HOW BIG IS THE CLOUD? PHILIP GOLDIE, Director, Server & Tools OSCAR TRIMBOLI, Director, Information Worker LINUS LAI, Associate Director, IDC #apc2010.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

HOW BIG IS THE CLOUD?

PHILIP GOLDIE, Director, Server & ToolsOSCAR TRIMBOLI, Director, Information WorkerLINUS LAI, Associate Director, IDC

#apc2010

@philgoldie@oscartr

…how big is the opportunity?…where is the opportunity?

…how do I capture the opportunity?

Copyright 2010 IDC. Reproduction is forbidden unless authorized. All rights reserved.

The Cloud and You:New Delivery Models Bring New Opportunities

The Cloud and You:New Delivery Models Bring New Opportunities

Linus LaiIDC Australia

© 2010 IDC

AgendaAgenda

Shifting Business Goals Impact

Technology Goals

The Cloud: What’s It All About, & Why

Should I care?

Leveraging Cloud Computing To Benefit Your Organization

5

© 2010 IDC

Shifting Business Goals Impact Technology Goals

The Cloud: What’s It All

About, & Why Should I

care?

Leveraging Cloud

Computing To Benefit Your Organization

6

© 2010 IDC

The “New Normal”The “New Normal”

Source: IDC Server Virtualization MCS 2007, 2008, 2009; IDC Datacenter and Cloud Survey 2010

Q. Prioritize the following business goals as they relate to your organization by allocating 100 points among them. The more points you allocate, the more important the business goal.

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

January 2007 October 2008 July/August 2009

January 2010

Other

Speed time to market

Increase market share

Improve quality/accuracy

Increase revenue

Increase customer satisfaction

Reduce costs

Business priorities are quickly returning to pre-recession status

Refocusing on “doing the right thing” again, not the least expensive

• For customers• For shareholders• For competitive advantage

Efficiency still matters, but not if it impacts business performance

• Availability• Flexibility

© 2010 IDC

Recovery and TransformationRecovery and Transformation

Key Market Transformations Telecom – fiber, 3G/4G wireless,

converged IP delivery, new distribution models

IT – market expansion through disruptive Cloud model, driving re-architecture of vendor models, offerings, identities

Ascendance of mobile devices – and apps – challenging primacy of the PC

Shift of customer “design point” toward SMB/consumer, emerging markets

8

© 2010 IDC

Shifting Business

Goals Impact

Technology Goals

The Cloud: What’s All About, & Why Should I care?

Leveraging Cloud

Computing To Benefit Your Organization

9

© 2010 IDC

What is Cloud Computing Today?What is Cloud Computing Today?

High Security Cloud

High Security Cloud

High Availability

Cloud

High Availability

Cloud

Test & Dev

Cloud

Test & Dev

Cloud HPC Cloud

HPC Cloud

Comms Cloud

Comms Cloud

Low CostCloud

Low CostCloud

Multi PurposeClouds

Multi PurposeClouds

Today

The Future

Cloud services are consumer and business products, services and solutions delivered and consumed in real-time over the Internet

They have the following key attributes• Shared• Self-service• Elastic• Usage-based pricing

10

© 2010 IDC

Cloud services will not replace traditional delivery models in all situations

Though cloud is not a large part of the overall spend, it’s growing much faster

This rapid growth is attractive & causing new entrants to emerge, and non-traditional IT vendors to pay attention

The age of influence for the product vendors is waning

Cloud Market Will Win More of Australia ICT SpendCloud Market Will Win More of Australia ICT Spend

5.5%

9.4%

22.5%

AUD million

Proportion of total

CAGR growth to 2014

* DC spend is categorised by server/storage hardware and software 11

© 2010 IDC

Uncertainty About Cloud is DissolvingUncertainty About Cloud is Dissolving

In 12 months, cynicism about cloud computing has nearly disappeared Clear that cloud computing alternatives will be considered for application

upgrade and replacement

0% 10% 20% 30% 40% 50%

Using Now

Planning to use within the next 6 months

Planning to use within the next 6 to 12 months

Planning to use after 12 months

Actively researching or testing cloud computing now

Source: IDC Cloud Computing Survey, April 2010 (N=600 in Aust, Korea, India, S’pore, PRC & HK) 12

© 2010 IDC

Customer Focus on Private CloudsCustomer Focus on Private Clouds

2011 will be a big year for "private clouds"…:

Why?• Continued concerns about cloud security, availability and performance

• Ongoing drive to maximize return on existing IT assets

• 2010 has been a big year for the announcement of "private cloud" offerings from virtually all major IT suppliers

• Clouds typically package infrastructure, platforms and applications together so…

Private cloud announcements will drive many strategic partnerships, joint ventures and acquisitions/mergers.

