HOUSING NEWS HOUSING NEWS March 2004 March 2004 Vol. 4 Vol. 4 No. 2 No. 2 Content Content s 1) Editorial 1) Editorial 2) NHB 2) NHB Update Update 3) Reverse 3) Reverse Mortgage Mortgage 4) Articles 4) Articles i) Regulation by Regulation by Kishor N Kishor N Kumbhare Kumbhare ii) Looking at ii) Looking at The Curves by The Curves by Ashok K Tiwari Ashok K Tiwari iii) iii) Importance of Importance of Decentralized Decentralized EDITORIAL EDITORIAL The end of the March 2004 quarter also marked the end of financial year 2003-04 which has once again remained buoyant for the housing finance sector. The growth of housing finance business in the recent years has witnessed a new trend in home-ownership pattern with growing segment of young generation desiring to own a house and working towards it. The traditional debt aversion has given way to acquisition of housing assets through long-term debt. The potential gain from capital appreciation remains an attractive incentive for investment in housing, besides the tax concessions available for the borrowers. We thought it will be useful to share our thought with the Readers on the reverse mortgage and how it can impact the Indian housing finance prospects. This is discussed at length in this issue of “Housing News”. A recent survey by the National Sample Survey Organisation revealed that there are still around eight million families in urban India staying in around 52, 000 slums with inadequate basic amenities. This calls for serious efforts on the part of the Government and all stakeholders for fulfilling the commitment towards overall habitat development and housing satisfaction. The recent announcement of a grant of Rs.500 crore by the Hon’ble Prime Minister for the development of Asia’s largest slum Dharavi in Mumbai is indeed a mammoth step in this direction. At the NHB, the significant developments during the quarter were refinance disbursal of around Rs.800 crore as well as successful launch of three issues of mortgage backed securitization amounting to a total pool size of Rs. 163.80 crore and issue size

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

HOUSING NEWSHOUSING NEWSMarch 2004March 2004 Vol. 4 No.Vol. 4 No.

22

ContentsContents1) Editorial 1) Editorial

2) NHB Update2) NHB Update

3) Reverse3) Reverse Mortgage Mortgage

4) Articles 4) Articles

ii)) Regulation byRegulation by Kishor N KumbhareKishor N Kumbhare

ii) Looking at Theii) Looking at The Curves by Ashok KCurves by Ashok K Tiwari Tiwari

iii) iii) Importance ofImportance of DecentralizedDecentralized Cooperation forCooperation for SustainableSustainable Urbanization byUrbanization by P.P. Pathrose P.P. Pathrose

5) News From5) News From the Press the Press

EDITORIALEDITORIAL

The end of the March 2004 quarter also marked the end of financial year 2003-04 which has once again remained buoyant for the housing finance sector. The growth of housing finance business in the recent years has witnessed a new trend in home-ownership pattern with growing segment of young generation desiring to own a house and working towards it. The traditional debt aversion has given way to acquisition of housing assets through long-term debt. The potential gain from capital appreciation remains an attractive incentive for investment in housing, besides the tax concessions available for the borrowers. We thought it will be useful to share our thought with the Readers on the reverse mortgage and how it can impact the Indian housing finance prospects. This is discussed at length in this issue of “Housing News”.

A recent survey by the National Sample Survey Organisation revealed that there are still around eight million families in urban India staying in around 52, 000 slums with inadequate basic amenities. This calls for serious efforts on the part of the Government and all stakeholders for fulfilling the commitment towards overall habitat development and housing satisfaction. The recent announcement of a grant of Rs.500 crore by the Hon’ble Prime Minister for the development of Asia’s largest slum Dharavi in Mumbai is indeed a mammoth step in this direction.

At the NHB, the significant developments during the quarter were refinance disbursal of around Rs.800 crore as well as successful launch of three issues of mortgage backed securitization amounting to a total pool size of Rs. 163.80 crore and issue size of Rs.144.75 crore. The details of these MBS transactions are also given inside.

The Indian economy is currently poised for double–digit growth and the latest reports on the GDP front have indeed provided substance to this optimism. We expect the housing sector will continue to grow and provide significant contribution to the overall growth in the coming years.

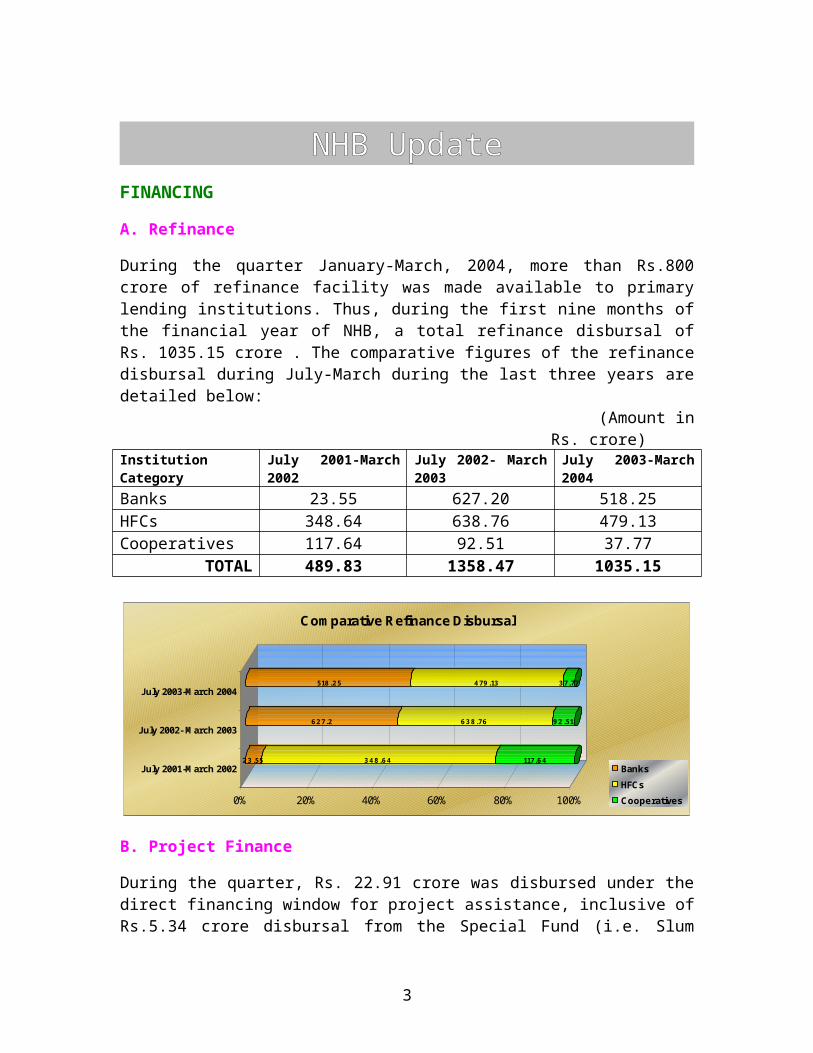

NHB UpdateFINANCING A. Refinance During the quarter January-March, 2004, more than Rs.800 crore of refinance facility was made available to primary lending institutions. Thus, during the first nine months of the financial year of NHB, a total refinance disbursal of Rs. 1035.15 crore . The comparative figures of the refinance disbursal during July-March during the last three years are detailed below:

(Amount in Rs. crore)

Institution Category

July 2001-March 2002

July 2002- March 2003

July 2003-March 2004

Banks 23.55 627.20 518.25HFCs 348.64 638.76 479.13Cooperatives 117.64 92.51 37.77

TOTAL 489.83 1358.47 1035.15

23.55 348.64 117.64

627.2 638.76 92.51

518.25 479.13 37.77

0% 20% 40% 60% 80% 100%

July 2001-March 2002

July 2002- March 2003

July 2003-March 2004

Comparative Refinance Disbursal

BanksHFCsCooperatives

B. Project Finance During the quarter, Rs. 22.91 crore was disbursed under the direct financing window for project assistance, inclusive of Rs.5.34 crore disbursal from the Special Fund (i.e. Slum Redevelopment & Low Cost Housing Fund). Thus, the total direct finance disbursal during the first nine months of NHB’s financial year 2003-04 stood at Rs.33.39 crore inclusive of disbursal of Rs.5.98 crore under the Special Fund.

