CHAPTER 1 Introduction 1.1. INTRODUCTION TO GHANA Housing is beginning to be a vital issue in government policy in Ghana, at least insofar as there is now an emerging shelter strategy.* Though government policy pro- nouncements suggest a shift to an enabling approach, the bulk of public sector funds probably continue to be spent on completed units for the few middle-class urban households. In any case, there appears to be little recognition of the credibility of renting and multi-occupancy as alternative tenure options, in spite of the fact that Ghanaian urban housing is still dominated by these two modes of occupancy. Not surprisingly, many of the housing-specific interventions devised by the state recently have failed to impact positively on the poor. With a per capita GNP value in the region of US$400, Ghana is listed as a low- income economy under the World Bank system of classification (World Bank, 1992: 214). The average rate of inflation over the 1980s was estimated at 42.5% by the World Bank (1992: 218), with a peak rate of 142% for late 1983 (Roe, 1991: 527). Recent performance has been disappointing with a deficit of C144.7 billion (C = cedis; C1000 = £1 in 1992–1993) for 1992—or 5.2% of the GDP. Much of this has resulted from the government’s handling of the economy in the run-up to the 1992 elections, when monetary policy was permitted to slip out of control in the gov- ernment’s bid to pacify a distraught electorate. 1.1.1. Accra Accra is Ghana’s capital city, principal administrative centre and the sole entry point for air travellers. The native population are from the Ga people, but like most capital cities, Accra today is very much a cosmopolitan centre. Ocial statistics put the city’s population at about 1.5 million in 1995, but many demographers and social analysts contend this is on the low side. Whatever the precise figure, most local scholars agree that the city’s population is growing at a faster rate (3.4% per annum) than the city’s managers have been able to cope with. This is not particularly surprising, given the continuing primacy of Accra, and its consequent attraction to the country’s internal migrants. *The emerging shelter strategy hardly mentions renting and multihabitation, let alone recognises their value. Housing Supply in Ghana 255

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER 1

Introduction

1.1. INTRODUCTION TO GHANA

Housing is beginning to be a vital issue in government policy in Ghana, at least

insofar as there is now an emerging shelter strategy.* Though government policy pro-

nouncements suggest a shift to an enabling approach, the bulk of public sector funds

probably continue to be spent on completed units for the few middle-class urban

households. In any case, there appears to be little recognition of the credibility of

renting and multi-occupancy as alternative tenure options, in spite of the fact that

Ghanaian urban housing is still dominated by these two modes of occupancy. Not

surprisingly, many of the housing-speci®c interventions devised by the state recently

have failed to impact positively on the poor.

With a per capita GNP value in the region of US$400, Ghana is listed as a low-

income economy under the World Bank system of classi®cation (World Bank, 1992:

214). The average rate of in¯ation over the 1980s was estimated at 42.5% by the

World Bank (1992: 218), with a peak rate of 142% for late 1983 (Roe, 1991: 527).

Recent performance has been disappointing with a de®cit of C144.7 billion

(C = cedis; C1000 = £1 in 1992±1993) for 1992Ðor 5.2% of the GDP. Much of this

has resulted from the government's handling of the economy in the run-up to the

1992 elections, when monetary policy was permitted to slip out of control in the gov-

ernment's bid to pacify a distraught electorate.

1.1.1. Accra

Accra is Ghana's capital city, principal administrative centre and the sole entry

point for air travellers. The native population are from the Ga people, but like most

capital cities, Accra today is very much a cosmopolitan centre. O�cial statistics put

the city's population at about 1.5 million in 1995, but many demographers and social

analysts contend this is on the low side.

Whatever the precise ®gure, most local scholars agree that the city's population is

growing at a faster rate (3.4% per annum) than the city's managers have been able

to cope with. This is not particularly surprising, given the continuing primacy of

Accra, and its consequent attraction to the country's internal migrants.

*The emerging shelter strategy hardly mentions renting and multihabitation, let alone recognises theirvalue.

Housing Supply in Ghana 255

The city's infrastructure (especially its arterial roads, drainage, water supply and

housing) is, in most parts, in a state of distress. Only 30.8% of the city's households

have the use of ¯ush toilets. Almost as many rely on removable buckets for domestic

sanitation. Less than 20% have functioning indoor plumbing (GSS, 1995). During

peak periods, especially in the mornings, many households are unable to draw water

from their taps, due to the sheer strain on the water network. Even more alarming is

the fact that the piped water supplied to the western half of the city is routinely con-

taminated with various bacterial agents. Along the main arterial roads and around

the central sections of the city, slow queues of vehicles are now common, owing to a

signi®cant increase in the volume of road tra�c.

In July 1995, many lives were lost in ¯oods attributed by environmental analysts

to blockage of the unmaintained urban drainage system by litter and silt, and non-

enforcement of building regulations. Since then, the Accra Metropolitan Assembly

has intensi®ed e�orts to clean up the city's landscape. Through generous Western

and Arab support, major investments are also underway to rehabilitate Accra's ailing

water, electricity, street and drainage networks.

According to data from the 1991/92 round of the Ghana Living Standards Survey

(GLSS), only 17.6% of Accra households own their homes, and 43.0% rent. As

many as 48.2% occupy rent-free accommodation. The tenure status of the remaining

1.3% is ambiguous. More than one-half (52.7%) of Accra households have use of

one room only: over 40% of these one-room households consist of four or more

members. Only 14.2% occupy three or more rooms (GSS, 1995).

1.1.2. Kumasi

Kumasi is the second largest city in Ghana and capital of the former Asante

Empire. Predominant in the city are the Akans, a group of people sharing the Twi

language, dominated by the local Asantes. The population statistics for the city are

subject to some disagreement. One of the authors estimates that in 1990 there were

about 800 000 (extrapolated from Tipple's 1986 data), but the 1984 Census (showing

a very low 490 000 in 1984) suggests that there were only about 600 000 people in the

city in 1990.*

Housing in Kumasi is dominated by compounds (57% of houses in 1986) which,

when complete, are roughly square on plan with a mean of about 12 rooms per

storey opening o� a central courtyard. As over 70% of households occupy one

room, and mean occupancy rates in the city are in excess of 3 persons per room,

single storey compounds tend to accommodate over 30 people. Multi-storey com-

pounds (16% of houses) contain a mean of 17 rooms (Malpezzi et al., 1990).

Non-compound housing tends to be in the form either of bungalows or two-storey

buildings set in relatively spacious plots or of apartment buildings of two or three

storeys. There is also a small government sector of relatively small, single household

dwellings. Though non-compound types constitute 43% of houses, their small size

*There is a general consensus that the census ®gures are low for urban areas.

256 Progress in Planning

relative to compounds reduces the number of people for whom they provide accom-

modation.

The compound/non-compound dichotomy in Kumasi tends to divide housing into

distinctly di�ering accommodation (Tipple and Willis, 1991; Tipple and Korboe,

1993; Korboe, 1992b), although there is nothing inherent in the compound form to

generate this. However, the communal life encouraged by the compound may suit

the poorer households as it improves the e�ciency of survival strategies such as

informal child care and mutual assistance in times of need. Households in the com-

pound houses tend to occupy single rooms and have particularly poor access to ser-

vices.

In 1986, only 12% of households in Kumasi (almost all of whom are in non-com-

pound housing) had a toilet which was not shared with other households and 30%

had no access to a toilet in the house (and most of these were in compounds). Even

when a house has a toilet and it is shared (as most are), the utility it provides may be

very low. In areas such as Mossi Zongo and Atonsu, each tap is shared by 102 per-

sons, or 24 households, and each toilet by 156 persons, or 31 households (Korboe,

1992b). Owners have tended to have much better access to services than other tenure

groups; 46% having exclusive use of a toilet and only 14% having none (Malpezzi et

al., 1990).

Further details on housing conditions in Kumasi can be found in Hellen et al.

(1991), Malpezzi et al. (1990), Tipple and Willis (1991) and Willis et al. (1990).

1.1.3. Berekum

According to Berekum's oral history, the town was established in the late 18th cen-

tury as a hunting-post settlement by an Asante chief. Thus, many of Berekum's `indi-

genes' see themselves as originating from Ashanti.

In the 1940s and 1950s, Berekum boasted a relatively large number of successful

cocoa planters, many of whom backed Busia's opposition United Party against

Nkrumah's Convention People's Party. According to McCaskie (1991: 512), these

``[capitalist cocoa farmers] . . .were opposed to the CPP's state-controlled cocoa-mar-

keting system''. The Berekum Traditional Council reports that many of the more suc-

cessful and powerful citizens ¯ed Berekum and other Brong towns under persecution

from Nkrumah. Most, but certainly not all, of them returned after Nkrumah's down-

fall in 1966.

In descending order, the main occupations are farming, trading and woodworking.

Both food crops and cash crops are grown. In the food crop sector, there is about an

even mix of subsistence and market-scale operations. With the continuing trend of

falling real earnings from cocoa, many cocoa planters have converted to food crop

production in recent years. The shift to food crop farming is made more inevitable

by the fact that many of the older cocoa plantations have been inherited (inevitably)

by joint heirs who have subdivided the original pro®table farms into holdings too

small to be pro®table as cocoa farms. In spite of the shift reported above, there

remains a signi®cant number of indigenes with substantial cocoa farms in the

Housing Supply in Ghana 257

Ashanti and Western Regions. It may be that far-o� farms are less attractive for

relocation, hence a lower rate of e�ective subdivision.

