Exclusive to Healthcare. Dedicated to People. SM Copyright 2013, INTEGRATED Healthcare Strategies. All rights reserved. HOSPITAL AND HEALTH SYSTEM STRATEGY 101 PRESENTED BY: PETE MITCHELL, CONSULTANT July 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Exclusive to Healthcare. Dedicated to People. SM

Copyright 2013, INTEGRATED Healthcare Strategies. All rights reserved.

HOSPITAL AND HEALTH SYSTEM STRATEGY 101

PRESENTED BY:

PETE MITCHELL, CONSULTANT

July 2014

Exclusive to Healthcare. Dedicated to People. SM

Table of contents

• Hospital Characteristics

– Ownership

– Size

– Market Dynamics

– Scope of Services

– Level of Integration

– Governance

• Hospital Economics

– Example Income Statement Mechanics and Productivity Measures

– Revenue: DRG payments

– Revenue: Payer Mix

– Expenses

1

Exclusive to Healthcare. Dedicated to People. SM

HOSPITAL CHARACTERISTICS

2

Exclusive to Healthcare. Dedicated to People. SM

Hospital Overview – Ownership Type

1. For-Profit, investor owned (~ 20% of Hospitals)

– Example: Hospital Corporation of America is the largest for-profit system

– 160+ Hospitals

– 110+ freestanding surgery centers

– Trades on NYSE: HCA

2. Not-for-Profit (Private), privately owned organizations (~ 56%)

– Example: Hospital Sisters Health System

– 13 Hospitals

– Clinic and outpatient network

– Religious affiliation

3. Public – State or local government owned (~20%)

– Example: Hennepin County Medical Center

– One Hospital in downtown Minneapolis

– Network of clinics in Minneapolis and select suburbs

4. Public – Federally owned (~4%)

– Example: 23 regional VA health care systems

– Minnesota is part of “VA Midwest Health Care Network”

– Over 150 hospitals

– Over 1700 facilities

3

Potential Source: Hospital and system websites or AHA

Exclusive to Healthcare. Dedicated to People. SM

Hospital Overview – Size

1. Beds

– Beds are the most common measure of size. Large hospitals have 500+ beds. Many hospitals have less than 25 beds.

– Hospitals with less than 25 beds and located 35 miles from any other facility may be eligible for “critical access” status

– Many hospitals report “licensed” beds, which can be misleading (a hospital can be licensed for 500 beds but have a floor of 100 beds completed dormant).

– The actual bed count is “staffed” beds, which are actively managed beds.

2. Admissions/Discharges/Days

– A more accurate measure of “size” is annual discharges (note: always exclude normal newborns from calculations)

• Admissions are the number of patients checked in to the hospital

• Discharges are the number of patients released from the hospital

• Annual Days represent the number of patient days over the course of the year.

• Average Daily Census (ADC) is the annual patient days / 365

• Average Length of Stay (ALOS) is a common statistic reviewed by administration and benchmarked nationally by patient condition. It is calculated by Total Days / Total Discharges

3. Occupancy

– Occupancy can be a good indicator of a hospital’s financial health. The occupancy rate is calculated by the ADC / average number of staffed beds.

• Occupancy rates from 66% to 80% is typically the “sweet spot” for financial performance

• Occupancy rates < 66% are typically under utilized facilities and can be challenging for financial performance

• Occupancy rates in > 80% are typically over utilized facilities and can be challenging for financial performance

4

Potential Source: Hospital and system websites or AHA

Exclusive to Healthcare. Dedicated to People. SM

Hospital Overview – Market Dynamics

(Developed Markets)

1. Drive Times / Primary Service Areas

2. Demographics

3. Competition

4. Market Share

5. Outmigration

5

Exclusive to Healthcare. Dedicated to People. SM

Market Dynamics - Drive times zones are established to

understand and segment the geographic market and

identify competitor proximity

Dignity Health

IASIS Healthcare

Mayo

Abrazo Health Care

Banner Health

All other (sub-acute & post-acute

excluded)

Health System Profiles

Note: 15 minute drive time zone represents 15 minutes from at least one JCL or SHC hospital. 30 minute drive time zones represent 16 - 30 minutes from at least one JCL or SHC hospital.