13

© 2010 IDC

0 10 20 30 40 50 60

2010

2013

2010

2013

2010

2013

2010

2013

2010

2013

2010

2013

2010

2013

2010

2013

2010

2013

2010

2013Bu

s.

apps

/O

LTP

Dec

'nsu

ppor

tEm

ail

Colla

b.Ap

pln

dev

IT In

fr

Stor

age

&

mng

mt

VOIP

Web

in

fr.Sc

i/en

g

Responses

Public

Private

Workloads in the Cloud - AustraliaWorkloads in the Cloud - Australia

14

© 2010 IDC 15

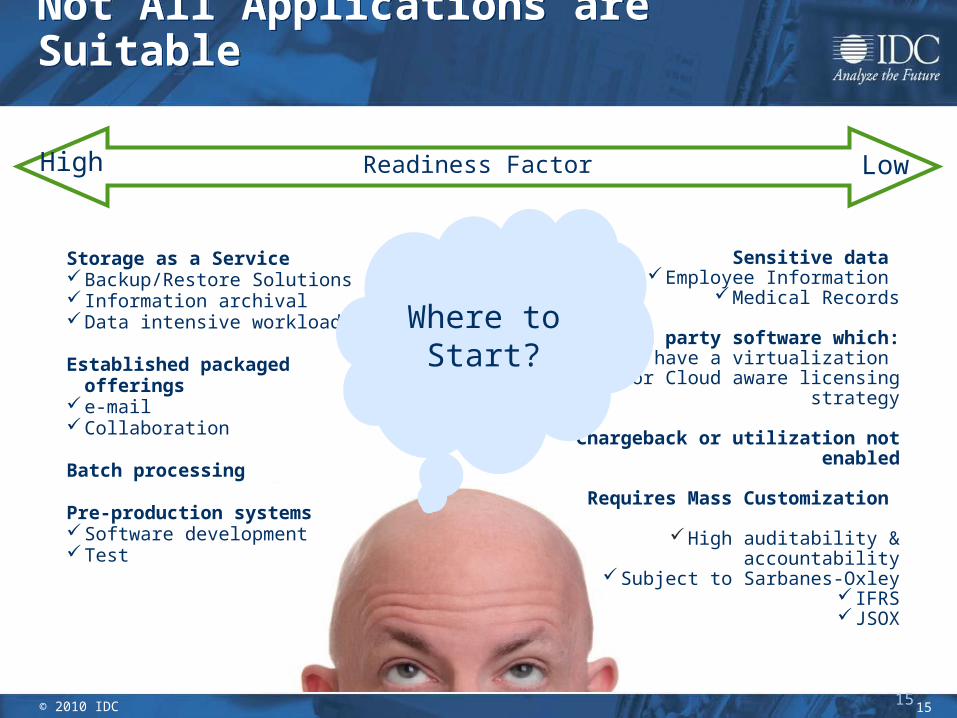

Not All Applications are SuitableNot All Applications are Suitable

Storage as a ServiceBackup/Restore Solutions Information archivalData intensive workloads

Established packaged offeringse-mailCollaboration

Batch processing

Pre-production systems Software developmentTest

Readiness Factor LowHigh

Sensitive data Employee Information

Medical Records

3rd party software which:Does not have a virtualization

or Cloud aware licensing strategy

Chargeback or utilization not enabled

Requires Mass Customization

High auditability & accountabilitySubject to Sarbanes-Oxley

IFRSJSOX

Where to Start?