The 1984 population census, deemed by local demographers to have under-enum-

erated urban populations gave Berekum's population as 22 264. We are informed by

community leaders that many of the larger properties in town belong to absentee

cocoa farmers and that a fair proportion of high-cost newly built houses belong to

so-called `Burgers' (a generic expression, derived from Hamburger, referring to

Ghanaian expatriates in Germany).

1.2. INTRODUCTION TO SUPPLY ISSUES

The components of housing supplyÐland, ®nance, building materials, labour, in-

frastructure, and the regulatory frameworkÐare dealt with brie¯y below in order to

establish the context within which housing developers work in urban Ghana. It has

been argued by many academics and sta� at the World Bank (1993) that the e�ec-

tiveness of housing supply is so closely tied up with these components that, by

enabling the e�cient supply of each (and the minimum disturbance caused by the

regulatory framework in reaching its ends), the supply side will be able to cope with

demand. While there are obvious problems with this argument for people at and

below the margin of a�ordability, the health of each component is, indeed, pertinent

to our discussion here and we will spend some time on them.

1.2.1. Land

The means of land allocation and leasing conditions in Ghana are well documen-

ted elsewhere (for example, Bentsi-Enchill, 1964; Ollennu, 1962). Most land in

Kumasi and Berekum is owned by stools, the symbols of authority of land-holding

kin-groups (abusua), under the allodial right of the Golden Stool of Asante. The allo-

cation of land for lease is in the hands of chiefs under the Asantehene's Lands O�ce

who can alienate land to members of the stool (as of right) or strangers in exchange

for a tribute, known as drink money (biri nsa) which, in Kumasi, now represents a

market value. Land title registration and document processing procedures are still

centralized in Accra.

For land in Accra, the owning bodies are represented by chiefs (Mantsemei), fetish

priests (wulomei), quarter heads (akutseiatsemei) and family heads (HUDA, 1990).

While there are some areas where stools gained the rights to allocate land (particu-

larly in Labadi), most quarter heads have remained in control of their land. There

are also some land-owning families. This rather complicated set of, often overlap-

ping, land allocating entities, has led to many very clouded titles with the subsequent

delays in development, legal costs, and multiple payment for the right of use of the

land. Recently, as part of the new stress on urban management, the land registration

system in Accra is being overhauled as a precursor to a national land registry.

258 Progress in Planning

In both Kumasi and Accra there has also been a `modern' sector, where land is al-

located through freehold or leasehold and administered directly by the government's

Lands Department.* In Kumasi, access to the few state-managed plots is becoming

very di�cult, even for the in¯uential. Although, o�cially, all of Kumasi's state-con-

trolled plots have already been allocated, some vacancies exist in the signi®cant num-

ber of allocated plots which have not yet been built on. Land law{ allows the

repossession of such plots for subsequent reallocation, but because de facto title

holders tend to command in¯uence, public servants charged with the responsibility of

administering state lands have di�culty re-entering such plots.

Each of the three urban centres under study has only an insigni®cant number of

freeholds. For Accra, records at the Lands Commission Secretariat indicate that free-

holds account for less than 0.1% of the total land area. State-controlled land is just

under 13%.

Speculation does not appear to be practised on a very large scale in Accra,

although it was more common in the 1970s. An average speculator tends to hold

only two or three plots and concentrates on the choicest locations and government

land (East Legon is particularly notorious in this respect). The prevalence of land liti-

gation in Ghana is likely to be a major deterrent. The few real estate developers who

are active are substantially expanding their acquisitions, even in the face of an o�cial

ban on grants of Accra stool lands since February 1991. Hearsay evidence suggests

that a small number of foreign nationals, mainly Arabs, are speculating on a small

scale in land.

Plots in Ghana are large by international standards. In established settlements in

Kumasi, such as Asokwa, Ayigya, Ridge and Patasi, the survey team found typical

plot measurements of 50� 70 m, 40� 66 m, 30� 40 m and 33�36 m (between 1200

and 3500 m2). Plot sizes of 26� 40 m, 30� 33 m and 26� 33 m (970±1040 m2) are

becoming increasingly common in less established parts of the city where chiefs are

carving out smaller, but still substantial, plots to maximize their gains.

In Kumasi, plots will typically have un-built space around 82±86% for villas (¯oor

space indices of 14±18%).{ Even at Suntreso, a government-built low income estate

with plot sizes only half as large as standard plots in the city, only 55 m2 of built

area were constructed on plots of 400 m2.

In Accra, the Tesano CFC Estates (low-density, middle-class housing) has net plot

sizes of 57� 33 m (about 1880 m2) and only four plots per hectare. The combined

e�ect of large plots and small built areas is low-density urban sprawl, resulting in

higher infrastructure costs and, therefore, a negative impact on prospects for servi-

cing.

Berekum's allocation system is unlike the other two and appears to be particularly

equitable. A written application (stating the broad purpose) together with a passport-

sized photograph must be submitted to the Traditional Council. The potential lessee

*There are no new freeholds currently being granted in Accra.{Speci®cally the Administration of Lands Act and the Conveyancing Decree (Act 123 of 1962 and NRC

Decree 275 of 1973 respectively).{Computed from data obtained from 43 randomly selected villa sites, supported by a small selection of

architects' designs at the Faculty of Environment and Development Studies at UST.

Housing Supply in Ghana 259

is then required to attend an interview to justify his application. Only if an appli-

cation is approved is the applicant made to pay the (token) fee (this is very unlike

the system in Ashanti and most other Ghanaian stool land areas). The fee for a 99-

year lease is a ®xed C25 000 (£25), irrespective of the applicant's place of origin, or

the location or size of the plot (plots average 26� 33 m, 958 m2). Out of the standard

fee, C4000 goes to the surveyor as remuneration, C9000 is paid to the District assem-

bly for development purposes and C12 000 is paid into the Traditional Council

account to pay expenses, and tributes to the paramount chief (omanhene), the queen

mother and divisional chiefs.

Administering the system is a Joint Allocation Committee comprising two mem-

bers of the Berekum District Assembly (essentially an elected body), four members of

the Traditional Council (i.e. chiefs), the Planning O�cer for Berekum, and the

Registrar of the Berekum Traditional Council (ex-o�cio). Each applicant is entitled

to one plot. If an applicant is deemed too young (under 20 years), the application is

deferred. A few applicants are rejected, mostly on account of drunkenness and this

holds for life. Traditional Council plots are now only available on the periphery of

Berekum. Central plots are more expensive, at a minimum of C400 000 and are only

accessible through native speculators.

Commercialization of community and ancestral land in Ghana is becoming

increasingly common; from pure tribute before the 1960s, drink money has become a

notional market price in modern times. In areas where the demand for residential

land has outstripped the pace at which the planning authority prepares its sector lay-

outs, land-holding chiefs are resorting to preparing their own (parallel) layouts.

While the frustration of such land-holders is understandable, the practice worsens an

already confused situation in which land documentation is grossly inadequate and

litigation rife.

Ministry of Works and Housing records show land litigation cases in Ghana conti-

nuing to rise. From 13 000 recorded in 1991, to 16 000 by March 1993. Among the

main reasons adduced by Lands Commission o�cials are:

. the complexity of title transfer and processing procedures;

. joint inheritance practices, and the resulting need to negotiate with several parties

rather than with one owner;

. multiple allocations by chiefs: such practices are essentially fraudulent, since chiefs

have accurate information on the status of plots within their jurisdiction;

. in some cases, litigation arises because of boundary disputes (Ghana lacks an e�-

cient cadastre).

1.2.1.1. Squatting. In most developing countries, squatting has been an alternativehousing supply strategy for many of the poor. In Ghana, however, it is very rare,owing mainly to the close watch kept on land by local chiefs and, perhaps, a fear of¯outing supernaturally underpinned laws of land occupation (Korboe, 1993a;Konadu-Agyemang, 1991; Tipple, 1984). There is a well-known informal settlementnear Accra, Ashaiman, which was acquired and partially developed by the state (as

260 Progress in Planning

temporary? dormitory housing for the workforce employed to construct the Tematownship and as a resettlement camp for households displaced in the creation of theindustrial town). Because it is government-owned land, it attracted others whomoved in as squatters. Elsewhere, however, there is little government land and squat-ting is largely restricted to high income households with in¯uence. In Kumasi, high-cost squatter housing may be found at Adiembra, where the state claims to haveacquired (but not paid the relevant compensation in respect of) a large parcel of landintended for a `working class' (TUC) housing estate.

The 4th Republican government has recently approved the regularization of titles

to in¯uential invaders of state land in the Kwashiman area of Accra on a site orig-

inally intended for a stadium. Within the same period, low-income households were

being evicted from public land at Agbogbloshie (also in Accra), where some 400

houses were a�ected in the dawn swoop of 31 July 1993. However, the households in

question were not squatters (invaders) in the regular sense as the Accra Metropolitan

Authority seeks to portray. Rather, they were people whose lands had been compul-

sorily acquired in the 1960s under authority of the Accra Industrial Estate

(Acquisition of Lands) Ordinance No. 28 of 1956. Since the relevant compensation

was paid by the state at the time of acquisition, and the land subsequently allocated

to Accra Brewery Ltd for industrial development, the a�ected households were

deemed to have lost their rights to the land.

