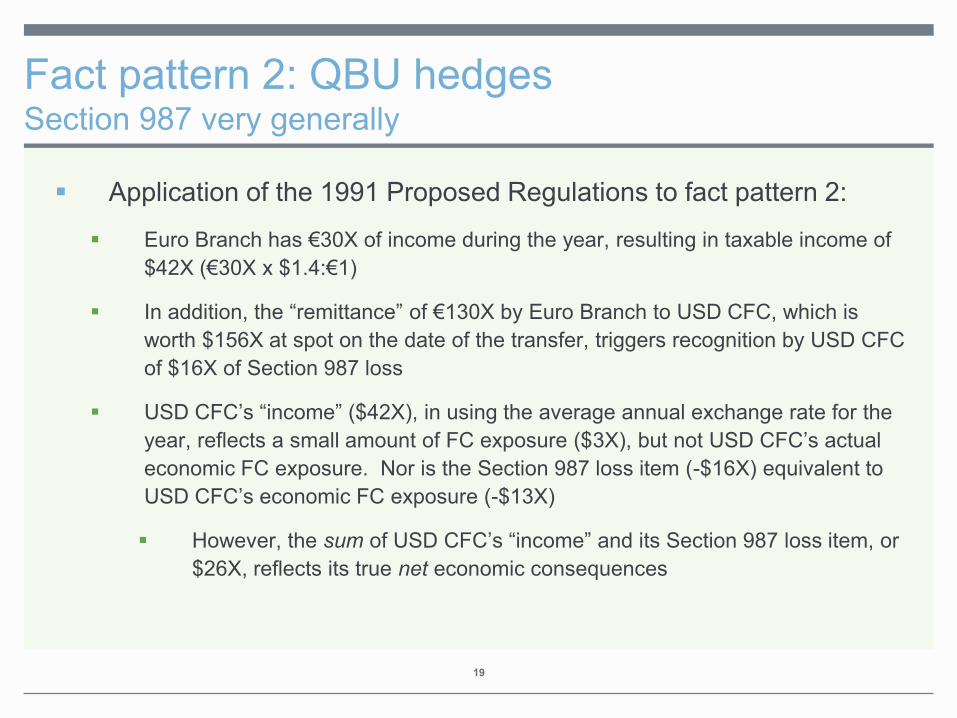

Fact pattern 2: QBU hedges Section 987 very generally

Application of the 1991 Proposed Regulations to fact pattern 2:

Euro Branch has €30X of income during the year, resulting in taxable income of $42X (€30X x $1.4:€1)

In addition, the “remittance” of €130X by Euro Branch to USD CFC, which is worth $156X at spot on the date of the transfer, triggers recognition by USD CFC of $16X of Section 987 loss

USD CFC’s “income” ($42X), in using the average annual exchange rate for the year, reflects a small amount of FC exposure ($3X), but not USD CFC’s actual economic FC exposure. Nor is the Section 987 loss item (-$16X) equivalent to USD CFC’s economic FC exposure (-$13X)

However, the sum of USD CFC’s “income” and its Section 987 loss item, or $26X, reflects its true net economic consequences

20

Fact pattern 2: QBU hedges Section 987 very generally

2006 Proposed Regulations

Items of income, gain, deduction or loss attributable to a Section 987 QBU separately translated into the owner’s functional currency. On the sale of an “historic item,” such as the inventory held by Euro Branch, generally, the amount realized is translated into the owner’s functional currency using the average annual exchange rate, and the adjusted basis is translated into the owner’s functional currency using the historic spot rate on the date the asset was transferred to or acquired by the Section 987 QBU

If there is a remittance during the year, the owner of the Section 987 QBU recognizes a portion of the “net unrecognized section 987 gain or loss” based on the owner’s “remittance proportion,” which is very generally the percentage of the CFC’s “basis” in its QBU (as defined) that is being remitted