(Amount in Rs.crore)

January-March 2004 January – March

2

2003General Fund 17.57 8.98Special Fund 5.34 5.92

TOTAL 22.91 14.90RESIDENTIAL MORTGAGE BACKED SECURITIZATION (RMBS)

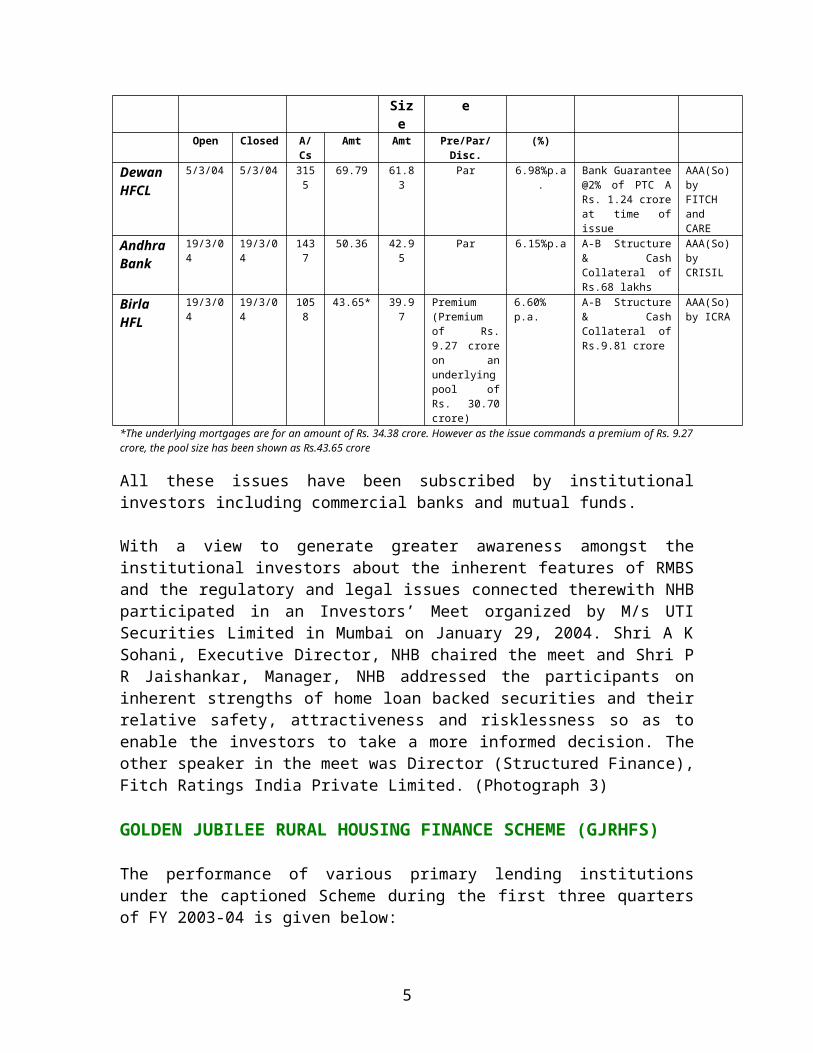

The first quarter of 2004 has witnessed three RMBS issues launched by NHB with loans originated by Dewan Housing Finance Corporation Limited, Andhra Bank, and Birla Home Finance Limited with a total pool size of Rs.163.80 crore of 5650 loans and the total issue size of Rs.144.75 crore. Significantly, all the issues were fully subscribed on the same day they were opened. This clearly indicates that investor confidence in NHB MBS issues have grown over the years.

The Andhra Bank issue assumes special significance in the perspective that it was the first ever RMBS issue of a public sector bank in India. With the growing interest evinced by the banks in housing finance and proactive policy pronouncement by the Reserve Bank of India in the form of reduced risk weight of 50 % on RMBS investment it is expected that more and more public sector banks will be forthcoming in taking part in RMBS in near future. (Photographs 1 & 2)

Details of these three RMBS issues are given below: (Amount in Rs. crore)

Originator

Issue Date Pool Size Issue

Size

PricingStructur

e

Coupon

Credit Enhancement

Rating

Open Closed

A/Cs

Amt Amt Pre/Par/Disc.

(%)

DewanHFCL

5/3/04 5/3/04 3155

69.79 61.83 Par 6.98%p.a.

Bank Guarantee @2% of PTC A Rs. 1.24 crore at time of issue

AAA(So) by FITCH and CARE

Andhra Bank

19/3/04

19/3/04

1437

50.36 42.95 Par 6.15%p.a A-B Structure & Cash Collateral of Rs.68 lakhs

AAA(So) by CRISIL

Birla HFL

19/3/04

19/3/04

1058

43.65* 39.97 Premium (Premium of Rs. 9.27 crore on an underlying pool of Rs. 30.70 crore)

6.60% p.a.

A-B Structure & Cash Collateral of Rs.9.81 crore

AAA(So) by ICRA

*The underlying mortgages are for an amount of Rs. 34.38 crore. However as the issue commands a premium of Rs. 9.27 crore, the pool size has been shown as Rs.43.65 crore

All these issues have been subscribed by institutional investors including commercial banks and mutual funds.

3

With a view to generate greater awareness amongst the institutional investors about the inherent features of RMBS and the regulatory and legal issues connected therewith NHB participated in an Investors’ Meet organized by M/s UTI Securities Limited in Mumbai on January 29, 2004. Shri A K Sohani, Executive Director, NHB chaired the meet and Shri P R Jaishankar, Manager, NHB addressed the participants on inherent strengths of home loan backed securities and their relative safety, attractiveness and risklessness so as to enable the investors to take a more informed decision. The other speaker in the meet was Director (Structured Finance), Fitch Ratings India Private Limited. (Photograph 3)

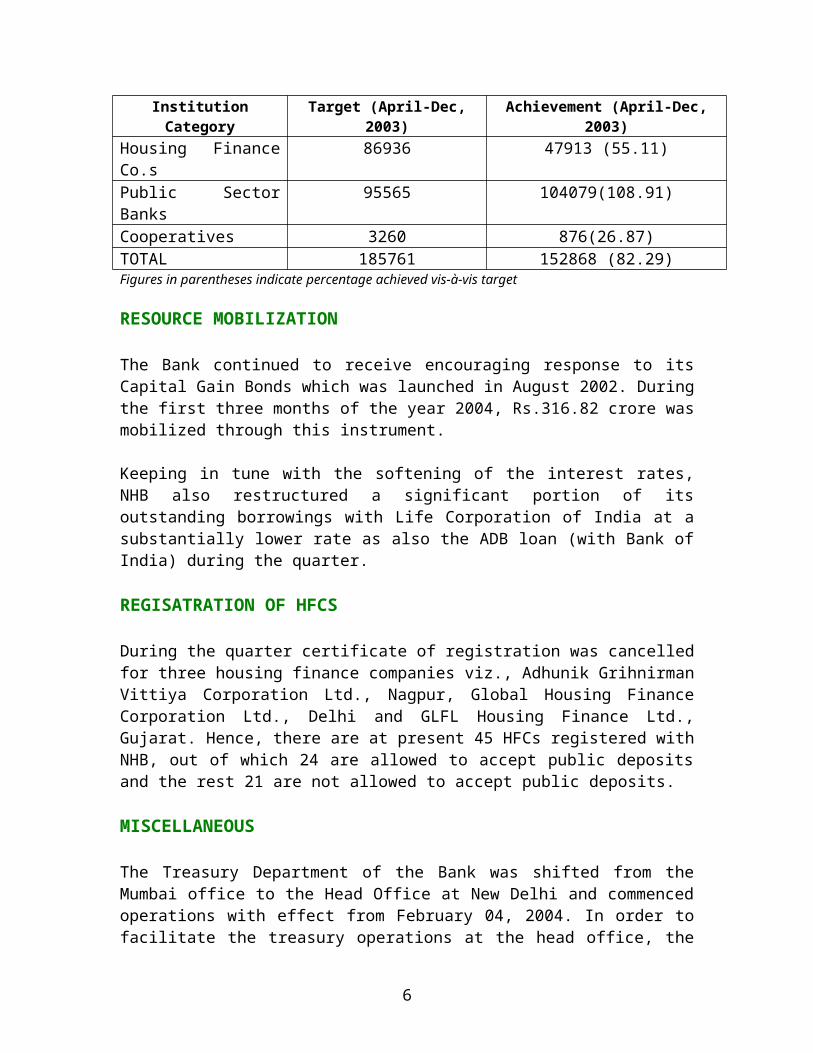

GOLDEN JUBILEE RURAL HOUSING FINANCE SCHEME (GJRHFS)

The performance of various primary lending institutions under the captioned Scheme during the first three quarters of FY 2003-04 is given below:

Institution Category

Target (April-Dec, 2003)

Achievement (April-Dec, 2003)

Housing Finance Co.s

86936 47913 (55.11)

Public Sector Banks 95565 104079(108.91)Cooperatives 3260 876(26.87)TOTAL 185761 152868 (82.29)Figures in parentheses indicate percentage achieved vis-à-vis target

RESOURCE MOBILIZATION

The Bank continued to receive encouraging response to its Capital Gain Bonds which was launched in August 2002. During the first three months of the year 2004, Rs.316.82 crore was mobilized through this instrument.