In discussing prices of land, we are referring to the amount of drink money paid

for a lease of 99 years which provides rights of surface user (usufruct) to a holder

from outside the lineage in whom the land is vested. In Kumasi, unserviced plots in

so-called ®rst class residential areas* attract lease prices of C2.5±4.0m; second class{attract C1.5±2.0m; and third class{ command C600 000±800 000. Some areas are es-

pecially attractive. The old colonial layout in the Ridge area fetch C5±6m per plot.

In June, 1993, sub-leases on serviced peripheral plots (at Atasomanso) were being

granted for C3m (Parakuo Estates Ltd, Kumasi); serviced plots at Kentenkrono were

C2.5m.

In Accra (August 1993), Ofankor plots (state plots o�ered on `kalabule'} terms)

were priced at C3±4m, although, for well-connected people, they could be obtained

o�cially through the Lands Commission for C1.8m plus C80 000/acre annual ground

rent; similarly government land at East Legon was on o�er at C12±15m kalabule for

half acre plots. At Airport West and East Cantonments estates, government plots

were available at as much as C20±25m through kalabule. Stool land at South

Ofankor was in excess of C2m for half an acre; Abofu plots (near Achimota Forest)

were C5m for 33� 33 m); at East Legon it was C7±10m for 25 m� 33 m to

*1st class includes: Asokwa and New Amakom, Atasomanso, Adiembra, Adiebeba, Ahodwo, AyigyaWest, Bomso, Danyame, Fankyinbra, Nhyiaeso, Patasi, Ridge, West Kwadaso.

{2nd class includes: Old Amakom, Asafo, Bimpeh Hill, Ayeduase, Anwomaso, Asokore Mampong,Kentinkrono, Dichemso Extension, Chirapatre, Gyinyase, Kwadaso, Manhyia Extension, New Tafo,Suntreso, Santasi.

{3rd class includes: Aboabo, Abrepo, Ahinsan, Akorem, Asuoyeboa, Old Atasomanso, Old Ayigya, Boadi,Emena, Breman, Bohyen, Asawasi, Old Tafo, Pankrono, Oforikrom.

}The term kalabule was commonly used before the 1981 Revolution to refer to the black market operatingin every conceivable good available and the high cedi prices of those goods. Its pejorative implicationhas, perhaps, heightened since Ghanaians have become used to life without a black market.

Housing Supply in Ghana 261

33� 33 m; at Amasaman: C600 000±C1m; and in the Kaneshie highway area, marshy

plots of 33� 46 m cost C3m.

These `prices' are very high for Ghana, but not in international terms. The see-

mingly astronomical (in Ghanaian terms) C25 million (C25m) is £25 000 (at 1993

conversion rates) and this `buys' over 1000 m2 of prime residential land on which

would be built a house worth £50 000±100 000 or more. The more usual C2m (£2000)

plot would be the basis for a house costing in excess of C20m (£20 000). Thus, land

cost is only 10% of building cost.

1.2.2. Finance

The World Bank recently reported that, among the countries for which it had rel-

evant data, Ghana had the highest house-price to income ratio (World Bank, 1989:

ii). In this context, it is particularly serious that formal sector housing ®nance is vir-

tually non-existent, indeed the formal ®nancing sector is relatively poorly developed.

It is reported* that only 10% of the nation's money supply (estimated at C88 bil-

lionУ88mÐin March 1993) is immediately available to the formal banking system

(about £9m). Thus, though people may be poor on average, there is a substantial

volume of cash in the informal sector which could be utilized for development pur-

poses. By devising truly encouraging interventions, it may be possible to attract such

latent capital for low-income housing investment. However, to date, government

intervention in housing ®nance has been ine�ective in serving the vast majority of

people.

As the highest interest rate reported for deposits over the period was only 16%, it

is not surprising that the savings/GDP ratio never rose above 4.34% (Osei, 1993).

GDP is reported to have grown at some 3% per annum over the same period. While

there have been de®nite improvements in economic performance since the mid-1980s,

when the government adopted tough adjustment measures as a pre-requisite for

further donor lending, these have been dampened somewhat by the double burden of

debt servicing and deteriorating terms of trade.

The major thrust of government housing ®nance currently is the Home Finance

Company (HFC). Lending portfolios of other public housing ®nance institutions

(Bank for Housing and Construction and the First Ghana Building Society) are

altogether negligible.

Incorporated in mid-1990, HFC administers three main schemes at present:

1. The 5-year pilot scheme (1991±1995) for which applicants are required to purchase

their housing new from registered real estate developers. Budgetary provision has

been made for some 3000 dwellings under this scheme at a concessionary real

interest rate of only 3.5% indexed to in¯ation. A 20% down-payment is required.

*According to Bank of Ghana sources referred to by the Managing Director of the Home FinanceCompany during a presentation at National Shelter Strategy Seminar, Accra, 4th, March, 1994.

262 Progress in Planning

2. The non-resident scheme under which expatriate Ghanaians, particularly those in

Western Europe, are being encouraged to own homes in Ghana. The real interest

rate for this category is 4.5%.

3. The uncompleted house scheme which allows applicants to take loans for complet-

ing outstanding works. Again, the real interest rate is 4.5%.

By 26 July 1993, applications under the pilot scheme (1) totalled 884 (worth C5.00

or C5.6m each), of which 800 had been approved (worth C4.443 or C5.5m each) and

disbursements had been made to 339 (worth C2.029 or C6m each). The gap between

approvals and disbursements is due wholly to developer delivery shortfalls. The bor-

rowers were all public servants, owing to the certi®able income requirement in the

collateral clause, and about 90% had institutional assistance from organizations such

as the Ghana National Petroleum Corporation, the Ghana National Procurement

Agency, the American-owned Volta Aluminium Company, and the Posts and

Telecommunications Corporation. No speci®c rationing mechanisms are applied

except those implicit in the points above.

The in¯ation rate used for interest determination is that declared by the Statistical

Service in its combined CPIs. From project take-o� in October 1991 up to July 1993,

the rate applied has averaged about 18% per annum, thus loans are charged for at

21±23% per annum.

HFC is seen by its o�cials primarily as a viable ®nancial enterprise; they have no

delusions of its being a major lender for low-income housing activity. Policy-makers,

on the other hand, have often advertised HFC as the long-awaited solution to the

problems of low-income housing ®nance. The extent of subsidy on HFC loans can be

judged through comparison with other loans. In July 1993, the bank rates for bor-

rowing ranged between 29 and 38%, with the lowest values reserved for agricultural

investments and the highest values applicable to the construction sector.

Registered private developers (the only suppliers whose products are acceptable to

the HFC) in search of economic viability ®nd it necessary to build for upper sectors

of the market. Thus, their houses are only a�ordable to public corporations and indi-

viduals with very high incomes. It is an open secret that a sizeable proportion of

such money comes from overseas employment and from dubious local and foreign

sources. Thus, the subsidized interest rates, paid for by the public purse, are redistri-

buting income from the poor majority to the fortunate few.

None of the above is available for the majority who develop in any informal way;

through not being one of the few registered real estate developers (members of

GREDA), through not having more than a traditional land lease (as land held thus

cannot be used as collateral), through not having planning permission, or any of the

other common disquali®ers from the formal sector which a�ect most housing actually

occupied by the poor.

1.2.2.1. Subsidies. Rent Controls are probably the main subsidy a�ecting poor resi-dents; a subsidy carried by landlords. PNDC Law 138 of 1986 forbids landlordsfrom raising rents without prior approval of the Ministry of Works and Housing. LI1318 of 6 March 1986, which raised o�cial rental levels 10-fold but still ®xed themat very low levels (C300 for a sandcrete room in a shared house), had a tenure of

Housing Supply in Ghana 263

one year and has therefore expired, in theory. However, the rent courts continue todetermine cases on the basis of rent levels stipulated in that legislative instrument. Ina tenancy adjudication at the Accra Rent O�ce in 1993, for example, it was ruledthat the landlord had no right to charge more than C410 for chamber-and-hall ac-commodation (a suite of two rooms) (Daily Graphic, 30 August 1993: 1). The land-lord had demanded C5000 from the tenant.

Rent controls have certainly in¯uenced the supply of rental accommodation, but

probably not as much as previously thought (e.g. in Malpezzi et al., 1990; Tipple and

Willis, 1991), because of the non-pecuniary nature of most rental housing supply in

Ghana. In emphasizing the `peace of mind' aspect of supply motivation, many of the

landlords in our sample compare to those in Mexico City, of whom Gilbert (1993:

53) states: ``landlords are not greatly concerned about the low rents they receive

because their main reason for building is to own property.''