6

Source: Mapquest

Exclusive to Healthcare. Dedicated to People. SM

Market Dynamics - Population

2013 P

op

ula

tio

n b

y Z

ip C

od

e

2013 Population by Zone

2013 Population by Age Cohort

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

85+

75-84

65-74

45-64

18-44

0-17

1,570,226

100,158 83,609

874,363 975,602

-

400,000

800,000

1,200,000

1,600,000

2,000,000

Po

pu

lati

on

Source: Claritas and Mapquest

7

Exclusive to Healthcare. Dedicated to People. SM

Market Dynamics – HH Income

2013 M

ed

ian

Ho

useh

old

In

co

me b

y Z

ip

2013 Median Household

Income by Zone

$-$10,000 $20,000 $30,000 $40,000 $50,000 $60,000 $70,000 $80,000 $90,000 $100,000

$-$10,000 $20,000 $30,000 $40,000 $50,000 $60,000 $70,000 $80,000 $90,000

$100,000

Me

dia

n H

H In

com

e

National Median Household Income

8

Source: Claritas and Mapquest

Exclusive to Healthcare. Dedicated to People. SM

Market Dynamics – Market Share (IP

Discharges)

15 Minute Drive Time Zone: Discharges by Hospital Year Ended 9/30/10 to 12/31/12

Potential Source: State Hospital Database

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

9/30/2010 12/31/2010 3/31/2011 6/30/2011 9/30/2011 12/31/2011 3/31/2012 6/30/2012 9/30/2012 12/31/2012

Cu

mu

lati

ve %

Ch

ange

Dis

char

ges

JCL (#3) SHC (#2) Banner (#1) Abrazo (#4) Dignity (#5)

All Other JCL Cum. % Change SHC Cum. % Change Banner Cum. % Change 15 Min Cum. % Change

9

Exclusive to Healthcare. Dedicated to People. SM

Market Dynamics – Inpatient Payer Mix

15 Min Zone Payer Mix CY 2010 and CY 2012

JCL Payer Mix CY 2010 and CY 2012

SHC Payer Mix CY 2010 and CY 2012

Potential Source: State Hospital Database

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2010 2012

Medicare Medicare Advantage AHCCCS/Medicaid Commercial HMO Self pay/other

-

50,000

100,000

150,000

200,000

2010 2012

Dis

char

ges

-

5,000

10,000

15,000

20,000

25,000

2010 2012

Dis

char

ges

-

5,000

10,000

15,000

20,000

25,000

30,000

2010 2012

Dis

char

ges

10

Exclusive to Healthcare. Dedicated to People. SM

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

WEI

PA

s

Discharges OP Adjustment CMI Adjustment

Market Dynamics – WEIPAs (Alt. measure of

productivity)

WEIPA Calculation by Hospital

WEIPA = Weighted Equivalent Inpatient Admission Discharges x OP Adjustment x CMI Adjustment

0

20

40

60

80

100

120

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Pai

d h

ou

rs /

WEI

PA

WEI

PA

s

Discharges OP Adjustment CMI Adjustment Paid hours / WEIPA

= Total gross charges / IP gross charges

11

Potential Source: State Hospital Database

Exclusive to Healthcare. Dedicated to People. SM

Market Dynamics – Example Hospital Profile

-

20,000

2010 2012

Self pay/other HMOCommercial AHCCCS/MedicaidMedicare Advantage Medicare

-

5,000

10,000

15,000

20,000

2010 2012

Primary/SecondaryTertiaryQuaternary

213

2,097

2,884

846

1,800

93

1,085

1,342 430

2,430

1,312

395 505

1,068

Behavioral Health Cardiovascular General Medicine General SurgeryGI Neonatology Neurosciences OB/GYNOncology Orthopedics Pulmonary RehabilitationSpine Trauma