15

© 2010 IDC

Cloud Stage 2009 2010 2011 2012 2013 2014

Virtualization 60% 65% 70% 80% 85% 95%

Standardization 15% 25% 30% 35% 45% 55%

Automation 15% 20% 25% 35% 45% 60%

Service level management 5% 8% 12% 18% 26% 35%

Self service 5% 7% 10% 14% 19% 25%

Investment focus areas 2009 2010 2011 2012 2013 2014Server devices Server devices Server devices Server devices Server devices Server devices

Storage devices Storage devices Storage devices Storage devices Storage devices Storage devices

C&SI Network devices Network devices Network devices Network devices Network devicesHardware, software deploy & support

Sys infrastructure management tools

Sys infrastructure management tools

Sys infrastructure management tools

Sys infrastructure management tools

Sys infrastructure management tools

Training C&SI C&SI C&SI C&SI C&SIHardware, software deploy & support

Hardware, software deploy & support

Hardware, software deploy & support

Hardware, software deploy & support

Hardware, software deploy & support

Training Training Training Training Training

Mapping the Journey:Private Cloud Adoption RatesMapping the Journey:Private Cloud Adoption Rates

A workload focus allows a cloud strategy to be builtConsider the Cloud as an extension of your sourcing strategy, not a technologyBuilding IT services in the Cloud is a long journey, comprised of many stepsHonest appraisal may reveal that enterprises cannot complete the journey on your ownSelective use of public cloud services, external private clouds and cloud appliances along

with existing delivery models will become the norm by 2015

16

© 2010 IDC

Shifting Business

Goals Impact Technology

Goals

The Cloud: What’s All

About, & Why Should I care?

Leveraging Cloud Computing To Benefit Your Organization

17

© 2010 IDC

Impact of the CloudThe Channel Viewpoint Impact of the CloudThe Channel Viewpoint

Source: IDC PartnerConnect Quick Poll (April 2010)

Do you view cloud computing as:

The majority of channels view the cloud as an interesting emerging model – and realize that it is redefining the channel

ecosystem and their business model. Importantly, 1 in 2 see it as an opportunity.

The majority of channels view the cloud as an interesting emerging model – and realize that it is redefining the channel

ecosystem and their business model. Importantly, 1 in 2 see it as an opportunity.

18

© 2010 IDC

The Move Towards ServicesImpact of the CloudThe Move Towards ServicesImpact of the Cloud

Source: IDC PartnerConnect Quick Poll (April 2010)

Do you currently/plan to offer cloud computing professional or consulting services?

Cloud is a highly consultative engagement with high professional services attach and it promotes channel transition to services

oriented business model.

Cloud is a highly consultative engagement with high professional services attach and it promotes channel transition to services

oriented business model.

19

© 2010 IDC

Channel Partners in Asia/Pacific IDC Partner Segmentation ModelChannel Partners in Asia/Pacific IDC Partner Segmentation Model

Product

ResaleServices

Product-oriented partners> 60% product

Logistic-oriented partners

Revenue: > 60% resale & <20% services

Value-added resellersRevenue: > 20% resale &

> 20% services

Services-oriented Partners

Revenue: > 60% services &< 20% resale

Hybridproduct/resale

Hybridproduct/services

Product

ResaleServices

Product-oriented partners> 60% product

Logistic-oriented partners

Revenue: > 60% resale & <20% services

Value-added resellersRevenue: > 20% resale &

> 20% services

Services-oriented Partners

Revenue: > 60% services &< 20% resale

Hybridproduct/resale

Hybridproduct/services

20

© 2010 IDC

Understanding if current Architecture (Infrastructure and Applications) is ready for Private/Hybrid Cloud

Migrating to a Cloud Architecture

Securing Converged IT Department Skill Sets

Defining Provisioning Policies when Migrating to Private Cloud

Defining Policies for Deploying Workloads in a Hybrid Environment

Charging Line of Business for Virtual Assets

Private Cloud ImplicationsWhat Activities will End-Users struggle with?Private Cloud ImplicationsWhat Activities will End-Users struggle with?