1.2.2.2. Rents and advance rents. In this low rent regime, in which mortgage ®nancingis lacking for all but the wealthiest urban dwellers, advance rent has, since the mid1980s, become an important way for owners to raise money to invest in extendingtheir houses. A large numbers of months' rent are now demanded both from newtenants and from those who are currently in residence as a substitute for subsequentmonthly payments. The authors also found evidence that landlords are increasinglyasking prospective tenants to build the required rooms (or else advance the full con-struction capital), the cost of which is then amortized against monthly rent values.

According to the Rent O�cer in Kumasi, interviewed in July 1993, the monthly

rent payable on single rooms is generally in the region of C2000.* Landlords and

tenants simply negotiate satisfactory rent levels. The Rent O�cer holds the view that

it is not unreasonable to evict tenants who insist on paying rents at the unrealistic

levels prescribed in PNDCL 138/LI 1318 (both of 1986), because the legislation has

actually expired even though it is still being applied by some authorities. According

to a few accommodation agents who have now set up in Kumasi, advance payments

are about 3 years rent or about C250 000 for single rooms and C1.5±3.6m for self-

contained accommodation.{Korboe's (Korboe, 1992a) prediction that housing could become more marketable

if it made economic sense seems to be supported by the rate at which residential

rooms are being converted to commercial use (service workshops, retail and whole-

sale outlets, etc.) in areas that have recently become accessible (as a result of the

road improvement programme). In areas such as Asafo and Ashanti New Town

where demand is high, there are many reports of eviction to allow such conversions

to be e�ected; in family houses along principal streets, some rooms have been

swapped so that street-side rooms are now held by the more prosperous who are

able to invest in commercial ventures. Often, these members would convert their

rooms to commercial uses and rent rooms elsewhere. General house improvements

are sometimes provided by would-be converters as a means of encouraging the co-op-

eration of resident members and unwilling family heads.

*This is C500 higher than our data show (see later).{This is twice the levels claimed in our data.

264 Progress in Planning

1.2.3. Building materials

During the 1970s and early 1980s, there were grave problems in obtaining building

materials. In 1980, for example, cement could be obtained at a government-con-

trolled (subsidized) price through o�cial channels which were very slow (but open to

corrupt payments), or through the black market at about 20 times the controlled

price. In either case, shortage was endemic. Now, however, although it is reported by

the World Bank (1990: 44) that there is (or, at least, was at the time of that study) a

routine shortfall in cement supply, building materials can be obtained reasonably

easily and there are many retail outlets in the major towns. In general, cementitious

products and components (sandcrete building blocks and in situ concrete elements)

are favoured by builders and house-owners alike, but they are not wet-cured; rather,

they are deliberately exposed to the sun to speed the drying process which consider-

ably reduces their strength.

The majority of sandcrete blocks are produced by small-scale entrepreneurs using

labour-intensive production methods and moving from site to site. Often, the sand

used is contaminated with pieces of polythene, stones, roots and other vegetable mat-

ter, and the mixing process is less than thorough. Mixes are weak by textbook stan-

dards. The standard mix required by regulation is 1 part cement to 6 parts sand, but

some use 1 to 9 so that one 50-kilo bag of cement is used to produce 25, 125 mm

blocks (i.e. 125 mm thick�300 mm high� 450 mm long). More commonly, the

cement is stretched even further to get about 35, 125 mm blocks from a bag of

cement at 1 part cement to 12 parts sand. Though most blocks are compacted satis-

factorily in purpose-built manual presses imported from overseas, a few manufac-

turers simply pat the damp mix into shape in wooden moulds. In such instances,

compaction pressures can be very low indeed. Notwithstanding the inadequacy of

curing practices and the routine presence of contaminants in sandcrete mixes, the

blocks produced have, so far, proved quite adequate for low-strength applications

such as simple, single-storey house construction.

Corrugated aluminium has replaced corrugated galvanized iron as the roof clad-

ding material of choice. The micro-concrete tile has been popular since its introduc-

tion in the late 1980s, but its use is restricted to high-cost housing because its weight

implies a need for more elaborate wood framing. As timber is increasingly valuable

as an export, sawn timber for extensive rafters and purlins has become rather expens-

ive in recent times. Ultimately, this has led to a situation whereby, for low-income

households at least, the micro-concrete tile roof is not a realistic alternative to the

traditional metal roof (Table 1).

1.2.4. Labour

Construction labour is relatively easy for a house-owner to obtain. Skilled labour

is typically engaged by recommendation. In the case of unskilled labourers, the pro-

spective builder will either advertise his need verbally (through friends and/or rela-

Housing Supply in Ghana 265

tives) or else he will rely on the skilled hands he has engaged to provide the required

number of labourers.

Porterage on building sites is dominated by (though not exclusively reserved for)

women, who are cheaper to employ and less demanding, possibly from a local per-

ception that women are less e�cient on manual jobs. Unskilled labour is daily-rated

at C1200±1500, with the lower rate paid for work with materials such as soil and

building blocks and the higher rate paid for (heavier) concrete mixes. On sites with

all-male labourers, C2000 is more common.

Masons earn about C2500±3000 for a day's work (C3000±3500 for master builders;

C4000 for relatively highly skilled technical school graduates able to read and inter-

pret drawings). Equivalent rates apply for carpentry and joinery works. Workers are

typically paid daily (at the close of work). The work-day on building sites usually

runs from 7 a.m. to 2 p.m. with a short break (about 30 min). On sites where all

workers are paid daily rates (still the most common approach adopted in house con-

struction), the owner will either undertake the supervision personally or ask a trusted

relative to do it on his behalf.

Alternatively, but less common in house building, the owner may invoke a phased-

task contract (PTC) system in which workers are contracted to complete a speci®ed

piece of work for an agreed sum, irrespective of the actual time input. The contract

is normally taken on by a master-builder who will recruit and pay his own wage-

workers. Typically, a sum will be advanced by the owner to help the master-builder

to discharge his ®nancial responsibilities.

A common practice in the PTC system is to break the entire job into three phases:

®rst, to the completion of the substructure; then up to the lintel; and ®nally, to the

conclusion of the entire works. Three distinct quotations will be provided by the con-

tractor to cover the three separate phases of construction. Each of these three phases

will generally be paid for in two equal instalments (at the commencement and on

completion of the contracted task). Skilled artisans and supervising foremen are com-

monly paid in instalments for PTC work.

For simple construction works, the master-builders are reasonably competent in

terms of their building skills. Typically, however, the way in which their fees are

determined is arbitrary, often owing more to the perceived income of the client rather

than the cost of the job; a rich client will be asked to pay more than a poor one.

TABLE 1. Prices of building materials (July 1993)

50 kg bag of cement C3200 in Kumasi (plus C140 transport and loading)Pack of 20 pcs 1.3� 2.6 m corrugated aluminiumroof sheets

C110 000

150� 300� 450 mm solid sandcrete block C200Wawa (relatively cheap softwood) C44 000 per cubic metre600 mm Naco-louvre blade C600 clear, or C650 frosted8-blade-height Naco-louvre carriers C8000 per pair1.3 m-wide, 1 m high jalousie window (includingframe) ®tted4 with glass (`Naco') louvres

C10 000 plus C3000 for burglar-proo®ng

4.5 litres of emulsion paint C30004.5 litres of oil paint C70001 cubic metre (approx. 1 tonne) of builder's sand C20001 cubic metre (approx. 1 tonne) of coarse aggregates C20 000

266 Progress in Planning

Artisan training is provided in two main ways. One route is through the polytech-

nics, technical schools and, in theory, the Junior Secondary Schools (JSSs). More

commonly, however, skills are simply acquired through apprenticeship.

1.2.5. Infrastructure

In most newly developing areas of Accra, Berekum, Kumasi and virtually all other

Ghanaian towns (with the exception, perhaps, of the planned port city of Tema), ser-

vicing lags behind building development. Currently, only eight of the country's 110

district capitals have comprehensive piped water networks (Economist Information

Unit, 1993: 16). At city level, the Ghana Water and Sewerage Corporation (GWSC)

is responsible for the treatment and supply of water as well as for drainage and sani-

tation. In the rest of the country (outside the three cities and a few of the other re-

gional capitals), responsibility for drainage and sanitation is divested to District

administrations.

As a means of improving overall access to basic servicing, the Ministry of Works

and Housing is seriously considering establishing an Infrastructure Fund from which

real estate developers can borrow. According to ministerial o�cials, such borrowing

is intended to serve primarily as bridging ®nance (rather than a gift) to help develo-

pers overcome some of their cash-¯ow problems. Lending to the real estate sector

would be at concessionary rates. It is not entirely clear how the seed capital would

be raised, except that the Ministry expects support from the World Bank, the

Ministry of Finance and local authorities. In the case of roads and drains, costs

would be recovered through property rates payable to the local authorities.

As usual, the stated emphasis is on low-income households, but the eventual out-

come is likely to be very di�erent. Just as existing ®nancial concessions to the real

estate lobby have failed to produce the anticipated low-cost housing units, the pri-

mary bene®ciary of this additional incentive is likely to be the formal sector develo-

per. Should this occur, the concession would be regressive, considering that the state

would not only be foregoing valuable revenue, but also taxing the poor to further

enrich the already wealthy realtor. If the broad plan should be pursued, therefore,

some redesign would be necessary to address this anomaly.

