Holistic View of Textile Value Chain of Africa Rajeev Arora Executive Director African Cotton & Textile Industries Federation www.actifafrica.com / www.cottonafrica.com

Holistic View of Textile Value Chain of Africa Rajeev Arora Executive Director African Cotton & Textile Industries Federation / .

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Holistic View of Textile Value Chain of Africa

Rajeev AroraExecutive Director

African Cotton & Textile Industries Federation

www.actifafrica.com / www.cottonafrica.com

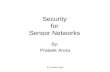

COTTON TRADEWORLD VS AFRICA

2011/12Million tons

2012/13Million tons

2013/14Million tons (projected)

World Production 28.042 26.684 25.63

Africa’s Share 5.6% 5.4% 6.0%

World Consumption 22.789 23.291 23.48

Africa’s Share 1.3% 1.5% 1.6%

World Imports 9.759 9.867 8.81

Africa’s Share 1.4% 1.7% 2.4%

World Exports 9.870 10.078 8.81

Africa’s Share 11.0% 12.6% 15.4%

Source ICAC June 2014

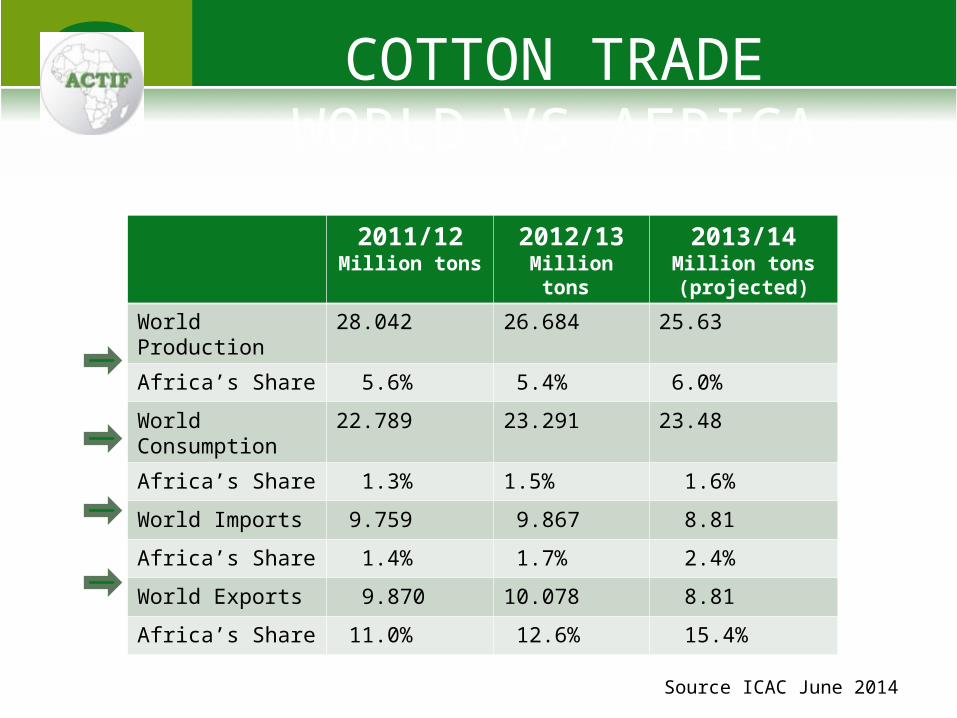

Supply & Use of CottonStatus in africa

Region 2013/14

Prod Imports Cons Exports

North Africa 119 154 184 87

Francophone Africa

902 n/a 17 892

Southern Africa 506 59 164 404

World 25,628 8,811 23,461 8,811

Source: ICAC June 2014, 000 Metric Tons

World Cotton

Million tons

Production

Mill Use

Lower cotton prices ahead

Supply & Use of CottonStatus in africa

Region 2018/19

Prod Imports Cons Exports

North Africa 120 200 280 40

Francophone Africa

1,200 n/a 25 1,175

Southern Africa 680 70 260 500

World 28,000 9,000 28,000 9,000

Source: Forecasts by Terry Townsend, ACTIF Consultant

000 Metric Tons

AGOA OPPORTUNITY

Total imports of textile & apparel products by USA stood at US$ 101Bn (Source: OTEXA, 2012)