CY 2012 Service Line Mix 2010 – 2012 r in Discharges

Payer Mix Acuity Level 2012 CMI = 1.49

CY 2012 Discharges by Zip = 12,301

(400) (200) - 200 400

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2010 2012

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2010 201215 Minute North 30 NE 30 SW 30 SE 30 Other AZ Outside AZ

70% 11% 0% 6% 1% 10% 3%

Percent of Discharges by Patient Origin Zone

70 2,344

2,789

767

2,778 11

547 80

403 768 1,619

- 67 58

12

Potential Source: State Hospital Database and Mapquest

Exclusive to Healthcare. Dedicated to People. SM

Market Dynamics – Outmigration

CY „12 Service Line Mix

Payer Mix

Acuity Level CMI = 1.37

Discharges originating in

15 min zone

Payer Mix Payer Mix

Acuity Level CMI = 1.47 Acuity Level CMI = 1.45

-

50

100

150

200

2010 2012

Dis

char

ges

(00

0s)

-

50

100

150

200

2010 2012

Dis

char

ges

(00

0s)

12,067

18,324

25,975

7,587

19,248 2,597

7,850

21,689

4,920

9,779

12,237

2,429 2,385 2,126

CY „12 Service Line Mix

Total Discharges

= 149,213

Remaining in Zone =

127,372 (85%)

Out-Migrating

= 21,841 (15%)

-

20

40

60

80

100

120

140

160

2010 2012

Dis

char

ges

(00

0s)

Other

Mayo

PhoenixChildren'sHosp.IASISHealthcare

MaricopaIntegratedHealth SystemDignity

Abrazo

Banner

SHC

JCL

-

5

10

15

20

25

2010 2012

Dis

char

ges

(00

0s)

CY „12 Service Line Mix

-

5

10

15

20

25

2010 2012

Dis

char

ges

(00

0s)

-

50

100

150

2010 2012D

isch

arge

s (0

00

s)

-

50

100

150

2010 2012

Dis

char

ges

(00

0s)

9,164

15,977

22,398

6,613

16,472

2,314

6,811

18,996

4,238

7,621

10,594

2,247 1,966 1,961

-

50

100

150

2010 2012

Dis

char

ges

(00

0s)

Quaternary

Tertiary

Primary/Secondary

9,164

15,977

22,398

6,613

16,472

2,314 6,811

18,996

4,238

7,621

10,594

2,247 1,966 1,961 Behavioral Health

CardiovascularGeneral MedicineGeneral SurgeryGINeonatologyNeurosciencesOB/GYNOncologyOrthopedicsPulmonaryRehabilitationSpineTrauma

2,903

2,347

3,577

974

2,776

283 1,039

2,693

682

2,158

1,643 182 419 165

-

50,000

100,000

150,000

200,000

1

Self pay/ other

HMO

Commercial

AHCCCS/ Medicaid

Medicare Advantage

Medicare

13

Potential Source: State Hospital Database

Exclusive to Healthcare. Dedicated to People. SM

Hospital Overview – Rural Markets: Critical

Access Hospitals

We just reviewed the situation in Phoenix, AZ where competition and access is plentiful. However, in many rural communities this is not the case. To promote coverage to these rural communities, in 1997 the government developed the designation of a “Critical Access Hospital.”