1.2.5.1. Water supply. Accra receives its water from two main catchments: the Kpongand Weija dams. These provide a daily output of 180 million and 86 million litres re-spectively, against an estimated 364 million litres of demand (GWSC ®gures).

In parts of Accra (e.g. Odorkor, Dansoman, Korle-Bu and Osu), supplies are only

reliable late at night or sometimes at dawn, forcing people to keep unsocial hours in

order to get a bucketful. Even in some more fortunate areas, water will only run

from upstairs taps when all those at ground ¯oor level have been turned o�. A simi-

lar situation prevails in parts of Kumasi as well.

It is reported for Kumasi that each water connection is shared by 46 persons (or

10 households) and that 58% of households have on-site connections (Kumasi

Health Education Project: KHEP, 1993). The situation is obviously worse in

Housing Supply in Ghana 267

Berekum. For a signi®cant proportion of the population also, contamination is a real

risk as a result of inappropriate water storage practices, which themselves betray the

unreliability of supply.

Statistics of persons per tap do not fully re¯ect the level of adequacy because

pressure is often low and taps can be dry for days, especially in elevated locations

and in poorer areas where the branch mains are inadequately sized. A multiplicity of

long private connections, improperly laid pipes and exposed lines easily su�ering

damage, are common in poorer areas and render supplies prone to contamination.

In Berekum, the water supply network is restricted to so-called primary lines. The

maximum connection length permitted from these is 400 ft, beyond which pressure

tends to drop to ine�cient levels. It is not surprising, therefore, that the overwhelm-

ing majority of houses in Berekum are without water connections. Gross pumping

capacity of the two mechanized boreholes is 27 000 l hour, the high-level tank holds

230 000 l. The town has 12 operational standpipes for which attendants have been

appointed. At these, water is sold for C10 per 18 l bucket. The GWSC revenue at-

tendant, regarded as a registered vendor, receives payments from drawers on a pay-

as-you-draw basis. Peak drawing periods are: 5.30±8.00 a.m. and 5.00±7.00 p.m.;

although pressure at night is adequate, the standpipes are locked between 9 p.m. and

5 a.m. As it is markedly more pro®table to sell through registered vendors, there

appears to be little incentive for GWSC (Berekum) to extend connections to unser-

viced houses.

GWSC in Berekum is reportedly unable to ®nance the purchase and installation of

meters for all service outlets. Thus, ¯at rates are applied depending on water-consum-

ing facilities and estimated number of persons. It is no secret that, with unmetered

supplies tending to be cheaper than metered ones, some owners of serviced houses

resell water to the public at a pro®table C10 per bucket; others permit unlimited

access to speci®c households for ®xed monthly fees.

During an observation of a public standpipe in Berekum, there were 46 buckets at

the standpipe at 6.20 a.m. and it took 1.5 min to ®ll a bucket under normal pressure

conditions. At 9.00 a.m., there were 22 buckets in the queue and it took nearly 5 min

to ®ll an average-sized bucket; clearly, search costs for water are high (in terms of

time). When one of the two functional boreholes is out of order, some of the town's

taps remain dry for a full week. Also, taps sited on high ground only have water

when the town's high-level tank is full. Under GWSC's Immediate Action Plan

funded by the ODA, Berekum is receiving two additional boreholes to supplement

the two functioning ones.

Key problems identi®ed by GWSC are the need to renew cast iron distribution

lines and the multiplicity of independent connections (incomprehensive networking)

which result in serious pressure losses. In spite of the inadequacy of potable water

supplies, about half of Ghana's treated water is lost through leaks and burst pipes,

according to the MoWH, which has instructed GWSC to address the leakage pro-

blem or else be denied approval for future tari� increases.

In urban areas, Ghana Water and Sewerage Corporation (GWSC) has discontin-

ued day-to-day management of state-owned standpipes, mainly because of misuse

and di�culties in recovering costs. As we have seen in Berekum, the practice of

268 Progress in Planning

water vending by small-scale private entrepreneurs has been formalized in place of

direct state control. There are 13 registered vendors in Accra (all in low-income hous-

ing areas). According to the Commercial Manager, this approach represents the

Corporation's new strategy for servicing low-income urban settlements.

Water charges are based on an increasing block tari� (IBT) system, costs per gal-

lon rise as consumption increases at the meter. Charges vary from C0.414 for the

®rst 13 600 l to C2.038 for after 900 000 l per month. This discriminates against

sharers and is particularly inappropriate since it is the urban poor, typically residing

in multi-occupied properties, who are penalized. Unmetered premises pay the mini-

mum monthly charge of C1279 per month (£1.28).

1.2.5.2. Sanitation. It is common for rubbish tips to be used as toilets by children byday and some adults by night. In some parts of Accra where houses lack sanitation,people relieve themselves into polythene bags and deposit these into the communityrefuse skips. Thus, the boundary between refuse disposal and excreta removal israther fuzzy.

In some urban areas, WCs are ®tted draining into individual septic tanks, but

many households in urban Ghana still depend on the daily removal of raw excreta

from the home through the bucket conservancy system. In Kumasi, KHEP (1993)

estimates that 40% of households rely wholly on public latrines, mainly of the aqua-

privy type, but undergoing conversion to a locally developed version of the

Ventilated Indirect Pit (VIP) type known as the Kumasi VIP or KVIP. The health

e�ects of the poor system is demonstrated in morbidity data in which it is estimated

that there are over 100 000 cases of sanitation-related diseases reported in Kumasi

per year, of which about 1000 are cases of cholera (KHEP, 1993).

Berekum public latrines are mostly aqua-privies, though there are a few KVIPs. A

short observation of an hour in the early morning (6.25±7.25 a.m. on Friday 2 April

1993), showed the following behaviour. The 20 squat-holes (16 for adults; 4 for chil-

dren) were used by 154 people (both sexes) after an average waiting time of 7 min;

average time spent inside the building was 6 min. In addition, an average of 8 people

per minute emptied chamber pots at one KVIP.*

KVIPs are proving unsuitable as public conveniences as they ®ll up within a week

of emptying and, thus, cannot be used to render the waste harmless through com-

posting. Many are being converted to simple pits with a provision for desludging,

while some disused KVIPs were being used as disposal points for the emptying of

chamber pots.

In the last few years, charges have been introduced for the use of public latrines as

part of a privatization package. There has been a considerable improvement in con-

ditions within the latrines in Kumasi (Christie and Harris, 1992), and in services pro-

vided as a result of this, e.g. free sections for children, although other parts of the

private operation of sanitation have been more problematic. Demand for sanitation

is still high, especially in peripheral areas. At Anloga, Kumasi, the demand is evident

*The stench from such latrines is particularly o�ensive and, under moderate wind conditions, could besmelt up to 400 metres away!

Housing Supply in Ghana 269

from the high patronage at the private enterprise wooden latrines built over the Sisai

stream. Charges are similar to the regular public latrines (C10 per visit), but excre-

ment simply drops into the stream in which children can be found bathing and,

further downstream, some poorer members of the unsuspecting population at Atonsu

obtain drinking water from the same stream. Gari (a `cereal' made from grated cas-

sava) is also prepared by groups of women some 30 m from two of the latrines. This

is particularly hazardous given that gari is a ®nished product, ready to eat once it

leaves the banks of the Sisai stream.*

The monthly fee charged by conservancy contractors for servicing bucket latrines

is C2000 in Accra; C3000 in Kumasi. The fee charged by conservancy contractors for

desludging aqua-privies in Kumasi is C2000 per session, but the e�uent is simply

allowed to spill out around the back of the latrine.

In some towns, landlords have been ordered to provide higher levels of servicing

to their tenants, but with no parallel measures adopted to increase their incomes

from renting. The following example, from Sunyani (near Berekum), illustrates this

situation:

The Sunyani District Assembly has given all landlords at Sunyani up to the end of this year to provideplaces of convenience in their houses or face prosecution at the law courts. The assembly, which held itssecond ordinary meeting of the year at Sunyani on Thursday, said the facilities should either be KVIPs orwater closets . . .The house noted that the public place of convenience in the town . . .cannot cope with [the]growing population and the best solution is for every household (sic) to provide its own facility. (DailyGraphic, 13 July 1993: 3)

An insigni®cant proportion of Accra and Kumasi houses, and none of those in

Berekum, are connected to main sewers. Furthermore, though there have been sug-

gestions that water-borne systems should be ®tted in both large cities, there is insu�-

cient water to service them. Perversely, water closets in use in Ghana tend to have

large cisterns which use more than 12 litres of water at each ¯ush. All WCs which

exist outside the very limited areas served by sewers, are connected to on-site septic

tanks and soak-away pits.

1.2.5.3. Refuse disposal. Under the `pay-as-you-dump' refuse levy system which wasadopted by the Accra Metropolitan Authority on 1 July 1993 (Daily Graphic, 13 July1993: 3), each trip to the city's communal refuse skips is intended to attract a fee ofC20. With refuse workers reporting reductions in the volumes of refuse deposited inthe community skips, it is probable that there has been an increase in ¯y-tipping bychildren (who are traditionally responsible for transporting refuse to approved dumpsites). While the move towards cost recovery is undeniably laudable, this mode oflevy collection is already encouraging people to store uncovered domestic refuse forlonger periods. A levy that is subsumed within property rates would not penalize themost e�cient, would not encourage the deliberate accumulation of domestic refuse,and would be more di�cult to evade.