Keeping in tune with the softening of the interest rates, NHB also restructured a significant portion of its outstanding borrowings with Life Corporation of India at a substantially lower rate as also the ADB loan (with Bank of India) during the quarter.

REGISATRATION OF HFCS

During the quarter certificate of registration was cancelled for three housing finance companies viz., Adhunik Grihnirman Vittiya Corporation Ltd., Nagpur, Global Housing Finance Corporation Ltd., Delhi and GLFL Housing Finance Ltd., Gujarat. Hence, there are at present 45 HFCs registered with NHB, out of which 24

4

are allowed to accept public deposits and the rest 21 are not allowed to accept public deposits.

MISCELLANEOUS

The Treasury Department of the Bank was shifted from the Mumbai office to the Head Office at New Delhi and commenced operations with effect from February 04, 2004. In order to facilitate the treasury operations at the head office, the Negotiated Dealing System (NDS) was installed for online trading of Government securities and Kastle Treasury package was installed. Moneyline Telerate Screens were also installed to provide information support to investment operations. Inter-office connectivity between Mumbai and Delhi office was established through leased line.

GTIC (India) Pvt. Ltd. is in the process of analysis, design, development and implementation of the Software for the Refinance Operations System. The proposed software package covers both the refinance operations and also the project finance operations of the Bank. GTIC (India) Ltd. has outlined the Software Project Management Plan (SPMP) and identified the system requirement on the basis of the analysis of the existing system. Accordingly, the Functional Requirement Specification (FRS) and the Acceptance Test Plan (ATP) for Part A of the project, encompassing the Accounting part and business logic development, was framed. Subsequent discussions between the company and the Refinance Department on the provisions/features in the FRS and ATP helped in identifying areas which needed modifications/correction. GTIC (India) Ltd has completed the construction of basic design of the package pertaining to the accounting logic and is currently enabling testing and acceptance of the same by way of familiarization of the users with the software. Part A of the project is expected to be implemented shortly. rajaBaaYaa£¸«’ïú¡¸ ‚¸¨¸¸¬¸ ¤¸ÿˆÅ ‚œ¸›¸½ ¬˜¸¸œ¸›¸¸ ˆÅ¸¥¸ ¬¸½ h-ú ž¸¸£·¸ ¬¸£ˆÅ¸£ ˆÅú £¸¸ž¸¸«¸¸ ›¸ú¢·¸ ˆ½Å ¬¸ûÅ¥¸� ˆÅ¸¡¸¸Ä›¨¸¡¸›¸ ‡¨¸¿ ƒ¬¸ˆ½Å œÏž¸¸¨¸ú ‚›¸ºœ¸¸¥¸›¸ ˆ½Å ¢¥¸‡ ˆÅ¢’¤¸Ö £ho h ¾ ‡¨¸¿ ¤¸ÿˆÅ ›¸½ ë™ú ˆ½Å œÏ¸¸£-�œÏ¬¸¸£ ˆ½Å ¢¥¸‡ ˆÅƒÄ ˆÅ™Ÿ¸ „“¸‡¿ ÿ— ¤¸ÿˆÅ ˆÅú -Ÿ¸½©¸¸ ¬¸½ ¡¸ ›¸ú¢·¸ £ú ¾ ¢ˆÅ œÏ½£µ¸¸ ‚¸¾£ œÏ¸½·¬¸¸›¸ ˆÅú ›¸ú¢·¸ ‚œ¸›¸¸ˆÅ£ ë™ú ˆ½Å œÏ¡¸¸½Š¸

5

ˆÅ¸½ „··¸£¸½î¸£ ¤¸ö¸¡¸¸ ¸¸‡ ‚¸¾£ ƒ¬¸Ÿ¸Ê ¤¸ÿˆÅ ˆÅ¸½� � ‚¸©¸¸·¸ú·¸ ¬¸ûÅ¥¸·¸¸ ž¸ú ¢Ÿ¸¥¸ú ½¾—

¤¸ÿˆÅ ˆÅú œ¸¢°¸ˆÅ¸ "‚¸¨¸¸¬¸ ž¸¸£÷¸ú" ˆÅ¸½ ¤¸¾¢ˆ¿ÅŠ¸ ‡¨¸¿ ¢¨¸÷÷¸ú¡¸ ¸Š¸÷¸ ˆ½Å œ¸¸“ˆÅ¸½¿ ¬¸½ ‚Ž¸ œÏ� �¢÷¸¬¸¸™ œÏ¸œ÷¸ íº‚¸ í¾— ¡¸í „¥¥¸½‰¸ ¢ˆÅ¡¸¸ ¸¸÷¸¸ í¾� ¢ˆÅ ¤¸ÿˆÅ ˆÅú "‚¸¨¸¸¬¸ ž¸¸£÷¸ú " œ¸¢°¸ˆÅ¸ ˆÅ¸½ ž¸¸£÷¸ú¡¸ ¢£¸¨¸Ä ¤¸ÿˆÅ ׸£¸ ¨¸«¸Ä 2001-2002 ˆ½Å ¢¥¸‡� ‚¸¡¸¸½¢¸÷¸ "¢í¿™ú Š¸¼í œ¸¢°¸ˆÅ¸" œÏ¢÷¸¡¸¸½¢Š¸÷¸¸� Ÿ¸½¿ "¸÷¸º˜¸Ä " œ¸º£¬ˆÅ¸£ ¢Ÿ¸¥¸¸ — 26 Ÿ¸¸¸Ä, 2004� � ˆÅ¸½ ‚¸¡¸¸½¢¸÷¸ ¬¸Ÿ¸¸£½¸í Ÿ¸½¿ ¡¸í œ¸º£¬ˆÅ¸£� ž¸¸£÷¸ú¡¸ ¢£¸¨¸Ä ¤¸ÿˆÅ ˆ½Å Š¸¨¸›¸Ä£ Ÿ¸í¸½™¡¸ ¬¸½� ¤¸ÿˆÅ ˆ½Å ‚š¡¸®¸ ¸ú ›¸½ œÏ¸œ÷¸ ¢ˆÅ¡¸¸ —�

"‚¸¨¸¸¬¸ ž¸¸£÷¸ú " œ¸¢°¸ˆÅ¸ ˆÅ¸½ ¢™¥¥¸ú ¤¸ÿˆÅ ›¸Š¸£ £¸¸ž¸¸«¸¸ ˆÅ¸¡¸¸Ä›¨¸¡¸›¸ ¬¸¢Ÿ¸¢÷¸ ׸£¸ ¨¸«¸Ä 2003 ˆ½Å� ¢¥¸‡ ¢™¥¥¸ú ¬÷¸£ œ¸£ ‚¸¡¸¸½¢¸÷¸ ¢í¿™ú Š¸¼í œ¸�¢°¸ˆÅ¸ œÏ¢÷¸¡¸¸½¢Š¸÷¸¸ Ÿ¸½¿ ™»¬¸£¸ œ¸º£¬ˆÅ¸£ ¢™¡¸¸ Š¸¡¸¸ — ¸›¸¨¸£ú, 2004 Ÿ¸½¿ ‚¸¡¸¸½¢¸÷¸ ¬¸Ÿ¸¸£¸½í� � Ÿ¸½¿ ¡¸í œ¸º£¬ˆÅ¸£ ž¸¸£÷¸ ¬¸£ˆÅ¸£, Š¸¼í Ÿ¸¿°¸¸¥¸¡¸ ˆÅú ¬¸¢¸¨¸ ¬¸ºªú ›¸ú›¸¸ £¿¸›¸ ¸ú ˆ½Å í¸˜¸¸½¿ ¬¸½� � � £¸¸ž¸¸«¸¸ ¢¨¸ž¸¸Š¸ ˆ½Å ‚¢š¸ˆÅ¸¢£¡¸¸½¿ ›¸½ œÏ¸œ÷¸� ¢ˆÅ¡¸¸ —