SSA enjoys Duty free Quota free access into US for Garment exports under AGOA

Total U.S. Apparel imports from Africa under AGOA US$ 864

Million (0.8%) (Source: ACT, 2012)

U.S. Textile & Apparel Imports from Sub Sahara

Africa (SSA)

SSA

World

EPA OPPORTUNITY

Africa enjoys duty free Quota free access into EU for Textile products through the Economic Partnership Agreement (EPA)

Total imports of textile & apparel products by EU stood at US$ 234Bn. (2012)

Total EU textile and apparel imports from Africa stood at US$ 9.3 Bn (4%)

EU Textile & Apparel Imports from Africa

Africa

World

Source: ITC calculations based on UN Comtrade

KEY CONSTRAINTS AFFECTING VALUE ADDITION

1) Lack of conducive policy environment for Textile Investments

2) High operating costs due to obsolete technology & equipment among others

3) High competition from dumping pricing from Asia

4) Poor infrastructure and poor connectivity / logistics

5) Reliance on expatriate workforce for technical support

7) High costs of doing business

KEY CONSTRAINTS AFFECTING VALUE ADDITION

8) Lack of political commitment for sustainable policies to bring FDI

9) Porous borders leading to dumping and smuggling

10) Second hand clothing

11) No anti dumping policies and to check cheap import.

12) Copyright infringement

13) High cost of finance

ROLE OF ACTIF

Foreign Direct Investments(FDI): ACTIF explores investment in the cotton textile & apparel value chain in Africa, including developing due diligence and match making for JV’s

B2B Linkages: ACTIF facilitates Business to Business linkages with member countries

Access to Information: ACTIF provides information access including reports and special studies for national policies and strategies

Market access: ACTIF actively develops linkages with member countries and regional economic communities (RECs) like EAC, COMESA, SADC

ROLE OF ACTIF

Policy & Advocacy: ACTIF is very active in advocacy activities in partnership with its members and partners to improve the policy environment across the region

COMESA CtC Strategy: ACTIF has been recognized as the private sector representative for the implementation of the COMESA Cotton to Clothing strategy. With support of our funding partners, ACTIF has developed an priority implementation plan from the strategy and is currently monitoring the implementation activities;