In most Ghanaian settlements known to the authors, domestic refuse is generally

uncovered, ¯y-tipping is common and organized collection from public disposal sites

is infrequent. Uncovered drains tend to be used for waste disposal. During a 10 min

*The potential for food carrying health hazards from one site to the whole city is considerable. See alsoHellen et al. (1991).

270 Progress in Planning

observation of Berekum refuse tip (an organized open type) beginning at 6.15 a.m.,

102 tippers visited it, of whom 80 were children. At the other end of the scale, in

some high-cost parts of Accra, private refuse removal contractors are charging

C2000 a month for a twice-weekly donkey-cart service which is proving pro®table

even at four houses per hectare.

1.2.5.4. Storm and waste water drainage. Apart from along the few major streets anda minority of residential roads, planned drainage is virtually absent in Kumasi, Bere-kum and Accra. Where drains exist, they are exposed and tend to be used for the dis-posal of litter and, thus, become blocked. Erosion of roads and pathways is a seriousproblem for access and safety; also it leads, in turn, to weakened house foundations.Standing water in blocked drainage ditches and eroded holes allows the breeding ofmosquitos and other disease vectors.

1.2.5.5. Electricity. As is the case with water, the supply of electrical power is notentirely satisfactory, though it is perhaps the more satisfactory of the two; indeedmost houses have a supply. In certain parts of Kumasi (particularly those close tothe industrial area), supplies are more erratic than average and can be lost in windyconditions. At Dichemso, for example, residents experience power failures almost ona daily basis: supply is typically lost from 7 p.m. to 9 or 10 p.m.

With both water and electricity, prospective customers are required to pay the full

cost of connecting their homes from the nearest mains/sub-mains. Major faults are

usually attended to within 48 h.

1.2.6. The regulatory system

The Town and Country Planning Ordinance (Cap 84 of 1945) is still the principle

planning law guiding physical development in urban Ghana. It has been amended by

The Local Government Law (PNDC Law 207 of 1988) and this has in turn been

superseded by the Local Government Act (Act 462 of 1993). The Local Planning

Authority (that is the local District Assembly) has the power to make plans, regulate

land uses, receive applications for permission to develop land and erect buildings,

remove structures which contravene regulations, and levy ®nes for people who con-

travene the laws. As with so many planning codes, the Ghanaian one is powerful to

control, but not capable of enabling, housing investment.

Despite several e�orts to introduce revised building regulations which would be

relevant throughout the country in urban areasÐnotably the Draft Ghana Building

Code in 5 parts (BRRI, 1979)Ðthe old codes still apply and are speci®c to cities.

Building in Kumasi, for example, is still regulated by the Public Health Board

Regulations of 1939 and the Kumasi Outline Town Planning Scheme, 1945 (Fry and

Drew, 1945). In them, minimum sites for plots are set at 232 m2 in central Kumasi,

335 m2 in the new areas being developed then as island plots (i.e. with no back

lanes), and 446 m2 (say 22.3� 20 m) elsewhere. Maximum plot coverage is a half

(two-thirds on the `island' plots). In the Kumasi Outline Town Planning Scheme,

most of the city was included in an area designated `B' in which plots should be no

Housing Supply in Ghana 271

smaller than 450 m2 with a maximum coverage of 30%. The outlying villages could

be developed with plots of 370 m2 and 60% maximum coverage.

In reality, it seems that one-third coverage is used as a rule of thumb by building

inspectors and planning o�cers. Covered space is de®ned to include enclosed open

spaces such as courtyards so that compound houses do not qualify and are, there-

fore, illegal. However, enforcement tends to be more subjective. In Accra, greater

care is taken over the scrutiny of drawings for new housing than in Kumasi or

Berekum. However, once underway, construction tends not to be scrutinized and

only the worst practices and most unsafe structural arrangements are commented

upon by the building inspectors. Impressionistic evidence points to a mixture of petty

corruption and incompetence as the reasons for this poor performance by the build-

ing inspectorate. In areas where compounds are common, the Statutory Planning

Committee tends to turn a blind eye to new compound development. O�cers in the

Kumasi Metropolitan Planning O�ce told us that they did not approve of com-

poundsÐnot only on the grounds of plot coverage, but also because they are not in

favour of multi-occupation. In the current circumstances of great need and within

Ghanaian culture, this seems to be a retrogressive attitude, but one that is all too

common in planning authorities in Africa.

A potentially serious issue arises for the potential builder who wishes to proceed in

advance of gaining land title, a process which takes many years to ®nally accomplish.

A development permit cannot be obtained until land title is secured and the lack of

this permit causes the full weight of the enforcement procedure to descend on the

`culprit'. The structure receives a visit from the building inspectors who paint `Stop

work immediately, by order' or `Produce permit' in red on the uncompleted struc-

ture. At this point, the owner is expected to `dash them small' (to give a payment)

before construction can proceed.

Thus the regulatory system, as currently practised, contains many of the problems

recognized as bottlenecks to housing supply: it is inhospitable to the housing that

most people can a�ord to own, it is not transparent, it depends on ful®lling subjec-

tive criteria (side-payments, in¯uence, etc.), and it imposes costs on the process either

through delays or through side-payments.

1.2.7. The need to increase supply

The Global Strategy for Shelter to the Year 2000 (UNCHS, 1990) calls for a policy

framework in each country which is capable of enabling the provision of housing for

all. This involves scaling up the supply mechanisms so that they eradicate the serious

shortages which exist and supply housing for the newly independent households

being formed through marriage, and the new population being born in, and mi-

grating to, urban areas. Ghana's population is estimated at 16.4 million (Population

Reference Bureau: PRB, 1993) with growth forecasts for the rest of the century in

the region of 3.1% per annum.

In recent research by the authors, the usefulness of the compound for low income

households (Korboe, 1993a), and the issue of family houses (Amole et al., 1993;

272 Progress in Planning

Korboe, 1992a) have been discussed. Each has called for a re-examination of the

compound form as it possesses much of worth in a society where most households

cannot a�ord a whole house (be it compound or tiny bungalow), and where all

houses are liable to be inherited by a group of people holding them in common but

having rights of use of parts of them.

The housing supply issue for Kumasi, and much of Sub-Saharan Africa, is further

complicated by the fact that housing is generally not sold (see Tipple, 1984). When

an individual begins to build, he/she is not starting a project which can be aborted if

the money is required for an emergency or if the project becomes too expensive.*

The builder is permanently committed to the house and so are his/her heirs.{Elsewhere, the motivations behind house building in urban Ghana have been

suggested to be mainly concerned with status and security for old age (Tipple and

Willis, 1992a; Korboe, 1992b).

Who, then is supplying new housing or extensions? What are they building? Do

would-be house-owners have a di�cult time in assembling the necessary inputs and

succeeding in the supply process? What problems are they encountering? These and

other issues have been the basis for a survey of house-owners in three centres in

Ghana, carried out by the Centre for Architectural Research and Development

Overseas, University of Newcastle upon Tyne, and the Department of Housing and

Planning Research, University of Science and Technology, Kumasi, and sponsored

by the Leverhulme Trust. In it, we surveyed owners who have built since 1987

(referred to below as recent builders), owners of long standing who have extended

since 1987 (recent extenders), owners of long standing who have not extended since

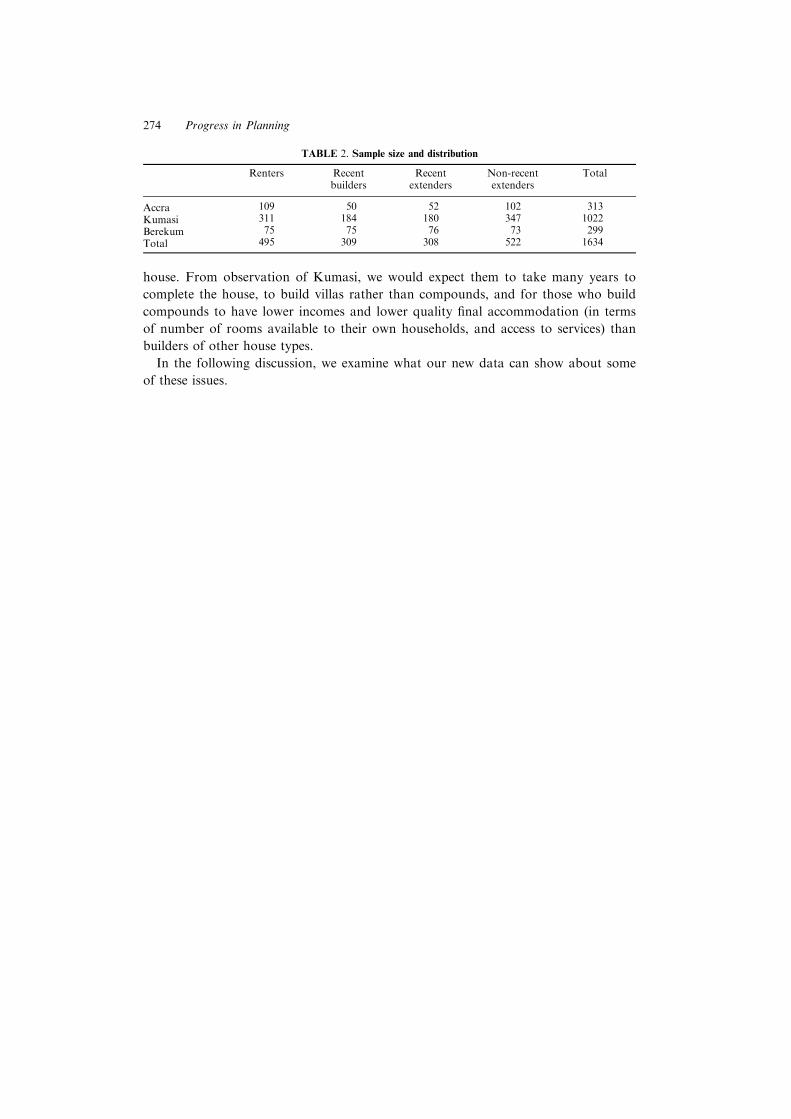

1987 (non-recent extenders), and renters (Table 2).

