Lippincott Williams & Wilkins is collaborating with JSTOR to digitize, preserve and extend access to Medical Care. http://www.jstor.org Hospital Reorganization after Merger Author(s): Richard J. Bogue, Stephen M. Shortell, Min-Woong Sohn, Larry M. Manheim, Gloria Bazzoli and Cheeling Chan Source: Medical Care, Vol. 33, No. 7 (Jul., 1995), pp. 676-686 Published by: Lippincott Williams & Wilkins Stable URL: http://www.jstor.org/stable/3766531 Accessed: 09-03-2015 19:26 UTC Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at http://www.jstor.org/page/ info/about/policies/terms.jsp JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTC All use subject to JSTOR Terms and Conditions

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Lippincott Williams & Wilkins is collaborating with JSTOR to digitize, preserve and extend access to Medical Care.

http://www.jstor.org

Hospital Reorganization after Merger Author(s): Richard J. Bogue, Stephen M. Shortell, Min-Woong Sohn, Larry M. Manheim, Gloria Bazzoli and Cheeling Chan Source: Medical Care, Vol. 33, No. 7 (Jul., 1995), pp. 676-686Published by: Lippincott Williams & WilkinsStable URL: http://www.jstor.org/stable/3766531Accessed: 09-03-2015 19:26 UTC

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at http://www.jstor.org/page/ info/about/policies/terms.jsp

JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected].

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

MEDICAL CARE Volume 33, Number 7, pp 676-686 ?1995 Lippincott-Raven Publishers

Hospital Reorganization After Merger

RICHARD J. BOGUE, PHD,* STEPHEN M. SHORTELL, PHD,t MIN-WOONG SOHN, MA, LARRY M. MANHEIM, PHD,? GLORIA BAZZOLI, PHD,* AND CHEELING CHAN, MS*

Major organizational changes among hospitals, like system affiliation, merger, and closure, would seem to offer substantial opportunities for hospi- tals and health systems to be strategic in the local reconfiguration of health services. This report presents the results of a unique survey on what hap- pened to hospitals after mergers occurring between 1983 and 1988, inclusive. Building on an ongoing verification process of the American Hospital Asso- ciation, surviving institutions from all 74 mergers that occurred during the study frame were surveyed in the fall of 1991. Responses were received from 60 of the 74 mergers (81%), regarding the primary, postmerger use of the hos- pitals involved. Topics surveyed included the premerger competition be- tween the hospitals and in their environment, and what happened to the hospitals after their mergers. Mergers frequently served to convert acute, in- patient capacity to other functions, with less than half of acquired hospitals continuing acute services after merger. In the context of health care reform, mergers may offer an expeditious way locally to restructure health services. Evidence on the postmerger uses of hospitals and about the reasons given for merger suggests that mergers may reflect two general strategies: elimination of direct acute competitors or expansion of acute care networks. Key words: hospital; merger; consolidation; reform; antitrust. (Med Care 1995;33:676- 686)

Taken as a group, closures, mergers, and system affiliation would seem to have great potential for accomplishing fast and major reconfiguration of local health services, because they affect entire organi-

*From the Hospital Research and Educational Trust, American Hospital Association, Chicago, Illinois.

tFrom the J. L. Kellogg Graduate School of Manage- ment, Northwestern University Evanston, Illinois.

tFrom the University of Chicago, Chicago, Illinois.

?From the Center for Health Services Policy and Re- search, Northwestern University, Evanston, Illinois.

This paper was drawn from a study entitled "Effects of Horizontal Consolidation of Hospital Markets,"which was funded by the Agency for Health Care Policy and Re- search (grant no. 1-R01-HS-06250-01).

Address correspondence to: Richard J. Bogue, PhD, Hospital Research and Educational Trust, American Hos- pital Association, 1 North Franklin, 29th Floor, Chicago, IL 60606.

zations and not just arrangements for some

patients or contracts. Such whole organiza- tion changes could facilitate reductions in a market's excess capacity, reconfigura- tion of the mix of local services, and creation of new and stronger networks of consoli- dated capabilities.

Much research has been conducted on

hospital affiliation with multihospital sys- tems.1-4 Despite the promise systems have been perceived to hold for administrative coordination and operational efficiencies,5 research has not shown that organizing hos-

pitals in multihospital systems results in lower health care costs.6,7 However, other benefits of system affiliation may exist, and the longer-term impact of systems on costs and performance measures remains an area for examination.2'3

676

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

HOSPITAL REORGANIZATION AFTER MERGER

Closures, the most complete of organiza- tional changes, would be presumed to result

directly in a reduction in underused capac- ity, perhaps contributing therefore to sub- stantial cost savings. Rural community hos-

pitals have been particularly vulnerable to closure since 1986,* outnumbering urban closures 194 to 151 through 1990, while rep- resenting just under half of total hospitals.8 Moreover, new hospitals are disproportion- ately located in more densely populated ar- eas.t The potential cost savings of closure

may be more than offset by the costs in terms of access to care, health status, and

subsequent losses to the local economy.9-11 Overall, except for a substantial literature

describing merger processes,12 relatively lit- tle empirical research has been conducted on mergers and consolidations.t A major barrier to research on mergers is their rarity, with 74 taking place between 1983 and 1988.