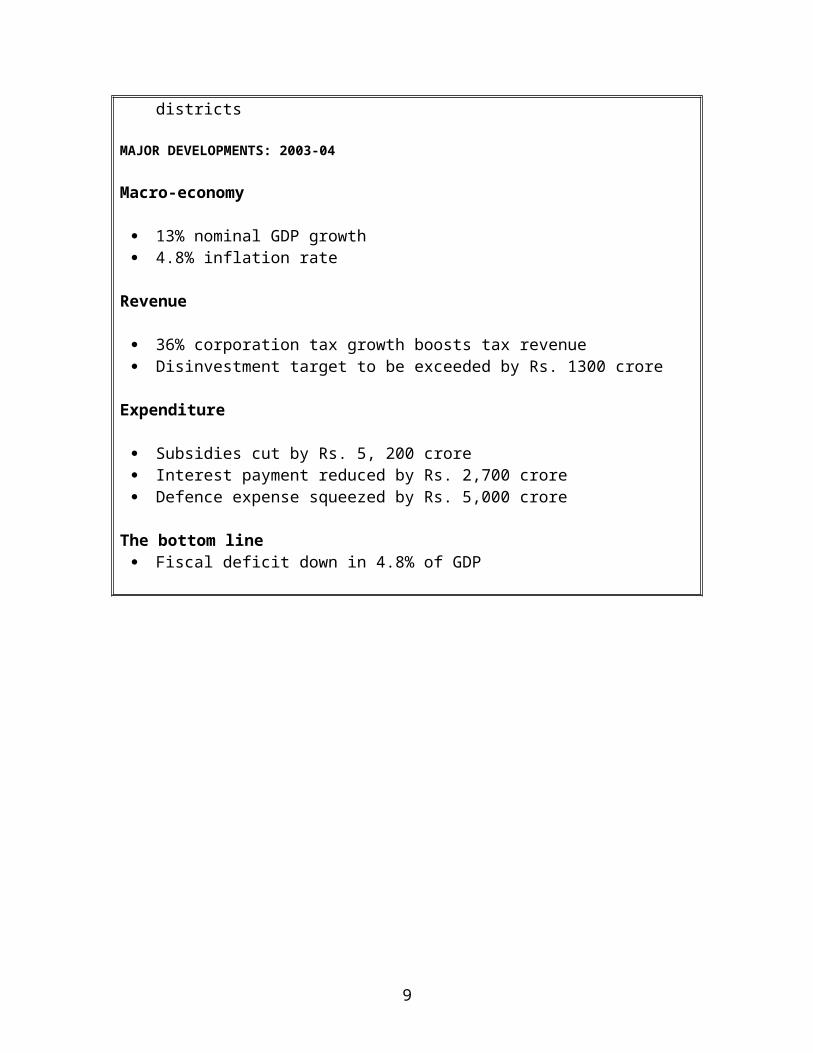

HIGHLIGHTS OF INTERIM BUDGET 2004

New schemes

Rs. 15,000 crore scheme to revitalize cooperative credit structure Rs. 25,000 crore defence modernization fund Farm income insurance scheme will be extended to 100 districts

MAJOR DEVELOPMENTS: 2003-04

Macro-economy

13% nominal GDP growth 4.8% inflation rate

Revenue

6

36% corporation tax growth boosts tax revenue Disinvestment target to be exceeded by Rs. 1300 crore

Expenditure

Subsidies cut by Rs. 5, 200 crore Interest payment reduced by Rs. 2,700 crore Defence expense squeezed by Rs. 5,000 crore

The bottom line Fiscal deficit down in 4.8% of GDP

7

New Rural Housing SchemeThe recent data released by the Census of India on Houses, Households, Amenities and Assets for 2001, indicate that total number of households in rural areas is 138.27 million as against the availability of 135.05 million houses (used as residences and residences-cum other purposes), of which nearly 11.40 million houses were non-serviceable kutcha/temporary houses needing replacement. Thus we may consider requirement of houses in rural areas as 14.6 million units Besides, if congestion and obsolescence factors as also the damage of houses due to vagaries of nature are taken into consideration, the requirement will further increase.

Although the housing finance in the country has witnessed significant growth of during the last few years owing to proactive policy initiatives including the fiscal concessions made available for the sector development, a major portion of financial disbursements by primary lending institutions are still confined to urban areas only. Housing loan in rural areas account for less than 15% of the total housing loan disbursements despite significant net work of Commercial banks and regional rural banks (RRBs) in rural areas. The low credit disbursals for housing by their rural branches are constrained by various factors e.g. non availability of clear land title, difficulties in assessing repayment capabilities of rural masses due to irregular income pattern etc., resulting in higher credit risk.

With a view to increasing flow of funds for improving the habitat conditions in rural areas, the Hon’ble Finance Minister announced the launch of a new rural housing scheme. The scheme will include insurance cover against defaults arising from any non-enforceability of security because of the defects in the title or title disputes, fiscal incentives for housing finance institutions and flexibility in repayment schedule to suit the income pattern of borrowers from rural area.

A Working Group was constituted by Ministry of Finance, Govt. of India, with members from Ministry of Finance, Ministry of Rural Development, Reserve Bank of India, NHB, IRDA, Oriental Insurance Company, State Bank of India and HDFC, to recommend measures for early formulation of a suitable scheme and its implementation.

8

Reverse Mortgage Reverse Mortgages first became popular in America. The U.S. Department of Housing and Urban Development (HUD) created one of the first reverse mortgages. HUD's Reverse Mortgage is a federally-insured private loan, and it's a safe plan that can give older Americans greater financial security. Many seniors use it to supplement social security, meet unexpected medical expenses, make home improvements, and more.

What is a reverse mortgage?

A Reverse Mortgage is a special type of home loan that lets a homeowner convert a portion of the equity in his or her home into cash. The equity built up over years of home mortgage payments can be paid to the owner. But unlike a traditional home equity loan or second mortgage, no repayment is required until the borrower(s) no longer use the home as their principal residence. In order to become eligible for HUD reverse mortgager the borrower has to be a homeowner, 62 years of age or older; own the home outright, or have a low mortgage balance that can be paid off at the closing with proceeds from the reverse loan; and must live in the home. The home must be in reasonable condition, and must meet HUD minimum property standards. In some cases, home repairs can be made after the closing of a reverse mortgage.

A Reverse Mortgage is a 'non-recourse' loan. This means there is 'no personal liability' to the borrower or his heirs. No matter what, the lender can only look to the property for repayment and if it is insured then the insurer would make up any shortage to the lender. Repayment is due after all Homeowners permanently vacate the home (die, sell, or permanently move out).

What's the difference between a reverse mortgage and a bank home equity loan?

With a traditional second mortgage, or a home equity line of credit, a borrower must have sufficient income versus debt ratio to qualify for the loan, and s/he is required to make monthly mortgage payments. The reverse mortgage is different in that it pays the borrower, and is available regardless of his current income. The amount one can borrow depends on age, the current interest rate, other loan fees, and the appraised value of the home etc. Generally, the more valuable the

9

home is, the older the borrower is, the lower the interest, the more one can borrow. The borrower doesn’t make payments, because the loan is not due as long as the house is his principal residence. Like all homeowners, he still is required to pay real estate taxes and other conventional payments like utilities, but with a federally insured HUD Reverse Mortgage, one cannot be foreclosed or forced to vacate the house because he "missed his mortgage payment."

Can the lender take the home away if one outlives the loan?

No, and nor is the loan due. One does not need to repay the loan as long as he or one of the borrowers continues to live in the house and keeps the taxes and insurance current. One can never owe more than his/her home's value.