14

http://www.cms.gov/Outreach-and-Education/Medicare-Learning-Network-MLN/MLNProducts/downloads/CritAccessHospfctsht.pdf

Critical Access Hospitals are: 1. Over 35 miles from any other Inpatient

Facility

2. Less than 25 inpatient beds

3. Provide 24/7 emergency department

4. Typically the “first line” where patients are

stabilized and then transferred to trauma

centers

5. Receive financial support from CMS

through a separate payment method (paid

at 101% of costs)

Exclusive to Healthcare. Dedicated to People. SM

Emergency Department – 24/7/365 care for walk-in or ambulance

• Advanced emergency departments can receive a “trauma center” designation from the American College of Surgeons. Levels determine the sophistication and on-site presence of surgeons:

– Level I – Highest designation: Meets all the lower level requirement and includes 24/7 coverage of surgical specialists (e.g., orthopedic, neuro, plastic, anesthesia, critical care)

– Level III – Lowest designation: and includes 24/7 coverage of medical physicians (e.g., ED physicians, internal medicine, critical care)

Hospitals – Scope of Services

15

Intensive Care Unit (“ICU”) • ICUs are for patients who need some type of medical

intervention to maintain normal functions (i.e.,

breathing). These patients typically are in the ICU until

stabilized at which point they can be transferred to a

normal hospital bed or long term care facility. ICUs are

staffed by Critical Care/Intensivists and highly trained

APCs.

Specialty focused facilities • Pediatrics

• Orthopedic

• Heart and Vascular

• Women’s / Birthing Center

• Oncology

Potential Source: Hospital websites

Exclusive to Healthcare. Dedicated to People. SM

Hospitals expanding capabilities

Horizontal Integration

• Hospitals have merged to become systems, with major markets typically served by 2-4 major health systems

• Independent rural facilities and specialty hospitals still exist

• Drivers of horizontal integration

– Expense/cost savings

– Streamlining of service lines (e.g., Heart Center)

– Payer relationships

– Growth opportunities are limited in saturated markets (Certificate of need requirements)

– Financial restructuring / capital constraints

Vertical Integration

• Hospitals moving up (or down) the supply chain of patients

• Acquisitions include physician organizations, long term care facilities, home healthcare capabilities.

• Vertical integration is a pre-requisite for ACOs

– Payer/Hospital integration is on the rise

• Drivers of vertical integration

– Population health mentality

– Expense/cost savings

– Streamlining of service lines (e.g., Heart Center)

– Payer relationships / ACO positioning

16

Potential Source: Hospital websites, annual reports, and/or tax records, audit reports

Exclusive to Healthcare. Dedicated to People. SM

Decision Making / Governance - Hospital

17

Board of Directors

C-Suite Administrators

Medical Staff Committees

Medical (Physician) Service Line Leaders

Operational/ Department

(Business) Leaders

Potential Source: Hospital websites, annual reports, and/or tax records, audit reports

Exclusive to Healthcare. Dedicated to People. SM

Decision Making / Governance - Health

System

18

Health System

Region B Region A

Hospital B

Hospital A

Hospital D

Hospital C

Physician Group

Board of Directors

C-Suite

Decision Making Boards / Leadership at

every level of the organization

Potential Source: Hospital websites, annual reports, and/or tax records, audit reports

Exclusive to Healthcare. Dedicated to People. SM

Hospital Characteristics Overview

19

Hospital Characteristic Strategic Implication Financial Impact

Ownership (Type – for-profit vs.

nonprofit vs. gov’t)

Determine overall financial and

strategic goals

Determine overall financial and

strategic goals

Size (Capacity, Occupancy, ALOS,

Beds, Etc)

Determines the ability to serve the

patient community

Occupancy and ALOS are key drivers

of profitability

Primary service areas, demographics,

competition, market share,

outmigration

Hospitals must react to local

demographics and market conditions.

Competition, market share, and

outmigration are major strategic

initiatives.