Perhaps the greatest barrier to exploring these events carefully may be the lack of a database capable of such research, especially at the facility level. Restructuring involves two or more hospitals in dissolution, assimi- lation, or creation of new corporate entities. As a result, in national databases, such as the American Hospital Association's (AHA) Annual Survey data or Medicare Cost Re-

ports, hospitals merged into new or other entities no longer report at the facility level.

*Community hospitals, using the American Hospital Association's definition, are "nonfederal, short-term gen- eral and other specialty hospitals open to the public."

tThe net percentage change, from 1980 to 1990, of the total number of urban community hospitals is 1.0%. For rural hospitals, there has been a net reduction of 14.4% over the same period.8

tTechnically, "merger" and "consolidation" are discrete types covering a wide spectrum of organizational changes. For tax purposes, at least eight different classes of restruc- turing have been identified.13 However, the precision of these distinctions would detract from research focusing on the causes and effects of corporate restructuring. Di- viding legal restructuring into mergers and consolidations follows Finkler and Horowitz14 and Mullner and An- dersen.15 Mergers involve the dissolution of one or more organizations and their assimilation by another, whereas consolidations involve the dissolution of two or more or- ganizations and the formation of a new entity.

Although rare and difficult to observe across cases, mergers may have profound ef- fects on the structure and the efficiency of local health care delivery. A report by the United Hospital Fund found that hospital mergers in New York kept some hospitals from closure, "not merely by diluting or

shifting financial pressure, but by creating stronger institutions overall."10 Stark- weather and Carman, in presenting detailed cases of the evolution of competition in three communities, illustrate a three-

hospital merger that resulted in dramatic

improvement in financial performance for the postmerger organization, except that it then became engaged in an expensive game of advertising to compete with the other

"mega-organizations" in the area.16 Wool-

ley's examination of the competitive effects of local mergers suggests that mergers may "increase efficiency by reducing overcon-

sumption"and "some ... of the cost savings [are] passed on to consumers."17 And a re- cent report by the Inspector General pro- vides some evidence of cost savings and re- ductions in Medicare inpatient usage as a result of merger.18

This study uses data from a thorough merger identification and verification proc- ess conducted during 1989 to 1990 by the AHA, and reports results of a unique 1991 to 1992 survey of merger survivors from the 74 confirmed mergers that occurred from 1983 through 1988. The year 1983 was chosen be- cause it precedes the impacts of large envi- ronmental changes in the 1980s (eg, reim- bursement changes and rapid growth in

system affiliation and managed care sys- tems). The effects of many of these changes were apparent by 1988.

Two general explanations for mergers are examined in this paper: 1) reduction of di- rect competition and increased vertical inte- gration, or 2) strengthening of horizontal networks. That is, mergers may represent two discrete kinds of strategic behavior and, as a consequence, result in different post- merger uses of merging hospitals.

677

Vol. 33, No. 7

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

BOGUE ET AL.

Some mergers may be designed to re- duce direct competitors. This strategy of re- ducing direct competition might be ob- served through mergers in which the acquired hospital is closed or drops its acute functions. The economic advantages accru- ing to an acquirer by reducing direct com- petitors seem readily apparent. Such a strat- egy would also seem to be capable of conferring greater localized control over a broader array of services-that is, increasing vertical integration by turning competitors' resources into complementary services. In both instances-outright closure or elimina- tion of acute functions in the acquired hos- pital-the merger results in the reduction of direct competitors.

Alternatively, mergers may be designed to expand the local or regional network of hos- pital services, most notably by using ac- quired hospitals to expand the geographic base of the set of services offered under the new entity's umbrella. One advantage of adopting an integrative approach to organ- izational change would be the increased ca- pability for marketing the new and geo- graphically broader set of locations and services to managed care plans and other re- gional insurance mechanisms. This second strategy of horizontal networking through merger might be observed when both hospi- tals retain acute care functions.

The survey of merger survivors used for this study examined the premerger charac- teristics of acquiring and acquired hospitals and the uses to which acquired hospi- tals were put after merger, including whether they retained an acute care func- tion. Other elements of information from the survey and other data sources that are used here to explore whether two different general strategies for merger can be dis- cerned include: similarities and comple- mentarities of the hospitals merging with each other; respondents' judgments about the degree of competition between the merging hospitals and in their market; and the respondents' judgments about the

relative importance of a series of possible reasons for merger.?