21

© 2010 IDC

Cloud ImplicationsOpportunities Require a New Mix of Skill SetsCloud ImplicationsOpportunities Require a New Mix of Skill Sets

Readiness Assessment

Services

Datacenter Assessments

Security Assessments

Application Virtualization Assessments

Cloud Strategy Development

Cloud Roadmap Development

Infrastructure Virtualization Strategy and Architecture

Application Sourcing

Strategies

Implementation &

Transformation Services

Infrastructure Virtualization

Migration Services

Application Virtualization

Services

Automation

Service Integration

Security and BCDR

Change Management

Policy Definition

Governance

Billing

Support

Multi Vendor Support

22

© 2010 IDC

Potential Go-to-Market ModelBlended Consulting & Integration ServicesPotential Go-to-Market ModelBlended Consulting & Integration Services

Customer

Vendor Account Management

Vendor Service Delivery

Sub-contractedPartners

Fu

ll S

erv

ice

E

nab

led

P

art

ne

rs

Access to Vendor/Partner Developed Knowledge Base

• A number of product (h/w & s/w) vendors are building out consulting capabilities to get their brand in front of the CIO

• However, the right skills are in short supply, so partners can and will play an important role

• Go-to-market conflict needs to mitigated and customer demand will be critical

23

© 2010 IDC

Adapt or Vanish:Hosting and Managed Infrastructure ServicesAdapt or Vanish:Hosting and Managed Infrastructure Services

Both hosting and managed infrastructure services remain viable business models,

However, it will be essential to transition delivery models to use cloud computing

The profitability of managed infrastructure offerings will rapidly erode as new players enter the market with cloud-based models

24

© 2010 IDC

Channel Partners in Asia/Pacific IDC Partner Segmentation ModelChannel Partners in Asia/Pacific IDC Partner Segmentation Model

Product

ResaleServices

Product-oriented partners> 60% product

Logistic-oriented partners

Revenue: > 60% resale & <20% services

Value-added resellersRevenue: > 20% resale &

> 20% services

Services-oriented Partners

Revenue: > 60% services &< 20% resale

Hybridproduct/resale

Hybridproduct/services

Product

ResaleServices

Product-oriented partners> 60% product

Logistic-oriented partners

Revenue: > 60% resale & <20% services

Value-added resellersRevenue: > 20% resale &

> 20% services

Services-oriented Partners

Revenue: > 60% services &< 20% resale

Hybridproduct/resale

Hybridproduct/services

25

© 2010 IDC

Potential Go-to-Market ModelPartnering to Deliver Applications via the CloudPotential Go-to-Market ModelPartnering to Deliver Applications via the Cloud

Cloud Datacenter Providers,

Telcos, Larger SIs with Cloud

Datacenter Resources

Local ISVs

Locally Delivered

Software as a Service

Platform as a Service Players (e.g. Force.com

and Azure)

• With Traditional On-Premise Licensing

International ISVs (e.g. SAP)

Internationally Delivered

Software as a Service

• Provision of a Virtualized Infrastructure for Delivery along with Customer Billing Capabilities

• Provision of a Plug and Play Cloud Infrastructure along with a Development Platform

26

© 2010 IDC

Channel Partners in Asia/Pacific IDC Partner Segmentation ModelChannel Partners in Asia/Pacific IDC Partner Segmentation Model

Product

ResaleServices

Product-oriented partners> 60% product

Logistic-oriented partners

Revenue: > 60% resale & <20% services

Value-added resellersRevenue: > 20% resale &

> 20% services

Services-oriented Partners

Revenue: > 60% services &< 20% resale

Hybridproduct/resale

Hybridproduct/services

Product

ResaleServices

Product-oriented partners> 60% product

Logistic-oriented partners

Revenue: > 60% resale & <20% services

Value-added resellersRevenue: > 20% resale &

> 20% services

Services-oriented Partners

Revenue: > 60% services &< 20% resale

Hybridproduct/resale

Hybridproduct/services

27

© 2010 IDC

Three Market Models for Reselling a Public Cloud Service…Three Market Models for Reselling a Public Cloud Service…

Referral – One time referral fee paid to reseller and

distributor

Annuity– A.k.a. pass through; recurring revenue

– May include renewals

– May include tiered programs (basic, gold, platinum, etc.)

White label – Allows partner to resell cloud service under

their own brand name

– Partner can add cloud capabilities to their other solutions and service offerings

– Pass through business model; partner gets X% gross margin

– Service delivered by cloud provider on cloud provider’s infrastructure

– Partner does first level support

Simple Referral fees are less popular, but not out of the question

Q.How would you prefer to be compensated for reselling the cloud service from a cloud provider?