Demographics and competitive

position determines payer mix

Scope of services (Trauma, ICU, ED,

specialty focus)

Services are required for licensing

and/or implemented to create a

leadership position within the market

(i.e., Heart Center of Excellence)

Service lines financial performance

vary by specialty

Level of integration Determines “integration” of services

and ability to manage population

health

The “physician organizations” are

typically subsidized by the hospitals

Governance

Within large systems, decision making

requires many levels of approval

Large systems can be less agile

Exclusive to Healthcare. Dedicated to People. SM

HOSPITAL ECONOMICS

20

Exclusive to Healthcare. Dedicated to People. SM

Gross Revenue 1,000,000$

Less: Contractual Allowances 600,000

Net Patient Service Revenue 400,000

Total Expenses 390,000

Operating Income (Loss) 10,000$

Operating Margin 2.5%

Hospital Profit and Loss Statement

Hospital Economics – Example P & L

21

Hospital’s typically operate

between (3.0%) to 3.0%

profitability

Exclusive to Healthcare. Dedicated to People. SM

Hospital Economics – Revenue: MS-DRG

Payment System

22

MS-DRG (Medicare Severity Diagnosis Related Groups ) payment system is how hospitals get paid for inpatient services. The DRG system was created by Yale School of Medicine and was adopted by Medicare as the reimbursement system for Inpatient Hospital Stays in 1982. The MS-DRG system was implemented in 2007. Private payers have also adopted the MS-DRG payment system.

• Trevor Jakubek authored a detailed presentation on this topic in June of 2013 (Saved on the P:)

The top Medicare procedures (by national volume) for 2012 are as follows:

Source: http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Medicare-Provider-Charge-Data/Inpatient2012.html

Rank DRG Definition Total

Discharges

Average

Covered

Charges

Average

Total

Payments

Average

Medicare

Payments

1 470 - MAJOR JOINT REPLACEMENT OR REATTACHMENT OF LOWER EXTREMITY W/O

MCC 432,007 $52,249.25 $14,469.80 $12,059.43

2 871 - SEPTICEMIA OR SEVERE SEPSIS W/O MV 96+ HOURS W MCC 347,249 $50,824.54 $13,867.78 $12,715.08

3 392 - ESOPHAGITIS, GASTROENT & MISC DIGEST DISORDERS W/O MCC 217,514 $21,988.72 $5,268.36 $4,127.22

4 292 - HEART FAILURE & SHOCK W CC 205,955 $26,084.52 $7,181.59 $6,296.91

5 690 - KIDNEY & URINARY TRACT INFECTIONS W/O MCC 197,146 $20,822.23 $5,503.43 $4,540.28

6 291 - HEART FAILURE & SHOCK W MCC 185,452 $39,370.72 $10,571.93 $9,687.82

7 194 - SIMPLE PNEUMONIA & PLEURISY W CC 181,714 $26,127.53 $6,965.02 $5,867.53

8 683 - RENAL FAILURE W CC 156,685 $25,745.19 $7,143.49 $6,155.45

9 190 - CHRONIC OBSTRUCTIVE PULMONARY DISEASE W MCC 143,163 $31,041.76 $8,031.95 $6,971.53

10 603 - CELLULITIS W/O MCC 142,752 $21,038.68 $6,007.25 $4,840.93

Exclusive to Healthcare. Dedicated to People. SM

Hospital Economics – Revenue: MS-DRG

Payment System

23

Payments vary by specialty - Hospitals focus on service line differentiation through providers, outreach locations, etc. to drive service line growth. The most profitable service lines typically include:

• Cardiology

• Orthopedics

• Neurosurgery (especially spine procedures)

• General Surgery

• Oncology

Whereas the least profitable service lines typically include:

• Women‟s health / OBGYN practices

• Psychiatry

• ICU / critical care unit

• Emergency Department

Exclusive to Healthcare. Dedicated to People. SM

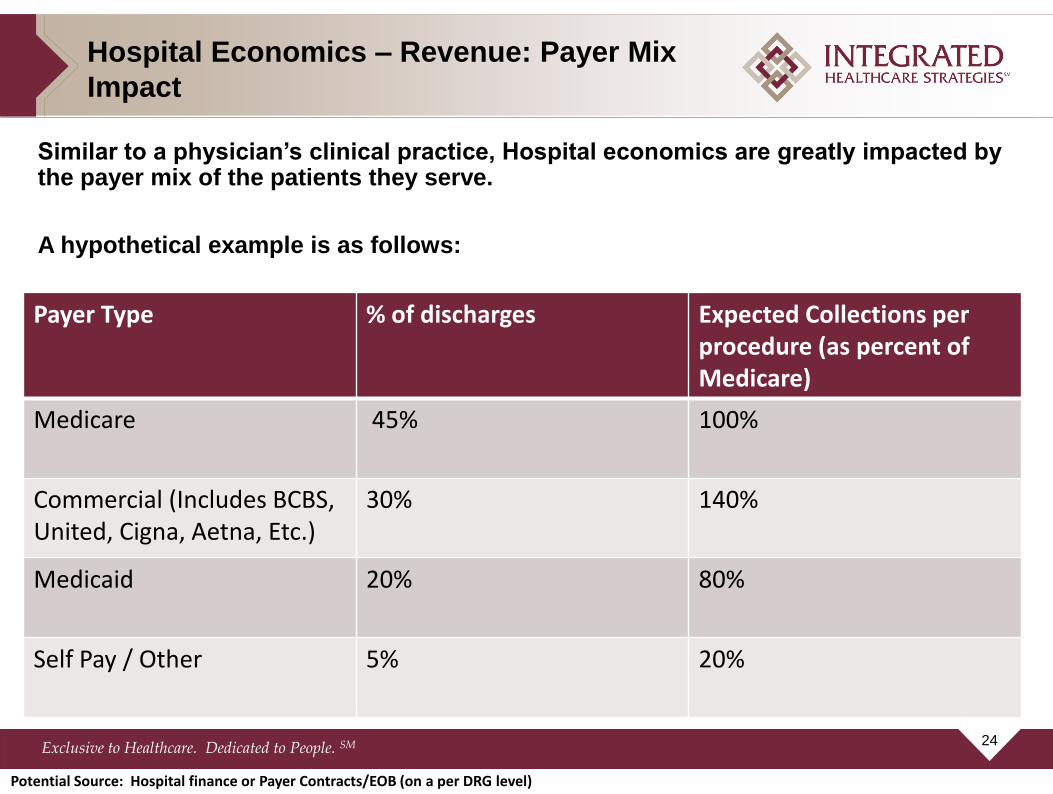

Hospital Economics – Revenue: Payer Mix

Impact

Similar to a physician‟s clinical practice, Hospital economics are greatly impacted by the payer mix of the patients they serve.

A hypothetical example is as follows:

24

Payer Type % of discharges Expected Collections per procedure (as percent of Medicare)

Medicare 45% 100%

Commercial (Includes BCBS, United, Cigna, Aetna, Etc.)

30% 140%

Medicaid 20% 80%

Self Pay / Other 5% 20%

Potential Source: Hospital finance or Payer Contracts/EOB (on a per DRG level)