Methods

During the 1980s, the AHA's Section for Health Care Systems engaged in an ongo- ing effort to track merger activity, princi- pally by checking the AHA's Annual Sur- vey each year and requesting reports of mergers from state and metropolitan hos- pital associations. Following up on that work in 1989 to 1990, the AHA's Division of Economic Analysis engaged in a careful identification and verification of general acute hospital mergers that occurred in the 1980s. The mergers were verified, and infor- mation characterizing each merger was gathered, via written communications and telephone interviews with those hospital personnel identified as best able to provide accurate information, often chief legal coun- sel. The data set includes the year of the merger, the old and new names of the insti- tutions involved, the city, state, an identifier for the specific type of merger that it repre- sented, and brief explanatory notes.

Those data were merged with 1983 AHA Annual Survey data for the component in- stitutions and 1988 Annual Survey data for the 74 resulting institutions. To enable analyses on the strategic purposes of merg- ers, acquiring hospitals were distinguished from acquired hospitals. Because more than two hospitals were rarely involved in the mergers, the database was limited to the two largest premerger institutions. For the pur- poses of this study, acquirers were defined as either the entity purchasing the assets of the other (in mergers, which occur when en- tity B is dissolved and subsumed by entity A) or as the larger of the two hospitals (in the case of consolidations, which occur when entities A and B dissolve to form entity C).

?For a copy of the survey instrument, contact the first author.

678

MEDICAL CARE

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

HOSPITAL REORGANIZATION AFTER MERGER

A hospital merger survey was designed specifically for this study. This survey sought information about the structures and rela-

tionships of the acquiring and the acquired general acute hospitals before and after

merger. Examples of such information in- clude what services were offered by the ac-

quiring and the acquired hospitals before the merger and whether each service was eliminated or modified at each facility as a result of the merger; what was the degree of

competition between the acquirer and the

acquired hospitals, and in their market in

general, before merger; and what were the reasons for the merger and what cost-containment efforts accompanied the

merger. In the fall of 1991, the survey was sent to

the chief executives of all 74 of the entities

resulting from the verified general acute

hospital mergers between 1983 and 1988. Efforts to maximize the response rate in- cluded telephone follow-up to the original survey, then sending a shortened survey in- strument, and then contacting state and

metropolitan hospital association staff. At least partial survey information was gath- ered for 60 of the 74 mergers, representing an 81% response rate for some survey items and reflecting the experience of 120 premer- ger hospitals. These survey data were ap- pended to the merger confirmation infor- mation and the Annual Survey data for all 74

mergers. Owing to the limited number of observa-

tions, this report is exploratory and the sta- tistical significance of tests should be inter-

preted with caution. On the other hand, the

survey respondents represent not a sample, but a large proportion of the universe of

possible observations. Testing the signifi- cance of effects with alpha set at 0.10 may be conservative.

Results

Hospitals in the Northeast region of the nation (the New England and Middle Atlan-

tic census divisions) were disproportionately involved in mergers, with 23% of the merg- ers and less than 15% of the hospitals. Meanwhile, merger activity appears to have been much lower than expected in the South (South Atlantic, East South Central, and West South Central census divisions), where 26% of the hospitals were in 1983, but

only 17% of the mergers. Table 1 shows some basic information

comparing acquiring to acquired hospitals before their mergers. Notice that, in terms of

acquiring or being acquired, there were no

significant differences in organizational form within the system-affiliated or the in-

dependent groups. As has been noted by many observers, however, not-for-profit sys- tem hospitals were disproportionately ac- tive, comprising 51.2% of acquiring system hospitals and 30% of all acquirers, 32.6% of

acquired system hospitals, and 20% of all

acquired hospitals, compared to about 12.5% of all hospitals in 1983.

A final note on organizational form re-

gards the low rate of involvement in merger by local government, nonsystem hospitals (representing 9% of acquiring and acquired hospitals, but making up 29% of hospitals nationwide in 1983). They had previously been found to be contract managed more than other groups of hospitals but not to be sought for system acquisition.2 Existing capital needs, underfunding, and a high pro- portion of uncompensated care would tend to make them unattractive merger part- ners,19 and some face governing and control mechanisms that inhibit their ability to inte-

grate with other hospitals.1

IEventually, health care reform appears likely to reduce the burden of uncompensated care through broader in- surance coverage and to increase government funding for some public and specially designated providers, but it re- mains to be seen if reducing these substantial barriers will make local government hospitals more attractive net- working partners. If the prevalence and distribution of uncompensated care becomes more equitable as a result of reform, it will provide a good opportunity to test whether governing and control mechanisms may present more intractable barriers than economic realities.