21

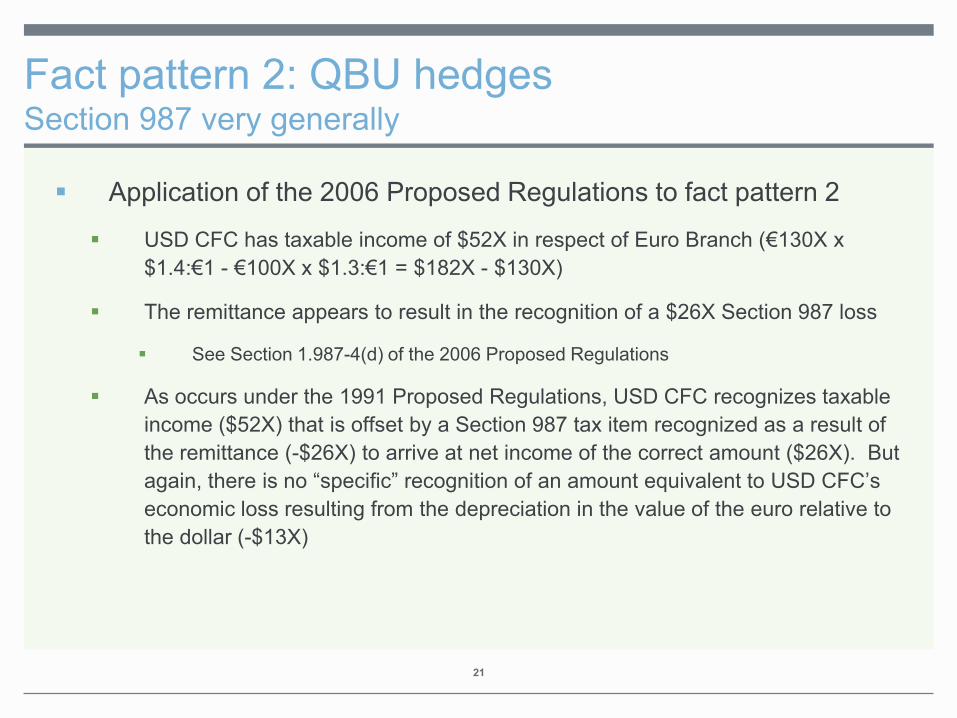

Fact pattern 2: QBU hedges Section 987 very generally

Application of the 2006 Proposed Regulations to fact pattern 2

USD CFC has taxable income of $52X in respect of Euro Branch (€130X x $1.4:€1 - €100X x $1.3:€1 = $182X - $130X)

The remittance appears to result in the recognition of a $26X Section 987 loss

See Section 1.987-4(d) of the 2006 Proposed Regulations

As occurs under the 1991 Proposed Regulations, USD CFC recognizes taxable income ($52X) that is offset by a Section 987 tax item recognized as a result of the remittance (-$26X) to arrive at net income of the correct amount ($26X). But again, there is no “specific” recognition of an amount equivalent to USD CFC’s economic loss resulting from the depreciation in the value of the euro relative to the dollar (-$13X)

22

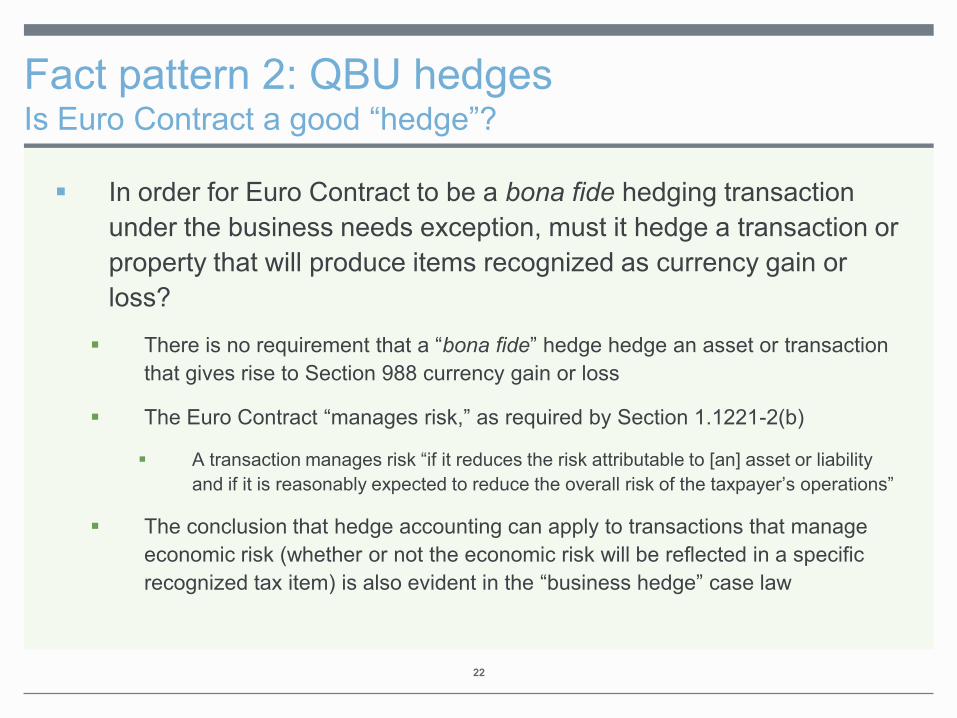

Fact pattern 2: QBU hedges Is Euro Contract a good “hedge”?