Bequeaths

When one sells the home or no longer use it for primary residence, he will repay the cash received from the reverse mortgage, plus interest and other fees, to the lender. The remaining equity in the home, if any, belongs to him or his heirs. None of his other assets will be affected by HUD's reverse mortgage loan. This debt will never be passed along to the estate or heirs.

How does one receive his payments?

There are five options:

Tenure - equal monthly payments as long as at least one borrower lives and continues to occupy the property as a principal residence.

Term - equal monthly payments for a fixed period of months selected.

Line of Credit - unscheduled payments or in installments, at times and in amounts of borrower's choosing until the line of credit is exhausted.

Modified Tenure - combination of line of credit with monthly payments for as long as the borrower remains in the home.

Modified Term - combination of line of credit with monthly payments for a fixed period of months selected by the borrowers.

10

Articles REGULATION1

Kishor. N. Kumbhare, Deputy Manager, NHB

o Overview:

Financial markets today are the biggest markets in the world. In keeping with the broad thrust of the ongoing programme of economic reforms, the mechanism of administrative controls over the individuals' decision of institution is required. The regulation of financial market therefore concerns us all.

o What is Regulation?

Regulation is an act which controls the individual decision of institution that would take inadequate account of the public interest. Regulation may be either self imposed or imposed through a third party. Self-imposed regulation could be through codes of conduct. Third party regulation could be in the forms of law, administrative rules, directions, taxations, etc. The regulatory framework shapes market behaviour and thus the design and practice of the regulatory framework determines the efficiency and performance of the regulated market.

o Why Regulation is required?

There exist markets for regulation in which consumers and producers compete. Since regulation can be regarded as a public good, the free rider problem suggests that the benefit to the individual consumer is likely to be small relative to the producer. A market without regulation does not work and may result in control by the Mafia with huge losses inflicted on the innocent and unwary. Regulation is an attempt to correct the market failure/imperfections, such as monopoly, externalities and lack of information. The social cost of the failure of a financial institution may be much higher than the private cost to the institution itself. The financial institutions left to themselves will accept more risk than in optimal from a systemic point

1 The standard disclaimer applies

11

of view, thus forming the basic case for government regulation of financial activities.

External regulation on private sector behaviour can be justified on the following grounds:

(i) In free market economy, public policy arguments call for competition and free trade.

(ii) Systemic risk issue which allows the State to prevent the failure of one participant to destabilize the whole system.

(iii) Regulations provide protection to poorly informed clients based on the view that small depositors and investors cannot assess properly the riskiness of financial institution they deal with.

(iv) If market participant believes that the state will undertake losses, then behaviour will change. A good example is State intervention preventing the failure of Unit Trust of India. Another example is how deposit insurance encourages depositors and bankers to engage in risky behaviour that forces the state to pay in the end. Thus, undermining market discipline and entailing regulation.

o What to regulate:

We can regulate product, functions or institution or a combination of all three. Problem arises when we have overlapping regulatory terrain, competing regulatory agencies and confused regulatory objectives. Regulation may be based on product types such that each regulatory authority specializes in are financial products. Under the framework, a securities regulation will concentrate in the oversight of securities activities, irrespective of type of financial institutions that are carrying out this business.

Financial regulation is generally conducted by the separate regulatory bodies, an investor protection arm and a systemic stability arm. The investor protection arm deals with retail depositors and small investors to ensure fair conduct, equitable competition and consumer protection. The systemic stability agency, on the other hand, looks at the larger player and wholesale activities. It would also be responsible for the safety structure and functioning of all systems and financial markets. Premature measures include capital adequacy requirement, prudential norms, limit on credit exposure, constraints on corrected lending and other rules aimed at preventing insolvency and an official safety net such as lender of last resort or deposit insurance.

12

o Features of Regulation:

(i) Regulation must have clear objectives which can prevent regulation from expanding beyond the minimum necessary to correct the market.

(ii) A regulatory agency must possess enforcement powers over the full range of the institution it is responsible for regulating.

(iii) A regulatory agency needs to have adequate resources to discharge its task effectively. It must have experienced, trained and professional staff to discharge the duty.

(iv) A regulatory agency must be able to take necessary decision without undue outside interference. It should be ensured that the regulatory agency is not exposed to the risk of regulation.

(v) Regulation should be comprehensive and free of regulatory gaps. There should be no scope for particular activities or types of intermediaries to escape effective regulation simply because there is doubt which agency should be responsible for regulating it.

(vi) The regulators must be in a position to respond quickly to market innovations to ensure that regulatory framework remains up to date and does not become ineffective or acts as a barrier to the legitimate evolution of the market.

(vii) A regulation imposes cost, both directly and indirectly. The direct cost of regulation is those needed to sustain the activities of the regulatory agencies. The indirect cost of regulation is more difficult to quantify, but are those incurred by a regulated industry as a result of the need to comply with regulatory requirements.

o Approach to Regulation:

The first line of protection against failure of any financial institution must be management’s own risk control. The growing complexity and variety of business suggests that neither the regulatory authorities nor informed customer can prevent internal management from making mistakes if internal controls do not work. The best defense against mistakes and fraud are proper internal governance. Proper internal controls, together with both internal and external

13

auditors, plus a proper disclosure policy would give the best incentives for internal management to perform according to proper rules.

Public disclosure rather than a private channel would be cheaper and reduce unwarranted expectations of what a regulator or supervisor can actually achieves. However, it is difficult, if not impossible, to guarantee full disclosure. It is doubtful whether free market work well enough in conditions where information is partial and poorly distributed and externalities exist. Thus, it is not really possible for the authorities to shift entirely to reliance on disclosure and to abandon their specialized supervisory function.

The public oversight function is one of monitoring and surveillance to ensure that systemic risks are not incurred at excessive public cost. When best practice and market standards are applied, any behaviour by regulators that deviates from the norm would be subject to public scrutiny. There is, therefore, greater pressure for establishing internal norm of performance, such as, capital adequacy standards, concentration on credits and risk management tools.

The application of certain regulatory tools, such as, required capital ratios, excessive limits, constraints on self-dealing, etc. are design to ensure that market participants comply with minimal standards of capital and risk exposures. It should be emphasized that effective regulator requires proper compliance and enforcement. Too many rules imposed too heavy a regulatory cost, with redundant or excessive information burdens. However, given very rapidly changing market condition, some degree of discretion can be more practical than rigid rules. On the other hand, excessive discretion can lead to systematic forbearance (time inconsistency) that undermines rules and could even be subject to corruption and abuse.

o Deregulation & why?

There are few reasons why deregulation is happening. Deregulation is mainly because of globalization, financial innovation and disintermediation, changing customer behaviour and excessive cost.

The globalization of financial market may increase systemic risk, through contagious financial disorder originating in poorly regulated financial centres. Depositors, investors and counterparties may be exposed to foreign jurisdiction risks which they are not in a position to monitor and control. Besides, the co-existence of uneven national regulations and global markets may severely distort competition between financial institutions.

14

Financial innovation i.e. derivatives trading creates transparency problems for regulators because of the speed and complexity of risk transformation. The appropriate response of market transparency is more extensive disclosure of financial information. But in the context of fast-moving derivatives business the difficulty is to formulate effective disclosure rules that do more that provide an outdated snapshot of risk exposure.

In addition, changing customer behaviour is resulting from aging population. Consumer expectations are likely to be higher as they now have access to more choices from more diversified market.

Finally, deregulation has occurred because of old regulations have not prevented the massive loss incurred by work wide bank failure. In the light of there heavy costs, government around the world have begun to look seriously at the cost of regulation.

o Conclusion:

Today, regulation is becoming more complex and demanding. It is demanding a more comprehensive approach than hitherto. It is bringing together multiple disciplines in an attempt to harness the forces of the market to improve the market stability. It stresses greater risk sensitivity, flexible supervision and more reliance on the market discipline. This is, of course no more than a further important step along the road to a more efficient and resilient financial system.

________________________________________________________________________(The author may be contacted at [email protected])

15

LOOKING AT THE CURVES – DOES SHAPE MATTER?2

-Ashok Kumar Tiwari, Deputy Manager, NHB

Interest rates are among the most closely watched and most widely discussed variables of an economy. The fact that normally at any given point of time, different rates of interest are associated with different terms to maturity gives rise to what is called the Term Structure of Interest Rates. Yield curve is nothing but the mapping of this term structure. The curve is derived by plotting the yields on bonds of different maturities but the same risk characteristics. The yield curve looked at most commonly is that associated with sovereign bonds which are assumed to be risk free.