The rather sparse literature on housing supply suggests that it is more di�cult in

the late 1980s and early 1990s than it was in the 1960s and 1970s (Gilbert, 1993;

Aina, 1988; Amis, 1988; Tipple and Willis, 1992b; Diko and Tipple, 1992; Korboe,

1993a; Wikan, 1990). Gone are the days of free land on the periphery of cities. Even

in Latin America, invasions resulting in self-improving neighbourhoods (Turner,

1976) are a thing of the past. Indeed, Gilbert (1993) found that peripheral squatters

in his Latin American sample now tend to be those households who cannot a�ord to

rent rooms in serviced neighbourhoods and are forced into shack ownership. The

even more sparse literature on extension activity gives few leads as to who extends

their housing rather than moving or building again.

As squatting is not an option in Ghana (Tipple, 1984; Konadu-Agyemang, 1991;

Korboe, 1992b), we would expect recent builders to be better o� than recent exten-

ders and non-recent extenders (both longer term owners) and much better o� than

renters. Intuitively, we would expect recent builders to be building better accommo-

dation for themselves than they currently occupy, but we could not suggest whether

they would be better or worse housed than renters before they move to the new

*Which, incidentally, is one of the pillars built by John Turner (1976) upon which sites and servicesschemes stand.

{There are a few developers who build houses to sell while incomplete, and a small group of developersbuilding for sale. However, the majority of Ghanaians have their own housing built through local con-tractors and will only sell in absolute extremis.

Housing Supply in Ghana 273

house. From observation of Kumasi, we would expect them to take many years to

complete the house, to build villas rather than compounds, and for those who build

compounds to have lower incomes and lower quality ®nal accommodation (in terms

of number of rooms available to their own households, and access to services) than

builders of other house types.

In the following discussion, we examine what our new data can show about some

of these issues.

TABLE 2. Sample size and distribution

Renters Recentbuilders

Recentextenders

Non-recentextenders

Total

Accra 109 50 52 102 313

Kumasi 311 184 180 347 1022

Berekum 75 75 76 73 299

Total 495 309 308 522 1634

274 Progress in Planning

CHAPTER 2

Who is supplying

In examining who the suppliers of houses are currently, it might be useful ®rst to

clarify who the non-suppliers are; who it is who have never become owners, who are

not making the decision to become owners or, if they own already, to extend. These

are the renters.

2.1. THE NON-SUPPLIERS : RENTERS

From earlier work on Kumasi (e.g. Malpezzi et al., 1990; Tipple and Willis, 1991),

we would expect that, in comparison with owners, renters would have smaller house-

holds with lower household income,* but higher per capita income. As we will see in

the analysis below, this is found to be the case. Renter households have a mean of

3.7 persons in Accra, 5.0 in Kumasi and 4.4 in Berekum. These small households

demonstrate that renters tend to be in an earlier stage of their lives than average, es-

pecially in Accra. However, as the household heads are in younger adulthood than

owners, it might be expected that they would have more children under 16 per adult

than owners. In fact, our sample have fewer, particularly in Accra where they have a

mean of only 1.5 children per renter household and only 0.6 children per adult.{As expected from earlier work, our sampled renters mostly occupy only one room

per household, typically in a multihabited house (usually in compound form) in

which they share services with all households.{ Their means are between 1.13 and

1.37 rooms (all have a median of 1 room) and their mean household occupancy rates

exceed three people per room in each location (median occupancy rates are between

three and four people per room), Kumasi being particularly crowded. We would also

expect that renters in our sample would pay relatively little in rent. As can be seen in

Table 3, despite the apparent collapse of the rent control regime operated until the

late 1980s, monthly rents are very low at only C1900 (£1.9) in Accra, C2400 (£2.4) in

Kumasi, and C1400 (£1.4) in Berekum. Rents per room are also very small (less than

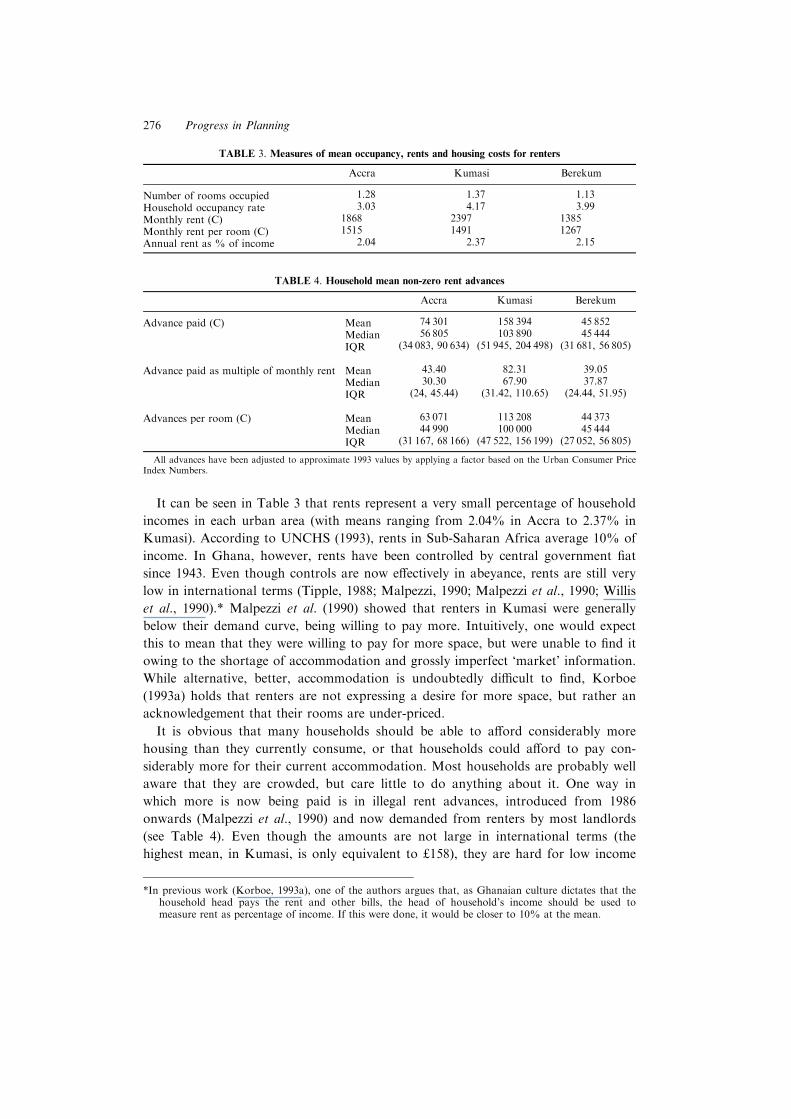

C1500±£1.50 per month).

*As explained later, expenditure is used as a proxy for income. In this paper, whenever reference is madeto income, the data are from the questions on expenditure.

{Grown-up children will tend to stay in their parents' house when it is di�cult to ®nd suitably pricedalternative accommodation. When large rent advances are demanded, the process is even more con-strained.

{Of the 310 renters sampled in the three cities, 50% share and 40% have no access to a kitchen.Equivalent ®gures for bathroom (87% and 5%), toilet (55% and 39%) and water supply (50% and45%) demonstrate the rarity of exclusive servicing for renters.

Housing Supply in Ghana 275

It can be seen in Table 3 that rents represent a very small percentage of household

incomes in each urban area (with means ranging from 2.04% in Accra to 2.37% in

Kumasi). According to UNCHS (1993), rents in Sub-Saharan Africa average 10% of

income. In Ghana, however, rents have been controlled by central government ®at

since 1943. Even though controls are now e�ectively in abeyance, rents are still very

low in international terms (Tipple, 1988; Malpezzi, 1990; Malpezzi et al., 1990; Willis

et al., 1990).* Malpezzi et al. (1990) showed that renters in Kumasi were generally

below their demand curve, being willing to pay more. Intuitively, one would expect

this to mean that they were willing to pay for more space, but were unable to ®nd it

owing to the shortage of accommodation and grossly imperfect `market' information.