BCI VALUE ADDITION PROJECT

TEXTILE VALUE CHAIN :VIEW OF ETHIOPIA & KENYA

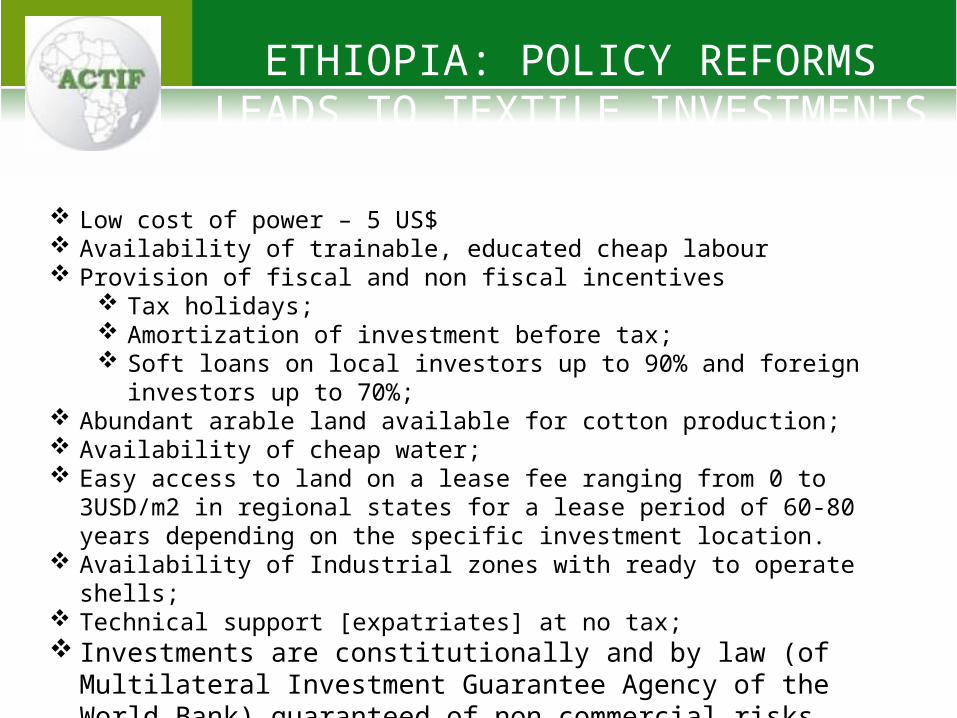

ETHIOPIA: POLICY REFORMS LEADS TO TEXTILE INVESTMENTS

Low cost of power – 5 US$ Availability of trainable, educated cheap labour Provision of fiscal and non fiscal incentives

Tax holidays; Amortization of investment before tax; Soft loans on local investors up to 90% and foreign investors up to 70%;

Abundant arable land available for cotton production; Availability of cheap water; Easy access to land on a lease fee ranging from 0 to 3USD/m2 in regional

states for a lease period of 60-80 years depending on the specific investment location.

Availability of Industrial zones with ready to operate shells; Technical support [expatriates] at no tax; Investments are constitutionally and by law (of Multilateral Investment

Guarantee Agency of the World Bank) guaranteed of non commercial risks.

COTTON MILL USE IN ETHIOPIA INCREASING WITH GROWING TEXTILE

INVESTMENTS

0

50

100

150

200

250

300

350

400

450

90/91 93/94 96/97 99/00 02/03 05/06 08/09 11/12

Source: ICAC

Thousand metric tons lint

Other SSA Countries

EthiopiaFranc Zone

Northern Africa

KEY ADVANTAGES IN ETHIOPIA

Low cost of power – 5 US$ Availability of trainable, educated cheap labour Provision of fiscal and non fiscal incentives

Tax holidays; Amortization of investment before tax; Soft loans on local investors up to 90% and foreign investors up to 70%;

Abundant arable land available for cotton production; Availability of cheap water; Easy access to land on a lease fee ranging from 0 to 3USD/m2 in regional

states for a lease period of 60-80 years depending on the specific investment location.

Availability of Industrial zones with ready to operate shells; Technical support [expatriates] at no tax; Investments are constitutionally and by law (of Multilateral Investment

Guarantee Agency of the World Bank) guaranteed of non commercial risks.

Kenya: the leading apparel exporter from africa under

agoa

KENYA: VALUE ADDITION ACTIVITIES

The government, under the Ministry of Industrialization & Enterprise development has placed the Textile Industry among its top 3 priority sectors. Impact so far:

Power Cost is now being subsided for Textile & Apparel Industries; Government is aggressively marketing the country for Textile

Investments;

Better Cotton Initiative Value Addition – A Niche Project for developing a full value chain project from Cotton farming under BCI to EU Market for finished garments. This project is the first of its kind in Africa and has the potential to be replicated in other countries;

OVERALL OBJECTIVE

Niche production of cotton via Better Cotton Initiative provides an opportunity to engage cotton farmers in a sustainable model of cotton production. The production activities are already under way spearheaded by the Fibre Directorate [Formerly CODA], supported by Solidaridad;

The overall objective of this project is to develop a full value chain project in Kenya, in collaborations with various institutions and support partners regionally and internationally;

The collaborations are targeting value addition of the certified BCI cotton up to finished garments and linkage to market in EU;