Yield curves can have different shapes depending on the term spread (or the slope of the curve). Shape of the curve tells us whether long term rates are higher or lower than short term rates. An upward sloping curve indicates that long term rates are higher than short term rates, whereas an inverted or downward sloping curve implies higher short term rates. Equal rates across maturities would give rise to a flat yield curve. In practice, different combinations of these shapes are also observed. For example, inverted in the short term, upward sloping in the medium term and flat towards the longer end of the curve.

What explains the different shapes of the yield curve? What information does a yield curve contain? We will have a brief review of the conceptual framework on shape and behaviour of the yield curve. In the second part of the article, we will take a look at the shape of the Indian yield curve vis-à-vis global standards.

Some of the theories that have been put forward to explain the shape of the yield curve are –

Pure expectations theory Market segmentation theory Liquidity premium theory

Pure expectations theoryThis theory assumes that bonds of different maturities are perfect substitutes. For example, one can buy a 2 year bond and hold it till maturity or buy a one year bond and when it matures, buy another one year bond. According to the theory, long term interest rates are derived from expectations of future short term rates. The interest rate on a long term bond will be equal to an average of short term interest 2 The standard disclaimer applies

16

rates that the market expects to occur over the life of the bond. For example, if one year interest rate over next five years is expected to be 5%, 6%, 7%, 8% and 9%, the interest rate on a five year bond will be the average of these one year rates, i.e. (5%+6%+7%+8%+9%)/5 = 7%.

This theory provides a simple explanation of the behaviour of the term structure, but does not explain the empirical fact that yield curves usually slope upwards. Future movement of short term rates may be derived by looking at the slope of the yield curve. For example, an upward sloping curve indicates that short term rates are expected to rise.

Market segmentation theoryUnder this theory, markets for different maturity bonds are seen as completely separate and differing yield curve patterns are explained by supply and demand characteristics associated with bonds of different maturities. This theory implies that yield curve would typically slope upwards. This is so because demand for long term bonds is relatively lower than that for short term bonds in the typical situation and hence long term bonds will have lower prices and higher yields.

Liquidity premium theoryThis is a combination of the above two theories and states that the interest rate on a long term bond will be equal to an average of short term interest rates expected over the life of the bond plus a liquidity premium that responds to supply and demand conditions for that bond. The key assumption is that bonds of different maturities are substitutes (i.e. the expected return on one bond does influence the expected return on a bond of a different maturity), but investors may prefer one bond maturity over another. Investors tend to prefer shorter term bonds (for less interest rate risk) and must be offered a positive liquidity premium to induce them to hold longer term bonds.

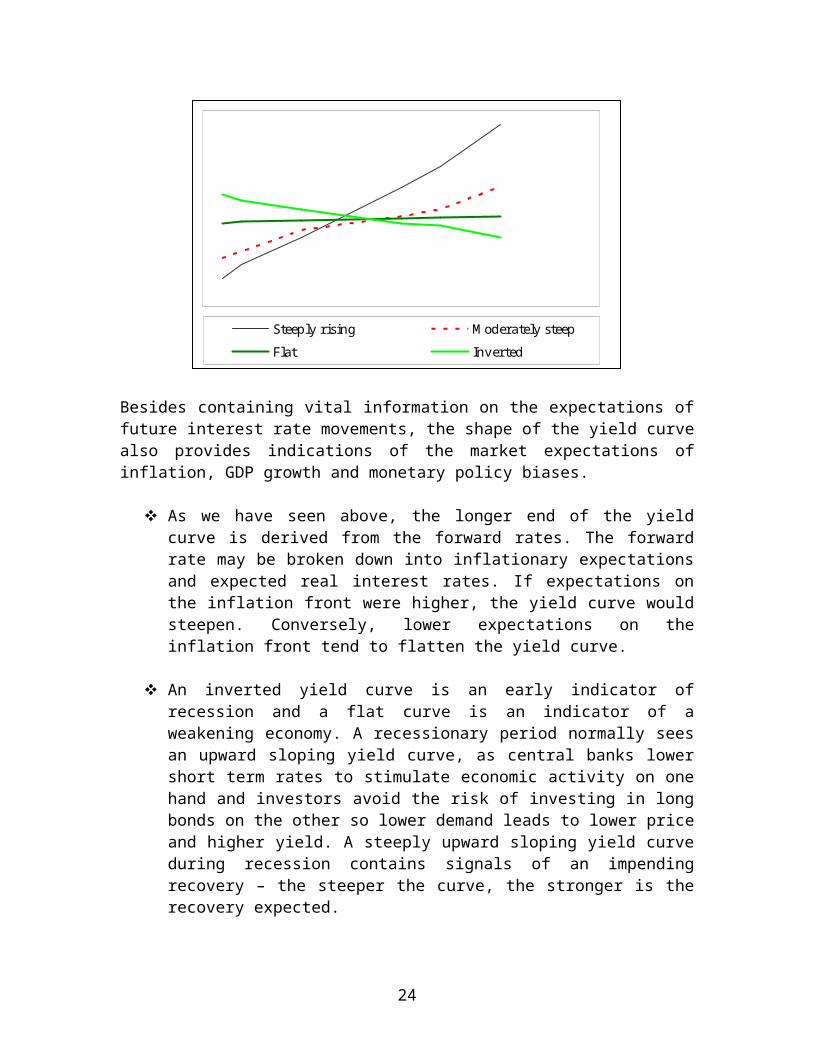

Market expectations of future short term interest rates may be derived by looking at the slope of the yield curve. Following chart shows different yield curve shapes and the future interest rate expectations that may be derived therefrom are shown in the table that follows –

Yield curve shape

Short term rates

Steeply rising Expected to riseModerately steep

Not expected to rise or fall much

Flat Expected to fall moderatelyInverted Expected to fall sharply

17

Steeply rising Moderately steepFlat Inverted

Besides containing vital information on the expectations of future interest rate movements, the shape of the yield curve also provides indications of the market expectations of inflation, GDP growth and monetary policy biases.

As we have seen above, the longer end of the yield curve is derived from the forward rates. The forward rate may be broken down into inflationary expectations and expected real interest rates. If expectations on the inflation front were higher, the yield curve would steepen. Conversely, lower expectations on the inflation front tend to flatten the yield curve.

An inverted yield curve is an early indicator of recession and a flat curve is an indicator of a weakening economy. A recessionary period normally sees an upward sloping yield curve, as central banks lower short term rates to stimulate economic activity on one hand and investors avoid the risk of investing in long bonds on the other so lower demand leads to lower price and higher yield. A steeply upward sloping yield curve during recession contains signals of an impending recovery – the steeper the curve, the stronger is the recovery expected.

Yield curve also indicates market expectations of future monetary policy measures. In weakening economic conditions, the monetary policy is expected to be easy and future interest rates soft and so the yield curve is flatter. In times of fast growth, interest rates are generally raised to prevent the economy from ‘overheating’. Similarly, the typical response of central banks to inflationary tendencies is a tightening of the monetary policy.

18

Thus, as the expected future rates are higher, the yield curve steepens.

Historical behaviour of yield curves in US and Japan would illustrate the above interpretations. The US yield curve during late 90s was flat and was inverted for a part of 2000. This was followed by a period of economic downturn. The Federal Reserve raised interest rates 6 times in 1999 & 2000 to fight the ‘irrational exuberance’ of the markets and to contain the possible inflationary impact on the US economy. The increase in short term rates resulted into inversion of the yield curve in 2000. Subsequently, reversing the interest rate policy, the US Fed moved on to a rate cutting spree and has cut the interest rate 13 times since January 2001. The series of rate cuts were resorted in an attempt to come out of the slowdown and also to fight the fears of deflation. Similarly, the economic slowdown and recession that set in in Japan in 90s was preceded by an inverted yield curve. There is also an apparent relationship between the period of inversion of the curve and the period of recession that follows. While the US curve was inverted for a few months and the US economy experienced a slowdown for a relatively shorter period of 2-3 years (now showing string signs of recovery), Japan had an inverted curve for over two years and the recessions there has extended to more than a decade.