While alternative, better, accommodation is undoubtedly di�cult to ®nd, Korboe

(1993a) holds that renters are not expressing a desire for more space, but rather an

acknowledgement that their rooms are under-priced.

It is obvious that many households should be able to a�ord considerably more

housing than they currently consume, or that households could a�ord to pay con-

siderably more for their current accommodation. Most households are probably well

aware that they are crowded, but care little to do anything about it. One way in

which more is now being paid is in illegal rent advances, introduced from 1986

onwards (Malpezzi et al., 1990) and now demanded from renters by most landlords

(see Table 4). Even though the amounts are not large in international terms (the

highest mean, in Kumasi, is only equivalent to £158), they are hard for low income

TABLE 3. Measures of mean occupancy, rents and housing costs for renters

Accra Kumasi Berekum

Number of rooms occupied 1.28 1.37 1.13

Household occupancy rate 3.03 4.17 3.99

Monthly rent (C) 1868 2397 1385

Monthly rent per room (C) 1515 1491 1267

Annual rent as % of income 2.04 2.37 2.15

TABLE 4. Household mean non-zero rent advances

Accra Kumasi Berekum

Advance paid (C) Mean 74 301 158 394 45 852

Median 56 805 103 890 45 444

IQR (34 083, 90 634) (51 945, 204 498) (31 681, 56 805)

Advance paid as multiple of monthly rent Mean 43.40 82.31 39.05

Median 30.30 67.90 37.87

IQR (24, 45.44) (31.42, 110.65) (24.44, 51.95)

Advances per room (C) Mean 63 071 113 208 44 373

Median 44 990 100 000 45 444

IQR (31 167, 68 166) (47 522, 156 199) (27 052, 56 805)

All advances have been adjusted to approximate 1993 values by applying a factor based on the Urban Consumer PriceIndex Numbers.

*In previous work (Korboe, 1993a), one of the authors argues that, as Ghanaian culture dictates that thehousehold head pays the rent and other bills, the head of household's income should be used tomeasure rent as percentage of income. If this were done, it would be closer to 10% at the mean.

276 Progress in Planning

households to gather together. In addition, they are paid not only by movers, but

also by sitting tenants in place of monthly rents. Many employees are now making

their contribution towards housing as periodic payments to cope with advances

rather than through monthly amounts.

Advance rent payments have been seen by Malpezzi et al. (1990) and Willis et al.

(1990) as a means of increasing the net present value of the very low rents in a period

of high in¯ation at a time when public opinion is unready to accept substantial

increases in rent to bring them closer to a market value. The receipt of advance rent for

several rooms by an owner can raise su�cient capital for adding to or improving on

servicing (e.g. a water supply) or the addition of a room. Korboe (1993a) found that

some renters volunteered rent advances in order to assist the landlords with repairs or

improvements. None of these behaviour patterns suggests rapacious landlords exploit-

ing powerless tenants, but there are undoubtedly some occurrences of this.

The percentage of renter households in our sample who actually paid advances

varies from 61% in Kumasi to 76% in Berekum. It can be seen from Table 4 that

non-zero advances vary from C46 000 or 39 months' rent at the mean in Berekum to

C158 000 and 82 months' rent in Kumasi.

We ®nd mean rents in Accra (see Table 3) to be 78% of those in Kumasi, while

rents per room are only slightly higher (102% of Kumasi values). Advances, which

are a sign of market pressure being applied (albeit imperfectly) to controlled rents,

are, however, considerably lower in Accra. Mean values for total advances, advances

per room, and advances as multiples of monthly rent in Accra are all between 50%

and 70% of those in Kumasi. These low levels of rent and advances in Accra are

counter-intuitive. Hearsay and frequent press reports in Ghana tell us that housing is

particularly di�cult to obtain in Accra, landlords are especially grasping, and

advances are set at impossibly high levels. However, our data give little support to

these assertions except in the narrow band at the top end of the market which pull

the mean value up 30% above the median.*

Why should rent advances be lower in Accra than in Kumasi? Is it a function of

the nearness of the seat of government acting as a check on illegal advances being

charged? It could be, but this is highly unlikely. Is it that the samples are very di�er-

ent? Our data on income appear to suggest similar samples. Is it that owners are

more generous with their tenants, waiving increases or reducing demands out of eth-

nic fellow-feeling; after all 26% of tenants in the Accra sample did not pay advances?

This idea is supported by Korboe (1992b, 1993a), who argues that the provision of

rental accommodation is often not related to pro®t-making. Thus, economic model-

ling is unlikely to prove reliable in predicting rental behaviour. Generosity would,

perhaps, be expected to be more in¯uential in Kumasi, where the Akan culture is

more homogeneous, than in Accra. The counter-argument would be that Kumasi has

always been a centre for cut-throat trading (kalabule) and, as renters su�er higher

levels of crowding there than in Accra, the bid price for accommodation is likely to

*As with so much hearsay evidence in Ghana, even among some academics, the band of opportunity inwhich the educated elite operate does not necessarily re¯ect reality for the poorer sections of the popu-lation who predominate.

Housing Supply in Ghana 277

be higher. Whatever reasons can be suggested, the conclusion is inescapable: rent

advances payable in new housing occupied by low income households in Accra are

lower than those in comparable areas in Kumasi.

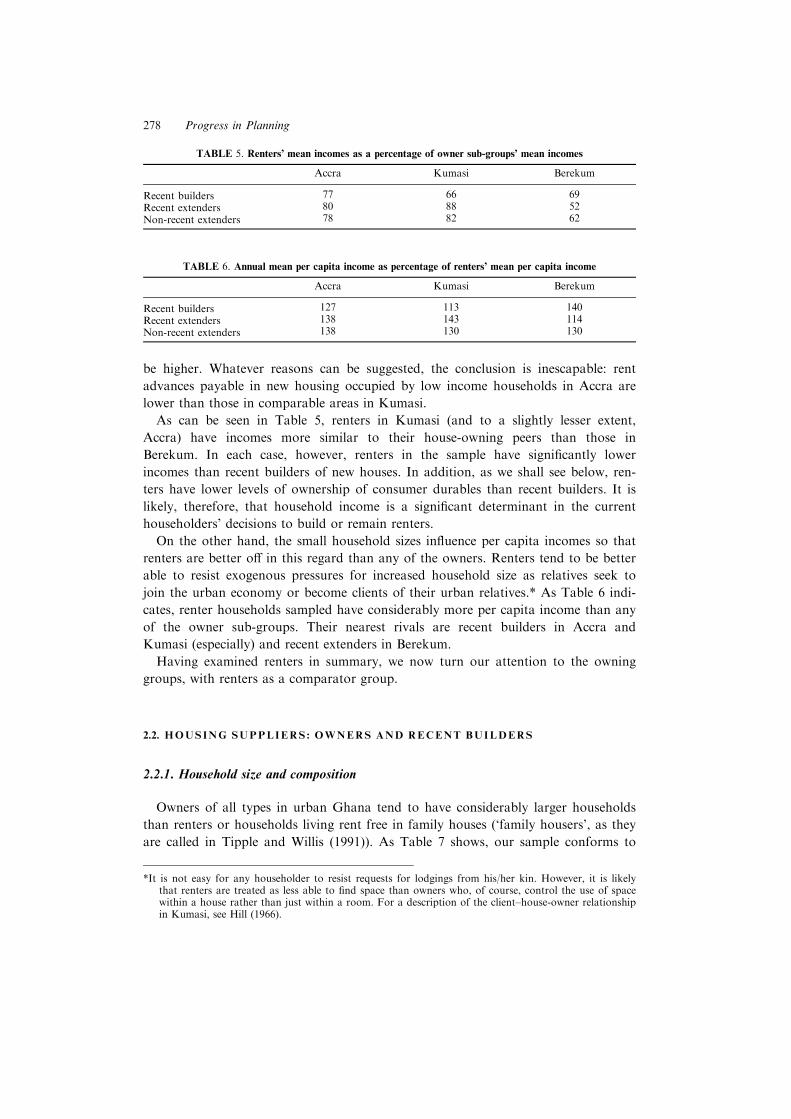

As can be seen in Table 5, renters in Kumasi (and to a slightly lesser extent,

Accra) have incomes more similar to their house-owning peers than those in

Berekum. In each case, however, renters in the sample have signi®cantly lower

incomes than recent builders of new houses. In addition, as we shall see below, ren-

ters have lower levels of ownership of consumer durables than recent builders. It is

likely, therefore, that household income is a signi®cant determinant in the current

householders' decisions to build or remain renters.

On the other hand, the small household sizes in¯uence per capita incomes so that

renters are better o� in this regard than any of the owners. Renters tend to be better

able to resist exogenous pressures for increased household size as relatives seek to

join the urban economy or become clients of their urban relatives.* As Table 6 indi-

cates, renter households sampled have considerably more per capita income than any

of the owner sub-groups. Their nearest rivals are recent builders in Accra and

Kumasi (especially) and recent extenders in Berekum.

Having examined renters in summary, we now turn our attention to the owning

groups, with renters as a comparator group.