679

Vol. 33, No. 7

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

BOGUE ET AL.

TABLE 1. Premerger Characteristics

Acquirer Acquired Test = Value N P Value

Organizational Form

System owned, leased, or sponsored x2 = 0.802 43 0.370

Investor-owned 6.9% 9.3%

Not-for-profit 51.2% 32.6%

Independent hospitals Z2 = 2.734 98 0.255

Investor-owned 3.1% 9.2%

Not-for-profit 36.7% 37.8%

Government, nonfederal 7.2% 6.1% Bed size 310.1 143.8 t = 5.575 72, 71 0.000 Mean occupancy rate, by region

North East 81.2% 73.2% t = 2.072 17,16 0.049 South 72.8% 66.1% t= 1.610 19,19 0.117

North Central 71.3% 57.9% t = 3.618 24, 24 0.001

West 60.5% 58.2% t = 0.375 12,12 0.712

For mergers of the form Hospital A + Hos-

pital B = New Entity C (consolidations; see

previous footnote on "mergers"and "consoli- dations"), the larger hospital was defined by our decision rules to be the acquirer, so, as

expected, Table 1 shows the acquiring hospi- tals to be much larger in terms of beds (ac- quirer mean, n = 310.1, 72; acquired mean = 143.8, 71; t = 5.575, P < 0.0001). However, separate analyses of mergers of the form

Hospital A + Hospital B = Hospital A, in which the acquirer was easily identified as the legal survivor of the merger and the ac-

quiring entity, found effects of a similar

magnitude (acquirer mean, n = 313.7, 37; ac-

quired mean = 133.2, 37; t = 4.734, P < 0.0001). We take this, along with a desire for

clarity and efficiency of expression, as strong justification for assigning the designation of

"acquirer" to the larger hospital in consoli- dations, and for using the term "merger" to include both mergers and consolidations.

Two other points are worth noting, how- ever, with regard to bed size. Smaller hospi- tals tend to be underrepresented in mergers, especially as acquirers, of course. Hospitals under 100 beds comprised 14% of acquirers, 38% of acquired, and 45% of all hospitals.

Meanwhile, mid-size

merge tween

hospitals tend to

disproportionately. Hospitals be- 100 and 499 beds represented two

thirds of acquirers, over 60% of acquired hospitals, but just under 49% of all hospitals in 1983.

Finally, Table 1 shows premerger occu-

pancy rates by region. Everywhere but in the West, acquiring hospitals had signifi- cantly higher occupancy rates than the

hospitals that were acquired through merger. Although this effect appears to be

marginal in the South (acquirer mean, n = 72.80%, 19; acquired mean = 66.1%, 19; t = 1.610, P = 0.117), the difference is quite real even there because this comparison is based on a large proportion of the popula- tion, not on a sample.

Here is one possible explanation for the lack of differentiation between acquirers and acquireds in the West. Increasing growth by managed care organizations and quick responsiveness to new payment methodologies in Medicare, and early ex- perimentation in large western states'Medi- caid programs (especially Medical in Cali- fornia, and Arizona's Health Care Cost Containment System) may already have be-

680

MEDICAL CARE

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

HOSPITAL REORGANIZATION AFTER MERGER

TABLE 2. Postmerger Uses of Acquired Hospitals

Rural (%) Urban (%) X2 N P Value

Retained acute care 15.3 27.1 5.299 59 0.071

Converted to other inpatient uses 15.3 25.4

Closed, vacated 0.0 16.9

gun stimulating a large shift from inpatient to outpatient procedures. This may have

squashed down occupancy rates even for

hospitals about to acquire others. In any event, it seems almost certain that the utili- zation experiences of hospitals in the West

during the 1980s do not generalize well to the rest of the nation.

Table 2 shows how acquired hospitals were utilized after merger. The fact that they continued to be used for acute services after 42% of the mergers supports our notion that

merger may be an effective means of recon-

figuring health services. Conversion from

general acute to nonacute inpatient uses (eg, psychiatric and substance abuse services, re- habilitation, and long-term care) occurred 41% of the time, whereas acquired hospitals were closed in 17% of the mergers.

In both urban and rural areas, the ac-

quired hospital was about as likely to be converted to nonacute inpatient care as it was to continue delivering acute inpatient care. Reimbursement policies may help ex-

plain many of these conversions because, for

example, these nonacute services are paid by Medicare on a more favorable basis than are acute services. Especially in light of the fact that acquirers continue to perform acute functions, the new parent of the acquired or-

ganization also retains nearby acute care ca-

pabilities with which to enhance referral and

placement patterns. Table 2 also emphasizes the importance of

inpatient capacity to rural communities. None of the 18 mergers involving rural hos- pitals was reported to have resulted in

closing, being vacated, or use for a non-

inpatient purpose. In addition, the relatively greater proportion of elderly residents in ru-

ral areas, and a more rapid growth of aging populations in rural areas,"1 may place a pre- mium on services used heavily by the eld-

erly, such as long-term and rehabilitation care.