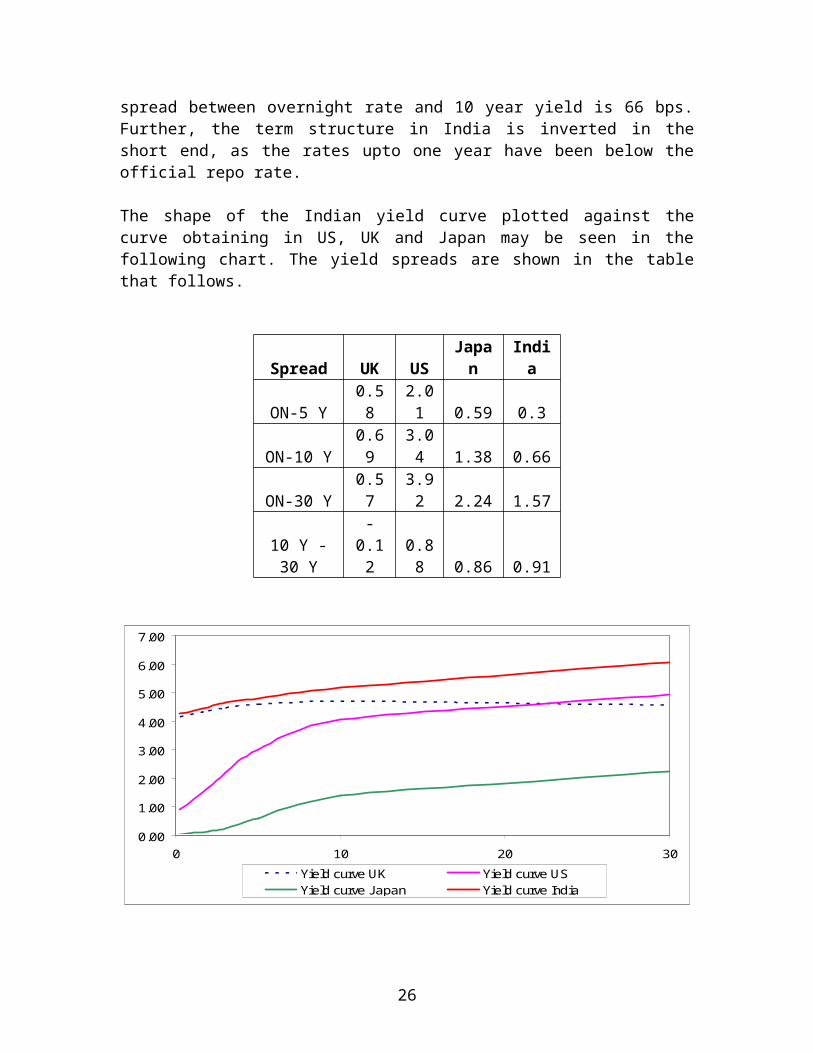

Is the Indian yield curve flat?The yield curve in India is flat by global standards. The entire spread of the yield curve is about 130 bps and the spread between overnight rate and 10 year yield is 66 bps. Further, the term structure in India is inverted in the short end, as the rates upto one year have been below the official repo rate.

The shape of the Indian yield curve plotted against the curve obtaining in US, UK and Japan may be seen in the following chart. The yield spreads are shown in the table that follows.

Spread UK USJapa

nIndi

a

ON-5 Y 0.582.01 0.59 0.3

ON-10 Y 0.693.04 1.38 0.66

ON-30 Y 0.573.92 2.24 1.57

10 Y - 30 Y

-0.12

0.88 0.86 0.91

19

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

0 10 20 30

Yield curve UK Yield curve USYield curve Japan Yield curve India

Is the flatness of Indian yield curve a pointer to an economic slowdown in the coming times? If we look into the reasons for flatness of the treasury curve, we find that the shape does not fully reflect the market expectations because of certain structural features specific to the Indian market. The flatness of the curve can be explained by the present stage of development of the market (longs only market, short selling prohibited), a bias towards longer end of the curve in new issuances and stickiness of the repo rate. Market participants are unable to express two way views or views on specific portions of the curve in the absence of short selling. Thus, the yield curve may not necessarily reflect the market expectations. Recent introduction of phase III of delivery Vs payment is a step towards further development of the market and may lead to better expression of market views. The issuance pattern in the last couple of years has been biased towards longer dated securities, leading to a shift in the trading interest towards the longer end of the curve. The shift has resulted into higher demand for these papers driving down their yields. Similar downward movement has not happened in the shorter maturity segment owing to lower demand in this segment. The stickiness of the repo rate also contributes to the flatness of the curve. During 2003-04, the repo rate has been cut only once by 50 basis points while the 10 year yield has declined by about 110 basis points.

Though the flat shape of the curve is a cause of concern, it does not indicate an impending recession. The flattening has happened over the past couple of years, as the central bank has resorted to aggressive rate cuts to spur economic growth and bond markets have witnessed a

20

sustained bull run. A correction (steepening) in the shape is expected as the economy grows.

The author is thankful to Shri T. V. Rao, AGM, NHB for generating interest in the subject. The author may be contacted at [email protected].

The Bank had organized an essay competition to commemorate the World Habitat Day on the themes of Importance of decentralized cooperation for sustainable urbanization and Need for and impact of micro–level capacity building and external support mechanism for effective city-to-city cooperation. The first prize winning entry was published in the last issue of the housing news. In this issue, the first part of the second prize winning entry is published. The concluding part of the article will be published in the next issue of the Housing News.

IMPORTANCE OF DECENTRALIZED COOPERATION FOR SUSTAINABLE URBANIZATION3

- P.P. PathroseManager, Federal Bank

3 The standard disclaimer applies

21

NEWS FRPM THE PRESS

IRS eligibility for Banks : 10% CRAR, Rs. 200-Crore Net-worth

Financial Express, January 2, 2004

The Reserve Bank of India (RBI) committee on interest rate derivative has recommended that banks with capital-to-risk weighted assets ratio (CRAR) of 10% and with minimum net-worth of 200 crore would only be considered for permission to trade in the interest rate futures market.

The committee headed by G Padmanabhan was also of the view that RBI can consider authorizing banks to undertake trading positions in interest rate futures after satisfying itself about the bank’s capabilities to undertake the above activities and considering the quality of internal and regulatory compliance.

Home Loan sector faces NPA pitfalls

Business Line, January 4, 2004

The buoyant Indian housing loan industry, growing at an average of 30 per cent, is besieged by the problems of falling interest margins and tendency by banks to compromise on due diligence, according to Value Notes Data base, a provider of business intelligence and research.

Although loan processing had been made simpler, there was a major issue of sustainability and viability of lenders, it was felt that there exists a real possibility that in trying to speed up processing time, some banks are compromising on the due diligence process. This raises the worrisome possibility of future non-performing assets.

NHB wants Gujarat to pay stamp duty On mortgage deed

Ahmedabad January 7, 2004

In order to further boost housing sector in the state, National Housing Bank (NHB), the apex bank and regulatory body for housing finance company, has asked the Gujarat Government to remit 2% stamp duty on the mortgage deed created by the borrower. Housing Finance Companies and scheduled banks lend only against the mortgage of the

Bank Staff to Get Home Loans at Market-Determined Rates for Perks Valuation

Financial Express, January 8, 2004

Housing loans rates have been reduced to market determined rates for perquisite valuation. Earlier, an individual entitled to a soft loan from his employer at a reduced rate of two per cent had to pay taxes on perquisites of eight per cent, as the government had fixed 10 per cent as the limit for housing loans for such

22

housing units and mortgage attracts stamp duty of 2% of the loan amount, which adds to the cost of the house.

purpose.

23

FIIs increase LIC Housing pie by 12%

Business Standard, January 9, 2004

Domestic investors have sold their shares in the country’s second largest housing finance company, LIC Housing Finance Ltd., but foreign indirect investors (FIIs) have seized the opportunity to increase their stake in it by as much as 12 per cent in the third quarter (October-December 2003) of the current fiscal.

Financial institution, IFCI has offloaded 5.08 per cent in LIC Housing Finance Ltd. Foreign institutional investors Merrill Lynch Capital Markets and Citigroup Global Markets Mauritius have increased their stake by 5.5 per cent in the company.