In order for Euro Contract to be a bona fide hedging transaction under the business needs exception, must it hedge a transaction or property that will produce items recognized as currency gain or loss?

There is no requirement that a “bona fide” hedge hedge an asset or transaction that gives rise to Section 988 currency gain or loss

The Euro Contract “manages risk,” as required by Section 1.1221-2(b)

A transaction manages risk “if it reduces the risk attributable to [an] asset or liability and if it is reasonably expected to reduce the overall risk of the taxpayer’s operations”

The conclusion that hedge accounting can apply to transactions that manage economic risk (whether or not the economic risk will be reflected in a specific recognized tax item) is also evident in the “business hedge” case law

23

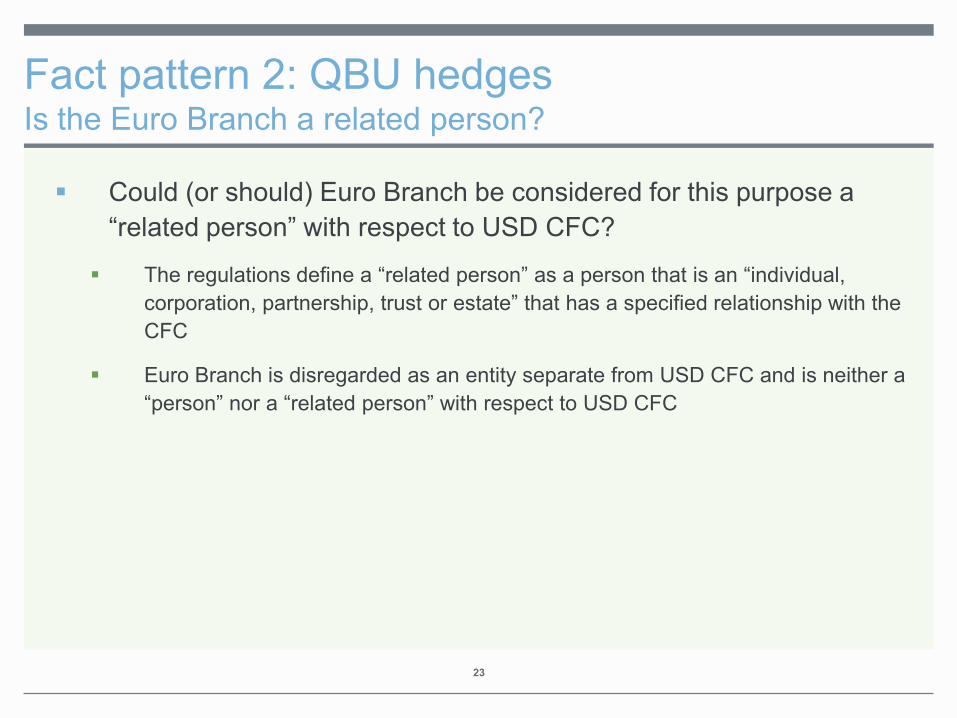

Fact pattern 2: QBU hedges Is the Euro Branch a related person?

Could (or should) Euro Branch be considered for this purpose a “related person” with respect to USD CFC?

The regulations define a “related person” as a person that is an “individual, corporation, partnership, trust or estate” that has a specified relationship with the CFC

Euro Branch is disregarded as an entity separate from USD CFC and is neither a “person” nor a “related person” with respect to USD CFC