Table 3 shows some similarities and com-

plementarities between the acquiring and

acquired hospitals, giving a first look at whether mergers may be designed for one of two general strategies: reduction of direct

competition or horizontal network forma- tion. The similarity ratios in Table 3 would be 1.00 when the acquiring and acquired hos-

pitals were the same, with ratios below 1.00

showing how much lower the values were for the acquired hospitals relative to the ac-

quiring hospitals. In mergers in which both hospitals re-

tained acute services, the acquirer and the

acquired had greater similarity in service mix, full-time equivalents per bed, and in

occupancy rates, the last effect not being significant, compared with mergers in which one hospital dropped acute care. Hospitals that eventually merged and yet kept acute services in both premerger facilities also had

greater complementarity in location (shown by greater distances). Similarity in service mix (suggested both by the proportion of services duplicated and the similarity of full- time equivalents per bed), yet complemen- tarity in service location, suggests a pattern of horizontal network development.

Meanwhile, in cases in which acute care was dropped at one of the hospitals, the

IOutmigration by the young, with concomitant reten- tion of elderly populations and increasing retirement in rural communities, has been noted as a source of substan- tial demographic pressure on rural systems of health care.20

681

Vol. 33, No. 7

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

BOGUE ET AL.

TABLE 3. Similarity of Merged Hospitals and the Retention of Acute Care Functions

Both Retain Acute One Drops Acute t nl, n2 P Value

Services duplicated 53.0% 40.4% 2.436 20, 38 0.018 Distance 4.9 miles 2.4 miles 1.733 20, 38 0.095 Similarity ratios

FTEs per bed acquired/acquirer 1.01 0.85 1.628 19, 38 0.109 Occupancy rates acquired/acquirer 0.95 0.86 1.218 19, 38 0.229 Beds acquired/acquirer 0.64 0.84 -0.767 19, 38 0.447

FTE, full-time equivalent.

greater disparity between the merging hos- pitals in terms of service mix suggests that the way had been paved before merger to lead up to the elimination of acute services at one of the hospitals. That is, dropping acute services in the acquired facility seems to have been presaged by a higher degree of

specialization in the merger entrants before merger. That most of this specialization be- fore merger occurred at the acquired hospi- tal is supported by the fact that 63% of the

nonduplicated services resided in the ac-

quirer and 37% in the acquired hospital. In addition to this clear signal of strategic be- havior leading toward a reduction in direct

competitors, the significantly closer proxim- ity of merger entrants when one drops acute services suggests a "clearing"of the immedi- ate field of competitors.

Tables 2 and 3 provide evidence of two different general merger strategies, one re-

ducing direct competitors and the other

building larger horizontal networks for hos-

pital care. Table 4 presents ratings of compe- tition provided by survey respondents.# When one of the hospitals dropped its acute functions, respondents indicated that the

merging hospitals had been highly competi- tive with each other for both inpatient and

#The items discussed in Tables 4 and 5 were seven- point Likert-type scales. The first two points of the scales on competition, shown in Table 4, were characterized as "Not at all Competitive"; the middle three points were defined as "Moderately Competitive"; the final two points were labeled "Highly Competitive."A similar structure was used for the reasons shown in Table 5 ("Not at all Im- portant, "Moderately Important," and "Very Important"). In both Tables, the presented data reflect scale points 6-7.

outpatient services before merger. But when both retained acute services, significantly fewer of the respondents judged the pre- merger competition between the two even- tual merger entrants to be high.

In addition, where one of the hospitals dropped acute care, respondents judged the overall market to be highly competitive at the time of the merger. This was not the case in markets in which both retained acute care. Table 4 shows quite clearly that the elimination of acute functions in one of the

merging hospitals was more often associ- ated with high degrees of competition.