Source: IDC PartnerConnect Quick Poll (April 2010) 28

© 2010 IDC

Positioning Cloud Resale for Your PartnersPositioning Cloud Resale for Your Partners

Pros Cons

Referral Program

Traditional VAR/Reseller Program

White Label Program

Ease of doing business Low partner investment and risk

Well understood business model Annuity type recurring revenue Partner maintains customer

relationship

Quick entry into cloud provider market Easy to integrate cloud offerings into

other partner solutions Partner owns the cloud brand

Not an annuity, no recurring revenue Partner less visible in customer’s

cloud planning Process intensive in two-tier model

Cloud provider must manage for channel conflict

Low margin business Will cloud providers see value of

distributors

Partner assumes more risk Tech support model complex

29

© 2010 IDC

Essential Guidance for PartnersQuestions to be AddressedEssential Guidance for PartnersQuestions to be Addressed

Private Cloud:

Have you got the right in-house skills?

Are vendors providing incentives & training for partners to develop specific skill-sets for the private cloud?

Are you able to leverage any productized professional services through from vendors to address private cloud type of requirements?

Do you have reasonable GTM conflict sufficiently addressed from vendors as you build out your own consulting capabilities?

Public Cloud:

How are you drafting commercial agreements with particular focus on SLAs?

How are you communicating your value proposition over going direct to the vendor to your customers?

What training and education are you receiving on the public cloud?

What about new consulting and integration skill-sets?

Are you involved in testing new partner programs to resell public cloud services?

30

© 2010 IDC

If you have additional questions, please contact me at:

Linus [email protected]+612 9925 2274

Questions?Questions?

31

ON PREMISE HOSTED PUBLIC

SaaS

PaaS

IaaS

$AUD 97mCAGR 44%

SOURCE: IDC

$AUD 54mCAGR 30%

$AUD 121mCAGR 58%

$AUD 128mCAGR 36%

$AUD 274mCAGR 15%

$AUD 70mCAGR 31.3%

$AUD 1,445mCAGR 7.5%

$AUD 1,622mCAGR 5.3%

$AUD 1,350mCAGR 6.2%

Wednesday September 1

Title Time Room Presenters

Microsoft Cloud Strategy 101 9:45 Arena 1B Gianpaolo Carraro

Influence of the Cloud on the Channel: How can Partners prepare themselves?

11:00 Room 8 Ted Keating (Cloud Consultant)

Successful Selling in the Cloud (Part 1) 12:00 Arena 1B Steve Iatropoulos & Partners

Cloudy With A Chance Of Virtualisation 12:00 Room 8 Jason Jacobs & Phillip Duff

Successful Selling in the Cloud: Winning with BPOS (Part 2)

13:45 Arena 1B Brian Holder & Partners

Microsoft Dynamics CRM 2011 & the Cloud

14:45 Room 7 Ross Dembecki & Craig Steere

How to Sell in the Cloud with Telstra 14:45 Room 8 Stephen Pech (Telstra) & Partners

Cloud Services Partner Panel: Partner perspectives and best practices

16:00 Room 8 Kathryn Saducas, Chris Sharp & Partner Panel

Title Time Room PresentersMicrosoft Technology Vision for Hosting and Service Providers

8:45 Room 8 Phil Meyer

Enabling Private Clouds 9:45 Room 8 Phil Meyer & Phil Goldie

Creating a residual income on-premise and in the cloud

9:45 Arena 1A

Brad Clarke

Deploying BPOS in Customer Environments

11:00 Room 8 Steve Iatropoulos, Vajira Weerakesera & Nick Beaugeard (HubOne)

Managing risk and security in the cloud: an overview of Microsoft best practice

12:00 Room 8 Stuart Strathdee

Private Cloud For The Public Sector 13:45 Room 5 Greg Stone, Philip Goldie

Land the Cloud Sale and delight your Customers

13:45 Room 8 Renee Gamble, Craig Martyn, Yvette Sutton, Phil Meyer & Kathryn Saducas

Executive Panel – Q&A with Tracey Fellows and other Microsoft executives

14:45 Arena 1B

Tracey Fellows, Evan Williams, Gianpaolo Carraro, Gary Cox, George Stavrakakis

Thursday September 2

1. attend the cloud track sessions

2. sign up today for 250 internal users BPOS at the GPS booth

3. Start the Azure conversation

the cloud #apc2010…

Related Documents