24

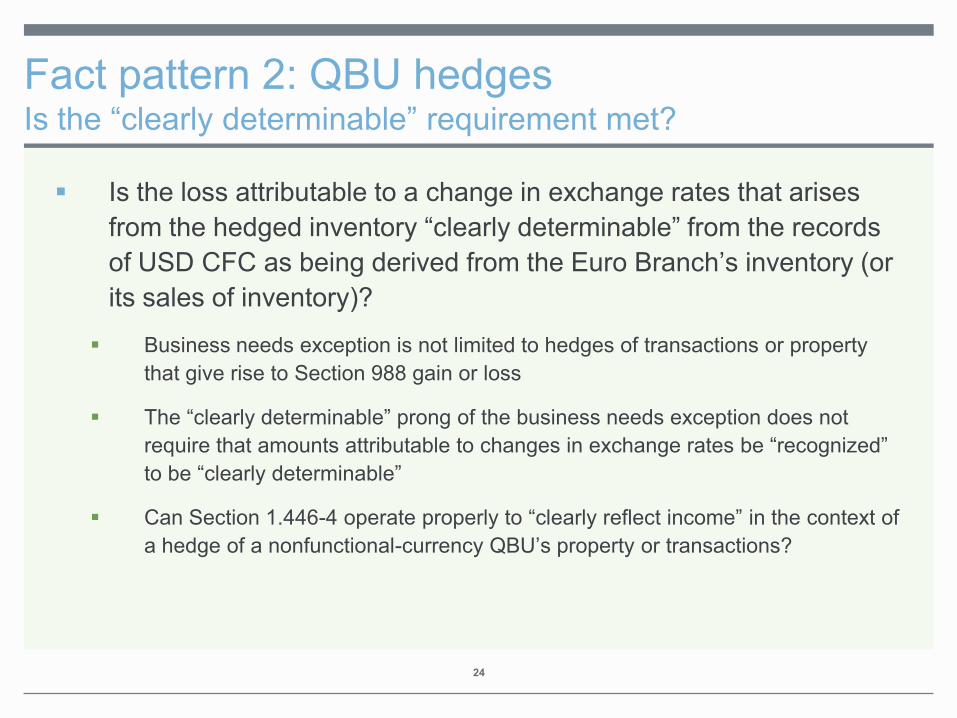

Fact pattern 2: QBU hedges Is the “clearly determinable” requirement met?

Is the loss attributable to a change in exchange rates that arises from the hedged inventory “clearly determinable” from the records of USD CFC as being derived from the Euro Branch’s inventory (or its sales of inventory)?

Business needs exception is not limited to hedges of transactions or property that give rise to Section 988 gain or loss

The “clearly determinable” prong of the business needs exception does not require that amounts attributable to changes in exchange rates be “recognized” to be “clearly determinable”

Can Section 1.446-4 operate properly to “clearly reflect income” in the context of a hedge of a nonfunctional-currency QBU’s property or transactions?

Variation on Fact Pattern 2: Hedging a QBU loan

Often, USD CFC will instead lend FC to its QBU, and then hedge the FC component of that loan

QBU is disregarded, so loan is as well, but the analysis of whether the FC gain/loss from the hedge is within the business needs exception is the same – does hedge manage risk of business needs property, and is the gain/loss from that property attributable to exchange rate changes clearly determinable as derived from that property?

The loan probably lowers foreign taxes, but not relevant to the subpart F analysis

Note a CFC in this situation can resort to self-help by making the QBU into a partnership and lending it the relevant currency, subject to issues discussed in connection with fact pattern 1