Table 5 shows the level of importance in

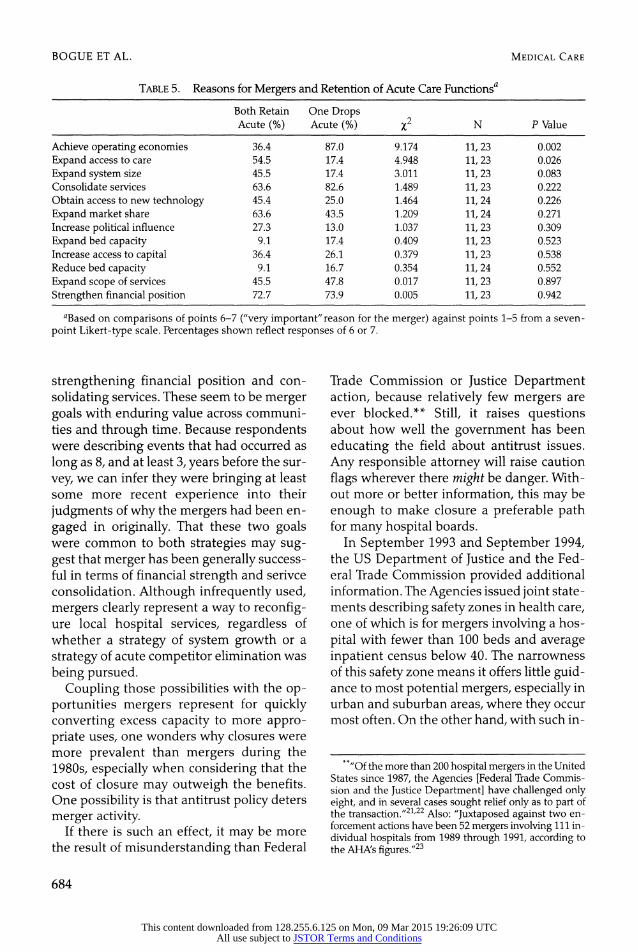

explaining their own mergers that respon- dents ascribed to each of a number of possi- ble reasons for merger. The results add cre- dence to the idea that there are two distinct

merger strategies-one type to reduce direct competitors and one to expand networks. For mergers in which both hospitals re- tained acute services, the reasons charac- terized as "very important" most often were 1) strengthen financial position, 2) expand market share, 3) consolidate services, and 4) expand access to care. For mergers in which one hospital dropped its acute functions, the four reasons that were most often described as very important were 1) achieve operat- ing economies, 2) consolidate services, 3) strengthen financial position, and 4) expand scope of services. Two of these four very im- portant reasons appear on both lists, sug- gesting a basic, common strategy for both types of mergers of strengthening financial position and consolidating services.

682

MEDICAL CARE

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

HOSPITAL REORGANIZATION AFTER MERGER

TABLE 4. Competition and Retention of Acute Care Functionsa

Both Retain One Drops Acute (%) Acute (%) X2 N P Value

Direct competition high for inpatient services 27.3 65.2 4.300 11, 23 0.038

Direct competition high for outpatient services 27.3 56.5 2.555 11, 23 0.110

Direct competition high for new technology 9.1 34.8 2.253 11, 23 0.112

Direct competition high for medical staff 9.1 30.4 1.884 11, 23 0.170

Direct competition high for nursing staff 27.3 39.1 0.458 11, 23 0.498

Overall market competition high at time of merger 22.2 59.1 3.476 9,22 0.062

Overall market competition high at time of survey 22.2 38.1 0.714 9, 21 0.398

aBased on comparisons of points 6-7 ("very high"competition) against points 1-5 from a seven-point Likert-type scale. Percentages shown reflect responses of 6 or 7. Direct competition refers to respondents'judgments about competition between the acquirer and acquired hospitals.

However, there was substantial diver-

gence between the two types as well. Merg- ers leading up to the elimination of acute services in one of the hospitals were effected

significantly more often to achieve operat- ing economies, which in the survey's list of

potential reasons may refer to maximizing the efficiency of inputs and outputs (ie, re- ferrals and placements). Mergers leading up to the retention of acute services in both fa- cilities were explained significantly more often as expanding access to care and ex-

panding system size.

Discussion

A key issue is how major organizational changes, such as closures, mergers, and sys- tem affiliations, can contribute to mitigating some of the pernicious problems in health care (eg, expensive, excess, acute care capac- ity). This study shows that mergers represent a significant mechanism for converting acute, inpatient capacity to other functions.

Especially in the context of health care re- form, and increased restructuring of health services delivery, mergers may offer an expe- ditious approach to structural change.

An important question, however, is when and where different strategic approaches to- ward merger are most appropriate. This

study offers evidence that mergers may

serve two distinct purposes: reducing direct

competitors or expanding acute care net- works. Where the strategy was to reduce di- rect competitors, the preferred targets seem to have been hospitals that were easier to

nudge out of acute care functions, and into nonacute functions, because they were mov-

ing toward specialization already. They were also very proximate geographically.