Exclusive to Healthcare. Dedicated to People. SM

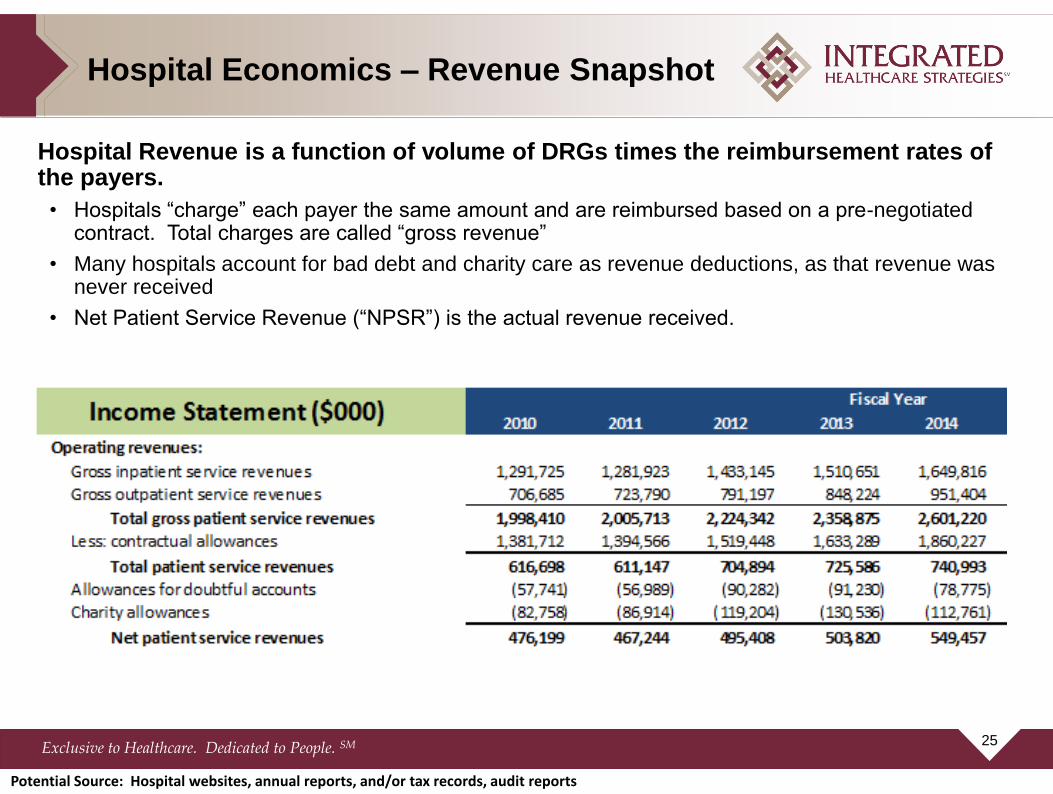

Hospital Economics – Revenue Snapshot

Hospital Revenue is a function of volume of DRGs times the reimbursement rates of the payers.

• Hospitals “charge” each payer the same amount and are reimbursed based on a pre-negotiated contract. Total charges are called “gross revenue”

• Many hospitals account for bad debt and charity care as revenue deductions, as that revenue was never received

• Net Patient Service Revenue (“NPSR”) is the actual revenue received.

25

Potential Source: Hospital websites, annual reports, and/or tax records, audit reports