This project is the first of its kind in Africa;

SPECIFIC OBJECTIVES

Improve the livelihoods of cotton farmers: The project involves working with a selected group of farmers that will ensure maximum socio economic impact to them and their households.;

Sustainable production: This project will emphasize sustainable production practices across the value chain, a concept that is growing in demand and practice in the modern world today;

Value Addition: The cotton produced in this project will be processed into high valued finished garments, thereby creating jobs and increasing earnings within the region as compared to sale of raw cotton;

Access to market: This project will enable the producers to access high valued end markets in response to the growing demand in Europe for sustainable cotton products.

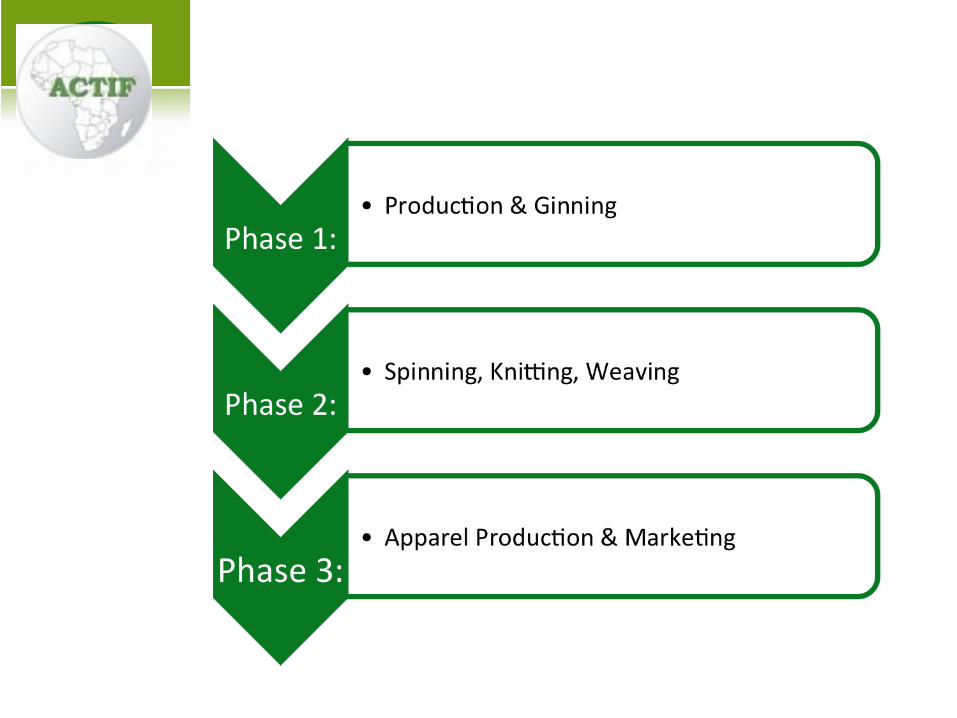

PHASE 1

PHASE 2 & 3: VALUE ADDITION

VALUE ADDITION ACTIVITIES

Overall Project Lead: To develop linkages & coordinate project implementation

Consultancy: Technical Assistance on Value Addition for Textile & Garment Companies

Consultancy: Technical Assistance in Marketing and Linkages to EU Retailers & Brands

VALUE ADDITION SUPPORT PARTNER

CAPTURING VALUE ADDITION

Value Addition x 10 times which can create 9 million jobs if 100% value is added to current African lint

Fibre

1 Kg

0.7 US$

0.5 person

Yarn

0.75 Kg

3.40 US$

0.75 person

Fabric

3.35Mtr

8.5 US$

2.0 persons

Garment

2 Trousers

15.50 US$

4.0 persons

Retail

2 Trousers

38.80 US$

Origin Africa Hosting

‘Africa Sourcing and Fashion Week’

21st – 23rd October 2015, Addis Ababa /

Ethiopia

www.originafrica.org

Related Documents