Where the overall strategy rests more on network-wide, horizontal growth of acute care capacity, preferred partners appeared to be those hospitals that were most similar to each other in terms of service mix. They were also in the general vicinity, but signifi- cantly less proximate. This second strategy would seem to have greater applicability across communities and in the future for several reasons. First, the number of some- what specialized and highly proximate hos-

pitals is simply much more limited. Second, reimbursement for nonacute functions is

becoming less favorable as payors learn to

apply the lessons of acute care payment to other areas. Third, and perhaps most signifi- cantly, the second strategy of network-wide horizontal growth seems to have much more capability for spanning larger geo- graphic areas, and therefore being a major factor in managed care contracting.

On the other hand, these two distinct

strategies share the common goals of

683

Vol. 33, No. 7

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

BOGUE ET AL.

TABLE 5. Reasons for Mergers and Retention of Acute Care Functionsa

Both Retain One Drops Acute (%) Acute (%) x2 N P Value

Achieve operating economies 36.4 87.0 9.174 11, 23 0.002

Expand access to care 54.5 17.4 4.948 11,23 0.026

Expand system size 45.5 17.4 3.011 11, 23 0.083 Consolidate services 63.6 82.6 1.489 11, 23 0.222 Obtain access to new technology 45.4 25.0 1.464 11, 24 0.226

Expand market share 63.6 43.5 1.209 11, 24 0.271 Increase political influence 27.3 13.0 1.037 11, 23 0.309

Expand bed capacity 9.1 17.4 0.409 11, 23 0.523 Increase access to capital 36.4 26.1 0.379 11,23 0.538 Reduce bed capacity 9.1 16.7 0.354 11, 24 0.552

Expand scope of services 45.5 47.8 0.017 11, 23 0.897

Strengthen financial position 72.7 73.9 0.005 11, 23 0.942

aBased on comparisons of points 6-7 ("very important" reason for the merger) against points 1-5 from a seven- point Likert-type scale. Percentages shown reflect responses of 6 or 7.

strengthening financial position and con-

solidating services. These seem to be merger goals with enduring value across communi- ties and through time. Because respondents were describing events that had occurred as

long as 8, and at least 3, years before the sur-

vey, we can infer they were bringing at least some more recent experience into their

judgments of why the mergers had been en-

gaged in originally. That these two goals were common to both strategies may sug- gest that merger has been generally success- ful in terms of financial strength and serivce consolidation. Although infrequently used, mergers clearly represent a way to reconfig- ure local hospital services, regardless of whether a strategy of system growth or a

strategy of acute competitor elimination was

being pursued. Coupling those possibilities with the op-

portunities mergers represent for quickly converting excess capacity to more appro- priate uses, one wonders why closures were more prevalent than mergers during the 1980s, especially when considering that the cost of closure may outweigh the benefits. One possibility is that antitrust policy deters

merger activity. If there is such an effect, it may be more

the result of misunderstanding than Federal

Trade Commission or Justice Department action, because relatively few mergers are ever blocked.** Still, it raises questions about how well the government has been

educating the field about antitrust issues.

Any responsible attorney will raise caution

flags wherever there might be danger. With- out more or better information, this may be

enough to make closure a preferable path for many hospital boards.

In September 1993 and September 1994, the US Department of Justice and the Fed- eral Trade Commission provided additional information. The Agencies issued joint state- ments describing safety zones in health care, one of which is for mergers involving a hos-

pital with fewer than 100 beds and average inpatient census below 40. The narrowness of this safety zone means it offers little guid- ance to most potential mergers, especially in urban and suburban areas, where they occur most often. On the other hand, with such in-

**"Of the more than 200 hospital mergers in the United States since 1987, the Agencies [Federal Trade Commis- sion and the Justice Department] have challenged only eight, and in several cases sought relief only as to part of the transaction."21'22 Also: "Juxtaposed against two en- forcement actions have been 52 mergers involving 111 in- dividual hospitals from 1989 through 1991, according to the AHAs figures."23

684

MEDICAL CARE

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

HOSPITAL REORGANIZATION AFTER MERGER

formation and increasing awareness about the rarity of antitrust challenges to hospital mergers, hospital boards of the future should grow less fearful of government in- tervention in a possible merger.

Several areas seem most ripe for further

exploration. Given the small number of

mergers and the complexities that make each unique, in-depth case studies could

provide useful insights. Whether mergers serve to reduce direct competition or to ex-

pand acute care networks is not of merely academic interest. If certain mergers result in stronger vertical or horizontal networks, as well as reduced acute care capacity, sys- tematic case analysis might give valuable

guidance to local decision makers, policy makers, and advocates of network-oriented reform. National Democratic leadership, the AHA, VHA Inc., and the Catholic Health As- sociation of the United States are among the advocates of such reform.

Finally, case-based looks at institutions and communities after merger would an- swer some of the most important questions. How does a community perceive the change and the resulting institution? Under what circumstances does a community turn away from the postmerger entity, and when does a community embrace it? Under what cir- cumstances is a merger obstructive to the public good, and when is merger right and helpful, leading to lower costs to the com- munity, improved access, or better quality?