Exclusive to Healthcare. Dedicated to People. SM

$5,977

$6,802 $6,432

$6,937 $7,011 $7,121 $6,994 $6,828

$8,430

$7,011

$5,606

$7,110

$9,630

$5,870

$6,769

$9,356

$7,223

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

Net

Pa

tien

t S

erv

ice

Re

ve

nu

e p

er

WE

IPA

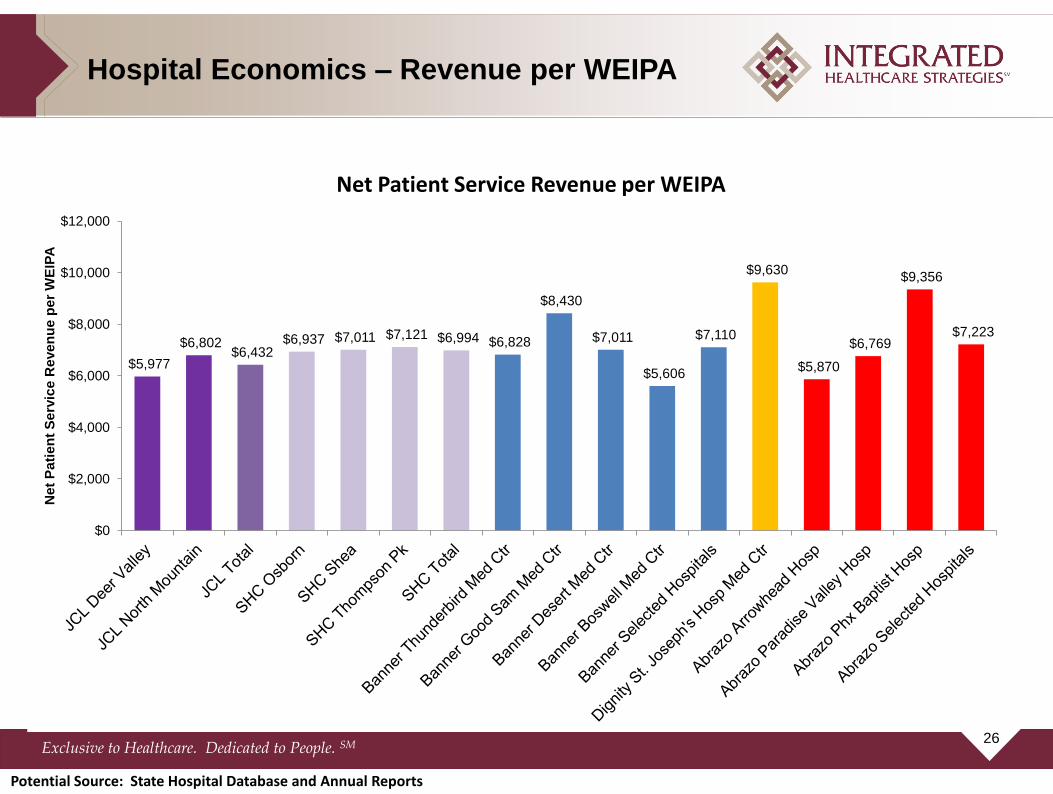

Hospital Economics – Revenue per WEIPA

Net Patient Service Revenue per WEIPA

26

Potential Source: State Hospital Database and Annual Reports

Exclusive to Healthcare. Dedicated to People. SM

Expenses are categorized into direct and indirect expenses:

• Direct expenses include labor, supplies, drugs, cleaning of the room, and other items directly correlated to patient care

• Indirect expenses include corporate overhead that is allocated to each department (and patient). Indirect expenses include the accounting department, HR expenses, general facilities maintenance, and other item that are not directly correlated to patient care

• Focus to “Break Even” at Medicare reimbursement

Hospital Economics – Expense Categories

27

Potential Source: Hospital websites, annual reports, and/or tax records, audit reports

Exclusive to Healthcare. Dedicated to People. SM

60.0

70.0

80.0

90.0

100.0

110.0

120.0

-

2,000

4,000

6,000

8,000

10,000

12,000

Pai

d h

ou

rs p

er

WEI

PA

Exp

en

ses

pe

r W

EIPA

Salaries, Wages, Benefits, Contract Labor All other non-capital expenses Depreciation Interest Paid hours per WEIPA

Hospital Economics – Expenses per

WEIPA

Operating Expenses per WEIPA

28

Potential Source: Hospital websites, annual reports, and/or tax records, audit reports

Exclusive to Healthcare. Dedicated to People. SM

DISCUSSION – IMPACT ON

PHYSICIAN SERVICES

29

Exclusive to Healthcare. Dedicated to People. SM

Market Strategies/Goals

Strategies Tactics

Improve Competitive Position

• Improve a service line (e.g. partner with orthopedic physicians) • Develop outreach clinics and satellite services • Programmatic growth incentives (through medical directorships, employment contracts, etc.)

Position organization for population health products

• Enhance primary care network including APCs, supervision, etc. • Ensure specialty specific coverage (employed or through coverage contracts) • Partner with payers (How should physician be paid for panel size?)

Cost per case (Break-even at Medicare)

• Service line co-management agreements • Supply utilization • Labor/staffing model optimization • Operational efficiency metrics (e.g. OR turnaround times) • ICU management and transfers

Ensuring physician coverage

• ED requirements 24/7 (e.g. Critical Access)

30

Related Documents