25

26

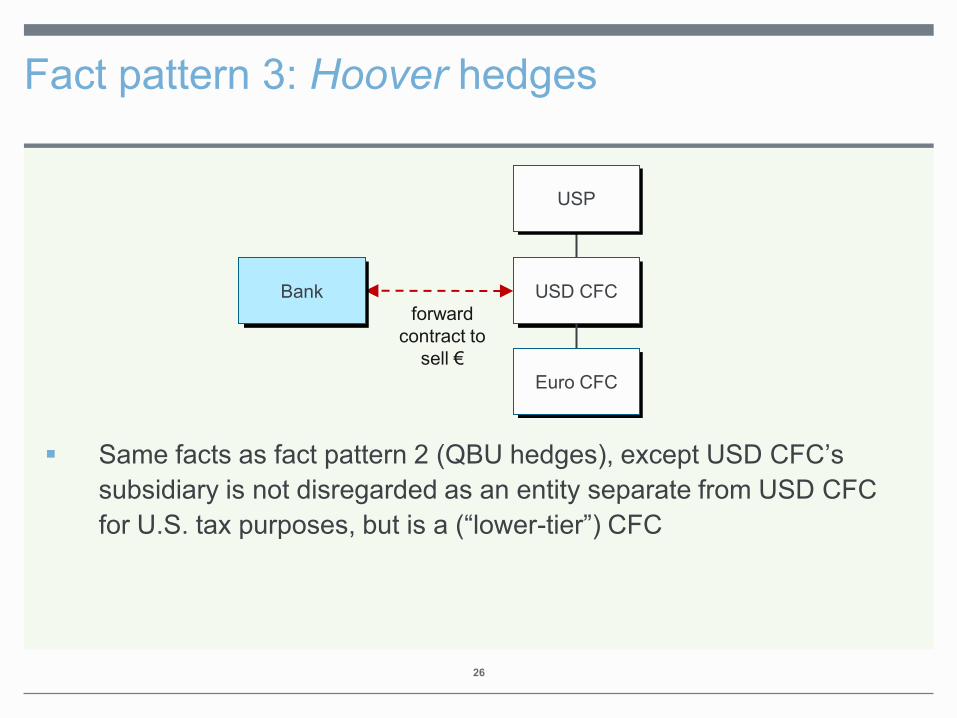

Fact pattern 3: Hoover hedges

Same facts as fact pattern 2 (QBU hedges), except USD CFC’s subsidiary is not disregarded as an entity separate from USD CFC for U.S. tax purposes, but is a (“lower-tier”) CFC

USP

USD CFC Bank

Euro CFC

forward contract to

sell €

27

Fact pattern 3: Hoover hedges Except in very limited circumstances involving members of a consolidated

group, a hedge of a position taken by a related party is not a “hedge” under Section 1.1221-2

Hoover itself rejected the argument that a taxpayer could hedge accounting volatility resulting from its ownership of a subsidiary, or receivables expected from that subsidiary

Fact pattern 3 is perhaps distinguishable from Hoover on the ground that, as a result of APB 23, a CFC can more meaningfully be said to “anticipate” (and therefore more credibly be argued to be hedging) a receivable from its subsidiary than can a U.S. person (at least, one committed to reinvest overseas earnings)

Again, note that all other things equal (which they rarely are), this issue can be avoided by checking the box for the lower-tier CFC

Michael Farber

Partner Davis Polk & Wardwell LLP Tel: 212-450-4704 Fax: 212-701-5704 E-mail: [email protected]

Mr. Farber is a member of Davis Polk’s Tax Department. He has advised clients on a variety of domestic and international transactions, including mergers, acquisitions, joint ventures and securities offerings, and he has regularly advised investment banks and other financial institutions, including JPMorgan Chase, Goldman Sachs, Bank of America, UBS and Deutsche Bank, in connection with their financial instruments, derivatives and capital markets activities.

Bar Admissions

State of New York

Education B.A., Rutgers University, 1991 J.D., George Washington University Law School, 1994

summa cum laude Book Reviews and Articles Editor, Law Review

Recognition Mr. Farber is listed as a leading lawyer in Chambers USA: America’s Leading Lawyers for Business and Legalease’s The Legal 500 United States.

Of Note

Co-Chair, Committee on Financial Instruments, New York State Bar Association Tax Section Professional History Partner, 2001-present Associate, 1995-2001 Law Clerk, Hon. H.E. Widener, Jr., U.S. Court of Appeals, Fourth Circuit 1994-1995

L.G. "Chip" Harter

Principal PricewaterhouseCoopers LLP Tel: 202-414-1308 E-mail: [email protected]

Chip Harter is a principal in the PricewaterhouseCoopers LLP Washington National Tax Practice. His practice focuses on advising multinational corporations and financial institutions on international tax planning and on tax issues arising with respect to financing transactions and financial instruments. As a senior technical review partner within PwC's national tax office, he participates in the review of the tax provisions of many financial institutions and multinational corporations. Mr. Harter joined PricewaterhouseCoopers in 1999 after having practiced tax law with Baker & McKenzie for 18 years. From 1989 through 1994, he was an Adjunct Professor of Taxation in the Graduate Tax Program of IIT Chicago-Kent College of Law. Mr. Harter is a past Chair of the Financial Transactions Committee of the American Bar Association Section of Taxation. His recent publications include: "The Devil is in the Details: Problems, Solutions and Policy Recommendations with Respect to Currency Translation, Transactions and Hedging," Vol. 89, No. 3 Taxes, p. 199 (March 2011) (with John D. McDonald, Ira G. Kawaller, and Jeffry P. Maydew); "Inherently Hedgeable: Hedging Foreign Currency Exposures Arising From Branch Operations of a CFC," Vol. 37, No. 5 International Tax Journal, p. 11 (Sept. - Oct. 2011) (with Rebecca Lee and David Shapiro); and "Hedges of Foreign Currency Risk Associated with Debt Instruments Held as Capital Assets," Vol. 36, No. 6 International Tax Journal, p. 5 (Nov. - Dec. 2010) (with Michael J. Harper). Mr. Harter earned a JD from the University of Chicago Law School in 1980, where he was Comments and Articles Editor of the University of Chicago Law Review, and he graduated magna cum laude from Harvard College in 1977. Following law school, Mr. Harter clerked for the Honorable Thomas R. McMillen, United States District Judge for the Northern District of Illinois.