Acknowledgments

The authors thank Simonetti Samuels, JD, Loyola University, for her efforts in verifying mergers and con- solidations while at the American Hospital Association, and Jeffrey Alexander, PhD, University of Michigan, for his assistance in survey design.

References 1. Sloan FA, Morrisey MA, Valvona J. Capital mar-

kets and the growth of multihospital systems. In: Ros- siter LF, Scheffler RM, eds. Advances in health economics and health services research, Vol. 7. Green- wich, CT: JAI Press, 1987:83.

2. Morrisey MA, Alexander JA. Hospital participa- tion in multihospital systems. In: Rossiter LF, Scheffler RM, eds. Advances in health economics and health services research, Vol. 7. Greenwich, CT: JAI Press, 1987:59.

3. Alexander JA, Morrisey MA. Hospital selection into multihospital systems: the effects of market, man-

agement, and mission. Med Care 1988;26:159.

4. Manheim LM, Shortell SM, McFall S. The effect of investor-owned chain acquisitions on hospital expenses and staffing. Health Serv Res 1989;24:461.

5. Zuckerman HS, Weeks LE. Multi-institutional

hospital systems. Chicago: Hospital Research and Edu- cational Trust, 1979.

6. Shortell SM. The evolution of hospital systems: unfulfilled promises and self-fulfilling prophecies. Medi- cal Care Review 1988;45:177.

7. Shortell SM, Morrison EM, Friedman B. Strategic choices for America's hospitals: managing change in tur- bulent times. San Francisco: Jossey-Bass, 1990.

8. American Hospital Association. Hospital clo- sures, 1980-1990: a statistical profile. Chicago, IL: American Hospital Association, Hospital Data Center, 1991.

9. Fickenscher K, Lagerwell-Voorman LM. An overview of rural healthcare. In: Shortell SM, Rein- hardt UE, eds. Improving health policy and manage- ment. Ann Arbor, MI: Health Administration Press, 1992:111.

10. United Hospital Fund. An analysis of hospital fi- nancial condition and hospital closure and merger. New York: United Hospital Fund, 1987.

11. Hart LG, Pirani MJ, Rosenblatt RA. Causes and

consequences of rural small hospital closures from the

perspectives of mayors. Seattle, WA: WAMI Rural Health Research Center, 1990.

12. Starkweather DB. Hospital mergers in the mak-

ing. Ann Arbor, MI: Health Administration Press, 1981.

13. Elrod JL Jr, Shields GB, Bergman JT. Merging health care institutions: a guidebook for buyers and sell- ers. Chicago: American Hospital Publishing, 1987.

14. Finkler SA, Horowitz SL. Merger and consolida- tion: an overview of activity in healthcare organizations. Healthcare Financial Management 1985;39(1):19.

15. Mullner RM, Andersen RM. A descriptive and financial ratio analysis of merged and consolidated

hospitals: United States, 1980-1985. In: Rossiter LF, Scheffler RM, eds. Advances in health economics and health services research, Vol. 7. Greenwich, CT: JAI Press, 1987:41.

16. Starkweather DB, Carman JM. Horizontal and vertical concentrations in the evolution of hospital com-

petition. In: Rossiter LF, Scheffler RM, eds. Advances in

685

Vol. 33, No. 7

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

BOGUE ET AL.

health economics and health services research, Vol. 7. Greenwich, CT: JAI Press, 1987:179.

17. Woolley JM. The competitive effects of horizontal mergers in the hospital industry. Journal of Health Eco- nomics 1989;8:271.

18. Office of the Inspector General, Department of Health and Human Services. Effects of hospital mergers on costs, revenues, and patient volume. Washington, DC: Office of the Inspector General, publication no. OEI-12-90-02450, 1992.

19. Friedman E. Public hospitals often face unmet capital needs, underfunding, uncompensated patient- care costs. JAMA 1987;257:10.

20. Hospital Research and Educational Trust. Working together to improve health services delivery: observations on collaboration by rural hospitals and health care systems. 1992:24.

21. US Department of Justice and the Federal Trade Commission. Statements of antitrust enforcement policy in the health care area. September 15,1993.

22. US Department of Justice and the Federal Trade Commission. Statements of Enforcement Policy and Analytic Priniciples Relating to Health Care and Anti- trust. September 27, 1994.

23. Burda D. Mergers thrive despite wailing about adversity. Modem Healthcare 1992;0ctober 12:26.

686

MEDICAL CARE

This content downloaded from 128.255.6.125 on Mon, 09 Mar 2015 19:26:09 UTCAll use subject to JSTOR Terms and Conditions

Related Documents