FIIs stake in LIC Housing in September was around 6 per cent. This rose to 18 per cent in the third quarter. Merrill Lynch Capital Markets has picked up 5.11 per cent while Citigroup Global Markets Mauritius has picked up another 2 per cent in the company. Public holding in LIC Housing declined by 3 per cent in the same period.

Unit Trust of India (UTI) also sold three per cent stake and held 5.92 per cent in the third quarter, while UTI Master Share Unit Scheme and Birla Sunlife Insurance offloaded their entire stake of 3 per cent and 1.08 per cent respectively. Templeton Mutual Fund’s Franklin India Prima Fund and Blue Chip Fund picked up another 6 per cent in the company.

Basel pact draft to Be ready by May 2004

Business Line , January 25, 2004

The Basel committee on banking supervision probably will complete the drafting of new global capital standards, the so-called Basel II rules, by the middle of May, 2004. The committee, made up of central bankers and regulators from 13 countries, then will present an “agreement in principle to a new accord”, or the completed rules.

The Basel II rules are replacing 1988 guidelines that banks set aside 8 cents for each dollar they lend. International bank regulators last week agreed to complete the rule-writing project by mid 2004. The panel previously had aimed to finish drafting the proposals by the end of last year in order to implement the rules by the end of 2006.

IFCI Merger with PNB gets board approval

Business Line, January 30, 2004

Yet another development financial institution (DFI) is set to fade away from the financial horizon with the approval being granted for Punjab National Bank’s (PNB) acquisition of the country’s oldest term-lending institution, IFCI Ltd.

The move towards the merger has been given in-principle clearance by the board of directors of both PNB and IFCI at meetings held in Mumbai and New Delhi respectively.

The merger moves has been catalyzed by the Ministry of Finance that was keen to once-and-for-all end the troubles of the ailing IFCI that had been making repeated sorties to the Government for assistance. Post merger, PNB’s business would increase by Rs. 30,000 crore.

24

25

LIC Housing Finance issues 75 notices

Economic Times, February 10, 2004

LIC Housing Finance has issued 75 notices to defaulters in the western region under the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 where there has been a payment default for 12 months and above and have issued 35,10, and 30 notices to defaulters in Mumbai, Pune and Nagpur respectively.

Sundaram Home Finance launches Online Property Search

Site

Financial Express, February 13, 2004

Sundaram Home Finance Ltd. launched an online property search portal for home buyers on February 12, 2004. The portal would give information on residential projects coming up in Chennai, Bangalore, Hyderabad, Kochi, Trichy, Madurai and Coimbatore. Currently, about 425 projects have been listed on the portal. Customers can also make online application for housing loan through this site.

26

SEBI calls for streamlined Corporate Governance system

Business Line, February 14, 2004

The Securities and Exchange Board of India (SEBI) has called for a “streamlined system of corporate governance” which will ensure greater good for a far greater number – in short, a better deal for all stakeholders of a corporate entity.

According to SEBI top brass, since global companies coming into the country will now look forward to such a system, the issue of corporate governance has to be taken seriously.

SEBI is also in favour of certain industry bodies turning themselves into self-regulatory organizations (SROs) to ensure disclosure compliance, especially in the case of initial public offering (IPOs).

The regulator is now in talks with organizations such as the Association of Merchant Bankers and the Association of Mutual Funds in India for effective dialogue on how some of the bodies can emerge as SROs.

While the Narayan Murthy Committee has already held its reconvened sittings for a fresh set of guidelines, SEBI is now in the process of completing discussions at various levels.

While Indian industry is urging legislative and regulatory bodies to have a re-look at some of the disclosure/compliance requirements for corporates, which are being imposed in the garb of corporate governance, SEBI has clarified that the key word in corporate governance today was “disclosures”.

After all, the general investor, who is not so well informed needs these disclosures and he relies on SEBI to ensure total investor protection, he pointed out.

Bankers on edge as home loan defaults creep up

Business Line , February 15, 2004

Concern is rising among a section of lenders on the home loan front with defaults showing a steady increase. Bankers say that the negative fallout of continued intense competition among banks and housing finance companies for an increased share in the booming home loan market is starting to show with repayments’ record of borrowers coming under increased stress.

Top officials of the banks dealing with housing finance put the blame on “reckless lending policies” by some

Housing Scheme for EPF employees:

Business Standard, February 26, 2004

The Andhra Pradesh government in collaboration with the Employees Provident Fund plans to launch a housing programme for provident fund members. Giving details of the programme in Guntur on February 24, 2004, Andhra Pradesh Health Minister K. Siva Prasad Rao said that in the first phase 3,000 housing units would be constructed on 13 acres of land belonging to the state

27

lenders because of which defaults are beginning occur at a greater regularity. The wrong practices mentioned include over-financing of the asset or a high proportion of loan compared to the asset value.

Bankers also argue that some of the defaults are the result of uncertain corporate life with job losses taking place on account of companies going in for restructuring or downsizing.

Default on home loans was more when there has been a definite intent in defrauding the system.

government in Guntur, at a cost of Rs. 30 crore. The EPF accumulations would be used for the programme. Employees with at least five years’ service were eligible to apply, he said adding the beneficiaries would be selected on basis of their seniority. Construction will start in June and complete by March, 2005

NHB asks HUDCO to Shun High-Exposure States

Financial Express, March 1, 2004

The National Housing Bank (NHB) has asked Housing & Urban Development Corporation (HUDCO) to stop lending to states to which it has overexposure. The states include Karnataka, Kerala, West Bengal and Andhra Pradesh. HFCs are required to identify project risks, evaluate risk mitigation through appraisal of project contract and evaluation of credit worthiness of the contracting entities. HUDCO had been facing problems of default especially from state government entities.

RBI to train Banks for Post Basel II era

Economic Times, March 15, 2004

The Reserve Bank of India will shortly begin talks with commercial banks on the Basel II accord to create a better understanding of the new norms. The exercise is also aimed at preparing banks for a smooth transition to the new order.

The new accord seeks to capture the relationship between capital adequacy and risk management. It

SEBI may accept securitization as ‘approved security’ soon

Hyderabad, March 13, 2004

Aimed at providing a major fillip to the Indian securitization market, the Securities and Exchange Board of India (SEBI) is seriously considering a proposal to accept securitization as an ‘approved security’ and to allow the securitization instruments to be traded on the bourses.

Not Yet Home

Financial Express, March 25, 2004

Opinion remains divided. Many top bankers are on record saying that Indian interest rates will have to continue moving south to align with global trends, while business leaders such as Deepak Parekh are emphatic that they have reached rock bottom. The broad consensus is that interest rates are unlikely to rise in the near future and the big difference between global interest rates and ours will ensure a continued bias towards softer

28

includes not just the quantitative measures of risk, but incorporates supervisory review and public disclosures into the international framework.

IBA’s chief executive said that the launch of Basel II accord is likely to trigger consolidation among banks. Under the Basel II norms, banks would have to allocate capital on the basis of risks and not all would be able to provide sufficient capital leading to consolidation.

rates. That is why banks continue to be reluctant to give fixed rate loans, especially beyond five years. The fact that inflation has been contained over the last few days supports this view.

Moreover, so long as there is surplus liquidity in the system and banks remain reluctant to lend to industry, they will be forced to keep rates flat in order to be able to compete for the safer but narrow personal finance market. On the personal finance front also, nationalized banks, which do not have access to funds of varying longer time maturity, are hard pressed to maintain spreads in a highly competitive market. Margins on home loans have flattened until they are wafer thin. Banks are particularly handicapped in the competition because both housing finance and big ticket infrastructure funding requires long term money (typically 10 year funds), and they have access only to short-term funds. However, the Reserve Bank is planning to come to their rescue by permitting banks to float long-term bonds in order to avoid an asset-liability mismatch. This will not only enhance their competitive ability but will reinforce downward bias in interest rates, rather than signal a hike.

29

Housing News congratulates

Shri Rakesh Bhalla,Shri R Rajagopalan and

Shri V Raghu

on being promoted as General Managers

AND

Shri V Rajan,Shri N Udayakumar and

Shri T V Rao

on being promoted as Assistant General Managers

of the National Housing Bank

30

Related Documents