Yaron Z. Reich

Yaron Z. Reich is a partner at Cleary Gottlieb Steen & Hamilton LLP based in the New York office. Mr. Reich’s practice focuses on taxation and related matters, including the tax aspects of corporate acquisitions, restructurings, insolvencies and financing techniques. He has extensive experience in international transactions, taxation of banks and other financial institutions, foreign investment in the United States, leveraged leasing and project finance, joint ventures, partnerships, real estate transactions, transfer pricing and tax litigation. Mr. Reich has published several significant articles on international tax issues and tax policy. He is distinguished internationally as one of the best tax lawyers by Chambers Global, Chambers USA, The International Who's Who of Business Lawyers, PLC Which Lawyer? Yearbook, The Legal Media Group Guide to the World's Leading Tax Advisers, The Best Lawyers in America and The Legal 500 U.S. Mr. Reich is widely published on the various aspects of taxation. His articles include: ● “The Case for a “Super-Matching” Rule,” Tax Law Review, Vol. 65 (2012) ● “International Arbitrage Transactions Involving Credible Taxes,” The Tax Magazine (March 2007) ● “Taxing Foreign Investors’ Portfolio Investments: Developments and Discontinuities,” Tax Notes (June 15, 1998) ● “U.S. Federal Income Taxation of U.S. Branches of Foreign Banks: Selected Issues and Perspectives,” Florida Tax Review, Vol. 2, No. 1 (1994) Mr. Reich joined the firm in 1979 and became a partner in 1986. He received an LL.M. degree in taxation from New York University School of Law in 1984, a J.D. degree from Columbia University School of Law, where he was a Kent and Stone Scholar and Special Issue Editor of the Columbia Law Review, in 1978, and an undergraduate degree, summa cum laude, from Columbia College in 1975. Mr. Reich served as law clerk to the Honorable Arlin M. Adams of the U.S. Court of Appeals for the Third Circuit. Mr. Reich is a member of the Bar in New York and is admitted to practice before the U.S. District Court for the Southern District of New York, the U.S. Claims Court and the Tax Court. He is a member of the New York State Bar Association and of the Executive Committee of its Tax Section, and has served as a co-chair of several of its committees.

Partner Cleary Gottlieb Steen & Hamilton LLP Tel: 212-225-2540 Fax: 212-225-3999 E-mail: [email protected]

Danielle Rolfes

International Tax Counsel Office of Tax Policy U.S. Treasury Department E-mail: [email protected]

Danielle E. Rolfes joined the Treasury Department in August 2011 as the Deputy International Tax Counsel, and has served as the International Tax Counsel since September 2012. The Office of the International Tax Counsel is the principal legal adviser to the Deputy Assistant Secretary (International Tax Affairs) and the Assistant Secretary (Tax Policy) on all aspects of international tax policy, including the development and review of legislative proposals, the promulgation of regulations and administrative guidance, the negotiation of tax treaties, and representing the United States in international organizations such as the Organisation of Economic Cooperation and Development. Prior to joining the Treasury Department, Ms. Rolfes was a partner, at Ivins, Phillips & Barker, where her practice focused on international tax planning for multinational corporations. Ms. Rolfes received her J.D., magna cum laude, from Harvard Law School in 2002, where she served as an editor of the HARVARD LAW REVIEW. Ms. Rolfes also holds an L.L.M. in Taxation (Georgetown University Law Center, 2005, with distinction) and a B.S. in Accountancy (Wright State University, 1997, summa cum laude). A certified public accountant, Ms. Rolfes is the author of AN ANALYSIS OF FIN 48 – ACCOUNTING FOR UNCERTAIN INCOME TAX POSITIONS (Matthew Bender, 3d ed. 2009) and a gold medal winner for achieving the highest score on the CPA examination in the State of Ohio. Prior to law school, Ms. Rolfes was an accountant at Procter & Gamble.

Related Documents